DISTRICT OF DELAWARE MARTIN BARTESCH, FRED...

68

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 1 of 68 PageID #: 151 UNITED STATES DISTRICT COURT DISTRICT OF DELAWARE MARTIN BARTESCH, FRED BRYANT And JOSEPH P. CRAIG, Individually And On Behalf Of All Others Similarly Situated, Case No. C.A. No. 11-cv-1173-RGA Plaintiffs, JURY TRIAL DEMANDED vs. BRENT M. COOK, MARTIN F. PETERSEN, JOHN T. PERRY, RICHARD D. CLAYTON, NICHOLAS GOODMAN, KRAIG T. HIGGINSON, REYNOLD ROEDER, BARRY MARKOWITZ, ALAN G. PERRITON, JAMES A. HERICKHOFF, and SCOTT E. DOUGHMAN, Defendants. AMENDED CLASS ACTION COMPLAINT Martin Bartesch, Fred Bryant and Joseph P. Craig (collectively, “Lead Plaintiffs” or “Plaintiffs”) allege the following based upon the investigation by Lead Plaintiffs’ counsel, which included, among other things: a review of the public documents, media interviews and reports, United States Securities and Exchange Commission (“SEC”) filings, wire and press releases published by and regarding Raser Technologies, Inc. (“Raser” or the “Company”); information provided a former employee of the Company; information obtained from publicly available documents regarding litigation involving the Company; securities analysts’ reports and advisories about the Company; and information readily available on the Internet. Lead Plaintiffs believe that substantial additional evidentiary support will exist for the allegations set forth herein after a reasonable opportunity for discovery.

Transcript of DISTRICT OF DELAWARE MARTIN BARTESCH, FRED...

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 1 of 68 PageID #: 151

UNITED STATES DISTRICT COURT DISTRICT OF DELAWARE

MARTIN BARTESCH, FRED BRYANT And JOSEPH P. CRAIG, Individually And On Behalf Of All Others Similarly Situated, Case No. C.A. No. 11-cv-1173-RGA

Plaintiffs, JURY TRIAL DEMANDED

vs.

BRENT M. COOK, MARTIN F. PETERSEN, JOHN T. PERRY, RICHARD D. CLAYTON, NICHOLAS GOODMAN, KRAIG T. HIGGINSON, REYNOLD ROEDER, BARRY MARKOWITZ, ALAN G. PERRITON, JAMES A. HERICKHOFF, and SCOTT E. DOUGHMAN,

Defendants.

AMENDED CLASS ACTION COMPLAINT

Martin Bartesch, Fred Bryant and Joseph P. Craig (collectively, “Lead Plaintiffs” or

“Plaintiffs”) allege the following based upon the investigation by Lead Plaintiffs’ counsel, which

included, among other things: a review of the public documents, media interviews and reports,

United States Securities and Exchange Commission (“SEC”) filings, wire and press releases

published by and regarding Raser Technologies, Inc. (“Raser” or the “Company”); information

provided a former employee of the Company; information obtained from publicly available

documents regarding litigation involving the Company; securities analysts’ reports and

advisories about the Company; and information readily available on the Internet. Lead Plaintiffs

believe that substantial additional evidentiary support will exist for the allegations set forth

herein after a reasonable opportunity for discovery.

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 2 of 68 PageID #: 152

NATURE OF THE ACTION AND OVERVIEW

1. This is a federal class action on behalf of purchasers (the “Class”) of the common

stock of Raser, who purchased or otherwise acquired the Company’s common stock between

May 11, 2009 through April 29, 2011, inclusive (the “Class Period”), seeking to pursue remedies

under the Securities Exchange Act of 1934 (the “Exchange Act”).

2. During the Class Period, non-Party Raser described itself as an environmental

energy technology company focused on geothermal power development and technology

licensing. In 2008, Raser reported the completion of a new geothermal power plant in Beaver

County, Utah called “Thermo No. 1.” According to the Company, Thermo No. 1 was a 10

megawatt (“MW”) geothermal plant which was due to become operational at or near full

capacity in the third quarter of 2009. In April 2009, the Company began selling power generated

by Thermo No. 1 to the City of Anaheim, California.

3. Raser utilized modular, binary-cycle generation units (PWPS PureCycle units) in

the construction of its Thermo No. 1 plant in order to decrease the level of on-site construction

activities and shorten development timelines compared to traditional geothermal power plant

development. Major construction of the Thermo No. 1 plant was completed in less than nine

months. Under the terms of the Company’s various financing agreements, Thermo No. 1 was

required to achieve full capacity output, net 10 MW, on a cost-effective basis by June 30, 2010.

4. Unbeknownst to the investment community, however, in its rush to complete

construction of the Thermo No. 1 plant, Raser failed to conduct adequate, or indeed any, early

well field development activities prior to beginning the construction phase of development.

According to Charles E. Levey, Vice President, Pratt & Whitney Power Systems, whose

2

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 3 of 68 PageID #: 153

subsidiary UTC Power Corp. supplied Raser with the generating units used at the Thermo No. 1

plant:

Back in 2006 Raser was a start-up company looking to “revolutionize” the geothermal power industry. Rather than drilling wells, developing well fields, and precisely characterizing geothermal resources prior to designing and building a powerplant - a process that can take years and cost millions of dollars - Raser would use land where they believed geothermal resources could be characterized at a fairly high level of certainty without expensive drilling, and would then develop the well field and build the power plant at the same time. [. . .]

Charles E. Levey, Lessons Learned from Raser Technologies’ “Revolutionary” Project , AOL

Energy (Oct. 20, 2011), http://energy.aol.com/2011/10/20/lessons-learned-from-raser -

technologies-revolutionary-project/ (emphasis added).

5. As a consequence of Raser’s failure to conduct adequate early well development

activities, the Company had selected a well field site for the Thermo No. 1 plant that was unable

to deliver output sufficient to generate net 10 MW of electricity. Specifically, the wells at the

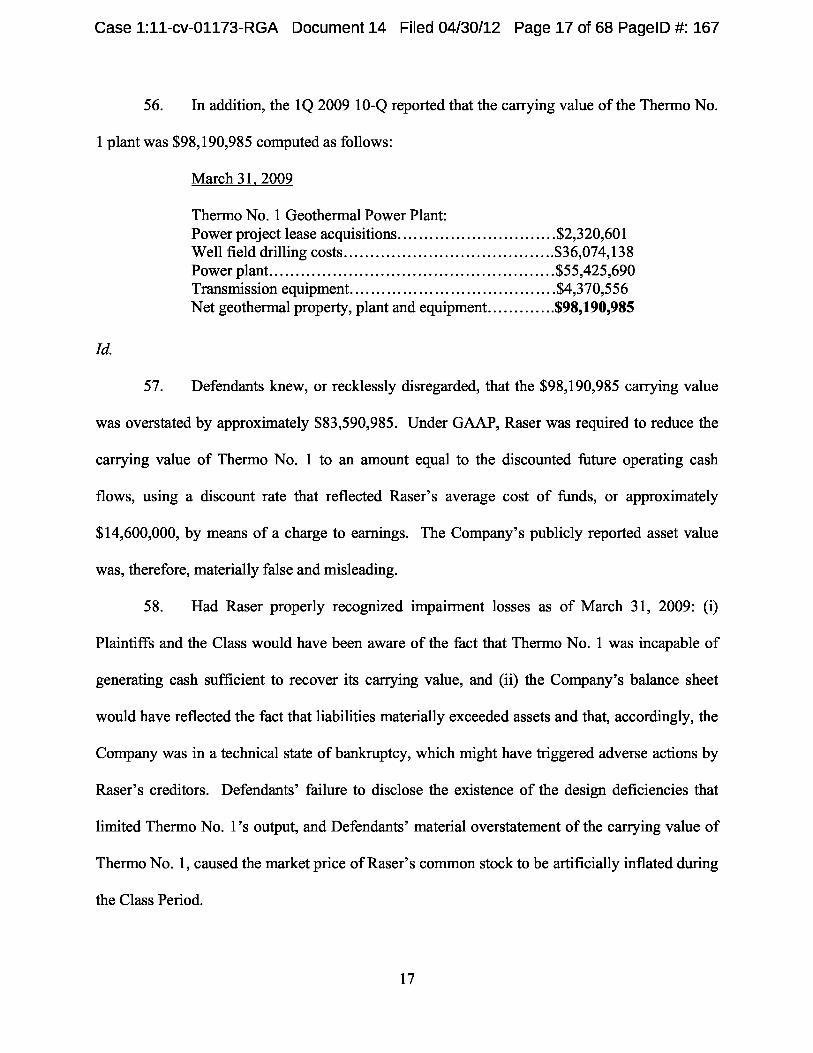

field site selected by Raser, and the well designs utilized by the Company, did not yield water at

a sufficiently high temperature to maximize Thermo No.1’s output due to the seepage of cold

water into the wells.

6. Thus, by the start of the Class Period, Defendants knew, or recklessly disregarded,

that the Thermo No. 1 plant could not achieve the planned net 10 MW output and, therefore,

there was no reasonable basis for Defendants’ public Class Period statements that the Company

expected the Thermo No. 1 plant to become operational at or near full capacity in the third

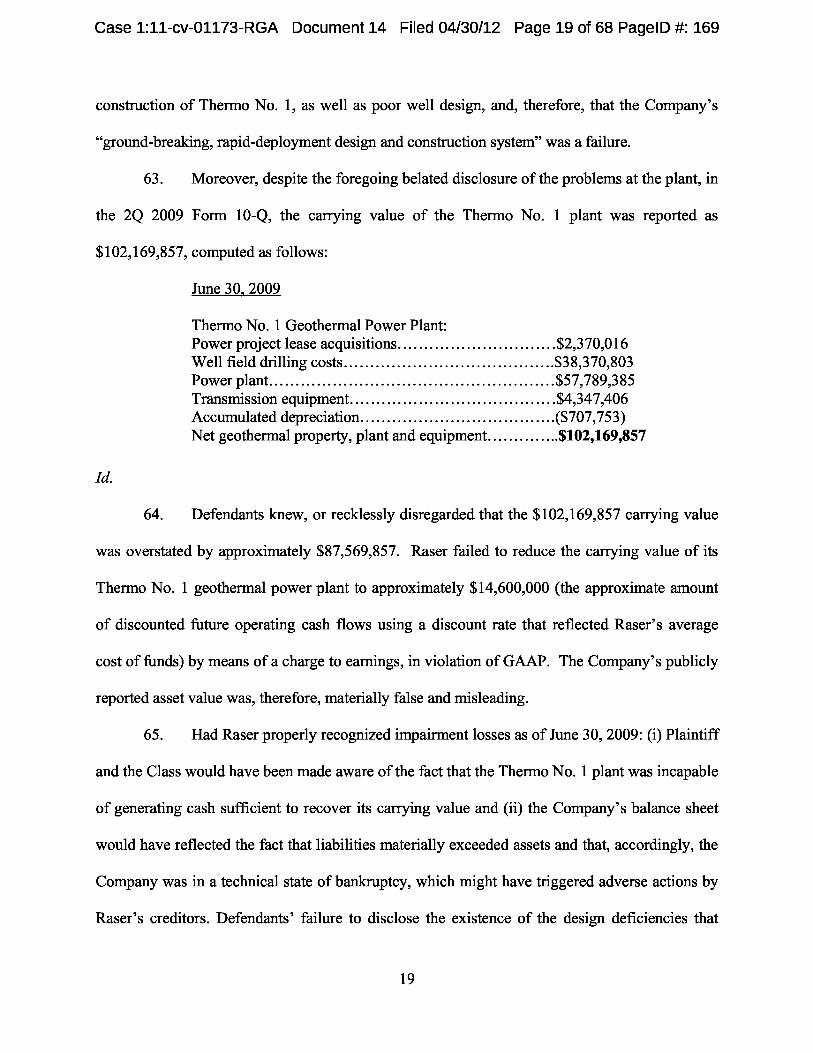

quarter of 2009.

7. Furthermore, Defendants knew, or recklessly disregarded, that Thermo No. 1

could not generate more than a net 6.6 MW of power and, at this level, it was impossible for the

Thermo No. 1 plant to operate at a profit, or for the cost of the plant to be recovered through

3

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 4 of 68 PageID #: 154

ongoing operations. Therefore, Defendants knew, or recklessly disregarded, that for accounting

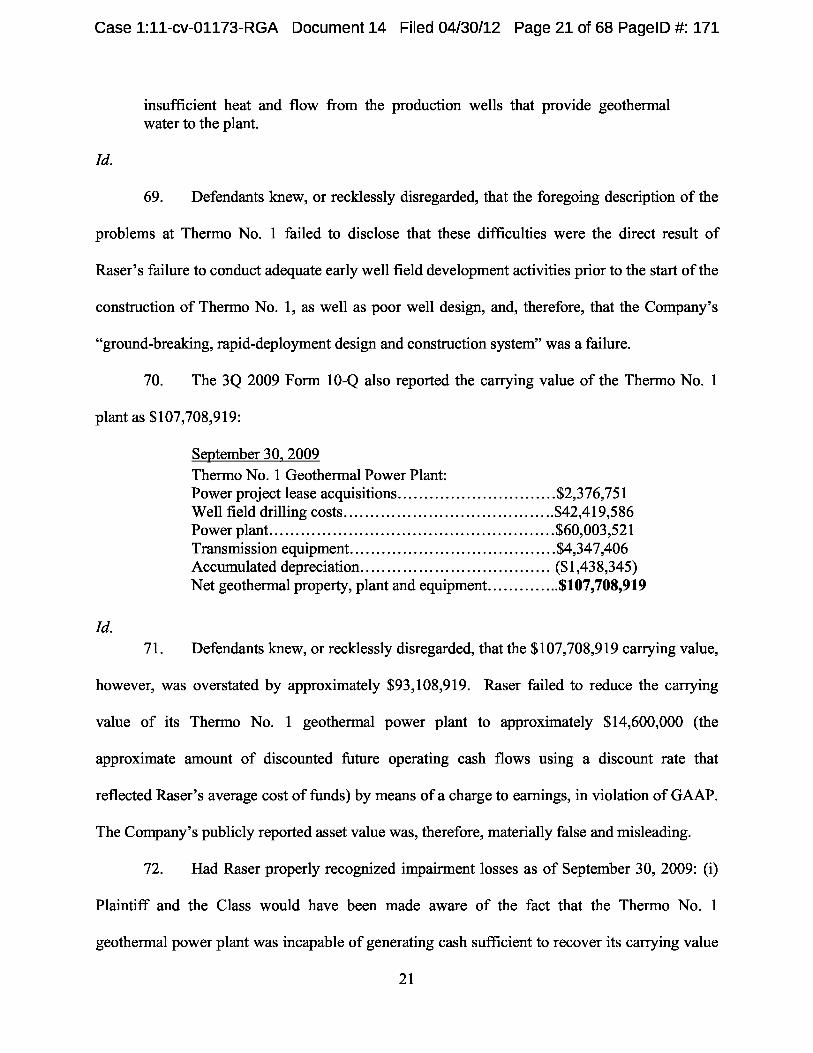

purposes, the Thermo No. 1 plant was impaired and that the carrying value for the plant on the

Company’s publicly reported financial statements was materially overstated.

8. While Defendants belatedly acknowledged problems with Thermo No. 1 in the

second fiscal quarter of 2009, they continued to lead investors to believe that these issues could

be remediated. Moreover, it was not until the second fiscal quarter of 2010 that Defendants

belatedly acknowledged that the value of Thermo No. 1 was impaired, recognizing a $52.2

million impairment loss. While substantial, the impairment charge taken by the Company was,

nonetheless, inadequate as Raser failed to reduce the carrying value of the plant to an amount

reflecting the approximate discounted future operating cash flows based on a discount rate

reflecting Raser’s average cost of funds as required by generally accepted accounting principles

(“GAAP”). In other words, despite the impairment charge, Defendants knew or recklessly

disregarded that the value of Thermo No. 1 was still overstated by approximately $15.4 million.

9. That the carrying value of Thermo No. 1 continued to be overstated by more than

50% was amply demonstrated when the Company announced that it had commenced a

solicitation process to sell Thermo No. 1. Raser acknowledged that “[b]ased on the solicitation

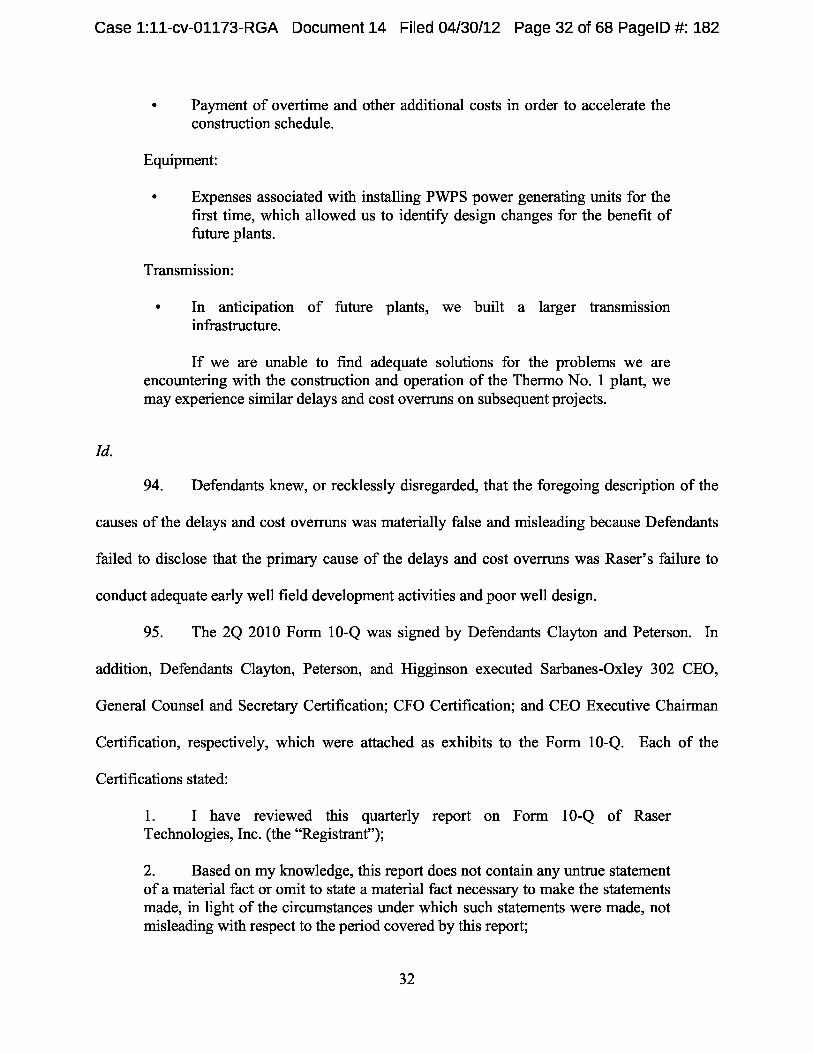

process and further evaluation of the performance of the plant,” it had further reduced the fair

value of Thermo No. 1 and expensed an additional $15.4 million. Thus, Defendants finally

publicly acknowledged what they had known from the start of the Class Period, namely, that due

to the inability of the plant to actually generate the output for which it was designed, the fair

value of the Thermo No. 1 plant was approximately $14.6 million.

10. In April 2011, only two-weeks after acknowledging the true value of the Thermo

No. 1 plant, Raser and its wholly-owned subsidiaries filed voluntary petitions for reorganization

4

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 5 of 68 PageID #: 155

in bankruptcy. All of the Company’s equity was ultimately wiped out in that restructuring,

eliminating millions of dollars in shareholder value.

11. Lead Plaintiffs and members of the Class, who were unaware of the undisclosed

problems with the Thermo No. 1 plant, purchased shares of Raser common stock at prices

artificially inflated by Defendants’ materially false and misleading statements and non-

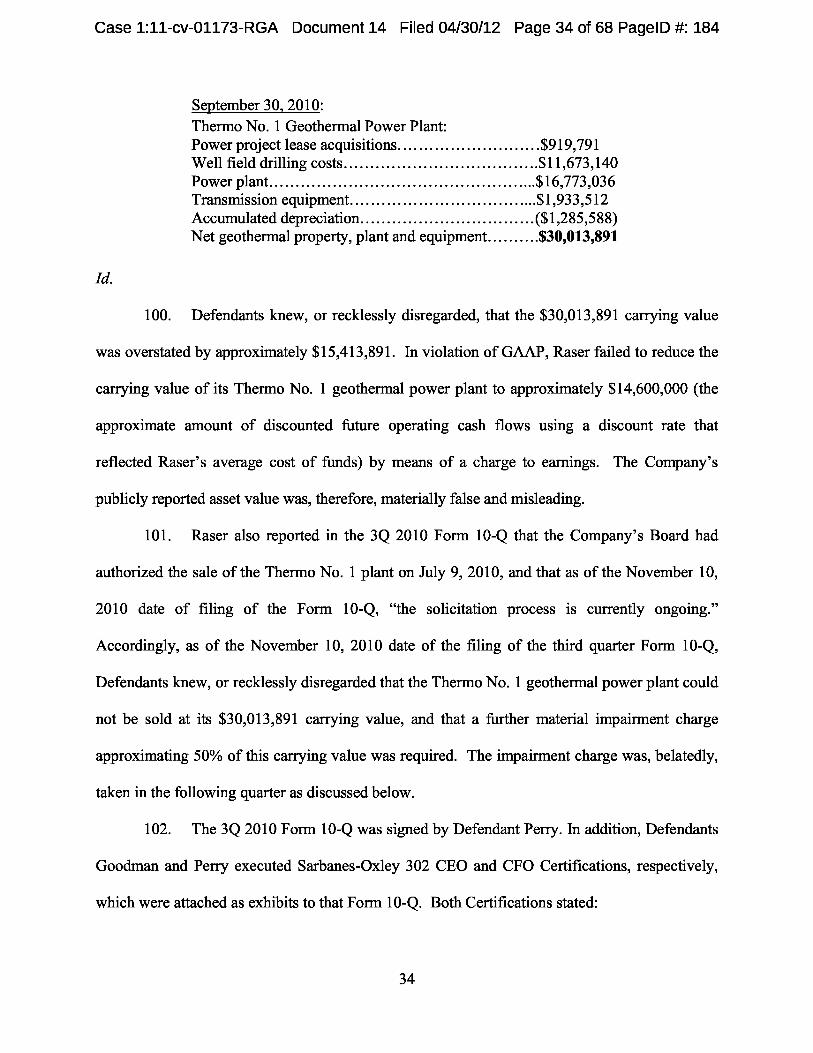

disclosures during the Class Period, and were damaged thereby.

JURISDICTION AND VENUE

12. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a) of

the Exchange Act, (15 U.S.C. §§ 78j(b) and 78t(a)), and Rule 10b-5 promulgated under Section

10(b) of the Exchange Act (17 C.F.R. § 240.10b-5).

13. This Court has jurisdiction over the subject matter of this action pursuant to

Section 27 of the Exchange Act (15 U.S.C. § 78aa), and 28 U.S.C. § 1331.

14. Venue is proper in this Judicial District pursuant to Section 27 of the Exchange

Act, 15 U.S.C. § 78aa and 28 U.S.C. § 1391(b). Many of the acts and transactions alleged herein

occurred in substantial part in this Judicial District.

15. In connection with the acts, conduct and other wrongs alleged in this Complaint,

defendants, directly or indirectly, used the means and instrumentalities of interstate commerce,

including but not limited to, the United States mails, interstate telephone communications and

the facilities of the national securities exchange.

5

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 6 of 68 PageID #: 156

PARTIES

Lead Plaintiffs

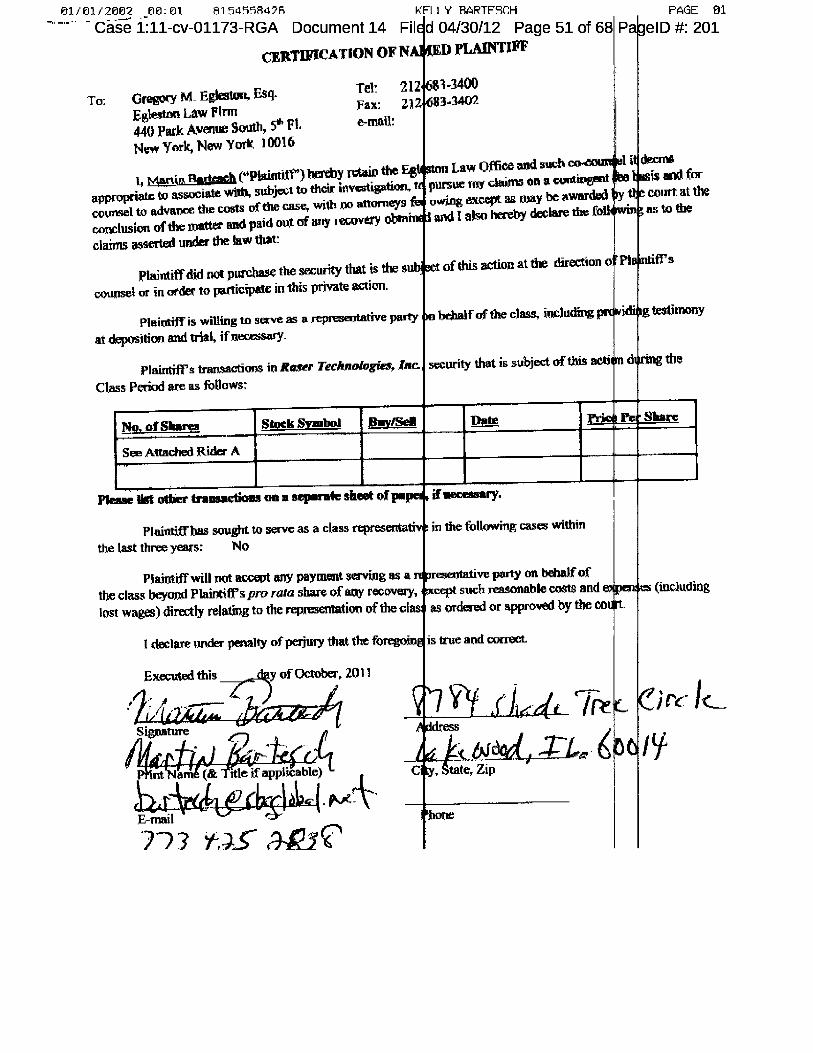

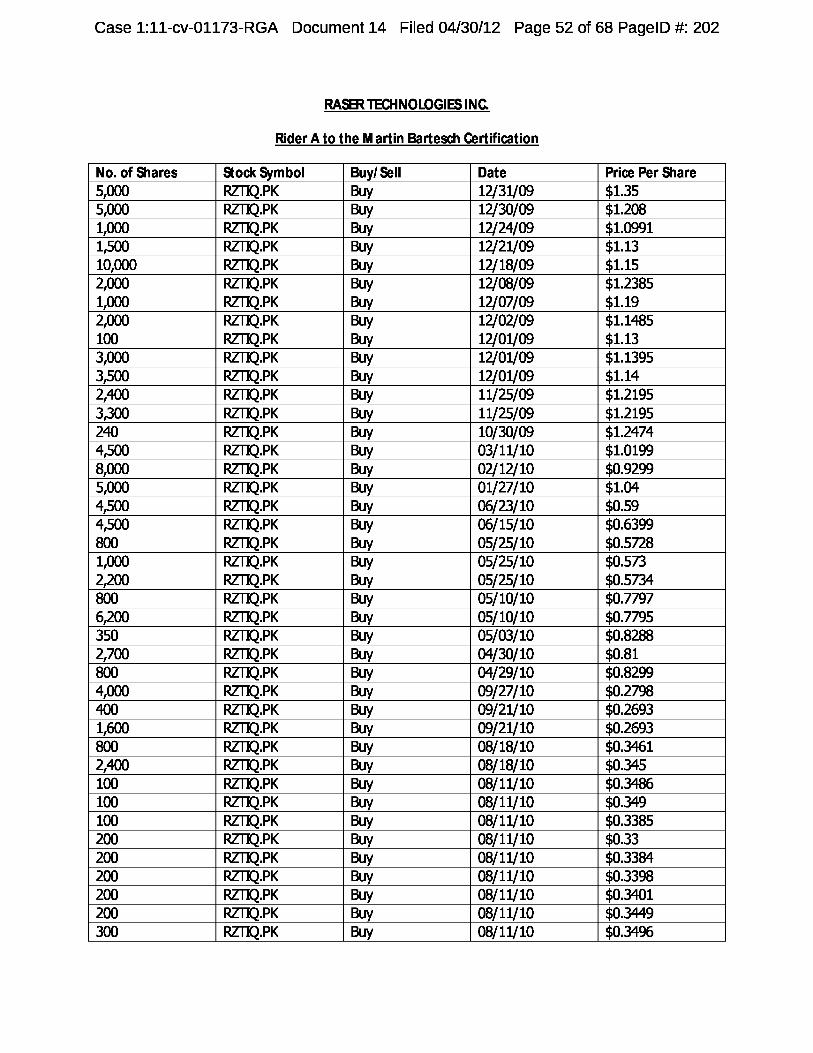

16. Plaintiff Martin Bartesch purchased Raser common stock at artificially inflated

prices during the Class Period as indicated in the certification attached hereto and has been

damaged thereby.

17. Plaintiff Fred Bryant purchased Raser common stock at artificially inflated

prices during the Class Period as indicated in the certification attached hereto and has been

damaged thereby.

18. Plaintiff Joseph P. Craig purchased Raser common stock at artificially inflated

prices during the Class Period as indicated in the certification attached hereto and has been

damaged thereby.

Non-Party

19. Non-party Raser was, during the Class Period, a Delaware corporation that

described itself as an environmental energy technology company focused on geothermal power

development and technology licensing. According to the Company’s periodic filings with the

SEC, Raser operated two business segments: (i) Power Systems and (ii) Transportation &

Industrial.

20. On April 29, 2011, Raser and its wholly-owned subsidiaries filed voluntary

petitions for reorganization under Chapter 11 of Title 11 of the United States Code in the United

States Bankruptcy Court for the District of Delaware. As a result of Raser’s filing for protection

under the Bankruptcy Code, it has not been named as a defendant. In September 2011, Raser

emerged from bankruptcy.

6

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 7 of 68 PageID #: 157

Defendants

21. Defendant Brent M. Cook (“Cook”) was the Company’s Chief Executive Officer

(“CEO”) from January 2005 until August 5, 2009, and a Director of the Company from October

2004 to August 5, 2009. Defendant Cook resigned from the Company on August 5, 2009.

Defendant Cook signed the Company’s 2009 first quarter Form 10-Q.

22. Defendant Martin F. Petersen (“Petersen”) was, at all relevant times herein,

Chief Financial Officer (“CFO”) (Principal Financial and Accounting Officer) of the Company.

Defendant Petersen signed the Company’s 2009 first quarter Form 10-Q, the second quarter

Form 10-Q, and the 2009 third quarter Form 10-Q.

23. Defendant John T. Perry (“Perry”) has been the Company’s CFO from March

22, 2010 to the present. Defendant Perry signed the Company’s 2010 first quarter Form 10-Q,

the 2010 second quarter Form 10-Q, and the 2010 third quarter Form 10-Q.

24. Defendant Richard D. Clayton (“Clayton”) was, at all relevant times herein, the

Principal Executive Officer, General Counsel and Secretary of the Company. Defendant Clayton

signed the Company’s 2009 second quarter Form 10-Q, the 2009 third quarter Form 10-Q, and

the 2009 Form 10-K.

25. Defendant Nicholas Goodman (“Goodman”) began serving as Chief Executive

Officer on January 25, 2010. On April 22, 2010, the Board of Directors appointed defendant

Goodman as a Class II Director to fill the vacancy resulting from the resignation of defendant

Cook on August 5, 2009. Defendant Goodman signed the Company’s 2009 Form 10-K.

26. Defendant Kraig T. Higginson (“Higginson”) was, at all relevant times herein,

the Chairman of the Board of Directors of the Company (the “Board”). Defendant Higginson

also served as the Company’s President from October 2003 to March 2004 and as the

7

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 8 of 68 PageID #: 158

Company’s CEO from March 2004 to January 2005. Defendant Higginson signed the

Company’s 2009 Form 10-K.

27. Defendant Reynold Roeder (“Roeder”) was, at all relevant times herein, a

Director of the Company and was also the Chairman of the Company’s Audit Committee.

Defendant Roeder signed the Company’s 2009 Form 10-K.

28. Defendant Barry Markowitz (“Markowitz”) was, all relevant times herein, a

Director of the Company. Defendant Markowitz also serves on the Audit, Nominating and

Governance, and Compensation Committees of the Company. Defendant Markowitz signed the

Company’s 2009 Form 10-K.

29. Defendant Alan G. Perriton (“Perriton”) was, at all relevant times herein, a

Director of the Company. Defendant Perriton signed the Company’s 2009 Form 10-K.

30. Defendant James A. Herickhoff (“Herickhoff”) was, at all relevant times herein,

a Director of the Company. Defendant Herickhoff signed the Company’s 2009 Form 10-K.

31. Defendant Scott E. Doughman (“Doughman”) was, at all relevant times herein, a

Director of the Company. Defendant Doughman signed the Company’s 2009 Form 10-K.

32. The individuals identified in paragraphs 21 through 31 above are collectively

referred to herein as “Defendants.”

BACKGROUND

33. At all relevant times, Raser operated two business segments: (i) Power Systems

and (ii) Transportation & Industrial.

34. The Company’s Power Systems segment was engaged in the development of

geothermal electric power plants, and its Transportation & Industrial segment was reported to be

engaged in improving the efficiency of electric motors, generators and power electronic drives

8

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 9 of 68 PageID #: 159

used in electric and hybrid electric vehicle propulsion systems. At all relevant times, Raser

touted its business strategy of “rapid deployment” of its “geothermal power projects.”

35. In a Form S-3 filed with the SEC on November 14, 2008, Raser reported:

During the first quarter of 2008, we entered into power purchase agreements with the City of Anaheim, California to provide a total of 22 MW of electricity from two of our future plants. Our Thermo No. 1 project is expected to be one of the two geothermal power plants to provide electricity to the City of Anaheim in accordance with the Anaheim power purchase agreements, and we expect to begin providing power from the Thermo No. 1 project to Anaheim beginning in the fourth quarter of 2008.

36. According to a qui tam complaint filed in the action entitled United States of

America and ex rel. Prescott Lovern v. The Prudential Insurance Co., et al. , Cause No. 11-cv-

1304 TSZ (W. D. Wash), filed on April 2, 2012 (the “Qui Tam Complaint”), Raser, through its

subsidiaries, entered into an Equity Capital Contribution Agreement with Merrill Lynch L.P.

Holdings, Inc. (collectively with other Merrill Lynch-related entities, “Merrill”) for a total

commitment of up to $31,175,092 in capital contributions that included debt and tax equity

capital “Thermo Note” to complete the construction of Thermo No. 1. (Qui Tam Complaint, ¶

15). After a previously committed, subsequent Second Funding Date Capital Contribution,

Merrill ended up with 99% secured ownership of Thermo No. 1, via “Class A Shares” in Thermo

No. 1. (Id.). The Qui Tam Complaint further states that the Prudential Insurance Company of

America (“Prudential”) and the Zurich American Insurance Company (“Zurich”) subsequently

acquired interests in the Thermo Note. ( Id., ¶ 17).

37. According to the Qui Tam Complaint, the terms of the investment financing

agreement provided that Raser, which began construction of Thermo No. 1 in August 2008,

complete the plant by the earlier of 180 days of the “Substantial Completion Date” (the date

9

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 10 of 68 PageID #: 160

construction of Thermo No. 1 was completed), or before June 15, 2009. (Qui Tam Complaint, ¶¶

18-19).

38. On November 10, 2008, an article in “Renewable Energy Development.com ”

reported that Raser had completed a new geothermal power plant in Beaver County, Utah called

“Thermo.” According to the article, the plant had a maximum capacity of 10 MW of electricity.

“This is a momentous occasion,” Defendant Cook at the plant’s ribbon cutting ceremony

reportedly stated. “This power generation plant with its ground-breaking, rapid-deployment

design and construction system and UTC Power’s low-temperature technology can make

geothermal a mainstream source of energy for the nation.” (Emphasis added).

39. It was Raser’s use of a “ground-breaking, rapid-deployment design,” however,

that caused the Thermo No. 1 plant to fail to meet its projected output. In its rush to meet the

deadlines specified in the investment financing agreement, Raser failed to conduct adequate field

development activities, such as the conduct of any seismic studies or targeted field surveys, prior

to the selection of its well field site for Thermo No. 1.

40. Confidential Witness No. 1 (“CW1”), a former employee of Raser who was

employed in a managerial position at the Company during part of 2008 and 2009, states that in or

about February 2009, Michael Albrecht (“Albrecht”), a geophysicist then-employed by Raser,

was asked to look into problems the Company was having at Thermo No. 1 by Raser’s Vice

President of Business Development. According to CW1, Albrecht was given unfettered access

to Raser’s files for that review.

41. CW1 stated that during that review, Albrecht determined that Raser had engaged

in little or no early well field development activities prior to the start of the construction of

Thermo No. 1. According to CW1, Albrecht learned that Raser had done no seismic studies and

10

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 11 of 68 PageID #: 161

even refused to purchase earlier seismic studies that had been done in that same area. CW1

further stated that Albrecht learned that decisions concerning the location of the well field had

not been made by geophysicists, but rather by Company executives and attorneys.

42. The Company’s failure to conduct adequate early well field development

activities, as described by CW1, was corroborated in an opinion article by Charles E. Levey,

Vice President, Pratt & Whitney Power Systems, whose subsidiary UTC Power Corp. supplied

the Company with the generating units used at the Thermo No. 1 plant and was sued by Raser

following the Company’s reorganization in bankruptcy. In an article entitled Lessons Learned

from Raser Technologies’ “Revolutionary” Project, Levey described the Company’s

“revolutionary” approach to developing geothermal power plants which was used in the

construction of Thermo No. 1: “ [r] ather than drilling wells, developing well fields, and

precisely characterizing geothermal resources prior to designing and building a powerplant - a

process that can take years and cost millions of dollars - Raser would use land where they

believed geothermal resources could be characterized at a fairly high level of certainty without

expensive drilling , and would then develop the well field and build the power plant at the same

time. . . .” AOL Energy (Oct. 20, 2011), http://energy.aol.com/2011/10/20/lessons-learned -

from-raser-technologies-revolutionary-project/ (emphasis added).

43. CW1 further stated that Albrecht learned that while the Company had obtained

water with a temperature of 370 degrees Fahrenheit (a temperature more than adequate to

maximize Thermo No. 1’s output) at a depth of 7,000 feet from certain of its wells, errors in the

designs of the wells caused cold water seepage at the 2,500 feet depth. This, in turn, reduced the

temperature of the water from the wells to the point where Thermo No. 1 could not generate net

10 MW of electricity. According to CW1, Albrecht attributed the well design problems, as well

11

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 12 of 68 PageID #: 162

as problems related to well field site selection, to Company executives and attorneys making

reservoir engineering and well design decisions, and intentionally deciding to forego

implementation of a fact based critical peer review process by adequate geo-scientists.

44. The allegations of the Qui Tam Complaint support CW1’s recitation of the

problems experienced at thermo No. 1 following its completion:

Thermo No. 1 was “substantially completed” in early 2009, but the plant did not work properly due to inadequate temperature and flow of hot water. The ... [Defendant Investors] were forced to continuously advance into the future, the “Guaranteed Final Completion Date”, because Thermo No. 1 never met the minimum functional specifications of the financing agreement’s terms and conditions, namely production of 6 MW of power. To date Thermo No. 1 does not meet these minimum specifications. Proof that Thermo No. 1 is an utter failure is the fact that the plant must draw power from the nearby fossil fuel “brown electric power” grid to power its own turbines, pumps and other equipment. Thermo No. 1 was supposed to produce [gross] 14 MW of power, but it produces no more than 2-3 MW of power with the aide of at 3-4 MW of brown electric power. At the time the Defendants applied for Section 1603 grant, Thermo No. 1 was not a commercially viable plant and shortly after receiving the Section 1603 grant Raser reclassified Thermo No. 1 as permanently impaired in accordance with “generally accepted accounting principles (GAAP) and the Energy Department should have been advised of this permanent impairment.

Qui Tam Complaint, ¶ 20 (insertions added).

45. According to CW1, Albrecht was also involved with planning for the drilling of a

new well in June 2009.1 CW1 states that Albrecht, Dr. Ben Barker, Raser’s Vice President of

Resource Management, other Company employees and the Company’s outside consultants met

at the Energy and Geoscience Institute in Salt Lake City, Utah, to design the well. CW1 states

that Albrecht believed that they had developed a well plan that would have been successful.

1 The Company’s interim report for the quarter ended June 31, 2009 filed with the SEC on Form 10-Q dated August 10, 2009 (the “2Q 2009 10-Q”) stated that “[a]s of June 30, 2009, we had finished drilling an additional well that we expect to use as a production well, pending the completion of testing.” Id., p. 9.

12

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 13 of 68 PageID #: 163

46. According to CW1, however, Albrecht subsequently learned that the well design

had been changed in order to save money on the amount of concrete to be used in its

construction. CW1 states that Albrecht contacted Defendant Peterson, then-Raser’s CFO, and

informed him that the revised well design would not work.

47. According to CW1, Albrecht also confronted Raser’s Controller Richard Holt,

who reported directly to Defendant Peterson, about the publicly reported carrying value of

Thermo No. 1. CW1 stated that Albrecht told Defendant Peterson that based on the problems

being experienced at the plant, the value attributed to Thermo No. 1 in March of 2009 was

grossly overstated. CW1 stated that Albrecht believed that the value for Thermo No. 1 was

around $60-70 million, not $120 million as reported, was spent in construction costs. According

to CW1, approximately 30 minutes after Albrecht spoke with Holt, Albrecht overheard Holt and

Defendant Peterson discussing how the Company could justify the valuation of Thermo No. 1 if

questioned at an upcoming shareholder meeting.

48. According to CW1, shortly thereafter in May 2009, Albrecht was asked to resign

from Raser.

49. Despite the fact that Defendants knew that Thermo No. 1 did not, and would

never, operate to capacity, in or about December 2009, Raser applied for a grant pursuant to

Section 1603 of the American Recovery and Reinvestment Act (the “Recovery Act”). Under

that section, eligible persons who placed into service specified energy properties during 2009,

2010 or 2011, could receive payments equal to 30% of the basis of the property. Eligible

property under this program included only property used in a trade or business or held for the

production of income.

13

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 14 of 68 PageID #: 164

50. According to the Qui Tam Complaint, Raser’s Section 1603 grant application

included reported Thermo No. 1 construction costs of $108 million. Corroborating the

information provided by CW1, the Qui Tam Complaint further alleged that these costs were

inflated by the Company:

The Conspirators knowingly submitted false, inflated construction costs as follows: 1) costs that were procured by kickbacks from contractors; 2) $4.9 million for the cost of turbine purchased from Pratt and Whitney in the fall of 2008, even though Raser never paid Pratt and Whitney for these turbines; 3) recording cost even when invoices were unpaid; 4) recording costs on a cash basis even when those invoices were paid in company stock rather than cash; 5) improperly reclassifying abandoned assets into capital expenses. (Raser drilled and abandoned several unsuccessful production wells in the fall and spring of 2008-2009 that it fraudulently included in its capital basis. It expensed these abandoned production wells on its balance sheet as abandoned, but when calculating its cost basis it recast the abandoned wells as “monitoring wells” and applied the cost to the Federal subsidy).

Id., ¶ 30.

THE MATERIALLY FALSE AND MISLEADING STATEMENTS

51. On May 11, 2009, the Company filed its interim report for the quarter ended

March 31, 2009 with the SEC on Form 10-Q (the “1Q 2009 10-Q”). In that filing, the Company

stated:

With the completion of the major construction items of the Thermo No. 1 geothermal power plant, we believe we have demonstrated our ability to quickly develop geothermal power projects using our rapid deployment business model .

Id. (emphasis added).

52. Defendants knew, or recklessly disregarded, that the foregoing statement was

materially false and misleading because Raser’s “rapid deployment business model,” which did

not utilize traditional early field development activities, such as seismic studies, was a failure.

As alleged above, inadequate well field testing and poor well design by Raser in the development

of Thermo No. 1 resulted in the seepage of cold water into the wells preventing the plant from

14

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 15 of 68 PageID #: 165

achieving its planned output of net 10 MW of electricity. Moreover, Defendants were aware of

the problems based upon the February 2009 review of Thermo No. 1 performed by Michael

Albrecht.

53. The 1Q 2009 10-Q also stated:

Thermo No. 1 Plant (Utah) We completed major construction of the cooling towers and transmission lines and installed the power generating units at the Thermo No. 1 geothermal power plant, located in Beaver County, Utah, in the fourth quarter of 2008. In April 2009, we began selling electricity generated by the Thermo No. 1 geothermal power plant to the City of Anaheim pursuant to a power purchase agreement we previously entered into with Anaheim. We expect the Thermo No. 1 geothermal power plant to become operational at or near full capacity early in the third quarter of 2009 . We have obtained all necessary permits to develop and operate the plant.

In 2007, with the help of external consulting geologists, we began evaluating preliminary geologic studies of possible geothermal resources near Beaver, Utah referred to as the Thermo Known Geothermal Resource Area (the “Thermo KGRA”). The area in and around the Thermo KGRA was targeted initially because multiple geologic studies had been performed over many years in the area, and because a geothermal well had been drilled in the area that reached a temperature of 345 degrees Fahrenheit. Our consulting geologists reviewed numerous studies on the area, including gravity, ground magnetic, telluric-magnetotelluric and self-potential surveys. They also reviewed data from dozens of thermal-gradient wells that have been drilled in and around the Thermo KGRA. After analyzing all of the available data, our consulting geologists concluded that the Thermo area was a high-prospect area and likely suitable for at least a 10 MW geothermal power plant.

Id. (emphasis added).

54. Defendants knew, or recklessly disregarded, that the statement concerning their

expectation that the Thermo No. 1 plant would become operational at, or near, full capacity early

in the third quarter of 2009 was materially false and misleading because it lacked any reasonable

basis. As alleged above, Defendants were aware that poor well field location and well design

prevented Thermo No. 1 from achieving its designed output of net 10 MW of electricity because

the water temperature from the Thermo No. 1 production wells was too low.

15

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 16 of 68 PageID #: 166

55. Similarly, the Defendants knew, or recklessly disregarded, that the statements

concerning the evaluation of the Thermo No. 1 site performed by Raser’s consultants were

materially misleading, even if literally true, because they created the impression that the

Company had performed adequate due diligence in its well field site selection prior to the start of

construction of Thermo No. 1. As described by CW1, Charles E. Levey of Pratt & Whitney

Power Systems, and as alleged in the Qui Tam Complaint, however, the Company failed to

conduct any traditional and adequate early well field development activities prior to the start of

the construction of Thermo No. 1. According to CW1, Albrecht learned that Dr. Joseph Moore,

of EGI, one of Raser’s outside consultants, used a self-potential survey that reaches only a few

hundred feet deep to determine well locations. The water at that depth, however, was cold water

that entered the wells at around 2500 ft. Raser used the self-potential survey method because

such surveys were very inexpensive. In addition, according to CW1, Albrecht learned that the

Company also used regional surveys, which did not focus on a specific local area, that were

inadequate to determine well field site selection. Albrecht, according to CW1, indicated that the

Company basically relied “on a cheap survey and Moore’s intuition and stretched imagination

instead of paying several hundred thousand dollars to conduct deep reaching surveys with

adequate resolution like the oil & gas industry . . . .” Thus, while Raser’s consultants may have

reviewed some earlier studies of the area as part of Raser’s rapid deployment business model, the

Company failed to conduct its own studies or drill its own wells in order to properly characterize

the well field prior to the start of construction of Thermo No. 1. As a consequence, the

temperature of the water from the Thermo No. 1 production wells was too low to operate the

plant at maximum capacity due to the presence of cooler water at the 2500 foot depth which

seeped into those wells.

16

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 17 of 68 PageID #: 167

56. In addition, the 1Q 2009 10-Q reported that the carrying value of the Thermo No.

1 plant was $98,190,985 computed as follows:

March 31, 2009

Thermo No. 1 Geothermal Power Plant: Power project lease acquisitions..............................$2,320,601 Well field drilling costs........................................$36,074,138 Power plant......................................................$55,425,690 Transmission equipment.......................................$4,370,556 Net geothermal property, plant and equipment............. $98,190,985

FAA

57. Defendants knew, or recklessly disregarded, that the $98,190,985 carrying value

was overstated by approximately $83,590,985. Under GAAP, Raser was required to reduce the

carrying value of Thermo No. 1 to an amount equal to the discounted future operating cash

flows, using a discount rate that reflected Raser’s average cost of funds, or approximately

$14,600,000, by means of a charge to earnings. The Company’s publicly reported asset value

was, therefore, materially false and misleading.

58. Had Raser properly recognized impairment losses as of March 31, 2009: (i)

Plaintiffs and the Class would have been aware of the fact that Thermo No. 1 was incapable of

generating cash sufficient to recover its carrying value, and (ii) the Company’s balance sheet

would have reflected the fact that liabilities materially exceeded assets and that, accordingly, the

Company was in a technical state of bankruptcy, which might have triggered adverse actions by

Raser’s creditors. Defendants’ failure to disclose the existence of the design deficiencies that

limited Thermo No. 1’s output, and Defendants’ material overstatement of the carrying value of

Thermo No. 1, caused the market price of Raser’s common stock to be artificially inflated during

the Class Period.

17

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 18 of 68 PageID #: 168

59. The 1Q 2009 Form 10-Q was signed by Defendants Cook and Peterson, who also

executed the Company’s Sarbanes-Oxley Section 302 CEO and CFO Certifications, respectively,

attached as exhibits to the Form 10-Q. Those Certifications, in pertinent part, both stated that:

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

60. Defendants Cook and Peterson knew, or recklessly disregarded, that the foregoing

statements were materially false and misleading for the reasons stated in ¶¶ 52, 54, 55 and 57

supra.

61. Raser filed its 2Q 2009 10-Q with the SEC on August 10, 2012. In that Form 10-

Q, the Company belatedly described some of the difficulties it was then-experiencing with the

Thermo No. 1 plant:

The Thermo No. 1 plant is currently producing approximately 5 MW (net) of electricity, which represents slightly less than half of the plant’s designed capacity. Thus far, we have been unable to operate the plant at full capacity due to insufficient heat from the production wells that provide geothermal water to the plant.

Id.

62. Defendants knew, or recklessly disregarded, that the foregoing description of the

problems at Thermo No. 1 failed to disclose that these difficulties were the direct result of

Raser’s failure to conduct adequate early well field development activities prior to the start of the

18

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 19 of 68 PageID #: 169

construction of Thermo No. 1, as well as poor well design, and, therefore, that the Company’s

“ground-breaking, rapid-deployment design and construction system” was a failure.

63. Moreover, despite the foregoing belated disclosure of the problems at the plant, in

the 2Q 2009 Form 10-Q, the carrying value of the Thermo No. 1 plant was reported as

$102,169,857, computed as follows:

June 30, 2009

Thermo No. 1 Geothermal Power Plant: Power project lease acquisitions..............................$2,370,016 Well field drilling costs........................................$38,370,803 Power plant......................................................$57,789,385 Transmission equipment.......................................$4,347,406 Accumulated depreciation.....................................($707,753) Net geothermal property, plant and equipment.............. $102,169,857

Id.

64. Defendants knew, or recklessly disregarded that the $102,169,857 carrying value

was overstated by approximately $87,569,857. Raser failed to reduce the carrying value of its

Thermo No. 1 geothermal power plant to approximately $14,600,000 (the approximate amount

of discounted future operating cash flows using a discount rate that reflected Raser’s average

cost of funds) by means of a charge to earnings, in violation of GAAP. The Company’s publicly

reported asset value was, therefore, materially false and misleading.

65. Had Raser properly recognized impairment losses as of June 30, 2009: (i) Plaintiff

and the Class would have been made aware of the fact that the Thermo No. 1 plant was incapable

of generating cash sufficient to recover its carrying value and (ii) the Company’s balance sheet

would have reflected the fact that liabilities materially exceeded assets and that, accordingly, the

Company was in a technical state of bankruptcy, which might have triggered adverse actions by

Raser’s creditors. Defendants’ failure to disclose the existence of the design deficiencies that

19

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 20 of 68 PageID #: 170

limited Thermo No. 1’s output, and Defendants’ material overstatement of the carrying value of

Thermo No. 1, caused the market price of Raser’s common stock to be artificially inflated during

the Class Period.

66. The 2Q 2009 Form 10-Q was signed by Defendants Clayton and Peterson, who

also executed the Company’s Sarbanes-Oxley Section 302 CEO and CFO Certifications,

respectively, attached as exhibits to the Form 10-Q. In addition, Defendant Higginson executed

a Sarbanes-Oxley Section 302 CEO and Executive Chairman Certification which was attached as

an exhibit to the 2Q 2009 Form 10-Q. Those Certifications, in pertinent part, each stated that:

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id. 67. Defendants Cook, Peterson, and Higginson knew, or recklessly disregarded, that

the foregoing statements were materially false and misleading for the reasons stated in ¶¶ 62 and

64 supra.

68. On November 9, 2009, the Company filed its interim report for the third fiscal

quarter of 2009 with the SEC on Form 10-Q (the 3Q 2009 Form 10-Q”). The 3Q 2009 Form 10-

Q, in pertinent part, stated:

The Thermo No. 1 plant is currently producing and transmitting approximately 5 MW of electricity, which represents approximately half of the plant’s designed capacity. Thus far, we have been unable to operate the plant at full capacity due to

20

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 21 of 68 PageID #: 171

insufficient heat and flow from the production wells that provide geothermal water to the plant.

Id.

69. Defendants knew, or recklessly disregarded, that the foregoing description of the

problems at Thermo No. 1 failed to disclose that these difficulties were the direct result of

Raser’s failure to conduct adequate early well field development activities prior to the start of the

construction of Thermo No. 1, as well as poor well design, and, therefore, that the Company’s

“ground-breaking, rapid-deployment design and construction system” was a failure.

70. The 3Q 2009 Form 10-Q also reported the carrying value of the Thermo No. 1

plant as $107,708,919:

September 30, 2009 Thermo No. 1 Geothermal Power Plant: Power project lease acquisitions..............................$2,376,751 Well field drilling costs........................................$42,419,586 Power plant......................................................$60,003,521 Transmission equipment.......................................$4,347,406 Accumulated depreciation.................................... ($1,438,345) Net geothermal property, plant and equipment.............. $107,708,919

Id. 71. Defendants knew, or recklessly disregarded, that the $107,708,919 carrying value,

however, was overstated by approximately $93,108,919. Raser failed to reduce the carrying

value of its Thermo No. 1 geothermal power plant to approximately $14,600,000 (the

approximate amount of discounted future operating cash flows using a discount rate that

reflected Raser’s average cost of funds) by means of a charge to earnings, in violation of GAAP.

The Company’s publicly reported asset value was, therefore, materially false and misleading.

72. Had Raser properly recognized impairment losses as of September 30, 2009: (i)

Plaintiff and the Class would have been made aware of the fact that the Thermo No. 1

geothermal power plant was incapable of generating cash sufficient to recover its carrying value

21

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 22 of 68 PageID #: 172

and (ii) the Company’s balance sheet would have reflected the fact that liabilities materially

exceeded assets and that, accordingly, the Company was in a technical state of bankruptcy,

which might have triggered adverse actions by Raser’s creditors. Defendants artificially inflated

the market price of Raser’s common stock by concealing the foregoing. Defendants’ failure to

disclose the existence of the design deficiencies that limited Thermo No. 1’s output, and

Defendants’ material overstatement of the carrying value of Thermo No. 1, caused the market

price of Raser’s common stock to be artificially inflated during the Class Period.

73. The 3Q 2009 Form 10-Q was signed by Defendants Clayton and Peterson, who

also executed the Company’s Sarbanes-Oxley Section 302 CEO and CFO Certifications,

respectively, attached as exhibits to the Form 10-Q. In addition, Defendant Higginson executed

a Sarbanes-Oxley Section 302 CEO Certification which was attached as an exhibit to the 3Q

2009 Form 10-Q. Those Certifications, in pertinent part, each stated that:

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

74. Defendants Cook, Peterson, and Higginson knew, or recklessly disregarded, that

the foregoing statements were materially false and misleading for the reasons stated in ¶¶ 69 and

71 above.

22

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 23 of 68 PageID #: 173

75. On March 18, 2010, Raser filed its annual report for the fiscal year ended

December 31, 2009 with the SEC on Form 10-K (the “2009 Form 10-K”). In that Form 10-K,

Raser reported that:

We have initiated the development of eight geothermal power plant projects in our Power Systems segment to date. We have placed one power plant in service to date, which we refer to as our Thermo No. 1 plant, and we are currently selling electricity generated by the Thermo No. 1 plant. The Thermo No. 1 plant is currently generating approximately 7 MW of electrical power (gross). After deducting the electricity required to power the plant, also known as parasitic load, the net power produced by the Thermo No. 1 plant is approximately 6 MW. In addition we also purchase power for remote pumps in our well field, which are required to ensure adequate flow of hot water. Both the gross output and the net output of the plant are below the amounts the plant was designed to produce, primarily due to issues related to the temperature of the resource from the well field. We are working to improve the electrical output of the plant and the temperature of the resource.

Id.

76. Defendants knew, or recklessly disregarded, that the foregoing description of the

problems at Thermo No. 1 failed to disclose that these difficulties were the direct result of

Raser’s failure to conduct adequate early well field development activities prior to the start of the

construction of Thermo No. 1, as well as poor well design, and, therefore, that the Company’s

“ground-breaking, rapid-deployment design and construction system” was a failure. Indeed,

Defendants tacitly admitted the failure of the Company’s rapid deployment strategy in

connection with Thermo No. 1 due to inadequate early well field activities in the section of the

2009 Form 10-K entitled Refine Rapid Deployment Strategy, stating “[w]e are also increasing

our focus on early well field development activities prior to beginning the construction phase of

development.” Id.

77. The 2009 Form 10-K further stated:

We obtained a grant of approximately $33.0 million, which we received in February 2010. Approximately $3.8 million of the grant funds were released to

23

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 24 of 68 PageID #: 174

us, as owner of the project. The remainder of the grant funds will be held in escrow until June 30, 2010, and the amounts to be released to the other parties that provided the debt and equity financing for the project will be determined based on the electrical output and the operational costs of the plant at that time. Up to $4.3 million of any amounts not released to these parties will be paid to Pratt Whitney Power Systems (“PWPS”) as final payment for the turbines in production at the Thermo No. 1 plant. Any remaining amount, after the payment to PWPS, will be released to us.

Id.

78. Accordingly, the 2009 Form 10-K reported that as of year end 2009, Raser

decreased the carrying value of its Thermo No. 1 plant by $29.2 million due to receipt of the

Section 1603 grant. Accordingly, after a $29.2 million adjustment, the carrying value of the

Thermo No. 1 plant was reported as $80,433,597:

December 31, 2009 Thermo No. 1 Geothermal Power Plant: Power project lease acquisitions..............................$2,514,581 Well field drilling costs........................................$31,813,747 Power plant......................................................$43,046,062 Transmission equipment.......................................$5,301,379 Accumulated depreciation.....................................($2,242,172) Net geothermal property, plant and equipment............. $80,433,597

Id. 79. Defendants knew, or recklessly disregarded, that the $80,433,597 carrying value,

however, was overstated by approximately $69,833,597. In violation of GAAP, Raser failed to

reduce the carrying value of its Thermo No. 1 geothermal power plant to approximately

$14,600,000 (the approximate amount of discounted future operating cash flows using a discount

rate that reflected Raser’s average cost of funds) by means of a charge to earnings. The

Company’s publicly reported asset value was, therefore, materially false and misleading.

80. Had Raser appropriately recognized impairment losses as of December 31, 2009:

(i) Plaintiff and the Class would have been made aware of the fact that the Thermo No. 1

geothermal power plant was incapable of generating cash sufficient to recover its carrying value

24

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 25 of 68 PageID #: 175

and (ii) the Company’s balance sheet would have reflected the fact that liabilities materially

exceeded assets and that, accordingly, the Company was in a technical state of bankruptcy, might

have triggered adverse actions by Raser’s creditors. Defendants’ failure to disclose the existence

of the design deficiencies that limited Thermo No. 1’s output, and Defendants’ material

overstatement of the carrying value of Thermo No. 1, caused the market price of Raser’s

common stock to be artificially inflated during the Class Period.

81. The 2009 Form 10-K was signed by Defendants Goodman, Higginson, Clayton,

Roeder, Markowitz, Perriton, Herrickhoff, and Doughman. In addition, Defendants Goodman

and Clayton executed Sarbanes-Oxley CEO and CFO Certifications, respectively, which were

attached as exhibits to the 2009 Form 10-K. Those Certifications, in pertinent part, each stated

that:

1. I have reviewed this annual report on Form 10-K of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

82. Defendants Goodman and Clayton knew, or recklessly disregarded, that the

foregoing statements were materially false and misleading for the reasons stated in ¶¶ 76 and 79

supra.

25

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 26 of 68 PageID #: 176

83. On May 10, 2010, Raser filed its interim report for the quarter ended March 31,

2010 with the SEC on Form 10-Q (the “1Q 2010 Form 10-Q”). In that Form 10-Q, the Company

stated:

The Thermo No. 1 plant is currently generating approximately 7 MW of electrical power (gross). After deducting the electricity required to power the plant, also known as parasitic load, and power for remote pumps in the well field, the net power produced by the Thermo No. 1 plant is approximately 6 MW. Both the gross output and the net output of the plant are below the amounts the plant was designed to produce, primarily due to issues related to temperature of the resource from the well field.

Id.

84. Defendants knew, or recklessly disregarded, that the foregoing description of the

problems at Thermo No. 1 was materially false and misleading because Defendants failed to

disclose that these difficulties were the direct result of Raser’s failure to conduct adequate early

well field development activities prior to the start of the construction of Thermo No. 1, as well as

poor well design, and, therefore, that the Company’s “ground-breaking, rapid-deployment design

and construction system” was a failure.

85. In addition, the 1Q 2010 Form 10-Q stated:

The Thermo No. 1 plant is currently transmitting approximately 6 MW of electricity to the City of Anaheim, which represents approximately two-thirds of the plant’s designed capacity. Thus far, we have been unable to operate the plant at full capacity due to insufficient heat and flow from the production wells that provide geothermal water to the plant . . . .

The Thermo No. 1 plant is the first ever large-scale commercial application of the PWPS Pure-Cycle units and the first plant built under our rapid-deployment approach so delays and overruns are not entirely unexpected. Some of the key drivers of the delays and cost overruns are as follows:

Well Field Development:

Increased costs to broaden previous well field plans.

Complications encountered by drilling contractors.

26

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 27 of 68 PageID #: 177

• High demand for drilling services and related materials due to the rapid increase in the price of oil.

• Higher than expected loads for well field pumps.

Construction:

• Wider than necessary step-outs for injection wells, which increased piping and electrical costs, due to concerns of lenders.

• Construction of primary access road improvements to accommodate wider access to Thermo No. 1 than previously anticipated.

• Additional costs incurred to connect piping from additional production wells to the plant.

• Additional costs incurred relating to establishing the greater Thermo area.

• Increased prices for steel, concrete and other commodities due to high demand.

• Payment of overtime and other additional costs in order to accelerate the construction schedule.

Equipment:

• Expenses associated with installing PWPS power generating units for the first time, which allowed us to identify design changes for the benefit of future plants.

Transmission:

• In anticipation of future plants, we built a larger transmission infrastructure.

If we are unable to find adequate solutions for the problems we are encountering with the construction and operation of the Thermo No. 1 plant, we may experience similar delays and cost overruns on subsequent projects.

Id.

86. Defendants also knew, or recklessly disregarded, that the foregoing description of

the causes of the delays and cost overruns was materially false and misleading because

27

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 28 of 68 PageID #: 178

Defendants failed to disclose that the primary cause of the delays and cost overruns was Raser’s

failure to conduct adequate early well field development activities and poor well design.

87. The 1Q 2010 Form 10-Q also reported that, excluding ongoing

construction/remediation costs, the Thermo No. 1 geothermal power plant operated at a loss of

$1 million for the quarter. Nonetheless, Raser, one again, failed to reduce the carrying value of

its Thermo No. 1 geothermal power plant to an appropriate value, approximately $14,600,000,

by means of a charge to earnings. Defendants, thus, knew, or recklessly disregarded, that the

Company’s publicly reported asset value was materially false and misleading.

88. Had Raser appropriately recognized impairment losses as of March 31, 2010: (i)

Plaintiff and the Class would have been made aware of the fact that the Thermo No. 1

geothermal power plant was incapable of generating cash sufficient to recover its carrying value

and (ii) the Company’s balance sheet would have reflected the fact that liabilities materially

exceeded assets and that, accordingly, the Company was in a technical state of bankruptcy,

which might have triggered adverse actions by Raser’s creditors. Defendants’ failure to disclose

the existence of the design deficiencies that limited Thermo No. 1’s output, and Defendants’

material overstatement of the carrying value of Thermo No. 1, caused the market price of Raser’s

common stock to be artificially inflated during the Class Period.

89. The 1Q 2010 Form 10-Q was signed by Defendant Perry. In addition, Defendants

Goodman and Perry executed Sarbanes-Oxley 302 CEO and CFO Certifications, respectively,

which were attached as exhibits to the Form 10-Q. Those Certifications, in pertinent part, each

stated that:

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

28

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 29 of 68 PageID #: 179

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

90. Defendants Goodman and Perry knew, or recklessly disregarded, that the

foregoing statements were materially false and misleading for the reasons stated in ¶¶ 84 and 85

supra.

91. On August 11, 2010, Raser filed its interim report for the period ended June 30,

2010 with the SEC on Form 10-Q (the “2Q 2010 Form 10-Q”). In that Form 10-Q, Defendants

finally admitted that Raser was incapable of getting the Thermo No. 1 geothermal power plant to

increase its power generation capability and, therefore, the Company was recognizing a $52.2

million impairment loss:

Although we placed the Thermo No. 1 plant in service in the first quarter of 2009 for accounting purposes, we were unable to operate the plant at designed capacity due primarily to mechanical deficiencies of the power generating units, lower than anticipated well field temperature and flow from certain wells and other inefficiencies which occurred as a result of overall design of the plant. Accordingly, we initiated several actions to improve the electrical output of the plant and the resource. These efforts included reworking certain production wells, the installation of bottom cycling operations and the replacement of recirculation pumps on each of the generating units with more efficient pumps. These efforts culminated in June 2010, at which time we evaluated the actual impact of these initiatives and the resulting overall performance of the plant. The results of this evaluation indicate that plant performance may improve from the current output level of approximately 6.6 megawatts, but most likely will not achieve originally designed electrical output levels. After evaluating the performance of the plant, we determined an evaluation of possible impairment of the Thermo No. 1 plant as of June 30, 2010 was warranted.

29

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 30 of 68 PageID #: 180

Based upon the impairment analysis, we determined that the Thermo No. 1 plant was impaired as of June 30, 2010. Accordingly, we computed the projected discounted future operating cash flows of the Thermo No. 1 plant using a discount rate that reflects the average cost of funds for our Thermo Subsidiary and determined that we incurred a loss resulting from the impairment totaling $52.2 million. This analysis required us to exercise significant judgments including, among other items, estimating that our geothermal power plant will produce electricity over the next 33.5 years, assuming our power purchase agreement will be renewed on similar terms upon expiration in 2028 and estimating operating and capital costs over the remaining useful life of the plant, the estimated cost of capital improvements required to upgrade the facility to produce 12 MW, the estimated cost of capital and the estimated selling price of the Thermo No. 1 plant at the end of its estimated useful life. Accordingly, we recognized an impairment of the Thermo No. 1 plant and expensed $52.2 million of capitalized costs during the second quarter of 2010. The effect of the impairment expense on net loss per share of common stock was $0.59 and $0.62 per share for the three months and six months ending June 30, 2010. Since the basis in the Thermo No. 1 plant decreased significantly as a result of the impairment, the new basis of $30.1 million will be depreciated on a straight-line basis over the remaining estimated useful life of the plant or 33.5 years. The reduction of the basis in the Thermo No. 1 plant on future periods will be to reduce quarterly depreciation expense from approximately $0.6 million per quarter to $0.2 million per quarter. The table below sets forth the capitalized costs relating to our property, plant and equipment, after reducing the costs for the impairment of the Thermo No. 1 plant as of June 30, 2010 and reducing the costs for the amount of the federal grant received as of December 31 2009, respectively:

June 30, 2010 Thermo No. 1 Plant: Power project lease acquisitions..............................$919,792 Well field drilling costs........................................$11,688,317 Power plant......................................................$16,827,944 Transmission equipment.......................................$1,927,957 Accumulated depreciation.....................................($1,264,010) Geothermal property, plant and equipment, net............ $30,100,000

Id.

92. Although a substantial impairment charge was recognized, Defendants knew, or

recklessly disregarded, that the $30,100,000 carrying value of Thermo No. 1 was still overstated

by approximately $15,500,000. In violation of GAAP, Raser failed to reduce the carrying value

of its Thermo No. 1 geothermal power plant to approximately $14,600,000 (the approximate

30

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 31 of 68 PageID #: 181

amount of discounted future operating cash flows using a discount rate that reflected Raser’s

average cost of funds) by means of a charge to earnings. The Company’s publicly reported asset

value was, therefore, materially false and misleading.

93. In addition, the 2Q 2010 Form 10-Q stated:

Although we placed the Thermo No. 1 plant in service in the first quarter of 2009 for accounting purposes, we were unable to operate the plant at designed capacity due primarily to mechanical deficiencies of the power generating units, lower than anticipated well field temperature and flow from certain wells and other inefficiencies which occurred as a result of overall design of the plant. . . .

The Thermo No. 1 plant is the first ever large-scale commercial application of the PWPS Pure-Cycle units and the first plant built under our rapid-deployment approach so delays and overruns are not entirely unexpected. Some of the key drivers of the delays and cost overruns are as follows:

Well Field Development:

• Increased costs to broaden previous well field plans.

• Complications encountered by drilling contractors.

• High demand for drilling services and related materials due to the rapid increase in the price of oil.

• Higher than expected loads for well field pumps.

Construction:

• Wider than necessary step-outs for injection wells, which increased piping and electrical costs, due to concerns of lenders.

• Construction of primary access road improvements to accommodate wider access to Thermo No. 1 than previously anticipated.

• Additional costs incurred to connect piping from additional production wells to the plant.

• Additional costs incurred relating to establishing the greater Thermo area.

• Increased prices for steel, concrete and other commodities due to high demand.

31

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 32 of 68 PageID #: 182

• Payment of overtime and other additional costs in order to accelerate the construction schedule.

Equipment:

• Expenses associated with installing PWPS power generating units for the first time, which allowed us to identify design changes for the benefit of future plants.

Transmission:

• In anticipation of future plants, we built a larger transmission infrastructure.

If we are unable to find adequate solutions for the problems we are encountering with the construction and operation of the Thermo No. 1 plant, we may experience similar delays and cost overruns on subsequent projects.

Id.

94. Defendants knew, or recklessly disregarded, that the foregoing description of the

causes of the delays and cost overruns was materially false and misleading because Defendants

failed to disclose that the primary cause of the delays and cost overruns was Raser’s failure to

conduct adequate early well field development activities and poor well design.

95. The 2Q 2010 Form 10-Q was signed by Defendants Clayton and Peterson. In

addition, Defendants Clayton, Peterson, and Higginson executed Sarbanes-Oxley 302 CEO,

General Counsel and Secretary Certification; CFO Certification; and CEO Executive Chairman

Certification, respectively, which were attached as exhibits to the Form 10-Q. Each of the

Certifications stated:

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

32

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 33 of 68 PageID #: 183

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

96. Defendants Clayton, Peterson, and Higginson knew, or recklessly disregarded,

that the foregoing statements were materially false and misleading for the reasons stated in ¶¶ 92

and 94 supra.

97. On November 10, 2010, Raser filed its interim report for the quarter ended

September 30, 2009 with SEC on Form 10-Q (the “3Q 2010 10-Q”). In that Form 10-Q, Raser

stated:

Although we placed the Thermo No. 1 plant in service in the first quarter of 2009 for accounting purposes, we were unable to operate the plant at designed capacity due primarily to mechanical deficiencies of the power generating units, lower than anticipated well field temperature and flow from certain wells and other inefficiencies which occurred as a result of overall design of the plant.

Id.

98. Defendants knew, or recklessly disregarded, that the foregoing description of the

problems at Thermo No. 1 was materially false and misleading because Defendants failed to

disclose that these difficulties were the direct result of Raser’s failure to conduct adequate early

well field development activities prior to the start of the construction of Thermo No. 1, as well as

poor well design, and, therefore, that the Company’s “ground-breaking, rapid-deployment design

and construction system” was a failure.

99. The 3Q 2010 10-Q also reported that the carrying value of the Thermo No. 1 plant

as $30,013,891:

33

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 34 of 68 PageID #: 184

September 30, 2010: Thermo No. 1 Geothermal Power Plant: Power project lease acquisitions...........................$919,791 Well field drilling costs.....................................$11,673,140 Power plant...................................................$16,773,036 Transmission equipment....................................$1,933,512 Accumulated depreciation.................................($1,285,588) Net geothermal property, plant and equipment.......... $30,013,891

Id.

100. Defendants knew, or recklessly disregarded, that the $30,013,891 carrying value

was overstated by approximately $15,413,891. In violation of GAAP, Raser failed to reduce the

carrying value of its Thermo No. 1 geothermal power plant to approximately $14,600,000 (the

approximate amount of discounted future operating cash flows using a discount rate that

reflected Raser’s average cost of funds) by means of a charge to earnings. The Company’s

publicly reported asset value was, therefore, materially false and misleading.

101. Raser also reported in the 3Q 2010 Form 10-Q that the Company’s Board had

authorized the sale of the Thermo No. 1 plant on July 9, 2010, and that as of the November 10,

2010 date of filing of the Form 10-Q, “the solicitation process is currently ongoing.”

Accordingly, as of the November 10, 2010 date of the filing of the third quarter Form 10-Q,

Defendants knew, or recklessly disregarded that the Thermo No. 1 geothermal power plant could

not be sold at its $30,013,891 carrying value, and that a further material impairment charge

approximating 50% of this carrying value was required. The impairment charge was, belatedly,

taken in the following quarter as discussed below.

102. The 3Q 2010 Form 10-Q was signed by Defendant Perry. In addition, Defendants

Goodman and Perry executed Sarbanes-Oxley 302 CEO and CFO Certifications, respectively,

which were attached as exhibits to that Form 10-Q. Both Certifications stated:

34

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 35 of 68 PageID #: 185

1. I have reviewed this quarterly report on Form 10-Q of Raser Technologies, Inc. (the “Registrant”);

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Registrant as of, and for, the periods presented in this report . . . .

Id.

103. Defendants Goodman and Perry knew, or recklessly disregarded, that the

foregoing statements were materially false and misleading for the reasons stated in ¶¶ 100 and

102 supra.

104. On April 15, 2011, Raser filed its 2010 Form 10-K with the SEC (the “2010 Form

10-K”). In the 2010 Form 10-K, the Company disclosed “[d]uring the third quarter of 2010 we

commenced the solicitation process of the sale of Thermo No. 1, or an interest therein. Based on

the solicitation process and further evaluation of the performance of the plant we further reduced

the value of the Thermo No. 1 plant and expensed an additional $15.4 million of capitalized costs

during the fourth quarter of 2010. We estimate that the fair value of the Thermo No. 1 plant, less

selling costs at December 31, 2010 totaled $14.6 million.”

105. Two weeks later, on April 29, 2011, Raser and its wholly-owned subsidiaries filed

voluntary petitions for reorganization under Chapter 11 of Title 11 of the United States Code in

the United States Bankruptcy Court for the District of Delaware. Upon the April 29, 2011 filing,

the common stock of Raser became virtually worthless.

106. On September 6, 2011, Raser filed a Form 8-K with the SEC. That Form 8-K

stated, in pertinent part, that:

35

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 36 of 68 PageID #: 186

On June 21, 2011, the Company filed with the Bankruptcy Court a [sic] initial Joint Plan of Reorganization of Raser Technologies, Inc. and its Affiliated Debtors (as amended, the “Plan”) and the Disclosure Statement with Respect to the Plan (as amended, the “Disclosure Statement”). A [sic] hearings regarding the Plan and the Disclosure Statement were held before the Bankruptcy Court and on August 30, 2011, the Bankruptcy Court entered its Order Confirming the Third Amended Plan of Reorganization of Raser Technologies, Inc. and Its Affiliated Debtors (the “Order”).

Among other things, the Plan provides that all common stock and other equity ownership interests in the Company are cancelled and that the holders of such securities do not receive any property or distribution under the Plan on account of such securities. Reference should be made to the Plan for the description and treatment of all of the classes of claimants under the Plan and other terms and conditions regarding implementation of the Plan.

Id. (emphasis added).

GAAP

107. Due to the pervasiveness of the Company’s fraudulent accounting activities and

the magnitude of the amounts involved, Defendants could not avoid knowing of them, as well as

the fact that they were concealed.

108. Extensive accounting manipulations of the sort alleged here are, necessarily, the

product of conscious behavior of the Company and its high-level executives. Certainly,

corporate books cannot “cook” themselves.

109. SEC Staff Accounting Bulletin No. 104, Revenue Recognition in Financial

Statements, states:

MD&A requires a discussion of liquidity, capital resources, results of operations and other information necessary to an understanding of a registrant’s financial condition, changes in financial condition and results of operations. This includes unusual or infrequent transactions, known trends or uncertainties that have had, or might reasonably be expected to have, a favorable or unfavorable material effect on revenue, operating income or net income and the relationship between revenue and the costs of the revenue. Changes in revenue should not be evaluated solely in terms of volume and price changes, but should also include an analysis of the reasons and factors contributing to the increase or decrease. The Commission stated in FRR 36 that MD&A should “give investors an opportunity to look at the

36

Case 1:11-cv-01173-RGA Document 14 Filed 04/30/12 Page 37 of 68 PageID #: 187

registrant through the eyes of management by providing a historical and prospective analysis of the registrant’s financial condition and results of operations, with a particular emphasis on the registrant’s prospects for the future.”

110. Item 7 of Form 10-K and Item 2 of Form 10-Q require the issuer to furnish

information required by Item 303 of Regulation S-K [17 C.F.R. § 229.303]. In discussing results

of operations, Item 303 of Regulation S-K requires the registrant to “[d]escribe any known trends

or uncertainties that have had or that the registrant reasonably expects will have a material

favorable or unfavorable or unfavorable impact on net sales or revenues or income from

continuing operations.”

111. The Instructions to Paragraph 303(a) further state, “[t]he discussion and analysis

shall focus specifically on material events and uncertainties known to management that would