Investing in distressed financial assets in Russia and Ukraine

Upload

vuongtuyenCategory

view

218download

0

Distressed For Control Investing

New Playbook for the Mega Cycle in Defaults

Atlanta ~ March 11, 2009

MatlinPatterson O er ieMatlinPatterson Overview

MatlinPatterson—$9+ billion in asset management for a globally diverse group of institutionalinvestors including government and corporate pension funds, endowments, foundations, andinsurance companies, as well as funds of funds and family offices

Private Equity Strategy: Investing globally in distressed securities and assets for corporatecontrol. $2.2 billion in Fund I—13 companies $1.7 billion in Fund II—fully deployed in 18companies; $5 billion in Fund III—54% drawn in 7 companies

Hedge Fund Strategy: Non-control distressed/value investing globally, est. ‘07• $200 million AUM, tripled since inception, +10.76% net first 2 months‘08

Founded in 1994 by David Matlin and Mark Patterson within Credit Suisse• Established independently in 2002, team of 60 investment and support professionals

Over 70 distressed control investments, exposures in 40 countries

Offices in New, London and Hong Kong

2 2

Di t d I ti i C t l d N C t l E i tDistressed Investing in Control and Non-Control Environments

Atlanta ~ December 5, 2007,“Distressed for Dummies”f

3

S bP iSubPrime

4

St t d P d tStructured Products

5

C dit C i iCredit Crisis

6

Did you ever think that making a speechDid you ever think that making a speech on economics is a lot like pissing down your leg? It seems hot to you, but it never does to anyone else.y

~Lyndon B. Johnsony

7

C t M k t C ditiCurrent Market Conditions

Does anything make sense?Does anything make sense?

8

C t M k t C ditiCurrent Market Conditions

B k t b ti i US t k k t D f lt t dBear market observation in US stock markets Default trends

Bank Market cap shrinkage

High yield pricing

Loan sector pricingp g

Loans verses Bonds

D f l dDefault trends

LBO Model

9

F B d B M k tFour Bad Bear Markets

10

Fi i l M k t CFinancials: Market Cap

11

Hi h Yi ld S d t T iHigh Yield Spread to Treasuries

2000

1600

1800

2000

1520

1000

1200

1400

ps

15202/26/09

600

800

1000bp

0

200

400

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

12Source: Bloomberg

Hi h Yi ld B d P i (1998 02/26/09)High Yield Bond Prices (1998 - 02/26/09)

PAR

58

13Source: Bloomberg

L d B k L P i (1998 02/28/09)Leveraged Bank Loan Prices (1998 - 02/28/09)

PAR

65 1365.13

14Source: Bloomberg

Hi h Yi ld M t it S h d l (U S )High Yield Maturity Schedule (U.S.)

200

250Leveraged Loans* High Yield Bonds

150

200

ons)

100($B

illi

0

50

2008 2009 2010 2011 2012 2013 2014 >2014

*Includes Term Loans, Revolvers, and Other Loans; Assumes Revolvers are Fully Drawn.

15Source: DealLogic, Fitch Ratings

y

M k t F t Th 2007 B bblMarket Factors - The 2007 Bubble

Ed Alt Q3 2007 “42% f hi h i ld t b d i d i 2003 t d B

D efau lt R ates vs. N ew Issuance Am o un t and Qu ality

Ed Altman, Q3 2007 – “42% of high-yield corporate bonds issued since 2003 were rated B- or lower, rising to nearly 50% in the first six months of this year”

$500

$600

12.0%

14.0%

$300

$400

llion

s 8.0%

10.0%

ate

%

$200

$300

US$

in B

i

4.0%

6.0%

Defa

ult R

a

$0

$100

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 1H070.0%

2.0%

16Source: CSFB and S&P LCD. Note: 2005 default data does not include the Calpine default.

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 1H07

HY B and Lower HY S plit B B and Higher Ins t. Loan B and Lower Ins t. Loan S plit B B and Higher Com bined Default Rate

D f lt T dDefault Trends

20%

16%

20%

12%

8%

4%

0%1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

HY Default Rate Prior Recession Today's Recession

17Source: Moody’s, Bloomberg

A E it C t ib ti t LBO (2001 2007)Average Equity Contribution to LBOs (2001-2007)

50%

40%

50%Rollover Equity Contributed Equity

Average: 36 2%

40.6%

30%

Average: 36.2%

%40.0%

39.5%

35.1%32.1% 33.3% 32.9%20%

6%3% 5% 3% 2% 2% 2%0%

10%

2% 2% 2%0%2001 2002 2003 2004 2005 2006 2007

Note: Equity includes common equity and preferred stock as well as holding company debt and seller note proceeds downstreamed to the

18Source: Standard and Poor’s LCD

operating company as common equity

Thi C lThis Cycle

C dit k t t b t t i i iCredit market stress, but no systemic crisis– Residential mortgages were early indicators that the world was over levered

• Direct leverage• Structured products (CDOs CDO2)• Structured products (CDOs, CDO )• Commercial real estate

Unwind will take time

Default triggers are staggered– Cov-lite deals– PIK-Toggle bonds– Lack of DIP Financing

This distressed cycle is economically driven affecting different sectors and credits at different timesdifferent times

– NOT a “V” shape– Market timers will be unsuccessful

Long/Short strategies will outperform

19

– Long/Short strategies will outperform

Di t d St t iDistressed Strategies

The FutureProfiting from the situation

20

B i C it li i i Di t d E i tBasics—Capitalizing in Distressed Environments

U d t d t ’ f di tUnderstand a sector or company’s causes of distress

Leverage consultants and board members

Is control available or not? Hedge funds don’t ask this question

Keep powder dry for the unforeseen, even after gaining controlp p y , g g

Change management, sometimes often (family companies?)

I i i h LBO d lIncentivize management more than LBO model

Seek out add-on complimentary acquisitions

Stress-test regulatory impact/intervention

Wear a helmet

21

Wear a helmet

CS L d L R t b I d t 2008CS Leveraged Loan Returns by Industry—2008

YTD D b 2008

-10 00%

-5.00%

0.00%YTD December 2008

-15.53%-16.48%

-20.35%21 17%

-20.00%

-15.00%

10.00%

-21.17%

-23.84%-24.12%-24.15%-25.61%

-27.79%-28.22%-28.75%-29.40%-29.71%-31.09%-31.41%

-32.54%-35 00%

-30.00%

-25.00%

-37.89%-38.20%-39.34%

-40.44%

-44.32%-45.00%

-40.00%

35.00%

-50.00%

Food/Toba

cco

Healthca

reore

st Prod

ucts

Utility

Manufac

turing

Non-D

urable

sFoo

d and D

rugEne

rgyServ

ice

Metals/

Minerals

ev L

oan I

ndex

Financia

lAero

space

Chemica

lsMed

ia/Tele

com

on Tec

hnolog

y

umer Dura

bles

Retail

Gaming

/Leisu

reHous

ingTrans

portati

on

22

Fo

For MCons

umer N Fo

MetCS Le

v MeInf

ormati

onCons

um

Ga T

Source: Credit Suisse

CS L d L R t b I d t 2009

5 00%

CS Leveraged Loan Returns by Industry—2009

F b 20093.90%

2.99% 2.82%2.54%

2.29% 2.10% 1 93%

3.00%

4.00%

5.00% February 2009

1.93% 1.72%1.47% 1.44%

0.86% 0.66%0.35%

0 11% 0 22%0.00%

1.00%

2.00%

-0.11% -0.22% -0.37%-0.81%

-3.00%

-2.00%

-1.00%

-4.31%-4.35%-4.85%

-5.15%6 00%

-5.00%

-4.00%

-6.00%

Service

Food and

Drug

mation

Techno

logy

Healthca

reEne

rgyHous

ing

mer Non

-Dura

bles

Aerosp

aceFoo

d/Tobacc

o

Forest

Produc

tsFina

ncial

Metals/

Minerals

SLe

v Lo

an Ind

exMan

ufactur

ing

Media/

Teleco

mRetail

onsumer D

urable

sUtili

tyTrans

portati

on

Gaming

/Leisu

reChem

icals

23

Inform

a

Consum CS

Con

Source: Credit Suisse

C tl I t ti S t /C iCurrently Interesting Sectors/Companies

Fi i l B k d Th iftFinancials—Banks and Thrifts

Infrastructure—Chemicals, utilities, energy

Home Building/Supply sectors

Non-Bank Financials—Mortgage Lenders/Insurance Companiesg g p

Casinos

M di R di blMedia: Radio, cable, newspapers

24

V l C ti D iValue Creation Drivers

“B Ri h ” “R W ll” “R W ll”“Buy Right” “Restructure Well” “Run Well”

DUE DILIGENCE ANDT

REORGANIZATION PHASEPOST-REORGANIZATION

ACQUISITION PHASE

REORGANIZATION PHASEPHASE

Expeditiously conduct due dili

Manage and dominate the i ti

Set agenda for management d b d i till “ fdiligence

Establish toe-hold position in fulcrum securities

d i f i f i

reorganization process

Replace management when necessary

d if i l l

and board—instill “sense of urgency”

Active board member

id i l i “Trade price for information”

Execute transactions in a highly expedited time frame

Identify optimal plan to satisfy most other stakeholders

Use bankruptcy process to

Provide strategic planning

Provide capital markets expertise

Advantage of non-disclosure Use bankruptcy process to shed business units, reject contracts, negotiate terms

Define business plan

Pursue selective acquisitions and divestitures

Aggressively manage exit opportunities

25

p

Creative structuring to solve intractable problems

opportunities

C t M k t C ditiCurrent Market Conditions

Old Playbook New TwistsOld Playbook, New Twists

26

R t t i T dRestructuring Trends

C hi l hCap structures this cycle are top heavy

DIP Financing is scarceg

Justice system is moving rapidly

Many players were early and have tainted portfolios

Little to no refinancing interest at the top of capital structures (banks are not lending and structured products are out of the market)

27

NRG C St d P t E (Old St l )NRG: Case Study: Post-Enron (Old Style)

M h ffili f E l EMerchant power affiliate of Excel Energy

$10B in NRG debt, no core holders of size – i.e. control is available

Retain R W Beck to evaluate 63 power plants around the world – outside/in due diligenceRetain R.W. Beck to evaluate 63 power plants around the world outside/in due diligence

Build intricate asset-by-asset model to predict sub debt recoveries 3 years hence

Acquire large blocks of sub debt in publicly traded markets without NRG’s knowledge

Meet with CEO of Excel to fine tune parent settlement offer to creditors

Hire NRG CEO through creditor committee, 7 months emergence from bankruptcy

3 MatlinPatterson Partners on 11 person board

MPAM controls 20% of NRG; 2nd largest shareholder controls 1%

$6 billion of emergence financing and refinancing – no NRG CFO

Re-list (IPO) NRG stock on NYSE

MatlinPatterson exits in 3 public secondaries monetizing 3X

28

MatlinPatterson exits in 3 public secondaries monetizing 3X

NRG B f Ch t 11 (Old St l ) 2002NRG: Before Chapter 11 (Old Style) - 2002

Secured DebtSecured Debt$4,000,000,000

Unsecured Debt$5 000 000 000$5,000,000,000

Total Debt: $9B

29

N C t l Pl T E lNon-Control Players Too Early…

Masonite*Masonite

30*Numbers are rounded to make the math easy.

M it *Masonite*

2006 KKR l d $3 1B d l2006 KKR led $3.1B deal

332mm EBITDA in 2006 Bank Debt$1 500 000 000

$2.27B debt

$650mm of equity

$1,500,000,000L+250

$650mm of equity

Equity

Junk Bonds$770,000,000

Equity$650,000,000

31*Numbers are rounded.

M it * Hit Th W ll 2008 Fi t H lf R ltMasonite Hits The Wall—2008 First Half Results

S l d li d 16 1% $972 1 f $1 158 3 i h fi i hSales declined 16.1% to $972.1mm from $1,158.3 mm in the first six months of 2007

O ti EBITDA d d 42 8% t $92 8 f $162 2Operating EBITDA decreased 42.8% to $92.8 mm from $162.2 mm

Adjusted EBITDA decreased 39.5% to $109.5 mm from $181.0 mm

Adjusted EBITDA margin decreased to 11.3% from 15.6%

Net debt increased $124.9 mm to $2,035.2 mm on June 30, 2008Net debt increased $124.9 mm to $2,035.2 mm on June 30, 2008

32*Numbers are rounded.

M it * T t l E t i V l ti Q4 2008Masonite Total Enterprise Valuation—Q4 2008

2006 LBO $3.1B

Bank Debt$1,500,000,000

November 2008 $1.5B

Bank Loan Value$1,200,000,000Junk Bonds

$770,000,000Bank Debt trading @ 80

Bank Loan Value$1,200,000,000

Bond Value$300,000,000

Equity$650,000,000 Bonds trading @ 40 Bond Value

$300,000,000

33*Numbers are rounded.

M it * I t ti l Pl P k M h 2009Masonite International Plan – Prepack March 2009

B k $300 d b 97 5% f iBanks get $300mm new debt, 97.5% of equity

Senior Subordinated Notes: 2.5 % of equity, plus warrants for 17.5%

Trade is unimpaired due to $160mm cash on the books

KKR Equity: NothingKKR Equity: Nothing

34*Numbers are rounded.

M it * T dMasonite Today

2006 LBO $3.1 Billion

Bank Debt$1,500,000,000

November 2008$1.5 Billion

J k B d

March 2009$550 Million

Equity

Junk Bonds$770,000,000

Bank Loan Value$1,200,000,000

New Loans$300,000,000

New Loans$300,000,000

Equity$650,000,000 Bond Value

$300,000,000

Equity$250,000,000

Bank Debt trading @ 36

Equity$250,000,000

35*Numbers are rounded.

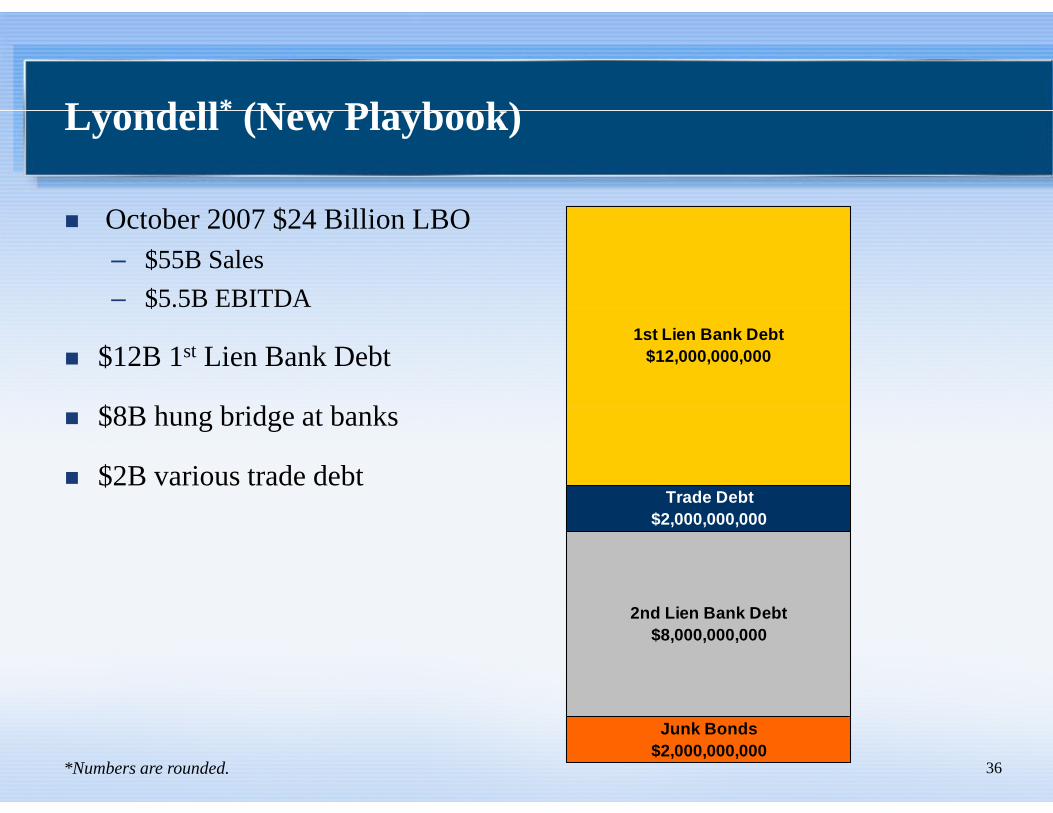

L d ll* (N Pl b k)Lyondell (New Playbook)

O b 2007 $24 Billi LBOOctober 2007 $24 Billion LBO – $55B Sales– $5.5B EBITDA$

$12B 1st Lien Bank Debt

$8B h b id b k

1st Lien Bank Debt$12,000,000,000

$8B hung bridge at banks

$2B various trade debtTrade Debt

$2,000,000,000

2nd Lien Bank Debt$8,000,000,000

36

Junk Bonds$2,000,000,000

*Numbers are rounded.

L d ll* R llLyondell – Roll up

O i i l D bt St t DIP R ll

DIP Financing$3,250,000,000

Original Debt Structure DIP Roll up

Trade Debt$2,000,000,000

Roll up$3,250,000,000

Old 1st Lien Bank Debt$8,750,000,000

1st Lien Bank Debt$12,000,000,000

Trade Debt$2,000,000,000

2nd Lien Bank Debt$8,000,000,000

2nd Lien Bank Debt$8,000,000,000

37

Junk Bonds, $2,000,000,000

Junk Bonds$2,000,000,000

*Numbers are rounded.

L d ll* C t V l tiLyondell – Current Valuation

P t DIP R ll T t l V l ti $7 9BDIP Financing$3,250,000,000

Post DIP Roll up

DIP trading @ 95

Total Valuation $7.9B

Trade Debt$2,000,000,000

Roll up$3,250,000,000 Roll up trading @ 95

Super Senior$6,200,000,000

Old 1st Lien Bank Debt$8,750,000,000 Old 1st Lien trading @ 15

Old 1st Lien Bank Debt$1,300,000,000

2nd Lien Bank Debt$8,000,000,000 Not trading

38

2nd Lien Bank Debt$400,000,000

Junk Bonds, $2,000,000,000 Not trading

*Numbers are rounded.

L d ll* (N Pl b k) F b R t t iLyondell (New Playbook) – February Restructuring

1 t Li b k d b i fili d d 451st Lien bank debt prior to filing traded at 45

DIP financing created $3.25B Super Senior

Roll up of existing 1st Lien by new money DIP providers upgraded $3.25 Billion of 1st Lien debt

Value transfer of roll up is $3.25B x (Super Senior Price of 95 – 1st Lien post re-org price of 15) = $2.6B

New cap structure creates fulcrum security potential down the road for private equity distressed control player

39*Numbers are rounded.

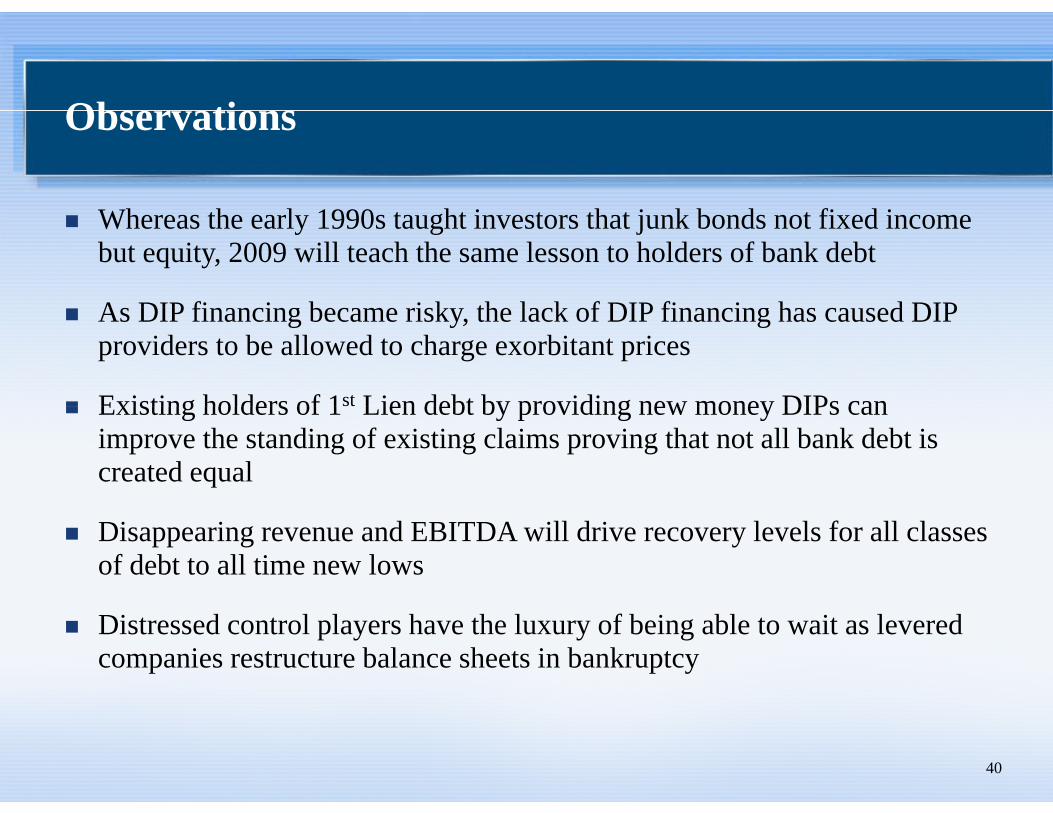

Ob tiObservations

Wh h l 1990 h i h j k b d fi d iWhereas the early 1990s taught investors that junk bonds not fixed income but equity, 2009 will teach the same lesson to holders of bank debt

A DIP fi i b i k th l k f DIP fi i h d DIPAs DIP financing became risky, the lack of DIP financing has caused DIP providers to be allowed to charge exorbitant prices

Existing holders of 1st Lien debt by providing new money DIPs canExisting holders of 1 Lien debt by providing new money DIPs can improve the standing of existing claims proving that not all bank debt is created equal

Disappearing revenue and EBITDA will drive recovery levels for all classes of debt to all time new lows

Distressed control players have the luxury of being able to wait as levered companies restructure balance sheets in bankruptcy

40

P ibl O t /C l iPossible Outcomes/Conclusions

C B k D b P i i M M k SCurrent Bank Debt Pricing May Make Sense

Recovery levels for Junk and Loans will be shocking

The Cost to Companies of Leverage could be permanently more expensive

DIP Lending will attract capital (Buyout dollars from PE)g p ( y )

Restructuring time frames will be lengthened

b l h ld i f i hAbsolute Managers should continue to outperform in the space

41

Di t d I tiDistressed Investing

Q & AQ & A

42

E l t N tExplanatory Notes

Thi i d i ff f i i i d i iThis presentation does not constitute an offer of any securities or investment advisory services.Any such offer may be made only by means of a definitive private offering memorandum whichwill contain a description of material terms and risks.

This presentation which has been furnished on a confidential basis is exclusively for the use ofThis presentation, which has been furnished on a confidential basis, is exclusively for the use ofthe person to whom it has been delivered by MatlinPatterson Capital Management, L.P., and it isnot to be reproduced or redistributed to any other person.

All information contained herein concerning the Fund is subject to revision and completion ForAll information contained herein concerning the Fund is subject to revision and completion. Forall of the foregoing reasons as well as other factors, past performance data contained hereincannot be construed as a prediction or indication of future results.

43

Now this is not the end It is not even theNow this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.

Wi Ch hill~Winston Churchill

44