Disclosure Statement Training: Departmental Administrators & Business Managers Basic Understanding...

39

Disclosure Statement Training: Departmental Administrators & Business Managers Basic Understanding of A-21, CASB, and DS2

-

Upload

tony-moxham -

Category

Documents

-

view

215 -

download

0

Transcript of Disclosure Statement Training: Departmental Administrators & Business Managers Basic Understanding...

Disclosure Statement Training: Departmental Administrators & Business Managers

Basic Understanding of A-21, CASB, and DS2

Disclosure Statement Training: Departmental Administrators & Business Managers

Presentor:Carolyn B. Taylor, Contracts and Grants Division([email protected])

Disclosure Web Site:www.busfin.uga.edu/disclosureAll Policies and Procedures related to the University Disclosure Statement may be found under the Disclosure Policies and Disclosure Procedure links

Policies are effective January 1, 2006

Training Offered Beginning in March 2006

Basic Understanding of A-21, CASB, and DS2 Cost Transfers, Program Income, & Cost Share Direct and F&A Costs Time and Effort Reporting Service Centers Account Maintenance & Close-out

You are Here Beginning in March 2006

Basic Understanding of A-21, CASB, and DS2

Why are you here?

What you should gain?

A better communication between C&G and departmental administrators/business managers concerning the new policies.

A better understanding of how A-21 and CASB effects what we do.

Course Objectives 1. What is A-21, CASB, and DS2? 2. Provide a basic understanding of DS2, CASB, and

OMB A-21 and how they fit together. 3. Will I ever use this in my Job? 4. Why are they important to me? 5. How can I ensure financial compliance? 6. Understanding the roles of OSP, Principle

Investigators, Departments Administrators and Business Managers and Contract & Grants.

Definitions What is A-21, CASB, and DS2? A-21 is the cost principles for higher

institutions as defined by the Office of Management and Budgets (OMB).

CASB is the Cost Accounting Standard Board.

DS2 is required for institutions of higher education and it states UGA’s policy and procedures regarding cost accounting practices.

What is DS2(Disclosure Stmt 2)? Documents and discloses the University cost accounting

practices Required to be submitted to cognizant agency and

cognizant audit agency. Policies and procedures, instructions, and guidelines for

individual investigators, department heads, and administrators need to be made available because it is their responsibility to understand and know them.

Provides Guidelines for “charging costs to sponsored awards” Defines University direct costing policies and procedures Cost-sharing policies Time and effort reporting policies and procedures Policies on “Service Centers”

How was it Developed?

Three working group committees were formed comprised of College and Departmental Business Managers and Faculty representatives

Steering Committee comprised of Associate/Assistant Deans, Department Head, and Center Director representatives

What does it do?

New Policies Cost Transfer Program Income Service Center

Existing Policies – Revised Cost Share Direct Cost Personnel Activity Report

What brought about the DS2?

A-21, A Federal Policy Document issued by OMB (Office of Management and Budget) which all Universities nation-wide must follow.

I thought it was just UGA?

Governing Body Federal funding is appropriated by

Congress, and it is allocated by the Office of Management and Budget (OMB).

The office of Management and Budget ensures proper stewardship of federal funding through prescribed cost principles, and administrative and audit requirements. (A-21, A-110, and A-133)

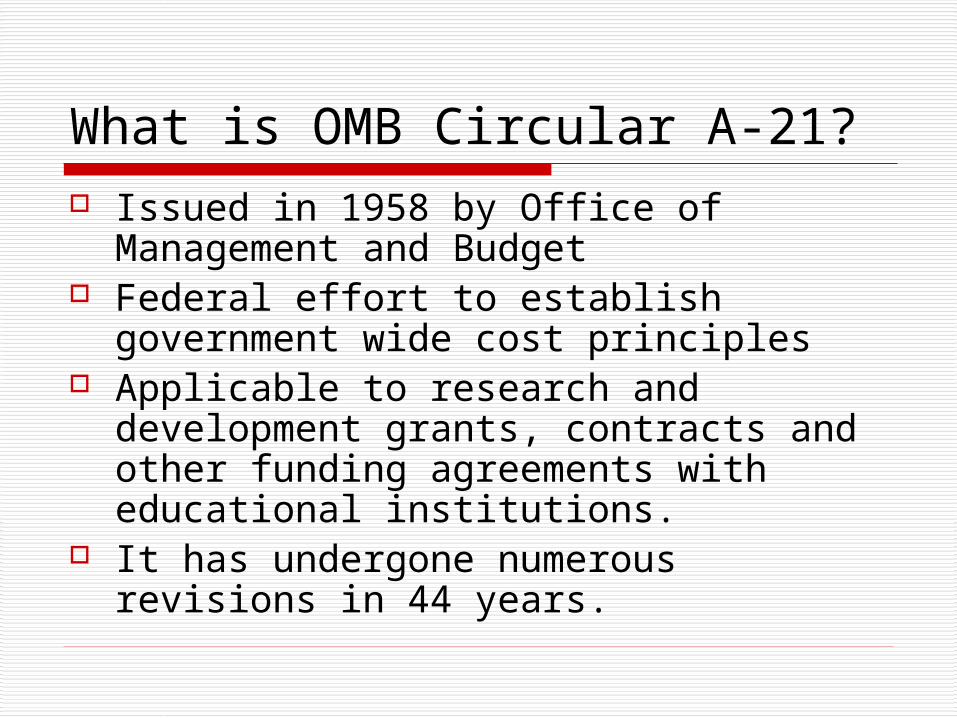

What is OMB Circular A-21? Issued in 1958 by Office of

Management and Budget Federal effort to establish government

wide cost principles Applicable to research and

development grants, contracts and other funding agreements with educational institutions.

It has undergone numerous revisions in 44 years.

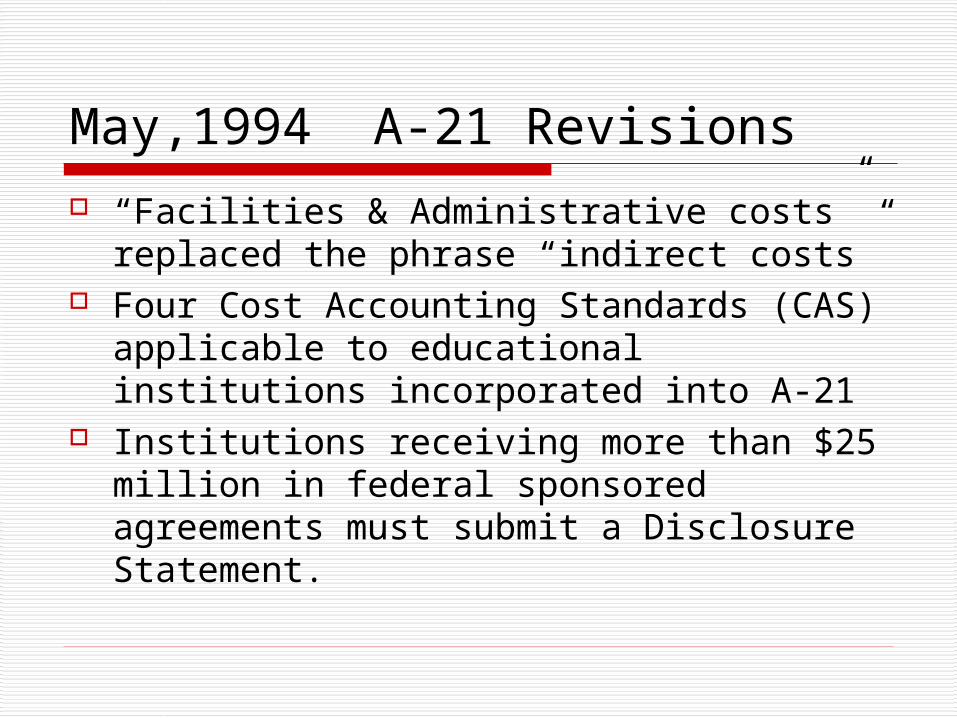

May,1994 A-21 Revisions

“Facilities & Administrative costs” replaced the phrase “indirect costs”

Four Cost Accounting Standards (CAS) applicable to educational institutions incorporated into A-21

Institutions receiving more than $25 million in federal sponsored agreements must submit a Disclosure Statement.

What is the purpose of the A-21?

The A-21 tells us what we need to do. It tells us we must be consistent.

Defines allowable and unallowable costs

Defines methods of F&A cost rate identification and calculation.

http://www.whitehouse.gov/omb/circulars/index.html

Who cares?

Will I Ever Use this in my job? Each of us are fiscal agents of the

University It is everyone’s responsibility to be

knowledgeable of University Policies and Procedures

Ignorance of the policies and procedures is not an excuse for not following them.

Why do I care about the rules? University of Alabama - $3.4 million in fines

for applying resources from an existing grant toward a new project

Harvard University- $3.3 million settlement. Improper Accounting on Federal Grant for “effort reporting” or “salary accounting”

Northwestern University - $5.5 million settlement

Johns Hopkins University - $2.6 Million Settlement

What does the A-21 Cost Principles do?

Requires a cost Be allowable Be allocable Be reasonable (prudent person test) Be treated consistently Be necessary to perform the aims of

the project Be permissible under the law

Specific Rules on Cost Allowability

Section J of Circular A-21 (hand out) Currently describes 54 types of costs Alphabetical order For some costs, also specifies

approval requirements, documentation and other provisions.

What can I do to ensure financial compliance for federally funded projects?

Ask yourself the following questions: Are you direct charging costs that are

facility and administrative (F&A)? Toner or paper for the printer, General office supplies or equipment

Are you shifting costs from grant to grant to use up the balance?

Are you charging salaries of individuals who do not work on the project?

Questions to ask (con’t)

Do you have adequate internal control procedures to avoid errors in charging the Federal government?

Are you charging costs without authorization?

Are you maintaining properly authorized timesheets for Biweekly and Salaried?

Questions to ask (con’t)

Are you reviewing status reports on a regular basis?

Are you removing encumbrances within four – six months after the project is completed?

Are you documenting adequately for cost transfers?

Questions to ask (con’t)

Are you reimbursing subcontractors and consultants with verifying if the service is completed?

Are you tracking the cost sharing committed?

Questions to ask (con’t)

Are you managing federally funded equipment properly?

What happens if we are not in compliance?

Audits

What types of Audits are there: Departmental Audits (Internal Audit) Compliance Audits (Internal Audit, State

Audits, Regents Audits, Sponsoring Agency Audits, and Federal Audits)

Annual OMB A-133 Audits Project Specific Programmatic and

Financial Audits (Office of Inspector General, OIG)

Audits

The purpose of an audit is to verify that we are doing what we say we are doing.

The auditors are testing our controls and detail transaction. They will request financial supporting documents such as time sheets, invoices, purchase orders and receipts.

Responsibilities

OSP – Review and approve proposal

packages and provide final approval on CAS exceptions and justifications.

Provide necessary assistance Provide CAS Exception approval when

appropriately justified by PI and Department

ResponsibilitiesPrincipal Investigator Prepares the proposal and complies with

the requirements. If need for subcontracts he collects

authorized budget and work statements from each subcontractor.

Prepares the budget and justification in accordance with allowable cost principles and applies the appropriate F&A rate.

If matching funds or in-kind contributions, secures written approval from each contributor.

Responsibilities

Principal Investigator (con’t) If any financial conflict of interest,

discloses existence. Routes completed information to

Office for Sponsored Programs (OSP) Pre-award spending or extensions of

time Scope of work and any modifications

and approval

ResponsibilitiesPrincipal Investigator (con’t) initiation of programmatic changes to the project initiation of hiring or assignment process and approval

of personnel assigned to the project assurance of integrity and safeguarding of notebooks

and scientific data compliance with timely submission of accurate interim

programmatic (technical) reports assurance of quality, timeliness, and programmatic

performance of subcontracts initiation of materials transfer agreement when

receiving biological materials from an outside source.

Responsibilities

Principal Investigator (con’t) Initiates expenditure of funds Initiates allocation of cost sharing

dollars if applicable Reviews invoices from and approves

payments to subcontractors Initiates request for rebudgeting Requests for cost transfers – if greater

than 90 days, must sign

Responsibilities

Principal Investigator (con’t) Reviews restricted account status reports

and resolves errors in timely manner When appropriated, request access to

residual balances Complies with requirements of the

personnel activity reports Prepares final programmatic narrative

report

Responsibilities

Department Administration and Business Managers:

Monthly reconciliation of project costs PAR forms Cost transfers Following UGA policy and procedures

Responsibilities

Contract & Grants: Monthly, Quarterly, Predetermined

and Final reports/billings Budget Amendment Reviews Establish Projects Establish Account Numbers

Responsibilities

Contract & Grants (con’t): Approve Cost Transfers Approve PAR’s Available to answer questions

www.busfin.uga.edu/disclosure

Summary

DS2 CASB OMB A-21 Training classes

Any Questions?