Disclaimer - Clipper Logistics · Disclaimer This presentation ... o E-fulfilment and returns...

30

Transcript of Disclaimer - Clipper Logistics · Disclaimer This presentation ... o E-fulfilment and returns...

2

Disclaimer

This presentation includes statements that are, or may be deemed to be, “forward-looking statements”. These forward-looking

statements can be identified by the use of forward-looking terminology, including the terms “believe”, “estimates”, “plans”, “projects”,

“anticipates”, “expects”, “intends”, “may”, “will”, or “should” or, in each case, their negative or other variations or comparable

terminology. These forward-looking statements include matters that are not historical facts and include statements regarding the

Company’s intentions, beliefs or current expectations.

Any forward-looking statements in this presentation reflect the Company’s current expectations and projections about future events. By

their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could cause actual results or

events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and

assumptions could adversely affect the outcome and financial effects of the plans and events described herein. Forward-looking

statements contained in this presentation regarding past trends or activities should not be taken as a representation that such trends or

activities will continue in the future. You should not place undue reliance on forward-looking statements, which speak only as of the

date of this presentation. No representations or warranties are made as to the accuracy of such statements, estimates or projections.

Please note that the Directors of the Company are, in making this presentation, not seeking to encourage shareholders to either buy or

sell shares in the Company. Shareholders in any doubt about what action to take are recommended to seek financial advice from an

independent financial advisor authorised by the Financial Services and Markets Act 2000.

3

Agenda

Highlights – Steve Parkin, Executive Chairman 1

Financial review – David Hodkin, Chief Financial Officer 2

Operational review – Tony Mannix, Chief Executive Officer

o Retail Focused Click and Collect

3

Summary and Q&A – Steve Parkin, Executive Chairman 4

Highlights – Steve Parkin,

Executive Chairman 1

4

5

Highlights – Financial*

Group revenue growth of 23.7% to £290.3m (2015: £234.8m), driven by strong growth in all divisions

Group Adjusted EBIT growth of 21.0% to £14.5m (2015: £12.0m):

o E-fulfilment and returns management services – EBIT of £8.1m, up 47.6% (2015: £5.5m)

o Non e-fulfilment logistics – EBIT of £10.7m, up 6.4% (2015: £10.1m)

o Commercial vehicles – EBIT of £2.3m, up 20.8% (2015: £1.9m)

Adjusted EPS of 10.3p, up 22.6% (2015: 8.4p); basic EPS up 41.1%

Proposed final dividend of 4.0 pence per share; total dividend of 6.0p per share

Net debt £18.8m; debt: EBITDA 0.96x

* The highlights are for the 12 months ended 30 April 2016, as compared to the 12 months ended 30 April 2015

Financial review – David Hodkin,

Chief Financial Officer 2

6

7

Summary Income Statement

Headline financials

Strong top-line performance in the year in all business

segments.

EBIT is the key metric, and saw further strong growth driven

by:

o contract evolution in the logistics business

o strong performance in commercial vehicles

o full year benefit of Servicecare (acquired Dec 2014).

No discontinuing or exceptional costs in current financial year.

Finance costs in line with prior year.

Dividends

Interim dividend of 2.0 pence per share, paid December 2015.

Final proposed dividend 4.0 pence per share, giving total

dividend of 6.0 pence per share (4.8 pence year to 30 April

2015).

1. Discontinuing costs comprise certain advertising, sponsorship and corporate entertaining expenses,

consultancy and professional fees in respect of potential investment opportunity appraisals and the costs of

operating the Chairman’s private office – all of which ceased at IPO

2. Exceptional costs comprise £0.6m IPO transaction costs and £0.2m costs in relation to the Servicecare

acquisition

3. EPS adjusted for discontinuing and exceptional costs and the tax thereon

£m Year to 30 April Change

2016 2015 %

Revenue 290.3 234.8 23.7%

Cost of sales (205.7) (165.6)

Gross profit 84.6 69.2

Other net gains 0.2 0.3

Admin expenses (70.3) (57.5)

Adjusted EBIT 14.5 12.0 21.0%

Discontinuing costs1 - (0.3)

Exceptional costs2 - (0.8)

Operating profit 14.5 10.9

Net finance costs (1.4) (1.4)

Profit before tax 13.1 9.5

Income tax (2.8) (2.2)

Net income 10.3 7.3

Earnings per share (p) 10.3 7.3

Adjusted earnings per share3(p) 10.3 8.4 22.6%

8

Continued strong growth in Logistics:

o Full year benefit of Servicecare (included within

e-fulfilment & returns management services), which

was immediately earnings- enhancing.

o Organic growth on existing contracts in both

e-fulfilment (Asos, SuperGroup, Wilko and John

Lewis), and non e-fulfilment (British American

Tobacco, SuperGroup, Bench and Sainsbury’s).

o Full year benefit of prior year contract wins including

Philip Morris.

o Part-year impact of wins in the year including M&Co,

Zara, Haddad and Pep&Co.

Strong growth in commercial vehicles driven by new vehicle

sales and aftersales.

£m Year to 30 April Change

2016 2015 %

E-fulfilment & returns management services 97.6 60.6 61.1%

Non e-fulfilment logistics 108.4 102.1 6.1%

Total value-added logistics services 206.0 162.7 26.6%

Commercial vehicles 85.6 73.6 16.4%

Inter-segment sales (1.3) (1.5)

Group total1 290.3 234.8 23.7%

£m Year to 30 April Change

2016 2015 %

E-fulfilment & returns management services 8.1 5.5 47.6%

Non e-fulfilment logistics 10.7 10.1 6.4%

Central logistics overheads (4.7) (4.1)

Total value-added logistics services 14.1 11.5 22.5%

Commercial vehicles 2.3 1.9 20.8%

Head office costs (1.9) (1.4)

Group total2 14.5 12.0 21.0%

Revenue

Adjusted EBIT

1. Excluding the impact of the Servicecare acquisition, Group revenue grew by 19.7%

2. Excluding the impact of the Servicecare acquisition, Group Adjusted EBIT grew by 16.5%

Segmental and business activity performance

9

Summary cash flow statement

Strong cash flow generated from operations: £17.1m (2015:

£9.7m).

Favourable working capital profile maintained.

£2.2m of deferred consideration paid relating to the

acquisition of Servicecare.

Capex incurred on new contracts including Zara, John Lewis

ancillary shed and Click & Collect largely recoverable over

contract terms through open book mechanism.

Dividends paid in line with stated policy at IPO.

£m Year to 30 April

2016 2015

Adjusted EBIT 14.5 12.0

Depreciation & amortisation 5.0 3.6

Other non-cash items1 0.5 0.1

Change in working capital 0.6 (0.6)

Net interest paid (1.4) (1.2)

Tax paid (2.1) (1.7)

Net cash flows before non-recurring items 17.1 12.2

Net cash flow on non-recurring items2 - (2.5)

Net cash flows from operating activities 17.1 9.7

Acquisition (2.2) (3.7)

Net capital expenditure (5.7) -

Net cash flows from investing activities (7.9) (3.7)

Net advance from/(repayment to) former parent - (14.2)

Net drawdown / (repayment of) bank loans (3.9) 9.6

Finance leases advanced 0.2 0.1

Repayment of capital on finance leases (3.2) (3.0)

Dividends paid (5.2) (1.9)

Net cash flows from financing activities (12.1) (9.4)

Net (decrease) / increase in cash & cash equivalents (2.9) (3.4)

1. Other non cash items comprise exchange differences share based payments, and movement in fair value of derivatives

2. Cash impact of discontinuing and exceptional costs which are described on slide 7

10

Summary balance sheet

Investment in fixed assets mainly incurred on new open

book contracts.

Net current liabilities position affects continuing positive

working capital model.

Net debt: EBITBA < 1.0.

New banking facilities put in place with Santander.

Unused facility as at 30 April 2016 £20.4m.

£m As at 30 April

2016 2015

Intangible assets 24.9 24.8

Property, plant & equipment 25.6 14.6

Non-current assets 50.5 39.4

Inventories 26.2 21.7

Trade & other receivables 39.9 33.4

Cash & cash equivalents 0.7 1.9

Current assets 66.8 57.0

Trade & other payables 72.2 61.7

Borrowings 6.6 5.3

Short term provisions 0.1 0.1

Current tax liabilities 1.7 0.7

Current liabilities 80.6 67.8

Borrowings 12.9 10.2

Long term provisions 0.8 0.8

Deferred tax liabilities 0.2 0.6

Non-current liabilities 13.9 11.6

Net assets 22.8 17.0

Net debt 18.8 13.6

Operational review – Tony Mannix,

Chief Executive Officer 3

11

12

New shared use site in Northampton – John Lewis the anchor

customer. The facility combines inbound pre-retail, forward orders and

Boomerang and is a main injection hub for Click & Collect.

New 2 year contract extension agreed with Wilko.

Enhanced processing operations set up for Asos, further developing the

Boomerang solution – spot dry cleaning, hand finishing, sewing and

buttoning.

Browns (a Farfetch brand) contract start up.

E-commerce update

13

Non e-commerce update

Growth in activities under Philip Morris contract, with the successful start-

up of “Package 2” (cigarettes).

Successful implementation of new 4 year national distribution contract for

M&Co.

Haddad/Flyers (Nike and Converse children’s products) new 3 year

contract signed with a requirement to double capacity.

Commenced additional packing activity with certain tobacco customers.

Retail Focused Click & Collect The New Model

15

Online sales in John Lewis

10% 12%

14% 17%

21%

26% 29%

33%

2007 2008 2009 2010 2011 2012 2013 2014

Online % share of trade

Continued strong growth

in online

Online represents 1/3 of

the JL business during the

last trading year

16

Click & Collect in John Lewis

0.8 1.4

2.8

4.3

6.5 7.1

2010 2011 2012 2013 2014 2015

Parcels (m)

Click & collect underpins

online growth

53% of online sales in

2015 via this channel

17

Customers are increasingly intolerant

18

The Click & Collect solution was developed to enhance carrier

solutions by creating a retail focused operational process

Fully integrated into the retailer on-line systems.

Full track & trace.

Next day delivery against a timed delivery schedule.

Parcels sorted into cages at sorter hub – parcel to cage “parent & child”

association to ease store handling/storage and efficiently provide in-store system

updates – complete transparency throughout.

Able to fully integrated with in-store systems to provide enhanced customer care

at store location.

Ease of returns via the network to provide potential for same day “Boomerang”

processing.

19

Volume & Retail

Knowledge

Retail Delivery

Established network

Track & Trace System CMS Providers

In-house Parcel Carrier

Expertise

Key Elements of the Solution

20

Track & Trace – Full Visibility

21

Customer Order Tracking

Mrs Smith

23

Phase 1

25

Shared user Developments

26

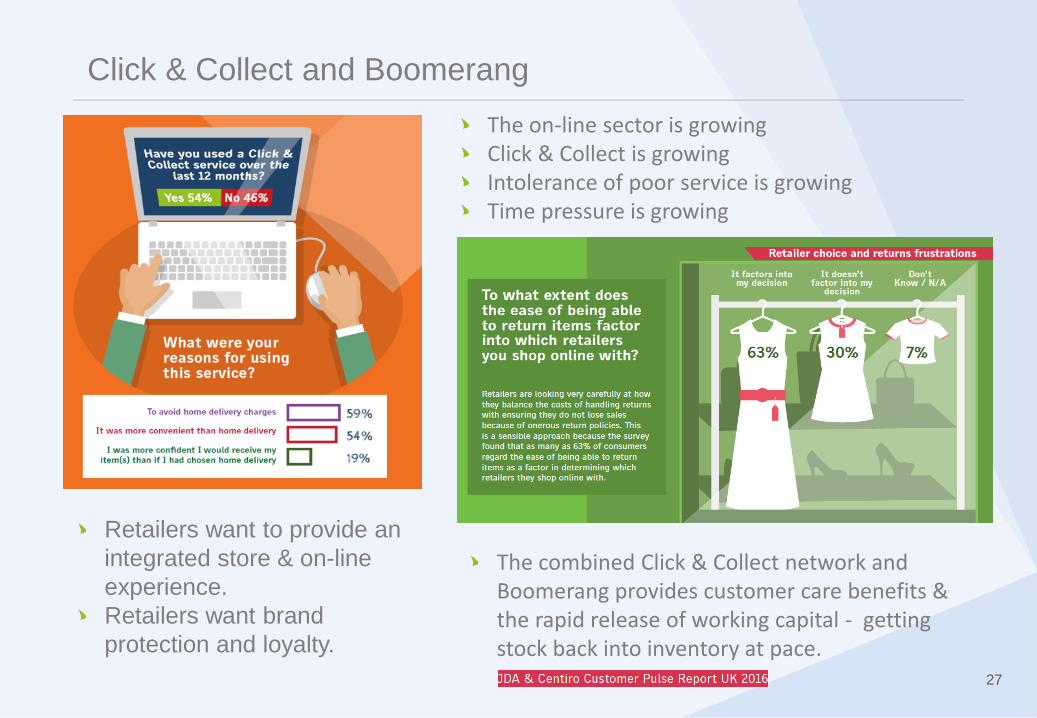

JDA & Centiro Customer Pulse 2016 Voice of the Online Customer

Key Findings from the 2016 UK Customer Pulse Survey: 53% UK adults experienced issues with online orders over the past 12 months (47% in 2015) 73% UK consumers would be likely to switch to an alternative retailer as a result of a

poor online experience (71% in 2015) Click & Collect continues to grow – 54% UK adults used C&C over last 12 months (49% in 2015)

UK: year-on-year sales in Q1 2016 grew at 15% [IMRG]

The online shopping revolution is set to continue:

Online sales in the UK, US, Germany and China will double in size over the next three year [OC&C Strategy Consultants, PayPal and Google]

26

27

Click & Collect and Boomerang

The on-line sector is growing Click & Collect is growing Intolerance of poor service is growing Time pressure is growing

Retailers want to provide an

integrated store & on-line

experience.

Retailers want brand

protection and loyalty.

The combined Click & Collect network and Boomerang provides customer care benefits & the rapid release of working capital - getting stock back into inventory at pace.

Reduced handling

Reduced transportation costs

Improved stock availability

Split orders can be

consolidated via the solution

“Enhanced” Integrated Click & Collect & Boomerang

28

29

Customers Want Efficient Choice

“Agility and ability” will be

vital to meet customer

aspirations – innovation

will be essential

Clipper will meet the

challenge

Summary and Q&A – Steve Parkin,

Executive Chairman 4

30