DIOCESE OF RIVERINA - Anglican Diocese of Tasmania

53

DIOCESE OF TASMANIA Insurance & Claims Procedure Manual for Parishes/Diocesan Entities 2010 Version 6.2

Transcript of DIOCESE OF RIVERINA - Anglican Diocese of Tasmania

DIOCESE OF TASMANIA

Insurance & Claims Procedure Manual for Parishes/Diocesan Entities 2010

Version 6.2

INDEX

Section Page

1. INTRODUCTION..................................................................................................................................... 1 STATUTORY NOTICES ................................................................................................................................ 1

Duty of Disclosure .............................................................................................................................. 1 Non-disclosure ................................................................................................................................... 1 Contracts Affecting Insurer's Rights to Recover from Third Parties................................................... 2

INCIDENT REPORTING ................................................................................................................................ 2 2. INSURANCE CONTACTS...................................................................................................................... 3

DIOCESAN INSURANCE CONTACTS:............................................................................................................. 3 ANGLICAN NATIONAL INSURANCE PROGRAM (ANIP) CONTACTS: ................................................................. 3

3. FREQUENTLY ASKED QUESTIONS .................................................................................................... 4 PROPERTY INSURANCE....................................................................................................................... 4

1. Do we have a claim? ............................................................................................................... 4 2. How do we make a claim?....................................................................................................... 4 3. How do we set our insurance values?..................................................................................... 4 4. Is property belonging to Employees and Volunteers insured?................................................ 4 5. Is property belonging to other people insured?....................................................................... 5

PUBLIC LIABILITY INSURANCE ............................................................................................................ 6 1. Are activities away from the Parish/Diocesan Entity included?............................................... 6 2. Is the liability of staff members insured? ................................................................................. 6 3. How do we show the Parish/Diocesan Entity has Public Liability Insurance? ........................ 6 4. Does our Public Liability insurance extend to include the Indemnity Clauses in contracts with Suppliers? .......................................................................................................................................... 6

VOLUNTEERS ........................................................................................................................................ 6 1. Are volunteers covered by Insurance?.................................................................................... 6

HIRE OF PARISH/DIOCESAN ENTITY PROPERTY.............................................................................. 6 1. Who must have Public Liability Insurance?............................................................................. 6 2. Can we arrange Public Liability Insurance for Hirers? ............................................................ 6

4. CLAIMS PROCEDURE........................................................................................................................... 7 INCIDENT REPORTING ................................................................................................................................ 7 PROPERTY ................................................................................................................................................ 7 PROPERTY IN TRANSIT ............................................................................................................................... 8 PUBLIC LIABILITY ....................................................................................................................................... 9 PROFESSIONAL INDEMNITY, MANAGEMENT LIABILITY (INCLUDING DIRECTORS & OFFICERS LIABILITY, EMPLOYMENT PRACTICES LIABILITY, STATUTORY LIABILITY) ...................................................................... 10 VOLUNTEERS PERSONAL ACCIDENT BUSINESS TRAVEL ......................................................................... 10 MOTOR VEHICLE...................................................................................................................................... 10

5. INSURANCE PROGRAM SUMMARY ................................................................................................. 11 LIST OF INSURANCES................................................................................................................................ 11

6. INSURANCE PROGRAM DETAILS..................................................................................................... 13 INDUSTRIAL SPECIAL RISKS ............................................................................................................. 13 EXCESS FIDELITY GUARANTEE/FRAUDULENT FUNDS TRANSFER............................................. 14 PUBLIC & PRODUCTS LIABILITY........................................................................................................ 15 PROFESSIONAL INDEMNITY.............................................................................................................. 16 MANAGEMENT LIABILITY ................................................................................................................... 17

Comprising the following Sub-Sections:........................................................................................... 17 I) DIRECTORS & OFFICERS LIABILITY - COVER FOR INSURED INDIVIDUALS.................................................... 17 II) ENTITY REIMBURSEMENT - COVER FOR PAYMENTS BY THE ENTITY TO DIRECTORS / OFFICERS .................. 17 III) ENTITY (ORGANISATION) LIABILITY - COVER FOR THE ENTITY BEING SUED IN ITS OWN RIGHT.................... 18 IV) EMPLOYMENT PRACTICES LIABILITY - COVER FOR BREACHES IN EMPLOYMENT LEGISLATION ................... 18 V) TRUSTEES LIABILITY - COVER FOR BREACHES IN TRUSTEE RESPONSIBILITIES .......................................... 18 VI) STATUTORY LIABILITY - COVER FOR FINES & PENALTIES FOLLOWING BREACHES OF SOME COMMONWEALTH / STATE ACTS .......................................................................................................................................... 19 VII) INTERNET LIABILITY - COVER FOR THE ENTITY’S INTERNET ACTIVITIES.................................................... 19 VIII) ENTITY CRISIS LIABILITY - COVER FOR THE ENTITY ARISING OUT OF A CRISIS LOSS ................................ 19

Parish Manual Page

i

Parish Manual Page

ii

VOLUNTEERS PERSONAL ACCIDENT .............................................................................................. 20 TRANSIT – CLERGY & EMPLOYEE TRANSFERS........................................................................................ 21 MOTOR VEHICLE................................................................................................................................. 22 CONSTRUCTION SPECIAL RISKS...................................................................................................... 23

i) Property Damage .......................................................................................................................... 23 ii) Public Liability............................................................................................................................... 23

HIRER’S LIABILITY (HIRE/USE OF PARISH/DIOCESAN ENTITY PROPERTY) ............................................... 24 BUSINESS TRAVEL ............................................................................................................................. 26 STALLHOLDERS PUBLIC LIABILITY................................................................................................... 27

Insured: ............................................................................................................................................ 27 Special note: Cover is available only on application by Market Operators................................... 27

PERSONAL ACCIDENT & SICKNESS ................................................................................................. 27 Insured Persons: .............................................................................................................................. 27

7. RISK MANAGEMENT........................................................................................................................... 29 While particularly designed for churches, many of the Guidelines would apply equally to schools, homes, aged care facilities & other activities. .................................................................................. 29

INTRODUCTION................................................................................................................................... 30 CHURCH SECURITY............................................................................................................................ 31

1.1 Key Security........................................................................................................................... 31 1.2 Electronic Equipment............................................................................................................. 31 1.3 Security Alarm Systems ........................................................................................................ 31 1.4 Fire Security........................................................................................................................... 32

THE HANDLING OF CHURCH MONEY ............................................................................................... 33 2.1 The Offering........................................................................................................................... 33 2.2 Petty Cash ............................................................................................................................. 34

REDUCING YOUR LIABILITY EXPOSURE.......................................................................................... 34 3.1 The Property .......................................................................................................................... 34 3.2 Working Bees ........................................................................................................................ 34 3.3 Youth Activities ...................................................................................................................... 35 3.4 Ministries Involving Young Children ...................................................................................... 35 3.5 Use of Private Motor Vehicles for Church-Related Activities ................................................ 36

8. AGREEMENTS & FORMS ................................................................................................................... 37 PERSONAL HIRE AGREEMENT.......................................................................................................... 38 MEMORANDUM OF HIRE OF FACILITY.............................................................................................. 39 LICENCE AGREEMENT – OPTIONAL CLAUSES................................................................................ 41 TASMANIA DIOCESE TRAVEL DECLARATION.................................................................................. 42 TASMANIA DIOCESAN INSURANCE FUND – PROPERTY INSURANCE CLAIM FORM .................. 43 ANGLICAN DIOCESE OF TASMANIA – INCIDENT REPORT FORM.................................................. 45 PUBLIC LIABILITY CERTIFICATE OF CURRENCY............................................................................. 47 VOLUNTEERS PERSONAL ACCIDENT CERTIFICATE OF CURRENCY........................................... 48 ANIP POLICIES TAKEN........................................................................................................................ 49 1 INDUSTRIAL SPECIAL RISKS (ISR).......................................................................................................... 49 2 AGGREGATE DEDUCTIBLE PROTECTION ................................................................................................. 49 3 PUBLIC LIABILITY/UMBRELLA LIABILITY (PL) ........................................................................................... 49 4 PROFESSIONAL INDEMNITY.................................................................................................................... 49 5 MANAGEMENT LIABILITY (INCLUDING DIRECTORS & OFFICERS LIABILITY, EMPLOYMENT PRACTICES LIABILITY, STATUTORY LIABILITY) ............................................................................................................................. 49 6 VOLUNTEERS PERSONAL ACCIDENT....................................................................................................... 49 7 TRAVEL ................................................................................................................................................ 49 8 CONSTRUCTION SPECIAL RISKS ............................................................................................................ 49 10 CLERGY TRANSIT................................................................................................................................ 49 11 HIRERS LIABILITY ................................................................................................................................ 49 12 MOTOR VEHICLE................................................................................................................................. 49 13 MARKET STALLHOLDERS LIABILITY....................................................................................................... 49 ANIP POLICIES NOT TAKEN ............................................................................................................... 49 1 STIPEND CONTINUANCE ........................................................................................................................ 49 2 PERSONAL ACCIDENT & SICKNESS ........................................................................................................ 49 3 EXCESS FIDELITY GUARANTEE/FRAUDULENT FUNDS TRANSFER ............................................................. 49 AMENDMENT SHEET .......................................................................................................................... 49

1. INTRODUCTION This manual is designed to assist, in a user-friendly manner, those who are involved in the administration of insurance. Our aim is to give you a document that is easy to read, answers your most frequently asked questions, outlines Claims Procedures & provides information on our insurances. After this introductory section the remaining sections deal with: Section

Insurance Contacts 2

Frequently asked questions 3

Claims Procedures 4

Summary of Insurances 5

Risk Management 6

Forms & Agreements 7

Every person who deals with insurance must be fully aware of what are termed “Statutory Notices” & the need to report incidents. We have included both these at this point because of their importance & you will see that the comments dealing with incident reports are repeated in the Claims Procedure Section.

Statutory Notices

Duty of Disclosure

We have a duty, under the Insurance Contracts Act 1984, to disclose to our Insurers every matter that we know, or could reasonably be expected to know, is relevant to the Insurers’ decision whether to accept the risk of the insurance &, if so, on what terms. We have the same duty to disclose those matters to the Insurers before we renew, extend, vary or reinstate a contract of general insurance. We therefore request that any unusual features, which might increase the likelihood of a claim under the policy, be advised to your Diocesan Insurance Contact (details in Section 2) at the Diocesan Office immediately they come to your attention.

Non-disclosure

If we fail to comply with the duty of disclosure, our Insurers may be entitled to reduce their liability under the contract in respect of a claim or may cancel the contract. If the non-disclosure is fraudulent, our Insurers may also have the option of avoiding the contract from its beginning.

Parish Manual Page

1

Contracts Affecting Insurer's Rights to Recover from Third Parties

Our policies contain a provision that may affect our rights to recover in respect of a loss which arises as a result of a contract between any of our insured organisations & another party. If, pursuant to a contract to which you are a party, the liability of that other party to you in respect of personal injury or loss or damage arising under the contract is excluded or limited, your ability to recover under the policy will be excluded or limited in the same way. In other words, if you enter into a contract that excludes or limits the other party's liability to you in the event of personal injury, loss or damage, the policy will not cover you. A copy of existing or new contracts to which you are a party & which may affect your insurances, should be sent to your Diocesan Insurance Contact (details in Section 2) at the Diocesan Office so that you may be advised concerning the impact of those contracts on your ability to recover under your insurances. Examples of such contracts are:

• a fire sprinkler maintenance agreement where the contract limits the liability of the contractor in the event of the system malfunctioning

• a lease that requires you to indemnify & hold harmless the Landlord • a hire agreement that requires you as the Landlord to accept responsibility for the hirer’s

negligence.

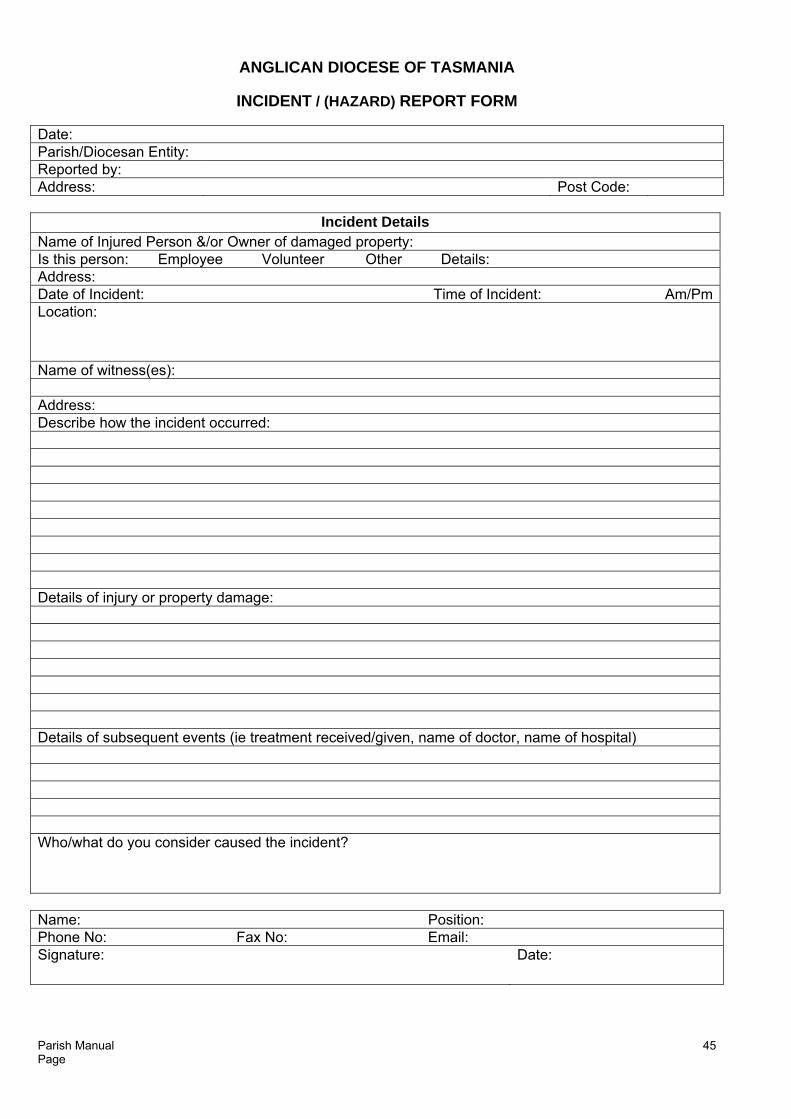

Incident Reporting This segment gives guidance on the action to be taken in those matters where something happens that may not give rise to an immediate claim. For example, a visitor to a Parish/Diocesan Entity property or a volunteer may trip and sustain a minor injury such as a strained wrist. The problem is that, at the time, it is difficult to foresee that medical complications may occur later, leading the injured person to make a claim against the Parish/Diocesan Entity. The safest rule is to gather immediately as much information as possible, take statements from any witnesses, draw a diagram or take a photograph of the accident scene & report the incident to your Diocesan Insurance Contact (details in Section 2) at the Diocesan Office. Naturally, the same procedure should be followed when it is obvious from the outset that there will be a claim. An Incident/Accident Report Form (included in this manual) should be completed & submitted to your Diocesan Insurance Contact (details in Section 2) at the Diocesan Office. NEVER, UNDER ANY CIRCUMSTANCES, ADMIT LIABILITY NOR MAKE ANY STATEMENT WHICH MAY LEAD THE INJURED PERSON TO BELIEVE THAT THE PARISH/DIOCESAN ENTITY ACCEPTS RESPONSIBILITY FOR THE INCIDENT. This may seem harsh but at one end of the scale it will help in the defence of spurious claims & at the other will not raise hopes that assistance or compensation may be forthcoming which is not available. If you are in doubt about what to do you should contact your Diocesan Insurance Contact (details in Section 2) at the Diocesan Office.

Parish Manual Page

2

2. INSURANCE CONTACTS

Diocesan Insurance Contacts: Your initial contact for all insurance matters is as follows: Mrs Lesley Metcalfe Assistant to the Registrar & Diocesan Insurance Contact Postal address: Anglican Diocese of Tasmania PO Box 748 Hobart TAS 7001 Telephone: (03) 6220 2019 Fax: (03) 6223 8968 Email: [email protected]

Anglican National Insurance Program (ANIP) Contacts: For more technical matters you may be referred to Alan Fong or Richard MacDonald at Registry in Melbourne Diocese, who administer the Anglican National Insurance Program. Alan & Richard’s contact details are: Postal address: The Anglican Centre

209 Flinders Lane MELBOURNE 3000

Email: [email protected] Phone: (03) 9653 4207 Fax: (03) 9653 4268 Email: [email protected] Phone: (03) 9653 4229 Fax: (03) 9653 4268

Parish Manual Page

3

3. FREQUENTLY ASKED QUESTIONS

PROPERTY INSURANCE

1. Do we have a claim?

The cover provided by the policy is very broad so in most cases, provided the total of the loss &/or damage is more than the excess for each claim you will have a valid claim. Refer to Section 3 for details of the cover.

2. How do we make a claim?

Refer to Section 4 for Claims Procedure. If you are unsure about what to do, please contact your Diocesan Insurance Contact (details in Section 2) with details of when, where & how the loss occurred. If possible, it would also be helpful if you give an estimate of the amount of the loss. He will advise you how to proceed. A Claim Form is included at the end of this Manual.

3. How do we set our insurance values?

Buildings and Contents are insured on a New for Old basis. Estimating the Value of Contents should not be a problem unless you have stained glass windows &/or a pipe organ. For these items it is best to obtain a professional opinion. It is always helpful to keep an off-site copy record (with photos if possible) of your Contents as the last thing you need is to lose your records in a disaster. This proved to be very important in a major loss in a Parish in Newcastle Diocese during 2000 & cannot be over emphasised. Professional Valuations are expensive but Buildings can be valued to a satisfactory level of accuracy by someone from your Parish/Diocesan Entity with knowledge of building costs. The values need to include Architects’ and Surveyors’ Fees, an allowance for the cost of Removal of Debris, & the cost of complying with Uniform Building Regulations, Local Council requirements etc. Parish/Diocesan Entity business income can be insured and an amount should be included to cover on-going expenses or loss of rent if income is interrupted or reduced because of an insured event. This is best reviewed with your Diocesan Insurance Contact.

4. Is property belonging to Employees and Volunteers insured?

The limit of cover for property of Employees and Volunteers whilst on Parish/Diocesan Entity duties and whilst such property is on Parish/Diocesan Entity property is $5,000 per person, provided not otherwise insured. A claim will be accepted only upon production of evidence that there is no other insurance, such as Home Contents, in force. This does not cover the Home Contents of Clergy in vicarages, for which they should make their own arrangements. Parish Manual Page

4

5. Is property belonging to other people insured?

The limit of cover for property of Employees and Volunteers whilst on Parish/Diocesan Entity duties and whilst such property is on Parish/Diocesan Entity property is $5,000 per person, provided not otherwise insured. A claim will be accepted only upon production of evidence that there is no other insurance, such as Home Contents, in force. This does not cover the Home Contents of Clergy in vicarages, for which they should make their own arrangements. Other than this, cover applies only to Parish/Diocesan Entity property unless specific arrangements are made.

Parish Manual Page

5

PUBLIC LIABILITY INSURANCE

1. Are activities away from the Parish/Diocesan Entity included?

Yes. If it is a Parish/Diocesan Entity activity, liability cover applies.

2. Is the liability of staff members insured?

Yes, but only in respect of authorised duties of your Parish/Diocesan Entity.

3. How do we show the Parish/Diocesan Entity has Public Liability Insurance?

When a Parish/Diocesan Entity conducts an activity, such as a Street Stall, on someone else’s property there is usually a request for a Certificate of Currency for Public Liability Insurance. A Certificate of Currency is included at the end of this manual so that you can provide a copy without delay.

4. Does our Public Liability insurance extend to include the Indemnity Clauses in contracts with Suppliers?

Always read the Contract very carefully and if it contains an Indemnity Clause refer it to your Diocesan Insurance Contact (details in Section 2) because the cover is very limited.

VOLUNTEERS

1. Are volunteers covered by Insurance?

Their liability is covered under our Public Liability insurances & also for injury under the Volunteers Personal Accident policy.

HIRE OF PARISH/DIOCESAN ENTITY PROPERTY

1. Who must have Public Liability Insurance?

Every Hirer must have PL Insurance with an Insurer licensed in Australia. If the Certificate of Currency supplied by the Hirer in response to this request shows an Insurer that you have any doubt about, refer it to your Diocesan Insurance contact (details in Section 2) for clarification. The rule is: no insurance no hire. If we don’t follow this rule we will be picking up liability for activities over which we have no control.

2. Can we arrange Public Liability Insurance for Hirers?

We have a facility to arrange PL Insurance for Personal Hirers wishing to hire property for personal use. The procedure and definition of “Personal Hirers” are set out on pages dealing with Hire of Parish/Diocesan Entity Property. We cannot & do not arrange cover for other Hirers and neither should you. Parish Manual Page

6

4. CLAIMS PROCEDURE This section is included for information purposes. It is designed to provide assistance in procedures to be followed in the event of any incident that might give rise to a claim occurring under any of your insurance policies. All claims are to be reported to your Diocesan Insurance Contact (details in Section 2). Firstly, some remarks on reporting incidents.

Incident Reporting This segment gives guidance on the action to be taken in those matters where something happens that may not give rise to an immediate claim. For example, a visitor to a Parish/Diocesan Entity property or a volunteer may trip and sustain a minor injury such as a strained wrist. The problem is that, at the time, it is difficult to foresee that medical complications may occur later leading the injured person to make a claim against the Parish/Diocesan Entity. The safest rule is to gather immediately as much information as possible, take statements from any witnesses, draw a diagram or take a photograph of the accident scene and report the incident to your Diocesan Insurance Contact (details in Section 2). Naturally, the same procedure should be followed when it is obvious from the outset that there will be a claim. NEVER, UNDER ANY CIRCUMSTANCES, ADMIT LIABILITY NOR MAKE ANY STATEMENT WHICH MAY LEAD THE INJURED PERSON TO BELIEVE THAT THE PARISH/DIOCESAN ENTITY ACCEPTS RESPONSIBILITY FOR THE INCIDENT. This may seem harsh but at one end of the scale it will help in the defence of spurious claims and at the other will not raise hopes that assistance or compensation may be forthcoming which are not available. If you are in doubt about what to do you should contact your Diocesan Insurance Contact (details in Section 2). The following paragraphs in this section set out the procedures for specific classes of insurance.

Property To enable the completion of the claim without delay & to minimise the possible damage, it is important that the following action be taken:

• All reasonable steps should be taken following loss or damage to protect the property from any further damage.

• Any loss by theft &/or wilful or malicious damage should be immediately advised to the nearest Police station.

• Report by telephone to your Diocesan Insurance Contact (details in Section 2) who will advise what further action is required. The Diocesan Office will submit the claim to Alan Fong or Richard MacDonald who will consider them & either approve or disallow the claim or contact the Parish/Diocesan Entity for further details.

• Within 14 days, submit a report in writing giving details of the incident, the loss or damage sustained & any other information relevant to a possible claim.

• Where authorised, pay the repairer’s account & send a copy of the receipted account to the Diocese for reimbursement.

Parish Manual Page

7

• Where a Loss Assessor is appointed, liaise with that person & provide all relevant information to the Assessor.

A Property Claim Form is included in this manual for your use.

Property in transit Should owned goods be delivered in a damaged condition or should there be any reason to suspect damage

1. The attention of the Carrier’s or Shipper’s Representative should be immediately drawn to same & the delivery receipt claused accordingly. In the event of suspected damage, it is suggested that the receipt be claused “Goods believed to be damaged. Accepted subject to survey in store”.

2. A letter of claim should be immediately lodged with the Carrier or Shipping Company’s

Agent.

3. The Diocesan Registry should be advised by telephone of any damage & an estimate of repair or replacement cost should be given. This notification will enable an Underwriter’s Surveyor to call, if required.

4. A claim form should be completed & returned together with the:

a) Delivery Receipt; b) Original Freight Note or Carbon Copy; c) Copy of letter of claim sent to Carrier or Shipping Company’s Agent & reply;

d) Original Invoices.

Parish Manual Page

8

Public Liability UNDER NO CIRCUMSTANCES MUST LIABILITY BE ADMITTED EITHER VERBALLY OR IN WRITING It must be remembered that this is a Legal Liability policy & as such only indemnifies us for our Legal Liability & not what we may believe to be a moral responsibility for injury or damage. An admission of liability on our part could void our policy. Upon the happening of any incident likely to give rise to a claim, the following points must be noted: 1. All reasonable steps should be taken following an accident or loss to protect the person or

property from any further injury or damage. 2. Advice must be forwarded to your Diocesan Insurance Contact (details in Section 2),

together with the originals of all correspondence received from a third party & any accompanying accounts.

3. No correspondence should be entered into with a third party except acknowledgment of

receipt of the claim. The acknowledgment letter should read as follows:

“Without Prejudice We acknowledge receipt of your correspondence concerning the incident at: ................................ This is receiving our attention.”

This is the only form of words acceptable in acknowledging receipt of a claim. 4. Do not give any interview or make any statement to a Loss Assessor or other person

investigating any accident or damage unless such person is acting on behalf of your Insurer or Principal.

Parish Manual Page

9

Professional Indemnity, Management Liability (including Directors & Officers Liability, Employment Practices Liability, Statutory Liability) These policies are written on what is known as a “claims made” basis. This means the policies cover claims notified during the period of insurance, rather than actually relating to the date of occurrence giving rise to the action against you. Any written or verbal contact from a party alluding to a breach of professional duty should be referred to your Diocesan Insurance Contact (details in Section 2) immediately. No correspondence or discussion should be entered into with the party making the allegation.

Volunteers Personal Accident Business Travel All claims under these insurances are to be reported as soon as possible to your Diocesan Insurance Contact (details in Section 2). An Incident/Accident Report Form should be completed (included in this manual) and sent to the Diocesan Office. In the case of injury to a Volunteer, the Form is to be accompanied by statements from any available witnesses.

Motor Vehicle Claims are lodged direct with Vero Insurance Ltd through its Claims First Response Unit. To lodge a claim simply contact Vero on 1800 222 043 - 24 hours a day, 7 days a week. During this call they will:

- Request you to quote your policy number, which is MSL071341823 - Take all relevant details over the phone – a Claim Form is not required

- Provide you with the name of the closest network repairer & confirm the appointment of an assessor. All claims, including windscreen claims, are subject to the policy excess.

Parish Manual Page

10

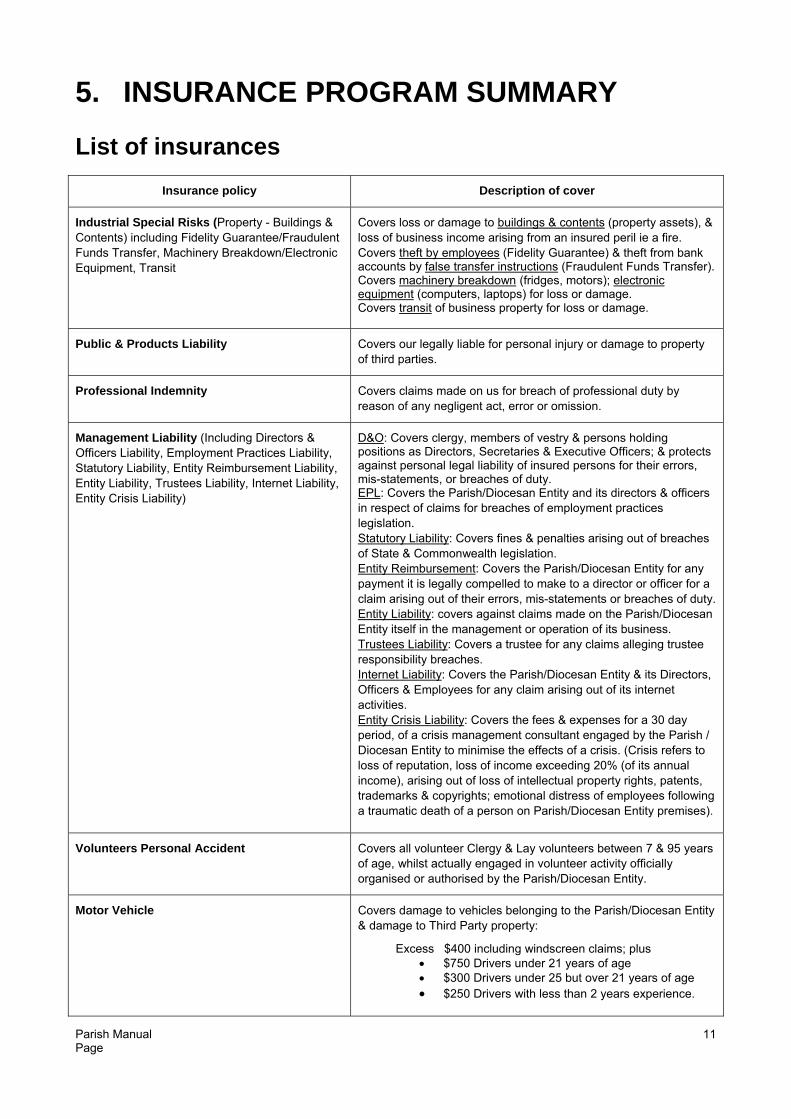

5. INSURANCE PROGRAM SUMMARY

List of insurances

Insurance policy Description of cover

Industrial Special Risks (Property - Buildings & Contents) including Fidelity Guarantee/Fraudulent Funds Transfer, Machinery Breakdown/Electronic Equipment, Transit

Covers loss or damage to buildings & contents (property assets), & loss of business income arising from an insured peril ie a fire. Covers theft by employees (Fidelity Guarantee) & theft from bank accounts by false transfer instructions (Fraudulent Funds Transfer). Covers machinery breakdown (fridges, motors); electronic equipment (computers, laptops) for loss or damage. Covers transit of business property for loss or damage.

Public & Products Liability Covers our legally liable for personal injury or damage to property of third parties.

Professional Indemnity Covers claims made on us for breach of professional duty by reason of any negligent act, error or omission.

Management Liability (Including Directors & Officers Liability, Employment Practices Liability, Statutory Liability, Entity Reimbursement Liability, Entity Liability, Trustees Liability, Internet Liability, Entity Crisis Liability)

D&O: Covers clergy, members of vestry & persons holding positions as Directors, Secretaries & Executive Officers; & protects against personal legal liability of insured persons for their errors, mis-statements, or breaches of duty. EPL: Covers the Parish/Diocesan Entity and its directors & officers in respect of claims for breaches of employment practices legislation. Statutory Liability: Covers fines & penalties arising out of breaches of State & Commonwealth legislation. Entity Reimbursement: Covers the Parish/Diocesan Entity for any payment it is legally compelled to make to a director or officer for a claim arising out of their errors, mis-statements or breaches of duty.Entity Liability: covers against claims made on the Parish/Diocesan Entity itself in the management or operation of its business. Trustees Liability: Covers a trustee for any claims alleging trustee responsibility breaches. Internet Liability: Covers the Parish/Diocesan Entity & its Directors, Officers & Employees for any claim arising out of its internet activities. Entity Crisis Liability: Covers the fees & expenses for a 30 day period, of a crisis management consultant engaged by the Parish / Diocesan Entity to minimise the effects of a crisis. (Crisis refers to loss of reputation, loss of income exceeding 20% (of its annual income), arising out of loss of intellectual property rights, patents, trademarks & copyrights; emotional distress of employees following a traumatic death of a person on Parish/Diocesan Entity premises).

Volunteers Personal Accident Covers all volunteer Clergy & Lay volunteers between 7 & 95 years of age, whilst actually engaged in volunteer activity officially organised or authorised by the Parish/Diocesan Entity.

Motor Vehicle Covers damage to vehicles belonging to the Parish/Diocesan Entity & damage to Third Party property:

Excess $400 including windscreen claims; plus • $750 Drivers under 21 years of age • $300 Drivers under 25 but over 21 years of age • $250 Drivers with less than 2 years experience.

Parish Manual Page

11

Parish Manual Page

12

Transit of Home Contents (Clergy/Employee Transfers)

Covers property of Clergy & Employees for moves between Parish/Diocesan Entities or appointments that are paid for by the Diocese/Parish/Diocesan Entity.

Construction Special Risks Covers material damage arising out of Construction Works & Public Liability following injury to third parties; during property construction & major maintenance projects.

Hirer’s Liability Covers private individuals who hire Parish/Diocesan Entity property for personal use. The provision of a public liability policy is a requirement of all hirers of Parish/Diocesan Entity property.

Stallholder’s Liability This policy provides public liability cover to Stallholders who do not have their own insurance when operating at a Parish/Diocesan Entity market.

Business Travel Covers persons travelling on official Parish/Diocesan Entity business interstate & overseas. Intrastate travel is also covered where the journey involves travel by air or an overnight stay.

6. INSURANCE PROGRAM DETAILS

INDUSTRIAL SPECIAL RISKS Covers loss of or damage to buildings & contents & loss of business income arising from an insured peril Basis of Settlement: Reinstatement or Replacement (unless otherwise specified). Risks Covered Section 1 Material damage (ie damage to property) Fire, lightning, storm, water, hail, flood, riots, vandalism, malicious damage, impact by vehicles, explosion, earthquake, aircraft & Combined Limit glass breakage. $20m each location

Parish Manual Page

13

Section 2 Business Interruption - loss of income (other than giving receipts) & extra costs incurred in maintaining income for up to 48 months (Cathedral 72 months) caused directly by the operation of an insured peril at the premises Sub-limits (Any one loss) Section 1 Accidental Damage $1,000,000Additional Extra Costs of Reinstatement $1,000,000Boarding Students’ property (other than money) excluding accidental damage, burglary and theft - $1,000 per student; provided not otherwise insured

$250,000

Boiler & Pressure Vessel Explosion $200,000Burglary & Theft from buildings & the like (other than money insured below) $500,000Electronic Equipment /Data Processing/Media Breakdown, Data Restoration Costs $500,000Electrical &/or Machinery Breakdown, Plant & Equipment (including Fusion) $500,000Episcopal Regalia including Worldwide transit $100,000Erosion, subsidence, earth movement or collapse (must be sudden & unexpected) $1,000,000Fidelity Guarantee/Fraudulent Funds Transfer $1,000,000Jewellery, Precious Metals, Gems & Stones $50,000Loss of Land Value $1,000,000Money – On premises during business hours, in locked safe or strong room out of business hours & transit including personal custody

$200,000

Money – On premises out of business hours not in locked safe or strong room $20,000Privately owned items not otherwise insured, including property at fetes, art & craft shows

$250,000

Property (excluding money) in transit anywhere in Australia $100,000

Property of Employees & Volunteers not otherwise insured (per person) (including whilst between home & work-authorised activities)

$50,000

Property undergoing repair, alteration or construction of new property not more particularly insured

$500,000

Rockeries, trees, shrubs & the like $100,000Spoilage of Food $25,000Standing timber, growing crops & pastures $50,000Temporary Accommodation Expenses $20,000Theft of Property in the Open Air $50,000Individual Works of Art, Antiques & Curios unless otherwise declared to Insurers $100,000

Section 2

Additional Increased Costs of Working to maintain normal operations $5,000,000

Accounts Receivable $100,000

Claims Preparation costs $1,000,000

Deductibles (sections 1 and 2 combined):

Any one claim: 1. Earthquake - $20,000 or 1% whichever is the lesser 2. Clergy, Employees & Volunteers Property - Nil 3. All other claims - Unchanged for each claim

EXCESS FIDELITY GUARANTEE/FRAUDULENT FUNDS TRANSFER Limit of Indemnity:

$5,000,000 above $1,000,000 (= total cover $6m) Parish Manual Page

14

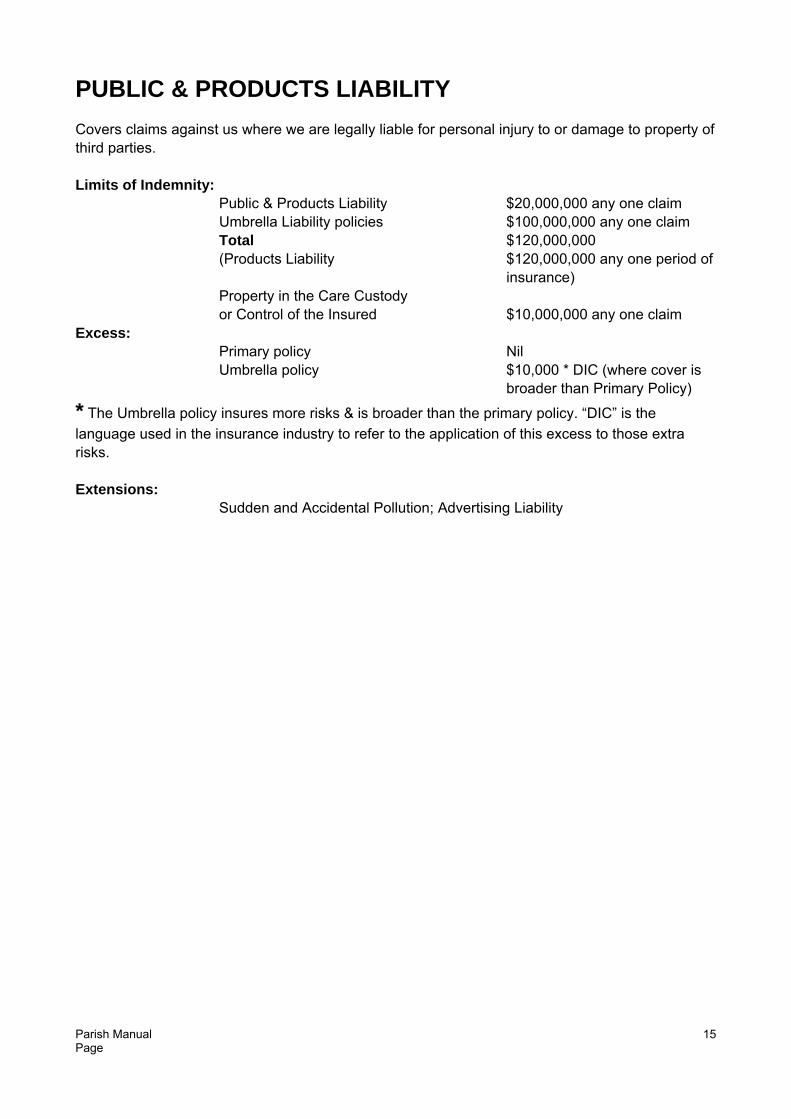

PUBLIC & PRODUCTS LIABILITY Covers claims against us where we are legally liable for personal injury to or damage to property of third parties. Limits of Indemnity: Public & Products Liability $20,000,000 any one claim Umbrella Liability policies $100,000,000 any one claim Total $120,000,000 (Products Liability $120,000,000 any one period of insurance) Property in the Care Custody or Control of the Insured $10,000,000 any one claim Excess: Primary policy Nil Umbrella policy $10,000 * DIC (where cover is

broader than Primary Policy)

* The Umbrella policy insures more risks & is broader than the primary policy. “DIC” is the language used in the insurance industry to refer to the application of this excess to those extra risks. Extensions: Sudden and Accidental Pollution; Advertising Liability

Parish Manual Page

15

PROFESSIONAL INDEMNITY Covers us against any claim made on us during the period of insurance for breach of professional duty by reason of any negligent act, error or omission. Limit of Indemnity:

$25,000,000 any one claim during the period of insurance; subject to one (1) automatic reinstatement up to $25m

Excess: $5,000 each & every claim

Extensions: Advance defence cost payment Medical Malpractice Dishonesty of Employees Loss of or damage to Documents Retroactive cover unlimited excluding known claims and circumstances - $1m Retroactive cover 10 years - $25m Trade Practices & Fair Trading Acts National Insurance Program Members & Program Manager Definition of Insured includes Contract Workers Libel & Slander

Parish Manual Page

16

MANAGEMENT LIABILITY This policy is an amalgamation of our current D&O (Directors & Officers Liability), EPL (Employment Practices Liability), & Statutory Liability into one management liability policy, plus inclusion of several new liability covers (details of all these set out below). There are now eight (8) sub-sections to this policy, with a brief précis of each set out as follows:

Comprising the following Sub-Sections: i) Directors & Officers Liability - cover for insured individuals Covers clergy, members of vestry & persons holding positions as Directors, Secretaries or Executive Officers in the Parish/Diocesan Entity against personal legal liability of the individual insured person for their errors, mis-statements, or breaches of duty committed in good faith in their official positions. Limits of Liability: $15,000,000 any one claim; $30,000,000 all claims during the period of

insurance Excess each Claim:

Entity / Organisation $5,000 Individual Directors & Officers Nil

Extensions:

Advance Defence costs payment Attendance at Enquiries Breach of Conditions - Severability Extended Reporting Period Financial Institutions cover for Funds – ie Anglican Development Fund Libel & Slander Occupational Health & Safety Legislation Outside Directorships of non-profit making organisations Retroactive Date – unlimited; subject to no known circumstances at inception of

the insurance Run off cover

ii) Entity Reimbursement - cover for payments by the entity to directors / officers Covers the Parish/Diocesan Entity for any payment it is legally compelled to make to or on behalf of a director or officer for any claim arising out of their errors, mis-statements or breaches of duty committed in good faith in their official positions. Limits of Liability: $15,000,000 any one claim; $30,000,000 all claims during the period of

insurance

Parish Manual Page

17

Excess each Claim: Entity / Organisation $5,000 Individual Directors & Officers Nil

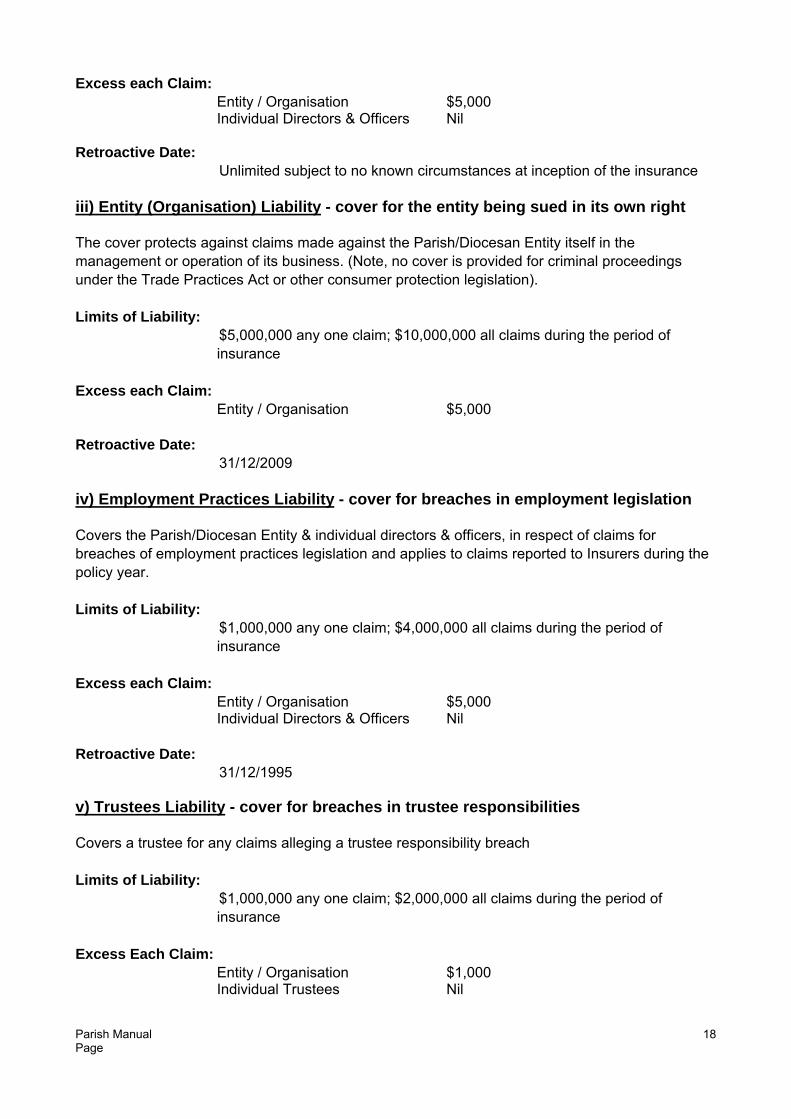

Retroactive Date: Unlimited subject to no known circumstances at inception of the insurance iii) Entity (Organisation) Liability - cover for the entity being sued in its own right The cover protects against claims made against the Parish/Diocesan Entity itself in the management or operation of its business. (Note, no cover is provided for criminal proceedings under the Trade Practices Act or other consumer protection legislation). Limits of Liability: $5,000,000 any one claim; $10,000,000 all claims during the period of

insurance Excess each Claim:

Entity / Organisation $5,000 Retroactive Date: 31/12/2009 iv) Employment Practices Liability - cover for breaches in employment legislation Covers the Parish/Diocesan Entity & individual directors & officers, in respect of claims for breaches of employment practices legislation and applies to claims reported to Insurers during the policy year. Limits of Liability: $1,000,000 any one claim; $4,000,000 all claims during the period of

insurance Excess each Claim:

Entity / Organisation $5,000 Individual Directors & Officers Nil

Retroactive Date: 31/12/1995 v) Trustees Liability - cover for breaches in trustee responsibilities Covers a trustee for any claims alleging a trustee responsibility breach Limits of Liability: $1,000,000 any one claim; $2,000,000 all claims during the period of

insurance Excess Each Claim:

Entity / Organisation $1,000 Individual Trustees Nil

Parish Manual Page

18

Retroactive Date: 31/12/1990 vi) Statutory Liability - cover for fines & penalties following breaches of some Commonwealth / State Acts Covers the Parish/Diocesan Entity, its Directors, Officers & Employees for their liability to pay fines & penalties arising out of innocent breaches of many of the Commonwealth and State Acts that govern their operations. Limits of Liability: $2,000,000 any one / all claims during the period of insurance Excess each Claim:

Entity / Organisation $5,000 Individual Directors & Officers Nil

Retroactive Date: 31/12/2000 vii) Internet Liability - cover for the entity’s internet activities Covers the Parish/Diocesan Entity, its Directors, Officers & Employees for any claim arising out of its internet activities. Limits of Liability: $1,000,000 any one claim; $2,000,000 all claims during the period of

insurance Excess each Claim:

Entity / Organisation $5,000 Individual Directors & Officers Nil

Retroactive Date: 31/12/2009 viii) Entity Crisis Liability - cover for the entity arising out of a crisis loss Covers the fees & expenses for a 30 day period, of a crisis management consultant engaged by the Parish/Diocesan Entity to minimise the effects of a crisis. (Crisis refers to loss of reputation, loss of income exceeding 20%, arising out of loss of intellectual property rights, patents, trademarks & copyrights; emotional distress of employees following a traumatic death of a person on Parish/Diocesan Entity premises). Limits of Liability: $250,000 any one claim; $500,000 all claims during the period of insurance Excess each Claim:

Entity / Organisation $5,000 Individual Directors & Officers Nil

Retroactive Date: 31/12/2009

Parish Manual Page

19

VOLUNTEERS PERSONAL ACCIDENT Cover for: volunteer Clergy & Lay volunteers between 7 & 95 years of age, whilst actually engaged in any volunteer activity officially organised or authorised by the Diocese/Parish/Anglican Entity. Necessary direct travel to, from & during such volunteer activity is also covered. Benefits:

Death & Capital benefits with usual table of maims $250,000 except for students under 18 years of age $20,000 but maims table calculated on $250,000 Non-Medicare Medical Expenses in respect of medical, $10,000 ambulance, hospital services not otherwise provided under Medicare incurred within one year of the accident. Note: The gap between fees charged & the amount recovered from Medicare is not insured.

Home Improvements/Hire of Equipment (for volunteers aged $500 75 to 95 years)

Home Help & Additional Expenses for Travel $1500

Weekly benefits –maximum 156 weeks

1. Temporary total disablement from engaging in *$1,500 pw usual profession, business or occupation arising from an accident

2. Temporary partial disablement from engaging in *$300 pw usual profession, business or occupation arising from an accident

* Where as a result of an accident, a volunteer's weekly income is reduced by less than the maximum stated above, compensation is limited to:

1. The actual weekly reduction in the volunteer's income, plus 2. Reimbursement for additional housekeeping &/or home help necessary as a direct

result of the accident. For volunteers over 75 years of age, benefits are limited to non-Medicare medical expenses, home help, additional travel expenses, home improvements/hire of equipment & funeral expenses only. Other benefits:

Volunteers who are retired or not in receipt of pre-disability earnings & not entitled to claim under another section, other than for medical expenses, will be entitled to claim reimbursement of the reasonable cost of home help & additional expenses for travel incurred as a result of injury causing total disability, up to $1,500.00 per week for 104 weeks.

Excess: Nil

Parish Manual Page

20

TRANSIT – Clergy & Employee Transfers Covers transit of home contents of Clergy & Employees for moves within Australia between Parishes/Diocesan Entities or appointments that are paid for by the Parish/Diocesan Entity. It is Diocesan practice to use this insurance and not that offered by the Carrier because it is substantially cheaper & provides better cover. Cover: Loss or damage including accidental damage. Limit: Replacement cost up to $250,000 any one transit. Excess: Nil Basis of Settlement: Replacement Value (New for Old) Extensions: Loading & unloading

Delayed unpacking – up to 30 days Cover during Storage available on request Temporary Accommodation expenses up to $100 per day in the event of total loss Packing is not a condition of cover No valuations required – Carrier’s inventory sufficient

Procedure: The Parish/Diocesan Entity will be contacted for the necessary

information when an appointment is announced. Premium: Where costs of a move are a Parish/Diocesan Entity responsibility,

the Parish/Diocesan Entity will be invoiced with the premium.

Parish Manual Page

21

MOTOR VEHICLE Covers vehicles belonging to the Parish/Diocesan Entity Limit of Indemnity: Section 1 – Own vehicle damage - Market Value or Sum Insured

whichever is the lesser Section 2 - Third Party property damage- $30,000,000 (Hazardous

Goods $500,000) Excess: $400 basic excess each claim; including windscreen claims

In addition to the basic excess, age/inexperienced driver excesses also apply as follows: Drivers under 21 years of age $750 Drivers under 25 but over 21 years of age $300 Drivers licensed less than 2 years $250 Unlicensed Drivers – No cover

Special Considerations: Automatic insurance for additional vehicles up to $100,000 (subject to

annual adjustment). Replacement vehicle provided for 21 days in case of theft of insured

vehicle. This does not apply to repairs following accidents. Damage to uninsured trailer limited to $500, no cover for contents of

trailer.

Parish Manual Page

22

CONSTRUCTION SPECIAL RISKS Covers the Principal, Contractors & Subcontractors for: i) Property Damage - Construction works, ancillary & temporary works, materials to be

incorporated therein, temporary buildings, hoarding & scaffolding for all declared projects;

ii) Public Liability - Liability to third parties caused by the Principal, Contractors or any

Subcontractors arising out of incidents at the site for all declared contracts. Policy Limits:

Contract Works $5,000,000 Public Liability $20,000,000 any one occurrence

Excesses Each Claim:

Property Damage - each claim $1,000

Public Liability - each claim $1,000 Personal injury NIL

Exclusion:

Contractor's &/or Subcontractors' tools of trade.

Parish Manual Page

23

HIRER’S LIABILITY (Hire/use of Parish/Diocesan Entity property) Covers liability of individual hirers for personal injury or damage to property arising out of the hire or use by them of Parish/Diocesan Entity property. The Insured: Any person who hires or uses Parish/Diocesan Entity property for a private personal function ie family event & who applies for this insurance in the agreed manner. Limit of Indemnity: $2,000,000 each claim Excess: $250 for property damage Nil for all others Hire or use of Parish/Diocesan Entity property The following notes & Agreements should be useful. The insurance program includes cover for the use by Anglican Church groups, of Parish/Diocesan Entity premises & property for purposes of Parish/Diocesan Entity activities. The liability of other persons, groups or companies who may use Parish/Diocesan Entity property is not included in the program & it is important that, in hiring the property, they understand their responsibility. This extends not only to care & safe custody of the property but also to indemnification of the Parish/Diocesan Entity for any liabilities that arise from their activities. The following table will assist to determine how you should deal with each case: Hirer

Action

Other Anglican Church Group

None

Person or Individual for Personal use ie Birthday parties & family celebrations

You may feel it advisable to ask for a formal agreement as set out in the attached “Memorandum of Hire of Facility”. At the very least you should advise them of their responsibilities for damage to the property, breakages & for liabilities arising from use of the hired facilities. If you choose the latter option, they are required to sign a copy of the “Personal Hire Agreement” as set out on the following page. Most Personal Hirers will avail of the option to extend our insurance program to cover their Public Liability risk. This extension is available on application by sending the original of the Personal Hire Agreement to the Diocesan Insurance Contact; refer Section 2 prior to use, & upon payment of a premium of $25.00 per day or as may be agreed with the Diocesan Insurance Contact; refer Section 2.

Parish Manual Page

24

Parish Manual Page

25

Hirer

Action

Non-Church group or club, Company, Government Body or other group

The facilities can only be hired when the Hirer has entered into the appropriate Memorandum of Hire of Facility. A copy of this Memorandum appears in the following pages together with some optional clauses, any of which you may wish to incorporate into your specific Memorandum. In summary, the Memorandum places all responsibility on the Hirer, including for purchase of Liability Insurance.

BUSINESS TRAVEL Covers persons travelling on official Parish/Diocesan Entity business, with cover provided on the following basis: Insured: All Clergy, Employees & Volunteers including accompanying spouses &

dependent children Journey: Any authorised intrastate where the journey involves a flight or overnight stay,

interstate or overseas business travel & the overseas part of authorised study leave including associated holiday travel commencing from residence or place of business (whichever is the last point of departure) & continuing on a 24 hour basis until return to residence or place of business (whichever is the first point of arrival).

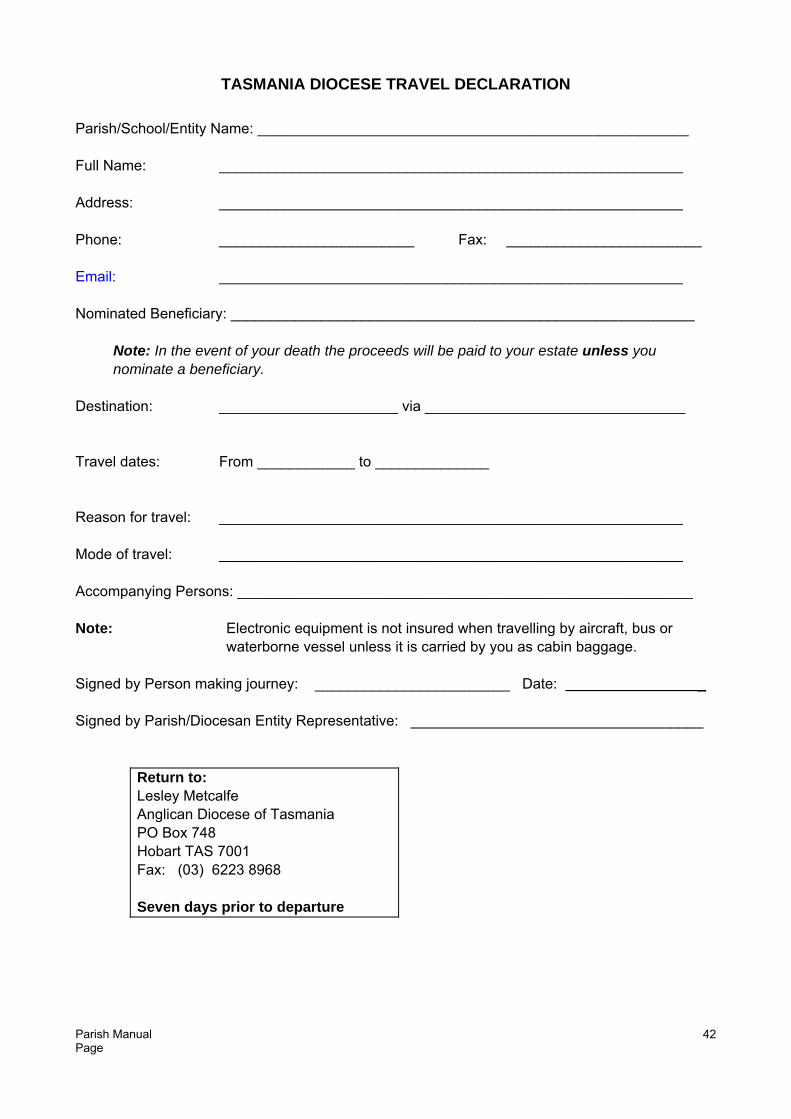

Holiday Travel: Incidental holiday travel is covered where it does not exceed 60% of the total

travel time. The maximum duration of any one trip shall be 90 days. A Travel Declaration must be completed (form provided in this Manual). Flights on Chartered Aircraft / Chartered Helicopters require prior approval from the Insurer and will attract an additional premium. Please advise your Diocesan Insurance Contact; refer Section 2 Accidental Death: Annual salary X 5 to a maximum of $500,000 or $250,000 for

accompanying spouses/partners or $10,000 for dependent children Sickness & Accident: Temporary Total Disability - $600 per week – not exceeding 100% of

earnings for 156 weeks subject to exclusion of the first 14 days disablement.

Kidnap & Ransom: $250,000 Medical expenses: Unlimited Surgical Benefit: $2,000 Political Evacuation: $20,000 per person – Annual Aggregate Limit $60,000 Loss of Deposits: $5,000 Personal Liability: $5,000,000 Baggage: $20,000 (Electronic equipment is subject to an excess of $250 per

claim & is not insured whilst travelling by aircraft, bus or waterborne vessel unless it is carried as cabin luggage).

Money/Travel Docs $1,000 Rental Vehicle Damage & Theft Waiver $5,000 Procedure: Any eligible person wishing to avail of this cover is required to

complete the form in this Insurance Manual & return to the Insurance Office at least 7 days before the journey begins.

Parish Manual Page

26

STALLHOLDERS PUBLIC LIABILITY Insured:

Covers individual stallholders in markets operated by the Parish/Diocesan Entity as declared to Insurers.

Limits of Liability:

Public Liability $10,000,000 any one occurrence Products Liability $10,000,000 any one period of insurance

Excess:

$1,000 each claim

Special note: Cover is available only on application by Market Operators.

PERSONAL ACCIDENT & SICKNESS

Insured Persons:

Nominated Clergy & Diocesan Staff, on a 24-hour basis anywhere in the world except USA and Canada Automatic cover on all additional/new Clergy/Staff – subject to declaration of all nominated persons & premium adjustment on expiry of policy

Benefits: Insured Persons

Capital Benefit

Temporary Total Disability

Temporary Partial Disability

Excess Benefit Term *

Clergy Bishop

$120,000

“

$500 Per week $1,000 Per week

30% of TTD

“

2 weeks

52

All Others

$120,000 $500 Per week 30 % of TTD 2 weeks 52

Note: The Benefit Term is the maximum number of weeks for which weekly

benefits are payable after the excess Benefits are payable to the parish except where the claim is made by a staff

member, when benefits are then payable to the staff member. Benefits payable are reduced by any entitlement under workers or accident

transport legislation. Excess: Disablement due to illness must exceed 14 days after which the benefit is

payable. Age Limits: 15-85 years

Exclusions: Death or bodily injury or sickness resulting from:

• taking part in a riot or civil commotion • engaging in any professional sporting activity

Parish Manual Page

27

• engaging in scuba diving, mountaineering, motor cycling whether as a driver or passenger, hunting, polo, riding or driving in any kind of race parachute or bungee jumping, or hang gliding unless agreed by the Insurer

• engaging in demolition or construction work (including alterations & extensions to buildings)

Parish Manual Page

28

7. Risk Management Any successful insurance program must include a Risk Management Program. This simply means that you must implement procedures that will reduce the likelihood of claims occurring which in turn will be reflected in the premiums you pay. A Guide to Risk Management for Churches has been prepared by Church Insurance Specialists, Ansvar Insurance Limited. It is included with their kind permission for your information & is recommended for implementation where applicable.

While particularly designed for churches, many of the Guidelines would apply equally to schools, homes, aged care facilities & other activities.

Parish Manual Page

29

A Guide to Risk Management for Churches

INTRODUCTION There was a time when Churches were considered to be the most attractive of all properties for insurance. Church property was viewed by most as sacred & there was almost an expectation that anyone who attempted to violate Church property would almost certainly be struck down by a bolt of lightning sent from God. Times have changed significantly. But it is wrong to simply blame changes in social attitudes within society. The Church itself has undergone rapid technological change. Today's Church may well have an expensive sound system, electronic musical instruments, & a computer in the Church Office. These items alone are sufficient to increase the temptation to those in our society who believe all property belongs to the community & should be shared around. Added to the risk of loss or damage to property is the expectation of the community to be compensated for damage to property or bodily injury should it occur during an activity organised by your Church. With many Churches now engaging in an ever increasing diversity of community based activities, a move toward risk prevention is essential. In this booklet, a number of simple risk management concepts are presented. Churches are often under severe financial constraints, which limit the degree of maintenance & security measures that may be considered. However, many of the suggestions are merely based on common sense and will rely solely on support from your membership. The reality for Churches today however, is that some will find it increasingly difficult to obtain favourable insurance terms unless risk prevention becomes a much higher priority. The three principle areas covered are: 1. Church security. 2. The handling of cash. 3. Reducing your liability exposure. Parish Manual Page

30

CHURCH SECURITY

1.1 Key Security

Firstly, is your Church always locked when unattended? This may seem a rather simple question, but burglars obtain easiest access through unlocked doors & windows. A random check of Churches on a Monday morning would reveal that many who answered "yes" to the question above would be in for a rude shock.

Suggestion 1: Appoint a person to be responsible for checking that all doors

& windows are locked after each activity & after worship services where the practice is to lock the Church.

Do you know who has a Church key? Church keys are usually handed out to the appropriate person on a practicality basis. But they are rarely handed back when that person finishes their appointment. Over a period of time some Churches lose track of their keys. The second easiest way to enter a building is by using a key. If your Church has lost control of its keys, one relatively cheap way to solve the problem immediately is to change all your locks. The sophistication of today's locks gives you the opportunity to control who has access to the various areas within your property.

Suggestion 2: Maintain a Key Security List.

1.2 Electronic Equipment

By far the most attractive items for the burglar fall under this category. Both musical instruments & sound equipment can be readily converted to cash. It is therefore very important that Churches firstly know what equipment they have, & secondly take precautions to ensure access is denied to the thief. Access to the sound equipment should be severely restricted. It is pleasing to note an increase in the number of Churches constructing audio rooms. A locked room with restricted access is a good risk prevention method. Microphones & musical instruments should also be kept in a locked room when not in use. It is a most disturbing sight for an insurance inspector to walk into a Church mid-week to see guitars, drum kits, keyboards & microphones all set up ready for worship next Sunday. This is a burglary waiting to happen.

Suggestion 3: Keep the audio equipment, including microphones in a locked

room or receptacle & restrict access. Lock away your portable musical instruments when not in use.

1.3 Security Alarm Systems

The relative financial state of your Church plays an important part in the quality of alarm system you can consider, if any. Church buildings often present problems for Security firms as the floor plans create difficulties in themselves. The fitting of an alarm is an area requiring

Parish Manual Page

31

expert advice. Before purchasing an alarm system, it is important that you seek advice from a Security firm. There are some measures which can be taken at minimal cost. Firstly, criminals do not usually like to be seen in action. Many Churches enjoy a prime location. Good, visible lighting can reduce the risk of burglary, the majority of which occur at night. To floodlight your building may increase your electricity bill, but it also discourages the burglar. Some Churches are appointing a Security Officer from within their own congregation. It is this person's role to wander around the building each evening to ensure doors & windows are locked and appliances turned off. This role can be filled by the member living closest to the Church.

Suggestion 4: a] Consult a Security firm for advice on alarms. b] Appoint a Church member as Security Officer.

1.4 Fire Security

Whilst the risk of burglary is the most obvious today, Churches are still burning down. Very few Churches have sprinkler systems due to the cost involved, so a cheaper, more practical alternative is required. Smoke detectors are now required as standard in many new buildings. They are surprisingly economical to fit. Fire extinguishers are also very important for any Public Building. You need to know the regulatory requirements & ensure that you are complying. This will also encompass the need for Fire Drills for all organisations within your Church. All exits should be clearly identified & instruction given at least once a year. The Fire Brigade will be able to assist you in this area & in the maintenance of your fire fighting equipment.

Suggestion 5: a] Install Smoke Detectors throughout the Church if you have no other early warning system

b] Ensure your Church is complying with Fire Prevention Regulations.

Parish Manual Page

32

THE HANDLING OF CHURCH MONEY

2.1 The Offering

Many Churches have had to dramatically amend their procedures over recent years. Leaving the offering sitting on the Communion Table during & for a short time after worship has resulted in substantial losses. All Churches should seriously consider purchasing a safe. These security devices are no longer 4 x 2 x 2 boxes weighing more than you care to mention. They can be cleverly concealed in walls, cupboards or floorboards & take up very little space. The procedure for handling the offerings will vary from Church to Church. However, the following procedures will minimise the risk of loss:

Suggestion 6: a] Remove the offering from the worship area before

the congregation begins to move after the service.

b] Where possible, have two people count the offering with both to sign off on the total for their mutual protection. A copy of the counting sheet should be made & kept in a separate file so the treasurer can verify that the monies counted agree with the monies banked. Where possible, the treasurer should not be involved in the counting or banking of monies, but oversees the process by ensuring that banked monies equal counted monies.

c] Always count the offering in a locked room. Do not allow children and other visitors into the room during counting.

d] If you do not have a safe in the Church, a responsible officer should take the offering from the premises after worship. NEVER LEAVE THE OFFERING AT THE CHURCH WHEN UNATTENDED OTHER THAN IN A LOCKED SAFE.

e] Deposit the offering at the Bank at the first opportunity. Night safe facilities are available & should be considered by Churches with large weekly offerings.

Parish Manual Page

33

2.2 Petty Cash

It is our belief that money is safer at the home of the Treasurer/s than at an unattended Church. Leaving money on the premises will be a recipe for repeat burglaries. It may be necessary to have a petty cash float in your Church Office. A lockable cash receptacle should be used & the float should be as low as possible. A filing cabinet should never be used as a lockable cash receptacle. Again, if you have a safe, lock the receptacle in the safe each night.

Suggestion 7: Do not leave cash on the Church premises when unattended,

other than in a safe.

REDUCING YOUR LIABILITY EXPOSURE

3.1 The Property

Many Church Boards believe their Church will never be the subject of a Public Liability claim because their members uphold the Biblical principle of not taking legal action against the Church. This is the first sign of complacency. Ask yourself this question. On any given Sunday, what percentage of the people at your Church are actually members? Your Church may be the subject of a claim if somebody is injured or property is damaged as a result of your people failing to act in a reasonable & prudent manner. This may sound like legal jargon, but basically, it means you must use common sense. The majority of Public Liability claims arise out of the accident waiting to happen, happening. Many claims relate to the failure of Churches to properly maintain their property. Insufficient funds to rectify the wobbly balustrade will not succeed as a defence, if it gives way & a person falls down the stairs.

Suggestion 8: Ensure you have an active Property Committee with expertise

in the area of building maintenance & fix what needs fixing today.

3.2 Working Bees

Working bees increase the exposure of Churches to liability claims substantially. Unskilled workers are often requested to perform tasks beyond their capabilities. It is essential that you have skilled supervision of all activities. It may be necessary for you to bring in an outside person to supervise. No Church wants to see one if its members injured, especially working for the Church.

Suggestion 9: Always appoint a Supervisor for each working bee & establish the skill levels of the workers before allocating the tasks.

Parish Manual Page

34

3.3 Youth Activities

The key to successful & safe Youth Programs hinges very heavily on the Supervisors. Young people like to have fun & they enjoy new experiences. Churches are to be encouraged to provide a full program for youth. However, it is imperative that the new experiences are old experiences for those supervising. When participating in any dangerous activity, experienced leaders must be used. If that experience is not available within your leadership, you need to obtain it from outside. Please refer to the Diocesan publication “Protection Policy for Children & Young People” to guide you in your children / young peoples activities. A copy should be held in your Parish / Entity Office. Motorised vehicles, (whether cars, motor bikes or go-karts), present a very real danger to young people. Activities where vehicles are used other than as a means of transport should be avoided.

Suggestion 10: Ensure your activities are responsibly supervised by

experienced leaders.

3.4 Ministries Involving Young Children

With the reduction of Government money in the Pre-school area in particular, many churches will become involved in alternative community services. Whilst the Government may be withdrawing funding, it is heavily targeting legislation at this area. It is important Churches commence Children’s Ministries with their eyes fully open. Great care is required in the area of choosing your leaders for these Ministries. In some cases, tertiary qualifications are required. Most liability claims involving children result from children being where they should not be. By far, the most common claims arise from children being scalded by hot water from an urn after tripping over the cord. Supervision is again the key. It may be necessary for you to prevent children from entering some areas of your property, such as the kitchen. The Diocesan Child Protection Risk Management Plan will assist you in the process for the selection of leaders & volunteers. The plan will also assist you in the identification & management of risks in your parish. The Plan has been posted on the Diocese’s website and your parish will have a hard copy.

Suggestion 11: Know the regulations relating to care of children & ensure you

comply.

Parish Manual Page

35

3.5 Use of Private Motor Vehicles for Church-Related Activities

Private vehicles owned by employees & volunteers are often used for authorised church activities in transporting people. As part of the Parish’s Duty of Care, the Parish should ensure that owners of each vehicle being used in this way have current registration, comprehensive insurance & a compulsory third party insurance policy in place. Also, as part of the Parish’s caring for its volunteers, the Parish should advise volunteers that it is in their best interest to have a current comprehensive motor vehicle insurance policy or at least a current third party property damage insurance policy, both of which should include liability cover for those incidents resulting in bodily injury which are not covered by the compulsory third party policy.

Suggestion 12: Ensure private vehicles have current registration & recommend

to owners of such vehicles that they have additional insurance to cover liability for bodily injury.

Parish Manual Page

36

8. AGREEMENTS & FORMS

The following Agreements & Forms are included for use by Parishes/Diocesan Entities. These should be photocopied for use as required.

Personal Hire Agreement Memorandum of Hire Facility Licence Agreement – Optional Clauses Travel Declaration Property Insurance Claim Form Incident Report Public Liability Certificate of Currency Volunteers Personal Accident Certificate of Currency

Parish Manual Page

37

PERSONAL HIRE AGREEMENT (♣Personal hire for ♣Personal use)

Persons hiring or using buildings & other property of the Parish/Diocesan Entity accept responsibility for the safe custody of the property during the term of the hire or use. They are required to indemnify the Parish/Diocesan Entity for any liability arising from the hire & use of the buildings &/or other property. I/we hereby confirm that I/we have read & fully understand & accept my responsibilities, as summarised above, in entering into this hiring agreement.

I/we have arranged my/our own insurance to cover the liabilities listed above & to indemnify the Parish/Diocesan Entity & enclose evidence of this arrangement by way of Public Liability Certificate of Currency.

Or

I/we request that the Parish/Diocesan Entity arrange insurance to cover these liabilities to $2,000,000 & I/we agree to pay the premium calculated at $25.00 per day/$…… per year. I/we accept that this insurance is subject to payment by me/us of the first $250.00 for any property damage.

Tick one box only

Date of Hire: .................................... Nature of Hire/Use: …………………………… Signed by the Hirer: ............................................................... Date....../......./......... Name of Hirer (please print): ................................................. Parish/Diocesan Entity: ….……………………………………………. ♣ Personal means: The hirer is a person or an unincorporated group meeting for a non-commercial, non-political, non-“cause/crusade” purpose where the meeting is not open to the general public & the hirer does not have a public liability policy. Examples of acceptable activities are:

• A private birthday party, celebration, wedding reception • Dance practice not associated with a dance school or lessons & no fees are charged • Friends who want a venue to read plays/poetry etc (but not rehearsals for a show) • Knitting groups who like to meet to compare work / ideas • Musicians using premises for non-commercial purposes (but not musicians who perform

elsewhere) • Informal support / self-help groups

Parish Manual Page

38

MEMORANDUM OF HIRE OF FACILITY Owner: Diocese of TASMANIA &/or Parish/Diocesan Entity Hirer Name: Address: Parish/Diocesan Entity Facility: Parish/Diocesan Entity Representative: Description of Facility: Date(s) of hiring from: to: Hiring Fee $ Obligations of the Hirer 1. To pay the hiring charges in the manner & time agreed.

2. To leave the facility in a satisfactory & clean condition (including any black/white boards).

3. To remove all rubbish.

4. Not to remove anything owned by the Parish/Diocesan Entity from the facility.

5. To lift (not drag) anything moved within the facility & to return to its original position.

6. Not to use any exhibits or decorations in the facility without the prior agreement of the

Parish/Diocesan Entity Representative.

7. To do no damage to the facility, its furniture & furnishings, accessories or environs & to report

to the Parish/Diocesan Entity any loss of damage to property & to pay for its repair or

replacement.

8. Not to permit smoking within the facility.

9. To switch off all lights, fans, heaters/air conditioners & other electrical equipment before

vacating the facility.

10. To secure windows & doors on vacating the facility.

11. To return any keys to the Parish/Diocesan Entity in the manner agreed.

12. To effect & keep in force public liability insurance cover with an Insurer acceptable to the

Owner at the Hirer’s expense for an amount not less than $5,000,000 which shall include the

following extensions:

• Liability for loss of or damage to property of the Owner

• Indemnity for claims made against the Owner arising out of the negligence of the Hirer

& to produce to the Parish/Diocesan Entity Representative evidence thereof in the form of a current

Public Liability Certificate of Currency.

Evening functions should conclude by 12:00 midnight & the premises vacated by 1:00 am. Parish Manual Page

39

13. During the period of hire, to create no nuisance either by way of noise or otherwise so as to

inconvenience adjoining owners or occupiers.

14. Not to carry out in or about the facility any illegal activity.