Digitalization - Death of the B2B salesman

72

Digitalization ‐ Death of the B2B salesman Valentin Dinkelbach Corporate Account Manager Siemens AG

Transcript of Digitalization - Death of the B2B salesman

Digitalization ‐ Death of the B2B salesmanValentin DinkelbachCorporate Account Manager Siemens AG

Restricted © Siemens AG 2016

Digitalization affects all business areas

Restricted © Siemens AG 2016

How the internet changes the information flowFrom passive consuming to proactive demanding

History Future

Customer Customer

Restricted © Siemens AG 2016

Death of a (B2B) sales man‘Forrester’s report by Andy Hoar and Peter O’Neill’

Buying environmentsimple complex

Solu

tion

type

sim

ple

com

plex

“Serve me” “Guide me”

“Show me” “Enlighten me”

Level of complexity drives customers’ expectation towards supplier

Forrester defines four different

Buyer Archetypes

Restricted © Siemens AG 2016

Death of a (B2B) sales man‘Forrester’s report by Andy Hoar and Peter O’Neill’

Buying environmentsimple complex

Solu

tion

type

sim

ple

com

plex

“Serve me” “Guide me”

“Show me” “Enlighten me”

Different Buyer Archetypes require individual sales attitudes

Estimated sales head

count developmen

t by 2020-33%

-25%

-15%

+10%

Restricted © Siemens AG 2016

What does this mean for the sales setup?

Explainer• Integrated support

tools• 24/7 availability• (Online) Training• Application

knowledge

Consultant• Process knowledge• Solution risk taking• New business model

to finance the consultancy is required

Order Taker• State-of-the-art

processes• Standardized

product master data• Online visibility• Price transparency

Navigator• Information broker• Internet Scout• Transactional

charges for services

Separate channels for information and purchase

Total Customer Experience

Integrated Marketing

Restricted © Siemens AG 2016

From grabbing attention to holding attention

From Gaussian to Bayesian data analysis

From eyeballs to Interfaces

Four mindset shifts marketers need to make now

From crafting messages to designing experiences

Source: Greg Satell, Forbes 2016, March 3rd

Restricted © Siemens AG 2016

Siemens supports the ‘Digital Marketing’ within the distributor channel

Ready to use for end customers

Ready to use for distributor staff

Ready to use in yourown marketing tools

Restricted © Siemens AG 2016

Persona: Digital Marketing Expert

EnergyEfficiencyBrochure

F&BApplicationBrochurePackaging

Web pagehosting

If you want to be ‚preferred supplier‘, your marketing content must be easily accessible, pre-selected by end-

customer industries, and covering relevant focus topics (Safety, Energy Efficiency, Legislative Changes, …).

Feed

s fro

m S

uppl

iers

Responsible for the production / selection of suitable marketing tools

Restricted © Siemens AG 2016

Integrated Marketing in B2B needs more than historical data

Cross-sellingPLC + Power supply; Control products + circuit protection .Up-sellingContactor -> Soft starter -> DriveSolution-sellingLOGO! + Drive + MCB + Motor protection

Value-sellingx + y + z = energy savings

Strategic-selling e.g.• Market launch• Stock clearance

Relevantinformationfor the userSales data

Technical data

Individual targets Additional service offer

Restricted © Siemens AG 2016

Valentin Dinkelbach

Corporate Account Manager

DF SDA

Gleiwitzer Straße 555

90475 Nürnberg

Phone: +49 (911) 895-2458

Cellular: +49 (172) 291 3377

E-Mail: [email protected]

Thank you for your attention!

siemens.com/answers

Winning togetherLEDVANCE and the Changing MarketOliver VoglerVP Strategy & Marketing

WINNING TOGETHER: LEDVANCE AND THE CHANGING MARKET

Dr. Oliver Vogler, VP Strategy & Marketing

EUEW General Convention, Sardinia, June 3, 2016231

CHAPTER 1: INTRODUCTION

YOU AND LIGHTING

In Electrical Wholesale, key players cover the majority of the market

13″5

9″5

4″7

IDEE

5″7

AD

9″3

IMELCO

23″0

t/o IMARK

GEWA

1″0

FEGIME

Large Corporates

22%

Buying Groups

Independents

Total Market

150-170’’

50%

28%

13″5

Rexel

9″1

Grainger

6″9

Sonepar

20″2

5″2

Wesco CED

233

CY 2015; Numbers in bn EURSource: DISC (US); EMR (RoW); Company Websites; Industry expert estimates

EUEW General Convention, Sardinia, June 3, 2016

Lamps1)11″13″

Lighting is an important category – that can be split into 3 main segments

3%

19%

20%

18%5%

7%

13%

15%

Further:Industrial MaterialSwitch GearHeatingSecurity

Lighting

Cables and Wires

Installation Material

Source: EMR, Frost & Sullivan 2015, values in EUR

234

Lighting represents almost one fifth of revenue… … with highest growth in “Over the Counter” Luminaires

Project Luminaires2)

2016

31″

2014

29″

"OTC" Luminaires2)

26″23″

1) Global Lamps Replacement2) Excl. LATAM and MEA

“Over the Counter” luminaires are……marketed directly via wholesaler…applicable for >50% of installations…easy-to-use w/o specification…fast-turning, volume-driven market

“Project” luminaires are……marketed via architects, light planners…wholesaler serves as fulfillment partner…includes customized luminaires…technology-driven market

EUEW General Convention, Sardinia, June 3, 2016

Expectations for the future of the lighting market different depending on research group (here: Lamps)

235

CAGR 2015-2020:

+1%

IHS (2015)

20

15

10

5

02015 2020

9.0

12.3

20

15

10

5

02015 2020

18.918.0

CAGR 2015-2020:

-2%

0

5

10

15

20

2015

15.3

2020

14.0

BCG (2015)F&S (2015)

CAGR 2015-2020:

-6%

Sources: Frost & Sullivan 2015; IHS 2015; BCG 2015 (based on interpolation)Comparable scope: Indoor only (therefore, e.g. HPD excluded)

GLSLPD HALCFLi LED Lamps

EUEW General Convention, Sardinia, June 3, 2016

EUR bn EUR bn EUR bn

Installer ElectricalWholesaleMarket

To explore the market trends, we have invested in some research

236

Frost & Sullivan 2015McKinsey & CompanyBoston Consulting GroupHISGartner

Voltimum Survey (April 2016) US DISC DATABASEEuro Marketing + Research (EMR)LEDVANCE Wholesaler Survey(May 2016)

Whitepaper with external researchers (July’16) Website for registration: www.ews2016.com

DACH:EU-N:EU-SW:EU-E:

3/4th

12/13th

19/20th

26/27th

MayMayMayMay

EUEW General Convention, Sardinia, June 3, 2016

N = 402

N = 273

N = 732

N = 357

Germany

UK

Italy

Turkey

CHAPTER 2: CHANGING MARKET

INDUSTRY TRENDS AROUND LIGHTING

There are big shifts that prompt your customers to demand more from you

238

• Top portfolio• Best in class product content• More training & education• Top multichannel experience• Agility• …

LEDification

Market ShiftsA

Smart Products

Tech ShiftsB

Multichannel

Service ShiftsC

NewDemands

NewExpectations /

Behaviors

EUEW General Convention, Sardinia, June 3, 2016

What’s your“winning model”???

LEDIFICATION

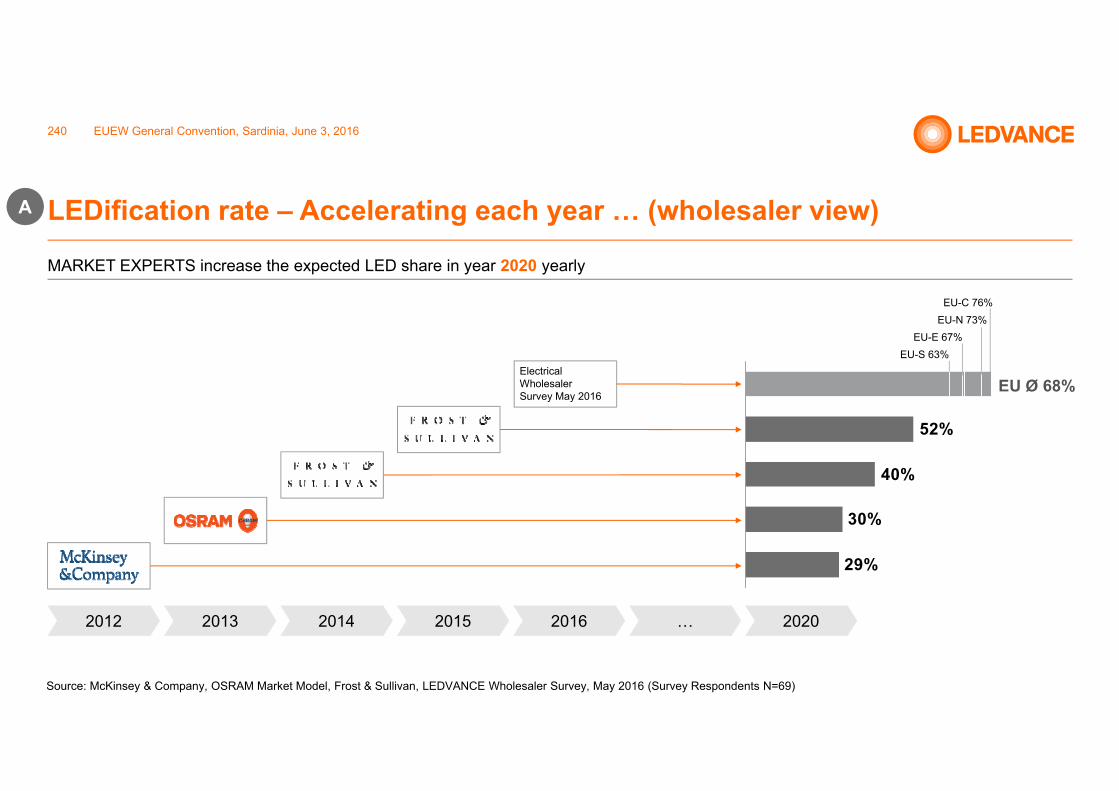

LEDification rate – Accelerating each year … (wholesaler view)

240

Electrical Wholesaler Survey May 2016

29%

30%

40%

52%

2013 2014 2015 2016 …2012 2020

EU-S 63%

EU Ø 68%

EU-E 67%EU-N 73%EU-C 76%

A

Source: McKinsey & Company, OSRAM Market Model, Frost & Sullivan, LEDVANCE Wholesaler Survey, May 2016 (Survey Respondents N=69)

MARKET EXPERTS increase the expected LED share in year 2020 yearly

EUEW General Convention, Sardinia, June 3, 2016

… "only one among other technologies"… "first choice" or "close to 100%"

LEDification rate – Accelerating each year … (installer view)

241

LED will be close to 100% of all lighting installations LED will often be the first choice for lighting installations LED will be only one among other technologies for lighting installations

ItalyN = 732

GermanyN = 402

UKN = 273

TurkeyN = 357 26%

25%

25%

16%

In 2016, LED will be …

75%

75%

74%

84%

A

Source: Voltimum Survey Among Electrical Installers, April 2016 (N=1764)

Panel of electrical installers after l&b 2016

EUEW General Convention, Sardinia, June 3, 2016

… while traditional technologies still make sense in several cases

242

Need“CHEAP INSTALLATION/

SHORT OPERATING TIME”“TOTAL COST OF

OWNERSHIP”“HIGH PERFORMANCE

LIGHTING”“MAXIMUM ENERGY &

CO2 SAVINGS”

Solution Halogen / CFL as price sensitive entry technologies

Fluorescent still more cost effective in many installations

High pressure discharge versatile and durable

LED retrofit Standardized / “OTC”LED luminaires

Global Market Today, in € 3’’6 1’’4 1’’1 6’’9 25’’8

Global Market 2020, in € 1’’1 0’’8 0’’6 7’’7 31’’9

Outdoor

Shop

Spor

t

Industry

TCO Calculation

LED LUMT8T5

Let’s manage this pro-actively!

A

Source: Frost & Sullivan, own calculations

EUEW General Convention, Sardinia, June 3, 2016

SMART PRODUCTS

Digitization and connected products Introducing the “Hype Cycle” ...

244

Expectations

Time

Robotic Vacuum Cleaner

ZigBeeWireless Music Systems for the Home

Innovation trigger

Through of Disillusionment

Slope of Enlightenment

Plateau of Productivity

Peak of Inflated Expectations

B

Source: Gartner 2015

EUEW General Convention, Sardinia, June 3, 2016

While Connected Home is still in the "Innovation Trigger" phase, installers see sales potential for smart lighting increasing after l+b

245

Electrical Installers about sales potentialfor smart lighting after l+b 2016

Expectations

Time

Connected Home

Intelligent Lighting

Innovation trigger

Through of Disillusionment

Slope of Enlightenment

Plateau ofProductivity

Peak of Inflated Expectations

44%

40%

47%

41%

Decreased Increased

3%

1%

6%

2%

B

Source: Gartner 2015, Voltimum Survey Among Electrical Installers, April 2016 (N = 1.764)

Gartner Hype Cycle for Connected Home, 2015

EUEW General Convention, Sardinia, June 3, 2016

... showing that lighting is good entry point to build smart solutions, with confirmed business potential by installers

246

Security

Shades/Blinds

Smart white goods 9%

10%

7%Entertainment

25%HVAC1

27%Lighting

22%

Source: Frost & Sullivan, Voltimum flash survey amongst electrical installers, April 2016 1 Heating, Ventilation and Air Conditioning

Light is …… in every room … replaceable (still “billions” of sockets)… always on power … both, functional and emotional

ELECTRICAL INSTALLERS estimate lighting to be the most important use case for Smart HomeSMART LIGHT is at the core of many applications

Smart Citizen

Smart Healthcare

Smart Infrastructure

Smart Mobility

Smart Building

Smart Governance and Education

Smart Energy

Smart Technology

EUEW General Convention, Sardinia, June 3, 2016

B

MULTICHANNEL

Wholesalers and installers with different expectations around purchasing online

248

Share of INSTALLERS who pick given aspects among the most

important when purchasing online

Share of WHOLESALERSwho believe given aspects are the most important for electrical installers when purchasing online

23%

22%

14%

14%

10%

9%

4%

13%

19%

13%

12%

18%

5%

3%

Rank RankGood product feature comparison

Delivery speed

Availability of auxiliary information

Better price than offline

Full range of portfolio

Ease of purchase process

Site / app optimized for mobile devices

Broad payment options

5%

19%

1

2

3

4

5

6

7

8

4

1

4

6

3

2

7

8

C

Source: Voltimum Survey Among Electrical Installers April 2016 (N=1764), LEDVANCE Survey, May 2016 (N=68)

EUEW General Convention, Sardinia, June 3, 2016

At the same time, multichannel becomes key –now also for pure digital players

249

EU: Large online fashion dealer goes offline with store concept

US: Opening more and more offline shops with online customer rating as shelf concept

APAC: USD 4 billion investment in a Chinese brick-and-mortar retailer

C

EUEW General Convention, Sardinia, June 3, 2016

Our challenge: Managing the customer journey… online and offline!

250

C

Reach & Penetration Education Drive Trial

Prospectivecustomer Clients

AdvertorialsAggre-gators

Online Video(all devices)

High Reach Display

Content Marketing

Mobile

(e)POSSEA

Re- and Look-Alike Targeting

Social Media

GTIN /ETIM

EUEW General Convention, Sardinia, June 3, 2016

CHAPTER 3: WHOLESALE

KEY DIFFERENTIATORS

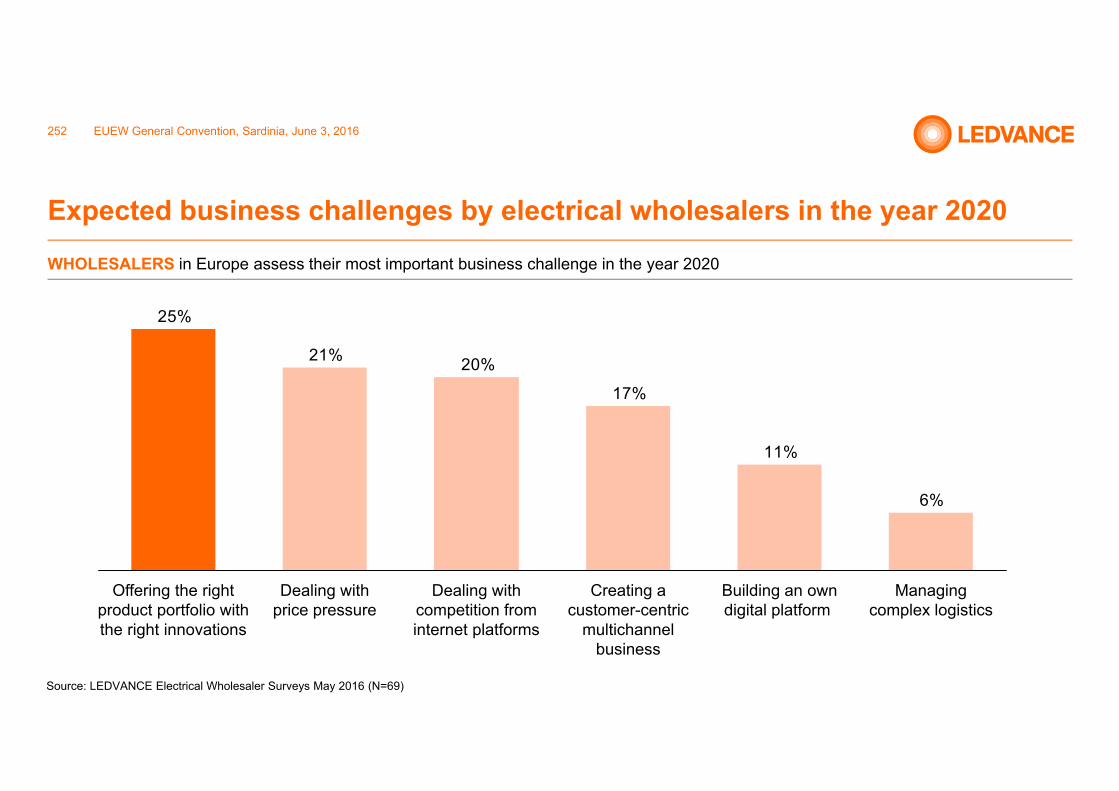

Expected business challenges by electrical wholesalers in the year 2020

252

Source: LEDVANCE Electrical Wholesaler Surveys May 2016 (N=69)

WHOLESALERS in Europe assess their most important business challenge in the year 2020

EUEW General Convention, Sardinia, June 3, 2016

6%

11%

17%

20%21%

25%

Managing complex logistics

Building an own digital platform

Creating a customer-centric

multichannel business

Dealing with competition from internet platforms

Dealing with price pressure

Offering the right product portfolio with the right innovations

Preliminary, we found five segments across countries –Content and Relationship more important than Price

253

PRELIMINARY

Need business convenience(e.g. payment terms)

Needlowestprice

Need broad product portfolio

Need trustedrelationship

28%

23%

7%

28%

14%

“I want it all”

“I just want best price”

“I want a trusted relationship and product innovation”

“I want business convenience &

good payment terms”

“I want a broad and available product portfolio “

Analytically derived installer segments based on a survey of their needs in four countries

Source: Voltimum Survey Among Electrical Installers April 2016 (N=1.764); Countries covered: DE, IT, UK, TR; Analytical method: Correspondence analysis based on 3 survey questions

EUEW General Convention, Sardinia, June 3, 2016

In a nutshell: How to find the “winning model”?

254

LEDification

Market ShiftsA

Smart Products

Tech ShiftsB

Multichannel

Service ShiftsC

NewDemands

NewExpectations /

Behaviors

EUEW General Convention, Sardinia, June 3, 2016

• “The right product for every need” – let’s not “over pace” with LED products

• Lighting is “ahead of the curve” in smart products – already tangible opportunity for installers

• In online business good product information, delivery speed and auxiliary information (e.g., rich media) are most important for installers

• Offering the right product portfolio with the right innovations is seen as the key business challenge

• Majority of installers is not (just) price driven but wants better content

Brand Positioning & Customer Centricity are key!

More to follow:www.ews2016.com

PRELIMINARY

CHAPTER 4: WINNING TOGETHER

YOU AND LEDVANCE

The “big old 3” in the lighting industry are adapting their business models to a changing market environment

256

Trend1)

in traditional business

• Carve-out of lighting and combine with other businesses around energy

• Introduction of new entrepreneurial corporate culture

“Current combines GE’s products and services in energy efficiency, solar, storage, and onsite power with our digital and analytical capabilities to provide customers […] with more profitable energy solutions” – Jeff Immelt, CEO GE

“As a standalone, listed company we will be committed to […] driving the transition to LED and connected lighting systems and services” – Eric Rondolat, CEO Philips Lighting

“As an independent unit, LEVANCE will be able to operate more freely on the market and realize strategic options such as partnerships more easily.”

– Olaf Berlien, CEO OSRAM

• Separation of technology and volume business

• Higher flexibility for alliances and partnerships

1) Decline in traditional (lamps) business in Q1 CY 2016 Sources: www.edisonreport.net; PHILIPS Prospectus; GE / PHILIPS / OSRAM Capital Market Days

Decision

• Separation of lighting and healthcare/electronics business

• Spin-off of lighting business for direct access to capital markets

Consequences

EUEW General Convention, Sardinia, June 3, 2016

Most of general lighting business will go with LEDVANCE moving forward

257

1) Cross-selling on behalf of “OSRAM GmbH” (not applicable for APAC)

LEDVANCE after CARVE OUTOSRAM before CARVE OUT

Sales: 57 Offices

Production: 34 Sites

Opto SemiconductorsSpeciality LightingLuminaires & Solutions

Digital Systems

ECG LED Drivers LED Modules LMS

Lamps (Traditional / LED)

Thermal / CFLi LPD HPD LED Lamps

LED Lamps

LED Lamps

Traditional Lamps

Thermal / CFLi LPD HPD

Electronics1

ECG / LED ModulesLED Drivers LMS

“OTC” Luminaires Smart Products

Sales: 50 Offices

Production: 17 Sites

EUEW General Convention, Sardinia, June 3, 2016

NEW:

Who we are

“WE HAVE ESTABLISHED A TEAM-ORIENTED, CUSTOMER-DRIVEN PERFORMANCE CULTURE AT LEDVANCE.”

Jes Munk HansenChief ExecutiveOfficer

Erol KirilmazChief Sales & MarketingOfficer

Peter MannhartChief OperationsOfficer

Bettina Kahr-GelengChief Human Relations Officer

Oliver NeubrandChief FinanceOfficer

258 EUEW General Convention, Sardinia, June 3, 2016

LEDVANCE KICKOFF CONFERENCE, May 2016259

How we look like

• Our new company brand

• One global firm• Re-start into more

entrepreneurship

• Our trusted brand for lamps • Association with quality• Demonstrating our heritage

and expertise

• Our new product brand for luminaires

• Leveraging both: “OSRAM quality” and “advancing light”

95%of products are sold in OSRAM brand

LEDVANCE KICKOFF CONFERENCE, May 2016260

58%OF CONSUMERS CLAIMTHEY WILL PURCHASE ASMART HOME PRODUCT INTHE NEXT TWO YEARS

250NEW OVER THE COUNTER LUMINAIRES TO BE LAUNCHED GLOBALLY STARTING FROM JULY

Our commitment to you

1. We are proud of our heritage and worldwide presence – illuminating people’s lives and advancing lighting technology for almost 100 years

2. We will continue to be your “one-stop shop” for almost all OSRAM branded products in general lighting

3. We continue to provide you with latest technology, e.g., in LED lamps, and are expanding our portfolio in luminaires and smart lighting products

4. We strive for continuous improvements in our knowledge of markets and end-user needs through local and application-oriented expert teams (e.g., for verticals)

5. You are the focus of our daily business – we are committed to the 3-level distribution approach!

YOU AND LEDVANCE

LET’S REDEFINETHE ROLE OF LIGHT …

… TOGETHER

MSSI – Market Surveillance Support Initiative

Fernando Ceccarelli Senior VP and General Manager, Power Distribution DivisionEaton EMEA

Working together for safe and compliant electrical products in Europe

© 2016 Eaton, All Rights Reserved.

What is MSSI?

• Joint initiative from CECAPI and CAPIEL, supported by ORGALIME.

A proactive industry lead scheme to monitor the market and support authorities to prevent non-compliant electrical products from entering the European market.

© 2016 Eaton, All Rights Reserved.

Why MSSI?

Non-compliant products are a risk to

• People• Property• Goods

Can damage the reputation of individuals and companies within the electrical industry.

© 2016 Eaton, All Rights Reserved.

The real cost of non-compliant products

Every day in Europe

• Approximately 12 people die in house fires.

• 10 – 20% of fires are due to electrical faults.*Non-compliant products

put people, goods and property at risk.

* Statistics from the EU Fire Safety Network and Forum for European Electrical Domestic Safety (FEEDS)

© 2016 Eaton, All Rights Reserved.

MSSI Overview

Working together for 100% compliant products and fair competition on the European market.Objective

Proactive sampling and testing to support local authorities to take action.Approach

Focus on MCBs, RCDs, MCCBs, SPDs, contactors, wiring accessories, and power distribution.Scope

© 2016 Eaton, All Rights Reserved.

MSSI Charter

• Published charter of the MSSI objectives, obligations and commitments.

• Signed by MSSI members, industry associations and CABs.

© 2016 Eaton, All Rights Reserved.

MSSI Members

© 2016 Eaton, All Rights Reserved.

MSSI Country industry associations

Spain -

UK -

Italy -

France -

Poland -

Germany -

© 2016 Eaton, All Rights Reserved.

MSSI Conformity Assessment Bodies (CABs)

© 2016 Eaton, All Rights Reserved.

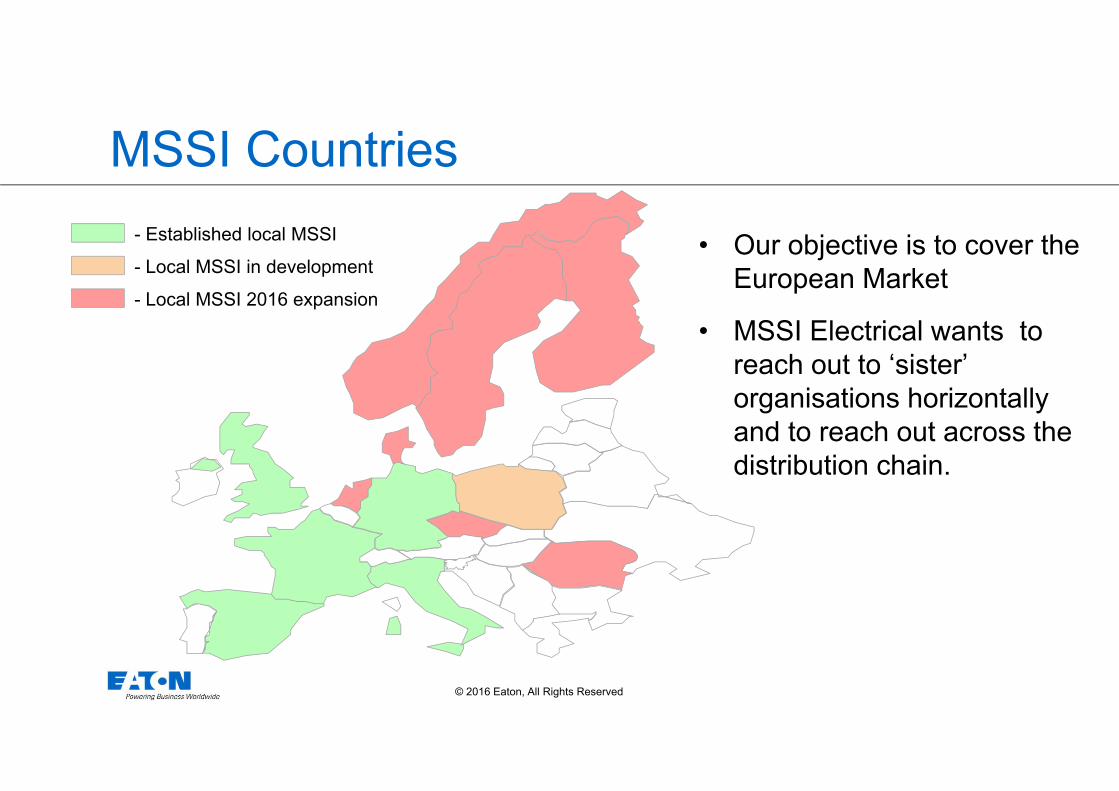

MSSI Countries- Established local MSSI

- Local MSSI in development

- Local MSSI 2016 expansion

• Our objective is to cover the European Market

• MSSI Electrical wants to reach out to ‘sister’ organisations horizontally and to reach out across the distribution chain.

© 2016 Eaton, All Rights Reserved.

MSSI Process

• Local MSSI working groups identify products and manage the process within each country.

• Common approach across all regions.• Can be slight differences

due to local laws.

Identify potentially non-compliant products

Third party CABs sample and test suspect products

If non-compliant - market surveillance authorities alerted and informed

Authorities take enforcement measures against non-compliant product

© 2016 Eaton, All Rights Reserved.

MSSI – Reaching out to the industry

• Officially launched at Light & Building 2016 - Frankfurt

• MSSI Electrical website live with Q&As, information etc.• www.mssi-electrical.org

• Knowledge and information sharing throughout the industry – manufacturers, industry associations, CABs.

© 2016 Eaton, All Rights Reserved.

Industry wide responsibility

The whole industry has a collective responsibility to ensure only compliant products are supplied, sold and used.• The revised Low Voltage Directive

places greater responsibility on operators within the supply chain.

• Importers, distributors and wholesalers assume greater responsibility for product imported into the EU.

© 2016 Eaton, All Rights Reserved.

Responsibilities of wholesalersThe European Commission ‘Blue Guide’ makes specific reference to the obligations of distributors within the renewed Low Voltage Directive.

• If the distributor also imports product then the distributor also assumes the further responsibilities of an importer.

• The distributor is a natural or a legal person in the supply chain, other than the manufacturer or the importer, who makes a product available on the market.

• Distributors are subject to specific obligations and have a key role to play in the context of market surveillance.

© 2016 Eaton, All Rights Reserved.

Risks and consequences for wholesalersWithout proper due diligence product which appears to be good could be highly dangerous.

• May cause fire, injury and loss of life.

• Loss of business reputation and confidence in products sold.

• Fines by enforcement agencies.

• Even possibility of imprisonment.

Product could appear to be good from the outside

Non-compliant - internally the reality is very different

© 2016 Eaton, All Rights Reserved.

Wholesalers play a key role

Wholesalers are a key link between manufacturers and installers.

• All products on offer MUST be compliant.

• Greater legal responsibility when importing products into the EU.

• Own brands and third party brands.

• Influence buying behaviour of installers.

• Help to spread the benefits of buying and using proven safe products.

© 2016 Eaton, All Rights Reserved.

How can MSSI help?MSSI can support through local country working groups:

• Point of contact for wholesaler associations to report suspect product found within the market.

• Coordinate testing and work with CABs and local enforcement agencies to remove non-compliant product from the market.

• Collaborate with wider industry groups such as in the UK EMS – lighting, cables, installers.

• Provide education, training and guidance tools.

© 2016 Eaton, All Rights Reserved.

Example guidance document

• MSSI working to produce guidance tools to help installers, wholesalers, customs authorities to identify potentially non-compliant products.

© 2016 Eaton, All Rights Reserved.

Benefits for wholesalers Maintain their reputation within the supply chain.

• Ability to demonstrate they have taken reasonable steps to place compliant product on the market.

Conformity to directives as a market operator.

• As wholesalers, they will be compliant with new LVD requirements

Confidence in product sold to installers

Reduced cost of guarantees and risks of liabilities

Increase the whole value of market

© 2016 Eaton, All Rights Reserved.

A few wordsJoao Bencatel – Chairman of

Conclusions

Guido Barcella – Chairman ofWorking towards the winning model

10083105

DigitizationLogisticsComunicationTechnology

powered by