Dick’s Sporting Goods, Equity Valuation and Analysis As of...

135

Dick’s Sporting Goods, Equity Valuation and Analysis As of November 1, 2007 Presented by: Nicholas Davis [email protected] Junior Ruiz [email protected] Joe Alvarez [email protected]

Transcript of Dick’s Sporting Goods, Equity Valuation and Analysis As of...

Dick’s Sporting Goods, Equity Valuation and Analysis As of November 1, 2007

Presented by: Nicholas Davis [email protected] Junior Ruiz [email protected] Joe Alvarez [email protected]

2

Dick’s Sporting Goods

Table of Contents

Executive Summary 4

Business & Industry Analysis 9

Company Overview 10

Industry Overview 11

Five Forces Model 13

Rivalry among Existing Firms 13

Threat of New Entrants 19

Threat of Substitute Products 22

Bargaining Power of Customers 23

Bargaining Power of Suppliers 26

Value Chain Analysis 27

Firm Competitive Advantage Analysis 33

Accounting Analysis 36

Key Accounting Policies 37

Potential Accounting Flexibility 40

Actual Accounting Strategy 41

Evaluation of the Quality of Disclosure 42

Potential “Red Flags” 55

Coming Undone (Undo Accounting Distortions) 56

Financial Analysis, Forecast Financials, and

Cost of Capital Estimation 59

Financial Analysis 59

Liquidity Analysis 59

Profitability Analysis 68

3

Capital Structure Analysis 74

IGR/SGR Analysis 76

Financial Statement Forecasting 79

Analysis of Valuations 89

Cost of Equity 89

Cost of Debt 92

Weighted Average Cost of Capital 92

Intrinsic Valuation Models 93

Discounted Free Cash Flows Model 101

Residual Income Model 103

Long Run Residual Perpetuity Model 104

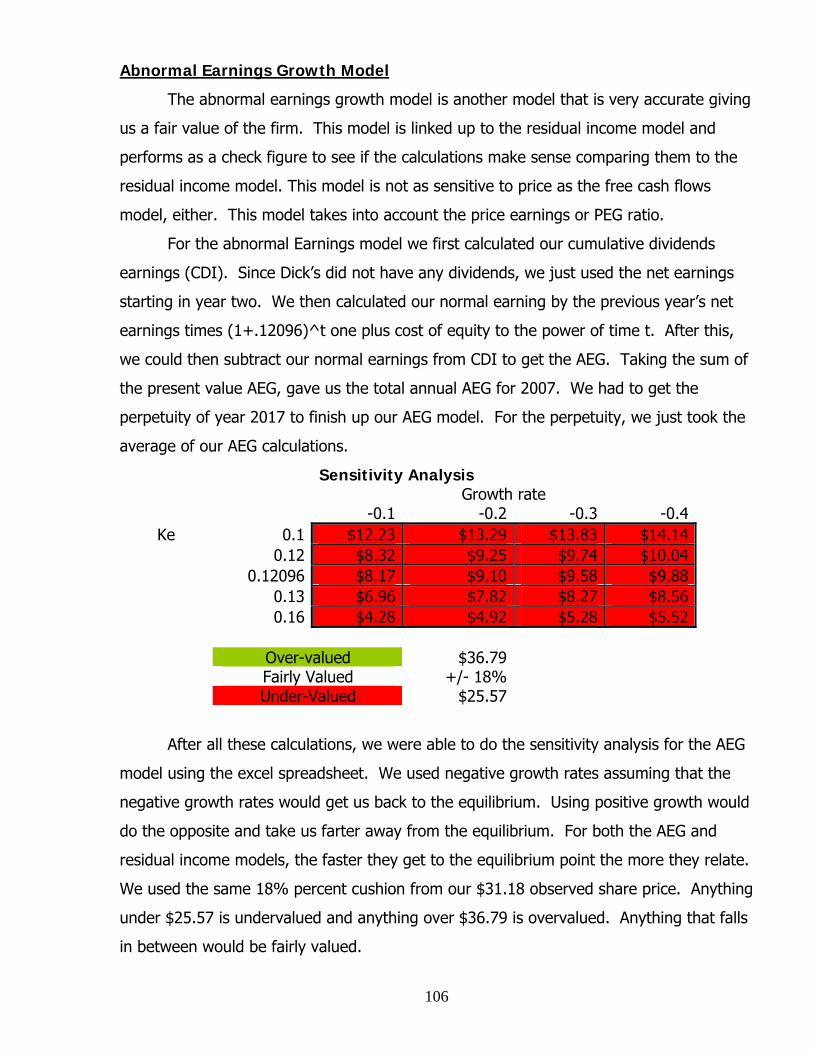

Abnormal Earnings Growth Model 106

Credit Analysis 109

Analyst Recommendation 111

Appendix 113

References 135

4

Executive Summary

Investment Recommendation: Overvalued, Sell November 1, 2007

Valuation EstimatesActual Price (11/1/2007): 31.18$

3114.16M3.39 B Financial Based Valuations

Shares Outstanding: 51.25 Mil Forward P/E: 20.71$ Avg. Daily Trading Volume(13 wk.): 931,737 Trailing P/E: 19.68$ Percent Institutional P/B: 28.32$ Ownership: 107.16% P.E.G.: 25.57$ Book Value Per Share: 8.33 P/EBITA: 41.68$ ROE: 18.15% P/FCF: 36.89$ ROA: 9.48% EV/EBITDA: 14.91$

Intrinsic Valuations revisedDiscount Dividend: n/a n/aFree Cash Flows: 15.84$ 43.53$

R2 Beta Ke Residual Income: 11.40$ 11.17$ 0.173 1.409 0.204 LR ROE: 14.83$ n/a0.186 1.468 0.211 AEG: 8.17$ 6.90$

2-year 0.195 1.559 0.2215-year 0.196 1.678 0.235 Altman Z-score10-year 0.186 1.696 0.237 2002 2003 2004 2005 2006

4.74 5.14 4.99 3.15 3.72Published Beta: 1.68 EPS:WACCBT 8.62% WACCAT 6.83% 2002 2003 2004 2005 2006Kd BT 4.99% Kd AT 2.99% 1.30 1.35 1.44 1.47 1.28

52 Week Range: $24.00 to $36.78DKS -NYSE(11/1/2007): $31.18

3-month1-year

Revenue:Market Capitalization:

Cost of Capital est.Estimated:

5

Industry Analysis

Dick’s Sporting Goods, is an authentic sporting goods retailer founded in 1948, by

Richard Dick Stack. Today they operate 322 stores in 34 states mainly in the eastern

parts of the United States. Their main target is to attract consumers seeking genuine

products with the latest trends and unique designs. One of Dick’s main goals is to be a

high quality retailer at competitive prices. Great customer service plays a major role to

Dick’s success and is a very important key.

The sporting goods industry consists of about 20,000 stores. This industry has

many competitors. Dick’s Sporting Good’s (DKS) direct competitors in the sporting

industry include: Big 5 Sporting Goods (BGFV), Hibbett Sport (HIB), and Cabela’s. Stores

like Wal-mart, Target, and Sears, that have sporting goods sections within the store can

also play a role in threat of substitute products. Firm’s then are forced to have price

wars in order to fight for market share. This is where economies of scale come into play.

With the sporting goods industry, becoming more and more fragmented, larger

companies have an advantage with their ability to sell a larger variety of brands and

products. Rivalry among existing firms is very high in the sporting goods industry and so

Dick’s must rely heavily on their key success factors, so that they won’t lose any market

share. Having strong customer and supplier relations is another key aspect. So really,

Dick’s has mixed strategies from both a cost leadership and differentiation strategies to

have a competitive advantage over the industry

Accounting Analysis

The valuation of the firm process begins with comparing the key success factors

from the five forces model and the key accounting policies. With generally accepted

accounting principals, accounting flexibility is allowed in many areas of reporting their

financial. This accounting flexibility can overvalue and undervalue financial statement

data. This flexibility plays an important factor, because it can influence managers to do

this for incentive purposes.

Operating and capital leases is one of the items that accounting flexibility allows in

the reporting. Most all sporting good’s retailers have operating and capital leases.

6

Operating leases are not recorded on the balance sheet, making shareholders believe

that they are more cost efficient. One of the most important things about operating

leases is that companies receive tax credits by expensing their lease payments. For

Dick’s, operating leases totaled up to be 2.8 billion dollars due through 2011. Operating

leases are by far the largest owed contractual obligation, with capital leases only

amounting to 7.8 million in comparison. Reporting operating leases over capital leases in

the sporting goods industry is the most popular method.

The amount of disclosure available from the 10-K’s reflect how well an outsider

can truly understand how the firm is operating. The subsequent section will give an

outlook on the quality and quantitative analysis of a firm. The footnotes provided are

made up to clear up any information that was not clear on the financials or any of the

disclosures. Dick’s 10-Ks were really easy to read and understand. Even Dick’s

competitors’ 10-K’s were well friendly formatted and made things easy to compare with

each other. Not being able to download the financial statement on excel was the only

negative thing about the 10-K’s.

The sales and expense ratio diagnostics was another tool in the valuation of Dick’s

Sporting Goods. Dick’s seemed to be lying at the industry average in most sales and

expense diagnostics if not above the average. These ratios gave us great insight in

comparison of Dick’s to the sporting goods industry. The only potential concerns or “red

flags” were the operating and capital leases, which most sporting goods store have since

it is allowed under GAAP.

Ratio Analysis, Forecast Financials, and Cost of Capital Estimation

The liquidity, profitability, and capital structure ratios were another key aspect to

the valuation of a firm process. We used these ratios as a guide in observing trends and

structure in the ratios that were linked together with the financials. Computing these

ratios not only gave us a sense where Dick’s compares within the sporting goods

industry, but they served as a mentor tool in the forecasting of the financials. After

forecasting the financial statements, we moved on and estimated Dick’s beta by using the

CAPM model, we estimated the cost of equity (Ke) by using the regression analysis. For

7

the regression, we used the St. Louis Fed to gather the constant maturity rates to get a

fair market risk free rate. The market risk premium was then subtracted to the risk free

rate for each maturity. The outcomes for beta were fairly consistent throughout. The

estimated weighted average cost of capital (WACC) was done using the formula; on a

before and after tax.

After analyzing the liquidity ratios, we can conclude that Dick’s was below the

industry average with regards to the current ratio and quick ratio. The inventory

turnover and working capital ratios showed positive indications placing Dick’s above the

industry average. The gross profit margin showed positive indications as well with Dick’s

over the top of its competitors. These were some good signs that Dick’s is growing and

has been profitable for the past years. These ratios show the liquidity, profitability, and

capital structure for the firm in the past 5 years calculated.

The internal growth and sustainable growth rates were calculated as well to help

us decide how fast Dick’s is growing. 14.6 % was average internal growth and the

sustainable was 39.08% in the past 5 years. The growth did not seem reasonable for our

future estimates and so we decided to go with 5%. We assumed 5% because of the

actual industry growth is between 3-4 percent. Dick’s seemed to be growing a little

faster than the industry and so that is how we decided to go with 5%.

Intrinsic Valuations Models

The valuations models we used include; Discounted Dividends Model, Residual

Income, Long-run Residual Income Perpetuity, and the Abnormal Growth Model. We did

not include the Discounted Dividends model because Dick’s does not pay any dividends,

and so it did not make any sense in our valuation. All these models gave us an implied

share price. The implied price tells us what the share price should be. With this price we

can determine if Dick’s Sporting Goods is under or overvalued. The estimated prices that

we calculated are all discounted back to present values. The WACC and Ke were all used

throughout the different models to be able to come out with the share price.

All of our intrinsic valuation models were fairly consistent with the implied prices.

We observed a price of $31.18 on November 1, 2007 and was a benchmark tool to

8

evaluate if the firm was under or overvalued. We even had an 18% spread of the

observed price. All of our models indicated Dick’s Sporting Goods to be overvalued.

Taking the value of the firm for Dick’s and doing the sensitivity analysis gave us most

values calculated under the $31.18. This demonstrates Dick’s being overvalued. All of

the models we used showed the same outcomes in respect to under and overvalues. The

AEG and the residual models are the most commonly used because they are the most

reliable in terms of confidence and accuracy.

After analyzing all the models discussed, we determined that Dick’s Sporting Goods

is overvalued and recommend selling the stock as of November 1, 2007. The Altman Z-

score showed Dick’s to be above 3.1 in the past years and even higher than 5 in 2003.

This credit analysis is a measure of the probability that a company will go bankrupt.

Dick’s seems to be profitable and less likely to go bankrupt. The Altman Z-score uses 5

different ratios from balance and income statements to calculate this measure. The

higher the ratio, the better the indication is that a company is at low risk of bankruptcy.

With this credit analysis, Dick’s seems to be a grade A investment. They have been over

the top of the industry average in most of the comparisons that we did.

9

Business and Industry Analysis

Company Overview

Dick’s Sporting Goods, is an authentic sporting goods retailer. Dick’s Sporting

Goods was founded in 1948, by Richard Dick Stack. It currently operates 322 stores in

34 states. Their stores are mainly located in the eastern parts of the United States.

Dick’s Sporting Goods main goal is to offer costumers the opportunity to “enhance

their performance and enjoyment of their sports activities.” (Dick’s 2006 10k) Its primary

focus is to attract consumers seeking genuine products rather than products on the latest

fashion trends or style. Dick’s is full line sports retailer in the specialty industry. Their

merchandise includes: sporting goods equipment, athletic apparel, footwear, outdoor

recreation equipment, fitness equipment, and fishing and hunting accessories, as well.

Dick’s goal is to be a high quality retailer offering well known brands such as Nike, North

Face, Columbia, Adidas, Callaway, and Under Armour. As well as a couple of their private

brand labels available only at their stores like Walter Hagan and Ativa. “We seek to

create a distinct look and feel for each specialty department to heighten the customer’s

interest in the products offered.” (Dick’s 2006 10k) Dick’s Sporting Goods focuses on the

customer is a key to their success.

The sporting goods industry consists of about 20,000 stores. This specialty retail

industry is very competitive and has many competitors. Dick’s Sporting Goods major

competitors consist of Cabela’s (CAB), Big 5 Sporting Goods (BGFV), and Hibbett Sporting

Goods (HIBB). Dick’s Sporting Goods has a market cap of $3.61 billion. Cabela’s is a

fierce rival to Dick’s Sporting Goods and growing fast. Cabela’s current market cap is

$1.56 billion. Hibbett is another well established sporting goods retail company with a

market cap of $765.15 million. Dick’s Sporting Goods is one of largest sporting goods

leading retailers. Dick’s Sporting Goods has been steadily increasing their sales and

profits by expanding their stores all over the United States. On July 29, 2004, Dick’s

Sporting Goods Inc. acquired all of Galyan’s Sports & Outdoor common stock and its 47

stores. Its continuous growth in sales and profits also allowed Dick’s to recently purchase

10

Golf Galaxy, Inc. and its 65 stores, “which became a wholly owned subsidiary of Dick’s by

means of a merger of Dick’s subsidiary with and into Golf Galaxy.” (Dick’s 2007 10K)

Dicks Sporting Goods has been increasing their sales and profits by expanding

their stores all over the United States. Their total assets and net sales have been

increasing over the past five years. This table indicates what portion has come from

sales growth and what portion has from the opening of new stores. (Invetopedia.com) As

for Dick’s, besides in year 2003 where comparable sales decrease to 2.1% it increase to

2.6% in 2004 which means that Dick’s was able to earn 2.6% more revenue compared to

year before. As for in year 2005 it remain the same and then a huge increase to 6.0% in

2006. This increase in 2006 is good because it shows that Dick’s is growing and that

consumers are willing to pay more for goods this year thus showing an increase to

revenue. The numbers are displayed below.

Total Assets, Net Sales, and Comparable Sales Growth 2002 2003 2004 2005 2006 Total Assets $321,982 $376,226 $543,360 $1,085,048 $1,187,789 Net Sales $1,272,584 $1,470,845 $2,109,399 $2,624,987 $3,114,162 Sales Growth 5.1% 2.1% 2.6% 2.6% 6.0%

Dick’s Sporting Goods stock price has increased from $19.20 in 2002 to $48.27 in

2007. The percentage change has really increased in the past years. If you compare the

price change from Dick’s Sporting Goods to its competitors, the price change really stands

out. Dick’s Sporting Goods direct competitors price change is not much different from the

past five years.

11

www.moneycentral.msn.com

Industry Overview

The retail industry “includes establishments engaged in selling merchandise for

personal or household consumption and rendering services incidental to the sale of the

goods” (www.osha.gov). According to the U.S. Department of Labor sporting goods

retailer companies are given the Standard Industrial Classification Number of 5941. The

sporting goods retail industry consists of retailers involved in the advertising and

distributing of “new sporting goods, including bicycles and bicycle parts, camping

equipment, exercise and fitness equipment, athletic uniforms, athletic apparel for men,

women and children, specialty sports footwear and other sporting goods, equipment and

accessories”(www.ibisworld.com).

The retail sporting goods industry consists of over 20,000 companies with

combined annual revenues of approximately $25 billion each year. The major

competitors of Dick’s Sporting Goods in this industry are Big 5 Sporting Goods, Cabela’s

Incorporated, and Hibbett Sporting Goods. Due to the fragmentation of the market,

companies must rely on their merchandising and marketing skills. For example, Dick’s

Sporting Goods has been involved in sponsoring several major and regional sports teams.

Sports apparel and footwear tends to be the largest sellers in most sporting goods stores,

this is mostly due to the cyclical nature of the sporting world.

12

There are four different types of sporting goods retailers. The first type is the

large specialty sporting goods stores and chains like Dick’s Sporting Goods, Cabela’s Inc.,

and Big 5 Sporting Goods. The second type are large discount retail stores like Wal-Mart,

Target, and Sears, that have a small sporting goods section located within them. The

third type of sporting goods stores are specialty shops that carry deeper lines of products

focused on a certain team or sport. The last type of stores is the online retail stores,

which provide a wide variety of products available for purchase over the internet. Even

though these smaller and larger companies are a part of the competition, they are not

specialized sporting goods stores with the same inventory and sales as Dick’s, so they do

not compete directly with Dick’s.

13

Five Forces Model

The five forces model is a tool used to analyze the profitability and competition in

a given market. The five segments of this model are used to evaluate an industry in

specific areas. The five forces model is made up of: rivalry among existing firms, threat

of new entrants, threat of substitute products, bargaining power of customers, and

bargaining power of suppliers. The first three parts of this model are used to analyze

potential competition in the industry. The last two parts focus on the power suppliers

and customers have in relation to the firm. Overall the model is used to evaluate

problems affecting the profitability of a firm in a market.

Sporting Goods Retail Industry Rivalry Among Existing Firms High

Threat of New Entrants Moderate Threat of Substitute Products High Bargaining Power of Buyers High

Bargaining Power of Suppliers Moderate

Rivalry among Existing Firms

In general the retail industry is highly competitive, forcing most companies to

compete on price. The sporting goods retail industry is extremely competitive, with many

factors weighing into the success of any individual company. Not only does the industry

face a very low growth rate, but it also has an extremely high fragmentation of the

market. Within the sporting goods retail industry companies must compete against each

other with very little differentiation between their products. But there are other factors

that determines the profitability of a firm, such as whether or not there are switching

costs, the scale of the economies, fixed -variable costs, the capacity level, and exit

barriers. These are all variables that contribute to the overall success of the firm.

14

Industry Growth Rate

Industry growth plays a very crucial role in the success of a firm. If the growth

rate is high, then existing firms in the market need not grab market share from each

other in order to grow. On the other hand if the market has little to no growth, then

companies must compete in order to be successful. In recent years the U.S. sporting

goods market has had moderate growth, with “sales barely matching the growth of the

economy” ( www.ita.doc.gov). According to the U.S. Department of Commerce real

apparent consumption has only grown 3 percent in recent years. This low growth rate

makes the industry extremely competitive, and many smaller companies have trouble

competing. As a result companies that already exist are forced to compete by acquiring

smaller companies that already has a consumer base. This is evident by companies like

Dick’s acquiring smaller companies like Golf Galaxy just this year.

Industry Sales Growth

2.95

1.9732.33

0.23

4

00.5

11.5

22.5

33.5

44.5

2002 2003 2004 2005 2006

The comparable same store sales’ is another way to see how the company and the

industry are doing. It measures the “productivity in the revenue and sales of a store in

comparison to its operation in the previous year” (Answers.com). Basically this shows

what portion of the overall sales was due to new store openings. This analysis is

15

important because for those companies that are growing quickly and establishing many

new stores, these figures can help differentiate between sales growths that come from

new stores and growth of existing stores. So the following table illustrates what the new

store openings contribute to the overall sales growth. Along the growth at the industry

level, these percentages show what portion of growth came from opening of new stores.

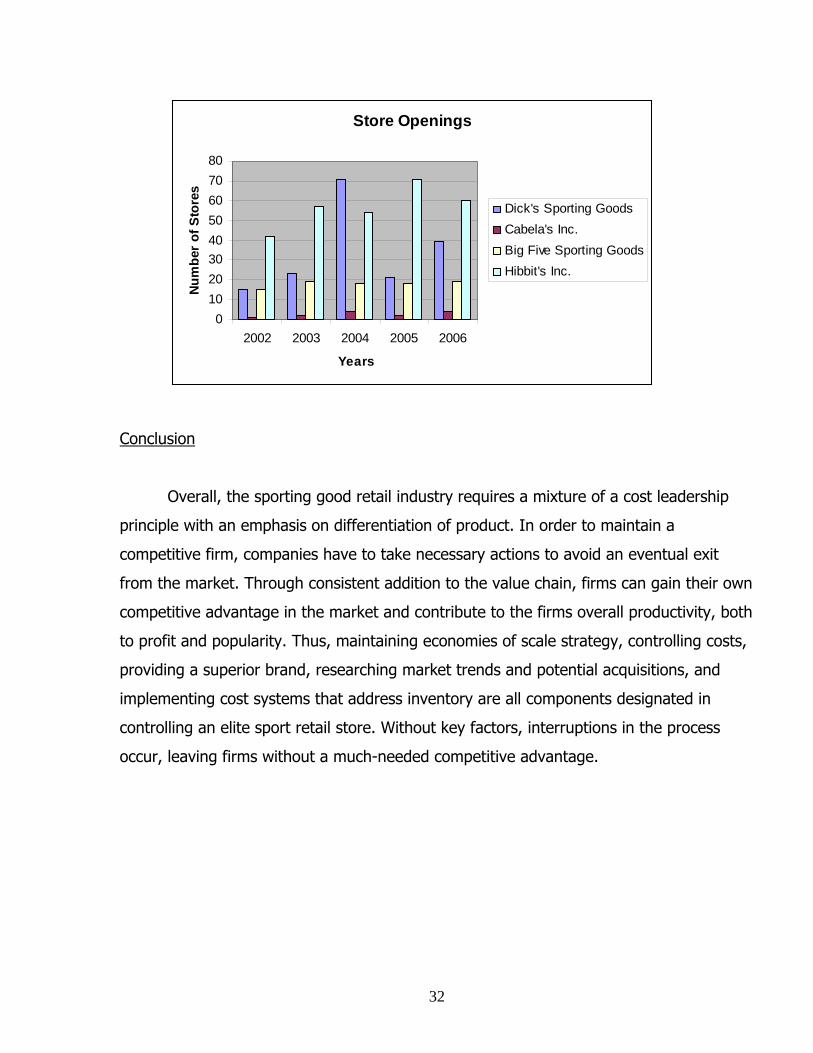

In 2006, there was a huge jump the new store openings sales growth. Following the

comparable same stores sales is a chart showing the amount of stores opening by each

company each year. Due to the slow industry growth rate, the pressure of competition

increases, forcing companies to buy out smaller companies which is apparent in the

chart.

Comparable Same Store Sales 2002 2003 2004 2005 2006Dick's Sporting Goods 5.10% 2.10% 2.60% 2.60% 6.00%Cabela’s Inc. 3.70% 0.60% -0.10% -6.20% 1.30%Big 5 Sporting Goods 3.90% 2.20% 3.90% 2.40% 4.00%Hibbett’s Sporting Goods 2.70% 3.90% 5.30% 5.70% 5.60%

Store Openings

01020304050607080

2002 2003 2004 2005 2006

Years

Num

ber

of S

tore

s

Dick's Sporting GoodsCabela's Inc.Big Five Sporting GoodsHibbit's Inc.

16

Concentration

Concentration is the number of companies an industry possesses, typically the

lower the number of companies in a given industry the higher the profit margins. The

retail sporting goods industry “is highly fragmented: the 50 largest companies hold less

than 50 percent of the market” (www.firstresearch.com). In recent years there has been

an over abundance of choices for consumers to choose from, with many of the large

chain superstores expanding and creating new stores. Large companies in the market

have a competitive advantage over smaller companies due to their ability to carry a wider

variety of products.

Market Share

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%45.00%50.00%

2002 2003 2004 2005 2006

Year

Perc

enta

ge C

hang

e

Hibbett SportsBig 5 Sporting GoodsCabela's Inc.Dick's Spoting Goods

Differentiation and Switching Costs

Most of the products and labels sporting goods stores carry are generally the same

throughout the entire industry. This similarity in quality and price causes an increase in

competition pressure and a result; companies have to find alternative ways to

differentiate their products and services. Since there is a similarity in products within this

industry, this allows costumers to switch from one firm to next. In other words, since the

products are very similar, “costumers are ready to switch from one competitor to another

purely on the basis of price”(Business analysis and Valuation). Because of these low

17

switching costs many companies in the industry must find a way to differentiate

themselves from each other. So firms have found alternate ways of using their resources

they already have to attract the consumers. Many of the larger sporting goods stores

have begun to change their entire store format to make their shopping experience more

enjoyable by adding entertainment aspects such as climbing walls, driving ranges, and

exercise facilities (www.ita.doc.gov). Another alternate way firms have used is to offer

promotions and sale discounts on their products.

Economies of Scale

Total Assets 2002 2003 2004 2005 2006 Dick's Sporting Goods 321.98 413.53 543.36 1,085.05 1,187.79 Cabela's Inc. 521.01 581.63 728.49 694.03 954.22Big 5 Sporting Goods 190.41 223.19 237.44 255.90 262.61Hibbett Sporting Goods 87.68 103.19 142.26 167.35 155.48

*in millions of dollars

The size of a company can make a huge difference, especially in the highly

competitive sporting goods retail industry. With the sporting goods industries becoming

more and more fragmented, larger companies have an advantage with their ability to sell

a larger variety of brands and products. As the figure above illustrates Dick’s Sporting

Goods and Cabela’s Incorporated are the two leading companies in the industry, making

it easier for these companies to draw customers to their stores due to their ability to offer

lower prices. The chart below shows the amount of stores increasing each year and

Dick’s is one of the leading competitors.

18

Store Openings

01020304050607080

2002 2003 2004 2005 2006

Years

Num

ber

of S

tore

s

Dick's Sporting GoodsCabela's Inc.Big Five Sporting GoodsHibbit's Inc.

Ratio of Fixed to Variable Costs

The ratio of fixed to variable cost is another indicator of how the company is

handling its operating costs. Fixed costs are expenses do not change despite the change

in companies activities. Common examples of fixed costs are lease payments and

salaries. Variable costs refers to expenses that do change in proportion to sales is

variable costs. This can include many things such as costs of goods sold, sales

commission, etc. If the ratio is low this indicates that companies are not locked in from

their obligation such as operating lease payments and have liberty to use their money in

different ways. But on the other hand, if the ratio is high this means that the companies

have many obligations to be met and are not so free to use their money for different

resources.

As for the sporting goods industry most of their fixed costs consists of operating

leases. As noted before companies are purchasing new stores and acquiring new leases

which require payments due for a certain amount of time. The same applies to the fix

salaries amount that companies pay their employees each year. Many companies invest

in large amounts of inventory to sell at lower prices to cover these costs. As for variable

costs, it can refer to many things such as all of cost of goods expenses, amount of fuel it

takes for a freight to distribute the goods, to the amount of packaging required for the

19

goods, etc. These variable costs vary each year relative to the amount of sales

produced.

Excess Capacity and Exit Barriers

Excess capacity in an industry is when supply exceeds demand, which creates an

incentive for a firm to cut prices in order to fill capacity. For larger companies in the

sporting goods retail industry, like Dick’s, Cabela’s, and Big 5 Sporting Goods, excess

capacity is very controllable, but for smaller companies it can be difficult to control due to

less pricing control. A firm within the sporting goods and retail industry could face

difficult exit barriers. For example, when a market is doing poorly, it would be costly for

firms to exit the industry. It will be an extremely challenging task to clear out their

assets. Regulation is another factor that would make it costly for any firm to leave the

industry. When a market is doing poorly some larger firms can face the problem of

turning customers off of their products if they try to leave that market, so in order to

keep a friendly customer base they must stay within the market.

Conclusion

The sporting goods retail industry is highly competitive, with a very fragmented

concentration. Because of its low growth rate companies must rely on their marketing

and merchandising skills in order to draw a bigger customer base. Larger companies

have a major advantage, because of deeper inventories and more options to choose

from.

Threat of New Entrants

New entrants are easily attracted to an industry when there is the potential for

earning major profits. New firms in an industry can add pressure to current companies

within an industry depending on how low the industry growth rate is. A key determinate

of industries profitability is the ease with which new companies can enter the market.

The major concerns when dealing with new entrants revolve around economies of scale,

distribution access, relationships between suppliers and consumers, and legal barriers.

20

Economies of Scale

It is important for any new company planning on entering an industry to first

realize the economies of scale in that industry. The sporting goods retail industry is

highly fragmented, with “50 largest companies hold less than 50 percent of the market.

Only about 150 companies have more than five stores”(www.firstresearch.com). Larger

companies do have an advantage over smaller new companies due to their ability to have

a much larger and broader inventory.

The market for sporting goods retail does have a very small growth rate however,

so newer companies must utilize their marketing and merchandising skills. Smaller

companies are able to compete if they carry a deeper line in a specialized sport, or if they

focus on a local market such as professional or college teams. New companies looking to

enter the sporting goods retail market could find it much easier to establish an online

website. Larger companies have taken advantage of internet shopping in recent years,

and have set up websites which makes it quick and easy for customers to purchase

items. According to the following chart, for a smaller company to even compete on the

same level as large companies in this industry, these are the values that they would be

up against. It is easy to conclude that smaller company’s entering in this market are at a

disadvantage.

Total Assets 2002 2003 2004 2005 2006 Dick's Sporting Goods 321.98 413.53 543.36 1,085.05 1,187.79 Cabela's Inc. 521.01 581.63 728.49 694.03 954.22Big 5 Sporting Goods 190.41 223.19 237.44 255.90 262.61Hibbett Sporting Goods 87.68 103.19 142.26 167.35 155.48

*in millions of dollars

21

Access to Channels of Distribution and Relationships

In any industry it is important to have channels of distribution, because the cost of

new channels can dissuade a company from entering the market. In the sporting goods

retail industry it is extremely important for new firms to develop relationships with

manufacturers and customers. Larger firms have a greater advantage in this due to the

larger orders placed through certain manufacturers, and the time spent in the market

developing a personal relationship with customers. The relationship that already exists

between the firms and their costumers make it extra difficult for new companies to enter

into the market. A smaller company can try to enter into a deeper product line in

specialty products or try to serve a local market.

Legal Barriers

In general the retail industry has very few legal barriers to entrance; this is true

for the sporting goods retail industry. Smaller companies that focus on a particular team

might need to create a contract in order to distribute that teams name products,

especially if they are creating the merchandise themselves. Because of the lack in legal

barriers the sporting goods retail industry has a higher risk of new companies entering

the market.

Conclusion

Due to the sporting goods retail market being extremely fragmented, the threat of

new entrants is always possible. The difficulty that new entrants have on entering the

industry also determines the amount of profits a certain firm is able to obtain. The are a

couple of factors that new entrants face, such as the large economies of scales where the

level of competition among existing firms is to high for new entrants. Another factor is

not being able to develop an relationship with suppliers so easily due to the already

existing relationships between existing firms and their suppliers. Finally one of the few

opportunities that smaller companies do have is the few amount of lack there of legal

barriers. But in all these companies do face a hard time competing against larger

companies and generally must become specialized stores in order to compete.

22

Threat of Substitute Goods

Another form of competition in the industry is the threat of substitute products.

Substitute products can be the similarity between the products sold between the

companies or it can also refer to the products that perform the same task. Within the

sporting goods industry the threat of substitute products are low when it comes to

apparel clothes or shoes, because these products are necessary when performing any

extracurricular activities. In other words, what can one wear when performing the task of

running? But for the larger format stores that have the different level of entertainment

within the stores, i.e. wall climbing, indoor track, etc., one can easily avoid the cost of

traveling to these stores and go somewhere else to perform the same activities. But still

it is important for companies to meet all the needs of its customers if it is going to

compete in this market.

Buyer’s Willingness to Switch

Because of the several different options a consumer has in the sporting goods

retail industry, it is important for a company to provide the consumer with the product

and price they are looking for. Since there are many types of consumers that are willing

to switch products just on price, makes for low switching cost which becomes a factor for

the sporting goods industry. But on the other hand, there are consumers that are not so

willing to incur the cost of shopping around just to find the lowest price possible also

plays a critical driver for this industry. Thus sporting goods stores must put a higher

emphasis on customer service in order to give the consumers a pleasant and enjoyable

experience. But the fact that there are costumer’s that are willing to switch becomes a

huge factor that sporting good stores must face at all times.

Relative Price and Performance

Substitute products for the consumers usually depend on whether or not they

perform the same task for the same price.( the book) As a result consumers are more

willing to switch purely on price. But when the prices are low, consumers might feel that

23

the products are low in value. So the sporting goods retail industry incorporated having

brand name products that commands a premium on price, consequently consumers feel

that these brand name products have a higher value since it costs more. Consumers are

always looking for the best quality at the lowest price. The sporting goods industry

acknowledges this area by carrying a variety of products. There are no name brands to

well known ones. It is also important that they carry high quality products sold at a

reasonable price since that is usually what consumers are looking for. In order for a

company to compete in this industry it must satisfy all of its customer’s needs by offering

these brand name products sold at a fair price. As a result, sporting goods stores have

begun a policy that allows customers to price match for their goods.

Conclusion

Because of the ease in which consumers can find a substitute product it is

important for companies in the sporting goods industry to provide a great shopping

experience for its customers. Due to the industries low switching costs it is important

that companies provide a customer friendly environment. This means providing quality

goods for a reasonable price, along with great customer service and support.

Bargaining Power for Costumers

Consumers have a bargaining power that initially creates a demand in the

industry. If the bargaining power of the consumer is high; this indicates that there are

many sellers and few buyers in the industry. On the other hand, if the bargaining power

of the buyers is low, it exemplifies that it has a limited affect on business operations. In

an industry where the concentration of buyers demonstrates that the bargaining power is

high and is sold “directly to the final customers”, this allows the industry to compete on

price.

The sporting goods retail industry consists of a market that is highly fragmented

and competitive. The companies consist of categories in large-format sporting good

stores and chain, discount and department stores, and specialty stores. These stores can

24

be located in various locations such as in the mall, or be free standing with a parking lot,

or near a recreational area. Since there are numerous of locations where a costumer

could initially purchase a sporting goods product, this reflects on the costumers

bargaining power of the companies. Also, this is an industry that consists of different

types of costumers such as enthusiast, intermediate, and a beginner level. All of these

factors determine the bargaining power of the costumer. (www.commerce.gov)

Price Sensitivity

“Price sensitivity determines the extent to which buyers care to bargain on price.”

(Business Analysis & Valuation) Consumers ultimately tend to seek the lowest price

possible. But there are certain factors that determine whether or not the consumer is

willing to incur the cost of finding the lowest price. Factors such as: the differentiation of

a product and the amount of suppliers in a certain area. When the products are similar

within the industry, costumers are more willing to switch products based entirely on

price.

In the sports goods industry products are either “sold in small quantities to the

general public” or in large quantities to major or regional sports team. At the general

public perspective there are three different types of costumers: beginning, intermediate

and enthusiast. If the costumer is at a beginning or even at an intermediate level, they

are more concern with price rather than quality. In a industry where there are low

switching cost and the product is undifferentiated, costumers are more inclined to

purchase their products at the nearest sporting goods store. This in turn impacts the

industry where they tend to compete in price wars. In retrospect, major and regional

teams usually have the resource and are more concern in purchasing sporting goods

products pertaining to their quality rather than price. The same applies to costumers who

are enthusiast. These types of costumers will incur the cost to go to the location that

offers the best type of quality. For these costumers, switching cost is relatively high and

differentiation does matter.

25

Relative Bargaining Power

The relative bargaining power refers to the ability a costumer has to switch from

one supplier to the other despite the price of the product and in turn eventually impacting

the company. In the sporting goods retail industry, top companies generally sell the

same products such as top brand name apparel and equipment causing this industry to

be undifferentiated and have low switching cost. Also there is a high level of competition

and as a result, costumers have a high relative bargaining power. This in turn affects the

company where they are forced to differentiate themselves from their competitors.

Companies can lower their price but this will ultimately have a negative impact since

there are low switching costs. They are not impacted when a single costumer decides

not to purchase their product. This leads companies to develop new strategies and ideas

of attracting the costumer. “Since there are more places and choices to shop, this has

created a survival of the fittest mentality where many retailers have opted to super-size

themselves in to larger stores and even creating stores that are more of an entertainment

to costumers.” Such as creating stores that have in-store features such as: climbing

walls, exercise facilities, basketball courts, golf driving ranges, and etc.

(www.commerce.gov). In the sporting goods retail industry, there is a high level of

competition, the products are undifferentiated, and there are low switching costs and

thus allowing costumers to have a high bargaining power over these companies.

Conclusion

In this sporting goods retail industry, there is a high level of competition. As a

result, companies in this industry must consider the factors that contribute to the

bargaining power that their consumers have over them. Factors such as price sensitivity

and the relative bargaining are crucial in analyzing and applying to their business strategy

in order to become profitable.

26

Bargaining Power of Suppliers

For any type of industry, there are suppliers where their business is to supply the

companies with materials or products. Companies acquire these products at a cost from

the supplier which basically determines their profitability (www.tutor2u.net). Suppliers

have a high bargaining power when there are many buyers and a few suppliers.

Subsequently, the products have a high value where companies are forced to incur cost

depending on the suppliers demand. Also the industries are not the supplier’s primary

costumer. When the bargaining power is low, this indicates that there is an ample

amount of suppliers and few costumers. Companies are able to bargain on prices with

their suppliers.

Price Sensitivity

As mentioned before, price sensitivity refers to the particular costumer willing to

look for the lowest price. In the case of suppliers, it is their willingness to allow

companies to bargain with their prices. In the sporting goods retail industry, companies

purchase their merchandise from different type of vendors since they carry a wide range

of products. Their products vary from top quality brand name goods to lower qualities

and for the average costumer they usually seek to get the best quality for the lowest

price. As a result, the bargaining power for suppliers is low. Since suppliers also use

sporting goods companies to sell their products and sell in larger bulk, they tend to allow

companies to bargain for their price.

Relative Bargaining Power

The relative bargaining power of suppliers deals with if they are able to sell their

products at the highest possible price. This depends on the amount of suppliers and

buyers in the industry, product differentiation, and the importance of their product

relative to the costumer. Analyzing these factors, determines the level of bargaining

power a supplier has over their costumer. In this industry there is an ample amount of

27

suppliers competing for retailer’s shelf space. But there are some suppliers that are able

to have a higher bargaining power than others. Sporting good retail stores incur

additional cost in order to have brand name products in their shelves. Therefore these

types of suppliers have been able to achieve differentiation within their products and sell

at a higher price. Since costumers do seek value in products, companies do find it

important that they carry top name products in their line. Although companies do carry

other similar products but a lesser value, the relative bargaining power for suppliers

would be moderate.

Value Chain of the Industry

The Overall Classification of the Industry

In order for a company to be successful, the industry has to have an available

niche that a company can grab and run with. Each company has two available strategies

that can eventually yield a more attractive competitive advantage: cost leadership or

product differentiation. While considering both, a company has to decide if they want to

distribute a mass produced product at a lower cost or select a unique product or style

that creates attraction to the public. In this type of industry, the majority of companies

incorporate a mixed strategy of cost leadership and product diversity to gain market

share or a competitive advantage. Surprisingly, if it were this easy sporting good stores

would enter the market consistently across the country.

Previously considered factors such as high rivalry among existing firms, moderate

threats of new entrants, high bargaining power of buyers, and low bargaining power of

suppliers lay out the difficulty in maintaining a competitive advantage in the considered

industry. Therefore, it is best to consider a two-headed strategy that in some way

incorporates both a low cost advantage and a unique approach. The sporting good retail

market is similar to any other retail market because established outlets already have

advantages. These advantages include good relationships with suppliers, an established

client base, and experience. Being a major competitor such as Dick’s Sporting Goods or

28

Foot Locker requires more than just a low cost strategy; a value chain is necessary to

fulfill an entrance. Although both strategies are necessary, a cost leadership strategy is

the focus with an emphasis of differentiation. In order to compete with the specialty

stores that only cater to a certain spectrum, lower cost driven stores have the ability to

diversify selection and compete on prices. Thus, “large chains have an advantage in

stocking a wide variety of goods” (www.hoovers.com). With an extensive selection of

products, competition is limited and profit margins potentially grow.

The decision to enter the sporting good retail industry breaks down into many

factors that add up to form a value chain. This chain consists of components involving

economies of scale, lower input costs, superior product variety, research and

development, and tight cost control systems. Also, an “aggressive pursuit of a creative,

optimistic strategy can propel a firm into a leadership position, paving the way for its

products and services to become the industry standard” (www.allbusiness.com). Without

some of these elements, the chain breaks and competitive advantage weakens against

the rest of the market.

Economies of Scale and Scope

Emphasizing economies of scale in this industry is proactively the best

consideration, but is hard to do as a newcomer to the market. Economies of scale refers

to when a as a company grows and amount of production increases, these companies will

then have a better opportunity of decreasing its costs. (investopedia.com) Therefore, big

companies already have a competitive advantage in lower costs and customer purchasing

price. The economies of scale can arise in by making large investments in the in

company’s size and products. By expanding its store size, opening more stores, and

purchasing larger quantities of products, companies are able to have more available

products thus reducing their costs in the long run. For example, companies like Dick’s

and Big Five sporting goods have been able expand their companies by creating larger

format stores and creating a chain of stores throughout the country either by merging

with another company or by acquisition. As for other companies like Hibbett’s, they have

29

been able to establish 202 of their stores in enclosed malls around the country (Hibbett’s

2007 10-K). As for economies of scope which is similar to economies of scale, it is

associated by the demand-side of changes by increasing scope of marketing and

distribution. For example, some companies promote and sell their products through

catalogs like Cabela’s, in which each year they mail out about 135 million catalogs in and

out of this country. (Cabela’s 2007 10-K) In all, each company has also been able to

advertise and sell their products through the internet. Being able to have products more

widely available to the consumers, allows companies the opportunity to decrease its costs

thus achieving the theories of economies of scales and scope thus having economic

growth.

Lower Input Costs

Without a cost advantage, the sporting good retail industry would only offer

specialty stores that cater to very specific needs. Certain aspects of the market require a

low cost input, which stems off the economies of scale philosophy. If agreements

between suppliers and stores do not form through contracts then cost can become an

issue. In order to sustain a profit margin, cost needs to be the main area of focus. Input

costs are minimized by eliminating overhead and maintaining a valuable relationship with

suppliers. When purchasing products in bulk, suppliers typically reduce price due to a

mass quantity. In order to create a reliable connection with a supplier the firm has to

move product in a timely manner. In addition, just as the firm has to sell its products, the

suppliers have to deliver their end of the bargain within a respectable period.

Superior Product Variety

The sporting goods retail industry in general has high demands for a selection of

the best products available on the market. Customers’ personal preferences and tastes

are segmented into different categories that a successful firm should be able to fulfill on a

consistent basis. As mention before, there are three types of costumers for the sporting

30

goods industry which includes costumer at a beginner, intermediate, and at a enthusiast

level. Since there are intermediate and enthusiast costumers, they tend to seek top

private labels offered at premium prices. Each company differs on what exclusive brand

offering they have to offer the costumer but each try to incorporate a line of these

products for the consumers. Furthermore, customers always want the best product at

their price; thus, a superior product variety yields more customer satisfaction. Happy

customers equal a positive return on investment. With superior products, competitors

face more market decisions and are forced to compete on selection. Knowing what type

of product to sell at the right time when comparing seasonal sports is important. In fact,

without any research into product popularity or customer taste a superior product variety

might not exist. Factors such as what type of costumers would purchase these products,

the time of year to sell a certain product, and as well as role of the economy, all come

into play on deciding the type of product quality and variety to offer to the consumers.

Research and Development

Through investing in research and development, firms can discover their ability to

market product more efficiently. In order to maintain an appropriate selection of product,

firms have to know the customer’s preference, willingness to buy at a price, and the

popularity of a product. Companies also need to be up to date with the following trends

and styles in order to appeal to their consumer base. Without knowledge of the market,

a firm cannot proactively accomplish any of these factors. In the sporting goods industry,

companies have invested in having a personal staff that continually searches for the

latest products out in the market. Companies have also been able to establish costumer

feedback either through their own personal website or catalogs. On each of the

company’s website, one is able to set up an account and be informed on the latest

products as well as giving back personal feedback. This is also an important tool for

companies to use on determining what products to have available.

31

Tight Cost Control Systems

Companies that try to achieve cost leadership generally focus on tight cost

controls. Companies have to develop a system that beneficial to their own company that

allows them to control their costs and maintain a competitive advantage in the industry in

other words, companies will have to find ways to monitor and lower their costs while still

maintaining a profit. One way that this is achieved is by having accessible distribution

centers that allows for stores to have their merchandise more readily available with out

incurring the cost of expensing extra money to receive the goods. Another way is having

inventory control where companies can set up a system at each store that will allow them

to know which items are out and which items are coming in. Also, being able to know

which stores are producing profits and ones that profits are declining also helps in

minimizing costs.

In the sporting goods industry, all of the companies in this industry

currently have more than two distribution centers that have products readily available to

be shipped to the stores. These distribution centers are usually equipped with mass

quantities of products that can facilitate one to two hundred stores. Among these

companies like Dick’s, Cabela’s, Big 5, and Hibbett’s, each have operating system that

allows them to track all of the inventory that has been purchased and sold. Over the past

years, most of these companies have grown in considerable portions, some being able to

establish about 20 to 30 stores per year. While old stores are still producing an desirable

amount of profits some are not. Therefore companies are shutting down these stores in

order to upgrade their existing stores. Companies in this industry are establishing on

average 40 to 50 stores per year, closing down not so profitable stores has been a huge

factor in minimizing costs. In this industry, companies must focus on economies of scale,

lower distribution and input costs, and maintaining an appropriate tight cost control

system to successfully achieve cost leadership.

32

Store Openings

01020304050607080

2002 2003 2004 2005 2006

Years

Num

ber

of S

tore

sDick's Sporting GoodsCabela's Inc.Big Five Sporting GoodsHibbit's Inc.

Conclusion

Overall, the sporting good retail industry requires a mixture of a cost leadership

principle with an emphasis on differentiation of product. In order to maintain a

competitive firm, companies have to take necessary actions to avoid an eventual exit

from the market. Through consistent addition to the value chain, firms can gain their own

competitive advantage in the market and contribute to the firms overall productivity, both

to profit and popularity. Thus, maintaining economies of scale strategy, controlling costs,

providing a superior brand, researching market trends and potential acquisitions, and

implementing cost systems that address inventory are all components designated in

controlling an elite sport retail store. Without key factors, interruptions in the process

occur, leaving firms without a much-needed competitive advantage.

33

Firm Competitive Advantage Analysis

Dick’s Sporting Goods is in an industry of high competition. Therefore, their main

business strategies to stay competitive have been unique. This lead Dick’s to adapt the

“store-within –a-store” feature which consists of larger format stores containing five

specialty stores within the store. They have achieved cost leadership by using strategies

such as economies of scale and scope, and lowering input costs. They have also

differentiated themselves by supplying great customer service and investing in brand

image. So really they mixed strategies from both a cost leadership and differentiation

strategies to become competitive advantage over the industry. Using these strategies

their profits have increased during the past five years.

Economies of Scale and Scope

Dick’s Sporting Goods have been expanding all over the United States, now with

stores in 34 states. They went from 22 stores in 1994 to 322 stores today and recently

this year acquiring Golf Galaxy and its 65 stores on February 13, 2007. They have

become America’s largest full-line sporting goods company. Dick’s Sporting Goods direct

competitors are much smaller with fewer stores. Dick’s Sporting Goods competitors

consist of Cabelas, Big 5 Sporting Goods, Hibbett Sporting Goods, and other smaller

privately owned stores. Wal-Mart could be a competitor, but we don’t use them as

competitors because their focus on sporting goods is not very large. Dick’s main concern

is their direct competitors that concentrate on sporting goods. Dick’s Sporting Goods

main advantage is that they have over 1,200 vendors they use. Disruption to supplies

could lead to losses in this retail industry, so Dick’s Sporting Goods has all these vendors

to prevent losses and to make sure they are getting the best prices for their merchandise.

Having all these vendors has enabled Dick’s Sporting Goods to acquire high quality

brands at discount prices to stay competitive. Dicks Sporting Goods does not have one

supplier that provides more than 15% of their inventory.

34

Lowering Input Costs

Dick’s Sporting Goods increase in productivity has allowed them to purchase large

masses of products from their suppliers. This can result in overcrowding merchandise in

their stores which can cause problems and would lead to discounts to customer to avoid

over crowdedness. Therefore, Dick’s Sporting Goods has two large distribution centers.

“We rely on two distribution centers along with a smaller return facility.” (Dick’s 2006

10K) They operate a 601,000 square foot and 725,000 square foot center in

Pennsylvania and in Indiana. Having these distribution centers allows Dick’s to reduce

individual store inventory investment, have a more timely replenishment of store

inventory needs, and reduce transportation costs. (Dick’s 2007 10-K) The sporting goods

retail industry is very seasonal and Dick’s Sporting Goods maintains inventory available

through their distribution centers. Along having distribution centers to minimize costs,

Dick’s has also incorporated a operating system that allows them to replenish their

inventory to maximize their productivity. By having this efficient operating system

enables Dick Sporting Goods to allocate their products more effectively resulting in an

increase their profit margins and reducing expenses on their inventory.

Customer Service

Dick’s Sporting Goods is a sporting goods store that invests money on hiring the

perfect candidates that know their sports to take care of their customers. “We were the

first full-line sporting goods retailer to have active members of the Professional Golfers’

Association working in our stores, and as of February 3, 2007 employed 279 PGA

professionals in our golf departments.” (Dicks 2006 10K) They have also hired bike

technicians to sale their bikes and service them, as well. They have professional fitness

trainers to sell their fitness equipment and inform the customers with the right

information. So customers that shop at Dick’s Sporting Goods are aware of the expertise

and that’s why they shop there.

35

Investment in Brand Image

In order to maintain the loyal customers in their stores, Dick’s has invested on

recognized brands such as Nike, Adidas, Under Armour, and Callaway. They have also

invested on their on brands such as Walter Hagan and Ativa to maintain the loyal ones

and attract new ones. Sports fans usually know what brands they like they stick to them.

Dick’s Sporting Goods is also advertising fan Friday’s to attract the sport’s fan to wear

their favorite teams on jerseys. This simply works for advertisement and the people that

don’t have anything to wear feel the desire to go buy their favorite jerseys.

In order for Dick’s Sporting Goods to stay on the competitive advantage they must

keep innovation with their brand image and quality. Great customer service will

encourage customers to keep shopping and to bring new customers, as well. Dick’s

Sporting goods can not just be differentiated though, they must be aware of the cost

leadership strategies to stay competitive.

Into the Future

Dick’s Sporting Goods is always on the verge of expansion and growth. They

recently acquired Golf Galaxy, which operated 65 stores in 24 states. Dick’s Sporting

Goods went from 22 stores in 1994 to 322 stores in 2007. The sporting retail industry is

steadily growing, but Dick’s Sporting Goods growth has been really increasing fast over

the past years. They hope to keep growing over the years to come. Dick’s Sporting

Goods really invests money on studying where they want to open new stores. They are

very careful on choosing their sites and locations according to the market and availability.

“New stores in new markets, where we are less familiar with the target customer and less

well-known, may face different or additional risks and increased costs compared to stores

operated in existing markets, or new stores in existing markets.” (Dick’s 2007 10K)

Being cautious and aware of the competition has helped them be successful in opening

new store that will stay open.

36

Accounting Analysis

The accounting analysis is a tool used to analyze the success of a certain firm

within the market. The analysis uses financial statements in order to have a better

understanding of how well a business is performing and what its future projection looks

like. There is room within accounting systems for managers to influence financial

statement data, making it important for the analysis to understand this and determine

what a manager “used to signal their proprietary information or what is merely disguised

reality” (Palepu and Healy).

Within the accounting analysis consists of 6 steps used to evaluate certain aspects

of the company’s financial statements. These 6 steps include: identify key accounting

polices, assess accounting flexibility, evaluate actual accounting strategy, evaluate the

quality of disclosure, identify potential red flags, and undo accounting distortions.

Identifying key accounting policies is a way to compare its key success factors and its

potential risk. Next a companies accounting flexibility must be measured. Since not all

companies have the same amount of flexibility due to constraints from accounting

standards, we have to keep this in mind when analyzing a company. If a certain

company has accounting flexibility it can use this to either provide information about its

economic situation or hide its true performance, so an evaluation of accounting strategy

must be performed. It is also important for an analyst to evaluate the quality of

disclosure, because even though managers are required to provide a minimum amount of

disclosure, they do have a considerable amount of say in what is released.

One of the most important steps the analyst will make is identifying possible red

flags that could point to questionable accounting. Finally the analyst will undo accounting

distortions if one feels that the company’s financial statements are misleading or

inaccurate. Using all of these steps will help create a successful accounting analysis.

37

Key Accounting Policies

In the accounting analysis it is important to “identify and evaluate the policies and

the estimates the firm uses to measure its critical factors and risks” (Palepu and Healy).

This step is directly influenced by key success factors and risks within the market. As

mentioned in the Five Forces Model Dick’s Sporting Goods key success factors are

economies of scale, tight cost control, and investment in brand image. Due to the

competitive nature of the sporting goods retail industry cost control becomes the most

significant factor. Brand image is a way for companies to invest in marketing the

company’s name; Dick’s utilizes an approach of big brand names for a competitive price.

Continuous Growth

The highly cost competitive market that is the sporting goods retail industry,

creates an atmosphere where companies must continue to grow and expand in order to

stay competitive in the industry. The chart below shows the comparable store net sale

increase percentage and the number of new stores Dick’s Sporting Goods has opened in

the last 5 years.

Sales Growth 2002 2003 2004 2005 2006Comparable store net sales increase 5.10% 2.10% 2.60% 2.60% 6.00%Number of Stores 141 163 234 255 294

*Calculated using Dick’s 2006 10-K

The chart show that not only is Dick’s Sporting Goods growing its sells, it has also

been expanding its store base over the last several years. As of August 4, 2007 Dick’s

Sporting Goods owns and operates 315 stores across 34 states. They also own Golf

Galaxy, a multi-channel golf specialty retailer, with 77 stores in 29 states (Dick’s 2006 10-

K). This merger took place in February 2007, and shows that Dick’s Sporting Goods is

wanting to expand its company into other parts of the industry. Gaylan’s Trading Inc.

was another merger that took place for the company in 2004. With these mergers and

the expansion of stores Dick’s Sporting Goods has significantly increased its sales growth

38

and net assets. However, because the opening of new stores is dependent on several

different factors there is a certain amount of risk associated with the opening of new

stores. This is something to watch for when dealing with Dick’s Sporting Goods, because

the industry is so seasonal.

Economies of Scale

Dick’s Sporting Goods use a system of store clustering to take advantage of

economies of scale in “advertising, promotion, distribution, and supervisory costs. We

seek to locate stores within separate trade areas within each metropolitan area, in order

to establish long-term market penetration”(Dick’s 2006 10-K). This clustering can be very

effective for their marketing and advertising program, in which they can “employ their

advertising strategy using a cost effective basis through the use of newspapers and local

and national television and radio advertising” (Dick’s 2006 10-K).

Their merchandise planning and allocation systems optimizes distribution of most

products to the stores by taking a combination of historical sales data and forecasted

data at an individual store and item level (Dick’s 2006 10-K). The company believes that

this helps with markdowns taken on merchandise and improves sales on these products.

Dick’s has a couple of distribution centers, which after a purchase is made it is sent

directly from the vendor to the distribution center, where it is processed and then

shipped to the store. All purchases made from vendors are done on a short-term

purchase order basis.

Operating and Capital Leases

Within the retail industry it is common for most companies to use operating leases

with their stores. This has a major benefit for a company since operating leases are not

recorded on the balance sheet, making shareholders believe that they are more cost

efficient. Dick’s Sporting Goods leases all of its stores for lease terms for 10-25 years

with multiple 5 year renewal options and which expire at various dates all the way to

2027 (Dick’s 2006 10-K). Dick’s Sporting Goods does give information in their 10-K about

amounts owed for both on and off balance sheet obligations including operating leases.

39

Operating leases total up to be 2.8 billion dollars due through 2011, this is a very

significant number. Operating leases are by far the largest owed contractual obligation,

with capital leases only amounting to 7.8 million in comparison. Two of Dick’s capital

lease agreements are from the estate of a former stockholder that mature in April 2021.

They also have a capital lease on a store with a fixed interest rate of 10.6% that matures

in 2024 (Dick’s 2006 10-K). It is apparent that Dick’s prefers to use operating leases

over capital leases, which is generally the case in the retail industry.

Goodwill

Dick’s Sporting Goods did record “$156.6 million of goodwill as the excess of the

purchase price of $369.6 million over the fair value of the net amounts assigned to assets

acquired and liabilities assumed” (Dick’s 2006 10-K). This means that sometimes

managers can over estimate the value of a company that is purchased, such as Gaylan’s

and Golf Galaxy, and goodwill is used to balance the balance sheet. Dick’s evaluation of

goodwill for “impairment requires judgments and financial estimates in determining the

fair value of the reporting unit”(Dick’s 2006 10-K). This means that they continually

reevaluate their goodwill to accurately report the difference between the purchase of

Gaylan’s and Golf Galaxy, and this is what these companies are really actually worth.

Conclusion

The key accounting policies a company uses are directly linked to the key success

factors and risks within a market. If an analyst sees that the company’s accounting

policies do not match its success factors then the analyst should be aware of potential

red flags within that companies financials. With Dick’s Sporting Goods we feel like there

is a good amount of information disclosure when dealing with their financials, and they

provided a decent amount of information regarding mergers and their leasing policy.

40

Areas of Accounting Flexibility

The Generally Accepted Accounting Principles (GAAP) is accounting guidelines for

presenting and reporting financial statements. Firms report financial information so that

investors can make informed decisions on future investments. GAAP allows flexible

methods for reporting data that could lead to distortion in the financial data and could

mislead investors, as well. Information reported should be consistent to improve the

quality and credibility of the financial statements. Balance sheets and income statements

have high amount of flexibility that can be manipulated by top management.

Operating vs. Capital Leases

Reporting operating vs. capital leases in one way flexible accounting helps

managers. In the operating lease, “the lessor transfers only the right to use the property

to the lessee (www.cr-ny.com).” The lessee is only renting the property and has no right

of ownership; therefore the lease can be booked as an expense in the income statement.

The booking of this expense would have no effect on the balance sheet and would be

considered an off balance sheet asset. Dick’s Sporting Goods and most of its competitors

have operating leases for most of their stores. Dicks Sporting Goods operating leases

range from 10-25 years. Dicks Sporting Goods only has two buildings that they have

capital leases on. One of these capital leases is the year 2021 and the other is till 2024.

These operating leases are expenses that do not show up on the balance sheets, which

cause the company’s assets and or liabilities to be understated. So with understated

expenses, the company is going to show overstated net income. The overstated of

owners equity and net income makes the company look more profitable and therefore

investors are more willing to invest.

On the other hand, capital leases are treated as paying interest on debt. When

you have capital leases you assume the risk of ownership. Capital leases do affect the

balance sheet, unlike operating leases. “If it is a capital lease, the lessor records the

present value of future cash flows as revenue and recognizes expenses. The lease

receivable is also shown as an asset on the balance sheet, and interest revenue is

recognized over the term of the lease, as paid (www.cr-ny.com).” Capital leases can be

41

listed as assets or liabilities on the financial statements. They show up as assets under

plant, property, and equipment. They can also show up liabilities under lease payments.

Companies use capital leases to benefit some of the tax shelters, depreciation, and

reduction in interest expenses.

Operating and Capital leases can be used by managers in several different ways.

The flexibility of GAAP to allow these reporting methods allows managers to cover up

some of the true numbers of the companies. The methods managers use does not mean

its wrong, but can compensate them by making their company seem more prosperous

and meet certain covenants.

GAAP also allows flexibility in the reporting of goodwill and intangible assets.

“Goodwill and other finite-lived intangible assets are tested for impairment on an annual

basis (Dick’s 2006 10K).” Valuation of goodwill and intangible assets requires estimation

from managers which could have some estimation error. These estimations could lead to

some degree of potential “red flags”. When the carrying value of the assets is greater

than the fair value of the assets, then their assets are going to be impaired. Dick’s

Sporting Goods Company reports in their 10K that they determine the fair value by using

independent appraisals in order to come out with the best estimate.

Actual Accounting Strategy

Financial reporting can have either high or low disclosure. High disclosure is when

a company gives a wide range of information for the public as well as the investor. The

company does not try to hide anything. The company discusses all items in great detail.

Low disclosure is the reporting of items in less detail only to satisfy the GAAP. Each

company has the ability to report their information in a conservative or aggressive basis.

Most companies in the sporting goods industry show a mixture of both conservative and

aggressive along with Dick’s Sporting Goods.

Most of the sporting goods industry report operating leases instead of capital

leases in order to hide the true performance of company. This is one strategy that Dick’s

Sporting Goods uses reporting their data. In 2006 they reported $7.8 million in capital

leases and $205.8 million of operating leases. As mentioned previously operating leases

42

are a significant amount of contractual obligations in comparison to capital leases. Dick’s

favors the use of operating leases over capital leases, which is easily seen through their

building construction method. Reporting of these financial data is considered to be an

aggressive accounting strategy. These accounting objectives are what managers choose

to do to best fit the company as well as to earn incentives.

Dick’s Sporting Goods also allow customers to return their merchandise if it is

defective. Dick’s also gives credit or markdowns on merchandise that is purchased and

later customers find same merchandise at lower prize within a time period. They offer

allowances for customer and suppliers to maintain a positive relationship. The recording

of these reimbursements and markdowns are considered to be a conservative strategy

along the industry’s disclosure in their 10K’s.

All companies in the sporting goods industry also offer define benefit plans. These

define benefit plans have several assumptions they have to make to get a well deserve

rate of return along with well estimated discount rate. Dick’s Sporting Goods offers

employee stock options as well as a retirement savings plan or 401(K). Employees must

have completed 1 year of employment and have reached age of 21 years or older to

receive this benefit. The companies make several changes to the rates they choose

constantly on their reporting. These changes have not seemed to have made an impact

on the numbers though. The numbers have stayed consistently through past years. The

reporting of these expenses is considered to be relatively conservative in the industry. All

of these different ways of reporting are acceptable by GAAP. The accounting strategies