Diapositiva 1s1.q4cdn.com/793210788/files/doc_downloads/SQMCorporate...Sodium nitrate + Potassium...

25

June 2013

Transcript of Diapositiva 1s1.q4cdn.com/793210788/files/doc_downloads/SQMCorporate...Sodium nitrate + Potassium...

June 2013

Statements in this presentation concerning the Company’s business outlook or future economic performances, anticipated profitability, revenues, expenses, or other financial items, anticipated cost synergies and product or service line growth, together with other statements that are not historical facts, are “forward-looking statements” as that term is defined under Federal Securities Laws.

Any forward-looking statements are estimates, reflecting the best judgment of SQM based on currently available information and involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those stated in such statements.

Risks, uncertainties, and factors that could affect the accuracy of such forward-looking statements are identified in the public filing made with the Securities and Exchange Commission, and forward-looking statements should be considered in light of those factors.

2

Important Notice

Overview

Fertilizers

Specialty Chemicals

Financial Information

3

Agenda

Photo: Evaporation Pond - Salar de Atacama, from which we produce potassium & lithium products

4

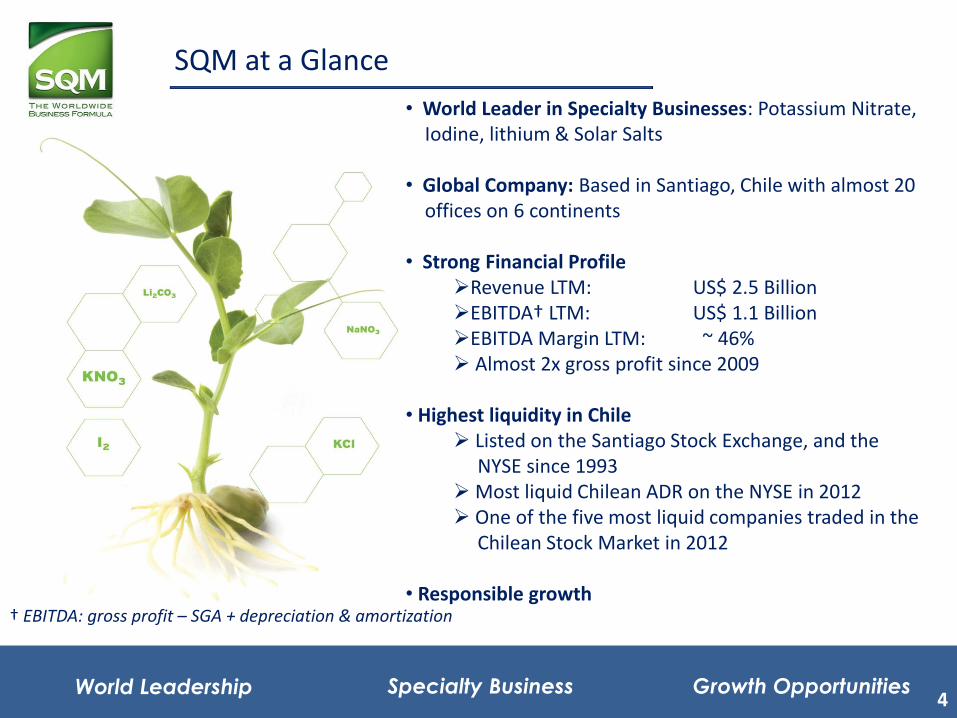

SQM at a Glance • World Leader in Specialty Businesses: Potassium Nitrate, Iodine, lithium & Solar Salts • Global Company: Based in Santiago, Chile with almost 20 offices on 6 continents • Strong Financial Profile

Revenue LTM: US$ 2.5 Billion EBITDA† LTM: US$ 1.1 Billion EBITDA Margin LTM: ~ 46% Almost 2x gross profit since 2009

• Highest liquidity in Chile Listed on the Santiago Stock Exchange, and the NYSE since 1993 Most liquid Chilean ADR on the NYSE in 2012 One of the five most liquid companies traded in the Chilean Stock Market in 2012

• Responsible growth

Specialty Business World Leadership Growth Opportunities 4

† EBITDA: gross profit – SGA + depreciation & amortization

5

SQM at a Glance

Specialty Business World Leadership Growth Opportunities

SQM: Proud to be the world’s largest producer of lithium, iodine, potassium nitrate and solar salts

Fertilizers Specialty Chemicals

Potassium

20%

Specialty Plant Nutrients

24%

Iodine

36%

Lithium

9%

Industrial Chemicals

9%

5

% of Contribution to SQM Consolidated Gross Profit for the first quarter of 2013

6

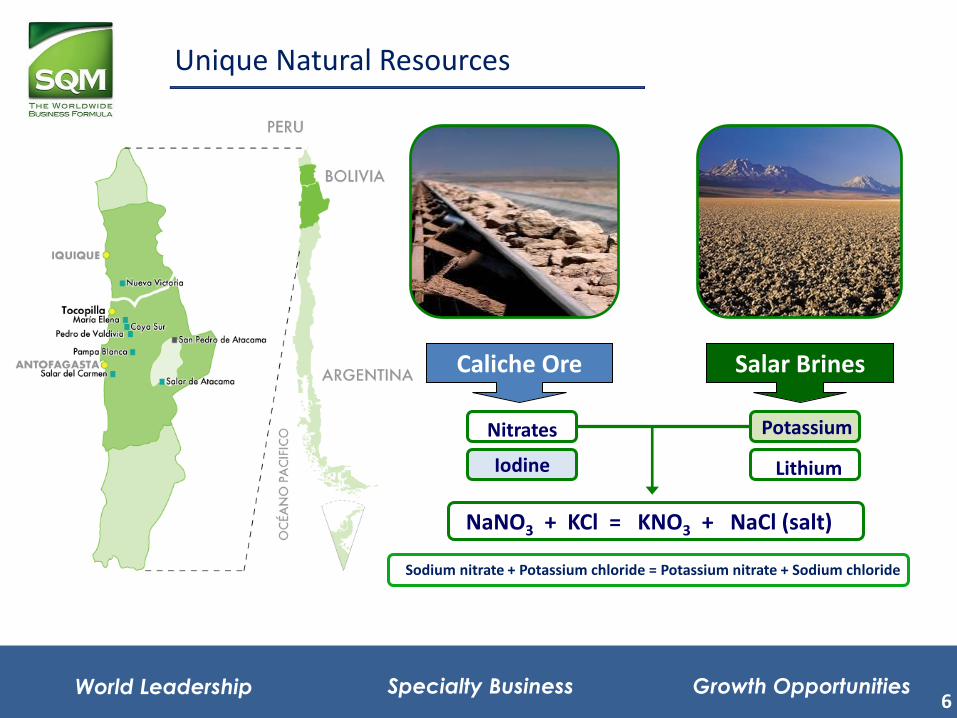

Unique Natural Resources

Caliche Ore Salar Brines

Nitrates

Iodine Iodine

Potassium

Lithium

Potassium

NaNO3 + KCl = KNO3 + NaCl (salt)

Sodium nitrate + Potassium chloride = Potassium nitrate + Sodium chloride

Specialty Business World Leadership Growth Opportunities 6

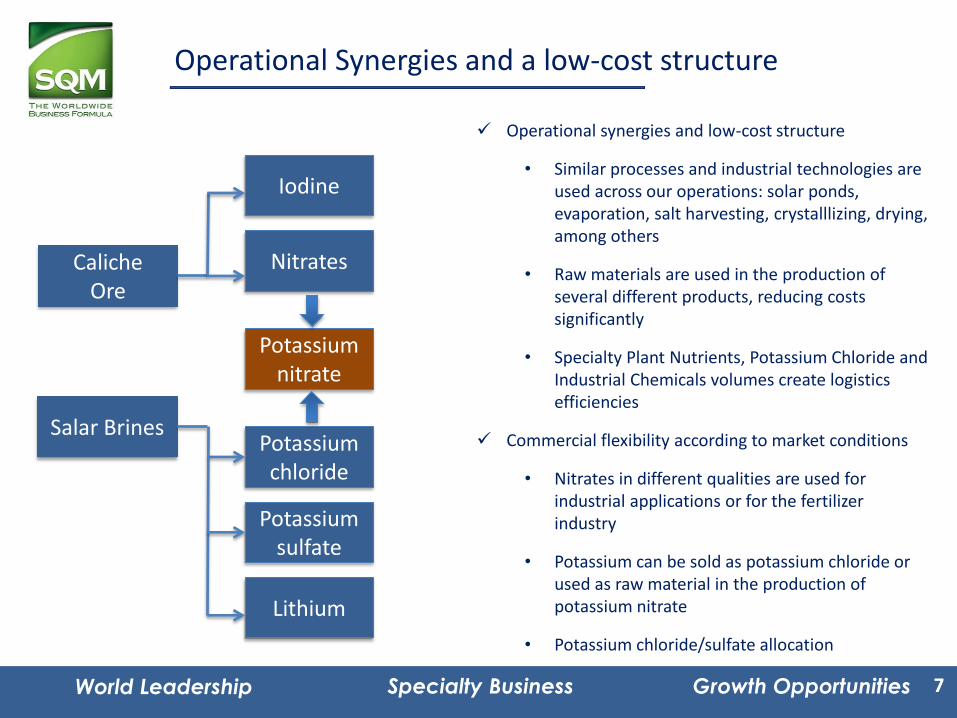

Operational Synergies and a low-cost structure

Caliche Ore

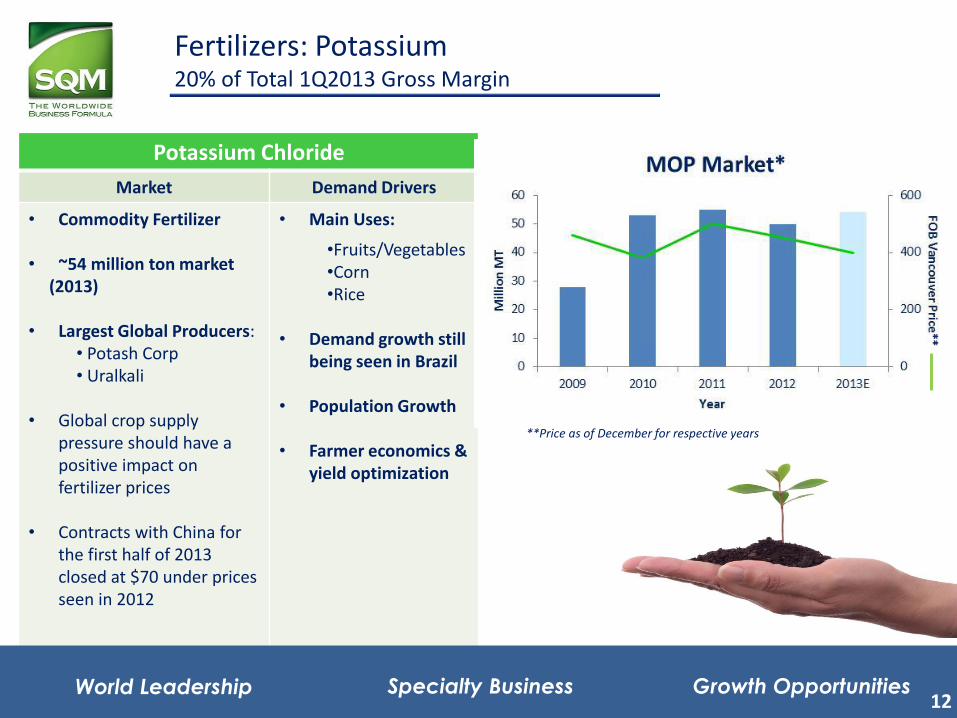

Salar Brines

Operational synergies and low-cost structure

• Similar processes and industrial technologies are used across our operations: solar ponds, evaporation, salt harvesting, crystalllizing, drying, among others

• Raw materials are used in the production of several different products, reducing costs significantly

• Specialty Plant Nutrients, Potassium Chloride and Industrial Chemicals volumes create logistics efficiencies

Commercial flexibility according to market conditions

• Nitrates in different qualities are used for industrial applications or for the fertilizer industry

• Potassium can be sold as potassium chloride or used as raw material in the production of potassium nitrate

• Potassium chloride/sulfate allocation

Iodine

Nitrates

Potassium chloride

Potassium sulfate

Lithium

Potassium nitrate

Specialty Business World Leadership Growth Opportunities 7

8

Overview

Fertilizers

Specialty Chemicals

Financial Information

Agenda

Photo: Potassium Nitrate Plant in Coya Sur

9

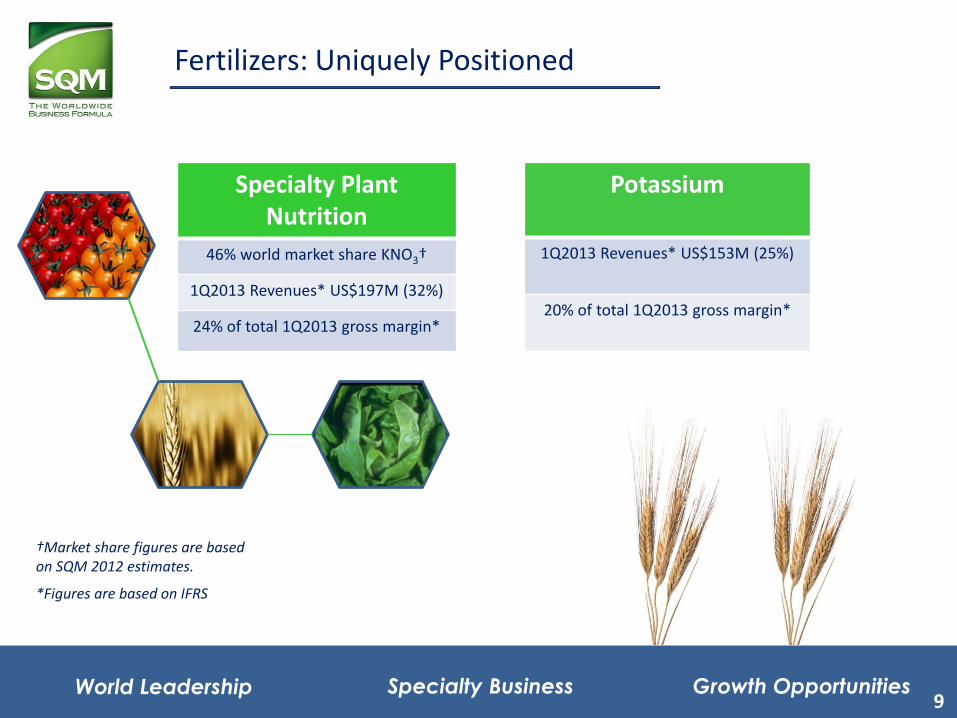

†Market share figures are based on SQM 2012 estimates.

*Figures are based on IFRS

Specialty Business World Leadership Growth Opportunities

Fertilizers: Uniquely Positioned

9

Specialty Plant Nutrition

46% world market share KNO3†

1Q2013 Revenues* US$197M (32%)

24% of total 1Q2013 gross margin*

Potassium

1Q2013 Revenues* US$153M (25%)

20% of total 1Q2013 gross margin*

10

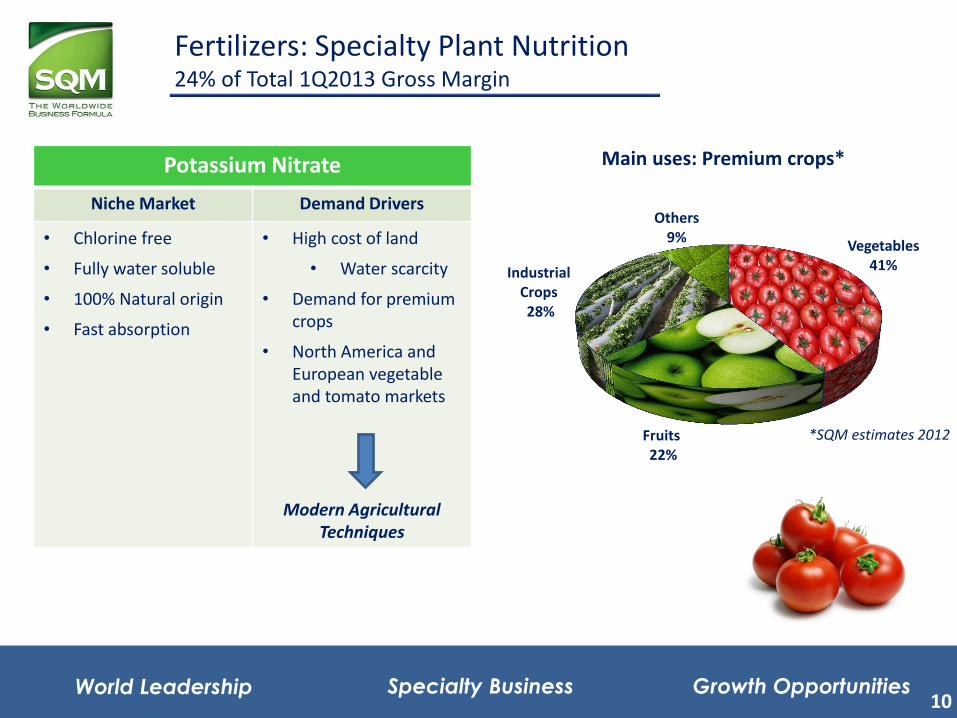

Potassium Nitrate

Niche Market Demand Drivers

• Chlorine free

• Fully water soluble

• 100% Natural origin

• Fast absorption

• High cost of land

• Water scarcity

• Demand for premium crops

• North America and European vegetable and tomato markets

Modern Agricultural Techniques

Fertilizers: Specialty Plant Nutrition 24% of Total 1Q2013 Gross Margin

Vegetables 41%

Fruits 22%

Industrial Crops 28%

Others 9%

Main uses: Premium crops*

*SQM estimates 2012

Specialty Business World Leadership Growth Opportunities 10

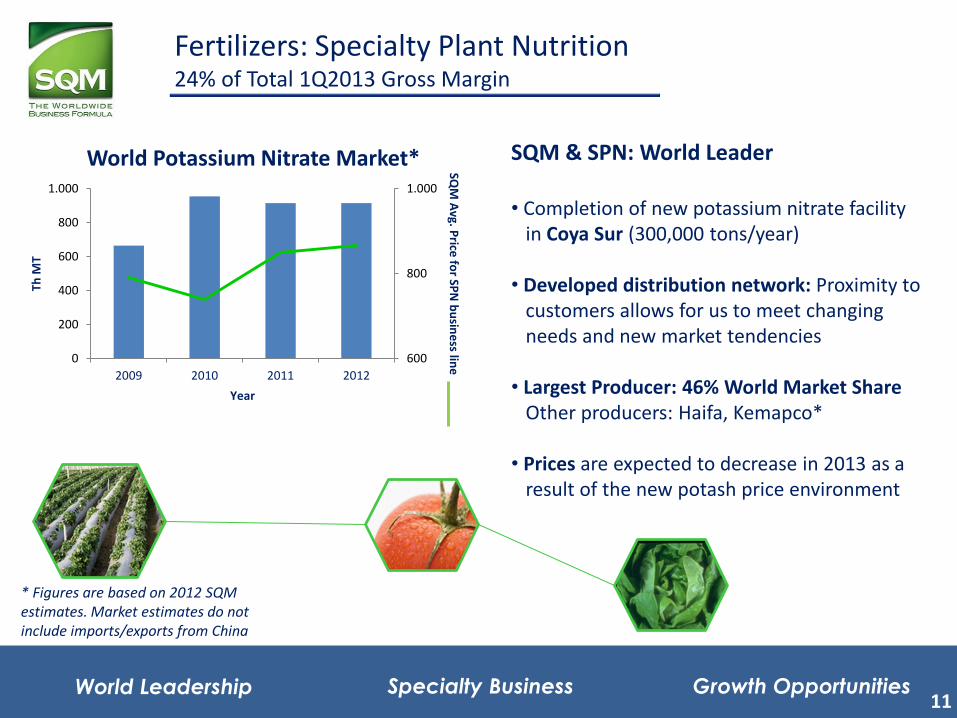

11

Fertilizers: Specialty Plant Nutrition 24% of Total 1Q2013 Gross Margin

SQM & SPN: World Leader • Completion of new potassium nitrate facility in Coya Sur (300,000 tons/year) • Developed distribution network: Proximity to customers allows for us to meet changing needs and new market tendencies • Largest Producer: 46% World Market Share Other producers: Haifa, Kemapco* • Prices are expected to decrease in 2013 as a result of the new potash price environment

Specialty Business World Leadership Growth Opportunities 11

* Figures are based on 2012 SQM estimates. Market estimates do not include imports/exports from China

600

800

1.000

0

200

400

600

800

1.000

2009 2010 2011 2012

SQ

M A

vg. Price

for SP

N b

usin

ess lin

e

Th M

T

Year

World Potassium Nitrate Market*

12

Fertilizers: Potassium 20% of Total 1Q2013 Gross Margin

Potassium Chloride

Market Demand Drivers

• Commodity Fertilizer • ~54 million ton market (2013) • Largest Global Producers:

• Potash Corp • Uralkali

• Global crop supply pressure should have a positive impact on fertilizer prices

• Contracts with China for

the first half of 2013 closed at $70 under prices seen in 2012

• Main Uses:

•Fruits/Vegetables •Corn •Rice

• Demand growth still being seen in Brazil

• Population Growth • Farmer economics &

yield optimization

Specialty Business World Leadership Growth Opportunities

*SQM estimates **Price as of December for respective years

12

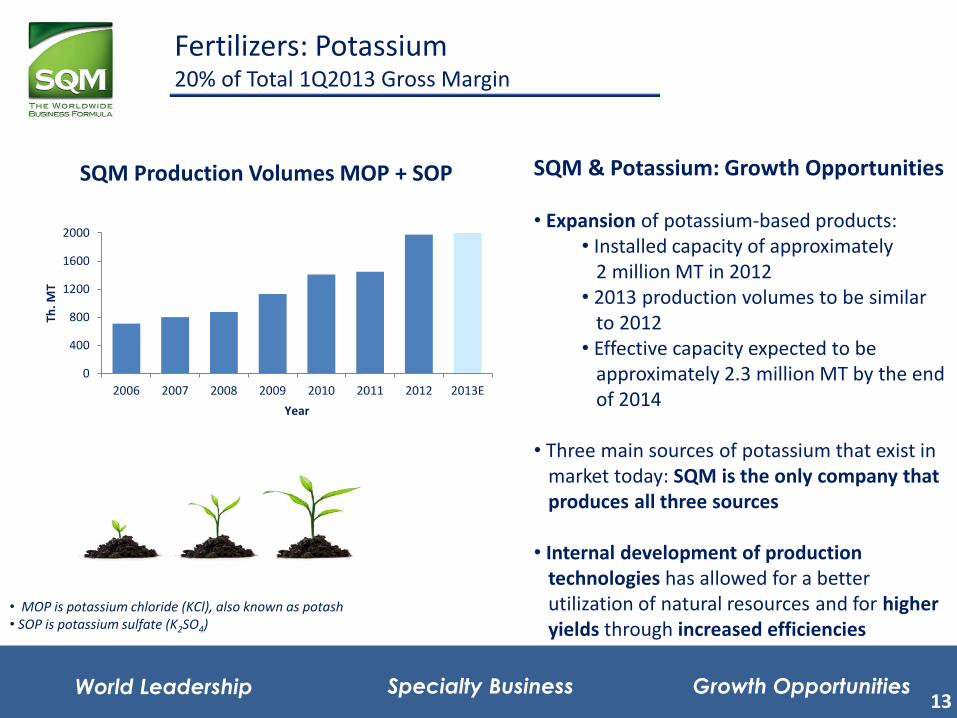

13

SQM & Potassium: Growth Opportunities • Expansion of potassium-based products:

• Installed capacity of approximately 2 million MT in 2012 • 2013 production volumes to be similar to 2012 • Effective capacity expected to be approximately 2.3 million MT by the end of 2014

• Three main sources of potassium that exist in market today: SQM is the only company that produces all three sources • Internal development of production technologies has allowed for a better utilization of natural resources and for higher yields through increased efficiencies

Fertilizers: Potassium 20% of Total 1Q2013 Gross Margin

• MOP is potassium chloride (KCl), also known as potash • SOP is potassium sulfate (K2SO4)

Specialty Business World Leadership Growth Opportunities 13

0

400

800

1200

1600

2000

2006 2007 2008 2009 2010 2011 2012 2013E

Th. M

T

Year

SQM Production Volumes MOP + SOP

14

Overview

Fertilizers

Specialty Chemicals

Financial Information

Agenda

Photo: Salar de Atacama

15

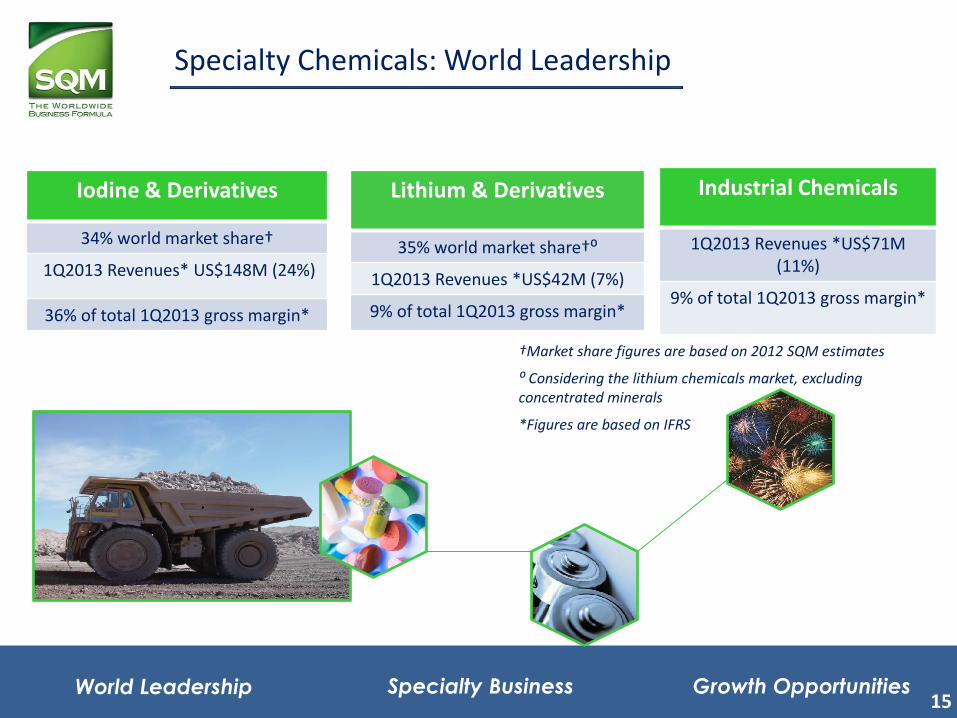

Specialty Chemicals: World Leadership

†Market share figures are based on 2012 SQM estimates

⁰ Considering the lithium chemicals market, excluding concentrated minerals

*Figures are based on IFRS

Specialty Business World Leadership Growth Opportunities 15

Iodine & Derivatives

34% world market share†

1Q2013 Revenues* US$148M (24%)

36% of total 1Q2013 gross margin*

Lithium & Derivatives

35% world market share†⁰

1Q2013 Revenues *US$42M (7%)

9% of total 1Q2013 gross margin*

Industrial Chemicals

1Q2013 Revenues *US$71M (11%)

9% of total 1Q2013 gross margin*

16

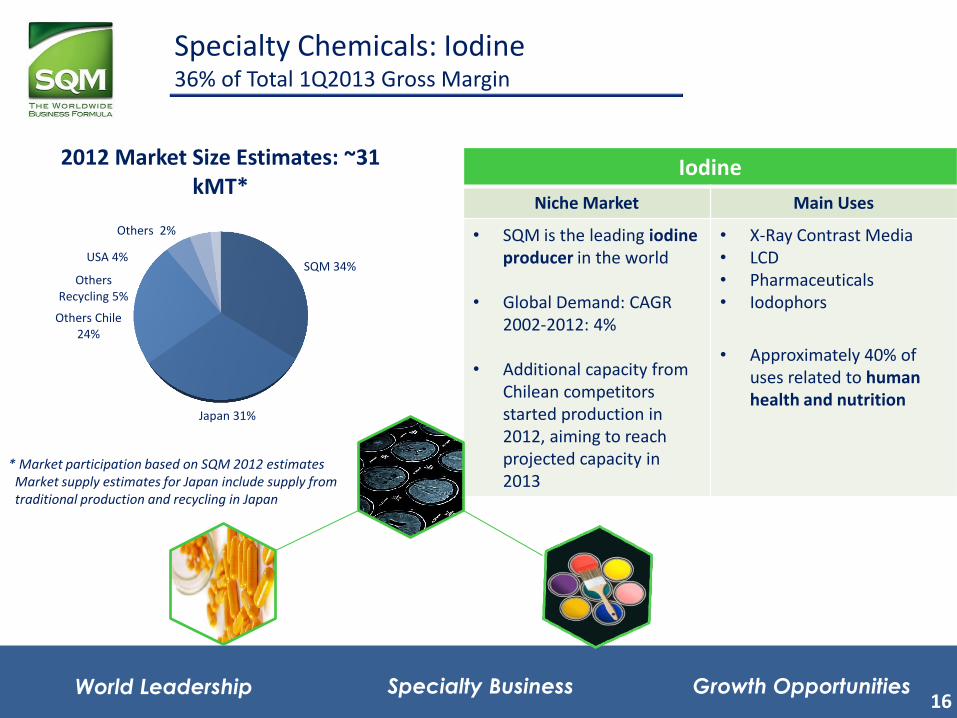

Specialty Chemicals: Iodine 36% of Total 1Q2013 Gross Margin

* Market participation based on SQM 2012 estimates Market supply estimates for Japan include supply from traditional production and recycling in Japan

Iodine

Niche Market Main Uses

• SQM is the leading iodine producer in the world

• Global Demand: CAGR

2002-2012: 4% • Additional capacity from

Chilean competitors started production in 2012, aiming to reach projected capacity in 2013

• X-Ray Contrast Media • LCD • Pharmaceuticals • Iodophors

• Approximately 40% of uses related to human health and nutrition

Specialty Business World Leadership Growth Opportunities 16

SQM 34%

Japan 31%

Others Chile 24%

Others Recycling 5%

USA 4%

Others 2%

2012 Market Size Estimates: ~31 kMT*

17

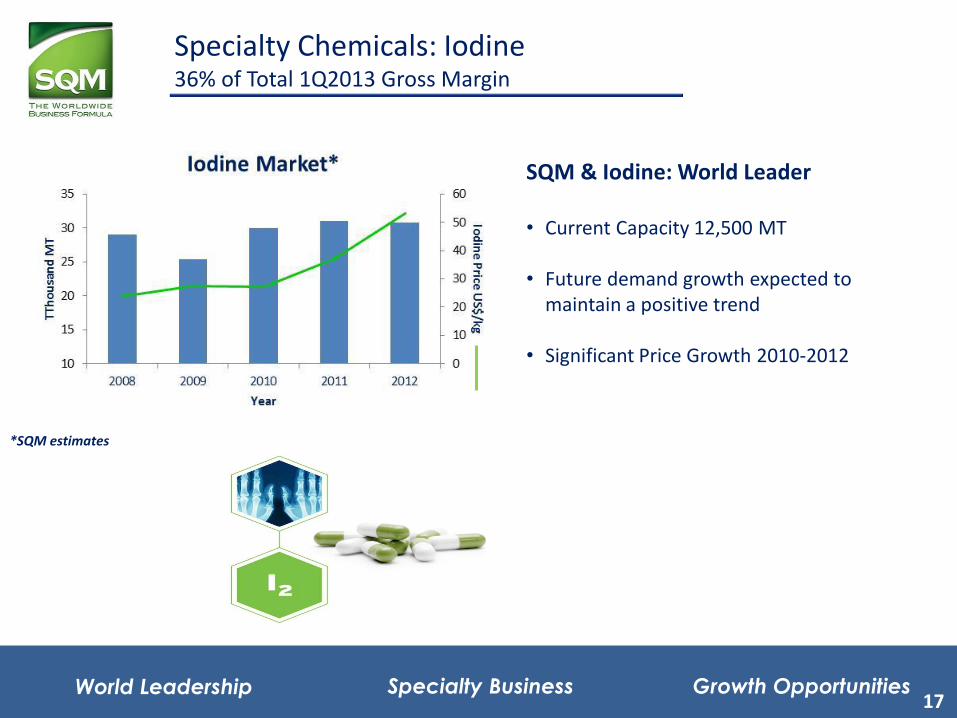

Specialty Chemicals: Iodine 36% of Total 1Q2013 Gross Margin

SQM & Iodine: World Leader • Current Capacity 12,500 MT • Future demand growth expected to

maintain a positive trend • Significant Price Growth 2010-2012

Specialty Business World Leadership Growth Opportunities

*SQM estimates

17

18

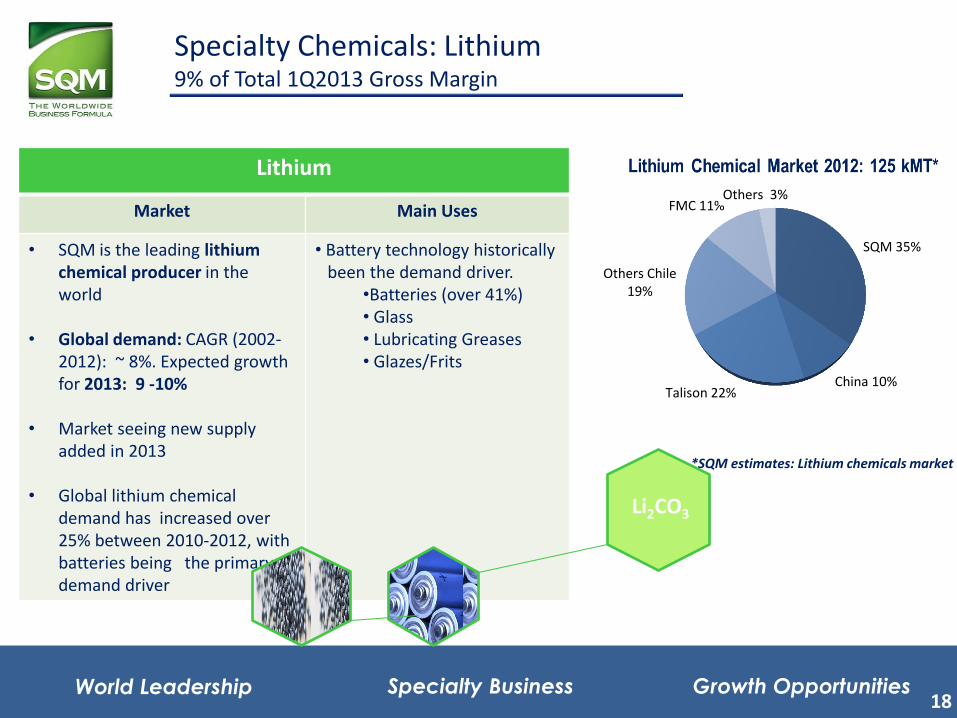

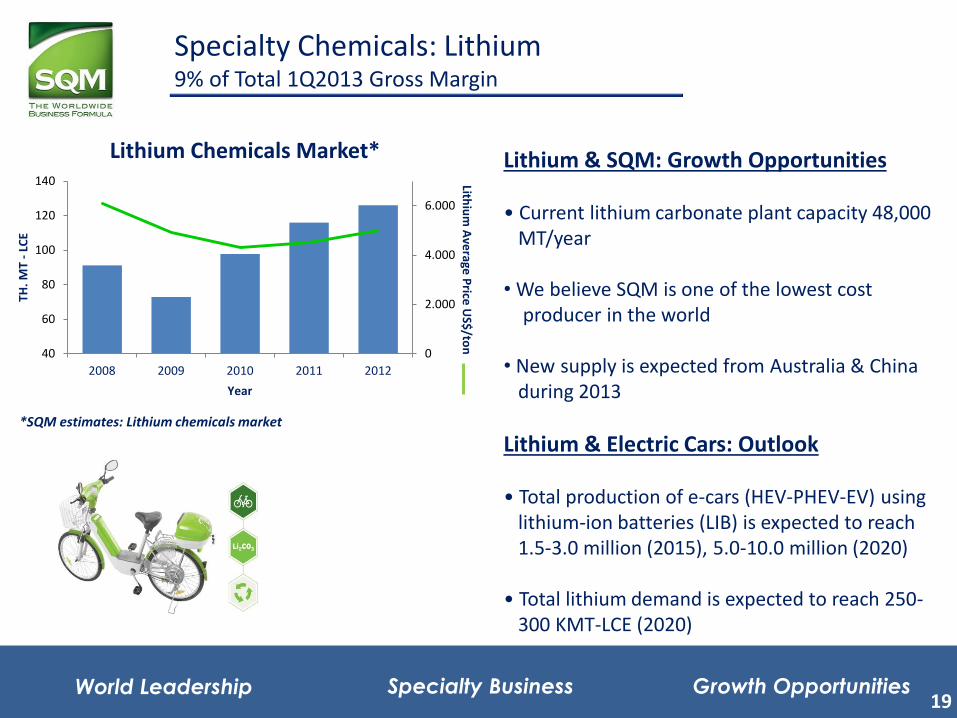

Specialty Chemicals: Lithium 9% of Total 1Q2013 Gross Margin

*SQM estimates: Lithium chemicals market

Specialty Business World Leadership Growth Opportunities

Lithium

Market Main Uses

• SQM is the leading lithium chemical producer in the world

• Global demand: CAGR (2002-

2012): ~ 8%. Expected growth for 2013: 9 -10%

• Market seeing new supply added in 2013

• Global lithium chemical

demand has increased over 25% between 2010-2012, with batteries being the primary demand driver

• Battery technology historically been the demand driver.

•Batteries (over 41%) • Glass • Lubricating Greases • Glazes/Frits

Li2CO3

18

SQM 35%

China 10% Talison 22%

Others Chile 19%

FMC 11% Others 3%

19

Lithium & SQM: Growth Opportunities • Current lithium carbonate plant capacity 48,000 MT/year • We believe SQM is one of the lowest cost producer in the world • New supply is expected from Australia & China during 2013

Lithium & Electric Cars: Outlook • Total production of e-cars (HEV-PHEV-EV) using lithium-ion batteries (LIB) is expected to reach 1.5-3.0 million (2015), 5.0-10.0 million (2020) • Total lithium demand is expected to reach 250- 300 KMT-LCE (2020)

Specialty Chemicals: Lithium 9% of Total 1Q2013 Gross Margin

*SQM estimates: Lithium chemicals market

Specialty Business World Leadership Growth Opportunities 19

0

2.000

4.000

6.000

40

60

80

100

120

140

2008 2009 2010 2011 2012

Lithiu

m A

verage

Price

US$

/ton

TH.

MT

- LC

E

Year

Lithium Chemicals Market*

20

Solar Salts: New demand for industrial nitrates for thermal energy storage in solar power plants means increasing our nitrate consumption

• Mixture of 60% sodium nitrate and 40% potassium nitrate

• Main projects: ACS Cobra-Sener, Aries, Rocketdyne, Abengoa, SAMCA, Solar Reserves

• 50 MW → ~30,000 MT of salts • 2012 solar salts are expected to reach ~ 180,000 MT . • 2013 sales expected to decrease to around

70,000 MT due to a delay of most projects until 2014 as a result of the financial situation in Europe

Specialty Chemicals: Industrial 9% of Total 1Q2013 Gross Margin

Traditional Industrial Chemical applications include: metal treatment, water treatment, pyrotechnics, explosives, glass manufacturing, among others

Specialty Business World Leadership Growth Opportunities 20

21

Overview

Fertilizers

Specialty Chemicals

Financial Information

Agenda

Photo: SQM offices in Santiago

22

1. Capacity expansion for potassium-based products in the Salar de Atacama

2. Preparing water supply for a potential iodine and nitrates expansion in first region, with increased plant efficiencies and higher quality products

3. Optimization railroad system, other projects aimed at improving yields and reducing costs

Capital Expenditure Program Approximately US$500 million for 2013

*Approximately 65% of capital expenditures will be related to expansion projects

Specialty Business World Leadership Growth Opportunities 22

23

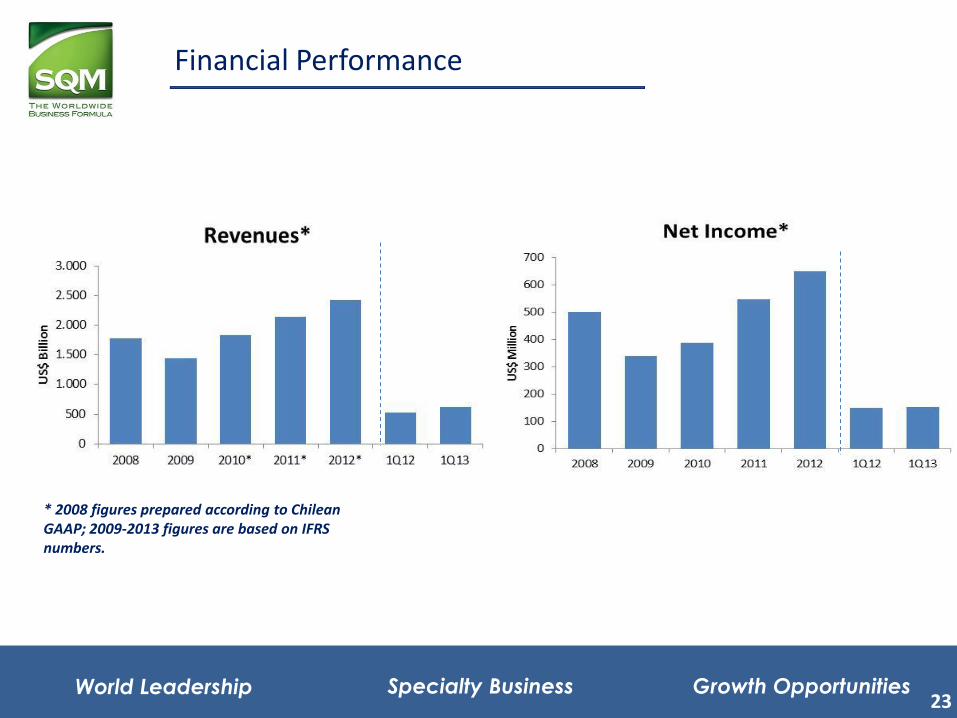

Financial Performance

* 2008 figures prepared according to Chilean GAAP; 2009-2013 figures are based on IFRS numbers.

Specialty Business World Leadership Growth Opportunities 23

24

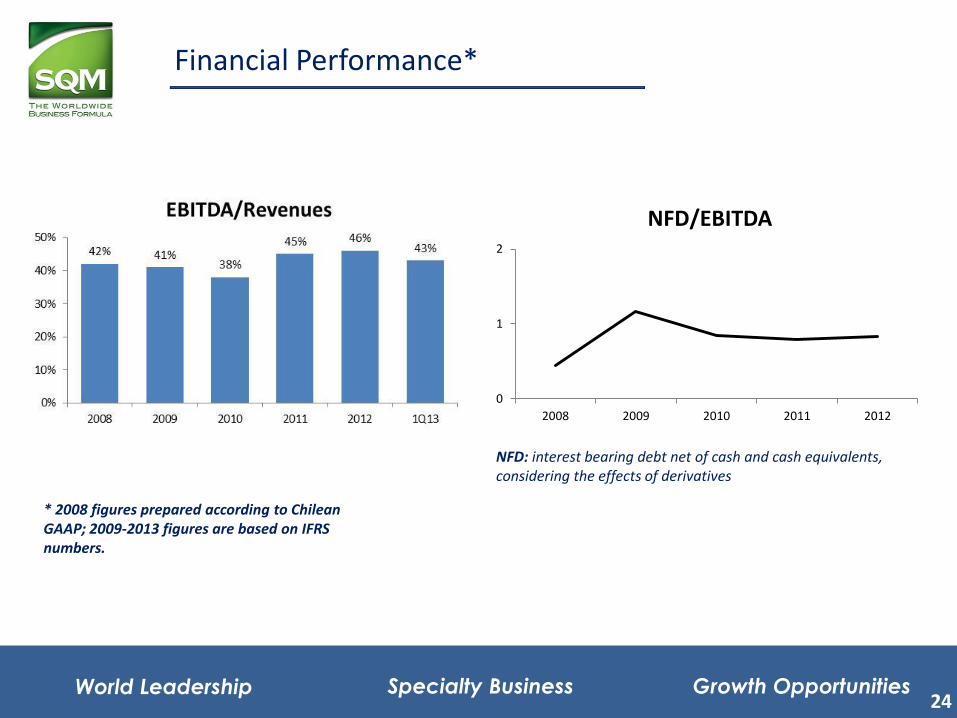

Financial Performance*

NFD: interest bearing debt net of cash and cash equivalents, considering the effects of derivatives

* 2008 figures prepared according to Chilean GAAP; 2009-2013 figures are based on IFRS numbers.

Specialty Business World Leadership Growth Opportunities 24

0

1

2

2008 2009 2010 2011 2012

NFD/EBITDA

25

Key Conclusions

Business flexibility according to market conditions

• Largest global producer, lowest cost producer, market growth.

• Specialty Plant Nutrition

• Iodine

• Lithium

• Solar Salts

• Growth opportunities and a low cost producer.

• Potassium

• Industrial Chemicals

• Solid financial position

• Focused on long-term growth

25 Specialty Business World Leadership Growth Opportunities

25