Developing Natural Gas Markets

23

DEVELOPING NATURAL GAS MARKETS Subbu Bettadapura Research Manager, Energy Practice, Frost & Sullivan October 2008

-

Upload

frost-sullivan -

Category

Business

-

view

1.865 -

download

1

Transcript of Developing Natural Gas Markets

DEVELOPING NATURAL GAS MARKETS

Subbu Bettadapura

Research Manager, Energy Practice, Frost & Sullivan

October 2008

2

Table of Contents

DEVELOPING NATURAL GAS MARKETS

Issues and Challenges

Key Drivers

Strategic Options to Develop Natural Gas Markets

Role of Regulators

1

2

3

4

3

21st Century - Age of Natural Gas

"The Asia-Pacific region is projected to become the largest consumer of oil and gas; If the 20th century was the age of oil, then the 21st century is poised to become the age of natural gas"

Chevron Asia Pacific Exploration and Production

4

1. ISSUES AND CHALLENGES

5

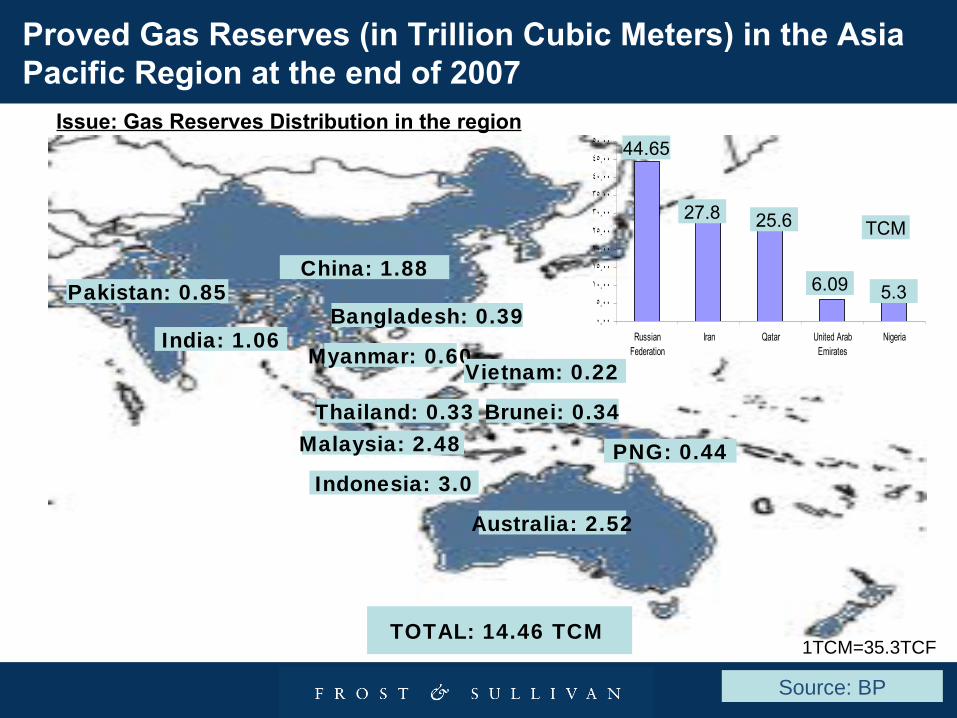

Proved Gas Reserves (in Trillion Cubic Meters) in the Asia Pacific Region at the end of 2007

TOTAL: 14.46 TCM

Source: BP

Malaysia: 2.48

Indonesia: 3.0

China: 1.88

Bangladesh: 0.39

Australia: 2.52

India: 1.06Myanmar: 0.60

Brunei: 0.34

PNG: 0.44

Pakistan: 0.85

Thailand: 0.33

Vietnam: 0.22

1TCM=35.3TCF

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

RussianFederation

Iran Qatar United ArabEmirates

Nigeria

44.65

27.8 25.6

6.09 5.3

TCM

Issue: Gas Reserves Distribution in the region

6

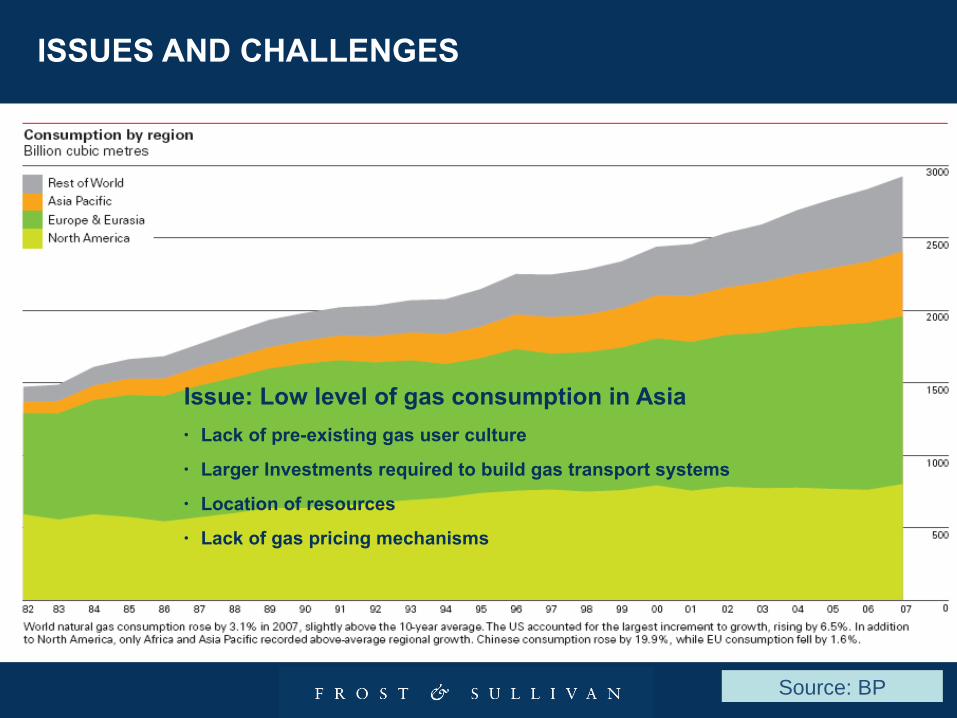

ISSUES AND CHALLENGES

Source: BP

Issue: Low level of gas consumption in Asia

• Lack of pre-existing gas user culture

• Larger Investments required to build gas transport systems

• Location of resources

• Lack of gas pricing mechanisms

7

ISSUES AND CHALLENGES (2)

Source: BP

0%

20%

40%

60%

80%

100%

Austra

lia

Bangl

ades

h

China

China

Hong

Kong

SARIn

dia

Indo

nesia

Japa

n

Mal

aysia

New Z

ealan

d

Pakist

an

Philipp

ines

Singap

ore

South

Kor

ea

Taiwan

Thaila

nd

Other

Asia

Pac

ific

Total

Asia

Pac

ific

Hydro electric

Nuclear Energy

Coal

Oil

Natural Gas

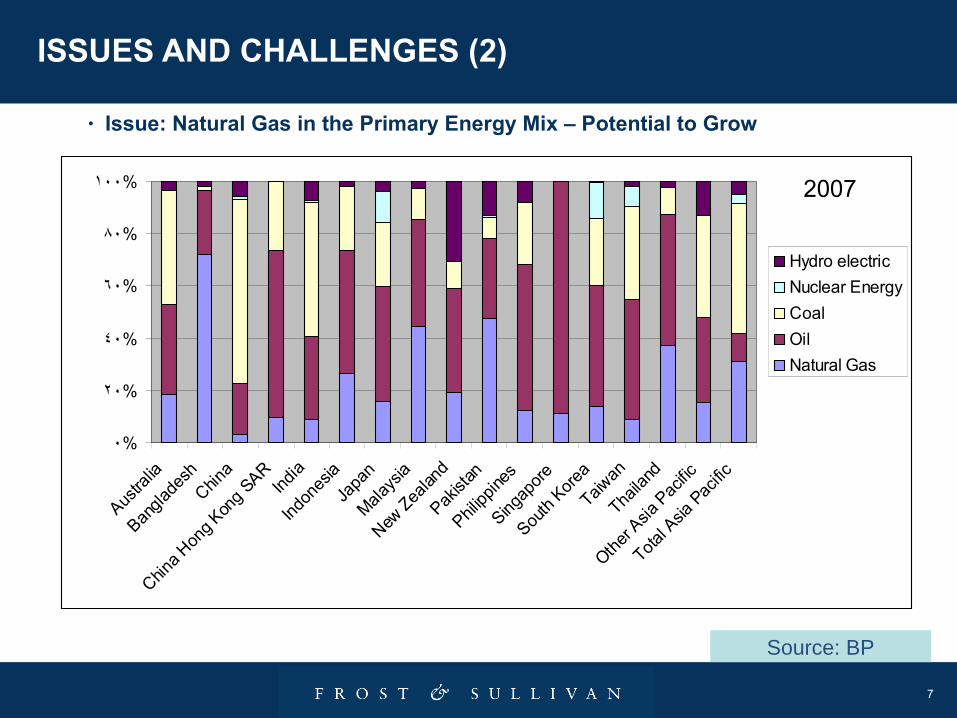

• Issue: Natural Gas in the Primary Energy Mix – Potential to Grow

2007

8

Power Generation Mix – ASIA, 2007

Source: Frost & Sullivan

Coal Nuclear + Coal + Gas Gas

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Chin

aIn

dia

Philippin

es

Indon

esia

Chines

e Tai

pei

South K

orea

Japan

Mal

aysia

Thaila

nd

Vietn

am

Pakis

tan

Bangla

desh

Singap

ore

Other

Nuclear

Hydro

Natural Gas

Oil

Coal

ISSUES AND CHALLENGES (3)

9

ISSUES AND CHALLENGES (4)

Challenge – High Cost of Developing Infrastructure

• Capital intensive projects requiring huge investments

• Escalating construction cost

• Sizeable market demand required to break even

Pluto Gas ProjectWestern AustraliaWoodside PetroleumProject Cost = $ 11.2 billion

Initial cost estimates = $ 6 billion to $ 10 billionSales Contracts: Kansai Electric and Tokyo Gas

First Gas Delivery: 2010

Platong Gas 2 Development ProjectThailandChevron, Mitsui and PTT E&PProject Cost, Initial estimates = $ 3.1 billionProject Start-up Q1, 2011

10

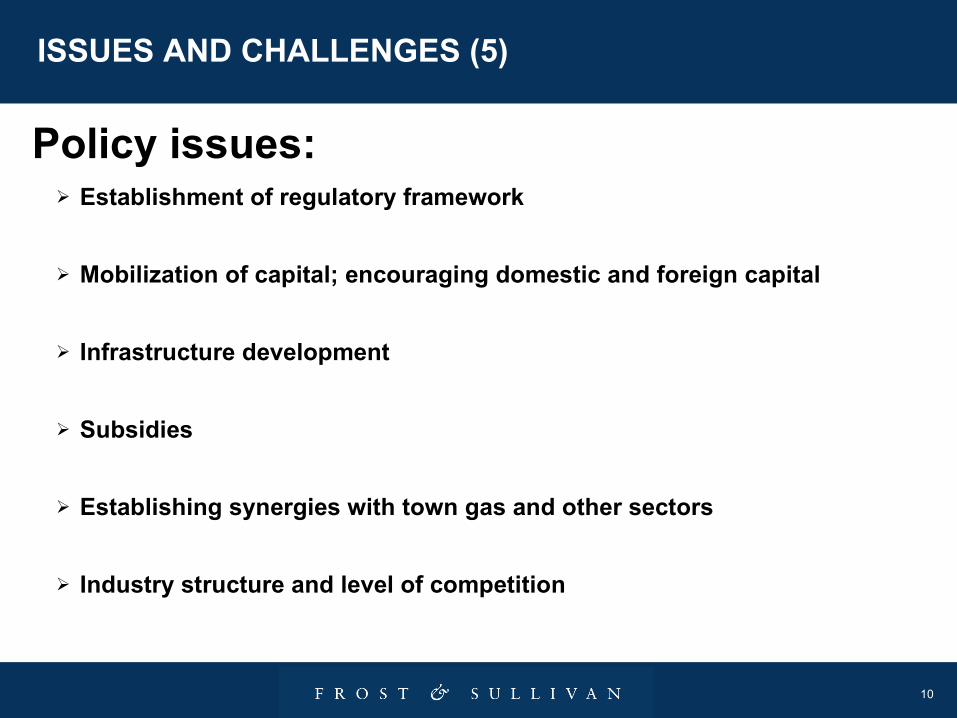

ISSUES AND CHALLENGES (5)

Policy issues: Establishment of regulatory framework

Mobilization of capital; encouraging domestic and foreign capital

Infrastructure development

Subsidies

Establishing synergies with town gas and other sectors

Industry structure and level of competition

11

2. KEY DRIVERS

12

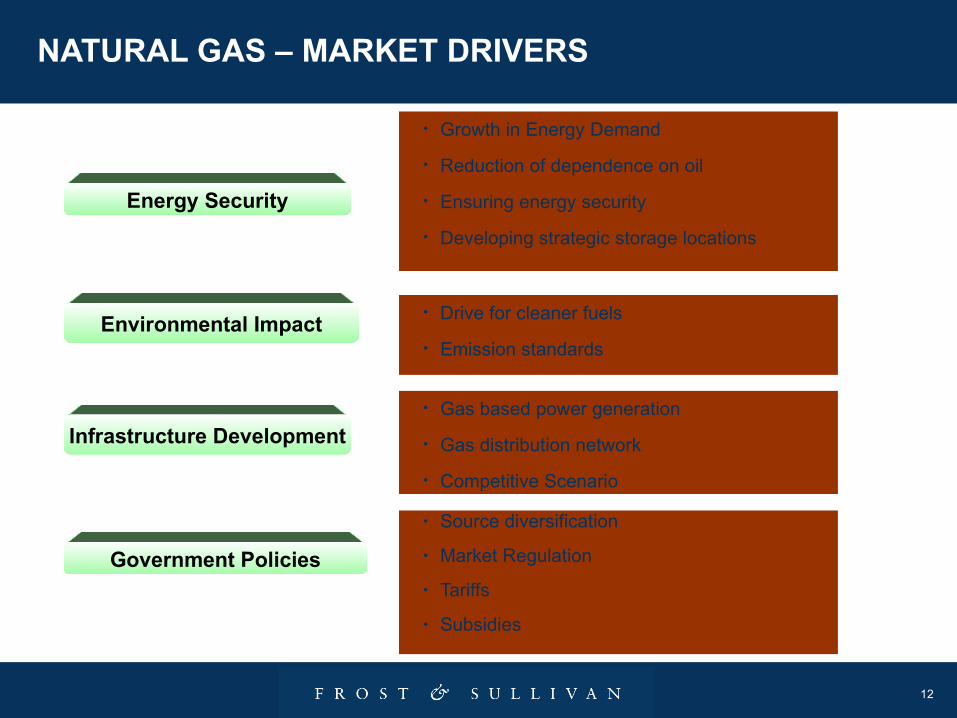

NATURAL GAS – MARKET DRIVERS

Government Policies

Energy Security

Infrastructure Development

• Source diversification

• Market Regulation

• Tariffs

• Subsidies

Environmental Impact• Drive for cleaner fuels

• Emission standards

• Growth in Energy Demand

• Reduction of dependence on oil

• Ensuring energy security

• Developing strategic storage locations

• Gas based power generation

• Gas distribution network

• Competitive Scenario

13

3. STRATEGIC OPTIONS TO DEVELOP

NATURAL GAS MARKETS

14

STRATEGIC OPTIONS

• Development of Infrastructure – LNG Terminals, Transnational/Cross-country Pipelines, Gas Distribution Network

• Markets develop rapidly once infrastructure is in place

• Develop long-term economic relationships with natural gas producing countries

• Develop demand – Gas based power generation, development of other

markets such as fertilisers

• Gas based power plants act as an anchor for natural gas demand. Other markets grow over this base demand

15

Demand from the power sector is crucial during the initial stages of a LNG

project to make the project viable

Power sector provides a base demand allowing secondary

markets to develop

Secondary Markets Develop (gas for industries/domestic

fuel)

TIME

LN

G

DE

MA

ND

Initial demand from power projects crucial to kick-start the LNG

market

The LNG markets in Japan and South Korea were kick-started by the power sector

Source: Frost & Sullivan

STRATEGIC OPTIONS (2)

16

STRATEGIC OPTIONS (3)

• Promote clean environment scenario

• Enforce stringent norms for meeting emission standards

• Gas based power generation

• Promote use of Natural Gas Vehicles (NGVs), especially for public transportation system

• Create awareness on global warming

• Plan for natural gas introduction in areas with no infrastructure

• Identify emerging energy centers

• Promote gas based technologies in these areas

17

STRATEGIC OPTIONS (4)

• Natural gas expansion plan to be linked with government policies

• Expand natural gas use as raw material and energy source

• Promoting use in industries

• Promoting residential and commercial use. Town gas infrastructure development

• Expand to vehicular segments

• Encourage natural gas technological knowledge in the supply chain

• Production, transportation, processing, distribution

• Vertical integration of gas based services

18

4. ROLE OF REGULATORS

19

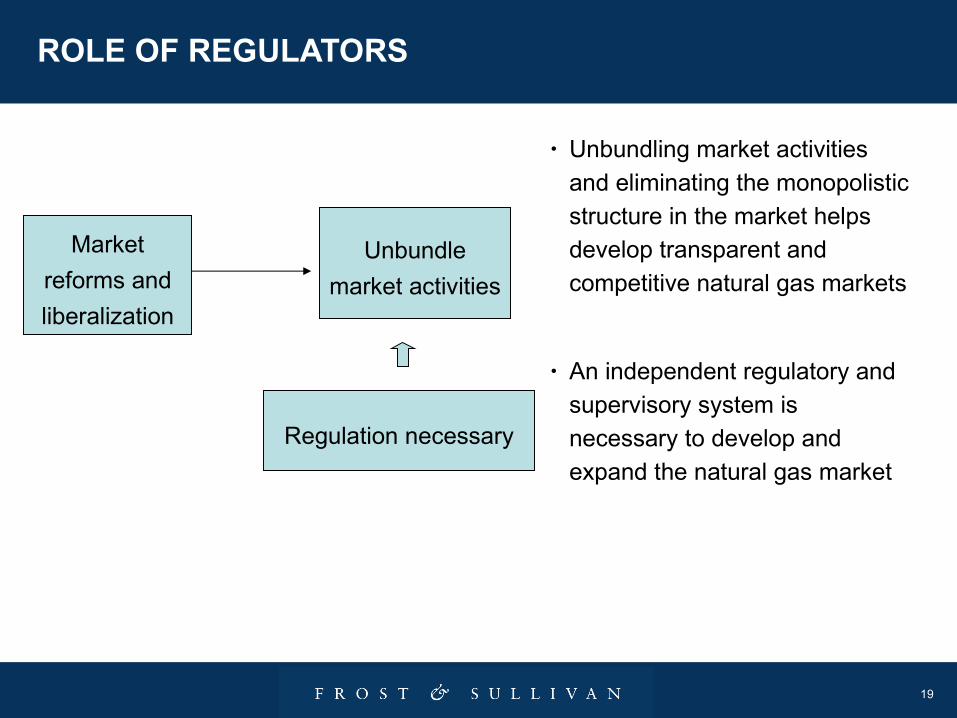

ROLE OF REGULATORS

• Unbundling market activities

and eliminating the monopolistic

structure in the market helps develop transparent and

competitive natural gas markets

• An independent regulatory and

supervisory system is

necessary to develop and

expand the natural gas market

Market

reforms and

liberalization

Unbundle

market activities

Regulation necessary

20

ROLE OF REGULATORS (2)

• Provide a stable, transparent & reliable regulatory regime

• Development of policies and infrastructure to foster market growth

• Ensure competition

• Competition is necessary for market development – Independent regulatory authority is required to ensure level playing field for all competitors

• Improve efficiency thereby lower costs

• Ensure security of supply

21

ROLE OF REGULATORS (3)

• Licensing

• Licenses for import, export, transmission, storage, distribution, etc

• Market Surveillance

• Regulate tariffs – ensure reasonable prices

• Regulate third party access to the system

• Monitor performance and service standards of gas companies

• Protect consumer rights

• Evaluation of subsidy policies

22

ROLE OF REGULATORS (4)

• Monitor cross-border trade

• Co-operation with other regional regulating agencies

• Regulate foreign investment

23

FROST & SULLIVAN

A GLOBAL GROWTH CONSULTING COMPANY