Developing national

19

~ Pergamon PII: S0301-4207(97)00008-1 Resources Policy. Vol. 23, No. 1/2, pp. 51-69. 1997 © 1997 Elsevier Science Ltd All rights reserved. Printed in Great Britain 0301-4207/97 $17.00 + 0.00 Developing national mining policies in Chile: 1974-96 Gustavo Lagos School of Engineering, Catholic University of Chile, Vicuna Mackenna 2860, Santiago, Chile (Tel: 562 552 2375; Fax: 562 552 4054; e-mail: glagosing.puc.cl) This paper discusses the mining development policies in Chile in the period 1974-96. This period includes the military government that took over the country from socialist President Allende in 1973, and the return to democracy with the election of President Aylwin in 1989 and of President Frei in 1993. The paper analyses the economic and mining policies of the military and democratic periods, and then the country's mining investment, production and exports under the prism of the main institutional development policies pursued. The analysis focuses on copper mining, where investment and growth have created a mining boom unpre- cedented worldwide in this century since the discovery of the flotation process in the early 1900s. Thus it is of special relevance to examine the set of circumstances that has made this boom possible. The main discussion during this period regards the legitimacy of foreign invest- ment in mining vs the capacity and potential of the state-owned company Codelco to be a protagonist of mining development. While the more liberal sectors of the political spectrum have supported the privatization of Codelco, the more conservative sectors support the con- tinued ownership of Codelco by the state. This discussion will be of no great consequence if the mining boom continues. Nevertheless aspects of the discussion in 1996 questioned the economic development model employed by the country since 1974. Crucial for the legitimacy of foreign investment is the assessment of the returns that the country is receiving from mining investment. Two studies released in 1996 conclude that the overall effects of foreign investment in mining are positive at the national and regional levels and that a Dutch disease scenario does not seem probable for the future. Moreover, it is evident that had the mining boom not occurred, the country's economic growth would have been lower during the period 1988-96. It also seems clear that the military government did not have identifiable viable options for a potentially successful mining policy at the time when the great policy decisions were taken. This has been validated by the policies adopted by the two demo- cratic governments in more recent years. This does not signify that all is perfect. Indeed there are policy changes to be adopted, but they seem to be directed at adjusting the model so that the country improves its returns rather than upsetting the whole economic-institutional model. © 1997 Elsevier Science Ltd. Introduction Chile's economy grew at a rate of 7%/yr on average during the period 1986-95 -- unprecedented for Chile this century. Mining has had an important role in Chi- le's economic growth during this period. Mining in Chile has experienced three phases since 1971. The first phase extended from 1971 to 1973 and included the nationalization of copper mining during the socialist government of President Salvador Allende. The second phase began in 1974, with the military government that seized power from President Allende, and ended in 1990 with the return to democ- racy. The third period extends from 1990 to the present (1996) and includes the terms of President Aylwin (1990-94) and of President Frei (1994-2000) where several major changes in development policies occurred. A common feature of all these periods has 51

-

Upload

andres-lozano -

Category

Documents

-

view

215 -

download

0

description

ambiental

Transcript of Developing national

~ Pergamon PII: S0301-4207(97)00008-1 Resources Policy. Vol. 23, No. 1/2, pp. 51-69. 1997

© 1997 Elsevier Science Ltd All rights reserved. Printed in Great Britain

0301-4207/97 $17.00 + 0.00

Developing national mining policies in Chile: 1974-96

Gustavo Lagos School of Engineering, Catholic University of Chile, Vicuna Mackenna 2860, Santiago, Chile (Tel: 562 552 2375; Fax: 562 552 4054; e-mail: glagosing.puc.cl)

This paper discusses the mining development policies in Chile in the period 1974-96. This period includes the military government that took over the country from socialist President Allende in 1973, and the return to democracy with the election of President Aylwin in 1989 and of President Frei in 1993. The paper analyses the economic and mining policies of the military and democratic periods, and then the country's mining investment, production and exports under the prism of the main institutional development policies pursued. The analysis focuses on copper mining, where investment and growth have created a mining boom unpre- cedented worldwide in this century since the discovery of the flotation process in the early 1900s. Thus it is of special relevance to examine the set of circumstances that has made this boom possible. The main discussion during this period regards the legitimacy of foreign invest- ment in mining vs the capacity and potential of the state-owned company Codelco to be a protagonist of mining development. While the more liberal sectors of the political spectrum have supported the privatization of Codelco, the more conservative sectors support the con- tinued ownership of Codelco by the state. This discussion will be of no great consequence if the mining boom continues. Nevertheless aspects of the discussion in 1996 questioned the economic development model employed by the country since 1974.

Crucial for the legitimacy of foreign investment is the assessment of the returns that the country is receiving from mining investment. Two studies released in 1996 conclude that the overall effects of foreign investment in mining are positive at the national and regional levels and that a Dutch disease scenario does not seem probable for the future. Moreover, it is evident that had the mining boom not occurred, the country's economic growth would have been lower during the period 1988-96. It also seems clear that the military government did not have identifiable viable options for a potentially successful mining policy at the time when the great policy decisions were taken. This has been validated by the policies adopted by the two demo- cratic governments in more recent years. This does not signify that all is perfect. Indeed there are policy changes to be adopted, but they seem to be directed at adjusting the model so that the country improves its returns rather than upsetting the whole economic-institutional model. © 1997 Elsevier Science Ltd.

Introduction

Chile's economy grew at a rate of 7%/yr on average during the period 1986-95 - - unprecedented for Chile this century. Mining has had an important role in Chi- le's economic growth during this period. Mining in Chile has experienced three phases since 1971. The first phase extended from 1971 to 1973 and included the nationalization of copper mining during the

socialist government of President Salvador Allende. The second phase began in 1974, with the military government that seized power from President Allende, and ended in 1990 with the return to democ- racy. The third period extends from 1990 to the present (1996) and includes the terms of President Aylwin (1990-94) and of President Frei (1994-2000) where several major changes in development policies occurred. A common feature of all these periods has

51

Developing national mining policies in Chile: G Lagos

been the state investment in mining, channelled mainly through the state-owned company Codelco (Corporacion del Cobre de Chile).

This paper describes the country's mining invest- ment, production, and exports during all three periods and analyses public policy during the two most recent periods. The analysis focuses on the copper primary industry, where investment and growth during the third period have created a mining boom unpre- cedented worldwide in this century since the dis- covery of the flotation process in the early 1900s, which resulted in the dominance of the US copper mining production for most of the century. Thus it is of special relevance to examine the set of circum- stances that has made this boom possible.

An overview of the Chilean economy

The stability and range of economic policies have been fundamental to Chile's economic growth over the last 10 years. An economic background analysis of the two periods under study is carried out in the following sections, followed by a description of Chi- le's exports, investment and copper production since 1970.

Economic policies of the military government: 1974-90

It is worthwhile recounting that at the time of the writ- ing of the foreign investment statute in 1974, a main factor in the development of the mining boom, the military had just taken over the government and Chile was in the midst of a severe political and economic crisis. In 1972 and 1973, under the socialist govern- ment of President Allende, gross domestic product (GDP) decreased by 6.8% overall. In 1973, the rate of inflation was 441%, the unemployment rate was 4.6%, and the economy was dominated by 596 state- owned companies, many of them recently expropri- ated, which generated 39% of the GDP (Hachette and Luders, 1992).

The economic policy of the military government consisted of assuring stable and high economic growth, eradicating extreme poverty, achieving full employment through highly productive activities and achieving stable prices. The instruments that the government chose to achieve these policies were: restoring the market as the main instrument for econ- omic decisions; restoring the private sector as the main agent of development; lowering trade barriers to achieve more competitive enterprises and to exploit the country's comparative advantages; opening the economy to foreign trade; treating all sectors in a non- discriminatory manner; developing an efficient fin- ancial market with the aim of improving savings and investment; and using interest rates, exchange rates, and the money supply to achieve the previous aims.

Some of the most important specific actions were: reducing all import tariffs to 10% by 1979 (from as

high as 750%); eliminating all foreign trade restric- tions; fixing the exchange rate at higher than market values to control inflation; authorizing foreign cur- rency accounts in the country and also setting no lim- its on the inflow of capital; and eliminating credit restrictions.

The application of these policies did not bring the overall expected results during the period 1974-82. Indeed in 1975 a severe economic depression affected the country because of the deep restructuring of the political and economic system. The GDP decreased by 12.9% and inflation was still extremely high, 379.2%. Some of the macroeconomic variables began to be controlled though. Such was the case of exports which increased for a second consecutive year, and of the fiscal deficit which fell significantly between 1973 and 1975.

Economic growth from 1976 to 1981 was 7.2%/yr but it brought with it the ingredients for disaster. The recession of 1982 and 1983, triggered by the need to return to more realistic values of the exchange rate and by the world's economic recession of 1982, was the deepest recession in Chile since the Great Depression of 1930. The GDP fell by 14.1% and the whole banking system had to be taken over by the government because it could not pay its foreign cur- rency debt. Approximately 50 of the most important companies that had been handed back to the private sector after 1974 were returned to the control of the state because of their incapacity to carry on with their activity (Hachette and Luders, 1992). During the recession, unemployment reached 22.2% and it remained over 10% until 1988. It is worthwhile noting that during the 17 years of the military government, unemployment was as an average 12%, in spite of the two long periods of economic growth, 1976-81 and 1984-90. Inflation which had at last been brought down from 497.8% in 1974 to 9.9% in 1982, went back up to 27.3% in 1983 and then fluctuated between 15 and 30% between 1984 and 1990. Gross invest- ment as a percent of GDP, which had been low since the beginning of the 1970s remained at an average of just over 15% in the period 1984-90.

During the first few years of the recovery after 1983 there was widespread social unrest. After more than 10 years of military government and economic reforms the country did not seem to be on a clear economic path. Salaries were at the lowest during the decade and unemployment remained high. The econ- omic policy underwent further change, correcting aspects which were unsuccessful during the period 1974-83. The main differentiating features with respect to the previous period were: reducing fiscal spending by decreasing expenditure on health, wel- fare and education by more than 20% during this per- iod; and maintaining an exchange rate closer to its market value, so that imports would be reduced and exports would be bolstered. The local currency lost about 60% of its value against the dollar between 1983 and 1989; also the payment of the external debt,

52

Developing national mining policies in Chile: G Lagos

an important matter for the economy since the 1970s, was renegotiated and a substantial reduction of inter- est rates was achieved; internal expenditures were maintained low to control inflation until 1988, when they were increased to help General Pinochet win the plebiscite of 1989. From 1987 onwards this economic policy was helped by the increase in the copper price which had been very low since the world economic recession of 1982.

One of the last actions of the military government in the economic arena, just in case the country voted for a return to democracy, was to make the Central Bank an autonomous institution, integrated by a Board politically balanced and stable in time, which could more realistically control some of the main macroeconomic variables.

In conclusion, low- and middle-income people were hit hard by the economic policies of this period. Although recovery was achieved, the standard of liv- ing in 1989 was still lower than that of 1981 and the overall response of the population, not only for econ- omic reasons though, was to vote for a return to democracy (Morande, 1993).

Economic policies of the democratic period: 1990- 96

The newly elected government of President Aylwin could not reverse the economic policies that had led to 6 years of impressive economic growth, yet it was committed to introducing social policies that would favour the poorer segments of the population which had suffered most from the military's economic poli- cies. The economic policies of President Aylwin's government were based on three principles:

(1) Continuing the free market economic reforms undertaken by the military, making only minor adjustments to them.

(2) Preserving the macroeconomic balance, including keeping fiscal spending below 2% of the GDP, controlling inflation, etc.

(3) Increasing public spending directed at improving social programmes such as housing, health and education. This was financed through tax reform that increased the value-added tax by 2%, provid- ing an additional US$700 million/yr to the Treas- ury.

The government was faithful to these principles and its achievements were evident: it controlled inflation and brought it back to 12% from the 20s that had been reached during election year; it maintained economic growth at the same levels as in the period 1984-89, ie, close to 7%/yr; it increased spending in real terms in health, education and housing by more than 85, 25 and 35%, respectively during the period; exports were maintained at about one-third of the GDP while sav- ings and investment increased to unprecedented levels as a percentage of GDP. The latter was due in part to the fact that the pension funds had accumulated by

1993 funds of approximately 40% of the GDP. The peso appreciated by more than 10% against the US dollar during the Aylwin Government possibly as a result of export and trade success, although some of this trend can be explained to differential interest rates between Chile and other countries (Morande, 1993).

The second democratic government, which assumed power in March 1994 and will stay until March 2000, continued to apply the same economic policies. Since 1990 investment spending in the coun- try has averaged 26.7% of GDP, and exports have remained at about one-third of the GDP. Inflation has been less than 10%/yr since 1994. The peso has appreciated vs the US$ by slightly more than 20% in the period 1990-96. This appreciation has produced serious problems for some of the exporting sectors, and there is real pressure now to stop or contain this trend. Nevertheless the reasons for the appreciation seem to be each time more clearly the increasing foreign investment and exports. Foreign investment has averaged over US$2.5 billion/yr since 1994, com- pared to US$1.25 billion in the four previous years. Thus it is difficult if not impossible to modify this trend without altering substantially the economic model.

Productivity gains have matched real increases in salaries so far, except during 1995-96 when pro- ductivity seemed to grow more than salaries (Tasc, 1996). Although infrastructure has increased close to 100% since 1990 there still are serious bottlenecks, especially in those sectors where there remain state- owned companies. The modernization of the state has been a goal of President Frei's government but advances have been scarce. The greater public spend- ing on social programmes has not yet proved effec- tive; most of the observed reduction in poverty seems to have originated in overall economic growth (Tasc, 1996).

It is in this context that since 1994 it has become apparent that Chilean GDP can grow at very high rates, ie, 7%, for long periods. Two elements are the base for such understanding: first productivity has been increasing steadily since 1990 and the dynamic Chilean economy can continue to have this increase in the future; and the second element is that invest- ment and savings have grown since the end of the 1980s to a point where sustainable high growth is pre- dictable (Tasc, 1996).

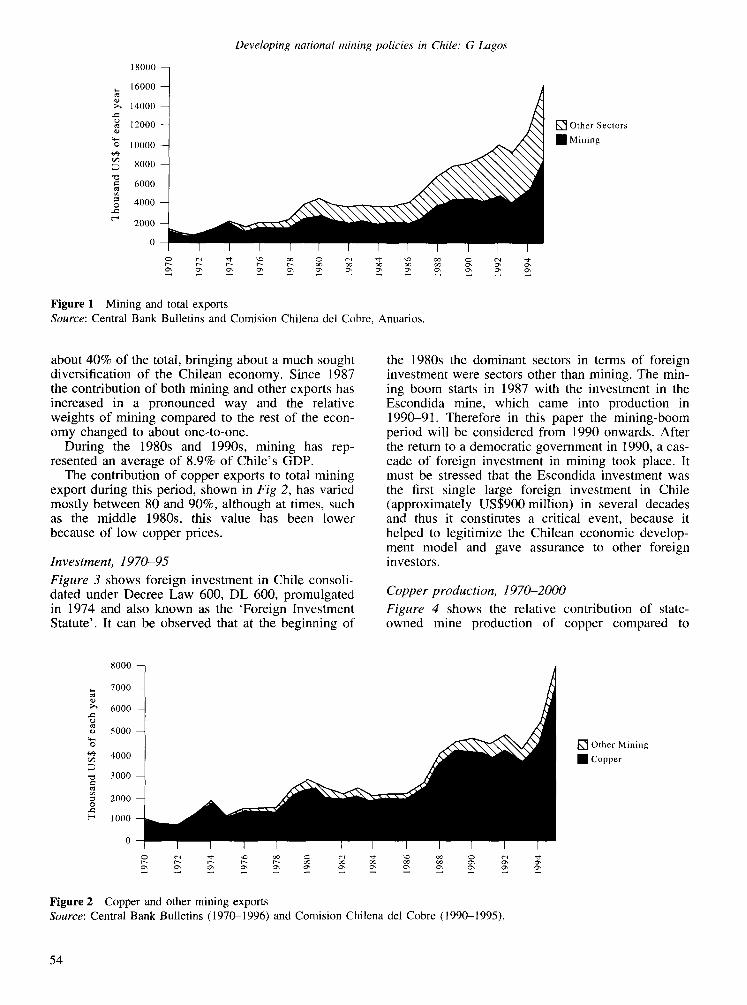

Exports, 1970-95 As noted in the introduction, investment spending and mineral exports are important characteristics of the three historical periods under study here. The follow- ing figures show the relative contributions of invest- ments and exports in mining, copper and the overall economy. Figure 1 shows Chile's mining and total exports. Prior to 1975, the contribution of other (nonmineral) sectors to the country's exports was negligible. Between 1975 and 1980, the contribution of other sectors to the country's exports increased to

53

18000

16000

~ 14000

~ 12000

1oooo

8000

~ 6o0o

4000

2000

Developing national mining policies in Chile." G Lagos

Figure 1 Mining and total exports Source: Central Bank Bulletins and Comision Chilena del Cobre, Anuarios.

[ ] Other Sectors

• Mining

about 40% of the total, bringing about a much sought diversification of the Chilean economy. Since 1987 the contribution of both mining and other exports has increased in a pronounced way and the relative weights of mining compared to the rest of the econ- omy changed to about one-to-one.

During the 1980s and 1990s, mining has rep- resented an average of 8.9% of Chile 's GDP.

The contribution of copper exports to total mining export during this period, shown in Fig 2, has varied mostly between 80 and 90%, although at times, such as the middle 1980s, this value has been lower because of low copper prices.

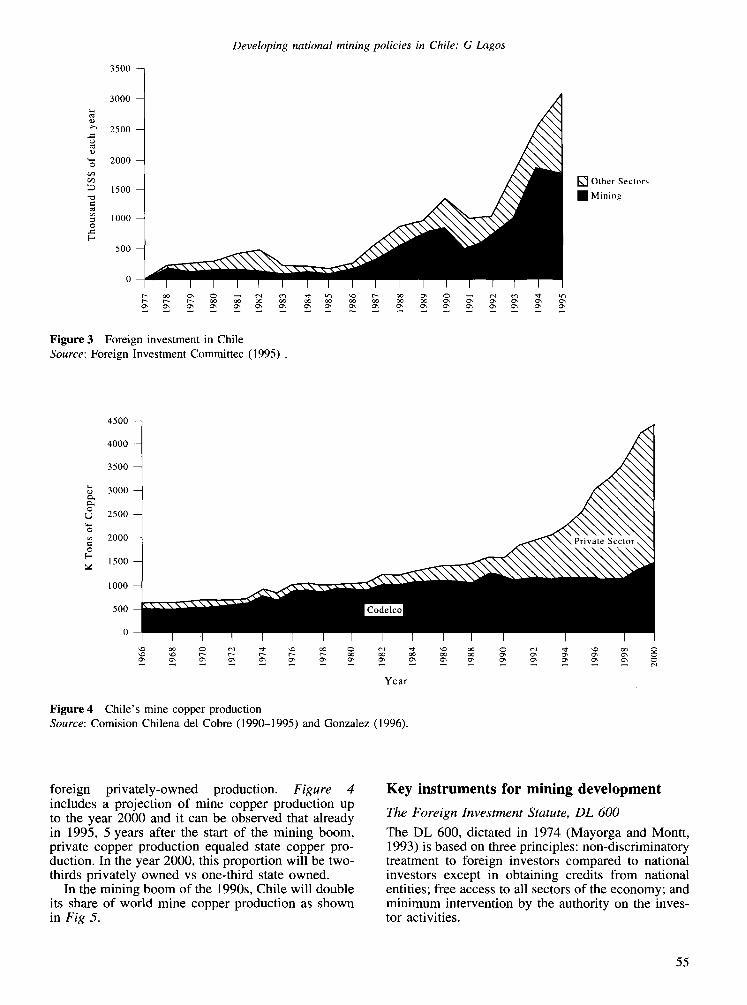

Investment, 1970-95

Figure 3 shows foreign investment in Chile consoli- dated under Decree Law 600, DL 600, promulgated in 1974 and also known as the 'Foreign Investment Statute'. It can be observed that at the beginning of

the 1980s the dominant sectors in terms of foreign investment were sectors other than mining. The min- ing boom starts in 1987 with the investment in the Escondida mine, which came into production in 1990-91. Therefore in this paper the mining-boom period will be considered from 1990 onwards. After the return to a democratic government in 1990, a cas- cade of foreign investment in mining took place. It must be stressed that the Escondida investment was the first single large foreign investment in Chile (approximately US$900 million) in several decades and thus it constitutes a critical event, because it helped to legitimize the Chilean economic develop- ment model and gave assurance to other foreign investors.

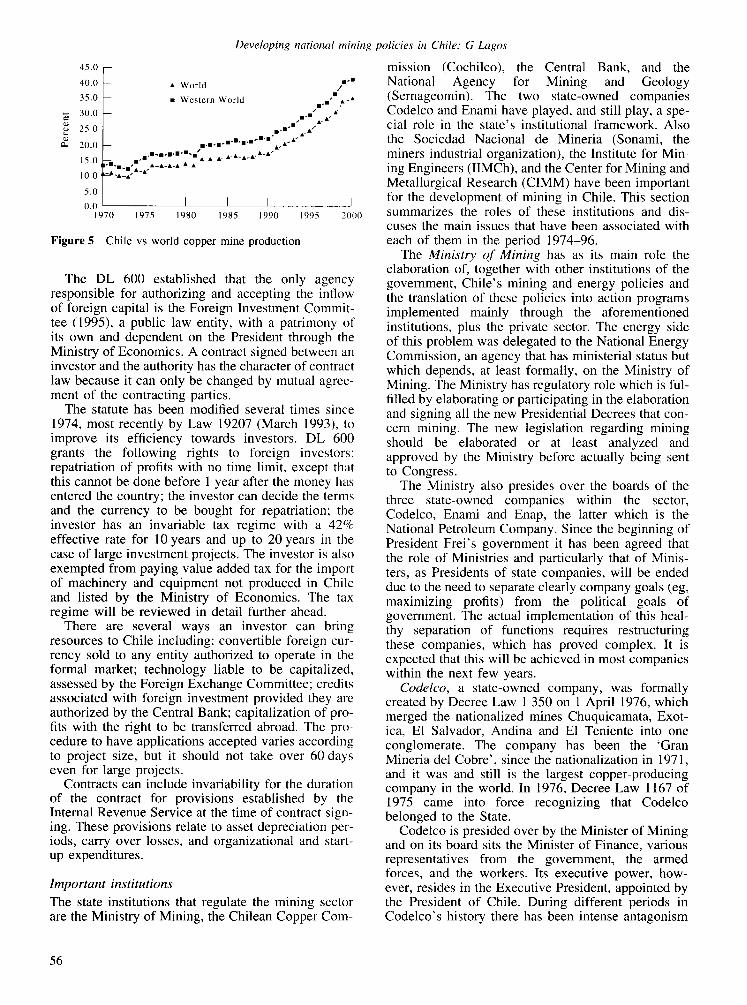

Copper production, 1970-2000

Figure 4 shows the relative contribution of state- owned mine production of copper compared to

8000 --

7000

6000

5000

4000

3000

= 2000 o

1000

Figure 2 Copper and other mining exports Source: Central Bank Bulletins (1970-1996) and Comision Chilena del Cobre (1990-1995).

[ ] Other Mining

• Copper

54

o e~

3500

3000

2500

2000

1500

1000

500

0

Developing national mining policies in Chile: G Lagos

[ ] Other Sectors

• Mining

Figure 3 Foreign investment in Chile Source: Foreign Investment Committee (1995) .

4500 --

4000

3500

3000

2500

2000 o

1500

1000

500

Y e a r

Figure 4 Chile's mine copper production Source: Comision Chilena del Cobre (1990-1995) and Gonzalez (1996).

foreign privately-owned production. Figure 4 includes a projection of mine copper production up to the year 2000 and it can be observed that already in 1995, 5 years after the start of the mining boom, private copper production equaled state copper pro- duction. In the year 2000, this proportion will be two- thirds privately owned vs one-third state owned.

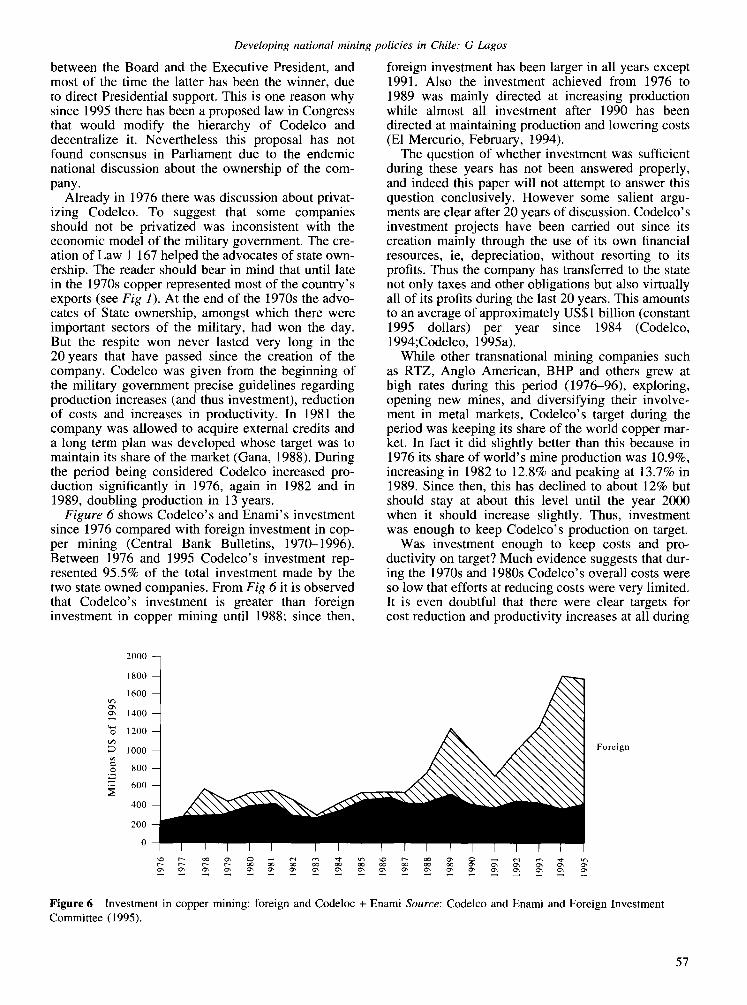

In the mining boom of the 1990s, Chile will double its share of world mine copper production as shown in Fig 5.

Key instruments for mining development

The Foreign Investment Statute, DL 600

The DL 600, dictated in 1974 (Mayorga and Montt, 1993) is based on three principles: non-discriminatory treatment to foreign investors compared to national investors except in obtaining credits from national entities; free access to all sectors of the economy; and minimum intervention by the authority on the inves- tor activities.

55

4 5 m 0 m

4 0 " 0 - -

3 5 " 0 - -

3 0 " 0 - -

2 5 " 0

2 0 " 0

1 5 " 0

1 0 " 0

5m0

0 " 0 1 9 7 0

• W o r l d

• W e s t e r n W o r l d

Developing national mining policies in Chile: G Lagos

mission (Cochilco), the Central Bank, and the • -" National Agency for Mining and Geology /

. ' , . , (Semageomin). The two state-owned companies m . l

- , Codelco and Enami have played, and still play, a spe- ,m m A.A"

, . , . , ,,~ cial role in the state's institutional framework. Also the Sociedad Nacional de Mineria (Sonami, the miners industrial organization), the Institute for Min- ing Engineers (IIMCh), and the Center for Mining and Metallurgical Research (CIMM) have been important

I for the development of mining in Chile. This section 2oo0 summarizes the roles of these institutions and dis-

cuses the main issues that have been associated with each of them in the period 1974-96.

The Ministry of Mining has as its main role the elaboration of, together with other institutions of the government, Chile's mining and energy policies and the translation of these policies into action programs implemented mainly through the aforementioned institutions, plus the private sector. The energy side of this problem was delegated to the National Energy Commission, an agency that has ministerial status but which depends, at least formally, on the Ministry of Mining. The Ministry has regulatory role which is ful- filled by elaborating or participating in the elaboration and signing all the new Presidential Decrees that con- cern mining. The new legislation regarding mining should be elaborated or at least analyzed and approved by the Ministry before actually being sent to Congress.

The Ministry also presides over the boards of the three state-owned companies within the sector, Codelco, Enami and Enap, the latter which is the National Petroleum Company. Since the beginning of President Frei's government it has been agreed that the role of Ministries and particularly that of Minis- ters, as Presidents of state companies, will be ended due to the need to separate clearly company goals (eg, maximizing profits) from the political goals of government. The actual implementation of this heal- thy separation of functions requires restructuring these companies, which has proved complex. It is expected that this will be achieved in most companies within the next few years.

Codelco, a state-owned company, was formally created by Decree Law 1 350 on 1 April 1976, which merged the nationalized mines Chuquicamata, Exot- ica, E1 Salvador, Andina and E1 Teniente into one conglomerate. The company has been the 'Gran Mineria del Cobre', since the nationalization in 1971, and it was and still is the largest copper-producing company in the world. In 1976, Decree Law 1167 of 1975 came into force recognizing that Codelco belonged to the State.

Codelco is presided over by the Minister of Mining and on its board sits the Minister of Finance, various representatives from the government, the armed Ibrces, and the workers. Its executive power, how- ever, resides in the Executive President, appointed by the President of Chile. During different periods in Codelco's history there has been intense antagonism

-- m m u m m m m m m A A A

• ' " " " " ~ • A. A'A'A'A'A-A¢

I I I I I 1 9 7 5 1 9 8 0 1 9 8 5 1 9 9 0 1 9 9 5

Figure 5 Chile vs world copper mine production

The DL 600 established that the only agency responsible for authorizing and accepting the inflow of foreign capital is the Foreign Investment Commit- tee (1995), a public law entity, with a patrimony of its own and dependent on the President through the Ministry of Economics. A contract signed between an investor and the authority has the character of contract law because it can only be changed by mutual agree- ment of the contracting parties.

The statute has been modified several times since 1974, most recently by Law 19207 (March 1993), to improve its efficiency towards investors. DL 600 grants the following rights to foreign investors: repatriation of profits with no time limit, except that this cannot be done before 1 year after the money has entered the country; the investor can decide the terms and the currency to be bought for repatriation; the investor has an invariable tax regime with a 42% effective rate for 10 years and up to 20 years in the case of large investment projects. The investor is also exempted from paying value added tax for the import of machinery and equipment not produced in Chile and listed by the Ministry of Economics. The tax regime will be reviewed in detail further ahead.

There are several ways an investor can bring resources to Chile including: convertible foreign cur- rency sold to any entity authorized to operate in the formal market; technology liable to be capitalized, assessed by the Foreign Exchange Committee; credits associated with foreign investment provided they are authorized by the Central Bank; capitalization of pro- fits with the right to be transferred abroad. The pro- cedure to have applications accepted varies according to project size, but it should not take over 60 days even for large projects.

Contracts can include invariability for the duration of the contract for provisions established by the Internal Revenue Service at the time of contract sign- ing. These provisions relate to asset depreciation per- iods, carry over losses, and organizational and start- up expenditures.

Important institutions The state institutions that regulate the mining sector are the Ministry of Mining, the Chilean Copper Corn-

56

Developing national mining policies in Chile." G Lagos

between the Board and the Executive President, and most of the time the latter has been the winner, due to direct Presidential support. This is one reason why since 1995 there has been a proposed law in Congress that would modify the hierarchy of Codelco and decentralize it. Nevertheless this proposal has not found consensus in Parliament due to the endemic national discussion about the ownership of the com- pany.

Already in 1976 there was discussion about privat- izing Codelco. To suggest that some companies should not be privatized was inconsistent with the economic model of the military government. The cre- ation of Law 1 167 helped the advocates of state own- ership. The reader should bear in mind that until late in the 1970s copper represented most of the country's exports (see Fig 1). At the end of the 1970s the advo- cates of State ownership, amongst which there were important sectors of the military, had won the day. But the respite won never lasted very long in the 20 years that have passed since the creation of the company. Codelco was given from the beginning of the military government precise guidelines regarding production increases (and thus investment), reduction of costs and increases in productivity. In 1981 the company was allowed to acquire external credits and a long term plan was developed whose target was to maintain its share of the market (Gana, 1988). During the period being considered Codelco increased pro- duction significantly in 1976, again in 1982 and in 1989, doubling production in 13 years.

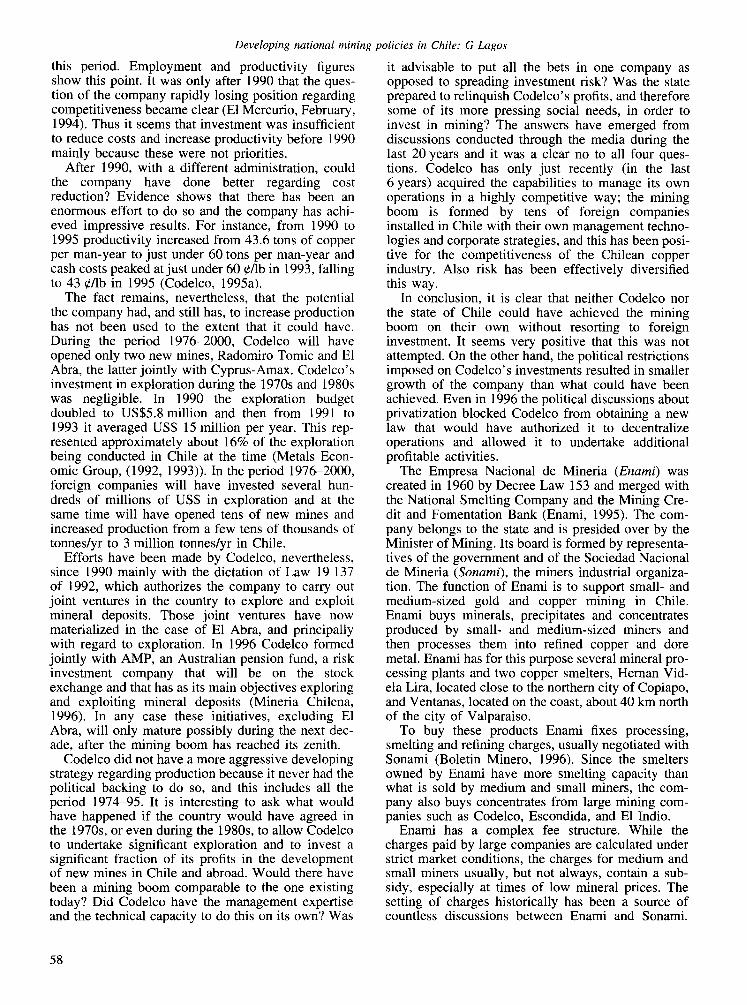

Figure 6 shows Codelco's and Enami's investment since 1976 compared with foreign investment in cop- per mining (Central Bank Bulletins, 1970-1996). Between 1976 and 1995 Codelco's investment rep- resented 95.5% of the total investment made by the two state owned companies. From Fig 6 it is observed that Codelco's investment is greater than foreign investment in copper mining until 1988; since then,

foreign investment has been larger in all years except 1991. Also the investment achieved from 1976 to 1989 was mainly directed at increasing production while almost all investment after 1990 has been directed at maintaining production and lowering costs (El Mercurio, February, 1994).

The question of whether investment was sufficient during these years has not been answered properly, and indeed this paper will not attempt to answer this question conclusively. However some salient argu- ments are clear after 20 years of discussion. Codelco's investment projects have been carried out since its creation mainly through the use of its own financial resources, ie, depreciation, without resorting to its profits. Thus the company has transferred to the state not only taxes and other obligations but also virtually all of its profits during the last 20 years. This amounts to an average of approximately US$1 billion (constant 1995 dollars) per year since 1984 (Codelco, 1994;Codelco, 1995a).

While other transnational mining companies such as RTZ, Anglo American, BHP and others grew at high rates during this period (1976-96), exploring, opening new mines, and diversifying their involve- ment in metal markets, Codelco's target during the period was keeping its share of the world copper mar- ket. In fact it did slightly better than this because in 1976 its share of world's mine production was 10.9%, increasing in 1982 to 12.8% and peaking at 13.7% in 1989. Since then, this has declined to about 12% but should stay at about this level until the year 2000 when it should increase slightly. Thus, investment was enough to keep Codelco's production on target.

Was investment enough to keep costs and pro- ductivity on target? Much evidence suggests that dur- ing the 1970s and 1980s Codelco's overall costs were so low that efforts at reducing costs were very limited. It is even doubtful that there were clear targets for cost reduction and productivity increases at all during

o

2000

1800

1600

1400

1200

1000

800

600

400

200

0

Fo r e ign

Figure 6 Investment in copper mining: foreign and Codeloc + Enami Source: Codelco and Enami and Foreign Investment Committee (1995).

57

Developing national mining policies in Chile: G Lagos

this period. Employment and productivity figures show this point. It was only after 1990 that the ques- tion of the company rapidly losing position regarding competitiveness became clear (El Mercurio, February, 1994). Thus it seems that investment was insufficient to reduce costs and increase productivity before 1990 mainly because these were not priorities.

After 1990, with a different administration, could the company have done better regarding cost reduction? Evidence shows that there has been an enormous effort to do so and the company has achi- eved impressive results. For instance, from 1990 to 1995 productivity increased from 43.6 tons of copper per man-year to just under 60 tons per man-year and cash costs peaked at just under 60 ¢/lb in 1993, falling to 43 ¢/lb in 1995 (Codelco, 1995a).

The fact remains, nevertheless, that the potential the company had, and still has, to increase production has not been used to the extent that it could have. During the period 1976-2000, Codelco will have opened only two new mines, Radomiro Tomic and E1 Abra, the latter jointly with Cyprus-Amax. Codelco's investment in exploration during the 1970s and 1980s was negligible. In 1990 the exploration budget doubled to US$5.8 million and then from 1991 to 1993 it averaged US$ 15 million per year. This rep- resented approximately about 16% of the exploration being conducted in Chile at the time (Metals Econ- omic Group, (1992, 1993)). In the period 1976-2000, foreign companies will have invested several hun- dreds of millions of US$ in exploration and at the same time will have opened tens of new mines and increased production from a few tens of thousands of tonnes/yr to 3 million tonnes/yr in Chile.

Efforts have been made by Codelco, nevertheless, since 1990 mainly with the dictation of Law 19 137 of 1992, which authorizes the company to carry out joint ventures in the country to explore and exploit mineral deposits. Those joint ventures have now materialized in the case of E1 Abra, and principally with regard to exploration. In 1996 Codelco formed jointly with AMP, an Australian pension fund, a risk investment company that will be on the stock exchange and that has as its main objectives exploring and exploiting mineral deposits (Mineria Chilena, 1996). In any case these initiatives, excluding E1 Abra, will only mature possibly during the next dec- ade, after the mining boom has reached its zenith.

Codelco did not have a more aggressive developing strategy regarding production because it never had the political backing to do so, and this includes all the period 1974-95. It is interesting to ask what would have happened if the country would have agreed in the 1970s, or even during the 1980s, to allow Codelco to undertake significant exploration and to invest a significant fraction of its profits in the development of new mines in Chile and abroad. Would there have been a mining boom comparable to the one existing today? Did Codelco have the management expertise and the technical capacity to do this on its own? Was

it advisable to put all the bets in one company as opposed to spreading investment risk? Was the state prepared to relinquish Codelco's profits, and therefore some of its more pressing social needs, in order to invest in mining? The answers have emerged from discussions conducted through the media during the last 20 years and it was a clear no to all four ques- tions. Codelco has only just recently (in the last 6 years) acquired the capabilities to manage its own operations in a highly competitive way; the mining boom is formed by tens of foreign companies installed in Chile with their own management techno- logies and corporate strategies, and this has been posi- tive for the competitiveness of the Chilean copper industry. Also risk has been effectively diversified this way.

In conclusion, it is clear that neither Codelco nor the state of Chile could have achieved the mining boom on their own without resorting to foreign investment. It seems very positive that this was not attempted. On the other hand, the political restrictions imposed on Codelco's investments resulted in smaller growth of the company than what could have been achieved. Even in 1996 the political discussions about privatization blocked Codelco from obtaining a new law that would have authorized it to decentralize operations and allowed it to undertake additional profitable activities.

The Empresa Nacional de Mineria (Enami) was created in 1960 by Decree Law 153 and merged with the National Smelting Company and the Mining Cre- dit and Fomentation Bank (Enami, 1995). The com- pany belongs to the state and is presided over by the Minister of Mining. Its board is formed by representa- tives of the government and of the Sociedad Nacional de Mineria (Sonami), the miners industrial organiza- tion. The function of Enami is to support small- and medium-sized gold and copper mining in Chile. Enami buys minerals, precipitates and concentrates produced by small- and medium-sized miners and then processes them into refined copper and dore metal. Enami has for this purpose several mineral pro- cessing plants and two copper smelters, Hernan Vid- ela Lira, located close to the northern city of Copiapo, and Ventanas, located on the coast, about 40 km north of the city of Valparaiso.

To buy these products Enami fixes processing, smelting and refining charges, usually negotiated with Sonami (Boletin Minero, 1996). Since the smelters owned by Enami have more smelting capacity than what is sold by medium and small miners, the com- pany also buys concentrates from large mining com- panies such as Codelco, Escondida, and E1 Indio.

Enami has a complex fee structure. While the charges paid by large companies are calculated under strict market conditions, the charges for medium and small miners usually, but not always, contain a sub- sidy, especially at times of low mineral prices. The setting of charges historically has been a source of countless discussions between Enami and Sonami.

58

Developing national mining policies in Chile: G Lagos

The subsidy can be considerable; in 1993, for instance, when copper prices were low, Enami's pro- fits were US$22million on total sales of over US$700 million, and the subsidy to small and medium miners was US$20 million (Lagos, 1994b).

According to the mining classification of Sernageo- min (Anuario de la Mineria Chilena, 1994), in 1994 there were approximately 9 000 people employed in small copper and gold mining and close to 23 thousand people employed in medium copper and gold mining. Large-scale copper mining employed that same year a total of 20610 people. Lagos (1994b)) has discussed the segmentation of mining in Chile as well as the policies of Enami.

The Chilean Copper Commission (Cochilco) was created in 1976 by Decree Law 1 349, the same year that Codelco was created (Direcmin, 1996). Its role, as defined by this law, is to design policies for the mining sector, regulate and control several aspects related to it, and assist the Ministry of Mining in its functions. Cochilco has a Board of Directors, presided over by the Minister of Mining, and includes the Min- ister of Defense, the Chief of the National Defense, and representatives of the Central Bank and of the President.

Regarding the design of policies its role is very ample and thus it is authorized to get involved in diverse aspects of the mining institutional framework. A special emphasis is put on the identification and development of strategic thinking regarding mining activities. On the regulatory side, its job is to ensure that regulations affecting the operation of mining companies, be they state-owned or private, are being followed. Cochilco works alongside the Foreign Investment Committee in the approval and control of foreign mining investment. It also looks after the adequate use of resources and their transparent use by Codelco and Enami. Cochilco evaluates, along with the Planning Ministry (Mideplan) the economic and technical feasibility of Codelco's and Enami's invest- ment programs and projects. Finally it also supervises in collaboration with the Central Bank the exports of copper.

Cochilco's real role has varied widely during dif- ferent periods since its creation. During the 1970s and early 1980s its action was mainly focused on studies of development strategies for the mining companies and for Chile. It helped to create some of the key aspects of the development policies of Codelco and of Chile's mining policy with regard to CIPEC, the Intergovernmental Committee of Copper Exporting Countries, created in 1967 which, following the steps of OPEC, attempted unsuccessfully to control copper prices by regulating the supply of copper to markets.

From the very start Cochilco had some of its main roles blocked by the much more powerful Codelco. This concerned especially the analysis and approval of investment projects of this company, but other regulatory aspects as well. The fact was that the Presi- dent of Codelco during the military government years

was a three- or even a four-star general of the army whereas the position of the head of Cochilco was much lower in the ranks of the armed forces. Codelco did not want Cochilco looking over its shoulder and in practice much of Cochilco's supervisory and control powers were cut down from the start to a formal role. It was not until the 1990s that Cochilco partly reco- vered some of the clout that it should have had all along.

In its relationship with Codelco, Cochilco has not always had a sufficient number of technical personnel with the appropriate experience to be an effective counterpart to Codelco's formidable teams of engin- eers and professionals. This does not mean that Codelco's projects were always right. There are many examples when they were proved ill-conceived, ex- post. A strong counterpart within the government to examine and analyze these projects would have been helpful in detecting and avoiding problems. One of the projects that went wrong was the development during the 1980s of sub-6 level in the E1 Teniente mine, one of the largest underground mines in the world. Several hundred million dollars were spent in this project and much of it could not be used after- wards due to rock explosions (or bursts), which required effectively closing down almost all pro- duction from that site. E1 Teniente thus saw its costs rise and the whole company suffered strongly from this event.

One of the most serious and shameful episodes of Codelco's short history occurred in 1993-94 when the company lost US$200 million due to futures trading by Juan Pablo Davila, the main futures operator of the company. One of the roles of Cochilco was and still is to supervise the transparency of the use of company financial resources. Yet, this episode was not detected by Cochilco, and obviously it was also undetected by Codelco itself. Although the blame for this episode can certainly not be put on Cochilco alone, the opposition political parties of the time were keen to ask why Cochilco and other state institutions such as the Central bank, did not fulfill their con- trolling role. Since 1994 Cochilco has undertaken the auditing of Codelco's activities, and also of Enami, in the area of futures operations and of other company activities judged to carry substantial risks. The audit- ing scheme implemented by Cochilco in 1995 is con- sidered integral, and its objective is to verify the pro- cedures that the companies use are in accord with the policies and mechanisms established by their boards and management. They include also technical audits in the areas of exploration, mining and metallurgical processes (Codelco, 1995b).

It is in this context that to many analysts the role of Cochilco is unclear and not justified throughout its 20 years of history. No one has made an integral evaluation of the efficacy of having such an institution and the outcome of an audit would certainly be nega- tive for some of the periods of its history. On the other hand, its present activities fill some important gaps in

59

Developing national mining policies in Chile: G Lagos

government thinking and actions, and it is not clear at all which institutions could achieve this if Cochilco did not exist. To name some of the important activi- ties not already mentioned: Cochilco is taking an active role in the international environmental treaties to which Chile has subscribed or that could have a bearing on mineral markets and exports; the Basel Convention; the ISO 14000; the Prior Informed Con- sent UNEP initiative; the International Maritime Organization, IMO, liability and compensation fund; the World Trade Organization, WTO, meetings, etc (Lagos, 1995a). Cochilco also represents the govern- ment in the International Copper Study Group based in Lisbon. On the domestic front, it commissioned two studies to estimate the effect of mining on mac- roeconomic performance and of foreign investment on economic growth. This subject became important in 1996 at the time of evaluating the efficiency, from the country's point of view, of developing mining through state-owned companies compared to privately owned companies. Amongst the latter, of special con- cern are those companies that repatriate their profits to their home countries. Also on the domestic front, Cochilco has carried out studies of the effect of Chile joining the North American Free Trade Agreement (NAFTA), the MERCOSUR (formed until 1996 by Brasil, Argentina, Paraguay and Uruguay), and also the 'Association' agreement subscribed to in June 1996 in Florence, Italy, between Chile and the Euro- pean Union.

In the end, the role of Cochilco should be measured for its technical powers, as a permanent task force that can be put to work on those strategic issues that are essential for mining. Regarding its control and regulatory functions, it should be hoped that it can carry out these without as much interference as in the past, remembering always nevertheless, that when a conflict arises between Codelco and Cochilco, the for- mer's political power will almost certainly outweigh Cochilco's reasoning. Thus Cochilco's contributions have been of mixed success and not always perceived as significant. But at present and especially looking at Chile's position in the world copper market, it would be an error to believe that the important gaps that this institution is helping to fill would be assumed by anyone else.

There are several other important institutions. The National Geology and Mining Service (Sernageomin) was created in 1981 and merged the Mining Service and the Institute for Geological Research. The pur- pose of Sernageomin is to carry out basic research in geology, control the mining property, ie, mining and exploration rights, generate basic technical and stat- istical information, and look after certain environmen- tal functions such as occupational health and safety and the permitting of the construction and operation of mining related installations, for instance tailing dams. The Center for Mining and Metallurgical Research (CIMM) was created in 1970, and its main purpose is to carry out research for Chilean mining

(CIMM, 1990-1993). Finally, the Institute of Mining Engineers of Chile was created on the 29 September 1930 and since then it has contributed to the develop- ment of mining and metallurgical engineering in Chile (Minerales, 1995), as well as having played an important role in the definition of policies by various governments. It publishes the Minerales Journal, a technical journal which is now on its 50th year of existence.

Copper and the Mining Law of 1982 The constitution of 1980 establishes that the absolute and exclusive owner of mineral deposits is the state of Chile, ratifying the concept expressed in the copper mines nationalization Law 17 450 of 1971. The Min- ing Law of 1982 (Law 18097 published in the Official Government Journal on 21 January 21 1982) has constitutional status, ie, it requires three-fifths of Parliament to modify it. The Law established that the state can grant an exploration or an exploitation per- mit or concession to a person or a company. These concessions are granted by a court and entitle the per- mit owner to appropriate all the minerals or permitted substances within the boundaries of the mining pro- perty. The exploration concession expires after 4 years whereas the exploitation concession is indefinite, provided an annual mining patent is paid. These concessions can coexist with the property of the land. For instance if a gold deposit is found in a farm that belongs to an individual, the mineral deposit belongs to the state and can be claimed in concession by anyone, including the individual who owns the land. This is usually not the case. The owner of the concession should pay the owner of the land for any detriment the mine causes to the original productive purpose of the land. A mining concession can be traded in the market by its owner.

The Mining Law of 1982 also establishes that indemnification in the case of expropriation by the state should be calculated on the basis of the net present value of future cash flows estimated at likely market prices. This procedure to estimate the indem- nification value is clearly different to what was estab- lished in the nationalization law of 1971, where 'excessive' profits obtained by the expropriated com- panies before 1971 were subtracted from the total compensation that the state paid the companies.

The two main motives behind the Mining Law of 1982 were in the short term to increase foreign invest- ment in mining and thus have more foreign currency to pay the external debt, which was high at that time, and in the longer term to increase the export capacity of Chile, a factor considered crucial for future econ- omic growth (Gana, 1988). It is important to remem- ber that in 1982 the prices of most base metals were quite low and that the perspectives of mining invest- ment and development were not the most promising. Also there were concerns about possible substitution away from copper by other materials in main markets. The Minister of Mines, Jose Pinera, who introduced

60

Developing national mining policies in Chile: G Lagos

the mining law and author of other key institutional changes in other spheres of the government, justified this law due to the need for Chile to exploit mining resources in an accelerated way. The Minister also made reference to the coexistence of Codelco, the main copper producer in Chile at that time, with foreign mining investment and copper production.

Thus the Mining Law of 1982 paved the way for foreign investment in mining by giving the following assurances to foreign investors: overriding in practice the constitutional clause (Constitution of 1980) which says that all mines are owned exclusively by the state of Chile (Gana, 1988), assuring foreign mining com- panies of the virtual property of the mine and that events such as a new nationalization could not occur; clear indemnization criteria in case of future expropri- ation; stability of the rules due to the constitutional status of the law; freedom of companies in decisions regarding mine development and other business activities.

The opposition political parties to the military government in the early 1980s, which have been in power since 1990, were opposed to the Mining Law on the grounds that the country was relinquishing its rights to make mining policy, ie, to decide key aspects such as the rate of exploitation of resources, the terms for financing new investments, or the conditions to acquire new capital goods (Gana, 1988). The new mining law also was interpreted as not requiring foreign mining companies to give information to Cochilco, or to the Central Bank, so that these insti- tutions could fulfill their obligations to control the development of the sector as established previously by Decree Law 1 349. It was later evident that this was not the case.

This discussion, which was conducted publicly even though there was a military regime in place, was enhanced when the mining code, the statute which made possible the application of the Mining Law, came into being in December 1983. The National Committee for the Defense of Copper was created in order to prevent the promulgation of the code. This Committee was formed by well known personalities, and even by some retired armed forces high officers who saw the code as a threat to the country's sover- eignty. In a last attempt to stop the code the Commit- tee announced that a future government would modify the mining law, but in the end the Committee was not successful in stopping or even changing the content of the mining code. The government argued that the way the country would benefit from foreign mining investment was through the payment of taxes, and that the alternative social cost for the state to divert resources to mining investment was too high to be paid. The Minister of Mines Pinera ridiculed the claims of the opposition by labeling them the Com- mittee 'for Maintaining Copper Underground' (Economia y Sociedad, 1984).

With hindsight it can be said today that a clearer vision of the future was on the side of the military

government and not on the side of the opposition at the time. Since 1990 the two democratic Presidents (elected from the opposition political parties of 1982 who so much criticized this law) have applied the DL600 and the Mining Law of 1982 with enormous success from the point of view of achieving mining investment.

As an aside, liquid and gaseous hydrocarbons and lithium are outside the concessionable regime estab- lished in the Mining Law of 1982, having a special regime which will not be discussed here. For strategic reasons, the state has the first option to buy thorium and uranium deposit concessions, no matter who dis- covers them. Mine deposits that are under the sea are also excluded from the concession regime unless there is access to them via an underground tunnel which connects them to land. Clay, rocks and other construc- tion materials are also excluded from the mining con- cession regime.

The mining right is paid annually in advance in the month of March and has a fixed value of approxi- mately US$5.5/ha of the concession land, as calcu- lated in 1996. In some cases of non-metallic sub- stances the patent has a lower value (Anuario de la Mineria Chilena, 1994). For exploration concessions the value of the right is approximately US$8.3/ha. Rights paid up to 5 years before the exploitation begins are accepted as expenses and do not pay tax. Rights paid during the exploitation are accounted as a part of the tax that the company pays.

Taxes

The Chilean tax system classifies tax payers in differ- ent categories (Astorga, (1991, 1994)):

• The first category of tax is paid by all companies, Chilean or foreign, and is 15% of profits. All min- ing companies, including companies under the foreign investment statute, pay this tax according to their effective income unless they have sales of under approximately US$3.5 million per year. Min- ing companies that have sales under this amount pay tax according to the presumed income, which will not be discussed here. Artisan miners have a different tax regime which is effectively from 1 to 4% of the sales for copper, gold and silver and 2% for all other minerals. This tax is discounted from the sales of minerals that these micro companies make to either Enami or to other companies estab- lished to process minerals from artisan mining throughout the country.

• An additional tax of 20% is applied to dividends and profit withdrawals made by companies which are not included in the Foreign Investment Statute DL600, plus other exceptions established for Chi- lean companies. Thus Chilean companies or foreign companies which have chosen the general tax regime are subject a tax rate of 35% of which 15% is paid at the company level and 20% at the level of the shareholder.

61

Developing national mining policies in Chile: G Lagos

• A foreign company can choose to be within the general tax regime if it so wishes but the trend is for them to choose the fixed tax regime established by DL600, which is equal to 42%, and which was characterized in Section 3. 1. Lately, nevertheless, some 9 mining companies have switched to the general tax regime (El Mercurio, August, 1996). A foreign company which has chosen the fixed tax regime pays a total of 42% of which 15% is paid at the company level and 27% is paid for repatri- ation of profits. The latter can be distributed in divi- dends, invested or spent in other ways in the home country of the foreign company. This leads to dou- ble taxing except in the case of Argentina with which Chile has an agreement to avoid double tax- ing. In 1996 Chile discussed such agreements with a number of countries including the Netherlands, Switzerland, Canada, Italy, Germany and the US.

If a company has chosen the fixed tax regime, it can decide to be transferred to the general tax regime but it can do so only once.

Two types of depreciation regimes are shown in the following table, a normal one and an accelerated one. The latter can be chosen for goods that have at least a useful life of 5 years.

Depreciation Heavy mining equipment Installation costs 5 Construction of 25 permanent installations Construction of 10 temporal facilities Heavy trucks 7 Heavy tools 10 Light tools 5

Recovery period (yr) Normal Accelerated 10 3

Both tax regimes, the general and fixed, avoid double taxation within Chile.

It has been observed that ever since the DL600 began to operate and in spite of the large investment in mining and of the increasing mining exports, foreign companies have been paying less than the established 42%. In many cases this occurs because companies have recently started producing and thus they are depreciating their capital and also are paying a heavy load for their investment loans. It is known however that there are at least two ways in which foreign companies can legally pay less than the estab- lished 42% tax in the long run: the first one is when they have obtained loans from their own parent com- pany in the home country at interest rates higher than those existing in the market, and the second one is when they buy technology services abroad from par-

ent or related companies at prices also above the mar- ket and which are accounted for as expenses.

These may explain why the Foreign Investment Committee in 1995 changed the criteria regarding the relationship between equity and debt from 15 and 85%, respectively to 30 and 70%. This is not in any case a solution to by-passing tax payments but it is obviously more favourable for the country and it remains to be seen if this change will affect foreign investment in mining.

During the 1980s (Mineria y Desarrollo, 1989) there was a public discussion regarding this matter which did not lead to a change of the tax laws, which allow for these dealings. In 1996 this discussion began again, perhaps in a more justified way since the country should expect to appropriate the mining rent established in the tax regime, especially after such gigantic investment has taken place. In 1995 and for the first time since the nationalization of copper in 1971, private mining companies, including foreign ones, are producing more than the Codelco. Yet the effective tax proceeds from foreign private mining companies are estimated to be about one-tenth of what Codelco contributed this year which was US$1 700mill ion (El Mercurio, August, 1996). It should be added that this estimate is not realistic since Escondida alone paid US$160mill ion in taxes in 1995. Also the amount paid by Codelco includes not only taxes but also dividends, thus the two values are not strictly comparable. Although there may be dis- cussion about the numbers, it is evident that the main question is valid.

To conclude, it seems advisable that the Govern- ment have a serious look at this problem, seeking to correct inefficiencies of the tax system for all compa- nies, not only foreign ones. One seemingly undesir- able outcome of this pressure would be to increase taxes for foreign companies, leading not necessarily to greater returns for the country but surely affecting one of the key aspects of the Chilean foreign invest- ment model, its long term stability.

The environment

Due to the existing mining boom in Chile, what occurs in the mining environment is not only important for the country but may be crucial for the image of sustainability of the mining industry world- wide.

Mining is concentrated in the northern provinces of Chile, a desert zone where there is little agriculture and no forestry. The development of many of the towns and of some of the cities was based on mining, and most employment there is still related to this activity. Yet, mining directly occupies just over 1% of the 4.5 million total Chilean labour force. Mines, especially large ones are usually located in remote areas, either at high altitude in the Andes Mountains or in the middle of the desert. The environmental impacts of mining can be especially important at a local level, with the exception of the atmospheric pol-

62

Developing national mining policies in Chile: G Lagos

lution created by copper smelters, which by far rep- resents the most serious mining impact. It should be added, however, that numerous mining projects are being set up in remote but non-desert areas, and in those cases it is necessary to require additional safeg- uards to protect the natural, and in many cases fragile, environment. This is the case of mining projects situ- ated in the Andean altiplano (high plateau areas).

Recently there has been a stronger trend toward developing mining projects in the extreme south of Chile, in areas where not only is there considerable precipitation but which are located in places that have great tourism potential, added to a natural environ- ment that could be fragile. In these cases, the regional authorities are proving to be more stringent regarding environmental issues such as protecting the land- scape, building up a stock of topsoil for subsequent land recovery efforts, implementing modes of con- struction of installations and infrastructure aimed at minimizing the risk of water pollution, etc.

Despite mining's importance in the country, its environmental impacts come way behind other activi- ties or effects, such as desertification, erosion, urban growth and industrial pollution (Lagos, 1994a).

Article 19, amendment 8 of the Constitution of 1980, states that every citizen has "the right to live in an environment free of contamination. It is the state's obligation to ensure that this right is not violated and to look after the preservation of nature". However, although this declaration was regularly quoted, it had little practical effect during the 1980s. Public compa- nies were among the worst contaminators of the environment during the decade and little was done to change their behaviour by the institutions responsible. The National Commission for Ecology was created but without a budget and with little power it could do nothing but keep a handful of concerned people employed.

From the mid 1980s onwards, public awareness about environmental issues began to develop and legal demands, many of them invoking the relevant but non-enforced article in the constitution, were presented across the country: The workers of the Chu- quicamata mine brought a case against their company because of the emission of smelter gases; landlords in the valleys of Puchuncavi and Catemu brought cases against the owners of the nearby Ventanas and Chagres smelters; the citizens of Chanaral against Codelco because the tailings from Salvador's pro- cessing plant had caused a bank to build up in the bay; fruit producers against the Paipote smelter; the citizens of E1 Arrayan against Disputada mining com- pany because of the danger posed by the expected collapse of the Perez Caldera tailings dam; the olive growers of the Huasco county against Compania Minera del Pacifico, CMP, because emission of par- ticles had caused the olive trees to reduce their pro- duction. In most of these cases the plaintive was not successful. The Perez Caldera tailings dam was agreed to be evacuated following an out-of-court

settlement and there may have been other out of court settlements which were kept secret so as not to encourage other suits. In a few cases the courts did order that the companies install monitors to obtain records.

During the same period, an increasing awareness of the rapidly changing international trend emphas- ized the need for the country's most pressing environ- mental problems to be solved and forced changes in legislation and in policies. In the mining sector some public companies began to allocate funds to solve the most serious environmental problems but it was too little too late.

Environmental issues are a relatively recent con- cern in Chile. Since the middle 1980s there has been some environmental concern within the private and public sectors, but these concerns did not lead to actions or investments, until the 1960s. Environmen- tal guidelines for state owned companies, such as Codelco and Enami, were set out first in 1990 and only then was the environment taken into account when formulating corporate strategy. Though it was slow in taking any action, the public sector did not lag far behind Chile's private industry in demonstrat- ing its regard for the environment. The Chilean Manu- facturers Association, Sofofa, had produced its first environmental policy only the year before in 1989.

Environmental regulation. The National Commission for the Environment (Conama), created in 1990 but whose full powers came only in 1994 with the dic- tation of the environmental law, identified some 2200 environmental laws and regulations in existence in 1991-92. Most of these were out of date and were either not applied at all or their application was sub- ject to the individual decision of some official or regu- latory agency. Since 1990, the state has participated more actively in environmental affairs and the compa- nies are making extraordinary progress toward defin- ing environmental policies.

It can be said that the situation in the country has changed radically with regard to enforcement, although only a small number of decrees and laws concerning the environment have been enacted during the period 1990-96. The most important legislation passed are Decree 185 of the Ministry of Mining, which regulates fixed sources of air pollution; Decree 4 (1992) of the Ministry of Health regarding air pol- lution in the Metropolitan Region; the 'Ley de Bases del Medio Ambiente' , Law number 19 300 (1994), providing the framework for environmental legis- lation; and the Basel Convention (1992) on the con- trol of transfrontier movements of hazardous waste. Other environmental regulations have been updated.

Law 19 300 established the Environmental Impact Study System, EISS, administered by Conama. The EISS is governed by a Board involving most Minis- ters, recognizing that environmental problems con- cern all the spheres of society. Thus Conama does not control itself all aspects of the environment, leaving

63

Developing national mining policies in Chile: G Lagos

this function to the Ministries which have done so for many years. For instance the Ministry of Health has regulatory powers regarding human health, while the Ministry of Agriculture still has control over all aspects regarding agriculture. Because of this there is understandably substantial duplication of functions, overlapping between different Ministries, and occasionally, strong differences regarding how, when and how much to enforce. Conama is a growing agency, and in 1995 it had close to 200 personnel distributed throughout the country. Its budget was approximately US$15 million. It is estimated that in 1997 its budget should double due to the increasing requirements imposed by the full application of the EISS.

Environmental Impact Studies (EISs) are contrac- ted and paid by the company that intends to initiate a project with measurable environmental impacts. The EIS is carried out by an accredited institution, either a consulting company or a university, after the refer- ence terms have been defined by the Regional Environmental Committee, Corema. This committee is formed by all the environmental regulatory bodies of the Government at regional level, ie, the Ministry of Health, the Ministry of Mines, the Ministry of Pub- lic Works, the Ministry of Housing, the Ministry of Agriculture, etc. The President of the Corema is the Regional Authority of the Government and its sec- retary is the regional representative of Conama. In this way, if the EIS is approved, all the environmental per- mits of the different Ministries must be granted, thus constituting a single window system.

The results of the EIS are submitted to the Corema which has 120 days, extendible to approximately 180 days, to evaluate and approve or reject the EIS. If after the period aforementioned the Corema has not finalized the evaluation, then the EIS is considered approved. The evaluation process includes the partici- pation of the community and other stakeholders, and the reformulation, if required, of the Environmental Management Plan, EMP, that must be formulated in each EIS. The EMPs include aspects such as preven- tion, mitigation, waste management, monitoring and follow up procedures, emergency plans, decom- missioning and post decommissioning. EMPs also include new standards, when there are no established national standards for specific emissions or other environmental effects. EISs are preventive instru- ments but they do not include the creation of decom- missioning, post-commissioning or emergency funds at the start or during a project. Environmental insurance is not a compulsory feature of EISs.

One of the most important aspects of the progress that has been made since 1990, before Law 19 300 was even drafted, toward achieving compliance with environmental standards at an international level was the tacit, unwritten agreement that was reached between the government and companies that were starting up large projects involving industrial devel- opment and natural resources. In general terms, it was

agreed that the companies would submit to inter- nationally accepted standards to protect the environ- ment. In the majority of cases this resulted in the com- panies undertaking Environmental Impact Studies, even though they were not required by public policy at the time. These EISs were subsequently analyzed and sanctioned by the regional and central authorities at first, and by the Coremas after their creation in 1992. In the mining sector, most of the medium sized and large new projects started since 1990 have con- ducted EISs, which in most cases have been approved by the authority. As of 1995, the number of mining- related EISs was close to 50 (Ibacache, 1995), about one half of all the EISs carried out in the country.

These mining EISs have used stricter standards than those applied elsewhere in Chile and in many cases are not even regulated in the Chilean legislation. An example of this are the standards required at present of tailings dams, which go far beyond the obsolete Decree 86 (1970) of the Ministry of Mining. Other examples for which there are no regulations and standards in the Chilean legislation concern the qual- ity of waters that are discharged into the sea, plans regarding the abandonment and reclamation of mining sites, and comprehensive hazardous waste regu- lations.

Due to this voluntary EIS system the large new mining projects that have started up operations since 1990 have environmental standards in most aspects that are on a par with mining projects in the developed countries. The contribution of foreign companies toward introducing the most modern environmental technology in terms of equipment, processes and management into Chile, has been instrumental for the domestic companies of the sector, as it has enabled the transfer of those technologies within the country, to the benefit of the national mining sector (Lagos, 1996b).

The EIS voluntary system will change to the formal Environmental Impact Study System, EISS, as soon as the Statutes of the environmental law are approved by the government. It has taken close to 30 months since the dictation of Law 19 300 (in January 1994) to reach agreement within the government regarding the content of these Statutes. The main discussion regarding the Statutes concerns the criteria to dis- tinguish between projects which do not have environ- mental requirements in order to get started, from those that require either an EIS or an environmental report or declaration, EID. The latter is aimed at those pro- jects that cause minor environmental impacts. The EID consists of a report made by the company and filed by the authority without going through the EIS evaluation and acceptance procedure. EIDs are thus a self-regulatory instrument. The aim of the Statute in this regard is not to clutter Conama and the insti- tutional system with thousands of EISs, since this load could simply not be handled by the small number of trained personnel in the different agencies.

64

Developing national mining policies in Chile: G Lagos

Other concerns regarding the Statutes are (Garc 'a and Solari, 1995):

• The lack of explicit mechanisms to define the refer- ence terms for EIS, which could end up in a lack of flexibility, ie, authorities requiring unnecessary features for a particular EIS, or not requiring the needed features of an EIS.

• Insufficient mechanisms for public-community participation in the development of an EIS. In 1995-96 there were several instances of confron- tation between the community and the authority due to specific decisions of EIS. In many cases these matters were resolved by courts, but in one case this was not sufficient and a confrontation occurred between the police and the people of a small town close to the capital Santiago. Although these cases have not involved the mining industry so far, they highlight that the interpretation of Law 19 300 regarding community participation can be very lax, either meaning that the local authority can invite the community to fully participate in a particular EIS or can ignore it.

• Some key permits may be left out of the EISS due to the reluctance of the respective Ministry to include this permit in the system. This is a key aspect of the single window feature of the EISS. If an important permit such as the change of land use from agricultural to mining is left out of the EISS, it could mean that this single permit could decide the go ahead or rejection of a specific project, with- out a reference to the EIS and also within a differ- ent time schedule.

Thus the transition from the voluntary EIS to the for- mal EISS is crucial for Chilean mining. I f Law 19 300 is not modified to strengthen some of the weaknesses that have been highlighted, the EISS could collapse, as has virtually happened in Mexico. If, on the other hand, it is decided to modify Law 19 300, this would open all the environmental system for discussion, hardly what is recommended for a stable develop- ment.

Law 19 300 includes also some mechanisms to manage mining operations that existed at the time when the law was being written in the early 1990s, which shall be referred to in this paper as 'old ' oper- ations. Indeed it is in this segment of the mining sec- tor that some of the most serious environmental impacts occur. For instance, five of the seven Chilean copper smelters, all of them owned by state compa- nies, do not comply at present with Chile 's air quality standards established in Decree 185 (Lagos, 1996a). Four of these smelters - - Chuquicamata, Ventanas, Caletones and Paipote - - have decontamination plans, an instrument established in Law 19 300 and previously in Decree 185, whereby these smelters are pledged to installing gas fixing technologies that will signify compliance by 1999. The remaining Potrer- illos smelter does not have yet a decontamination plan and it is expected that it will have one in the next

few years. Possibly Caletones and Potrerillos will not comply with air quality standards until the first few years of the next decade.

Established decontamination plans do have their problems though. In May 1995 an air pollution epi- sode at Paipote, one of the smelters that belongs to Enami, was followed by demonstrations from groups of citizens from Copiapo, a neighbouring city. At first their petition was to close the smelter but when realiz- ation dawned that this would mean the loss of many jobs in the northern city of Copiapo, the community wanted the decontamination plan to go ahead of schedule. Nevertheless this plan could not be achi- eved ahead of schedule, but the smelter will make extra efforts in predicting atmospheric conditions that can lead to episodes and it will work at a reduced capacity during those periods where episodes are more likely to occur. This confrontation, which con- cluded successfully for Enami, is a result of decon- tamination plans being devoid of community partici- pation mechanisms.

Nevertheless many other aspects of the environ- mental management of these 'old ' operations are not included in Law 19 300. Thus for instance some of the largest copper mines in the world still do not have sanctioned hazardous waste management plans, or decommissioning and post decommissioning pro- cedures.