Developing markets for our metal - Oxford Platinum Lecture 2015

13

Developing markets for our metal Anglo American Platinum Oxford, 15 May 2015 Kleantha Pillay, Head of Market Development, Anglo American Platinum 1

-

Upload

anglo-american -

Category

Business

-

view

481 -

download

0

Transcript of Developing markets for our metal - Oxford Platinum Lecture 2015

Developing markets for our metal Anglo American Platinum Oxford, 15 May 2015

Kleantha Pillay, Head of Market Development, Anglo American Platinum

1

PLATINUM

CAUTIONARY STATEMENT

2

PLATINUM

Agenda

Anglo American Platinum and developing markets for our metal 1

3 Partnering for success: London Hydrogen Network Expansion Project

Supporting the adoption of fuel cell vehicles a priority 2

3

PLATINUM

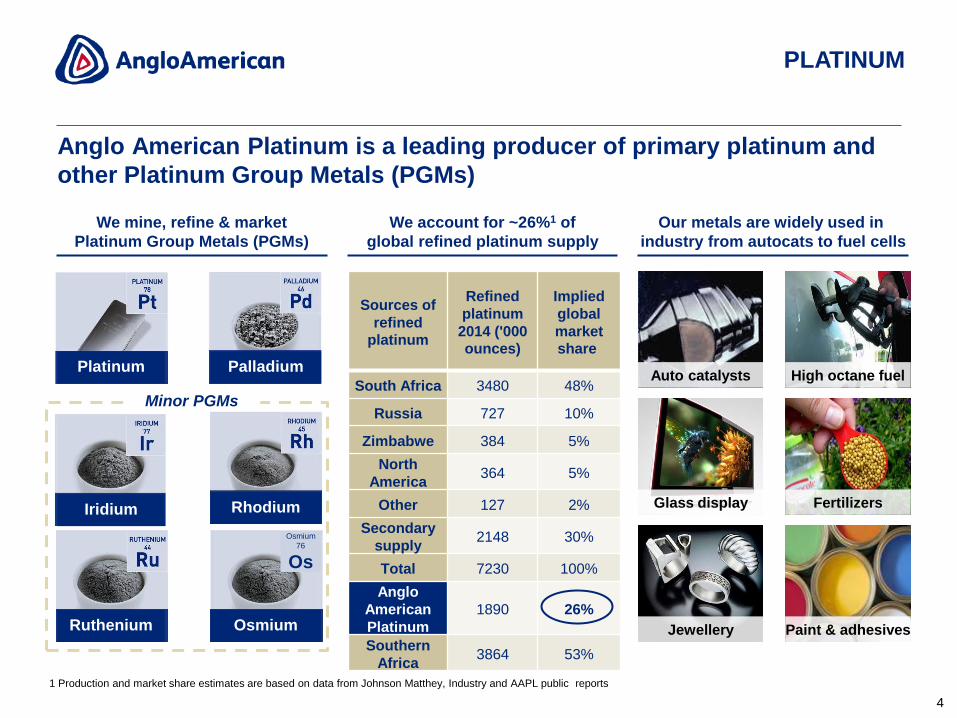

Anglo American Platinum is a leading producer of primary platinum and

other Platinum Group Metals (PGMs)

7%

63%

Minor PGMs

We mine, refine & market

Platinum Group Metals (PGMs)

We account for ~26%1 of

global refined platinum supply

Our metals are widely used in

industry from autocats to fuel cells

4

High octane fuel

Fertilizers

Paint & adhesives

Glass display

Auto catalysts

Jewellery

Platinum

Iridium

Ruthenium Osmium

Rhodium

Palladium

Osmium

76

Os

Sources of

refined

platinum

Refined

platinum

2014 ('000 ounces)

Implied

global

market share

South Africa 3480 48%

Russia 727 10%

Zimbabwe 384 5%

North

America 364 5%

Other 127 2%

Secondary

supply 2148 30%

Total 7230 100%

Anglo

American

Platinum

1890 26%

Southern

Africa 3864 53%

1 Production and market share estimates are based on data from Johnson Matthey, Industry and AAPL public reports

PLATINUM

New demand for PGMs is created through investment in research,

product development, commercialisation and marketing

Investment

model

Direct into

universities/

research facilities

Direct investment Equity investment Indirect investment and/or

advocacy programmes, leveraging

partners with similar interests

Profit pool

Example

Projects

FC : Fuel cell Co / Leveraged funding

FC mining

equipment

FC Rural

Electrification

5

Research Early stage

businesses

Mature

businesses

Product

development

FC Vehicle

We proactively develop markets for our metal,

investing in opportunities across product lifecycle & geography

Overview of our current portfolio

PLATINUM

Agenda

Anglo American Platinum and developing markets for our metal 1

3 Partnering for success: London Hydrogen Network Expansion Project

Supporting the adoption of fuel cell vehicles a priority 2

6

PLATINUM

Fuel cell electric vehicles offer the largest opportunity for Platinum

0

10

20

30

BEV GLDV (US) GLDV (EU) DLDV (US) DLDV (EU) FCEV

2011

2020

2025

Source: Platinum Group Metals for Light duty vehicle, US DOE, 2014

Fractions of Pt, Pd and Rh for US vehicles in 2020 and 2025 based on Tier 3 emissions standard and engine sizes of 2.5 & 2.2 litres respectively

Fractions of Pt, Pd and Rh for EU vehicles in 2020 and 2025 based on euro 6 adoption and engine sizes of 1.4 & 1.3 litres respectively

Grams PGM by powertrain for light duty vehicles

0

10

20

30

BEV GLDV (US) GLDV (EU) DLDV (US) DLDV (EU) FCEV

0

10

20

30

BEV GLDV (US) GLDV (EU) DLDV (US) DLDV (EU) FCEV

7

PLATINUM

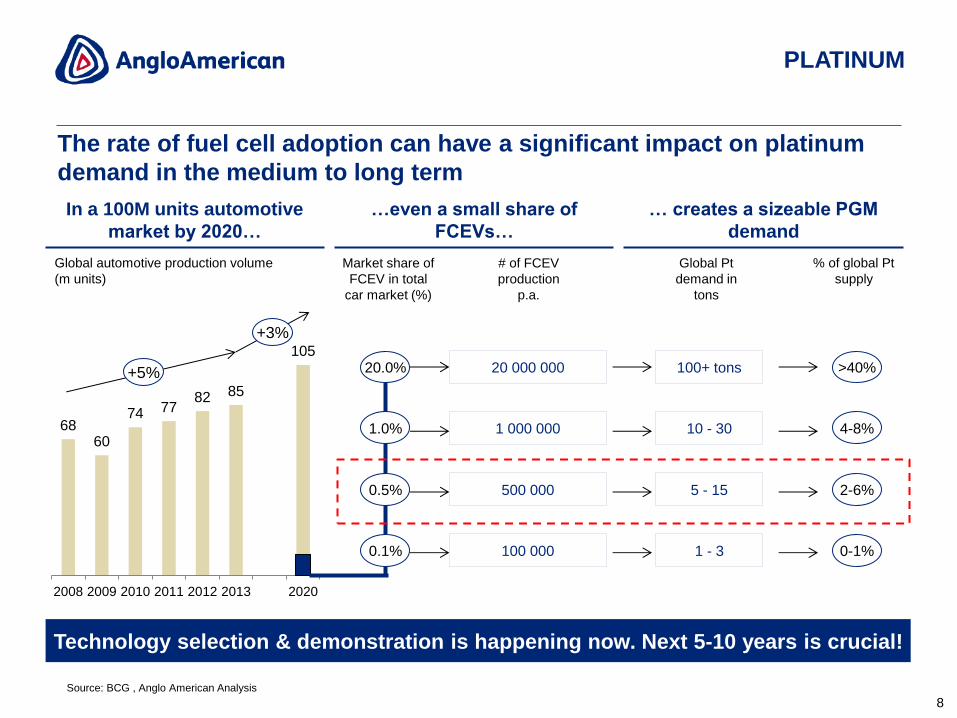

In a 100M units automotive

market by 2020…

…even a small share of

FCEVs…

… creates a sizeable PGM

demand

68 60

74 77 82 85

105

2008 2009 2010 2011 2012 2013 2020

Global automotive production volume

(m units)

+5%

+3%

20.0%

1.0%

0.5%

0.1%

Market share of

FCEV in total

car market (%)

20 000 000

1 000 000

500 000

100 000

Global Pt

demand in

tons

% of global Pt

supply

>40%

4-8%

2-6%

0-1%

# of FCEV

production

p.a.

100+ tons

10 - 30

5 - 15

1 - 3

Source: BCG , Anglo American Analysis

Technology selection & demonstration is happening now. Next 5-10 years is crucial!

The rate of fuel cell adoption can have a significant impact on platinum

demand in the medium to long term

8

PLATINUM

Agenda

Anglo American Platinum and developing markets for our metal 1

3 Partnering for success: London Hydrogen Network Expansion Project

Supporting the adoption of fuel cell vehicles a priority 2

9

PLATINUM

To be successful, fuel cell vehicles must overcome three main barriers

Cost competitiveness

1

Fuel cell applications must

achieve at least cost parity

when compared to competing

technologies

Infrastructure accessibility

3

Supporting infrastructure must

be accessible, convenient and

‘familiar’

Consumer acceptance

2

Consumer perception around

safety, and other technology

misconceptions must be

addressed

10

PLATINUM

Anglo American Platinum is partnering with and supporting companies

and programmes working to address these barriers

Cost competitiveness

1

Infrastructure accessibility

3

Consumer acceptance

2

The London Hydrogen Network Expansion Project (LHNE)

11

PLATINUM

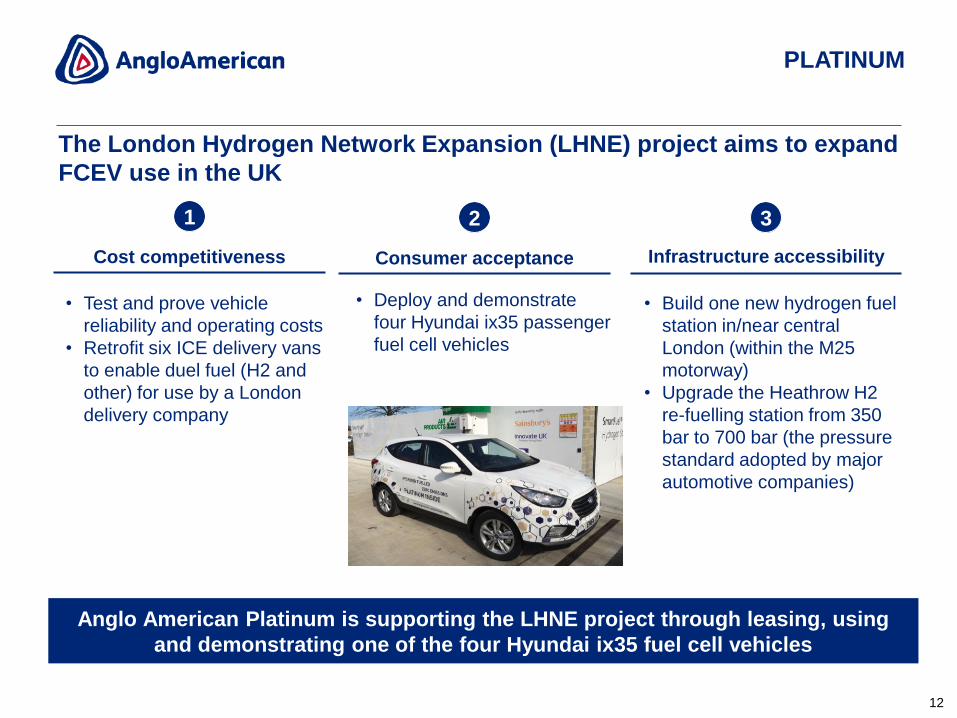

The London Hydrogen Network Expansion (LHNE) project aims to expand

FCEV use in the UK

Anglo American Platinum is supporting the LHNE project through leasing, using

and demonstrating one of the four Hyundai ix35 fuel cell vehicles

• Test and prove vehicle

reliability and operating costs

• Retrofit six ICE delivery vans

to enable duel fuel (H2 and

other) for use by a London

delivery company

• Deploy and demonstrate

four Hyundai ix35 passenger

fuel cell vehicles

• Build one new hydrogen fuel

station in/near central

London (within the M25

motorway)

• Upgrade the Heathrow H2

re-fuelling station from 350

bar to 700 bar (the pressure

standard adopted by major

automotive companies)

Cost competitiveness

1

Infrastructure accessibility

3

Consumer acceptance

2

12

PLATINUM

13

Innovative business models and leadership required to accelerate roll-out

of refuelling stations

Source: ITM Power

• California targeting 68 stations to support early

adopters (~20,000 FCEVs)

• Germany targeting 400 stations by 2023

• Hydrogen refuelling technology available

• Existing manufacturing partners and capabilities

• Retail & distribution partners available

• ‘First-mover’ disadvantage means that

innovative business models and leadership is

required

A small number of concentrated

stations is enough to support early markets