Determinants of Technological Progress: Recent Trends and...

60

105 Determinants of Technological Progress: Recent Trends and Prospects 3 As discussed in the previous chapter, the pace at which technologies spread between and within countries has picked up. As a result, most developing countries are narrowing the technological divide that separates them from high-income countries. Nevertheless, the tech- nology gap remains large; for many, including several low-income countries, it is widening rather than closing, in part because of the slowness with which technologies spread within countries. For virtually all developing countries, the domestic pace of technological progress is determined mainly by the speed with which already existing technologies are adopted, adapted, and successfully applied domestically, and done so throughout the economy, not just in the main cities. This chapter explores some of the major determinants of this kind of within-country diffusion of technology. It adopts an analyti- cal framework that distinguishes between the factors that dictate the extent to which an economy is exposed to external technologies on the one hand and the efficiency with which it absorbs them on the other hand. Among the most important channels through which low- and middle-income countries are exposed to foreign technologies are trade; foreign direct investment (FDI); and contacts with highly skilled diaspora members (nationals working abroad) and with other information net- works, including those of academia and the media. Maintaining an open environment to such flows is critical for accessing technology at least cost. However, no matter how com- pellingly useful a technology may be, the process by which it spreads within a country can be lengthy. The speed with which a country absorbs and adopts technology depends on many fac- tors, including the extent to which a country has a technologically literate workforce and a highly skilled elite; promotes an investment climate that encourages investment and per- mits the creation and expansion of firms using higher-technology processes; permits access to capital; and has adequate public sec- tor institutions to promote the diffusion of critical technologies where private demand or market forces are inadequate. The process of technology absorption is also subject to virtuous circles. Scale economies in technologically sophisticated sectors and in learning by doing tend to make the acquisition of technology a nonlinear process, character- ized initially by slow penetration until some threshold is reached, followed by a period of rapid acceleration, and finally by a period of slower diffusion as saturation is achieved. As a consequence, while gaps in technological achievement create opportunities for acceler- ated growth and convergence in lagging economies, they can also lead to divergence if the conditions for technology adoption in lagging countries are insufficient. Many tech- nologies operate synergistically to reinforce the demand for each other and the effective- ness and capacity of supply.

Transcript of Determinants of Technological Progress: Recent Trends and...

105

Determinants of TechnologicalProgress: Recent Trends andProspects

3

As discussed in the previous chapter, the paceat which technologies spread between andwithin countries has picked up. As a result,most developing countries are narrowing thetechnological divide that separates them fromhigh-income countries. Nevertheless, the tech-nology gap remains large; for many, includingseveral low-income countries, it is wideningrather than closing, in part because of theslowness with which technologies spreadwithin countries. For virtually all developingcountries, the domestic pace of technologicalprogress is determined mainly by the speedwith which already existing technologies areadopted, adapted, and successfully applieddomestically, and done so throughout theeconomy, not just in the main cities.

This chapter explores some of the majordeterminants of this kind of within-countrydiffusion of technology. It adopts an analyti-cal framework that distinguishes between thefactors that dictate the extent to which aneconomy is exposed to external technologieson the one hand and the efficiency with whichit absorbs them on the other hand. Among themost important channels through which low-and middle-income countries are exposed toforeign technologies are trade; foreign directinvestment (FDI); and contacts with highlyskilled diaspora members (nationals workingabroad) and with other information net-works, including those of academia and themedia. Maintaining an open environment tosuch flows is critical for accessing technology

at least cost. However, no matter how com-pellingly useful a technology may be, theprocess by which it spreads within a countrycan be lengthy.

The speed with which a country absorbsand adopts technology depends on many fac-tors, including the extent to which a countryhas a technologically literate workforce and ahighly skilled elite; promotes an investmentclimate that encourages investment and per-mits the creation and expansion of firmsusing higher-technology processes; permitsaccess to capital; and has adequate public sec-tor institutions to promote the diffusion ofcritical technologies where private demand ormarket forces are inadequate.

The process of technology absorption is alsosubject to virtuous circles. Scale economiesin technologically sophisticated sectors and inlearning by doing tend to make the acquisitionof technology a nonlinear process, character-ized initially by slow penetration until somethreshold is reached, followed by a period ofrapid acceleration, and finally by a period ofslower diffusion as saturation is achieved. Asa consequence, while gaps in technologicalachievement create opportunities for acceler-ated growth and convergence in laggingeconomies, they can also lead to divergence ifthe conditions for technology adoption inlagging countries are insufficient. Many tech-nologies operate synergistically to reinforcethe demand for each other and the effective-ness and capacity of supply.

Although the process of technological dif-fusion has a clear logic, the process is by nomeans mechanical. It occurs through interac-tions among individuals, entrepreneurs, firms,and governments. The role of government isboth direct, as a supplier of many technologi-cal services, and indirect. In particular, theefficiency with which firms can diffuse tech-nology within the domestic economy dependson the overall political and economic context,the level and distribution of human capital,the quality of the macroeconomic environ-ment, and the rules and regulations governingthe conduct of business, all of which are heav-ily influenced by governments.

This chapter discusses the principal chan-nels through which developing countries areexposed to advanced technology, analyzes themain determinants of domestic absorptivecapacity, and indicates likely future trends intechnological diffusion. The following sixmain messages emerge from this analysis.

The principal channels by whichdeveloping countries are exposed toexternal technology—which includetrade, FDI, and a highly skilled dias-pora—have increased substantially overthe past several decades. The share ofimported high-tech products in grossdomestic product (GDP) has risen bymore than half in both low- and middle-income regions since the mid-1990s,that of imports of capital goods by 37percent, that of imports of intermediategoods by 26 percent, and that of FDI in-flows by sixfold since the 1980s. Finally,the size and sophistication of global di-asporas has increased markedly, alongwith substantial improvements in thetechnology by which migrants can trans-mit their know-how and interact withtheir home economies.

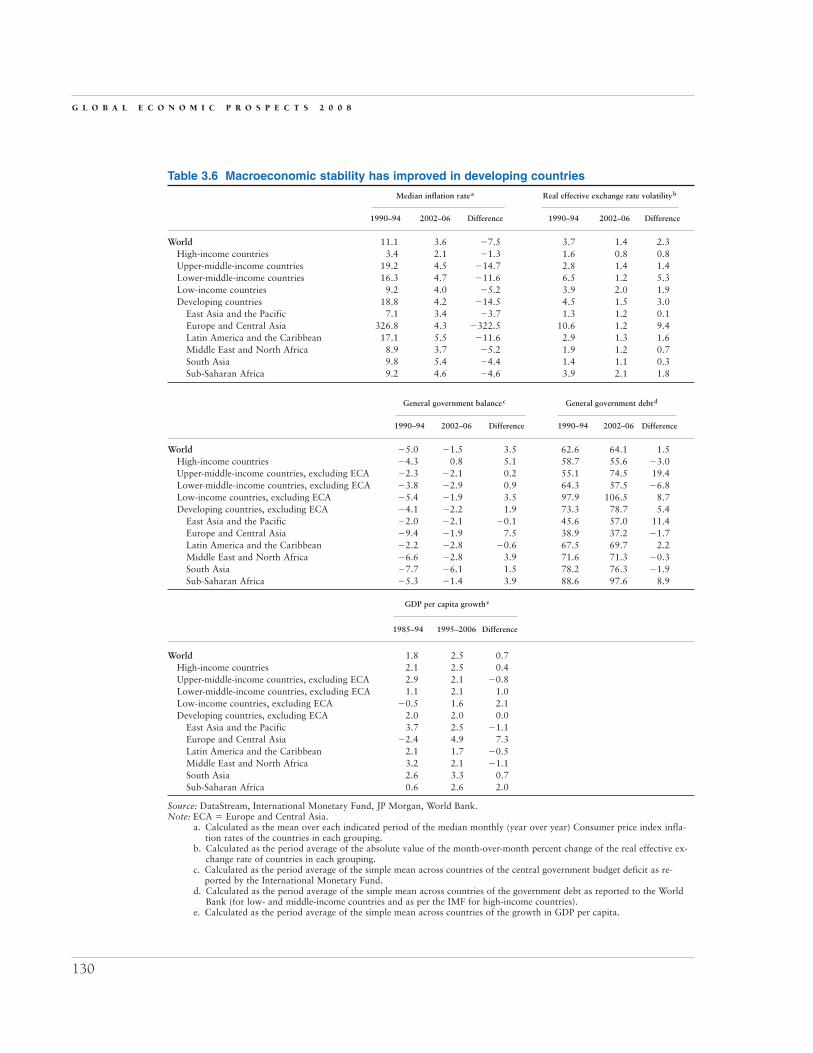

The ability to absorb foreign technol-ogy, which depends on domestic policiesand institutions, has also improved inmany developing countries. Reflectingrising school enrollment, literacy rates inlow-income countries have increased

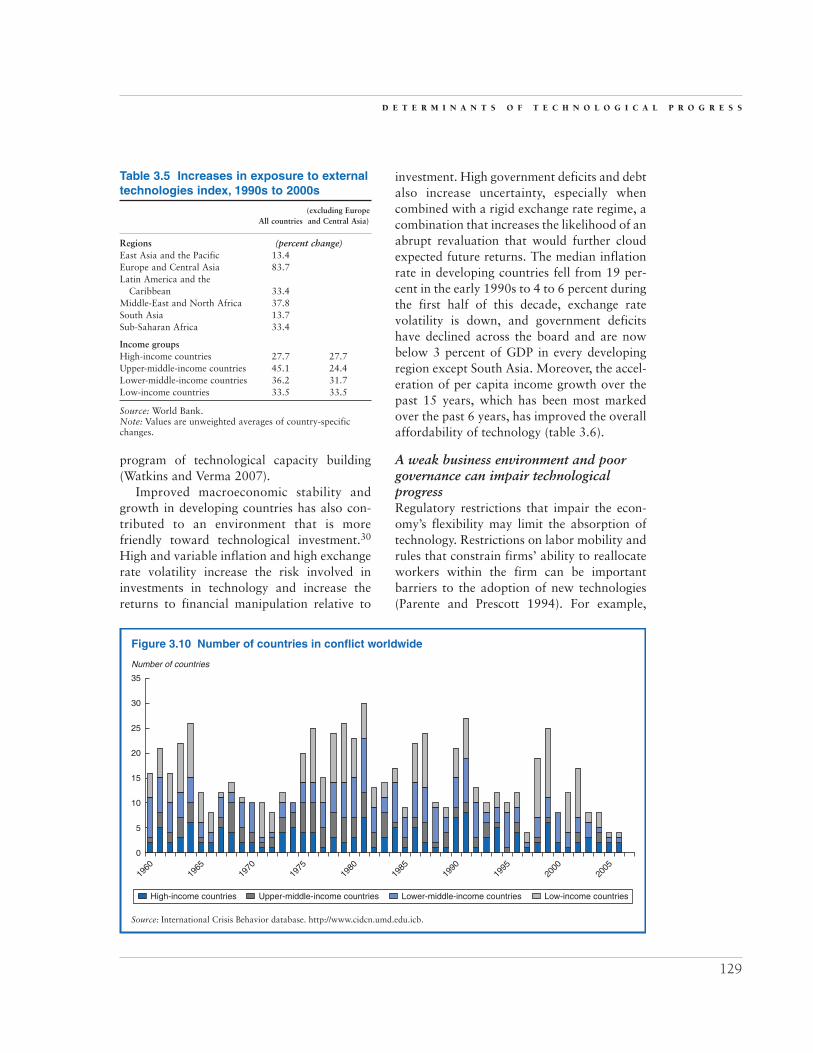

from less than 50 percent in 1990 tomore than 62 percent, and among youththey now exceed 74 percent. In addition,the macroeconomic, governance, and in-vestment climate that innovative firmsand entrepreneurs need to operate is im-proving. More countries are operatingin a context of close to stable prices (me-dian inflation in low-income countriesdeclined from 9.2 to 4.2 percent be-tween 1990 and 2006) and flexible ex-change rate regimes, while governmentfinances are better balanced.

Technological diffusion amongmiddle-income countries has benefitedfrom the reorientation of global produc-tion processes. Advances in communica-tions and transport technology havegiven rise to the growth of global pro-duction networks, facilitating increasedtrade and technological advances inmany developing countries, particularlymiddle-income developing countries.Until recently, low wages and a solid, iflow, level of basic technological literacyhave been sufficient to capture a signifi-cant role in global networks in manycountries. As wages rise, however, thesecountries will need to make substantialadditional investments in human capitalto maintain their share of global produc-tion and continue the technological con-vergence of the past few years. They willalso need to adopt a more proactive ap-proach to developing local competenciesand to using research and development(R&D) and outreach programs to bol-ster the diffusion process.

For low-income countries, poor tech-nological adaptive capacity and limiteddissemination of often simple technolo-gies to the countryside are severely con-straining technological progress. Despiteprogress in basic technological literacy,extremely low levels of income, weakgovernance structures, and, in somecases, ongoing conflict continue tostymie the ability of low-income, and

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

106

especially Sub-Saharan African, coun-tries to obtain and absorb new tech-nologies. Nevertheless, the potential fortechnological progress through thegreater dissemination of relatively sim-ple technologies is huge.

The absence or low quality of somebasic technologies that governments his-torically provide hinders technologicaldiffusion by the private sector. Thesebasic technologies often represent essen-tial complementary technologies whoseabsence can prevent the successful adop-tion of a new-to-the-market technology.

The relatively rapid disseminationof new communications technologiesthroughout the developing world, in-cluding in low-income countries, offersa ray of hope. These potentially trans-formational technologies are enabling,often for the first time, the kinds ofarm’s-length transactions that may becritical to firm development and thespread of technology in these countries.New technologies are frequently intro-duced and promoted by members ofnational diasporas, both directly throughnetworks and indirectly through invest-ments financed from remittances.

The rest of this chapter is devoted toexploring how developing countries absorbexternal technology. The next section presentsan analytical framework for technologicalprogress. This is followed by a discussion ofhow trade, FDI, and migration expose coun-tries to new technologies and can promote in-ternal diffusion of those technologies. The sec-tion also discusses trends in these flows andthe potential magnitude of associated techno-logical progress and how this may havechanged over time. The chapter then turns toan analysis of the domestic factors that facili-tate the absorption of new technologies. Thissection first examines how government poli-cies, and the business environment in general,facilitate the creation and expansion of innova-tive firms. It then looks at how levels of humancapital—from literacy rates to R&D capacity—

affect countries’ ability to absorb technologyfrom abroad. The chapter concludes with aspeculative view of the prospects for technolog-ical progress and some policy messages.

Drivers of technologicalprogress: A framework

The process by which countries adopt,adapt, and absorb external technologies is

complicated. The overall framework followedin this chapter (depicted in figure 3.1) draws onprevious work done at the World Bank, in par-ticular, the 1998 World Development Reporton the knowledge economy (World Bank 1998)and several regional and country-specific policyanalyses of technology and technological com-petencies. In addition, it relies upon the acade-mic literature on technology diffusion, includ-ing an excellent review article by Keller (2004);several articles by Coe and Helpman concern-ing the role of FDI; case studies of the processof technology diffusion by Chandra andKolavalli (2006); empirical work on the tech-nological influence of imports by Lumenga-Neso, Olarreaga, and Schiff (2005); and thediscussion by Rodrik (2004) on the impact ofmarket failures on innovation incentives.

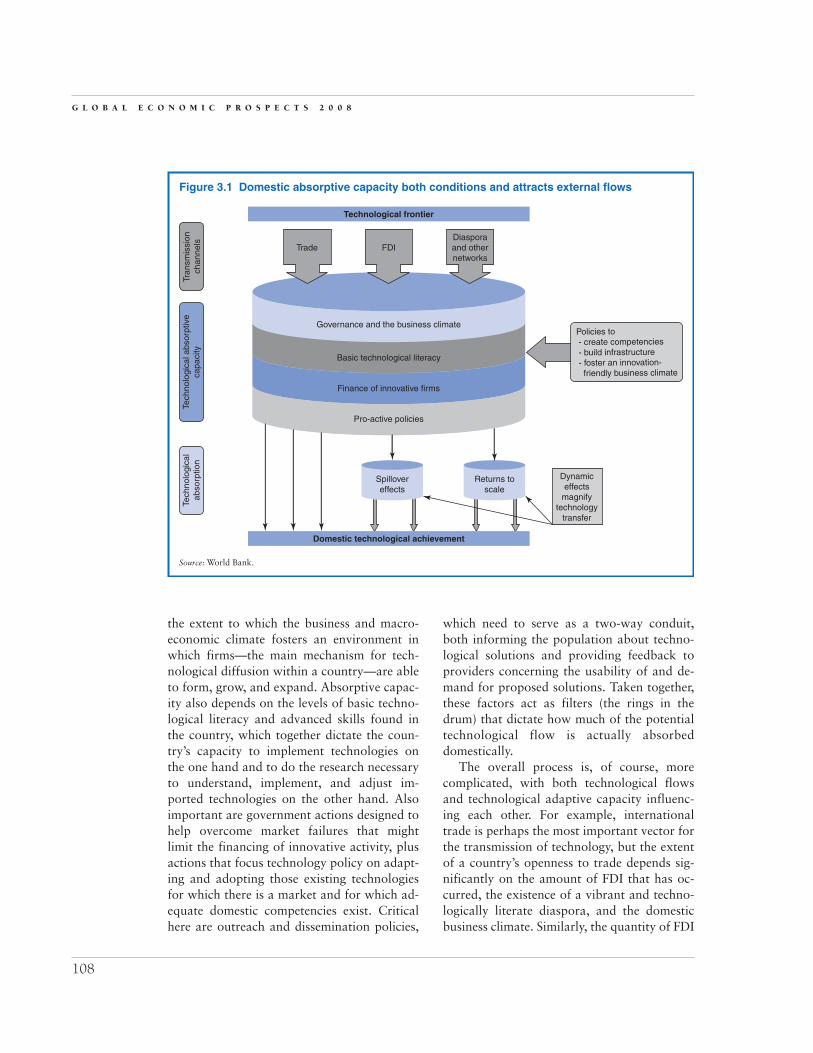

Exposure to external flows interacts with domestic capacity to diffusetechnologyFor the purposes of analytical simplicity, theframework presents technological progressin developing countries as a process wherebyan economy is exposed to higher-technologybusiness processes, products, and servicesthrough foreign trade; FDI; and contacts withits diaspora and other communication chan-nels, including academic and international or-ganizations (the large arrows at the top of thefigure). Exposure to new ideas and techniquesis, however, not sufficient to ensure techno-logical progress on the ground. The extent towhich these flows are translated into techno-logical progress depends on the technical ab-sorptive capacity of the economy (representedby the ringed drum). This in turn depends on

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

107

the extent to which the business and macro-economic climate fosters an environment inwhich firms—the main mechanism for tech-nological diffusion within a country—are ableto form, grow, and expand. Absorptive capac-ity also depends on the levels of basic techno-logical literacy and advanced skills found inthe country, which together dictate the coun-try’s capacity to implement technologies onthe one hand and to do the research necessaryto understand, implement, and adjust im-ported technologies on the other hand. Alsoimportant are government actions designed tohelp overcome market failures that mightlimit the financing of innovative activity, plusactions that focus technology policy on adapt-ing and adopting those existing technologiesfor which there is a market and for which ad-equate domestic competencies exist. Criticalhere are outreach and dissemination policies,

which need to serve as a two-way conduit,both informing the population about techno-logical solutions and providing feedback toproviders concerning the usability of and de-mand for proposed solutions. Taken together,these factors act as filters (the rings in thedrum) that dictate how much of the potentialtechnological flow is actually absorbeddomestically.

The overall process is, of course, morecomplicated, with both technological flowsand technological adaptive capacity influenc-ing each other. For example, internationaltrade is perhaps the most important vector forthe transmission of technology, but the extentof a country’s openness to trade depends sig-nificantly on the amount of FDI that has oc-curred, the existence of a vibrant and techno-logically literate diaspora, and the domesticbusiness climate. Similarly, the quantity of FDI

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

108

Returns toscale

Spillovereffects

Pro-active policies

Finance of innovative firms

Basic technological literacy

Governance and the business climate

Source: World Bank.

Figure 3.1 Domestic absorptive capacity both conditions and attracts external flows

Technological frontier

Domestic technological achievement

Tech

nolo

gica

lab

sorp

tion

Dynamiceffects

magnifytechnology

transfer

Diasporaand othernetworks

FDITrade

Tran

smis

sion

chan

nels

Tech

nolo

gica

l abs

orpt

ive

capa

city

Policies to - create competencies - build infrastructure - foster an innovation- friendly business climate

and its overall effectiveness depends on thequality and technological literacy of the laborforce.

Increasing returns and spillover effectscan magnify these effects . . .Both domestic and external determinants oftechnological transfer are affected to varyingdegrees by increasing returns to scale andspillover effects that can magnify the absorp-tive impact of these flows. Access to foreignmarkets may allow domestic firms to grow andexploit economies of scale associated withsome technologies, raising the overall wealthand technological sophistication of an econ-omy. Meanwhile, the technological spilloversthat can be expected from FDI, includingdemonstration effects and the transfer of busi-ness process and human capital to domesticfirms through employee turnover, are likely tobe greater the more qualified is the labor force.Both FDI and trade can contribute to clustereffects and networking externalities that in-crease the potential for spillovers and to tech-nological diffusion from individual sectors andfirms to the rest of the economy. Alternatively,economies of scale and agglomeration effectsmay prevent entry by new firms in some mar-kets, cutting off otherwise promising opportu-nities for technological learning. In addition,imitators may limit entrepreneurs’ ability tocapture the returns to new-to-the-marketinnovations, thereby reducing incentives fortechnological progress.

. . . but a lack of financing can stymieinnovation Affordability issues can influence both the sizeof initial inflows and a country’s technologicalabsorptive capacity. Even if profitable invest-ments in technology are available and the do-mestic environment encourages the absorptionof new technologies, low incomes may makenew technologies unaffordable to individualsand firms in developing countries. At the ex-treme, individuals near subsistence levels maybe unwilling to risk adopting a new-to-the-market technique, may be unable to generate

adequate savings to invest in a new technol-ogy, or may lack the collateral required to bor-row. Thus poverty is a major cause, as well asa result, of low levels of technology.

Affordability is also an issue at the macrolevel. Low incomes constrain government fi-nance, limiting the government’s capacity toput into place both the level of physical infra-structure and the investments necessary todevelop a level of domestic human capitalcapable of supporting and exploiting evensimple technologies.

Policy should not impede innovative firmsFinally, firms, entrepreneurship, and govern-ment action that actively supports the diffu-sion of economically relevant and profitabletechnologies are the grassroots mechanisms bywhich technologies diffuse within countries.Firms must be able, and entrepreneurs permit-ted, to profit from the exploitation of new-to-the-market-technologies if those technologiesand products are to diffuse. This means thatpolicy must be welcoming of such profits andthat both R&D and dissemination efforts notonly need to focus on creating or adaptingproducts and ideas (domestic or foreign) tothe local market, but also must give priority toassisting firms to exploit them.

External transmission channels

This section presents data and describes re-cent trends concerning the external chan-

nels through which developing countries areexposed to foreign technologies. Where rele-vant, it also draws on the literature to com-ment on how specific elements in a country’stechnological absorptive capacity (discussed inmore detail later in this chapter) interact withthese external flows to determine the extent towhich these channels translate into technolog-ical achievement.

TradeTrade is one of the most important mechanismsby which embodied technological knowledge(in the form of both capital and intermediate

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

109

goods and services) is transferred across coun-tries. Imports of technologically sophisticatedgoods help developing countries raise the qual-ity of their own products and the efficiencywith which they are produced. Countries canalso absorb new technology by exporting tocustomers who implicitly or explicitly provideguidance in meeting the specifications requiredfor access to global markets. For developingcountries with low R&D intensity, trade open-ness and exposure to foreign competitionprovide powerful inducements to adopt moreadvanced technology in both exporting andimport-competing firms and are likely to pro-duce large technology spillovers and produc-tivity gains (Schiff and Wang 2006a).

However, the extent to which exposure toforeign technologies is reflected in the exportand import patterns of individual countriesdepends on, among other things, the absorp-tive capacity of individual countries. As Soub-botina (2006) discusses, countries with rela-tively weak domestic scientific capacities tendto follow a more passive approach to technol-ogy absorption that is characterized by limitedefforts to leverage the technology imported byforeign firms operating on their soil. For thesecountries, most technology transfers takeplace either through imports of high-techgoods, or perhaps through an apparentlyhigh-tech export sector that is, in reality, dom-inated by assembly operations associated withelevated imports of high-tech goods. Wheresophisticated domestic capacities coexist witha significant degree of basic technological lit-eracy in the population, technology diffusionis enhanced and, in general, the technologicalcontent of exports is higher.

Following Soubbotina (2006) classifica-tions, “traditionalist slow learners,” such asBangladesh and Burkina Faso, which have lowlevels of technological competency and tech-nological literacy, tend to rely to a large extenton imports of machinery and equipment.Other countries, such as Malaysia, Mexico,and the Philippines, appear to follow a “pas-sive FDI-dependent” learning style. For thesecountries, the share of high- and medium-tech

goods in their manufactured exports is higherthan these goods’ share in manufacturingvalue added, reflecting the dependence oftheir high-tech exports on imports of techno-logically sophisticated components and therelatively low technological complexity ofdomestic manufacturing operations. By con-trast, “active FDI-dependent” countries, suchas Chile and Hungary, strike a better balancebetween the share of high-tech goods and ser-vices in overall exports and domestic valueadded, reflecting greater domestic technologi-cal competencies. For the Russian Federationand some of the other countries that belongedto the former Soviet Union, a strong techno-logical base and relatively low import sharesof high-tech goods reflect their more advancedlearning style, which places greater emphasison domestically developed technologies.Nevertheless, these technologies mainly feedinto products that serve the local market,because both high costs and quality concernskeep these sectors from being internationallycompetitive.

The potential for technology transferthrough imports has risenImports improve domestic technology becauseembodied technology both allows firms to em-ploy more efficient production processes andaffords the possibility that firms can copymore advanced products and processes. At thesame time, competition from technologicallysuperior imports may boost domestic produc-tivity.1 Developing countries that have a largeshare of imports from high-income countrieswith large R&D expenditures have signifi-cantly higher productivity than developingcountries that import from advanced coun-tries with lower R&D expenditures (Coe,Helpman, and Hoffmaister 1997).2 There alsois evidence for a positive relationship betweenaccess to imported intermediate goods andperformance (Handoussa, Nishimizu, andPage 1986). More recent literature highlightsthe indirect benefits for developing countriesfrom North–North trade in R&D. The ex-change of high-tech goods and services among

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

110

high-income economies contributes to an in-crease in the global stock of knowledge andeventually becomes available to developingcountries through North–South trade. Finally,technology diffusion, like trade, tends to be re-gional, with the largest transfers coming fromnatural trading partners, for example, Jordanbenefits more from the European Union andMexico benefits from Canada and the UnitedStates (Schiff and Wang 2006b).

However, the extent to which importedtechnology boosts the sophistication of do-mestic technological activity either directly orindirectly through spillovers depends on thequality of a country’s technological absorptivecapacity. Thus while using an imported capitalgood can lift the technological content of ac-tivity in a country, to the extent that importerspay competitive prices for the technology,there may be no net gain to the country (Eatonand Kortum 2001). Moreover, the businessclimate may be too weak or the technologicalliteracy of the local labor force may be toolow to successfully adapt the machinery tolocal conditions (Dahlman, Ross-Larson, andWestphal 1987; Rosenberg 1976). As a result,the country may not realize the potential pro-ductivity improvements available from im-ported technology (Pack 2006).

Developing countries’ high-tech importshave increasedTo the extent that a developing country canmake use of or imitate sophisticated goods, itslevel of technological achievement should in-crease in line with the quality and technologicalsophistication of imported goods. Since the mid-1990s, the share of imported high-tech productsinGDPhas increasedbymore than50 percent inlow-income countries and by 70 percent in mid-dle-income countries (table 3.1).3 Among devel-oping regions, East Asia and the Pacific hasthe highest share of high-tech imports in GDP(8.4 percent), with the highest share being forMalaysia (37 percent) and the Philippines(18 percent), but Europe and Central Asia hasexperienced the largest increase, reflecting thetransition of many of the region’s countries tomarket economies and their improved access tohigh-tech products following the relaxation ofCold War export restrictions. Among regionsdominated by middle-income countries, high-tech imports represent 3.8 percent of GDP inLatin America and the Caribbean and 3.6 per-centofGDPintheMiddleEastandNorthAfrica,less than in Sub-Saharan Africa (4.5 percent).

Low-income countries have also improvedtheir exposure to high-technology embeddedin foreign products. After hovering around

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

111

Table 3.1 Trade in technology goods has increased in developing countries

Share of high-tech exports Imports of high-tech goods Imports of capital goods in world high-tech exports

1994–96 2002–04 % change 1994–96 2002–04 % change 1994–96 2002–04 % change

(% of GDP) (% of GDP) (% of GDP)

RegionsEast Asia and the Pacific 5.9 8.4 42 11.6 12.8 10 9.9 19.0 93Europe and Central Asia 3.2 7.2 125 7.1 14.7 107 1.0 2.7 163Latin America

and the Caribbean 2.4 3.8 61 5.4 7.2 32 2.1 3.4 61Middle East and North Africa 2.5 3.6 44 6.3 8.9 42 0.1 0.2 29South Asia 1.4 2.1 53 3.1 3.8 22 0.2 0.3 58Sub-Saharan Africa 3.2 4.5 39 9.3 10.5 14 0.1 0.1 4

Income groupsHigh-income countries 3.4 4.7 38 5.5 7.0 27 86.5 74.3 �14Upper-middle-income countries 4.2 7.2 71 8.7 13.1 51 6.6 9.6 47Lower-middle-income countries 3.2 5.4 70 6.9 9.2 33 6.7 15.7 137Low-income countries 1.8 2.7 53 4.9 5.7 17 0.3 0.4 53

Source: World Bank calculations using Centre d’Etudes Prospectives et d’Informations Internationales’ database, Banque Analytiquede Commerce International.

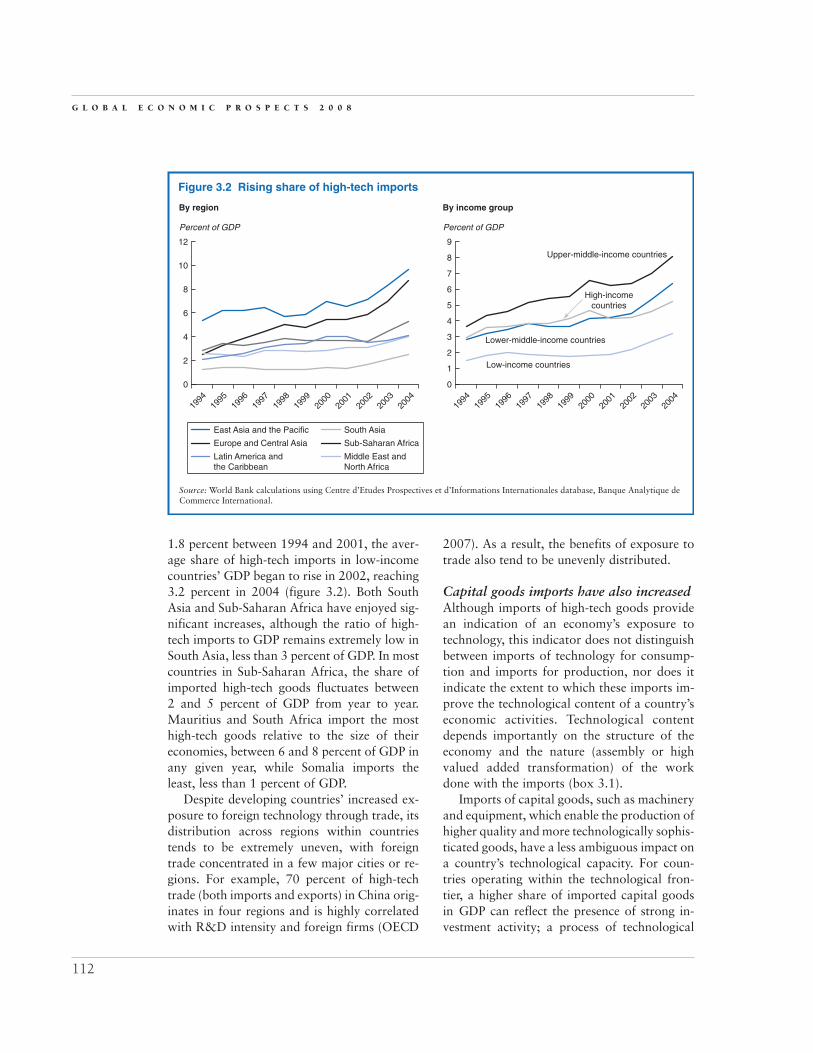

1.8 percent between 1994 and 2001, the aver-age share of high-tech imports in low-incomecountries’ GDP began to rise in 2002, reaching3.2 percent in 2004 (figure 3.2). Both SouthAsia and Sub-Saharan Africa have enjoyed sig-nificant increases, although the ratio of high-tech imports to GDP remains extremely low inSouth Asia, less than 3 percent of GDP. In mostcountries in Sub-Saharan Africa, the share ofimported high-tech goods fluctuates between2 and 5 percent of GDP from year to year.Mauritius and South Africa import the mosthigh-tech goods relative to the size of theireconomies, between 6 and 8 percent of GDP inany given year, while Somalia imports theleast, less than 1 percent of GDP.

Despite developing countries’ increased ex-posure to foreign technology through trade, itsdistribution across regions within countriestends to be extremely uneven, with foreigntrade concentrated in a few major cities or re-gions. For example, 70 percent of high-techtrade (both imports and exports) in China orig-inates in four regions and is highly correlatedwith R&D intensity and foreign firms (OECD

2007). As a result, the benefits of exposure totrade also tend to be unevenly distributed.

Capital goods imports have also increasedAlthough imports of high-tech goods providean indication of an economy’s exposure totechnology, this indicator does not distinguishbetween imports of technology for consump-tion and imports for production, nor does itindicate the extent to which these imports im-prove the technological content of a country’seconomic activities. Technological contentdepends importantly on the structure of theeconomy and the nature (assembly or highvalued added transformation) of the workdone with the imports (box 3.1).

Imports of capital goods, such as machineryand equipment, which enable the production ofhigher quality and more technologically sophis-ticated goods, have a less ambiguous impact ona country’s technological capacity. For coun-tries operating within the technological fron-tier, a higher share of imported capital goodsin GDP can reflect the presence of strong in-vestment activity; a process of technological

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

112

Figure 3.2 Rising share of high-tech imports

Percent of GDP

Source: World Bank calculations using Centre d’Etudes Prospectives et d’Informations Internationales database, Banque Analytique deCommerce International.

0

2

12

4

10

8

6

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

By region

1994

Percent of GDP

0

1

9

2

6

4

3

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

8

7

5

By income group

1994

Upper-middle-income countries

Low-income countries

Lower-middle-income countries

High-incomecountries

East Asia and the Pacific

Europe and Central Asia Sub-Saharan Africa

Middle East andNorth Africa

Latin America andthe Caribbean

South Asia

upgrading; and, over the longer term, arelatively sophisticated structure of produc-tion.4 As a result, relatively technologically so-phisticated middle-income countries importmore capital goods (as a share of GDP) than lesssophisticated low-income countries (table 3.1).

Overall, the share of capital goods in theGDP of developing countries has risen substan-tially over the past decade. Upper-middle-income countries saw a 51 percent increase inthe share of these goods in GDP, while lower-middle-income countries have boosted their re-liance on such goods by 33 percent. The formergroup of countries continues to have the largestshare of capital goods in GDP, about 13 per-cent, more than double the share of low-income countries. As a consequence, the gapbetween low-income countries (especially theLeast Developed Countries [UNCTAD 2007])and other developing countries has widened.Europe and Central Asia saw the biggest re-gional increase in imports of capital goods,reflecting the substantial economic recovery inthese countries following the recession that ac-companied the transition to market economies.As was the case for high-tech imports, SouthAsia has the lowest level of imports of capitalgoods and has shown little improvement,

presumably reflecting the relatively autarchicpolicies that governments in the region havefollowed until recently. By contrast, Sub-Saha-ran Africa imports substantially more capitalgoods, although the ratio of capital goods im-ports to GDP has increased less than in otherdeveloping regions since the mid-1990s, withthe exception of East Asia and the Pacific. Thestory is particularly varied in Latin America,where some countries, such as Costa Rica andMexico, increased their imports of capitalgoods following liberalization policies in theearly 1990s, while others did not. The increasein the share of capital goods in GDP was par-ticularly notable in Costa Rica, where it rosefrom about 7 percent in the mid-1990s to about18 percent in 2002–04.

Exports of technological goods have also expandedParticipation in high-tech export markets hasalso been identified as a channel through whichtechnology is diffused within developing coun-tries. Many case studies suggest that exportingfirms in developing countries benefit from im-plicit and explicit technological transfers thatoccur as a result of their interactions with for-eign buyers. Benefits accrue because foreign

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

113

Based on a breakdown of trade flows by technol-ogy level and by production stage, Lemoine and

Ünal-Kesenci (2003) highlight the following divergentintegration paths adopted by China, India, and Turkey,which all started from a relatively similar degree ofindustrial specialization about 10 years ago:

• China has become an assembly country,strongly integrated into the international seg-mentation-of-production processes in Asia.Most of China’s imports of high-tech productsare parts and components. These high-tech im-ports are predominantly incorporated into theproduction of exports and are not used to mod-ernize domestic production capacities. Given its

Box 3.1 Technology imports: Different paths fordifferent countries

level of development, China’s exports display anoutstandingly strong high-tech content.

• India is characterized by limited participation ininternational division-of-production processesand by a low level of imports in high-tech prod-ucts. These high-tech imports are evenly distrib-uted among the different stages of productionand the different sectors, while high-tech exportsare concentrated in chemical industries.

• Turkey’s high-tech imports consist mainly of cap-ital goods and correspond to a classical form oftechnology transfer aimed at upgrading indige-nous industrial capacities. Turkey’s foreign tradeis strongly structured by its traditional comple-mentaries with Europe.

buyers may have higher quality standards thandomestic buyers. Foreign buyers may also as-sist with process improvements and provide in-formation about and experience with foreignmarkets. Moreover, the additional demandthat foreign markets provide may allow for theexploitation of economies of scale that justifymore capital-intensive production (see, for ex-ample, Hobday 1995 and Rhee, Ross-Larson,and Pursell 1984 on the effects of learning byexporting in East Asia). Technology transfersthrough exports may be most important inproduction networks with clearly articulatedsupply chains (Gereffi 1999; Hobday 1995).5

Spillovers may also be common in labor-inten-sive sectors where production processes are rel-atively simple and the relevant knowledge iswidely available in industrial countries (Enosand Park 1987; Hou and Gee 1993).

Unfortunately, these efficiency benefits fromexporting are not confirmed by econometricstudies (Keller 2004), which generally find thatthe positive relationship between exportingand productivity results largely from the self-selection of firms into the export market.6

Whatever the magnitude of spillovers fromexports and of concerns surrounding the re-export nature of some high-tech exports, theexport of technology products is neverthelessan important indicator of technologicalachievement. High-tech exports offer betterprospects for future growth than lower-techgoods because their market has been expandingmore rapidly and because they offer superiorspillover potential by transmitting skills andgeneric knowledge that can be used in other ac-tivities (Guerrieri and Milana 1998). High-techexports are also less vulnerable to easy entry bylower-wage competitors, substitution by tech-nical change, and market shifts (Lall 2001).

Although high-income countries continue todominatetheworldmarketforhigh-techgoods,7

middle-income countries have substantially in-creased their market share since the mid-1990s.Lower-middle-incomecountriesmore thandou-bled their global share of high-tech exports, in-creasing themfrom6.6percent in the mid-1990sto 15.7 percent in 2002–04 (3.4 to 5.0 percent

if China is excluded). Moreover, the share ofhigher-technology goods in the total merchan-dise exports of these countries has also been in-creasing (figure 3.3). Much of this increase re-flected the transfer of manufacturing processesfrom high-income countries to developingcountries, notably those in East Asia and the Pa-cific. China was a major beneficiary of thisprocess, increasing its global market share ofhigh-techexports fromabout3percent to11per-cent, but so too were other countries. ThePhilippines, for example, increased its marketshare from 0.9 percent to about 2.0 percent.Upper-middle-income countries made less spec-tacular progress, increasing their global marketshare from 6.5 percent to 10.5 percent, althoughsome countries, such as Costa Rica, the CzechRepublic, and Hungary, were able to increasetheir high-tech markets significantly.8 In Sub-Saharan Africa, South Africa is the largest ex-porter of high-tech products, but its share has re-mained small and stable at about 0.08 percent.

The relative performance of differentmiddle-income regions reflects different levels

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

114

Figure 3.3 Exports of low-, medium-, andhigh-technology goods

Percent of total merchandise exports

Source: World Bank calculations using Centre d’EtudesProspectives et d’Informations Internationales database,Banque Analytique de Commerce International.

0

20

40

10

25

15

5

35

30

1994–96 2002–04

High-techexports

1994–96 2002–04

Medium-techexports

1994–96 2002–04

Low-techexports

Lower-middle-income countries

Low-income countries

High-income countries

Upper-middle-income countries

of technological capabilities and learningstyles. Since the early 1990s, Latin Americahas almost doubled its share of high-techproducts in world markets and now has thesecond largest market share after East Asiaand the Pacific. However, in contrast with Eu-rope and Central Asia and the Middle Eastand North Africa, it has done so with rela-tively little input from imported technology(imports of high-tech and capital goods as ashare of GDP in Latin America and theCaribbean are half the rate of Europe andCentral Asia). Partly as a consequence, Europeand Central Asia has gained market share inhigh-tech goods much more quickly thanLatin America, and based on recent perfor-mance, is poised to overtake that region soon.

Low-income countries remain marginalplayers in the world market for high-techgoods, and even though their global share ofexports of medium-tech goods has doubled, be-tween the mid-1990s and 2002–04, it remainslow at 0.8 percent. The share of low-incomecountries in world exports of low-tech goodsis more substantial and has increased from3.5 percent to 5.2 percent. Among these coun-tries, Vietnam has improved its global marketshare of low-tech products from 0.2 to 0.8 per-cent, a 250 percent increase. India remains themost important exporter of low-tech productsin this income group with 2 percent of theworld market, second after China among de-veloping countries, which accounts for about17 percent of the world’s low-tech exports.

Overall exposure to foreign technologieshas increasedOverall, the increased participation of devel-oping countries in global trade has substan-tially increased their exposure to foreign tech-nologies. For middle-income countries, thisexposure and the attendant expansion of high-tech exports have likely yielded important sidebenefits that are reflected in the sustainedacceleration in developing country growthrates over the past 15 years. While the increasein trade openness has been generalized, theextent to which countries have been able to

translate that into improved export perfor-mance and an increase in the technologicalsophistication of their own exports has varied,with countries like those in Europe and CentralAsia that have relatively well-educated popula-tions and a strong institutional structure hav-ing extracted the greatest benefits. Amongother countries, notably low-income countries,weak absorptive capacity may be restrictingthe extent to which their economies have ben-efited from the increased exposure.

Foreign direct investmentLike trade, FDI can be a powerful channel forthe transmission of technology to developingcountries by financing new investment, bycommunicating information about technologyto domestic affiliates of foreign firms, andby facilitating the diffusion of technology tolocal firms.

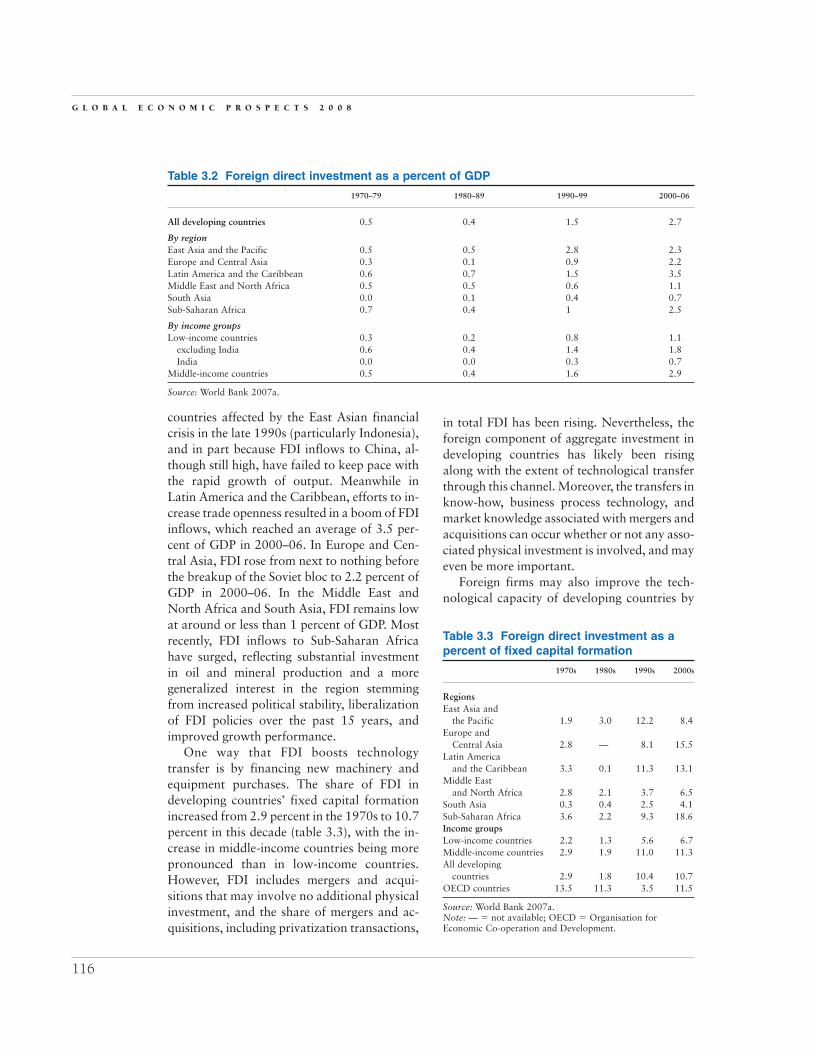

Foreign investors bring both equipmentand know-howMeasuring the technological contribution ofFDI is particularly difficult, in part becausethe standard measure from the balance of pay-ments includes both physical (brownfield andgreenfield) investments and financial invest-ments (mergers and acquisitions). This said,FDI inflows to developing countries rose from$10 billion in 1980 to an estimated $390 bil-lion in 2007, or from 0.4 to 2.9 percent ofGDP, with the bulk of the increase occurringduring the late 1990s in response to the liber-alization of FDI policies.9 Assuming that for-eign firms employ a higher level of technologythan the average domestic firm, then this ris-ing trend will have increased the average levelof technology in these countries, as well astheir exposure to higher technologies.

FDI as a share of GDP has risen in all de-veloping regions and income groups since the1980s, but the increase has been concentratedin middle-income countries, where FDI rose toalmost 3 percent of GDP (table 3.2). East Asiaand the Pacific had the highest ratio during the1990s, but it has since declined, in part be-cause of a collapse in FDI inflows to a few

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

115

countries affected by the East Asian financialcrisis in the late 1990s (particularly Indonesia),and in part because FDI inflows to China, al-though still high, have failed to keep pace withthe rapid growth of output. Meanwhile inLatin America and the Caribbean, efforts to in-crease trade openness resulted in a boom of FDIinflows, which reached an average of 3.5 per-cent of GDP in 2000–06. In Europe and Cen-tral Asia, FDI rose from next to nothing beforethe breakup of the Soviet bloc to 2.2 percent ofGDP in 2000–06. In the Middle East andNorth Africa and South Asia, FDI remains lowat around or less than 1 percent of GDP. Mostrecently, FDI inflows to Sub-Saharan Africahave surged, reflecting substantial investmentin oil and mineral production and a moregeneralized interest in the region stemmingfrom increased political stability, liberalizationof FDI policies over the past 15 years, andimproved growth performance.

One way that FDI boosts technologytransfer is by financing new machinery andequipment purchases. The share of FDI indeveloping countries’ fixed capital formationincreased from 2.9 percent in the 1970s to 10.7percent in this decade (table 3.3), with the in-crease in middle-income countries being morepronounced than in low-income countries.However, FDI includes mergers and acqui-sitions that may involve no additional physicalinvestment, and the share of mergers and ac-quisitions, including privatization transactions,

in total FDI has been rising. Nevertheless, theforeign component of aggregate investment indeveloping countries has likely been risingalong with the extent of technological transferthrough this channel. Moreover, the transfers inknow-how, business process technology, andmarket knowledge associated with mergers andacquisitions can occur whether or not any asso-ciated physical investment is involved, and mayeven be more important.

Foreign firms may also improve the tech-nological capacity of developing countries by

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

116

Table 3.3 Foreign direct investment as apercent of fixed capital formation

1970s 1980s 1990s 2000s

RegionsEast Asia and

the Pacific 1.9 3.0 12.2 8.4Europe and

Central Asia 2.8 — 8.1 15.5Latin America

and the Caribbean 3.3 0.1 11.3 13.1Middle East

and North Africa 2.8 2.1 3.7 6.5South Asia 0.3 0.4 2.5 4.1Sub-Saharan Africa 3.6 2.2 9.3 18.6Income groupsLow-income countries 2.2 1.3 5.6 6.7Middle-income countries 2.9 1.9 11.0 11.3All developing

countries 2.9 1.8 10.4 10.7OECD countries 13.5 11.3 3.5 11.5

Source: World Bank 2007a.Note: — � not available; OECD � Organisation for Economic Co-operation and Development.

Table 3.2 Foreign direct investment as a percent of GDP

1970–79 1980–89 1990–99 2000–06

All developing countries 0.5 0.4 1.5 2.7

By regionEast Asia and the Pacific 0.5 0.5 2.8 2.3Europe and Central Asia 0.3 0.1 0.9 2.2Latin America and the Caribbean 0.6 0.7 1.5 3.5Middle East and North Africa 0.5 0.5 0.6 1.1South Asia 0.0 0.1 0.4 0.7Sub-Saharan Africa 0.7 0.4 1 2.5

By income groupsLow-income countries 0.3 0.2 0.8 1.1

excluding India 0.6 0.4 1.4 1.8India 0.0 0.0 0.3 0.7

Middle-income countries 0.5 0.4 1.6 2.9

Source: World Bank 2007a.

financing R&D. Multinational corporationsundertake most of their R&D activities intheir home country or in other high-incomecountries.10 Nevertheless, the role of develop-ing countries appears to be rising. R&Dspending in developing countries by majority-owned foreign affiliates of U.S. parent compa-nies increased from $0.9 billion in 1999 to$1.6 billion in 2003 (Bureau of EconomicAnalysis 2007). The contribution of multina-tionals’ R&D to total measured R&D activityin developing countries varies from more than60 percent in Hungary to less than 5 percent inIndia (figure 3.4).

FDI may generate technology spillovers In addition to its technological impact on thefirm directly touched by the investment, FDImay also affect the level of technology indomestic firms.11 Spillovers can arise whenworkers receive training or accumulate experi-ence working for multinationals and thenmove to domestic firms or set up their own en-terprise (Fosfuri, Motta, and Ronde 2001;Glass and Saggi 2002). For example, withinsix years of the beginning of FDI-led export

growth in Mauritius, 50 percent of all firmsoperating in export-processing zones were lo-cally owned, founded, managed, and staffed—in many cases by employees who had receivedon-the-job training in foreign enterprises andhad left to set up their own companies (Rhee,Katterback, and White 1990).

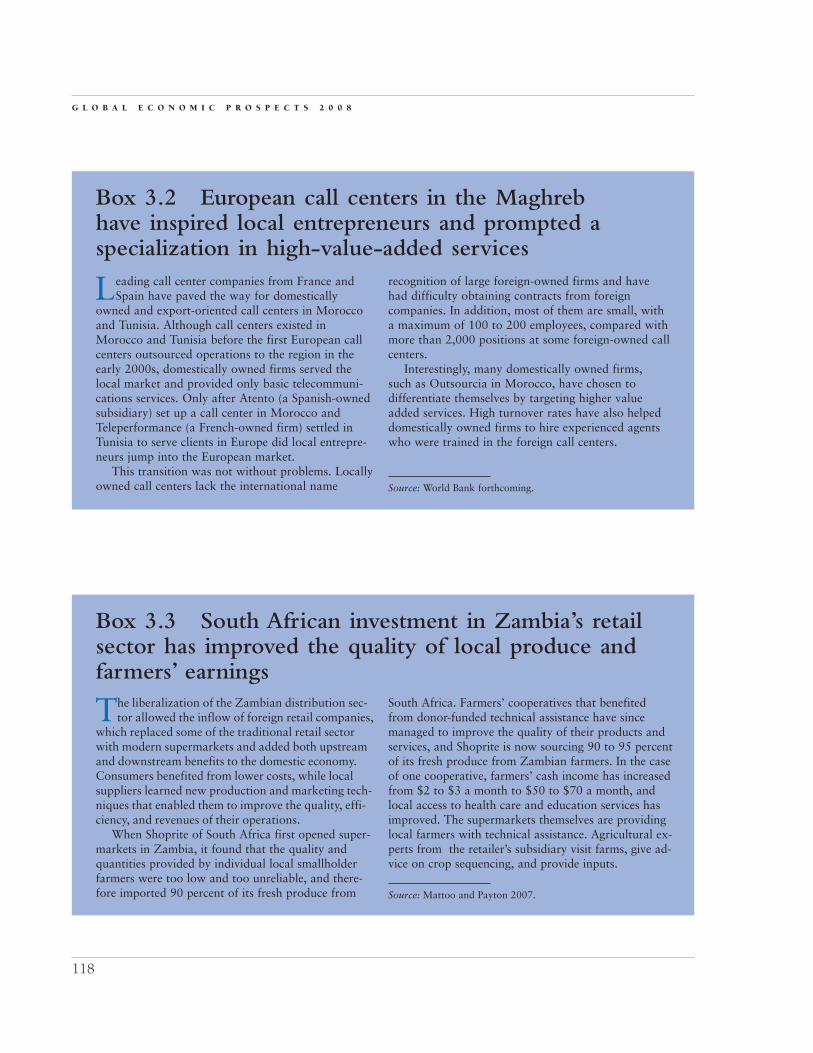

Already existing local firms may also ob-serve the actions of foreign firms and learnabout new products, equipment, marketingtechniques, and management practices. For ex-ample, 25 percent of the managers of Czechfirms and 15 percent of the managers of Latvianfirms report that they learned about new tech-nologies by observing foreign firms as they en-tered their industry (Javorcik and Spatareanu2005). In Morocco and Tunisia, domesticallyowned international call centers have risen inimitation of foreign firms (box 3.2).

If multinational entry leads to an increasein demand for intermediates, it may result inthe expansion of upstream domestic industries(see the experience with Zambian supermar-kets in box 3.3). Downstream industries mayalso benefit from the increased competitionand added variety of inputs created by the for-eign investment. In addition, foreign investorsmay provide advice, designs, direct produc-tion assistance, or marketing contacts to sup-pliers, which the latter can then deploy morebroadly than simply providing cheaper ormore reliable inputs to the foreigners.12

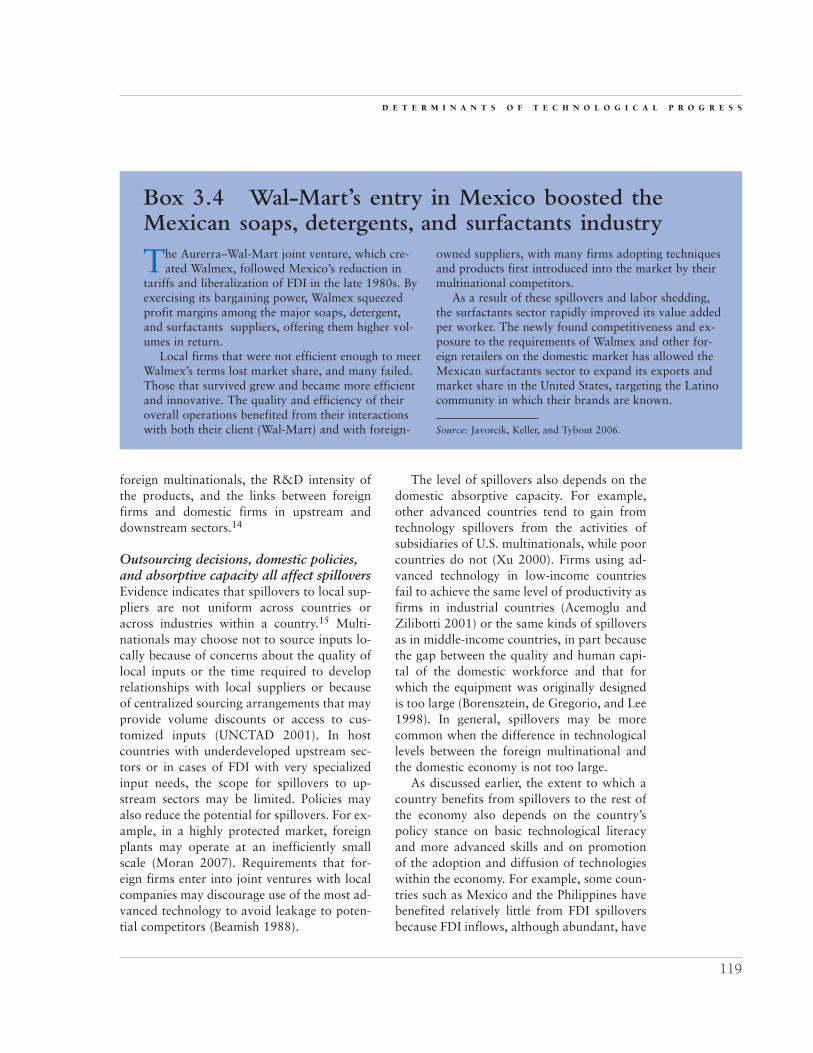

The entry of multinationals is likely to in-crease competition for the domestic firmswithin the industry, potentially forcing themto improve their efficiency and introducenew technologies or business strategies(Blomstrom, Kokko, and Zejan 2000), as inWal-Mart’s joint venture in Mexico (box 3.4).Such competition can make surviving domes-tic competitors stronger, but other domesticfirms may be driven out of business, lose mar-ket share, and experience a loss of high-skilledworkers and higher costs for intermediategoods resulting from increasing demand fromthe foreign-owned firms.13 These effects mayvary by industry depending on factors suchas the market structure before the entry of

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

117

Figure 3.4 Share of foreign affiliates inbusiness R&D expenditure

0

Hunga

ry

Brazil

Lithu

ania

Mex

ico (2

001)

Thaila

ndChin

a

Latvi

a

Slovak

Rep

ublic

Estonia

India

(199

9)

Argen

tina

Poland

Turk

ey (2

000)

Chile

(200

2)

10

20

30

70

50

40

60

Sources: OECD; Activity of Foreign Affiliates database.http://www.sourceoecd.org; UNCTAD 2005; Eurostat;R&D statistics.

Note: The year is 2003 unless otherwise indicated.

Percent

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

118

The liberalization of the Zambian distribution sec-tor allowed the inflow of foreign retail companies,

which replaced some of the traditional retail sectorwith modern supermarkets and added both upstreamand downstream benefits to the domestic economy.Consumers benefited from lower costs, while localsuppliers learned new production and marketing tech-niques that enabled them to improve the quality, effi-ciency, and revenues of their operations.

When Shoprite of South Africa first opened super-markets in Zambia, it found that the quality andquantities provided by individual local smallholderfarmers were too low and too unreliable, and there-fore imported 90 percent of its fresh produce from

Box 3.3 South African investment in Zambia’s retailsector has improved the quality of local produce andfarmers’ earnings

South Africa. Farmers’ cooperatives that benefitedfrom donor-funded technical assistance have sincemanaged to improve the quality of their products andservices, and Shoprite is now sourcing 90 to 95 percentof its fresh produce from Zambian farmers. In the caseof one cooperative, farmers’ cash income has increasedfrom $2 to $3 a month to $50 to $70 a month, andlocal access to health care and education services hasimproved. The supermarkets themselves are providinglocal farmers with technical assistance. Agricultural ex-perts from the retailer’s subsidiary visit farms, give ad-vice on crop sequencing, and provide inputs.

Source: Mattoo and Payton 2007.

Leading call center companies from France andSpain have paved the way for domestically

owned and export-oriented call centers in Moroccoand Tunisia. Although call centers existed inMorocco and Tunisia before the first European callcenters outsourced operations to the region in theearly 2000s, domestically owned firms served thelocal market and provided only basic telecommuni-cations services. Only after Atento (a Spanish-ownedsubsidiary) set up a call center in Morocco andTeleperformance (a French-owned firm) settled inTunisia to serve clients in Europe did local entrepre-neurs jump into the European market.

This transition was not without problems. Locallyowned call centers lack the international name

Box 3.2 European call centers in the Maghreb have inspired local entrepreneurs and prompted aspecialization in high-value-added services

recognition of large foreign-owned firms and havehad difficulty obtaining contracts from foreigncompanies. In addition, most of them are small, witha maximum of 100 to 200 employees, compared withmore than 2,000 positions at some foreign-owned callcenters.

Interestingly, many domestically owned firms,such as Outsourcia in Morocco, have chosen todifferentiate themselves by targeting higher valueadded services. High turnover rates have also helpeddomestically owned firms to hire experienced agentswho were trained in the foreign call centers.

Source: World Bank forthcoming.

foreign multinationals, the R&D intensity ofthe products, and the links between foreignfirms and domestic firms in upstream anddownstream sectors.14

Outsourcing decisions, domestic policies,and absorptive capacity all affect spilloversEvidence indicates that spillovers to local sup-pliers are not uniform across countries oracross industries within a country.15 Multi-nationals may choose not to source inputs lo-cally because of concerns about the quality oflocal inputs or the time required to developrelationships with local suppliers or becauseof centralized sourcing arrangements that mayprovide volume discounts or access to cus-tomized inputs (UNCTAD 2001). In hostcountries with underdeveloped upstream sec-tors or in cases of FDI with very specializedinput needs, the scope for spillovers to up-stream sectors may be limited. Policies mayalso reduce the potential for spillovers. For ex-ample, in a highly protected market, foreignplants may operate at an inefficiently smallscale (Moran 2007). Requirements that for-eign firms enter into joint ventures with localcompanies may discourage use of the most ad-vanced technology to avoid leakage to poten-tial competitors (Beamish 1988).

The level of spillovers also depends on thedomestic absorptive capacity. For example,other advanced countries tend to gain fromtechnology spillovers from the activities ofsubsidiaries of U.S. multinationals, while poorcountries do not (Xu 2000). Firms using ad-vanced technology in low-income countriesfail to achieve the same level of productivity asfirms in industrial countries (Acemoglu andZilibotti 2001) or the same kinds of spilloversas in middle-income countries, in part becausethe gap between the quality and human capi-tal of the domestic workforce and that forwhich the equipment was originally designedis too large (Borensztein, de Gregorio, and Lee1998). In general, spillovers may be morecommon when the difference in technologicallevels between the foreign multinational andthe domestic economy is not too large.

As discussed earlier, the extent to which acountry benefits from spillovers to the rest ofthe economy also depends on the country’spolicy stance on basic technological literacyand more advanced skills and on promotionof the adoption and diffusion of technologieswithin the economy. For example, some coun-tries such as Mexico and the Philippines havebenefited relatively little from FDI spilloversbecause FDI inflows, although abundant, have

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

119

The Aurerra–Wal-Mart joint venture, which cre-ated Walmex, followed Mexico’s reduction in

tariffs and liberalization of FDI in the late 1980s. Byexercising its bargaining power, Walmex squeezedprofit margins among the major soaps, detergent,and surfactants suppliers, offering them higher vol-umes in return.

Local firms that were not efficient enough to meetWalmex’s terms lost market share, and many failed.Those that survived grew and became more efficientand innovative. The quality and efficiency of theiroverall operations benefited from their interactionswith both their client (Wal-Mart) and with foreign-

Box 3.4 Wal-Mart’s entry in Mexico boosted theMexican soaps, detergents, and surfactants industry

owned suppliers, with many firms adopting techniquesand products first introduced into the market by theirmultinational competitors.

As a result of these spillovers and labor shedding,the surfactants sector rapidly improved its value addedper worker. The newly found competitiveness and ex-posure to the requirements of Walmex and other for-eign retailers on the domestic market has allowed theMexican surfactants sector to expand its exports andmarket share in the United States, targeting the Latinocommunity in which their brands are known.

Source: Javorcik, Keller, and Tybout 2006.

been oriented toward exploiting low wagesand have not built many links to the domesticeconomy. In contrast, countries like Singaporehave actively sought to maximize the technol-ogy spillovers from FDI by investing in thedomestic skills and competencies necessary tosupport high-skill and high value added indus-tries and by welcoming and promoting FDI insuch sectors (Lall 2003).

Spillovers might be highly concentrated in certain regions within a countryGeographic proximity also determines theextent of technological spillovers observed.The closer a local firm is to a foreign-ownedfirm, the more frequently will the firms’ em-ployees interact with each other, increasing thelikelihood that employees (and their acquiredknowledge) will move between the two firms.The spatial aspect is also important for verti-cal spillovers between foreign-owned firmsand their local suppliers, which are often lo-cated close to each other (Jaffe 1989).

The existence of such cluster effects mayexplain why FDI tends to be geographicallyconcentrated within a country mainly aroundlarge cities or coastal states. In Russia, for ex-ample, more than two-thirds of the FDI stockin 2000 was in Moscow and three surround-ing regions (Broadman and Recanatini 2005).Similarly, almost half of FDI flows in India goto the Mumbai and Delhi areas (Reserve Bankof India 2007), while in China, almost 90 per-cent of FDI flows go to the western coastal re-gion (Kui-Yin and Lin 2007). This said, be-cause of data limitations and conceptualproblems, econometric support for the notionthat such clusters generate important technol-ogy spillovers is limited (Lipsey and Sjohom2005), with some studies supporting their ex-istence (see Girma and Wakelin 2001 for theelectronics sector in the United Kingdom) andothers not (see Aitken and Harrison 1999 forVenezuela and Sjoholm 1998 for Indonesia).

Developing countries also purchase foreignhigh-tech firmsOutward FDI, that is, the purchase of foreignfirms by domestically owned ones, and the

licensing of technologies are two other, moredirect mechanisms by which developing coun-tries acquire foreign technologies and researchexpertise.

Over the past 20 years, firms domiciled indeveloping countries have increasingly turnedto foreign acquisitions as a means of expandingtheir market share and gaining control overtechnology. Cross-border mergers and acquisi-tions by multinational corporations located indeveloping countries increased from $400 mil-lion in 1987 (less than 1 percent of globalmerger and acquisition transactions) to almost$100 billion in 2006 (almost 9 percent of globalmerger and acquisition transactions) (WorldBank 2007a). Although technology may not bethe primary motivator in many of these pur-chases, technology transfer is associated withnearly all of them in the form of control overpatents and knowledge of manufacturingprocesses, marketing, and business process ex-pertise. Table 3.4 summarizes some of the moretechnologically important recent acquisitionsof high-tech firms by developing country firms.

Developing country firms may seek to ac-quire a brand or a marketing or distribution net-work. Examples include the Thai Union FrozenCompany’s purchase of the Chicken of the Seabrand; the South African Brewery’s purchase ofMiller Brewing (a major U.S. beer maker); andMalaysian Berjaya’s purchase of Taiga, thelargest Canadian distributor of building materi-als. Developing country firms may also purchaseforeign firms to acquire R&D capacity. For ex-ample, the Chinese company Shanghai Automo-tive Industry Corporation bought Sangyong ofthe Republic of Korea to enhance its R&Dcapabilities in sport utility vehicles. Accessingforeign technology also takes the form of estab-lishing R&D centers in developed countries. Forexample, Huawei Technologies and ZTECorporation, both Chinese companies, haveestablished R&D centers in Sweden.

Developing countries can also licenseforeign technologiesDeveloping countries can also gain access totechnology through licensing, which typically

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

120

involves the purchase of production or distri-bution rights for a product and the underlyingtechnical information and know-how for pro-ducing it. As measured by the payment of in-ternational royalties and fees in countries’balance of payments, licensing fees paid by de-veloping countries increased from $7 billion in1999 to $22 billion in 2006, about a fivefoldincrease when expressed as a percentage ofdeveloping country GDP.16 The increase wassharpest for oil- and mineral-exporting coun-tries, reflecting higher prices for oil andcontracts that often expressed these fees as apercentage of revenues or profits. Nevertheless,licensing fees paid by other developing coun-tries also tripled, and for both low- and middle-income countries these fees represented a largershare of overall GDP than they did for oil- andmineral-exporting countries (figure 3.5).

Licensing can be used as a substitute forFDI. Uncertainty about the policy environ-ment may lead multinationals to sell technol-ogy rather than to exploit the technologythrough foreign investment (domestic firmsmay have more information or may be betterplaced than foreigners to deal with a poor pol-icy environment). Evidence suggests that bothFDI and licensing respond to an adequate busi-ness environment, and factors such as patentprotection may shift incentives for investorsfrom FDI toward licensing (Maskus 2002).Where protection of intellectual property

rights is weak, multinationals may be less will-ing to license technology for fear of it beingcopied by domestic firms. Alternatively, theymay only be willing to license out-of-datetechnologies (Maskus 2000). Data on U.S.multinationals show that the likelihood ofentering into licensing agreements increases asdeveloping countries increase their protectionof intellectual property rights (Antras, Desai,and Foley 2007).

Some countries have pursued a licensing-based strategy of technology acquisition in the

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

121

Table 3.4 Selected purchases of high-tech firms by companies in developing countries,early 2000s

Acquiring company Country of acquirer Year Acquired firm Country of acquired Industry

Netcare South Africa 2006 General Health Care United Kingdom HealthTata Tea India 2006 Tetley United Kingdom Tea Videocon Industries Ltd. India 2006 Daewoo Electronics Korea, Rep. of ElectronicsChalkis China 2005 Le Cabanon France Food processingEssel Propack India 2005 Telcon Packing United Kingdom Tube packingWipro India 2005 New Logic Austria SemiconductorsOrascom Egypt, Arab Rep. of 2005 Wind Italy TelecommunicationsLenovo China 2004 IBM United States PC manufacturingTCL China 2004 Alcatel France TelecommunicationsRanbaxy India 2004 RPG France PharmaceuticalsBOW Technology Group China 2003 Hynix Korea, Rep. of PC manufacturingPKN Orlen Poland 2002 BP (500 petrol stations) United Kingdom Downstream oil

Source: World Bank 2007a.

Figure 3.5 Licensing payments have risensharply

0Oil andmineral

exporters

Other Oil andmineral

exporters

Others

1990–04

1995–99

2000–06

0.05

0.25

Percent of GDP

0.15

0.10

0.20

Sources: Balance of Payments Database (IMF) and WorldDevelopment Indicators.

Middle-income countries Low-income countries

belief that domestic firms will be able to up-grade their own technological capacities byworking with licensed technology. For exam-ple, in the 1950s and 1960s, Japan kept itseconomy relatively closed to FDI to encouragemultinationals that wished to gain from thegrowing Japanese market to license technol-ogy to domestic firms (Pack and Saggi 1997).China has also encouraged joint ventures, asopposed to FDI, to maximize technologytransfers to local firms. This strategy is likelyto work only if the country has sufficient mar-ket power. Moreover, such discriminatorypolicies run the risk of resulting in the transferof substandard technologies (Hoekman andJavorcik 2006). In contrast, several LatinAmerican countries discouraged the licensingof technology from abroad because of con-cerns about unfair pricing and competitionwith local technologies, a strategy that re-tarded or skewed technological developmentin that region (Pack and Saggi 1997).

The bulk of international royalties and feesstems from intrafirm transfers. In part, thismay reflect a preference by multinationalfirms to transfer more advanced technologiesonly to wholly owned subsidiaries rather thanto partially owned affiliates and to enter mar-kets through wholly owned subsidiaries ratherthan through joint ventures (Javorcik 2006;Mansfield and Romeo 1980). However, it mayalso mean that these fees are being used as amechanism for repatriating profits, perhapsfor tax reasons. As a result, the level of royal-ties and fees may not be a market-based re-flection of the value of technology purchasedby the local subsidiary (Robbins 2006).

Partly because of intrafirm payments and ofthe close relationship between licensing andFDI, economists have had difficulty in evaluat-ing the impact of licensing on technologytransfer. Nevertheless, a few case studies havedocumented its benefits. Brazil and Koreaachieved considerable success in absorbingnew technologies through licensing (Correa2003), and licensing agreements were animportant factor for the success of flori-culture in Kenya, maize in India, and the

electronics sector in Taiwan, China (Chandraand Kolavalli 2006). The latter study alsohighlights that even though licensing may en-able rapid acquisition of product and processknow-how, it also requires a significant level oflocal technological capability to put thelicensed technology to work.

International migrationAlong with trade and FDI, international mi-grants are another important channel for thetransmission of technology and knowledge.From the perspective of developing countries,however, the direction of technology transfercan be both outward (as migrants take awayscarce skills) or inward (through contacts withthe diaspora).

The direction and scale of technology flowsthat result from international migration areless clear than for FDI and trade. On the onehand, the brain drain associated with bettereducated citizens of developing countriesworking in high-income countries is a seriousproblem for many developing countries. Onthe other hand, the contribution that these in-dividuals would have made had they stayedhome is uncertain given the lack of opportuni-ties in some countries. Moreover, developingcountries can benefit from the immigration,albeit often temporary, of managers and engi-neers that often accompanies FDI; the returnof well-educated developing country emi-grants; and the contacts with a technologicallysophisticated diaspora.

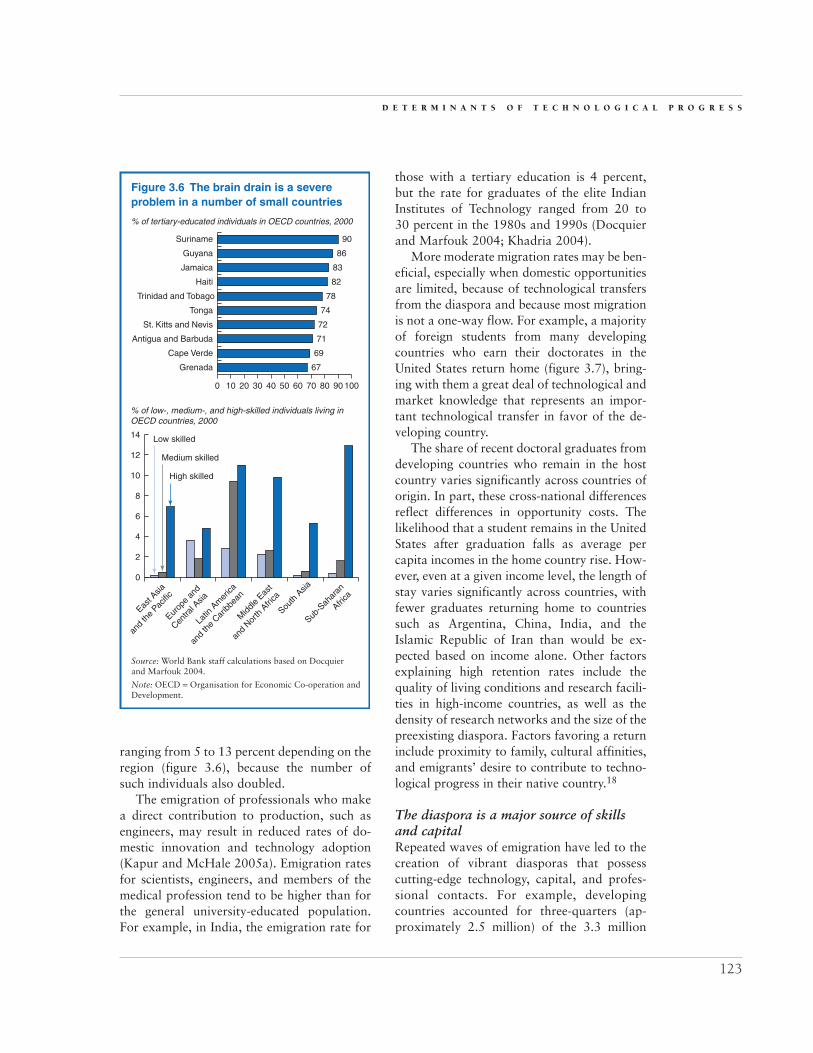

High rates of skilled out-migration imply anet transfer of human capital and scarce re-sources (in the form of the cost of educatingthese workers) from low- to high-incomecountries (UNCTAD 2007; World Bank2006a). For some countries, the brain drainrepresents a significant problem: emigrationrates of highly educated individuals can ex-ceed 60 percent in some small countries (fig-ure 3.6), and since 1990, the highly educateddiaspora of developing countries has doubledin size.17 However, the share of developingcountry tertiary-educated individuals livingabroad remained stable and relatively low,

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

122

ranging from 5 to 13 percent depending on theregion (figure 3.6), because the number ofsuch individuals also doubled.

The emigration of professionals who makea direct contribution to production, such asengineers, may result in reduced rates of do-mestic innovation and technology adoption(Kapur and McHale 2005a). Emigration ratesfor scientists, engineers, and members of themedical profession tend to be higher than forthe general university-educated population.For example, in India, the emigration rate for

those with a tertiary education is 4 percent,but the rate for graduates of the elite IndianInstitutes of Technology ranged from 20 to30 percent in the 1980s and 1990s (Docquierand Marfouk 2004; Khadria 2004).

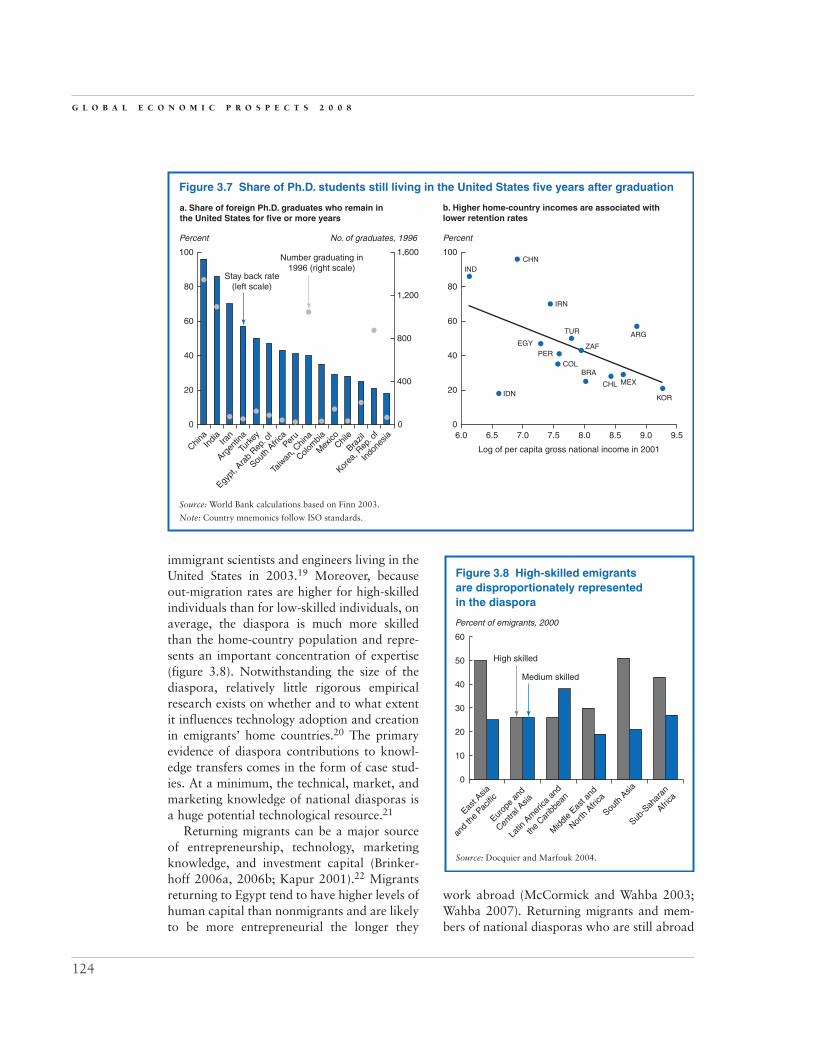

More moderate migration rates may be ben-eficial, especially when domestic opportunitiesare limited, because of technological transfersfrom the diaspora and because most migrationis not a one-way flow. For example, a majorityof foreign students from many developingcountries who earn their doctorates in theUnited States return home (figure 3.7), bring-ing with them a great deal of technological andmarket knowledge that represents an impor-tant technological transfer in favor of the de-veloping country.

The share of recent doctoral graduates fromdeveloping countries who remain in the hostcountry varies significantly across countries oforigin. In part, these cross-national differencesreflect differences in opportunity costs. Thelikelihood that a student remains in the UnitedStates after graduation falls as average percapita incomes in the home country rise. How-ever, even at a given income level, the length ofstay varies significantly across countries, withfewer graduates returning home to countriessuch as Argentina, China, India, and theIslamic Republic of Iran than would be ex-pected based on income alone. Other factorsexplaining high retention rates include thequality of living conditions and research facili-ties in high-income countries, as well as thedensity of research networks and the size of thepreexisting diaspora. Factors favoring a returninclude proximity to family, cultural affinities,and emigrants’ desire to contribute to techno-logical progress in their native country.18

The diaspora is a major source of skillsand capital Repeated waves of emigration have led to thecreation of vibrant diasporas that possesscutting-edge technology, capital, and profes-sional contacts. For example, developingcountries accounted for three-quarters (ap-proximately 2.5 million) of the 3.3 million

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

123

% of tertiary-educated individuals in OECD countries, 2000

Source: World Bank staff calculations based on Docquierand Marfouk 2004.

Note: OECD = Organisation for Economic Co-operation andDevelopment.

St. Kitts and Nevis

Antigua and Barbuda

Cape Verde

Grenada

Tonga

Trinidad and Tobago

Suriname

Jamaica

Guyana

Haiti

0 605040302010 70 80 100

90

86

83

82

78

74

72

71

69

67

90

Figure 3.6 The brain drain is a severeproblem in a number of small countries

% of low-, medium-, and high-skilled individuals living inOECD countries, 2000

0

10

14

4

6

12

8

2

Low skilled

Medium skilled

East A

sia

and

the

Pacific

Europ

e an

d

Centra

l Asia

Latin

Am

erica

and

the

Caribb

ean

Midd

le Eas

t

and

North

Afri

ca

South

Asia

Sub-S

ahar

an

Africa

High skilled

immigrant scientists and engineers living in theUnited States in 2003.19 Moreover, becauseout-migration rates are higher for high-skilledindividuals than for low-skilled individuals, onaverage, the diaspora is much more skilledthan the home-country population and repre-sents an important concentration of expertise(figure 3.8). Notwithstanding the size of thediaspora, relatively little rigorous empiricalresearch exists on whether and to what extentit influences technology adoption and creationin emigrants’ home countries.20 The primaryevidence of diaspora contributions to knowl-edge transfers comes in the form of case stud-ies. At a minimum, the technical, market, andmarketing knowledge of national diasporas isa huge potential technological resource.21

Returning migrants can be a major sourceof entrepreneurship, technology, marketingknowledge, and investment capital (Brinker-hoff 2006a, 2006b; Kapur 2001).22 Migrantsreturning to Egypt tend to have higher levels ofhuman capital than nonmigrants and are likelyto be more entrepreneurial the longer they

work abroad (McCormick and Wahba 2003;Wahba 2007). Returning migrants and mem-bers of national diasporas who are still abroad

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 8

124

Figure 3.7 Share of Ph.D. students still living in the United States five years after graduation

Percent No. of graduates, 1996

0

20

40

100

80

60

Percent

0

20

40

100

80

60

9.56.0 6.5 7.0 7.5 8.0 8.5 9.0

ChinaIn

dia

Argen

tina

Iran

Turk

ey

Egypt

, Ara

b Rep

. of

South

Afri

caPer

u

Taiw

an, C

hina

Colom

bia

Mex

icoChil

e

Brazil

Korea

, Rep

. of

Indo

nesia

0

400

800

1,200

1,600

Stay back rate(left scale)

Number graduating in1996 (right scale)

Log of per capita gross national income in 2001

INDCHN

IDN

IRN

EGY

TUR

PERCOL

ZAF

BRA

ARG

CHL MEX

KOR

a. Share of foreign Ph.D. graduates who remain inthe United States for five or more years

b. Higher home-country incomes are associated withlower retention rates

Source: World Bank calculations based on Finn 2003.

Note: Country mnemonics follow ISO standards.

Source: Docquier and Marfouk 2004.

Figure 3.8 High-skilled emigrantsare disproportionately representedin the diaspora

Percent of emigrants, 2000

0

40

60

10

20

50

30

East A

sia

and

the

Pacific

Europ

e an

d

Centra

l Asia

Latin

Am

erica

and

the

Caribb

ean

Midd

le Eas

t and

North

Afri

ca

South

Asia

Sub-S

ahar

an

Africa

Medium skilled

High skilled

have made major contributions to technologi-cal progress in their home countries (box 3.5).

The diaspora also contributes to technologytransfers and adoption by strengthening tradeand investment linkages. The high-skilled dias-pora of countries such as India has contributedto the growth of the information technologysector, outsourcing (Kapur and McHale 2005b;Pandey and others 2006), and FDI in theirhome countries. The flow of outward FDI fromthe United States is strongly correlated with thestock of migrants from the origin country.23

Nearly half of the $41 billion in FDI that Chinareceived in 2000 may have originated from itsdiaspora abroad (Wei 2004). Similarly, 60 per-cent of the increase in bilateral trade in differ-entiated products within Southeast Asia may beattributable to ethnic Chinese networks (Rauchand Trindade 2002).24 Moreover, technologyappears to diffuse more efficiently through

culturally and nationally linked groups, andshared ethnicity appears to counteract the kindof home bias effects that underpin the geo-graphic network or the cluster effects that givehigh-density R&D zones an innovation advan-tage (Agrawal, Kapur, and McHale 2004).

Diaspora networks and returnees helppromote technology adoptionThe diaspora’s political engagement in homecountries can also improve local technologicalabsorptive capacity, both through return andby exercising pressure on home country politi-cians from afar. Many leaders of developingcountries were educated abroad and returnedto strengthen political institutions in their coun-tries of origin (Easterly and Nyarko 2005). Inaddition, migrants have often played a valuablerole in the transfer of market-based institutions,such as venture capital, entrepreneurship, and

D E T E R M I N A N T S O F T E C H N O L O G I C A L P R O G R E S S

125

An émigré from Bangladesh working in the finan-cial sector in the United States returned to help

create the Grameen Phone network and make mobilephones available to poor people in remote villages(Sullivan 2007). Through its successful Village PhoneProgram, the network has provided business oppor-tunities to some 260,000 Village Phone operators,mostly poor rural women. Grameen Phone now has15 million customers, more than 10 times the maxi-mum potential client base initially estimated byBangladesh Telecom.

In India, Sam Pitroda, a global entrepreneur who divides his time between India and the United States,founded the Center for Development of Telematics,which developed rural automatic telephone exchangesand introduced shared public call offices all over the country, thus expanding access to cheap and reli-able domestic and international calling. The rela-tively low-cost telephone exchanges are designed tooperate without air conditioning and require signifi-cantly less maintenance than conventional ex-changes. The technology has been exported to sev-eral other developing countries.

Box 3.5 Technological transfers through the diasporaand return migrants: Some examples