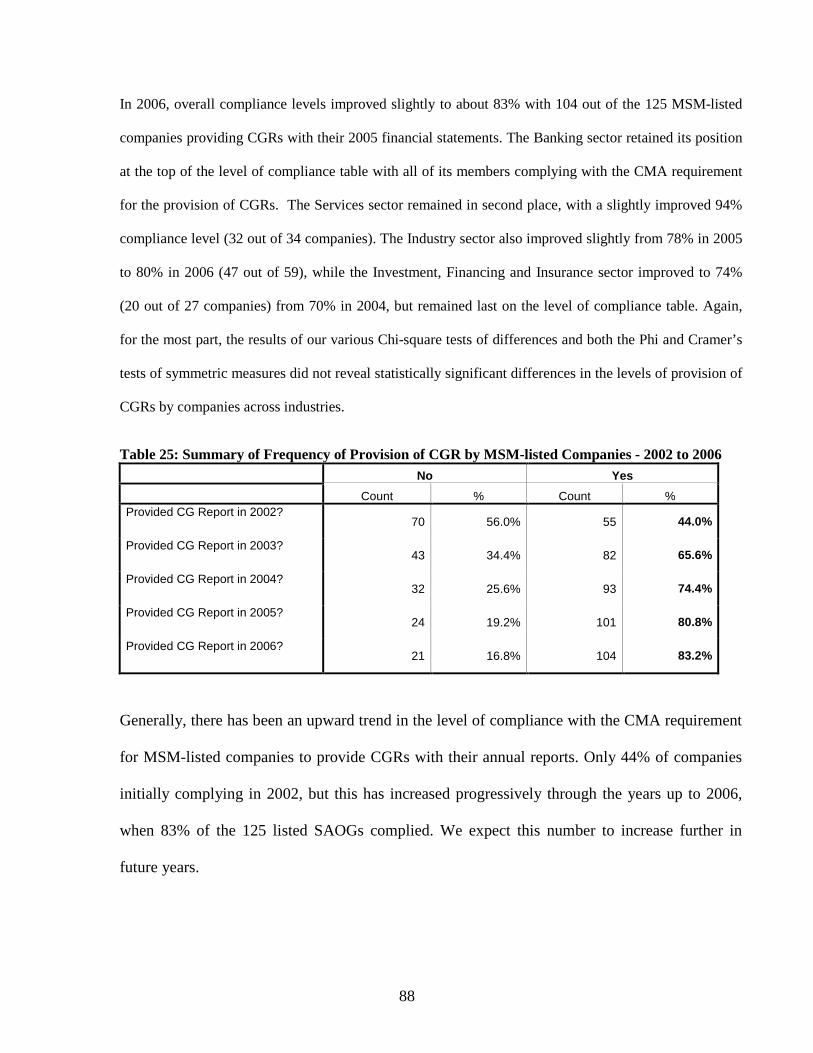

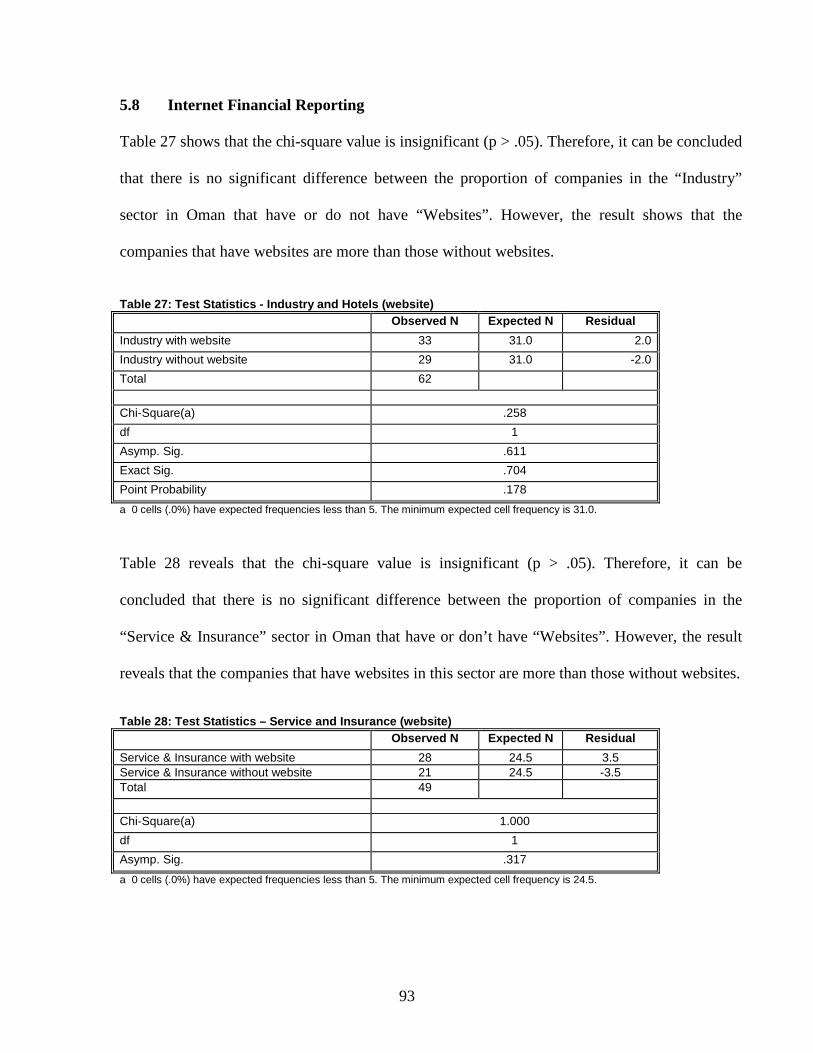

Determinants of Effective Corporate Governance in States ... corporate governance .pdf · 7...

107

Determinants of Effective Corporate Governance in States with Varying Ownership Structures: An International Comparison of Emerging and Western-like Markets FINAL REPORT December 2007

Transcript of Determinants of Effective Corporate Governance in States ... corporate governance .pdf · 7...

Determinants of Effective Corporate Governance in States

with Varying Ownership Structures: An International

Comparison of Emerging and Western-like Markets

FINAL REPORT

December 2007

2

Table of Contents

Table of Contents ........................................................................... 2

List of Tables .................................................................................. 4

List of Figures ................................................................................. 5

Abstract ....................................................................................... 6

Acknowledgements ........................................................................ 7

Scientific Committee ...................................................................... 7

Project Staff .................................................................................... 7

1. Introduction ................................................................................ 8

2. Overall Plan of the Project ......................................................... 9

2.1 In-depth Planning and Literature Review .................................. 9

2.2. Test sample data collection: Oman, UAE & Singapore ........... 10 2.3. Test sample data analysis: Oman & UAE vs. Singapore ......... 11

2.4. Hypotheses and model development ....................................... 11

2.5. Presentation of preliminary results (conference) .................... 11

2.6. Review/restructure of hypothesis and model (if required) ..... 12

2.7 Full sample data collection: Oman, the UAE & Singapore ...... 12

2.8 Full sample data analysis: Oman & UAE vs. Singapore.......... 12

2.9 Presentation of project results (conferences & seminars) ..... 12

2.10 Write-up of project results and reports ................................... 12

3

3. Literature Review .................................................................... 13

4. Institutional Framework .......................................................... 34

5. Data Analysis and Discussion of Results ................................ 50

6. Summary and Conclusions ........................................................ 97

References .................................................................................. 100

Appendices ................................................................................. 106

4

List of Tables

Table Description Page 1 Suggested list of items to be provided in MSM-listed Company’s report on CG 39 2 Comparative analysis of Corporate Governance Codes 43

3A UAE and Omani companies with websites 50 3B Chi-square test statistics on UAE and Omani companies with websites 50 4A Provision of “company history” information by UAE and Omani companies 51 4B Chi-square test statistics on company history information 51 5A Provision of “products and services” information by UAE and Omani companies 52 5B Chi-square test statistics on “products and services” information 52 6A Provision of financial information by UAE and Omani companies 53 6B Chi-square test statistics on financial information 53 7A Descriptive Statistics 68 7B Model Summary(b) 68 7C Results of regression model 68 8A Group Statistics – Banks Vs. Insurance sector 73 8B Group Statistics – Banks Vs. Services sector 73 8C Group Statistics – Banks Vs. Industry sector 73 8D Group Statistics – Big firms vs. Others 73 8E Group Statistics – Blockholders vs. Non-blockholders 73 8F Model Summary(b) - relevance and timeliness of corporate disclosure 73 8G Regression Results on relevance and timeliness of corporate disclosure 74 9A Model Summary(b) - corporate governance and disclosure 75 9B Regression results on corporate governance and disclosure 75 10 Test Statistics - Industry and Hotels (website) 76 11 Test Statistics - Service (website) 76 12 Test Statistics – Banks 77 13 Test Statistics - Insurance 77 14 Test Statistics - All sectors 78 15 Test Statistics - Industry and Hotels’ (Types) company history 78 16 Test Statistics – Services sector company history 79 17 Test Statistics – Banks company history 79 18 Test Statistics – Insurance sector company history 80 19 Test Statistics – All Sectors company history 80 20 Statistical Tests of Provision of CGR in 2002 by Industrial Classification 81 21 Statistical Tests of Provision of CGR in 2003 by Industrial Classification 83 22 Statistical Tests of Provision of CGR in 2004 by Industrial Classification 84 23 Statistical Tests of Provision of CGR in 2005 by Industrial Classification 86 24 Statistical Tests of Provision of CGR in 2006 by Industrial Classification 87 25 Summary of Frequency of Provision of CGR by MSM-listed Companies - 2002 to 2006 88 26 Multivariate Regression Results 91 27 Test Statistics - Industry and Hotels (website) 93 28 Test Statistics – Service and Insurance (website) 93 29 Test Statistics – Banks (website) 94 30 Test Statistics – All Sectors (website) 94 31 Test Statistics - Industry and Hotels company history 95 32 Test Statistics – Service and Insurance company history 95 33 Table 33: Test Statistics - Banks company history 96 34 Test Statistics – All Sectors company history 96

5

List of Figures

Figure Description

Page

1 Organisational Chart of the Omani Capital Market Authority (CMA) 37 2 Organisational Chart of the UAE Securities & Commodities Authority 42 3 Comparison of disclosing “Company History” between Oman and UAE companies 51 4 Comparison of disclosing “Product and Service” information by Oman and UAE companies 52 5 Comparison of disclosing Financial Information between Oman and UAE companies 53 6 Comparison of disclosing Annual Reports between Oman and UAE companies 54 7 Comparison of disclosing Financial Highlights between Oman and UAE companies 54

8A Provision of Annual Reports 70 8B Provision of Annual Reports with Management Report 70 8C Provision of Backward Versus Forward-looking information 71 8D Disclosure of Good news versus Bad news 71 8E Disclosure of Quarterly Reports 72 8F Number of Quarterly Reports missed 72 9 Provision of CGR in 2002 by Industrial Classification 81

10 Provision of CGR in 2003 by Industrial Classification 82 11 Provision of CGR in 2004 by Industrial Classification 84 12 Provision of CGR in 2005 by Industrial Classification 85 13 Provision of CGR in 2006 by Industrial Classification 87

6

Abstract

Corporate governance has become one of the most topical issues in the modern business world today. The recent spectacular corporate failures, such as those of Enron and WorldCom in the USA and Parmalat in Italy, have made it a central issue, with various governments and regulatory authorities making efforts to install stringent governance regimes to ensure the smooth running of corporate organizations, and prevent such failures. A corporate governance system is defined as a more-or-less country-specific framework of legal, institutional and cultural factors shaping the patterns of influence that shareholders (or stakeholders) exert on managerial decision-making. Corporate governance mechanisms are the methods employed, at the firm level, to solve corporate governance problems. Our project examined the key determinants of effective corporate governance practices in Oman, the UAE and Singapore. The main objective was to undertake an in-depth comparative examination of the effect of various factors on governance practices and disclosure across established Western-like and emerging economies. We explored and compared corporate ownership structures and corporate governance forms and mechanisms in Oman, the UAE, and Singapore. Data collection for the project proceeded in two main stages. In the first stage, relevant data on corporate governance disclosure and practices of listed companies and their corporate attributes for the years 2002 and 2004 were collected on a test sample basis. This was followed by a substantive full sample data collection process in the second stage. The results of data analysis for the project indicate that there are differences in some of the factors that influence corporate governance in Oman, the UAE and Singapore. In the UAE, we found that three of the corporate governance mechanisms appear to be strong enough to affect the firm’s performance. The null hypotheses of no significant relationship between the firm’s performance and the three variables (the governmental ownership, the dividends payout ratio, and debt equity ratio) were rejected. The other null hypotheses could not be rejected. In Oman, we found that rather surprisingly, ownership structure is not an important determinant when it comes to corporate governance matters. Traditional determinants such as firm size, performance and auditor status appear to be the more important. This tallies with findings in other countries, particularly western developed nations. We did not find a lot of evidence in support of other factors such as diffuseness of ownership and industrial sector. In Singapore, we found that ownership structure is not of great significance in governance matters. Rather, factors such as firm size and profitability appear to be the most important determinants. Sound corporate governance practices appear to support and contribute to superior corporate performance by SGX-listed companies. Our findings represent a confirmation that some corporate governance mechanisms in one system could have different effect on the firm performance in another system.

7

Acknowledgement We would like to acknowledge the support of the Research Affairs Offices of Sultan Qaboos

University and United Arab Emirates University. We greatly appreciate the excellent

research leadership and full support of Dr. Maitha S. Al-Shamsi, the Assistant Provost for

Research and Director of eFORS of UAEU, and Professor Amer Ali Al-Rawas, the Deputy

Vice Chancellor for Postgraduate Studies and Research, SQU (and his predecessor, Professor

Ali Bemani). We appreciate the financial support provided for this project by the two

universities. We would also like to express our special thanks to all members of the Scientific

Committee, past and present, for their excellent guidance and valuable comments. They

devoted a great deal of their time, and without their thoughtful advice and tireless

perseverance and supportive enthusiasm over the duration of this project, it may not have

been possible to achieve this successful completion.

Scientific Advisory Council SQU (Oman) UAEU (UAE)

Professor Ali Awad Yousif Professor Abdel-Mohsen Onsy Mohamed

Mrs Shekha N. Al-Akhzami Professor Reyadh Al Mehiadeb

Mr Fahad S. Hosni

Project Staff

Personnel-SQU (Oman) Personnel-UAEU (UAE)

Dr. Peter B. Oyelere (PI - SQU) Dr. Khaled Al-Jifri (PI - UAEU)

Dr Ehab Mohammed Dr Mohamed Moustafa*

Dr Divesh Sharma (Consultant)**

Research Assistants

* Replaced Dr Kalu Ojah, the initial co-investigator, who left UAEU at the beginning of the project. Dr Mohamed Moustafa left UAEU in 2006.

**Left Singapore to take up new appointment overseas.

8

1. INTRODUCTION

Corporate governance has become one of the most topical issues in the modern business world

today. The recent spectacular corporate failures, such as those of Enron and WorldCom in the USA

and Parmalat in Italy, have made it a central issue, with various governments and regulatory

authorities making efforts to install stringent governance regimes to ensure the smooth running of

corporate organizations, and prevent such failures. The extent of success garnered by these regimes,

relative to their costs, is a major issue currently being debated and researched in various countries of

the world. One issue, on which there is consensual agreement amongst almost all stakeholders across

the world, is that proper and adequate corporate governance procedures are necessary to secure and

retain investor confidence in the global marketplace.

Following on developments around the world, regulatory authorities in different countries have been

responding to the need for greater transparency and accountability with regards to corporate

governance disclosure. The Capital Markets Authority in Oman, for example, instituted requirements

for corporate governance disclosure on companies listed on the Muscat Securities Market from 2002,

while the authorities in Singapore instituted the second edition of their Code of Corporate

Governance in 2005. The UAE's regulatory authorities recently solicited for comments on its draft

Corporate Governance Code. The aim of this research project is to undertake a comprehensive

documentation of corporate governance developments in Oman and the UAE, and compare these

with developments in Singapore. Particular attention will be paid to various important elements,

including the level and quality of corporate governance disclosure by listed companies, current

corporate governance practices, transparency and accountability in the communication of corporate

9

governance practices, and the impact of corporate attributes such as ownership structure, size,

profitability, etc. on corporate governance practices and disclosure.

2. OVERALL PLAN OF THE PROJECT

As stated above, the original plan of this project is to undertake an in-depth comparative examination

of the effect of ownership structure and practices on corporate governance across established

Western-like and emerging economies. It was aimed at exploring and comparing corporate

ownership structures and corporate governance forms, practices and mechanisms in Oman, the UAE,

and Singapore.

The overall plan of the project involves the following broadly-defined stages:

• In-depth planning and literature review • Test sample data collection: Oman, UAE & Singapore • Test sample data analysis: Oman & UAE vs. Singapore • Hypotheses and model development • Presentation of preliminary results (conference) • Review/restructure of hypothesis and model (if required) • Full sample data collection: Oman, the UAE & Singapore • Full sample data analysis: Oman & UAE vs. Singapore • Presentation of project results (conferences & seminars) • Write-up of project results and reports

2-1 In-depth Planning and Literature Review

This stage, which was carried out between February and April 2004, involved a series of in-depth

planning meetings and consultation between members of the research team on the subject matter of

the research and their planned involvement. It also involved a research visit to the Abu Dhabi

Securities Market (ADSM) and its regulatory agency, the Securities and Commodities Authority

10

(SCA). During this stage, a detailed scope-outline for the review of relevant extant literature was

also agreed as follows:

Initial literature review enabled the team to conceptualise and identify key issues to focus on during

the research project. These were identified to include:

a. Accountability and transparency of corporate governance disclosure by listed companies: Particular attention to be paid to corporate awareness of their responsibility and willingness to disclose financial and corporate governance information to members of the public. Possible corporate attribute differentials in accountability and disclosure levels will also be investigated.

b. The level and quality of corporate governance disclosures by listed companies, including a longitudinal study of differentials/improvements between intervening years. Particular considerations will be given to possible differentials based on organizational attributes including ownership structure.

c. Salient corporate governance practices amongst listed companies including best and worst disclosure practices.

d. Development of a corporate governance disclosure index of listed companies. e. Comparison of these issues across the three regulatory jurisdictions covered by the project.

2-2 Test sample data collection: Oman, UAE & Singapore

Data collection for the project was planned to be in two main stages:

a. Test sample data collection: This is aimed at collecting relevant data on corporate governance disclosure and practices of listed companies and their corporate attributes for the years 2002 and 2003. The test nature of this process enables us to determine the level of response to our request for information from the companies.

b. Full sample data collection: This will entail collecting the substantive research data on corporate governance practices and disclosure as well as the corporate attributes of MSM-listed companies for 2004 and 2005.

For both stages, data were sourced through the annual reports of the companies, the database of the appropriate regulatory authority and, as necessary, a questionnaire administered on the companies to solicit additional corporate governance information. The first stage of the data collection process was concluded during Summer 2004.

11

2-3 Test sample data analysis: Oman & UAE vs. Singapore

Similar to the data collection process, data analysis was planned to progress in two main stages as

follows:

a. Test sample preliminary data analysis: The test sample data collected are analysed in the light of the corporate governance issues earlier conceptualized and identified. As part of the analytical process, the volume and quality of data availability for the research process are determined.

b. Substantive data analysis: Data collected on the listed company’s corporate governance practices and disclosures, as well as corporate attributes for the 2004 and 2005 accounting periods are analysed vis-à-vis the research’s main goals.

In both stages of data analysis, various statistical tools including exploratory data analysis, univariate

and multivariate techniques are employed as necessary.

2-4 Hypotheses and model development

Based on the outcome of the literature review, test sample data collection and analysis, it was

planned to develop and set-up relevant hypotheses and models for the research project. Given the

different stages of development of the three securities markets and their corporate governance

regulatory frameworks, it is anticipated that the nature of hypotheses and models developed for the

three jurisdictions will differ.

2-5 Presentation of preliminary results (conference)

Some of the preliminary results of the project, including conceptual and exploratory papers, were

submitted for presentation at relevant international conferences. The comments and feedback

received at such events were useful for further development of the project.

12

2-6 Review/restructure of hypothesis and model (if required)

Based on comments and feedback received, the research hypotheses and models were reviewed and

restructured as necessary. The aim of this process was to improve upon the original models and

allow for possible non-availability of data in any of the three research jurisdictions.

2-7 Full sample data collection: Oman, the UAE & Singapore

This is the second stage of the data collection process. Based on the experience gained from the test

sample data collection process, the full sample data collection for companies listed on the stock

exchanges of the three countries was undertaken. The full sample data collection process took non-

availability of data variables, as ascertained during the test sample data collection process, into

consideration.

2-8 Full sample data analysis: Oman & UAE vs. Singapore

In this second stage of the data analysis process, the research team proceeded to carry out the full

sample data analysis for the three research jurisdictions based on the full sample data collected so

far.

2-9 Presentation of project results (conferences & seminars)

The results of the project were presented at a number of international conferences and seminars.

Further presentations are planned for 2008

2-10 Write-ups of project results and reports

Finally, the project results and reports were written up by the research team. It is envisaged that a

number of research publications will emanate from this research project including conference

proceedings, journal articles and a book on corporate governance.

13

3. LITERATURE REVIEW

The advent of limited liability incorporation in the nineteenth century could be said to be the starting

point for corporate governance issues (Vinten, 1998). However, the subject has received little

attention in the last three decades, with the subject being brought from obscurity to the center of

attention of many academic and professional studies. This interest appears more appropriate at this

time, when business executives and auditors are continually being held to higher standards of

accountability and responsibility. Corporate governance has assumed a central place in the continued

effort to sanitize corporate reporting and shore up public confidence in financial markets around the

world. The issue seems to revolve around putting the right rules, regulations and incentives in place

to ensure transparency and accountability in the management of the affairs of corporate entities

(Cadbury Report, 1992). Corporate governance is receiving a lot of attention both in the

professional and academic literature (Brown 1999; Levitt 1998; Beasley et al. 1999; DeZoort and

Salterio 2001). It is viewed as an indispensable element of market discipline (Levitt 2000) and this

is fuelling demands for strong corporate governance mechanisms by investors and other financial

market participants (Blue Ribbon Committee 1999; Ramsay 2001). Arguably, emerging economies,

such as member nations of the GCC are likely to require more effective and stronger governance

mechanisms than their western developed counterparts if they are to become equal, full and active

participants in the global financial marketplace.

The term corporate governance describes the system by which companies are directed and

controlled. The overall objective of good governance is to ensure sustained growth or survival of

companies and the attainment of multiple goals of corporate stakeholders, that is, investors,

14

employees, and society in general (Charkham, 1994). It is defined as the system by which companies

are controlled, directed and made accountable to shareholders and other stakeholders; control being

understood as including indirect influences of financial markets (Demirag, 1998). Hence control is a

major element of corporate governance, both in terms of environment and organizational activities

(Committee of Sponsoring Organizations of the Treadway Commission (COSO), 1992; Public

Oversight Board (POB), 1993; Cohen and Hanno, 2000).

Organisational and financial control appears to be a major problem for a number of corporate

organizations in recent times and concerns are being expressed about the standards of accountability

and financial reporting of public companies. A number of big-name corporate collapses such as

Enron, Worldcom, Barlow Clows and Levitt, the Bank of Credit and Commerce International

(BCCI), Polly Peck International and Baring Bank, have made investors wary of corporate

governance systems. Major criticisms of the systems include the generous responsibilities given to

company directors with little accountability, the opportunity for the use of creative accounting

methods to manage accounting numbers, the lack of independence of auditing in some of the cases,

and short-terministic approach to setting the company’s strategy and future plans (Demirag, 1998).

Some extant literature documents corporate governance practices in various countries, including

Canada (Elloumi and Gueyie, 2001), Italy (Brunetti and Cecon, 1998), Japan (Doi, 1998), The

Netherlands (Groot, 1998), Poland (Dockery and Herbert, 2000), Turkey (Arat and Ugur, 2003), and

the UK (Demirag, 1998; Ezzamel and Willmot, 1993; Writer, 2001; Vinten, 2001; Weir and Laing,

2001). Others provide evidence of regional or multi-country practices including Dockery, Herbert

and Taylor (2000) – Europe, Walker and Fox (2002) – East Asia, Demirag (1998) – the UK and

15

International Comparison, and Vinten (2000) – UK and US. These studies examine different aspects

of the structure and practice of corporate governance. While a lot of research attention is being

focused on the subject, relatively few studies providing evidence of the practice in GCC countries

are currently in the public domain. Given the emerging nature of the economies of these nations, the

installation of effective corporate governance mechanisms is arguably more pertinent for them, if

they are to become full and active participants in the global financial marketplace. It is therefore

important that relevant and vigorous academic enquiries be pursued on the subject in these countries.

Comparative studies of corporate governance, performance pressures, and accountability of

management reveal significant variations among countries (Charkham, 1994). Some of these

differences may be traced to cultural differences (Hostede, 2001), institutional differences (North,

1990), political structures, and ownership forms (Thomsen and Pedersen, 1995), as well as board

composition and characteristics (Finkelsrein and Hambrick, 1996). Cultural differences between

countries, industries, and companies can explain a great deal of the diversities in corporate

governance structures and processes in different countries (Kuada and Gullestrup, 1998). For

example, the extent to which corporate governance is legally regulated will depend on the degree of

uncertainty avoidance in a society. To avoid uncertainty, societies may institute formal and/or

informal rules, which are used as regulatory mechanism to ensure that deliberate steps are taken to

guard against unacceptable future conditions. Hence, in societies where a viable coalition of

stakeholders is the primary objective of corporate governance, regulations encourage long-term

orientation of management decisions and professionalism in their implementation.

16

Despite the impact of cultural differences on corporate governance, there is evidence suggesting that

most of the issues and challenges of corporate governance in a rapidly changing global business

environment are similar, irrespective of geographical locations. Byrne (1996; 1997), for example,

found that too few people were constantly appearing on the same boards, and consequently,

attending too few board meetings, and that many board members had vested interest in the

companies and hence could not devote their full attention to management and control issues that

require objectivity and independence. Despite cultural differences, this is common in many other

countries, and notably so in GCC countries.

The literature on corporate governance has been primarily concerned with the principle-agent

relationship, with investors (the principals) employing managers (the agents) to run firms on their

behalf (Demirag, 1998). This concern has led to three distinct flows of thoughts on corporate

governance systems. The first is centered on issues regarding the principal (financial investors), the

second on the agent (board of directors and management in general), and the third on the

remuneration of principals and managers. Recently, the debate has extended beyond shareholders to

include other corporate stakeholders such as suppliers, purchasers and employees. Under this view,

agents are assumed to act in their own self-interests, irrespective of possible detriments to the

principal (Jensen and Meckling, 1976; Fama and Jensen 1983; Baysinger and Hoskisson 1990;

Bathala and Rao 1995). Effective corporate governance is an important cornerstone in the variety of

contractual mechanisms designed to monitor agents’ behaviour. Those performing the monitoring

function should be independent of those being monitored (Cohen et al, 2002).

17

Despite the existence of different corporate governance structures, the basic building blocks of the

structures are similar. They include the existence of a company, directors, accountability and audit,

directors’ remuneration, shareholders and the annual general meeting (AGM). Cadbury (1992),

Greenbury (1995) and Hampel (1998) called for greater transparency and accountability in areas

such as board structure and operation, directors’ contracts and the establishment of board monitoring

committees. In addition, they all stressed the importance of the non-executive directors’ monitoring

role. Cleghorn (1997) argues that there is no one system of corporate governance that is suitable for

all organizations, or even the same organization at all times. Given the three principal roles of boards

of directors of: (1) safeguarding the interests of stakeholders; (2) overseeing long-term strategic

development and performance; and (3) selecting, evaluating and compensating top management,

there are bound to be differences in how this is approached in different settings. Perhaps of even

greater importance is how the level of accountability achieved as a result of effective corporate

governance strategies is transparently communicated to all stakeholders.

This research project examines various corporate governance issues in Oman and the UAE, and

compares these to developments in Singapore. Particular attention is paid to various corporate

governance mechanisms, and the key organizational attributes contributing to good corporate

governance practices.

In April 2002, the Capital Markets Authority (CMA) in Oman published a Corporate Governance

Code, which requires all companies listed on the MSM to disclose their corporate governance

practices. This was amended and re-issued in April 2003. In the UAE, the Abu Dhabi Securities

Market (ADSM) has published a three-stage listing rule, which deals with corporate governance

18

matters, as well as a draft Corporate Governance Code: Guidelines for Best Practice. In Singapore,

the Corporate Governance Committee issued a report which formed the basis of the Code of

Corporate Governance in March 2001. This was subsequently upgraded and re-issued in 2005. The

next section details the institutional framework for the current research project in each of these three

different jurisdictions, including descriptions of their key financial and capital market institutions.

As mentioned previously corporate governance is a multi-disciplinary research field and has a range

of meanings and definitions depending on how one uses it and which discipline and which country

one is considering. Traditional finance literature has indicated several mechanisms that help solve

corporate governance problems, however the use of these mechanisms depends on the corporate

governance system prevalent in the country. So we will shed the light on the governance systems,

which deal with the corporate governance at the level of the countries, before discussing in details

the governance mechanisms, which deal with the corporate governance at the level of the firms.

A system of corporate governance is defined as a more-or-less country-specific framework of legal,

institutional and cultural factors shaping the patterns of influence that stakeholders (e.g. managers,

employees, shareholders, creditors, customers, suppliers and the government) exert on managerial

decision-making. Among others, Scott (1985), De Jong (1989), and Moerland (1995a,b) propose

four groups of relatively rich, industrialized countries for which more or less resembling so-called

corporate systems can be identified: (1) Anglo-Saxon countries (the USA, the UK, Canada and

Australia), (2) Germanic countries (Germany, the Netherlands, Switzerland, Sweden, Austria,

Denmark, Norway and Finland), (3) Latin countries (France, Italy, Spain and Belgium) and (4) Japan

(which is considered an isolate).

19

Arguing that the debate on corporate governance in an international context is hampered by the lack

of a coherent framework and based on the previous classification, Weimer and Pape (1999) proposed

a taxonomy of systems of corporate governance based on the following eight characteristics which

All have legal, institutional and cultural dimensions:

a. The prevailing concept of the firm; b. The board system; c. The salient stakeholders able to exert influence on managerial decision-making; d. The importance of stock markets in the national economy; e. The presence or absence of an external market for corporate control; f. The ownership structure; g. The extent to which executive compensation is dependent on corporate performance; h. The time horizon of economic relationships.

Weimer and Pape assayed these characteristics for the different country groups and distinguished

between "market-oriented" and "network-oriented" systems of corporate governance. The paramount

characteristic of the market-oriented systems is an active external market for corporate control,

which serves as a mechanism for independent shareholders to influence managerial decision-making.

Such markets include: stock market, labour market and hostile takeover market.

By contrast, in the network-oriented systems "oligarchic" groups substantially control managerial

decision-making via networks of relatively stable relationships (same terminology used by Moerland

(1995a, b)). The most common forms of networks are cross-shareholdings and inter- locking

directorships. The market-oriented systems prevail in the Anglo-Saxon countries. Largely based on

the identity of oligarchic groups, different classes of network-oriented systems can be recognized for

Germanic countries (e.g. Germany, where banks and employees are influential), Latin countries (e.g.

France and Italy, where family control is relatively important), and Japan (where banks serve as the

nucleus of mutually related, vertically and horizontally integrated groups of firms).

20

Franks and Mayer (1997) and Shleifer and Vishny (1997) provide a similar classification of

governance systems with two kinds of systems as follows: (1) Market-oriented systems, such as

those in US and UK, that tend to rely more on managerial compensation and the market for

corporate control to solve corporate governance problems and (2) Large shareholders oriented

systems, such as those in Germany, France or Spin, which tend to use control by large incumbent

shareholders to align the behaviour of managers and owners. Some researchers , such as Cuervo

(2002) among others, term the shareholders control systems in German, France and Spain" the

Continental European systems", and the market control systems in US and UK "Anglo-Saxon

systems".

The large shareholder control or Continental European system is characterised by the following

features:(1) ownership is concentrated; banks, companies, and families are large shareholders; (2)

control is assumed to be exercised by large shareholders; (3) the board of directors is controlled by

internal directors or external directors linked to large shareholders; (4) capital markets are relatively

illiquid and have limited control ability; (5) there exist implicit contracting and close personal trust

relationships among managers; (6) long-term lender-borrower relationships and bank ownership of

equity are maintained; (7) there is no active market for control; that is, management does not face

hostile takeover bids; and (8) banks play major role in corporate governance, trough equity stakes,

proxies given to them by small investors and bankers' position on the boards of firms (Baums

(1993); Kester (1997) and Cuervo (2002)).

The market control or Anglo-Saxon system is characterised by the following features: (1) ownership

is diffuse except for institutional investors; (2) control is vested in the board of directors, with

external directors playing an important role; (3) capital markets are very liquid and there is a

developed market for corporate control and takeover market; and (4) there is more defence of the

21

ownership rights of shareholders over the rights of debtholders than in the Continental European

model; that is, legal protection acts as a substitute for ownership structure La Porta et al., (1997).

Neither system is perfect. In the market control system, the reduction in the operation of the market

for corporate control gave rise to activism by large institutional investors Useem (1993). In the large-

shareholder control system, abuses by managers and large shareholders led to the establishment of

codes of good corporate governance (Cadbury Commission, 1992). So, the more recent years have

been witnessed a new line of research describes, analyzes and tries to reach "the best" or practically

speaking the "good" code of corporate governance mechanisms within specific system, namely for

each country or for each several countries share almost same features.

Traditional finance literature has indicated several mechanisms that help solve corporate governance

problems (Jensen and Meckling (1976); Fama (1980); Fama and Jensen (1983b); Jensen (1986);

Jensen (1993); and Turnbull (1997). There is a consensus on the classification of corporate

governance mechanisms to two categories: internal and external mechanisms. However, there is a

dissension on the contents of each category and the effectiveness of each mechanism. In addition,

the topic of corporate governance mechanisms is too vast and rich research area to the extent that no

single paper can survey all the corporate governance mechanisms developed in the literature and

instead the papers try to focus on some particular governance mechanisms.

Jensen (1993) criticises the existing governance mechanisms in USA, UK, Japan and Germany and

outlines four basic categories of individual corporate governance mechanisms: (1) legal and

regulatory mechanisms; (2) internal control mechanisms; (3) External control mechanisms; and (4)

product market competition. In their survey of corporate governance, Shlifer and Vishny (1997)

22

concentrate on: incentive contracts, legal protection for the investors against the managerial self-

dealing, and the ownership by large investors. Shlifer and Vishny point out the costs and benefits of

each governance mechanism.

Denies (2001) provides the following four mechanisms: (1) legal and regulatory mechanisms exist

outside the firm; (2) internal control mechanisms within a firm, (which include; the board of

directors; executive compensation and ownership; non executive owners; and debt); (3) external

control mechanisms such as the corporate takeover market; and (4) product market competition.

Then Denis and McConnell (2003) survey the international corporate governance concentrating on

countries other than United States and using a dual classification of corporate governance

mechanisms (They use systems as synonym to mechanisms) as follows: (1) internal governance

mechanisms including: boards of directors and ownership structure and (2) external ones including:

the takeover market and the legal regulatory system.

Farinha (2003) surveys two categories of governance (or disciplining) mechanisms, the first one is

the external disciplining mechanisms including: takeovers threat; product market competition;

managerial labour market and mutual monitoring by managers; security analysts; the legal

environment; and the role of reputation. The other category is the internal disciplining mechanisms

which include: large and institutional shareholders; board of directors; insider ownership;

compensation packages; debt policy; and dividend policy.

Large shareholders and institutional investors (Demsetz (1983); Demsetz and Lehn (1985); and

Shleifer and Vishny (1986)) can be seen as potential controllers of equity agency problems as their

increased shareholdings can give them a stronger incentive to monitor firm performance and

23

managerial behaviour. This potentially helps to circumvent the free rider-problem associated with

ownership dispersion. Another potential benefit relates to the potential challenge that large

shareholders offer to outside raiders, thus increasing the takeover premium Burkart (1995).

Consistent with these benefits, Mikkelson and Ruback (1985) and Holderness and Sheehan (1985)

report positive abnormal returns around the announcement of outsiders' acquisition of large equity

positions. In the UK, Sudarsanam (1996) looks at the relation between block acquisitions and

subsequent takeover attempts for the target companies and reports that large block acquisitions

(between 5% and 30% of the target's shares) not just lead to significant abnormal returns

surrounding its announcement but also influence the likelihood of takeover bids, hostile bids and the

success of bids.

One rather intuitive way by which equity agency costs can be reduced is by increasing the level of

managers' stock ownership, which may permit a better alignment of their interests with those of

shareholders. In fact, in the extreme case where the manager's share ownership is 100%, equity

agency costs are reduced to zero (Jensen and Meckling, 1976). As managerial ownership increases,

managers bear a large fraction of the costs of shirking, perquisite consumption and other value-

destroying actions. Further, larger share ownership by managers reduces the problem of different

horizons between shareholders and managers if share prices adjust rapidly to changes in firm’s

intrinsic value.

A limitation, however, of this mechanism as a tool for reducing agency costs is that managers may

not be willing to increase their ownership of the firm because of constraints on their personal wealth.

24

Additionally, personal risk aversion also limits the extension of this monitoring device as the

allocation of a large portion of the manager's wealth to a single firm is likely to translate into a badly

diversified portfolio (Beck and Zorn, 1982). Management buyouts, whereby insiders increase

dramatically their shareholdings in the firm, provide a natural field study for the effects of insider

ownership in the reduction of conflicts between owners and managers.

In accordance with the proposition that larger managerial ownership reduce agency costs, Kaplan

(1989) finds that following large management buyouts, firms experience significant improvements in

operating performance. He interprets this evidence as suggesting that operating changes were due to

improved management incentives instead of layoffs or managerial exploitation of shareholders

through inside information. Smith (1990) reports similar results and notes that the amelioration

observed in operating performance is not due to reductions in discretionary expenditures such as

research and development, advertising, maintenance or property, plant and equipment.

In a study of the effects of changes in ownership structure on performance for a sample of thrift

institutions that converted from mutual to stock ownership, Cole and Mehran (1998) find that

changes in performance are significantly associated with changes in insider ownership. They

document that the greater the increase in insider ownership, the greater the performance

improvement, which is consistent with the alignment of interests hypothesis arising from a larger

insider ownership. Also consistent with that hypothesis of Subrahmanyam, Rangan and Rosenstein

(1997) who find evidence, in a sample of successful bidders in bank acquisitions, of a positive

association between bidder returns and the level of insider ownership when the latter exceeds 6%.

Research by Morck, Shleifer and Vishny (1988), McConnell and Servaes (1990) and Hermalin and

Weisbach (1991) is also consistent with the view that insider ownership can be an effective tool in

25

reducing agency costs, although they report a non- monotonic relation. This functional form has been

related to the observation that, within a certain ownership range, managers may use their equity

position to entrench themselves against any disciplining attempts from other monitoring mechanisms.

However, some other studies find no evidence of a positive relationship between insider ownership

and performance (see, for instance, Demsetz and Lehn, 1985; Loderer and Sheehan, 1989;

Holderness and Sheehan, 1988; Denis and Denis, 1994; and Loderer and Martin, 1997). Moreover,

the studies that find a positive relationship typically present results that have very low explanatory

power (R2s usually between 2% and 6%).

A possible explanation for these mixed results is that many of the studies do not properly distinguish

the possibility of alignment of interests across a certain range of ownership values and of

entrenchment over another range. Furthermore, these analyses usually do not take into account the

possibility that several different mechanisms for alignment of interests can be used simultaneously,

with substitution effects with insider ownership. It is quite conceivable that different firms may use

different mixes of corporate governance devices (Rediker and Seth, 1995).

These different mixes can, however, all be optimal as a result of varying marginal costs and benefits

of the several monitoring instruments available for each firm. If so, then one would not be able to

observe a relationship between performance and any of these particular mechanisms.

A different type of monitoring vehicle is related to the potential links between managerial

compensation and firm performance. In theory, a strong relation between compensation and firm

performance would enable a better alignment of interests between shareholders and managers

(Jensen and Murphy, 1990). Relevant elements of the compensation package typically include stock

26

related rewards, deferred cash compensation and dividend policy-dependent compensation.

Evidence of such a significant link is, however, not strong. Lewellen, Loderer and Martin (1987), for

example, find evidence in support of the hypothesis that compensation packages are designed to

reduce agency costs. However, a comprehensive analysis of CEO pay in the US by Jensen and

Murphy (1990) concludes that most compensation contracts are characterised by a general absence

of real management incentives and that observed compensation patterns are inconsistent with the

implications of formal agency models of optimal contracting. Similarly, Yermack (1995) reports that

observed stock options performance incentives have no significant association with explanatory

variables related to agency costs reduction. In the UK, Gregg, Machin and Szymansky (1993) reach

similar conclusions as they find a very weak relation between pay and performance for the period

1983-88 and no relation after that. They observe however, a strong association between pay and

asset growth.

Jensen and Murphy (1990) and Shleifer and Vishny (1997) argue that the empirically observed lack

of sensitivity of pay to performance is caused by legal and political external factors common to

many countries. In addition, Haubrich (1994) shows that it may not be optimal to include a large

sensitivity of pay to performance in managers' compensation contracts as this would require a large

risk tolerance from the part of managers, which is not an efficient incentive system for more risk-

averse managers. Furthermore, Yermack (1997) documents that managers can time stock options to

their advantage as he finds that stock options are granted just before the announcement of good news

and tend to be delayed until after bad announcements. Shleifer and Vishny (1997) view the overall

evidence on the relationship between pay and performance as suggesting that it is "problematic to

argue that incentive contracts completely solve the agency problem (p. 745)".

27

The theoretical background of this mechanism has been dated back to the ideas of Manne (1965) and

recently was developed by Jensen and Meckling (1976), Grossman and Hart (1980) and Fama and

Jensen (1983) given that there is an active market for corporate control. Due to the free rider

problem, small shareholders have little incentive to monitor management but this problem can

potentially be avoided by the use of the takeover mechanism. According to this view, if management

is inefficient or not acting in shareholders' interests, a "raider" could make a takeover bid, buying the

firm at a low price, managing it better and eventually selling it back with a profit. A feature of the

takeover mechanism is that it potentially applies in an indiscriminate way to all firms, in this sense

one may call it a general disciplining mechanism. In support of this perspective, Easterbrook and

Fishel (1991) and Jensen (1993) regard takeovers in the US as an essential corporate governance

mechanism to control managers' discretionary actions.

The empirical evidence showing that takeovers lead to significant positive price impacts on the

takeover target is consistent with this perspective (although also with alternative views, e.g.

synergistic gains). However, the takeover mechanism is not without problems. Grossman and Hart

(1980) point out that this mechanism can be undermined if shareholders can free ride on the raider's

improvement of the corporation (by refusing to sell their shares) unless the corporate charter or law

includes exclusionary devices able to deal with this free riding problem. In addition, takeovers

involve not just the costs needed to induce reluctant shareholders but also search costs, bidding costs

and other transaction costs (Williamson, 1970) that make takeovers in practice a very expensive

solution.

Therefore, in the presence of this monitoring mechanism alone, managers are free to deviate from an

optimal performance as long as they don't cause the firm price to decline more than the costs of a

28

takeover. Moreover, in recent years the adoption of defensive tactics, corporate charter amendments

or even anti-takeover legislation have further increased the costs and risks of takeovers, notably in

the US.

Also, takeover corrections of managerial failure have the disadvantage that they are ex-post

corrections, whereas other mechanisms may be ex-ante or "deterring" disciplining devices. As such,

when disciplining takeovers occur, it is usually too late to avoid the huge direct and indirect costs

associated with the effects of past sub-optimal managerial actions. Thus, in this sense one can argue

that the takeover threat is a more efficient mechanism than the takeover itself, although the

credibility of that threat may require the observation of some hostile takeover activity in the market.

Consistent with the view that takeovers are a source of managerial discipline, Martin and McConnell

(1991) find evidence of increased management turnover after successful takeovers, and more

frequent turnover when acquired companies previously underperformed their industry. Shivdasani

(1993) shows results consistent with the view that hostile takeovers provide discipline when internal

governance mechanisms such as the board of directors fail to control management's non value

maximising behaviour.

Also, Mikkelson and Partch (1997) document that the decrease in takeover activity in the US from

1984-88 to 1989-93 was accompanied by a reduction in disciplinary pressure on managers. They

show that the relation between management turnover and performance is significant only during the

period where the takeover market was more active.

In most of Continental Europe, with the exception of the UK, hostile takeovers are, however, rare.

Franks and Mayer (1994) attribute this fact to the particular structure of most European capital

29

markets, characterised by a small number of listed companies and a relatively high concentration of

ownership as compared to the US and UK.

In their analysis of UK takeovers, Franks and Harris (1989) report shareholder wealth impacts of

takeovers similar to those observed in the US. Kennedy and Limmack (1996) analyse the

performance of takeover targets in the pre-takeover period and its relationship with subsequent CEO

turnover and find evidence consistent with takeovers acting in the UK as disciplinary mechanisms on

managers. They observe that CEO turnover tends to increase following takeovers, and that target

firms that do replace CEOs after takeovers ("disciplinary takeovers") experience lower returns

before takeover than other targets. In contrast, Franks and Mayer (1996) reject the hypothesis that in

the UK hostile takeovers perform a disciplining function. They assert that the apparent rejection of

hostile bids by target management seems to be derived not from managerial entrenchment but from

opposition to post-takeover redeployment of assets or renegotiation over bid terms.

In another UK study, Sudarsanam, Holl and Salami (1996) present the result that a better previous

relative performance of bidder over target (measured by their relative market-to-book ratio) is a

significantly positive influence on target's abnormal returns surrounding a takeover bid

announcement but a negative one bidder's returns. This result is not strictly in accordance with a

disciplinary perspective of takeovers where value enhancements would be expected to occur for both

targets and bidders. Sudarsanam, Holl and Salami (1996) interpret their evidence, instead, as

consistent with Roll's (1986) hypothesis that bidder managers may suffer from "hubris" that leads

them to overestimate the benefits of a takeover and pay excessive takeover premia. The UK evidence

on the disciplinary role of takeovers thus appears to be, in contrast to US studies, inconclusive.

C.2 Managerial Labour Market and Mutual Monitoring by Managers

30

Fama (1980) argues that "each manager has a stake in the performance of the managers above and

below him and, as a consequence, undertakes some amount of monitoring in both directions (p.

293)". This is related to the view that the managerial labour market may use the performance of the

firm to determine each manager's opportunity wage. Additionally, each manager may sense that his

marginal product is likely to be a positive function of the efficiency of managers not just below but

also above him. Managers are then reckoned to perceive a gain in stepping over inefficient managers

located above. Fama (1980) thus reckons that the existence of a managerial labour market is a key

factor influencing the level of mutual monitoring by managers. Alongside this indirect influence,

Fama (1980) sees this market as exercising a direct pressure on the firm to sort and compensate

managers according to their performance in order to prevent the best managers from leaving and

keep the firm's attractiveness to potentially highly performing managers.

Consistent with the monitoring role of the board of directors, Coughlan and Schmidt (1985) present

evidence that poor performance increases the likelihood of top management turnover and that

corporate boards managerial compensation decisions are related to the firm's performance. In

accordance with Fama's (1980) assertion that the managerial labour market uses information on past

performance to set wages and define alternative job opportunities for executives, Gilson (1989)

analyses the subsequent careers of executives resigning from firms that experienced financial

distress. He finds that these executives hold around one-third fewer seats on the boards of other

companies. Also, Kaplan and Reishus (1990) report evidence consistent with top executives of

dividend-reducing firms being 50% less likely to receive additional directorships than executives of

on dividend-reducing companies. Cannella, Fraser and Lee (1995) report similar results in their

study of the careers of executives of failing Texan banks. In addition, they find that the labour

market distinguishes between managers who lose their prior positions for reasons beyond their

31

control and those that were directly involved in the institution's failure. They report that managers

associated with banks that fail for reasons arguably beyond the managers' control are twice more

likely to regain comparable banking posts than managers at other failed banks.

However, the effectiveness of mutual monitoring by managers has been questioned. As Hansen and

Torregrosa (1992) observe, "imprecise measurement of manager efforts (due to bad judgment, moral

hazard or poor information) and managerial entrenchment limit the effectiveness of the internal

assessment mechanism (p. 1539)". Fama (1980) concedes that, at board level, top management may

engage in collusive arrangements, which might result in the expropriation of security holders'

wealth. Consistent with these assertions, Warner, Watts and Wruck (1988) present evidence of

inefficient internal assessment mechanisms over top management. They report that only when

unfavourable firm performance is extreme do internal mechanisms seem to lead to management

changes and, even so, the response to bad performance doesn't seem to come without a considerable

time lag. Also, Mace (1986) and Lorsh and MacIver (1989) find that CEOs tend to dominate the

nomination process of new board members.

Another external factor that can influence corporate governance is the legal environment. This may

manifest itself in several ways. One is in the form of legislation that directly affects the efficiency, or

the cost, of one or more monitoring devices. For instance, in the US many States have passed

legislation designed to avoid or increase the costs of hostile takeovers. This causes a severe impact

on the existence of the takeover device as a general mechanism to control managerial actions within

these States. Another example is the existence of legal rules giving a particular importance to

dividend policy as a potential instrument for dealing with potential equity agency problems. This is

the case with Brazil, Chile, Colombia, Greece and Venezuela, countries where companies face

32

mandatory dividend rules.

In other nations, the role of the legal environment can be somewhat more subtle. In the UK, this has

taken the form of a number of committees that set up recommendations destined to improve

corporate governance practices at the board of directors' level. These have been materialised in the

Cadbury (1992), Greenbury (1995) and Hampel (1998) Reports. Recommendations emanating from

these reports have been adopted by the London Stock Exchange in the form of an official

requirement for listed companies to state the extent of their compliance with these recommendations,

although the rules formulated by these committees have not been made directly compulsory.

An important insight on the consequences of this kind of state-originated recommendations has been

given by Dahya, McConnel and Travlos (2002), who analyse the relationship between CEO turnover

and corporate performance before and after the publication of the Cadbury (1992) Code in the UK.

They find that after the issuance of the Code, the negative relationship between CEO turnover and

performance becomes much stronger, with the increase in sensitivity between these two variables

being concentrated among adopters of Cadbury's (1992) recommendations.

Another important area of the legal environment, which also may influence corporate governance

devices, is that concerned with the protection of minority shareholders. Laporta, Lopez-de-Silanes,

Shleifer and Vishny (1997) find that the existence and efficiency of legal rules protecting investors

are a major determinant of the development of local capital markets. If the extent of the corporate

governance problem is conceivably a deterrent to external capital raising, this can be interpreted as

suggesting that the quality of the legal system of investor protection is a major determinant on the

ability of firms and investors to set up appropriate corporate governance structures Some other

aspects of the general legal environment may also lead to consequences for corporate governance.

33

For instance, the UK Company Law defines a mandatory rights issue requirement (pre-emptive

rights) for equity issues that can be waived in general terms by means of a special resolution

approved annually by shareholders.

As Franks, Mayer and Renneboog (1998) observe, this requirement affects the relative costs of

alternative forms of corporate control, providing investors in the UK with the power to impose

control changes as part of the condition of the provision of new finance. In the US, although similar

rights issues requirements are allowed to be included in companies' articles of association, they are

not compulsory and seldom exist in practice. This in effect may be in part responsible for the

different governance structures observable in these countries. Also consistent with the perspective

that the legal environment has a significant impact on the structure of corporate governance is Black

and Coffee's (1994) comparative study of the legal structures in the US and the UK surrounding

institutional investors' behaviour. They observe that the regulation of each type of institutional

investor is a partial determinant of institutional investors' willingness to be involved in monitoring

managerial actions.

They also point out that another potentially important factor influencing institutional shareholders'

activism is the existence of legal barriers to institutional coalition formation. Similarly, Black (1998)

suggests that some legal rules, namely the 13D filing requirement with the SEC for groups of

shareholders acting together on a voting issue, are a plausible partial explanation for the general lack

of shareholder activism by American institutional investors.

34

4. INSTITUTIONAL FRAMEWORK

This report presents initial findings of a comprehensive investigation of corporate governance

developments and practices in Oman and the UAE, as compared to developments in Singapore. The

project examined various facets of corporate governance as an issue for companies listed on the

MSM in Oman, the ADSM and DFM in the UAE, and the SGX in Singapore. The environment and

institutional framework of the location of the research project are discussed in this section.

4.1 Oman - Muscat Securities Market

The government of the Sultanate of Oman realized sometime ago that in order to keep pace with

international developments and enable the vision of a solid economy that will be recognised

internationally, it was necessary to have a strong financial sector based on well-established financial

companies. This is expected to provide a suitable enabling environment for successful companies

and projects that will add value to the country’s economic cycle. To realise these objectives, it was

decided to set up a Stock Exchange, the Muscat Securities Market (MSM), set up by Royal Decree

53/88 of 21 June 1988. The decree set the legal framework for the establishment of the market as an

independent organisation to regulate and control the Omani securities market and to participate with

other organisations in setting up the infrastructure of the Sultanate’s financial sector. After ten years

of continuous growth of the national economy in general and the market in particular, and to cope

with new developments in the local and international financial sector, particularly in the securities

industry, it was decided that there was a need for better control and regulation of market activities,

so as to provide better protection to investors. To achieve this, it was decided to split the functions of

regulation and market activities, both of which were until then functions of the MSM. Existing laws

and regulations were amended to bring the market closer to international standards of practice,

35

where the norm is to have an independent regulator, with regulatory authority over the Exchange and

market participants.

The MSM was restructured by the issue of two Royal Decrees 80/98 and 82/98. Royal Decree 80/98

of 9 November 1998 provided for the establishment of two separate entities:

• a regulator, to be named the Capital Market Authority (CMA), which will be a governmental

authority responsible for organizing and overseeing the issue and trading of securities in the

Sultanate; and

• an exchange, to be named the Muscat Securities Market (MSM), where all listed securities

shall be traded. The exchange shall also be a governmental entity, financially and

administratively independent from the authority but subject to its supervision. The board of

directors shall be elected from among members of public (governmental commercially

oriented) corporations, listed companies, intermediaries, and the Central Bank of Oman.

Royal Decree 82/98 of 25 November 1998 established the Muscat Depository and Securities

Registration Company, a closed joint stock company, as the sole provider, of the services of

registration and transfer of ownership of securities and safe keeping of ownership documents

(depository) in the Sultanate. This company is linked through an electronic system to the MSM for

easy data transfer.

The CMA was established as a public authority in accordance with Royal Decree No.80/98 issued on

9 November 1999, and effective from 15 January 2000. The major responsibilities of the Authority

are to organise, licence, and monitor the issue and trading of securities, to supervise the operation of

36

the Muscat Securities Market, and to supervise all companies operating in the field of securities

(Source: www.cma-oman.gov.om). The Authority, with a mission to “maintain fair, efficient

and transparent" market activities, has the following objectives:

the advancement of the competence of the market and protection of investors from unfair and

unsound commercial practices;

the provision of opportunities for the investment of savings and funds in securities in the

interest of the national economy;

the regulation and control of the issue of securities in the Primary Market and the definition of

the requirements of prospectuses on securities offering for public subscription;

the facilitation and expedition of the mobilization of funds invested in securities and to

guarantee response to the supply and demand factors with the aim of determining the prices of

such securities and protecting small investors by establishing the bases of sound and fair

dealing among the different categories of investors;

the undertaking of studies and making recommendations to different official bodies on the laws

in force and their amendment to be in line with the requirements of the securities market;

contacting and engaging financial markets overseas in a continuous process of acquiring and

exchanging information and experiences in order to keep pace with advanced dealing methods

in the global markets and to accelerate the development of the Omani financial market; and

the establishment of principles of professional conduct, self-supervision and good behavior

among intermediaries and dealers, and the encouragement and qualification of the

intermediaries and other employees of the market in order to raise their academic and practical

competence.

37

Figure 1: Organisational Chart of the Omani Capital Market Authority (CMA)

Source: The CMA website

Figure 1 depicts the organizational chart of the CMA. Since 2000, the CMA has implemented a

number of measures aimed at strengthening its regulatory role and improving the performance

MSM-listed companies. These include: the introduction of controls on related party transactions in

the public joint-stock companies, introduction of new requirements for the appointment of board

directors, the measures taken with regard to the falling companies, etc. Perhaps the most important

measure implemented to date was the introduction of a Code of Corporate Governance for

companies listed on the MSM in June 2002 as amended in April 2003. As this Code is central to the

objective of this research project, it is discussed further in Section 3.12 of this report.

38

4.2 The Omani Corporate Governance Code – June 2002 and April 2003

In a timely response to developments across the world of capital markets regulation, the CMA, in

June 2002, published its Corporate Governance Code (Circular No. 11/2002), which was later

amended and replaced by Circular No. 1/2003 of April 2003. The Code, which was slated to apply to

financial statements published by MSM-listed companies from June 3, 2002, required all listed

companies to publish a section on corporate governance in their financial statements. A copy of the

Corporate Governance Code is attached as Appendix 1 to this study.

The Code contains 28 articles requiring companies to disclose corporate governance issues such as

the composition of their board of directors (BOD), number of meetings and functions of the BOD,

audit committee composition, expertise and terms of reference, audit and internal control matters,

appointment and terms of appointment of executive management, disclosure of related party

transactions, certification of CG report by company auditor and disclosure of areas of non-

compliance with CG Code requirements. While it is not as elaborate as other Corporate Governance

codes such as the Combined Corporate Governance Code in the UK and the Code of CG in

Singapore, the Omani CMA Code can be said to provide adequate coverage of the key disclosure

issues of relevance in a market with a nascent disclosure culture.

MSM-listed companies are required to disclose key corporate governance issues in a separate section

of their annual report. A list of suggested items to be included in their report on CG is presented in

Table 1 below.

39

Table 1: Suggested list of items to be provided in MSM-listed Company’s report on CG

1 Company’s philosophy on code of governance and a descriptive report on how the company has applied the principles of corporate governance as stated in annexure 1.

2 Board of Directors: 2.1 Composition and category of directors for example executive, non-executive, independent and

nominee director (with institution represented as lender or as equity investor). 2.2 Attendance of each director at the board meetings and the last AGM. 2.3 Number of other boards or board committees he/she is a member or chairperson. 2.4 Number of board meetings held and dates of the meetings.

3 Audit Committee and other committees: 3.1 Brief description of terms of reference 3.2 Composition, name of members and Chairperson 3.3 Meetings and attendance during the year

4 Process of nomination of the directors

5 Remuneration matters: 5.1 Details of remuneration to all directors and top 5 officers individually including salary, benefits,

perquisites, bonuses, stock options, gratuity and pensions etc 5.2 Details of fixed component and performance linked incentives along with the performance

criteria 5.3 Service contracts, notice period and severance fees

6 Details of non-compliance by the company 6.1 Penalties, strictures imposed on the company by MSM/CMA or any statutory authority, on any

matter related to capital markets, during the last three years

7 Means of communications with the shareholders and investors: 7.1 Whether half-yearly results were sent to each shareholder 7.2 Name of the web-site where these were posted 7.3 Whether the web-site of the company displays official news releases 7.4 Presentations made to institutional investors or to the analysts 7.5 Whether MD&A is part of annual report or not 8 Market price data: 8.1 High/low during each month in the last financial year 8.2 Performance in comparison to board based index of MSM (relevant sector) 8.3 Distribution of shareholding 8.4 Outstanding GDRs/ADRs/Warrants or any Convertible instruments, conversion date and likely

impact on equity

9 Specific areas of non-compliance with the provisions of corporate governance and reasons 10 Professional profile of the statutory auditor 11 Any other important aspect

40

The disclosure of these important pieces of corporate governance information should go a long way

in promoting transparency and accountability, thereby bolstering investor confidence. For this to be

achieved, MSM-listed companies would need to respond in a positive and timely manner to the

CMA's requirements. In the current study, we document the corporate governance reporting

practices of MSM-listed companies between 2002 and 2006.

4.3 The State of Corporate Governance in the UAE

The UAE has an open economy with a high per capita income and sizable annual trade surplus. Its

wealth is based on oil and gas output, and the fortunes of the economy fluctuate with the prices of

those commodities. Since the UAE discovered the oil 30 years ago, the country has undergone a

profound transformation from an impoverished region of small desert principalities to a modern state

with a high standard of living (the World Factbook, 2006).

The UAE corporate sector began to develop in the middle of the seventies, which witnessed the

creation of many companies due to the rise in oil prices and the strong interest of the federal

government to build a strong national economy. All companies operate under Federal Commercial

Law No 8/1984 and its amendments.

Over the past five years, the UAE corporate sector has grown rapidly due to the inception of the

country’s official stock market and the federal tendency toward privatizing some large infrastructure

companies. The main regulatory bodies in the UAE corporate sector are the Ministry of Economy,

the Central Bank, and the Emirates Securities & Commodities Authority (ESCA). In addition, the

41

State of Audit (i.e., Federal Auditing Organization) has the right to monitor any company that is

financed with federal funds.

The UAE stock market was inaugurated in 2000 and is represented by two governmental security

exchanges, Dubai and Abu Dhabi, under the supervision of the ESCA. Compared to other stock

markets in the region, the UAE stock market is a relatively new and small one. However, from 2004

to today, it has enlarged, gained strength, and became more active in terms of the number of IPOs

and the listed companies, market capitalization, and the range of market participants such as

brokerage firms and investment funds.

Due to the diffusion of corporate governance themes all over the world and to the continued merging

between the country’s economy and the global economy, the UAE has recently given more attention

to the application of international standards of corporate governance to all listed companies on the

local securities markets. The ESCA issued in April 2007 “Corporate Governance Regulations for

Joint-Stock Companies and Criteria for Institutional Discipline”. This document is designed to

improve the corporate governance system for the listed firms, and it focuses mainly on independence

within the board, the qualities and responsibilities of the board, and the requirements for both of

executives and disclosure. This would greatly strengthen the internal control system and improve

the integrity of financial reporting, competition, and market trust. The corporate governance practice

is still in its early stages and needs to be developed and regulated. There is speculation that the

UAE will fully implement a code of corporate governance in 2010.

42

The organizational chart of the ESCA is presented in Figure 1 below. Table 2 provides a

comparative analysis of the CG Codes of Oman, UAE and Singapore.