Detection and Estimation Theory - MBWCLmoblie123.cm.nctu.edu.tw/EnD106/Overview of detection...

68

Institute of Communications Engineering, EE, NCTU 1 Detection and Estimation Theory Sau-Hsuan Wu Institute of Communications Engineering National Chiao Tung University

-

Upload

hoangnguyet -

Category

Documents

-

view

262 -

download

4

Transcript of Detection and Estimation Theory - MBWCLmoblie123.cm.nctu.edu.tw/EnD106/Overview of detection...

Institute of Communications Engineering, EE, NCTU 1

Detection and Estimation Theory

Sau-Hsuan WuInstitute of Communications Engineering

National Chiao Tung University

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 2

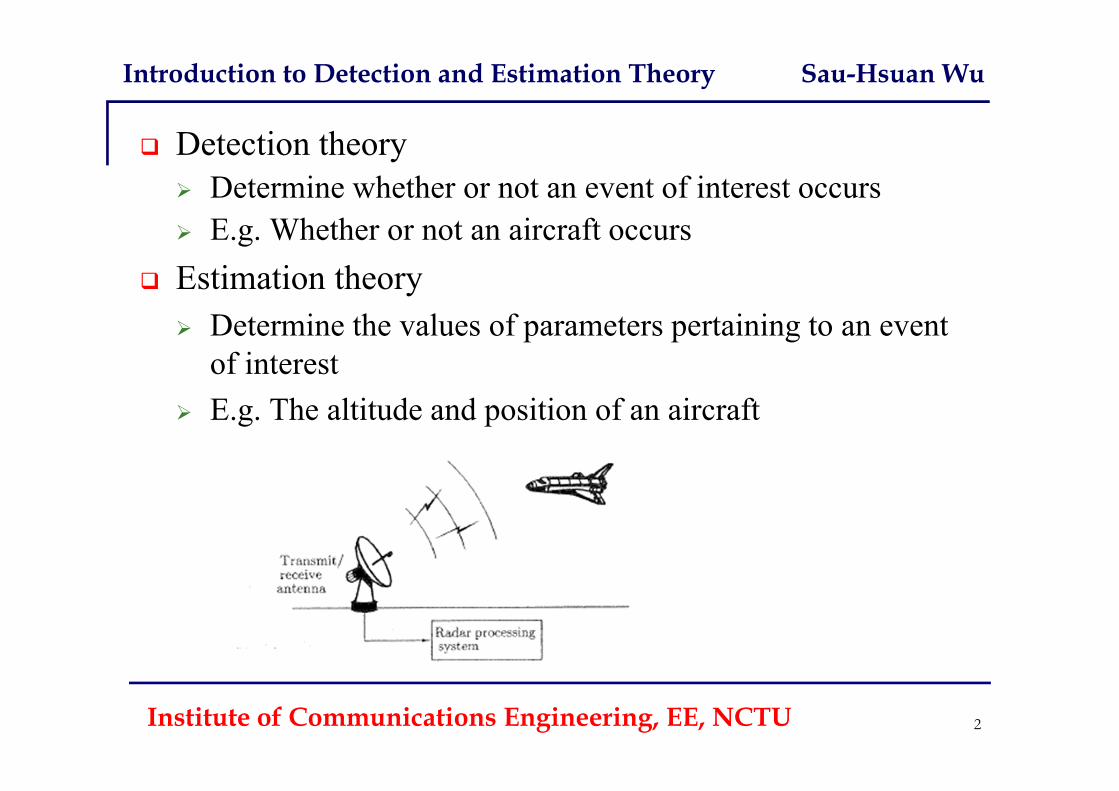

Detection theory Determine whether or not an event of interest occurs E.g. Whether or not an aircraft occurs

Estimation theory Determine the values of parameters pertaining to an event

of interest E.g. The altitude and position of an aircraft

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

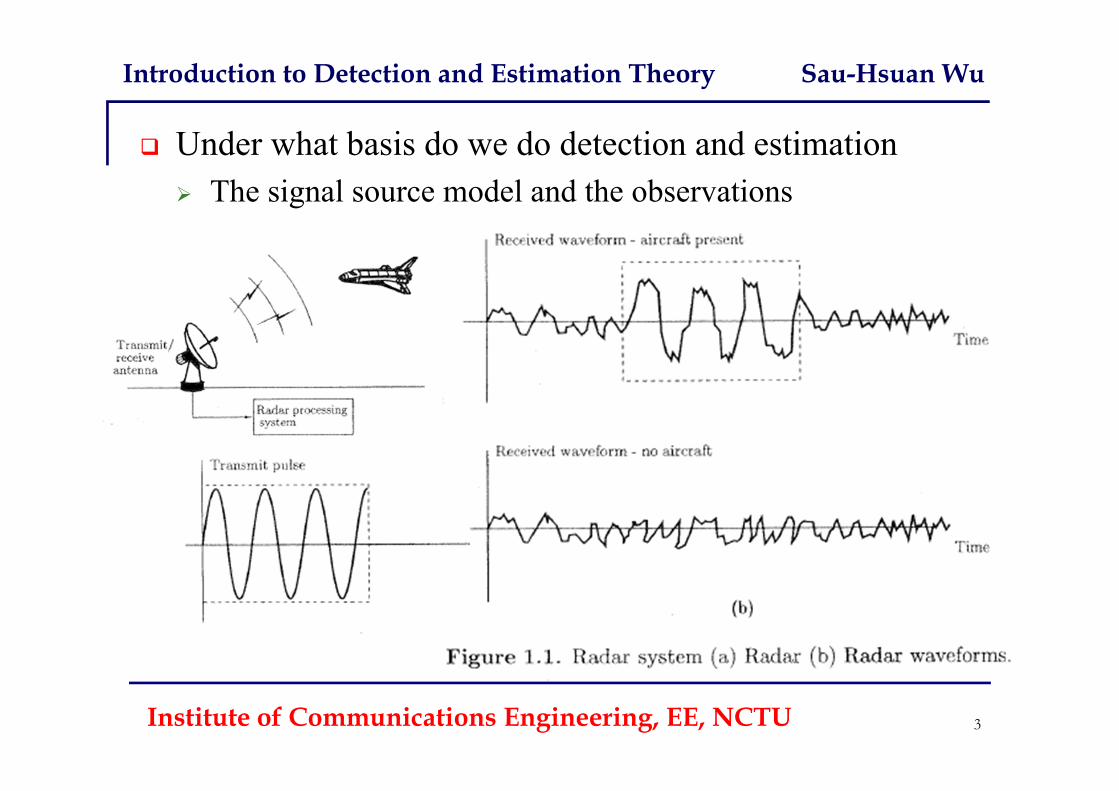

Under what basis do we do detection and estimation The signal source model and the observations

Institute of Communications Engineering, EE, NCTU 3

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

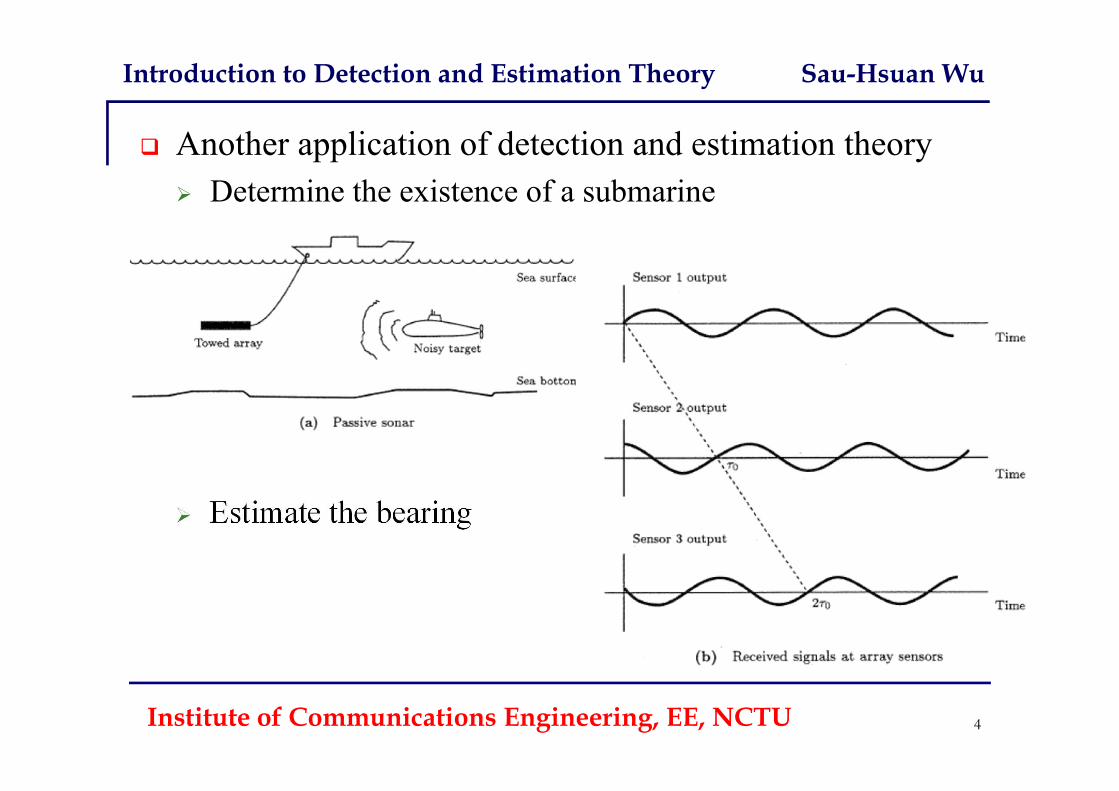

Institute of Communications Engineering, EE, NCTU 4

Another application of detection and estimation theory Determine the existence of a submarine

Estimate the bearing

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 5

Many more applications Biomedicine: estimate the heart rate or even heart diseases Image analysis: estimate the size, position and orientation of

an object in an image Seismology: estimate the underground distance of an oil

deposit Communications: estimate the signal distortion and

determine the transmitted symbols Economics: estimate the Don-Jones industrial average

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 6

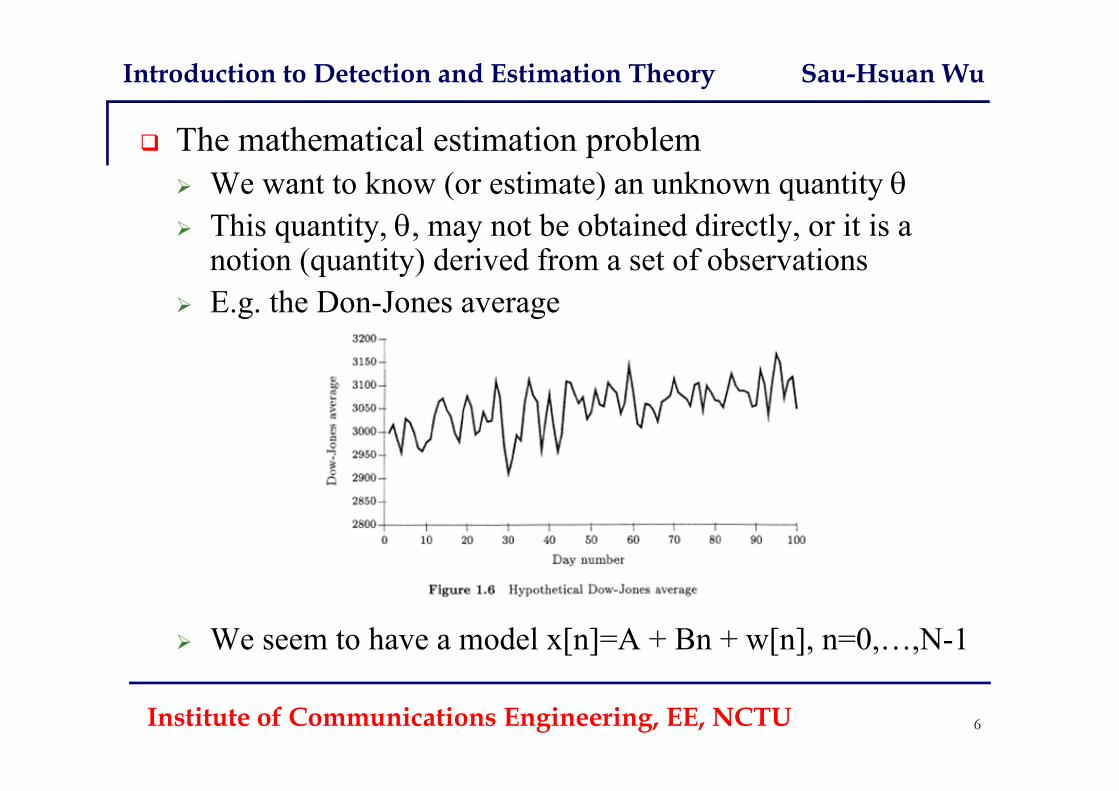

The mathematical estimation problem We want to know (or estimate) an unknown quantity This quantity, , may not be obtained directly, or it is a

notion (quantity) derived from a set of observations E.g. the Don-Jones average

We seem to have a model x[n]=A + Bn + w[n], n=0,…,N-1

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 7

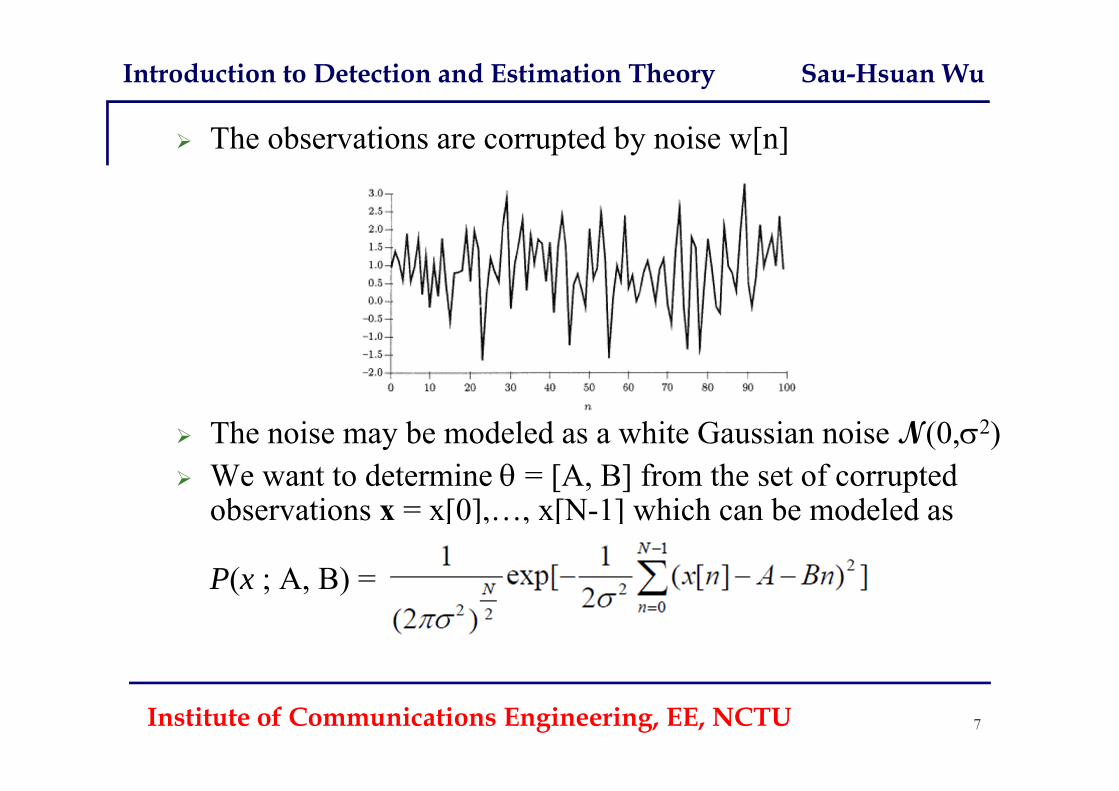

The observations are corrupted by noise w[n]

The noise may be modeled as a white Gaussian noise N(0,2) We want to determine = [A, B] from the set of corrupted

observations x = x[0],…, x[N-1] which can be modeled as

P(x ; A, B) =

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Our goal is to determine according to the observations, namely Examples:

x[n] = A1 + w[n], n=0,…,N-1 x[n] = A2 + B2 n + w[n], n=0,…,N-1

Â1= x[n]/N and ? Can we try the least square method

How many other kinds of methods can we use Minimum variance unbiased estimator (MVU) Best linear unbiased estimator (BLUE) Maximum likelihood estimator (ML) Bayesian estimator: MMSE, MAP, and …

Institute of Communications Engineering, ECE, NCTU 8

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

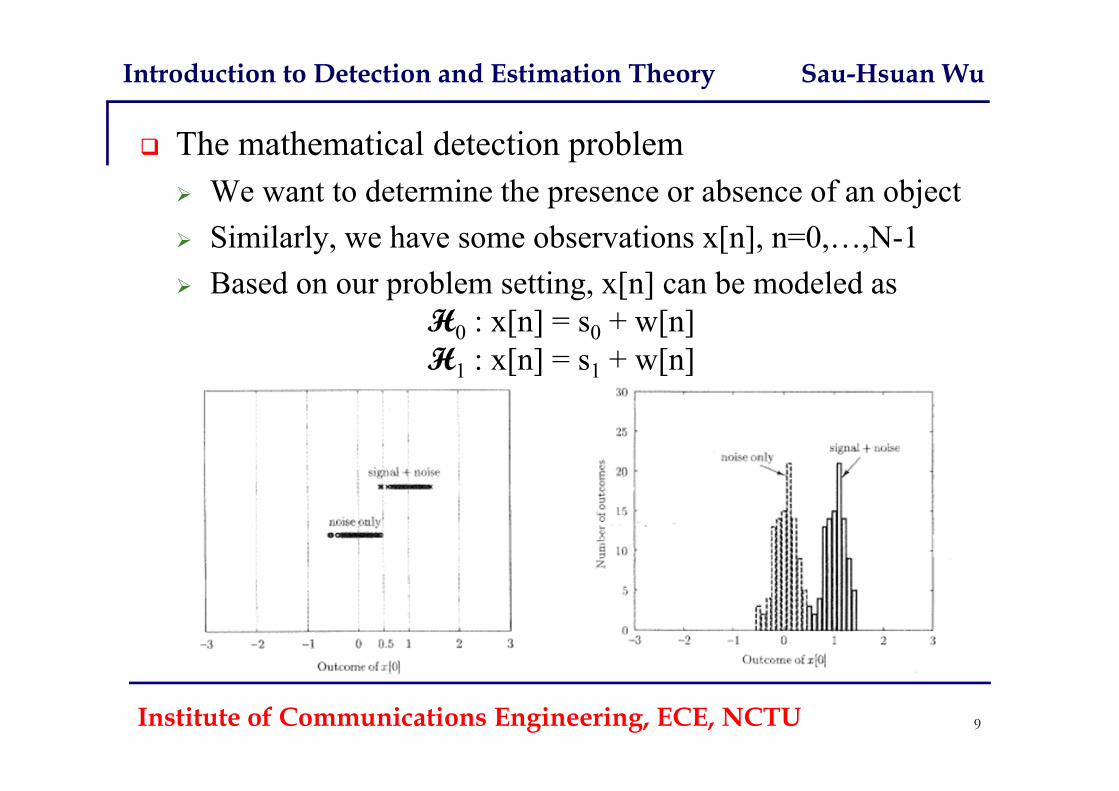

The mathematical detection problem We want to determine the presence or absence of an object Similarly, we have some observations x[n], n=0,…,N-1 Based on our problem setting, x[n] can be modeled as

H0 : x[n] = s0 + w[n]H1 : x[n] = s1 + w[n]

Institute of Communications Engineering, ECE, NCTU 9

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

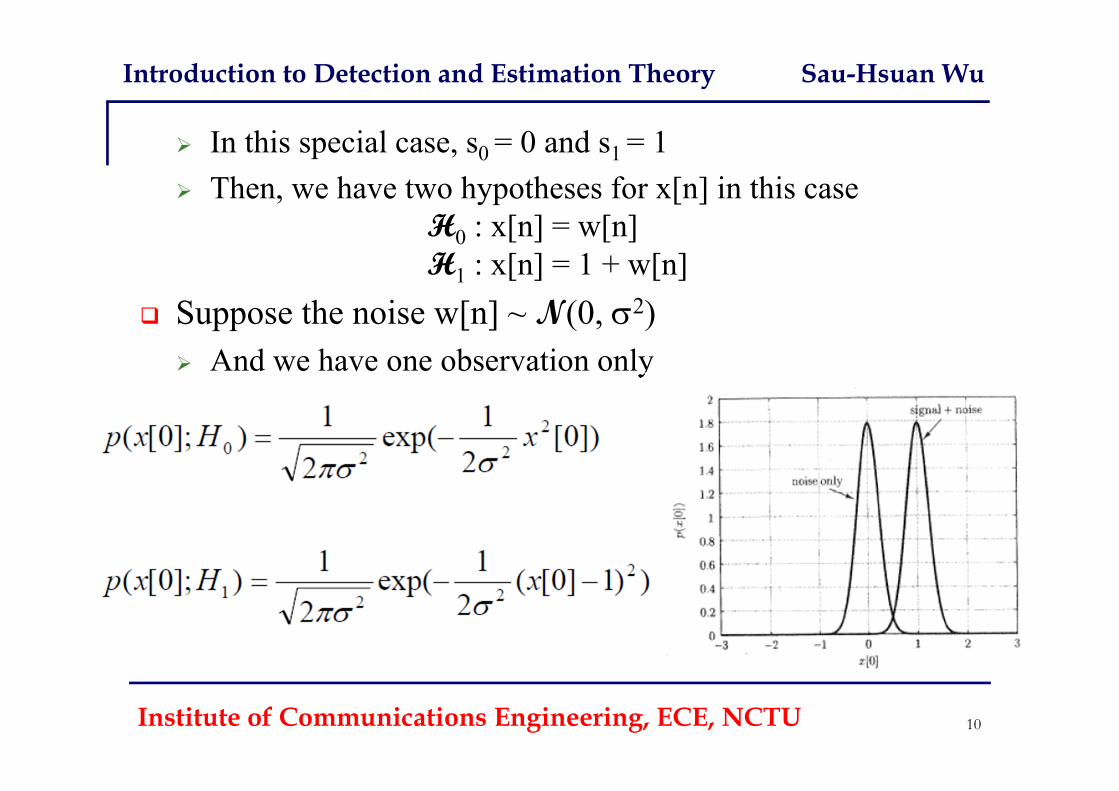

In this special case, s0 = 0 and s1 = 1 Then, we have two hypotheses for x[n] in this case

H0 : x[n] = w[n]H1 : x[n] = 1 + w[n]

Suppose the noise w[n] ~ N(0, 2) And we have one observation only

Institute of Communications Engineering, ECE, NCTU 10

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

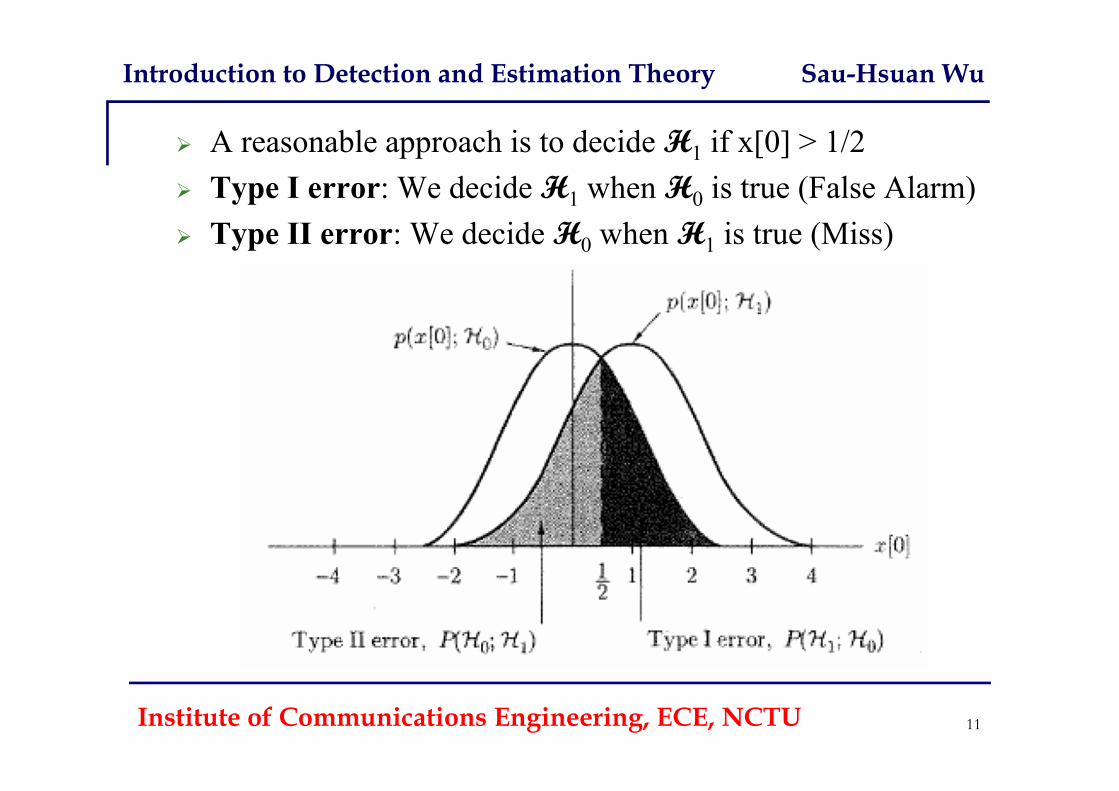

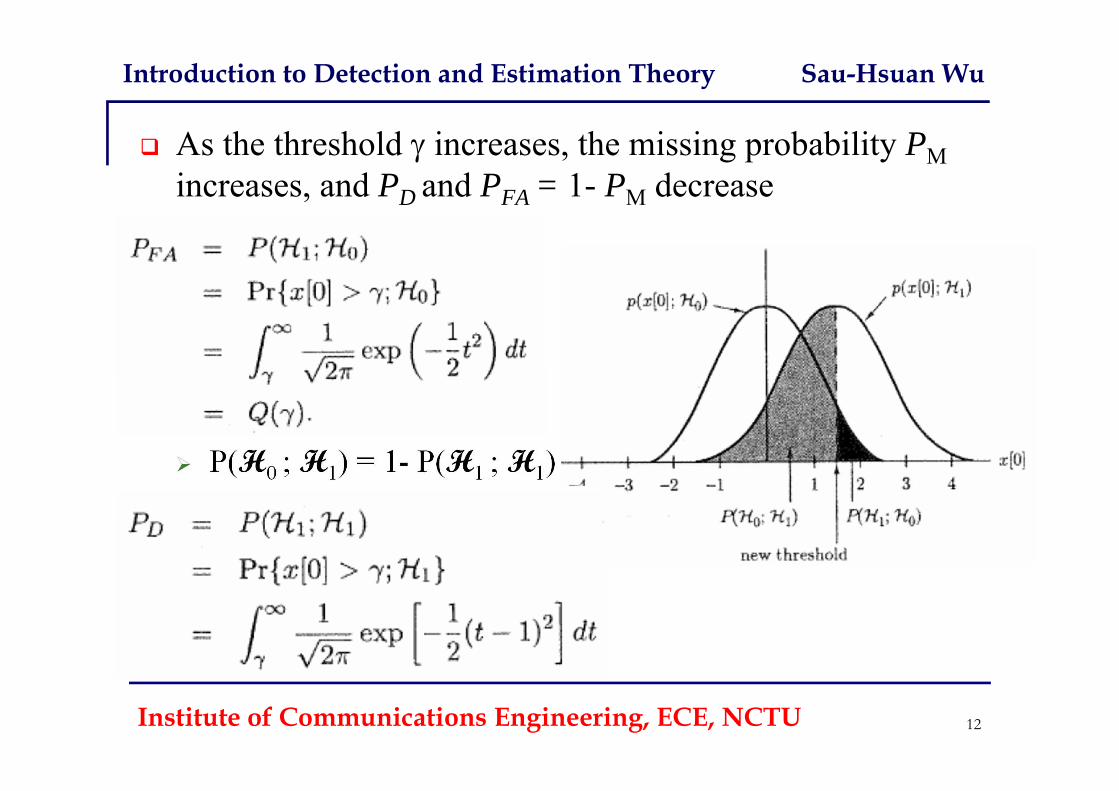

A reasonable approach is to decide H1 if x[0] > 1/2 Type I error: We decide H1 when H0 is true (False Alarm) Type II error: We decide H0 when H1 is true (Miss)

Institute of Communications Engineering, ECE, NCTU 11

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

As the threshold increases, the missing probability PMincreases, and PD and PFA = 1- PM decrease

P(H0 ; H1) = 1- P(H1 ; H1)

Institute of Communications Engineering, ECE, NCTU 12

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

In general, we have multiple observations x[n], n=0,…,N-1H0 : x[n] = w[n]H1 : x[n] = A + w[n]

We would decide H1 if T = x[n]/N >

The detection performance increases with d2 = NA2/ 2

Other approach for detection Neyman-Pearson approach

When H0 and H1 are thought of random variables Maximum likelihood (ML) detector Maximum a posterior (MAP) detector Composite hypothesis testing

Institute of Communications Engineering, ECE, NCTU 13

Detection Theory

Institute of Communications Engineering, ECE, NCTU 14

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

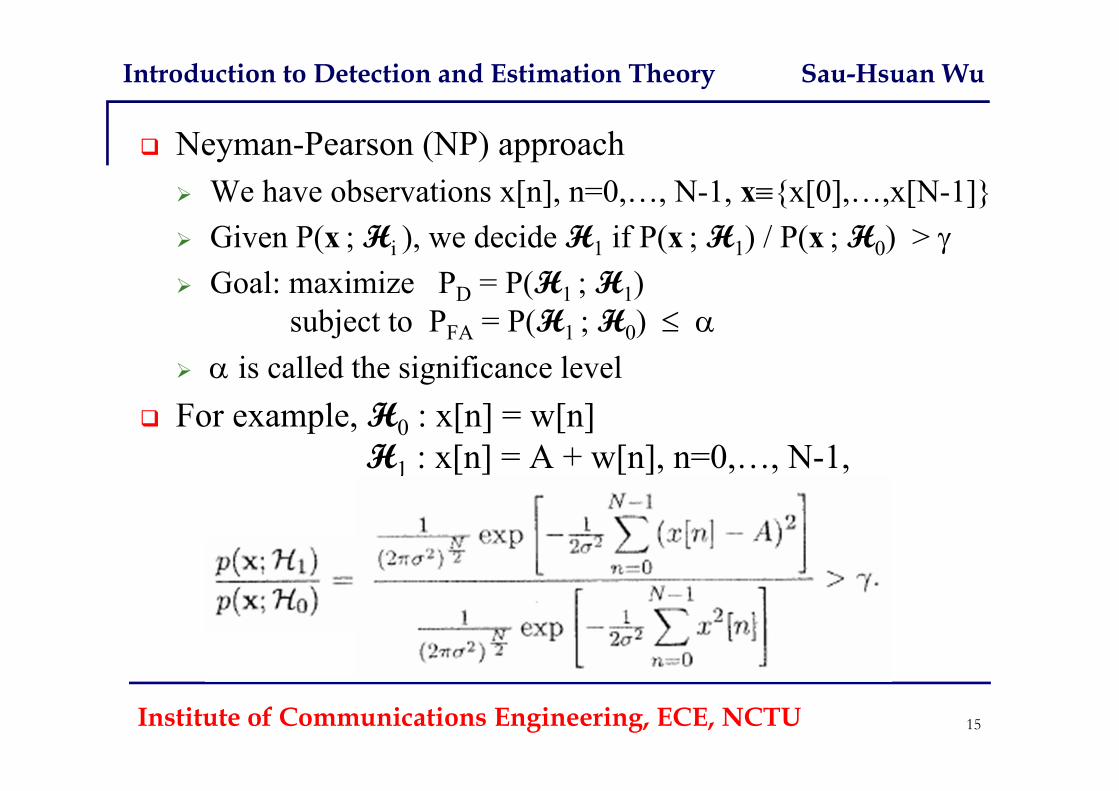

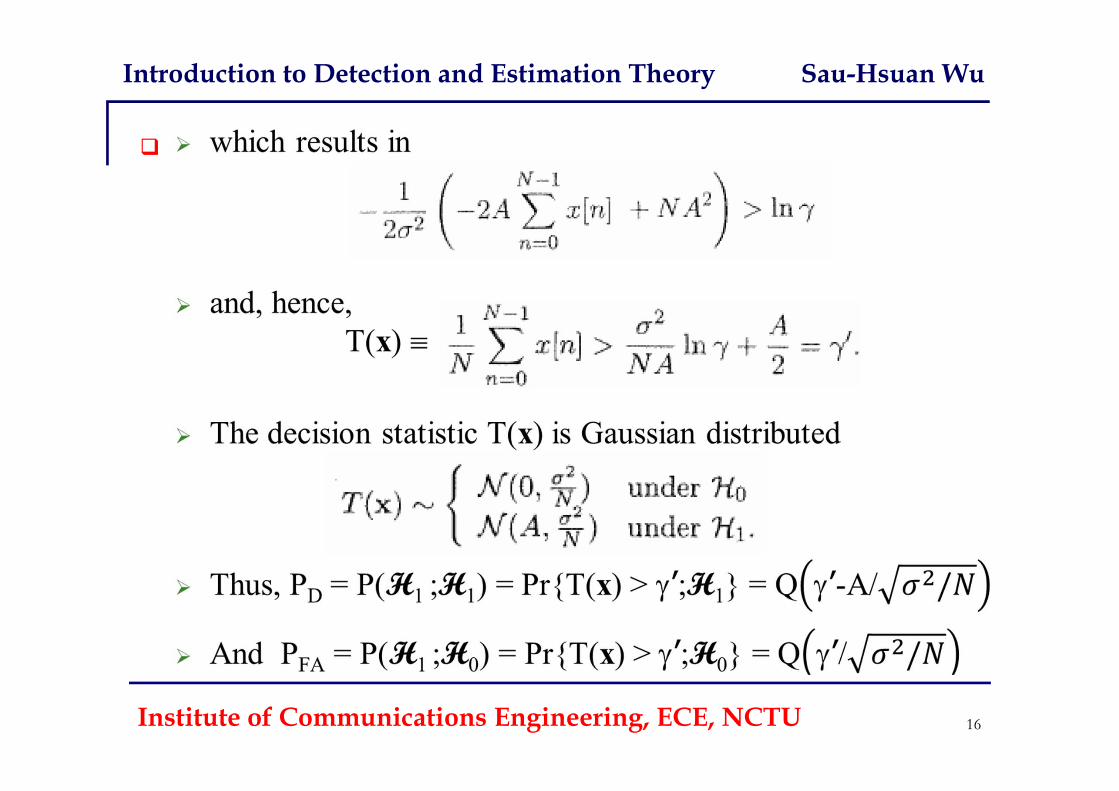

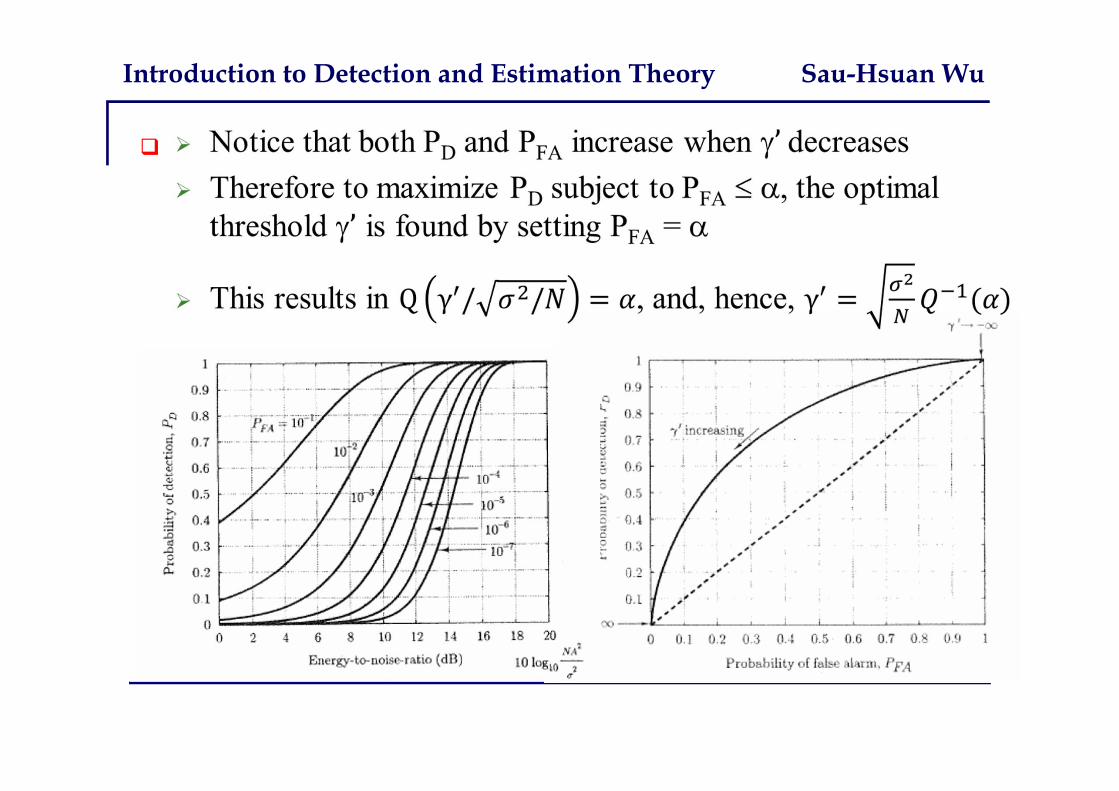

Neyman-Pearson (NP) approach We have observations x[n], n=0,…, N-1, x{x[0],…,x[N-1]} Given P(x ; Hi ), we decide H1 if P(x ; H1) / P(x ; H0) > Goal: maximize PD = P(H1 ; H1)

subject to PFA = P(H1 ; H0) is called the significance level

For example, H0 : x[n] = w[n]H1 : x[n] = A + w[n], n=0,…, N-1,

Institute of Communications Engineering, ECE, NCTU 15

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, ECE, NCTU 16

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

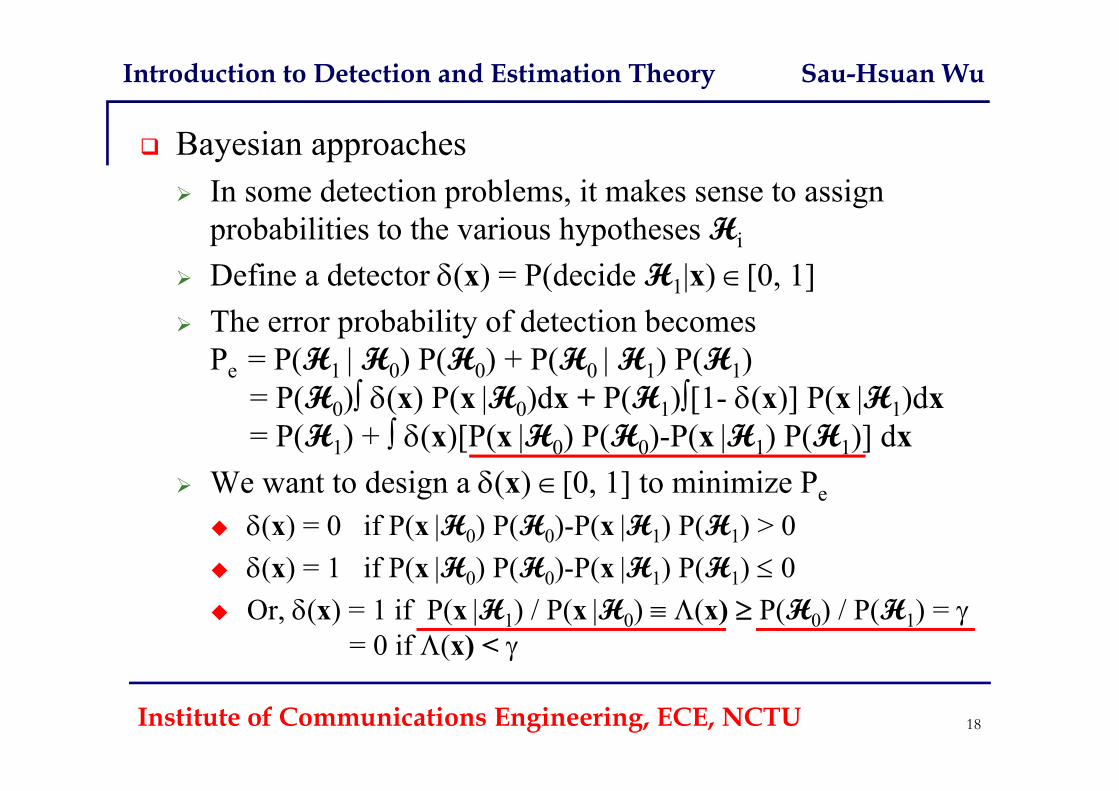

Bayesian approaches In some detection problems, it makes sense to assign

probabilities to the various hypotheses Hi

Define a detector (x) = P(decide H1|x) [0, 1] The error probability of detection becomes

Pe = P(H1 | H0) P(H0) + P(H0 | H1) P(H1)= P(H0) (x) P(x |H0)dx + P(H1)[1- (x)] P(x |H1)dx = P(H1) + (x)[P(x |H0) P(H0)-P(x |H1) P(H1)] dx

We want to design a (x) [0, 1] to minimize Pe (x) = 0 if P(x |H0) P(H0)-P(x |H1) P(H1) > 0 (x) = 1 if P(x |H0) P(H0)-P(x |H1) P(H1) 0 Or, (x) = 1 if P(x |H1) / P(x |H0) (x) P(H0) / P(H1) =

= 0 if (x) <

Institute of Communications Engineering, ECE, NCTU 18

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

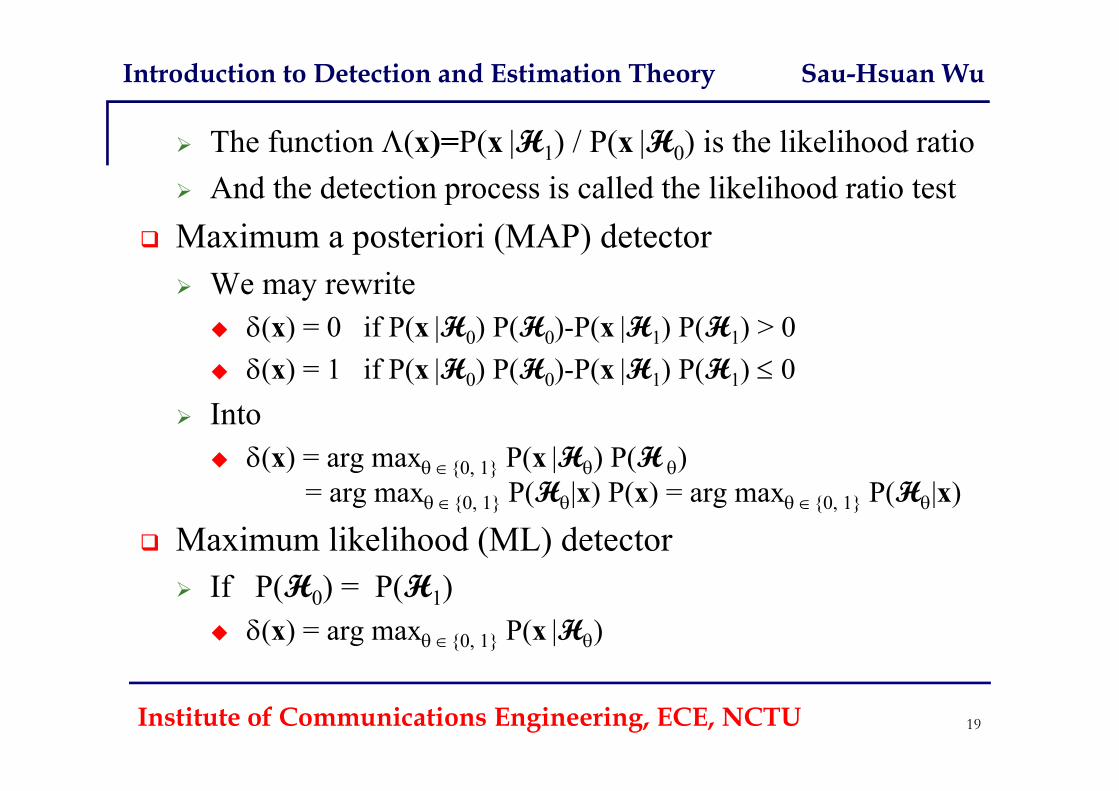

The function (x)=P(x |H1) / P(x |H0) is the likelihood ratio And the detection process is called the likelihood ratio test

Maximum a posteriori (MAP) detector We may rewrite

(x) = 0 if P(x |H0) P(H0)-P(x |H1) P(H1) > 0 (x) = 1 if P(x |H0) P(H0)-P(x |H1) P(H1) 0

Into (x) = arg max {0, 1} P(x |H) P(H )

= arg max {0, 1} P(H|x) P(x) = arg max {0, 1} P(H|x)

Maximum likelihood (ML) detector If P(H0) = P(H1)

(x) = arg max {0, 1} P(x |H)

Institute of Communications Engineering, ECE, NCTU 19

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

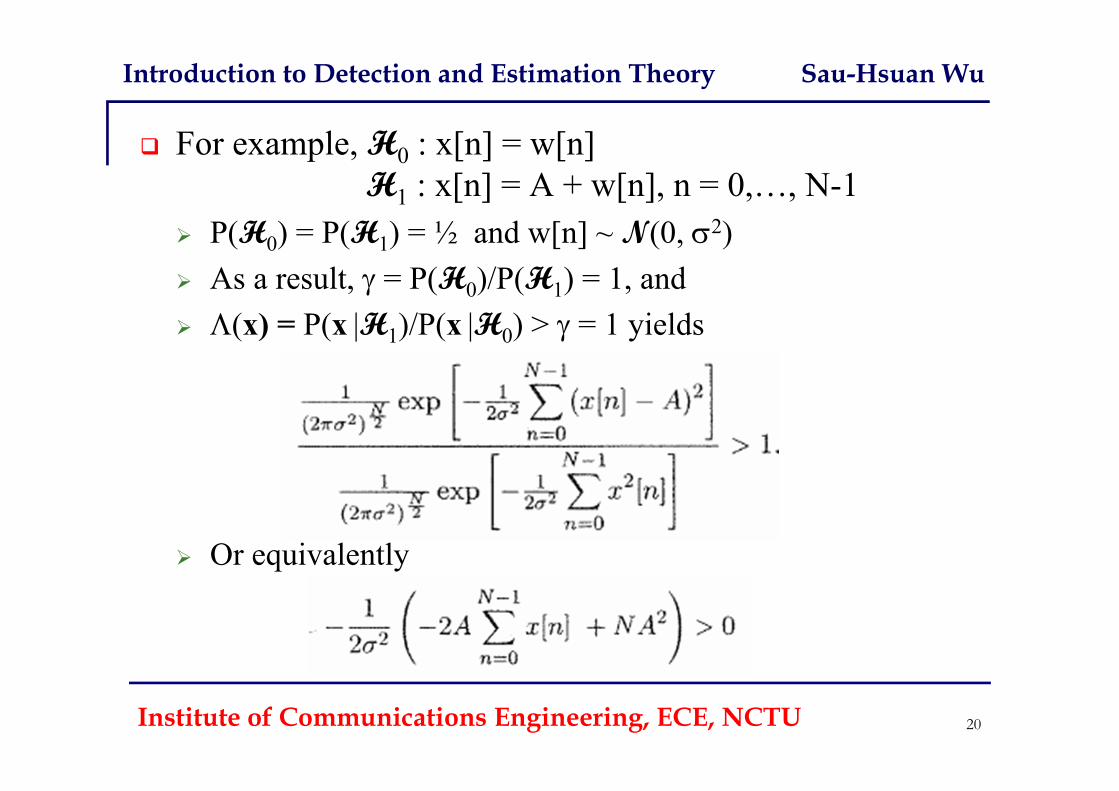

For example, H0 : x[n] = w[n]H1 : x[n] = A + w[n], n = 0,…, N-1

P(H0) = P(H1) = ½ and w[n] ~ N(0, 2) As a result, = P(H0)/P(H1) = 1, and (x) = P(x |H1)/P(x |H0) > = 1 yields

Or equivalently

Institute of Communications Engineering, ECE, NCTU 20

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

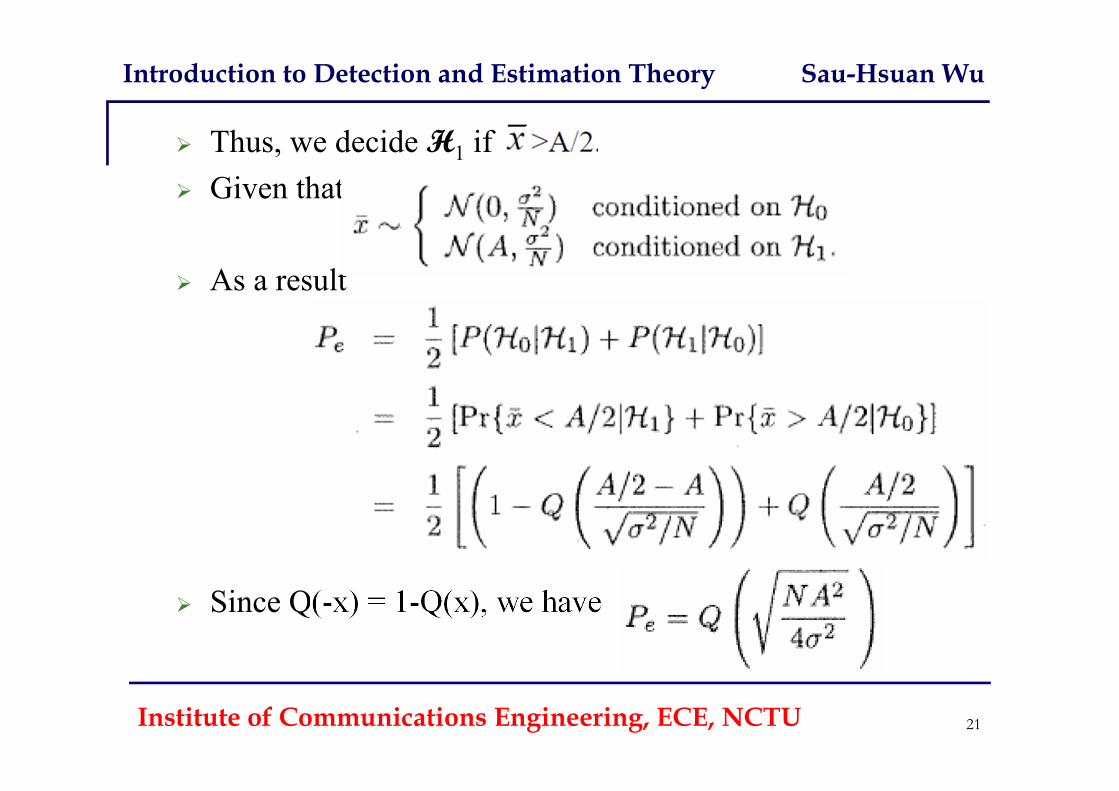

Thus, we decide H1 if Given that

As a result

Since Q(-x) = 1-Q(x), we have

Institute of Communications Engineering, ECE, NCTU 21

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

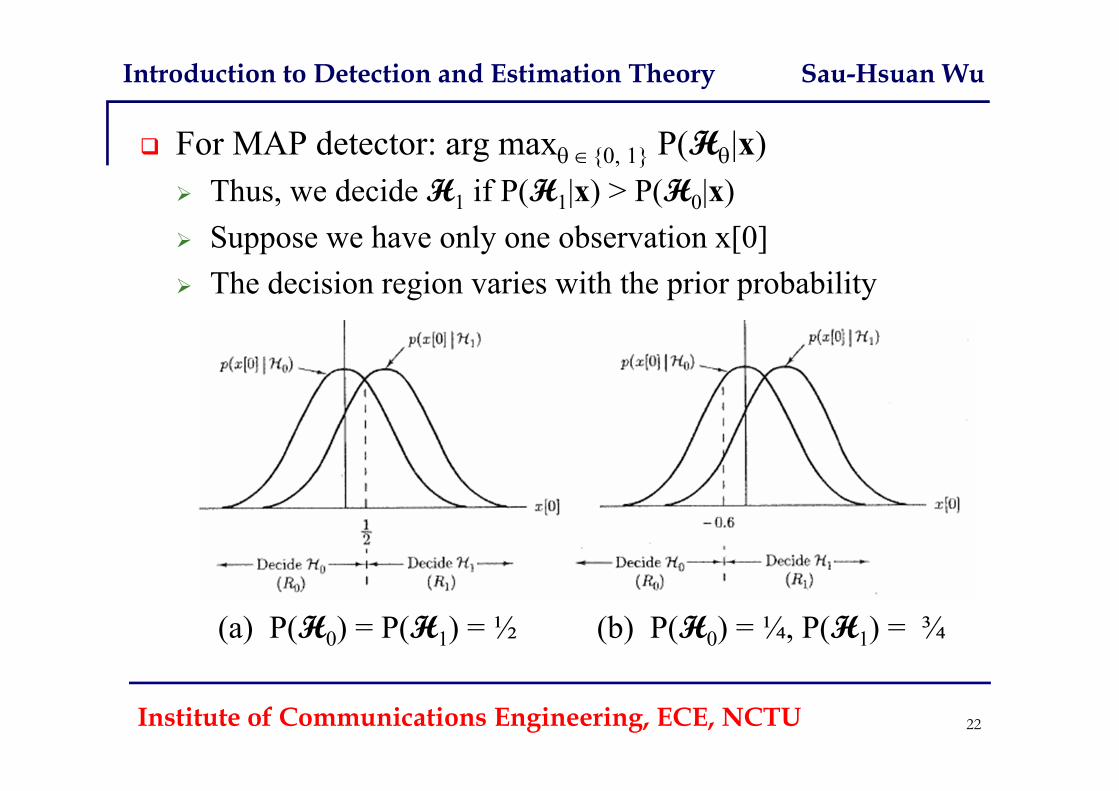

For MAP detector: arg max {0, 1} P(H|x) Thus, we decide H1 if P(H1|x) > P(H0|x) Suppose we have only one observation x[0] The decision region varies with the prior probability

(a) P(H0) = P(H1) = ½ (b) P(H0) = ¼, P(H1) = ¾

Institute of Communications Engineering, ECE, NCTU 22

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

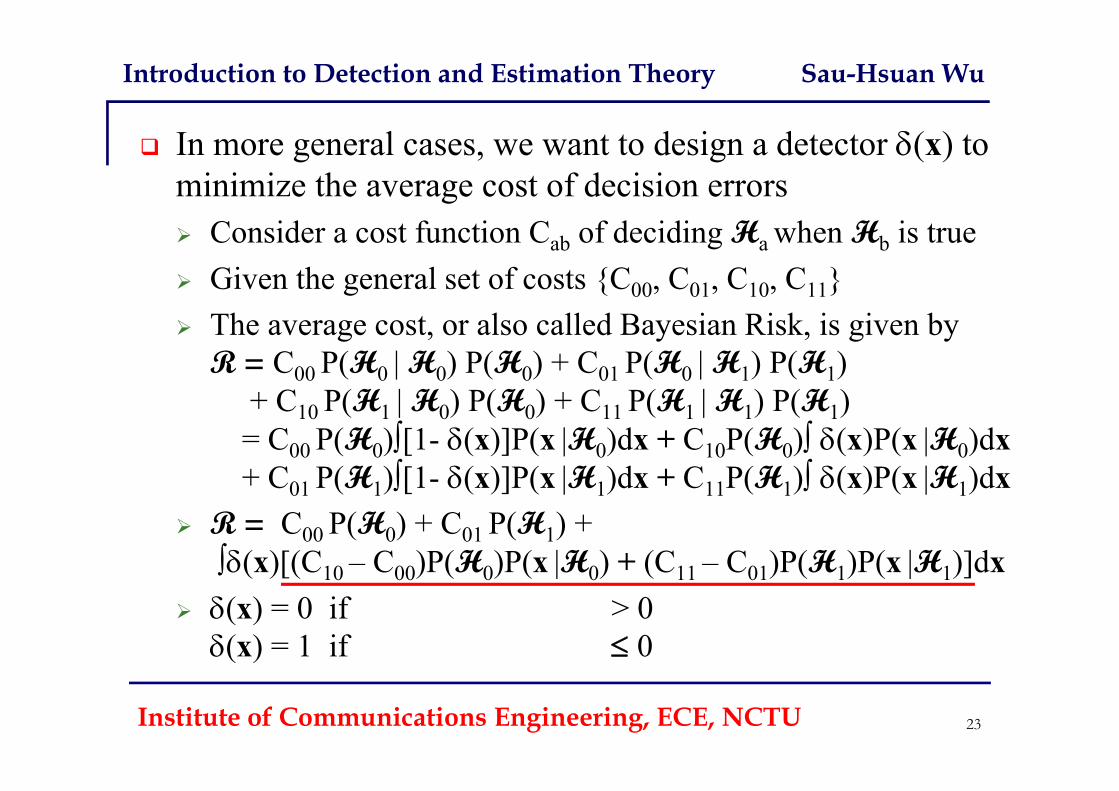

In more general cases, we want to design a detector (x) to minimize the average cost of decision errors Consider a cost function Cab of deciding Ha when Hb is true Given the general set of costs {C00, C01, C10, C11} The average cost, or also called Bayesian Risk, is given by

R = C00 P(H0 | H0) P(H0) + C01 P(H0 | H1) P(H1)+ C10 P(H1 | H0) P(H0) + C11 P(H1 | H1) P(H1)

= C00 P(H0)[1- (x)]P(x |H0)dx + C10P(H0) (x)P(x |H0)dx+ C01 P(H1)[1- (x)]P(x |H1)dx + C11P(H1) (x)P(x |H1)dx

R = C00 P(H0) + C01 P(H1) +(x)[(C10 – C00)P(H0)P(x |H0) + (C11 – C01)P(H1)P(x |H1)]dx

(x) = 0 if > 0(x) = 1 if 0

Institute of Communications Engineering, ECE, NCTU 23

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

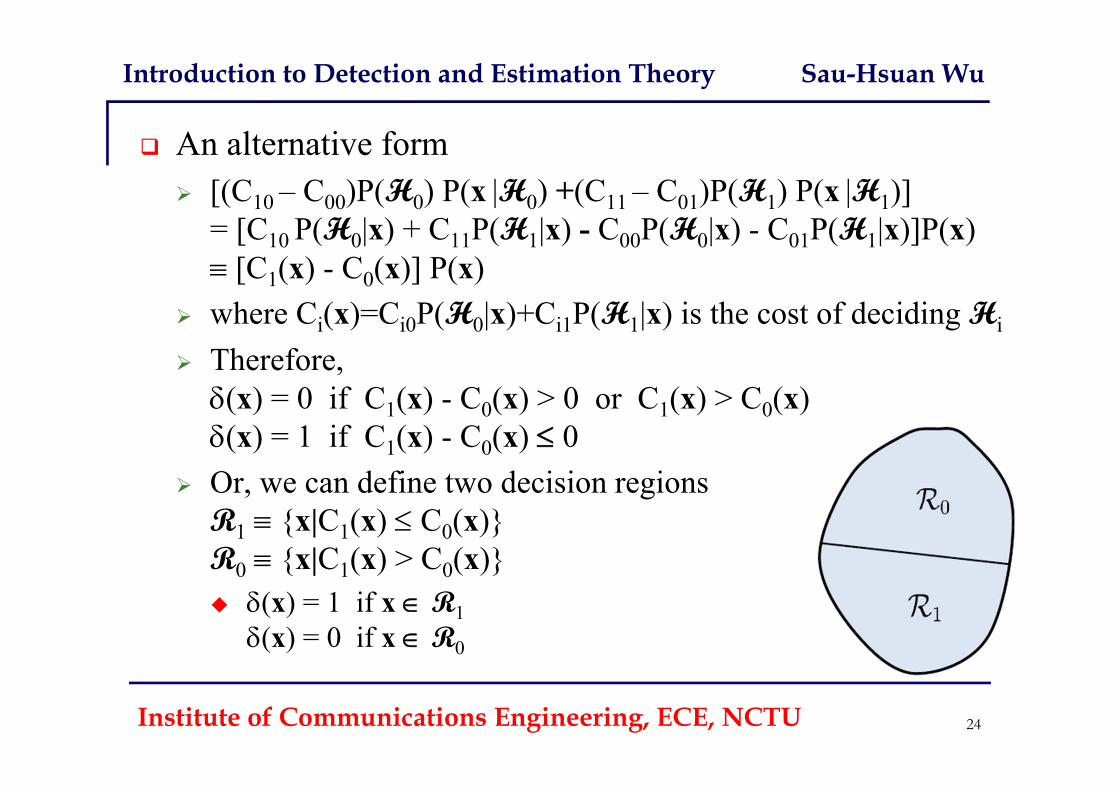

An alternative form [(C10 – C00)P(H0) P(x |H0) +(C11 – C01)P(H1) P(x |H1)]

= [C10 P(H0|x) + C11P(H1|x) - C00P(H0|x) - C01P(H1|x)]P(x) [C1(x) - C0(x)] P(x)

where Ci(x)=Ci0P(H0|x)+Ci1P(H1|x) is the cost of deciding Hi

Therefore, (x) = 0 if C1(x) - C0(x) > 0 or C1(x) > C0(x)(x) = 1 if C1(x) - C0(x) 0

Or, we can define two decision regionsR1 {x|C1(x) C0(x)} R0 {x|C1(x) > C0(x)} (x) = 1 if x R1

(x) = 0 if x R0

Institute of Communications Engineering, ECE, NCTU 24

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

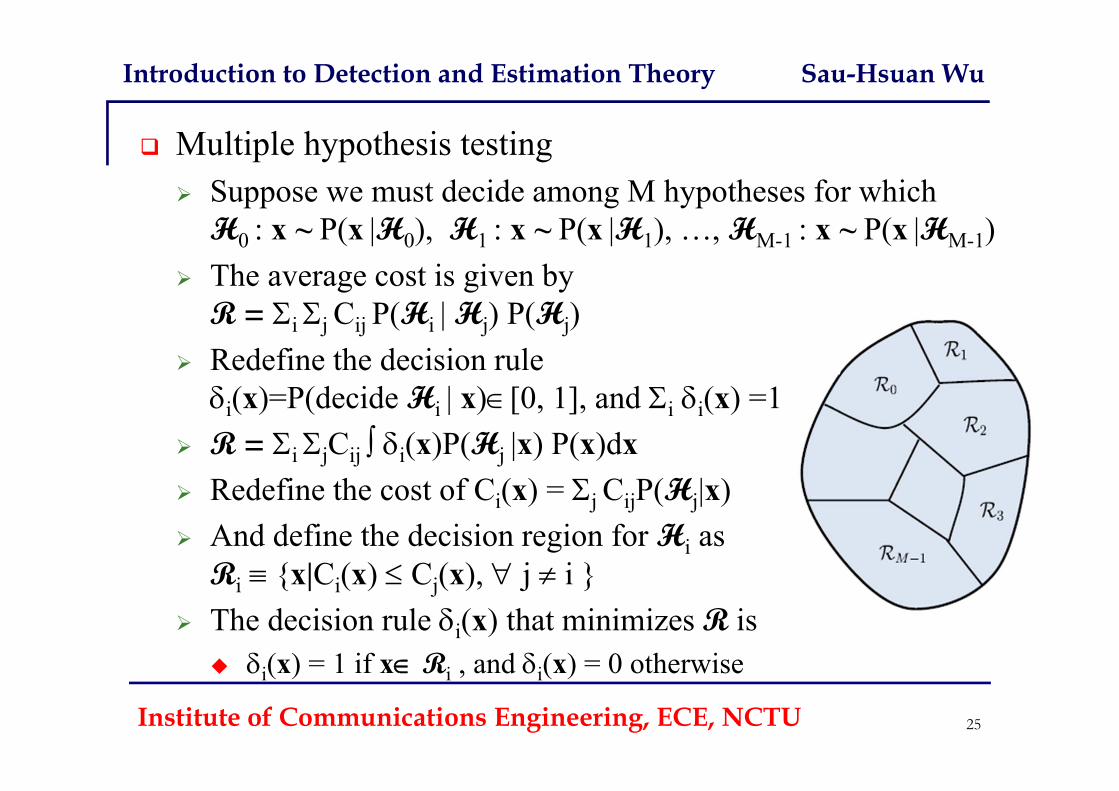

Multiple hypothesis testing Suppose we must decide among M hypotheses for which

H0 : x ~ P(x |H0), H1 : x ~ P(x |H1), …, HM-1 : x ~ P(x |HM-1) The average cost is given by

R = i j Cij P(Hi | Hj) P(Hj) Redefine the decision rule i(x)=P(decide Hi | x)[0, 1], and i i(x) =1

R = i jCij i(x)P(Hj |x) P(x)dx Redefine the cost of Ci(x) = j CijP(Hj|x) And define the decision region for Hi as

Ri {x|Ci(x) Cj(x), j i } The decision rule i(x) that minimizes R is

i(x) = 1 if x Ri , and i(x) = 0 otherwise

Institute of Communications Engineering, ECE, NCTU 25

Estimation Theory

Institute of Communications Engineering, ECE, NCTU 26

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 27

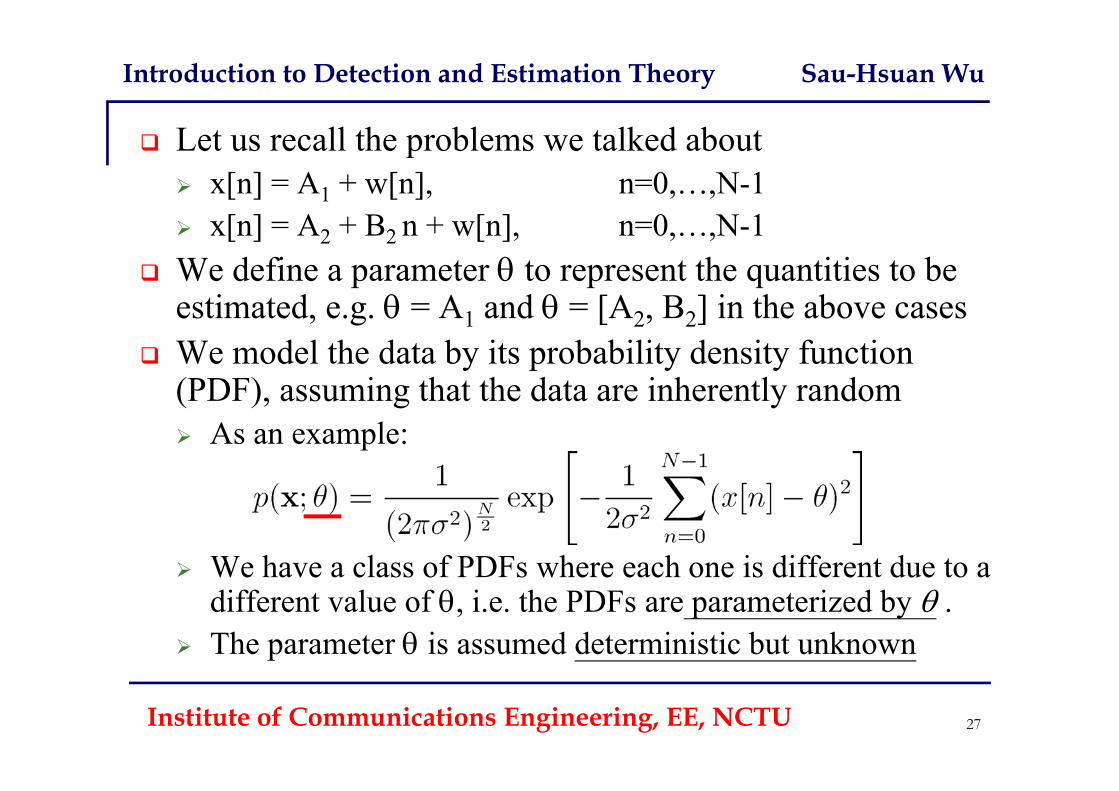

Let us recall the problems we talked about x[n] = A1 + w[n], n=0,…,N-1 x[n] = A2 + B2 n + w[n], n=0,…,N-1

We define a parameter to represent the quantities to be estimated, e.g. = A1 and = [A2, B2] in the above cases

We model the data by its probability density function (PDF), assuming that the data are inherently random As an example:

We have a class of PDFs where each one is different due to a different value of , i.e. the PDFs are parameterized by .

The parameter is assumed deterministic but unknown

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 28

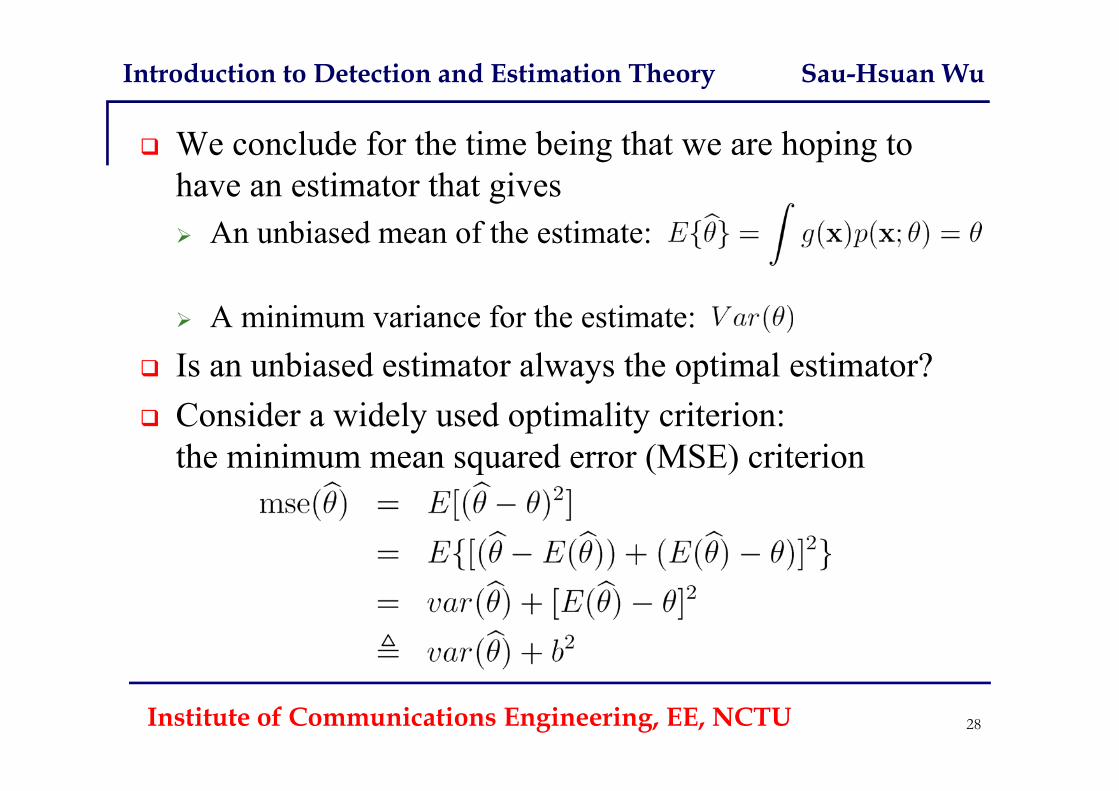

We conclude for the time being that we are hoping to have an estimator that gives An unbiased mean of the estimate:

A minimum variance for the estimate: Is an unbiased estimator always the optimal estimator? Consider a widely used optimality criterion:

the minimum mean squared error (MSE) criterion

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 29

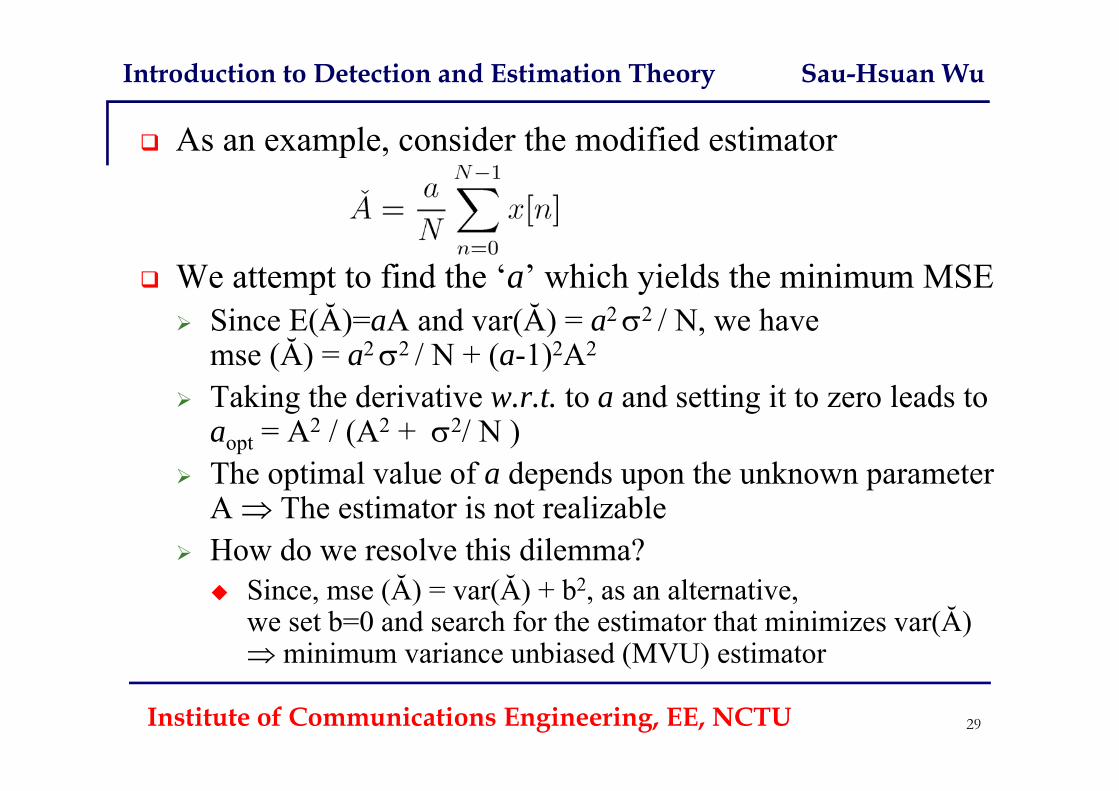

As an example, consider the modified estimator

We attempt to find the ‘a’ which yields the minimum MSE Since E(Ă)=aA and var(Ă) = a2 2 / N, we have

mse (Ă) = a2 2 / N + (a-1)2A2

Taking the derivative w.r.t. to a and setting it to zero leads toaopt = A2 / (A2 + 2/ N )

The optimal value of a depends upon the unknown parameter A The estimator is not realizable

How do we resolve this dilemma? Since, mse (Ă) = var(Ă) + b2, as an alternative,

we set b=0 and search for the estimator that minimizes var(Ă) minimum variance unbiased (MVU) estimator

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 30

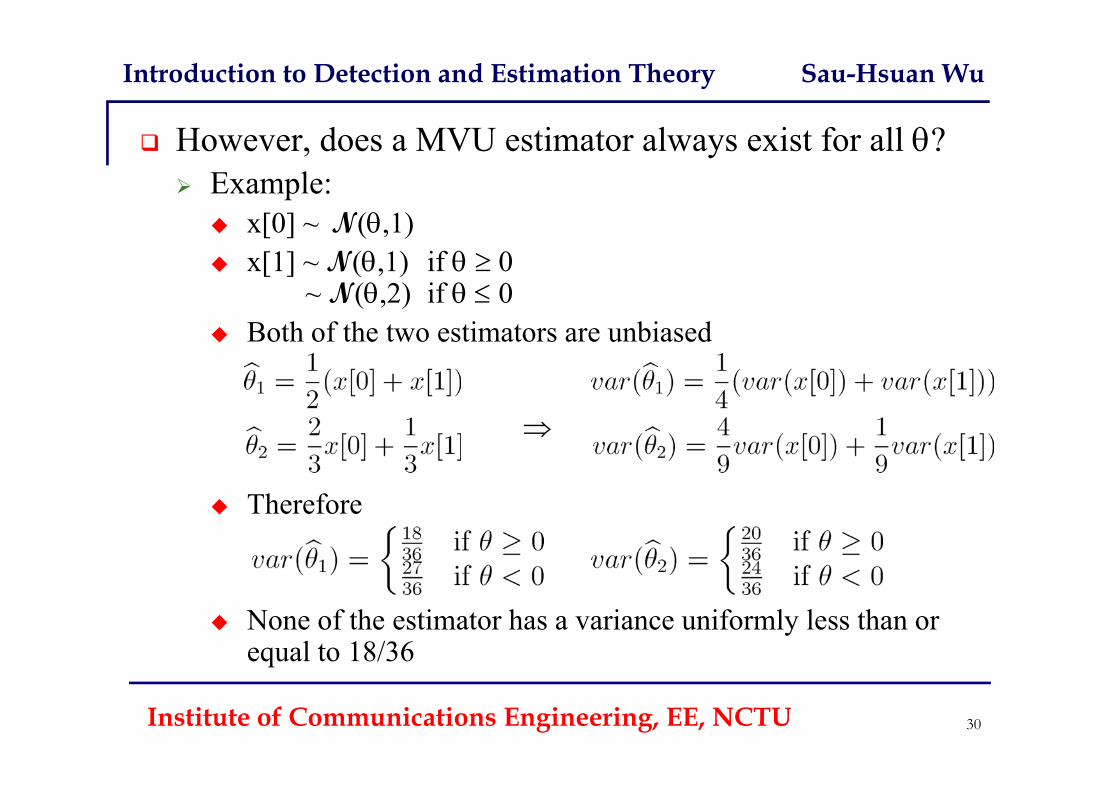

However, does a MVU estimator always exist for all ? Example:

x[0] ~ N(,1) x[1] ~ N(,1) if 0

~ N(,2) if 0 Both of the two estimators are unbiased

Therefore

None of the estimator has a variance uniformly less than or equal to 18/36

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 31

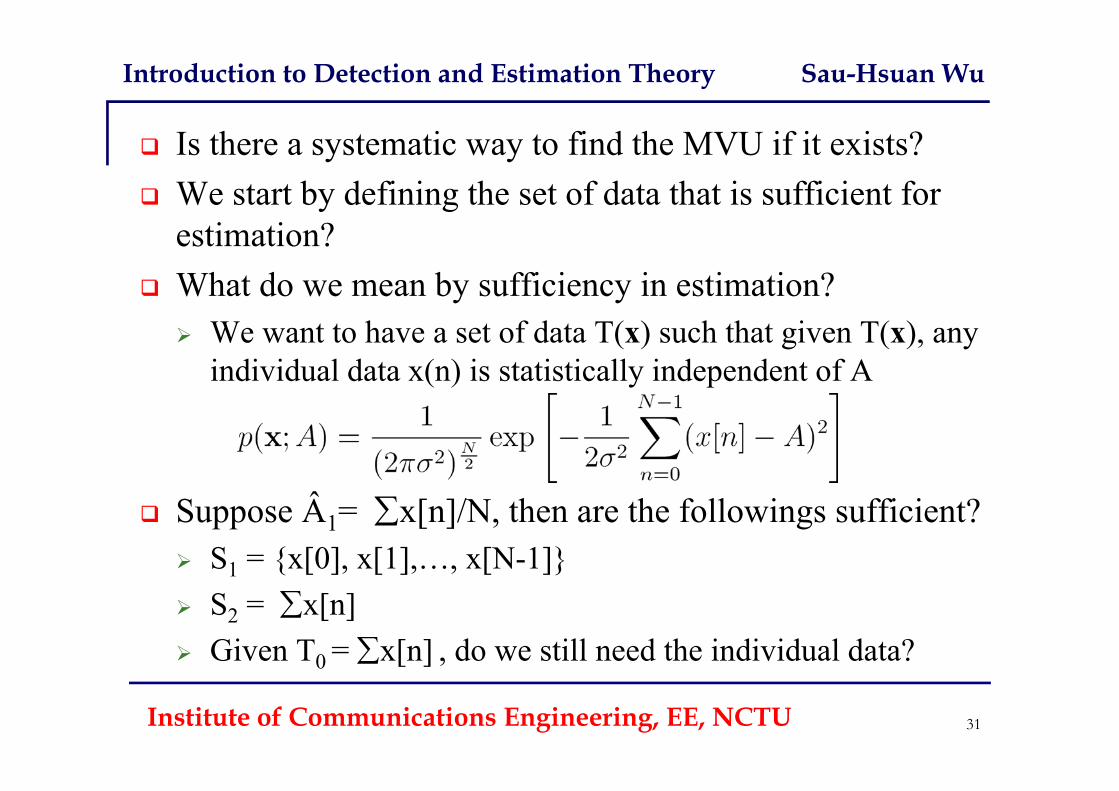

Is there a systematic way to find the MVU if it exists? We start by defining the set of data that is sufficient for

estimation? What do we mean by sufficiency in estimation? We want to have a set of data T(x) such that given T(x), any

individual data x(n) is statistically independent of A

Suppose Â1= x[n]/N, then are the followings sufficient? S1 = {x[0], x[1],…, x[N-1]} S2 = x[n] GivenT0 = x[n] , do we still need the individual data?

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

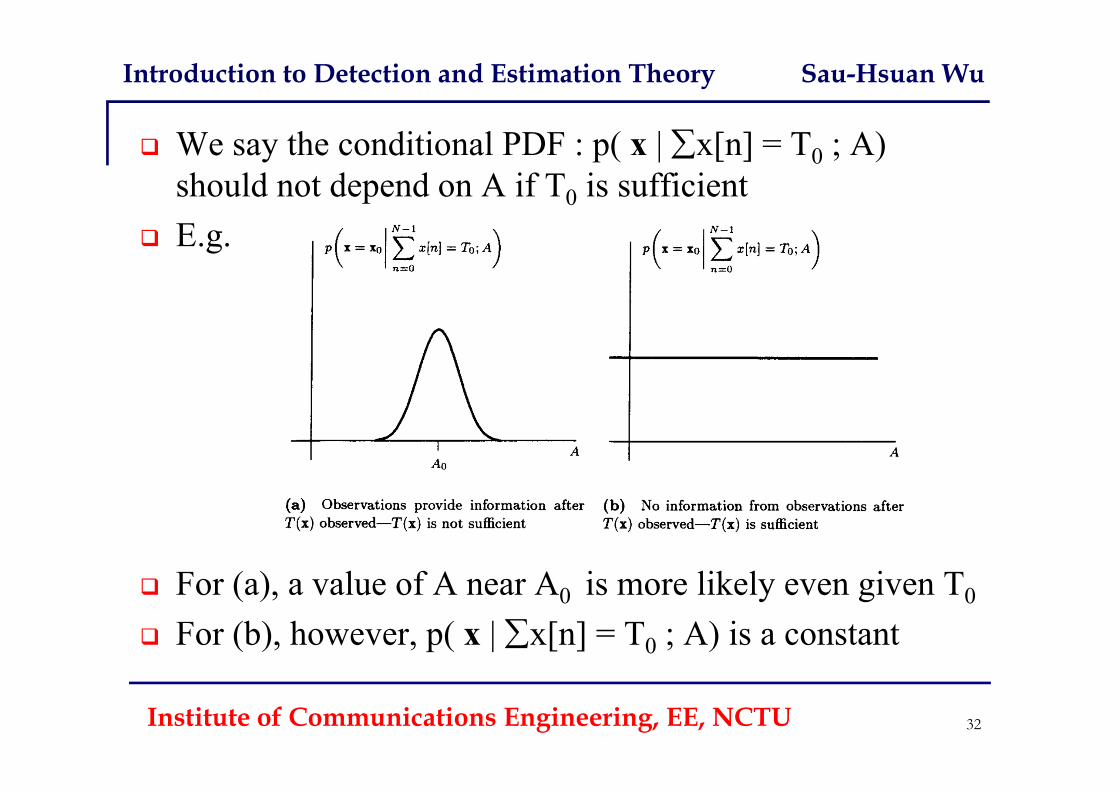

Institute of Communications Engineering, EE, NCTU 32

We say the conditional PDF : p( x | x[n] = T0 ; A) should not depend on A if T0 is sufficient

E.g.

For (a), a value of A near A0 is more likely even given T0

For (b), however, p( x | x[n] = T0 ; A) is a constant

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 33

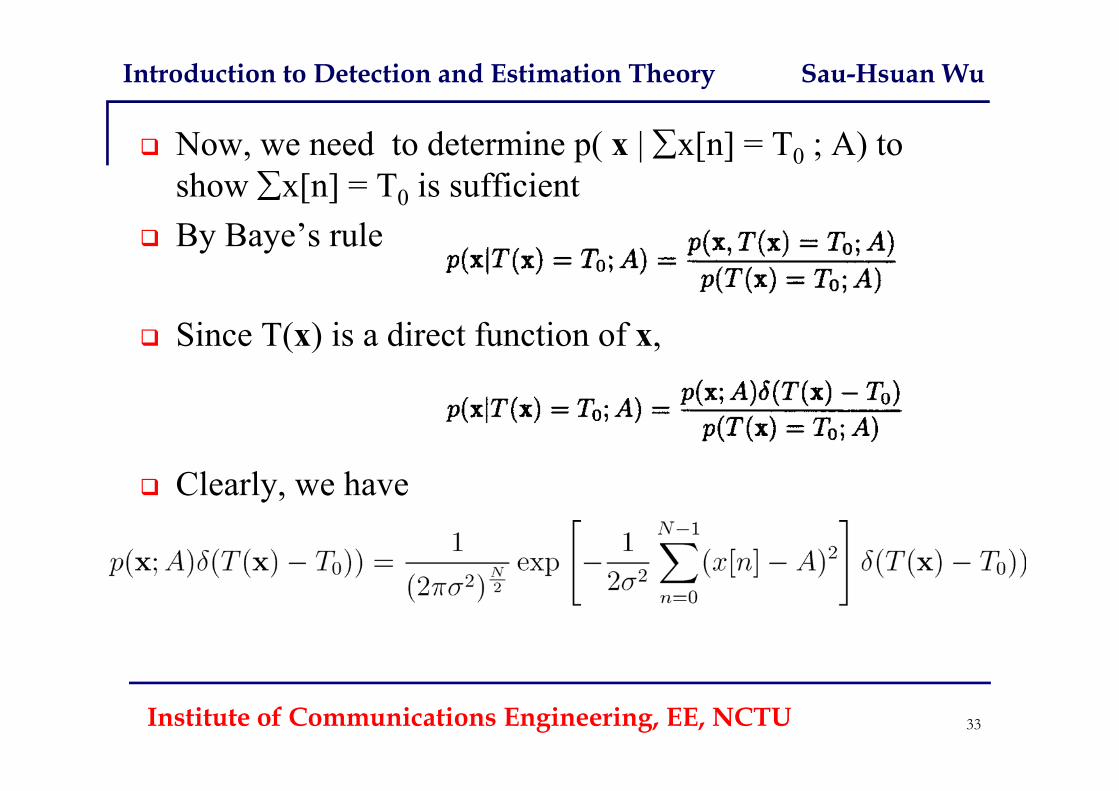

Now, we need to determine p( x | x[n] = T0 ; A) to show x[n] = T0 is sufficient

By Baye’s rule

Since T(x) is a direct function of x,

Clearly, we have

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 34

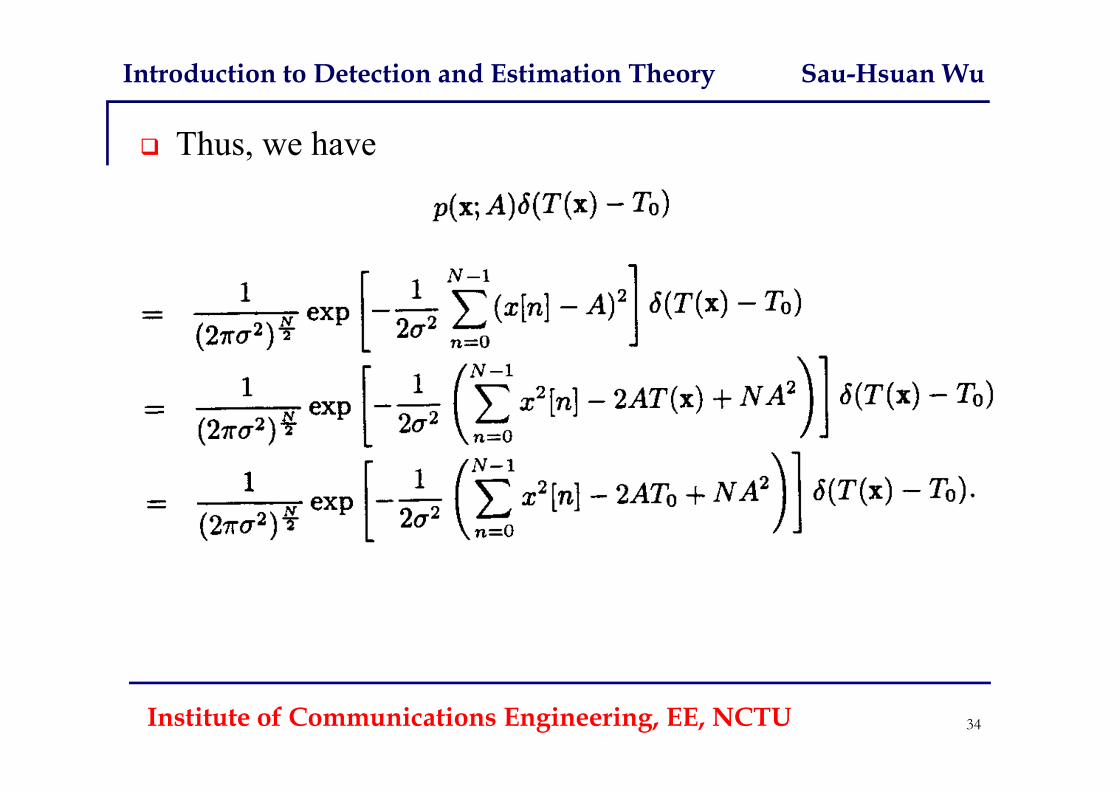

Thus, we have

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 35

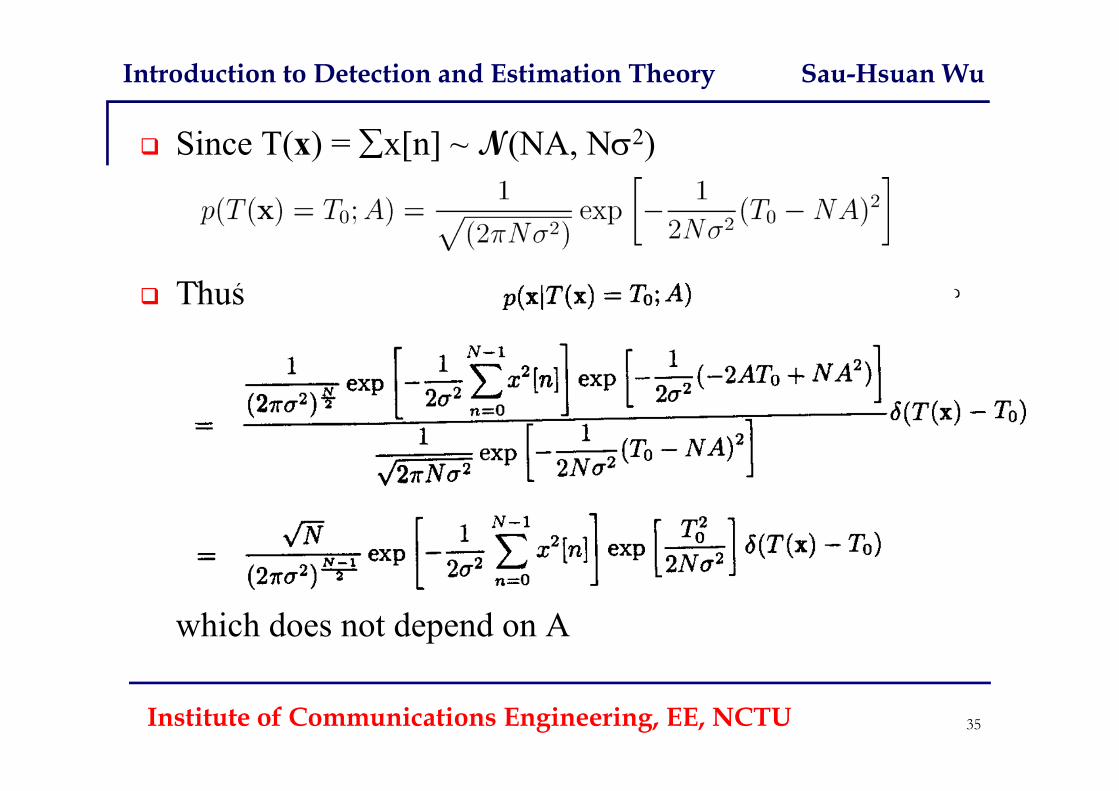

Since T(x) = x[n] ~ N(NA, N2)

Thus

which does not depend on A

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 36

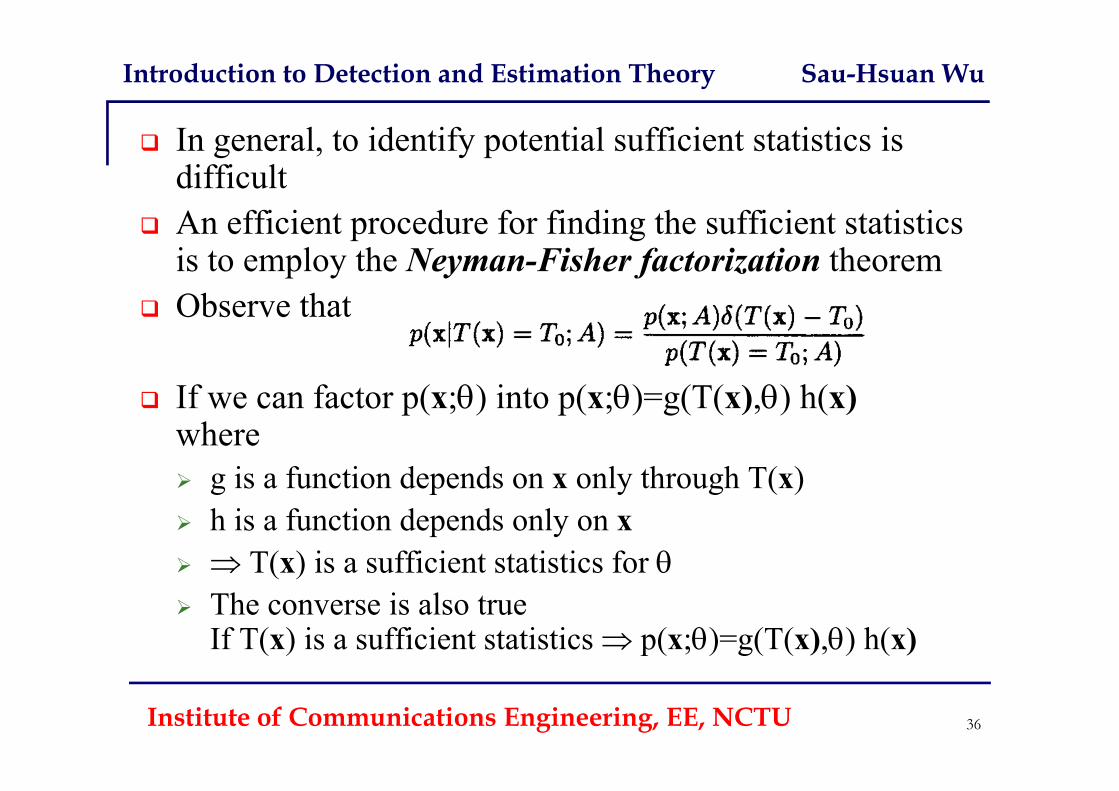

In general, to identify potential sufficient statistics is difficult

An efficient procedure for finding the sufficient statistics is to employ the Neyman-Fisher factorization theorem

Observe that

If we can factor p(x;) into p(x;)=g(T(x),) h(x)where g is a function depends on x only through T(x) h is a function depends only on x T(x) is a sufficient statistics for The converse is also true

If T(x) is a sufficient statistics p(x;)=g(T(x),) h(x)

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 37

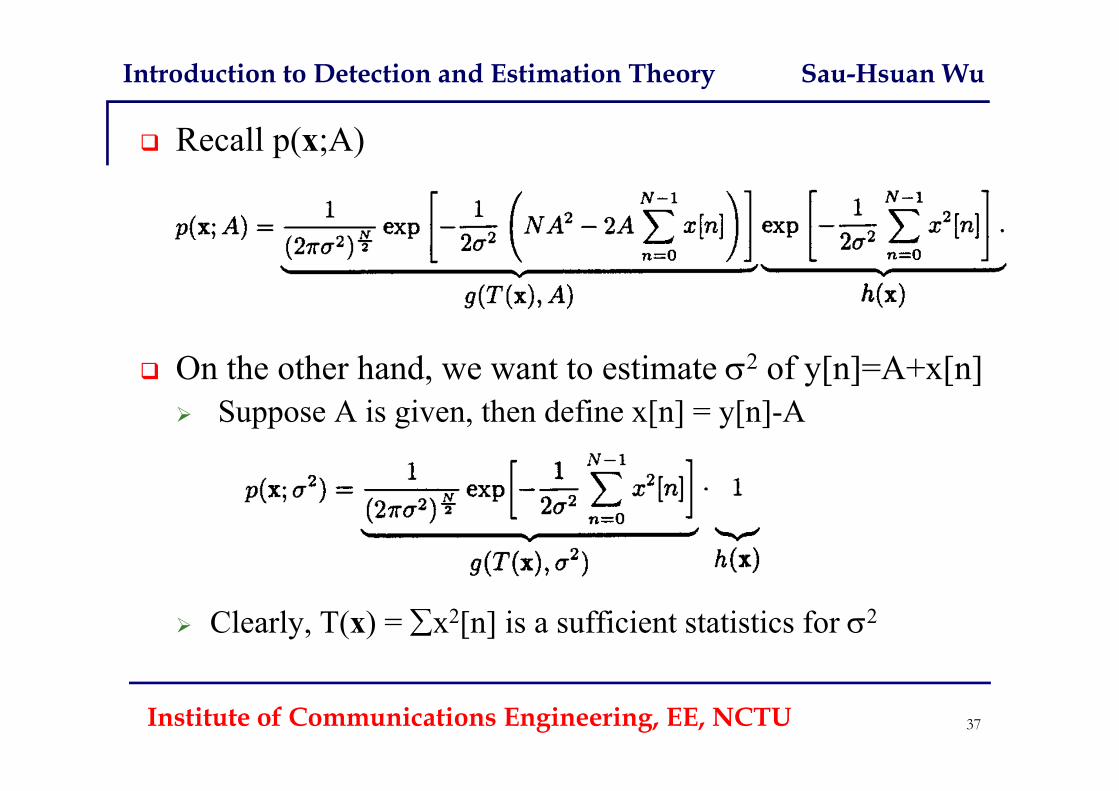

Recall p(x;A)

On the other hand, we want to estimate 2 of y[n]=A+x[n] Suppose A is given, then define x[n] = y[n]-A

Clearly, T(x) = x2[n] is a sufficient statistics for 2

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 38

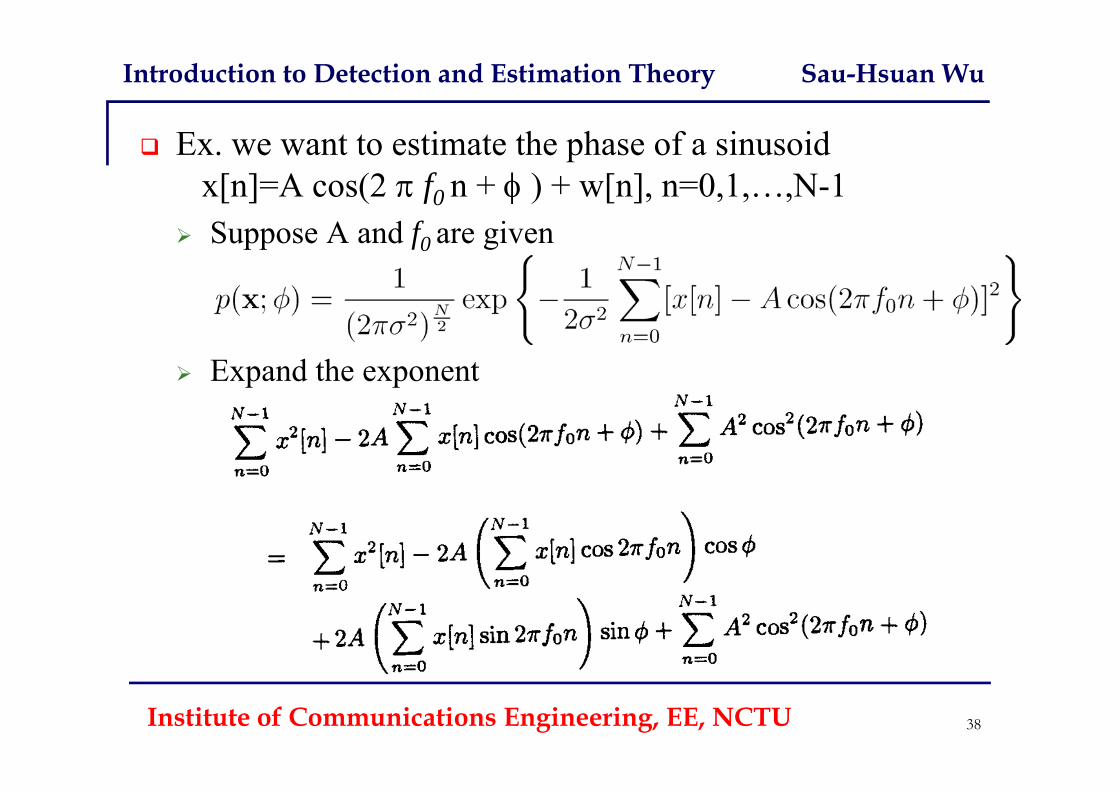

Ex. we want to estimate the phase of a sinusoidx[n]=A cos(2 f0 n + ) + w[n], n=0,1,…,N-1

Suppose A and f0 are given

Expand the exponent

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 39

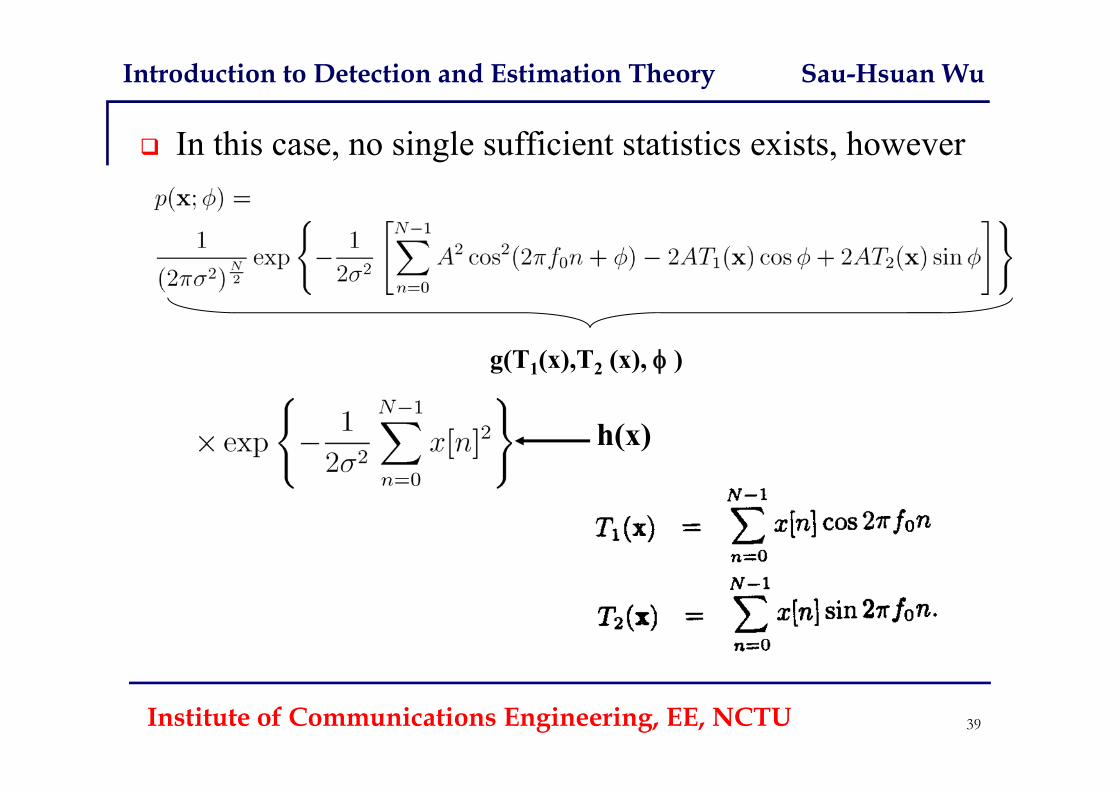

In this case, no single sufficient statistics exists, however

g(T1(x),T2 (x), )

h(x)

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 40

The r statistics T1(x), T2(x),…, Tr(x) are jointly sufficient if p(x | T1(x), T2(x),…, Tr(x) ; ) does not depend on

If p(x ; ) = g(T1(x), T2(x),…, Tr(x) , ) h(x) {T1(x), T2(x),…, Tr(x)} are sufficient statistics for

Now, we know how to obtain the sufficient statistics How do we apply them to help obtain the MVU estimator? The Rao-Blackwell-Lehmann-Scheffe Theorem If is an unbiased estimator of and T(x) is a sufficient

statistic for , then is unbiased and A valid estimator for (not dependent on ) Of lesser or equal variance than that of for all If T(x) is complete, then is the MVU estimator

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 41

Finally, a statistic is complete if there is only one function, say g, of the statistic that is unbiased

is solely a function of T(x) If T(x) is complete is unique and unbiased

Besides, for any unbiased estimator Then, must be the MVU In summary, the MVU can be found by Taking any unbiased and carrying out Alternatively, since there is only one function of T(x) that

leads to an unbiased estimator find the unique g(T(x)) that makes unbiased

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

The Best Linear Unbiased Estimator (BLUE) The constraints or limitations on finding the MVU Do not know the PDF Not able to produce the MVU estimator even if the PDF is

given Faced with our inability to determine the optimal MVU

estimator, it is reasonable to resort to a suboptimal one An estimator which is linear in the data The linear estimator is unbiased as well and has minimum

variance The estimator is termed the best linear unbiased estimator Can be determined with the first and the second moments of

PDF, thus complete knowledge of the PDF is not necessary

Institute of Communications Engineering, ECE, NCTU 42

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 43

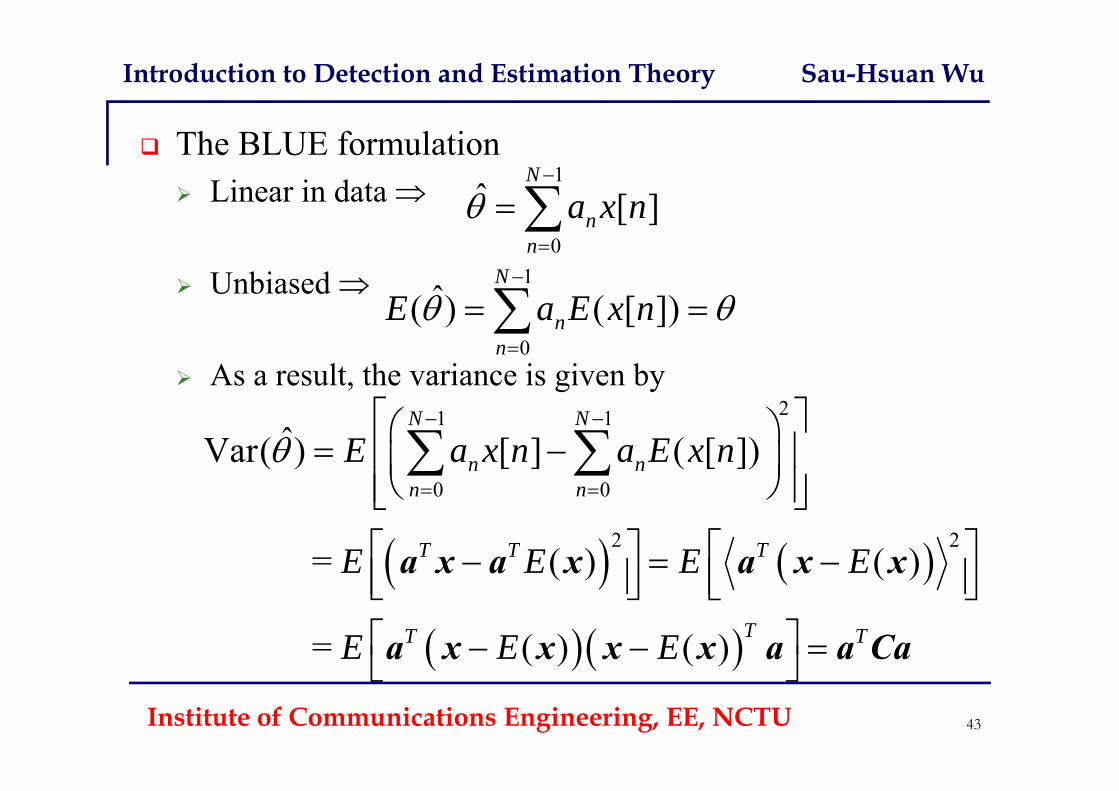

The BLUE formulation Linear in data

Unbiased

As a result, the variance is given by

1

0

ˆ [ ]N

nn

a x n

1

0

ˆ( ) ( [ ])N

nn

E a E x n

21 1

0 0

22

ˆVar( ) [ ] ( [ ])

= ( ) ( )

= ( ) ( )

N N

n nn n

T T T

TT T

E a x n a E x n

E E E E

E E E

a x a x a x x

a x x x x a a Ca

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 44

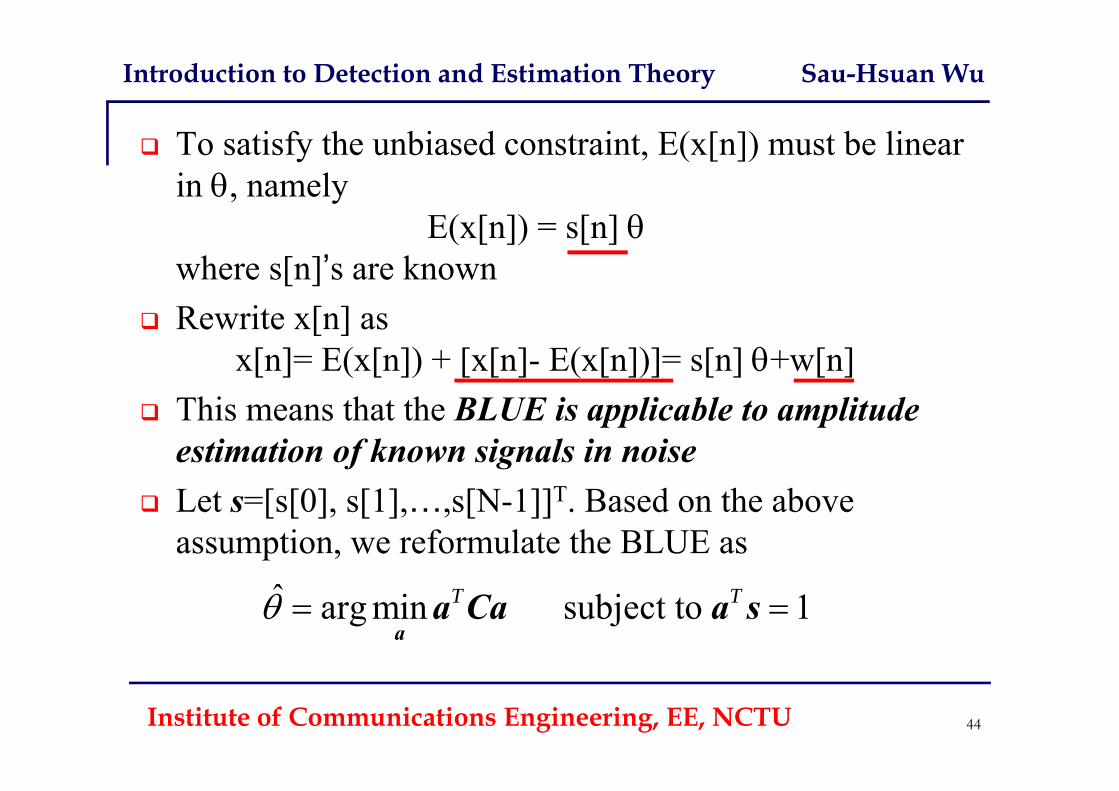

To satisfy the unbiased constraint, E(x[n]) must be linear in , namely

E(x[n]) = s[n] where s[n]’s are known

Rewrite x[n] as x[n]= E(x[n]) + [x[n]- E(x[n])]= s[n] +w[n]

This means that the BLUE is applicable to amplitude estimation of known signals in noise

Let s=[s[0], s[1],…,s[N-1]]T. Based on the above assumption, we reformulate the BLUE as

ˆ arg min subject to 1T T a

a Ca a s

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 45

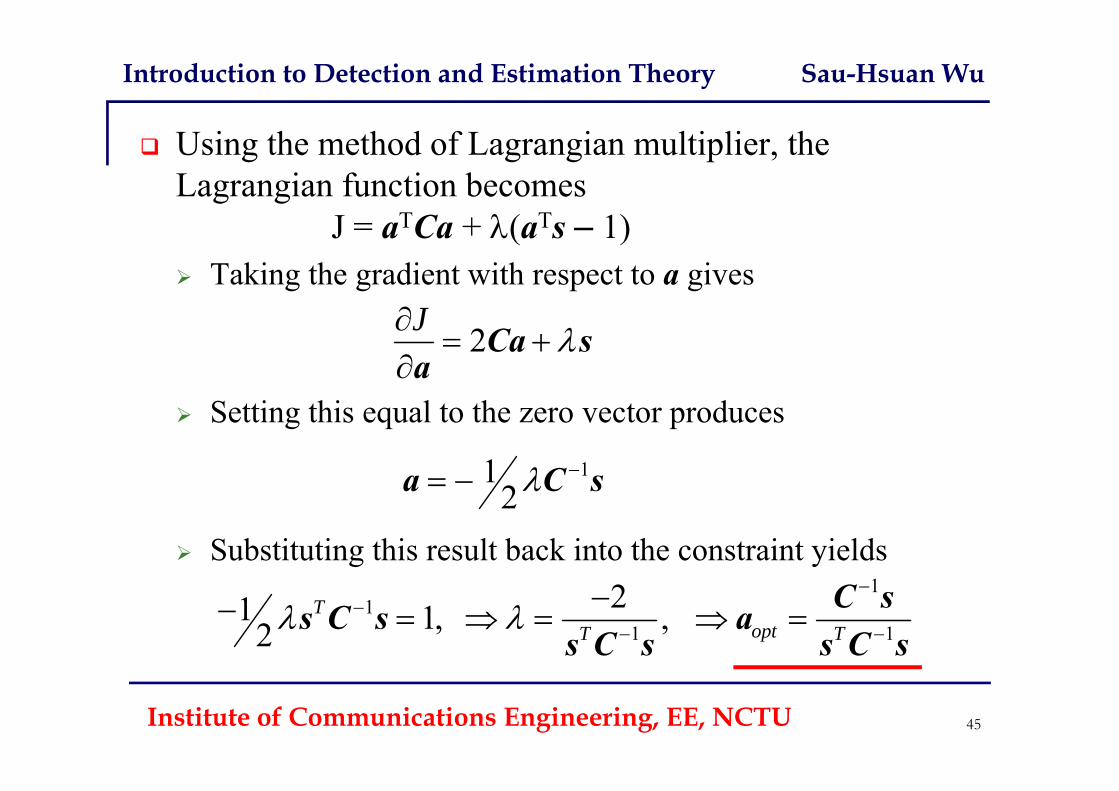

Using the method of Lagrangian multiplier, the Lagrangian function becomes

J = aTCa + (aTs – 1) Taking the gradient with respect to a gives

Setting this equal to the zero vector produces

Substituting this result back into the constraint yields

2J

Ca s

a

112

a C s

11

1 121 1, , 2

ToptT T

C ss C s a

s C s s C s

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 46

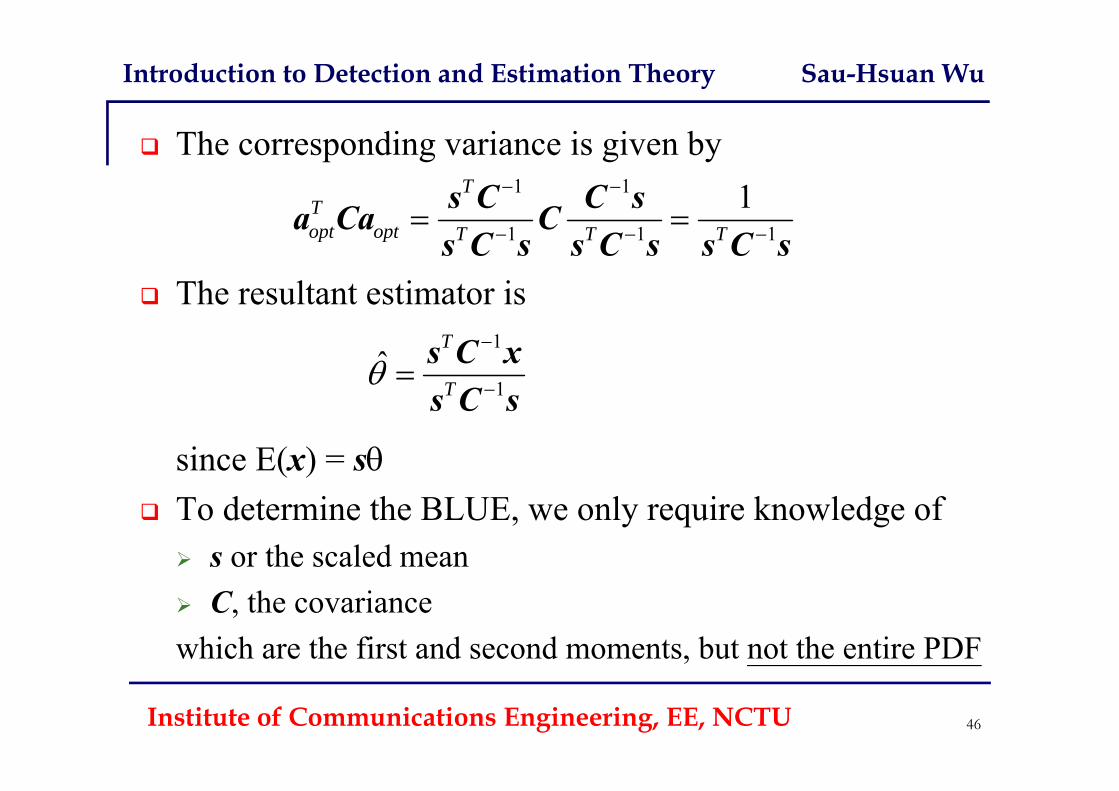

The corresponding variance is given by

The resultant estimator is

since E(x) = s To determine the BLUE, we only require knowledge of s or the scaled mean C, the covariancewhich are the first and second moments, but not the entire PDF

1 1

1 1 11T

Topt opt T T T

s C C sa Ca Cs C s s C s s C s

1

1ˆ

T

T

s C xs C s

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 47

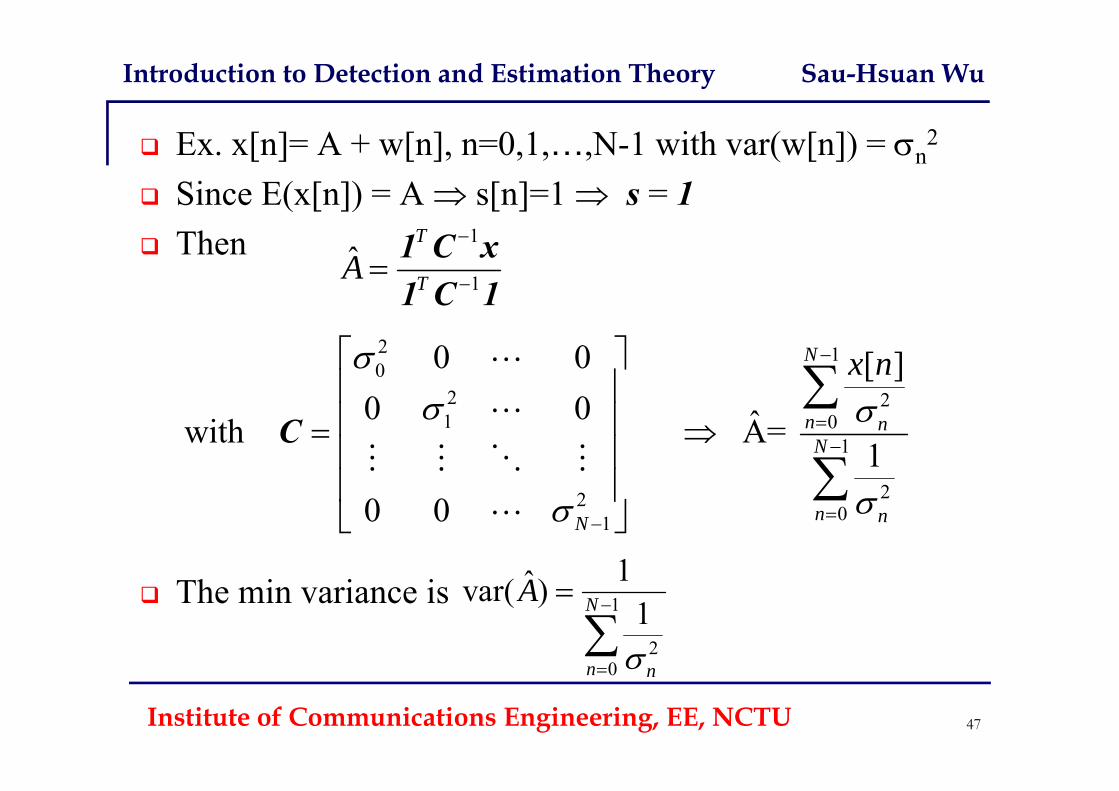

Ex. x[n]= A + w[n], n=0,1,…,N-1 with var(w[n]) = n2

Since E(x[n]) = A s[n]=1 s = 1 Then

The min variance is

1

1ˆ

T

TA

1 C x1 C 1

1

20

1ˆvar( )1N

n n

A

2 10

2 21 0

1

2201

0 0 [ ]0 0 ˆwith A=

10 0

N

n nN

n nN

x n

C

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

48Institute of Communications Engineering, EE, NCTU

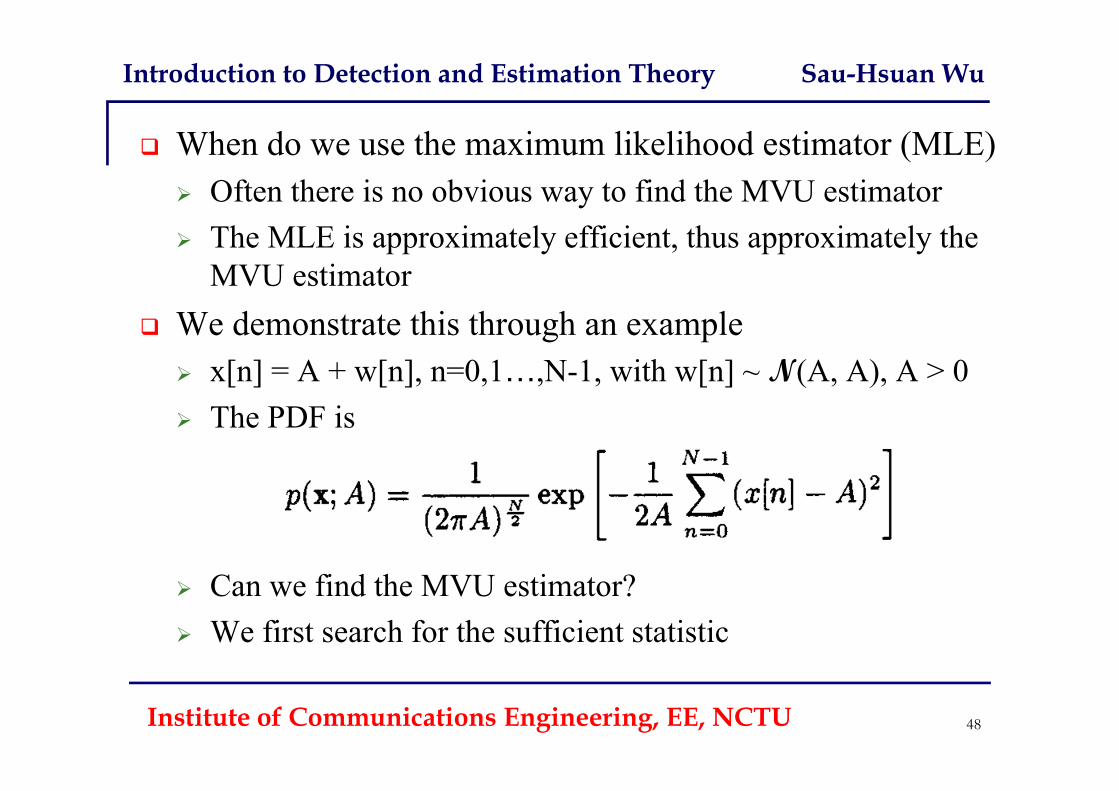

When do we use the maximum likelihood estimator (MLE) Often there is no obvious way to find the MVU estimator The MLE is approximately efficient, thus approximately the

MVU estimator We demonstrate this through an example x[n] = A + w[n], n=0,1…,N-1, with w[n] ~ N(A, A), A > 0 The PDF is

Can we find the MVU estimator? We first search for the sufficient statistic

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

49Institute of Communications Engineering, EE, NCTU

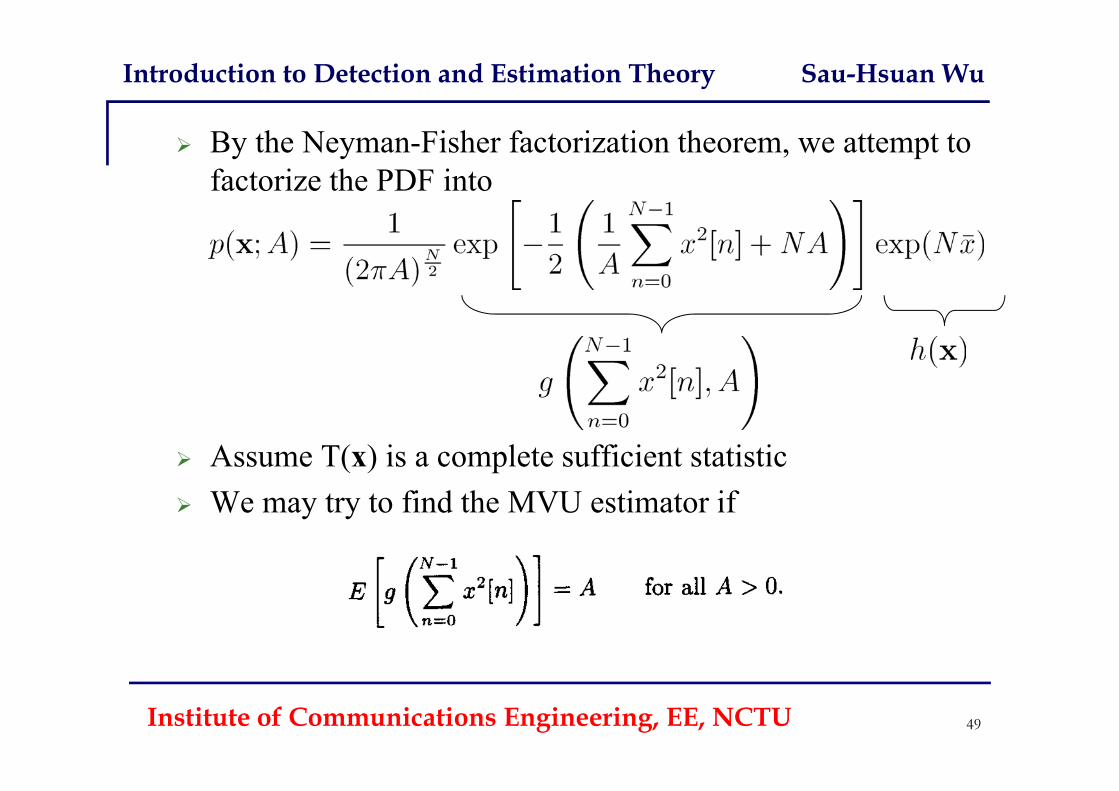

By the Neyman-Fisher factorization theorem, we attempt to factorize the PDF into

Assume T(x) is a complete sufficient statistic We may try to find the MVU estimator if

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

50Institute of Communications Engineering, EE, NCTU

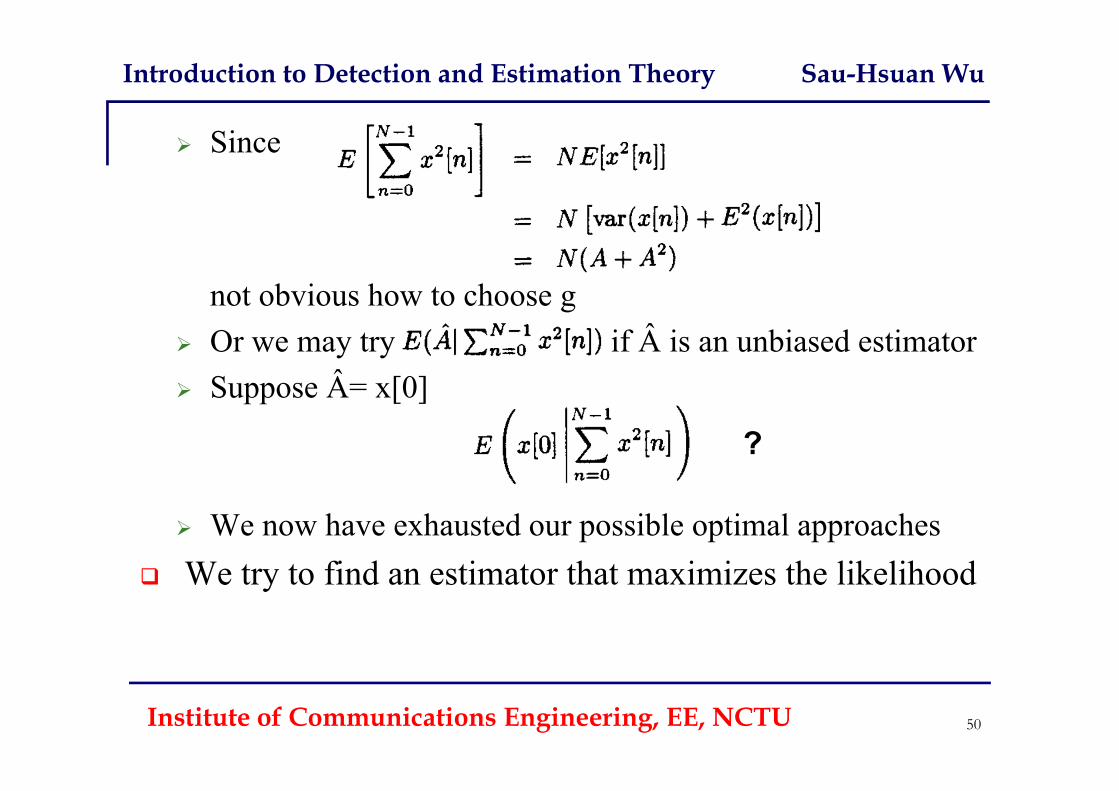

Since

not obvious how to choose g Or we may try if  is an unbiased estimator Suppose Â= x[0]

We now have exhausted our possible optimal approaches We try to find an estimator that maximizes the likelihood

?

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

51Institute of Communications Engineering, EE, NCTU

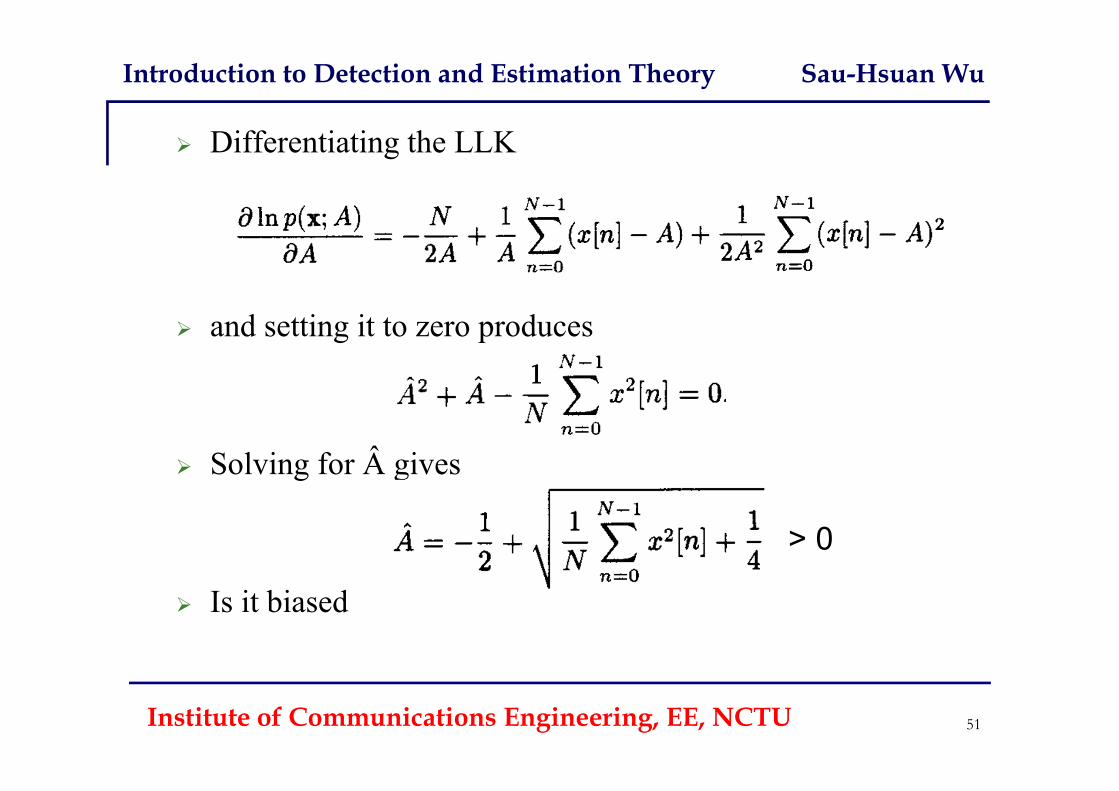

Differentiating the LLK

and setting it to zero produces

Solving for  gives

Is it biased

> 0

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

52Institute of Communications Engineering, EE, NCTU

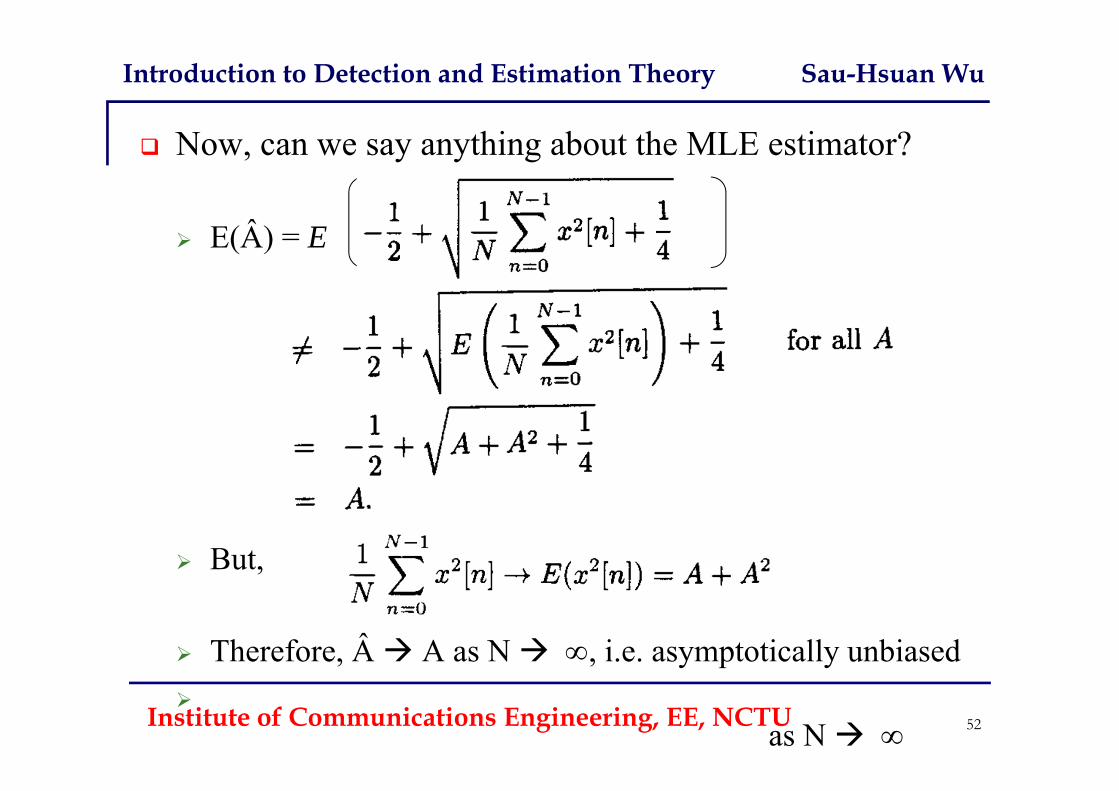

Now, can we say anything about the MLE estimator?

E(Â) = E

But,

Therefore, Â A as N , i.e. asymptotically unbiased

as N

The Bayesian Philosophy and General Estimators

Institute of Communications Engineering, ECE, NCTU 53

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 54

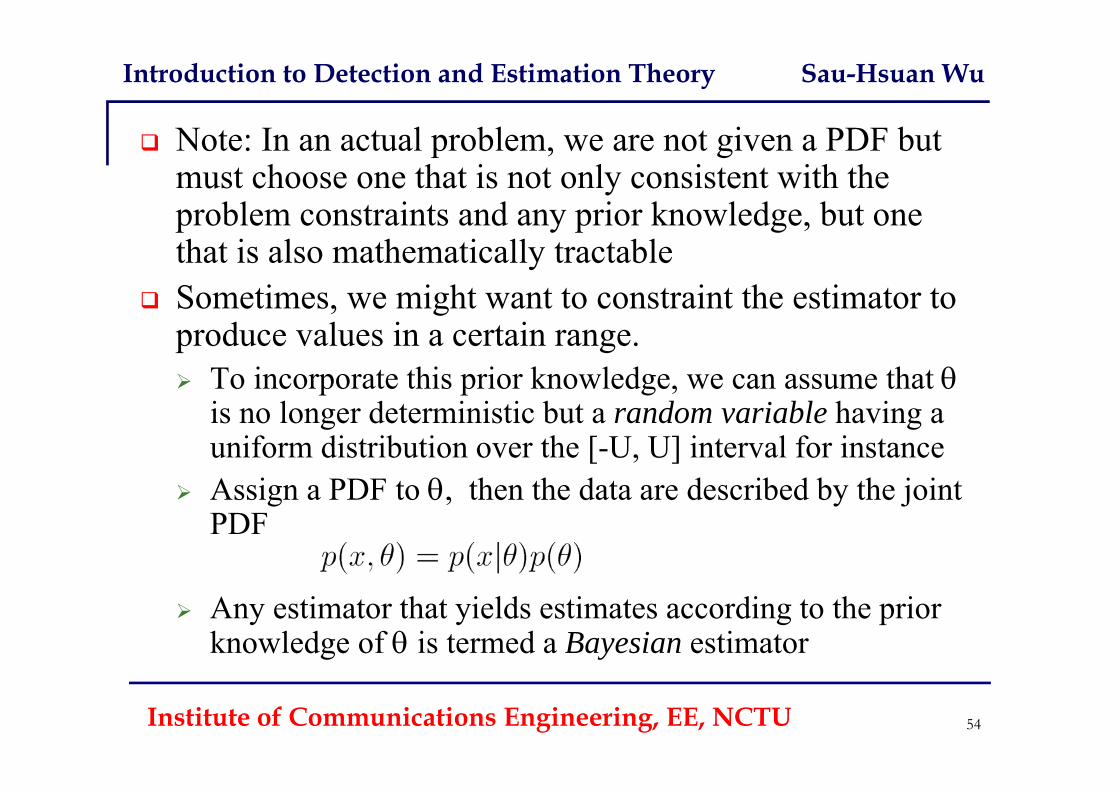

Note: In an actual problem, we are not given a PDF but must choose one that is not only consistent with the problem constraints and any prior knowledge, but one that is also mathematically tractable

Sometimes, we might want to constraint the estimator to produce values in a certain range. To incorporate this prior knowledge, we can assume that

is no longer deterministic but a random variable having a uniform distribution over the [-U, U] interval for instance

Assign a PDF to , then the data are described by the joint PDF

Any estimator that yields estimates according to the prior knowledge of is termed a Bayesian estimator

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

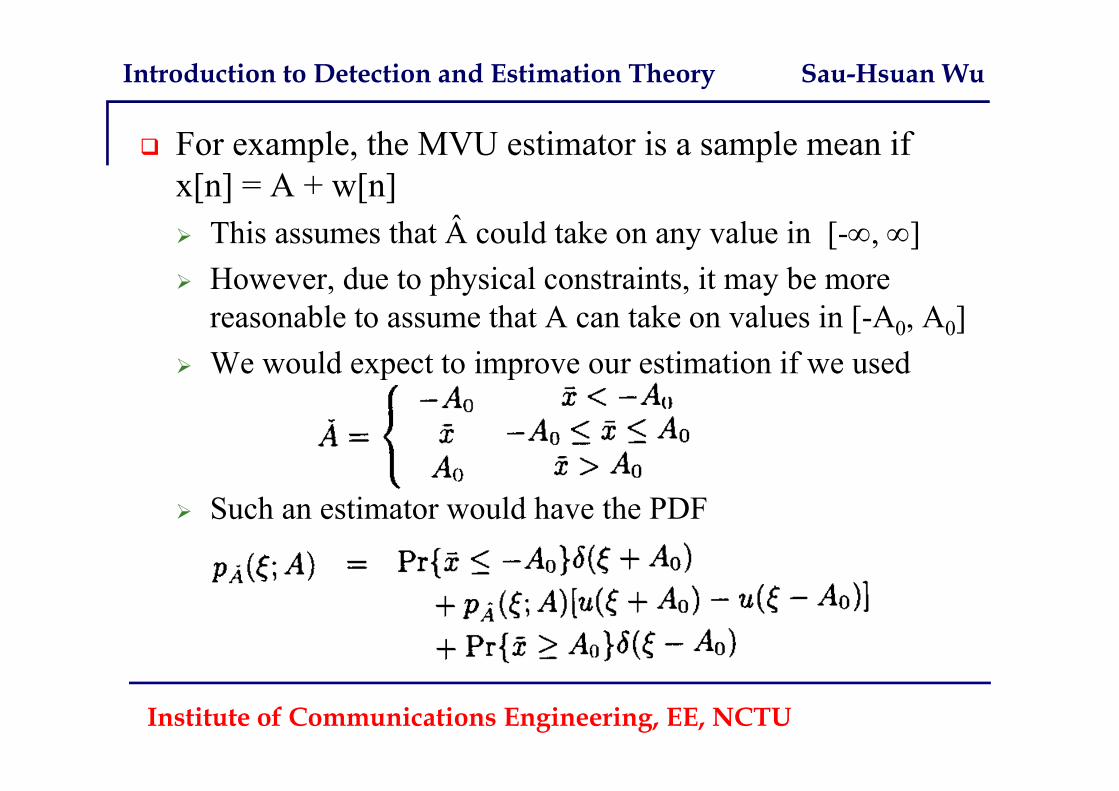

For example, the MVU estimator is a sample mean if x[n] = A + w[n] This assumes that  could take on any value in [-, ] However, due to physical constraints, it may be more

reasonable to assume that A can take on values in [-A0, A0] We would expect to improve our estimation if we used

Such an estimator would have the PDF

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

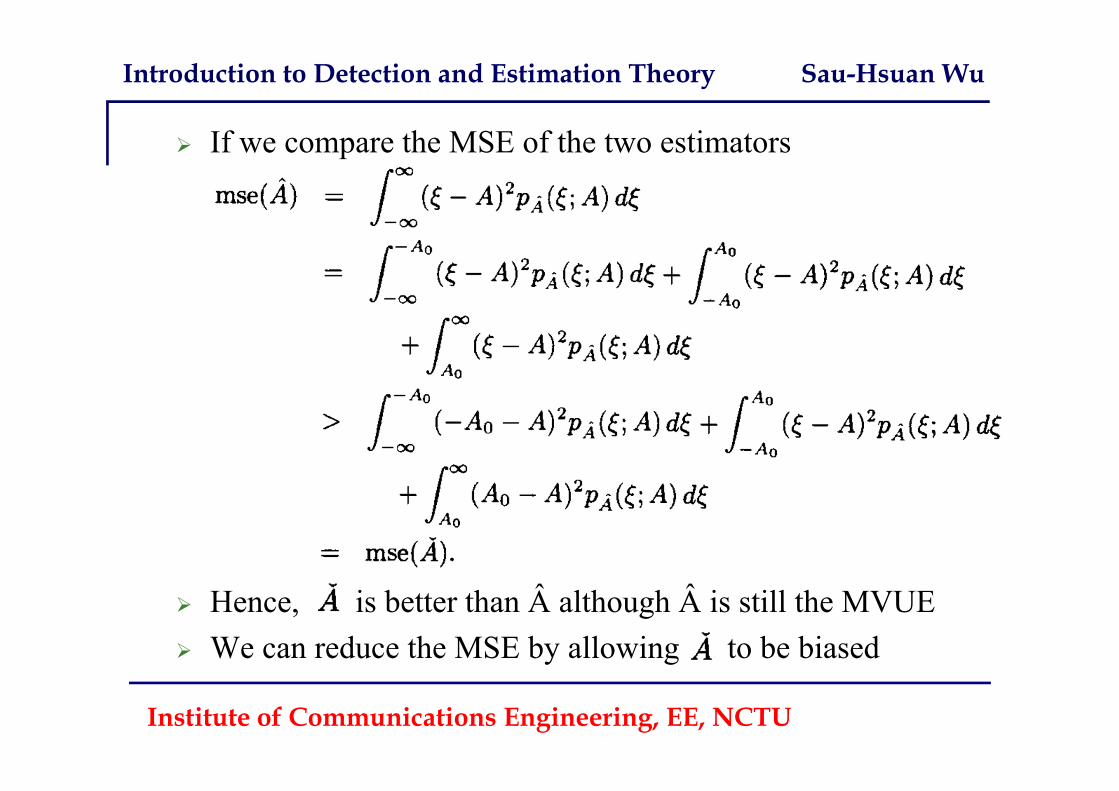

If we compare the MSE of the two estimators

Hence, is better than  although  is still the MVUE We can reduce the MSE by allowing to be biased

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

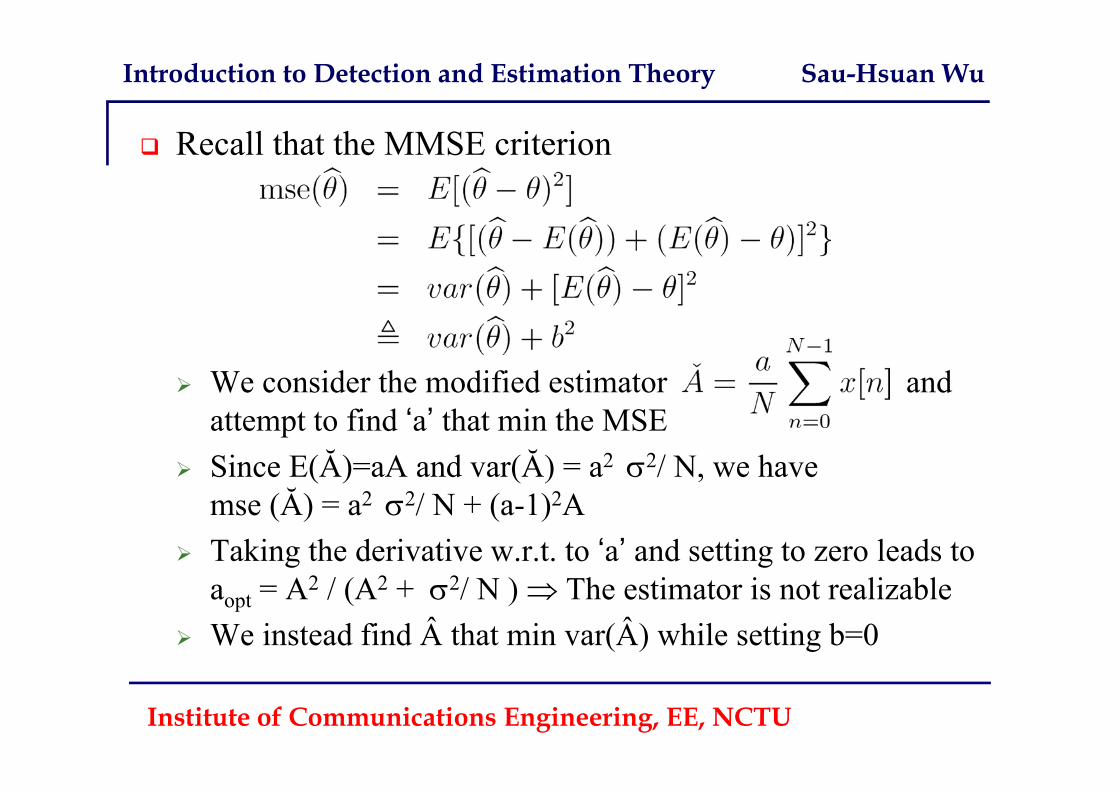

Recall that the MMSE criterion

We consider the modified estimator and attempt to find ‘a’ that min the MSE

Since E(Ă)=aA and var(Ă) = a2 2/ N, we havemse (Ă) = a2 2/ N + (a-1)2A

Taking the derivative w.r.t. to ‘a’ and setting to zero leads toaopt = A2 / (A2 + 2/ N ) The estimator is not realizable

We instead find  that min var(Â) while setting b=0

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

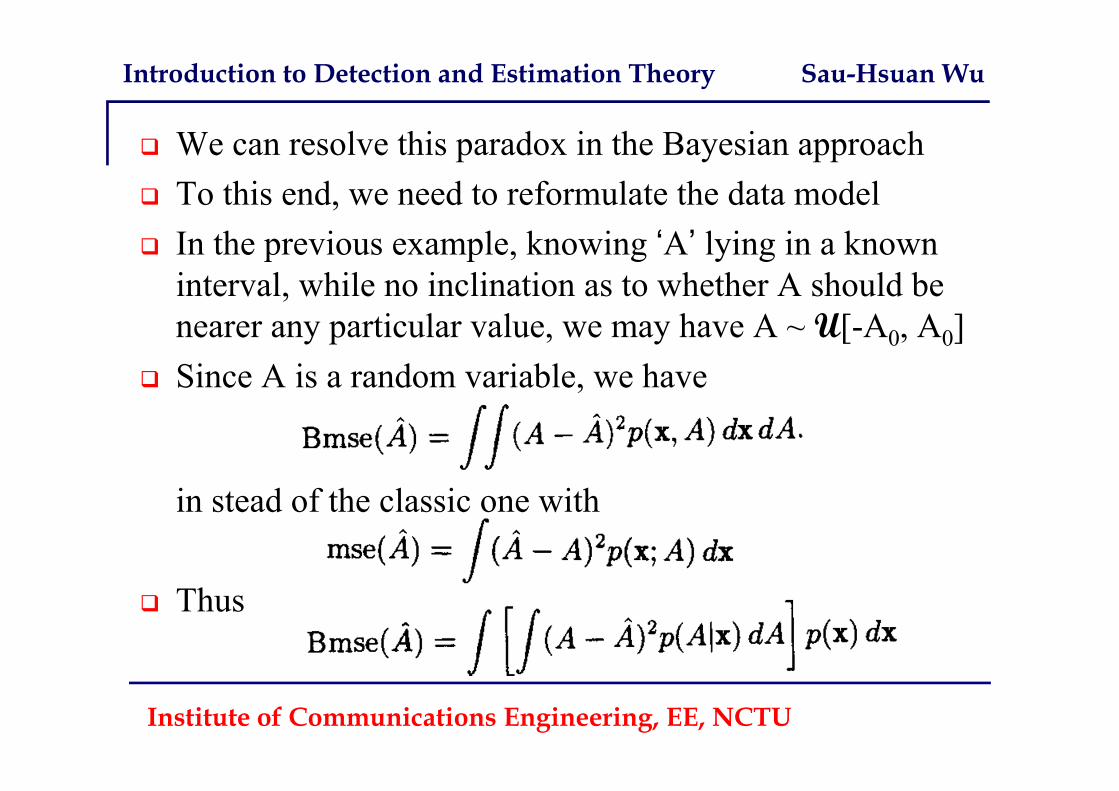

We can resolve this paradox in the Bayesian approach To this end, we need to reformulate the data model In the previous example, knowing ‘A’ lying in a known

interval, while no inclination as to whether A should be nearer any particular value, we may have A ~ U[-A0, A0]

Since A is a random variable, we have

in stead of the classic one with

Thus

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

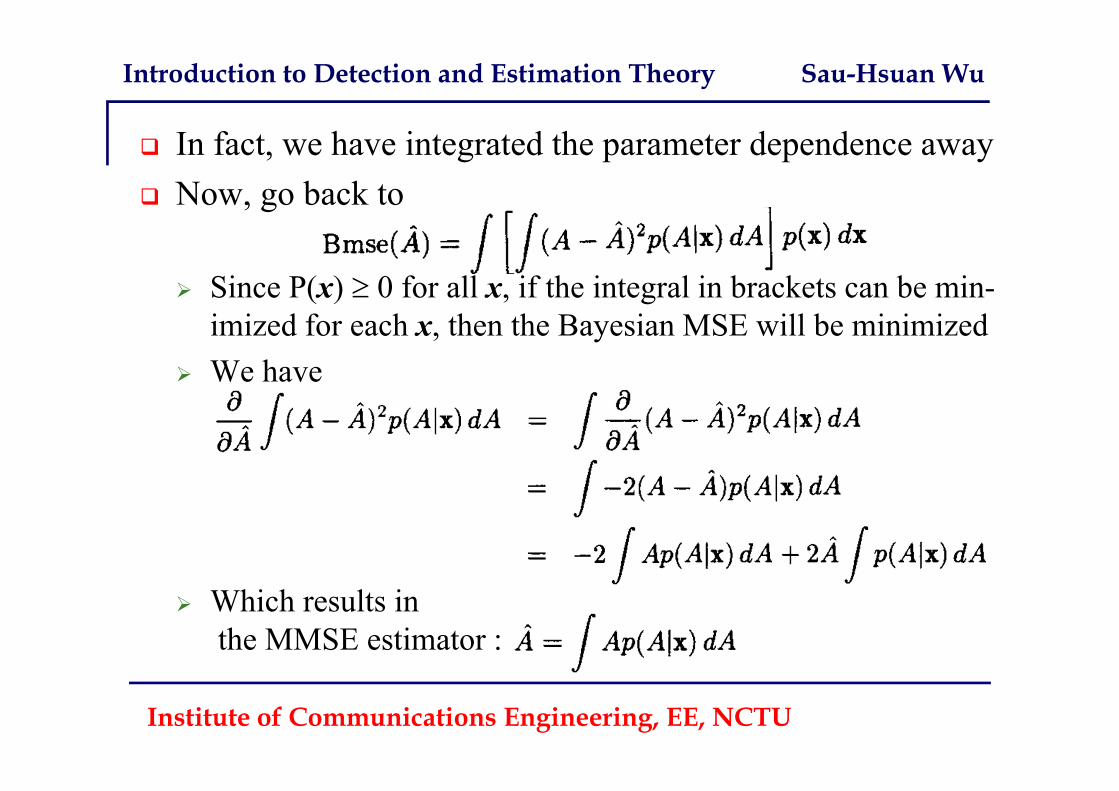

In fact, we have integrated the parameter dependence away Now, go back to

Since P(x) 0 for all x, if the integral in brackets can be min-imized for each x, then the Bayesian MSE will be minimized

We have

Which results inthe MMSE estimator :

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

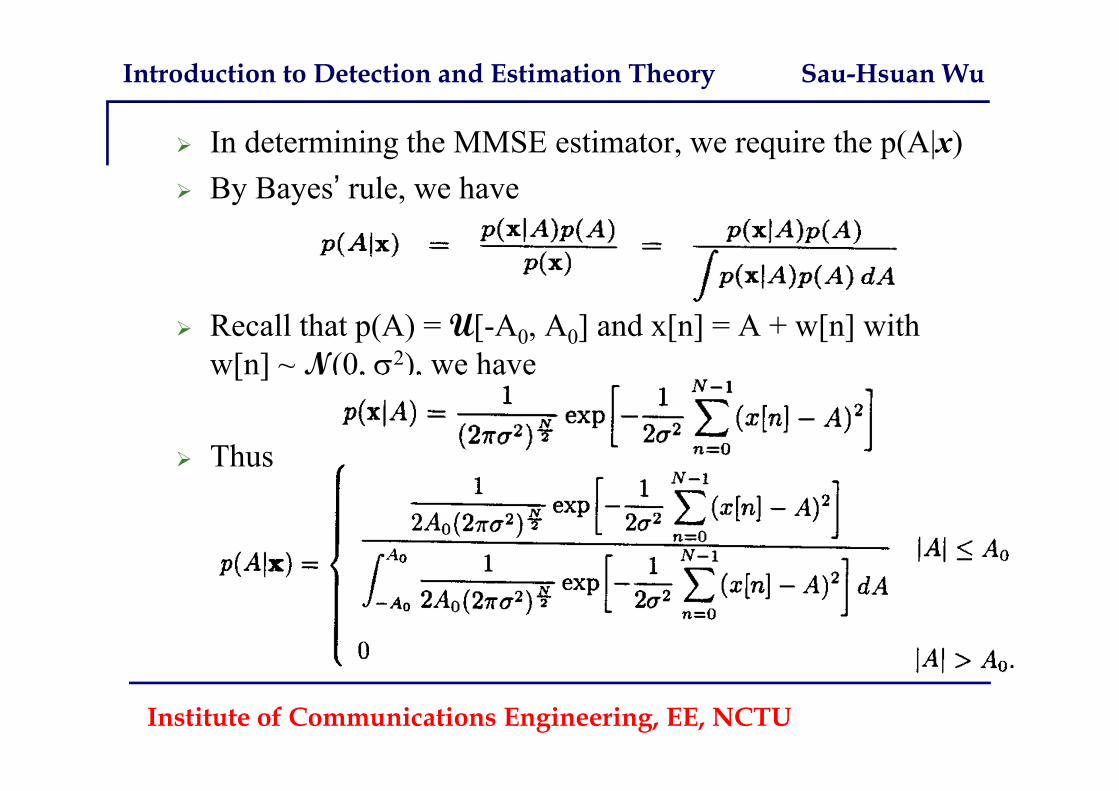

In determining the MMSE estimator, we require the p(A|x) By Bayes’ rule, we have

Recall that p(A) = U[-A0, A0] and x[n] = A + w[n] with w[n] ~ N(0, 2), we have

Thus

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

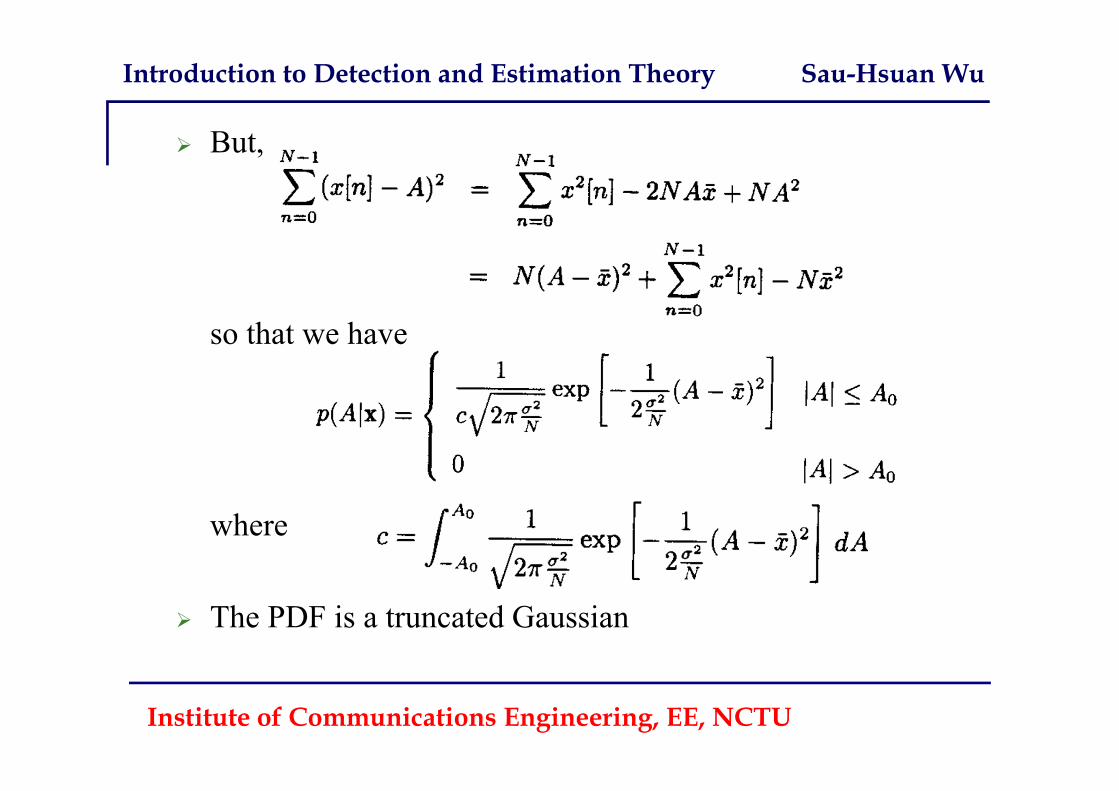

But,

so that we have

where

The PDF is a truncated Gaussian

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

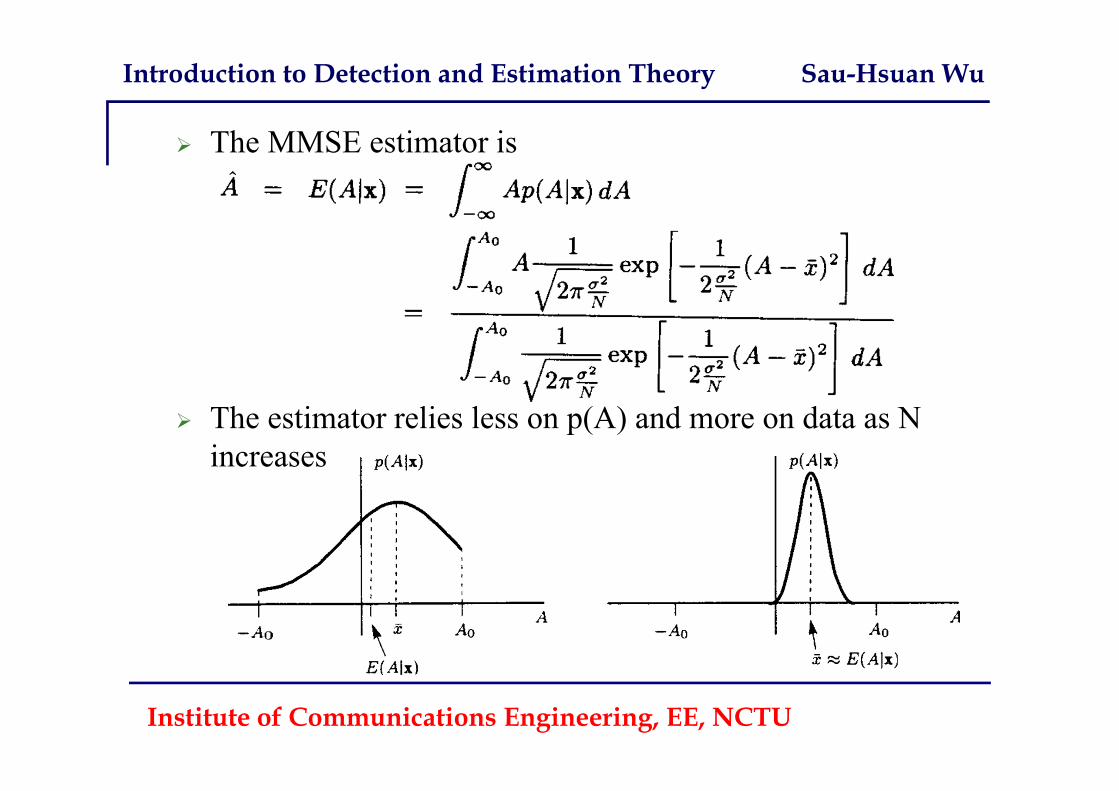

The MMSE estimator is

The estimator relies less on p(A) and more on data as N increases

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

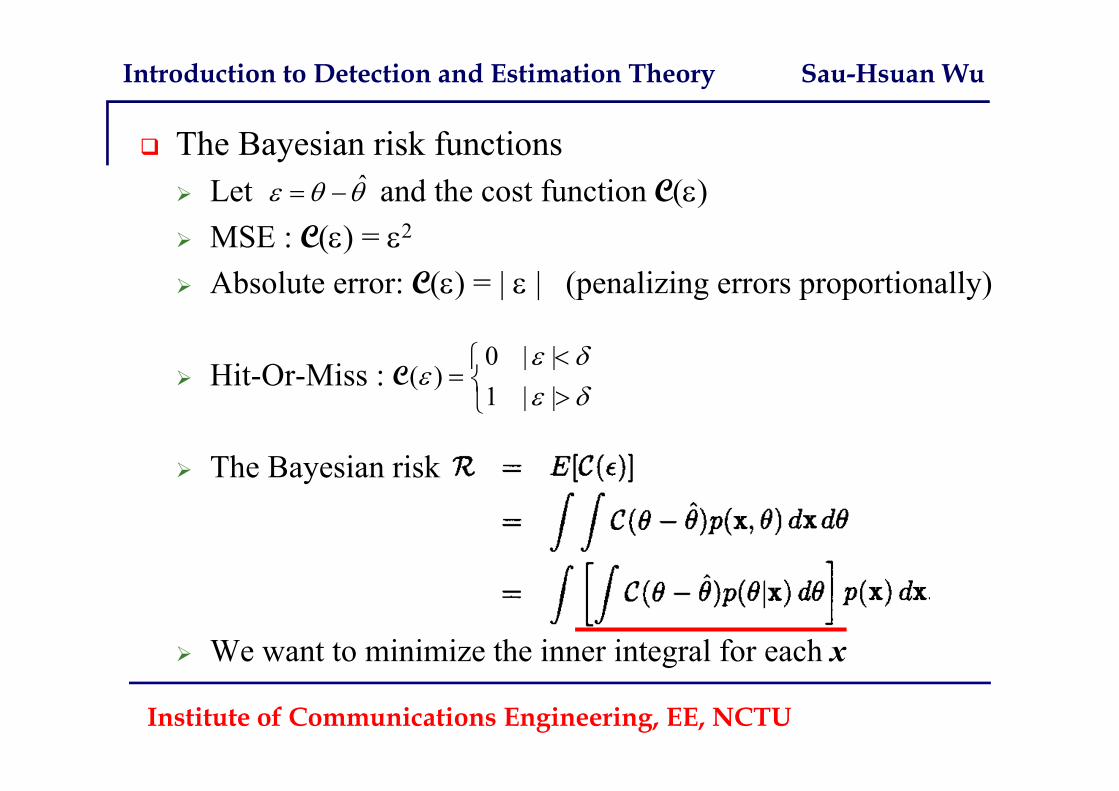

The Bayesian risk functions Let and the cost function C() MSE : C() = 2

Absolute error: C() = | | (penalizing errors proportionally)

Hit-Or-Miss :

The Bayesian risk

We want to minimize the inner integral for each x

ˆ

0 | |( )

1 | |

C

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

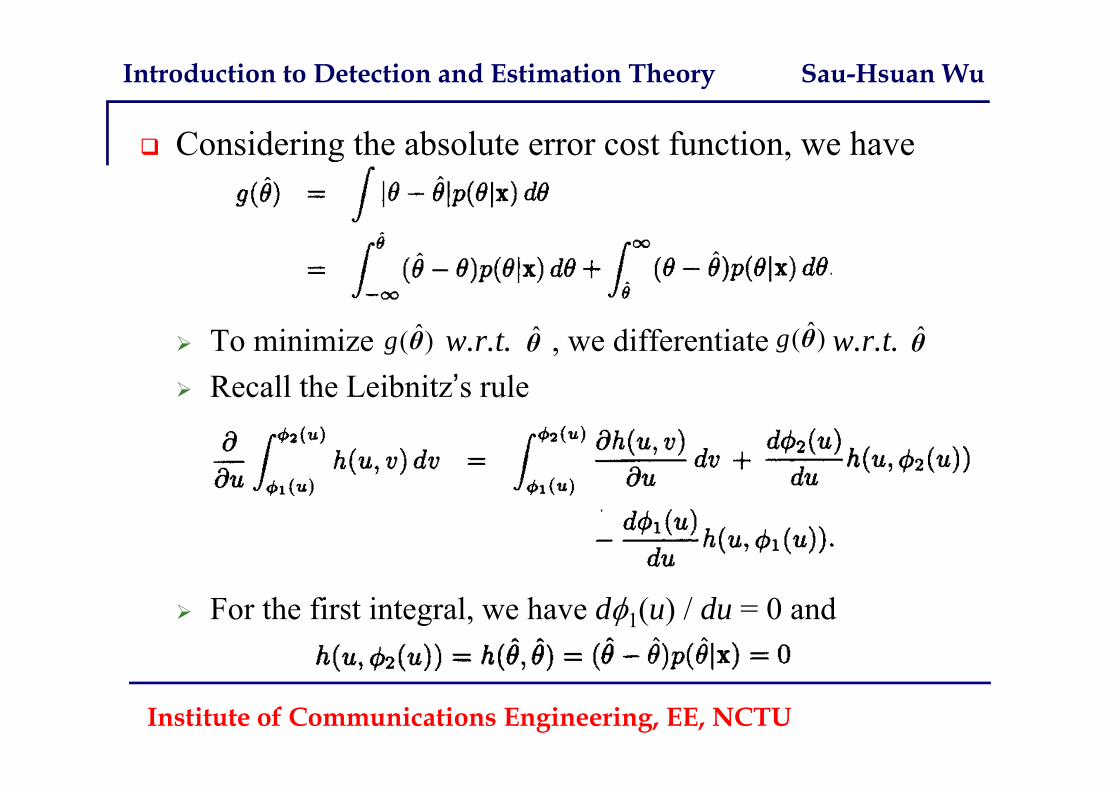

Considering the absolute error cost function, we have

To minimize w.r.t. , we differentiate w.r.t. Recall the Leibnitz’s rule

For the first integral, we have d1(u) / du = 0 and

θ̂ˆ( )g θ ˆ( )g θ θ̂

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

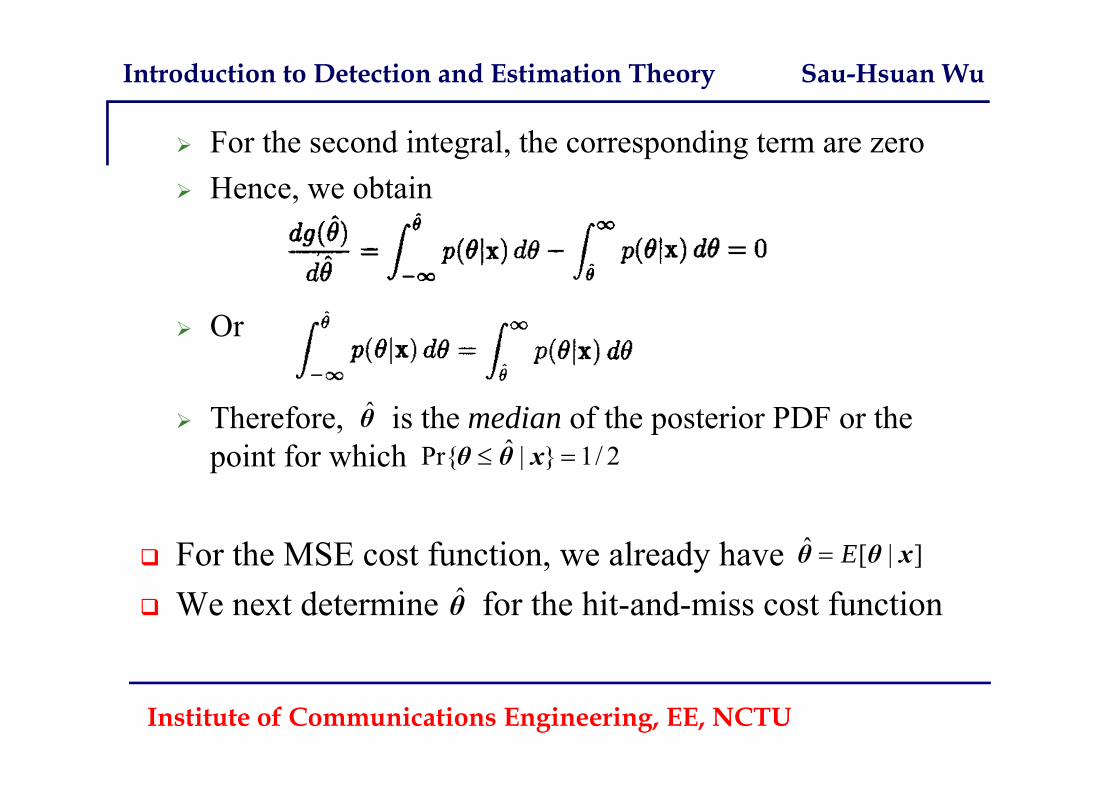

For the second integral, the corresponding term are zero Hence, we obtain

Or

Therefore, is the median of the posterior PDF or the point for which

For the MSE cost function, we already have We next determine for the hit-and-miss cost function

θ̂ˆPr{ | } 1/ 2 θ θ x

ˆ [ | ]Eθ θ x

θ̂

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

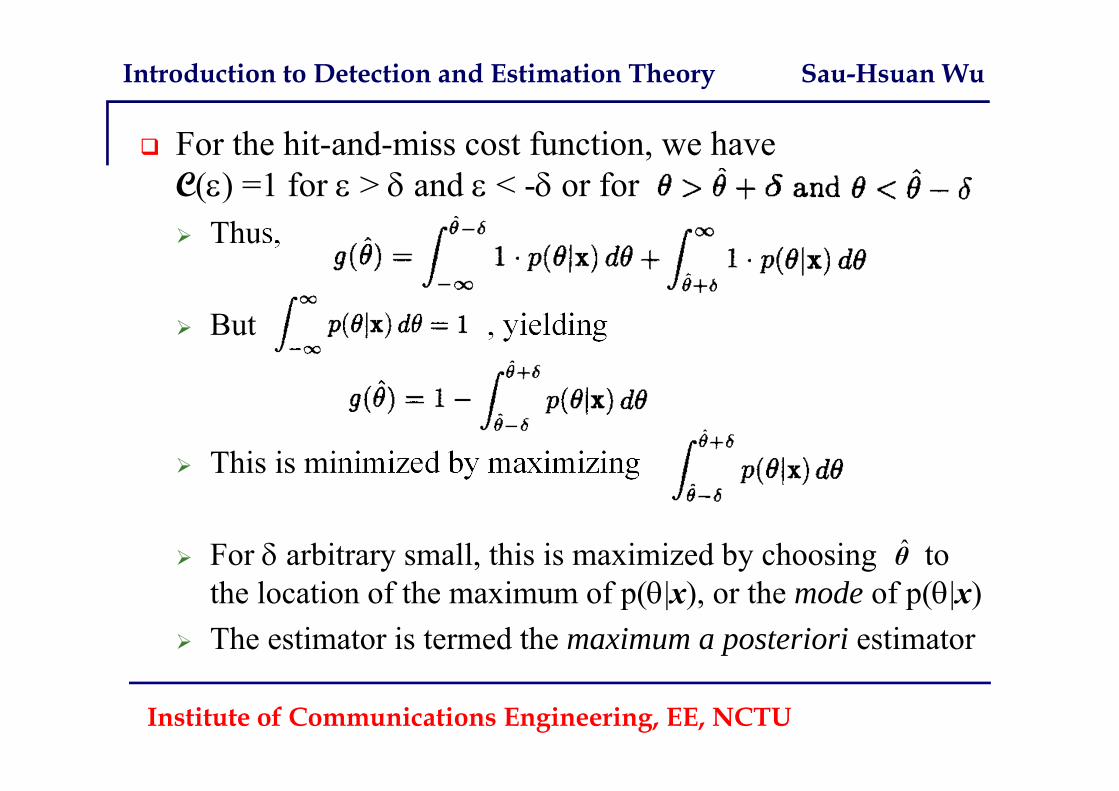

For the hit-and-miss cost function, we have C() =1 for > and < - or for Thus,

But , yielding

This is minimized by maximizing

For arbitrary small, this is maximized by choosing to the location of the maximum of p(|x), or the mode of p(|x)

The estimator is termed the maximum a posteriori estimator

θ̂

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU

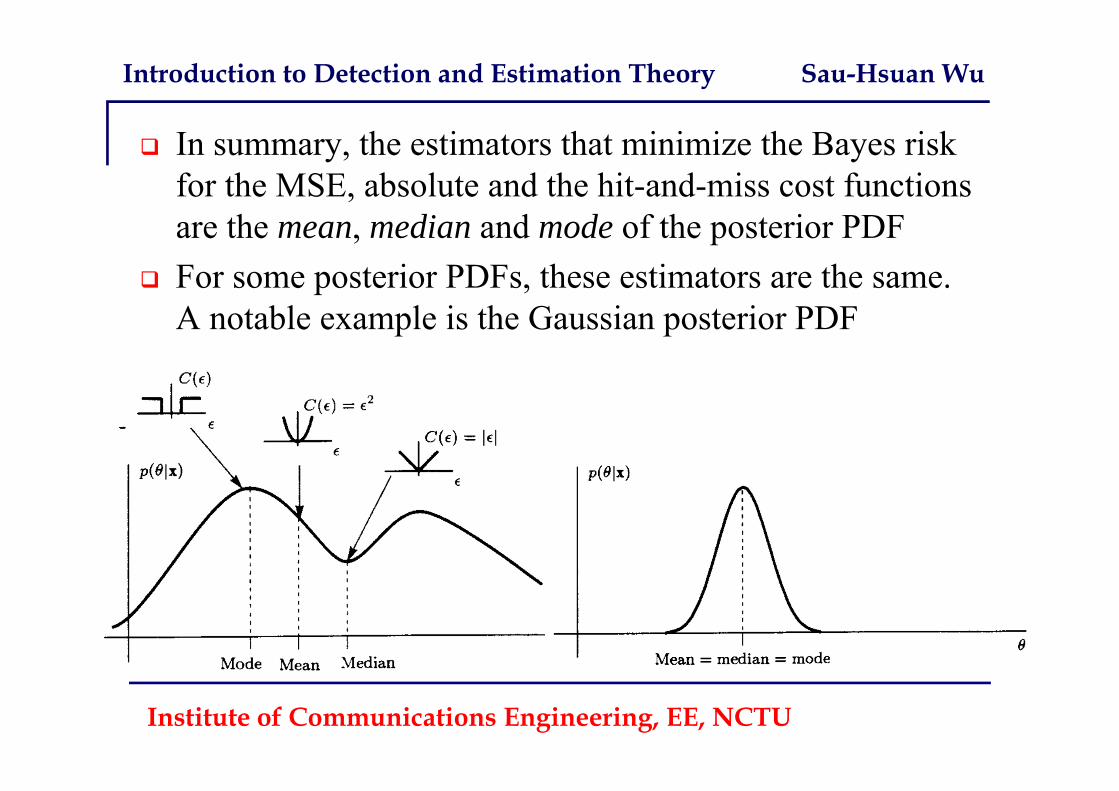

In summary, the estimators that minimize the Bayes risk for the MSE, absolute and the hit-and-miss cost functions are the mean, median and mode of the posterior PDF

For some posterior PDFs, these estimators are the same. A notable example is the Gaussian posterior PDF

Introduction to Detection and Estimation Theory Sau-Hsuan Wu

Institute of Communications Engineering, EE, NCTU 68

Summary Detection theory

Neyman-Pearson detector Bayesian detector, including

MAP estimator ML detector Multiple hypothesis testing

Estimation theory MUV estimator Sufficient statistics The BLUE estimator The ML estimator The general Bayesian estimators