Desynchronising Global Economy

40

2012 Global Outlook: De-synchronizing the Global Economy December 2011 Neal M. Soss, Managing Director Chief Economist 212-325-3335 [email protected] ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES ARE IN THE DISCLOSURE APPENDIX. FOR OTHER IMPORTANT DISCLOSURES, PLEASE REFER TO https://firesearchdisclosure.credit-suisse.com.

Transcript of Desynchronising Global Economy

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 1/40

2012 Global Outlook:

De-synchronizing the Global Economy

December 2011

Neal M. Soss, Managing Director

Chief Economist

212-325-3335

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES ARE IN THE DISCLOSURE APPENDIX. FOR OTHER IMPORTANT

DISCLOSURES, PLEASE REFER TO https://firesearchdisclosure.credit-suisse.com.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 2/40

2

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 3/40

3

Chasm: Monetary Policy versus Credit Stress

Monetary policy responseThe financial system is in a fragile state. Some institution, market, or

instrument seems always at the edge of breaking down – or just over that

edge. Very low interest rates throughout the developed world pose a

significant challenge to the profitability of traditional financial business models

by reducing the rewards of maturity transformation. New regulatory initiatives,

including especially higher capital-to-asset ratio requirements on ever more

strictly construed asset classifications, inhibit the volume and profitability of credit transformation. (No surprise there – that’s what deleveraging the

developed economies is all about.)

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 4/40

4

Ultra-low interest rates tend to be more persistent than ultra-high ones.

This partly reflects the asymmetry in the efficiency of monetary policy in

stimulating versus restraining economic activity. It also partly reflects the

arithmetic of fiscal sustainability: low interest rates suppress the debt service

cost entry for debtor governments, while high interest rates contribute to

explosive debt-to-GDP dynamics. Finally, the exit from ultra-low interest ratesis higher interest rates – that is, a bear market in bonds. Bear markets tend to

expose and magnify financial fragilities; therefore, human nature tends to

incline the monetary authorities to a more cautious pace of raising interest

rates.

While ultra-low interest rates are still performing their corrosive role on

the profitability of the financial sector business model, the sector is also

trying to accommodate an emergent regulatory environment.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 5/40

5

One dimension of that regime is clear enough in outline. Banks and other

financial intermediaries will be required to hold more capital per unit of assets

– that is, to deleverage. There are two ways to raise a capital-asset ratio: add

capital or subtract assets. Raising capital has the potentially undesirable

feature of diluting existing shareholders. So banks will seek to accomplish at

least some of their deleveraging by shedding assets. But when all (or a large

subset of all) financial intermediaries are seeking to disgorge assets, market

prices will tend to weaken, bid-ask spreads to widen, liquidity to evaporate,

perceived counter-party risk to rise, term funding to run for the hills – in sum,

the syndrome that has manifested repeatedly since the summer of 2007.

When this syndrome of financial fragility is present, the only balance

sheet adequate to absorb the orphaned assets is the central bank’s –

hence QE.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 6/40

6

The Bank of Japan has been at this longest and has gone furthest – to the

point of buying ETFs on its own stock market. The Bank of England and the

US Fed have undertaken significant QE, arguably with more of a focus on aportfolio balance effect to encourage holding of riskier assets. The ECB has so

far dipped its toe tentatively into these waters, but we expect considerable

expansion of its efforts, at least selectively, toward Europe’s troubled

sovereigns.

The bottom line is that QE is probably a necessary component of

managing the ongoing restructuring of the global financial system.

That’s the First World central bank response. For the rest of the world, more

conventional monetary policy responses are still available (because policy

rates are still well above zero). Central banks in Australia and Brazil havealready begun to cut rates to counter the risks to global economic growth and

financial stability. We expect more of the same from them and expect others,

such as India and Thailand, to join the easing policy posture soon enough.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 7/40

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 8/40

8

At the same time, the ECB under President Draghi has proved to be more

active than expected, already cutting rates by 50 bps to 1.00%. We expect

more. In our view, this greater activism may augur well for more forcefulinterventions from the ECB in government bond markets. The ECB must be

viewed as being in an asymmetrical posture whereby the cash rate for euros

could come down but cannot be expected to rise while the public finances of

much of the Continent are in tatters and the growth outlook ranges fromanemic to something worse.

The familiar workings of the Capital Asset Pricing Model imply that the

variance (or volatility) of capital asset prices includes the expected variance of the rate of interest on cash over the expected holding period of the asset plus

twice the covariance of that cash rate with the remaining market risks.

When the central bank effectively puts the variance and the covariance

to zero, the volatility of all capital asset prices should be suppressed,putting a bullish underpinning to risk asset markets of all kinds –

whether longer-dated bonds or credit instruments or equities. That's the

monetary conditions contribution.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 9/40

9

Credit conditions are different. The quarter-century from 1982 to 2007

featured ever-easier access to credit, whether for US homeowners or Greek

citizens. That credit boom allowed for more consumption-smoothing than

would otherwise have occurred, suppressing the volatility of real economic

performance in what came to be called the Great Moderation. It is patently

clear that the terms and standards of access to credit are no longer in a

secular easing – just ask American homeowners or Greek public-sector

workers or, if reports are to be believed, certain euro zone banks seeking term

funding. Credit underwriting standards now fluctuate around a tighter meanthan prevailed in 2007, with little sense that Basel 3 and other regulatory

innovations will allow for, let alone encourage, renewed secular easing.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 10/40

10

That implies less consumption-smoothing by households or investment-

smoothing by businesses or even counter-cyclical fiscal operations by (many)

governments than was possible during the Great Moderation. And that, in turn,

implies a more volatile fundamental economic backdrop for risk assets. That

volatility has perhaps already begun to manifest itself in the inadequate

recovery from the last recession experienced by nearly all First World

countries and by the repeated pattern of alternating speed-up and slowdown

scares in the last few years. This is a force for increasing the volatility –

and correlation – of capital asset prices, whether manifested in yield curveshapes, credit spreads, or equities prices. In the context of an efficient-frontier

tradeoff between risk and return, this should be a force suppressing risk asset

prices.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 11/40

11

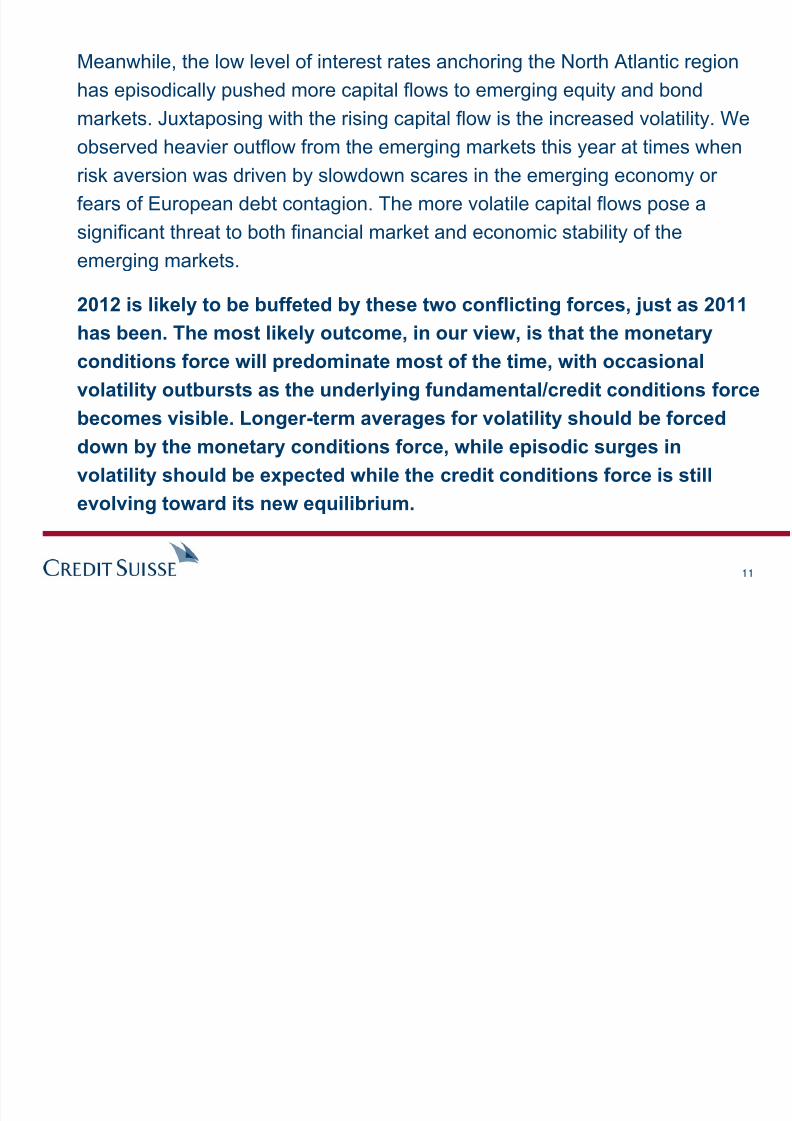

Meanwhile, the low level of interest rates anchoring the North Atlantic region

has episodically pushed more capital flows to emerging equity and bond

markets. Juxtaposing with the rising capital flow is the increased volatility. We

observed heavier outflow from the emerging markets this year at times when

risk aversion was driven by slowdown scares in the emerging economy or

fears of European debt contagion. The more volatile capital flows pose a

significant threat to both financial market and economic stability of the

emerging markets.

2012 is likely to be buffeted by these two conflicting forces, just as 2011

has been. The most likely outcome, in our view, is that the monetary

conditions force will predominate most of the time, with occasional

volatility outbursts as the underlying fundamental/credit conditions force

becomes visible. Longer-term averages for volatility should be forced

down by the monetary conditions force, while episodic surges in

volatility should be expected while the credit conditions force is still

evolving toward its new equilibrium.

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 12/40

12

Developed market policy rate forecastsFed funds rate; ECB repo rate; BoE bank rate

Emerging market nominal interest rates

0

1

2

3

4

5

6

05 06 07 08 09 10 11 12

Forecast

ECBBoEFed

3

4

5

6

7

8

Dec05 Dec06 Dec07 Dec08 Dec09 Dec10 Dec11 Dec12

Forecast

Source: Thomson Reuters DataStream, Credit Suisse Source: Thomson Reuters DataStream, Credit Suisse Emerging

Market Economics Team

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 13/40

13

US growth outlookChina growth outlook

Source: BEA, Credit Suisse

Source: NBS, Credit Suisse

-10

-8

-6

-4

-2

0

2

4

1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

QoQ% ann. rate

YoY%

Forecast

3

6

9

12

15

1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

YoY%

Forecast

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 14/40

14

Euro area growth outlookUK growth outlook

Source: Thomson Reuters DataStream, Credit Suisse Source: Thomson Reuters DataStream, Credit Suisse

-12

-10

-8

-6

-4

-2

0

2

4

1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

QoQ% ann. rate

YoY%

Forecast

-10

-8

-6

-4

-2

0

2

4

6

1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

QoQ% ann. rate

YoY%

Forecast

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 15/40

15

-1

0

1

2

3

4

5

6

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13

1985-2010 average growth rate @ 3.5%

2003-07 average growth rate @ 4.8%Fcst.

Global GDP growth

Source: IMF, Credit Suisse

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 16/40

16

Euro area shares of world imports12m ma; excludes intra euro zone trade

Source: Haver Analytics®, IMF, Credit Suisse Source: Bureau of Census, China Customs, IMF, Credit Suisse

US and China export shares to euro zone12m ma

15%

16%

17%

18%

00 01 02 03 04 05 06 07 08 09 10 1111%

12%

13%

14%

15%

16%

00 01 02 03 04 05 06 07 08 09 10 11

US

China

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 17/40

17

Foreign claims of euro area banks on emerging markets and the US

%, ultimate risk basis, End-March 2011

Source: BIS, IMF, Credit Suisse

81%

51%

20%

31%

12%

3%

13%

31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

EM Europe LTAM EM APAC US

% of total foreign claims

% of 2010 GDP

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 18/40

18

European bank deleveragingEuropean banks' share of total claims on the US, ultimate risk basis

Source: Credit Suisse

65%

70%

75%

80%

85%

Mar-05

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 19/40

19

European banks are scaling back internationally,

especially in money marketsData to April 2011, euro millions

Source: European Central Bank euro area BoP data, Credit Suisse

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

External liabilities, Money marketinstruments, MFIs

External assets, Money market

instruments, MFIs

External assets, Bonds and notes, MFIs

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 20/40

20

2012 financing needs for various euro area sovereigns €bn

Net Financing2012

BondRedemptions

Total FinancingNeed

Austria 8 14 22Belgium 13 28 41Finland 7 6 13France 83 99 182Germany 25 157 182Italy 32 193 225Netherlands 12 34 46Spain 40 50 90Total 220 581 801NOTE: These funding needs exclude those of Ireland, Portugal, and Greece, for which some financing will come fromEFSF issuance. Source: Credit Suisse

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 21/40

21

Brazil’s and Italy’s 5yr sovereign CDS spreadsbps

Source: the BLOOMBERG PROFESSIONAL™ service

0

100

200

300

400

500

600

700

J a

n - 0 7

M

a r - 0 7

M a

y - 0 7

J u l - 0 7

S e

p - 0 7

N o

v - 0 7

J a

n - 0 8

M

a r - 0 8

M a

y - 0 8

J u l - 0 8

S e

p - 0 8

N o

v - 0 8

J a

n - 0 9

M

a r - 0 9

M a

y - 0 9

J u l - 0 9

S e

p - 0 9

N o

v - 0 9

J a

n - 1 0

M

a r - 1 0

M a

y - 1 0

J u l - 1 0

S e

p - 1 0

N o

v - 1 0

J a

n - 1 1

M

a r - 1 1

M a

y - 1 1

J u l - 1 1

S e

p - 1 1

N o

v - 1 1

Brazil 5y CDS

Italy 5y CDS

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 22/40

22

Cross-country differences in the ratio of

gross government debt to GDP do not

generally explain cross-country differences

in sovereign risk spreads

Results of a regression of the log of CDS spreads in

November 2011 on the ratio of gross government debt

to GDP (as forecast by the IMF for the end of 2011)

for a sample including 41 countries drawn both from

the emerging markets and from the developed markets

Source: Credit Suisse, Haver Analytics®, and the IMF’s WorldEconomic Outlook

Source: Credit Suisse, Haver Analytics®, and the IMF’s WorldEconomic Outlook

R2

= 0.0281

3

4

5

6

7

8

9

0 50 100 150 200 250

Gross Govt debt (% of GDP)

L o g C D S

s p r

e a d v s

R2 = 0.0104

3

4

5

6

7

8

9

-15 -10 -5 0 5

Govt deficit as % of GDP

L o g C D S

s p

r e a d v s

… and neither do the cross-country

differences in the ratio of government fiscal

deficits to GDP

Results of a regression of the log of CDS spreads inNovember 2011 on the ratio of general governmentbalances to GDP (as forecast by the IMF for 2011) for asample including 41 countries drawn both from theemerging markets and from the developed markets

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 23/40

23

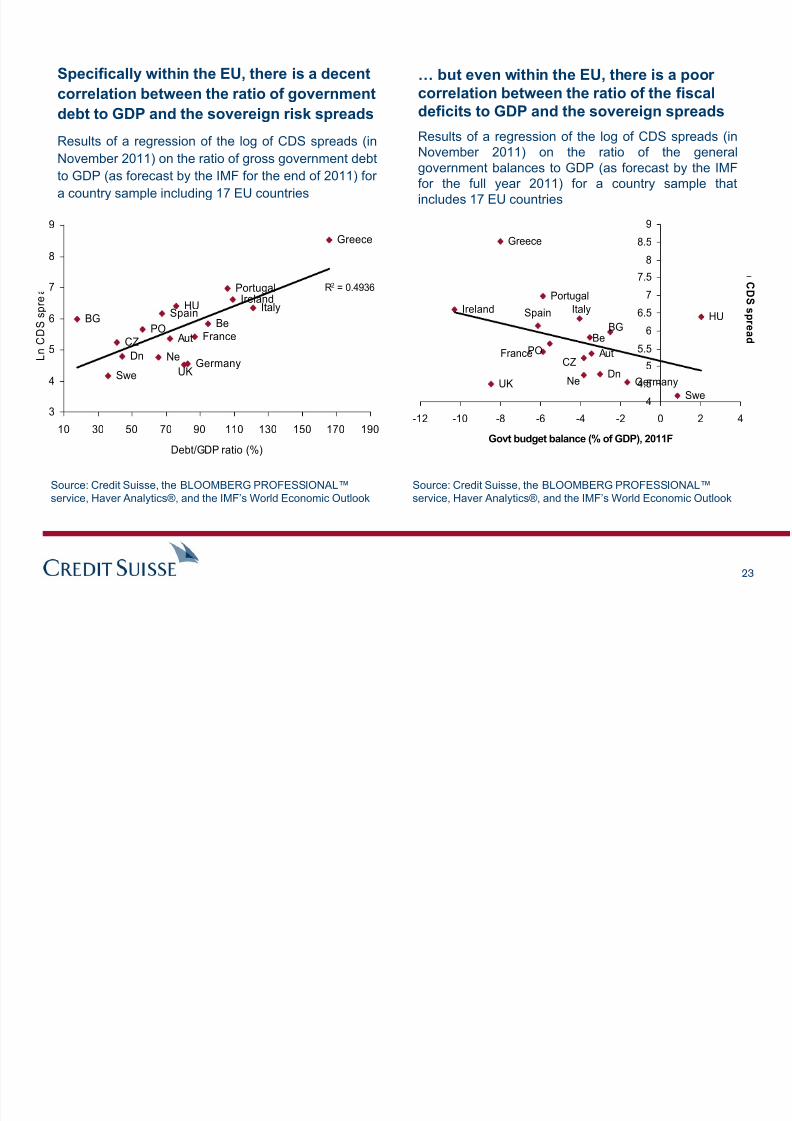

Specifically within the EU, there is a decent

correlation between the ratio of government

debt to GDP and the sovereign risk spreads

Results of a regression of the log of CDS spreads (in

November 2011) on the ratio of gross government debt

to GDP (as forecast by the IMF for the end of 2011) for

a country sample including 17 EU countries

Source: Credit Suisse, the BLOOMBERG PROFESSIONAL™service, Haver Analytics®, and the IMF’s World Economic Outlook

Source: Credit Suisse, the BLOOMBERG PROFESSIONAL™service, Haver Analytics®, and the IMF’s World Economic Outlook

… but even within the EU, there is a poor

correlation between the ratio of the fiscal

deficits to GDP and the sovereign spreadsResults of a regression of the log of CDS spreads (inNovember 2011) on the ratio of the generalgovernment balances to GDP (as forecast by the IMFfor the full year 2011) for a country sample thatincludes 17 EU countries

France

Germany

Greece

IrelandItaly

Portugal

Spain

UK

CZ

HU

POBG

AutBe

Dn Ne

Swe

R2 = 0.4936

3

4

5

6

7

8

9

10 30 50 70 90 110 130 150 170 190Debt/GDP ratio (%)

L n C D S

s p r e

Swe

NeDn

Be

Aut

BG

PO

HU

CZ

UK

Spain

Portugal

ItalyIreland

Greece

Germany

France

4

4.5

5

5.5

6

6.5

7

7.5

8

8.5

9

-12 -10 -8 -6 -4 -2 0 2 4

Govt budget balance (% of GDP), 2011F

C D S s p

r e a d

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 24/40

24

Affordability is at an all-time high, but housing

demand remains anemic

Source: Credit Suisse, NAR, MBA

80

100

120

140

160

180

200

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

J a n - 0 1

J a n - 0 2

J a n - 0 3

J a n - 0 4

J a n - 0 5

J a n - 0 6

J a n - 0 7

J a n - 0 8

J a n - 0 9

J a n - 1 0

J a n - 1 1

0

100

200

300

400

500

600 Affordability Index (LHS)

MBA Purchase Index (RHS)

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 25/40

25

Household formation is running below trend by almost

3 million

Source: Credit Suisse

101,000

103,000

105,000

107,000

109,000

111,000

113,000

115,000

117,000

A p r - 0

0

O c t - 0

0

A p r - 0

1

O c t - 0

1

A p r - 0

2

O c t - 0

2

A p r - 0

3

O c t - 0

3

A p r - 0

4

O c t - 0

4

A p r - 0

5

O c t - 0

5

A p r - 0

6

O c t - 0

6

A p r - 0

7

O c t - 0

7

A p r - 0

8

O c t - 0

8

A p r - 0

9

O c t - 0

9

A p r - 1

0

O c t - 1

0

A p r - 1

1

Number of Households, (Ths., NSA)

1 std Dev (based on 2000 -2005 trend)

-1 std Dev (based on 2000 -2005 trend)

Trend Rate

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 26/40

26

US household formation with projection

Source: Credit Suisse

Household Formation Scenario

100

105

110

115

120

125

00 04 08 12 16 20

mn

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 27/40

27

US services consumption growth (y/y%) in recoveries

Source: Credit Suisse

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

1 5 9 13 17 21 25 29 33 37 41

2009

2001

1991

Months from start of recovery

Q4 Estimate

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 28/40

28

US real retail sales and real discretionary services spending

Source: Credit Suisse

5.88

5.9

5.92

5.94

5.96

5.98

6

6.02

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

US Real Retail Sales (log level)

US Real Discretionary Services Spending (loglevel)

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 29/40

29

US Debt/GDP

Source: Credit Suisse, Reinhart and Rogoff

0

20

40

60

80

100

120

140

1790 1810 1830 1850 1870 1890 1910 1930 1950 1970 1990 2010

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 30/40

30

Global oil demandNatural logs, seasonally adjusted

Source: IEA, Credit Suisse Source: IEA, Credit Suisse

OECD and non-OECD oil demandNatural logs, seasonally adjusted

11.15

11.20

11.25

11.30

11.35

11.40

11.45

1995 1998 2001 2004 2007 2010

Global oil demand HP-filter trend

Annualized

growth = 1.39%

Annualized

growth = 1.34%

10.1

10.2

10.3

10.4

10.5

10.6

10.7

10.8

1995 1998 2001 2004 2007 2010 2013

10.6

10.7

10.8

10.9

11.0

11.1

11.2

11.3Non-OECD (lhs) OECD (rhs)

Non-OECD annualized

growth = 4.46%

OECD annualized

growth = 1.02%

Non-OECD annualized

growth = 1.73%

OECD

annualized growth = -1.21%

output gap

C f

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 31/40

31

Correlation between core inflation and commodity pricesCorrelation of yearly changes since January 2001; note that India uses WPI, and China uses non-food CPI

Source: the BLOOMBERG PROFESSIONAL™ service, Thomson Reuters DataStream, Credit Suisse

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

US Japan Euro India China

YoY Correlation with CCI (CRB) and Core CPI

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 32/40

32

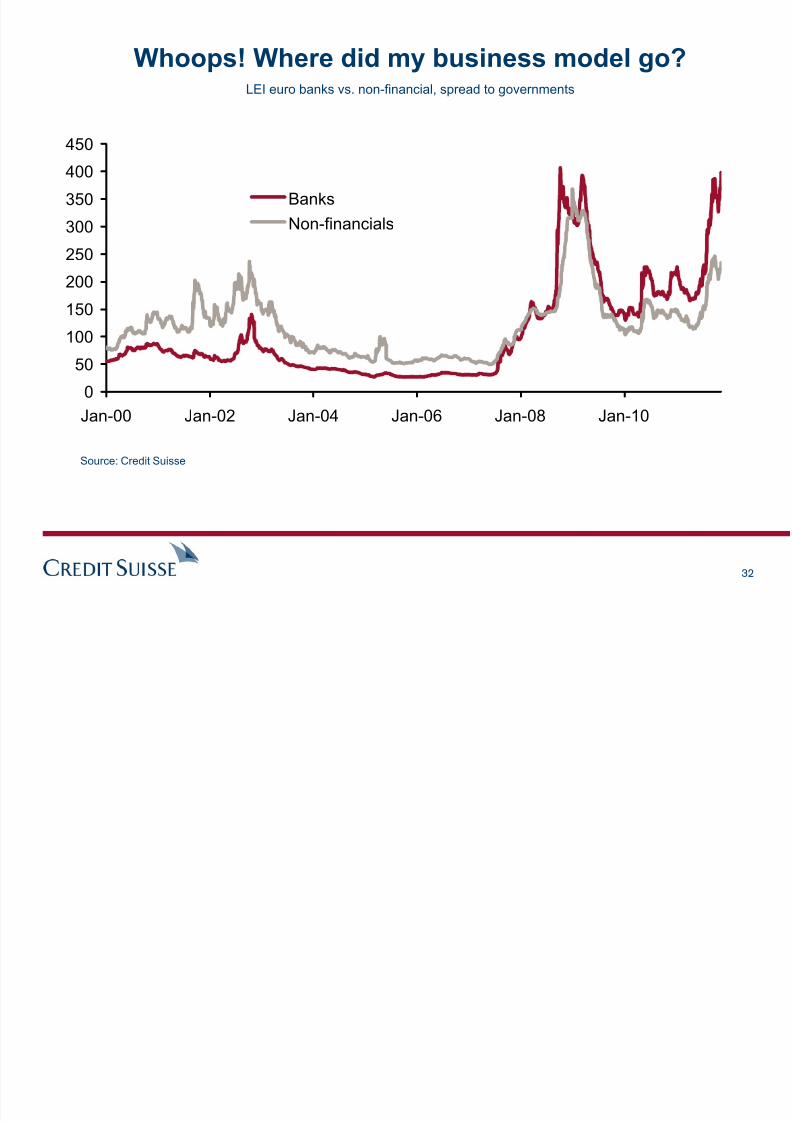

Whoops! Where did my business model go?LEI euro banks vs. non-financial, spread to governments

Source: Credit Suisse

0

50

100

150

200

250

300

350

400

450

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Banks

Non-financials

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 33/40

33

Net interest receipts by sector in Japantrillions of yen

Source: Cabinet Office, Credit Suisse

(38.4)

13.7

(5.0)

32.3

(22.1)

(0.4)

(6.9)

34.3

(4.7)

(5.4)

(5.2)

23.3

(60.0) (40.0) (20.0) 0.0 20.0 40.0

Non-financial

corporate

Households

General

government

Financial

2009

1997

1991

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 34/40

34

Savers pay the piper $bn

Source: Bureau of Economic Analysis, Federal Reserve, Credit Suisse

0

200

400

600

800

1000

1200

1400

1600

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10

Personal Interest Income

Personal Debt Service Payments

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 35/40

35

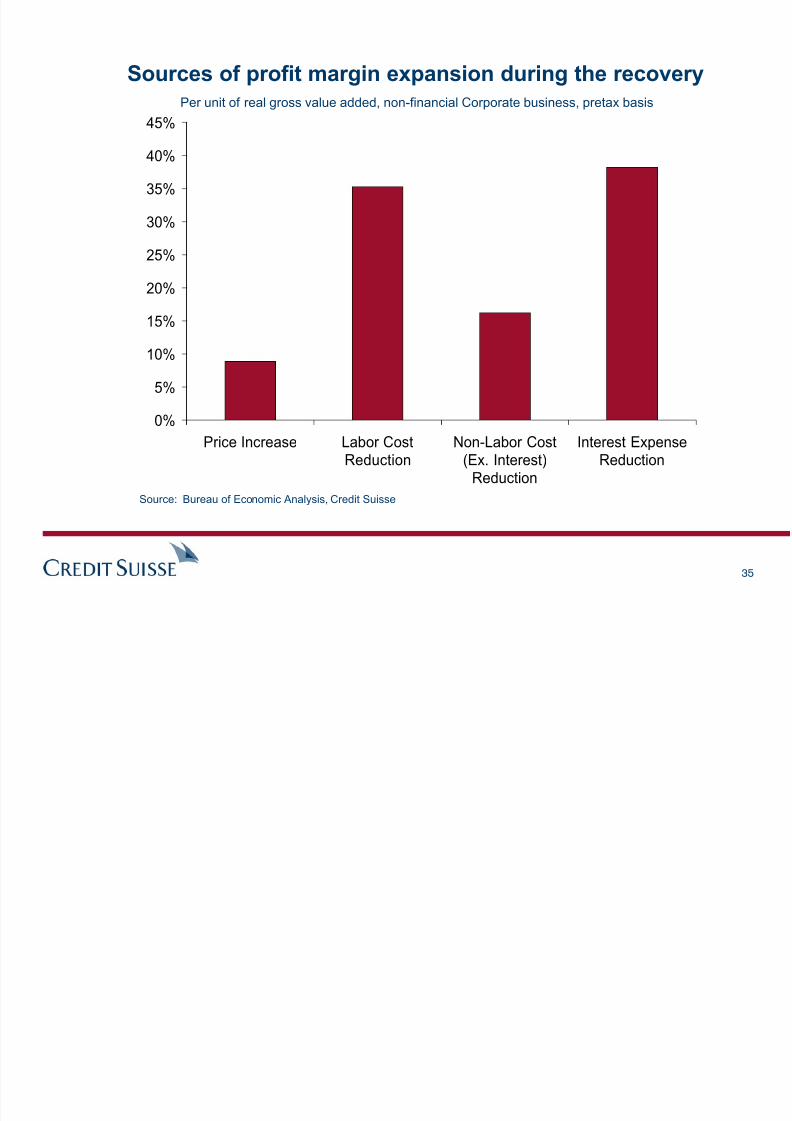

Sources of profit margin expansion during the recoveryPer unit of real gross value added, non-financial Corporate business, pretax basis

Source: Bureau of Economic Analysis, Credit Suisse

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Price Increase Labor CostReduction

Non-Labor Cost(Ex. Interest)

Reduction

Interest ExpenseReduction

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 36/40

36

Profits, GDP, and stock prices over the last decade1Q 2002=100

Source: Credit Suisse

60

80

100

120

140

160

180

200

220

240

'02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Corporate Profits

Nominal GDP

S&P 500

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 37/40

37

US – Number of live births and the year they turn 65Live births in millions. The year they turn 65 marked on top of the line

Source: US Census Bureau, Centers for Disease Control and Prevention, Credit Suisse

2015

2020

2025

20302035

2040

2045

2050

2055

2060

20652070

2011

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

1 9 4 6

1 9 5 0

1 9 5 5

1 9 6 0

1 9 6 5

1 9 7 0

1 9 7 5

1 9 8 0

1 9 8 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

2 0 0 9

Post-World

War II

baby boom

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 38/40

38

Gross pension replacement rates for the average male earner Gross pension entitlement divided by gross pre-retirement incomes, 2008

Source: OECD, Credit Suisse

31.9 34.5

39.442.0

49.1

64.5

20

30

40

50

60

70

UK Japan US Germany France Italy

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 39/40

39

Economic dependency ratios – the G6 comparedRatio of non-workers to workers

Source: ILO, Credit Suisse

1.2

1.0

1.1

1.3

1.6

0.90.9 0.9 1.0

1.2

1.4

1.1

0.6

0.7

0.8

0.91.0

1.1

1.2

1.3

1.4

1.5

1.6

Germany US UK Japan France Italy

1980 2012

7/31/2019 Desynchronising Global Economy

http://slidepdf.com/reader/full/desynchronising-global-economy 40/40