DEPRECIATION CA. ( Dr.) Gurmeet S. Grewal B. Com (Hons.), FCA,, PhD. CAL (IIAM) Grewal & Singh...

38

DEPRECIATION CA. (Dr.) Gurmeet S. Grewal B. Com (Hons.), FCA,, PhD. CAL (IIAM) Grewal & Singh Chartered Accountants New Delhi, Chandigarh, Yamuna Nagar, Jammu Phones: 09811242856 & 09266942856 Emails: [email protected] and [email protected]

-

Upload

bertha-dorsey -

Category

Documents

-

view

223 -

download

0

Transcript of DEPRECIATION CA. ( Dr.) Gurmeet S. Grewal B. Com (Hons.), FCA,, PhD. CAL (IIAM) Grewal & Singh...

DEPRECIATION

CA. (Dr.) Gurmeet S. Grewal

B. Com (Hons.), FCA,, PhD. CAL (IIAM)

Grewal & SinghChartered Accountants

New Delhi, Chandigarh, Yamuna Nagar, JammuPhones: 09811242856 & 09266942856

Emails: [email protected] [email protected]

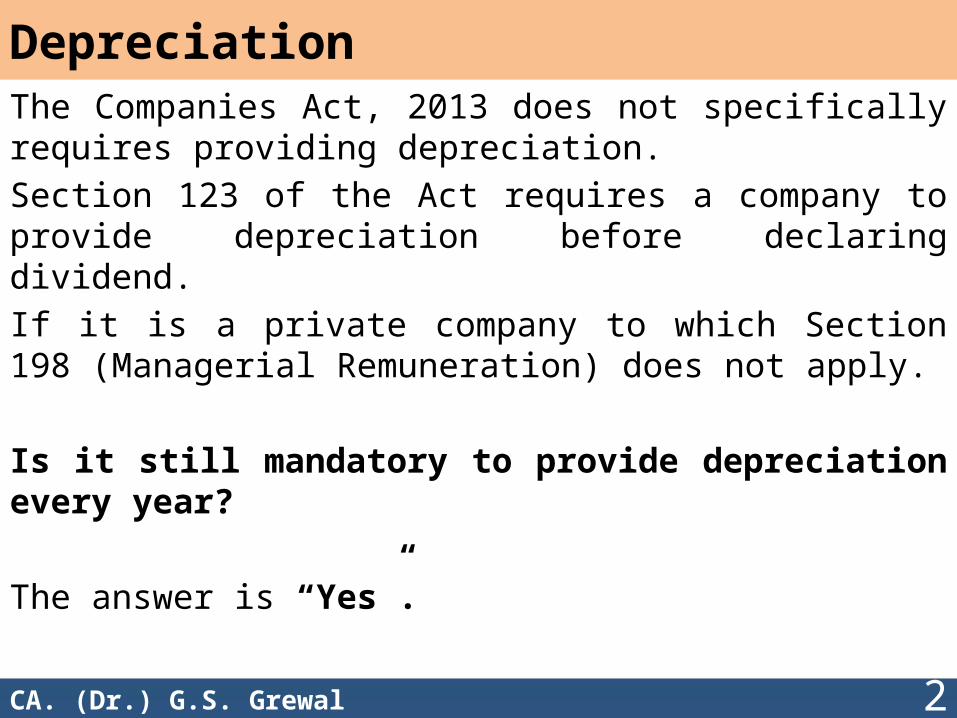

DepreciationThe Companies Act, 2013 does not specifically requires providing depreciation.

Section 123 of the Act requires a company to provide depreciation before declaring dividend.

If it is a private company to which Section 198 (Managerial Remuneration) does not apply.

Is it still mandatory to provide depreciation every year?

The answer is “Yes”. 2CA. (Dr.) G.S. Grewal

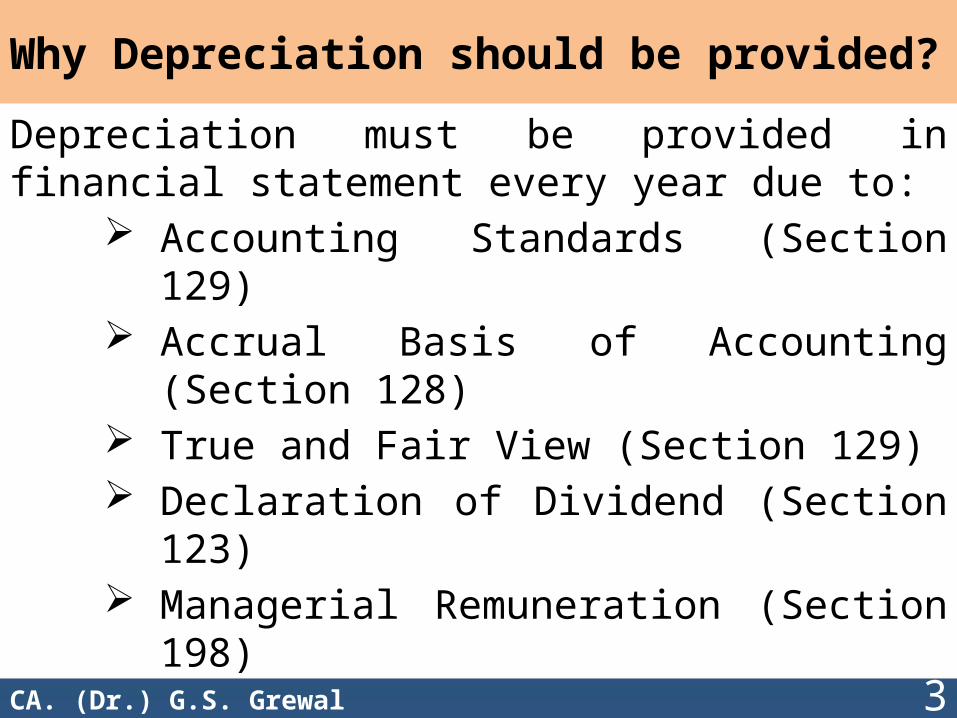

Why Depreciation should be provided?

Depreciation must be provided in financial statement every year due to:

Accounting Standards (Section 129) Accrual Basis of Accounting (Section 128) True and Fair View (Section 129) Declaration of Dividend (Section 123) Managerial Remuneration (Section 198)

3CA. (Dr.) G.S. Grewal

AS 6 – Depreciation Accounting

Para 3.1 Definition of Depreciation:– …Depreciation is allocated so as to charge a fair

proportion of the depreciable amount in each accounting period during the expected useful life of the asset.

Para 29- Main Principle:– The depreciable amount of a depreciable asset

should be allocated on systematic basis to each accounting period during the useful life of the asset.

4CA. (Dr.) G.S. Grewal

Accounting Standards

Section 129 requires that accounting standards notified in section 133 must be followed for preparing the financial statements.

In case any of the accounting standard is not followed, it must be disclosed along with reason for not following and its financial effect.

5CA. (Dr.) G.S. Grewal

Accrual Basis of Accounting

Section 128 of the Act provides that financial statements shall be prepared following the accrual basis of accounting.

Depreciation is the cost of use of asset It is a systematic allocation of cost of the asset over its Useful Life.

If depreciation is not provided it will mean that accrual basis of accounting is not followed.

6CA. (Dr.) G.S. Grewal

True and Fair ViewThe expression “True and Fair View” means

“True” suggests that the financial statements are factually correct and have been prepared according to applicable reporting framework such as the accounting standards and they do not contain any material misstatements that may mislead the users. Misstatements may result from material errors or omissions of transactions & balances in the financial statements.

“Fair” implies that the financial statements present the information faithfully without any element of bias and they reflect the economic substance of transactions rather than just their legal form.

7CA. (Dr.) G.S. Grewal

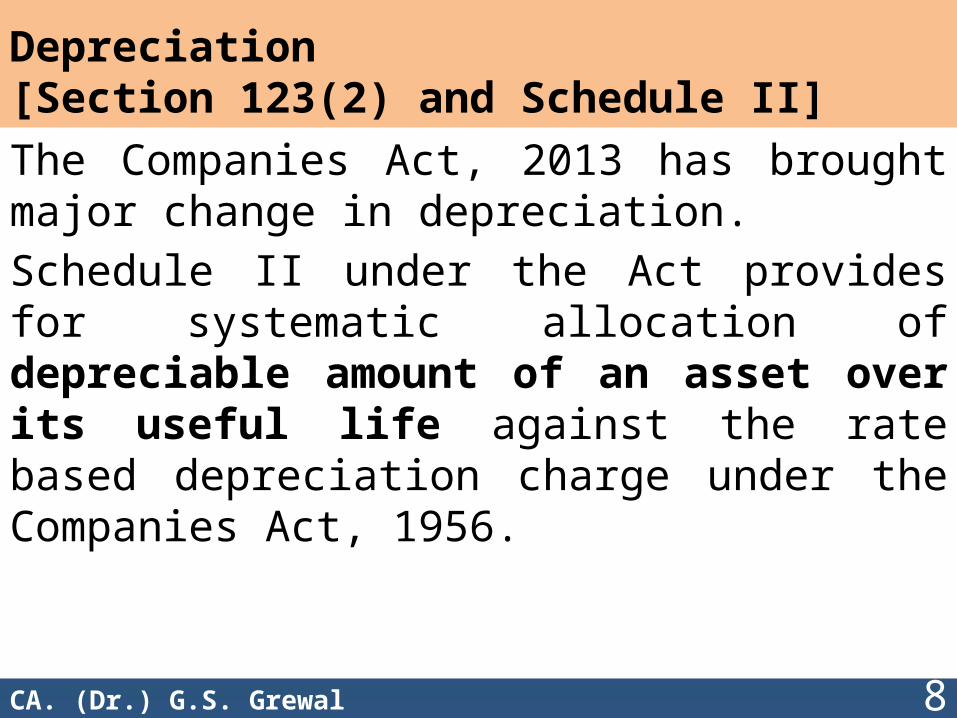

Depreciation [Section 123(2) and Schedule II]

The Companies Act, 2013 has brought major change in depreciation.

Schedule II under the Act provides for systematic allocation of depreciable amount of an asset over its useful life against the rate based depreciation charge under the Companies Act, 1956.

8CA. (Dr.) G.S. Grewal

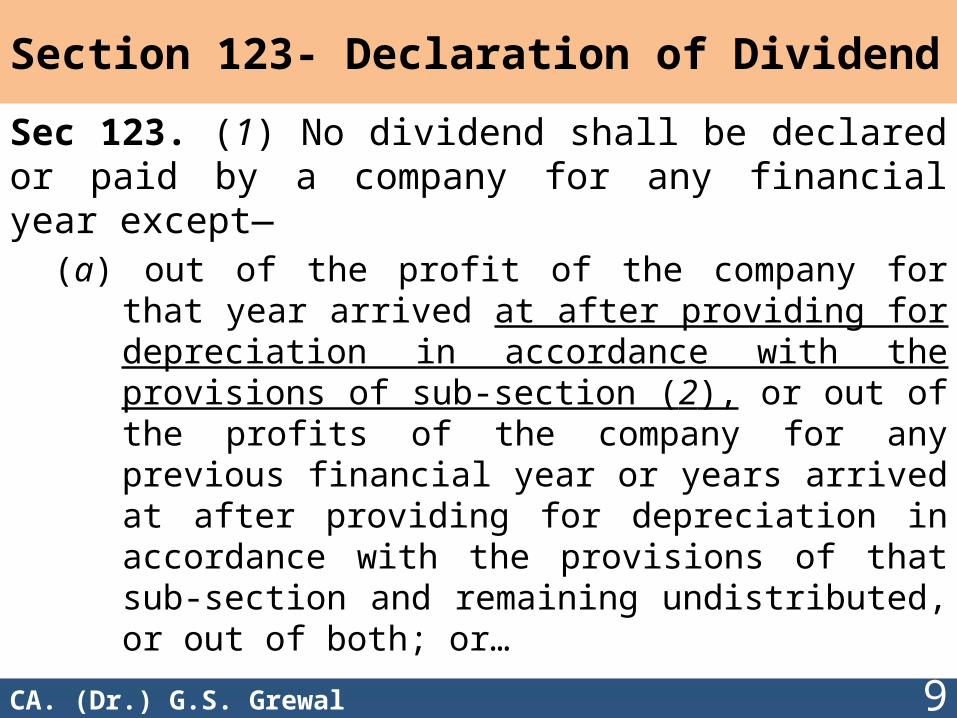

Section 123- Declaration of Dividend

Sec 123. (1) No dividend shall be declared or paid by a company for any financial year except—

(a) out of the profit of the company for that year arrived at after providing for depreciation in accordance with the provisions of sub-section (2), or out of the profits of the company for any previous financial year or years arrived at after providing for depreciation in accordance with the provisions of that sub-section and remaining undistributed, or out of both; or…

9CA. (Dr.) G.S. Grewal

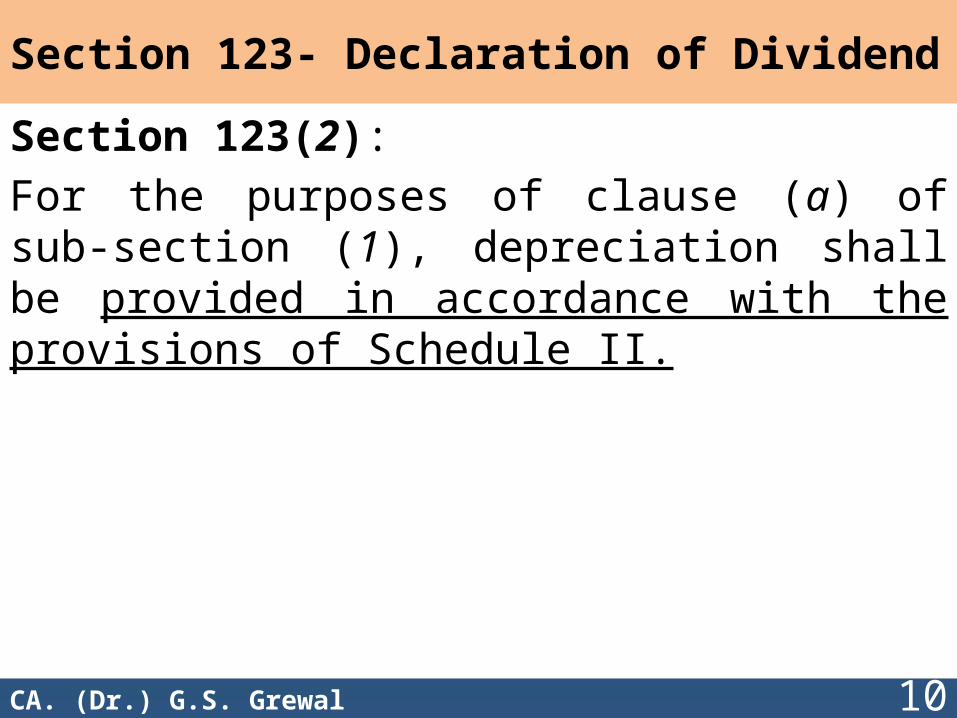

Section 123- Declaration of Dividend

Section 123(2):

For the purposes of clause (a) of sub-section (1), depreciation shall be provided in accordance with the provisions of Schedule II.

10CA. (Dr.) G.S. Grewal

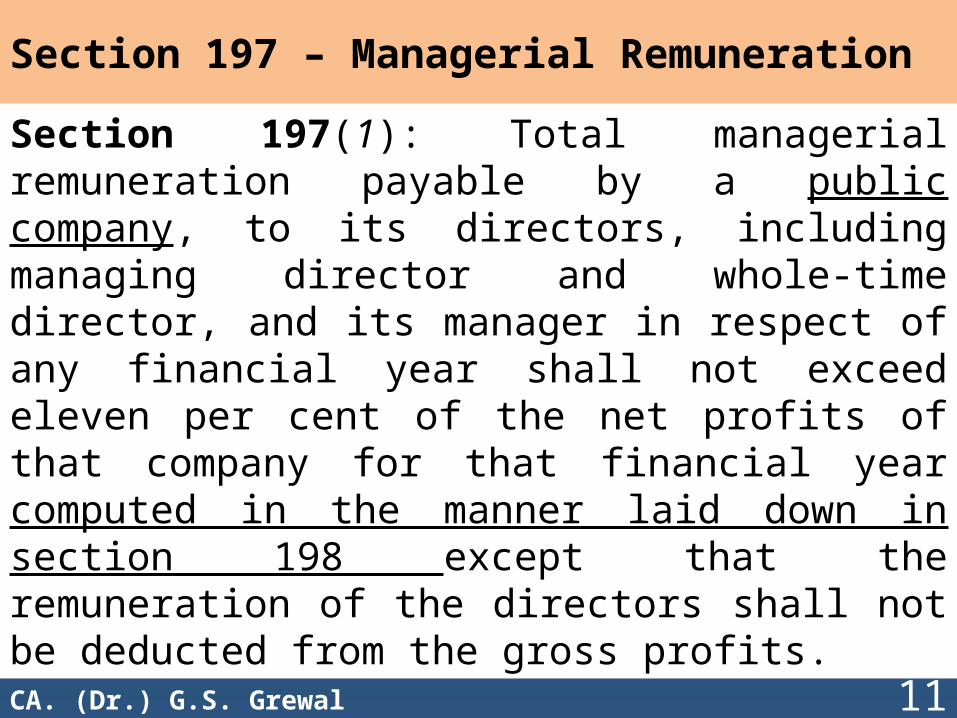

Section 197 – Managerial Remuneration

Section 197(1): Total managerial remuneration payable by a public company, to its directors, including managing director and whole-time director, and its manager in respect of any financial year shall not exceed eleven per cent of the net profits of that company for that financial year computed in the manner laid down in section 198 except that the remuneration of the directors shall not be deducted from the gross profits.

11CA. (Dr.) G.S. Grewal

Section 198 – Computation of Net Profits

Section 198(1): In computing the net profit of a company in any financial year for the purpose of section 197….

Section 198(4): In making the computation aforesaid, following sums shall be deducted, namely…

(k) depreciation to the extent specified in section 123;

12CA. (Dr.) G.S. Grewal

Schedule II – Useful Lives to Compute DepreciationPart A- • Depreciation is a systematic allocation of the

depreciable amount of an asset over its useful life. • Useful life is the period over which an asset is

expected to be available for use by an entity or the number of production units expected to be obtained from the asset by the entity.

• Useful life of an asset shall not ordinarily be different from the useful life specified in Part C and the residual value of an asset shall not be more than 5% of the original cost (Revised by Notification dated 29.8.2014)

13CA. (Dr.) G.S. Grewal

Schedule II – Useful Lives to Compute DepreciationPart A- • Where a company uses a useful life different from that

specified in Part C or uses residual value different from that specified above justification for the difference shall be disclosed in its financial statement.

• Justification in this behalf should be supported by technical advice.

14CA. (Dr.) G.S. Grewal

Schedule II – Useful Lives to Compute DepreciationPart A- • For intangible assets, the provision of

accounting standards applicable for the time being in force shall apply except for toll roads for which method is prescribed in the Schedule.

15CA. (Dr.) G.S. Grewal

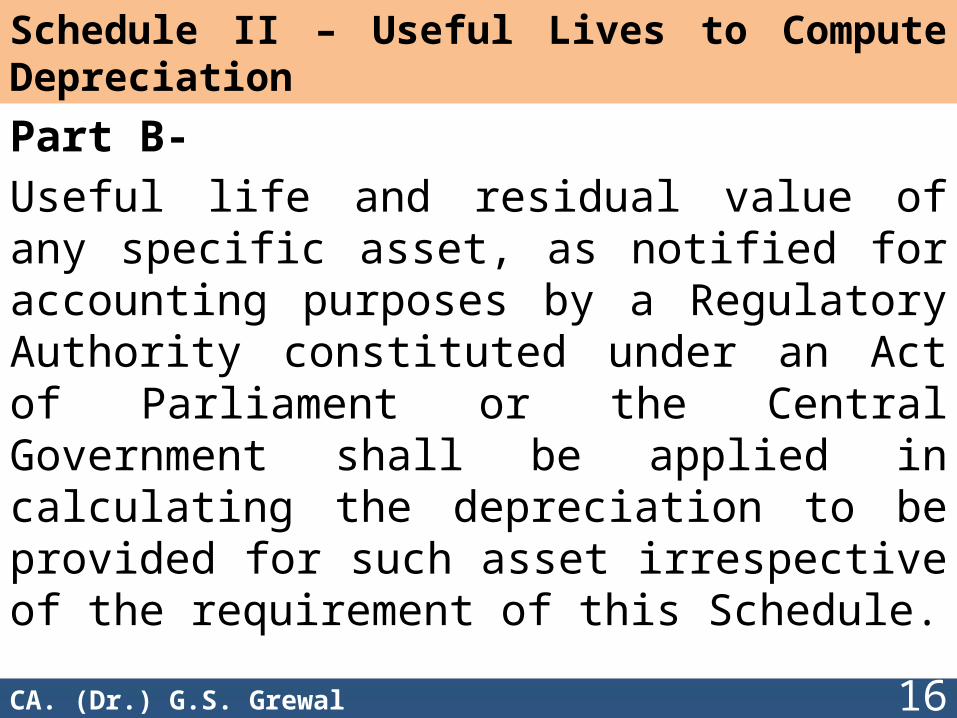

Schedule II – Useful Lives to Compute Depreciation

Part B-

Useful life and residual value of any specific asset, as notified for accounting purposes by a Regulatory Authority constituted under an Act of Parliament or the Central Government shall be applied in calculating the depreciation to be provided for such asset irrespective of the requirement of this Schedule.

16CA. (Dr.) G.S. Grewal

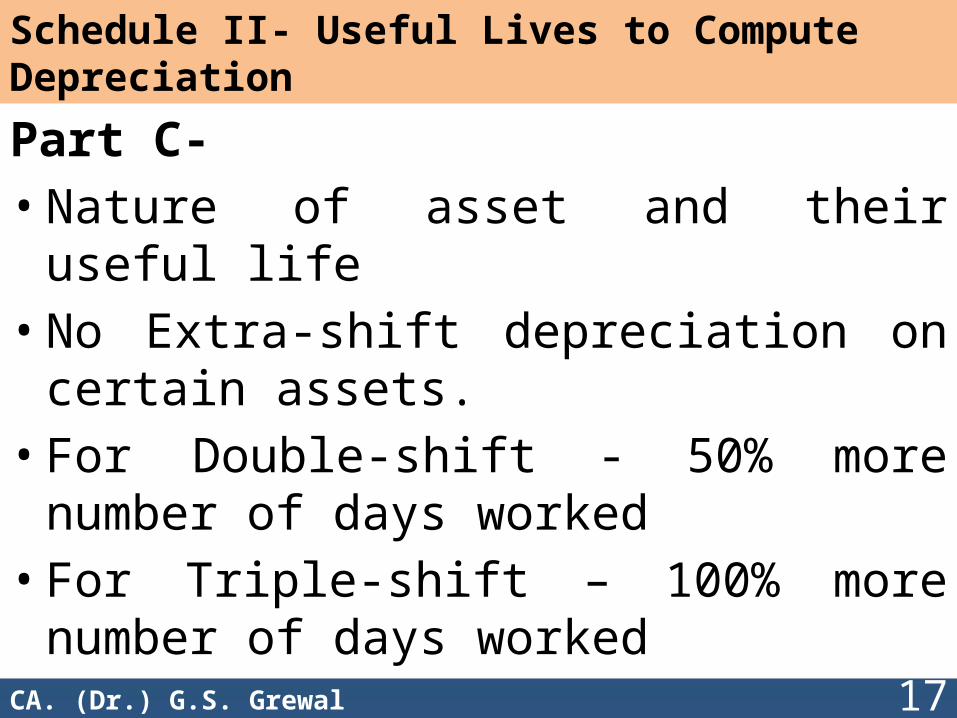

Schedule II- Useful Lives to Compute Depreciation

Part C- • Nature of asset and their useful life• No Extra-shift depreciation on certain

assets.• For Double-shift - 50% more number of

days worked• For Triple-shift – 100% more number of

days worked

17CA. (Dr.) G.S. Grewal

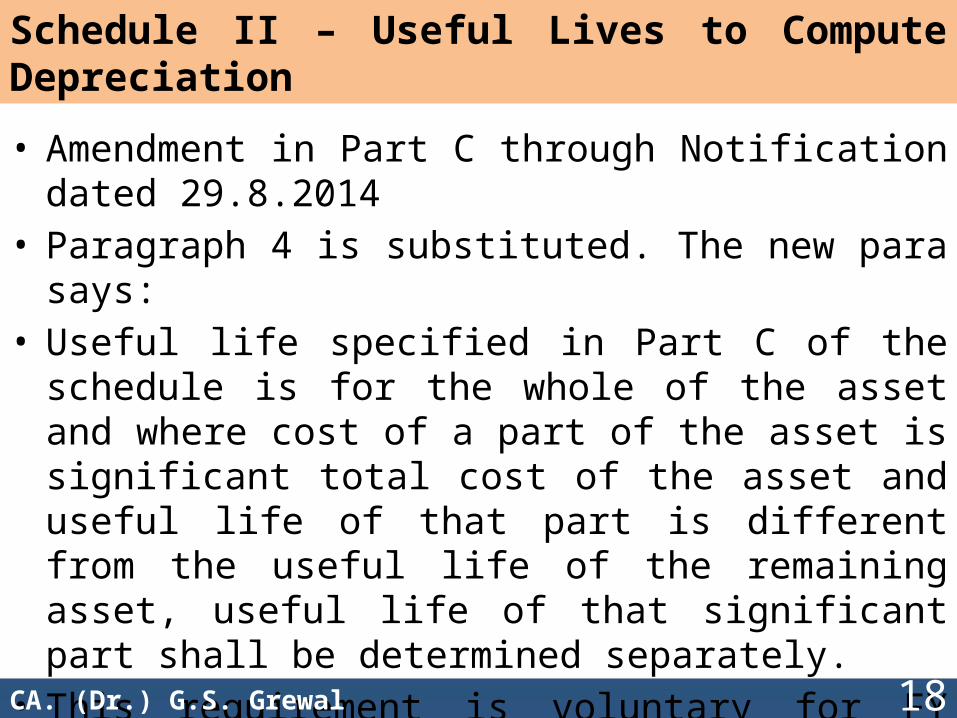

Schedule II – Useful Lives to Compute Depreciation

• Amendment in Part C through Notification dated 29.8.2014

• Paragraph 4 is substituted. The new para says:• Useful life specified in Part C of the schedule is for the

whole of the asset and where cost of a part of the asset is significant total cost of the asset and useful life of that part is different from the useful life of the remaining asset, useful life of that significant part shall be determined separately.

• This requirement is voluntary for FY 2014-15 but mandatory thereafter.

18CA. (Dr.) G.S. Grewal

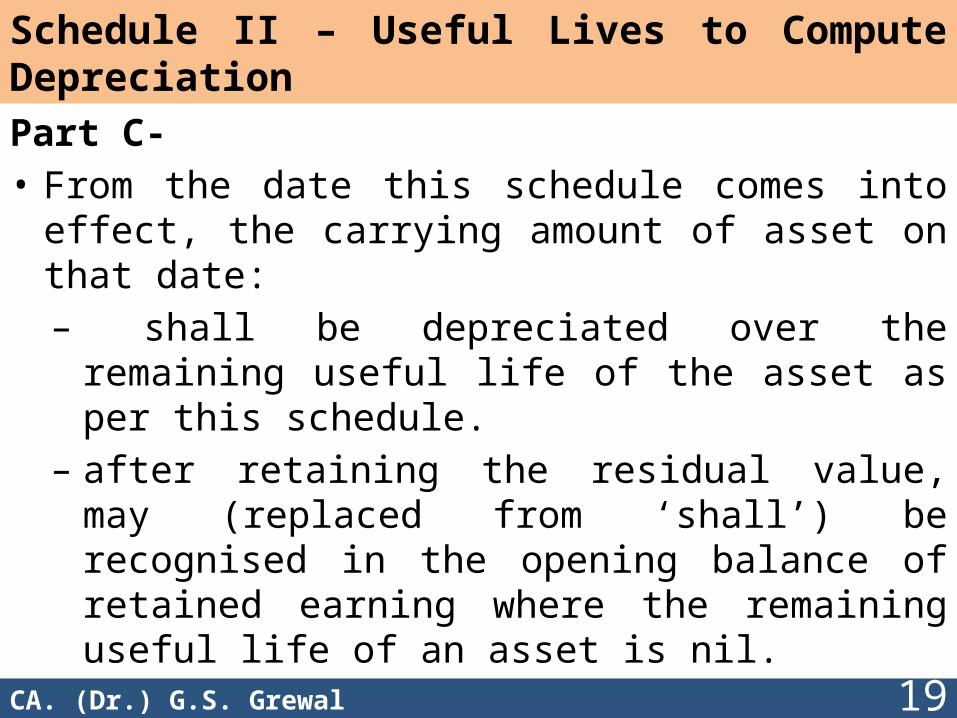

Schedule II – Useful Lives to Compute DepreciationPart C- • From the date this schedule comes into effect, the

carrying amount of asset on that date:– shall be depreciated over the remaining useful

life of the asset as per this schedule.– after retaining the residual value, may (replaced

from ‘shall’) be recognised in the opening balance of retained earning where the remaining useful life of an asset is nil.

19CA. (Dr.) G.S. Grewal

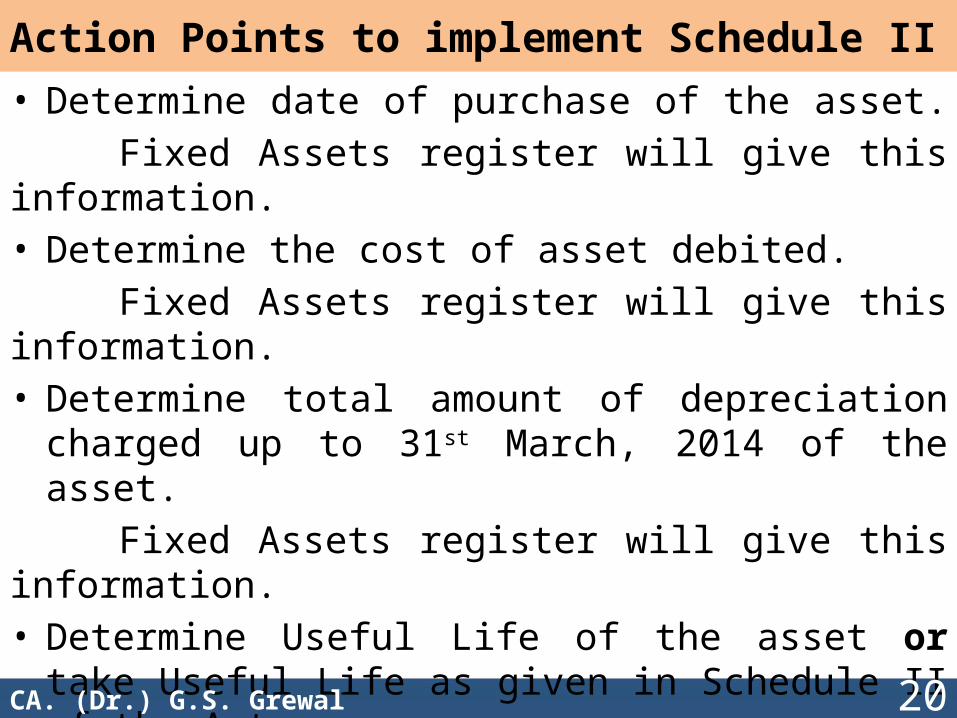

Action Points to implement Schedule II• Determine date of purchase of the asset.

Fixed Assets register will give this information. • Determine the cost of asset debited.

Fixed Assets register will give this information. • Determine total amount of depreciation charged up to

31st March, 2014 of the asset.

Fixed Assets register will give this information. • Determine Useful Life of the asset or take Useful Life

as given in Schedule II of the Act.• If Useful Life is different from that given in Schedule II

of the Act, give reason.

20CA. (Dr.) G.S. Grewal

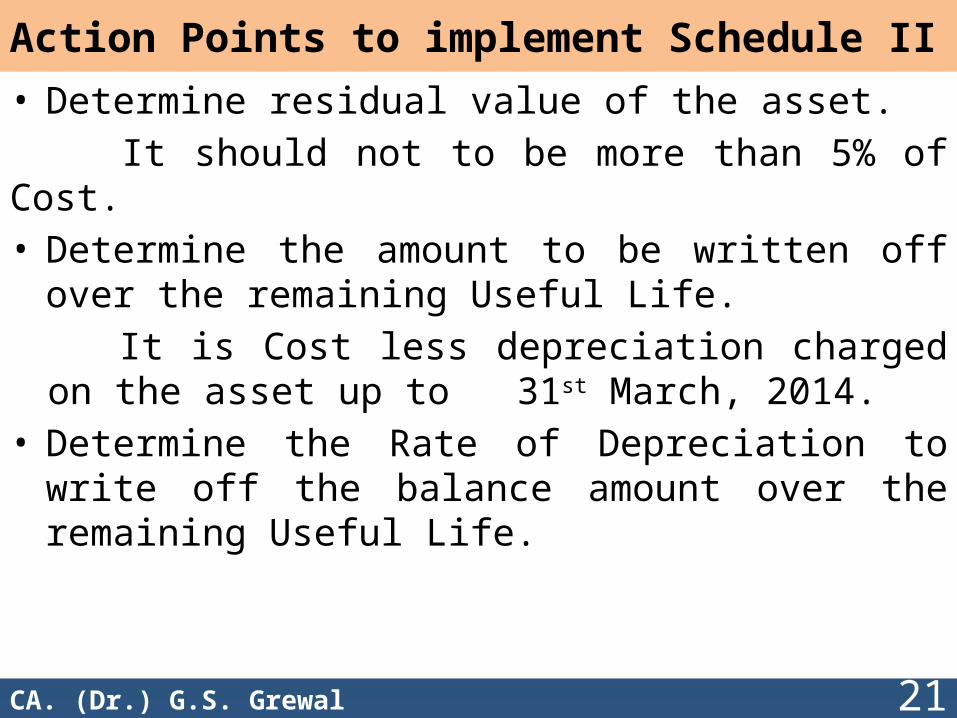

Action Points to implement Schedule II• Determine residual value of the asset.

It should not to be more than 5% of Cost.• Determine the amount to be written off over the

remaining Useful Life.

It is Cost less depreciation charged on the asset up to 31st March, 2014.

• Determine the Rate of Depreciation to write off the balance amount over the remaining Useful Life.

21CA. (Dr.) G.S. Grewal

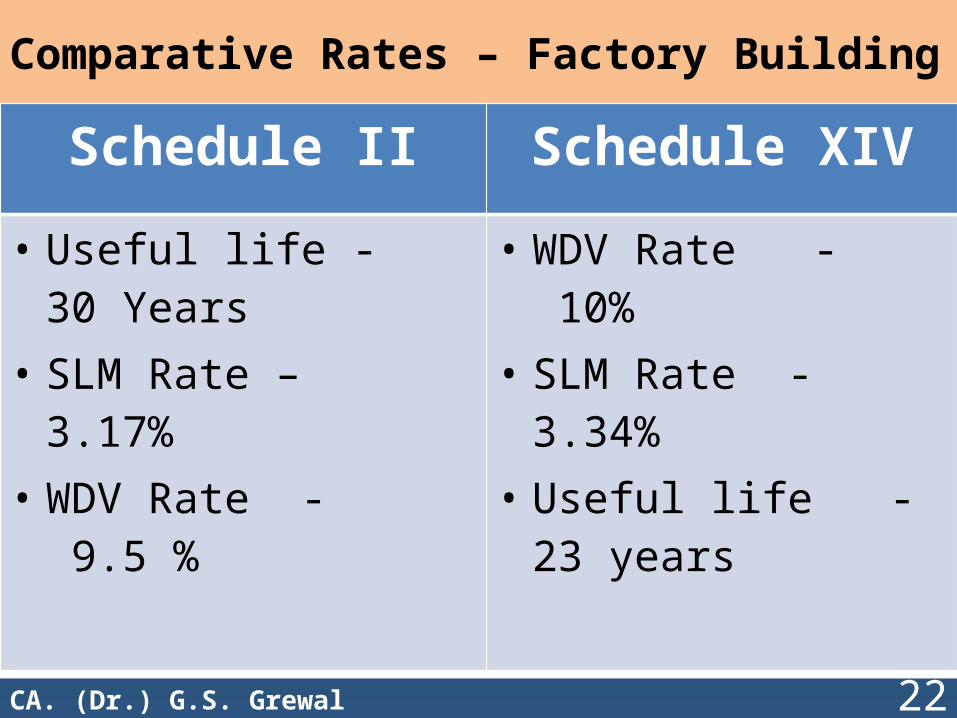

Comparative Rates – Factory Building

22CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful life - 30 Years• SLM Rate – 3.17%• WDV Rate - 9.5 %

• WDV Rate - 10%• SLM Rate - 3.34%• Useful life - 23 years

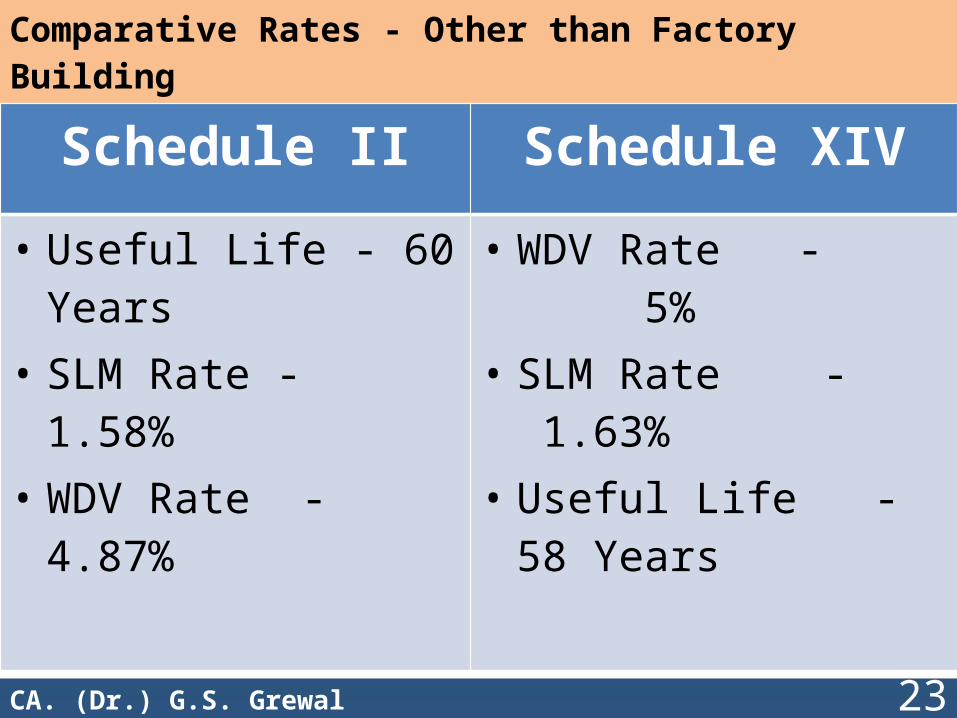

Comparative Rates - Other than Factory Building

23CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful Life - 60 Years• SLM Rate - 1.58%• WDV Rate - 4.87%

• WDV Rate - 5%• SLM Rate - 1.63%• Useful Life - 58 Years

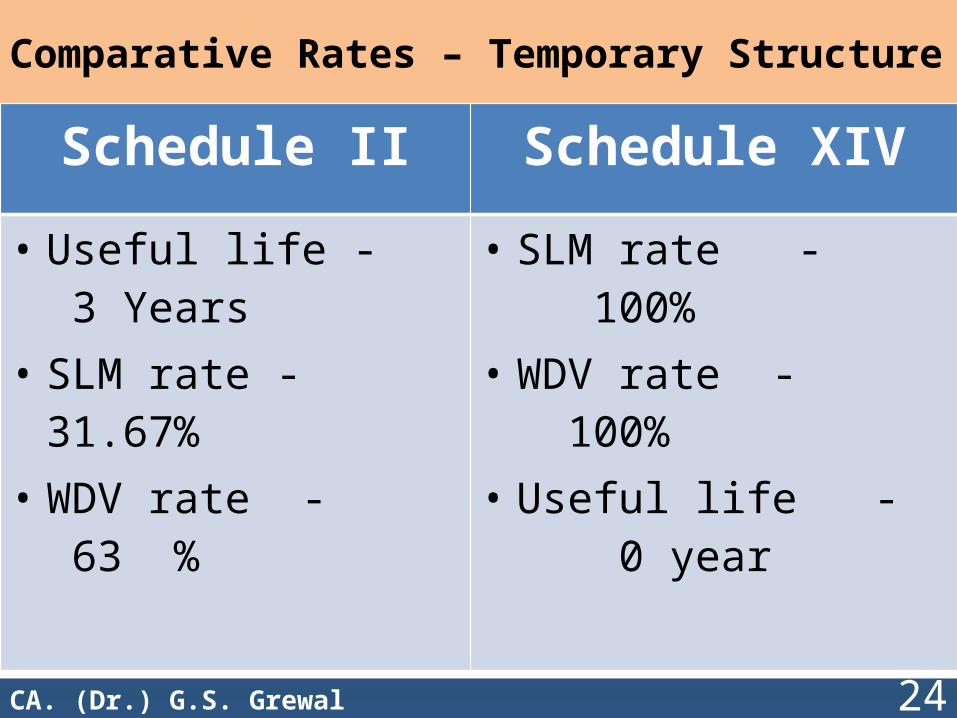

Comparative Rates – Temporary Structure

24CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful life - 3 Years• SLM rate - 31.67%• WDV rate - 63 %

• SLM rate - 100%• WDV rate - 100%• Useful life - 0 year

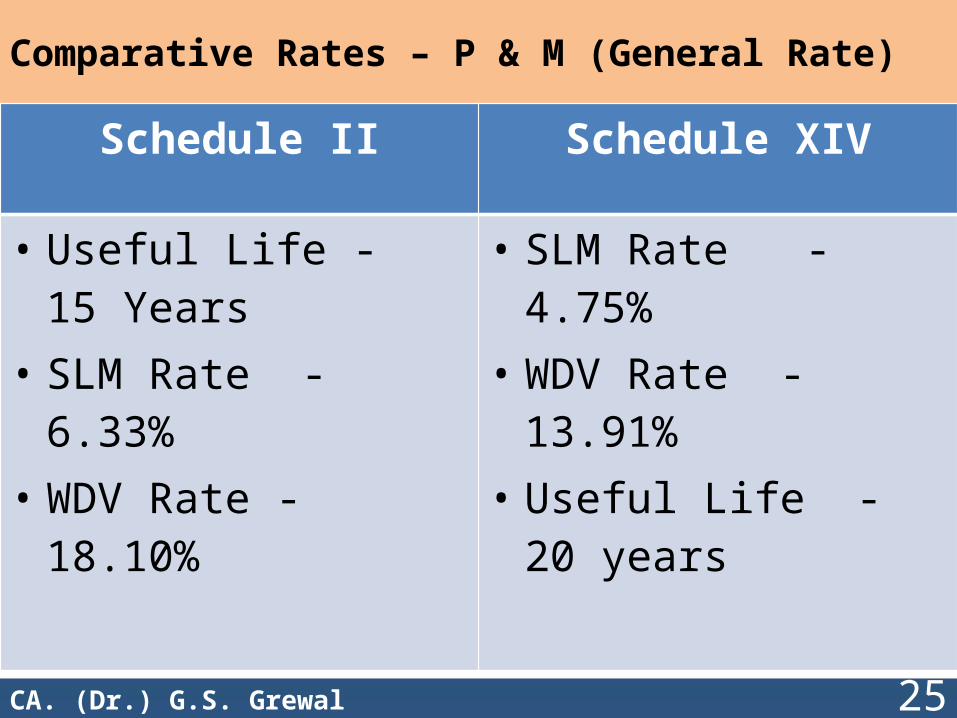

Comparative Rates – P & M (General Rate)

25CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful Life - 15 Years• SLM Rate - 6.33%• WDV Rate - 18.10%

• SLM Rate - 4.75%• WDV Rate - 13.91%• Useful Life - 20 years

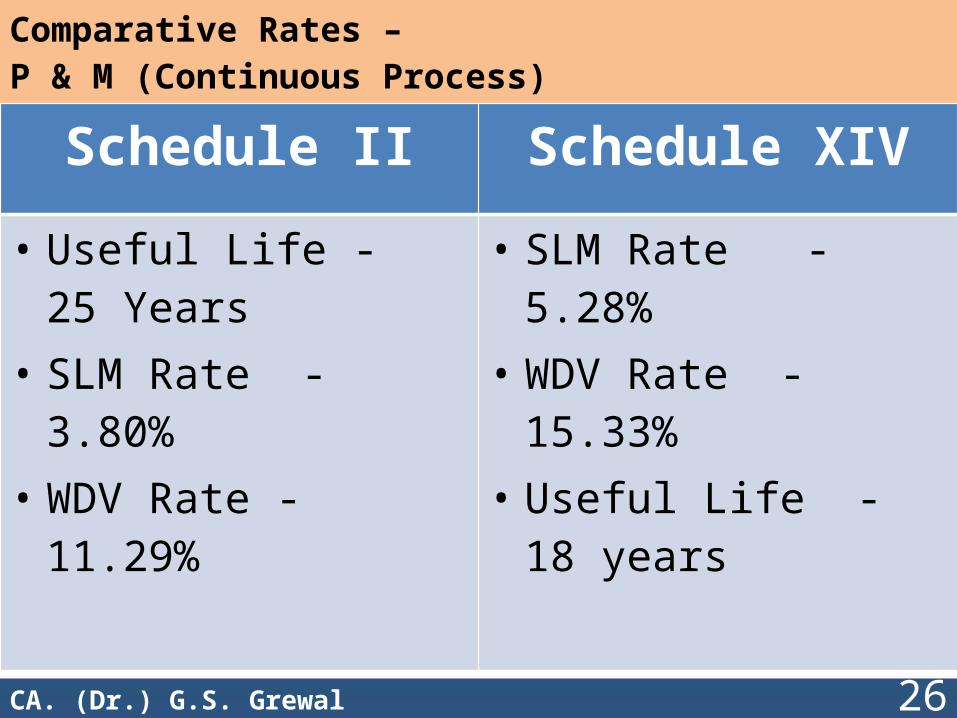

Comparative Rates – P & M (Continuous Process)

26CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful Life - 25 Years• SLM Rate - 3.80%• WDV Rate - 11.29%

• SLM Rate - 5.28%• WDV Rate - 15.33%• Useful Life - 18 years

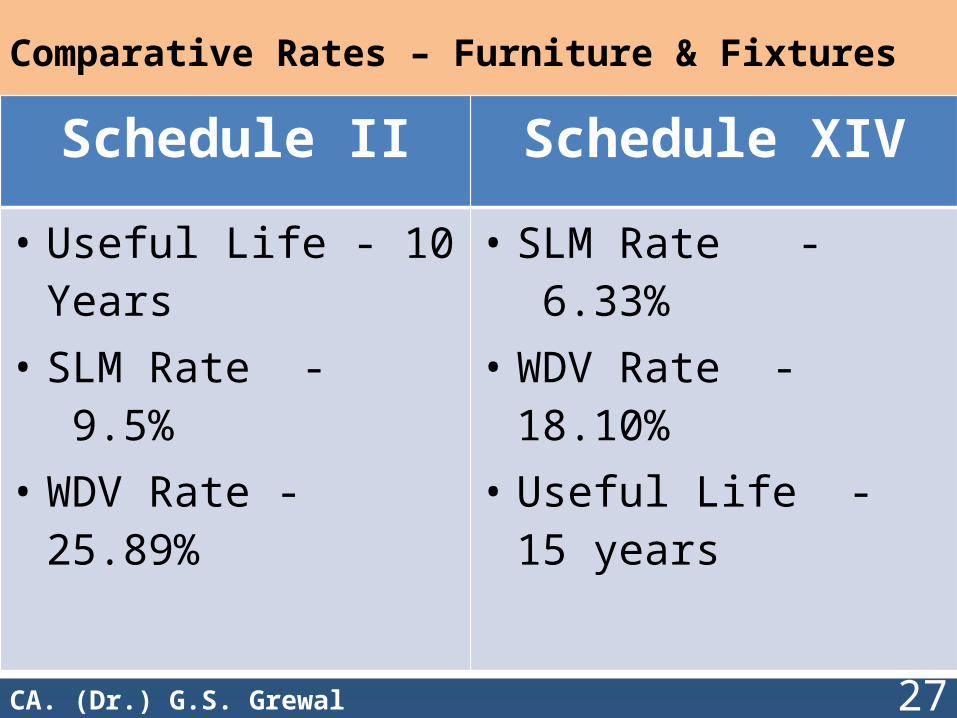

Comparative Rates – Furniture & Fixtures

27CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful Life - 10 Years• SLM Rate - 9.5%• WDV Rate - 25.89%

• SLM Rate - 6.33%• WDV Rate - 18.10%• Useful Life - 15 years

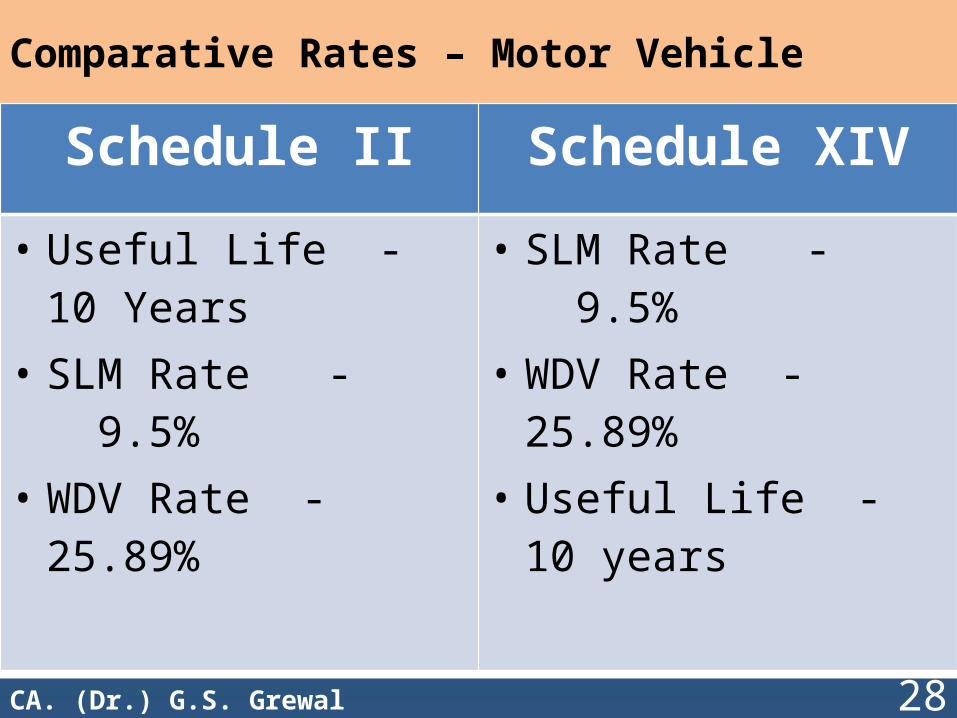

Comparative Rates – Motor Vehicle

28CA. (Dr.) G.S. Grewal

Schedule II Schedule XIV

• Useful Life - 10 Years• SLM Rate - 9.5%• WDV Rate - 25.89%

• SLM Rate - 9.5%• WDV Rate - 25.89%• Useful Life - 10 years

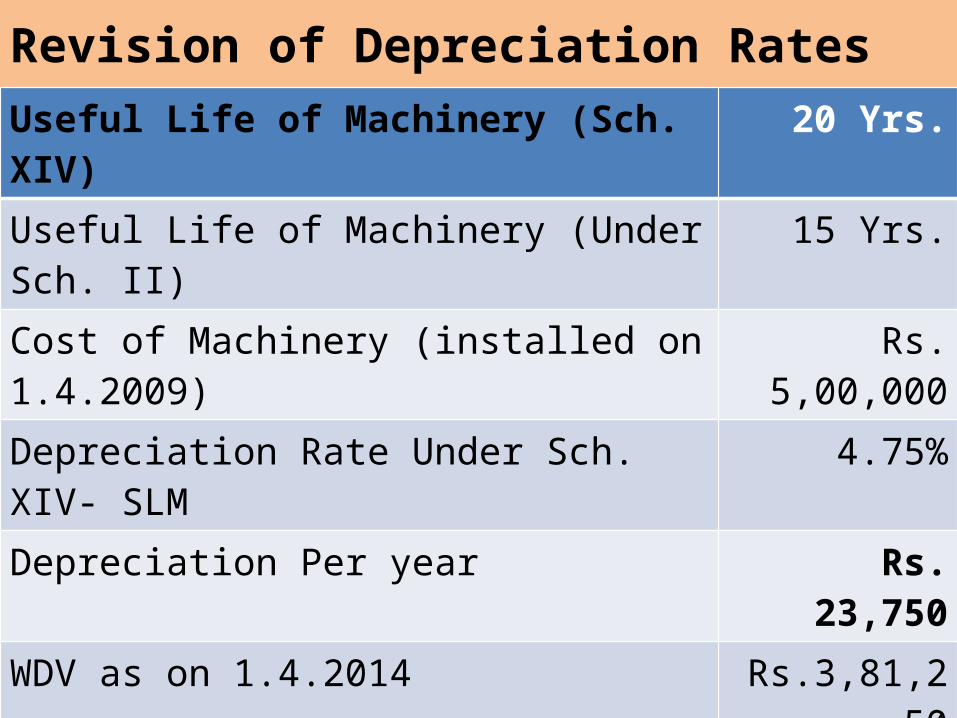

Revision of Depreciation RatesUseful life of Machinery (under Sch. XIV)

-

29CA. (Dr.) G.S. Grewal

Useful Life of Machinery (Sch. XIV) 20 Yrs.

Useful Life of Machinery (Under Sch. II) 15 Yrs.

Cost of Machinery (installed on 1.4.2009) Rs. 5,00,000

Depreciation Rate Under Sch. XIV- SLM 4.75%

Depreciation Per year Rs. 23,750

WDV as on 1.4.2014 Rs.3,81,250

Remaining Useful Life Sch. II on 1.4.2014 10 Yrs.

Dep. Rate for remaining Useful Life –SLM 7.125%

Depreciation Per year Rs. 35,625

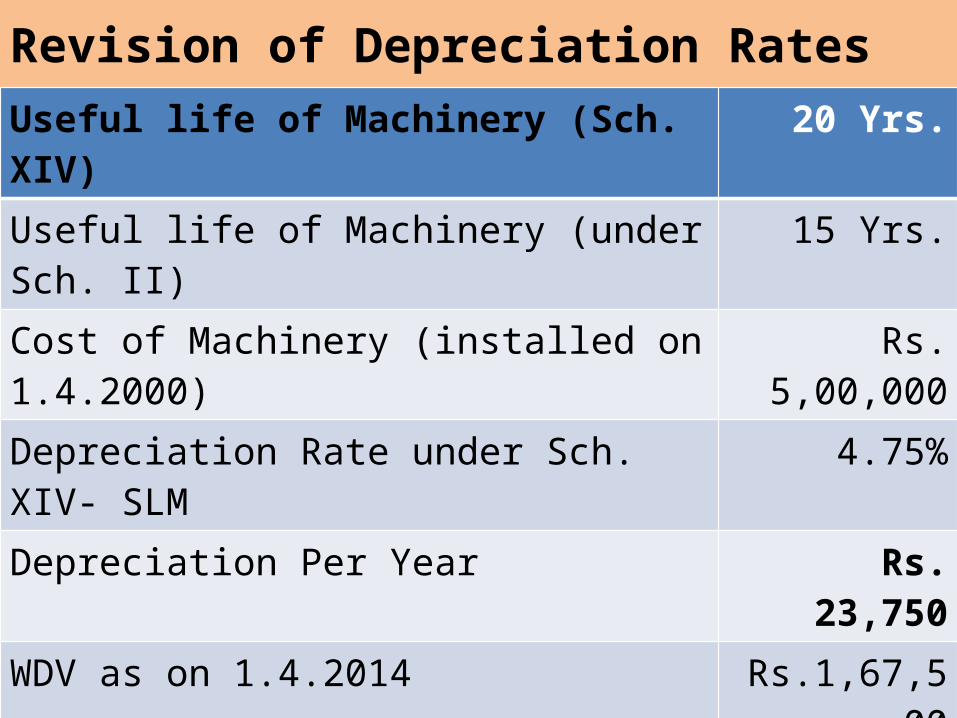

Revision of Depreciation RatesUseful life of Machinery (under Sch. XIV)

-

30CA. (Dr.) G.S. Grewal

Useful life of Machinery (Sch. XIV) 20 Yrs.

Useful life of Machinery (under Sch. II) 15 Yrs.

Cost of Machinery (installed on 1.4.2000) Rs. 5,00,000

Depreciation Rate under Sch. XIV- SLM 4.75%

Depreciation Per Year Rs. 23,750

WDV as on 1.4.2014 Rs.1,67,500

Remaining Useful Life Sch. II on 1.4.2014 1 Yr.

Dep. rate for remaining useful life –SLM 100%

Residual Value (5% of Rs. 5,00,000) Rs. 25,000

Depreciation (Rs. 1,67,500 – Rs. 25,000) Rs. 1,42,500

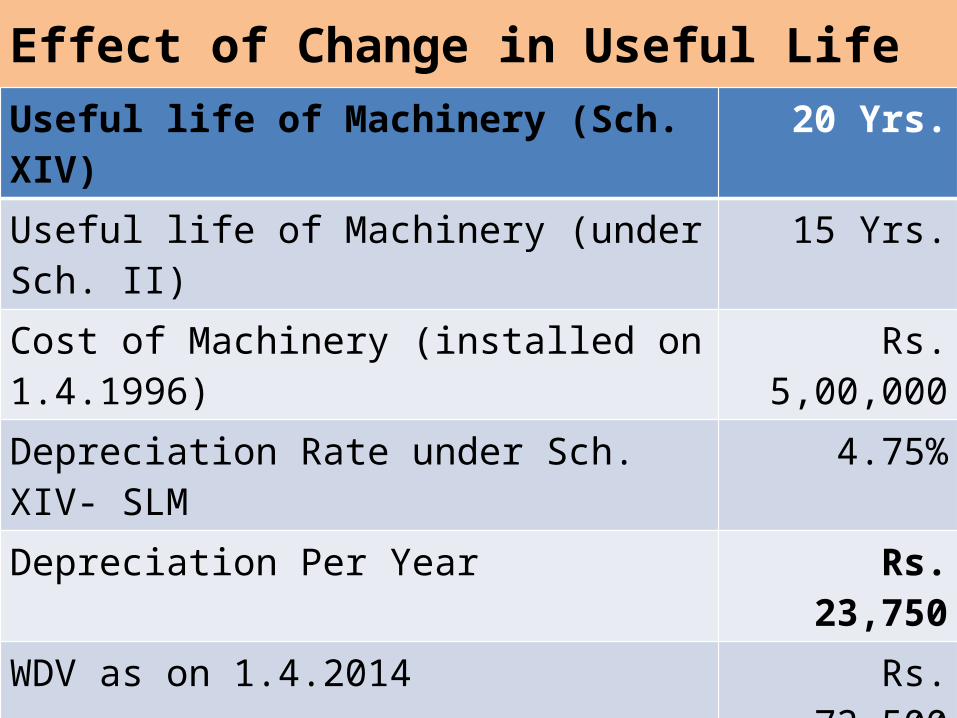

Effect of Change in Useful LifeUseful life of Machinery (under Sch. XIV)

-

31CA. (Dr.) G.S. Grewal

Useful life of Machinery (Sch. XIV) 20 Yrs.

Useful life of Machinery (under Sch. II) 15 Yrs.

Cost of Machinery (installed on 1.4.1996) Rs. 5,00,000

Depreciation Rate under Sch. XIV- SLM 4.75%

Depreciation Per Year Rs. 23,750

WDV as on 1.4.2014 Rs. 72,500

Remaining Useful Life Sch. II on 1.4.2014 Nil

Amount to be debited to Opening Balance of Surplus Account

Rs. 47,500

Revision of Depreciation Rate

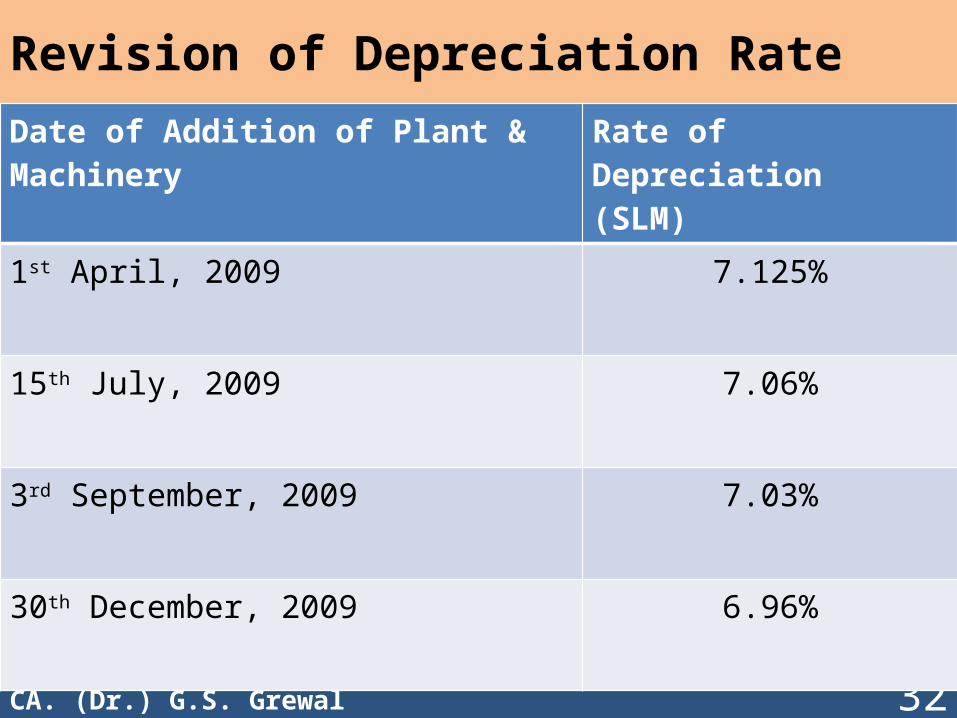

32CA. (Dr.) G.S. Grewal

Date of Addition of Plant & Machinery

Rate of Depreciation(SLM)

1st April, 2009 7.125%

15th July, 2009 7.06%

3rd September, 2009 7.03%

30th December, 2009 6.96%

Revision of Depreciation RatesUseful life of Machinery (under Sch. XIV)

-

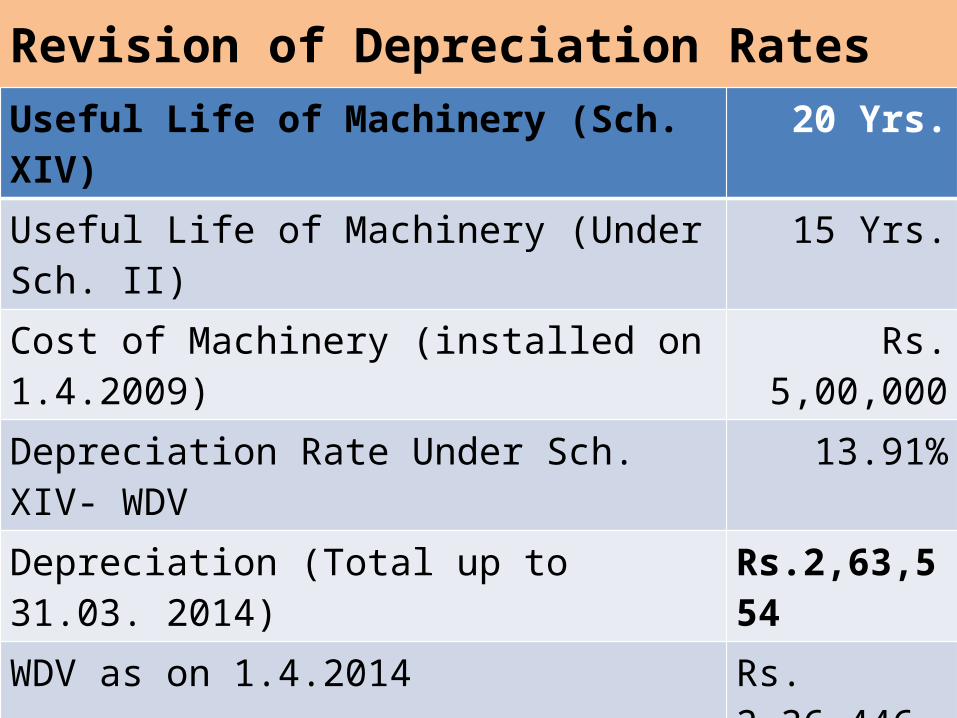

33CA. (Dr.) G.S. Grewal

Useful Life of Machinery (Sch. XIV) 20 Yrs.

Useful Life of Machinery (Under Sch. II) 15 Yrs.

Cost of Machinery (installed on 1.4.2009) Rs. 5,00,000

Depreciation Rate Under Sch. XIV- WDV 13.91%

Depreciation (Total up to 31.03. 2014) Rs.2,63,554

WDV as on 1.4.2014 Rs. 2,36,446

Remaining Useful Life Sch. II on 1.4.2014 10 Yrs.

Dep. Rate for remaining Useful Life –WDV 18.10%

Depreciation for the year (2014 – 15) Rs. 42,797

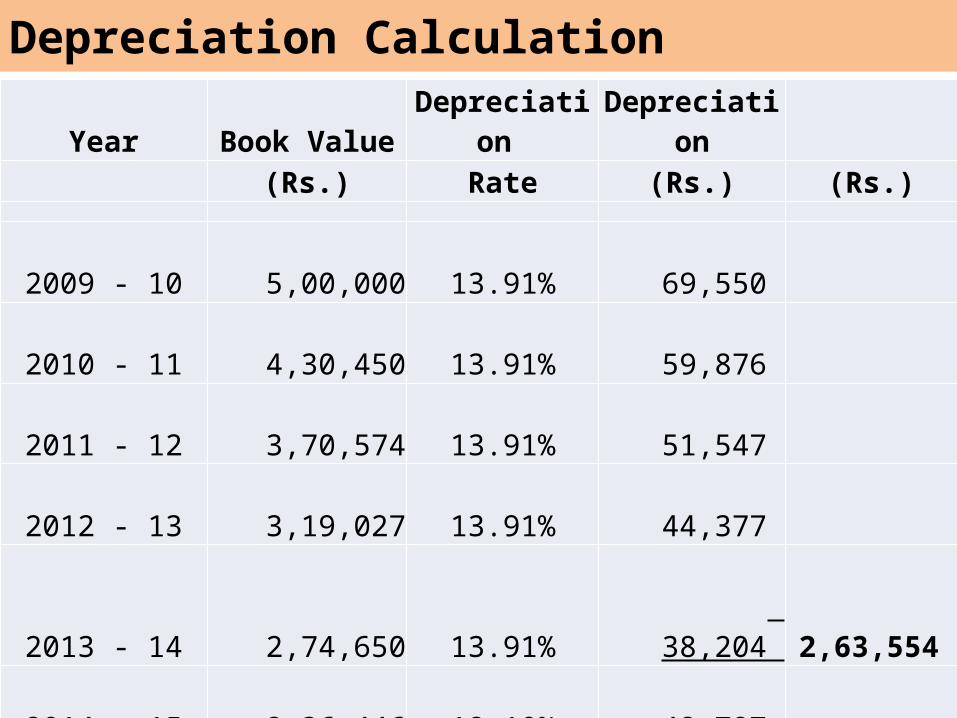

Depreciation Calculation

34CA. (Dr.) G.S. Grewal

Year Book Value Depreciation Depreciation(Rs.) Rate (Rs.) (Rs.)

2009 - 10

5,00,000 13.91% 69,550

2010 - 11

4,30,450 13.91% 59,876

2011 - 12

3,70,574 13.91% 51,547

2012 - 13

3,19,027 13.91% 44,377

2013 - 14

2,74,650 13.91% 38,204 2,63,554

2014 - 15

2,36,446 18.10% 42,797

Revision of Depreciation RatesUseful life of Machinery (under Sch. XIV)

-

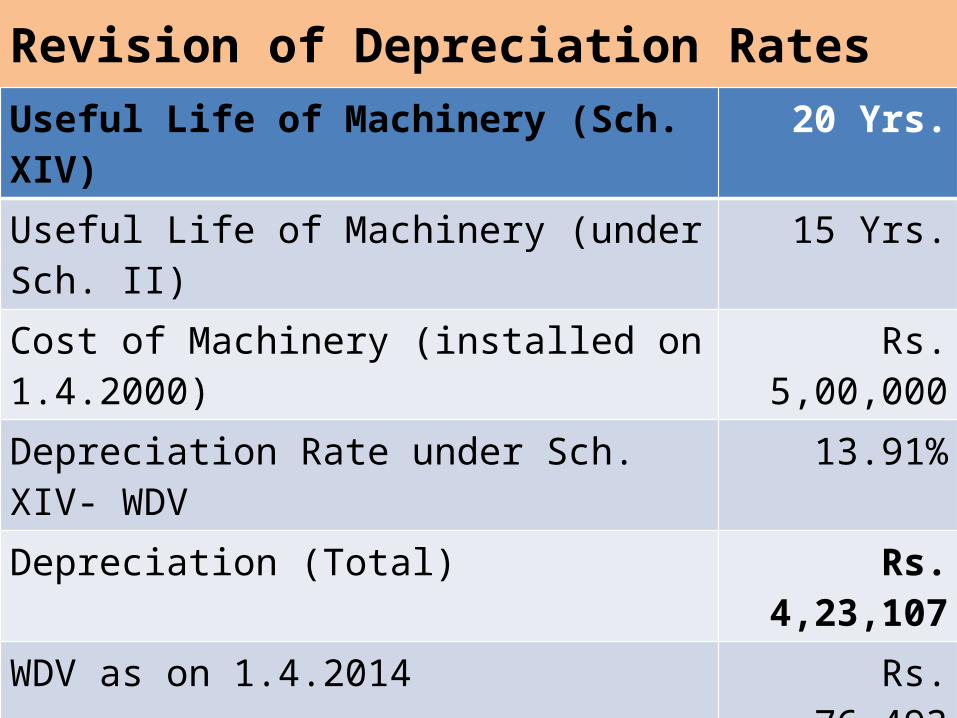

35CA. (Dr.) G.S. Grewal

Useful Life of Machinery (Sch. XIV) 20 Yrs.

Useful Life of Machinery (under Sch. II) 15 Yrs.

Cost of Machinery (installed on 1.4.2000) Rs. 5,00,000

Depreciation Rate under Sch. XIV- WDV 13.91%

Depreciation (Total) Rs. 4,23,107

WDV as on 1.4.2014 Rs. 76,493

Remaining Useful Life Sch. II on 1.4.2014 1 Yr.

Dep. rate for remaining Useful Life –WDV 100%

Realisable Value Rs. 25,000

Depreciation for the Year Rs. 51,493

AS – 26, Intangible Assets

Para 63. The depreciable amount of an intangible asset should be allocated on a systematic basis over the best estimate of its useful life. • There is a rebuttable presumption that the

useful life of an intangible asset will not exceed ten years from the date when the asset is available for use.

• Amortisation should commence when the asset is available for use.

36CA. (Dr.) G.S. Grewal

AS – 26, Intangible assets

Para 72. The amortisation method used should reflect the pattern in which the asset's economic benefits are consumed by the enterprise. • If that pattern cannot be determined reliably, the

straight-line method should be used. • The amortisation charge for each period should

be recognised as an expense unless another Accounting Standard permits or requires it to be included in the carrying amount of another asset.

37CA. (Dr.) G.S. Grewal

THANK YOU

CA. (Dr.) Gurmeet S. [email protected] , [email protected]

Phone: 011-29842641, 29833394Mobile: +91-9811242856 & 09266942856

CA. (Dr.) G.S. Grewal 38