Denver International Airport · Denver International Airport Independent Accountant’s Report on...

21

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures Hotel and Transit Center Program December 31, 2015

Transcript of Denver International Airport · Denver International Airport Independent Accountant’s Report on...

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program December 31, 2015

Denver International Airport December 31, 2015

Contents

Independent Accountant’s Report on the Application of Agreed-upon Procedures .......................................................................... 1

Additional Information

Definitions .......................................................................................................................................... 2

Overview of the Project ...................................................................................................................... 4

Procedures .......................................................................................................................................... 7

Appendix A – DEN Cost Allocation Methodology and Testing Results ......................................... 10

Appendix B – Total Contract Values ............................................................................................... 18

Independent Accountant's Report on the Application of Agreed-upon Procedures

Mr. Timothy M. O’Brien, CPA, Denver City Auditor City and County of Denver Denver, Colorado

We have performed the procedures enumerated in the attachment to this report, which were agreed to by you, solely to assist you with respect to evaluating Denver International Airport’s (DEN) cost allocation methodology of the Hotel and Transit Center Program (HTC) as of and for the year ended December 31, 2015. The management of DEN is responsible for its aforementioned financial statement elements, accounts and items. This agreed-upon procedures engagement was conducted in accordance with attestation standards established by the American Institute of Certified Public Accountants. The sufficiency of the procedures is solely the responsibility of the parties specified in this report. Consequently, we make no representation regarding the sufficiency of the procedures described in the attachment to this report for the purpose for which this report has been requested or for any other purpose.

We were not engaged to, and did not, conduct an examination, the objective of which would be the expression of an opinion on the specified components, accounts and items described above. Accordingly, we do not express such an opinion. Had we performed additional procedures, other matters might have come to our attention that would have been reported to you.

This report is intended solely for the information and use of the specified parties listed above and is not intended to be and should not be used by anyone other than these specified parties.

Denver, Colorado June 28, 2016

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

2

Definitions

• “Capital assets” – Tangible or intangible assets acquired for use in operations that will benefit more than a single fiscal period. Typical examples are land, improvements to land, easements, water rights, buildings, building improvements, vehicles, machinery, equipment, works of art and historical treasures, infrastructure, and various intangible assets. 1

• “CIP” – Capital Improvement Projects. See page 6.

• “Contract values” – Maximum allowable spend per contract terms that is equal to project expenses incurred plus encumbered amounts and unprocessed encumbrance change orders.

• “City” – The City and County of Denver, Colorado.

• “Department of Finance” – The City and County of Denver, Colorado’s Department of Finance unifies the City’s accounting and financial functions under the Chief Financial Officer.

• “Design costs” – Costs associated with the design and studies done for the program.

• “DEN” – Denver International Airport.

• “DEN Finance” – The Denver International Airport Finance Unit lead by the Executive Vice President – Chief Financial Officer. The Sr. Vice-President of Business Operations (currently vacant) leads the team consisting of the Director of Accounting/Controller, Director of Fiscal Policy, Director of Procurement, and Director of Financial Risk & Analysis.

• “Direct costs” – Direct costs are those costs associated with the physical construction of the program.

• “External Consultant” – A third party company engaged by the City and County of Denver Department of Finance to provide program financial assurance and change management oversight services for the Denver International Airport Hotel and Transit Center and Other Capital Improvement Projects Program.

1 Governmental Accounting Standards Board Statement (GASB) No. 34, Basic Financial Statements – and Management’s Discussion

and Analysis – for State and Local Governments

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

3

• “General Contractors” – Four external design and construction contractors hired to complete the design and construction work for the Denver International Airport Hotel and Transit Center and Other Capital Improvement Projects Program. The fifth general contractor is Denver International Airport, who directly hired sub-contractors to complete the hotel furniture, fixtures and equipment / operating supplies and equipment, insurance, permits, art and management.

• “Hotel” – The 519-room hotel operated through a management agreement with Westin.

• “HTC” – Hotel and Transit Center Program.

• “HTC Program Manager” – Project Manager for the Hotel and Transit Center and Other Capital Improvements Program, hired in 2011, who oversees the completion of the projects.

• “Indirect costs” or “Construction distributable costs” – Costs associated with the non-physical construction cost of the direct cost contractors. For example, costs classified as construction distributable costs include design costs, construction general conditions, certain equipment, and construction bonds and insurance. These costs are allocated across the components of the project.

• “Other Capital Improvement Projects” – Projects included in DEN’s master capital plan which were undertaken during the Hotel and Transit Center Program.

• “PTC” – Plaza and Transit Center – A component of the Hotel and Transit Center Program,

which consist of an open-air plaza that connects the transit center and hotel to the existing Jeppesen Terminal. The Transit Center consists of a commuter rail station which serves commuter trains connecting DEN with downtown Denver’s Union Station.

• “Denver Airport Station” – The Denver International Airport Rail Station portion of the Hotel and

Transit Center Program.

• “STRP” – South Terminal Redevelopment Program – This is the original name of the project, which became the Hotel and Transit Center Program.

• “Work Breakdown Structure” – The detail of work performed provided in the cost estimate of work in the general contractor’s contract.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

4

Overview of the Project (As documented from discussions with the HTC Program Manager, DEN Finance and the External Consultant) In early 2011, Denver International Airport (DEN) announced the development of the South Terminal Redevelopment Program (STRP), which later was renamed the Denver International Airport Hotel and Transit Center Program (HTC). The initial budget estimate for the design and construction costs for HTC was $500,000,000. After initially hiring Parsons Transportations Group to serve as HTC project manager, in the fall of 2011, DEN hired a City and County of Denver employee as HTC Project Manager, who reports directly to the DEN Chief Operating Officer. In 2013, DEN leadership, with the approval of City Council, increased the budget of HTC to $544,117,417 as outlined in Table 1 on page 5. Also in 2013, an External Consultant was hired by the City’s Department of Finance to provide oversight services for the HTC. The External Consultant was charged with establishing the original allocation of costs from each of the general contracts to each component of the HTC and Other Capital Improvement Projects. Allocations were based on the External Consultant’s analysis at the lowest level of the Work Breakdown Structure detail available for the specific scope assigned to each contractor. The original budget of $544,117,417 included only the portion of the train station that DEN was originally planning to fund. An additional $53,196,720 was budgeted for the Denver Airport Station when a dispute arose as to which entity would pay for the remaining portion of the train platform and rail line. During this time period, other Capital Improvement Projects at DEN were approved. The HTC Program Manager asserted that Other Capital Improvements Projects were part of DEN’s master capital plan and not considered part of the HTC program, and therefore, were budgeted separately from the HTC Program. The amount for the Other Capital Improvements Projects was budgeted at $74,773,523. In 2014, the HTC Project Manager and External Consultant communicated to the DEN Leadership that HTC would exceed the approximate $544 million baseline budget by approximately 5-10%. Table 2 outlines the baseline budget after the $44 million increase. In November 2015, the Westin Hotel and Conference Center and Other Capital Improvement Projects were placed in service. The Public Transit Center and Denver Airport Station were placed in service during April 2016.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

5

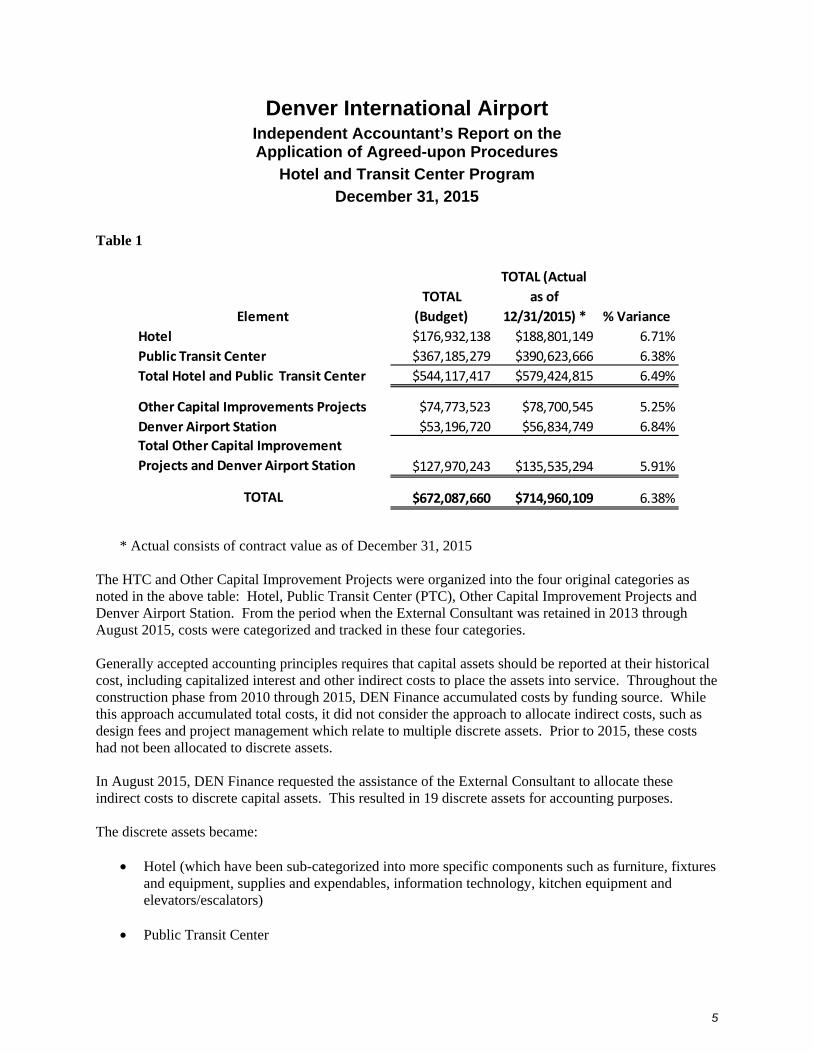

Table 1

ElementTOTAL

(Budget)

TOTAL (Actual as of

12/31/2015) * % VarianceHotel $176,932,138 $188,801,149 6.71%Public Transit Center $367,185,279 $390,623,666 6.38%Total Hotel and Public Transit Center $544,117,417 $579,424,815 6.49%

Other Capital Improvements Projects $74,773,523 $78,700,545 5.25%Denver Airport Station $53,196,720 $56,834,749 6.84%Total Other Capital Improvement Projects and Denver Airport Station $127,970,243 $135,535,294 5.91%

TOTAL $672,087,660 $714,960,109 6.38%

* Actual consists of contract value as of December 31, 2015

The HTC and Other Capital Improvement Projects were organized into the four original categories as noted in the above table: Hotel, Public Transit Center (PTC), Other Capital Improvement Projects and Denver Airport Station. From the period when the External Consultant was retained in 2013 through August 2015, costs were categorized and tracked in these four categories. Generally accepted accounting principles requires that capital assets should be reported at their historical cost, including capitalized interest and other indirect costs to place the assets into service. Throughout the construction phase from 2010 through 2015, DEN Finance accumulated costs by funding source. While this approach accumulated total costs, it did not consider the approach to allocate indirect costs, such as design fees and project management which relate to multiple discrete assets. Prior to 2015, these costs had not been allocated to discrete assets. In August 2015, DEN Finance requested the assistance of the External Consultant to allocate these indirect costs to discrete capital assets. This resulted in 19 discrete assets for accounting purposes. The discrete assets became:

• Hotel (which have been sub-categorized into more specific components such as furniture, fixtures and equipment, supplies and expendables, information technology, kitchen equipment and elevators/escalators)

• Public Transit Center

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

6

• Transit Center • Commercial Vehicle Lane • Central Plant • Terminal Interface • Plaza • Level 5 Bridges • Roads

• Other Capital Improvement Projects

• Automated Ground Transportation System (AGTS) • Baggage System • Level 4 Shell • ASD-X Relocation • East Airfield Storm Drainage • Level 4 and 6 Bridges • Storm Sewer • Excavate Runways Taxiways Pond-927 • Sanitary Sewer Tie-In • Excavation

• Denver Airport Station

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

7

Procedure #1 From DEN’s records we obtained a listing of payment applications and contractor payments relating to the Hotel and Transit Center Program (HTC). From the records and based on the contractor payment information and/or DEN allocation methodology, we obtained a schedule showing the costs allocated to each of the independent and integrated projects, specifically:

• Westin Hotel and Conference Center • Public Transit Center • Public Plaza

Results: We obtained a listing of payment applications relating to the HTC Program and Other Capital Improvement Projects from DEN Finance. We obtained the HTC and Other Capital Improvement Projects schedule from the DEN External Consultant. The schedule was subtotaled into the 19 subcategories and which then collectively totaled into the original four categories, specifically:

• Hotel • Public Transit Center • Other Capital Improvement Projects • Denver Rail Station

Procedure #2 From the list in procedure #1, payments totaling at least 20% of the total payments were randomly selected to determine whether the payment applications were complete and mathematically accurate. We randomly selected payment applications utilizing randomizer software to achieve a minimum of 20% of total HTC and Other Capital Improvement Projects costs. 60 payment applications were selected for testing. For these 60 items, invoices and supporting detail were obtained from DEN Finance. Results: Five of the 60 payment applications were altered after original submission by the contractor. These alterations took the form of amounts struck through and new amounts written in as approval for payment. Documentation supporting the changes were not included in the documentation provided.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

8

One of the 60 payment applications was missing the approval signature of the contractor. Nine of the 60 payment applications were missing approval signatures of the Project Manager. Procedure #3 For the payments from procedure #2, we obtained supporting documentation for recorded expenditures relating to the HTC Program and compared the amounts and descriptions of the supporting documentation to that on the provided schedules and to the amounts recorded in the general ledger. Results: Invoice descriptions were compared to the general ledger descriptions. We noted no exceptions. Initially, we could not agree amounts paid per the monthly payment applications and general ledger to the total HTC cost allocation spreadsheet because our selections were by invoices whereas each payment application included multiple invoices. Monthly payment applications were components of each contractor’s project-specific coding. Payment applications were traced into these project-specific coding totals, which were agreed to the total project codes’ values as noted in each contractor’s estimate of work. The HTC cost allocation spreadsheet, created by the External Consultant, was reviewed and utilized by DEN HTC project management and DEN Finance to allocate costs to discrete assets. From discussions with DEN Finance and External Consultant, total costs were allocated based on total contract values, due to previous years’ tracking of costs by project code and by funding source rather than grouping by discrete asset. For example, costs associated with insurance required to be maintained by contractors were coded to a project code and funding source, which was not further assigned or allocated to what would become the discrete asset. DEN Finance provided us with a reconciliation of payment applications to the HTC Program and Other Capital Improvement Projects costs. According to DEN Finance and External Consultant, the entire HTC and Other Capital Improvement Projects programs are not fully in service as of December 31, 2015, and additional work remains to be completed in 2016. See Appendix B for reconciliation of 2016 remaining contract value amendments and/or change orders. DEN Finance consulted with the HTC project management team and the External Consultant to understand how costs are allocated to the discrete assets for the HTC and Other Capital Improvement Projects Programs. Therefore, we were able to agree total values by contractor on the December 31, 2015 payment applications to total costs per contractor on the HTC and Other Capital Improvement Projects spreadsheet.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

9

We selected the December 2015 payment applications for each of the four general contractors, outlined in Appendix A, to compare the total value of the contract on the payment application to the total costs paid to each contractor. Since the payment applications were coded to project codes and not to the discrete assets, the External Consultant asserted he used architectural and design drawings to substantiate a basis to allocate certain costs. For the four external general contractors, we agreed the 60 payment application payment amounts in Procedure #2 to supporting documentation and approvals. In addition to the 60 payment applications, we then viewed the December 2015 payment application for each external general contractor containing the total approved contract value, which was allocated across the projects based on a percentage allocation methodology. See Appendix A for testing results. Procedure #4 From the information provided by DEN management, the procedures performed above, and based on the contractor payment information and/or DEN allocation methodology, we obtained a summary of total expenditures for each of the independent and integrated projects under the program, specifically:

• Westin Hotel and Conference Center • Plaza and Public Transit Center • Other Capital Improvement Projects • Denver Rail Station

Results: See Appendix B – Total Contract Values Procedure #5 As available, and from information provided by DEN Finance, we prepared a budget to actual comparison for each of the projects under the HTC program. See Table 1 in the Overview of the Project section on page 5 for this schedule prepared by DEN Finance.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

10

Appendix A – DEN Cost Allocation Methodology and Testing Results Background: The External Consultant prepared the HTC Program and Other Capital Improvement Projects cost allocation spreadsheet used by us in testing DEN’s cost allocation methodology. The External Consultant met with DEN project management, including the HTC Project Manager and his team as well as general contractors to understand the nature of the construction work being performed. In these discussions over the course of approximately three years, the External Consultant was able to accumulate cost data at the general contractor level. Subcontractors’ costs were included in the applicable general contractor totals thus were not required to be tracked separately by the External Consultant. This level of information drives the costs being allocated to discrete assets of the HTC and Other Capital Improvement Projects Program. DEN Finance noted that contracts were not bid into smaller projects within HTC and Other Capital Improvement Projects. For example, the contractor who performed the concrete work bid all concrete as one fixed price. Initially, the cost of the concrete was not allocated to specific projects, such as hotel and plaza and transit center. Therefore, the External Consultant utilized general contractor designs and architectural drawings, in addition to their own professional judgment, to substantiate cost allocation. For example, the cost of concrete was allocated based on square feet and cubic yards. Based on discussions with DEN Finance, we noted, initially, in the early phases of the projects, project codes were created to track costs. During the project there were some inconsistencies on the use of these project codes which may have been due in part to the turnover in DEN Finance personnel. This resulted in the External Consultant re-defining project codes of the project in 2013 based on the detail of projects outlined in the general contractor contracts. For construction contracts, details on the schedule of values line items identified in contracts or payment applications were used by the External Consultant to allocate costs. For services contracts (indirect costs) and subcontractors directly hired by DEN, categories or sub-categories were evaluated and professional judgment exercised by the External Consultant and HTC Project Management to allocate costs to the appropriate component. As the project progressed, the External Consultant reviewed each component as part of change management, and costs were allocated to a component based on actual outcomes of the contractor work. As discussed with the External Consultant, as updated information became available from the analysis of designs and progressing scope, indirect costs were allocated as deemed reasonable by HTC Project Management and the External Consultant.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

11

General Contractors: We discussed with the External Consultant, HTC Project Manager, and DEN Finance the costs associated with each general contractor to understand how each contractor invoiced work performed. Each general contractor’s methodology helped determine how DEN and the External Consultant tracked and allocated project costs to the discrete assets. Listed below is detail regarding the work each contractor performed, in addition to DEN’s methodology of allocating total costs to each project (hotel, plaza and transit center, other capital projects and Denver Airport Station). The four general contractors were:

• Gensler (GEN) • Architectural lead for hotel and transit center

• Mortenson, Hunt, Saunders (MHS)

• Construction Manager / General Contractor for Hotel, Public Transit Center, and Denver Airport Station

• Kiewit (KWT)

• General Contractor for civil works and bridges, including enabling (earthwork performed)

• Parsons (PAR) • Design lead for civil works and original Program Management

The fifth contractor was DEN itself:

• Airport (DEN) • Hotel Furniture, Fixtures and Equipment; Hotel Operating, Supplies and Expendables • Insurance • Permits • Art • Management

Each of DEN’s contracts were tested individually for categorization of costs directly to the discrete assets.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

12

Testing Results: Gensler Gensler’s work primarily consisted of design costs associated with the hotel, plaza and public transit center. Allocations of cost were made by the External Consultant and DEN HTC Project Management. Based on an understanding of the contract and interview of the External Consultant and DEN HTC Project Management, we understood that 67% of Gensler’s design work was to the Plaza and Transit Center, and 33% of costs were coded to the hotel. The percentages were a matter of professional judgment based upon the External Consultant and HTC Project Manager’s discussions with employees of Gensler, field engineers, and the HTC Project Management Team. Therefore, it was not possible to agree amounts directly from individual payment applications to discrete assets. Gensler’s costs were allocated based on direct construction costs of each discrete asset. Since MHS performed the direct construction work of the hotel, plaza and public transit center, we tested Gensler’s cost allocation by viewing the MHS direct cost allocation. Results and Observations: We could not agree the allocation percentage to substantive evidence such as a written analysis. DEN management represented the HTC Project Manager, External Consultant, field engineers and Gensler project managers, provided input into these percentages – the allocation was based on professional judgment and the understood scope of the projects. However no written documentation of this analysis was able to be provided. Of a total of 10 payment applications, ten payment applications were approved by the contractor, engineer/Project Manager and DEN HTC Project Management. One payment application did not have engineer/Project Manager approval. The total contract amount through the December 2015 payment application was $35,389,987 (see Appendix B). This amount was identified as the final approved amount for Gensler in the April 6, 2015 City Council minutes. MHS Much of MHS’ work consisted of direct construction costs such as concrete work on the projects identified above. The budget for MHS was entered into the Payment Application Schedule of Values by Construction Specification Institute (CSI) codes. CSI is an industry standard coding used to track cost over the life cycle of a project into categories such as concrete, steel, mechanical, electrical, etc. For example, CSI code 23 is designated “mechanical”.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

13

The budget was further broken down and tracked by base scope, allowances and contingencies. For direct costs of the project, each line is allocated across the assets differently. Many of the allocations are based on architectural designs to support the allocation. We tested the allocations by viewing a sample of the architectural designs and drawings. Results and Observations: Ten payment applications were selected for testing.

• Two of the payments applications contained adjustments to amounts originally disclosed on the payment application.

• One payment application did not contain a project manager’s signature. • All of the payment applications included DEN HTC Project Management signatures. • For one payment application, modifications to amounts due were physically altered without

supporting documentation. According to DEN Finance, DEN HTC Project Management would verbally communicate with the contractor but the length of time for a new payment application to be submitted would exceed the Prompt Payment policy as prescribed by the City and County of Denver.

The total contract amount on the December 2015 payment application was $385 million. This final amount was approved in Amendment 2 of the MHS Contract.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

14

The direct cost tested were for concrete work. The amount of direct costs for concrete was $44,179,702. We tested the allocation by agreeing the basis used by the External Consultant to drawings which contained square footage of each component of the HTC Program and Other Capital Improvements Program. Costs allocated to discrete assets based upon square footage from drawings provided by the contractor: Table 2

Component Project % Allocation Actual AllocationAllocation based on

correct measurement Variance

Hotel Hotel 27.33% 12,074,313 12,075,677 1,364

PTC Transit_Center 45.04% 19,898,538 20,669,481 770,943

PTC Comm_Veh_Lane 6.18% 2,730,306 1,254,815 (1,475,491)

PTC Terminal_Interface 0.14% 61,852 70,662 8,810

PTC Plaza 3.55% 1,568,379 1,778,667 210,288

PTC L5_Bridges 1.47% 649,442 649,442 0

CIP AGTS 0.81% 357,856 329,284 (28,572)

CIP Level_4_Shell 0.36% 159,047 159,048 1

CIP L_4_6_Bridges 3.82% 1,687,665 2,206,815 519,150

Denver Airport Station

Denver Airport Station11.30%

4,992,306 4,982,924 (9,382)

Total budgeted allocable cost per contract 100.00% 44,179,702 44,176,814 (2,888)

MHS code "03 33" (Concrete)

*Each Project's drawings were based upon square footage or cubic yards, as applicable.

Within the Plaza and Transit Center discrete assets, costs allocated for the commercial vehicle lane could not be supported by source amounts (drawings) as noted above. Based upon discussions with the External Consultant cost allocated to this discrete asset for concrete were incorrectly based upon measurements which included roads not part of MHS’ work. This only affected the allocation of costs to components, not the total costs to be allocated. The cost for Automated Gate Transportation System (AGTS) concrete could not be supported by drawings as square footage of the provided support at the time of fieldwork could not be ascertained.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

15

Kiewit Twelve payment applications totaling $31,687,327 from Kiewit were selected for testing. The original Kiewit contract was broken out into 12 task orders which were set up generally based on the scope of work to be performed, excavation, storm drain, etc. According to the External Consultant, the Kiewit contract was analyzed at the lowest level of detail it could ascertain, which was the unit price line item level per the contract and schedule of values. Through this analysis, scope components were created, which represented a rollup of the approximate 1,700 unit price line items into 49 scope components. Allocations made by the External Consultant to the four scope elements (Hotel, PTC, Other Capital Improvement Projects and Denver Airport Station) was performed by the HTC Program Management team in support of the program baseline estimate established in March 2013, based on our discussions with the External Consultant. Results and Observations: One payment application did not have contractor and engineer/Project Manager approvals, however contained DEN approvals. Total Kiewit contract value was $117,999,000 as evidenced on the December 2015 payment application. Total value approved to be paid to Kiewit based on documents provided to us was $117,860,418 per change order #2. The difference is $138,582, which according to change order #2 represents a reduction in the scope of work as described in Kiewit’s Task Order #13. Much of Kiewit’s work supported multiple scope components. The External Consultant asserted that where work was reasonably determined to be applicable and necessary for multiple scope components, professional judgment was applied for allocation, using the unit price item level of detail as a guide. The direct cost tested for Kiewit was $14,173,780 which related to earthwork excavation for the foundation of the “Phase II Nox” as described in the Kiewit invoice. (Please note “Nox” represents the area north of the point where a bridge crosses Pena Boulevard, just after the turn north on Pena Boulevard to the terminal up to the hotel). The cost was allocated to the discrete assets below: Table 3

Component Project % Allocation $ Allocation Source Amount** Variance

Hotel Hotel 10.00% 1,417,318 1,275,629 (141,689)

PTC Transit_Center 10.00% 1,417,318 1,275,629 (141,689)

Denver Airport Station

Denver Airport Station80.00%

11,339,024 11,622,401 283,377

Total budgeted allocable cost per contract 100.00% 14,173,660 14,173,660 (0)

KWT code "9 010" (Phase II Nox)

**Cubic yards were used as basis for measurement. Per drawings, cubic yards allocated to Denver Airport Station was 82% and 18% to Hotel/Transit Center.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

16

In comparing the $14,173,660 to the December 2015 payment application, the amount, which is one of 19 separate sub-tasks of Task Order #9, differed from the original contract amount for Task Order #9 by approximately $2.3 million. The External Consultant and HTC Program Management asserted Task Order #13 costs were distributed to the original 12 task orders, resulting in the difference of $2.3 million. We also viewed drawings of the excavation site of the “bowl”, which outlined cubic yards of earth which was removed. The allocations are supportable to total cubic yards from drawings within 2% points, thus driving the variance noted above in Table 3. Parsons Sixteen payment applications from Parsons totaling $26,169,947 were selected for testing. The nature of the Parsons work was related to design work for the Plaza and Transit Center, therefore costs were classified as indirect and distributable across the components of the Plaza and Transit Center, in a similar manner to Kiewit. Parsons provided design work for the civil works, and Kiewit performed the civil and earth work of the “bowl”. These costs were allocated based on the direct cost allocation of each project. Results and observations: All of the payment applications contained the required approvals. One invoice for $1,589,711.16 contained a variance to the general ledger of $443.52. Total Parsons contract value was $115,100,000, as evidenced on the December 2015 payment application. For three of the payment applications, modifications to amounts to be paid were handwritten without documentation to support the change.

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

17

DEN Twelve payment applications totaling $6,506,913 to sub-contractors were randomly selected to test for categorization within the four projects. Results and observations: All payment applications contained DEN HTC Project Management signatures of approval and sub-contractor approval. See below for categorization of costs.

Sample No. Amount Allocation

1 47,422.98 100% to Hotel2 49,988.00 100% to Hotel3 1,992.56 100% to Hotel4 2,500,000.00 100% to Hotel5 1,690,500.00 100% to Hotel6 33,796.82 100% to Bridges7 21,723.20 100% Baggage8 25,677.97 100% to Denver Rail Station9 80,261.93 100% to transit center

10 1,555,550.00 100% to transit center11 340,000.00 65% Plaza, 35% Transit12 160,000.00 65% Plaza, 35% Transit

6,506,913.46$

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

18

Appendix B – Total Contract Values Total contract value, through December 31, 2015, provided by the HTC Project Management and External Consultant:

By Project / By Contractor MHS KWT GEN PAR DIA

TOTAL 2015

Hotel 132,991,131 8,406,764 11,324,795 9,208,000 26,870,458 188,801,148 Plaza and Public Transit Center 231,100,681 39,977,235 20,880,093 74,815,000 23,850,657 390,623,666 Other Capital Improvement Projects 12,387,876 37,758,247 3,185,099 17,265,000 8,104,324 78,700,546 Denver Rail Station 8,520,312 31,856,754 - 13,812,000 2,645,683 56,834,749

Total 385,000,000 117,999,000 35,389,987 115,100,000 61,471,122 714,960,109

The estimated contract adjustments below are expected to be incurred in 2016 as the project is completed:

Contractor

Anticipated 2016 Change Orders or

Amendments**Gensler -$ MHS 1,506,126 Kiewit - Parsons 1,400,000 DIA - Contingency 972,220

3,878,346$

**Provided by DEN Finance

Denver International Airport Independent Accountant’s Report on the Application of Agreed-upon Procedures

Hotel and Transit Center Program

December 31, 2015

19

Additional Information As of December 31, 2015, the hotel and other components of the public transit center and other capital improvement projects were placed into service. Once in service, DEN Finance determined whether costs were to be capitalized or expensed in accordance with generally accepted accounting principles. Below is a breakdown, by component, of costs determined to be placed in service and capitalized or expensed. Costs, anticipated costs, and amounts encumbered, are also recorded to construction in progress as these assets were not placed in service:

ConstructionComponent Capitalized Expensed * In Progress Total

Hotel 185,510,382 3,851,829 - 189,362,211 Transit Center - 18,585,230 280,419,276 299,004,506 Commercial Vehicle Lane 8,170,666 577,072 - 8,747,738 Central Plant 6,390,469 664,668 - 7,055,137 Terminal Interface 7,960,179 575,471 - 8,535,650 Plaza 31,382,789 2,392,344 - 33,775,133 Level 5 Bridges 17,794,960 1,339,140 - 19,134,100 Roads 13,024,010 957,236 - 13,981,246 Automated Gateway Transit System 3,755,546 375,095 - 4,130,641 Baggage System 1,127,271 425,668 - 1,552,939 Level 4 Shell 3,932,294 372,857 - 4,305,151 ASD-X Relocation - 2,966,768 - 2,966,768 East Airfield Storm Drainage 2,241,136 661,663 - 2,902,799 Level 4 and 6 Bridges 39,068,690 2,403,119 - 41,471,809 Storm Sewer 8,089,027 388,210 - 8,477,237 Runways and Taxiways 4,046,412 376,682 - 4,423,094 Sanitary Sewer Tie-In 3,740,138 375,816 - 4,115,954 Excavation 3,894,369 376,255 - 4,270,624 Denver Airport Station - 4,595,388 52,151,984 56,747,372

Total 340,128,338 42,260,511 332,571,260 714,960,109

As of December 31, 2015

∗ Items expensed were expensed for financial reporting purposes under generally accepted accounting principles. The majority of these items were expensed in years prior to 2012 as DEN management determined it was uncertain if the costs would be used in the final construction due to design changes which had occurred.