Demerger -Key accounting and regulatory aspectsX(1)S(e43tfn2jfmsnyi55klwm1n… · ·...

30

Demerger - Key accounting and regulatory aspects Rekha Bagry November 2011 www.pwc.com

Transcript of Demerger -Key accounting and regulatory aspectsX(1)S(e43tfn2jfmsnyi55klwm1n… · ·...

Demerger - Key accounting and regulatory aspects

Rekha BagryNovember 2011

www.pwc.com

Overview

• Demerger backdrop

• Company Law Implications

PwC

• Accounting Implications

• Case Studies

2

Demerger - Backdrop

PwC 3

Why Demerger?

Family

Arrangement

Unlock Value

Pre IPO

Segregation

PwC 4

Corporate

Restructuring JV / Alliance Balance Sheet

sizing

Better focus Regulatory

Important Regulations

SEBI

Companies

Stamp Duty

FDI

Indirect Tax

Overseas Tax Regulations

PwC 5

Companies Act

IFRS / Accounting Standard

Exchange Control

Indirect Tax

Direct Tax

CCI Regulations

Listing Agreement

Demerger – A backdrop

• Demerger not been defined in the Companies Act, 1956

• Synonymous with what is popularly known as ‘Spin Off’./’Hive-off’

• Term commonly used In Indian context since defined in tax laws

- Provisions introduced by the Finance Act, 1999

PwC

- Tax implications different from sale of business

• In Indian context context, demerger involves court process

6

Demerger – Company Law implications

PwC 7

Demerger – Companies Act Implications

• Effected through a Scheme of Arrangement under the

provisions of Sections 391-394

• Rights, assets and liabilities of the “undertaking” to vest with

the Resulting Company

• Approvals

PwC 8

Companies Act

Implications

– Shareholders & creditors - 3/4th in value and majority

in number

– Jurisdictional High court(s)/ NCLT

– Regulatory authorities (RD, ROC etc.)

• Scheme effective from Appointed date and operative from

Effective date

- Appointed date can be retrospective / prospective

Sections 391 - 394

Total No. of Members 2000

Total No. Members present 100

No. of members who voted on the resolution

95

Total no. of valid votes 90

PwC 9

Total no. of valid votes 90

Total issued and paid-up share capital

Rs. 500 Cr (i.e. 50 cr shares of Rs.10/- each)

Total issued & paid-up share capital held by members whose votes are valid

Rs. 300 Cr

Qualifying majority Minimum 46 members holding paid-up share capital of Rs. 225 cr or more

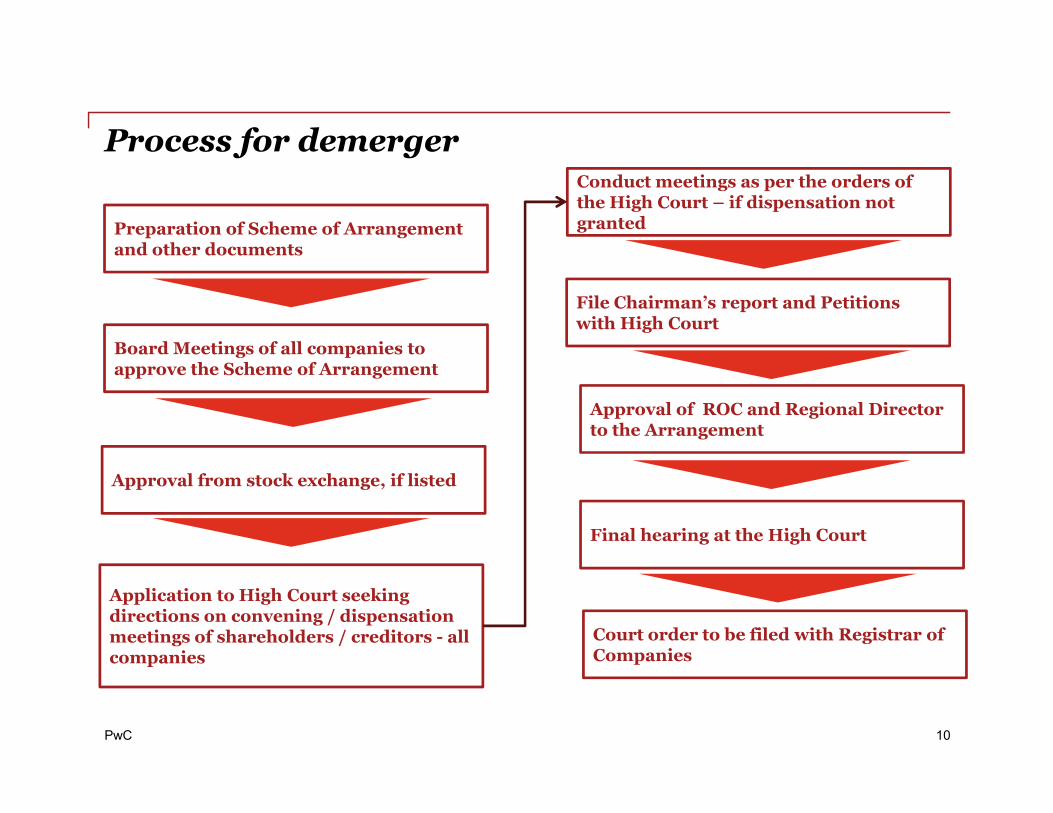

Process for demerger

Board Meetings of all companies to approve the Scheme of Arrangement

Conduct meetings as per the orders of the High Court – if dispensation not granted

File Chairman’s report and Petitions with High Court

Approval of ROC and Regional Director

Preparation of Scheme of Arrangement and other documents

PwC 10

Court order to be filed with Registrar of Companies

Final hearing at the High Court

Approval of ROC and Regional Director to the Arrangement

Application to High Court seeking directions on convening / dispensation meetings of shareholders / creditors - all companies

Approval from stock exchange, if listed

Demerger – Some company law aspects (1/2)

• Whether Scheme of Arrangement can be modified / withdrawn ?

• Whether valuation can be challenged by the Court ?

• Is it necessary to follow court process for both the companies ?

Shareholders

Issue of shares

PwC

for both the companies ?

• Whether Resulting Company can be a Foreign Company ?

• Whether combination of authorized share capital possible in case of demerger ?

11

A CoB Co

Demerger

• A Co demerges undertaking into

B Co

• B Co issues shares to

shareholders of A Co

Demerger – Some company law aspects (2/2)

• Can shareholder meeting be conducted through postal ballot ?

• Who can vote in case of joint shareholders ?

• Whether a person can represent more than 1 shareholder ?

Shareholders

Issue of shares

PwC 12

than 1 shareholder ?

• Whether voting by proxy possible ?

• Whether voting can be by show of hands?

A CoB Co

Demerger

• A Co demerges undertaking into

B Co

• B Co issues shares to

shareholders of A Co

Demerger – Accounting implications

PwC 13

Demerger - Accounting

• No specific Accounting standard prescribed for demerger

• AS-14 deals with merger; Applicability to demerger ?

• Generally, resulting company records all assets and

liabilities at book values to comply with tax neutrality Accounting

PwC 14

conditions

- Excess of net assets received by the resulting company

over the face value of shares issued is credited to

Reserves; incase of deficit debited to Goodwill account

• In books of demerged company, the value of net assets

transferred is adjusted against reserves

Accounting

Implications

Demerger – Some accounting aspects

• Whether resulting company can transfer difference arising pursuant to Scheme to General Reserve ?

• Whether assets can be recorded at fair value on demerger ?

PwC

• Whether deferred tax liability / asset gets transferred on demerger ?

15

Case Studies

PwC 16

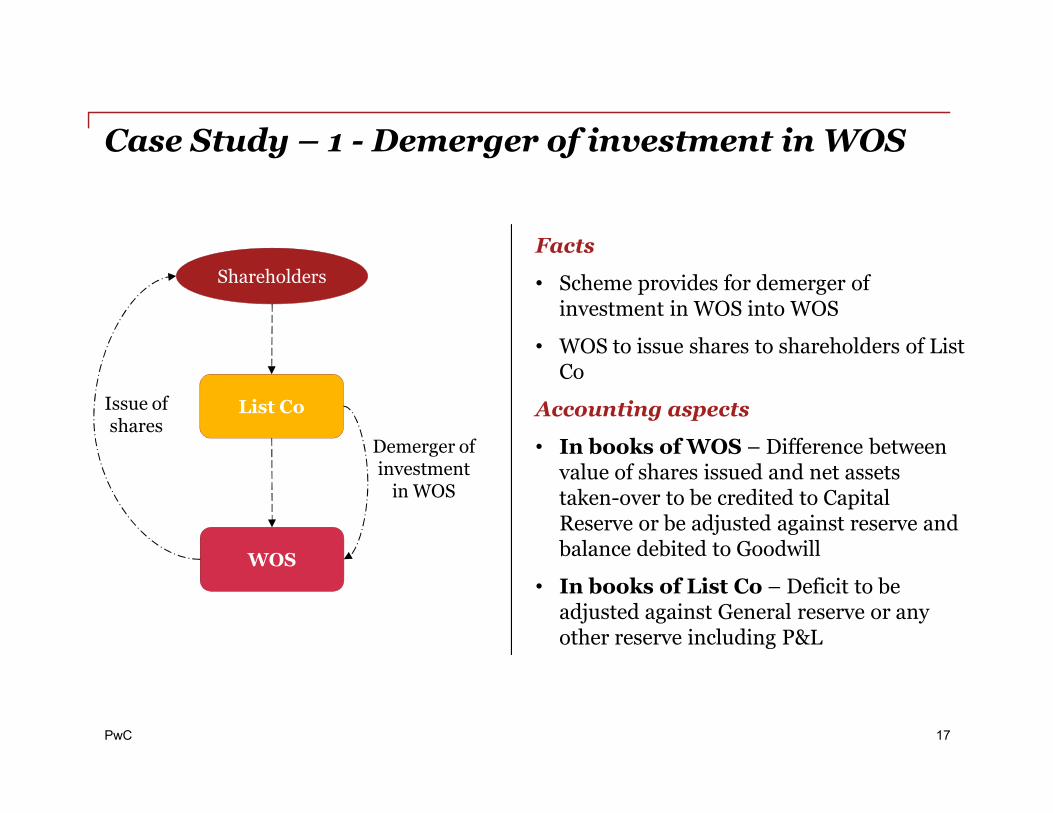

Case Study – 1 - Demerger of investment in WOS

Shareholders

List CoIssue of

Facts

• Scheme provides for demerger of investment in WOS into WOS

• WOS to issue shares to shareholders of List Co

Accounting aspects

PwC 17

List Co

WOS

Issue of shares

Demerger of investment

in WOS

Accounting aspects

• In books of WOS – Difference between value of shares issued and net assets taken-over to be credited to Capital Reserve or be adjusted against reserve and balance debited to Goodwill

• In books of List Co – Deficit to be adjusted against General reserve or any other reserve including P&L

Case Study – 2 – Demerger to WOS; share issue by parent (1/2)

Facts

Scheme provides for

• Creation and utilization of business reconstruction reserve

• demerger of business to wholly owned subsidiary of List Co.

List Co

100%

Issue of shares

Shareholders

PwC 18

subsidiary of List Co.

- List Co to issue equity shares to the shareholders of Op Co

Accounting aspects

In books of Op Co. – Excess of assets over liabilities to be adjusted in following order–

• Securities premium

• General reserve

• P&L

WOS Op Co

100%

Demerger

Case Study – 2 – Demerger to WOS; share issue by parent (2/2)

Accounting aspects

• In books of WOS - Deficit of assets over liabilities to be adjusted against Goodwill and in case of excess against General Reserve

• In books of List Co –

- Face value of shares issued to be debited to Business Reconstruction reserve (‘BRR’)

PwC

reserve (‘BRR’)

- An identified amount from Securities Premium account to be transferred to BRR to be utilised for adjusting interalia following expenses –

◦ Impairment, amortization and / or write off of goodwill and other intangible assets, if any, arising on preparation of consolidated accounts of List Co;

◦ Scheme expenses

◦ Costs in connection with financing/refinancing acquisitions;

- Balance in BRR to be transferred to General reserve

19

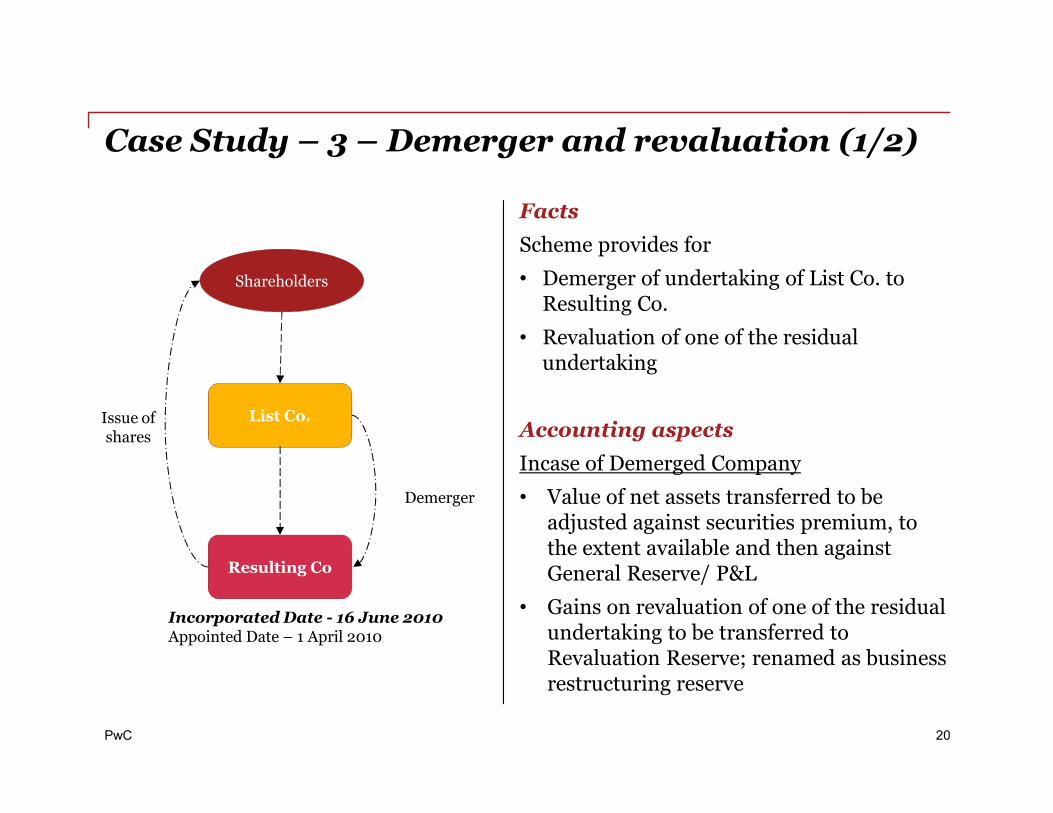

Case Study – 3 – Demerger and revaluation (1/2)

List Co.

Shareholders

Facts

Scheme provides for

• Demerger of undertaking of List Co. to Resulting Co.

• Revaluation of one of the residual undertaking

PwC 20

List Co.

Resulting Co

Demerger

Incorporated Date - 16 June 2010Appointed Date – 1 April 2010

Issue of shares Accounting aspects

Incase of Demerged Company

• Value of net assets transferred to be adjusted against securities premium, to the extent available and then against General Reserve/ P&L

• Gains on revaluation of one of the residual undertaking to be transferred to Revaluation Reserve; renamed as business restructuring reserve

Case Study – 3 – Demerger and revaluation (2/2)

Accounting aspects –

• Incase of Demerged Company (Contd…)

- Balance in BRR to be used to meet costs, expenses including on account of write down of the revalued undertaking

• Incase of Resulting Company (Contd…)

PwC

- Excess of net assets over share issued to be transferred to General Reserve and in case of deficit, be debited to Goodwill / Securities Premium account

Company Law aspects -

• Transfer of Authorised Share Capital of Demerged Company to Resulting Company

• Borrowing limits of the Resulting Company in terms of section 293 (1) (d) to be enhanced by a particular amount

• Resulting Company not in existence as on the Appointed Date; incorporated prior to effective date.

21

Case Study – 4 - Demerger from Foreign Co

Facts

• Scheme provides for transfer of ‘Indian Undertaking’ from Foreign Cos to List Co.

Accounting aspects -

• In books of List Co. – The value of net assets, after adjustment of diminution in value of

List Co.

Chain of

100%

Transfer of Indian undertaking

PwC

after adjustment of diminution in value of investment in subsidiary to be recorded as Goodwill; Goodwill to be adjusted against balance in the securities premium account

Company Law aspects -

• Indian undertaking were registered as branch

• Approval of High Court where List Co. was incorporated and jurisdiction where branch was registered taken

Slide 22

Chain of Subsidiaries

Branch in India

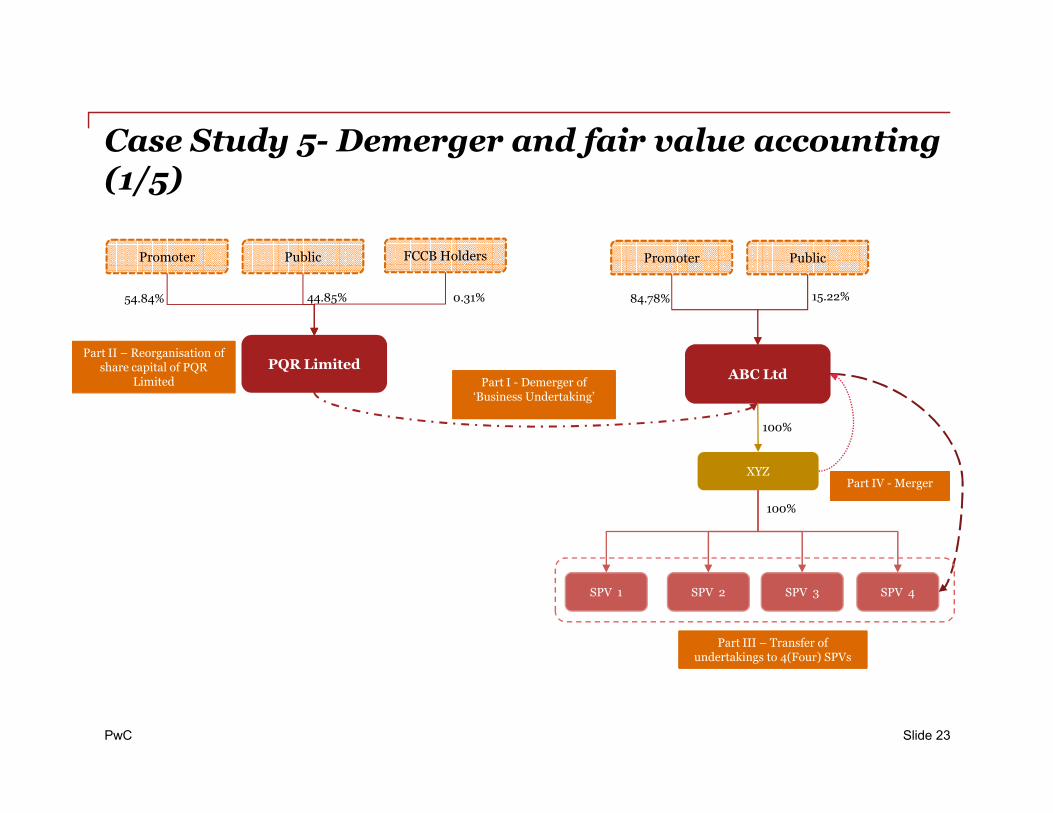

Case Study 5- Demerger and fair value accounting (1/5)

PQR Limited

Promoter Public

54.84% 44.85%

FCCB Holders

0.31%

ABC Ltd

Promoter Public

84.78% 15.22%

Part I - Demerger of ‘Business Undertaking’

Part II – Reorganisation of share capital of PQR

Limited

PwC Slide 23

XYZ

SPV 2 SPV 3 SPV 4SPV 1

100%

100%

Part III – Transfer of undertakings to 4(Four) SPVs

Part IV - Merger

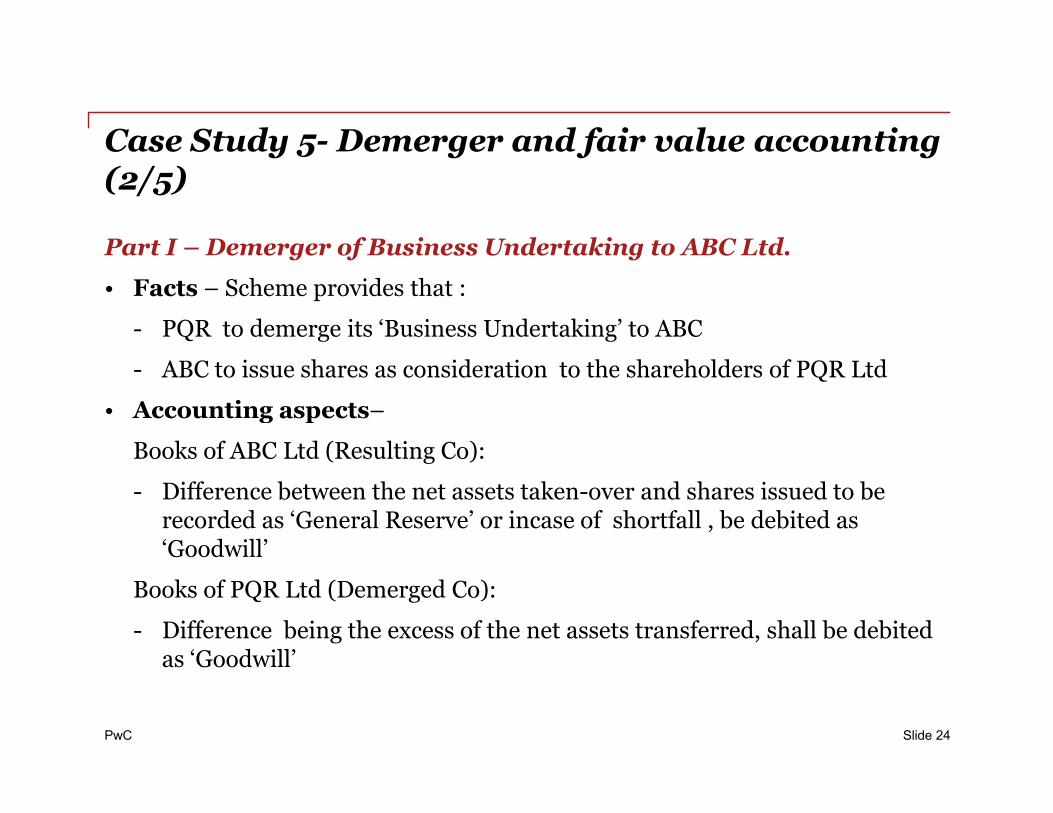

Case Study 5- Demerger and fair value accounting (2/5)

Part I – Demerger of Business Undertaking to ABC Ltd.

• Facts – Scheme provides that :

- PQR to demerge its ‘Business Undertaking’ to ABC

- ABC to issue shares as consideration to the shareholders of PQR Ltd

• Accounting aspects–

PwC

• Accounting aspects–

Books of ABC Ltd (Resulting Co):

- Difference between the net assets taken-over and shares issued to be recorded as ‘General Reserve’ or incase of shortfall , be debited as ‘Goodwill’

Books of PQR Ltd (Demerged Co):

- Difference being the excess of the net assets transferred, shall be debited as ‘Goodwill’

Slide 24

Case Study 5- Demerger and fair value accounting (3/5)

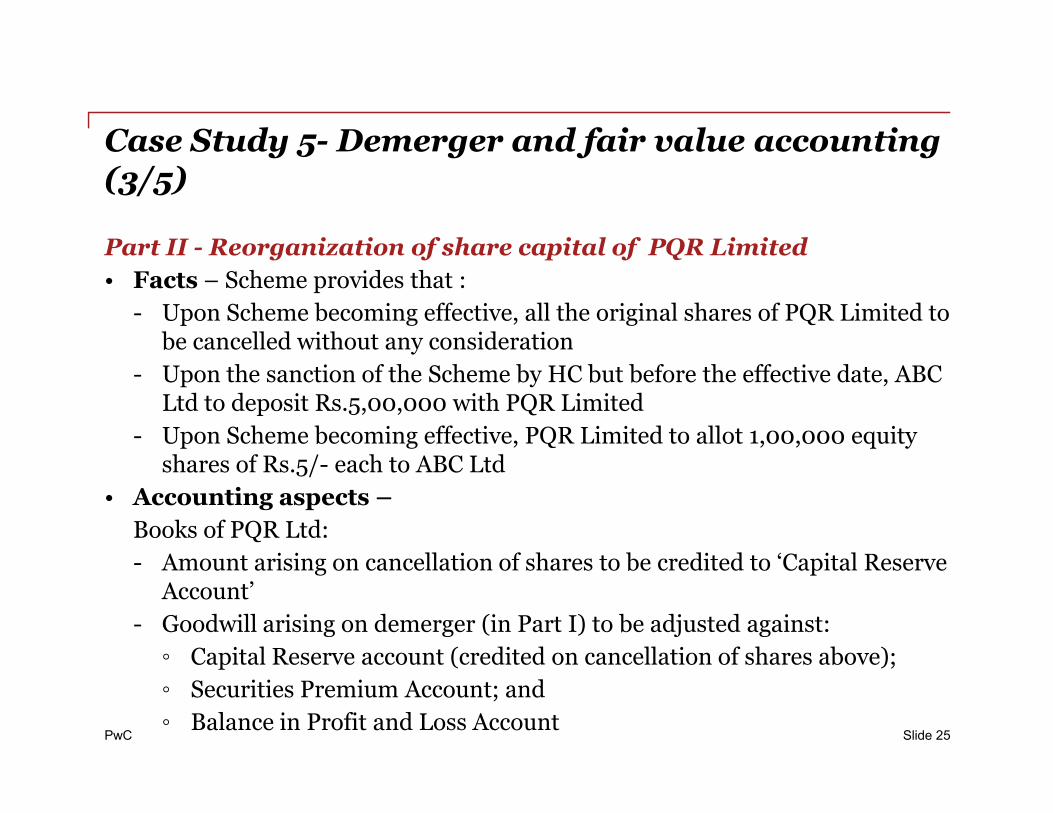

Part II - Reorganization of share capital of PQR Limited

• Facts – Scheme provides that :

- Upon Scheme becoming effective, all the original shares of PQR Limited to be cancelled without any consideration

- Upon the sanction of the Scheme by HC but before the effective date, ABC Ltd to deposit Rs.5,00,000 with PQR Limited

PwC

Ltd to deposit Rs.5,00,000 with PQR Limited

- Upon Scheme becoming effective, PQR Limited to allot 1,00,000 equity shares of Rs.5/- each to ABC Ltd

• Accounting aspects –

Books of PQR Ltd:

- Amount arising on cancellation of shares to be credited to ‘Capital Reserve Account’

- Goodwill arising on demerger (in Part I) to be adjusted against:

◦ Capital Reserve account (credited on cancellation of shares above);

◦ Securities Premium Account; and

◦ Balance in Profit and Loss AccountSlide 25

Case Study 5- Demerger and fair value accounting (4/5)

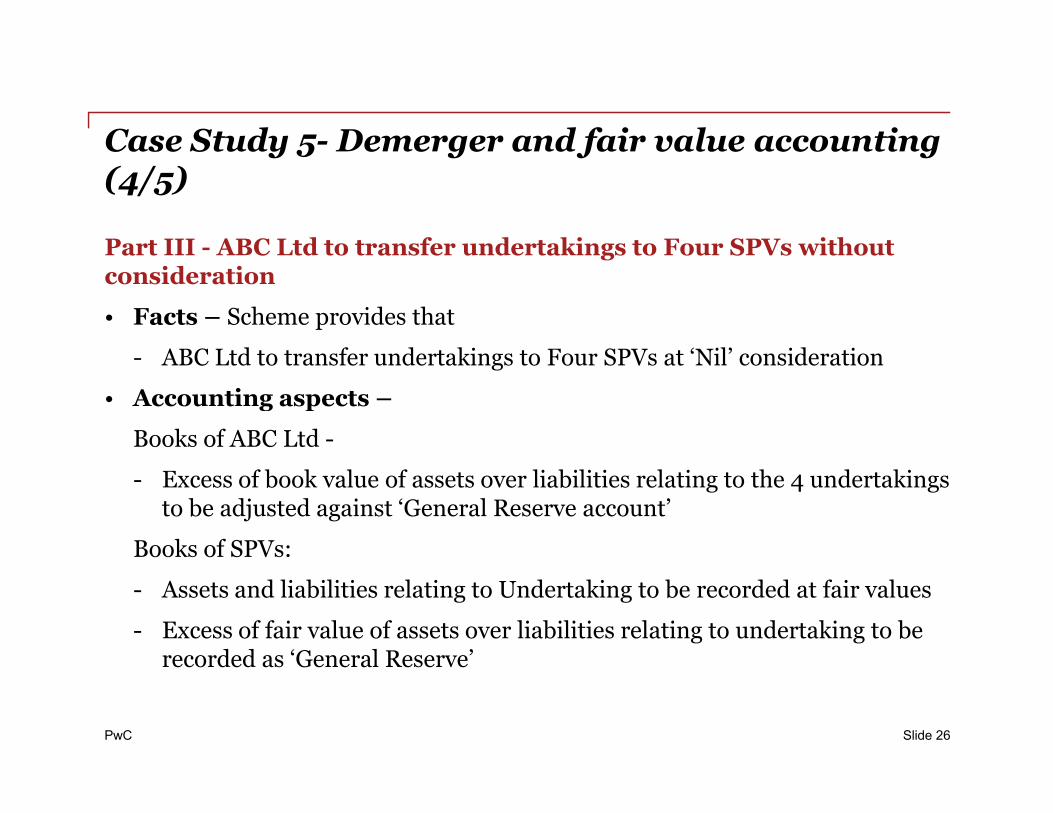

Part III - ABC Ltd to transfer undertakings to Four SPVs without consideration

• Facts – Scheme provides that

- ABC Ltd to transfer undertakings to Four SPVs at ‘Nil’ consideration

• Accounting aspects –

PwC

• Accounting aspects –

Books of ABC Ltd -

- Excess of book value of assets over liabilities relating to the 4 undertakings to be adjusted against ‘General Reserve account’

Books of SPVs:

- Assets and liabilities relating to Undertaking to be recorded at fair values

- Excess of fair value of assets over liabilities relating to undertaking to be recorded as ‘General Reserve’

Slide 26

Case Study 5- Demerger and fair value accounting (5/5)

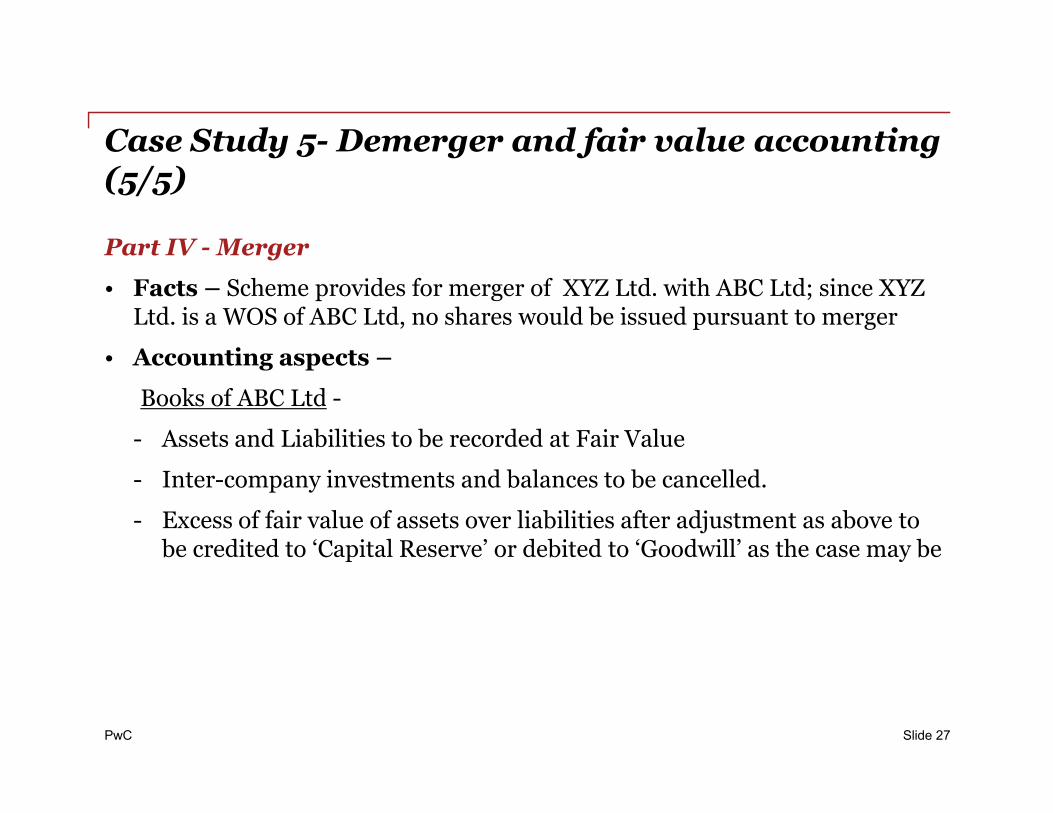

Part IV - Merger

• Facts – Scheme provides for merger of XYZ Ltd. with ABC Ltd; since XYZ Ltd. is a WOS of ABC Ltd, no shares would be issued pursuant to merger

• Accounting aspects –

Books of ABC Ltd -

PwC

Books of ABC Ltd -

- Assets and Liabilities to be recorded at Fair Value

- Inter-company investments and balances to be cancelled.

- Excess of fair value of assets over liabilities after adjustment as above to be credited to ‘Capital Reserve’ or debited to ‘Goodwill’ as the case may be

Slide 27

Case Study 6 – A variant to Classical Demerger (1/2)

Facts

• Scheme provides for demerger of identified business into WOS

Accounting aspects –

Promoters Public

47% 53%

List Co

Pre Demerger

100%Demerger

PwC 28

• In books of WOS –

― Difference between value of shares issued and net assets taken-over to be credited to General Reserve or be debited to Goodwill ad the case may be

― Mark to market diminution of Fixed Income Securities to be charged to General Reserve Account

WOS

Promoters Public

47% 53%

List Co

Post Demerger

WOS

30% 37%33%

Case Study 6 – A variant to Classical Demerger (2/2)

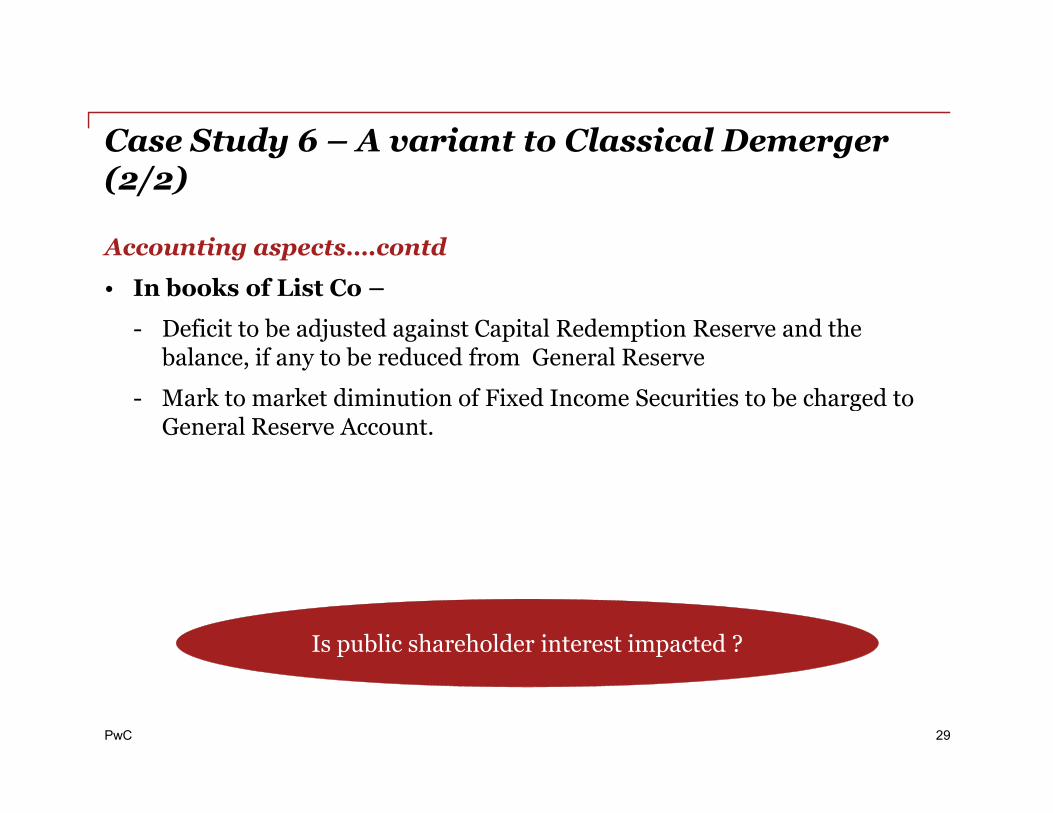

Accounting aspects….contd

• In books of List Co –

- Deficit to be adjusted against Capital Redemption Reserve and the balance, if any to be reduced from General Reserve

- Mark to market diminution of Fixed Income Securities to be charged to

PwC

- Mark to market diminution of Fixed Income Securities to be charged to General Reserve Account.

29

Is public shareholder interest impacted ?

Thank You

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers Private Ltd, its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2011 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC”

refers to PricewaterhouseCoopers Private Limited (a limited liability company in India), which is

a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of

which is a separate legal entity.