Delivery Mechanisms for MSME Financing Study Delivery Mechanisms for MSME Financing A Synthesis...

27

Special Study Delivery Mechanisms for MSME Financing A Synthesis Report (Regional) January 2005 OPER No: PE04-280S ab0 cd Project Evaluation Department FOR OFFICIAL USE ONLY. This document has a restricted internal distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without the Bank’s authorisation.

Transcript of Delivery Mechanisms for MSME Financing Study Delivery Mechanisms for MSME Financing A Synthesis...

Special Study

Delivery Mechanisms for MSME Financing

A Synthesis Report

(Regional)

January 2005

OPER No: PE04-280S

ab0cdProject Evaluation Department

FOR OFFICIAL USE ONLY. This document has a restricted internal distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without the Bank’s authorisation.

PREFACE

The principal aim of this evaluation special study is to synthesise the lessons learned from the Bank’s experience of operations targeting micro, small and medium-sized enterprises (MSMEs). The study outlines the development of the Bank’s approach to the MSME sector in the transition and summarises the principal findings of PED evaluations of MSME operations. The study derives key generic lessons from earlier evaluations and makes recommendations intended to improve the Bank’s ability to monitor and analyse the impact of operations on the MSME sector with the early transition countries particularly in mind. The report has been executed by William Keenan, Senior Evaluation Manager. The operations teams and other relevant Bank staff commented on an early draft of the special study and the Secretary General has been consulted on the final draft of this report. Information on the operations was obtained from relevant teams and departments of the Bank and its files as well as from external sector and industry sources. PED would like to take this opportunity to thank all those who contributed to the production of this report.

TABLE OF CONTENTS

Page

PREFACE ABBREVIATIONS AND DEFINED TERMS II 1. SCOPE AND METHODOLOGY OF THE SPECIAL STUDY 1 1.1 Introduction 1 1.2 Defining Micro, Small and Medium-Sized Enterprises 1 1.3 ‘Other Frameworks’ and ‘Standalone Operations’ 2 2. THE BANK’S APPROACH TO SMEs AND MSEs IN THE TRANSITION 3 2.1 The Approach as Outlined in Early EBRD ‘Transition Reports’ 3 2.2 Development of EBRD Strategy and Operational Policy for the SME Sector 4 2.3 Emphasising Sound Banking and Sustainability 5 2.4 MSME Business Volumes 5 2.5 TC Support for MSME Operations 6 3. PED’s PRINCIPAL EVALUATION FINDINGS (MSME OPERATIONS) 10 3.1 Thematic Special Study Report on SME Promotion and Financing (June 2000) 10 3.2 Operation Performance and Evaluation Ratings 1994-2003 10 3.2.1 Evaluation Special Studies on MSME Programmes 10 3.2.2 Standalone Operations and Small Frameworks 11 3.3 Regional Variations in Effectiveness of Equity-Based Programmes 13 4. GENERIC LESSONS FROM PED EVALUATIONS OF MSME OPERATIONS 16 5. RECOMMENDATIONS 20 5.1 Defining the Target Group 20 5.2 Devising Institutional and Market Performance Indicators for the Collection of Data for Impact Analysis 21

LIST OF APPENDICES

Appendix 1 MSME Definitions Appendix 2 Examples of Indicators for the Analysis of Transition

and Social Impacts of MSME Operations

i

EVALUATION SPECIAL STUDY DELIVERY MECHANISMS FOR MSME FINANCING

(REGIONAL)

ABBREVIATIONS

DIF Direct Investment Facility DTM Deal Tracking Module EC European Commission ETC Early transition countries EU European Union FOPC Financial and Operations Policies Committee IFI International Finance Institution MSE Micro and Small Enterprise MSME Micro, Small and Medium-Sized Enterprise OCE Office of the Chief Economist (EBRD) PB Participating bank PED Project Evaluation Department (EBRD) PEFs Private Equity Funds PPFs Post-Privatisation Funds TC Technical Cooperation TI Transition Impact

DEFINED TERMS

Bank Equity Team Team focussing on equity in banks Equity Funds Team Team investing in private equity funds Non-Bank Financial Institutions Team Team developing insurance, leasing and non-bank products the Evaluation Team Staff of the Project Evaluation Department who carried out the

post-evaluation the Operation Team The staff in the Banking Department and other respective

departments within the Bank responsible for operation appraisal, negotiation and monitoring.

ii

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 1 of 21 A Synthesis Report

1. SCOPE AND METHODOLOGY OF THE SPECIAL STUDY 1.1 INTRODUCTION

This study discusses the evolution of the European Bank for Reconstruction and Development’s policies for micro, small and medium-sized enterprises (MSMEs) in its countries of operations. It also considers the effectiveness of the delivery mechanisms and instruments the Bank has used to finance MSMEs, based on previously reported evaluation findings. This study is based on a review of internal Bank documents, including Board policy papers, select project approval documents, project monitoring reports and evaluation reports and special studies carried out previously by the EBRD’s independent Project Evaluation Department (PED). The evaluation team has also considered the experience of other international financial institutions (IFIs) in financing MSMEs, as well as equity experience with small and medium-sized enterprises (SME) in market economies. Section 2 of the report outlines the development of the Bank’s approach to MSMEs in the transition process and illustrates the volumes of MSME business it has undertaken. Section 3 considers the relative effectiveness of the principal MSME financing mechanisms the Bank has used, based on evaluation findings. Section 4 presents a number of generic lessons derived from PED evaluations, while Section 5 makes recommendations to enhance the monitoring of future operations and the analysis of their impact.

1.2 DEFINING MICRO, SMALL AND MEDIUM-SIZED ENTERPRISES (MSMES)

While in recent years the Bank has focused increasing attention on the MSME sector, to date it has not adopted a single definition of what constitutes a micro, small or medium-sized enterprise. In the absence of such a definition, the evaluation team has defined MSME investments as those operations identified in the Bank’s data warehouse as having an MSE or SME component.1 The table below lists the main investment programmes and frameworks that the EBRD has developed for the MSME sector. In addition, the Bank has conducted a substantial volume of MSME business through a large number of stand-alone operations and smaller frameworks, and has built, since 1998, a portfolio of investments in microfinance banks that it has supported with senior loans.

Principal MSME Programmes and

Frameworks Year

commenced Cumulative EBRD commitments

to 31 Dec 2003 € mm Regional Venture Funds (Russia) 1993/94 242 Russia Small Business Fund 1994 192 Post-Privatisation Funds 1997 112 Microfinance banks 1997 68 Direct Investment Facility (DIF) 1998 25 EU/EBRD SME Finance Facility 1999 633 US/EBRD SME Financing Facility2 2000 6 Other frameworks 1995 533 Stand-alone operations 1993/94 2,618 TOTAL 4,429

1 ‘Micro and small enterprises’ (MSEs) are a subset of ‘small and medium enterprises’ (SMEs). Investments are classified in the Bank’s project database as either ‘framework’ (with sub-operations) or ‘stand-alone’. Where the title or description of the operation indicates SME or MSE focus, the investment has been taken as an MSME investment for the purposes of this special study. 2 Investment commitments only. TC commitments are considered in section 2.5.

Page 2 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

At the outset it is important to recognise that the number of individual transactions generated by EBRD funds varies greatly depending on the objectives and structure of the investment programme concerned. For example, as of 1 March 2004, a total of 28 projects had been approved through the Direct Investment Facility (DIF). The current portfolio at that date comprised 19 projects and there was one exit in 2003. By contrast, the small lending programmes that specialise in low-value, short-term, loans generate many times more transactions. The Russia Small Business Fund (RSBF), in approximately 10 years of operation, had disbursed a total of US$ 1.5 billion through over 182,000 sub-loans by the end of March 2004 by continually recycling sub-borrowers’ loan payments. It is not possible, simply on the basis of the number of transactions generated, to make sensible in-depth comparisons of the performance of programmes that differ widely in their design and intent. Both the DIF and the RSBF have received Partly Successful overall ratings in PED evaluations (see Section 3.2 below). Investment volumes are considered in Section 2. The main purpose of this study is to synthesise the findings from the evaluation of MSME operations to identify generic lessons and recommendations that can be applied to future projects, particularly projects targeted at the early transition countries. Appendix 1 to this study outlines the definitions of MSME that the European Commission and some other bodies applied in their policies. Generally, these take the number of employees as a primary criterion, and they may also take balance sheet size and sales into consideration. A conclusion of this study is that the EBRD should adopt a definition of what is deemed to constitute a micro, small or medium-sized enterprise, and that the definition should be applied by banking teams. Consistently applied, this should enhance the quality of data collection and make it easier to monitor transition impact. This issue is addressed further in Section 5 below.

1.3 ‘OTHER FRAMEWORKS’ AND ‘STAND-ALONE OPERATIONS’ The principal MSME investment programmes and frameworks are identified in the previous section. For the purposes of this study, projects approved under smaller frameworks are grouped together under the heading ‘other frameworks’. These include, for example the multi-bank SME credit lines in Georgia and Uzbekistan and the Kazakhstan Small Business Programme. All other projects with an MSME orientation that are not included in ‘other frameworks’ are considered to be ‘stand-alone operations’ for the purposes of this study. In total, 33 ‘other frameworks’ have been identified and 203 projects have been classified as stand-alone operations.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 3 of 21 A Synthesis Report

2. THE BANK’S APPROACH TO MICRO, SMALL AND MEDIUM-SIZED ENTERPRISES IN TRANSITION

2.1 THE APPROACH AS OUTLINED IN EARLY EBRD ‘TRANSITION REPORTS’

The first EBRD Transition Report, published in 1994, began with a discussion of the meaning of transition and distinguished between the concepts of development, transition and stabilisation. It noted that while the concepts are very different, the relationships between them are strong. The report observed: “development is a summary term which includes as its basic element the advancement, in a number of key dimensions, of the standard of living of individuals”. The report argued that transition to an open market economy “is not only an intermediate goal contributing to economic development. It may also be regarded as an ultimate objective in itself. The market economy, in contrast to central planning, gives, in principle, the individual the right to basic choices over aspects of his or her life: occupation and place of work, where to live, what to consume, what risks to take or avoid and so on. The right to these choices may be seen as a basic liberty and as a fundamental aspect of standard of living. Of course, the notion of liberty goes far beyond the elements of choice described but these choices may be regarded as basic to it. Thus the transition is also an end in itself.” Clarifying the Bank’s definition of transition further, the report said: “the transition from a command to a market economy is the movement towards a new system for the generation and allocation of resources. It involves changing and creating institutions, particularly private enterprises.”3 The 1994 Transition Report went on to discuss the ingredients of transition and address some measurement issues. It noted that the privately owned enterprise is “the basic element of the market economy”, while the market is “the key arena in which enterprises and households interact”, and financial institutions are at the heart of a market economy since they “play fundamental roles as links for the allocation of resources over time (channelling savings and investment), for the allocation and assessment of risks, for payments mechanisms and for the enforcement of financial discipline.” The report then set out the EBRD classification system for transition indicators, which was designed to provide some possibility for empirical measurement or assessment. With some refinements, this classification has been applied over the last decade to monitor progress towards transition and assess the contribution of Bank projects to that progress.

The second EBRD Transition Report, published in 1995, further analysed the transition and

the role of investment in the process. A chapter was devoted to small and medium-sized enterprises, a type of activity that the Bank had identified as deserving special attention in the context of transition for two main reasons. The first reason was that SMEs were perceived to generate economic benefits beyond the boundary of the economic enterprise, which were not reflected fully in the enterprise’s own profitability. The second reason was that SMEs could become an engine for transition and growth, provided national governments adopted effective policies to remove handicaps and restrictions that remained from the days of central economic planning and created an environment to enable SME activity to function.

3 The report explained the connection with stabilisation in these terms: “stabilisation concerns basic macroeconomic variables including inflation, balance of payments, debt, unemployment and output shocks. Progress in achieving macroeconomic stability will be an important determinant of achievements in the transition, but it is very different from the transition itself.”

Page 4 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

2.2 DEVELOPMENT OF EBRD STRATEGY AND OPERATIONAL POLICY FOR THE SME SECTOR

A review of the Bank’s operational priorities was undertaken during a retreat of the EBRD’s Board of Directors and senior management in January 1999, leading to the adoption of the paper “Moving Transition Forward: Operational Priorities for the Medium Term” by the Board in March 1999. The principal documents approved by the Board are listed below.

Approval date Document title

Mar 99 Moving Transition Forward: Operational Priorities for the Medium Term Apr 99 Working Paper – Bank approaches to promoting business start-ups and

SMEs: A look forward Oct 99 Implementing the Bank’s SME Strategy – Organisational Structure and

Responsibilities Nov 99 Promoting SMEs in the Transition: the Bank’s Strategy

In “Moving Transition Forward” it was noted that the Bank had carried out a careful strategic review of its operational priorities in the light of the substantial changes in the region since 1994 and, in particular, the impact of the August 1998 banking and financial crisis in the region. The document reiterated the basic tenets of the EBRD mandate: “The Bank implements its mandate primarily by financing sound investment projects. Through its projects it works to expand and improve markets, to help build the institutions necessary for underpinning the market economy, and to demonstrate and promote market-oriented skills and sound business practices. In pursuing transition impact, the Bank applies sound banking principles to all its operations and ensures that it is additional to alternative market sources of finance.” The document stressed that “the level and nature of the Bank’s activities in a given country will be strongly influenced by its commitment to reform.” The document identified a number of priority activities for the Bank, with two principal activities focussing on (i) building financial sectors, and (ii) growth of SMEs, as described in the following box.

• A successful transition requires a sound financial sector which commands the confidence of the

population, facilitates transactions, and intermediates effectively and efficiently between savers and investors. The financial sector is therefore a priority for the Bank. The Bank’s focus is on building financial sectors that serve the needs of the real economy, including those of small and medium-sized enterprises. The Bank will develop a strategic view of the challenges facing the financial sector in each country, paying special attention to competition, decentralisation and variety in the provision of services. It will help build the necessary financial institutions by investing in them, by transferring skills and by requiring sound business practices. Based on its investor experience and working with other IFIs and the national authorities, the Bank will promote sector reform, in particular sound regulation. It will work with a broad range of instruments and promote both bank and non-bank financial institutions and the development of capital markets.

• Business start-ups and the growth of small and medium-sized enterprises (SMEs) are vital to the transition particularly through the nurturing of entrepreneurship, new jobs and social stability. Building on its substantial experience, the Bank will intensify its activities to promote start-ups and the growth of SMEs. The Bank will use and combine a full range of instruments including credit lines, microlending, equity and venture funds and technical assistance. The EBRD supports banks and other financial institutions that have an institutional commitment to SMEs. The Bank sees its support for SMEs as part of a broader policy framework. This framework includes local and regional infrastructure, training and networks for self-help. It also includes efforts to dismantle impediments to SME development. As the EBRD cannot take on all elements of this framework itself, it will work closely with partners, particularly the European Union (EU), and including bilateral institutions and other IFIs.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 5 of 21 A Synthesis Report

The document “Moving Transition Forward” was followed in April 1999 by a paper submitted to the Financial and Operations Policies Committee (FOPC) entitled “Working Paper – Bank approaches to promoting business start-ups and SMEs: A look forward.” The paper was submitted as information on work in progress rather than as a policy statement. In October 1999 the Board approved “Promoting SMEs in the Transition: The Bank’s Strategy,” which was accompanied by an information note: “Implementing the Bank’s SME Strategy – Organisational Structure and Responsibilities.” The strategy was based on integrating three pillars of SME promotion, namely finance, work on the investment climate and SME support networks. The information note explained the formation of a dedicated Small Business Finance Team “responsible for all micro and small enterprise (MSE) finance projects, such as RSBF, and including the establishment of microfinance banks.” The note said that the Bank Lending Team within the Banking Department’s Financial Institutions group would “continue to provide credit lines which reach the SME segment and where the underlying credit evaluation processes of the intermediary are distinct from the MSE lending approach.” Other responsibilities for developing SME business were carried out by the Bank Equity Team (focusing on equity in banks), the Equity Funds Team (investments in private equity funds) and the Non-Bank Financial Institutions Team (development of leasing and factoring products).

2.3 EMPHASISING SOUND BANKING AND SUSTAINABILITY

The April 1999 Working Paper “Bank approaches to promoting business start-ups and SMEs: A look forward” noted that donor-sponsored facilities such as the small business programmes and the regional venture funds have to demonstrate that “the kind of facility they offer is profitable, hence inducing replication.” Other instruments also aimed at building “commercially viable, and therefore sustainable, institutions.” The above references to key policy and strategy documents make it clear that the Bank’s earliest formulations of its MSME strategy placed emphasis on the sustainability of operations as a necessary condition for transition impact and sound banking. Indeed, the working paper “A look forward” identified a key conclusion “that operations must be designed in a way that ensures sustainability” as a general lesson drawn from PED evaluations as well as from the experience of other IFIs and public bodies offering SME financing and support. There is now an extensive literature on this subject matter. See, for example: • “Development of Financing Policies and Mechanisms for Small and Medium

Enterprises”, Final Report TA 3534 – PRC, Asian Development Bank, 2002 • “A Market-Oriented Strategy for Small and Medium-Scale Enterprises”, IFC Discussion

Paper Number 40, 2000 • “Strategic Evaluation of Financial Assistance Schemes to SMEs”, Final Report, European

Commission – DG Budget, December 2003. 2.4 MSME BUSINESS VOLUMES

The table in section 1.2 above lists the main programmes and frameworks developed by the Bank for the MSME sector. Between 1994 and 2003, signed EBRD commitments to SME and MSE investments totalled approximately €4.4 billion equivalent, or a little under 20 per cent of all signed commitments over the 10-year period. The charts below show the distribution of SME and MSE commitments year-by-year and cumulatively. Until 1999 the bulk of EBRD investment commitments with an SME focus comprised stand-alone operations. Since then, as the Bank has developed programmes and frameworks specifically for the MSME sector, these

Page 6 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

have accounted for an increasing proportion of MSME-related commitments. This is clearly illustrated in the charts below.

Annual Commitments to MSME Operations, 1994-2003

0

100

200

300

400

500

600

700

800

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

ME

UR

O

Microbanks

US/EBRD

EU/EBRD

DIF

PPF

RVF

RSBF

OtherframeworksStand-aloneoperations

Cumulative Commitments to SME/MSE Operations, 1994-2003

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

ME

UR

O

Microbanks

US/EBRD

EU/EBRD

DIF

PPF

RVF

RSBF

Other frameworks

Stand-aloneoperations

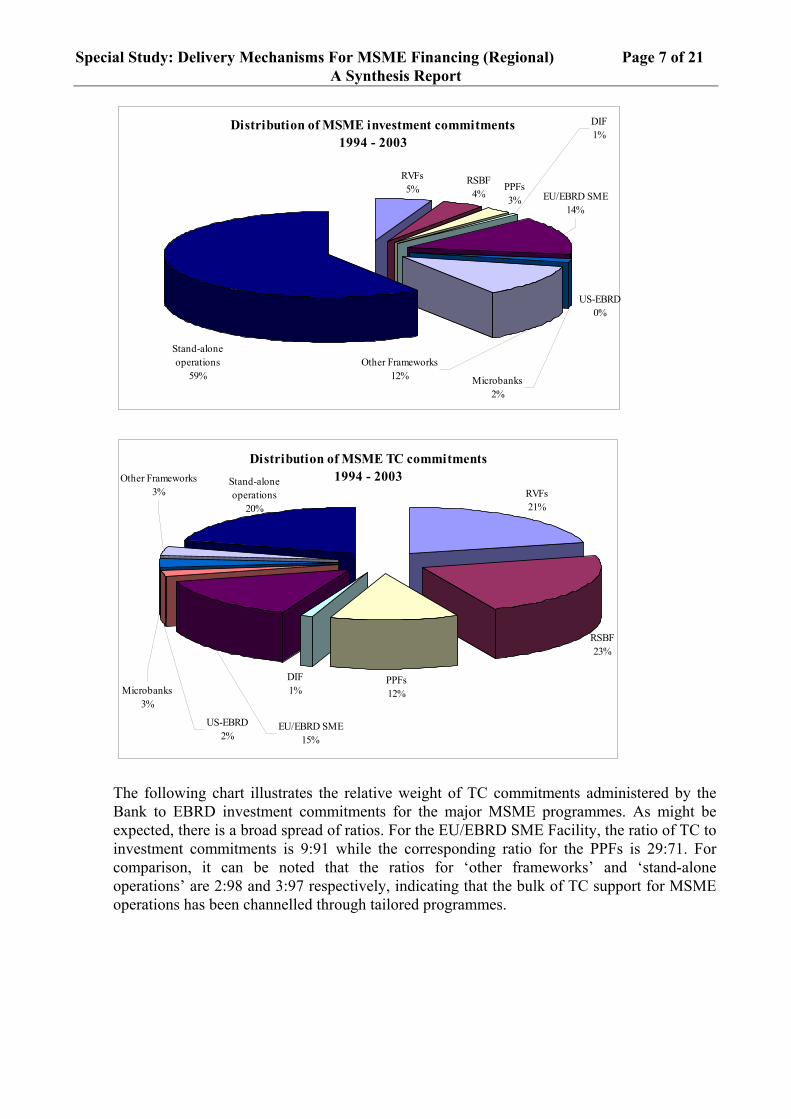

2.5 TC SUPPORT FOR MSME OPERATIONS Through end 2003 just under €490 million of technical cooperation (TC) funds were committed to support projects and programmes identified as MSME operations for the purposes of this special study. About €93 million of this was spent on the TurnAround Management (TAM) and Business Advisory Services (BAS) programmes, which are business support rather than investment operations. Therefore, approximately €397 million of TC funding was applied to support debt and equity operations, amounting to around €4.4 billion in total. While this implies an average TC commitment of nine cents per euro of investment commitment, there are wide variations in the level of TC support for different programmes. The following charts show the distribution of MSME investment commitments to end 2003, and the distribution of accompanying TC commitments.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 7 of 21 A Synthesis Report

Distribution of MSME investment commitments1994 - 2003

RVFs5%

RSBF4%

PPFs3%

Microbanks2%

Other Frameworks12%

DIF1%

Stand-alone operations

59%

US-EBRD0%

EU/EBRD SME14%

Distribution of MSME TC commitments1994 - 2003

RVFs21%

RSBF23%

PPFs12%

DIF1%

Other Frameworks3%

Stand-alone operations

20%

US-EBRD2%

EU/EBRD SME15%

Microbanks3%

The following chart illustrates the relative weight of TC commitments administered by the Bank to EBRD investment commitments for the major MSME programmes. As might be expected, there is a broad spread of ratios. For the EU/EBRD SME Facility, the ratio of TC to investment commitments is 9:91 while the corresponding ratio for the PPFs is 29:71. For comparison, it can be noted that the ratios for ‘other frameworks’ and ‘stand-alone operations’ are 2:98 and 3:97 respectively, indicating that the bulk of TC support for MSME operations has been channelled through tailored programmes.

Page 8 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

74%

26%

69%

31%

71%

29%

85%

15%

91%

9%

84%

16%

0%

20%

40%

60%

80%

100%

RVFs RSBF PPFs DIF EU/EBRDSME

Microbanks

Relative weight of TC to investment commitments

Investment commitments TC commitments

The above charts give a sense of the relative volumes of TC funds consumed by different programmes. While some stand-alone investment operations have used TC funds, it can be seen that the bulk of such funding has been used in connection with programmes specially designed for the MSME sector. Intuitively, this should enhance the effectiveness of the TC expenditure, yielding increasing cumulative benefits since the programmes operate over periods of years with substantial geographical coverage. The US/EBRD SME Financing Facility is omitted from the above chart because it is a special case. The relative weight of TC to investment commitments in the facility (76:24) needs a word of explanation. The EBRD Board approved the facility in June 2000, with the United States Department of the Treasury providing up to US$ 50 million to the Bank for TC and for on-lending via local financial institutions to micro, small and medium-sized enterprises. It envisaged that up to US$ 34 million of this would be on-lent, although up to 50 per cent of the US contribution could be used for TC with the consent of the donor. The EBRD undertook to make available up to US$ 100 million in parallel financing to local banks. It can be seen that design of the facility envisaged a substantial allocation of available funds to TC. As of 31 March 2004, a total of US$ 32 million of the available US$ 50 million of US funds had been committed, of which US$ 7.8 million (24 per cent) comprised loans to local intermediaries and US$ 24.3 million (76 per cent) was dedicated to TC operations, including policy dialogue and regional legal and regulatory issues. It is important to remember that, while each of the programmes discussed here is concerned with the MSME sector, they differ greatly one from another in their structure and in the kinds of sub-operations they support. For this reason it is not possible to draw conclusions about the relative effectiveness and efficiency of TC expenditure by different programmes simply on the basis of the split between TC and investment commitments illustrated in the above charts. For example, downscaling programmes with local banks tend to make large numbers of lower- value loans for shorter periods, whereas banks in the EU/EBRD SME Finance Facility tend to make larger loans with longer tenors. In order to make comparisons about the TC value for money delivered by different programmes, it is necessary to devise a set of measurement criteria that can be applied to all programmes while taking account of their diverse structures. An approach has been proposed in the recent paper from the Office of the Chief Economist, “Transition Impact and Subsidies in the EBRD’s Micro, Small and

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 9 of 21 A Synthesis Report

Medium-Sized Enterprise Financing Operations” (CS/FO/04-18). The present study refrains from further analysis in this respect.

Page 10 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

3. PED’s PRINCIPAL EVALUATION FINDINGS (MSME OPERATIONS) 3.1 THEMATIC SPECIAL STUDY REPORT ON SME PROMOTION AND FINANCING (June 2000) In response to the SME strategy initiative undertaken in 1999, PED commissioned a team of

consultants to study whether past EBRD and other IFI experience provided a basis for more defined guidelines on promoting SMEs. The resulting report identified five main lessons that had been learned commonly by other IFIs4 working in SME and MSE finance, which were found to correspond with EBRD experience.

The Main Lessons Commonly Learned: a) In designing projects for SME and MSE financing, more attention has to be given to

institutional aspects, in particular the financial viability of the credit programme or microfinance institution.

b) The selection of a committed intermediary is essential to the success of SME/MSE financing projects. The intermediary should also have sufficient institutional capacity to expand activities over time and be able to mobilise additional resources, including public deposits.

c) In order to become sustainable, SME/MSE financing projects have to be accompanied by efforts to build up institutional capacity for sub-loan handling. This requires substantial input of TC. Such TC, as a subsidy to the receiving institution, is judged to be more efficient than subsidising the sub-loans themselves.

d) SME/MSE financing projects should be embedded in a broader framework, which also addresses the legal and supervisory framework for such activities and institutions. EU-Phare has found its network of business support centres to be very helpful in pipeline development for its loan programmes.

e) Institutional sustainability and programme impact on the financial sector and on the target group have to be monitored more closely than has been done in the past.

3.2 OPERATION PERFORMANCE AND EVALUATION RATINGS 1994 – 2003

This section of the synthesis report provides an overview of the principal ratings assigned by PED in evaluations of operations that have targeted the MSME sector.

3.2.1 Evaluation Special Studies on MSME Programmes

The following table summarises the principal ratings assigned to large SME investment and support programmes evaluated by PED in recent years.

4 The IFIs studied were: IFC, World Bank, EIB, Asian Development Bank and EU-Phare.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 11 of 21 A Synthesis Report

SPECIAL STUDY Evaluation year

Overall rating

Transition impact

Risk to potential Additionality

INVESTMENT PROGRAMMES

Post-Privatisation Funds 2001 Partly

successful Marginal High Verified at large

Direct Investment Fund 2001 Partly

successful Good High Verified in all respects

Equity Funds 2002 Successful Satisfactory High Verified in all respects

EU/EBRD SME Finance Facility 2003 Successful Good Medium Verified at

large Russia Small Business Fund 2003 Partly

successful Satisfactory

/ Good High Verified in all respects

Micro Finance Institutions 2004 Partly

successful Satisfactory

/ Good High Verified at large

Grain Receipts Programme 2004 Highly

successful Excellent Low Verified at large

In addition to the above-listed investment programmes, PED has evaluated the BAS and TAM support programmes with the following principal ratings:

SUPPORT PROGRAMMES

Business Advisory Servies (BAS) 1997 Successful Good Medium N/A

Turn-Around Management Group (TAM)

2004 Highly successful Excellent High N/A

General conclusion 1: The Bank has been broadly successful in developing an effective approach to MSME investment and support through tailored programmes. Those programmes that have been rated Partly Successful overall, or Marginal or Satisfactory on transition impact, share common risks relating to questions of sustainability and exit. General conclusion 2: Partner Bank (PB) intermediaries should work toward replacing EBRD funding with funds from other sources in order to secure sustained benefit from Bank interventions. Where the Bank takes an equity stake, it is essential to set out an exit strategy that is realistic and takes account of the specific in-country environment.

3.2.2 Stand-alone Operations and Small Frameworks

During the ten year period 1994 – 2003, PED evaluated more than 80 MSME-related projects carried out as stand-alone operations or under small frameworks. The evaluated projects accounted for over 70 per cent by volume of identified MSME operations ready for evaluation. Overall some 81 per cent of the evaluated projects received transition impact

Page 12 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

ratings of Satisfactory, Good or Excellent. It follows that 19 per cent of projects received transition impact ratings of Marginal, Unsatisfactory or Negative. The following chart shows a breakdown of the TI ratings from more recent evaluations undertaken between 2000 and 2003.

Transition Impact ratings of small frameworks and standalone operations evaluated 2000-2003

10%

3%

50%50%

28%40%

13%

5%3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Small frameworks (10) Standalone operations(40)

NegativeUnsatisfactoryMarginalSatisfactoryGoodExcellent

As seen above, the TI ratings of projects under small frameworks show a more consistent pattern than those of stand-alone projects. Some 90 per cent of small frameworks were rated Satisfactory or Good for TI compared with 78 per cent for stand-alone operations. It may be that small frameworks over time will achieve more stable results than stand-alone operations. Whether this is the case should become apparent in coming years as more evaluation results become available. The following chart breaks down further the TI ratings assigned to stand-alone operations evaluated between 2000 and 2003.

Transition Impact ratings of stand-alone operations evaluated 2000-2003

10%

60%

45%

20%

78%

20%

36%

30%

22%10%

9%

30%

20%9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 (10) 2001 (11) 2002 (10) 2003 (9)

Year of evaluation (number of projects evaluated)

Negative

Unsatis factory

Marginal

Satis factory

Good

Excellent

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 13 of 21 A Synthesis Report

The decline observed in the 2001 and 2002 evaluation results is consistent with the problems that confronted the Bank, project sponsors, banks participating in SME credit lines and end borrowers in the aftermath of the 1998 financial crisis in the region. The following year (2003) has shown a strong recovery of transition achievement as assessed and analysed after project completion. Section 4 below derives a number of key generic lessons from evaluations of MSME operations.

3.3 REGIONAL VARIATIONS IN EFFECTIVENESS OF EQUITY-BASED PROGRAMMES

While some MSME programmes have focused on a specific country or region,5 others have had a wider geographical spread. An examination of previous evaluation studies and reports allows some conclusions to be drawn regarding the relative effectiveness of the various delivery mechanisms in different transition environments. As might be expected, some kinds of operations - for example, private equity - which have shown some success in more advanced countries, have been less successful in the early transition countries where private equity is a poorly understood concept. Looking at PED evaluations to date, it is particularly interesting to consider what kinds of EBRD intervention appear more likely to succeed in the early transition countries (ETCs), and for what reasons. Equity funds appear to be particularly sensitive to local conditions. This is not surprising, since the concept of equity and, moreover, of equity sale, transfer or trading was unknown in the former command economies. The table below summarises the findings of evaluation studies that considered the performance of the Bank’s post-privatisation funds (PPFs), private equity funds (PEFs) and the Direct Investment Facility (DIF). Programme / Instrument

More successful in … Less successful in …

Post-privatisation funds

PPF’s have been more successful in markets that are of sufficient size to enable the fund to acquire the necessary critical mass. Larger regional funds have performed better than smaller national funds, except in countries of sufficient economic size to support a substantial volume of economic investment. However, even within regions there may be significant national differences that affect funds’ operations (as seen in the Baltic countries). Fund organisation to give the Bank sufficient protection, and the quality of the fund manager, are essential ingredients of success.

The PPF mechanism is not recommended for replication. Newly privatised companies often lack transparency and have low standards of corporate governance. The privatisation of SMEs, once begun, is usually concluded relatively quickly, thus limiting the demand for this kind of intervention and restricting it to a short timeframe. In addition, it is difficult to hire qualified fund managers for such funds on a permanent basis, and fly-in fund management support has not performed adequately.

5 Examples of programmes with such a focus are the EU/EBRD SME Facility, which aimed initially at the accession countries, and the Russia Small Business Fund.

Page 14 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

Programme / Instrument

More successful in …

Less successful in …

Equity funds

Promising signs of graduation prospects through exit were found in CEE and more developed regions of Russia. Within CEE, conditions for equity funds were found to be more favourable in more advanced transition environments such as the Baltic countries, Poland and Hungary. Funds that took large stakes in ‘medium’ to ‘large’ enterprises in the advanced parts of the region were found to have the best prospects. Nevertheless, care must be taken to select investment targets that have a reasonable prospect of providing an exit route. In Ukraine, the strategy of investing in local companies that can be transformed to appeal to a foreign strategic investor has had some success.

Private equity funds have performed poorly in Central Asia and the Caucasus, having proved to be unsustainable in low-transition environments. The scope for private equity funds in ETCs is limited by the following constraints: poor understanding of the concept of equity by both government administrators and individual entrepreneurs; unwillingness of private owners to share ownership and control; and an undeveloped legal and administrative infrastructure. The design of funds must take account of the above factors as well as the poor liquidity of SME holdings, absence and lack of early prospect of a functioning local capital market and few sale opportunities to local trade buyers. The design must also allow for high transaction costs, including compliance costs for SMEs, which lead to diseconomies of scale. In general, returns have been poor on individual equity stakes below US$ 2 million, and the setting up of new funds for low-transition and slow-reforming countries is not recommended.

DIF The skills transfer to private business and the Bank’s resident offices through DIF is particularly beneficial in the ETCs, which are the least likely to produce bankable mainstream operations. DIF has acquired some critical mass in the low-transition countries. Belarus and Moldova may be suitable for DIF operations due to their early transition status, provided the Bank’s position can be adequately protected in the prevailing difficult investment climate.

Alternative vehicles are available in more advanced transition countries. European Russia and Ukraine are also served by other instruments. For the Russian Far East, a designated managed fund may be more appropriate, given the distance from London and the high costs of DIF operations. To sharpen focus and make effective use of resources, DIF should exclude the Balkans, where other SME schemes are operating.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 15 of 21 A Synthesis Report

General conclusion 3: The analysis brings out the diversity and heterogeneity of the Bank’s countries of operations. It is clear from the experience of the past decade, in relation to equity as well as debt, that some mechanisms have functioned more effectively in some countries and regions than others. This experience enables the Bank to tailor instruments to achieve maximum effectiveness given the characteristics of particular environments, targeting instruments more precisely than in the past.

Page 16 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

4. GENERIC LESSONS FROM PED EVALUATIONS OF MSME OPERATIONS

The following generic lessons have been synthesised from PED evaluation reports on MSME-related projects. The lessons have been formulated with the Bank’s targeting of early transition countries particularly in mind. LESSONS RELATING TO DEBT OPERATIONS

4.1 Conditional credit lines are suitable instruments for MSMEs The Bank’s experience confirms that conditional credit lines in various forms are suitable instruments for ensuring that funds are used to finance MSMEs. Properly structured Bank-to-bank credit lines can help achieve the dual objectives of supplying the real economy with term loan funds and developing the financial sector.

4.2 Technical assistance on the credit level alone may not be sufficient While technical assistance on credit procedures may be necessary to ensure the success of lending programmes through PBs, the Bank should recognise that assistance on the credit level alone may not be sufficient. PBs may require general support on issues such as strategy development, review of organisational structure, improvement of management skills or risk control and management. Organisational changes may be necessary to introduce proper segregation of duties in PBs between staff engaged in the promotion of lending business, staff engaged in loan appraisal and staff engaged in monitoring.

4.3 Sustainability depends on financial viability The issue of sustainability is directly linked to the financial viability and profitability of loan operations. In the case of small loan operations, the Bank should ensure that technical assistance to downscaling PBs includes training in product costing and the calculation of product profitability. EBRD monitoring reports should also include regular screening of the profitability of the local intermediary’s MSME loan products.

4.4 Continuing TC support may be required in weak environments In early transition countries where the financial sector is underdeveloped and bank supervision is weak, the continuing support of TC-funded credit advisors may be required to ensure the transfer of the necessary skills. When second and subsequent rounds of credit advisory assistance are organised by the Bank, cost-sharing arrangements should be negotiated wherever possible to maximise the effective use of limited TC resources and to strengthen the PB’s sense of ownership and commitment in respect of the technical assistance provided.

4.5 Seek candidates for MSME lending operations among existing local institutions Before participating in new small business banks, the EBRD should carefully examine the local financial sector and assess the capabilities and potential of existing institutions. The Bank’s experience in several countries is that existing local banks can be motivated to enter the small business segment with TC support. It has been demonstrated that specially-created banks with expatriate management can achieve high loan officer productivity in the short term. However, the total cost in the form of IFI equity, credit lines and donor-funded TC to specially-created banks is high. By working with existing banks, EBRD can capitalise on existing branch networks and deposit portfolios, thereby expanding effective intermediation alongside the institution-building goal.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 17 of 21 A Synthesis Report

4.6 Wider application of lessons learned Lessons learned in designing SME credit line operations are applicable to other potential products and support programmes, for example, the development of finance tools such as leasing. One of the most relevant considerations for the design of other programmes is the importance of timely implementation and phasing to maintain the value and usefulness of TC inputs. Another consideration is the introduction, to the extent possible, of loan conditions that serve the dual function of providing the client with new management information tools as well as satisfying the Bank’s monitoring requirements. Lastly, programmes must tailor their features to reflect specific country conditions that may affect project success.

4.7 Apply appropriate lessons from advanced transition countries in ETCs When developing operations with existing banks in early transition countries, it is important to take account of lessons learned from early operations in countries where the transition is more advanced. In particular, the Bank should ensure that demand exists for term financing in foreign currency and it should work with local banks to develop appropriate lending policies and credit skills. It should also develop corrective action programmes, where necessary, to upgrade and improve local bank management skills and systems. It should ensure that banks have identified an adequate pipeline of bankable sub-projects with the assistance of credit advisors where necessary. It should require banks to report on sub-projects systematically and ensure that monitoring reports assess sub-projects on a regular basis. Lastly, it should evaluate the quality of PB reports on sub-loan portfolios through periodic field visits. LESSONS RELATING TO EQUITY OPERATIONS

4.8 Achieving satisfactory risk distribution In the design of equity funds, market size and possibilities for achieving returns to scale are important considerations to achieve satisfactory investment performance and diversify risk. Funds targeting SMEs in one country or one region of a country may be extremely risky and prone to fail if the area does not offer a sufficient number of diversified opportunities. A more satisfactory risk distribution may be achieved with multi-country and/or multi-regional funds.

4.9 Fund manager selection is critical Careful fund manager selection is critical to the success of equity funds. The Bank should assess potential candidates fully prior to engagement to ensure that they meet the following criteria: specific experience investing equity in SMEs in a transition environment; strong working relationships with potential strategic sponsors; capacity to provide institutional support to the fund and investee companies; ability to monitor investments and become involved proactively in investee companies; a clear and motivating investment strategy that is consistent with the manager’s ambitions, capacity and capabilities; and skill in helping to formulate investment strategy and operational policies suitable to the environment.

4.10 Fund manager must be free of conflicting interests Fund managers must be able to exercise independent professional judgement and be free of conflicting interests or pressures. Investment guidelines should discourage investment by the fund in companies in which the fund manager holds an interest, either directly or through another fund. Similarly, the Bank should carefully consider, on a case-by-case basis, whether it is appropriate for investment funds in which it holds a stake to be permitted to invest in companies in which the EBRD is an equity investor, either directly or through another fund (if possible, the Bank should consider having a veto power over such investments by the fund).

Page 18 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

4.11 Equity funds may need several years to show positive financial returns The Bank’s experience suggests that equity funds may require at least five to six years to break even. This is consistent with the conclusions of the European Venture Capital Association, which estimates that performance in private equity funds can be measured only when a certain degree of maturity (at least four years) and a certain number of exits are achieved. The underlying assumption is that capital gains on well performing investments can only be realised towards the end of a fund’s lifetime, while losses on problem cases are recorded when they become anticipated.

4.12 A realistic exit strategy is needed from the outset Equity funds must develop a realistic exit strategy from investee companies. In early and intermediate transition environments where capital markets are underdeveloped and illiquid, it is not realistic to propose exit via the local market. In such an environment, the exit prospects may depend on targeting companies for investment that have the potential to appeal in due course to strategic investors. Through appropriate contractual arrangements, for example, by using strong shareholders’ agreements, the Bank and the fund manager may be able to influence the timing of exits to enhance investment returns.

4.13 Some additional lessons can be derived from examination of SME equity experience in

market economies:

• An official Australian report in 1997, the Financial System Enquiry (Wallis Report), considered the suitability of external equity investment for SMEs. The report noted that many SMEs were not suitable for external equity investment as they lacked growth prospects, owner-managers may not be willing to accept dilution of their control (and possibly the increased accountability that follows) and the personal affairs of the owner-manager(s) may not be separate from the business.6

• A Bank of England report “Finance for Small Firms. A Seventh Report,” January 2000,

noted: “Venture capital accounted for just 3 per cent of external finance for SMEs between 1995 and 1997. This is in part due to the “equity gap” where the funding requirements of a company are greater than those that can be met by the small-scale providers of finance, but not substantial enough to be considered by the large equity providers. Demand-side issues are also important and relatively few small businesses are prepared to accept a reduction in ownership and control in return for equity finance.”

• A subsequent Bank of England report in 2004 (“Finance for Small Firms. An Eleventh

Report”) highlighted the logjam that results when economic conditions curtail exit opportunities: “The available data show that 2002 was a difficult year for both venture capital funds and the businesses in which they invest. As also reported last year, venture capital funds had to continue to support existing investee businesses through later rounds of funding in 2003, at a time when they had expected to have sold them on. Thus, their capacity for new investment remained limited.”

6 Source: “Developments in SME Financing in Australia: Wallis Report Findings”, School of Commerce Research Paper Series: 01-4, The Flinders University of South Australia.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 19 of 21 A Synthesis Report

General conclusion 4: In this connection, it is worthwhile to note that a downturn in the business cycle may contribute to the curtailment of exit opportunities in the case of equity funds, and to deterioration in the repayment record in the case of small business loans. Since the 1998 financial crisis many countries of operations have been experiencing business expansion. An approaching contraction would signal an expected reduction in the quality of loan and equity portfolios, a phenomenon that banks and borrowers in countries of operations have not, by and large, had to face yet in the transition in connection with a change in the business cycle.

Page 20 of 21 Special Study: Delivery Mechanisms For MSME Financing (Regional) A Synthesis Report

5. RECOMMENDATIONS As noted above, there has been some inconsistency in the definitions of what constitutes an MSME in the Bank’s operations. A conclusion reached by the evaluation team is that this, looking forward, will hamper to Bank’s ability to collect data for impact analysis that is comparable over time. The following recommendations are proposed to improve the Bank’s ability to monitor and analyse the impact of operations on the MSME sector.

5.1 DEFINING THE TARGET GROUP7

The target group for early EBRD credit lines to intermediary banks was not always consistently defined. This was highlighted, for example, by PED evaluations in the 1990s of credit lines to leading Baltic banks. On a number of occasions, the evaluations found that to begin with, certain banks were content to lend mainly to established existing clients at the higher end of the range of permissible exposures. An evaluation lesson, to the effect that eligibility guidelines on credit lines should be strengthened, was applied subsequently. Nevertheless, the absence of a consistently applied MSME definition hinders the Bank’s capacity to record and report meaningfully over time trends and characteristics of MSME sub-operations. The development of a database showing changes in institutional and market-performance indicators collected from banks participating in the EBRD’s MSME credit lines could enhance transition impact analysis and policy dialogue initiatives. It is important to seek a definition of MSMEs that can be suitably applied in the business environments in the Bank’s countries of operations, particularly the ETCs.8 It is important also to distinguish between defining what constitutes an MSME and defining a micro-, small or medium-sized loan. Some practitioners have tended to allow sub-loan size to be the determining factor in the classification of MSME operations, using loan size as a proxy measure. While this may appear to have the merit of simplicity, it seems appropriate to look more closely to the characteristics of borrowing enterprises in deciding what constitutes an MSME. Nevertheless, it may be important also to define sub-loan size, especially when the intermediating bank is using a lending methodology designed for particular sub-sectors of the MSME population. This particularly applies to lending methodologies designed for micro and/or small borrowers. Care must be taken to ensure that the methodology is not stretched to embrace loans to larger, more complex enterprises, which require more sophisticated credit analysis. RECOMMENDATION: The EBRD should adopt standard definitions of what constitute micro, small and medium-sized enterprises to achieve consistency in performance monitoring, data collection and impact analysis. The primary criterion for an enterprise to be considered an MSME should be number of employees. It seems appropriate to adopt the EU criteria of fewer than 10 employees for a microenterprise, fewer than 50 for small and fewer than 250 for medium-sized (see appendix 1). Annual sales or balance sheet total may be used as an additional eligibility check. The Bank should consider applying an independence criterion to exclude enterprises that are part of a larger grouping. In cases where a lending programme is reliant

7 Appendix 1 shows some MSME definitions adopted by the EC, IFC and other bodies. 8 It is recognised that many of the Bank’s countries of operations have their own definition of SME enshrined in law. However, the evaluation team considers it appropriate for the Bank to adopt a single consistent definition for analytical purposes.

Special Study: Delivery Mechanisms For MSME Financing (Regional) Page 21 of 21 A Synthesis Report

on a particular lending methodology, loan size limits should be set that take account of the capacity of the lending methodology and the skills and experience levels of intermediating banks.

5.2 DEVISING INSTITUTIONAL AND MARKET PERFORMANCE INDICATORS FOR THE COLLECTION OF DATA FOR IMPACT ANALYSIS To achieve consistency and comparability in the monitoring and analysis of operations, it is desirable to apply a uniform set of indicators for the collection of data. This approach should assist the analysis of transition and social impact of operations and sub-operations, particularly in the early transition countries. Since the lower financial returns that are anticipated from investments in these countries are expected to be compensated by transition and social impacts, it is important to adopt practical measures by which to analyse these impacts. Ongoing monitoring is required to ensure that EBRD and donor objectives are met. While donor requirements for information must be satisfied, the thoroughness and extent of monitoring should be guided by sound banking and transition impact requirements to allow the Bank to make effective investment decisions. See also Appendix 2 of this report. RECOMMENDATIONS: It is recommended that the EBRD should devise a set of indicators to facilitate the measurement and analysis of transition and social impacts of MSME operations. Both institutional and market performance indicators are required. Institutional indicators should measure financial performance and management capacity. Standard financial indicators should be supplemented by measuring the financial impact of implicit and explicit subsidies, including the subsidy implicit in below-market funding from all sources. Profitability by product type should also be estimated for intermediating banks. The dynamics of organisation development should be monitored to assess growth in management capacity in line with the Bank’s institution building goals. Relevant factors are formal and informal training of local loan officers; the replacement of consultants and expatriate managers with suitably qualified local staff in middle-management and, eventually, senior positions; growth of capacity to handle effectively larger SME loans and legal and accounting matters in-house. Market performance indicators should be designed to permit monitoring and comparison of real-sector impact over time. Client-based information includes details of market sector, time in business, levels of sales and fixed assets, employment numbers and profitability. To measure market penetration information should be gathered on the tenor of intermediating banks’ sub-loans, average loan size and numbers of repeat borrowers. It is recommended that, where possible, the collection of data on MSME lending should encompass loans made from intermediating banks’ own funds, as well as loans from the EBRD’s credit lines. The EBRD and other IFIs offer incentives of various kinds to intermediating banks to encourage them to expand their MSE and SME portfolios. As an indication that such lending is being developed on a sustainable basis, the Bank looks for evidence that intermediating banks are prepared to allocate their own funds for lending to MSME borrowers in addition to using IFI credit lines. In order to analyse more fully the impact of EBRD interventions, the Bank should seek information to measure also the above institutional and market performance indicators as they relate to client banks’ MSME lending from their own funds.

APPENDIX 1

MSME DEFINITIONS SOME DEFINITIONS OF ENTERPRISE TYPE BY NUMBER OF EMPLOYEES Micro Small Medium Large OFFICIAL DEFINITIONS European Commission1 Less than 10 Less than 50 Less than 250 Not defined IFC2 10 or less > 10 < 50 50 to 300 Not defined World Bank3 Less than 10 10 to 49 50 to 200 Not defined Canada (Industry Canada)4

0 to 4 5 to 19 20 to 499 500 and over

UK (DTI)5 0 to 9 10 to 49 50 to 249 250 and over PROGRAMME DEFINITIONS

EU/EBRD Facility 10 or less 50 or less 250 or less Not defined US/EBRD Facility 20 or fewer 100 or fewer 250 or fewer Not defined OTHER DEFINITIONS BEEPS6 Not defined 2 to 49 50 to 249 250 and over ‘Spotlight on SEE’7 Less than 10 10 to 49 Less than 250 Not defined

ADDITIONAL MEASUREMENT CRITERIA Micro Small Medium European Commission - either Turnover or Balance sheet total

≤ € 2 million ≤ € 2 million

≤ € 10 million ≤ € 10 million

≤ € 50 million ≤ € 43 million

IFC – either Annual sales or Total assets

$100k or less $100k or less

> $100k <$3mm > $100k <$3mm

$3mm to $15mm $3mm to $15mm

LOAN SIZE DEFINITIONS

Micro Small Medium EU/EBRD Facility Less than €30k Less than €125k

US/EBRD Facility Up to $20k Up to $100k (exceptionally $125k)

Up to $500k

A microlending methodology Less than $10k >$10k <$50k >$50k

1 The EC also sets Turnover and Sales limits and an ‘independence criterion’ to ensure that enterprises which are part of a larger grouping and could therefore benefit from a stronger economic backing than genuine SMEs, do not benefit from SME support schemes. 2 Source: IFC 2004 Annual Review – Small Business Activities. 3 Source: “Small and Medium Enterprises across the Globe: A New Database”, World Bank Policy Research Working Paper 3127, August 2003. 4 “Small and Medium-Sized Enterprise (SME) Financing in Canada”, Industry Canada, 2002. The report defines SMEs as “Firms with less than 500 employees and less than $50 million in annual revenues”. 5 Department of Trade and Industry 6 BEEPS = EBRD/World Bank Business Environment and Enterprise Performance Survey 7 “Spotlight on South-Eastern Europe. An overview of private sector activity and investment”, EBRD, April 2004

APPENDIX 2

EXAMPLES OF INDICATORS FOR THE ANALYSIS OF TRANSITION AND SOCIAL IMPACTS OF MSME OPERATIONS

In section 5.2 of the special study it is recommended that EBRD should devise a set of indicators to facilitate the measurement and analysis of transition and social impacts of MSME operations. Both quantitative and qualitative indicators are useful. The table below identifies some of the elements which should be considered in devising a set of indicators. It should be noted that these are examples only and that the list is not intended to be prescriptive or exhaustive. INSTITUTIONAL INDICATORS MEASURE INSTITUTIONAL CHANGE THROUGH

• Financial performance

• Management capacity

MEASURE MARKET PERFORMANCE THOUGH

• Client-based information

• Market penetration

EXAMPLES - Standard financial indicators - Financial impact of both explicit and implicit subsidies including ‘soft’ funding - Product profitability - Training of loan officers - Training in other banking and management skills - Local replacement of consultants and expatriate management - Market sector of client’s business - Time in business - Basic financial information (e.g. sales, fixed assets, profitability) - Employee numbers - Average loan size - Loan numbers and tenors (maturities) - Repeat borrowing patterns - Comparison with other lenders

Technical Cooperation: Where TC funds have been allocated, full details of the utilisation of funds should be reported on a regular basis. Information on consultant support to branches and business segments would assist monitoring processes and the assessment of value-for-money obtained from TC inputs.