Delivering value Delivering commitments - Ence presentation_ENG.pdfprice of wood pulp or wood, ......

27

Delivering value Delivering commitments December 2017

-

Upload

duongquynh -

Category

Documents

-

view

228 -

download

1

Transcript of Delivering value Delivering commitments - Ence presentation_ENG.pdfprice of wood pulp or wood, ......

Delivering value

Delivering commitments

December 2017

Disclaimer

The information contained in this presentation has been prepared by Ence Energía y Celulosa, S.A. (hereinafter, "Ence").

This presentation includes data relating to future forecasts. Any data included in this presentation which differ from other data based on historical information, including, in a merely expository manner, those which refer to the financial situation of Ence, its business strategy, estimated investments, management plans, and objectives related to future operations, as well as those which include the words "anticipate", "believe", "estimate", "consider", "expect" and other similar expressions, are data related to future situations and therefore have various inherent risks, both known and unknown, and possess an element of uncertainty, which can lead to the situation and results both of Ence and its sector differing significantly from those expressly or implicitly noted in said data relating to future forecasts.

The aforementioned data relating to future forecasts are based on numerous assumptions regarding the current and future business strategy of Ence and the environment in which it expects to be situated in the future. There is a series of important factors which could cause the situation and results of Ence to differ significantly from what is expounded in the data relating to future forecasts, including fluctuation in the price of wood pulp or wood, seasonal variations in business, regulatory changes to the electricity sector, fluctuation in exchange rates, financial risks, strikes or other kinds of action carried out by the employees of Ence, competition and environmental risks, as well as any other factors described in the document. The data relating to future forecasts solely refer to the date of this presentation without Ence being under any obligation to update or revise any of said data, any of the expectations of Ence, any modification to the conditions or circumstances on which the related data are based, or any other information or data included in this presentation.

The information contained in this document has not been verified by independent experts and, therefore, Ence neither implicitly nor explicitly gives any guarantee on the impartiality, precision, completeness or accuracy of the information, opinions and statements expressed herein.

This document does not constitute an offer or invitation to acquire or subscribe to shares, in accordance with the provisions of Royal Legislative Decree 4/2015, of 23 October, approving the consolidated text of the Securities Market Act. Furthermore, this document does not constitute a purchase, sale or swap offer, nor a request for a purchase, sale or swap offer for securities, or a request for any vote or approval in any other jurisdiction.

3

Ence at a glance A hidden value

Leading European eucalyptus pulp (BHKP) producer with close to 1.1 Mn tons of

installed capacity and largest Spanish renewable energy generator with agroforestry

biomass (170 Mw)

Superior eucalyptus pulp demand growth fuelled by tissue consumption mega-trend

(7.6% CAGR 2006-2016)

Strong competitive position in Europe: highly efficient facilities, just in time service and

differentiated offering

Solid earnings secured by stable regulation in the biomass Energy business

Powerful and recurrent cash flow generation: €92 Mn Recurrent Free Cash Flow in

9M17 and over €120 Mn expected for 2017

Solid balance sheet and strong liquidity: 1.0 Net Debt / EBITDA and € 250 Mn cash

available at 30 September 2017

Clear Strategic Plan 2016-2020 on track aiming at doubling EBITDA and increasing its

resiliency through investments in both the Pulp and Energy businesses

Supportive shareholder base with strong entrepreneurial track record

4

Supportive shareholder base With a strong entrepreneurial track record

Shareholding structure (30/09/2017) Board of directors

Juan Luis Arregui (Retos Operativos XXI), Chairman of the Board, founder of Gamesa

and former Vice Chairman of Iberdrola

Mr. Ignacio de Colmenares

CEO y Vice Chairman

Mr. Juan Luis Arregui

Chairman

Mr. Oscar Arregui

Mr. Javier Echenique

Mr. Pascual Fernández

Mr . Luis Lada

Mr . Jose Carlos del

Álamo

Mr. Fernando Abril-

Martorell

Mrs. Isabel Tocino

Mr. José Guillermo Zubía

Mr . Pedro Barato

Mr. Victor Urrutia

Mr. Jose Ignacio Comenge

*Treasury stock: updated September 2017

28,0%

6,3%

5,7%

5,5%0,6%

53,9%

Retos Operativos XXI, S.L. Asúa Inversiones S.L.

Fuente Salada S.L. Alcor Holding, S.A.

Treasury Stock Free float

- Mr. Victor Urrútia

- Mr. Jose Ignacio Comenge

- Mr. Juan Luis Arregui

5

Pulp & Energy Two complementary and isolated businesses

2016 EBITDA breakdown

• Leading European producer with c. 1.1

Mn tons of installed capacity

• Cyclical business largely dependent on

USD based global pulp prices

• Based on Ence`s wood supply

management expertise

• Strong operating know –how and efficient

facilities with c.60 years experience

• Leverage policy: maximum 2.5x Net Debt

/ EBITDA, long term capital market

financing and high liquidity

75% 25%

• Largest operator in Spain with 170 MW

of installed capacity

• Regulated business with high visibility and

attractive returns

• Based on Ence`s agroforestry biomass

supply management expertise

• Strong operating know –how and efficient

facilities with c.20 years experience

• Leverage policy: maximum 5.0x Net Debt /

EBITDA, non recourse bank project

financing and sufficient liquidity

Pontevedra

Navia

Huelva

Mérida

Facilities Location

Eucalyptus pulp production Biomass energy generation

Ciudad Real

Jaen

Taylor made management policy per business and ring fenced financing

Cordoba

6

Chemical Market Pulp industry 59 million tons in 2016

Ence is the leading European hardwood pulp producer with c. 1.1 Mn tons of installed capacity,

competing in the global Chemical Market Pulp industry

Total Paper Grade

fiber consumption

414 Mn Tons

Fiber Source Pulp Processing Integrated vs.

Market Pulp

Pulp Type

Recycled

fiber:

244 Mnt

Virgin Pulp:

170 Mnt Chemical:

142 Mnt

Mechanical:

28 Mnt

Source: RISI – Jan 2017; PPPC G-100 Dic 2016

Market:

59 Mnt

Integrated:

83 Mnt Softwood and

other:

27 Mnt

32 Mnt Hardwood

Chemical Market Pulp

industry

7

Hardwood pulp vs. Softwood pulp Eucalyptus pulp is cheaper to produce than softwood pulp

Most hardwood pulp comes from eucalyptus wood

Best suited for paper products with high smoothness,

opacity and uniformity (i.e. tissue)

Softwood pulp (BSKP)

Eucalyptus only grows under very specific climate conditions, usually in warm subtropical regions.

More abundant pines are better adapted to cold climates

Low production cost High production cost

Substitutive

materials

80%

of final paper

products allow

for different

proportions of

both pulp

types

Hardwood pulp (BHKP)

Forestry yield: 12 – 18 m3 / ha / year

Harvesting cycle: 12 - 15 years

Industrial yield: 2.6 – 3.0 m3 / ton of pulp

Iberian Globulus

Most softwood pulp comes from pine wood

Best suited for paper requiring higher durability and

strength (i.e. printing & writing)

Forestry yield: 2 – 4 m3 / ha / year

Harvesting cycle: 50 - 70 years

Industrial yield: 4.8 - 5.2 m3 / ton of pulp

Nordic Scots pines

8

Tight global Market Pulp supply and demand balance Global demand reached 94% of capacity in 2016

China, Europe and North America are net importers of hardwood pulp (BHKP)

2

20

3

Demand Supply

3

Rest of the World

6 7

7 3

Demand Supply

13 10

Softwood pulp (BSKP)

Hardwood pulp (BHKP)

Source: RISI – Jan 2017; Hawkins Wright - Dec 2016; PPPC G-100 - Dic 2016

China

11

8

Demand

19

Western Europe

9 4

7

8

Supply

12

South America

23

4 2

4 14

Demand Supply

North America

8

16

(Mn Tons)

Demand

16

Supply

2

9

Superior demand growth for Eucalyptus pulp Which is leading global market pulp demand growth

Last 10 years total market pulp demand evolution

0

5

10

15

20

25

30

35

40

45

50

55

60

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BSKP: + 1.3% CAGR

The more efficient and best suited eucalyptus pulp is gaining market share against other hardwood and softwood pulp,

following a demand increase of over 10 Mn tons in the last 10 years

Source: PPPC G-100

BHKP: + 3.6% CAGR

+ 2.1% CAGR Mn tons

Last 10 years hardwood pulp demand evolution

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BEKP: + 7.6% CAGR

Source: PPPC G-100

Mn tons

Other BHKP: - 2.4% CAGR Other : - 4.9% CAGR

10

Fuelled by tissue consumption mega-trend Linked to increasing living standards in developing countries

24

15 15

11

6 5 5

3 1 1 0,1

NorthAmerica

WesternEurope

Japan Oceania Latam EasternEurope

China MiddleEast

OtherAsia

Africa India

Tissue paper per-capita consumption (kg/year)

85% of world population 15%

59% of Ence pulp sales are oriented to the fastest

growing tissue market, which has increased by

c.10 Mn tons in the last 10 years

3,0%

2,5%

1,5%

-1,4%

-4,6%

-5,0% -3,0% -1,0% 1,0% 3,0%

End global paper market demand growth

(CAGR 2005 – 2015)

Tissue

Specialties

Packaging

P&W

Newsprint

Ence 2016 pulp sales by end paper market

Packaging: 2%

Tissue: 59% Specialties: 31%

P&W: 8%

Source: RISI

Source: RISI

11

High demand growth requires pulp capacity additions But there are no new large project starts expected for next 3 years

Tight global supply and demand balance should be maintained in the coming years

Eucalyptus pulp annual demand and supply increase

(2013 – 2016)

Source: Ence estimates Source: PPPC G-100; PPPC SRN Feb 2017

1,3

1,6

1,1

1,7

1,4

0,8

1,3 1,3 1,3 1,2

0,0

0,5

1,0

1,5

2,0

2,5

2013 2014 2015 2016 Average

Demand Supply

Mn Tons

Expected hardwood pulp annual supply and demand increase

(2017 – 2020)

1,4

1,6

1,4 1,4 1,5

0,3

1,0

-0,3 -0,5

0,1

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

2017E 2018E 2019E 2020E Average

Demand Supply

Mn Tons

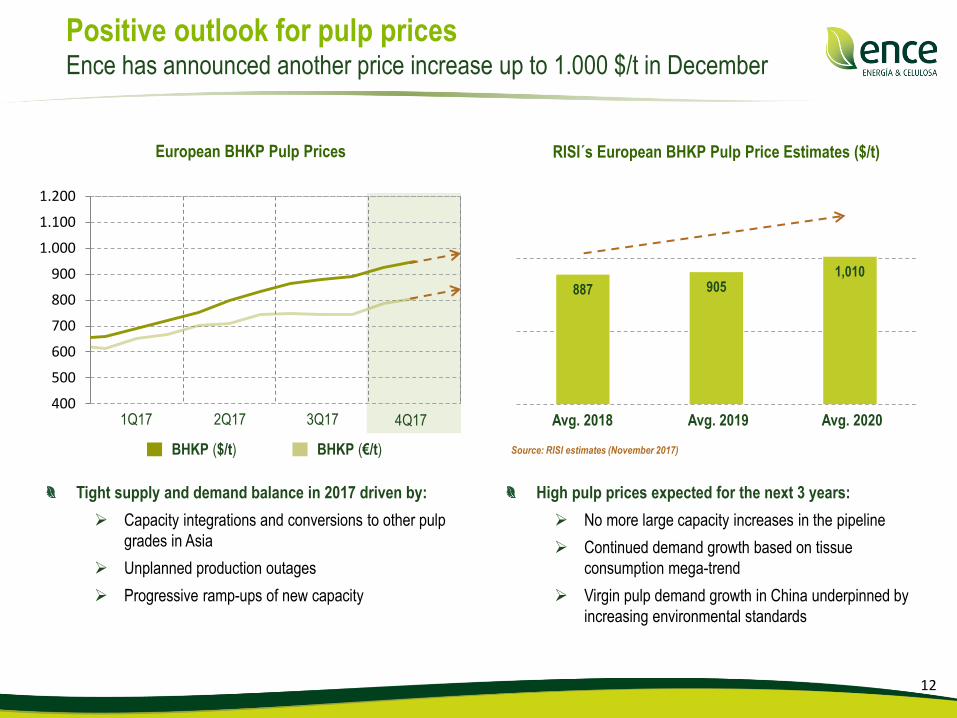

887 905 1,010

Positive outlook for pulp prices Ence has announced another price increase up to 1.000 $/t in December

12

European BHKP Pulp Prices RISI´s European BHKP Pulp Price Estimates ($/t)

Tight supply and demand balance in 2017 driven by:

Capacity integrations and conversions to other pulp

grades in Asia

Unplanned production outages

Progressive ramp-ups of new capacity

High pulp prices expected for the next 3 years:

No more large capacity increases in the pipeline

Continued demand growth based on tissue

consumption mega-trend

Virgin pulp demand growth in China underpinned by

increasing environmental standards

BHKP ($/t) BHKP (€/t)

1Q17 2Q17 3Q17

Source: RISI estimates (November 2017)

400

500

600

700

800

900

1.000

1.100

1.200

4Q17 Avg. 2018 Avg. 2019 Avg. 2020

Increased market tightening in the long run No new large project starts expected for next 3 years

13

Source: ENCE estimates

Expected Annual Increase for Global Market Hardwood Supply and Demand (Mn t) 1

Continued demand growth based on

global tissue consumption mega-trend

Virgin pulp demand growth in China

underpinned by increasing environmental

standards

No new large project starts expected for

next 3 years

Ongoing capacity conversions to other

pulp grades

Recurring unplanned production outages

1) Estimates correspond to the expected increase in supply and demand of market pulp for paper production. It excludes therefore the production of integrated pulp and other pulp grades such as Dissolving Pulp or Fluff

Mn t 2017 2018 2019 2020 2017 - 2020

ESTIMATED BHKP DEMAND INCREASE 1,4 1,6 1,4 1,4 5,8

China 1,0 1,1 1,0 1,0 4,1

Other Asia / Africa / Oceania / Middle East 0,2 0,2 0,2 0,2 0,8

Europe 0,0 0,1 0,1 0,1 0,3

North America 0,0 0,1 0,0 0,0 0,1

Latin America 0,1 0,1 0,1 0,1 0,4

ESTIMATED BHKP SUPPLY INCREASE 0,3 1,0 -0,3 -0,5 0,5

APP (OKI) 1,2 0,6 0,2 0,2 2,2

FIBRIA (TRES LAGOAS) 0,5 1,4 1,9

FIBRIA (ARACRUZ) -0,1 -0,2 -0,3

KLABIN (PUMA) 0,5 0,5

SUZANO (IMPERATRIZ, MUCURI & MARANHAO) -0,1 0,3 0,2

ENCE (NAVIA & PONTEVEDRA) 0,1 0,1 0,2

METSA (AANEKOSKI) 0,1 0,1

UPM (KYMI) 0,1 0,1

CMPC (GUAIBA) -0,6 0,6 0

TAIWAN P&P and RFP (Calhoun) -0,1 -0,1

ARAUCO (VALDIVIA) -0,1 -0,1

APRIL (RIZHAO)

APRIL (KERINCI)

OTHER UNEXPECTED CLOSURES / CONVERSIONS -0,2 -0,2 -0,2 -0,2 -0,8

SURPLUS / (DEFICIT) (1,1) (0,6) (1,7) (1,9) (5,3)

-1,0 -1,2 -0,6 -3,4-0,6

14

Softwood supply and demand will also remain balanced On continued demand growth and limited supply additions

Any new greenfield pulp project takes from 3 to 6 years to be completed

Expected Annual Increase for Global Market Softwood Supply and Demand (Mn t) 1

Mn t 2017 2018 2019 2017 - 2019

ESTIMATED BSKP DEMAND INCREASE 0,6 0,6 0,6 1,8

China 0,5 0,5 0,5 1,5

Other Asia / Africa / Oceania / Middle East 0,1 0,1 0,1 0,3

Europe 0,0 0,0 0,0 0,0

North America 0,0 0,0 0,0 0,0

Latin America 0,0 0,0 0,0 0,0

ESTIMATED BSKP SUPPLY INCREASE 0,4 0,5 0,3 1,2

METSA (AANEKOSKI) 0,1 0,6 0,7

SCA (OSTRAND) 0,1 0,4 0,5

SVETLOGORSKY (BELARUS) 0,2 0,1 0,3

SODRA (VARO) 0,2 0,2

DOMTAR (ASHDOWN + PLYMUTH) 0,1 0,1

IP (RIEGELWOOD) 0,1 0,1

CLEARWATER (LEWINSTON) 0,1 0,1

KLABIN (PUMA) 0,1 -0,1 0,0

STORA (SKUTSKAR) -0,2 -0,2

OTHER UNEXPECTED CLOSURES / CONVERSIONS -0,2 -0,2 -0,2 -0,6

BALANCE 0,2 0,1 0,3 0,6

BSKP supply and demand will also remain

balanced for the coming years

BSKP prices in Europe have recovered over

$80/t since the beginning of the year

1) Estimates correspond to the expected increase in supply and demand of market pulp for paper production. It excludes therefore the production of integrated pulp and other pulp grades such as Dissolving Pulp or Fluff.

Source: ENCE estimates

15

New capacity managed by incumbents In a concentrated supply market

Softwood pulp (BSKP) global market share

Top 10 softwood pulp producers account for 65% of

global BSKP market share

Hardwood pulp (BHKP) global market share

Source: RISI 2016 Source: RISI 2016

International Paper:

12%

Koch Ind.: 9%

Arauco: 7%

Paper

Excellence: 6% Sodra: 5%

All other: 36% Fibria +

Klabin: 19%

APRIL: 11%

Suzano: 10%

CMPC: 9%

Arauco: 6% El dorado:

5%

All other: 29%

UPM: 5%

Cenibra: 3%

Ence: 3%

Mercer: 6%

Ilim: 5%

Stora: 4%

Top 10 hardwood pulp producers account for 74% of

global BHKP market share

Altri: 3%

Domtar: 5%

Metsa: 6%

16

Iberian pulp is the most competitive in Europe

Narrowing the gap with Latams and widening it with Nordics

-

50

100

150

200

250

300

350

400

450

500

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

80% of softwood pulp demand could be substituted with hardwood pulp

Estimated delivered cash cost

for the European pulp market

€ / Ton

Mn Tons

Source: Hawkins Wright (August 2017)

At current exchange rates:

• 1,2 $/€

• 3,1 BRL/$

Western European Pulp Market:

16 Mn Tons

BSKP

BHKP

Source: RISI, EPIS, Ence

Demand Source

7

9

7

2

5

260

330 368

397

2

LATAM

(BHKP)

IBERIA

(BHKP)

NORTHERN.EUR

(BSKP)

NORTHERN.EUR

(BHKP)

Mn Tons

17

Ence has well located and highly efficient facilities

Focused on cash cost reduction

Ence is already the most competitive pulp producer in Europe

Ence Current and Expected Cash Cost Reduction

2014a 2015a 2016a 1H17a 2017e 2018e 2019e 2020e

405.6

359.0 356.7

339 337 329

325

STRATEGIC PLAN 1

344.5

1) Under a conservative assumption of 720 $/t pulp price and 1.25 $ exchange rate

18

Just in time service and differentiated offering Ence key competitive advantages in the Pulp business

Just in time service

High client diversification

> 100 customers

JIT short shipping

deliveries (5-7 days)

Smaller coastal vessels

De-commoditized products

TCF + ECF qualities

7 de-commoditized products

High White

High Porosity

Low Fibre Bundles

High Softness High Bulk

Low Energy Refining

High Stability

Premium

Pulp

50 days / 36€/t

JIT deliveries and de-commoditized products strengthen Ence's positioning among its diversified client base

1

1,05

1,1

1,15

1,2

1,25

1,3

1,35

1,4

31-12-12 31-12-13 31-12-14 31-12-15 31-12-16 31-12-17 31-12-18

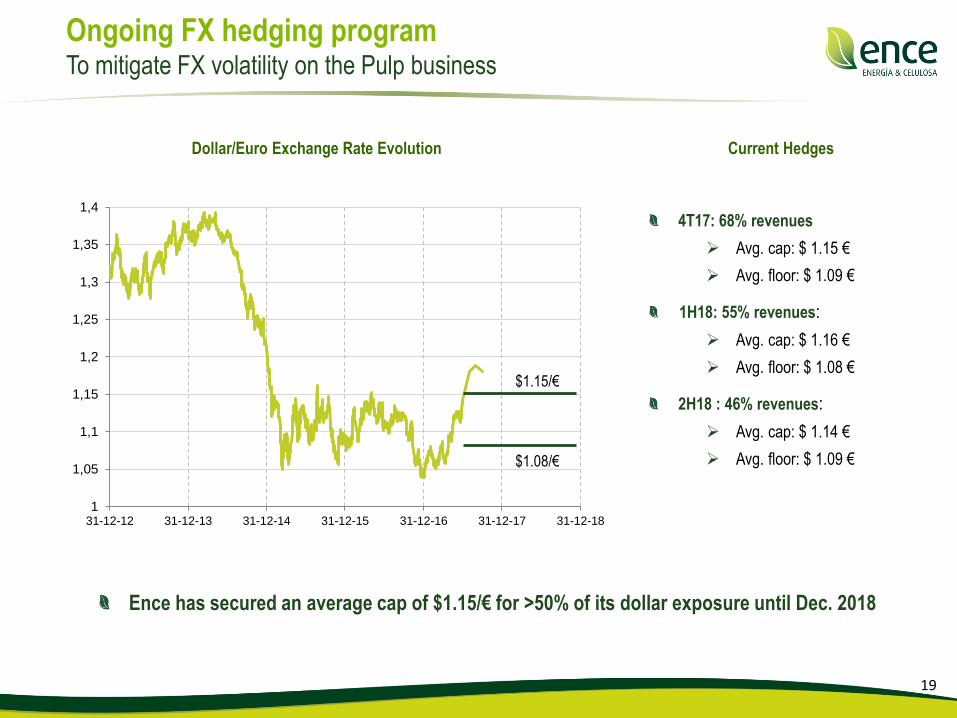

Ongoing FX hedging program To mitigate FX volatility on the Pulp business

19

$1.15/€

$1.08/€

4T17: 68% revenues

Avg. cap: $ 1.15 €

Avg. floor: $ 1.09 €

1H18: 55% revenues:

Avg. cap: $ 1.16 €

Avg. floor: $ 1.08 €

2H18 : 46% revenues:

Avg. cap: $ 1.14 €

Avg. floor: $ 1.09 €

Ence has secured an average cap of $1.15/€ for >50% of its dollar exposure until Dec. 2018

Dollar/Euro Exchange Rate Evolution Current Hedges

20

Ence is also the largest agroforestry biomass player in Spain With 170 MW of installed capacity

Ciudad Real 16 Mw

Jaen 16 Mw

Mérida 20 Mw

Huelva 50 Mw

Huelva 41 Mw

Current estimated annual EBITDA of €50 Mn

Cordoba 27 Mw

21

Energy business earnings secured by stable regulation Strengthening the resiliency of Ence´s business model

104 104 104

94 94 94

0

20

40

60

80

100

120

2017 2018 2019

Average Cap Average Floor

€ / Mwh

Regulated price collar 2017-2019

(regulated pool price + Ro)1

Continued cost cutting initiatives to offset the small effect of a lower Regulated IRR from 2020

1 Includes regulated pool price collar + average remuneration for the operation of our plants (Ro) of €57 /MWh

Low exposure to regulated return on investment

(Regulated IRR)

7.4%

5.5%

Current Ri 2020 Worst CaseScenario

- €3.8 Mn EBITDA

Our worst case scenario is an Regulated IRR based on a

regulated return of 5.5% from 2020

EBITDA impact of just 3.8 Mn€ for our 6 operating plants and new Huelva project (without Regulated IRR)

Regulated electricity price plus the remuneration for the

operation (Ro) to cover all the operating costs of a

standard plant

22

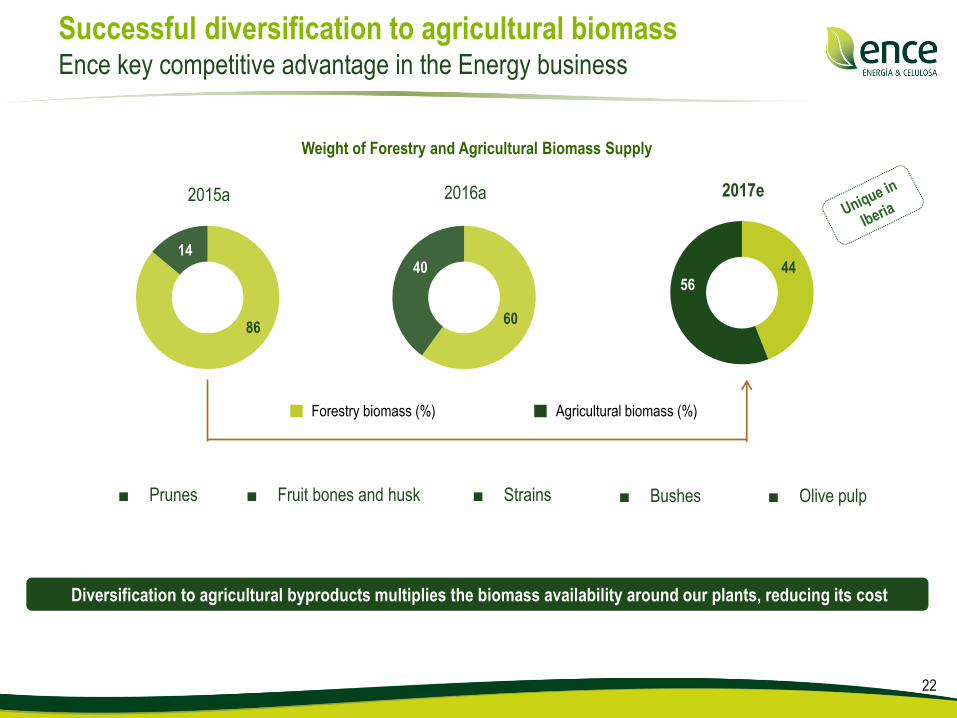

Successful diversification to agricultural biomass Ence key competitive advantage in the Energy business

Weight of Forestry and Agricultural Biomass Supply

Diversification to agricultural byproducts multiplies the biomass availability around our plants, reducing its cost

86

14

60

40 44 56

2015a 2016a 2017e

Forestry biomass (%) Agricultural biomass (%)

■ Fruit bones and husk ■ Strains ■ Bushes ■ Prunes ■ Olive pulp

2015 2016 2017e

€120 Mn

23

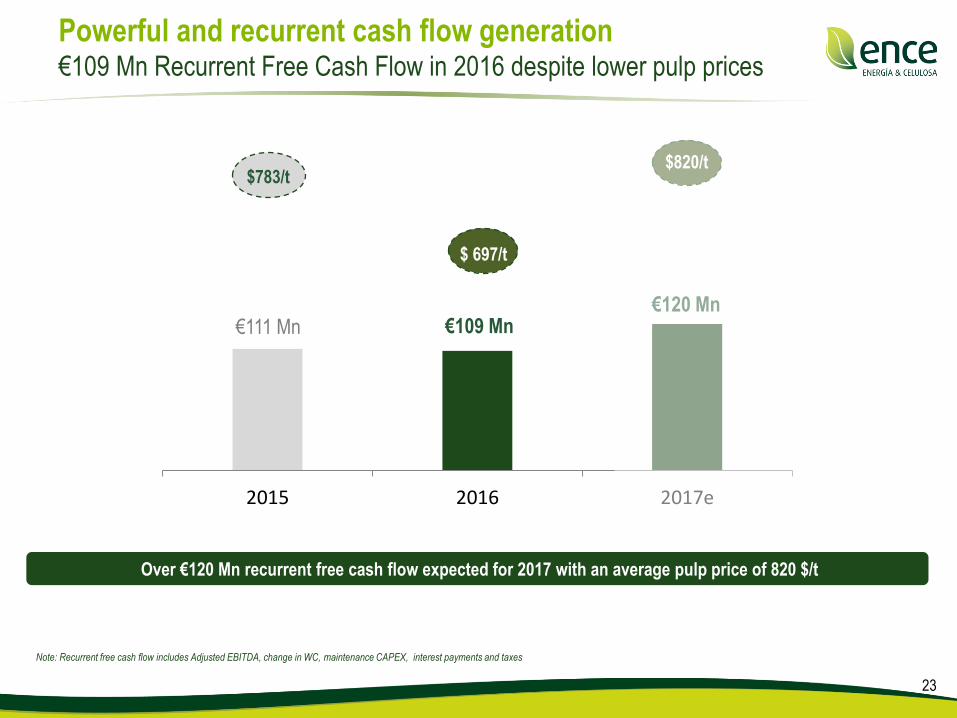

Powerful and recurrent cash flow generation €109 Mn Recurrent Free Cash Flow in 2016 despite lower pulp prices

$783/t

$ 697/t

Note: Recurrent free cash flow includes Adjusted EBITDA, change in WC, maintenance CAPEX, interest payments and taxes

€111 Mn €109 Mn

Over €120 Mn recurrent free cash flow expected for 2017 with an average pulp price of 820 $/t

$820/t

24

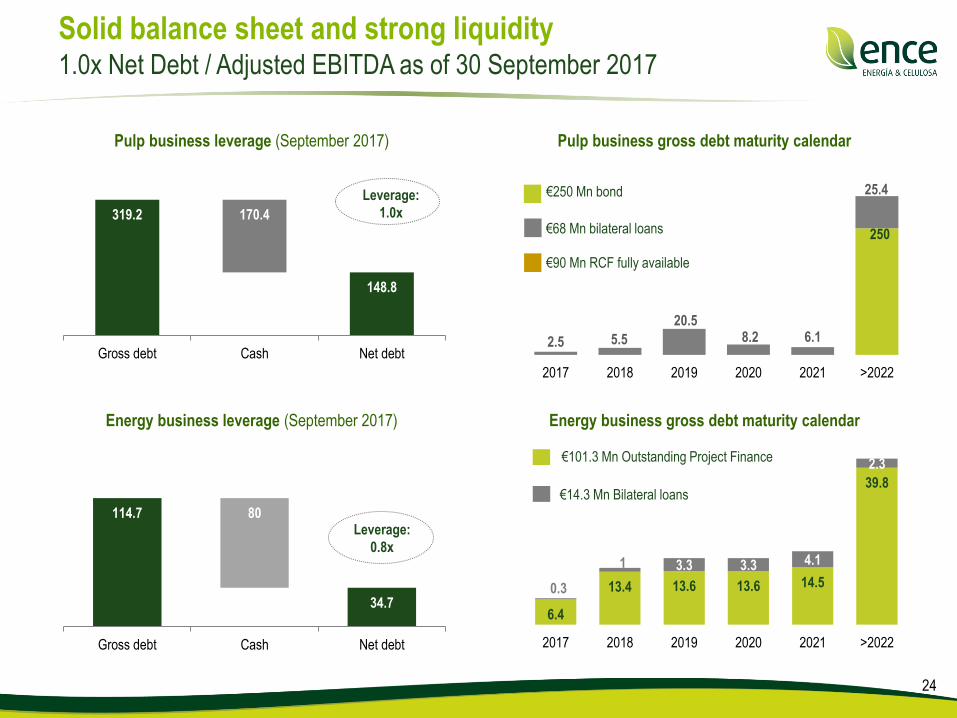

Solid balance sheet and strong liquidity 1.0x Net Debt / Adjusted EBITDA as of 30 September 2017

Pulp business leverage (September 2017) Pulp business gross debt maturity calendar

Energy business leverage (September 2017) Energy business gross debt maturity calendar

Leverage:

0.8x

Leverage:

1.0x

€250 Mn bond

€68 Mn bilateral loans

€101.3 Mn Outstanding Project Finance

€14.3 Mn Bilateral loans

€90 Mn RCF fully available

319.2

148.8

170.4

Gross debt Cash Net debt

250

2.5 5.5

20.5 8.2 6.1

25.4

2017 2018 2019 2020 2021 >2022

114.7

34.7

80

Gross debt Cash Net debt

6.4

13.4 13.6 13.6 14.5

39.8

0.3

1 3.3 3.3 4.1

2.3

2017 2018 2019 2020 2021 >2022

Next steps for the Pulp business 150,000 t capacity expansion in 2018 - 2019 aiming at €22 Mn EBITDA growth 1

25

70,000 t capacity expansion

in Pontevedra between 2018 and 2019

During 1Q17 maintenance downtime in Pontevedra, we have

prepared 30,000 t capacity expansion that will be completed

during March 2018 annual maintenance downtime

Additional 40,000 t expansion in Pontevedra between 2018

and 2019 maintenance downtimes

80,000 t capacity expansion

in Navia between 2H18 and 1H19

2015 a 2016 a 2017e 2018e 2019e 2020e Total

Net Capex (€ Mn) 2 -2 -1 35 41 52 -8 117

Production sold (000, t) 898 931 972 991 1,040 1,120

Cash cost (€/t) 358 357 339 337 329 325

Pulp Business Strategic Plan Summary (at 720 $/t pulp price and 1.25 $ exchange rate)

Between winter 2018 and spring 2019, we will expand

capacity by 80,000 t in Navia

Total capacity expansion will be done with just one

shutdown

1) €22 Mn EBITDA growth vs 2017 resulting from 150,000 t capacity expansion, under a conservative assumption of 720 $/t pulp price and 1.25 $ exchange rate

2) After non core forestry assets Divestment Plan

Next steps for the Energy business New Huelva 40 Mw power plant pushing annualized EBITDA up to €61 Mn

New Huelva 40 Mw biomass power plant

New Huelva 40 Mw biomass power plant project on

track to start up in 2H 2019

€11 Mn annual EBITDA target, without regulated IRR

EPC closed in July and early works agreed in October

Synergies with our 50 Mw and 41 Mw plants already

operating in the same location

Capex: €87 Mn

Financing: 60%

Currently analyzing opportunities to accelerate the Energy business growth through

acquisitions in Spain and Europe to reach an EBITDA target of €78 Mn by 2020

26

Acquisition date: December 2016

EV: €34 Mn (€22 Mn for Ence stake)

2016 EBITDA: €5.5 Mn

2017 Expected EBITDA: €7.5 Mn

Acquisition date: August 2017

EV: €29 Mn (€26 Mn for Ence stake)

2016 EBITDA: €4 Mn

2017 Expected EBITDA: €5 Mn

Successful M&A track record

Delivering value

Delivering commitments