Ashiana Housing - A Shareholder Friendly Real Estate Business Model

Delivering Real Shareholder Value:Analysis of Leading Performance in the Automotive Supply Base

December 2013

© 2013 Deloitte Consulting GmbH

Introduction & Auto Industry Analysis

“Top Performers” in Total Shareholder Value Creation

Winning Themes of Top Performers and Examples

Delivering Real Shareholder Value:

Analysis of Leading Performance in the Automotive Supply Base

1 Delivering Real Shareholder Value

© 2013 Deloitte Consulting GmbH

The combined strengths and recognition as market leaders allows Deloitte and IHS to

deliver deep insights and perspectives on how suppliers can improve performance

Delivering Real Shareholder Value2

Deloitte and IHS Partnering Together to Bring Their Collective Strengths to the Table

• Largest professional services firm globally with > 200.000 professionals and $32b USD in revenues

• Recognized by independent analysts as the leader in consulting services focused on strategy, operations management, IT, HR, and financial consulting

• Unmatched ability to bring professionals from various regions and technical disciplines (e.g., tax, consulting, enterprise risk management, etc.) in serving our clients

• Global Manufacturing practice comprised of more than 750 partners and 12,000 industry professionals in over 45 countries

• Teams of automotive specialists based in critical automotive markets around the world, including Beijing, Detroit, Munich, Nagoya, Nashville, Sao Paulo, Seoul, Shanghai, Stuttgart, Sydney, Tokyo, and Torino

About Deloitte

• 6,700 professionals serving 165 countries and speaking 50 languages

• Recognized as the leader in providing macroeconomic forecasts that are the most consistently accurate in the world.

• Interconnected information, expertise and analytics across industries and workflows

• Expert insight and analysis based on comprehensive foundational information

• Deep expertise on key challenges and issues across the globe

• Best-in-class solutions across workflows and industry value chains

About IHS

© 2013 Deloitte Consulting GmbH

While shifting production capacity to Asia is ongoing, diversification, consolidation

and change of business model driven by eMobility become increasingly important

Delivering Real Shareholder Value3

Trends in European Automotive Supply Base Industry

• The propulsion segment is dominated by the trend to downsize powertrains while increasing output.

• The trend towards electrification while present, maybe somewhat overstated.

Regional shifts

Technology

Suppliers

Financing & Investing

Competition

New powertrains

•Managing capital investments will become key for suppliers due to a growing need for flexibility in production capacity and footprint

•OEMs driving global mega-platforms:‒ 70% production volume on

mega-platforms by 2020‒ Getting in on leading-edge

platforms critical for suppliers

‒ Capacity demand alignment crucial as demand patterns change

•Weak spots in the tier 2/3 level introduce risks to the value chain. Expected insolvencies will drive continued consolidation

•Suppliers beginning to develop non-automotive products in an effort to diversify

•Redefinition of mobility will give rise to new business models and competition

•Consumer demand shifts:‒ Growth patterns shifting: Smaller cars

packed with technology content, as well as different geographies

‒ Suppliers will need to adapt product portfolio to market and get global organically or inorganically

•Shifting of production capacity to Asia

• Increasing importance of strategic alliances, JVs and direct investments in emerging markets

Market development

© 2013 Deloitte Consulting GmbH

Global light vehicle output growth indicates a flatter curve until 2020 while the global

capacity utilization will continue to increase over the next 7 years

Delivering Real Shareholder Value4

0%

20%

40%

60%

80%

0

20

40

60

80

100

120

Em

erg

ing

Sh

are

Pro

du

cti

on

Mil Global LV Output

Developed Emerging Emerging %

2000

2010

2020

0% 20% 40% 60% 80% 100%

Global Segmentation

Small Mid-Size Large

Current Situation: Global Light Vehicle Output Growth 2010 - 2020

Insights

• Stronger production output growth expectations especially in the emerging markets will further reduce the European share in LV output

• However, reduction of the European share in the global LV output is expected to slow down beyond 2015

0

50

100

150

0%

20%

40%

60%

80%

100%

202020192018201720162015201420132012

Straight Uti Copy Production

Ca

pa

city

(m

io)

Util

iza

tion

ra

te

Global Capacity Utilization

© 2013 Deloitte Consulting GmbH

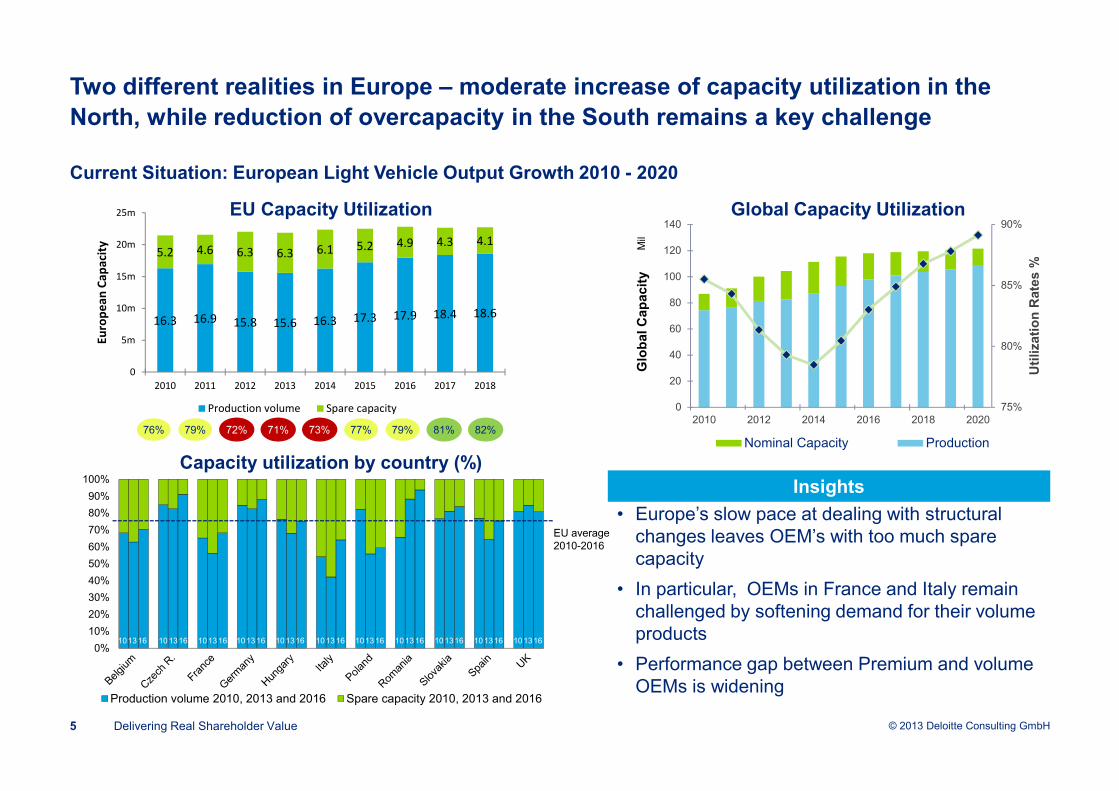

Two different realities in Europe – moderate increase of capacity utilization in the

North, while reduction of overcapacity in the South remains a key challenge

Delivering Real Shareholder Value5

75%

80%

85%

90%

0

20

40

60

80

100

120

140

2010 2012 2014 2016 2018 2020

Uti

lizati

on

Rate

s %

Glo

bal C

ap

acit

y

Nominal Capacity Production

Mil

77%76% 79% 72% 71% 73% 79% 81% 82%

16.3 16.9 15.8 15.6 16.3 17.3 17.9 18.4 18.6

5.2 4.6 6.3 6.3 6.1 5.2 4.9 4.3 4.1

0

5m

10m

15m

20m

25m

2010 2011 2012 2013 2014 2015 2016 2017 2018

Eu

rop

ea

n C

ap

aci

ty

Production volume Spare capacity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Production volume 2010, 2013 and 2016 Spare capacity 2010, 2013 and 2016

EU average 2010-2016

1013 16 10 1316 10 13 16 1013 16 10 1316 10 13 16 1013 16 10 13 16 10 1316 10 1316 10 1316

Insights

EU Capacity Utilization Global Capacity Utilization

Capacity utilization by country (%)

• Europe’s slow pace at dealing with structural changes leaves OEM’s with too much spare capacity

• In particular, OEMs in France and Italy remain challenged by softening demand for their volume products

• Performance gap between Premium and volume OEMs is widening

Current Situation: European Light Vehicle Output Growth 2010 - 2020

© 2013 Deloitte Consulting GmbH

Delivering Real Shareholder Value:

Analysis of Leading Performance in the Automotive Supply Base

6 Delivering Real Shareholder Value

Introduction & Auto Industry Analysis

“Top Performers” in Total Shareholder Value Creation

Winning Themes of Top Performers and Examples

© 2013 Deloitte Consulting GmbH

Our study analyzed 214 suppliers globally including 18 suppliers from Germany to

identify the “Top Performers” in the Automotive supply base

Delivering Real Shareholder Value7

Objective and Scope of Study

Objective

Scope

Analyze performance of global automotive supply base to identify themes that have generated superior shareholder value (SHV) over the last decade, as well as strategic and operational levers that have helped suppliers create shareholder value

Our study analysed 214 suppliers globally (>$500M in annual revenue,>$250M for German suppliers) and focused on trends by region, segment, and size of suppliers to understand performance and drivers of shareholder value over a 10-year period (2002-2012)

Regions # Suppliers

Japan 91

Europe 48

�Germany (18)

North America 43

China/India 18

Rest of World 14

Sizes # Suppliers

>$10B 28

$5B-$10B 31

$2B-$5B 58

$1B-$2B 53

<$1B 43

Segments # Suppliers

Electronics/Electrical

31

Powertrain 75

Chassis 65

Exteriors 46

Interiors/HVAC 39

© 2013 Deloitte Consulting GmbH

A systematic approach was used to analyze SHV1 performance to identify top

performers and derive strategic and operational levers for execution

Delivering Real Shareholder Value8

Study Approach

Who are the Winners?

Ap

pro

ac

hR

es

ult

An

aly

sis

How did they perform vs. the

rest of suppliers?

What droveperformance and

what were the winning themes?

What were the strategic and

operational levers for execution?

Identification of 60"Top

Performers" of the 214

suppliers analyzed

Analyze Total Shareholder Return (TSR) performance in last 10 (2002-2012) years to identify the "Top Performers"

6 winning themes by

which ‘theme leaders’

have exceled in the

marketplace

Correlate performance drivers to superior theme execution among "Top Performers" and identify winning themes and ‘theme leaders’

Identification of strategic

and operational levers

for execution

Deep dive ‘theme leaders’ and identify strategic and operational levers they used to execute on themes

1 Shareholder Value (SHV)

Performance assessment

of regional aspects in

connection with

segmental analysis

Analyze supplier financial performance across income statement, balance sheet and capital structure metrics

© 2013 Deloitte Consulting GmbH

Auto suppliers (in scope) have outperformed their respective regional indices on TSR,

except in China / India, with the German suppliers doing very well compared to DAX

Delivering Real Shareholder Value9

Total Shareholder Return (TSR) Performance

-

200

400

600

800

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Japan

Nikkei

Suppliers

-

200

400

600

800

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Europe / Germany

Suppliers Europe

Suppliers Germany

Stoxx 50

Dax

-

200

400

600

800

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

China / India

Suppliers

BSE Sensex

Hang Seng

-

200

400

600

800

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

North America

Suppliers

S&P

© 2013 Deloitte Consulting GmbH

-60%

-40%

-20%

0%

20%

40%

60%

80%

020406080100120140

Suppliers1 have generated over $160 Billion in shareholder value in the last decade,

however, there is a significant value creation gap between high performers vs. others

Delivering Real Shareholder Value10

Shareholder Returns1 (2002 – 2012)

• Top publicly listed auto suppliers globally have created ~$160 billion in shareholder value over the last 10 years

• Relative to their own baseline, over a 10 year period

- The top third performers have cumulatively generated 449% in shareholder value

- The middle third have cumulatively generated 106%

- And the bottom third have destroyed 9% of the total shareholder value over the same period

• The findings imply that significant shareholder value premium has been generated by superior performance in the auto supply industry

1 10 Year Market Cap data only available for 120 suppliers; Source: Capital IQ, Deloitte Methodology

Top 1/3rdBottom 1/3rd

$89 B(449% cumulative)

($6 B)(-9%

cumulative)Middle 1/3rd

$78 B(106% cumulative)

Perc

ent M

ark

et C

ap C

hange (

2002 –

2012)

2002 Market Cap

$ 68 B $73 B $19 B

2012 Market Cap

$62 B $151 B $109 B

Change ($6 B) $78 B $89 B

Insights

© 2013 Deloitte Consulting GmbH

$275 $147

$33 $161

0

50

100

150

200

250

300

2002-2007 2007-2009 2009-2012 2002-2012

0

20

40

60

80

100

2002-2007 2007-2009 2009-2012 2002-2012

In total Automotive suppliers have recovered only 23% of the value lost during the

crisis, Top performers have recovered all of their lost market cap post-downturn

Delivering Real Shareholder Value11

Market Cap Change1 (2002 – 2012) in $ Billion

-10

0

10

20

30

40

50

60

2002-2007 2007-2009 2009-2012 2002-2012

-50

0

50

100

150

2002-2007 2007-2009 2009-2012 2002-2012

Source: Capital IQ, Deloitte Methodology

1 2009 is considered till the month of March – trough of S&P 500 Index, all other years are considered till the month of October

Pre-downturn Financial downturn

Post-downturn Overall

To

p 3

rdB

ott

om

3rd

Mid

dle

3rd

89

78

-6

• Automotive suppliers in aggregate recovered only 23% of the value lost during the financial downturn

• However, the top 3rd have recovered most of the value lost during the downturn, while the bottom third have continued to see a slight value erosion

Insights

+23%

+ 8 %

- 44 %

- 111 %

© 2013 Deloitte Consulting GmbH

0

5

10

15

20

25

NA Europe Japan China / India Rest of world

0

5

10

15

20

25

Chassis /Brakes

Powertrain Electrical /Electronics

Interiors /HVAC

Exteriors

Greater number of “Top Performers” aligned to Chassis and Powertrain, and a higher

percentage domiciled in emerging economies

12 (20%)

21 (35%)

13 (22%)

6(10%)

8(13%)

22(37%)

17(28%)

6(10%)

8(13%)

7(12%)

Total = 60

Top PerformersTotal = 60

Top Performers

Delivering Real Shareholder Value12

10%8%

18%

11%

5%7%

0%

4%

8%

12%

16%

20%

NA Germany Europe Japan China /India

Rest ofworld

InsightsShare of Top Performer from total figures

• A greater number of “Top Performers” can be found in the segments Chassis/ Breaks and Powertrain – low level of E/E top performers is surprising

• Europe hosts the most “Top Performers” followed by Japan. Nevertheless, China / India show a positive trend

Number of Suppliers by Segment and by Region

# of suppliers by segment # of suppliers by region

© 2013 Deloitte Consulting GmbH

Region Analysis: China, India and Emerging Markets suppliers with high Revenue

Growth and ROA. Germany’s major suppliers outperformed their European peers

Delivering Real Shareholder Value13

10-year Revenue Growth (CAGR) and Average ROA Performance

10 Year CAGR - Revenue Growth

Average Return on Assets (%)

-20,0%

-10,0%

0,0%

10,0%

20,0%

30,0%

40,0%

-5,0% -3,0% -1,0% 1,0% 3,0% 5,0% 7,0% 9,0% 11,0% 13,0% 15,0%

China / India Europe

NA Japan

Rest of World Germany

Insights

• Suppliers in China, India and Emerging Markets achieved higher than industry revenue growth with double-digit increases

• Japanese suppliers show comparable revenue growth with only few outliers and above average ROA figures

• US suppliers display a more fragmented picture with only a few top performers and below average overall figures

• European suppliers are centered around market averages on an overall basis with certain exceptions

• German suppliers outperformed their European peer group and excelled in the Electronics and Powertrain segments

10 Year Revenue (Median)

10 Year ROA (Median)

Japan 6.3% 8.8%

China / India 26.4% 7.8%

Europe 6.9% 6.5%

Germany 8.4% 6.8%

North America 4.6% 6.3%

RoW 21.0% 8.2%

Total 8.7% 6.3%

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

Segment Analysis – Powertrain: Performance of German Suppliers in comparison to

global competitors show only moderate growth level but strong ROA performance

Delivering Real Shareholder Value14

10-year Revenue Growth (CAGR) and Average ROA Performance

Insights

• Major automotive challenges in the coming decade are characterized by mandatory improvements in fuel efficiency, driven by increasingly stringent emission legislations that are impacting the Powertrain domain

• Engine downsizing, improving transmission efficiency, light-weighting, hybrid powertrains and increase engine management reliability/efficiency are the key trends being considered in the technology roadmap for the Powertrain domain

• The Powertrain segment is very attractive for future M&A activities. Overcapacity in the Powertrain domain is not estimated to be above the industry average. It is expected that M&A activity would be utilized to add to current product portfolio rather than to consolidate the market

10 Year CAGR - Revenue Growth

Average Return on Assets (%)

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

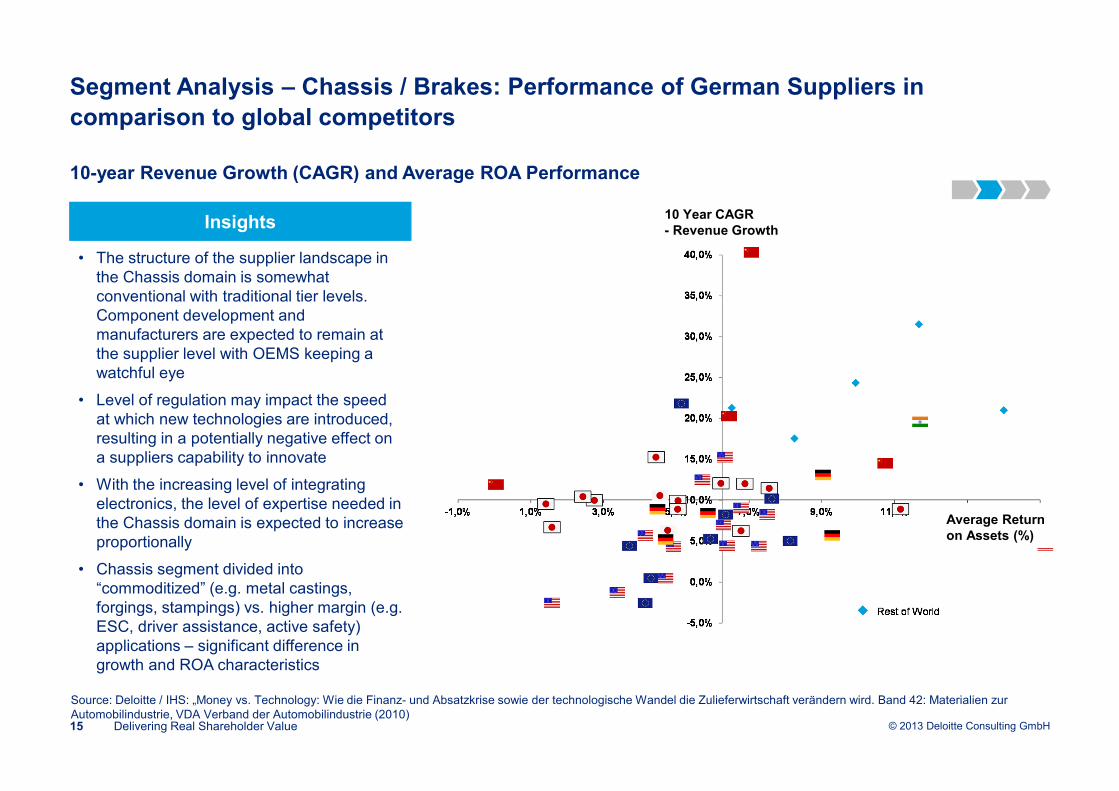

Segment Analysis – Chassis / Brakes: Performance of German Suppliers in

comparison to global competitors

Delivering Real Shareholder Value15

10-year Revenue Growth (CAGR) and Average ROA Performance

10 Year CAGR - Revenue Growth

Average Return on Assets (%)

Insights

• The structure of the supplier landscape in the Chassis domain is somewhat conventional with traditional tier levels. Component development and manufacturers are expected to remain at the supplier level with OEMS keeping a watchful eye

• Level of regulation may impact the speed at which new technologies are introduced, resulting in a potentially negative effect on a suppliers capability to innovate

• With the increasing level of integrating electronics, the level of expertise needed in the Chassis domain is expected to increase proportionally

• Chassis segment divided into “commoditized” (e.g. metal castings, forgings, stampings) vs. higher margin (e.g. ESC, driver assistance, active safety) applications – significant difference in growth and ROA characteristics

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

Segment Analysis – Electronics: Performance of German Suppliers in comparison to

global competitors show strong revenue growth, only second to India

Delivering Real Shareholder Value16

10-year Revenue Growth (CAGR) and Average ROA Performance

10 Year CAGR - Revenue Growth

Average Return on Assets (%)

Insights

• It is expected that about 80% of innovations will be made in electronics presenting this domain a significant potential for future growth and new innovations

• However, the ever-changing electronics world offers non- automotive suppliers the potential to enter the automotive industry triggering a higher level of competition for established suppliers

• Emergence of embedded software content creates significant disruption in the domain – new suppliers entering industry and capturing profit streams. Traditional suppliers struggling to “manage ecosystem”

• Low-cost electronics manufacturing traditionally based in Asia with local suppliers is expected to enter the European market in the short to medium term – mainly in hardware

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

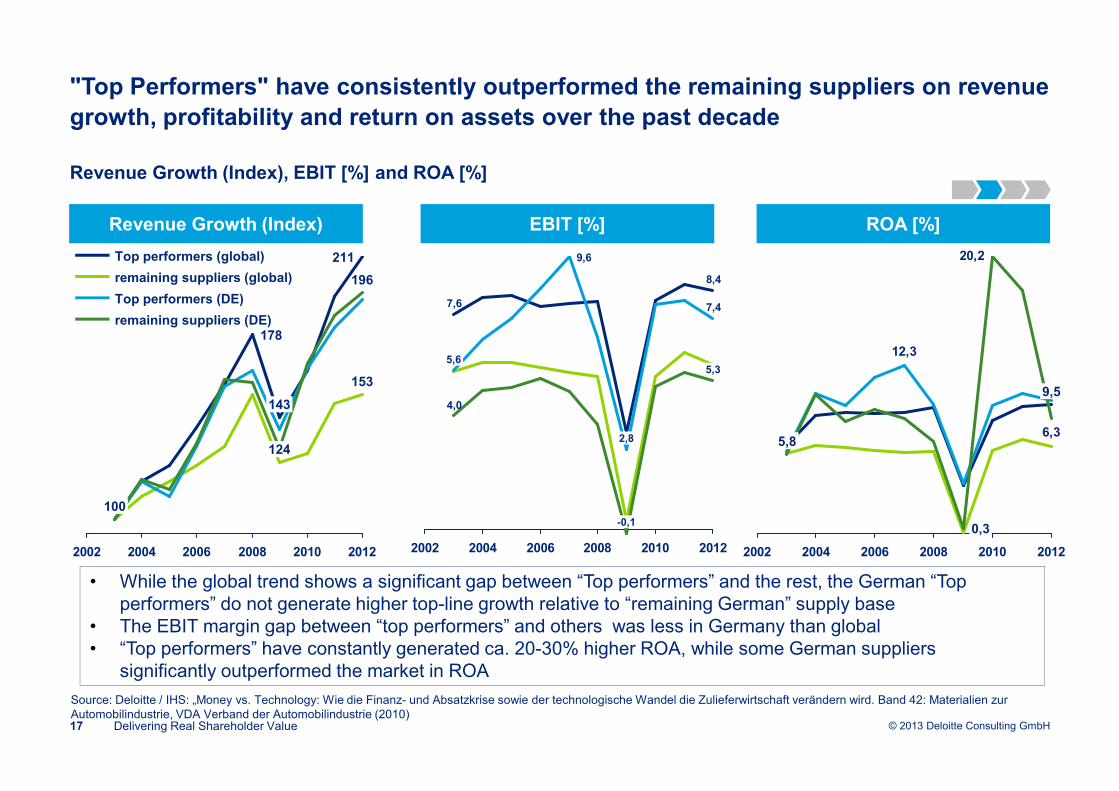

"Top Performers" have consistently outperformed the remaining suppliers on revenue

growth, profitability and return on assets over the past decade

Delivering Real Shareholder Value17

Revenue Growth (Index), EBIT [%] and ROA [%]

2002 2004 2006 2008 2010 2012

196

153

211

124

143

178

100

remaining suppliers (DE)

Top performers (DE)

remaining suppliers (global)

Top performers (global)

7,6

8,4

7,4

9,6

4,0

2002 2004 2006 2008 2010 2012

2,8

5,65,3

-0,1

6,3

12,3

20,2

2002 2004 2006 2008 2010 2012

5,95,8

9,5

0,3

Revenue Growth (Index) EBIT [%] ROA [%]

• While the global trend shows a significant gap between “Top performers” and the rest, the German “Top performers” do not generate higher top-line growth relative to “remaining German” supply base

• The EBIT margin gap between “top performers” and others was less in Germany than global• “Top performers” have constantly generated ca. 20-30% higher ROA, while some German suppliers

significantly outperformed the market in ROA

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

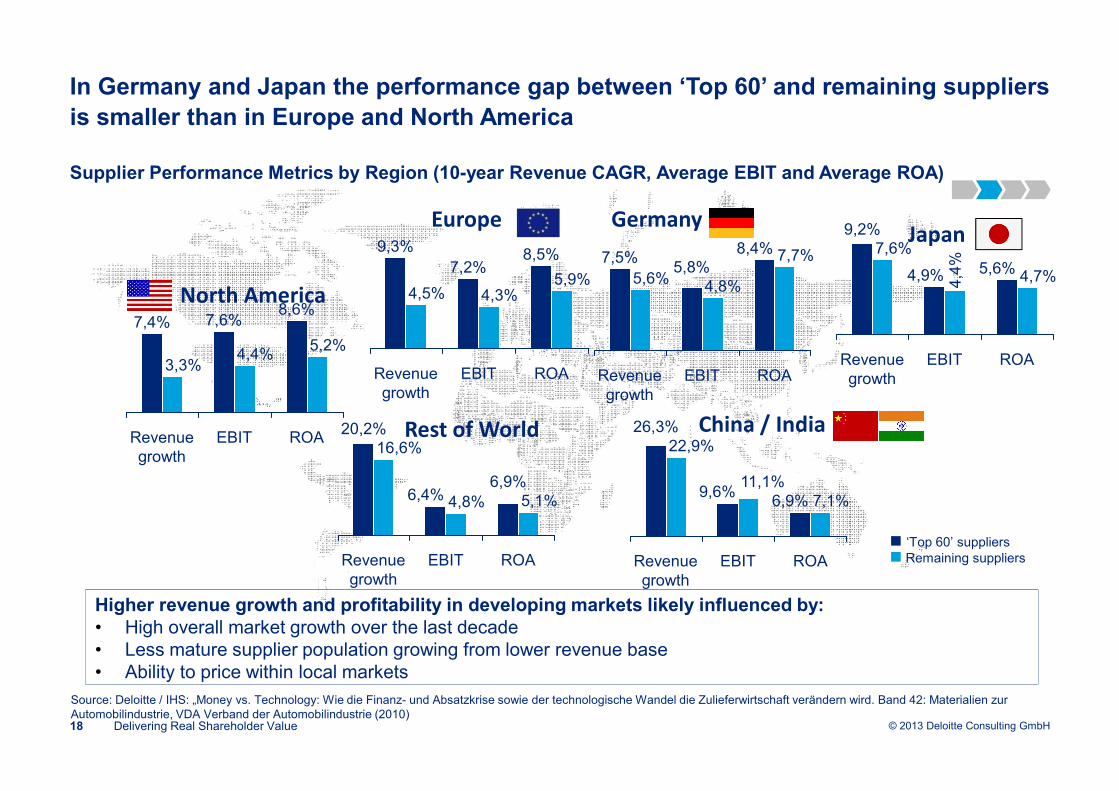

In Germany and Japan the performance gap between ‘Top 60’ and remaining suppliers

is smaller than in Europe and North America

Delivering Real Shareholder Value18

Supplier Performance Metrics by Region (10-year Revenue CAGR, Average EBIT and Average ROA)

Higher revenue growth and profitability in developing markets likely influenced by:• High overall market growth over the last decade• Less mature supplier population growing from lower revenue base• Ability to price within local markets

North America

EuropeJapan

China / IndiaRest of World

‘Top 60’ suppliersRemaining suppliers

Revenue growth

9,3%

EBIT

4,5%

7,2%

4,3%

8,5%

5,9%

ROA3,3%

7,4%

Revenue growth

7,6%

EBIT

4,4%5,2%

ROA

8,6%

4,8%

EBIT

6,9%5,1%

ROA

6,4%

Revenue growth

16,6%20,2%

ROA

4,7%5,6%

EBIT

4,4

%

4,9%

Revenue growth

7,6%9,2%

ROA

7,1%6,9%

EBIT

11,1%9,6%

Revenue growth

22,9%26,3%

Revenue growth

7,5%

EBIT

5,6%5,8%

4,8%

8,4% 7,7%

ROA

Germany

Source: Deloitte / IHS: „Money vs. Technology: Wie die Finanz- und Absatzkrise sowie der technologische Wandel die Zulieferwirtschaft verändern wird. Band 42: Materialien zur Automobilindustrie, VDA Verband der Automobilindustrie (2010)

© 2013 Deloitte Consulting GmbH

Delivering Real Shareholder Value:

Analysis of Leading Performance in the Automotive Supply Base

19 Delivering Real Shareholder Value

Introduction & Auto Industry Analysis

“Top Performers” in Total Shareholder Value Creation

Winning Themes of Top Performers and Examples

© 2013 Deloitte Consulting GmbH

Financial and operational metrics that drove superior performance among the 60 “Top

Performers” were analyzed and classified into “winning themes” that drove success

Delivering Real Shareholder Value20

Three Step Approach to Identify “Winning Themes”

Revenue GrowthPremium / Leading

edge platforms

Return on Capital

EmployedOperating Margins

Cash Conversion

CycleLiquidity

Leveraged Free

Cash Flow

Shareholder Value

Actions

Customer / Market

revenue mix

Regional revenue

mix

Gross Profit

Margin

Asset TurnoverR&D Turnover

Financial

Performance

Metrics

Operational

Performance

Metrics

Top Line Drivers

Bottom Line

Drivers

Capital Structure Drivers

Regress TSR against performance

metrics

STEP 1

Identify key performance drivers

STEP 2

Classify into winning themes and

identify “theme leaders”

STEP 3

© 2013 Deloitte Consulting GmbH

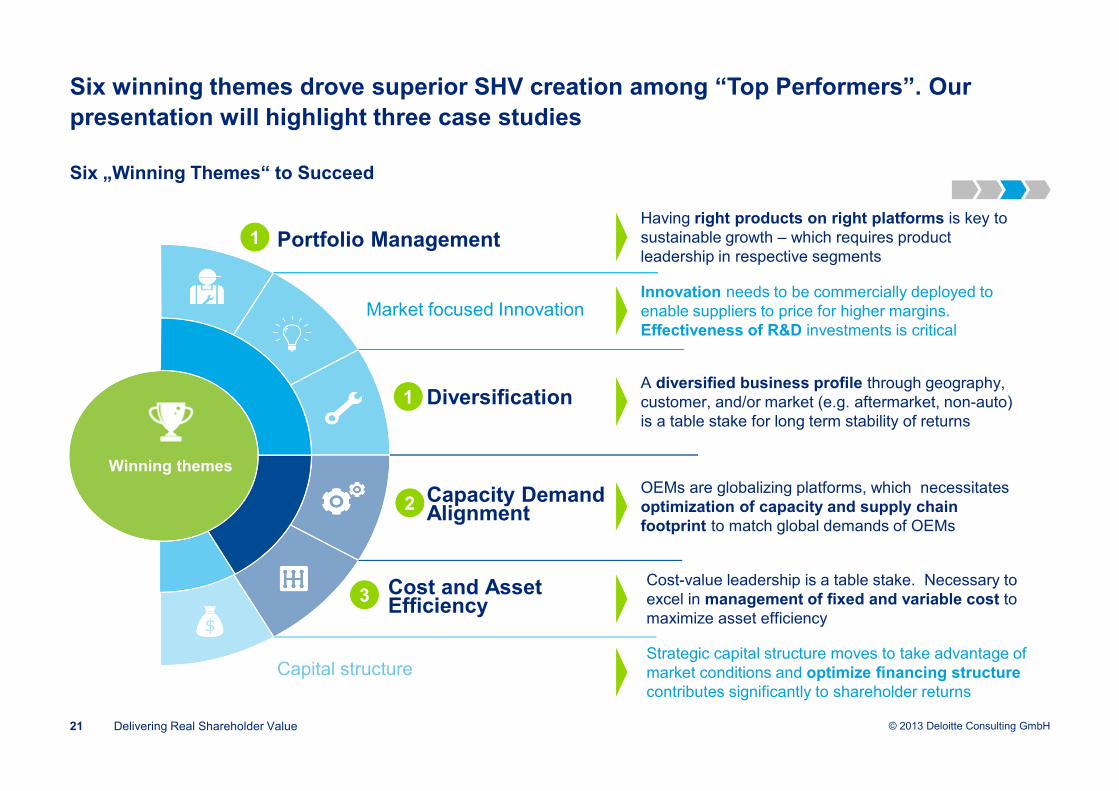

Winning themes

Six winning themes drove superior SHV creation among “Top Performers”. Our

presentation will highlight three case studies

Delivering Real Shareholder Value21

Six „Winning Themes“ to Succeed

Portfolio Management

Market focused Innovation

Diversification

Capacity Demand Alignment

Capital structure

Having right products on right platforms is key to sustainable growth – which requires product leadership in respective segments

Innovation needs to be commercially deployed to enable suppliers to price for higher margins. Effectiveness of R&D investments is critical

A diversified business profile through geography, customer, and/or market (e.g. aftermarket, non-auto) is a table stake for long term stability of returns

OEMs are globalizing platforms, which necessitates optimization of capacity and supply chain footprint to match global demands of OEMs

Strategic capital structure moves to take advantage of market conditions and optimize financing structure contributes significantly to shareholder returns

Cost and Asset Efficiency

Cost-value leadership is a table stake. Necessary to excel in management of fixed and variable cost to maximize asset efficiency

2

1

3

1

© 2013 Deloitte Consulting GmbH

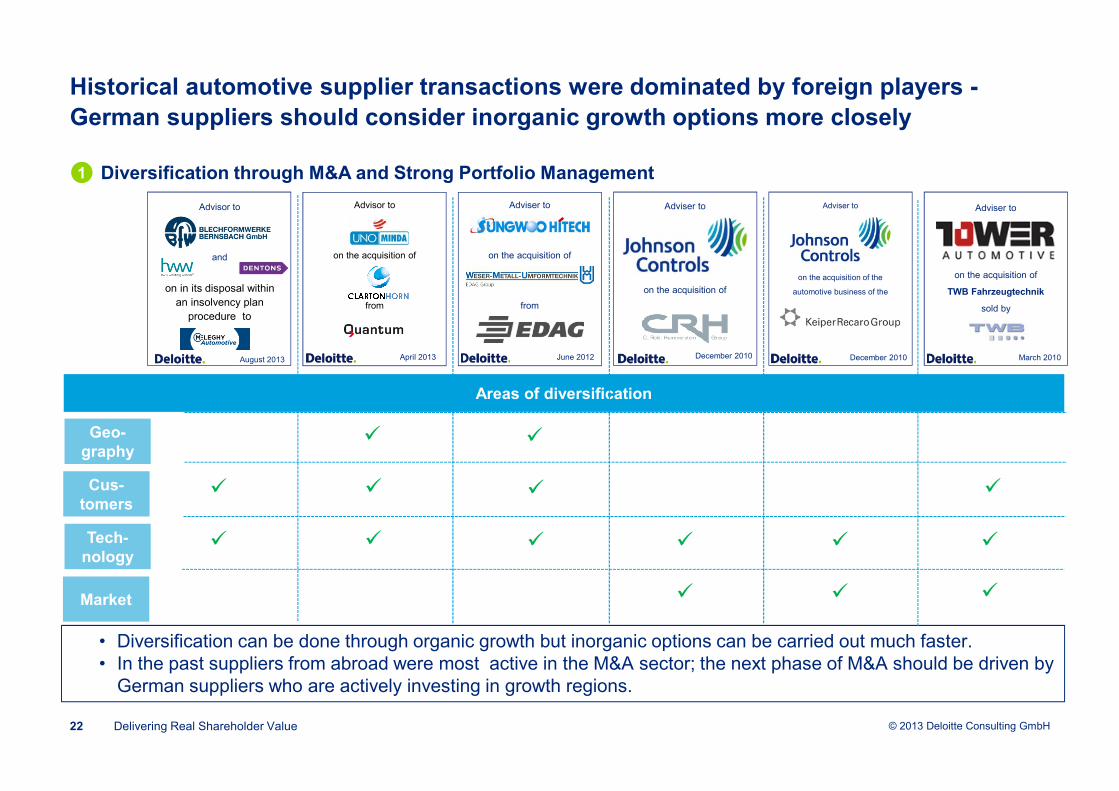

Historical automotive supplier transactions were dominated by foreign players -

German suppliers should consider inorganic growth options more closely

Delivering Real Shareholder Value22

Diversification through M&A and Strong Portfolio Management

June 2012

Adviser to

on the acquisition of

from

Adviser to

on the acquisition of

December 2010

Adviser to

on the acquisition of the

automotive business of the

December 2010

Adviser to

on the acquisition of

TWB Fahrzeugtechnik

sold by

March 2010August 2013

Advisor to

and

on in its disposal within an insolvency plan

procedure to

• Diversification can be done through organic growth but inorganic options can be carried out much faster.• In the past suppliers from abroad were most active in the M&A sector; the next phase of M&A should be driven by

German suppliers who are actively investing in growth regions.

Areas of diversification

Geo-graphy

Cus-tomers

Tech-nology

Market

�

�

�

�

�

�

��

��

�

�

April 2013

Advisor to

on the acquisition of

from

�

�

�

1

© 2013 Deloitte Consulting GmbH

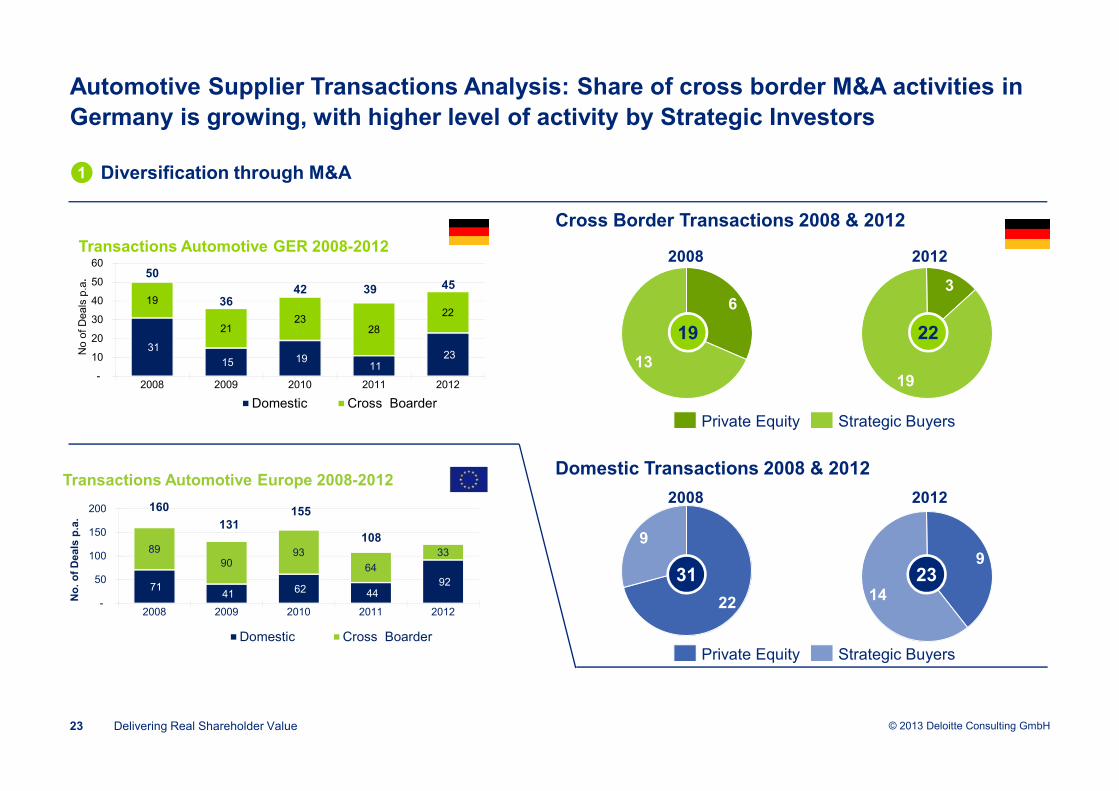

Automotive Supplier Transactions Analysis: Share of cross border M&A activities in

Germany is growing, with higher level of activity by Strategic Investors

Delivering Real Shareholder Value23

Diversification through M&A1

31

15 19 11

23

19

2123

28

22

-

10

20

30

40

50

60

2008 2009 2010 2011 2012

No o

f D

eals

p.a

.

Transactions Automotive GER 2008-2012

Domestic Cross Boarder

394236

4550

71 41 62 44

92

8990

93

64

33

-

50

100

150

200

2008 2009 2010 2011 2012

No

. o

f D

eals

p.a

.

Transactions Automotive Europe 2008-2012

Domestic Cross Boarder

160

131155

108

Cross Border Transactions 2008 & 2012

13

6

19

3

22

9

9

14

Strategic BuyersPrivate Equity

2008 2012

Private Equity Strategic Buyers

Domestic Transactions 2008 & 2012

2008 2012

19 22

31 23

© 2013 Deloitte Consulting GmbH

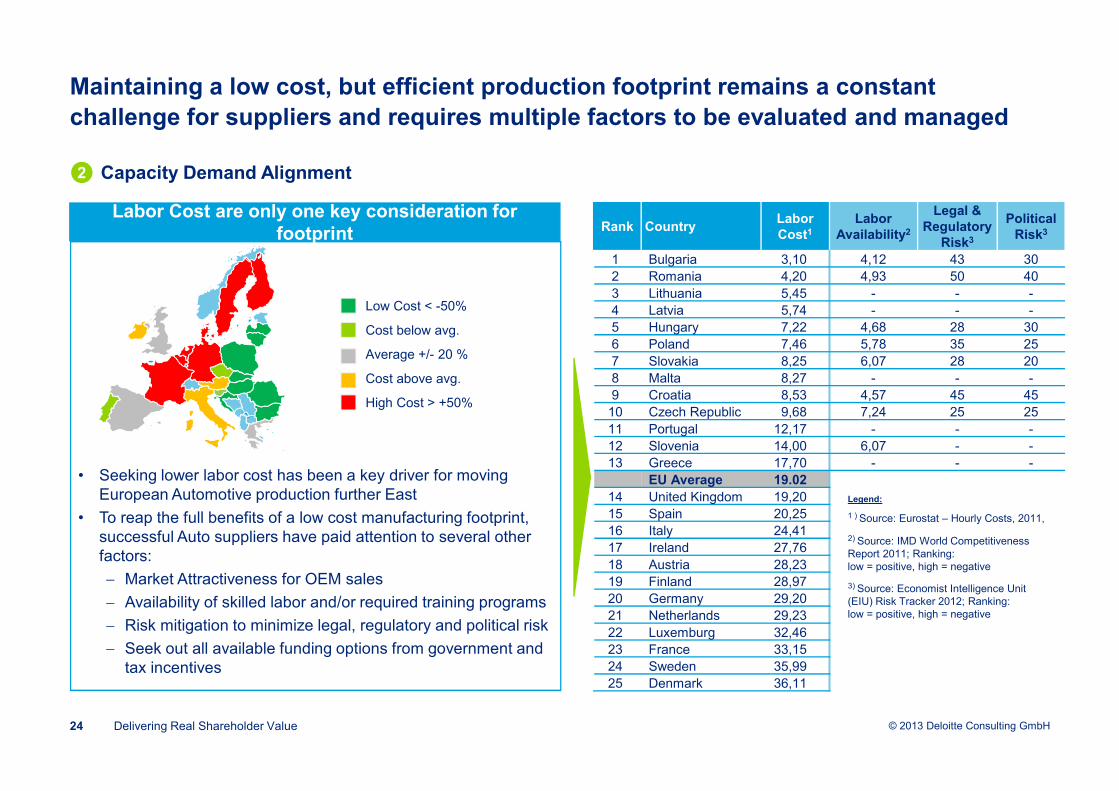

Maintaining a low cost, but efficient production footprint remains a constant

challenge for suppliers and requires multiple factors to be evaluated and managed

Delivering Real Shareholder Value24

• Seeking lower labor cost has been a key driver for moving European Automotive production further East

• To reap the full benefits of a low cost manufacturing footprint, successful Auto suppliers have paid attention to several other factors:

− Market Attractiveness for OEM sales

− Availability of skilled labor and/or required training programs

− Risk mitigation to minimize legal, regulatory and political risk

− Seek out all available funding options from government and tax incentives

Rank CountryLabor Cost1

Labor Availability2

Legal & Regulatory

Risk3

Political Risk3

1 Bulgaria 3,10 4,12 43 302 Romania 4,20 4,93 50 403 Lithuania 5,45 - - -4 Latvia 5,74 - - -5 Hungary 7,22 4,68 28 306 Poland 7,46 5,78 35 257 Slovakia 8,25 6,07 28 208 Malta 8,27 - - -9 Croatia 8,53 4,57 45 4510 Czech Republic 9,68 7,24 25 2511 Portugal 12,17 - - -12 Slovenia 14,00 6,07 - -13 Greece 17,70 - - -

EU Average 19.02

14 United Kingdom 19,2015 Spain 20,2516 Italy 24,4117 Ireland 27,7618 Austria 28,2319 Finland 28,9720 Germany 29,2021 Netherlands 29,2322 Luxemburg 32,4623 France 33,1524 Sweden 35,9925 Denmark 36,11

Low Cost < -50%

Cost below avg.

Average +/- 20 %

Cost above avg.

High Cost > +50%

Labor Cost are only one key consideration for footprint

1 ) Source: Eurostat – Hourly Costs, 2011,

2) Source: IMD World Competitiveness Report 2011; Ranking: low = positive, high = negative

3) Source: Economist Intelligence Unit (EIU) Risk Tracker 2012; Ranking: low = positive, high = negative

Legend:

Capacity Demand Alignment2

© 2013 Deloitte Consulting GmbH

A strong footprint across regions and continuous optimization efforts are required to

cost-effectively align shifting customer demands with manufacturing capacity

Delivering Real Shareholder Value25

Capacity Demand Alignment

• Footprint optimization for 18 plants in Europe and development of a future state “product - technology competence matrix” across the production network

• Reconfiguration master plan includes ~20 relocations, 3 programs for insourcing, several launch shifts and equipment transfers to mitigate CAPEX investments

• Structural changes led to >1% annual savings in COGS beyond all other operational improvements

Footprint Optimization – Case Study

Standardize product & process portfolio globally & best country allocation for new programs

Regular footprint review is required to align program to plant allocation with shifts in demand

Establish CoC plants to build additional competencies among product & process know-how

Knoweldge transfer & best practice sharing across plants, processes and technologies

Key Takeaways

EU Footprint

(sanitized)

Manufacturing Technology

Products

Key Technologies Category I Category II

EuropeCentral

Plant 1

Plant 2

Plant 3

Plant 4

Plant 5

Technology & Product Competences

within the Production Network Lead Plant

CoC

Plant

2

© 2013 Deloitte Consulting GmbH

There are no “magic” methods for achieving sustainable cost efficiency, but bottom

line impact can be greatly enhanced by establishing cross-functional teams

Delivering Real Shareholder Value26

Cost and Asset Efficiency

Mainly Functional Optimization Holistic Approach

• Drive improvement projects across functions and across products

• Involve CFTs already for the generation of ideas

• Cost down projects are often limited to functional silos and product lines

• No early involvement of other functions

• Adapt cross-functionality in target setting, steering, reporting and decision making

• Set up cross-functional decision committees

• Provide methodology and approaches for cross functional collaboration

• Involve ideas of suppliers (benchmarks & best practice)

• Decision structures and target systems per function lead to conflicting targets and no decisions

• No cross functional decision board existing

• Insufficient collaboration methods and tools

• Limited involvement of supplier know-how

Organi-zation

Gover-nance

Methods

1-2%

Time

Potential

Cost reduction program 1

Cost reductionprogram 2

Cost reduction program n

3%

3%

Functional Optimization

Holistic Cross Functional Approach

Time

Additional potential5-15%

Potential

Today Today

3

© 2013 Deloitte Consulting GmbH

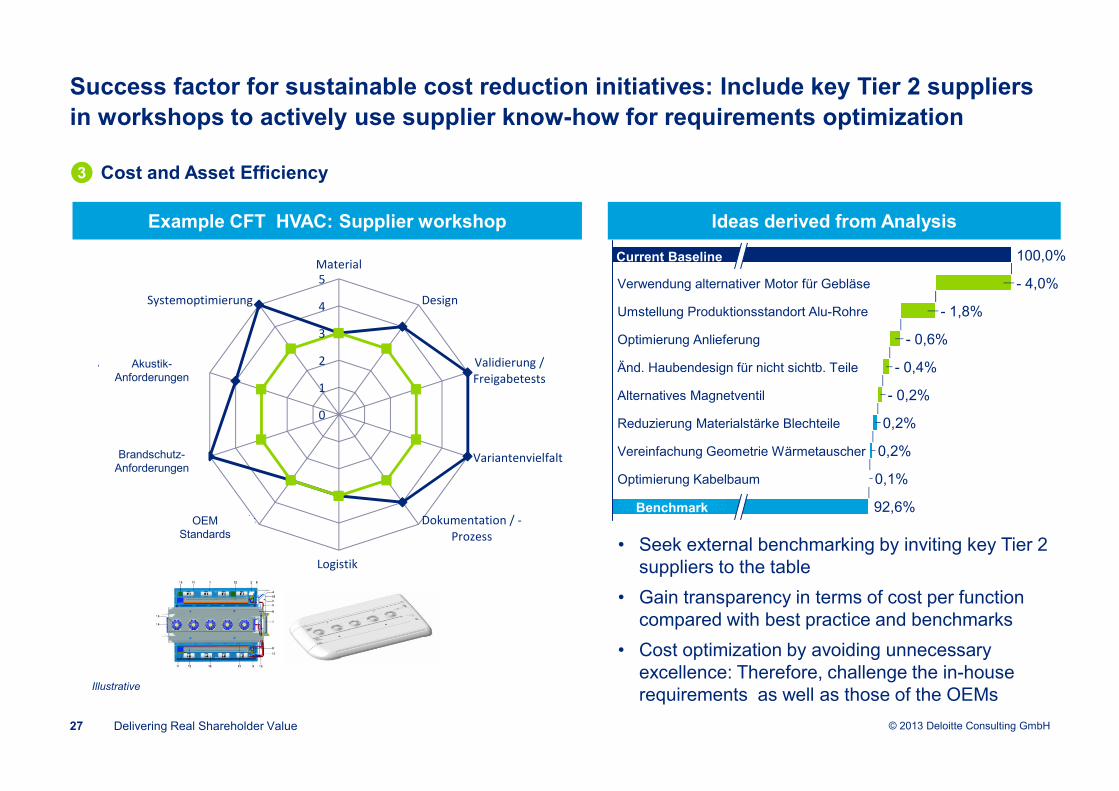

Success factor for sustainable cost reduction initiatives: Include key Tier 2 suppliers

in workshops to actively use supplier know-how for requirements optimization

Delivering Real Shareholder Value27

Cost and Asset Efficiency

- 1,8%

- 4,0%

100,0%

- 0,2%

0,2%

0,2%

92,6%

- 0,4%

0,1%

- 0,6%

Verwendung alternativer Motor für Gebläse

Umstellung Produktionsstandort Alu-Rohre

Optimierung Anlieferung

Änd. Haubendesign für nicht sichtb. Teile

Alternatives Magnetventil

Reduzierung Materialstärke Blechteile

Vereinfachung Geometrie Wärmetauscher

Optimierung Kabelbaum

Benchmark

Current Baseline

• Seek external benchmarking by inviting key Tier 2 suppliers to the table

• Gain transparency in terms of cost per function compared with best practice and benchmarks

• Cost optimization by avoiding unnecessary excellence: Therefore, challenge the in-house requirements as well as those of the OEMs

Ideas derived from AnalysisExample CFT HVAC: Supplier workshop

Illustrative

0

1

2

3

4

5

Material

Design

Validierung /

Freigabetests

Variantenvielfalt

Dokumentation / -

Prozess

Logistik

Daimler Standards

(EMV)

Brandschutzanforde

rungen

Akkustikanforderun

gen

Systemoptimierung

Akustik-Anforderungen

Brandschutz-Anforderungen

OEM Standards

3

© 2013 Deloitte Consulting GmbH

Addressing the winning themes will require a full focus, and an eye on future

challenges, improving cross-functional costs and preparing for market consolidation

Delivering Real Shareholder Value28

Key Takeaways for German Suppliers based on Global Study Results

Drive winning themes in parallel

Focus on portfolio and innovation to escape price pressure

Take advantage of supplier consolidation

All six winning themes need to be considered to be prepared for future trends in Automotive supply base industry and stay ahead of the competition

High pressure on price from OEMs will remain constant. Therefore, rewarding suppliers with technological innovative products, active portfolio management and top cost performance

Globalization and consolidation of the Auto supply base will be on-going. Suppliers with strong financial performance will have a good opportunity to actively participate in the consolidation and seek out growth opportunities

© 2013 Deloitte Consulting GmbH

Contacts

29

Deloitte Consulting GmbHRosenheimer Platz 481669 MunichGermany

Michael A. MaierDirector

Tel: +49 (0)89 29036 [email protected]

www.deloitte.com/de

Deloitte & ToucheCorporate Finance GmbHSchwannstr. 640476 DüsseldorfGermany

Siegfried FrickPartner

Tel: +49 (0)211 8772 [email protected]

www.deloitte.com/de

Ausblick Manufacturing 2/2013

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about or www.deloitte.com/de/UeberUns for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 200,000 professionals, all committed to becoming the standard of excellence.

This presentation contains general information only, and none of Deloitte Consulting GmbH or Deloitte Touche Tohmatsu Limited (“DTTL”), any of DTTL’s member firms, or any of the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. In particular this presentation cannot be used as a substitute for such professional advice. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this presentation.

© 2013 Deloitte Consulting GmbH