Degree 04 Financial Management - Commonwealth of Learning

104

FINANCIAL MANAGEMENT

Transcript of Degree 04 Financial Management - Commonwealth of Learning

FINANCIAL MANAGEMENT

Financial Management Dr. Gaofetoge Ntshadi Ganamotse Adeelah Tariq Rapelang D.Sekatle Commonwealth of Learning Edition 1.0. ____________________

Commonwealth of Learning© 2013 Any part of this document may be reproduced without permission but with attribution to the Commonwealth of Learning using the CC‐BY‐SA (share alike with attribution). http://creativecommons.org/licenses/by‐sa/4.0

Commonwealth of Learning 4710 Kingsway, Suite 2500 Burnaby, British Columbia

Canada V5H 4M2 Telephone: +1 604 775 8200

Fax: +1 604 775 8210 Web: www.col.org

E‐mail: [email protected]

ACKNOWLEDGEMENTS

These training materials have drawn so much from the available literature. The

commonwealth of learning extends its gratitude to the many authors who have made their

materials available through online or print publication. Many thanks to Mr. Sekatle, who has

initiated the writing of these materials.

Financial Management Page | i

TABLE OF CONTENTS

Table of Contents ........................................................................................................................................... i

COURSE OVERVIEW....................................................................................................................................... 1

Course Introduction .................................................................................................................................. 1

Course Goals ............................................................................................................................................. 1

Course Description .................................................................................................................................... 2

Required Readings .................................................................................................................................... 4

Assignments and Projects ......................................................................................................................... 5

Assessment Methods ................................................................................................................................ 5

Course Schedule ........................................................................................................................................ 5

STUDENT SUPPORT ....................................................................................................................................... 6

Academic Support ..................................................................................................................................... 6

How to Submit Assignments ..................................................................................................................... 6

Technical Support ..................................................................................................................................... 6

UNIT ONE ‐ INTRODUCTION TO FINANCIAL MANAGEMENT ........................................................................ 7

Unit 1 Introduction ................................................................................................................................... 7

Unit 1 Objectives ....................................................................................................................................... 7

Unit 1 Readings ......................................................................................................................................... 7

Unit 1 Assignments and Activities ............................................................................................................. 7

Topic 1.1 Finance and Forms of Business ................................................................................................. 8

Topic 1.1 Introduction ........................................................................................................................... 8

Topic 1.1 Objectives .............................................................................................................................. 8

Finance .................................................................................................................................................. 8

FORMS OF BUSINESS OWNERSHIP ....................................................................................................... 9

Topic 1.1 Summary ............................................................................................................................. 12

Topic 1.2 CONCEPTS and Principles of Financial Management .............................................................. 13

Topic 1.2 Introduction ......................................................................................................................... 13

Topic 1.2 Objectives ............................................................................................................................ 13

Financial management ........................................................................................................................ 13

The Finance Function and its Organization ......................................................................................... 14

Financial Management and Economics .............................................................................................. 15

Page | ii Financial Management

Financial Management and Accounting ............................................................................................. 15

Role of the Financial Manager ............................................................................................................ 16

Topic Summary ................................................................................................................................... 18

Unit 1 References ................................................................................................................................ 19

Unit 1 – Summary ................................................................................................................................... 20

Assignments and Activities ................................................................................................................. 20

Summary ............................................................................................................................................. 20

Next Steps ........................................................................................................................................... 20

UNIT Two ‐ FINANCIAL INSTITUTIONS AND MARKETS ................................................................................ 21

Unit 2 Introduction ................................................................................................................................. 21

Unit 2 Objectives ..................................................................................................................................... 21

Unit 2 Readings ....................................................................................................................................... 21

Unit 2 Assignments and Activities ........................................................................................................... 21

Topic 2.1 Financial Institutions ............................................................................................................... 22

Introduction ........................................................................................................................................ 22

Objectives............................................................................................................................................ 22

Major Customers of Financial Institutions .......................................................................................... 22

Commercial Banks ............................................................................................................................... 23

Mutual Funds ...................................................................................................................................... 26

Securities Firms ................................................................................................................................... 27

Insurance Companies .......................................................................................................................... 27

Pension Funds ..................................................................................................................................... 28

Savings institutions ............................................................................................................................. 28

Finance companies.............................................................................................................................. 29

Comparison of the Key Financial Institutions ..................................................................................... 29

Consolidation of Financial Institutions ................................................................................................ 30

Globalization of Financial Institutions ................................................................................................. 30

Topic Summary ................................................................................................................................... 31

Topic 2.2 FINANCIAL Markets ................................................................................................................. 32

Topic 2.2 Introduction ......................................................................................................................... 32

Topic 2.3 Objectives ............................................................................................................................ 32

Types of Markets ................................................................................................................................. 32

Financial Management Page | iii

Types of Market Securities.................................................................................................................. 35

Topic Summary ................................................................................................................................... 45

Unit 2 – References ............................................................................................................................. 47

Unit 2 – Summary ................................................................................................................................... 47

Assignments and Activities ................................................................................................................. 47

Summary ............................................................................................................................................. 47

Next Steps ........................................................................................................................................... 47

UNIT THREE ‐ FINANCIAL STATEMENTS ...................................................................................................... 48

Unit 3 Introduction ................................................................................................................................. 48

Unit 3 Objectives ..................................................................................................................................... 48

Unit 3 Readings ....................................................................................................................................... 48

Unit 3 Assignments and Activities ........................................................................................................... 49

Topic 3.1 STATEMENTS of Comprehensive Income and Financial Position ............................................ 50

Topic 3.1 Introduction ......................................................................................................................... 50

Topic 3.1 Objectives ............................................................................................................................ 50

Components of the Statement Comprehensive Income .................................................................... 50

Two Statements .................................................................................................................................. 50

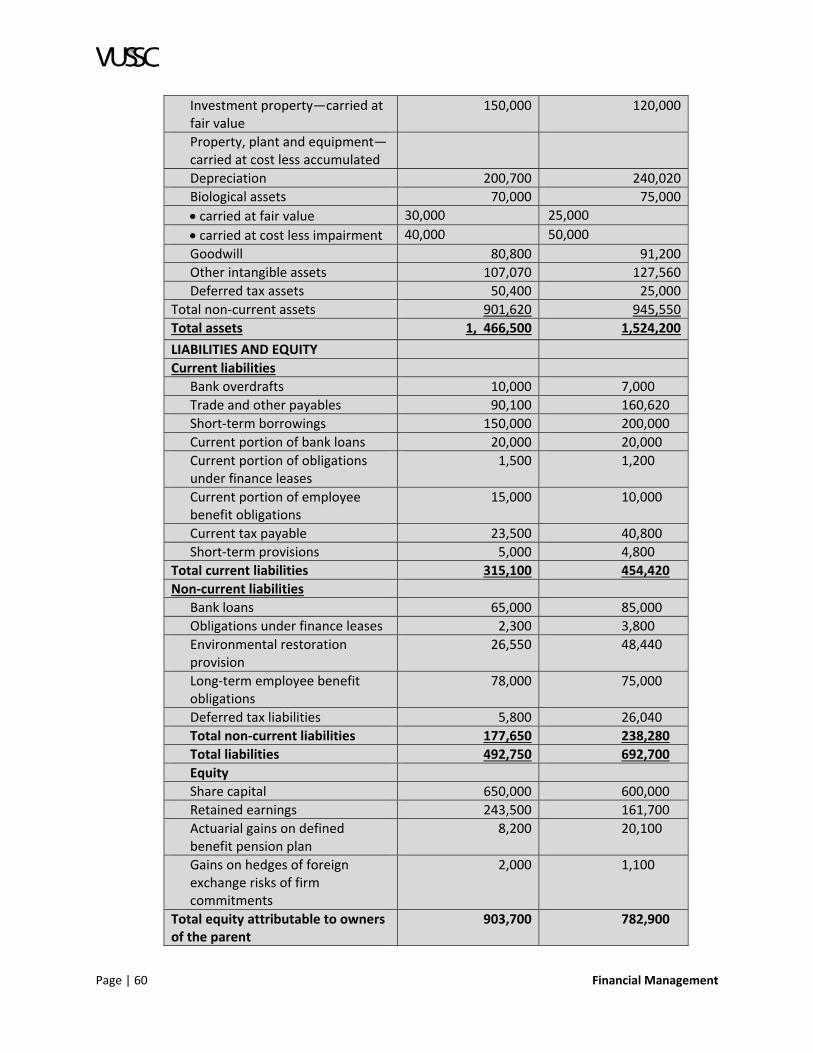

Components of the Statement of Financial Position (Balance sheet) ................................................ 57

Topic 3.2 Analysis of the Financial Statements ....................................................................................... 62

Topic 3.2 Introduction ......................................................................................................................... 62

Topic 3.2 Objectives ............................................................................................................................ 62

Introduction to Ratio Analysis ............................................................................................................. 62

Liquidity Measures .............................................................................................................................. 64

Profitability Measures ......................................................................................................................... 66

Efficiency Ratios .................................................................................................................................. 68

Investment Ratios ............................................................................................................................... 71

TOPIC SUMMARY ................................................................................................................................ 72

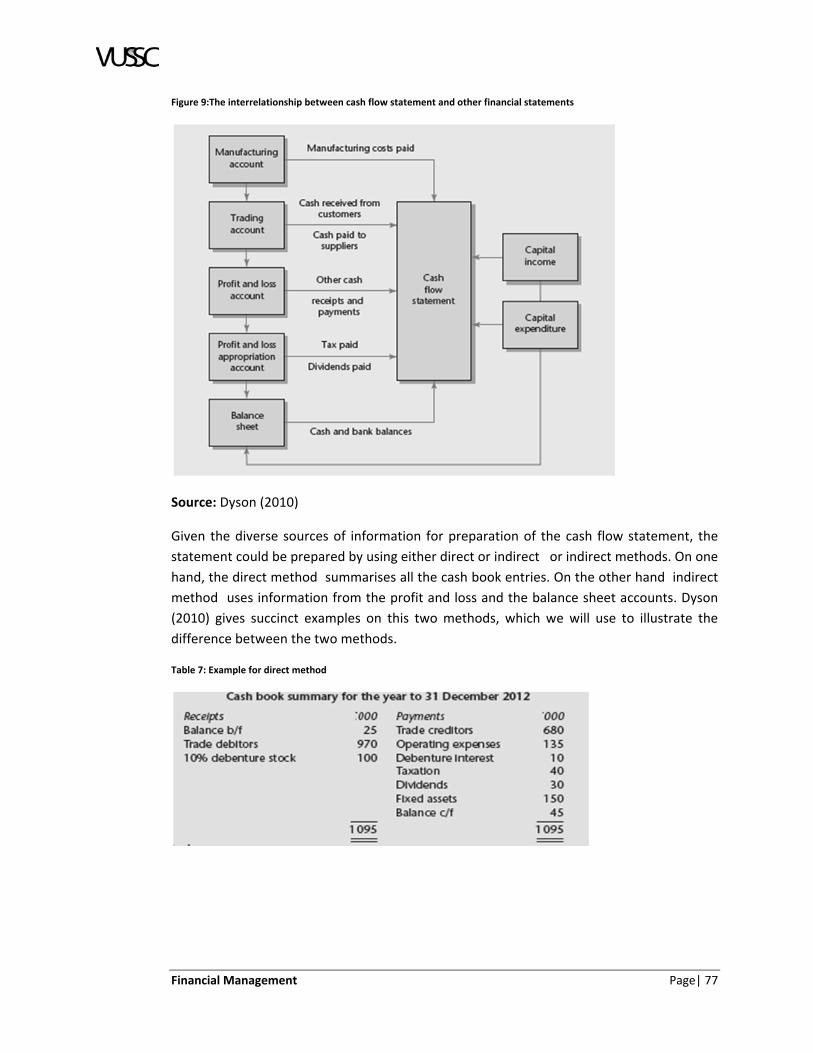

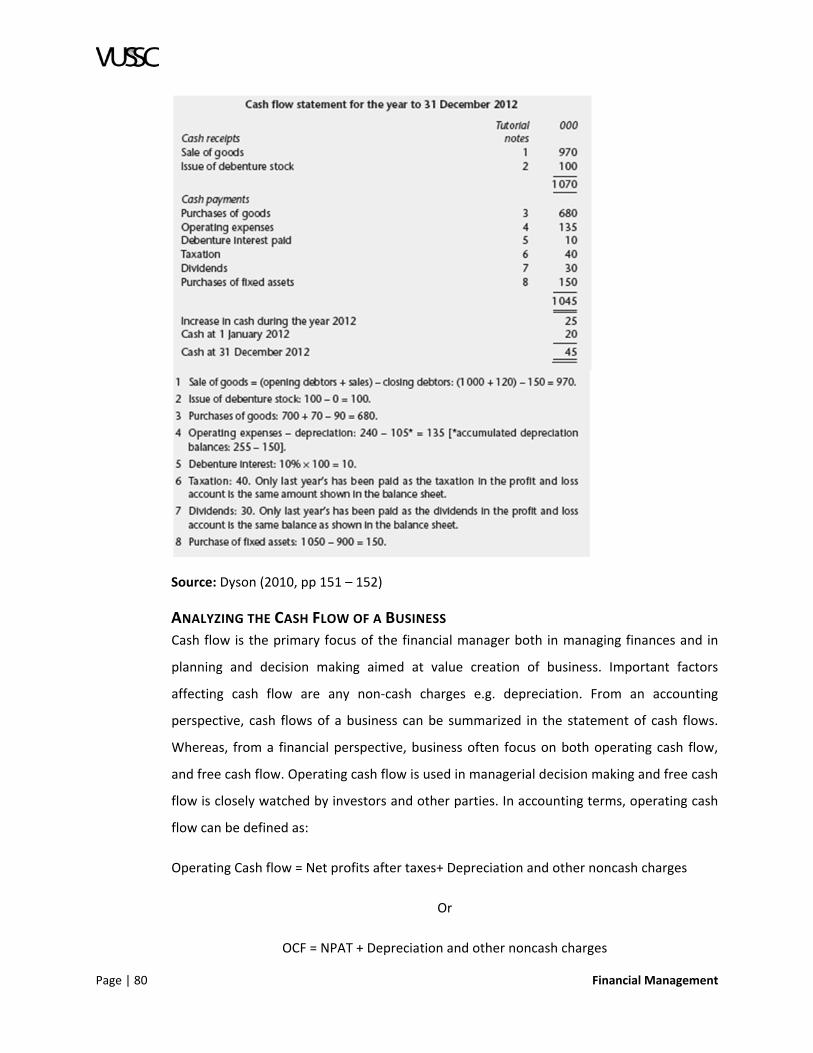

Topic 3.3 Statement of Cash Flows ......................................................................................................... 75

Topic 3.3 Introduction ........................................................................................................................ 75

Topic 3.3 Objectives ............................................................................................................................ 75

Cash flows ........................................................................................................................................... 75

Presentation of the cash flow statement (ias 7) ................................................................................. 76

Page | iv Financial Management

Analyzing the Cash Flow of a Business ................................................................................................ 80

Unit 3 References ................................................................................................................................ 83

Unit 3 ‐ Summary .................................................................................................................................... 85

Assignments and Activities ................................................................................................................. 85

Summary ............................................................................................................................................. 85

Next Steps ........................................................................................................................................... 85

UNIT FOUR ‐ FINANCIAL PLANNING ............................................................................................................ 86

Unit 4 Introduction ................................................................................................................................. 86

Unit 4 Objectives ..................................................................................................................................... 86

Unit 4 Readings ....................................................................................................................................... 86

Unit 4 Assignments and Activities ........................................................................................................... 86

Topic 4.1 – Introduction to Financial Planning ....................................................................................... 87

Topic 4.1 Introduction ........................................................................................................................ 87

Topic 4.1 Objectives ............................................................................................................................ 87

Strategic Financial Plans ...................................................................................................................... 87

Operating Financial Plans .................................................................................................................... 87

Summary ............................................................................................................................................. 88

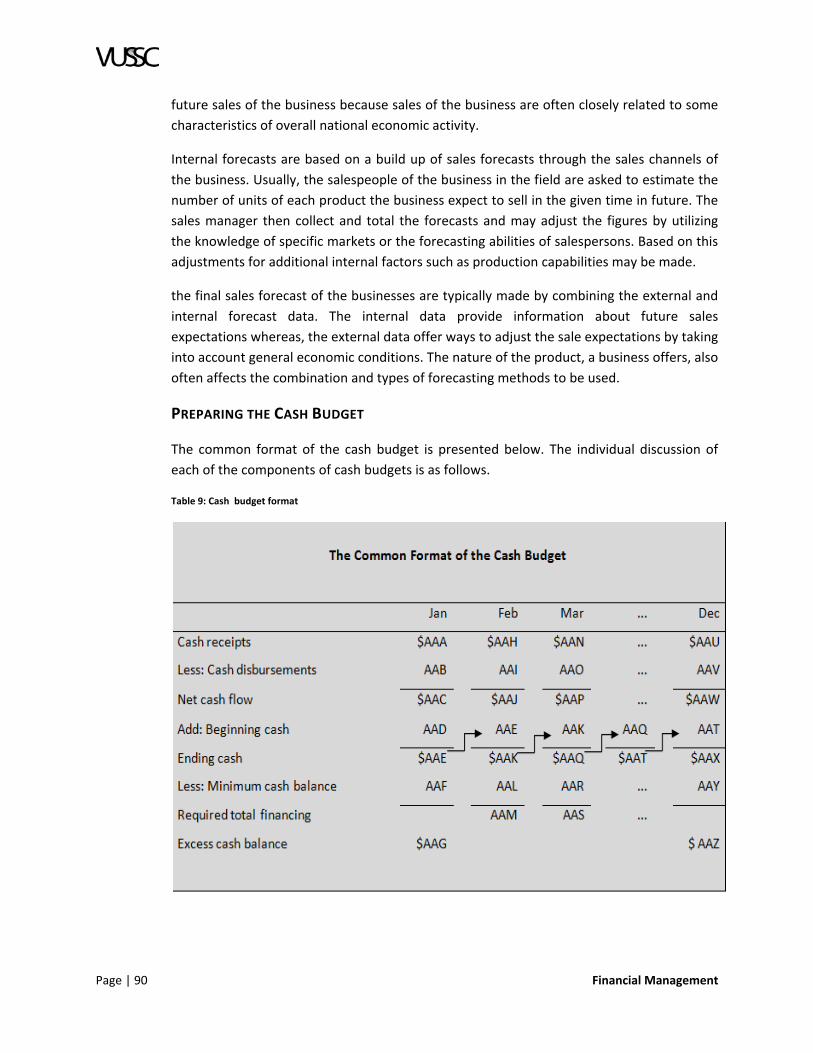

Topic 4.2 ‐ Cash Budgets for Cash Planning ............................................................................................ 89

Topic 4.2 Introduction ......................................................................................................................... 89

Topic 4.2 Objectives ............................................................................................................................ 89

What is a Cash Budget ........................................................................................................................ 89

The Sales Forecast ............................................................................................................................... 89

Preparing the Cash Budget ................................................................................................................. 90

Cash Receipts ...................................................................................................................................... 91

Cash Disbursements ............................................................................................................................ 93

Net Cash Flow, Ending Cash, Financing and Excess Cash .................................................................... 94

Evaluating the Cash Budget ................................................................................................................ 95

Managing the Uncertainty in the Cash Budget ................................................................................... 95

Summary ............................................................................................................................................. 96

Topic 4.3 Pro Forma Financial Statements: A Tool For Profit Planning .................................................. 97

Topic 4.3 Introduction ......................................................................................................................... 97

Topic 4.3 Objectives ............................................................................................................................ 97

Financial Management Page | v

Pro Forma Financial Statements ......................................................................................................... 97

Preceding Year’s Financial Statements ............................................................................................... 97

Sales Forecast ...................................................................................................................................... 99

Preparing the Pro Forma Statements ................................................................................................. 99

Pro forma Income Statement ............................................................................................................. 99

Types of Costs and expense Consideration ...................................................................................... 100

Pro Forma Balance Sheet .................................................................................................................. 100

Evaluating the Pro Forma Statements .............................................................................................. 103

Topic 4. Summary ............................................................................................................................. 103

Unit 4 – References ........................................................................................................................... 104

Unit 4 – Summary ................................................................................................................................. 104

Assignments and Activities ............................................................................................................... 104

Summary ........................................................................................................................................... 105

Next Steps ......................................................................................................................................... 106

UNIT FIVE ‐ SHORT TERM FUNDS MANAGEMENT .................................................................................... 107

Unit 5 Introduction ............................................................................................................................... 107

Unit 5 Objectives ................................................................................................................................... 107

Unit 5 Readings ..................................................................................................................................... 107

Unit 5 Assignments and Activities ......................................................................................................... 107

Topic 5.1 – Working Capital Management ........................................................................................... 108

Topic 5.1 Introduction ....................................................................................................................... 108

Topic 5.1 Objectives ......................................................................................................................... 108

Working Capital and Net Working Capital ........................................................................................ 108

The Goals of Working Capital Management ..................................................................................... 109

Cash and motives for holding cash ................................................................................................... 109

Reasons for Holding Cash Balances .................................................................................................. 109

Cash Flow Cycle ................................................................................................................................. 110

The cash conversion cycle ................................................................................................................. 110

Cash conversion cycle’s funding requirements ................................................................................ 111

Permanent versus seasonal funding needs ...................................................................................... 111

Aggressive versus conservative funding strategy ............................................................................. 112

Topic 5.1 Summary ........................................................................................................................... 112

Page | vi Financial Management

Topic 5.2 – Inventory Management ...................................................................................................... 114

Topic 5.2 Introduction ....................................................................................................................... 114

Topic 5.2 Objectives .......................................................................................................................... 114

Inventory: An overview ..................................................................................................................... 114

Level versus Seasonal Production ..................................................................................................... 114

ABC inventory system ....................................................................................................................... 115

Economic Ordering Quantity ............................................................................................................ 115

Carrying Costs ................................................................................................................................... 115

Deriving Economic Ordering Quantity Formula ................................................................................ 117

Total costs for inventory ................................................................................................................... 118

Safety Stock and Stock outs .............................................................................................................. 119

Just‐in‐Time (JIT) Inventory Management ........................................................................................ 119

Topic 5.2 Summary ........................................................................................................................... 120

Topic 5.3 – Current Liabilities Management ......................................................................................... 121

Topic 5.3 Introduction ....................................................................................................................... 121

Topic 5.3 Objectives .......................................................................................................................... 121

Accounts Payable Management ....................................................................................................... 121

Role of Accounts payable in cash conversion cycle .......................................................................... 121

Credit terms ...................................................................................................................................... 122

Effects of stretching accounts payable ............................................................................................. 125

.......................................................................................................................................................... 125

Accruals ............................................................................................................................................. 125

Sources of Un secured short term financing: ................................................................................... 125

Commercial Bank loans ..................................................................................................................... 126

Loan Interest Rates ........................................................................................................................... 126

Fixed rate and floating rate ............................................................................................................... 126

Computing interest ........................................................................................................................... 126

The single payment notes ................................................................................................................. 127

Lines of credit .................................................................................................................................... 128

Interest rate: ..................................................................................................................................... 129

Operating change restrictions........................................................................................................... 129

Compensating balances .................................................................................................................... 129

Financial Management Page | vii

Annual cleanups ................................................................................................................................ 130

Revolving credit agreement .............................................................................................................. 130

Commercial paper ............................................................................................................................. 131

Interest rate on commercial paper ................................................................................................... 131

Secured short term financing............................................................................................................ 132

Characteristics of secured short term financing ............................................................................... 132

Collateral and terms .......................................................................................................................... 132

Accounts receivable as collateral ...................................................................................................... 133

Pledging accounts receivable ............................................................................................................ 133

Factoring accounts receivable .......................................................................................................... 134

Inventory as collateral....................................................................................................................... 135

Floating inventory liens ..................................................................................................................... 135

Trust receipt inventory loans ............................................................................................................ 135

Warehouse receipt loans .................................................................................................................. 136

Topic Summary ................................................................................................................................. 136

Unit 5 – References ........................................................................................................................... 137

Unit 5 – Summary ................................................................................................................................. 137

Assignments and Activities ............................................................................................................... 137

Summary ........................................................................................................................................... 138

FINAL ASSIGNMENT/MAJOR PROJECT ...................................................................................................... 139

COURSE SUMMARY ................................................................................................................................... 140

Topics Learned ...................................................................................................................................... 140

Application of Knowledge and Skill ....................................................................................................... 143

Course Evaluation ................................................................................................................................. 144

COURSE APPENDICES ................................................................................................................................ 145

Appendix 1 – Solution to topic 3.2 (Financial Analysis) .................................................................. 146

Appendix 2: Unit Four Assignment’s Solution ................................................................................. 149

Financial Management Page | 1

COURSE OVERVIEW

COURSE INTRODUCTION

Financial management is an introductory course which provides the applied and realistic

view of financial management for today’s’ entrepreneurs. It is the basis of fundamental

concepts of business finance, investment and an understanding of financial calculations. It

sets a ground understanding of the elements of Financial Management in an Enterprise by

describing the corporation and its operating environment. The contents of this course

provide the understanding, knowledge and essential skills; any manager should have when

considering proposing project and assessing its financial viability and impact on the

business.

The course integrates elements of financial accounting and financial management. The

financial accounting focuses on key financial statements such as Income Statements,

Balance Sheets, and Cash Flow Statements, and their roles in the measurement of

performance through the use of financial and non‐financial measures. Whereas, the

financial Management focuses on decision making associated with designing, implementing

and managing an enterprise. This course will help entrepreneurs to support accounting, risk

management, improve operational planning, controls and decision making. Entrepreneurs

will be able in order to impede the misuse of funds, maximize the profit and wealth of the

business in Long Run. In addition to this, the course along with other courses, e.g., business

plan development, operations management etc, in program provides the basis for further

studies related to finance which are important to most managerial people.

This course assumes that the students have prior accounting knowledge as it is designed to

build on the introduction to business accounting, business planning and management

accounting courses. However, the course can also be taken by those who have basic

practical accounting knowledge.

COURSE GOALS

Upon completion of the financial management course you will be able to:

Page | 2 Financial Management

1. Understand the nature of finance management and the theoretical and conceptual

underpinning of the frameworks for the financial management

2. Identify the nature, characteristics and use of financial statements as financial reporting

system

3. Distinguish between financial and non‐financial performance measurement.

4. Use the relevant costs for decision making, particularly pricing.

5. Highlight the issues in the determination of the cost of products or services and activities

and the implications for cost control and pricing.

6. Analyze the relationships between activity cost, volumes and profit, and their role for

planning and decision making

7. Make important financing and investment decisions by establishing working capital

policies

8. Recognize the impact of management decisions on the financial health of a business

9. Employ effective financial management techniques to maximize profit and wealth of the

business.

10. Understand the financial planning process, including strategic and short‐term financial

plans.

COURSE DESCRIPTION

To meet the above course objectives, the course is divided into 5 units. A general overview

of financial management is introduced in Unit 1. Financial institutions and markets are

covered in unit 2. The different types of financial statements are examined in unit 3, Unit 4

covers the different areas of financial planning whilst unit 5 covers financial decision

making. The valuation and capital budgeting issues are covered in unit 6. Each of the units is

further subdivided into topics, see the list below. Assessment of learning is provided at the

end of each topic and a summative assessment of each unit if given at the end of each unit:

Financial Management Page | 3

Unit 1: Introduction to Financial Management

Topic 1.1: Finance and Forms of Business

Topic 1.2: Concepts and Principles of Management

Unit 2 Financial Markets and Institutions

Topic 2.1: Financial Institutions

Topic 2.2: Financial Markets

Unit 3 Financial Statements

Topic 3.1: Statements of Comprehensive Income and Financial Position

Topic 3.2: Analysis of the Financial Statements

Topic 3.3: Statement of Cash flows

Unit 4: Financial Planning

Topic 4.1: Introduction to Financial Planning

Topic 4.2 Cash Budgets for Cash Planning

Topic 4.3 Pro‐forma Financial Statements: A tool for Profit Planning

Unit 5: Financial Decision Making

Topic 5.1: Working Capital Management

Topic 5.2: Inventory Management

Topic 5.3: Current Liabilities Management

Page | 4 Financial Management

REQUIRED READINGS

Materials relating to financial Management can be found on the web, as well as in the

Library:

1. Geoffrey, A. Hirt, Bartley R. Danielsen Stanley B. Block (2009) Foundations of Financial

Management. McGraw Hill. ISBN: 0073363774 / 0‐07‐336377‐4

2. Brigham F. Eugene and Houston F. Joel (2012) Fundamentals of Financial management.

South‐ Western, Cengage Learning, Ohio IBN 13: 978‐0‐538‐47712‐3

3. Chandra Prassana (2010) Fundamentals of Financial Management. Tata McGraw Hill.

New Delhi in

http://books.google.co.uk/books?id=osy4UMOgpG4C&printsec=frontcover&dq=fUNDAME

NTALS+OF+FINANCIAL+MANAGEMENT,&hl=en&sa=X&ei=yJN_UZnaBMX5PLrDgdAD&sqi=2

&ved=0CFIQ6AEwAw accessed 24/04/13

4. Firer, C.; Ross, S.; Westerfield, R. and Jordan, B. (2004). Fundamentals of

Corporate Finance. McGraw Hill, New York.

5. International Accounting Standards Board (2009) Presentation of Financial

statements in http://www.iasplus.com/en/standards/standard5 accessed 23rd April

2013

6. International Accounting Standards Board (2009) International Financial Reporting

Standard for Small and Medium-sized Entities (IFRS for SMEs) in

http://eifrs.iasb.org/eifrs/sme/en/IFRSforSMEs2009.pdf accessed 25/04/2013

7. Subramanyam, K.R. and Wild John. J (2009) Financial Statement analysis, 10TH Edition

McGraw‐Hill Irwin, New York. –in http://highered.mcgraw‐

hill.com/sites/dl/free/0073379433/597452/Subramanyam_fsa_sample_Ch01.pdf accessed

23/04/2013

8. Stolowy, H. And Lebas, Michel J. (2002) Corporate Financial Reporting – A Global

Perspective. Thomson Learning. London.

9. Dyson, John R. (2010) Accounting for non accounting Students. Pearson Education

Limited. Harlow. In http://web.kku.ac.th/chrira/Non%20Acct.%20Dyson.pdf accessed

26/04/2013

10. Gitman, Lawrence J. And Chad J. Zutter (2012) Principles of managerial finance, 13th Ed.

P. cm. The Prentice Hall

Financial Management Page | 5

11. Lorenzo P, Argentina and Allende, Sarria (2010) Working Capital Management, Oxford

University press Inc.

12. Brealey, R.A; Myers, S.C; Allen, F. (2006) Principles of corporate finance, 6th Ed.

dandelon.com

13. Gitman, Lawrence J. (2002) Principles of managerial finance, 10th Ed. P. cm. The

Prentice Hall

14. Sagner, James (2011), Essentials of Working Capital Management, John Wiley and sons.

Inc

15. Gitman, Lawrence J. Web Chapter Financial Markets and Institutions available at

http://wps.aw.com/wps/media/objects/5448/5579249/FinancialMarketsandInstitutions.pd

f

ASSIGNMENTS AND PROJECTS

Assessment of learning for this course will be done through end of topic activities, end of

unit activities and one major end of course assignment. The end of topic activity is designed

to reinforce the students learning at the end of the topic whilst the end of unit tests the

attainment of the course objective in relation to a specific unit. The end of course

assessment requires the student to consolidate all the knowledge and skills acquired from

the course. This will be developed by the respective institutions.

ASSESSMENT METHODS

The end of topic and end of unit assessments could be used for seminar activities by your

institution. For the course assessment, participating universities could provide their

students with financial statements from companies for students to work with and advise

management for these companies accordingly. This could either be a group project or

individual project depending on the assessment structure of the participating universities.

An end of year examination could also be given to the students.

COURSE SCHEDULE

This course is designed to be completed within 12 to 16 weeks of the final year of a degree

in entrepreneurship programme.

Page | 6 Financial Management

STUDENT SUPPORT

ACADEMIC SUPPORT

The course assumes that the participating institutions would have within their structures,

some means of supporting student learning. The module assumes that besides the normal

lectures, student learning will be facilitated through use of seminars, designed to accord

the students’ time to work through the activities either as a group or as individuals. Also, it

is assumed that personal tutorials will be arranged to give students a chance to reinforce

their learning through a one to one intervention as needed by students.

The student handbook, developed by the respective institutions, will provide information

with regards to access of resources, e.g. library, lecturer and/or facilitators.

HOW TO SUBMIT ASSIGNMENTS

Submission of assignments is to be in line with the policies and guidelines of the respective

participating institutions. These should be included in the course handbook, to facilitate

motivation of student learning.

TECHNICAL SUPPORT

Where appropriate, the participating institutions should avail the course lecture slides in

online sites such as blackboard or Moodle. Such information to be provided in the course

handbook.

Financial Management Page | 7

UNIT ONE ‐ INTRODUCTION TO FINANCIAL MANAGEMENT

UNIT 1 INTRODUCTION

The unit provides a general overview of the concept of financial management. The students

are introduced to financial management, the concepts and principles used within the scope

of the subject. The important concepts are defined.

UNIT 1 OBJECTIVES

Upon completion of this unit, the students will be able to:

1. Differentiate between different forms of businesses and explain the finance implications

for each.

2. Explain the concepts and principles of financial management

UNIT 1 READINGS

To complete this unit, you are required to read the following chapters:

1. Geoffrey, A. Hirt, Bartley R. Danielsen Stanley B. Block (2009)

2. Brigham, F. Eugene and Houston, F. Joel (2012) ‐ Chapter 1

3. Chandra Prassana (2010) Chapter 1

UNIT 1 ASSIGNMENTS AND ACTIVITIES

While crude end of topic assessment id provided in this course to assess student learning.

The end of the participating universities will develop end of unit assessment is to be

designed by the participating institutions.

Page | 8 Financial Management

TOPIC 1.1 FINANCE AND FORMS OF BUSINESS

TOPIC 1.1 INTRODUCTION

When deciding on which form of ownership to go for, entrepreneurs look for different

considerations, such as suitability, legality and tax implications. There are three main forms

of; sole proprietorship, partnership and the company; however there is an extension to the

company which is the close corporation. Each of these has advantages and disadvantages.

The most influencing factor to decisions of ownership is the country’s respective company

law/laws of incorporation. The nature of the business and the founding structure of the

business calls for careful management of the finances to lead to the achievement of the

aspirations of the owners, which is growth. Efficient management of finance entails,

acquiring and investing the financial resources of an organisation profitably. This topic

introduces financial management by explaining the forms of businesses and implications for

finance and the concepts and principles of financial management

TOPIC 1.1 OBJECTIVES

Upon completion of this Topic you will be able to:

1. Explain the nature of finance

2. To explain the forms of businesses and finance implications

FINANCE

Finance is known as the art and science of managing money finance is broad and dynamic

field and it directly affects the lives of every person and every organization. Every individual

and organization earns or raises money and spends or invests money. Finance is concerned

with the process, institutions, markets, and instruments involved in the transfer of money

among individuals, businesses, and governments. Basic principles of finance, such as those

in this course, can be universally applied in business organizations of different types.

Financial Management Page | 9

FORMS OF BUSINESS OWNERSHIP

There are three most common legal forms of business organization, the sole proprietorship,

the partnership and the corporation. However some other specialized forms of business

also exist. Among the business organizations, the large number of businesses are sole

proprietorships. However, corporations are significantly dominant with respect to receipts

and net profits.

SOLE PROPRIETORSHIP

A sole proprietorship is a business founded and owned by one person. It is the simplest

form of business to start and enjoys less government regulation. In real life there are more

sole proprietorships than any other type of business businesses that later become large

corporations start out as small sole proprietorships.

The advantages are the owner of a sole proprietorship keeps all the profits, there is only

one person to make decision hence quickening the decision making process, there is also no

conflict on decisions made. Flexibility is enhanced and there is total responsibility and

ownership of tasks to be carried out. Above all the owner takes all the profits. However

disadvantages are; the owner has unlimited liability for business debt, meaning that

creditors can look to the proprietor’s personal assets for payment. Because there is no

distinction between personal and business income, all business income is taxed as personal

income, there is no sharing of ideas on decision making which might lead to less efficient

solutions. The owner might be overloaded and overworked because he has no one to help.

The life of a sole proprietorship is limited to the owner’s life span and therefore has no

continuity; above all the amount of capital can be raised by a sole is minimal to the extent

of his savings. This limits the business from exploiting new opportunities. Ownership of a

sole proprietorship may be difficult to transfer since this requires the sale of the entire

business to a new owner, (Firer et al., 2004)

PARTNERSHIP

A partnership is a kind of a business whereby two or more owners join together as partners

to co‐own the business. The partners share in gains or losses and contribute capital, and are

responsible for achieving the goals of the organisation. We will have to understand that for

partnership to start, there are certain arrangements and agreements entered into, such as,

Page | 10 Financial Management

all partners might be liable for the debts of an organisation (have unlimited liability for all

partnership debt) this happens in a general partnership1

Because partners do things together, in should be tabulated in their partnership agreement

as to how they contribute as well and their profit/loss sharing ratios. The agreement might

be informal oral agreement, however it is advisable that it be formalised in pen and paper

for ease of conflict resolution. In a limited partnership, one or more partners will be

involved actively in running the business, thereby having unlimited liability, while some of

the partners will not participate in the running of the business (sleeping partners). A limited

partner’s liability for business debts is limited to the amount that partner contributes to the

partnership.

The advantages of a partnership are that; it is easy to form and inexpensive, the same as a

sole proprietorship. The capital contributed can be quite substantial as compared to a sole

trader; there could be a wide array of ideas in decision making and work may be shared

among active partners. However a partnership also has its disadvantages; its lifespan is

limited, because when a partner dies the partnership has to be dissolved. Transfer of

ownership by a general partner is not easy because the partnership has to be dissolved and

new one must be formed. Because partners act for and on behalf of the partnership,

decisions taken by partners render other partners liable.

Starting a partnership means people intend to work together for a common good, it goes

without saying that some will be charged with certain responsibilities for and on behalf of

other partnership, for it to be successful, it should be based upon trust and honesty. A

written agreement is very important especially if it spells out clearly the rights and duties of

the partners; it helps solve misunderstandings later on. Firer et al. (2004) argue that the

primary disadvantages of sole proprietorships and partnerships as forms of business

organization are (1) unlimited liability for business debts on the part of the owners, (2)

limited life of the business, and (3) difficulty of transferring ownership. These three

disadvantages add up to a single, central problem: The ability of such businesses to grow

can be seriously limited by an inability to raise cash for investment.

1 http://www.myownbusiness.org/s4/

Financial Management Page | 11

CORPORATION

The corporation is the most important form (in terms of size) of business organization in

most countries. It is considered a legal “person” separate and distinct from its owners, and

it has many of the rights, duties, and privileges of an actual person. Corporations can

borrow money and own property, can sue and be sued, and can enter into contracts. A

corporation can even be a general partner or a limited partner in a partnership, and a

corporation can own stock in another corporation (Firer et al, 2004).

Starting a corporation is by far strenuous, lengthy and more complicated than starting the

other forms of business organization, this is because it requires the preparation of the

memorandum of association as well the articles of incorporation, which are quite

comprehensive documents. According to the Company Laws of various countries the

articles of incorporation must contain a number of things, including the corporation’s

name, its intended life (which can be forever), its business purpose, and the number of

shares that can be issued2.

The bylaws are rules describing how the corporation regulates its own existence. For

example, the bylaws describe how directors are elected. The bylaws may be amended or

extended from time to time by the stockholders. In a large corporation, the stockholders

and the managers are usually separate groups. The stockholders elect the board of

directors, who then select the managers. Management is charged with running the

corporation’s affairs in the stockholders’ interests. In principle, stockholders control the

corporation because they elect the directors. As a result of the separation of ownership and

management, the corporate form has several advantages. Ownership (represented by

shares of stock) can be readily transferred, and the life of the corporation is therefore not

limited. The corporation borrows money in its own name. As a result, the stockholders in a

corporation have limited liability for corporate debts. The most they can lose is what they

have invested. The relative ease of transferring ownership, the limited liability for business

debts, and the unlimited life of the business are the reasons why the corporate form is

superior when it comes to raising cash. If a corporation needs new equity, it can sell new

shares of stock and attract new investors. The number of owners can be huge; larger

corporations have many thousands or even millions of stockholders.

2 http://highered.mcgraw‐hill.com/sites/dl/free/0072946733/301389/Ross_Sample_ch01.pdf

Page | 12 Financial Management

TOPIC 1.1 SUMMARY

This topic has highlighted the importance of financial management for the various forms of

business. Whilst financial management is deemed important for all forms of companies,

there are differences in the requirements for financial management depending on the type

of ownership of the business.

Self‐Reflection Question

How is the finance function organised in the different forms of companies?

Financial Management Page | 13

TOPIC 1.2 CONCEPTS AND PRINCIPLES OF FINANCIAL MANAGEMENT

TOPIC 1.2 INTRODUCTION

Managers, be they of a for‐profit or not‐for‐profit companies or those managing large or

small firms, constantly have to make finance related decisions. The main aim of such

decisions is to generate value to the owners of the business through the operations of the

company. People who are responsible for such role in a company are said to be performing

a financial management role. This topic introduces the students to the concept of financial

management. The main focus of financial management, the role of the finance manager

and the decisions facing those charged with the financial management responsibilities are

articulated.

TOPIC 1.2 OBJECTIVES

At the end of the topic, the learners will be able to:

1. Define financial management

2. Explain the nature of the finance function

3. Explain the role of a financial manager in an organisation

FINANCIAL MANAGEMENT

Financial management is concerned with decisions on assets acquisition, generation of the

required capital to acquire the necessary assets as well as decisions on how to maximize.

Shareholders/owners value through the operations of the firm. As such, financial managers

have to think about answering these basic questions;

1. What long term investments should we take on? The kind of buildings, materials,

machinery and equipment needed.

2. Where will the long term finances to pay for the investments are acquired from? This

will involve as to whether the entrepreneur will rely on savings from the profits made,

borrow from external sources or engage in more owners to contribute the capital.

Page | 14 Financial Management

3. How do we intend to manage the day to day financial activities? Such as collecting from

customers and paying suppliers, as well as making any disbursements concerning the

business.

Assuming the manager is the entrepreneur, these are not the only questions that s/he will

have to answer; they may not be exhaustive, however these are some of the most

important. Financial management therefore deals with a wide range of issues as such;

simply put; the acquisition of funds into the business and how to invest those funds in the

best possible manner to ensure organizational growth as well increasing the owners,

wealth. In this case we can believe in an organisation someone charged with these

responsibility is fit to be called the “Financial Manager”, let us now look at what the

Financial Manager is.

THE FINANCE FUNCTION AND ITS ORGANIZATION

People in different areas of responsibility within the business interact with finance

personnel and procedures to get their jobs done. In order to make useful forecasts and

effective decisions, financial personnel must be willing and able to talk to individuals in

other areas of the firm. Financial management function can be broadly described by taking

into consideration its role within the organization, its relationship to economics and

accounting, and the primary activities of the financial manager.

The size and importance of the financial management function depend on the size of the

firm. Financial management can be performed by the accounting department in small firms.

Whereas, a separate finance department linked directly to the company president or CEO

through the chief financial officer (CFO) is required in medium to large firms. The lower

portion of the organizational chart in Figure 1.1 represents the structure of the finance

function in a usual medium‐to‐large‐size firm.

The treasurer focus tends to be more external and is commonly responsible for handling

financial activities, such as financial planning and fund raising, making capital expenditure

decisions, managing cash, managing credit activities, managing the pension fund, and

managing foreign exchange. The controller focus more internal and typically handles the

Financial Management Page | 15

accounting activities, such as corporate accounting, tax management, financial accounting,

and cost accounting.

FINANCIAL MANAGEMENT AND ECONOMICS

Financial managers must have an understanding of the economic framework such as

different levels of economic activity and changes in economic policy. The financial

managers need to use economic theories as guidelines for efficient business operation e.g.

supply‐and‐demand analysis, profit‐maximizing strategies, and price theory etc. The most

important economic principle used in financial management is marginal analysis, which

helps managers to make financial decisions and take actions, only when the added benefits

exceed the added costs.

FINANCIAL MANAGEMENT AND ACCOUNTING

Financial management and accounting activities of a business are closely related and are

not easily distinguishable. In small firms the controller often carries out the finance

function, and in large firms many accountants are closely involved in various finance

activities. However, there are two basic differences between finance and accounting; one is

related to the emphasis on cash flows and the other to decision making.

EMPHASIS ON CASH FLOWS

The accounting function primarily develops and reports data for measuring the

performance of the firm, and assessing its financial position. The accountant uses

standardized and generally accepted principles to prepare financial statements on accrual

basis.

On the other hand, the primary emphasis of financial manager is on the inflow and outflow

of cash i.e. cash flows. The financial manager maintains solvency of the business by

planning the cash flows necessary to satisfy its obligations and to acquire assets needed to

achieve the goals of the business. Regardless of its profit or loss, cash basis are used to

recognize the revenues and expenses only with respect to actual inflows and outflows of

cash to make sure that a business must have a sufficient flow of cash to meet its obligations

as they come due.

Page | 16 Financial Management

Example:

In accounting terms Bamboo limited is profitable, but in terms of actual cash flow it is

a financial failure. Its lack of cash flow resulted from the uncollected account

receivable in the amount of 110,000. Without adequate cash inflows to meet its

obligations, the firm will not survive, regardless of its level of profits. As the example

shows, the financial manager must look beyond financial statements to obtain insight

into existing or developing problems because the accrual accounting data do not fully

describe the conditions of a business. However, accountants are sensitive to the

importance of cash flows, and financial managers use and understand accrual‐based

financial statements. By concentrating on cash flows, the financial managers should

be able to avoid insolvency and achieve the financial goals.

DECISION MAKING

The second key difference between finance and accounting is related to decision making.

Accountants devote their attention to the collection and presentation of financial data. On

the other hands, the attention of financial managers is devoted to evaluate the accounting

statements, develop additional data and make decisions on the basis of their assessment of

the associated risks and returns. This does not mean that accountants never make decisions

or that financial managers never gather data. Rather, the primary focuses of accounting and

finance are distinctly different.

ROLE OF THE FINANCIAL MANAGER

In addition to financial analysis and planning, the financial manager’s primary activities

include making investment decisions and making financing decisions. Investment decisions

determine the mix and the type of assets held by the business. Financing decisions

determine the mix and the type of financing used by the business. These types of decisions

can be viewed in terms of the firm’s balance sheet, as shown in Error! Reference source not

found.. However, the decisions are actually made on the basis of their cash flow effects on

the overall value of the firm.

Financial Management Page | 17

Figure 1: The decisions made by finance managers

Source: Gitman et al. (2012)

As mentioned above, as companies grow and become owned by increased numbers of

individuals/organizations (shareholders), the owners are not directly involved in the day to

day decision making but employ managers to represent their interests and make decisions

on their behalf. Therefore the financial Manager would be expected to answer the

questions raised above.

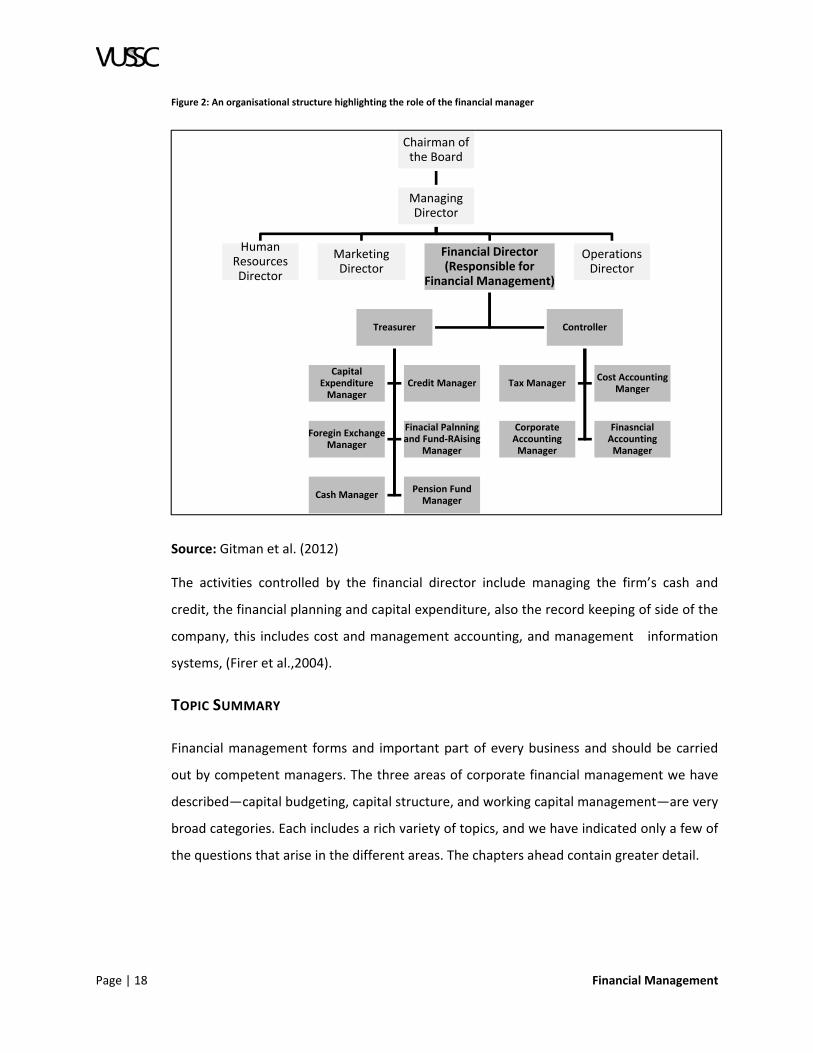

The roles and responsibilities of the Financial Manager are usually associated with the top

officer of an organization for example, the Financial Director or the Chief Finance Officer.

The adoption of organizational structure highlighting the financial activities within a firm is

shown in Figure 2.

Page | 18 Financial Management

Figure 2: An organisational structure highlighting the role of the financial manager

Source: Gitman et al. (2012)

The activities controlled by the financial director include managing the firm’s cash and

credit, the financial planning and capital expenditure, also the record keeping of side of the

company, this includes cost and management accounting, and management information

systems, (Firer et al.,2004).

TOPIC SUMMARY

Financial management forms and important part of every business and should be carried

out by competent managers. The three areas of corporate financial management we have

described—capital budgeting, capital structure, and working capital management—are very

broad categories. Each includes a rich variety of topics, and we have indicated only a few of

the questions that arise in the different areas. The chapters ahead contain greater detail.

Chairman of the Board

Managing Director

Human Resources Director

Marketing Director

Financial Director (Responsible for

Financial Management)

Treasurer

Capital Expenditure Manager

Credit Manager

Foregin Exchange Manager

Finacial Palnning and Fund‐RAising

Manager

Cash Manager Pension Fund Manager

Controller

Tax Manager Cost Accounting

Manger

Corporate Accounting Manager

Finasncial Accounting Manager

Operations Director

Financial Management Page | 19

Self‐Reflection Question

In your own words, describe the responsibilities that Financial Managers are charged

with in an organisation and the kind of decisions that they have to make, your answer

should reflect on the discussion above.

UNIT 1 REFERENCES

1. Geoffrey, A. Hirt, Bartley R. Danielsen Stanley B. Block (2009) Foundations of Financial

Management. McGraw Hill. ISBN: 0073363774 / 0‐07‐336377‐4

2. Brigham, F. Eugene and Houston, F. Joel (2012) Fundamentals of Financial management.

South‐ Western, Cengage Learning, Ohio, ISBN 13: 978‐0‐538‐47712‐3

3. Chandra Prassana (2010) Fundamentals of Financial Management. Tata McGraw Hill.

New Delhi in

http://books.google.co.uk/books?id=osy4UMOgpG4C&printsec=frontcover&dq=fUNDAME

NTALS+OF+FINANCIAL+MANAGEMENT,&hl=en&sa=X&ei=yJN_UZnaBMX5PLrDgdAD&sqi=2

&ved=0CFIQ6AEwAw accessed 24/04/13

Page | 20 Financial Management

UNIT 1 – SUMMARY

ASSIGNMENTS AND ACTIVITIES

The end of topic assignments have been employed to assess student learning for this unit.

Further activities could be incorporated in the students’ assignments that are to be

developed by the respective participating institutions.

SUMMARY

The topics covered in this unit underscore the importance of financial management for the

various forms of companies. The roles of finance managers in an organisation have been

outlined. The financial decisions the managers have to make in order to realise value to

stakeholders from the operations of the company call for managers to be more analytical in

the performance of their day to day finance activities. These issues are covered in the units

that follow.

NEXT STEPS

Having understood the basics of financial management, we shall now explore more

important avenues in an organisation, remember that activities of an organisation are

recorded and reported, we will therefore look at the various reports and how they are used

in an organisation to make economic sense.

Financial Management Page | 21

UNIT TWO ‐ FINANCIAL INSTITUTIONS AND MARKETS

UNIT 2 INTRODUCTION

Financial institutions are responsible to channel the savings of individuals, businesses and

governments into loans or investments. Financial institutions serve its users as the main

source of funds. Majority of individuals and businesses rely heavily on funds from financial

institutions, in the form of loans for their financial support. They are regulated by

regulatory guidelines from governments and are required to operate within these

guidelines. Financial markets are the intermediaries that facilitate an efficient transfer of

resources from severs to who need for them. The financial markets are responsible to

contribute in economic development by providing channels for allocation of savings to

investment.

UNIT 2 OBJECTIVES

Upon completion of this unit you will be able to:

1. Explain how financial institutions serve as intermediaries between investors and

firms.

2. Explain various types of financial institutions and how they work.

3. Provide an overview of financial markets.

4. Explain how investors and business firms trade money market and capital market

securities in the financial markets in order to satisfy their needs.

5. Identify the major securities exchanges.

6. Understand derivative securities and explain why investors and firms use them.

7. Describe the role of foreign exchange market.

UNIT 2 READINGS

To complete this unit, you are required to read the following chapters:

Gitman, Lawrence J. Web Chapter Financial Markets and Institutions available at

http://wps.aw.com/wps/media/objects/5448/5579249/FinancialMarketsandInstitutions.pd

f

UNIT 2 ASSIGNMENTS AND ACTIVITIES

(a) Identify the major financial institutions present in your country and explain the major

services offered by them. (Hint: Identify minimum 2 and maximum of 4 institutions.)

(b) Identify a major organized securities exchange in your country and explain how it is

different from a organized securities exchange in a foreign country. (Hint: Difference on the

basis of number and type of requirements to be listed on a securities exchange for trading.)

Page | 22 Financial Management

TOPIC 2.1 FINANCIAL INSTITUTIONS

INTRODUCTION

Financial institutions are the intermediaries and channel the savings of individuals,

businesses and governments into loans or investments. With trillions dollar worth of

financial assets under the control of financial institutions, they are regarded as major

players in the financial marketplace. They frequently serve businesses and individuals as the

main source of funds. Some financial institutions lend the money, accepted from

customers’ savings deposits, to other customers or to businesses that needs them.

Generally, many individuals and businesses rely heavily on funds, in the form of loans, from

institutions for their financial support. The government establishes regulatory guidelines for

financial institutions and these institutions are required to operate within these guidelines.

OBJECTIVES

Upon completion of this topic you will be able to:

1. Understand how different financial institutions serve as intermediaries between

investors and firms.

2. Identify different types of financial institutions and the services provided by them.

MAJOR CUSTOMERS OF FINANCIAL INSTITUTIONS

The major suppliers and the major demanders of funds to and from financial institutions

are individuals, businesses and government. The large portion of funds in financial

institutions are provided by the individual consumers’ savings. Individuals not only are the

suppliers of the funds to financial institutions but are also the demanders of funds from

financial institutions in the form of loans. Although, the net suppliers for financial

institutions are individuals, as a group the amount of money saved by individuals is more

than what they borrow. Also, businesses primarily deposit some of their funds in checking

accounts with various commercial banks or financial institutions. Businesses also borrow

funds from financial institutions like individuals, but businesses are considered as the net

demanders of funds. The amount of money borrowed by businesses is more than what is

saved by them.

Governments are another customer of financial institutions. They maintain deposits of tax

payments, temporarily idle funds and Social Security payments in commercial banks.

Governments do not borrow funds directly from financial institutions, although they

indirectly borrow from them by selling their debt securities to various institutions. The

government is another net demander of funds like businesses and typically borrows more

than what it saves.

There are different types of financial institutions and few most important financial

institutions that facilitate the flow of funds from investors to business firms are commercial

Financial Management Page | 23

banks, mutual funds, security firms, insurance companies and pension funds. A detailed

discussion of each of these financial institutions can be found below.

COMMERCIAL BANKS

Deposits from savers are accumulated by commercial banks and are used to provide credit

to businesses, individuals and government agencies. Thus they provide service to the

investors who desire to invest funds in the form of deposits. Commercial banks provide

personal loans to individuals and commercial loans to business firms by using the deposited

funds. The deposited funds are also used to purchase debt securities issued by business

firms or government agencies. Commercial banks serve as a key source of credit to facilitate

expansion of businesses. In the past, commercial banks were the only dominant direct

lenders to businesses. However, in recent years other types of financial institutions have

begun to advance more loans to the businesses. The objective of the commercial banks are

to generate earnings for their owners which is similar to most other types of business firms.

Generally, the commercial banks generate earnings by receiving a higher return by using

their funds as compared to the cost they incur from obtaining deposited funds. The paid

average annual interest rate on the obtained deposits is usually lower than the rate of

return earned on the funds. For example, a bank may pay an average annual interest rate of

3 percent on the obtained deposits and may receive a return of 8 percent on the invested

funds as loans or as investments in securities. Commercial banks can charge a higher rate of

interest on high risk loans, however, with higher risk loans they are more exposed to the

possibility that these loans will default.

The traditional and very important function of commercial banks are accepting deposits

and using those funds for loans or to purchase debt securities. In addition to this function,

banks now perform many additional functions as well. In particular, commercial banks

generate fees by providing services such as foreign exchange, traveller’s cheques, personal

financial advising, insurance and brokerage services. In short, the commercial banks are

able to offer customers one stop shopping experience.

SOURCES AND USES OF FUNDS AT COMMERCIAL BANKS

Mainly, most of the funds of commercial banks are obtained by accepting deposits from

investors (customers). These customers of commercial banks are usually individuals, but

some of them are firms and government agencies that have excess cash. Some of these

deposits are held at banks for very short periods, such as a month or less than a month.

Commercial banks also able to attract deposits for longer time periods by offering

certificates of deposit, which specify a minimum deposit level e.g. 2,000 and a particular

maturity time frame (such as 1 year or so). Because most of the commercial banks offer

certificates of deposit with various different maturities, they effectively diversify the times

at which the deposits are withdrawn by investors.

Page | 24 Financial Management

Deposits at commercial banks are insured up to a certain amount by an independent

agency to maintain stability and public confidence e.g. Federal Deposit Insurance

Corporation (FDIC) in United States. It guarantee the safety of depositor's accounts in

member banks. The insurance of deposits helps to reduce the fear of depositors about the

possibility of a bank’s failure. Therefore, it decreases the possibility that all depositors will

try to withdraw their deposits from banks simultaneously. As a result the banking system

can efficiently facilitates the flow of funds from savers to borrowers.

Most of the funds of commercial banks are either used to provide loans or to purchase debt

securities. In both of the cases they serve as creditors that provide credit to those

borrowers who need funds. Commercial banks provide commercial loans to businesses,

make personal loans to individuals and purchase debt securities issued by business firms or

government agencies. Most business firms rely heavily on commercial banks as a source of

funds. Some of the commonly known means by which commercial banks extend credit to

businesses are term loans, lines of credit and investment in debt securities issued by firms.

Term loans are provided by banks for a medium‐term to finance the investment of a

business in machinery or buildings. For example, consider a manufacturer of toy trucks that

plans to produce toys and sell them to retail stores. The manufacturer will need funds to

purchase the machinery for producing toy trucks, to make lease payments on the

manufacturing facilities and to pay its employees. With the passage of time, the business

will generate cash flows that can be used to cover mentioned expenses. However, there is a

time lag between the cash outflow (expenses) and cash inflow (revenue). This time lag

occurs because of the difference in time when the business must cover these expenses and

when it receives revenue. The term loan enables the business to cover its expenses until a