Defining “Materiality” and “Significant Deficiency”

26

#ACIDCAA ACI’s 4 th DCAA & DCMA Audit & Compliance Boot Camp J. Catherine Kunz Partner Defining “Materiality” and “Significant Deficiency” Key Qualitative and Quantitative Factors Jennifer P. Flickinger Partner July 21-22, 2014 Tweeting about this conference?

Transcript of Defining “Materiality” and “Significant Deficiency”

#ACIDCAA

ACI’s 4th DCAA & DCMA Audit & Compliance Boot Camp

J. Catherine Kunz

Partner

Defining “Materiality” and “Significant Deficiency”

Key Qualitative and Quantitative Factors

Jennifer P. Flickinger

Partner

July 21-22, 2014

Tweeting about this conference?

#ACIDCAA

Agenda

• Defining Materiality

• Applying Materiality to Business Systems • Material Noncompliances

• Significant Deficiencies

• Impacts of Material Noncompliances and Significant Deficiencies

• Avoidance and Defense

#ACIDCAA

Materiality Defined

• No definition of Material or Materiality in FAR 2.101

• Lack of definition leaves contractor looking for clues in regulations, government guidance, financial accounting and case law

Merriam-Webster: “having real importance or great

consequences”

#ACIDCAA

Materiality Defined - GAAP

• Recognizes that materiality judgments must be made in light of surrounding circumstances

• Require both quantitative and qualitative characteristics

“Information is material if omitting or misstating it could influence decisions that users make …..In other words, materiality is an entity-specific aspect of relevance

#ACIDCAA

Materiality - DCAA

•DCAA does not define materiality • Provides only vague guidance

• Yet the concept of materiality is found throughout the DCAM

“The concept of materiality recognizes that some matters, either individually or in the aggregate, are important for fair presentation of a subject matter

or an assertion while others are not” (2-309)

#ACIDCAA

Materiality - DCAA

•DCAA provides one useful quantitative guideline within its guidance • FAR defective pricing clauses provide that the

Government is entitled to remedies if a contract price was increased by “any significant amount”

• DCAA guidance states that price adjustments of $50,000 or less than 5% of contract price are normally considered immaterial

#ACIDCAA

Materiality – DCAM

• Some guidance is provided with respect to ICAPS (3-405)

• Materiality is determined based on the importance of the contractor accounting or management systems relative to government contracts

• Auditors must consider the dollar values of transactions • Total dollar value of transactions processed

• Total government contract costs

• Total contractor operations

#ACIDCAA

Materiality - DCMA

•Guidance is again vague (DCMA-INST 208) • Materiality is a matter of professional

judgment

• Judgments consider surrounding circumstances

• Involve qualitative and quantitative considerations

#ACIDCAA

Materiality - CAS

• Establishes qualitative criteria for Materiality in 9903.305: • Absolute dollar amount

• Amount of contract cost compared to the amount under comparison

• Relationship between a cost and a final cost objective (e.g., direct versus indirect cost)

• Impact on government funding

• Cumulative effect of individual material items

• Cost of administrative procedure of a price adjustment

#ACIDCAA

Materiality - CAS

• CASB addressed materiality in its Statement of Operating Procedures (1977/1979) • Cost of an accounting practice shall not exceed its benefit

• “…allocation of costs shall not be so stringently interpreted that the desired benefits are negated by excessive administrative costs.”

• Throughout the Preambles the board routinely declines to establish quantitative criteria, preferring to preserve “exercise of judgment”

#ACIDCAA

APPLYING MATERIALITY TO BUSINESS SYSTEMS

#ACIDCAA

Material Noncompliance

•DCAA audit guidance (12-PAS-012(R)): • A material non-compliance “indicates a

significant deficiency/material weakness exists and that the contractor has not complied in all material respects with the DFARS criteria”

#ACIDCAA

Material Noncompliance

•What makes a noncompliance material? • Nature and Frequency of the noncompliance

• Whether the noncompliance is material considering nature of the compliance requirements

• Root cause

• Effect of compensating controls

• Possible future consequences

• Qualitative considerations, including the needs and expectations of the reports users

#ACIDCAA

Material Noncompliances

•Additional factors for consideration: • History of noncompliances found in contractor

assertions requiring correction

• Identification of material noncompliances with applicable Government contract laws and regulations (i.e., FAR subpart 31.2 or CAS)

#ACIDCAA

Material Weakness

•Defined as “a deficiency or combination of deficiencies in internal controls such that there is a reasonable possibility that a material noncompliance … will not be prevented, detected and corrected on a timely basis”

#ACIDCAA

Material Weaknesses

•Not necessary to demonstrate an actual monetary impact to the government to report a material weakness/material noncompliance

• Only that there is a reasonable possibility that it could happen

#ACIDCAA

Significant Deficiency

•DFARS 252.242-7005 (a) definition: • “A shortcoming in the system that materially affects the ability of

officials of the Department of Defense to rely upon information produced by the system that is needed for management purposes”

•DCAA guidance clarifies that “a significant deficiency will generally represent a material weakness in internal control”

#ACIDCAA

Significant Deficiency

•DCAM provides further insight: • Deficiencies “with significant dollar impact on existing

or future contracts or which require the contractor take corrective action” (4-303.2)

• Systemic problems (4.707.7)

• When a weakness requires additional audit procedures to protect the Government’s interest because the contractor’s internal controls are unlikely to accomplish an applicable control objective (5-109)

#ACIDCAA

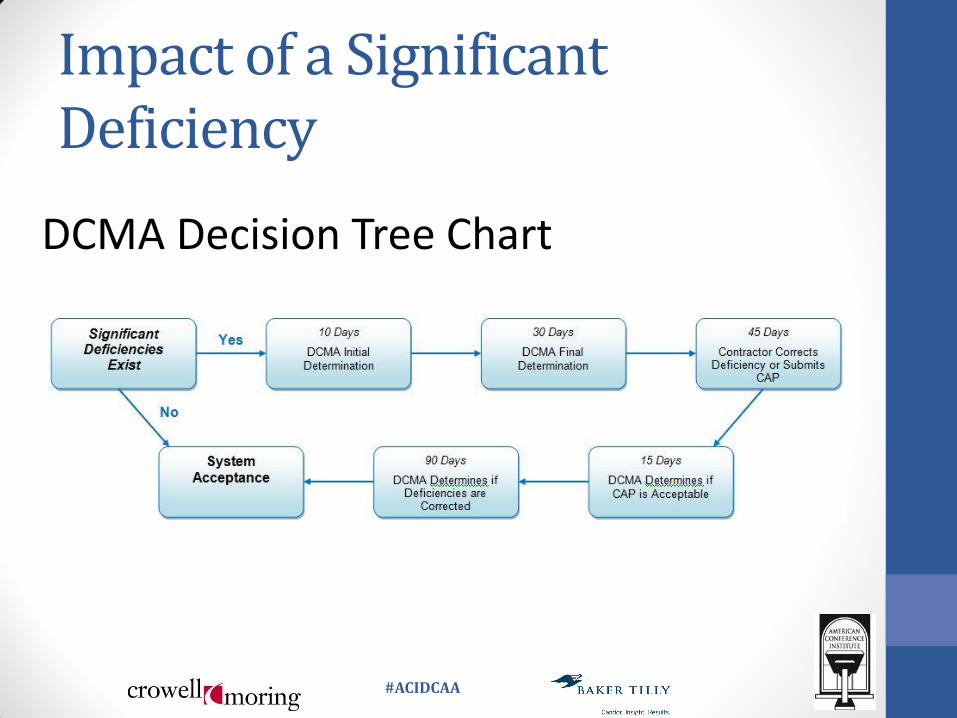

Impact of a Significant Deficiency

DCMA Decision Tree Chart

#ACIDCAA

Impact of a Significant Deficiency • Payment withholds of 5% for one

disapproved system or up to 10% for two or more disapproved systems

• Withholds must be reduced: • from 5% to 2% when implementation of an approved

corrective action plan (“CAP”) begins • By half when the government fails to act within 90 days

of receiving notice of a completed CAP • Eliminate the withhold when the ACO has a reasonable

expectations that all significant deficiencies are cured

#ACIDCAA

Impact of a Significant Deficiency • DCMA position: Withhold reduction

is prospective only

• Government must pay contract price upon delivery, essentially liquidating any withholds under the contract

• Timing of reductions and end of withholds is open ended

#ACIDCAA

Impact of a Significant Deficiency • Non-compliance with Business

System criteria can lead to lost business • Results recorded in DCMA’s Contractor Business Analysis

Repository (CBAR)

• This system can include draft audit report data, potentially leading PCOs to rely on draft findings when awarding/negotiating a contract

• Non-compliance with Business System criteria can lead to increased compliance and monitoring costs

#ACIDCAA

Avoidance and Defense

•Materiality is a very difficult argument to win outside of litigation • Materiality is in the eye of the beholder

• Focus on DCAA’s assertion of materiality or “reasonable possibility” of harm

•No case law exists surrounding materiality and its application to business systems

#ACIDCAA

Avoidance and Defense

• Your best defense is a good offense • Adequately document policies, procedures, and controls captured

in a surveillance plan

• Identify primary controls, as well as compensating controls

• In anticipation of a Business System review, reconcile policies, procedures, and controls to DFARS Business System criteria

• Perform self-assessment, document results, implement applicable

corrective action plans

• Demonstration of training offered to employees and applicable

rosters

• Process flows for each system (high and low level detail)

#ACIDCAA

Avoidance and Defense

•Document materiality considerations when making unique business decisions regarding cost allowability and selecting cost accounting practices • This is especially true where the Standards require

contractors to deal with “material variances” (e.g., CAS 403, 407, and 418).

#ACIDCAA

Avoidance and Defense

•Define materiality and significant deficiency clearly within your policies and procedures • Accrual threshold • An account balance amount that will not trigger an unallowable

cost scrub • Amount below which employees are not required to justify price

reasonableness when they buy something

•Doing so puts the Government in a defensive position • They must now prove why your

definition of materiality is incorrect