morgan stanley November 2007 Morgan Stanley & Co. Incorporated

Next Generation WealthDefining A New DirectionThe Morgan Stanley Private Wealth Management/Campden Wealth Next Generation Wealth Report 2014

campdenresearch.com | i

Copyright © Campden Wealth Limited 2014

The contents of this publication are protected by copyright.All rights reserved. The contents of this publication, eitherin whole or in part, may not be reproduced, stored in adata retrieval system or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recordingor otherwise, without written permission of the publisher.Action will be taken against companies or individualpersons who ignore this warning. The information set forthherein has been obtained from sources which we believeto be reliable but this is not guaranteed. This publicationis provided with the understanding that the authors andpublisher shall have no liability for any errors, inaccuraciesor omissions therein and, by this publication, the authorsand publisher are not engaged in rendering consultingadvice or other professional advice to the recipient withregard to any specific matter. In the event that consultingor other expert assistance is required with regard to anyspecific matter, the services of qualified professionalsshould be sought.

First published 2014 by Campden Wealth Limited.17 State StreetNew York, NY 10004 USA

Campden Wealth LimitedT +44 (0)207 214 0555F +44 (0)207 214 0501E [email protected] www.campdenwealth.com

ISBN: 978-1-904471-19-6

ii | campdenresearch.com

campdenresearch.com | 1

ContentsPreliminariesAbout the Research 3About Morgan Stanley Private Wealth Management 3About Campden Wealth 4Foreword 5

Executive SummaryThe meaning of wealth 7Values are aligned 8A new philanthropy twist 8Investing interests and experience 8Forging adviser bonds 9Unplugging 9Formal education and more details sought 9

1. The Face of the Next Generation Key findings 11

1.1 The sample 12 1.2 Communication is key 13 1.3 Tracking the path to empowerment 14 1.4 The lost generation? 15 1.5 Higher education sought 16

2. Identifying Values and Lifestyle Key findings 17

2.1 What is wealth? 18 2.2 Family values aligned 21 2.3 Comfort comes with age 21 2.4 Parents strongly influence spending 22 2.5 Careers seen as central 24 2.6 Borrowing seen acceptable for core things 26

3. Philanthropy and the Family Key findings 29

3.1 Not your father’s philanthropy 30 3.2 Education remains top focus 30 3.3 Getting started 32 3.4 Finding a voice 32

2 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

4. Investing Through a Next-Gen Lens Key findings 35

4.1 Faith and interest in markets persists 36 4.2 Starting with the basics 37 4.3 Mission-related investments: high interest; little action 39 4.4 The risk/reward trade off 39 4.5 Equity leads on-line trading 41 4.6 Sourcing investment advice 42

5. Wealth Adviser Relationships Key findings 43

5.1 Getting their feet wet 44 5.2 Adviser relationships found stronger than many think 45 5.3 Hiring an adviser 46 5.4 Most Important Services 48 5.5 Engaging and Communication 49

6. Preparing for Transition Key findings 51

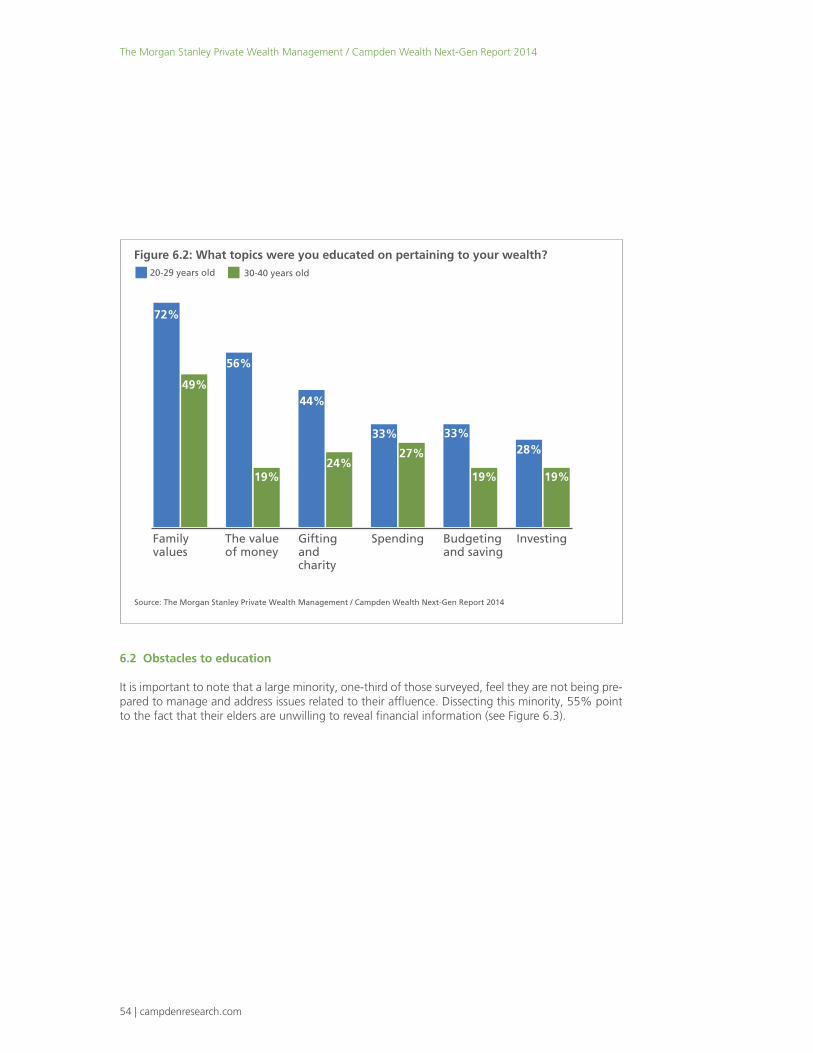

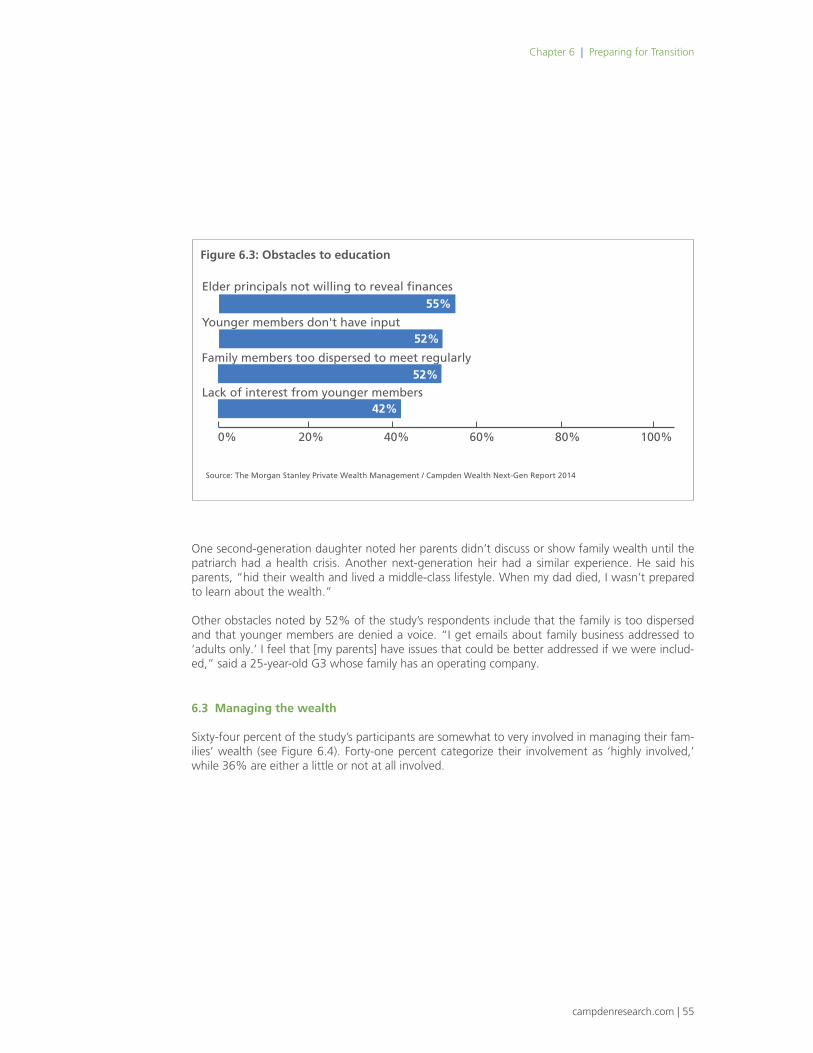

6.1 Families focus on values 52 6.2 Obstacles to education 54 6.3 Managing the wealth 57 6.4 Next-Gen feel ready to watch over wealth 57 6.5 Informal education is most common 57

7. Conclusion 61

Methodology 63

About the Author 64

About the Research Associate 64

Figures 67

campdenresearch.com | 3

About the Research

The Morgan Stanley Private Wealth Management/Campden Wealth Next Generation Wealth Report 2014 examines in detail the preferences, needs and challenges faced by the new inheritors as they step into roles as stewards and wealth creators and re-creators. It is a follow-up to last year’s research piece, which compared the concerns of the Next Generation and those of their elders as they face the responsibilities, benefits and challenges of wealth transition. The research is based on both qualitative and quantitative data from North America-based ultra-affluent individuals between the ages of 18-40 years old conducted in the second half of 2013.

About Morgan Stanley Private Wealth Management

Morgan Stanley Private Wealth Management (PWM) is an established global leader in wealth man-agement, dedicated to serving ultra-high-net-worth individuals, families and their foundations. Founded in 1977, Morgan Stanley PWM has been committed to helping its clients preserve and grow their financial, family and social capital for over 35 years.

Today Private Wealth Management oversees approximately $200 billion in assets and is the division exclusively focused on ultra-high-net-worth clients within Morgan Stanley. With over 350 private wealth advisers working out of over 40 offices, PWM maintains a presence in most metropolitan areas throughout the United States. The scale of Morgan Stanley PWM’s business allows it to provide a broad range of institutional-level services, delivered through the highly personalized experience of a small financial boutique.

Morgan Stanley PWM clients include many of the world’s most prominent and successful individuals and families—including 20% of the Forbes 400*. Some are entrepreneurs whose wealth is closely tied to the companies they founded, and others are executives whose companies Morgan Stanley has helped take public. Morgan Stanley PWM also serves artists, athletes, entertainers and families whose fortunes were created generations ago.

The breadth and depth of PWM’s personal client relationships have given Morgan Stanley PWM extensive experience in dealing with the complex and unique needs of the wealthy, and this insight is embodied in the team assembled to serve them. Drawing on a deep understanding of Morgan Stanley PWM’s clients’ financial lives, the firm helps them manage investments with an unwavering focus on their financial strategy and personal goals. Morgan Stanley PWM helps them structure their wealth and customize solutions based on an objective view of their needs.

* As of 12/31/2013

Preliminaries |

4 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

About Campden Wealth

Campden Wealth is the leading independent provider of information, news and education for gen-erational family business owners and family offices globally in person, in print, via research and online. Campden Wealth supplies market insight on key sector issues for its client community and their advisers and suppliers. Through in-depth studies and comprehensive methodologies, Campden Wealth provides unique and proprietary data and analysis based on primary sources. For more infor-mation about Campden Wealth and to see all previous reports please visit campdenresearch.com or email [email protected]. Campden Wealth also publishes the leading international business titles CampdenFB, aimed at members of family-owned companies in at least their second generation and CampdenFO, the international magazine for family offices and private wealth advisers. Campden Wealth further enhanced its international reach and community with the acquisition of the Institute of Private Investors (IPI), the leading membership network of private investors in the United States, founded in 1991.

For more information please visit www.campdenwealth.com

For inquiries, please contact Mindy RosenthalT: (+1) 212-693-1300E: [email protected]

campdenresearch.com | 5

Preliminaries |

Foreword

Dear Reader,

Over 30 years ago, we created Morgan Stanley Private Wealth Management to help a very exclusive group of clients address the complex and diverse challenges associated with significant wealth. From the beginning, we viewed this mission as a multi-generational endeavor. We provide the fullrange of products, services and intellectual capital needed to help our clients build enduring family legacies, generation after generation. We offer this study in that spirit.

The Next Generation Wealth Report 2014 is based on research conducted among young people from ultra-high-net-worth families. We endeavored to understand how the younger generations were preparing themselves to act as effective stewards of family wealth and as wealth creators in their own right. We were heartened to see that they overwhelmingly share their parents' core val-ues, and we were fascinated by the ways in which attitudes towards financial matters are evolving from generation to generation. We hope that you will find this study to not only be interesting, but also helpful in bringing the generations of your family together in productive conversation.

Since our inception, we have strived to live up to our promise of "doing first class business in a first class way" because our clients deserve no less. As you read through the following pages, I invite you to explore the opportunities Morgan Stanley Private Wealth Management can make available to you and your family.

Sincerely,

Douglas J. KettererHead of Strategy and Client Management

6 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Dear Reader,

The long-term success of a family ultimately rests with the ability of the younger generation to find its place and voice so that it can continue the family legacy while also stewarding and creating wealth. To do this, the ultra-affluent must determine a way to provide the Next Generation with the opportunity, tools and encouragement to develop.

During the spring and fall of 2013 Campden Wealth and Morgan Stanley Private Wealth Manage-ment conducted surveys and interviews of 87 ultra-high-net-worth individuals under the age of 40 to determine their views, challenges and needs on an array of topics, including investments, philan-thropy, adviser relationships and family values. This research is a companion piece to the Morgan Stanley Private Wealth Management/Campden Research Next Generation Study 2012, which com-pared the Next Generations with older generations to determine where they aligned and diverged on issues of sustaining long-term wealth.

We would like to thank all of the study’s participants for their willingness to share their personal ex-periences and time so that all families of affluence can better navigate the challenges of transition.

We would also like to thank Morgan Stanley Private Wealth Management for its continued and generous support of this valuable research project.

Additionally, I would like to thank the Campden Wealth/Institute for Private Investors team for their dedication and commitment to this research project.

It is our hope that the research will provide a stronger understanding of the Next Generation so that families and the financial services professionals who support them can better assist future generations in becoming the stewards, leaders, entrepreneurs and guardians of their family wealth and legacy.

Mindy Rosenthal

President, Institute for Private InvestorsManaging Director, N.A., Campden Wealth

campdenresearch.com | 7

Executive Summary |

Executive Summary

Communication + Education = Empowerment. That is the formula for a thriving Next Generation, which this study defines as individuals between the ages of 18 and 40 years old.

Understanding what needs to be accomplished for a family to prosper into the future is a first step. Successful execution, however, lies in determining how best to communicate with the Next Gener-ation and when to start informing them about the specific details of their wealth. Success lies not only in the process of teaching the Next Generation at levels commensurate with the skills they will need, but also focusing training within their individual interests and aptitudes.

Effective communication depends on understanding the interests, needs and requirements of the Next Generation and is central to the education process. As George Bernard Shaw said, “The single biggest problem with communication is the illusion that it has taken place.”

The Next Generation represents a broad swathe of individuals. The Next Generation Wealth Report 2014 builds on the findings of the 2012 study, which identified key needs and concerns of younger family members and compared and contrasted them to those of their elders. The goal of this second study is to further define what constitutes being a next-generation family member. It examines the influence of factors such as age and familial experience with wealth. And it addresses the following questions:

• What would they like to achieve with their wealth and how do they view their relationship to it?

• What constitutes philanthropy, how do they seek to approach giving and what do they wish to achieve?

• Are they comfortable with investments, how much experience do they have and in what areas?

• How do they feel about their family wealth advisers and how have they interacted with them?

• How prepared do they consider themselves for wealth transition and what resources would better ready them for this transition?

The meaning of wealthTo effectively communicate with the Next Generation about wealth management, it is critical that one understands how he or she view wealth and what he or she would like to achieve with it.

Affluence, at its core, is certainly about money, and what it can buy in terms of material goods, in-fluence and access, as well as the safety net it creates around typical life concerns regarding health-care, education and retirement. But for a good number of the study’s participants, it is something much more. Over half consider themselves stewards charged with sustaining the family wealth for future generations. And many view it in the context of a responsibility to support and promote causes that speak to their family values.

8 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Younger next-generation members, under 30 years old, and those from families that have had ex-perience with affluence, tend to be more altruistic than their older or newer-to-affluence cohorts.

Values are alignedFeelings about wealth often originate in parental values, and for older families of affluence, the values of grandparents. A strong work ethic, coupled with a desire to build a career and maintain it even after significant inheritances of wealth, are the norm. Most do not believe it is acceptable to borrow money for luxury goods, though they are comfortable doing so for education and first homes. And while older families appear to be more comfortable with borrowing money, it is largely in the context of investments and new business opportunities.

A new philanthropy twistPhilanthropy has long been part of the fabric of the ultra-high-net-worth community. It can be a highly effective means to communicate family values and teach the Next Generation joint-deci-sion-making, how to serve on a committee and the fundamentals of wealth management.

It is important to understand that, while the Next Generation is as philanthropic in spirit as the older generations, what they consider to be philanthropy and the way in which they approach the topic may differ greatly. To truly engage them, one needs to appeal to their interests and strategies of giving.

In general, the Next Generation is most comfortable with gifts whose impact can be measured and supported by data. They tend to want to make a distinct impact on the charity or organization they are supporting and so lean toward smaller organizations, where they often find an opportunity to be hands on.

Investing interests and experienceIn keeping with the Next Generation’s focus on philanthropy, they continue to express interest in mission-related investments, which are structured to provide a social or environmental as well as a financial return. Promoting this class of investments is a good way in which to attract the attention of the Next Generation and offers an opportunity for an opening conversation on investing. Though less than 5% of participants in the study are active in this area, about one-third is somewhat active in impact investments and another 21% in green opportunities.

Over 80% of the study participants are experienced stock and bond investors, with over half defin-ing themselves as highly experienced. Not surprisingly, with age comes an increase in investment sophistication. Those aged between 30 and 40 years old tend to be far more willing to take on additional risk for the possibility of higher returns. They are more experienced than their younger counterparts in investing in traditionally riskier and more sophisticated asset classes such as private equity, direct investments and hedge funds.

campdenresearch.com | 9

Forging adviser bondsMost of the Next Generation begin working with family advisers about the time they start learn-ing to invest, typically in their late teens and twenties. There is a direct correlation between how educated, and by association, how empowered, a next-generation family member is or feels she is and her comfort and happiness with family advisers and wealth plans. The majority of this study’s participants are engaged with advisers—but only half are highly likely to retain their family adviser. This percentage is far higher than other research findings and is likely influenced by the more so-phisticated wealth management education and higher level of wealth management participation of the respondents in this study.

UnpluggingDespite their reputed love of social media, high connectivity and all things technological, when it comes to communicating with their advisers the Next Generation overwhelmingly prefers in-person interaction, phone conversations and email.

Online access is favoured for tasks associated with viewing data, such as reviewing holdings and performance statements. Additionally, over half of the study respondents trade on-line and consider mobile trading platforms to be important.

Formal education and more details soughtMost of the Next Generation learn about their wealth and financial matters in an unstructured fash-ion, but a strong majority are interested in participating in more formal programs.

Families tend to informally discuss issues of affluence, and the Next Generation learn by observing and engaging in family conversations. These conversations are largely focused on values but also the basics of financial prudence such as spending, saving and budgeting as well as philanthropy. Although this year’s participants communicate well with elders, there remains a desire to obtain more details on the specifics of their family wealth and expected inheritances.

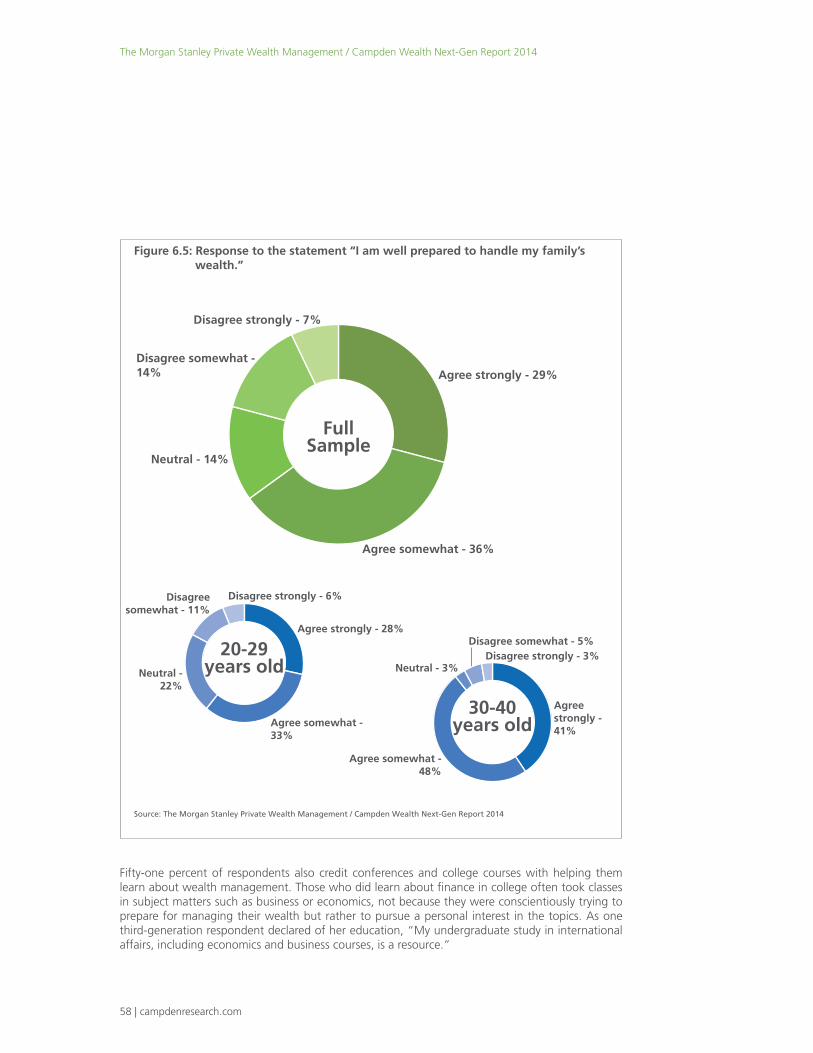

Unsurprisingly, those aged between 30 and 40 years old are more engaged in managing the family wealth than those under 30 years old and, as a result, feel ready to take on a greater number of financial responsibilities.

*A note about the data sample

The data in the study is examined based on two sample groups. One sample group represents questionnaire responses of the full sample consisting of 87 North American ultra-affluent individuals between the ages of 18-40. This data was reported in aggregate. Unless otherwise specified, the data results are from this full sample group.

A 57-member sub-sample was reported at a granular, individual level. Information gleaned from this sample was used to construct two demographic categories: generation (within affluent family) and age (of the next-generation member).

Executive Summary |

10 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 11

The Face of the Next Generation

KEY FINDINGS

From the sample of 87 North American ultra-high-net-worth individuals:

n Thirty-eight percent of those sampled are between 18 and 29 years old; 62% are between 30 and 40 years old

n Over half, 57%, have a family net worth higher than $100 million

n Approximately 65% have received some distributions

n More than half, 58%, share assets with other family members

n Thirteen percent are first generation; 35% are second generation; 52% are third generation

n Ninety-seven percent hold an undergraduate college degree; 48% have advanced degrees

1Chapter 1 | The Face of the Next Generation

12 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

This study takes an in-depth look at the attitudes, knowledge, experiences and preferences of next-generation wealth creators and inheritors. We define the Next Generation as individuals who are between 18 and 40 years old, covering a period of time that begins when young adults start learning the specifics of their wealth and ends as they assume positions of responsibility for manag-ing it. While they can be wealth creators, approximately 90% of the research sample is comprised of those who have inherited their wealth.

This research is the companion to the 2012 Morgan Stanley Private Wealth Management/Campden Research study Next Generation Wealth: the new face of affluence, which considered the ways in which the experiences of older generations impacted the thoughts and feelings of younger gen-erations regarding wealth stewardship and re-creation, as well as where their views aligned and diverged. Here we come back to take a closer look at the Next Generation—their values; investment interests and acumen; thoughts on and experiences with adviser relationships; philanthropic inter-ests and pursuits; family dynamics; and wealth transition readiness. 1.1 The sample

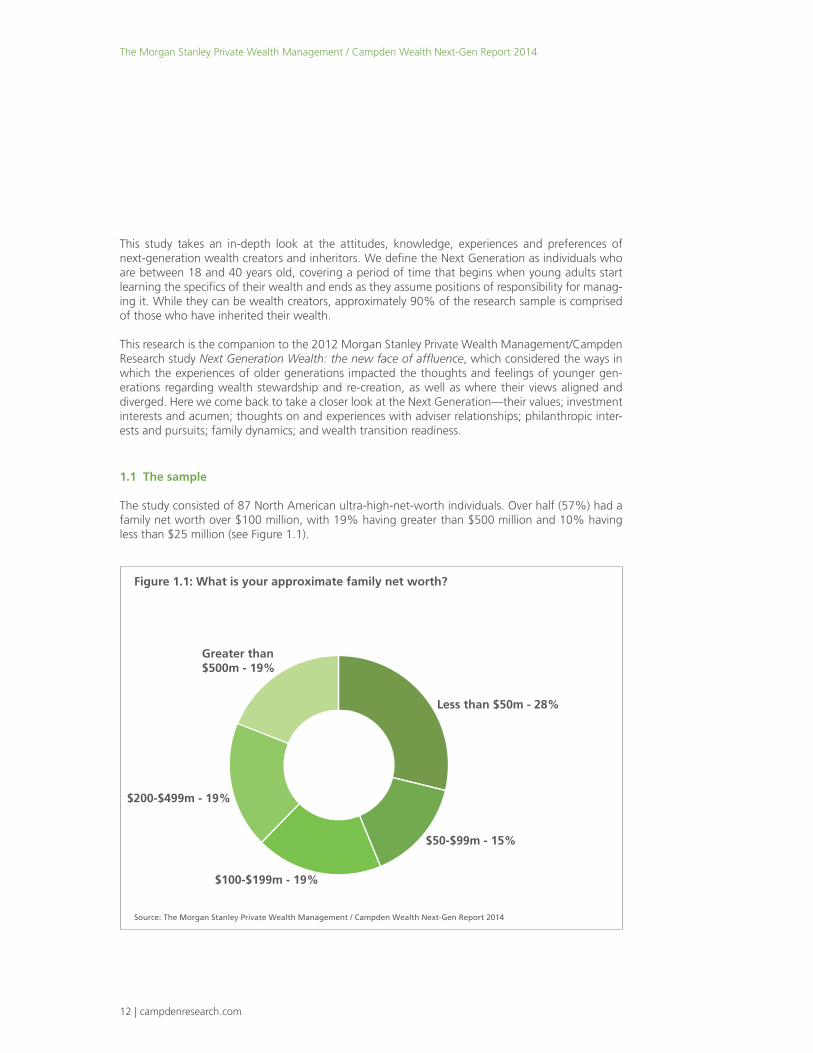

The study consisted of 87 North American ultra-high-net-worth individuals. Over half (57%) had a family net worth over $100 million, with 19% having greater than $500 million and 10% having less than $25 million (see Figure 1.1).

Figure 1.1: What is your approximate family net worth?

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Greater than $500m - 19%

Less than $50m - 28%

$50-$99m - 15%

$100-$199m - 19%

$200-$499m - 19%

campdenresearch.com | 13

The majority had previous experience with wealth transition and, therefore, had addressed issues pertaining to managing wealth on some levels. In general, age is a factor when it comes to inher-itance; the older the family member, the more likely they are to have received a greater portion of their inheritance. Approximately 65% of the respondents have received some distribution of family wealth. Though almost all said they had an individual net worth of less than $25 million because they had yet to inherit the bulk of their potential share of family wealth.

“I am a rich kid in name only,” said one 25-year-old scion of a family with a net worth between $200 million-$499 million. He added that he would need to wait until his 50s before receiving the bulk of his inheritance.

1.2 Communication is key

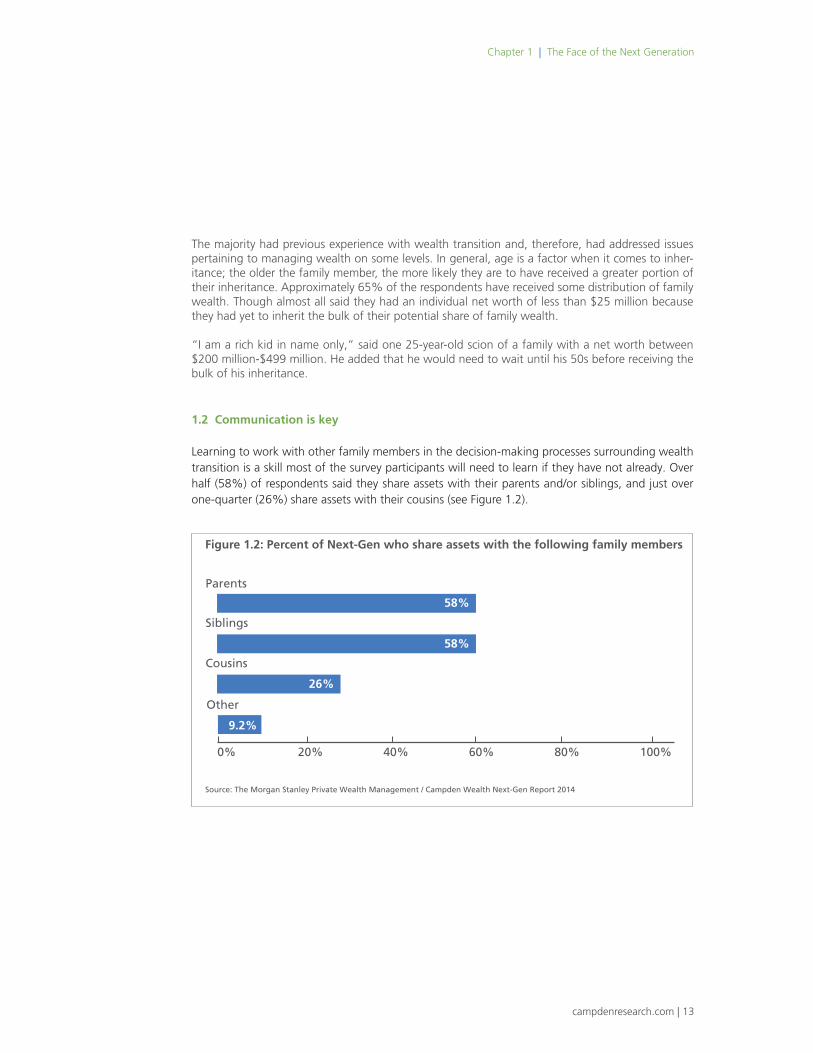

Learning to work with other family members in the decision-making processes surrounding wealth transition is a skill most of the survey participants will need to learn if they have not already. Over half (58%) of respondents said they share assets with their parents and/or siblings, and just over one-quarter (26%) share assets with their cousins (see Figure 1.2).

Figure 1.2: Percent of Next-Gen who share assets with the following family members

Cousins

26%

Other

9.2%

Siblings

23% 58%

Parents

18% 58%

0% 20% 40% 60% 80% 100%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 1 | The Face of the Next Generation

14 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

“I was chosen, in part, because I’m one of the only siblings who’s speaking to everyone,” said a second-generation sibling from a large family who now runs her family office. Being able to com-municate is essential, she underscored.

1.3 Tracking the path to empowerment

In the 2012 Next Generation Wealth study, we documented the path to empowerment, whereby those in their early 20s began to learn the details of their family’s wealth picture and how the dis-tribution of wealth would impact their lives. As they entered their 30s, the Next Generation began to take responsibility for stewarding wealth, while many of those in their late 30s and early 40s assumed a leadership role in managing the family wealth. This often involves taking the lead role in the family office, if one exists.

Over the course of this report, we will try to answer several pressing questions pertaining to the 18-40 year olds in our sample: How aligned with the values and concerns of their parents are these next generations? What are their spending habits and who influences their decision-making? What are they seeking from advisers?

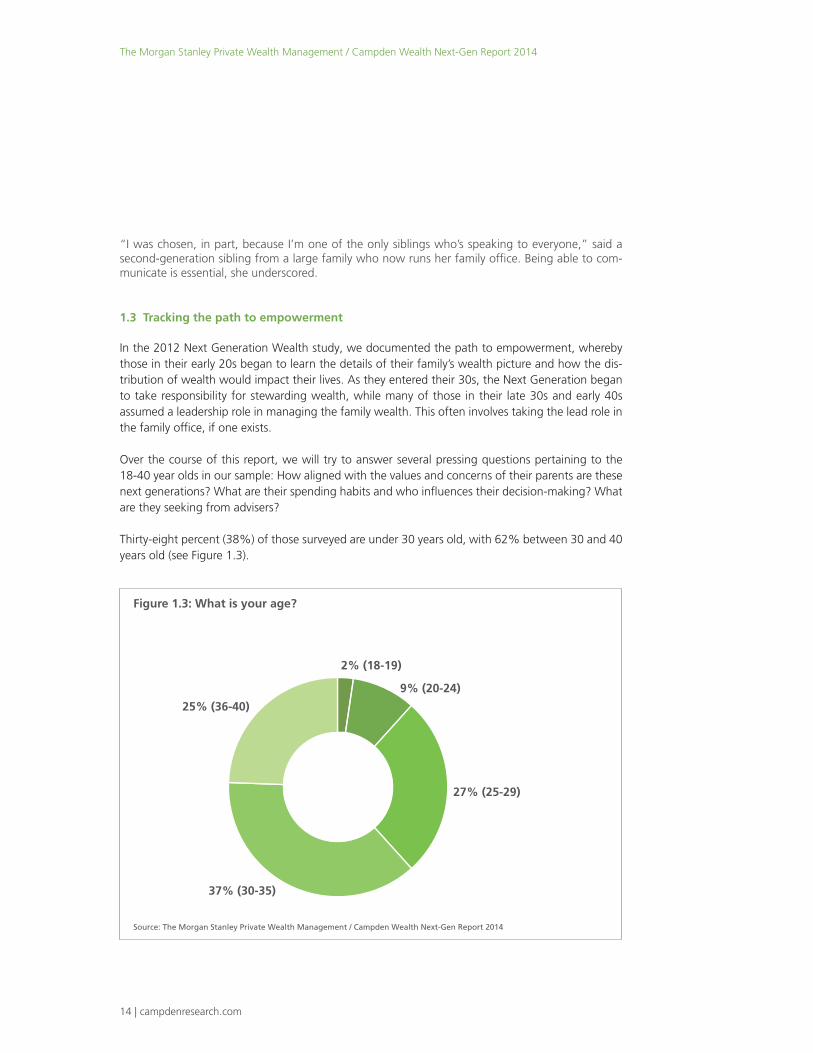

Thirty-eight percent (38%) of those surveyed are under 30 years old, with 62% between 30 and 40 years old (see Figure 1.3).

Figure 1.3: What is your age?

2% (18-19)

9% (20-24)

27% (25-29)

37% (30-35)

25% (36-40)

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 15

1.4 The lost generation?

All too often, the second generation is not as prepared as future generations for wealth transition. This can be the result of family inexperience with transition, that the wealth creators are so focused on building the wealth they are not thinking about passing it on, or it can be the result of personality and relationship factors associated with strong matriarchs and patriarchs and their children.

In the 2012 Next Generation Wealth study, we anecdotally delved into this, positing a “Grandpar-ent Effect,” whereby wealth creators will often turn to a grandchild to lead the family. In this study we will take a deeper look at the impact that proximity to the wealth creator has on preparedness for wealth stewardship and roles related to wealth re-creation. We will compare the second-gener-ation to later generations in order to examine the impact of generational learning experience. We will also compare the experiences of second-generation family members in this study to those sur-veyed for the 2012 study. The differences between experiences may be attributed to the changes in attitudes associated with having younger parents who may have different feelings about preparing their children for ultra-affluence.

Just over half (52%) of the study’s respondents represented third or later generations, with 38% drawn from the second generation (see Figure 1.4).

Figure 1.4: What generation are you relative to the family's wealth creation?

1st - 10%

2nd - 38%

3rd - 24%

4th or greater - 28%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 1 | The Face of the Next Generation

16 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

1.5 Higher education sought

The respondents are a highly educated group. Almost all (97%) hold a college degree, and just under half (48%) hold advanced degrees. Just under a tenth (8%) said they received doctorate degrees or MBAs.

A number of those interviewed said they considered their education to be helpful in understanding issues pertaining to managing their wealth. This was particularly the case for those who held MBAs. But even those respondents who did not study to become wealth stewards and creators found courses in areas such as economics helpful.

campdenresearch.com | 17

Identifying Values and Lifestyle

2Chapter 2 | Identifying Values and Lifestyle

KEY FINDINGS

n Over half (55%) of respondents see themselves as stewards

n Those in their 20s appear more altruistic than those between 30 and 40 years old

n Third and later generations (defined as ≥G3) found to be more focused on the greater good

n Two-thirds (64%) believe their values are highly aligned with those of their elders

n About one-quarter (26%) of those under 30 years old are uncomfortable with their wealth

n Fifty-two percent expect to focus on investing once they inherit; 67% on their careers

n Older generations are more open to borrowing, particularly for business opportunities and investments

18 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

The most important factors influencing how next-generation family members approach their roles as wealth stewards and creators are the values and lifestyle habits passed on by their parents, grandparents and other family members. Having a solid understanding of the basics of wealth management and identifying the roles played by family advisers is paramount to the success of the family. But the lessons learned by watching how a family conducts itself when it comes to spending, savings, debt, philanthropy, entrepreneurialism and work will set the tone for how and if a family successfully passes on wealth to the Next Generation.

As a parent interviewed in the 2012 Next Generation Wealth study summed up the sentiment, “Create the values so children can make their own way and deal responsibly with assets.” Added another, “Our emphasis is teaching values. Forget about the money. It’s not about the money.”

2.1 What is wealth?

How a person views the meaning of wealth influences what they are trying to achieve with it. Some consider wealth in terms of money that can be spent or invested. Others see it more in terms of responsibility—the ability to affect change, provide for future generations or empowerment to pursue passions.

The Next Generation overwhelmingly defines wealth as total net worth, with 79% of respondents affirming this belief (see Figure 2.1). However, more than half (55%) of respondents also consider wealth as something for future generations. For these family members, the stewardship and preser-vation of wealth for generations to come will often impact spending and investment decisions. “We know the money is there, but none of us live as if the money is there. We’re all adjusting to what it means to be wealthy,” said a 34-year-old.

0% 20% 40% 60% 80% 100%

79%

55%

48%

46%

41%

40%

Providing for future generations

Total Net Worth

Ability to help the community

Empowerment to pursue what is important to me

Liquid Assets

Freedom from worry

Figure 2.1: How do you define wealth?

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 19

For 48% of respondents, ultra-affluence is a means of empowerment to pursue important goals or careers that might not have been possible had they needed to rely solely on their own incomes. “It feels weird, but this is a luxury, and luxury is not normal in the business world,” said a fourth-gen-eration son who used family money to support his business.

Often related to empowerment is the ability to help the community. As one wealth creator noted, “Wealth is defined to me as more freedom to help the community, be on the board of a credit union, help orphans and be in leadership groups.”

Some differences surface when comparing those between 30 and 40 years old with those aged between 20 and 29 as well as when comparing the group of second-generation (G2) respondents with those who have more familial experience with wealth.

The younger Next Generation group appears to be a little more altruistic than the older Next Gen-eration group. For example, 63% of those under 30 years old view wealth in terms of stewardship and providing for future generations, compared to 46% of those 30 to 40 years old (see Figure 2.1a). Additionally, 58% of the younger Next Generation group considers their affluence a vehicle to help the community, in contrast to 38% of the older Next Generation. Just under three-quarters (74%) of the younger Next Generation said their financial status let them pursue things that were important to them compared to 54% of those respondents aged between 30 and 40.

Providing for future generations

Figure 2.1a: Younger respondents found to be more altruistic

Ability to help the community

Empowerment to pursue what is important to me

63%

30-40 years old20-29 years old

46%

58%

38%

74%

54%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 2 | Identifying Values and Lifestyle

20 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

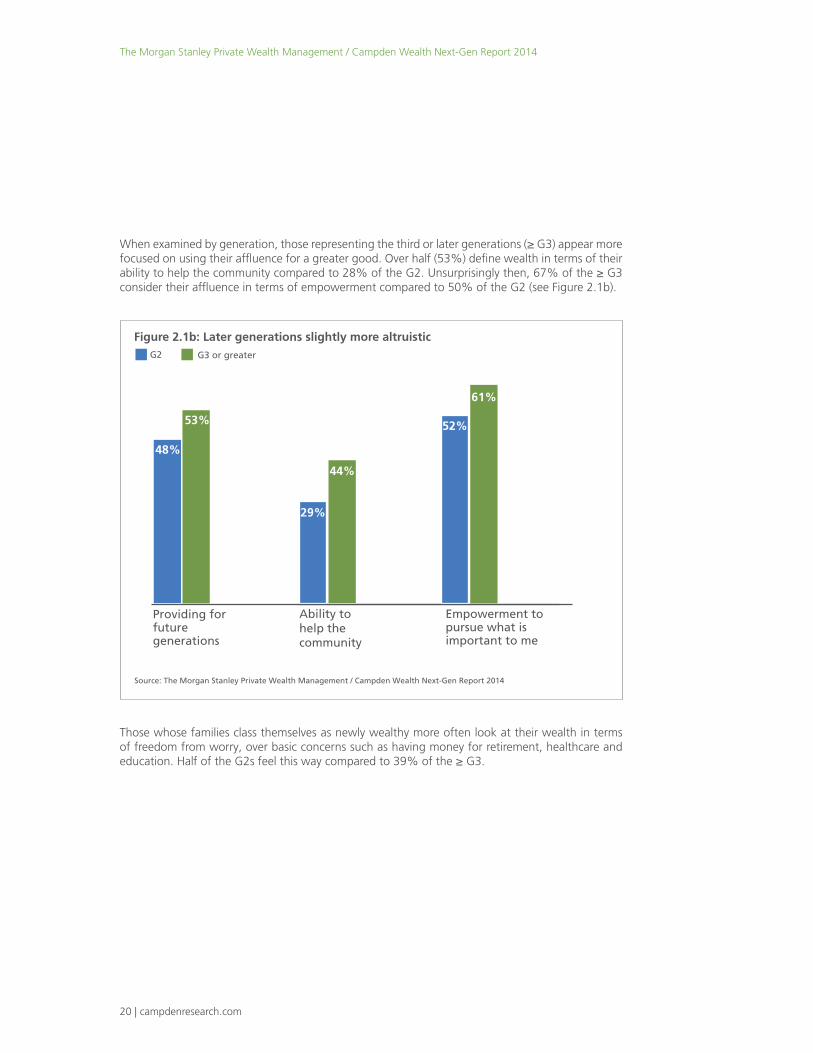

When examined by generation, those representing the third or later generations (≥ G3) appear more focused on using their affluence for a greater good. Over half (53%) define wealth in terms of their ability to help the community compared to 28% of the G2. Unsurprisingly then, 67% of the ≥ G3 consider their affluence in terms of empowerment compared to 50% of the G2 (see Figure 2.1b).

Those whose families class themselves as newly wealthy more often look at their wealth in terms of freedom from worry, over basic concerns such as having money for retirement, healthcare and education. Half of the G2s feel this way compared to 39% of the ≥ G3.

Figure 2.1b: Later generations slightly more altruisticG3 or greaterG2

Ability to help the community

Empowerment to pursue what is important to me

53%

29%

61%

52%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Providing for future generations

48%

44%

campdenresearch.com | 21

2.2 Family values aligned

Younger family members tend to base their values and attitudes regarding wealth on personal expe-rience and the actions of their parents and grandparents. Informal interactions, such as discussions around the dinner table, family gatherings and stories told by grandparents, all help to instill a sense of what is important to their families.

An overwhelming 95% state they recognize what is important to their families. And 64% believe their values are highly aligned with those of their parents. A mere 6% said they feel they have sig-nificantly different belief systems.

Across all of the age and generation groups examined, the study respondents underscored that they believe their family values help guide their lives. “The values are in the DNA of the family. Dad always said, ‘it’s part of your job to give back to the community,’” said a member of the third-gen-eration.

Another second-generation daughter who runs her family’s office said she took on this responsibility after seeing how her mother dedicated her life to caring for her family. “She existed to protect the family. Her example helps me maintain strong relationships with my brothers and sisters,” she said.

2.3 Comfort comes with age

Learning to become comfortable with wealth often comes with maturity and experience. It is not uncommon for younger inheritors to fear that people will judge them or, conversely, befriend them for their money. Many are concerned that others will attribute their accomplishments to privilege or they may feel this way themselves. Challenges can arise around everyday social situations with friends who have less disposable income than they do—should they supplement their friends or engage in less-expensive activities?

Indeed, 26% of those under the age of 30 say they are uncomfortable with their wealth while no respondent 30 years and older states this. “I only talk about my wealth with very good friends who know I have some money but no idea how much,” noted one younger survey respondent.

Comfort, however, does not require transparency. “It would be assumed that I would always pick up the tab,” added a 40-year-old, who said he did not reveal he had wealth to friends of lesser means.

Just under half of the study’s participants (47%) say they are either completely or very comfortable with their wealth, with 41% being somewhat comfortable (see Figure 2.2).

Chapter 2 | Identifying Values and Lifestyle

22 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

One reason for discomfort surrounding wealth is that 30% of those in the study said their re-lationships with friends, spouses and partners have been negatively affected by their affluence. “Many members of our extended family don’t work, and they have little kids,” said a 39 year-old fourth-generation family member. “They are not doing the best job teaching the fifth generation how to grow up wealthy,” he added. Still, 39% consider their wealth a positive and almost as many (31%) said it had no effect on their relationships with loved ones.

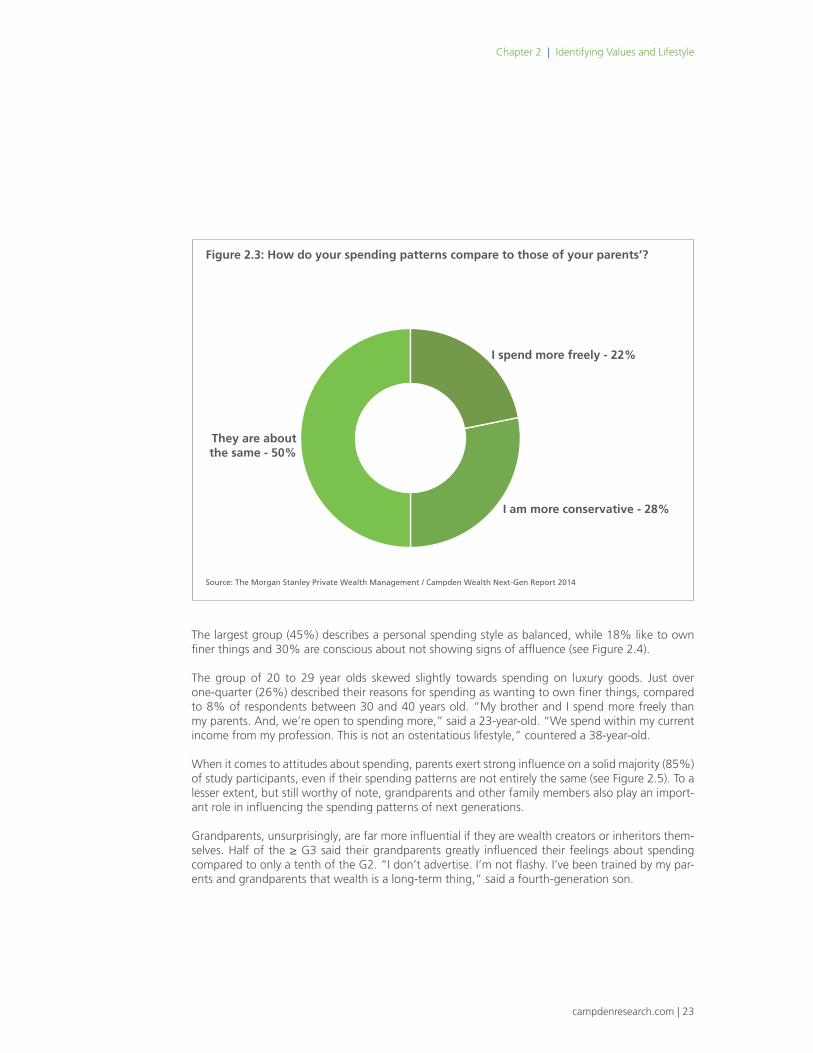

2.4 Parents strongly influence spending

Half (50%) of the study participants report spending patterns similar to those of their parents, with the other half roughly split between perceiving they are more conservative (28%) and thinking they spend more freely (22%) (see Figure 2.3).

Figure 2.2: How comfortable are you with your wealth?

Completely comfortable - 17%

Comfortable - 30%Somewhat comfortable - 41%

Uncomfortable - 12%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 23

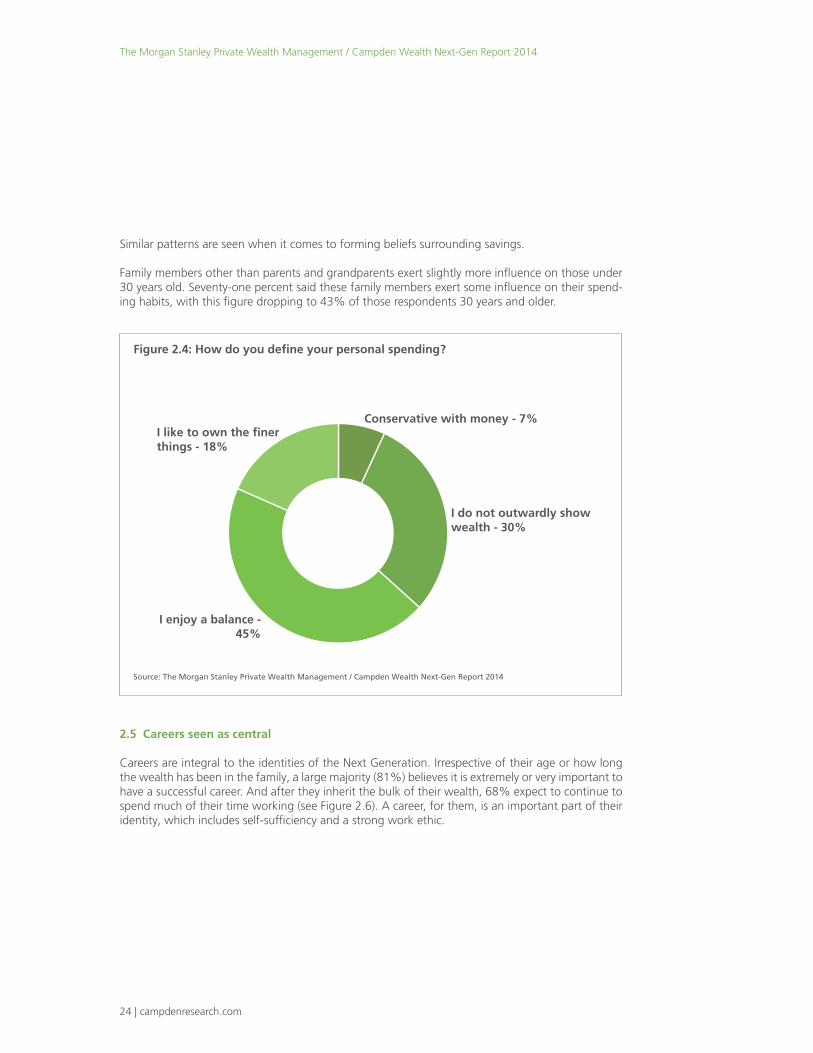

The largest group (45%) describes a personal spending style as balanced, while 18% like to own finer things and 30% are conscious about not showing signs of affluence (see Figure 2.4).

The group of 20 to 29 year olds skewed slightly towards spending on luxury goods. Just over one-quarter (26%) described their reasons for spending as wanting to own finer things, compared to 8% of respondents between 30 and 40 years old. “My brother and I spend more freely than my parents. And, we’re open to spending more,” said a 23-year-old. “We spend within my current income from my profession. This is not an ostentatious lifestyle,” countered a 38-year-old.

When it comes to attitudes about spending, parents exert strong influence on a solid majority (85%) of study participants, even if their spending patterns are not entirely the same (see Figure 2.5). To a lesser extent, but still worthy of note, grandparents and other family members also play an import-ant role in influencing the spending patterns of next generations.

Grandparents, unsurprisingly, are far more influential if they are wealth creators or inheritors them-selves. Half of the ≥ G3 said their grandparents greatly influenced their feelings about spending compared to only a tenth of the G2. “I don’t advertise. I’m not flashy. I’ve been trained by my par-ents and grandparents that wealth is a long-term thing,” said a fourth-generation son.

Figure 2.3: How do your spending patterns compare to those of your parents’?

I am more conservative - 28%

They are about the same - 50%

I spend more freely - 22%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 2 | Identifying Values and Lifestyle

24 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Similar patterns are seen when it comes to forming beliefs surrounding savings.

Family members other than parents and grandparents exert slightly more influence on those under 30 years old. Seventy-one percent said these family members exert some influence on their spend-ing habits, with this figure dropping to 43% of those respondents 30 years and older.

2.5 Careers seen as central

Careers are integral to the identities of the Next Generation. Irrespective of their age or how long the wealth has been in the family, a large majority (81%) believes it is extremely or very important to have a successful career. And after they inherit the bulk of their wealth, 68% expect to continue to spend much of their time working (see Figure 2.6). A career, for them, is an important part of their identity, which includes self-sufficiency and a strong work ethic.

Figure 2.4: How do you define your personal spending?

Conservative with money - 7%

I do not outwardly show wealth - 30%

I enjoy a balance - 45%

I like to own the finer things - 18%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 25

Figure 2.5: To what extent do the following influence your views about spending?

no influencestrong influence some influence

18%

52% 31%

42%

8%

51% 31%

7% 67% 26%

Friends and associates6% 46% 48%

School

4% 21% 75%

Religion

Other family members

26% 35% 39%

Grandparents

85% 15%

Parents

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Figure 2.6: Once you inherit wealth, how much of your time do you foresee dedicating to the following:

none of my timemuch of my time some of my time

19% 79% 2%Philanthropy

Creating new wealth through a business38% 38% 24%

20% 77% 3%Travel / Leisure

Stewarding the family’s wealth42% 50% 8%

Active in my community

10% 82% 8%

Investing

51% 44% 5%

Working

68% 30% 2%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 2 | Identifying Values and Lifestyle

26 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Working, investing and stewarding wealth are the top activities to which the Next Generation plan to allocate the majority of their time once they inherit. “I will get more hands-on and involved in managing the wealth,” said a member of a multi-generational family of his post-inheritance plans. While not their main focus, the Next Generation also plan to spend time on travel and leisure ac-tivities in addition to philanthropic pursuits. Over three-quarters of the study respondents plan to spend some of their time engaging in these pursuits.

2.6 Borrowing is acceptable for core things

The Next Generation is comfortable borrowing for activities that will contribute to their self-suffi-ciency or personal wealth. Over two-thirds (67%) said it is highly appropriate to borrow for educa-tion, and 53% feel the same way when it comes to borrowing for business opportunities. Taking on debt or tapping family wealth for a primary residence is also deemed highly appropriate by 63% of respondents (see Figure 2.7). Conversely, using family wealth or taking on debt for personal luxuries is deemed entirely unacceptable, with no respondents selecting this as a viable option.

32% 35% 21% 6% 6%Education

21% 42% 29% 2% 6%Primary residence

15% 38% 36% 8% 3%Business opportunities

7% 18% 38% 21% 16%For investments

3% 14% 34% 26% 23%Other homes

1% 7% 32% 60%At will

7% 28% 65%

For personal luxuries

Figure 2.7: When is it appropriate to borrow money?somewhat appropriateextremely appropriate very appropriate

not very appropriate not at all appropriate

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 27

“It’s okay to borrow for education—the best investment you can make in your family—or to start a business or to buy a home. No luxuries,” summed up a 39-year-old fourth-generation son. “Our parents may have assisted with the down payment for a home, but other than that, the home was affordable on our salaries,” added a second-generation daughter.

Those under 30 years old are slightly more inclined to borrow to start businesses, with 67% be-lieving this is highly appropriate compared to 43% of 30-40 year olds who think in the same way.

Those from third and later generation families who have more experience with wealth appear to be far more open to borrowing than second-generation inheritors although neither group is comfort-able borrowing for luxury goods (see Figure 2.7a).

Business opportunities

Figure 2.7a: Those experienced with wealth are more open to borrowing than second-generation inheritors

For investments

Education

G3 or greaterG2

37%

56%

16%

31%

42%

58% 58%61%

Primary residence

11%

22%

Other homes

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 2 | Identifying Values and Lifestyle

28 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 29

Chapter 3 | Philanthropy and the Family

Philanthropy and the Family

3KEY FINDINGS

n Sixty percent believe it is highly important to support charitable initiatives

nMany seek data to gauge effectiveness of gifts and hands-on experience

nThere is a clear and strong interest in impact/venture philanthropy

nForty-five percent of G2s are involved in philanthropy compared to 67% of G3s+

nThirty percent contribute to the philanthropic process but have no decision-making authority

nAlmost half (49%) are highly interested in serving on a non-profit board

nTwenty-five percent of respondents sit on their family’s grant-making committee

30 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Most North American families of significant means are philanthropic. Supporting charitable causes and philanthropic institutions is a central part of these families’ values—belief systems they are clearly passing on to the Next Generation. In fact, 60% of the study’s participants consider it highly important to use their family’s wealth to make a positive social or environmental impact, with only 13% considering it unimportant to do so.

But transmitting the spirit of charitable giving, community involvement and working for a cause that extends beyond the needs of the family does not necessarily translate into passing on similar interests or approaches. This chapter examines differences and commonalities between the way the Next Generation and the older generation view philanthropy, what they find of interest, how they approach it and what they are seeking to achieve.

3.1 Not your father’s philanthropy

The Next Generation tends to have a more expansive view of how they seek to impact change or provide support for causes or groups they consider important. For them, impact investments that retain double-bottom line remits of being profitable and having a social mandate, and business ventures aimed at boosting local employment, are ways of giving back to society. “My parents and I have very different views of philanthropy,” noted a 39-year-old third-generation son. “They have a passion for giving, which I find overrated. I would rather invest in companies, in plants.”

Additionally, these new generations of philanthropists often use performance data to track what the charity or foundation has achieved with donations and whether or not their cause is being addressed. Such data is also used to track the charity’s progress towards achieving its stated goals, and the effectiveness of its drive for self-sufficiency in recipient communities. A number of the study respondents noted that it is important to see their money at work and that they are not interested in simply writing a check.

These trends have put pressure on charities and institutions to measure and report progress, as well track donations and report what specifically has been done with those funds and how and if they have achieved goals. Additionally, they have created a generational shift in giving whereby the younger generation will often seek out charities where they can visit or work to see the impact of their gifts.

3.2 Education remains top focus

Education is by far the most common area of strong interest for the study participants, in-line with their parents’ interests. Sixty-five percent of those surveyed said they are highly interested in edu-cation and that 69% of their parents also focus their philanthropic efforts on education (see Figure 3.1).

campdenresearch.com | 31

With the support of 36% of respondents, Impact or Venture Philanthropy attracts the second-high-est level of interest, an area that attracts only 22% of parental support.

Arts and Culture is an area of high interest for 30% of the Next Generation but less so as compared to 34% of their parents. While the percentage difference is not that significant, the focus of their giving is. The Next Generation tends to be less interested in giving to traditional arts institutions such as classical production companies and concert halls, as well as art and history museums, a trend that threatens to pose a negative economic impact on established institutions. Recent examples of this impact include the New York City Opera, which was forced to close due to bankruptcy in 2013, and the San Francisco Opera, which has been noted in the press* as having financial difficulties and seeking actively to recruit the largess of the American ultra-affluent youth.

But it is also the case that many young donors often have less money to gift than their parents and they want to contribute to organizations where they will have the most impact. “Mom is on the board of well-known cultural institutions. I’d rather give $1 million to where it will really be more meaningful, such as my boarding school,” said a second-generation inheritor.

Added one fourth-generation heir whose father donates to a symphony orchestra, “I want the hands-on experience that giving to a small organization provides. Being younger, I want the de-monstrative results.”

*State of the Arts: Despite Recession, Optimism Abounds, Janos Gereben, San Francisco Examiner, October 25, 2009, and San Francisco Opera Survives and Thrives, Janos Gereben, San Francisco Examiner, January 18, 2011.

Chapter 3 | Philanthropy and the Family

Education

Figure 3.1: Philanthropic areas of high interest

Impact or Venture Philanthropy

Science

ParentsChildren

Environ-ment

Arts/Culture

Healthcare Public Policy

65%69%

36%

22%

31%

21%

30%27%

30%34%

26%

34%

23%

14%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

32 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

3.3 Getting started

The time at which a next-generation family member becomes involved in giving seems linked more to the family dynamic and personal readiness than to the age of the family member. For this reason, members of the third and later generation in this study are more actively involved in philanthropic pursuits. These families have had multi-generational experience with wealth and the time to devel-op a philanthropic plan, including philanthropic vehicles such as family foundations, donor-advised funds, mission statements and organized governance around gifting.

Almost two-thirds (63%) of respondents in the third or later generation said they are very (24%) or somewhat (39%) involved, compared to 47% of those from the second generation, broken down into those who are very (18%) or somewhat (29%) involved (see Figure 3.2). The fact that just under one-quarter of the Next Generation are very involved in philanthropy is a reflection of readiness, priority and individual wealth as opposed to an indicator of apathy or an uncaring attitude toward philanthropy. As we saw in Chapter 2, 79% of respondents expect to be involved in philanthropy once they inherit their wealth. Many of the Next Generation are now focusing on personal matters, building careers, gaining a college education and learning about their wealth.

Philanthropy can be a highly effective way to teach the Next Generation about values, some of which can be classed as family values; social and fiscal responsibility; working together and deci-sion-making with other family members. As we documented in the earlier 2012 Next Generation Wealth study, 73% of families said they used philanthropy to teach about wealth.

Families with older wealth and formal giving strategies often use philanthropy for this purpose, thereby engaging and exposing their children to philanthropy and getting them involved earlier than some families newer to affluence.

3.4 Finding a voice

The Next Generation can serve in a number of formalized roles when it comes to charitable strate-gies, particularly as a part of the processes and procedures created for decision-making in families with governance systems. The most common role played by the Next Generation in their family’s philanthropy is one of having input but no decision-making authority (30%). One-quarter sit on grant committees, while 20% serve on investment committees. One-third have no role at all. It is not uncommon for families new to affluence to have not yet developed systems of governance for this area of wealth management.

Over three-quarters (78%) of the Next Generation are interested in serving on the board of a non-profit, with just under half (49%) very or extremely interested (see Figure 3.3).

campdenresearch.com | 33

Chapter 3 | Philanthropy and the Family

Figure 3.2: How actively involved are you in family philanthropic pursuits?

Not at all involved - 11%

Very involved - 23%

Somewhat involved - 36%

Not too involved - 30%

Very involved - 18%

Somewhat involved - 29%

Not too involved -

41%

Not at all involved - 12%

Very involved - 24%

Somewhat involved - 39%

Not too involved - 30%

Not at all involved - 7%

G2

G3

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Full Sample

34 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Next-generation heirs from families with more experience in handling wealth are slightly more in-clined to sit on a board. Interestingly, those between 20 and 29 years old are more interested than their older counterparts, with 63% highly interested compared to 46% of those aged between 30 and 40 years.

Figure 3.3: How interested are you in serving on the board of a non-profit?

Not very interested - 14%

Extremely interested - 30%

Very interested - 19%Somewhat interested -

29%

Not at all interested - 8%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 35

Chapter 4 | Investing Through a Next-Gen Lens

Investing Through a Next-Gen Lens

4KEY FINDINGS

n Seventy-five percent start learning about investments in their late teens or 20s

n Seventy-eight percent look to financial markets to generate some wealth

n Eighty-six percent invest in stocks and bonds

n Forty-two percent of those between 30 and 40 years old are experienced direct investors

n Mission-related investments attract high interest but little participation

n Fifty-nine percent of the Next Generation trade on-line; younger generations are more digitally active than older Next Generation

n Mobile trading platforms are important

36 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Capital markets, for many next-generation family members, are synonymous with volatility, his-torically low interest rates and their associated bond yields and moderate long-term equity per-formance. The majority (75%) of the study participants first started learning about investments in their late teens or twenties. As a result, they associate the financial markets with great upheaval. Despite this, they do see the need to invest although they understand capital markets alone will not be enough to sustain family wealth. This is why 42% of the older Next Generation study respon-dents are opportunistically making direct investments in companies. The younger Next Generation needs to become familiar with traditional investments first, before pursuing more complex wealth generation strategies.

As one 29-year-old summed up the sentiment, “At best we are cautiously optimistic. At worst, pessimistic and confused about these economic times.”

The next-generation inheritors expect diversified portfolio strategies to deliver growth but not enough to keep pace with inflation, family spending and family expansion. Respondents are keenly interested in learning about investing and taking a role in managing their investments. They are active in and want to learn more about the traditional investments found in high-net-worth port-folios—stocks, bonds, hedge funds, private equity, etc. — but are also seeking to create wealth through direct investments.

4.1 Faith and interest in markets persists

Over three-quarters (78%) of those in the study believe they will generate wealth through the financial markets (see Figure 4.1).

Neutral - 12%

Agree strongly - 43%

Agree somewhat - 35%

Disagree strongly - 2%

Figure 4.1: Please indicate how much you agree or disagree with the following statement: "I expect to generate wealth through the financial markets."

Disagree somewhat- 8%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 37

And just under two-thirds said they are very or extremely interested in actively managing their investments and believe it is important to self-direct their investments (see Figure 4.2). “There is a generational shift,” noted a 26-year-old member of a multi-generational family. “This generation all went to university and developed a similar mindset—critical and smart. And we apply this to our own lives and our practices of investing.” These investors do see value in working with advisers but want to be engaged in the process. They seek to be informed of planned investment changes and often want the power of the final approval when making financial decisions.

4.2 Starting with the basics

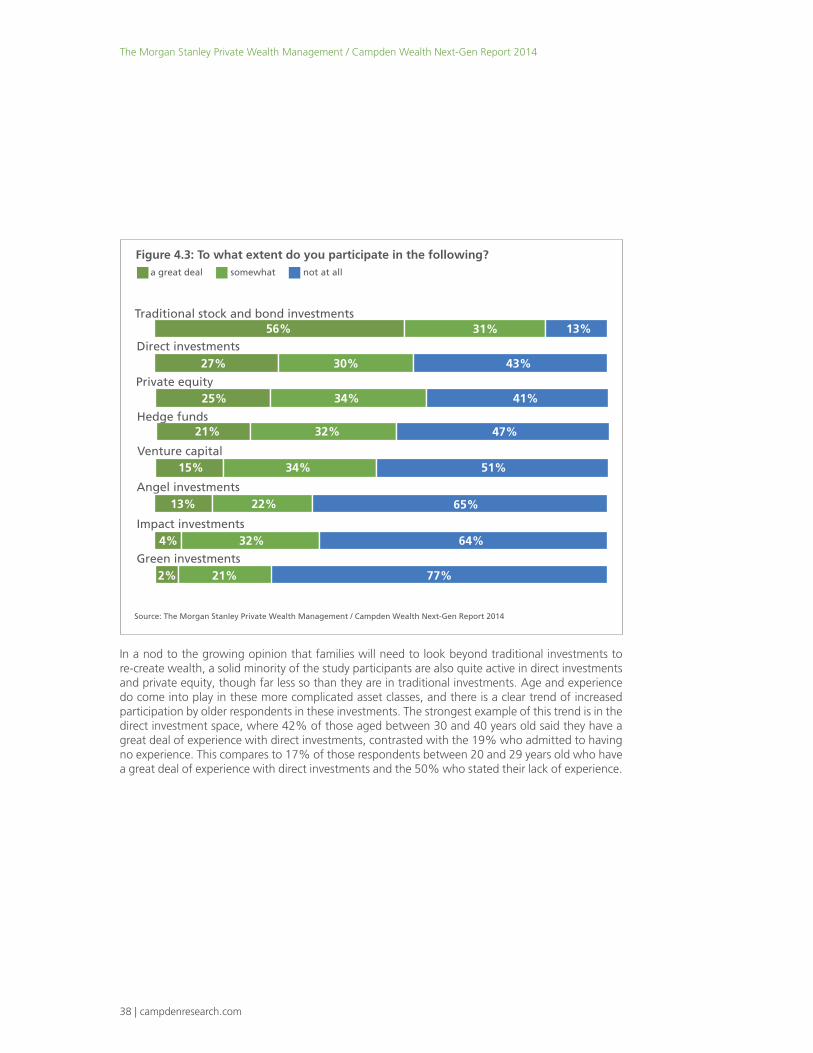

A large majority of the study's Next Generation has experience investing. Not surprisingly, their most common experience is in traditional stocks and bonds. This is consistent with the fact that most portfolios have allocations to these asset classes, and they are a natural place to start investing. Stocks and bonds are not as complex as other asset types and do not carry the higher minimums, lock-ups and capital commitments associated with alternative investments. A mere 13% of the study’s respondents said they do not participate in traditional investments, while 56% participate a great deal (see Figure 4.3).

Chapter 4 | Investing Through a Next-Gen Lens

Somewhat interested - 21%

Extremely interested - 37%

Very interested - 26%

Not at all interested - 1%

Figure 4.2: How interested are you in actively managing your investments?

Not very interested - 15%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

38 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

In a nod to the growing opinion that families will need to look beyond traditional investments to re-create wealth, a solid minority of the study participants are also quite active in direct investments and private equity, though far less so than they are in traditional investments. Age and experience do come into play in these more complicated asset classes, and there is a clear trend of increased participation by older respondents in these investments. The strongest example of this trend is in the direct investment space, where 42% of those aged between 30 and 40 years old said they have a great deal of experience with direct investments, contrasted with the 19% who admitted to having no experience. This compares to 17% of those respondents between 20 and 29 years old who have a great deal of experience with direct investments and the 50% who stated their lack of experience.

Figure 4.3: To what extent do you participate in the following?not at alla great deal somewhat

Venture capital15% 34% 51%

Traditional stock and bond investments56% 31% 13%

21% 32% 47%

Private equity25% 34% 41%

Impact investments4% 32% 64%

Green investments2% 21% 77%

Angel investments13% 22% 65%

Direct investments27% 30% 43%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Hedge funds

campdenresearch.com | 39

Chapter 4 | Investing Through a Next-Gen Lens

The Next Generation tends to take a long-term view on investing. A clear 91% said they are will-ing to put off financial benefits today in exchange for higher income or lower taxes in the future. “That’s why I like private equity and real estate. On the exit, you make your money. It’s especially good if no one needs the money now,” said a fourth-generation family member.

4.3 Mission-related investments: high interest, little action

There is a lot of interest in and focus on socially conscious investments, such as the green and impact spaces. In fact, 61% of respondents stated that it is highly important to align values and investing while only 6% consider this unimportant. More than half (56%) said they would accept lower returns in exchange for a positive social impact.

Angel investing is also attractive to many in the Next Generation, promising an entry onto the ground floor of what could be the next break-away company and the ability to gain experience in evaluating companies at a relatively low barrier to investment.

Interest, however, does not always translate into action. A full 77% of those in the study have no investment experience in the green space and almost two-thirds have no experience with angel and impact investments. The relative infancy of the mission-related investment space may, in part, account for this combination of strong interest and lack of activity. One younger study participant voiced a concern echoed by many: “The world of impact investing has yet to demonstrate it can produce market returns.” Those groups who do have experience, made up largely of the older survey participants, describe their participation level as moderate.

4.4 The risk/reward trade off

Moderate risk for the possibility of moderate gains is the most sought-after investment strategy. A solid 60% of respondents identify with this approach, while 25% identify themselves as risk-takers and 15% as risk-averse (see Figure 4.4).

Older, more experienced investors are more comfortable with risk. While 33% of those aged be-tween 30 and 40 years old will take substantial risk for the possibility of substantial reward, only 11% of those under 30 feel comfortable with this investment approach. Conversely, 22% of the younger study participants will take little risk even if this minimizes potential gains. This is a clear and direct contrast to the mere 6% of respondents aged 30 to 40 years old who would make the same decision.

Additionally, those from established families tend to be more cautious. “You learn from your par-ents and grandparents to be conservative with money,” said a third-generation son. While only 11% of those from families in the third or later generations would take on substantial risk, a higher 39% of those in the second generation would be more willing. Said a second-generation son, “I come from a different time than my parents, who were raised in poverty. I’m not as frugal and am willing to take some risks.”

40 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Figure 4.4: How would you describe your level of investment risk?

I take little risk, even if it means minimizing the gains I make -15% I take substantial risk

for the possibility of substantial gains - 25%

I take moderate risk for the possibility of moderate gains - 60%

Substantial Risk - 11%

Moderate Risk - 70%

Low Risk - 19%

Substantial Risk - 39%

Moderate Risk - 54%

Low Risk - 7%

Low Risk - 6%

Substantial Risk - 33%

Moderate Risk - 61%

30-40 years oldModerate Risk - 67%

Low Risk - 22%Substantial Risk -

11%

20-29 years old

G2

G3

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Full Sample

campdenresearch.com | 41

The multiple-generation families in this study are focused on maintaining wealth. This is not neces-sarily a reflection of the market at large, but rather of the particular sample set used in this report. However, one can confidently discern that families focused on addressing education and long-term wealth sustainability are more likely to be able to preserve wealth and less likely to meet the fate of ‘shirt sleeves to shirt sleeves’ in three generations.

4.5 Equity leads on-line trading

Some 59% have on-line trading accounts separate from their primary investment accounts. Of those, two-thirds use the on-line brokerages of firms for investments. “I have brokerage accounts on-line. Most on-line accounts have technologically reasonable platforms,” noted one such study participant.

Staying up to date with the latest technology is a challenge for firms looking to anticipate what will and will not be utilized and valued by clients. Mobile trading platforms appear to be important to those who trade on-line. Keeping in mind that 59% of the study participants have on-line trading accounts, it is important to note that more than half of all participants in the study think it either highly or somewhat important to have a mobile trading platform. Stocks are most commonly traded on-line, with 20% of those surveyed trading them ‘often.’

6%

Stocks

Figure 4.5: On-line trading activity

Bonds

Options and Futures

SometimesOften

ETFs

Mutual Funds

Currencies

Commodoties

20% 28% 48%

6% 22% 28%

20% 26%

5% 13% 18%

8% 26% 34%

10% 16%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

6%

5% 13% 18%

Chapter 4 | Investing Through a Next-Gen Lens

42 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

All other asset classes examined in the study were traded often by less than 10% of the study’s participants. Bonds are the second most-traded investment (34% of respondents trade them often or sometimes) trailed by options and futures and, following that, ETFs.

The study's younger participants are more active in trading on-line than those aged between 30 and 40 years old. For example, 42% of those aged from 20 to 29 years old often trade stocks compared to 18% of those aged from 30 to 40 years old. With this in mind, it is worth noting that the older participants are just as likely to have on-line accounts and value mobile trading platforms as the younger participants.

4.6 Sourcing investment advice

Like their parents and grandparents, the Next Generation most often looks to their financial advisers for financial advice and news. Sixty percent of those in the study said they consider their financial advisers to be a highly important source for such information. Accountants and friends and family were the next most valued resources; 46% rated accountants highly important, while 44% rated friends and family in the same vein (see Figure 4.6).

Figure 4.6: How important to you are the following sources of financial advice and news?

somewhat importanthighly important not very important

60% 22%

Accountant

Financial Adviser

Attorney

Friends and family

Newspapers and magazines

Internet/blogs

Personal finance websites

Television

18%

46% 20% 34%

44% 36% 20%

34% 13% 53%

39%31% 30%

31%29% 40%

29%13% 58%

7% 22% 71%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 43

Chapter 5 | Wealth Adviser Relationships

Wealth Adviser Relationships

5KEY FINDINGS

n Seventy-nine percent began working with advisers in their late teens or 20s

n Adviser interaction often begins around the same time Next-Gen begins learning about investments

n Established relationships are critical to Next Generation client retention

n Non-discretionary managers and advisers are sought

n Experience matters, coupled with long-term commitment

n Traditional forms of communication most desired for adviser engagement

n Many access and monitor account data on-line

44 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

The sooner the better—that’s the overwhelming sentiment of the Next Generation when it comes to when they feel it is best to begin working with advisers. Three-quarters of the study’s respon-dents said it is best to begin interacting with advisers as early as possible. “At 15-18, it’s a great time because there is a comfortable awareness of the world and the impact of what you do,” said a 26-year-old study participant.

5.1 Getting their feet wet

Most affluent children learn about wealth in stages. A typical learning curve starts in the pre-teen years and younger, when children often receive their first allowance and learn about spending (see Figure 5.1). As they enter young adulthood, they learn the value of money, budgeting and savings while gradually becoming more familiar with giving. Most often they become educated on invest-ments in their late teens and 20s.

“I do believe in financially fit kids,” said a mother of a young child, describing the oft-expressed opinion on starting a child’s financial education at a young age.

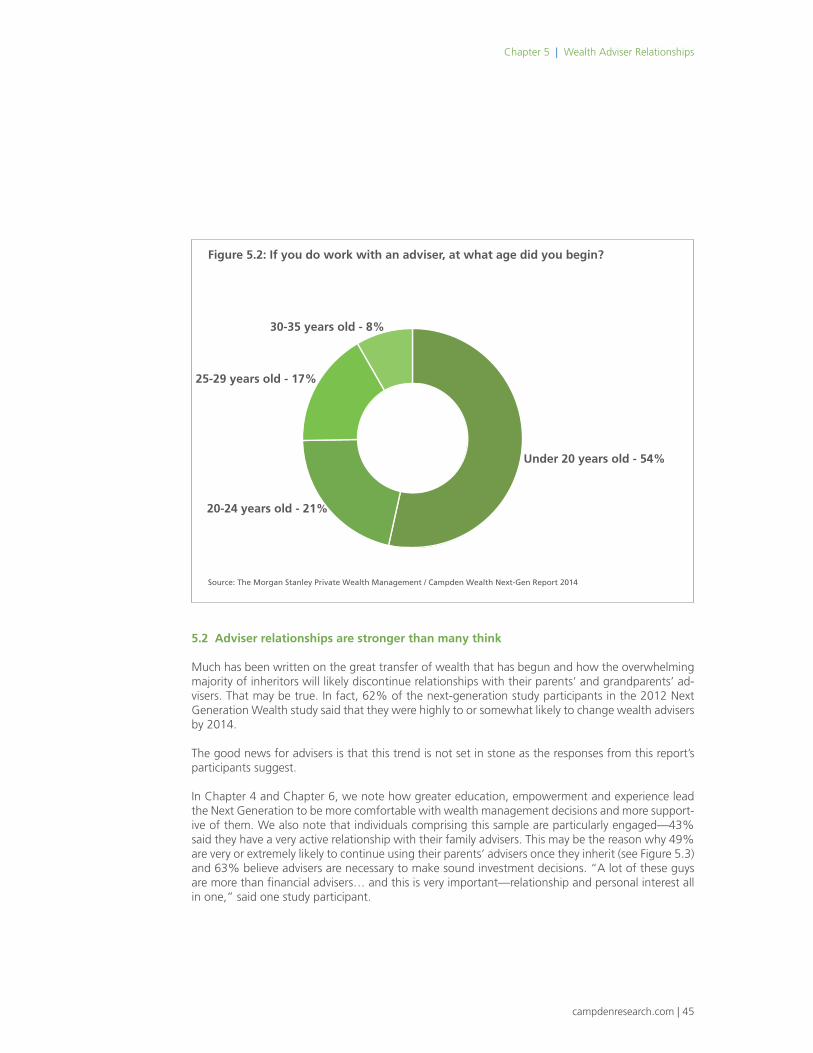

The largest percentage of the study’s respondents began working with their families’ advisers once they had been introduced to the fundamentals of wealth, at the beginning of their lessons on investing (see Figure 5.2). Of those working with family advisers, 41% started to do so when they were under 20 years old while 38% began to engage with family advisers in their 20s. However, 14% said they haven’t started to work with advisers yet—60% of these respondents are under the age of 30.

Figure 5.1: At what age did you learn about the following:teenschild pre-teen 20s 30s

23% 23% 31% 18% 5%The value of money

31% 27% 28% 13% 1%

Spending

15% 25% 34% 24%Budgeting and saving

3% 8% 27% 48% 8% 6%Investing

16% 16% 31% 26% 6% 5%

Gifting and charity

14% 14% 30% 35% 7%

My family’s wealth

1% 1%

not yet

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 45

Chapter 5 | Wealth Adviser Relationships

5.2 Adviser relationships are stronger than many think

Much has been written on the great transfer of wealth that has begun and how the overwhelming majority of inheritors will likely discontinue relationships with their parents’ and grandparents’ ad-visers. That may be true. In fact, 62% of the next-generation study participants in the 2012 Next Generation Wealth study said that they were highly to or somewhat likely to change wealth advisers by 2014.

The good news for advisers is that this trend is not set in stone as the responses from this report’s participants suggest.

In Chapter 4 and Chapter 6, we note how greater education, empowerment and experience lead the Next Generation to be more comfortable with wealth management decisions and more support-ive of them. We also note that individuals comprising this sample are particularly engaged—43% said they have a very active relationship with their family advisers. This may be the reason why 49% are very or extremely likely to continue using their parents’ advisers once they inherit (see Figure 5.3) and 63% believe advisers are necessary to make sound investment decisions. “A lot of these guys are more than financial advisers… and this is very important—relationship and personal interest all in one,” said one study participant.

Figure 5.2: If you do work with an adviser, at what age did you begin?

Under 20 years old - 54%

20-24 years old - 21%

30-35 years old - 8%

25-29 years old - 17%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

46 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Just as engagement can lead to higher adviser retention rates, the reverse relationship might hold true. Nineteen percent of the study's participants had no engagement with their family’s wealth advisers. A good many of these are part of the 31% who are not likely to continue using their par-ents’ advisers. Additionally, 80% of those who have hired an adviser attach almost no importance to being contacted by a family adviser as a reason to hire them. If there is no existing relationship between the next-generation member and the adviser, then the fact that the adviser already works for the family will count for little in having their services retained by the Next Generation.

5.3 Hiring an adviser

Experience, reputation and control are the top drivers when selecting an adviser, according to the 56 study participants who have experience hiring an adviser (see Figure 5.4). Fees are also highly important.

The Next Generation wants to be involved in portfolio allocations and have the final say on in-vestment decisions impacting their accounts. For this reason, they lean toward non-discretionary managers and brokers. “You have to be the main architect of what you do,” said the daughter of a wealth creator.

Figure 5.3: How likely are you to continue using your parents' advisers?

Extremely likely - 23%

Very likely - 26%

Somewhat likely - 20%

Not at all likely - 15%

Not very likely - 16%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 47

Fees have become more of a focus for all private investors post-2007, especially since manager per-formance has become increasingly recognized as commoditized. For 64% of the next-generation members in this report, fees represent a highly important consideration. Interestingly, participants are split on the types of fee structures they prefer, with 48% leaning toward commissions and 52% preferring asset-based pricing. While not a main factor, age still remains an important consideration for the Next Generation. In keeping with their emphasis on experience, the Next Generation wants their advisers to be old enough to have gained valuable work experience, but they also want advisers who can grow with them in the long term. “Thirty to fifty-five is in the right range for us. That way we can grow with

Figure 5.4: If you’ve hired an adviser on your own, how important were the following in your decision:

somewhat importanthighly important not very important

Adviser works on team with other wealth advisers24%37% 39%

Family’s adviser contacted me6% 14% 80%

Gender of adviser5% 11% 84%

Adviser is an estate planning expert18% 39% 43%

Age of adviser34%24% 42%

30% 24% 46%

Family referral

Referrals by friends/colleagues34% 34% 32%

Level of fees charged64% 22% 14%

Level of your control over your accounts72% 22% 6%

Reputation of firm73% 16% 11%

Work experience of adviser74% 18% 8%

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

Chapter 5 | Wealth Adviser Relationships

48 | campdenresearch.com

The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

each other,” said a third-generation inheritor, adding, “You don’t want someone in their twenties. They are simply not mature enough.” Reflecting on his ideal age range for his advisers, a next-gen-eration family member who runs his family office agreed: “I have to keep the family office going for at least one more generation, or about 30 to 35 years. So if you have a sage adviser who’s 75, there is concern that the person won’t be around for long.”

5.4 Most Important Services

The Next Generation has similar preferences as older generations when it comes to the services they deem most important. Approximately three-quarters of the study’s participants rank investment advice (77%), tax planning (75%) and asset allocation advice (72%) as highly important (see Figure 5.5).

Figure 5.5: How important are the following adviser services?somewhat importanthighly important not very important

Introduction to new investments26%64% 10%

Estate and legacy planning21%66% 13%

Asset allocation advice72% 15% 13%

Investment advice

77% 16% 7%

Tax planning19%75% 6%

Financial education47% 26% 27%

Loan/credit42% 26% 32%

45% 30% 25%Introduction to new business opportunities

Source: The Morgan Stanley Private Wealth Management / Campden Wealth Next-Gen Report 2014

campdenresearch.com | 49

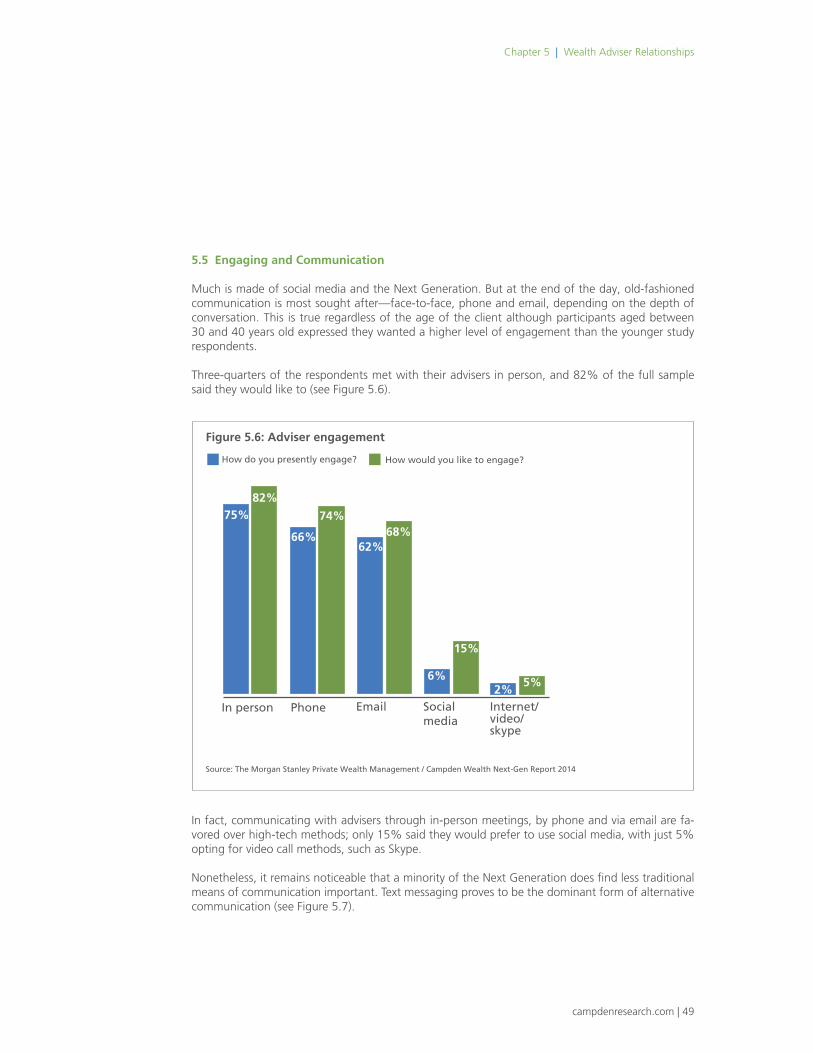

5.5 Engaging and Communication Much is made of social media and the Next Generation. But at the end of the day, old-fashioned communication is most sought after—face-to-face, phone and email, depending on the depth of conversation. This is true regardless of the age of the client although participants aged between 30 and 40 years old expressed they wanted a higher level of engagement than the younger study respondents.

Three-quarters of the respondents met with their advisers in person, and 82% of the full sample said they would like to (see Figure 5.6).