Deferred Income Annuities

44

DEFERRED INCOME ANNUITIES www.myAbaris.com @myAbaris

-

Upload

abaris-financial-inc -

Category

Economy & Finance

-

view

347 -

download

1

Transcript of Deferred Income Annuities

D E F E R R E DINCOME ANNUITIES

www.myAbaris.com @myAbaris

2

We’ve talked about aging, retirement, longevity, and annuities generally.

DEFERRED INCOME ANNUITIES

NOW LET’S NARROW THE FOCUS TO

3

WHAT YOU ALREADY KNOW

LONGEVITY RISK is the risk that you live a lot longer than you expect.

Although pensions and Social Security protect against longevity risk, defined contribution plans like 401(k)s DON’T AUTOMATICALLY.

4

WHAT YOU ALREADY KNOW

Once you’ve done this, you’ll want to make sure you’re using a platform (like ours) that allows you to COMPARE DIFFERENT INSURERS’ OFFERINGS SIDE-BY-SIDE.

DEFERRED INCOME ANNUITIES are one effective way to use a portion of your retirement savings to protect against outliving your money.

But they’re not for everyone, so you’ll need to figure out if you’re the RIGHT FIT by using Abaris’ tools or speaking with your financial advisor.

5

SIDENOTE: We don’t like acronyms, but we’ll make one exception here

DEFERRED INCOME ANNUITY DIAALSO KNOWN AS

6

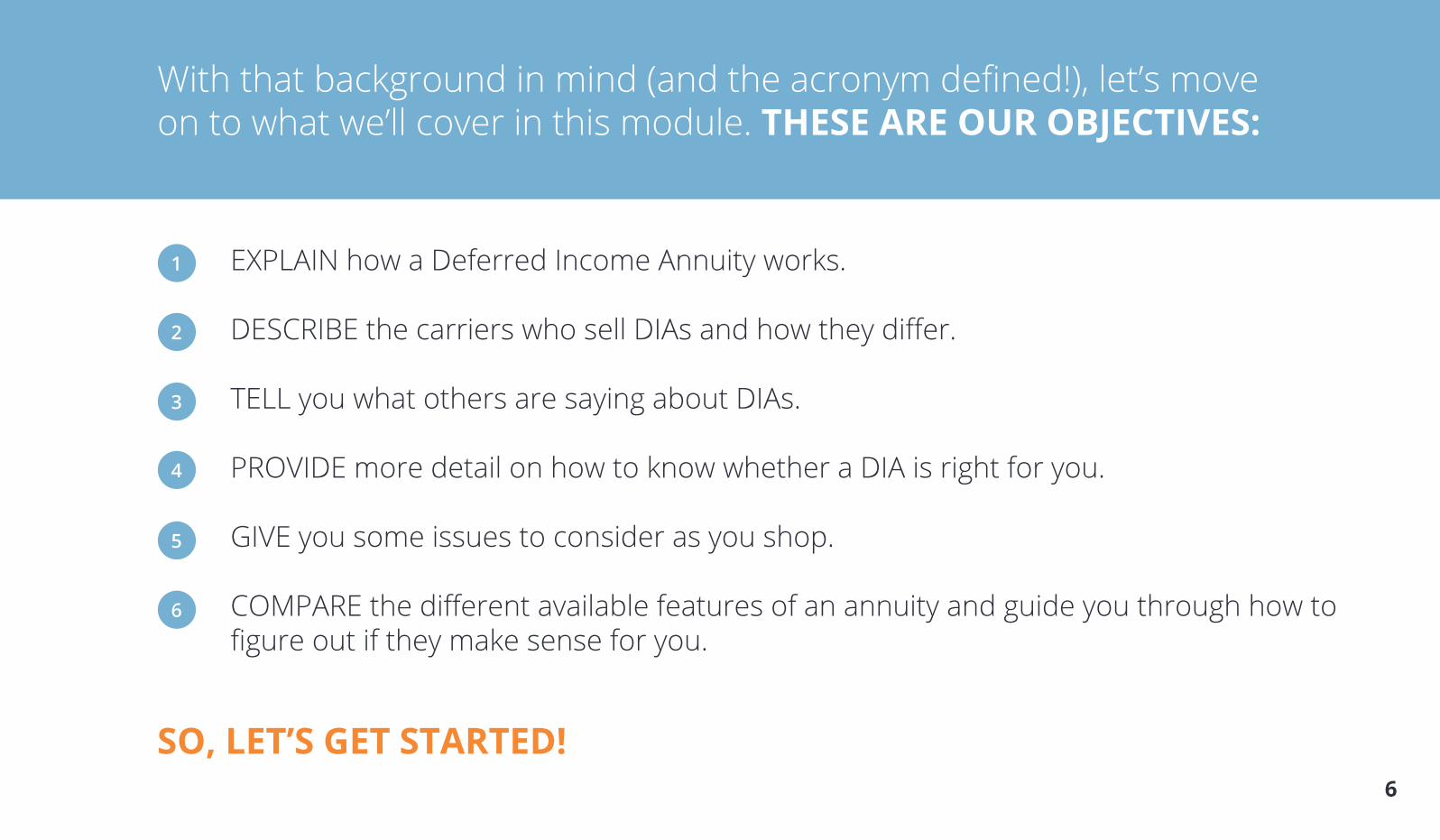

With that background in mind (and the acronym defined!), let’s move on to what we’ll cover in this module. THESE ARE OUR OBJECTIVES:

EXPLAIN how a Deferred Income Annuity works.

DESCRIBE the carriers who sell DIAs and how they differ.

TELL you what others are saying about DIAs.

PROVIDE more detail on how to know whether a DIA is right for you.

GIVE you some issues to consider as you shop.

COMPARE the different available features of an annuity and guide you through how to figure out if they make sense for you.

1

2

3

4

5

6

SO, LET’S GET STARTED!

7

EXPLAIN

How a Deferred Income Annuity works

STEP

1

8

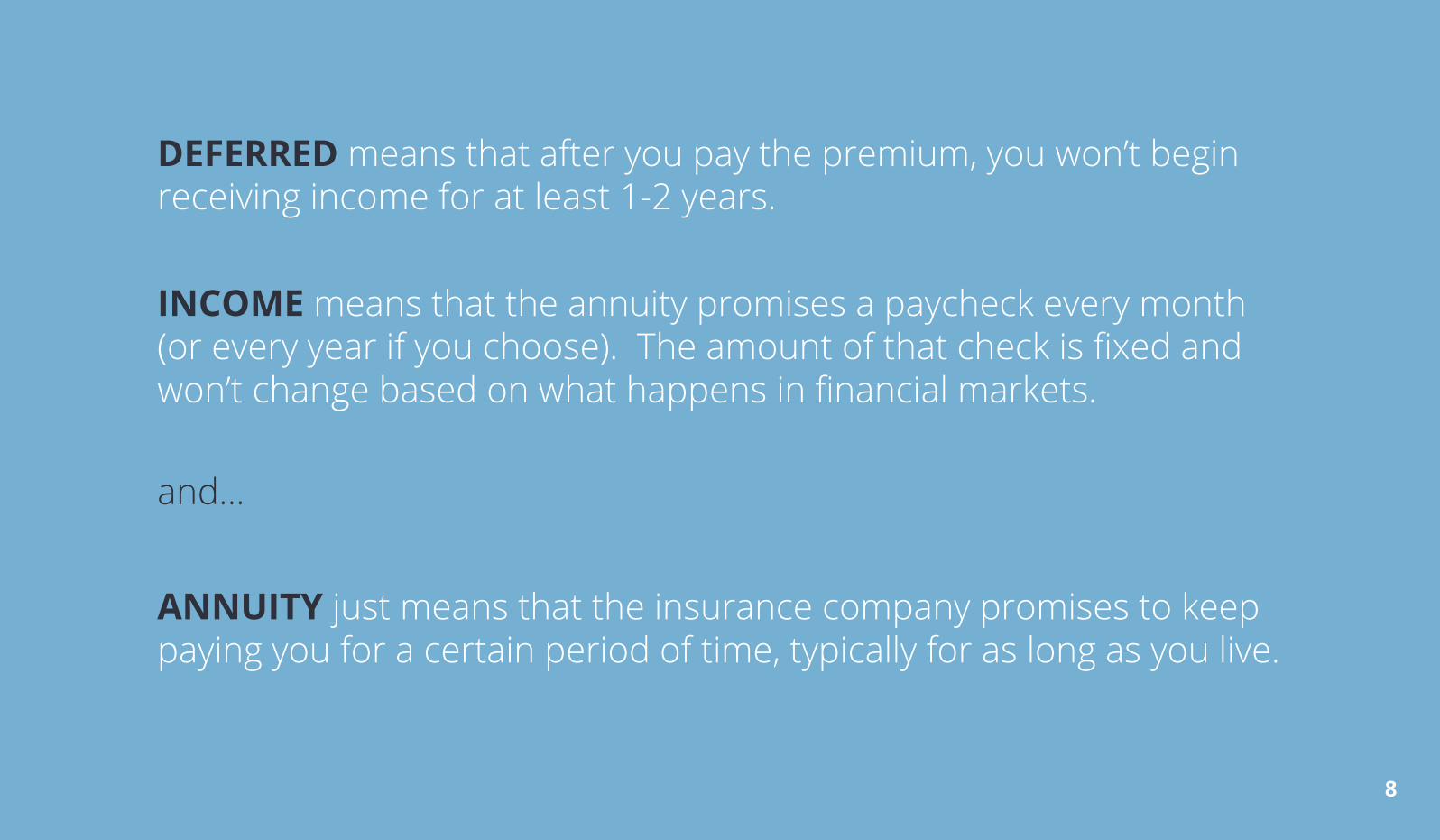

DEFERRED means that after you pay the premium, you won’t begin receiving income for at least 1-2 years.

INCOME means that the annuity promises a paycheck every month (or every year if you choose). The amount of that check is fixed and won’t change based on what happens in financial markets.

ANNUITY just means that the insurance company promises to keep paying you for a certain period of time, typically for as long as you live.

and...

9

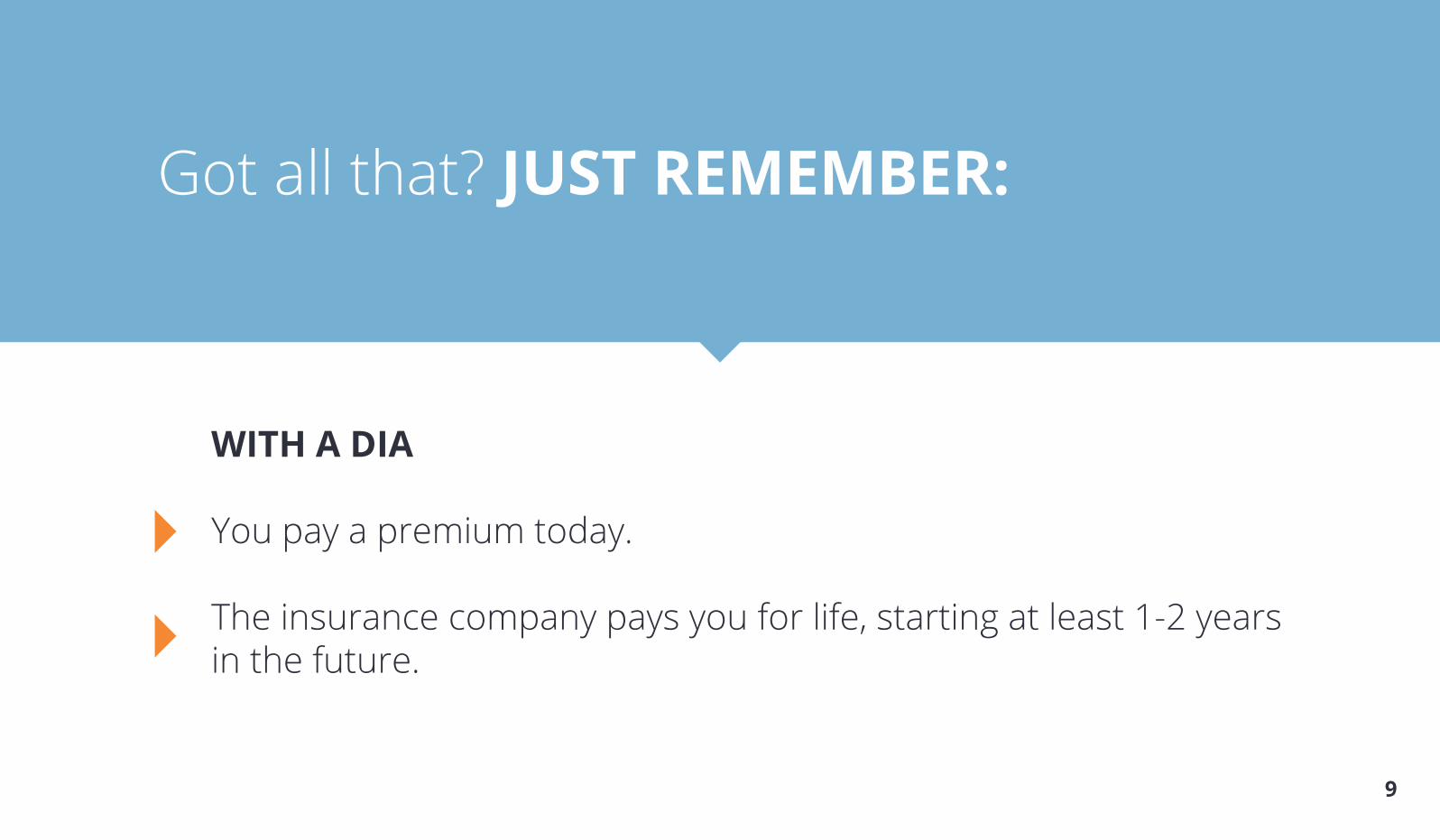

Got all that? JUST REMEMBER:

WITH A DIA

You pay a premium today.

The insurance company pays you for life, starting at least 1-2 years in the future.

10

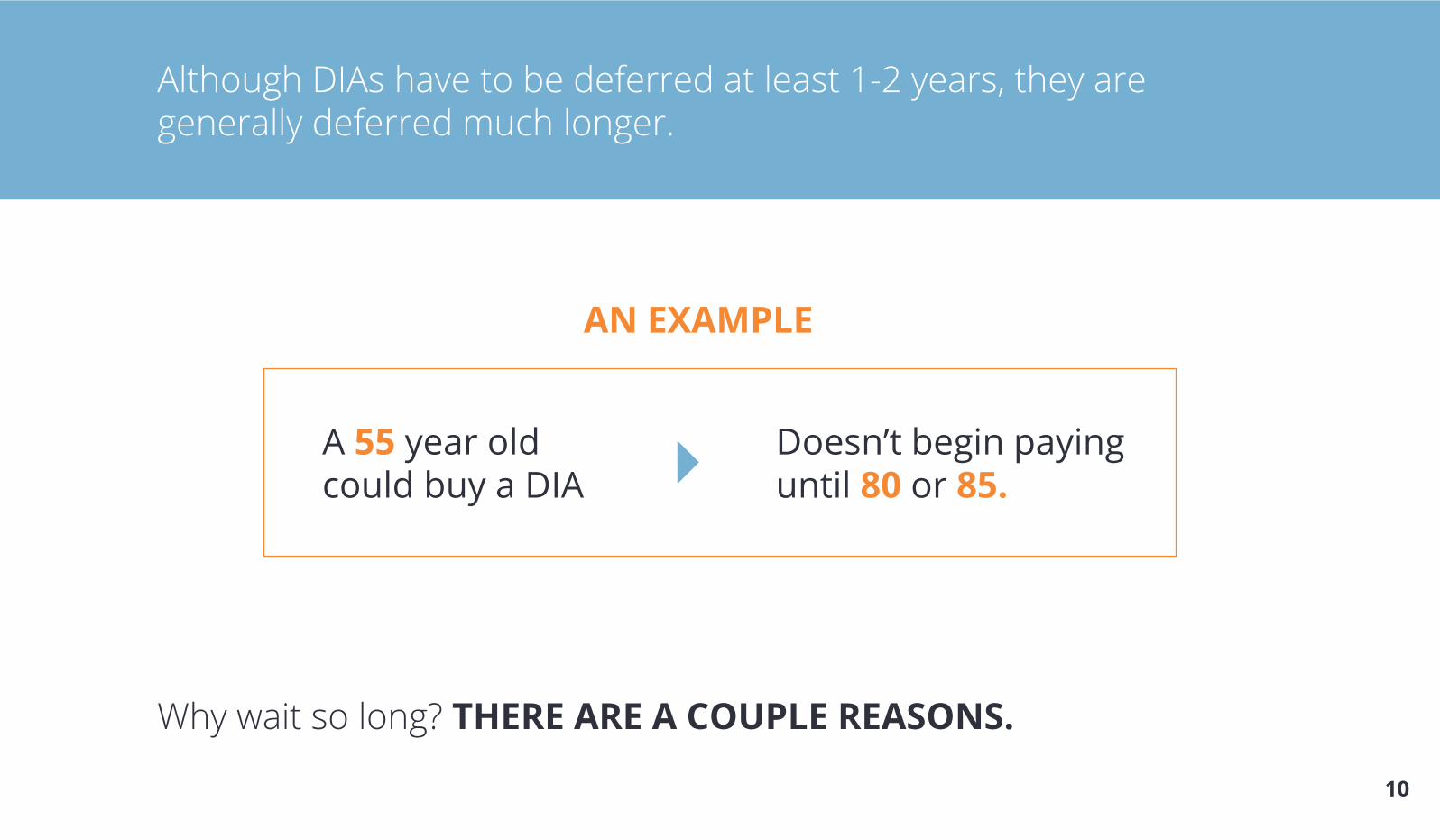

Although DIAs have to be deferred at least 1-2 years, they are generally deferred much longer.

Why wait so long? THERE ARE A COUPLE REASONS.

A 55 year old could buy a DIA

Doesn’t begin paying until 80 or 85.

AN EXAMPLE

11

FIRST, The longer you let the insurance company invest your money, the more it will grow.

12

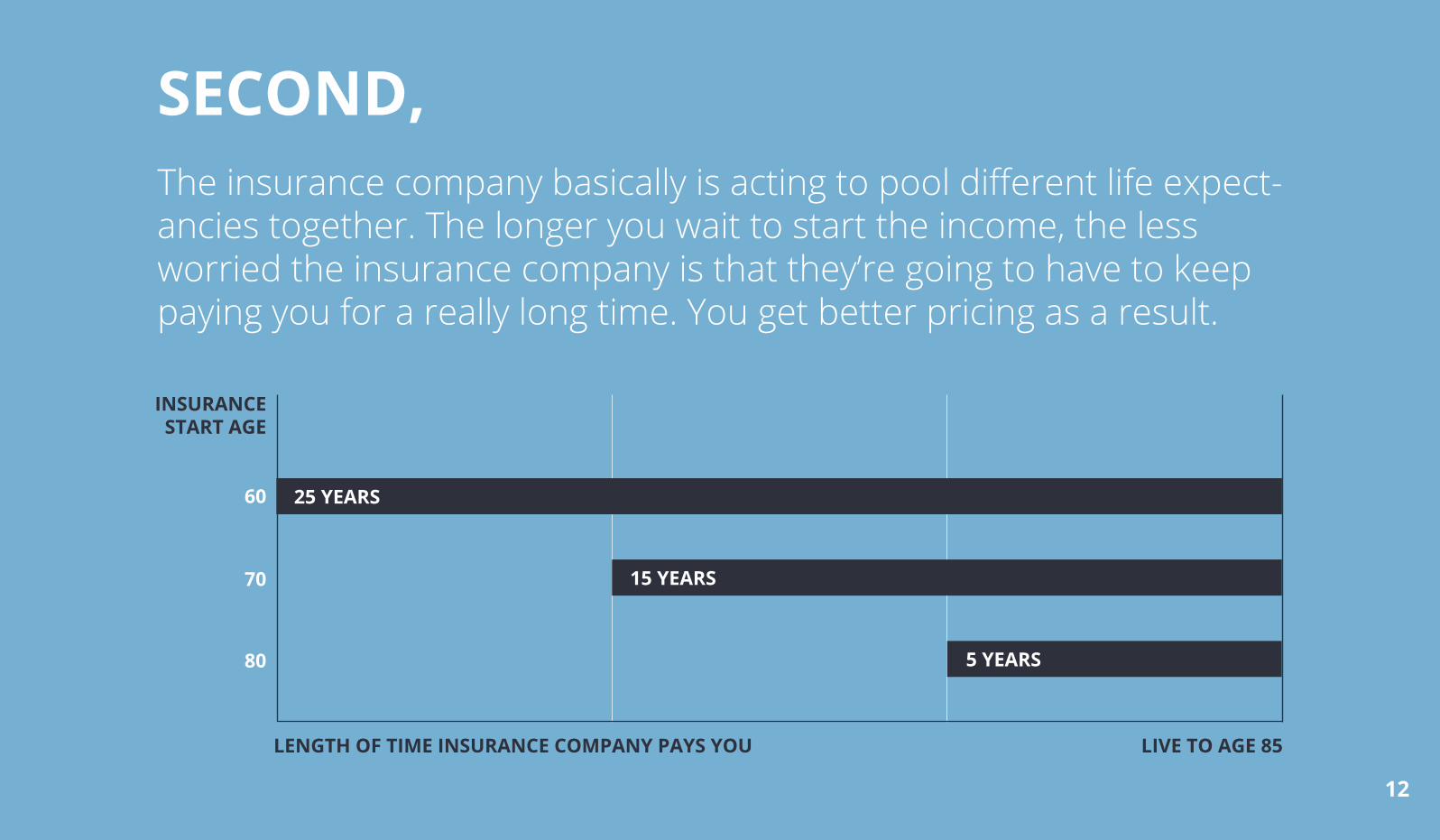

The insurance company basically is acting to pool different life expect-ancies together. The longer you wait to start the income, the less worried the insurance company is that they’re going to have to keep paying you for a really long time. You get better pricing as a result.

SECOND,

INSURANCE START AGE

60

70

80

LENGTH OF TIME INSURANCE COMPANY PAYS YOU LIVE TO AGE 85

25 YEARS

15 YEARS

5 YEARS

13

DESCRIBE

The carriers who sell DIAs and how they differ

STEP

2

14

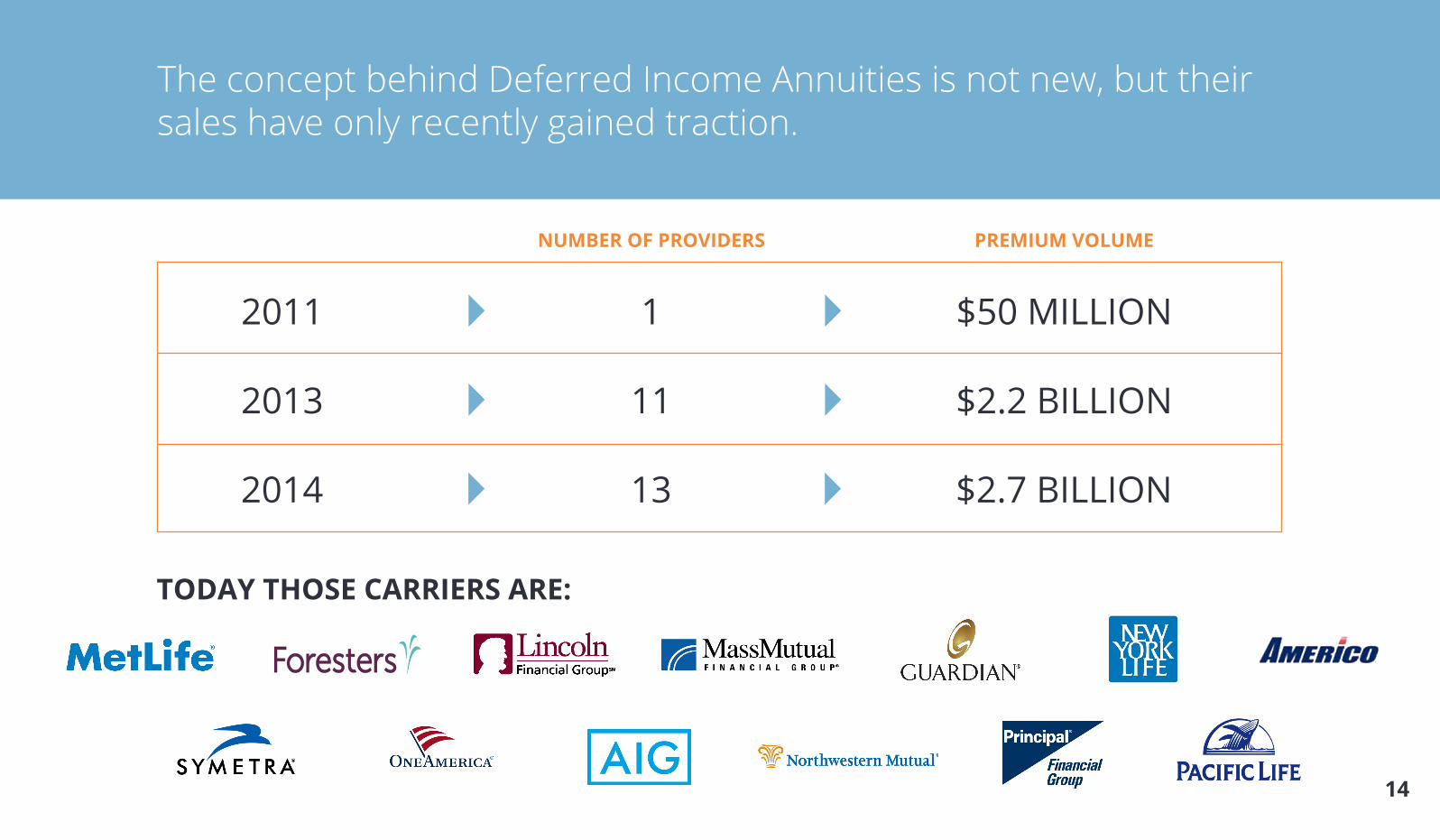

The concept behind Deferred Income Annuities is not new, but their sales have only recently gained traction.

TODAY THOSE CARRIERS ARE:

2011 1 $50 MILLION

$2.2 BILLION2013 11

NUMBER OF PROVIDERS PREMIUM VOLUME

$2.7 BILLION2014 13

15

Through our platform, we sell DIAs from

We’re working hard to get more insurers on board to make the process even better for you.

16

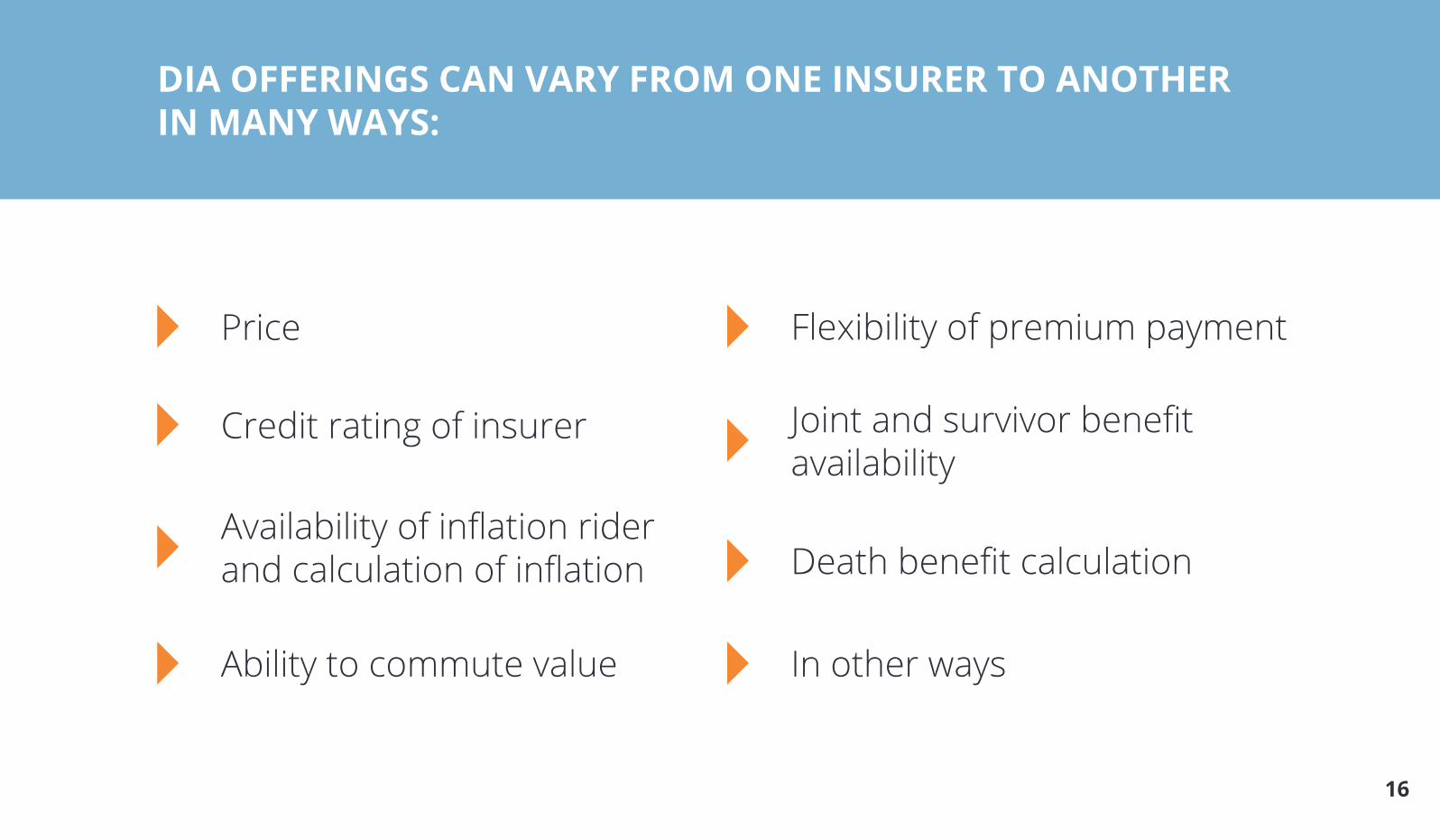

DIA OFFERINGS CAN VARY FROM ONE INSURER TO ANOTHERIN MANY WAYS:

Price

Credit rating of insurer

Ability to commute value

Flexibility of premium payment

Joint and survivor benefit availability

Death benefit calculation

In other ways

Availability of inflation rider and calculation of inflation

17

TELL

You what others are saying about DIAs

STEP

3

18

“[The insurers’] latest brainchild: the deferred income annuity, which has seen explosive growth since it was introduced three years ago, thanks mainly to its simplicity.”

“Many workers long for the sense of security that only an old-fashioned pension can provide. The big insurers are well aware of this, and that’s why many of them are offering new ways for investors to buy and build a pension on their own.”

“Beyond protection against outliving your money, however, deferred income annuities can give you peace of mind by reducing the stress of making your money last till you’re 100.”

“The advantage to this approach is that waiting to collect allows you to receive substantial future payments with a much smaller upfront sum than you would shell out with an immediate annuity.”

19

PROVIDE

More detail on how to know whether a DIA is right for you

STEP

4

20

WHO THEY’RE RIGHT FOR

Deferred Income Annuities only make sense for some people, but for those in the right age bracket and with the right goals, they can be a very powerful tool.

21

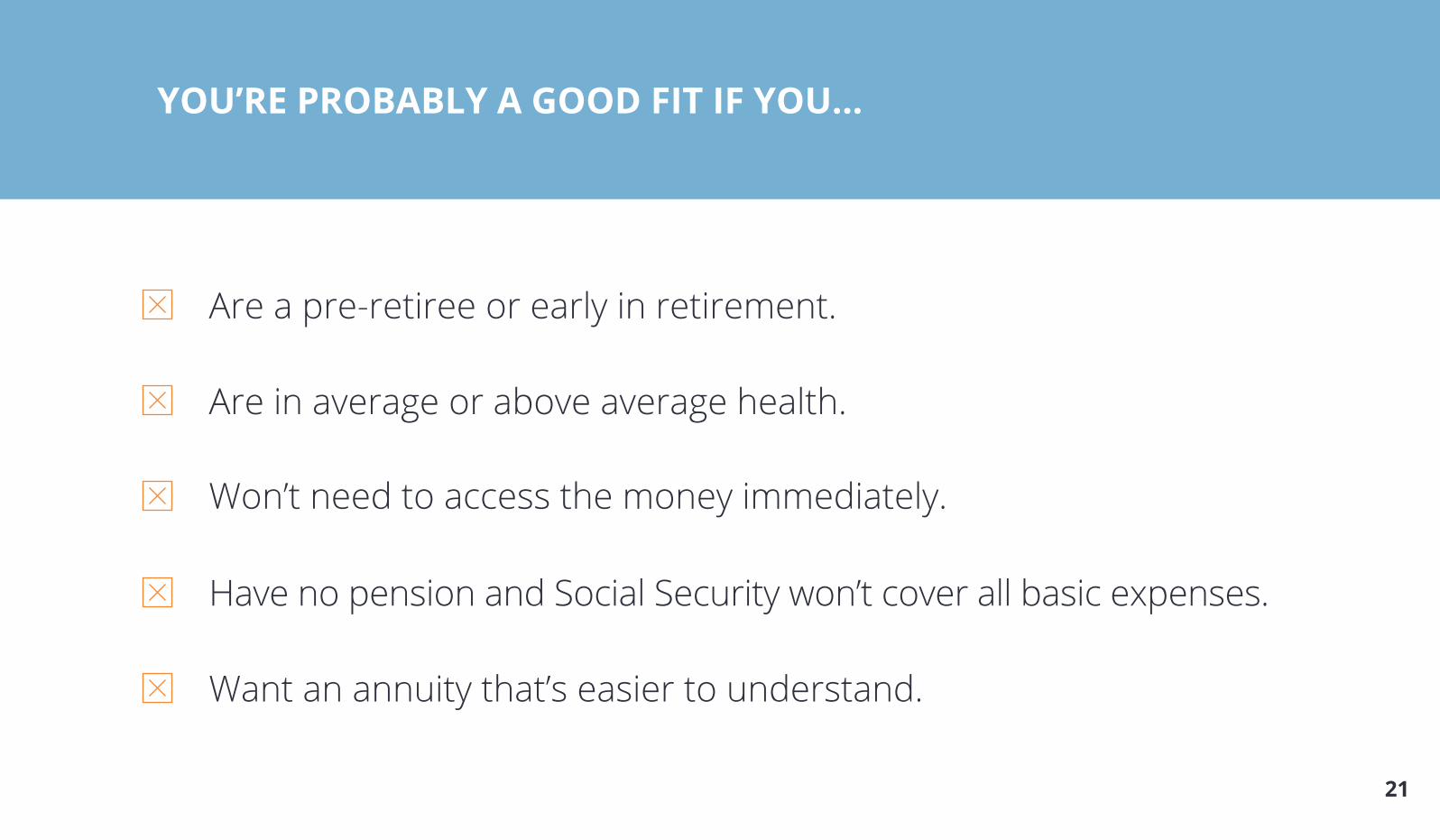

YOU’RE PROBABLY A GOOD FIT IF YOU...

Are a pre-retiree or early in retirement.

Are in average or above average health.

Won’t need to access the money immediately.

Have no pension and Social Security won’t cover all basic expenses.

Want an annuity that’s easier to understand.

22

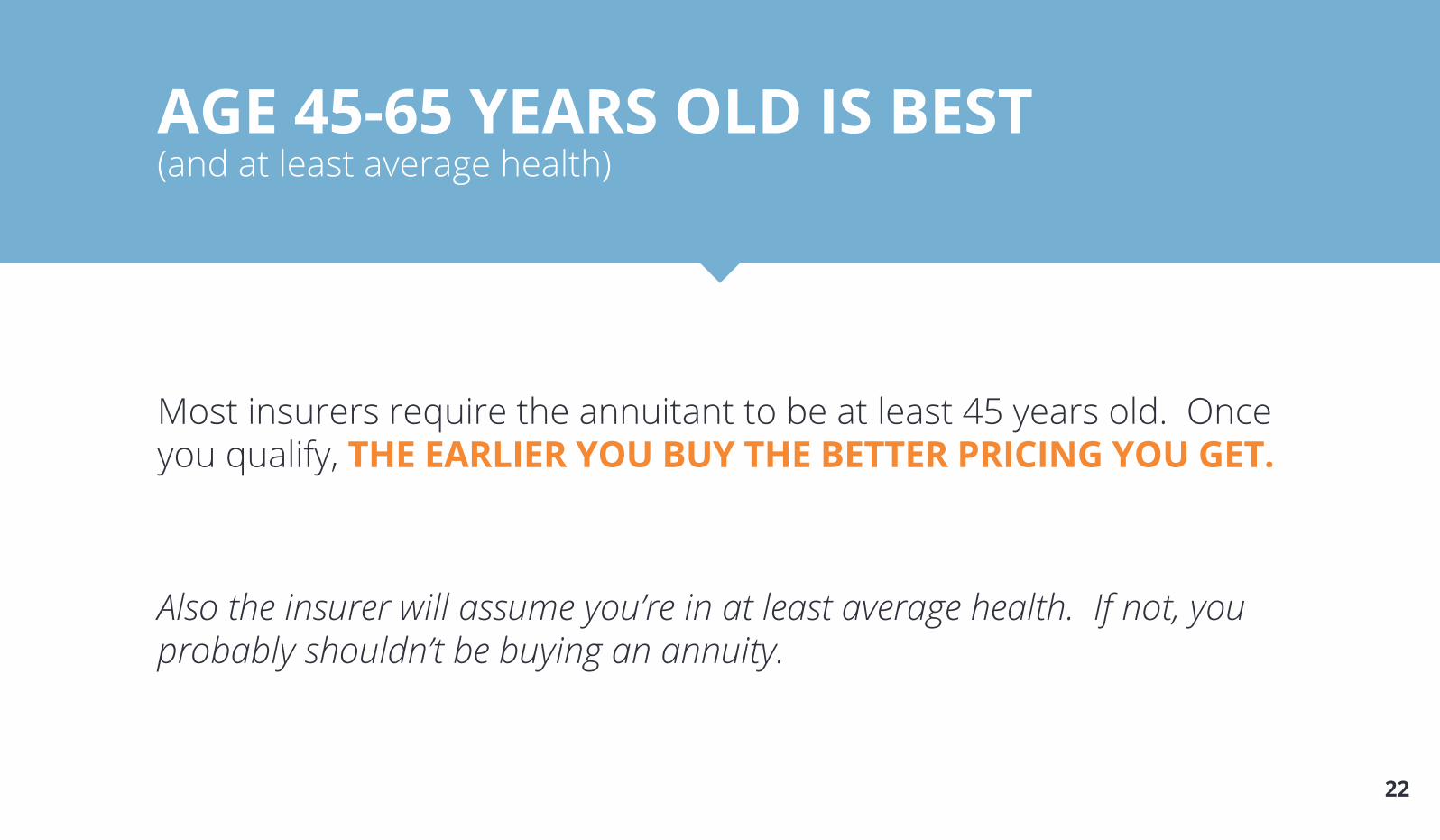

AGE 45-65 YEARS OLD IS BEST(and at least average health)

Most insurers require the annuitant to be at least 45 years old. Once you qualify, THE EARLIER YOU BUY THE BETTER PRICING YOU GET.

Also the insurer will assume you’re in at least average health. If not, you probably shouldn’t be buying an annuity.

23

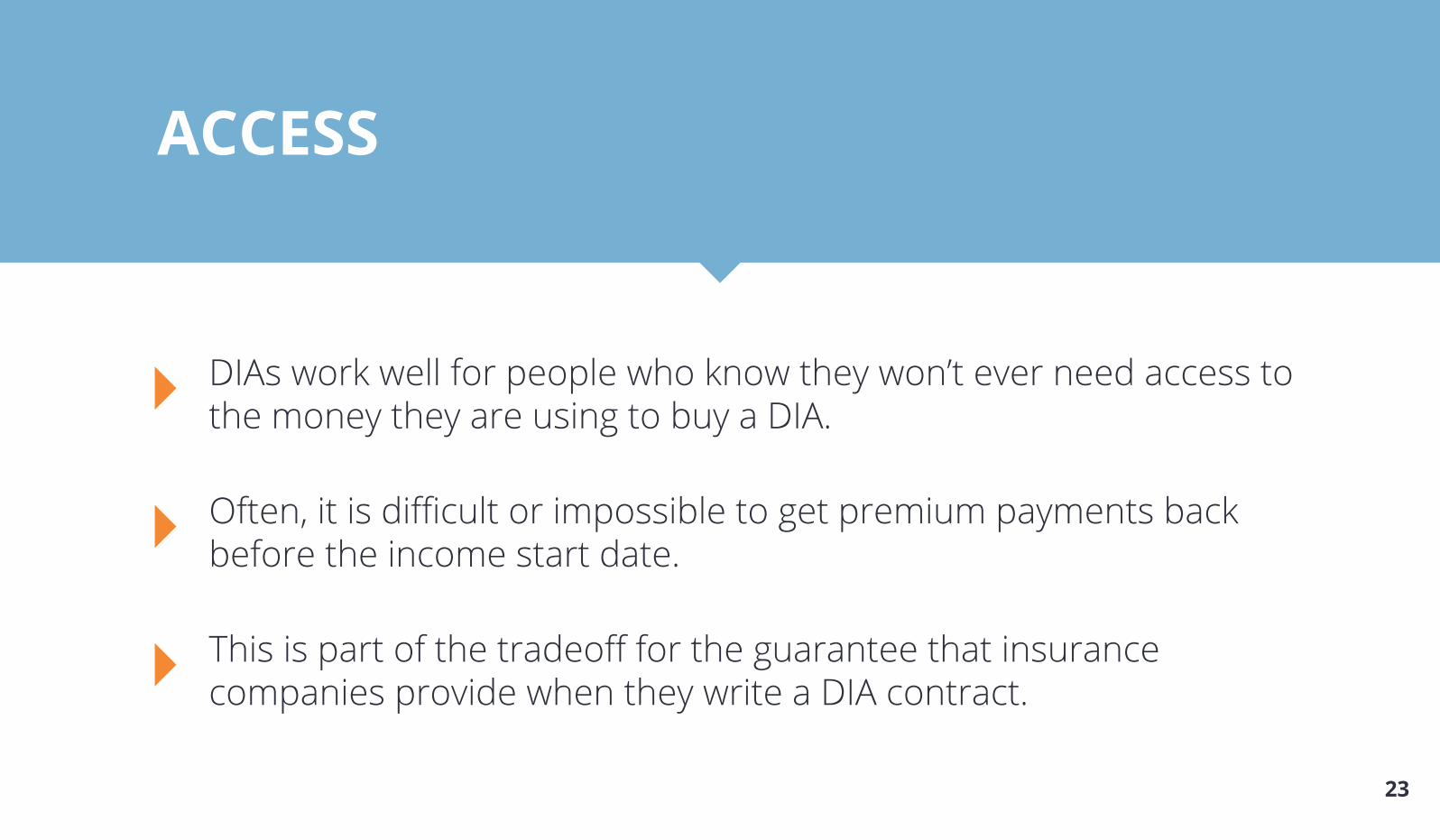

ACCESS

DIAs work well for people who know they won’t ever need access to the money they are using to buy a DIA.

Often, it is difficult or impossible to get premium payments back before the income start date.

This is part of the tradeoff for the guarantee that insurance companies provide when they write a DIA contract.

24

OTHER SOURCES OF INCOME

DIAs work well for people whose living expenses will be GREATER THAN the amount they will receive (or expect to receive) from Social Security or a pension.

25

EASE OF USE

DIAs CAN BE GREAT FOR THOSE WHO VALUE SIMPLICITY.

Relative to most annuities, DIAs are simpler to understand and, unlike many other annuities, they don’t require you to pay any fees on an ongoing basis.

26

GIVE

You some issues to consider as you shop

STEP

5

27

GUARANTEED PAYMENTSAND INFLATION

IT’S IMPORTANT TO UNDERSTAND THAT THE PAYOUT YOU RECEIVE IS GUARANTEED.

No matter what happens in the stock market, with interest rates or other financial barometers, the dollar amount of your payout is guaranteed not to change. You’ve transferred those risks to the insurer when you bought the DIA.

28

GUARANTEED PAYMENTSAND INFLATION

IF YOU PURCHASE AN ANNUITY WITH INFLATION PROTECTION, your payout would be increased during the payout phase depending on consumer prices or the inflation increase level you selected.

BUT, THERE IS ONE SMALL CAVEAT AND IT INVOLVES INFLATION.

IF YOU PURCHASE A DIA WITHOUT INFLATION PROTECTION, the amount of money you receive every month is the same but the purchasing power of that money declines. This means that the amount of stuff you can buy with the same amount of money goes down over time. For a further discussion of inflation and annuities, check out our Inflation module.

29

CREDIT RISK

LIKE WITH ALL ANNUITIES, you should carefully consider the insurance company’s financial health when purchasing a DIA. Credit ratings (although imperfect) are a shorthand way of assessing the credit risk of the insurer. Most experts, including Abaris, do not recommend purchasing an annuity from an insurance company with a credit rating below A. At Abaris, we only carry insurers with credit ratings in the top quartile of the insurers based on the Comdex Index.

30

COMPARE

The different available features of an annuity and guide you through how to figure out if they make sense for youST

EP 6

31

NOW IT’S TIME TO TALK TRADEOFFS

The simplest DIA involves you getting a payment starting at the Income Start Date and continuing as long as you are alive.

THE CHECK IS THE SAME AMOUNT FOR AS LONG AS YOU LIVE.

But there are some features that you can add to the simplest DIA. We’re going to cover two of the most important types here.

32

One involves protecting yourself against passing away earlier than expected.

1

33

The other involves protecting yourself against inflation, or the risk that the constant payment won’t have the same purchasing power in the future.

Let’s take a few minutes to explain these features. In annuity parlance, these features are called Riders (Don’t ask us why. We also think it’s a silly name!).

2

34

DECISION #1

Do I purchase a Deferred Income Annuity with a Death Benefit, Period Certain, Return of Premium or Cash Refund feature included or not?With a Cash Refund, Death Benefit, Return of Premium or Period Certain feature, if you die younger than expected, your beneficiaries will receive some money. They are each slightly different, but this is the general gist.

‘‘‘‘

35

YOU’LL LIKE IT BECAUSE...

In the unfortunate event of your death, your beneficiaries still get something.

36

YOU WON’T LIKE IT BECAUSE...

Makes the annuity more expensive. All of these riders are essentially protection against dying younger than you expect, not living longer than you expect. Obviously, you’ll have to pay the insurance company more for protection against this additional risk.

Even with a Cash Refund or Death Benefit feature you usually aren’t getting the full value of your annuity back, only a portion. That’s because of a financial concept called The Time Value of Money.

DIAs are best at providing guaranteed lifetime income for you, but not the most efficient way to make sure money passes to your heirs. A Cash Refund feature gets away from the fundamental goal of a DIA, which is to protect you and your spouse against the risk of living a long time (not a short time).

37

Unless you can’t do without it, we recommend AGAINST purchasing a DIA with a Cash Refund, Death Benefit, Period Certain or Return of Premium feature.

VERDICT

Always remember, a DIA is insurance against longevity.It’s not an investment.

38

DECISION #2

Do I purchase a Deferred Income Annuity with inflation protection?‘‘ ‘‘

With an inflation protection feature, your payments will increase over time at the rate of some measure of inflation. This means that as the prices of the things you pay for in retirement increase, your income will increase along with them. For many, this is the ultimate form of guaranteed retirement income because it promises consistent purchasing power.

39

YOU’LL LIKE IT BECAUSE...

Inflation hasn’t been a real concern in recent memory. However, in other time periods in the United States it has quickly eroded the value of money and income. Inflation protection makes this the insurance company’s problem, not yours.

Inflation can be hard to predict. When you’re buying an annuity you don’t know what the rate of inflation will be during the accumulation period or the distribution period. Inflation protection helps remove the worry around this ambiguity.

In essence, inflation protection will better align your income and expenses in retirement which is in the spirit of the purpose of DIAs in the first place.

40

YOU WON’T LIKE IT BECAUSE...

Inflation protection isn’t free. Because the insurance company is taking on the risk that inflation will be higher than expected, they expect to be compensated for this in the form of a higher premium or a lower overall payout to you.

Inflation protection doesn’t cover you between the time you buy the annuity and the income start date. This is still risk you have to assume.

Inflation may not be high in the future. If inflation turns out to be lower than expected, you will have paid more for the inflation protection than it was actually worth.

41

Inflation protection is a VALUABLE FEATURE for the majority of people looking to purchase a DIA. For most, this feature allows a DIA to better match the goal of ensuring adequate guaranteed retirement income.

If you are going to purchase an inflation rider, ABARIS recommends purchasing a rider that ties your payments to an inflation measure known as CPI-U as it best captures the prices of goods that the majority of retirees typically purchase.

VERDICT

42

Buying a DIA is an important decision. We hope our materials have made the process easier to understand.

If you’d like personalized advice on whether an annuity might beright for you

We’re always excited to hear from you, REALLY!

JUST CONTACT OUR TEAM

43

END NOTES

Slide 09: Minimum deferral periods vary state to state.

Slide 14: Sources: New York Life, LIMRA and Retirement Income Journal.

44

DISCLAIMERThe information contained in this presentation, is provided for general informational purposes as a convenience to Abaris Financial Inc. customers and Internet users and is based upon information generally available to the public from sources believed to be reliable. Although we believe the information provided herein is reliable, we have not verified this information and we do not guarantee its accuracy, completeness, timeliness or availability. Any examples shown in this presentation are purely hypothetical and have been included for demonstrational purposes only. This information is subject to change without notice. This information is not a substitute for obtaining advice from a qualified professional. Therefore, you should not rely solely upon this information in making any decision. This information is not and does not constitute an offer to sell or a solicitation of an offer to buy any security, service or product.

Abaris Financial Inc., Philadelphia, PA is neither a registered broker-dealer nor a registered investment adviser. Nothing in this presentation, including links to other material, is intended as legal or tax advice. Abaris Financial Inc.’s Licensed Producers do not give legal or tax advice. Taxpayers should seek advice based on their particular circumstances from an independent tax advisor.