December 5, 2007 Webinar “Critical Year-End Strategies” S. James Park, J.D., LL.M. Mat Sorensen,...

15

December 5, 2007 Webinar “Critical Year-End Strategies” S. James Park, J.D., LL.M. Mat Sorensen, J.D. Hosted By: Mark J. Kohler, CPA, JD www.kkolawyers.com 856 South Sage Dr., Suite 2, Cedar City, Utah Telephone 435.586.9366 / Facsimile 435.586.9491 © Kyler Kohler & Ostermiller, LLP 2006

-

Upload

gloria-anne-caldwell -

Category

Documents

-

view

214 -

download

0

Transcript of December 5, 2007 Webinar “Critical Year-End Strategies” S. James Park, J.D., LL.M. Mat Sorensen,...

December 5, 2007

Webinar

“Critical Year-End Strategies”

S. James Park, J.D., LL.M. Mat Sorensen, J.D.Hosted By: Mark J. Kohler, CPA, JD

www.kkolawyers.com856 South Sage Dr., Suite 2, Cedar City, Utah

Telephone 435.586.9366 / Facsimile 435.586.9491

© Kyler Kohler & Ostermiller, LLP 2006

Disclaimer- Although the information contained in this Presentation may be extremely useful and helpful, please understand that the presentation of this information does not constitute an attorney-client relationship. Moreover, the information contained in this Presentation is for general guidance only. It is strongly recommended that each individual or entity obtain their own legal advice, particularly applied to their own set of circumstances, facts and specific situation. Kyler Kohler & Ostermiller, LLP is not responsible or liable for any advice that is taken and applied in a situation without direct consultation and representation specific to that individual’s or company’s needs.

Instructor Notes

© Kyler Kohler & Ostermiller, LLP 2006

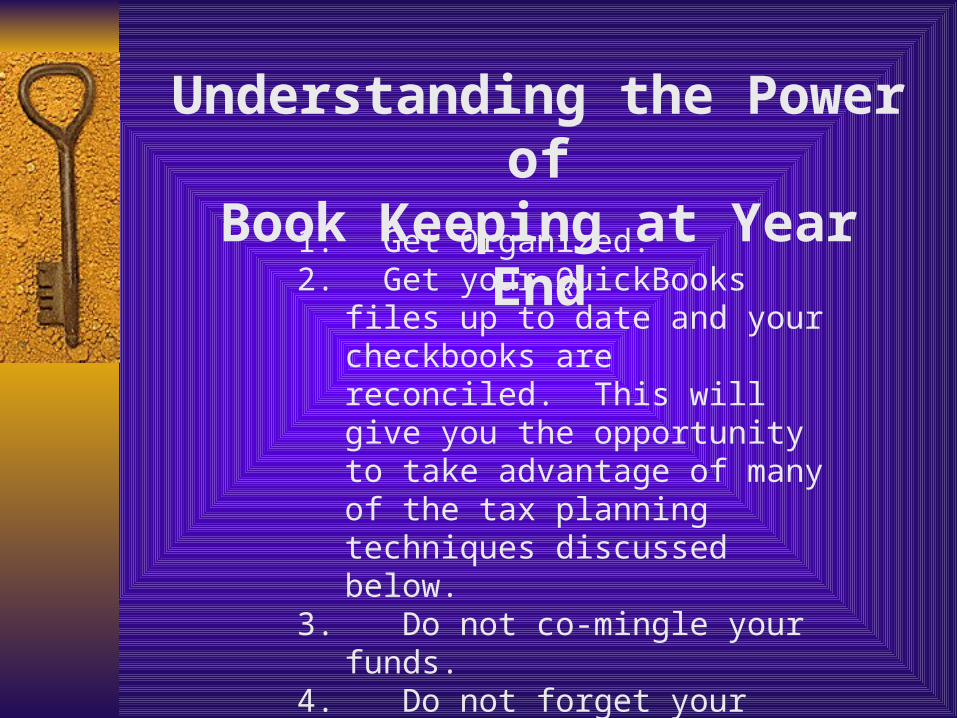

1. Get Organized.2. Get your QuickBooks files up to

date and your checkbooks are reconciled. This will give you the opportunity to take advantage of many of the tax planning techniques discussed below.

3. Do not co-mingle your funds.4. Do not forget your quarterly and

annual filings.5. Get ready for tax season and save

yourself hundreds if not thousands.

Understanding the Power ofBook Keeping at Year End

S-Corporation SalaryFor Year End

Salary/Dividend Splitting

Sole-Proprietorship

Limited LiabilityCompany S-Corporation

100kRevenue

50kExpenses

50kNet Income

Self Employment Tax 15.3%

$7,500 (approx)

Before regular income taxand itemized deductions

100kRevenue

50kExpenses

21,750kNet-Income from S-Corp

No Self Employment tax on the S-Corp Flow Thru Income

$3,327 SAVINGS!! (approx)

Before regular income taxand itemized deductions

25kSalary

3,825kEmployment taxes(approx)

•This is sample of what one taxpayer may choose to report as payroll. Each taxpayer should analyze their individual situation for the amount of payroll that is appropriate.

Maximize Your Retirement Plan

ContributionContribution / Deduction

• IRA (Traditional/Roth): $4,000 - $5,000 if you are over 50 years old.

• SIMPLE Plan: $10,500 - $12,500

• 401(k), 403(b), 457 Plans: $15,500 with 25% match up to $45,000

• SEP: Maximum $45,000 or 25% of compensation

• Other Defined Benefit Plans: From $50,000 to $300,000

Phase out limitations/Minimum Payroll amounts

• Single AGI Phase out: 52k – 62k•Roth 99k – 114k

• Married AGI Phase out: 83k – 103k• Roth 156k – 166k

• Equal to Salary amount, not to $12,500, or $15,000 if using catch up provisions

• Catch up provision of $5,000

• Equal to Salary amount, not to exceed $45,000

•Salary Calculations will be specific to each plan using the participant’s age and salary

Retirement PlanningDEADLINES:

• Existing IRA (Traditional/Roth) contributions: 4/15/2008

• Traditional to Roth conversions: 12/31/2007

• Employee contributions to a 401(k): 12/31/2007

• Employer contributions: By tax filing deadline, including extensions

• Note: In order for a self-employed individual or an employee to make a contribution in 2007 or take the accompanying deduction, the Plan must be adopted (or created) by 12/31/2007.

Maximizing Medical Expense

Deductions

- Insurance may be deductible on 1040 if self-employed

ItemizedDeductions

Health SavingsAccount (HSA)

Health Reimbursement

Arrangement (HRA)

- Everything else limited to 7.5% AGI

- Must maintain high deductible insurance policy

- Must utilize 3rd party admin

- Fixed payments, balances carry forward.

- $2,850 Individual- $5,650 Family

- No insurance requirement

- Self-administered

- No limits

- Reimbursement procedure

THE HEALTHY HIGH EXPENSES

Paying spouse or children before Year End

S-Corp or C-Corp

Director feeNo SE Tax

Employee15.3% FICA

FamilySole Prop

or SMLLC

Pay Children-NO FICA

Standard Deduction$5,350 – 2007

for earned income

Service or management

Fee

FamilyLLC

Over age 18 Under age 18Must be owned 100%

by Mom and/or Dad

Retirement Plan orHealth Reimbursement Plan

OPTION 1

OPTION 2

OPTION 3

529College Savings Plan

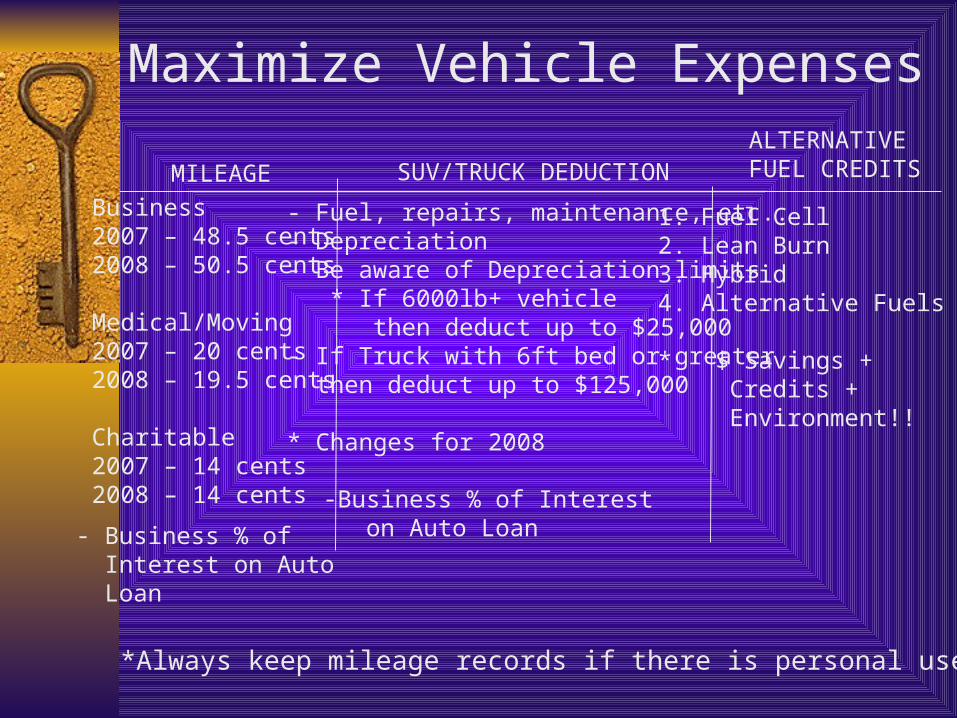

Maximize Vehicle Expenses

Business2007 – 48.5 cents2008 – 50.5 cents

Medical/Moving2007 – 20 cents2008 – 19.5 cents

Charitable2007 – 14 cents2008 – 14 cents

- Fuel, repairs, maintenance, etc..- Depreciation- Be aware of Depreciation limits * If 6000lb+ vehicle then deduct up to $25,000- If Truck with 6ft bed or greater then deduct up to $125,000

* Changes for 2008

MILEAGE SUV/TRUCK DEDUCTIONALTERNATIVEFUEL CREDITS

1. Fuel Cell2. Lean Burn3. Hybrid4. Alternative Fuels

* $ Savings + Credits + Environment!!

-Business % of Interest on Auto Loan- Business % of

Interest on Auto Loan

*Always keep mileage records if there is personal use

Understanding Acceleration or Deferral of

Income/ExpensesGenerally, you should defer income if at all possible. But in certain instances it may pay to accelerate income, for example:

• Too many deductions: If your itemized deductions exceed your taxable income, you should accelerate as much income as possible to fully utilize them.

• Change in income level: Anticipated changes in employment or gains from the sale of assets, etc. next year that could bump you into a higher bracket, making the tax on the accelerated income lower this year.

• Change in filing status: An upcoming marriage or divorce that will put you in a higher tax bracket may warrant the acceleration of income this year.

Understanding Acceleration or Deferral of

Income/ExpensesHere are a couple examples of how to do it:

• Year end bonus: Negotiate with your employer the timing of the bonus.

• Collect receivables: The timing of your collection may be critical.• Payment of expenses: Prepay or defer. Timing, timing, timing. • Incentive Stock Options: Exercise the option and dispose of the

stock (it has to make sense). • IRA or Plan Withdrawals: In the event that you are over 59 ½, you

might consider making withdrawals. • Installment Notes: The sale you made in a previous year can be

undone if you need the income this year rather than in the future. (Early pay-off; Use the note as collateral for a loan; or Sell the note to a third party) Any of these will trigger the otherwise deferred gain.

• Dividends: Timing, timing, timing.

Utilizing Cost Segregationand Depreciation

With CostSegregation

Without Cost Segregation

Assumption- $260,000 residential rental purchased in 2007, with a Land value of $65,000 (25%), $20,000 in 5-year property, and $24,000 in 15-year property. Remaining $151,000- Building.

Taxpayer – 30% tax bracket (25% Federal – 5% State)

Beware of Depreciation Recapture at Ordinary Rates!

Depreciation Expense- $31,662

*Potential Tax Savings - $12,740

Depreciation Expense w/ §179 -$49,262

Depreciation Expense- $6,795

* Assuming 25% Federal Rate and 5% State.

Intangible Oil and Gas DrillingCost Tax Deduction

(“IDCs”)- Invest in a “Drilling Program” on U.S. Soil

- Find a project with Diversity and beware of Exploratory Projects

- 90% to 100% dollar for dollar tax write off

- On going cash flow

- Liquidity to sell interest in years to come

- 1031 Exchange into the investment if you choose

EDUCATIONAL EXPENSE:

Buy Mark Kohler’s NEW BOOKBefore year end!!!

Visit www.lawyersareliars.com for more information

For more information, please contact us at:

KYLER, KOHLER & OSTERMILLER, LLP856 South Sage Dr., Suite 300

Cedar City, Utah 84720Tel: 435.586.9366 Fax: 435.586.9491

www.kkolawyers.com

THANK YOU