December 31, 2017 T. RowE PRICE PRFDX Equity … #6 PRFDX PAFDX RRFDX REIPX Equity Income Fund...

64

PRFDX PAFDX RRFDX REIPX Equity Income Fund Equity Income Fund– Advisor Class Equity Income Fund– R Class Equity Income Fund– I Class ANNUAL REPORT December 31, 2017 T. ROWE PRICE The fund invests in value-oriented stocks.

Transcript of December 31, 2017 T. RowE PRICE PRFDX Equity … #6 PRFDX PAFDX RRFDX REIPX Equity Income Fund...

Proof #6

PRFDX

PAFDX

RRFDX

REIPX

Equity Income Fund

Equity Income Fund– Advisor Class

Equity Income Fund– R Class

Equity Income Fund– I Class

aNNualREPORT

December 31, 2017

T. RowE PRICE

The fund invests in value-oriented stocks.

Proof #6

REPORTS ON THE WEB

Sign up for our Email Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

HIGHLIGHTS

• U.S.stockssurgedin2017asstrongercorporateearningsandsteadyeconomicgrowthpushedthemajorbenchmarkstorecordlevels.

• TheEquityIncomeFundreturned16.18%fortheyearandlaggedtheS&P500Indexbutoutperformeditsstyle-specificbenchmark,theRussell1000ValueIndex.

• Everysectorcontributedtoabsolutereturns.ComparedwiththeS&P500Index,consumerstaplesaddedthemosttorelativeperformance,whileinformationtechnologywasthebiggestdetractorduetoourunderweighttoIT,thebest-performingsector.ComparedwiththeRussell1000ValueIndex,industrialsandbusinessservicescontributedthemosttorelativereturns,whileutilitieswasthesoledetractor.

• Stockvaluationslookstretchedandotherassetpricesappearincreasinglyexpensivefollowingthepastyear’srally.Weanticipateabumpierridein2018asgeopoliticalrisksandhigherabsolutevaluationsarebalancedbyfavorableeconomicdataandcorporateearnings.

T. Rowe Price Equity Income Fund

TheviewsandopinionsinthisreportwerecurrentasofDecember31,2017.They are not guarantees of performance or investment results andshouldnotbe takenas investmentadvice. Investmentdecisionsreflectavarietyof factors,and themanagers reserve the right tochange theirviews about individual stocks, sectors, and the markets at any time.As a result, the views expressed should not be relied upon as a fore-castof the fund’s future investment intent.Thereport iscertifiedunderthe Sarbanes-Oxley Act, which requiresmutual funds and other publiccompanies to affirm that, to the best of their knowledge, the informa-tionintheirfinancialreportsisfairlyandaccuratelystatedinallmaterialrespects.

Proof #6

T. Rowe Price Equity Income Fund

Manager’s Letter

1

Fellow Shareholders

A recovery in corporate profits, steady economic growth overseas, and optimism

about the Trump administration’s plans for tax reform drove U.S. stocks higher in

2017. The S&P 500 Index and other major benchmarks surged to record levels into

December as earnings rebounded after more than a year of declining profits and the

U.S. economy showed signs of growing strength. The improving economic backdrop

worldwide allayed concerns about rising U.S. interest rates and geopolitical tensions

in a few countries. In this supportive environment, the Equity Income Fund posted a

double-digit return for the year.

The Equity Income Fund returned 10.05% and 16.18% for the six and 12 months ended December 31, 2017, respectively, trailing the S&P 500 Index, which returned 11.42% and 21.83%. (Returns for the Advisor, R, and I Class shares reflect different fee structures.) The fund outperformed the Russell 1000 Value Index, its style-specific benchmark, which returned 8.61%

and 13.66% over the corresponding periods. The fund outperformed its peer group, the Lipper Equity Income Funds Index, over the six-month period but lagged it for the full year.

The Equity Income Fund’s underperformance against the S&P 500 Index reflects the unusually large disparity in returns for growth and value stocks in 2017, when growth stocks returned more than twice as much as value stocks in the large-cap universe, according to

TotalReturnPeriodsEnded12/31/17 6Months 12Months

EquityIncomeFund 10.05% 16.18%

EquityIncomeFund–AdvisorClass 9.85 15.84

EquityIncomeFund–RClass 9.74 15.52

EquityIncomeFund–IClass 10.11 16.31

S&P500Index 11.42 21.83

Russell1000ValueIndex 8.61 13.66

LipperEquityIncomeFundsIndex 9.55 16.43

Performance Comparison

Proof #6

2

Russell indexes. The strong outperformance of growth stocks hurt the Equity Income Fund’s relative performance against the S&P 500 Index, which encompasses both growth and value stocks. Because we invest in undervalued companies with long-term appreciation prospects, it is unsurprising that the fund lagged the S&P 500 Index in a year when growth stocks widely outpaced value.

Effective March 1, 2018, the performance benchmark of the Equity Income Fund will change to the Russell 1000 Value Index from the current S&P 500 Index. We believe that the Russell 1000 Value Index is a more appropriate style-specific benchmark that better aligns with our value-focused investment style. Moreover, the Russell 1000 Value Index better captures our investment universe and provides a more accurate performance comparison when one investment style dominates another over a prolonged period. The benchmark change will not affect day-to-day management of the Equity Income Fund or its investment style, which remains unchanged since the fund’s 1985 inception.

Every sector contributed to the fund’s absolute returns for the year. Compared with the S&P 500 Index, consumer staples followed by real estate stocks contributed the most to relative performance, while information technology was the biggest detractor due to our underweight to IT, the best-performing sector in the S&P 500 Index. Measured against the Russell 1000 Value Index, industrials and business services and IT stocks, respectively, contributed the most to relative returns, while utilities were the sole detractor.

MaRkET ENvIRONMENT

The major U.S. stock market indexes repeatedly rose to record levels in the year’s second half as earnings beat expectations and investors anticipated that corporate tax cuts would boost profits even further. Signs of a global growth pickup grew more plentiful over 2017, pointing to “the broadest synchronized upswing the world economy has experienced in the last decade,” as the International Monetary Fund stated in July. The S&P 500 Index ended 2017 near a record high, joining other global stock benchmarks that finished at all-time or multiyear highs. The strong performance in the U.S. and other major markets occurred even as the Federal Reserve continued to tighten its accommodative monetary policy in place since the 2008 financial crisis. The Fed raised short-term interest rates three times over the year and signaled three more increases in 2018.

Proof #6

3

Large-cap shares outperformed their smaller peers. Growth stocks widely outpaced value stocks across all market capitalizations, according to various Russell indexes. In both the S&P 500 and Russell 1000 Value Indexes, nine out of 11 sectors advanced and two fell. IT stocks performed the best in both benchmarks, driven by outsized gains in a handful of high-growth technology and Internet stocks. Materials, consumer discretionary, financials, and health care were the next-best performers. On the other hand, telecommunication services stocks retreated as wireless companies contended with slowing growth and stiffer price competition. Energy stocks also declined as low oil prices weighed on the sector in the year’s first half. However, cooperation among the world’s major oil producers to curb output drove oil prices higher and helped energy stocks pare their losses by year-end.

PORTfOLIO REvIEW

The Equity Income Fund seeks to buy well-established, large-cap companies that typically have a strong record of paying dividends and appear to be undervalued by the market. The fund’s holdings tend to be solid, higher-quality companies going through a period of underperformance, reflecting our dual focus on valuation and dividend yield. We rely on the insights of T. Rowe Price’s large team of equity analysts and use an active, research-driven investment approach to select individual stocks based on their unique merits, rather than picking stocks based on broader market or economic trends. As of December 31, 2017, the dividend yield of the Equity Income Fund was 2.55% versus 1.88% for the S&P 500. All but two companies in the fund paid a dividend over the past 12 months.

Stock selection was strongest in the consumer staples sector, which produced several of the fund’s top contributors. Tyson Foods helped returns as the meat company reaped the rewards of its longstanding plan to focus on branded and prepared foods, which helped it report surprisingly strong earnings in 2017. We also benefited from our position in Wal-Mart as the retailer stepped up efforts to improve its e-commerce business. We owned Wal-Mart for its huge network of brick-and-mortar stores, which we reasoned gives it an edge over other big-box retailers and other e-commerce players as same- and next-day delivery becomes more widespread, and we are pleased to see its online initiatives start to pay off. Our consumer staples exposure rose

Proof #6

4

over the past six months as we took advantage of attractive valuations in a few companies. We initiated a position in Kimberly-Clark and added to Philip Morris International on weakness after the cigarette maker delivered underwhelming earnings. (Please refer to the portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

The industrials and business services sector added value, largely owing to our position in Boeing, the fund’s top contributor to returns.

Boeing shares climbed to a record high in 2017 as the aerospace company reaped the benefits of productivity gains, cost cuts, and rising global air traffic growth. We continue to like Boeing but regard

the company’s reward-to-risk ratio as slightly less favorable following the recent months’ rally and have reduced our position accordingly. Defense industry electronics maker Harris was another significant contributor. Harris shares rose amid expectations for increased U.S. defense spending and lower corporate taxes resulting from the recent tax overhaul. We believe Harris has strong growth

PercentofNetAssets 6/30/17 12/31/17

Financials 25.8% 26.3%

HealthCare 11.2 11.6

IndustrialsandBusinessServices 11.8 10.3

Energy 9.4 9.6

InformationTechnology 8.1 8.3

ConsumerStaples 6.3 7.8

ConsumerDiscretionary 8.1 7.6

Utilities 6.8 5.5

Materials 4.9 5.4

TelecommunicationServices 2.9 3.0

RealEstate 2.1 2.1

OtherandReserves 2.6 2.5

Total 100.0% 100.0%

Historicalweightingsreflectcurrentindustry/sectorclassifications.

Sector Diversification

Equity Income S&P500Asof12/31/17 Fund Index

Price/BookRatio 2.3X 4.4X

Price/EarningsRatio(Basedonnext12months’estimatedearnings)* 16.1X 19.8X

HistoricalBeta(Basedonmonthlyreturnsforfiveyears) 1.0 1.0

*Sourcefordata:IBES.Statisticsarebasedonthecompaniesinthefund’sportfolioandarenotaprojectionoffuturefundperformance.

Financial Profile

Proof #6

5

tailwinds for the next several years as the U.S. military upgrades its communication systems and the company sells more products overseas. On the other hand, our position in industrial conglomerate GE weighed on returns. GE shares sank to a multiyear low by year-end as the company struggled to overhaul its sprawling operations and investors expressed skepticism about a turnaround plan unveiled by its new chief executive. For more than a year, we have gradually trimmed our GE position as we waited for evidence that would help us determine whether management would be able to fix some of the company’s businesses. GE ranked among our biggest sales for the year.

Information technology stocks contributed to absolute returns. Despite our lack of exposure to several high-flying tech names, we added value through our holdings in Microsoft, which is strongly benefiting from its ongoing push into cloud-based computing services, and in semiconductor manufacturing equipment maker Applied Materials.

OuTLOOk

U.S. stocks benefited in 2017 from better-than-expected earnings, synchronized global growth, tame inflation, and a more benign regulatory environment. Most of the risks that investors feared at the outset of the year—such as a shift toward U.S. protectionism, a misstep in monetary policy by the Fed, or a geopolitical crisis—failed to materialize. The U.S. economy is in solid shape, and the underpinnings for stronger corporate profits growth are intact. The recent passage of the corporate tax reform bill should be a strong tailwind for the market over the next year. However, stock valuations look stretched and other asset prices appear increasingly expensive following the past year’s rally. Widespread optimism about the U.S. economy and stock market has led to a sense of confidence among many investors who assume that the supportive conditions of the past year will persist into 2018. We believe that much of the good news is already priced into financial markets and worry that investor confidence will turn into complacency.

We would not be surprised to see the stock market grind higher in the coming months, aided by the recent tax overhaul. However, our outlook is tempered by several risks to global growth. An unexpected slowdown in China, whose economy outpaced expectations in 2017, would have negative repercussions for global financial markets. Tensions on the Korean peninsula or in the Middle East could flare up

Proof #6

6

again, with potentially adverse consequences for oil prices arising from a Mideast conflict. On the economic front, stronger U.S. growth could increase inflation pressures, leading the Fed to raise interest rates at an unexpectedly fast pace that could curb stock price gains.

We anticipate a bumpier ride in 2018 as geopolitical risks and higher absolute valuation levels are balanced by positive economic data and corporate earnings. Thanks to T. Rowe Price’s strengths in fundamental research and the collective insights of our equity analysts, we are well equipped to navigate what will likely be a more volatile environment and continue to identify higher-quality, undervalued companies for your fund. We are confident that our disciplined investment approach, thoughtful stock selection, and attention to valuation will allow us to continue delivering solid shareholder returns over the long term.

Thank you for investing with T. Rowe Price.

Respectfully submitted,

John D. Linehan President of the fund and chairman of its Investment Advisory Committee

Heather McPherson Associate portfolio manager

January 10, 2018

The committee chairman has day-to-day responsibility for managing the fund and works with committee members in developing and executing the fund’s investment program.

Proof #6

7

T. Rowe Price Equity Income Fund

Risks of Investing in the Fund

Valueinvestorsseektoinvestincompanieswhosestockpricesarelowinrelationtotheirrealworthorfutureprospects.Byidentifyingcompanieswhosestocksarecurrentlyoutoffavorormisunderstood,valueinvestorshopetorealizesignificantappreciationasotherinvestorsrecognizethestock’sintrinsicvalueandthepricerisesaccordingly.Thevalueapproachcarriestheriskthatthemarketwillnotrecognizeasecurity’sintrinsicvalueforalongtimeorthatastockjudgedtobeundervaluedmayactuallybeappropriatelypriced.

Glossary

Dividend yield:Theannualdividendofastockdividedbythestock’sprice.

Earnings growth rate – current fiscal year:Measurestheannualizedpercentchangeinearningspersharefromthepriorfiscalyeartothecurrentfiscalyear.

Lipper indexes:Fundbenchmarksthatconsistofasmallnumber(10to30)ofthelargestmutualfundsinaparticularcategoryastrackedbyLipperInc.

Price-to-earnings (P/E) ratio – current fiscal year:Avaluationmeasurecalculatedbydividingthepriceofastockbyitsreportedearningspersharefromthelatestfiscalyear.Theratioisameasureofhowmuchinvestorsarewillingtopayforthecompany’searnings.ThehighertheP/E,themoreinvestorsarepayingforthecompany’scurrentearnings.

Price-to-earnings (P/E) ratio – next fiscal year:Avaluationmeasurecalculatedbydividingthepriceofastockbyitsestimatedearningsforthenextfiscalyear.Theratioisameasureofhowmuchinvestorsarewillingtopayforthecompany’sfutureearnings.ThehighertheP/E,themoreinvestorsarepayingforthecompany’sexpectedearningsgrowthinthenextfiscalyear.

Price-to-earnings (P/E) ratio – 12 months forward:Avaluationmeasurecalculatedbydividingthepriceofastockbytheanalysts’forecastofthenext12months’expectedearnings.Theratioisameasureofhowmuchinvestorsarewillingtopayforthecompany’sfutureearnings.ThehighertheP/E,themoreinvestorsarepayingforthecompany’searningsgrowthinthenext12months.

Projected earnings growth rate (IBES):Acompany’sexpectedearningspersharegrowthrateforagiventimeperiodbasedontheforecastfromtheInstitutionalBrokers’EstimateSystem,whichiscommonlyreferredtoasIBES.

Russell 1000 value Index:Anindexthattrackstheperformanceoflarge-capstockswithlowerprice-to-bookratiosandlowerforecastedgrowthvalues.

S&P 500 Index:Anunmanagedindexthattracksthestocksof500primarilylarge-capU.S.companies.

RussellInvestmentGroupisthesourceandownerofthetrademarks,servicemarks,andcopyrightsrelatedtotheRussellindexes.Russell®isatrademarkofRussellInvestmentGroup.

Proof #6

8

T. Rowe Price Equity Income Fund

TWENTY-fIvE LaRGEST HOLDINGS

Percentof NetAssets 12/31/17

JPMorganChase 3.9%WellsFargo 2.8ExxonMobil 2.6MorganStanley 2.2Microsoft 2.1

VerizonCommunications 2.0Johnson&Johnson 1.9Total 1.9DowDuPont 1.9Qualcomm 1.8

Anthem 1.8StateStreet 1.7Twenty-FirstCenturyFox 1.7Harris 1.7SouthernCompany 1.6

Boeing 1.6Citigroup 1.5JohnsonControlsInternational 1.5CiscoSystems 1.5Becton,Dickinson&Company 1.5

Loews 1.4U.S.Bancorp 1.4Pfizer 1.4TysonFoods 1.4FifthThirdBancorp 1.3

Total 46.1%

Note:Theinformationshowndoesnotreflectanyexchange-tradedfunds(ETFs),cashreserves,orcollateralforsecuritieslendingthatmaybeheldintheportfolio.

Portfolio Highlights

Proof #6

9

T. Rowe Price Equity Income Fund

MaJOR PORTfOLIO CHaNGESListedindescendingorderofsize.

SixMonthsEnded12/31/17

Largest Purchases Largest Sales

Kimberly-Clark*SouthernCompanyGlaxoSmithKlineBrighthouseFinancial*AmericanInternationalGroup*TransCanada*ChubbWellsFargoPhilipMorrisInternationalCVSHealth*

BoeingRoyalDutchShell**IllinoisToolWorksAmericanExpress**AmeripriseFinancialXCELEnergy**AppliedMaterialsCarnival**GEExelon

12MonthsEnded12/31/17

Largest Purchases Largest Sales

SouthernCompanyKimberly-Clark*AmericanInternationalGroup*TysonFoods*U.S.BancorpWellsFargoChubbTransCanada*Becton,Dickinson&CompanyGileadSciences

BoeingRoyalDutchShell**AmericanExpress**BankofAmericaAES**GEXCELEnergy**Carnival**AmeripriseFinancialMarsh&McLennan

*Positionadded. **Positioneliminated.

Portfolio Highlights

Proof #6

T. Rowe Price Equity Income Fund

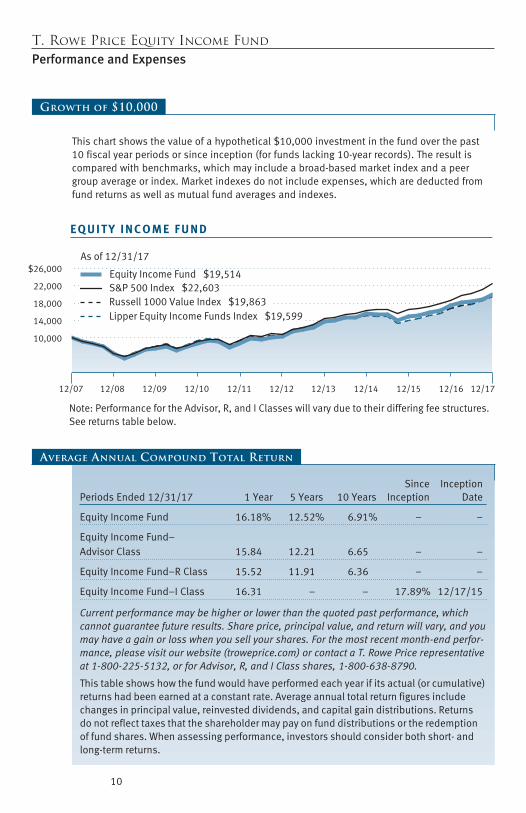

Performance and Expenses

10

Equity Income Fund $19,514

As of 12/31/17

12/07 12/08 12/09 12/10 12/11 12/12 12/13 12/14 12/15 12/16 12/17

E Q U I T Y I N C O M E F U N D

Lipper Equity Income Funds Index $19,599

S&P 500 Index $22,603

Note: Performance for the Advisor, R, and I Classes will vary due to their differing fee structures. See returns table below.

10,000

14,000

18,000

22,000

$26,000

Russell 1000 Value Index $19,863

Growth of $10,000

Thischartshowsthevalueofahypothetical$10,000investmentinthefundoverthepast10fiscalyearperiodsorsinceinception(forfundslacking10-yearrecords).Theresultiscomparedwithbenchmarks,whichmayincludeabroad-basedmarketindexandapeergroupaverageorindex.Marketindexesdonotincludeexpenses,whicharedeductedfromfundreturnsaswellasmutualfundaveragesandindexes.

Since InceptionPeriodsEnded12/31/17 1Year 5Years 10Years Inception Date

EquityIncomeFund 16.18% 12.52% 6.91% – –

EquityIncomeFund–AdvisorClass 15.84 12.21 6.65 – –

EquityIncomeFund–RClass 15.52 11.91 6.36 – –

EquityIncomeFund–IClass 16.31 – – 17.89% 12/17/15

Current performance may be higher or lower than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will vary, and you may have a gain or loss when you sell your shares. For the most recent month-end perfor-mance, please visit our website (troweprice.com) or contact a T. Rowe Price representative at 1-800-225-5132, or for Advisor, R, and I Class shares, 1-800-638-8790.

Thistableshowshowthefundwouldhaveperformedeachyearifitsactual(orcumulative)returnshadbeenearnedataconstantrate.Averageannualtotalreturnfiguresincludechangesinprincipalvalue,reinvesteddividends,andcapitalgaindistributions.Returnsdonotreflecttaxesthattheshareholdermaypayonfunddistributionsortheredemptionoffundshares.Whenassessingperformance,investorsshouldconsiderbothshort-andlong-termreturns.

Average Annual Compound Total Return

Proof #6

11

T. Rowe Price Equity Income Fund

Fund Expense Example

Asamutualfundshareholder,youmayincurtwotypesofcosts:(1)transactioncosts,suchasredemptionfeesorsalesloads,and(2)ongoingcosts,includingmanagementfees,distributionandservice(12b-1)fees,andotherfundexpenses.Thefollowingexampleisintendedtohelpyouunderstandyourongoingcosts(indollars)ofinvestinginthefundandtocomparethesecostswiththeongoingcostsofinvestinginothermutualfunds.Theexampleisbasedonaninvestmentof$1,000investedatthebeginningofthemostrecentsix-monthperiodandheldfortheentireperiod.

Pleasenotethatthefundhasfourshareclasses:Theoriginalshareclass(InvestorClass)chargesnodistributionandservice(12b-1)fee,AdvisorClasssharesareofferedonlythroughunaffiliatedbrokersandotherfinancialintermediariesandchargea0.25%12b-1fee,RClasssharesareavailabletoretirementplansservicedbyintermediariesandchargea0.50%12b-1fee,andIClasssharesareavailabletoinstitutionallyorientedclientsandimposeno12b-1oradministrativefeepayment.Eachshareclassispresentedseparatelyinthetable.

actual ExpensesThefirstlineofthefollowingtable(Actual)providesinformationaboutactualaccountvaluesandexpensesbasedonthefund’sactualreturns.Youmayusetheinformationonthisline,togetherwithyouraccountbalance,toestimatetheexpensesthatyoupaidovertheperiod.Simplydivideyouraccountvalueby$1,000(forexample,an$8,600accountvaluedividedby$1,000=8.6),thenmultiplytheresultbythenumberonthefirstlineundertheheading“ExpensesPaidDuringPeriod”toestimatetheexpensesyoupaidonyouraccountduringthisperiod.

Hypothetical Example for Comparison PurposesTheinformationonthesecondlineofthetable(Hypothetical)isbasedonhypotheticalaccountvaluesandexpensesderivedfromthefund’sactualexpenseratioandanassumed5%peryearrateofreturnbeforeexpenses(notthefund’sactualreturn).Youmaycomparetheongoingcostsofinvestinginthefundwithotherfundsbycontrastingthis5%hypotheticalexampleandthe5%hypotheticalexamplesthatappearintheshareholderreportsoftheotherfunds.Thehypotheticalaccountvaluesandexpensesmaynotbeusedtoestimatetheactualendingaccountbalanceorexpensesyoupaidfortheperiod.

EquityIncomeFund 0.66%

EquityIncomeFund–AdvisorClass 0.94

EquityIncomeFund–RClass 1.21

EquityIncomeFund–IClass 0.54

Theexpenseratioshownisasofthefund’sfiscalyearended12/31/16.Thisnumbermayvaryfromtheexpenseratioshownelsewhereinthisreportbecauseitisbasedonadifferenttimeperiodand,ifapplicable,includesacquiredfundfeesandexpensesbutdoesnotincludefeeorexpensewaivers.

Expense Ratio

Proof #6

12

T. Rowe Price Equity Income Fund

Fund Expense Example (continued)

Note:T.RowePricechargesanannualaccountservicefeeof$20,generallyforaccountswithlessthan$10,000.ThefeeiswaivedforanyinvestorwhoseT.RowePricemutualfundaccountstotal$50,000ormore;accountselectingtoreceiveelectronicdeliveryofaccountstatements,transactionconfirmations,prospectuses,andshareholderreports;oraccountsofaninvestorwhoisaT.RowePricePersonalServicesorEnhancedPersonalServicesclient(enrollmentintheseprogramsgenerallyrequiresT.RowePriceassetsofatleast$250,000).Thisfeeisnotincludedintheaccompanyingtable.Ifyouaresubjecttothefee,keepitinmindwhenyouareestimatingtheongoingexpensesofinvestinginthefundandwhencomparingtheexpensesofthisfundwithotherfunds.

Youshouldalsobeawarethattheexpensesshowninthetablehighlightonlyyourongoingcostsanddonotreflectanytransactioncosts,suchasredemptionfeesorsalesloads.Therefore,thesecondlineofthetableisusefulincomparingongoingcostsonlyandwillnothelpyoudeterminetherelativetotalcostsofowningdifferentfunds.Totheextentafundchargestransactioncosts,however,thetotalcostofowningthatfundishigher.

ExpensesPaid Beginning Ending DuringPeriod* AccountValue AccountValue 7/1/17to 7/1/17 12/31/17 12/31/17

Investor ClassActual $1,000.00 $1,100.50 $3.49

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,021.88 3.36

advisor ClassActual 1,000.00 1,098.50 5.02

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,020.42 4.84

R ClassActual 1,000.00 1,097.40 6.40

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,019.11 6.16

Equity Income Fund

Proof #6

13

T. Rowe Price Equity Income Fund

ExpensesPaid Beginning Ending DuringPeriod* AccountValue AccountValue 7/1/17to 7/1/17 12/31/17 12/31/17

I ClassActual $1,000.00 $1,101.10 $2.97

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,022.38 2.85

*Expensesareequaltothefund’sannualizedexpenseratioforthe6-monthperiod,multipliedbytheaverageaccountvalueovertheperiod,multipliedbythenumberofdaysinthemostrecentfiscalhalfyear(184),anddividedbythedaysintheyear(365)toreflectthehalf-yearperiod.TheannualizedexpenseratiooftheInvestorClasswas0.66%,theAdvisorClasswas0.95%,theRClasswas1.21%,andtheIClasswas0.56%.

Equity Income Fund (continued)

Fund Expense Example (continued)

Proof #6

14

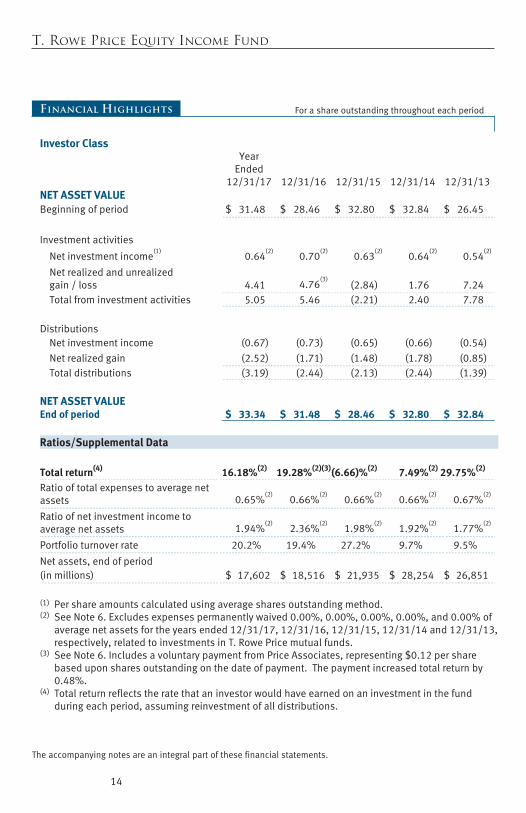

T. Rowe Price Equity Income Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

Investor Class

Year Ended

12/31/17

12/31/16

12/31/15

12/31/14

12/31/13

NET ASSET VALUE

Beginning of period

$ 31.48

$ 28.46

$ 32.80

$ 32.84

$ 26.45

Investment activities

Net investment income(1)

0.64(2)

0.70(2)

0.63(2)

0.64(2)

0.54(2)

Net realized and unrealized gain / loss

4.41

4.76

(3) (2.84)

1.76

7.24

Total from investment activities

5.05

5.46

(2.21)

2.40

7.78

Distributions

Net investment income

(0.67)

(0.73)

(0.65)

(0.66)

(0.54)

Net realized gain

(2.52)

(1.71)

(1.48)

(1.78)

(0.85)

Total distributions

(3.19)

(2.44)

(2.13)

(2.44)

(1.39)

NET ASSET VALUE

End of period $ 33.34 $ 31.48 $ 28.46 $ 32.80 $ 32.84

Ratios/Supplemental Data Total return(4) 16.18%(2) 19.28%(2)(3)(6.66)%(2) 7.49%(2) 29.75%(2)

Ratio of total expenses to average net assets

0.65%

(2) 0.66%

(2) 0.66%

(2) 0.66%

(2) 0.67%

(2)

Ratio of net investment income to average net assets

1.94%

(2) 2.36%

(2) 1.98%

(2) 1.92%

(2) 1.77%

(2)

Portfolio turnover rate

20.2%

19.4%

27.2%

9.7%

9.5%

Net assets, end of period

(in millions)

$ 17,602

$ 18,516

$ 21,935

$ 28,254

$ 26,851

(1) Per share amounts calculated using average shares outstanding method. (2) See Note 6. Excludes expenses permanently waived 0.00%, 0.00%, 0.00%, 0.00%, and 0.00% of

average net assets for the years ended 12/31/17, 12/31/16, 12/31/15, 12/31/14 and 12/31/13, respectively, related to investments in T. Rowe Price mutual funds.

(3) See Note 6. Includes a voluntary payment from Price Associates, representing $0.12 per share based upon shares outstanding on the date of payment. The payment increased total return by 0.48%.

(4) Total return reflects the rate that an investor would have earned on an investment in the fund during each period, assuming reinvestment of all distributions.

Proof #6

15

T. Rowe Price Equity Income Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

Advisor Class

Year Ended

12/31/17

12/31/16

12/31/15

12/31/14

12/31/13

NET ASSET VALUE

Beginning of period

$ 31.40

$ 28.40

$ 32.74

$ 32.77

$ 26.39

Investment activities

Net investment income(1)

0.54(2)

0.62(2)

0.53(2)

0.56(2)

0.45(2)

Net realized and unrealized gain / loss

4.40

4.74

(3) (2.82)

1.74

7.24

Total from investment activities

4.94

5.36

(2.29)

2.30

7.69

Distributions

Net investment income

(0.56)

(0.65)

(0.57)

(0.55)

(0.46)

Net realized gain

(2.52)

(1.71)

(1.48)

(1.78)

(0.85)

Total distributions

(3.08)

(2.36)

(2.05)

(2.33)

(1.31)

NET ASSET VALUE

End of period $ 33.26 $ 31.40 $ 28.40 $ 32.74 $ 32.77

Ratios/Supplemental Data Total return(4) 15.84%(2) 18.94%(2)(3)(6.92)%(2) 7.18%(2) 29.44%(2)

Ratio of total expenses to average net assets

0.94%

(2) 0.94%

(2) 0.93%

(2) 0.93%

(2) 0.94%

(2)

Ratio of net investment income to average net assets

1.64%

(2) 2.08%

(2) 1.68%

(2) 1.66%

(2) 1.49%

(2)

Portfolio turnover rate

20.2%

19.4%

27.2%

9.7%

9.5%

Net assets, end of period

(in millions)

$ 422

$ 521

$ 686

$ 1,392

$ 2,561

(1) Per share amounts calculated using average shares outstanding method. (2) See Note 6. Excludes expenses permanently waived 0.00%, 0.00%, 0.00%, 0.00%, and 0.00% of

average net assets for the years ended 12/31/17, 12/31/16, 12/31/15, 12/31/14 and 12/31/13, respectively, related to investments in T. Rowe Price mutual funds.

(3) See Note 6. Includes a voluntary payment from Price Associates, representing $0.12 per share based upon shares outstanding on the date of payment. The payment increased total return by 0.48%.

(4) Total return reflects the rate that an investor would have earned on an investment in the fund during each period, assuming reinvestment of all distributions.

Proof #6

16

T. Rowe Price Equity Income Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

R Class

Year Ended

12/31/17

12/31/16

12/31/15

12/31/14

12/31/13

NET ASSET VALUE

Beginning of period

$ 31.35

$ 28.35

$ 32.67

$ 32.72

$ 26.36

Investment activities

Net investment income(1)

0.44(2)

0.53(2)

0.45(2)

0.46(2)

0.37(2)

Net realized and unrealized gain / loss

4.40

4.74

(3) (2.82)

1.75

7.22

Total from investment activities

4.84

5.27

(2.37)

2.21

7.59

Distributions

Net investment income

(0.47)

(0.56)

(0.47)

(0.48)

(0.38)

Net realized gain

(2.52)

(1.71)

(1.48)

(1.78)

(0.85)

Total distributions

(2.99)

(2.27)

(1.95)

(2.26)

(1.23)

NET ASSET VALUE

End of period $ 33.20 $ 31.35 $ 28.35 $ 32.67 $ 32.72

Ratios/Supplemental Data Total return(4) 15.52%(2) 18.63%(2)(3)(7.18)%(2) 6.91%(2) 29.07%(2)

Ratio of total expenses to average net assets

1.22%

(2) 1.20%

(2) 1.19%

(2) 1.19%

(2) 1.20%

(2)

Ratio of net investment income to average net assets

1.35%

(2) 1.80%

(2) 1.44%

(2) 1.39%

(2) 1.23%

(2)

Portfolio turnover rate

20.2%

19.4%

27.2%

9.7%

9.5%

Net assets, end of period

(in thousands)

$ 99,972

$ 134,460

$ 203,518

$ 353,908

$ 351,544

(1) Per share amounts calculated using average shares outstanding method. (2) See Note 6. Excludes expenses permanently waived 0.00%, 0.00%, 0.00%, 0.00%, and 0.00% of

average net assets for the years ended 12/31/17, 12/31/16, 12/31/15, 12/31/14 and 12/31/13, respectively, related to investments in T. Rowe Price mutual funds.

(3) See Note 6. Includes a voluntary payment from Price Associates, representing $0.12 per share based upon shares outstanding on the date of payment. The payment increased total return by 0.48%.

(4) Total return reflects the rate that an investor would have earned on an investment in the fund during each period, assuming reinvestment of all distributions.

Proof #6

17

T. Rowe Price Equity Income Fund

Financial Highlights For a share outstanding throughout each period

I Class

Year Ended

12/31/17

12/31/16

12/17/15(1)

Through

12/31/15

NET ASSET VALUE

Beginning of period

$ 31.48

$ 28.47

$ 28.27

Investment activities

Net investment income(2)

0.69(3)

0.88(3)

–(3)(4)(5)

Net realized and unrealized gain / loss

4.40

4.61(6)

0.20

Total from investment activities

5.09

5.49

0.20

Distributions

Net investment income

(0.70)

(0.77)

–

Net realized gain

(2.52)

(1.71)

–

Total distributions

(3.22)

(2.48)

–

NET ASSET VALUE

End of period $ 33.35 $ 31.48 $ 28.47

Ratios/Supplemental Data Total return(7) 16.31%(3) 19.40%(3)(6) 0.71%(3)(4)

Ratio of total expenses to average net assets

0.55%(3)

0.54%(3)

0.58%(3)(4)(8)

Ratio of net investment income to average net assets

2.06%(3)

2.89%(3)

1.15%(3)(4)(8)

Proof #6

18

T. Rowe Price Equity Income Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

Year Ended

12/31/17

12/31/16

12/17/15(1)

Through

12/31/15

Ratios/Supplemental Data (continued) Portfolio turnover rate

20.2%

19.4%

27.2%

Net assets, end of period

(in millions)

$ 4,235

$ 3,521

$ 6

(1) Inception date (2) Per share amounts calculated using average shares outstanding method. (3) See Note 6. Excludes expenses permanently waived 0.00%, 0.00% and 0.00% of average net

assets for the years ended 12/31/17, 12/31/16 and for the period ended 12/31/15, respectively, related to investments in T. Rowe Price mutual funds.

(4) See Note 6. Excludes expenses in excess of a 0.05% contractual operating expense limitation in effect through 4/30/18.

(5) Amounts round to less than $0.01 per share. (6) See Note 6. Includes a voluntary payment from Price Associates, representing $0.12 per share

based upon shares outstanding on the date of payment. The payment increased total return by 0.45%.

(7) Total return reflects the rate that an investor would have earned on an investment in the fund during each period, assuming reinvestment of all distributions.

(8) Annualized

Proof #6

T. Rowe Price Equity Income Fund December 31, 2017

Portfolio of Investments ‡ Shares/Par $ Value

(Cost and value in $000s)

19

COMMON STOCKS 95.8%

CONSUMER DISCRETIONARY 7.6%

Auto Components 0.6%

Adient 1,840,000 144,808

144,808

Automobiles 0.3%

Ford Motor 4,500,000 56,205

56,205

Hotels, Restaurants & Leisure 1.0%

Las Vegas Sands 3,080,000 214,029

214,029

Leisure Products 0.5%

Mattel 7,175,000 110,352

110,352

Media 4.1%

Comcast, Class A 6,590,000 263,929

News Corp, Class A 11,800,000 191,278

Twenty-First Century Fox 11,190,000 381,803

Walt Disney 660,000 70,957

907,967

Multiline Retail 0.9%

Kohl's 3,170,000 171,909

Macy's 1,310,000 32,999

204,908

Specialty Retail 0.2%

L Brands 920,000 55,402

55,402

Total Consumer Discretionary 1,693,671

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

20

CONSUMER STAPLES 7.8%

Beverages 1.3%

Diageo (GBP) 1,480,000 54,249

PepsiCo 1,900,000 227,848

282,097

Food & Staples Retailing 1.5%

CVS Health 960,000 69,600

Wal-Mart 2,735,000 270,081

339,681

Food Products 2.6%

Archer-Daniels-Midland 4,560,000 182,765

Kellogg 1,370,000 93,133

Tyson Foods, Class A 3,750,000 304,012

579,910

Household Products 1.1%

Kimberly-Clark 2,090,000 252,179

252,179

Personal Products 0.4%

Coty, Class A 4,700,000 93,483

93,483

Tobacco 0.9%

Philip Morris International 1,908,900 201,675

201,675

Total Consumer Staples 1,749,025

ENERGY 9.6%

Oil, Gas & Consumable Fuels 9.6%

Apache 4,410,000 186,190

Canadian Natural Resources 620,000 22,146

Chevron 2,070,000 259,143

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

21

EQT 470,000 26,752

ExxonMobil 6,975,000 583,389

Hess 4,710,000 223,584

Occidental Petroleum 3,660,000 269,596

Total (EUR) 7,810,000 431,112

Total, Rights, 1/3/18 (EUR)(1) 7,850,000 —

TransCanada 3,100,000 150,784

Total Energy 2,152,696

FINANCIALS 26.3%

Banks 12.9%

Bank of America 1,460,000 43,099

Citigroup 4,575,000 340,426

Fifth Third Bancorp 9,800,000 297,332

JPMorgan Chase 8,090,000 865,145

KeyCorp 8,950,000 180,521

PNC Financial Services Group 1,520,000 219,321

U.S. Bancorp 5,820,000 311,836

Wells Fargo 10,450,000 634,001

2,891,681

Capital Markets 6.6%

Ameriprise Financial 1,200,000 203,364

Bank of New York Mellon 3,470,000 186,894

Franklin Resources 1,290,000 55,896

Morgan Stanley 9,300,000 487,971

Northern Trust 1,525,000 152,332

State Street 3,935,000 384,096

1,470,553

Insurance 6.8%

American International Group 4,350,000 259,173

Brighthouse Financial (1) 2,770,000 162,433

Chubb 1,585,000 231,616

Loews 6,460,000 323,194

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

22

Marsh & McLennan 1,445,000 117,608

MetLife 5,350,000 270,496

Willis Towers Watson 479,503 72,256

XL Group 2,580,000 90,713

1,527,489

Total Financials 5,889,723

HEALTH CARE 10.9%

Biotechnology 1.1%

Gilead Sciences 3,360,000 240,710

240,710

Health Care Equipment & Supplies 1.9%

Becton, Dickinson & Company 790,000 169,108

Medtronic 3,200,000 258,400

427,508

Health Care Providers & Services 1.8%

Anthem 1,800,000 405,018

405,018

Pharmaceuticals 6.1%

Bristol-Myers Squibb 3,040,000 186,291

GlaxoSmithKline (GBP) 7,300,000 129,277

GlaxoSmithKline, ADR 2,490,000 88,320

Johnson & Johnson 3,100,000 433,132

Merck 3,770,000 212,138

Pfizer 8,520,000 308,595

1,357,753

Total Health Care 2,430,989

INDUSTRIALS & BUSINESS SERVICES 10.2%

Aerospace & Defense 3.4%

Boeing 1,205,000 355,366

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

23

Harris 2,645,000 374,664

United Technologies 226,900 28,946

758,976

Air Freight & Logistics 1.2%

UPS, Class B 2,250,000 268,087

268,087

Airlines 0.8%

Delta Air Lines 1,680,000 94,080

Southwest Airlines 1,450,000 94,903

188,983

Building Products 1.5%

Johnson Controls International 8,830,000 336,511

336,511

Commercial Services & Supplies 0.2%

Stericycle (1) 750,000 50,993

50,993

Electrical Equipment 0.9%

Emerson Electric 3,050,000 212,554

212,554

Industrial Conglomerates 0.5%

GE 6,150,000 107,318

107,318

Machinery 1.7%

Flowserve 2,650,000 111,645

Illinois Tool Works 810,000 135,148

Pentair 1,740,000 122,879

369,672

Total Industrials & Business Services 2,293,094

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

24

INFORMATION TECHNOLOGY 8.3%

Communications Equipment 1.5%

Cisco Systems 8,500,000 325,550

325,550

Electronic Equipment, Instruments & Components 0.4%

TE Connectivity 1,010,000 95,990

95,990

Semiconductors & Semiconductor Equipment 3.5%

Analog Devices 670,000 59,650

Applied Materials 3,380,000 172,786

Qualcomm 6,375,000 408,127

Texas Instruments 1,365,000 142,561

783,124

Software 2.3%

CA 1,150,000 38,272

Microsoft 5,510,000 471,325

509,597

Technology Hardware, Storage & Peripherals 0.6%

Apple 230,000 38,923

Hewlett-Packard Enterprise 3,500,000 50,260

Western Digital 720,000 57,262

146,445

Total Information Technology 1,860,706

MATERIALS 5.4%

Chemicals 3.1%

Akzo Nobel (EUR) 470,000 41,240

CF Industries 5,730,000 243,754

DowDuPont 5,820,000 414,501

699,495

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

25

Construction Materials 0.7%

Vulcan Materials 1,265,000 162,388

162,388

Containers & Packaging 1.0%

International Paper 3,720,000 215,537

215,537

Metals & Mining 0.6%

Nucor 2,200,000 139,876

139,876

Total Materials 1,217,296

REAL ESTATE 2.1%

Equity Real Estate Investment Trusts 2.1%

Equity Residential, REIT 2,030,000 129,453

Rayonier, REIT 5,890,000 186,301

Weyerhaeuser, REIT 4,110,000 144,918

Total Real Estate 460,672

TELECOMMUNICATION SERVICES 3.0%

Diversified Telecommunication Services 2.8%

CenturyLink 3,725,000 62,133

Telefonica (EUR) 11,650,000 113,445

Verizon Communications 8,630,000 456,786

632,364

Wireless Telecommunication Services 0.2%

Vodafone (GBP) 9,650,000 30,503

30,503

Total Telecommunication Services 662,867

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

26

UTILITIES 4.5%

Electric Utilities 3.5%

Edison International 2,570,000 162,527

Exelon 2,120,000 83,549

PG&E 2,806,697 125,825

Southern Company 7,490,000 360,194

Westar Energy 1,080,000 57,024

789,119

Multi-Utilities 1.0%

NiSource 8,430,000 216,398

216,398

Total Utilities 1,005,517

Total Miscellaneous Common Stocks 0.1% (2) 17,407

Total Common Stocks (Cost $14,455,061) 21,433,663

CONVERTIBLE PREFERRED STOCKS 1.6%

HEALTH CARE 0.7%

Health Care Equipment & Supplies 0.7%

Becton, Dickinson & Company, Class A, 6.125%, 5/1/20 2,702,575 155,806

Total Health Care 155,806

UTILITIES 0.9%

Electric Utilities 0.7%

NextEra Energy, 6.123%, 8/2/19 2,836,650 161,577

161,577

Proof #6

T. Rowe Price Equity Income Fund

Shares/Par $ Value

(Cost and value in $000s)

27

Multi Utilities 0.2%

DTE Energy, 6.50%, 10/1/19 685,550 37,361

37,361

Total Utilities 198,938

Total Convertible Preferred Stocks (Cost $308,421) 354,744

CORPORATE BONDS 0.5%

Mattel, 6.75%, 12/31/25 (3) 66,910,000 67,747

Western Digital, 10.50%, 4/1/24 31,950,000 37,022

Total Corporate Bonds (Cost $98,755) 104,769

BOND MUTUAL FUNDS 0.3%

T. Rowe Price Institutional Floating Rate Fund, 3.80% (4)(5) 6,468,844 64,818

Total Bond Mutual Funds (Cost $63,108) 64,818

SHORT-TERM INVESTMENTS 1.7%

Money Market Funds 1.7%

T. Rowe Price Government Reserve Fund, 1.24% (4)(6) 384,704,346 384,704

Total Short-Term Investments (Cost $384,704) 384,704

Total Investments in Securities

99.9% of Net Assets (Cost $15,310,049) $ 22,342,698

‡ Shares/Par are denominated in U.S. dollars unless otherwise noted. (1) Non-income producing (2)

The identity of certain securities has been concealed to protect the fund while it completes a purchase or selling program for the securities.

(3)

Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be resold in transactions exempt from registration only to qualified institutional buyers -- total value of such securities at period-end amounts to $67,747 and represents 0.3% of net assets.

(4) Affiliated Company (5) SEC 30-day yield (6) Seven-day yield

Proof #6

T. Rowe Price Equity Income Fund

28

ADR American Depositary Receipts EUR Euro GBP British Pound REIT

A domestic Real Estate Investment Trust whose distributions pass-through with original tax character to the shareholder

Proof #6

T. Rowe Price Equity Income Fund

29

The accompanying notes are an integral part of these financial statements.

Affiliated Companies

($000s)

The fund may invest in certain securities that are considered affiliated companies. As defined by the 1940 Act, an affiliated company is one in which the fund owns 5% or more of the outstanding voting securities, or a company that is under common ownership or control. The following securities were considered affiliated companies for all or some portion of the year ended December 31, 2017. Net realized gain (loss), investment income, change in net unrealized gain/loss, and purchase and sales cost reflect all activity for the period then ended.

Affiliate

Net Realized Gain(Loss)

Change in NetUnrealizedGain/Loss

InvestmentIncome

T. Rowe Price Institutional Floating Rate Fund $ — $ (380) $ 2,757 T. Rowe Price Government Reserve Fund — — 3,781 Totals $ —# $ (380) $ 6,538+ Supplementary Investment Schedule Affiliate

Value12/31/16

PurchaseCost

SalesCost

Value12/31/17

T. Rowe Price Institutional Floating Rate Fund $ 62,465 $ 2,733 $ — $ 64,818 T. Rowe Price Government Reserve Fund 495,652 ¤ ¤ 384,704 $ 449,522^

# Capital gain/loss distributions from mutual funds represented $0 of the net realized gain (loss).

+ Investment income comprised $6,538 of dividend income and $0 of interest income. ¤ Purchase and sale information not shown for cash management funds. ^ The cost basis of investments in affiliated companies was $447,812.

Proof #6

30

T. Rowe Price Equity Income Fund December 31, 2017

($000s, except shares and per share amounts)

Statement of Assets and Liabilities

Assets

Investments in securities, at value (cost $15,310,049) $ 22,342,698

Dividends and interest receivable 41,567

Receivable for shares sold 30,884

Receivable for investment securities sold 26,842

Other assets 1,307

Total assets 22,443,298

Liabilities

Payable for shares redeemed 30,989

Payable to Price Associates (Note 6) 30,812

Investment management fees payable 9,983

Payable for investment securities purchased 9,263

Due to affiliates 1,212

Payable to directors 17

Other liabilities 2,660

Total liabilities 84,936

NET ASSETS $ 22,358,362 Net Assets Consist of:

Accumulated undistributed net realized gain $ 364,113

Net unrealized gain 7,002,000

Paid-in capital applicable to 670,662,272 shares of $0.0001 par value capital stock outstanding; 2,000,000,000 shares authorized 14,992,249

NET ASSETS $ 22,358,362

Proof #6

31

T. Rowe Price Equity Income Fund December 31, 2017

The accompanying notes are an integral part of these financial statements.

Statement of Assets and Liabilities

NET ASSET VALUE PER SHARE

Investor Class ($17,602,305,147 / 527,991,820 shares outstanding) $ 33.34

Advisor Class ($421,504,745 / 12,671,641 shares outstanding) $ 33.26

R Class ($99,971,883 / 3,011,125 shares outstanding) $ 33.20

I Class ($4,234,580,447 / 126,987,686 shares outstanding) $ 33.35

Proof #6

T. Rowe Price Equity Income Fund

($000s)

Statement of Operations

32

Year Ended

12/31/17Investment Income (Loss)

Income Dividend $ 577,846 Interest 1,848 Other 2

Total income 579,696

Expenses Investment management 117,552 Shareholder servicing

Investor Class 19,938 Advisor Class 722 R Class 195 I Class 22 20,877

Rule 12b-1 fees Advisor Class 1,175 R Class 568 1,743

Prospectus and shareholder reports Investor Class 293 Advisor Class 11 R Class 2 I Class 378 684

Custody and accounting 645 Registration 401 Legal and audit 151 Directors 72 Proxy and annual meeting 2,040 Miscellaneous 42 Waived / paid by Price Associates (349)

Total expenses 143,858

Net investment income 435,838

Proof #6

T. Rowe Price Equity Income Fund

($000s)

Statement of Operations

33

The accompanying notes are an integral part of these financial statements.

Realized and Unrealized Gain / Loss

Net realized gain (loss) Securities 2,570,981 Futures 4,244 Foreign currency transactions 100

Net realized gain 2,575,325

Change in net unrealized gain / loss

Securities 353,480 Payable to Price Associates (Note 6) (30,812) Other assets and liabilities denominated in foreign currencies 207

Change in net unrealized gain / loss 322,875

Net realized and unrealized gain / loss 2,898,200

INCREASE IN NET ASSETS FROM OPERATIONS $ 3,334,038

Proof #6

T. Rowe Price Equity Income Fund

($000s)

34

Statement of Changes in Net Assets

Year Ended

12/31/17 12/31/16Increase (Decrease) in Net Assets

Operations Net investment income $ 435,838 $ 523,931 Net realized gain 2,575,325 1,246,357 Change in net unrealized gain / loss 322,875 2,055,307 Increase in net assets from operations 3,334,038 3,825,595

Distributions to shareholders

Net investment income Investor Class (351,812) (435,481) Advisor Class (7,554) (11,473) R Class (1,492) (2,584) I Class (80,705) (68,754)

Net realized gain Investor Class (1,245,150) (957,764) Advisor Class (30,047) (28,210) R Class (7,064) (7,246) I Class (297,129) (181,061)

Decrease in net assets from distributions (2,020,953) (1,692,573)

Capital share transactions*

Shares sold Investor Class 1,093,046 1,487,940 Advisor Class 57,532 96,766 R Class 15,805 23,621 I Class 1,018,067 3,744,307

Distributions reinvested Investor Class 1,519,616 1,328,942 Advisor Class 37,149 39,229 R Class 8,556 9,830 I Class 368,740 246,156

Shares redeemed Investor Class (4,589,821) (8,155,729) Advisor Class (225,816) (352,668) R Class (66,336) (115,926) I Class (883,784) (623,653)

Decrease in net assets from capital share transactions (1,647,246) (2,271,185)

Proof #6

T. Rowe Price Equity Income Fund

($000s)

35

The accompanying notes are an integral part of these financial statements.

Statement of Changes in Net Assets

Year Ended

12/31/17 12/31/16 Net Assets

Decrease during period (334,161) (138,163) Beginning of period 22,692,523 22,830,686

End of period $ 22,358,362 $ 22,692,523

Undistributed net investment income – 5,639

*Share information

Shares sold Investor Class 33,062 50,120 Advisor Class 1,746 3,242 R Class 483 797 I Class 30,766 124,094

Distributions reinvested Investor Class 45,610 42,209 Advisor Class 1,117 1,247 R Class 258 312 I Class 11,060 7,773

Shares redeemed Investor Class (138,945) (274,717) Advisor Class (6,773) (12,046) R Class (2,019) (3,998) I Class (26,701) (20,229)

Decrease in shares outstanding (50,336) (81,196)

Proof #6

36

T. Rowe Price Equity Income Fund December 31, 2017

Notes to Financial Statements

T. Rowe Price Equity Income Fund (the fund) is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund, organized as a Maryland corporation, is the successor to the T. Rowe Price Equity Income Fund pursuant to an agreement and plan of reorganization for a change in domicile, effective October 30, 2017. The reorganization and redomiciliation had no effect on the fund’s investment objective and strategies or on the fund’s net assets. The fund seeks a high level of dividend income and long-term capital growth primarily through investments in stocks. The fund has four classes of shares: the Equity Income Fund (Investor Class), the Equity Income Fund–Advisor Class (Advisor Class), the Equity Income Fund–R Class (R Class), and the Equity Income Fund–I Class (I Class). Advisor Class shares are sold only through unaffiliated brokers and other unaffiliated financial intermediaries, and R Class shares are available to retirement plans serviced by intermediaries. I Class shares generally are available only to investors meeting a $1,000,000 minimum investment or certain other criteria. The Advisor Class and R Class each operate under separate Board-approved Rule 12b-1 plans, pursuant to which each class compensates financial intermediaries for distribution, shareholder servicing, and/or certain administrative services; the Investor and I Classes do not pay Rule 12b-1 fees. Each class has exclusive voting rights on matters related solely to that class; separate voting rights on matters that relate to all classes; and, in all other respects, the same rights and obligations as the other classes.

NOTE 1 - SIGNIfICaNT aCCOuNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Proof #6

37

T. Rowe Price Equity Income Fund

Investment Transactions, Investment Income, and Distributions Investment transactions are accounted for on the trade date basis. Income and expenses are recorded on the accrual basis. Realized gains and losses are reported on the identified cost basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Income tax-related interest and penalties, if incurred, are recorded as income tax expense. Distributions from REITs are initially recorded as dividend income and, to the extent such represent a return of capital or capital gain for tax purposes, are reclassified when such information becomes available. Income distributions are declared and paid by each class quarterly. Distributions to shareholders are recorded on the ex-dividend date. A capital gain distribution may also be declared and paid by the fund annually.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the respective date of such transaction. The portion of the results of operations attributable to changes in foreign exchange rates on investments is not bifurcated from the portion attributable to changes in market prices. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class accounting Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to all classes, investment income, and realized and unrealized gains and losses are allocated to the classes based upon the relative daily net assets of each class. To the extent any expenses are waived or reimbursed in accordance with an expense limitation (see Note 6), the waiver or reimbursement is charged to the applicable class or allocated across the classes in the same manner as the related expense. The Advisor Class and R Class each pay Rule 12b-1 fees, in an amount not exceeding 0.25% and 0.50%, respectively, of the class’s average daily net assets.

Proof #6

38

T. Rowe Price Equity Income Fund

Rebates Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $144,000 for the year ended December 31, 2017.

In-kind Redemptions In accordance with guidelines described in the fund’s prospectus, and when considered to be in the best interest of all shareholders, the fund may distribute portfolio securities rather than cash as payment for a redemption of fund shares (in-kind redemption). Gains and losses realized on in-kind redemptions are not recognized for tax purposes and are reclassified from undistributed realized gain (loss) to paid-in capital. During the year ended December 31, 2017, the fund realized $542,179,000 of net gain on $1,206,417,000 of in-kind redemptions.

New accounting Guidance In March 2017, the FASB issued amended guidance to shorten the amortization period for certain callable debt securities, held at a premium. The guidance is effective for fiscal years and interim periods beginning after December 15, 2018. Adoption will have no effect on the fund’s net assets or results of operations.

On August 1, 2017, the fund implemented amendments to Regulation S-X, issued by the Securities and Exchange Commission, which require standardized, enhanced disclosures, particularly related to derivatives, in investment company financial statements. Adoption had no effect on the fund’s net assets or results of operations.

Indemnification In the normal course of business, the fund may provide indemnification in connection with its officers and directors, service providers, and/or private company investments. The fund’s maximum exposure under these arrangements is unknown; however, the risk of material loss is currently considered to be remote.

NOTE 2 - vaLuaTION

The fund’s financial instruments are valued and each class’s net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business. However, the NAV per share may be calculated at a time other than the normal close of the NYSE if trading on the NYSE is restricted, if the NYSE closes earlier, or as may be permitted by the SEC.

Proof #6

39

T. Rowe Price Equity Income Fund

fair value The fund’s financial instruments are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) is an internal committee that has been delegated certain responsibilities by the fund’s Board of Directors (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations. Specifically, the Valuation Committee establishes procedures to value securities; determines pricing techniques, sources, and persons eligible to effect fair value pricing actions; oversees the selection, services, and performance of pricing vendors; oversees valuation-related business continuity practices; and provides guidance on internal controls and valuation-related matters. The Valuation Committee reports to the Board and has representation from legal, portfolio management and trading, operations, risk management, and the fund’s treasurer.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based

Proof #6

40

T. Rowe Price Equity Income Fund

on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

valuation Techniques Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made. OTC Bulletin Board securities are valued at the mean of the closing bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the closing bid and asked prices for domestic securities and the last quoted sale or closing price for international securities.

For valuation purposes, the last quoted prices of non-U.S. equity securities may be adjusted to reflect the fair value of such securities at the close of the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will affect the value of some or all of its portfolio securities, the fund will adjust the previous quoted prices to reflect what it believes to be the fair value of the securities as of the close of the NYSE. In deciding whether it is necessary to adjust quoted prices to reflect fair value, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. The fund uses outside pricing services to provide it with quoted prices and information to evaluate or adjust those prices. The fund cannot predict how often it will use quoted prices and how often it will determine it necessary to adjust those prices to reflect fair value. As a means of evaluating its security valuation process, the fund routinely compares quoted prices, the next day’s opening prices in the same markets, and adjusted prices.

Actively traded equity securities listed on a domestic exchange generally are categorized in Level 1 of the fair value hierarchy. Non-U.S. equity securities generally are categorized in Level 2 of the fair value hierarchy despite the availability of quoted prices because, as described above, the fund evaluates and determines whether those quoted prices reflect fair value at the close of the NYSE or require adjustment. OTC Bulletin Board securities, certain preferred securities, and equity securities traded in inactive markets generally are categorized in Level 2 of the fair value hierarchy.

Proof #6

41

T. Rowe Price Equity Income Fund

Debt securities generally are traded in the OTC market. Securities with remaining maturities of one year or more at the time of acquisition are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service, which considers the yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities. Generally, debt securities are categorized in Level 2 of the fair value hierarchy.

Investments in mutual funds are valued at the mutual fund’s closing NAV per share on the day of valuation and are categorized in Level 1 of the fair value hierarchy. Assets and liabilities other than financial instruments, including short-term receivables and payables, are carried at cost, or estimated realizable value, if less, which approximates fair value.

Thinly traded financial instruments and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. The objective of any fair value pricing determination is to arrive at a price that could reasonably be expected from a current sale. Financial instruments fair valued by the Valuation Committee are primarily private placements, restricted securities, warrants, rights, and other securities that are not publicly traded.

Subject to oversight by the Board, the Valuation Committee regularly makes good faith judgments to establish and adjust the fair valuations of certain securities as events occur and circumstances warrant. For instance, in determining the fair value of an equity investment with limited market activity, such as a private placement or a thinly traded public company stock, the Valuation Committee considers a variety of factors, which may include, but are not limited to, the issuer’s business prospects, its financial standing and performance, recent investment transactions in the issuer, new rounds of financing, negotiated transactions of significant size between other investors in the company, relevant market valuations of peer companies, strategic events affecting the company, market liquidity for the issuer, and general economic conditions and events. In consultation with the investment and pricing teams, the Valuation Committee will determine an appropriate valuation technique based on available information, which may include both observable and unobservable inputs. The Valuation Committee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants, transaction information can be reliably obtained, and prices are deemed representative of fair value. However, the Valuation Committee may also consider other valuation methods

Proof #6

42

T. Rowe Price Equity Income Fund

such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; or some combination. Fair value determinations are reviewed on a regular basis and updated as information becomes available, including actual purchase and sale transactions of the issue. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions, and fair value prices determined by the Valuation Committee could differ from those of other market participants. Depending on the relative significance of unobservable inputs, including the valuation technique(s) used, fair valued securities may be categorized in Level 2 or 3 of the fair value hierarchy.

valuation Inputs The following table summarizes the fund’s financial instruments, based on the inputs used to determine their fair values on December 31, 2017:

($000s) Level 1 Level 2 Level 3 Total value

Quoted Prices

Significant Observable

Inputs

Significant unobservable

Inputs

InvestmentsinSecurities,except: $ 449,522 $ — $ — $ 449,522

CommonStocks 20,633,837 799,826 — 21,433,663

ConvertiblePreferredStocks — 354,744 — 354,744

CorporateBonds — 104,769 — 104,769

Total $ 21,083,359 $ 1,259,339 $ — $ 22,342,698

There were no material transfers between Levels 1 and 2 during the year ended December 31, 2017.

NOTE 3 - DERIvaTIvE INSTRuMENTS

During the year ended December 31, 2017, the fund invested in derivative instruments. As defined by GAAP, a derivative is a financial instrument whose value is derived from an underlying security price, foreign exchange rate, interest rate, index of prices or rates, or other variable; it requires little or no initial investment and permits or requires net settlement. The fund

Proof #6

43

T. Rowe Price Equity Income Fund

invests in derivatives only if the expected risks and rewards are consistent with its investment objectives, policies, and overall risk profile, as described in its prospectus and Statement of Additional Information. The fund may use derivatives for a variety of purposes, such as seeking to hedge against declines in principal value, increase yield, invest in an asset with greater efficiency and at a lower cost than is possible through direct investment, or to adjust credit exposure. The risks associated with the use of derivatives are different from, and potentially much greater than, the risks associated with investing directly in the instruments on which the derivatives are based. The fund at all times maintains sufficient cash reserves, liquid assets, or other SEC-permitted asset types to cover its settlement obligations under open derivative contracts.

The fund values its derivatives at fair value and recognizes changes in fair value currently in its results of operations. Accordingly, the fund does not follow hedge accounting, even for derivatives employed as economic hedges. Generally, the fund accounts for its derivatives on a gross basis. It does not offset the fair value of derivative liabilities against the fair value of derivative assets on its financial statements, nor does it offset the fair value of derivative instruments against the right to reclaim or obligation to return collateral. As of December 31, 2017, the fund held no derivative instruments.

Additionally, during the year ended December 31, 2017, the fund recognized $4,244,000 of gain on equity derivatives, included in realized gain(loss) on Futures on the accompanying Statement of Operations.

futures Contracts The fund is subject to equity price risk in the normal course of pursuing its investment objectives and uses futures contracts to help manage such risk. The fund may enter into futures contracts to manage exposure to interest rates, security prices, foreign currencies, and credit quality; as an efficient means of adjusting exposure to all or part of a target market; to enhance income; as a cash management tool; or to adjust credit exposure. A futures contract provides for the future sale by one party and purchase by another of a specified amount of a specific underlying financial instrument at an agreed-upon price, date, time, and place. The fund currently invests only in exchange-traded futures, which generally are standardized as to maturity date, underlying financial instrument, and other contract terms. Payments are made or received by the fund each day to settle daily fluctuations in the value of the contract (variation margin), which reflect changes in the value of the underlying financial instrument. Variation margin is recorded as unrealized gain or loss until the contract is closed. The value of a futures contract included

Proof #6

44

T. Rowe Price Equity Income Fund

in net assets is the amount of unsettled variation margin; net variation margin receivable is reflected as an asset and net variation margin payable is reflected as a liability on the accompanying Statement of Assets and Liabilities. Risks related to the use of futures contracts include possible illiquidity of the futures markets, contract prices that can be highly volatile and imperfectly correlated to movements in hedged security values, and potential losses in excess of the fund’s initial investment. During the year ended December 31, 2017, the volume of the fund’s activity in futures, based on underlying notional amounts, was generally less than 1% of net assets.

NOTE 4 - OTHER INvESTMENT TRaNSaCTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

Other Purchases and sales of portfolio securities other than short-term securities aggregated $4,415,244,000 and $7,587,495,000, respectively, for the year ended December 31, 2017.

NOTE 5 - fEDERaL INCOME TaXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

Proof #6

45

T. Rowe Price Equity Income Fund

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Reclassifications to paid-in capital relate primarily to redemptions in kind and a tax practice that treats a portion of the proceeds from each redemption of capital shares as a distribution of taxable net investment income or realized capital gain. Reclassifications between income and gain relate primarily to per-share rounding of distributions. For the year ended December 31, 2017, the following reclassifications were recorded to reflect tax character (there was no impact on results of operations or net assets):

Undistributednetinvestmentincome $ 86

Undistributednetrealizedgain (794,991)

Paid-incapital 794,905

($000s)

Distributions during the years ended December 31, 2017 and December 31, 2016, were characterized for tax purposes as follows:

($000s)

December 312017 2016

Ordinaryincome $ 497,969 $ 559,495

Long-termcapitalgain 1,522,984 1,133,078

Totaldistributions $ 2,020,953 $ 1,692,573

Proof #6

46

T. Rowe Price Equity Income Fund

At December 31, 2017, the tax-basis cost of investments, including derivatives, and components of net assets were as follows:

Costofinvestments $ 15,326,200

Unrealizedappreciation $ 7,413,759

Unrealizeddepreciation (427,910)

Netunrealizedappreciation(depreciation) 6,985,849

Undistributedordinaryincome 23,638

Undistributedlong-termcapitalgain 356,678

Late-yearordinarylossdeferrals (52)

Paid-incapital 14,992,249

Netassets $ 22,358,362

($000s)

The difference between book-basis and tax-basis net unrealized appreciation (depreciation) is attributable to the deferral of losses from wash sales for tax purposes. In accordance with federal tax laws applicable to investment companies, net specified losses realized between November 1 and December 31 are not recognized for tax purposes until the subsequent year (late-year ordinary loss deferrals); however, such losses are recognized for financial reporting purposes in the year realized.

NOTE 6 - RELaTED PaRTY TRaNSaCTIONS