December 2019 Legislative Council Staff Economic & Revenue ...

49

Economic & Revenue Forecast Presentation to the Joint Budget Committee December 20, 2019 December 2019 Legislative Council Staff

Transcript of December 2019 Legislative Council Staff Economic & Revenue ...

Economic & Revenue Forecast

Presentation to the Joint Budget CommitteeDecember 20, 2019

December 2019 Legislative Council Staff

2

Economic Outlook

3

2.1%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Gov't Consumption & Investment

Net Exports

Gross Private Investment

Personal Consumption Expenditures

Consumers continue to drive growth in economic activity

Contributions to Real Gross Domestic Product (GDP)

Annualized Change over the Prior Quarter

Source: U.S. Bureau of Economic Analysis. Seasonally adjusted annual rates.

Real GDP

4

Employment growth continues, but will slow further as

the labor market tightens

-6%

-4%

-2%

0%

2%

4%

6%

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Source: U.S. Bureau of Labor Statistics. Seasonally adjusted. Colorado nonfarm employment estimates include estimates of

revisions expected by Legislative Council Staff as a part of the annual rebenchmark process.

Colorado

U.S.

Year-over-Year Change in Nonfarm Employment

2.0%1.5%

5

$24

$25

$26

$27

$28

$29

$30

$31

2007 2009 2011 2013 2015 2017 2019

Wages will continue to rise as labor shortages in many

industries persist, constraining business growth and profits

Source: U.S. Bureau of Labor Statistics. Seasonally adjusted. Adjusted for inflation using the CPI-U for all urban areas.

Real Average Hourly Earnings

2019 Dollars

U.S.

Colorado

$28.29

$30.63

6

30

40

50

60

70

2007 2009 2011 2013 2015 2017 2019

Contracting

Expanding

Manufacturing activity remains in contractionary

territory and business activity has slowed

Source: Institute for Supply Management.

Institute for Supply Management Indices

Diffusion Index

Manufacturing

Business Activity

7

80

85

90

95

100

105

110

115

120

125

$0

$50

$100

$150

$200

U.S. ExportsMillions of Dollars

Goods

Services

A strong dollar makes imports cheaper, but exports

more expensive

Source: Federal Reserve Board of Governors & Bureau of Economic Analysis (balance of payments basis). Seasonally adjusted.

Trade Weighted U.S. DollarIndex of the Dollar to Foreign Currencies

Appreciating

Depreciating

Broad Index

8

2.0%

2.3%

-0.6%

2.0%

2.9%

-1.6%

-0.1%

4.2%

1.9%

2.2%

2.4%

Headline

Core

Energy

Food

Housing

Apparel

Transportation

Medical Care

Recreation

Education

Other

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

2009 2011 2013 2015 2017 2019

Inflationary pressures remain fairly subdued

Source: U.S. Census Bureau. Seasonally adjusted.

CPI-U Inflation, U.S. City AverageYear-over-Year Change in Prices November 2019 over November 2018

HeadlineCore

9

Crude oil prices remain subdued by strong supply,

weaker demand

Source: Energy Information Administration.

Average weekly prices through December 13, 2019.

West Texas Intermediate

Crude Oil PriceDollars per Barrel

$0

$40

$80

$120

$160

Crude Oil ProductionMillions of Barrels per Month

Source: Energy Information Administration. Three-month

moving averages. Data are through August 2019.

2

4

6

8

10

12

14

16

18

140

180

220

260

300

340

380

420Colorado

Right Axis

United States

Left Axis

10

Economic Outlook

U.S. and Colorado economic growth will continue, but at

slower rates

• Labor markets will tighten further, constricting business growth

and profits with higher wages

• Inflationary pressures will remain subdued on slower global

economic demand for goods and slowing housing costs

• Energy, manufacturing, and export industry activity expected to

remain soft into 2020

Recessionary risk for 2020 has eased, but risk remains elevated

for the forecast period.

11

General Fund Budget Outlook

12

$4

$6

$8

$10

$12

$14

Ongoing shifts in taxpayer behavior and slowing economic

growth are expected to drive General Fund revenue growth

Source: Colorado Office of the State Controller and Legislative Council Staff December 2019 forecast.

Gross General Fund RevenueBillions of Dollars

Change Relative to September Expectations

FY 2019-20: –$10.9M

FY 2020-21: +$166.1M

3.0%4.1%

4.1%

14.1%

Year-over-Year

Growth

7.2%

13

$7

$8

$9

$10

$11

$12

$13

$14

$15

$16

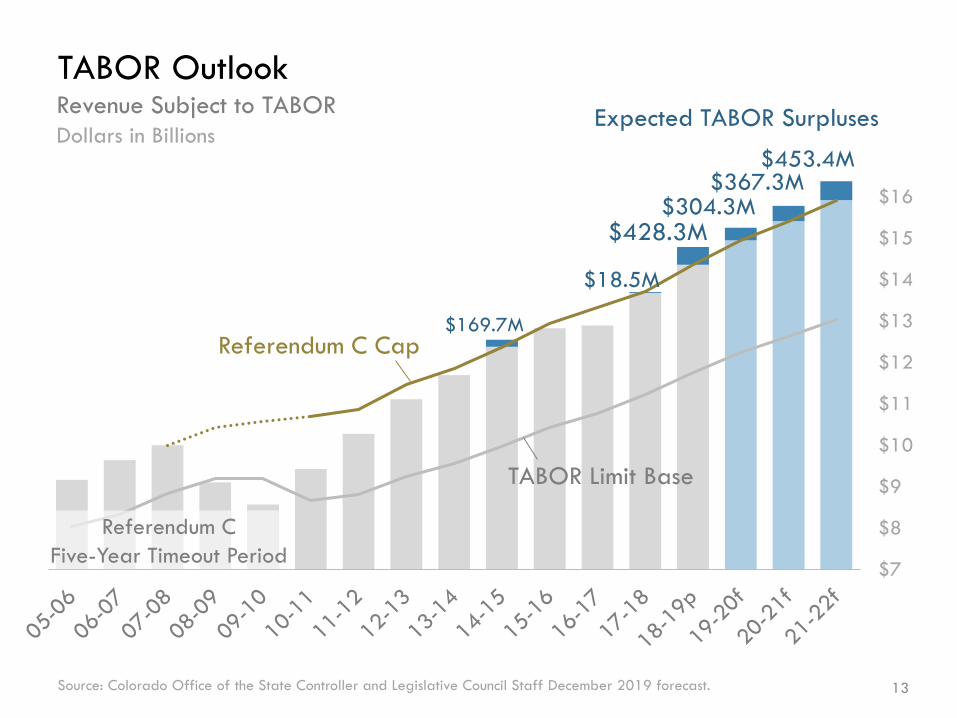

TABOR Outlook

Source: Colorado Office of the State Controller and Legislative Council Staff December 2019 forecast.

Revenue Subject to TABOR

Dollars in Billions

Referendum C

Five-Year Timeout Period

Referendum C Cap

TABOR Limit Base

Expected TABOR Surpluses

$169.7M

$428.3M

$18.5M

$304.3M$367.3M

$453.4M

14

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2018-19 2019-20 2020-21 2021-22

Expected TABOR Refunds & General Fund Budget Impacts

TABOR surplus revenue is set aside in the year in which a

surplus occurs to pay refunds in the following budget year

TABOR Surplus & Set Aside:

Refunded in Fiscal Year: 2019-20 2020-21 2021-22 2022-23

Source: Colorado Office of the State Controller and Legislative Council Staff December 2019 forecast.

*This amount includes $0.1 million in underrefunds from the FY 2014-15 surplus.

Dollars in Millions

$428.5M*

Income Tax Rate Reduction

Reimbursements to Local Govts for Property Tax Exemptions

$304.3M

$367.3M

$453.4M

Sales Tax Refund Mechanism

15

$0

$200

$400

$600

$800

$1,000

$1,200

$0

$200

$400

$600

$800

$1,000

$1,200

Changes relative to

September:

+$120.5 million

Last Year FY 2018-19 General Fund ReserveDollars in Millions

Source: Legislative Council Staff forecasts based on current law.

7.25%

Reserve

Requirement

$814.2M

Surplus Above

Required Reserve

11.3% Reserve

$452.4M

December 2019

Forecast

September 2019

Forecast

The change is attributable

to a new assumption for

the FY 2018-19 year-end

balance based on the

Basic Financial Statements.

This amount will be

updated with the release

of the CAFR.

$814.2M

10.2% Reserve

$331.8M

16

$0

$200

$400

$600

$800

$1,000

$1,200

$0

$200

$400

$600

$800

$1,000

$1,200

Changes relative to

September:

+$62.3 million

Source: Legislative Council Staff forecasts based on current law.

8.3% Reserve

$871.1M 7.25%

Reserve

Requirement

$871.3M

Surplus Above

Required Reserve $121.6M

8.8% Reserve

$184.0M

Current Year FY 2019-20 General Fund ReserveDollars in Millions

Higher beginning balance

(carried over from FY 2018-19)

Higher TABOR refund obligation:

Increased cash funds revenue

expectations (+51.5M)

Small adjustments to

appropriations, transfer amounts

December 2019

Forecast

September 2019

Forecast

17

-$100

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1-$100

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1

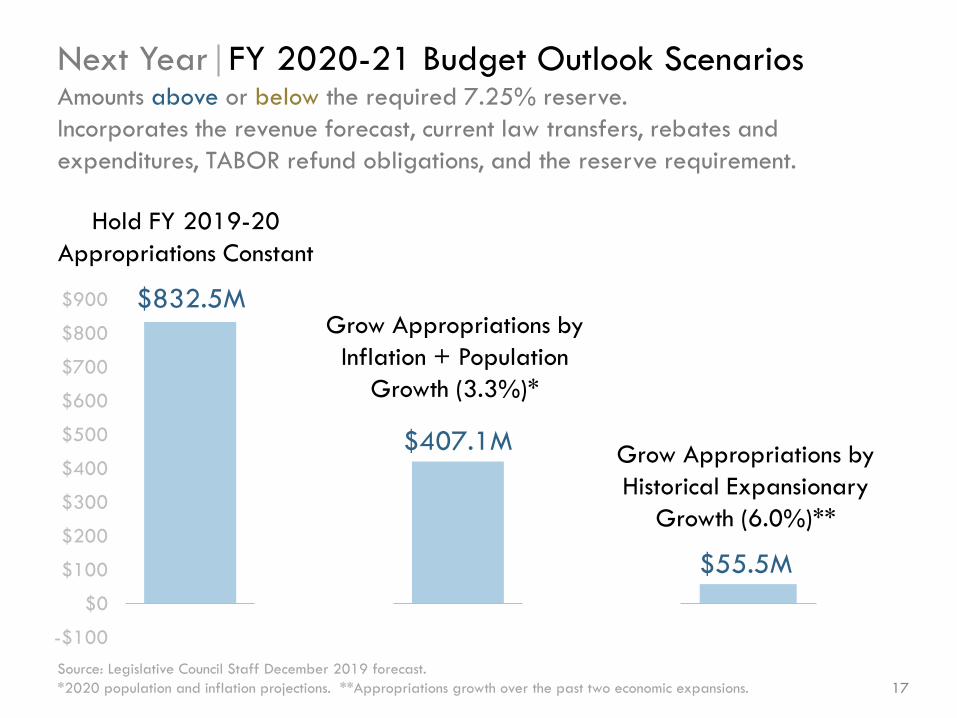

Next Year FY 2020-21 Budget Outlook ScenariosAmounts above or below the required 7.25% reserve.

Incorporates the revenue forecast, current law transfers, rebates and

expenditures, TABOR refund obligations, and the reserve requirement.

$832.5M

Source: Legislative Council Staff December 2019 forecast.

*2020 population and inflation projections. **Appropriations growth over the past two economic expansions.

Hold FY 2019-20

Appropriations Constant

Grow Appropriations by

Inflation + Population

Growth (3.3%)*

Grow Appropriations by

Historical Expansionary

Growth (6.0%)**

$407.1M

$55.5M

18

Risks to the Forecast

Upside Risks for FY 2019-20

• Ongoing shifts in taxpayer behavior with federal tax law changes

• Taxation of out-of-state (including online) sales tax collections

Available General Fund Collections Data as a Share of Total Fiscal Year Collections*

*Six-year average of actual collections data, FY 2013-14 to FY 2018-19p.

7%

14%23%

31%

38%46%

57%

62%69%

83%

90%

99%

100%

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Period 13

September Forecast

December Forecast

March Forecast

How Much Do We Know About FY 2019-20?

June Forecast

19

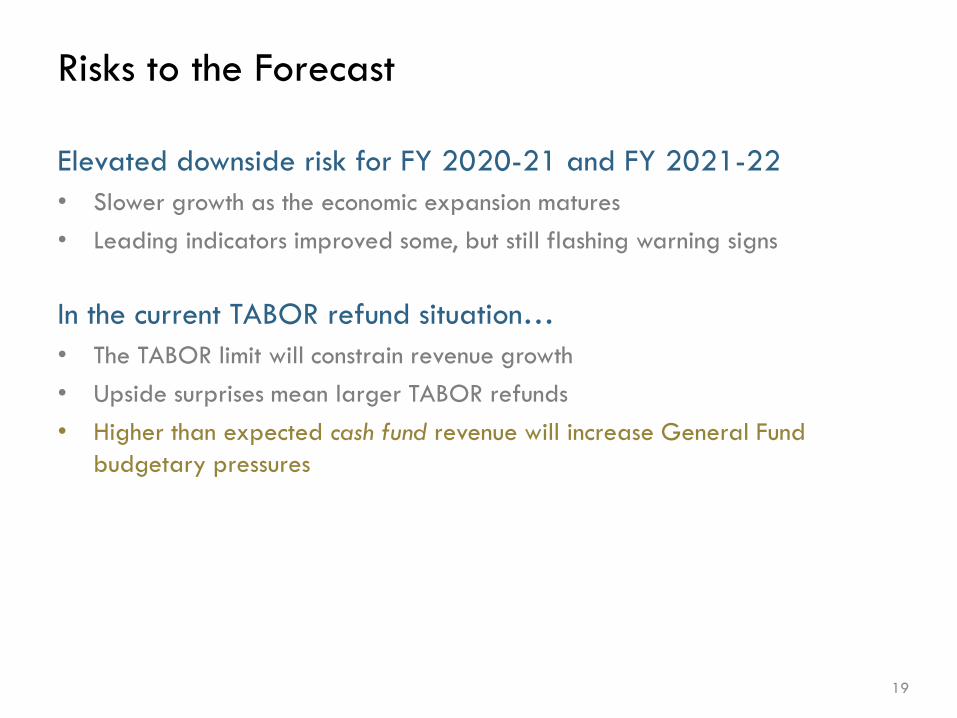

Risks to the Forecast

Elevated downside risk for FY 2020-21 and FY 2021-22

• Slower growth as the economic expansion matures

• Leading indicators improved some, but still flashing warning signs

In the current TABOR refund situation…

• The TABOR limit will constrain revenue growth

• Upside surprises mean larger TABOR refunds

• Higher than expected cash fund revenue will increase General Fund

budgetary pressures

20

TABOR Refunds are refunded from General Funds

Cash Funds

General Funds

In a TABOR surplus situation…

General

Funds

TABOR Refunds

General Fund dollars in = General Fund dollars out

Amount

available for

the General

Fund Budget

TABOR Limit

21

General Funds

Cash Funds

TABOR Refunds

TABOR Refunds are refunded from General Funds

Cash Fund dollars in = General Fund dollars out

General

Funds

In a TABOR surplus situation…

Amount

available for

the General

Fund Budget

TABOR Limit

22

$235.7

$142.4 $112.8 $117.4

$361.7

$429.7$417.6 $440.5

$0

$100

$200

$300

$400

$500

$600

Dollars in Millions

Severance Taxes Are Noisy

Gross

Severance Taxes

Net Severance

Tax Revenue

Ad Valorem

Credit

$597.4$572.1 $557.9

$530.4

Source: Legislative Council Staff calculations base on the December 2019 forecast.

23

$264.7

$5.2 $4.0 $126.2

$235.7

$142.4 $112.8 $117.4

$0

$100

$200

$300

$400

$500

$600

Dollars in Millions

Severance Taxes Are Noisy

Source: Office of the State Controller and Legislative Council Staff December 2019 forecast (f).

Net Severance Tax Revenue

24

K-12 Enrollment Forecast

25

K-12 Public School Enrollment Full-Time Equivalent (FTE) Students

Source: Colorado Department of Education and Legislative Council Staff December 2019 forecast.*Percent change from 2018-19, when kindergarten students were counted as 0.5 FTE.

Region Actual

2019-20 Percent

Change*

Metro Denver 494,190 3.2% Northern 91,722 4.8% Colorado Springs 124,019 4.7%

Pueblo 33,370 4.0% Eastern Plains 26,898 4.4% San Luis Valley 7,414 2.8%

Mountain 25,489 2.6% Southwest Mountain

13,589 4.1%

Western 51,909 3.3%

Statewide Total 868,597 3.6%

26

810,000

820,000

830,000

840,000

850,000

860,000

870,000

880,000

Total K-12 Enrollment

Before Full-Day

Kindergarten

After Full-Day

Kindergarten

Total Enrollment if

Kindergarten = 1.0 FTE

Actual Total

Enrollment

Source: Colorado Department of Education and Legislative Council Staff December 2019 forecast (f).*Prior to 2019-20, kindergarten students were counted as 0.5 FTE.

Student FTE

27

Region Actual

2019-20 Percent

Change* Estimated

2020-21 Percent Change

Estimated 2021-22

Percent Change

Average Growth**

Metro Denver 494,190 3.2% 491,985 -0.4% 490,832 -0.2% -0.3% Northern 91,722 4.8% 93,069 1.5% 93,690 0.7% 1.1% Colorado Springs 124,019 4.7% 125,051 0.8% 125,791 0.6% 0.7%

Pueblo 33,370 4.0% 33,139 -0.7% 32,809 -1.0% -0.8% Eastern Plains 26,898 4.4% 27,188 1.1% 27,456 1.0% 1.0% San Luis Valley 7,414 2.8% 7,489 1.0% 7,545 0.7% 0.9%

Mountain 25,489 2.6% 25,368 -0.5% 25,272 -0.4% -0.4% Southwest Mountain

13,589 4.1% 13,615 0.2% 13,680 0.5% 0.3%

Western 51,909 3.3% 52,002 0.2% 52,064 0.1% 0.1%

Statewide Total 868,597 3.6% 868,907 0.0% 869,138 0.0% 0.0%

K-12 Public School Enrollment Full-Time Equivalent (FTE) Students

Source: Colorado Department of Education and Legislative Council Staff December 2019 forecast.*Percent change from 2018-19, when kindergarten students were counted as 0.5 FTE.**Compound average annual growth rate between 2019-20 and 2021-22.

28

Assessed Valuation Forecast

29

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0f

202

1f

202

2f

Nonresidential

Residential

Assessed Values in Colorado

Year

Total

Assessed

Value

Percent

Change

2014 $91.6 3.3%

2015 $105.3 15.0%

2016 $101.4 -3.7%

2017 $111.6 10.1%

2018 $115.9 3.8%

2019 $135.6 17.0%

2020f $140.1 3.4%

2021f $152.2 8.6%

2022f $155.1 1.9%

Dollars in Billions

Source: Colorado Division of Property Taxation and Legislative Council Staff December 2019 forecast (f).

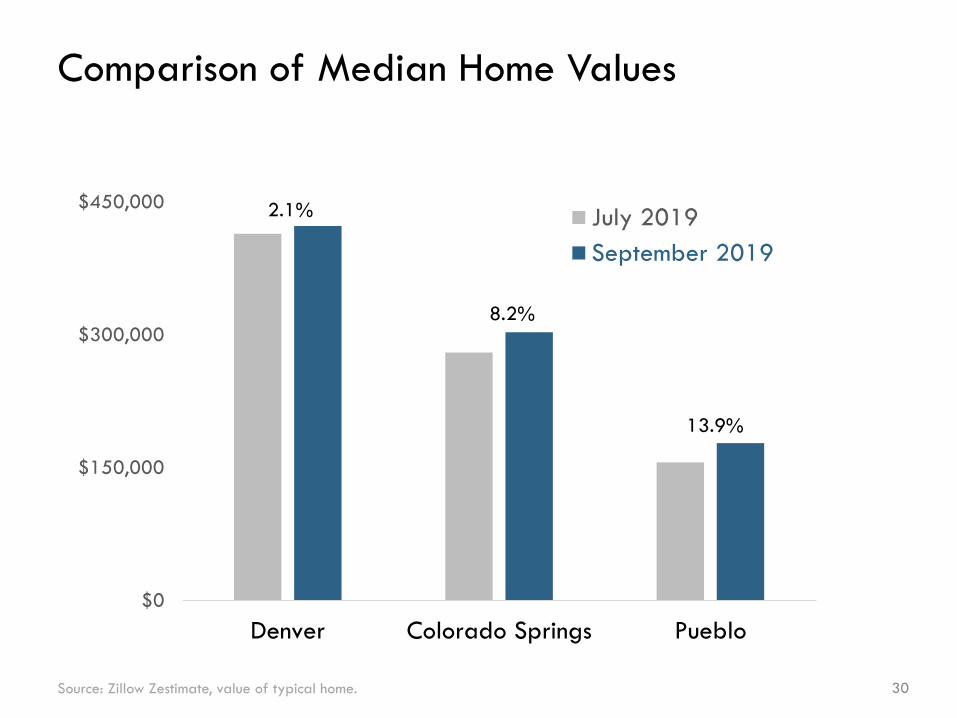

30

$0

$150,000

$300,000

$450,000

Denver Colorado Springs Pueblo

July 2019

September 2019

8.2%

13.9%

2.1%

Comparison of Median Home Values

Source: Zillow Zestimate, value of typical home.

31

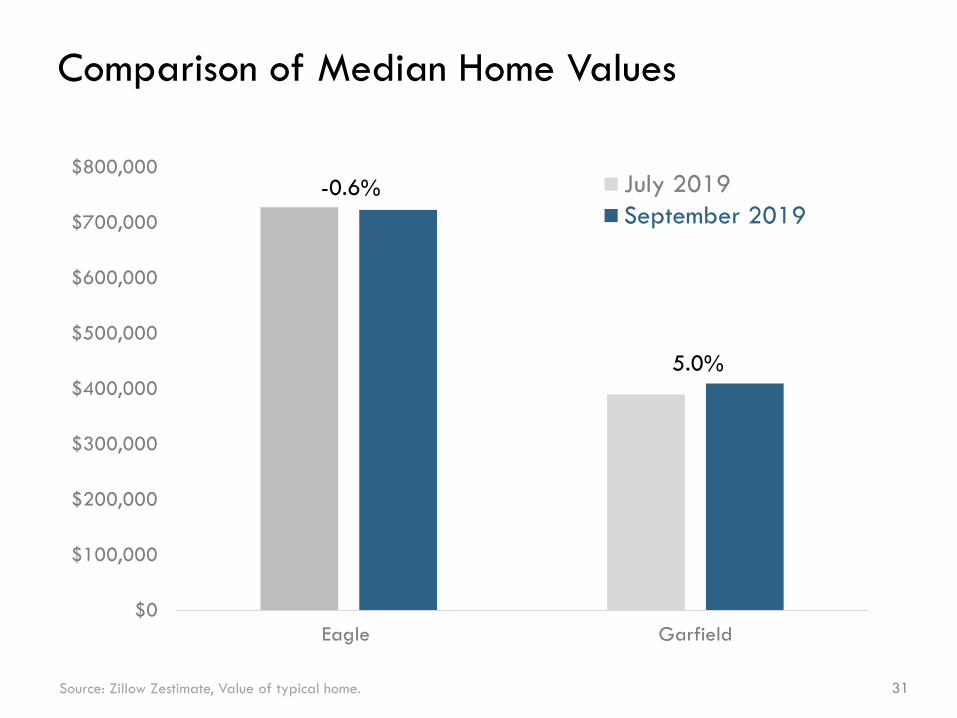

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

Eagle Garfield

July 2019

September 2019-0.6%

5.0%

Comparison of Median Home Values

Source: Zillow Zestimate, Value of typical home.

32

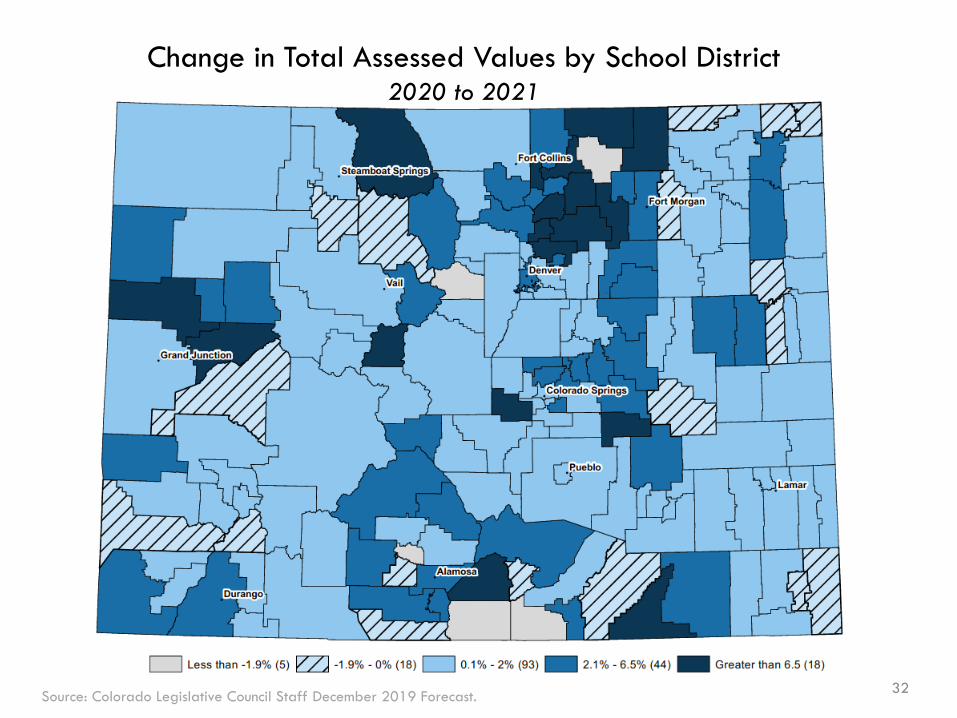

Change in Total Assessed Values by School District2020 to 2021

Source: Colorado Legislative Council Staff December 2019 Forecast.

33

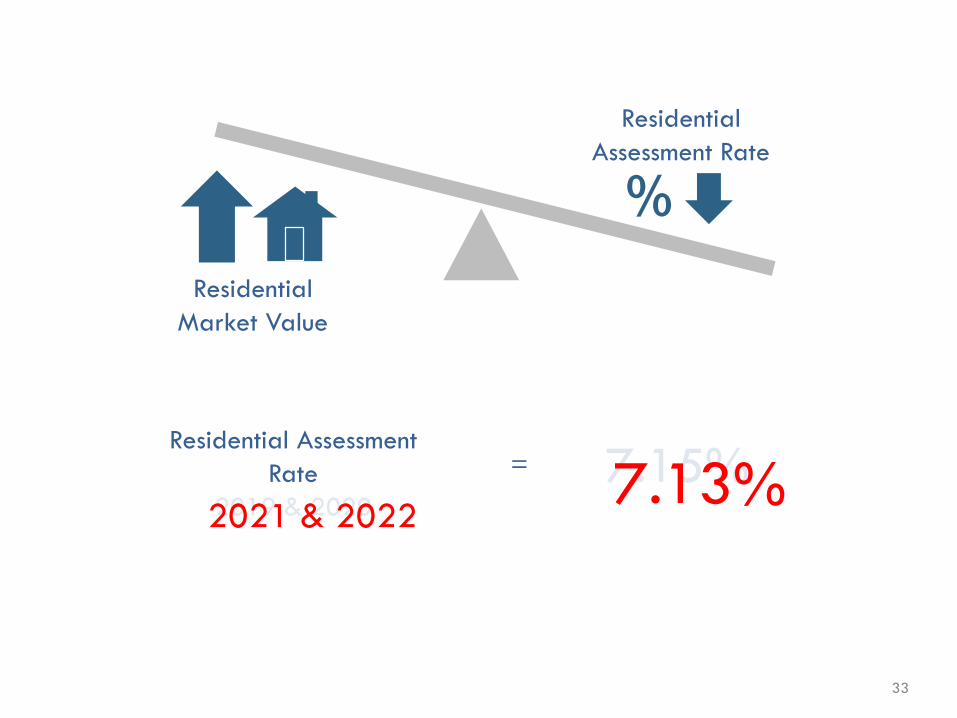

Residential

Market Value

Residential

Assessment Rate

%

Residential Assessment

Rate

2019 & 2020

7.15%=

2021 & 20227.13%

34

$0

$20

$40

$60

$80

$100

$120

Jan2014

Jan2015

Jan2016

Jan2017

Jan2018

Jan2019

Jan2020

Historic Price Upper bound 95%

Confidence Interval

$90.52

Lower bound 95%

Confidence Interval

$31.68

Forecast WTI

$59.50

But the forecast is not without risks

Source: U.S. Energy Information Administration, December 2019 Short Term Energy Outlook.

West Texas Intermediate (WTI) Crude Oil Price

35

What does the price of oil mean for the RAR?

Baseline* Scenario 1 Scenario 2

Implied Price of

Oil, Dec 2020$59.50 $50.50 $68.50

RAR 7.13% 7.00% 7.15%

Change in 2021

AV from baseline$0 -$2.7 billion $1.6 billion

-1.7% 1.0%

*Legislative Council Staff December 2019 forecast.

RAR = Residential assessment rate.

36

School Finance Outlook

37

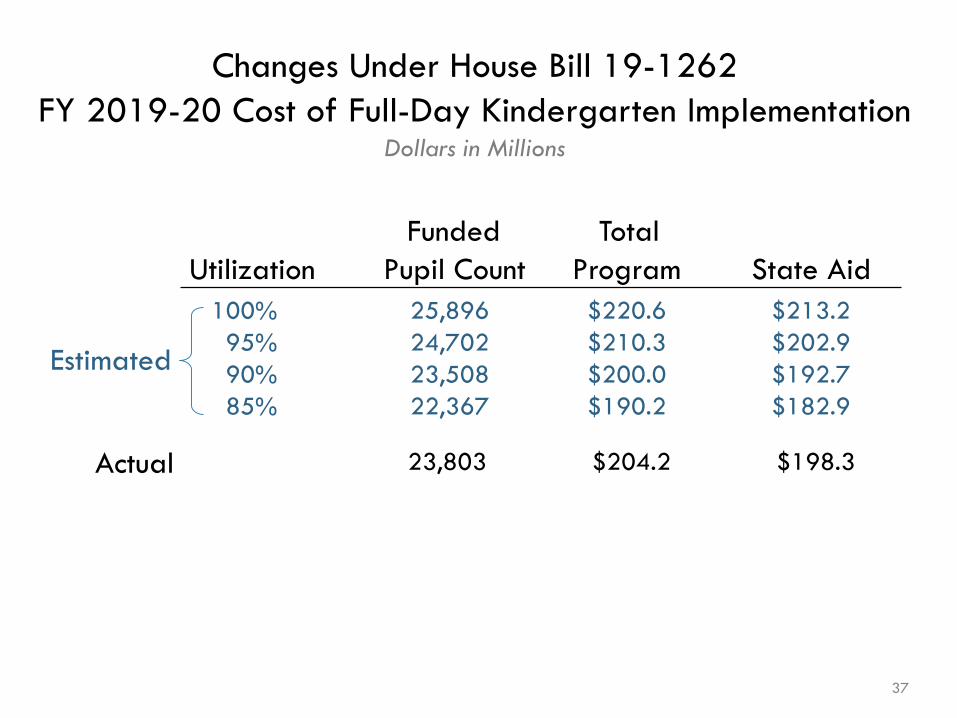

Estimated

23,803 $204.2 $198.3

Funded Total

Utilization Pupil Count Program State Aid

100% 25,896 $220.6 $213.2

95% 24,702 $210.3 $202.9

90% 23,508 $200.0 $192.7

85% 22,367 $190.2 $182.9

Actual

Changes Under House Bill 19-1262

FY 2019-20 Cost of Full-Day Kindergarten ImplementationDollars in Millions

38

$4,620 $4,629 $4,620

$2,966 $2,977 $2,977

$-

$1,000

$2,000

$3,000

$4,000

$5,000

Change in Expectations for FY 2019-20 School Finance FundingDollars in Millions

Source: Legislative Council Staff December 2019 forecast.

Local Share

+$11 million

State Aid

+$9 million

Local

Share

State Aid

Local Share

+$11 million

State Aid

Current Law

Appropriation

$572 million

December 2019 Expectations

The General Assembly's Choices Range From:

Hold at $572 million Increase to $581 millionBS Factor:

39

$4,629 $4,707

$2,977 $3,054

$-

$1,000

$2,000

$3,000

$4,000

$5,000

FY 2019-20 FY 2020-21

Year-over-Year Change in School Finance Funding

FY 2019-20 to FY 2020-21Dollars in Millions

Local Share

State Aid

State Aid*

+$78 million

Local Share

+$77 million

Source: Legislative Council Staff December 2019 forecast.

*Assumes a constant Budget Stabilization Factor.

40

Implications for Balancing General Fund (GF) and

State Education Fund (SEF) Contributions in 2020-21

• $9M required increase in 2019-20; $78M increase in state aid

requirement in 2020-21year-over-year reduces flexibility.

• Increasing 2019-20 SEF spending by $9M implies $15 million

(0.4%) GF increase in 20-21.

• Increasing BS Factor by $9M implies $3 million (0.1%) GF

decrease in 2020-21.

41

Adult Corrections Population Forecast

42

The prison population is down 2.7 percent since February

Source: Department of Corrections, Office of Planning and Analysis. Monthly data.

1,800

1,850

1,900

1,950

2,000

2,050

2,100

16,500

16,700

16,900

17,100

17,300

17,500

17,700

17,900

18,100

18,300

January 2016 January 2017 January 2018 January 2019

Male Left Axis

Female Right Axis

43

Case filings are down, and so are admissions

Source: Office of the State Court Administrator (case filings) and Department of Corrections, Office of Planning and Analysis

(new court commitments). Monthly data; both series shown as six-month moving averages.

300

350

400

450

500

550

600

650

3,000

3,500

4,000

4,500

5,000

5,500

2016 2017 2018 2019

Case Filings Trends

FY 2015-16: +12.8 percent

FY 2016-17: +12.0 percent

FY 2017-18: +5.6 percent

FY 2018-19: +3.0 percent

FY 2019-20: - 4.3 percent (FYTD)

New Court Commitment Trends

FY 2016-17: +11.7 percent

FY 2017-18: +8.3 percent

FY 2018-19: +0.7 percent

FY 2019-20: -10.3 percent (FYTD)

New Court Commitments Right Axis

Monthly Case Filings Left Axis

44

Trend in commitments has reduced inmate expectations

Adult Inmate Population Forecasts as of June 30

Source: Department of Corrections and *Legislative Council Staff December 2019 forecast.

20,135

20,522

20,623

19,619

20,101 20,136

20,136

20,432

20,940

21,483

19,95119,614 19,505 19,564

17,000

18,000

19,000

20,000

21,000

22,000

23,000

24,000

FY 2013 2014 2015 2016 2017 2018 2019 2020* 2021* 2022*

Actual

December 2018 Forecast

December 2019 Forecast

45

Forecast uncertainty remains elevated

Source: Legislative Council Staff December 2019 forecast.

• This forecast always contains (bidirectional) error– Current year forecast error averages about 1.7 percent, or 328 inmates

– Budget year forecast error is about 2.1 percent, or 413 inmates

• Trajectory of new court commitments is most important

determinant of forecast accuracy

• Other risks include:

– Implementation of SB 19-143

– More parole board members and judges

– Supreme Court decision in Allman v. People

– Termination of Denver Community Corrections contracts

46

Parole caseload growth will continue

Adult Parole Caseload Forecasts as of June 30

Source: Department of Corrections and *Legislative Council Staff December 2019 forecast.

8,746

8,116

7,865

8,402 8,286

8,752

9,352

9,297

9,687

10,242

9,757

9,95910,033

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

FY 2013 2014 2015 2016 2017 2018 2019 2020* 2021* 2022*

Actual

December 2018 Forecast

December 2019 Forecast

47

Juvenile Corrections Population Forecast

48

All DYS Populations are FallingAverage Daily Populations through FY 2021-22

Source: CDHS Division of Youth Services and *Legislative Council Staff December 2019 forecast.

851

797

740

693

651 647

578

488452

426

308

291 282 275257 263 254 242 237 234

332

281

246 247220 210 213

184149 141

0

100

200

300

400

500

600

700

800

900

FY 2013 2014 2015 2016 2017 2018 2019 2020* 2021* 2022*

Commitment

Detention

Parole

New court commitments to

DYS decreased 29.1 percent

during FY 2018-19

49

Questions?

Kate WatkinsChief Economist • Legislative Council Staff

[email protected] • (303) 866-3446

www.leg.colorado.gov/lcs