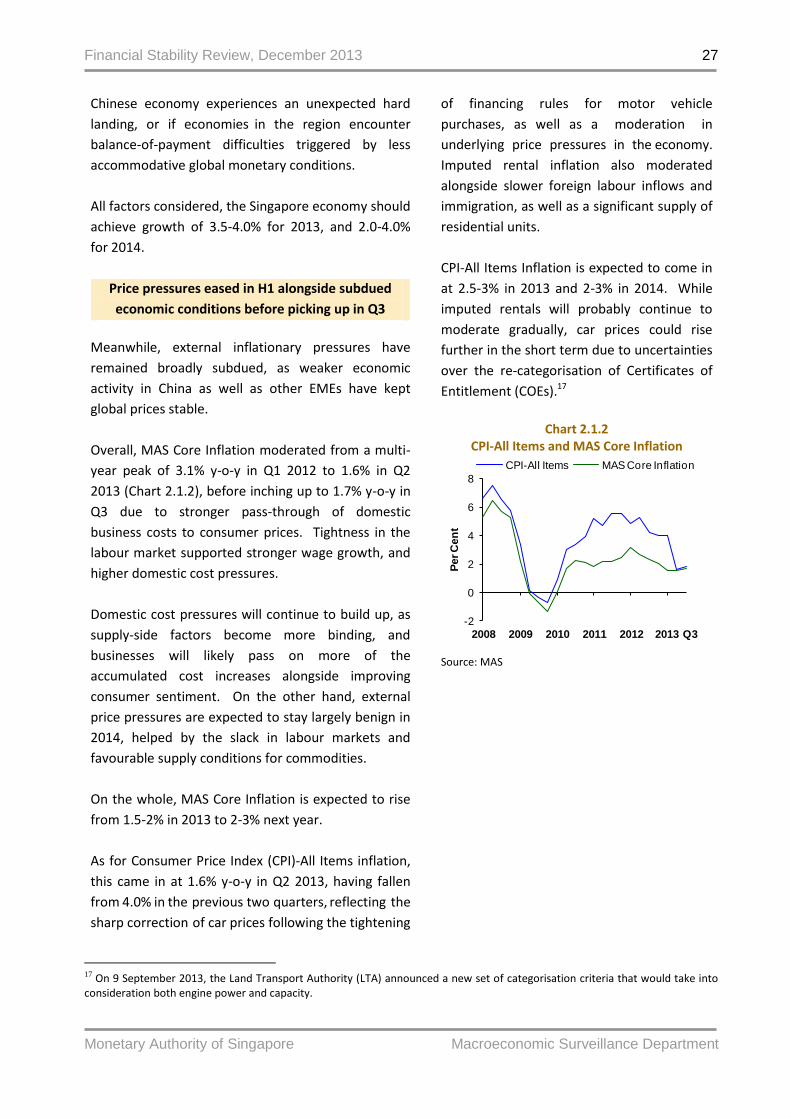

December 2013 - CFS · Financial Stability Review, December 2013 Monetary Authority of Singapore...

91

Transcript of December 2013 - CFS · Financial Stability Review, December 2013 Monetary Authority of Singapore...

December 2013

Macroeconomic Surveillance Department

Monetary Authority of Singapore

ISSN 1793-3463 Published in December 2013 Macroeconomic Surveillance Department Monetary Authority of Singapore http://www.mas.gov.sg All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanised, photocopying, recording or otherwise, without the prior written permission of the copyright owner except in accordance with the provisions of the Copyright Act (Cap. 63). Applications for the copyright owner's written permission to reproduce any part of this publication should be addressed to: Macroeconomic Surveillance Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117 Printed by Oxford Graphic Printers Pte Ltd

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

PREFACE i

OVERVIEW ii

1 GLOBAL ENVIRONMENT

1.1 G3 Macroeconomic Environment and Financial System 1

Box A: A Twist to the Search for Yield Story? 5

1.2 Asia Macroeconomic Environment and Financial System 8

Box B: Intermediating Banking Flows in Asia 19

Box C: Potential Impact of Abenomics on Asia: Boon or Bane? 22

2 SINGAPORE’S MACROECONOMIC ENVIRONMENT AND FINANCIAL SYSTEM

2.1 Macroeconomic Developments and Financial Markets 26

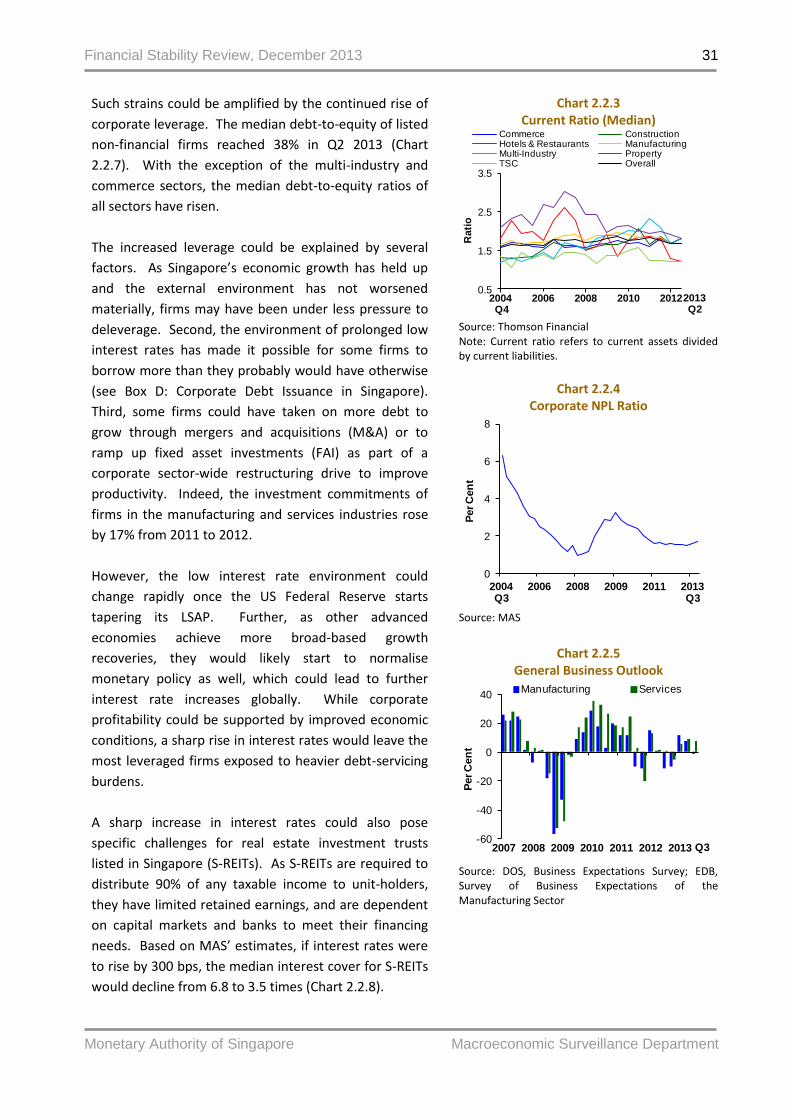

2.2 Corporate Sector 30

Box D: Corporate Bond Issuance in Singapore 35

2.3 Household Sector 38

Box E : Update on the Singapore Private Residential Property Market 41

Box F: Singapore Household Sector: When the Tide Goes Out 44

2.4 Banking Sector 49

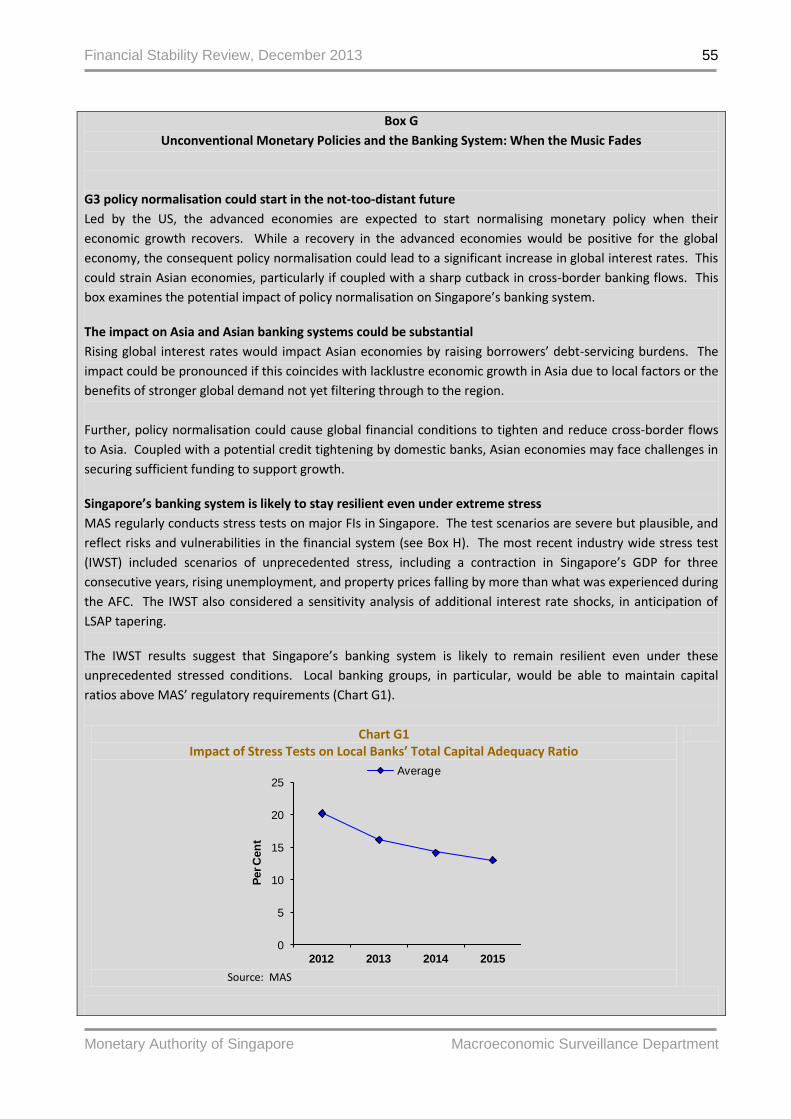

Box G: Unconventional Monetary Policies (UMP) and the Banking System: When the Music Fades

55

Box H: Stress Testing Financial Institutions: Going the Distance 57

2.5 Non-Bank Financial Sector

2.5.1 Insurance Sector 61

Box I: Monitoring the Singapore Insurance Sector’s Systemic Importance and Emerging Risks

64

2.5.2 Capital Markets Sector 66

Box J: Shadow Banking in Singapore? 69

Box K: Over-the-Counter (OTC) Derivatives Reforms: Still A Ways to Go 73

STATISTICAL APPENDIX 75

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

Definitions and Conventions

As used in this report, the term “country” does not in all cases refer to a territorial entity that is a state as

understood by international law and practice. As used here, the term also covers some territorial entities that

are not states but for which statistical data are maintained on a separate and independent basis.

In this report, the following country groupings are used:

Euro zone comprises Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy,

Luxembourg, Malta, Netherlands, Portugal, Slovakia, Slovenia and Spain

“G3” refers to the euro zone and United Kingdom, Japan, and the United States

“G20” refers to the Group of Twenty comprising Argentina, Australia, Brazil, Canada, China, France,

Germany, India, Indonesia, Italy, Japan, Mexico, Russia, Saudi Arabia, South Africa, South Korea,

Turkey, the United Kingdom, the United States and the European Union

“Asia-10” comprises China (CHN), Hong Kong (HK), India (IND), Indonesia (IDN), Korea (KOR), Malaysia

(MYS), the Philippines (PHL), Singapore (SGP), Taiwan (TWN) and Thailand (THA)

“Asia-7” comprises India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand

“NEA-3” comprises Hong Kong, Korea and Taiwan

“SEA-5” comprises Indonesia, Malaysia, the Philippines, Singapore and Thailand

Abbreviations used for financial data are as follows:

Currencies: Chinese Renminbi (RMB), Euro (EUR), Hong Kong Dollar (HKD), Indian Rupee (INR),

Indonesian Rupiah (IDR), Japanese Yen (JPY), Korean Won (KRW), Malaysian Ringgit (MYR), Philippine

Peso (PHP), Singapore Dollar (SGD), Taiwan Dollar (TWD), Thai Baht (THB), US Dollar (USD)

Stock Indices: Bombay Stock Exchange Sensitive Index (SENSEX), FTSE Bursa Malaysia KLCI (FBMKLCI),

Hang Seng Index (HSI), Ho Chi Minh Stock Index (VNINDEX), Jakarta Composite Index (JCI), Korea

Composite Stock Price Index (KOSPI), Nikkei 225 (NKY), Philippine Stock Exchange Index (PSEI),

Shanghai Composite Index (SHCOMP), Stock Exchange of Thailand Index (SET), Straits Times Index (STI),

Taiwan TAIEX Index (TWSE)

Other Abbreviations

ABSD Additional Buyer Stamp Duty

ACU Asian Currency Unit

ADB Asian Development Bank

ADM Asian Dollar Market

AFC Asian Financial Crisis

ASEAN Association of Southeast Asian Nations

AUM Assets Under Management

BCBS Basel Committee on Banking Supervision

BIS Bank for International Settlements

BoE Bank of England

BoJ Bank of Japan

CAR Capital Adequacy Ratio

CCP Central Counterparty

CCR Core Central Region

CCS Credit Counselling Singapore

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

CDP Central Depository

CDS Credit Default Swap

CFTC Commodity Futures Trading Commission

CIS Collective Investment Scheme

CLO Collateralised Loan Obligation

CMBS Commercial Mortage-Backed Security

COE Certificate of Entitlement

CPF Central Provident Fund

CPI Consumer Price Index

CPSS Committee on Payment and Settlement Systems

DBU Domestic Banking Unit

DOS Department of Statistics

EBIT Earnings Before Interest and Tax

EC European Commission

EC Executive Condominium

ECB European Central Bank

EDB Economic Development Board

EME Emerging Market Economy

EMIR European Markets Infrastructure Regulation

ESM European Stability Mechanism

ETF Exchange-Traded Fund

EU European Union FAI Fixed Asset Investment FDI Foreign Direct Investment FI Financial Institution

FLS Funding for Lending Scheme

FMC Fund Management Company

FMI Financial Market Infrastructure

FSAP Financial Sector Assessment Programme

FSB Financial Stability Board

FSOC Financial Stability Oversight Council

FSR Financial Stability Review

GDP Gross Domestic Product

GFC Global Financial Crisis

GLS Government Land Sales

ICAAP Internal Capital Adequacy Assessment Process

IIF Institute of International Finance

IMF International Monetary Fund

IMFC International Monetary and Financial Committee

IOSCO International Organisation of Securities Commissions

IPTO Insolvency and Public Trustee’s Office

IWST Industry-Wide Stress Test

JGB Japanese Government Bond

LIBOR London Interbank Offered Rate

LCR Liquidity Coverage Ratio

LGFV Local Government Financing Vehicle

LSAP Large-Scale Asset Purchase

LTA Land Transport Authority

LTD Loan-to-Deposit

LTRO Long Term Refinancing Operations

LTV Loan-to-Value

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

M&A Mergers and Acquisitions

MAS Monetary Authority of Singapore

MMF Money Market Fund

MSD Macroeconomic Surveillance Department

MSR Mortgage-Servicing Ratio

NAO National Audit Office

NAV Net Asset Value

NEER Nominal Effective Exchange Rate

NIM Net Interest Margin

NPL Non-Performing Loan

OCR Outside Central Region

ODRG OTC Derivatives Regulators Group

OIF Offshore Insurance Fund

OIF Other Investment Fund

OIS Overnight Indexed Swap

OTC Over-the-Counter

PE Private Equity

PFMI Principles for Financial Market Infrastructures

PIK Payment-in-Kind

PPI Property Price Index

RBC Risk-Based Capital

RBI Reserve Bank of India

RCR Rest of Central Region

REIT Real Estate Investment Trust

ROA Return on Assets

S&P Standard & Poor’s

SBL Securities Borrowing / Lending

SEC Securities and Exchange Commission

SFA Securities and Futures Act

SFV Structured Finance Vehicle

SGS Singapore Government Securities

SGX Singapore Exchange Ltd

SGX-DC Singapore Exchange Derivatives Clearing Ltd

SIBOR Singapore Interbank Offered Rate

SIF Singapore Insurance Fund

SLOOS Senior Loan Officer Opinion Survey

SME Small and Medium-Sized Enterprise

SMX Singapore Mercantile Exchange

SOR Swap Offer Rate

SSM Single Supervisory Mechanism

STI Straits Times Index

TDSR Total Debt-Servicing Ratio

TED Treasury-Interbank

TR Trade Repository

TSC Transport, Storage and Communication

UMP Unconventional Monetary Policy

URA Urban Redevelopment Authority

WEO World Economic Outlook

WMP Wealth Management Product

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

i

PREFACE

The Monetary Authority of Singapore (MAS) conducts regular assessments of Singapore’s

financial system. Potential risks and vulnerabilities are identified, and the ability of the

financial system to withstand potential shocks is reviewed. The analysis and results are

published in the annual Financial Stability Review (FSR). The FSR aims to contribute to a

better understanding among market participants, analysts and the public of issues

affecting Singapore’s financial system.

Section 1 of the FSR provides a discussion of the macroeconomic environment and

financial markets both globally and in Asia. Section 2 starts by outlining key developments

in Singapore’s macroeconomic environment and financial system. This is followed by an

analysis of the corporate and household sectors, then the banking sector, which plays a

dominant role in Singapore’s financial landscape. Finally, a review of the non-bank

financial sector, which includes the insurance sector and capital market infrastructure and

intermediaries, is also provided.

The production of the FSR was coordinated by the Macroeconomic Surveillance

Department (MSD) team which comprises Chan Lily, Ng Heng Tiong, Patricia Chua, Foo

Suan Yong, Gay Bing Yong Kenneth, Ho Ruixia Cheryl, Ho Xinyi, Lam Mingli Angeline, Lee

Jia Sheng Harry, Lee Su Fen, Lim Ju Meng Aloysius, Lim Weilun, Qiu Qiaoling Angeline,

Soon Shu Ning Gael, Tan Si Jie, Teoh Shi-Ying, Wong Siang Leng, Yam Yujian, Yeo Siok Lee

Denise, Yeoh Lye Choon Brian, Yip Ee Xiu, Yoe Xue Ting Selene and Zhong Kemin under the

general direction of Dr Lam San Ling, Executive Director (MSD). Valuable statistical and

charting support was provided by members of the MSD Statistics Unit. The FSR also

incorporates contributions from the following departments: Banking Departments I, II &

III, Capital Markets Intermediaries Department, Economic Analysis Department, Economic

Surveillance and Forecasting Department, Insurance Department, International

Department, Investment Intermediaries Department, Market Conduct Department,

Markets Policy & Infrastructure Department, Monetary and Domestic Markets

Management Department, Prudential Policy Department and Specialist Risk Department.

The FSR reflects the views of the staff of the MSD and the contributing departments.

The FSR may be accessed in PDF format on the MAS website:

http://www.mas.gov.sg/Regulations-and-Financial-Stability/Financial-Stability/2013/Financial-Stability-

Review-2013.aspx

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

ii

OVERVIEW

G3 macroeconomic and financial

conditions have improved in 2013,

but challenges remain

The G3 economies have recovered in 2013 – the

US shrugged aside fiscal headwinds, the euro

zone exited from recession, and Japan’s growth

was aided by robust exports and consumption.

The risk of bank defaults in the G3 has receded as

banks’ balance sheets have strengthened.

Deposit outflows have abated while cost cutting

and lower provisions have boosted earnings. G3

sovereign borrowing costs have stayed low, due

to a combination of forceful policy actions, ample

global liquidity, and search for yield by some

investors.

But challenges remain. In the euro zone, credit

quality concerns could impede credit growth and

in turn threaten the fragile recovery. If global

liquidity tightens or market sentiment turns

abruptly, funding costs could rise rapidly for

countries with weaker fundamentals. Emerging

market economies (EMEs) could also come under

pressure, with implications for G3 corporates and

banks that have strong presence in these regions.

In the longer term, structural reforms in the G3

are needed to improve the sustainability of public

finances, break the adverse feedback loops

between sovereigns and banks, and enhance

economic competitiveness.

Unconventional monetary policies

(UMP) cannot be in place indefinitely;

policy normalisation needs to be

carefully planned and communicated

Much of the improvements in G3 economic and

financial conditions have been underpinned by

unconventional monetary policies (UMP).

However, these policies cannot be in place

indefinitely because they have potential

implications for monetary and financial stability.

As G3 policymakers consider policy

normalisation, it is important that they do so in

carefully-considered steps that are clearly

communicated.

Asia’s economic growth and financial

markets have held up amid abundant

global liquidity and risk appetite …

Turning to Asia, economic growth has held up

despite mixed conditions. UMP has helped to

bolster global growth in the near term, in turn

providing support for Asia. Some authorities

have also adopted fiscal measures to provide a

fillip to growth.

Meanwhile, the abundant global liquidity and risk

appetite underpinned by UMP have combined

with record low interest rates in the region to

keep financial markets buoyant for the most part.

… but considerable downside risks lie ahead

However, considerable risks lie ahead.

Uncertainties surrounding the G3 economic

recovery and domestic restructuring efforts in

Asia cloud the growth outlook for the region.

Although Asia is more resilient now than during

the Asian Financial Crisis (AFC), the financial

market turbulence in recent months attests to

the strains that G3 policy normalisation can have

on the region.

Of particular concern is the build-up of private

and public sector debt in recent years. If G3

policy normalisation triggers an abrupt tightening

of financial conditions, debt-servicing burdens in

Asia can rise sharply. A dip in confidence can

lead to currency depreciation, which can add to

debt repayment costs for those who had

borrowed in foreign currencies. With volatile

capital flows, banks may come under foreign-

currency funding pressure. They may also tighten

credit supply as defaults rise, leading to a vicious

cycle of declining asset quality, tightening credit

and slowing growth. The potential impact across

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

iii

Asia could be uneven, depending on market

perceptions of which economies are more

susceptible to external shocks.

Singapore’s economy and financial markets

have been resilient …

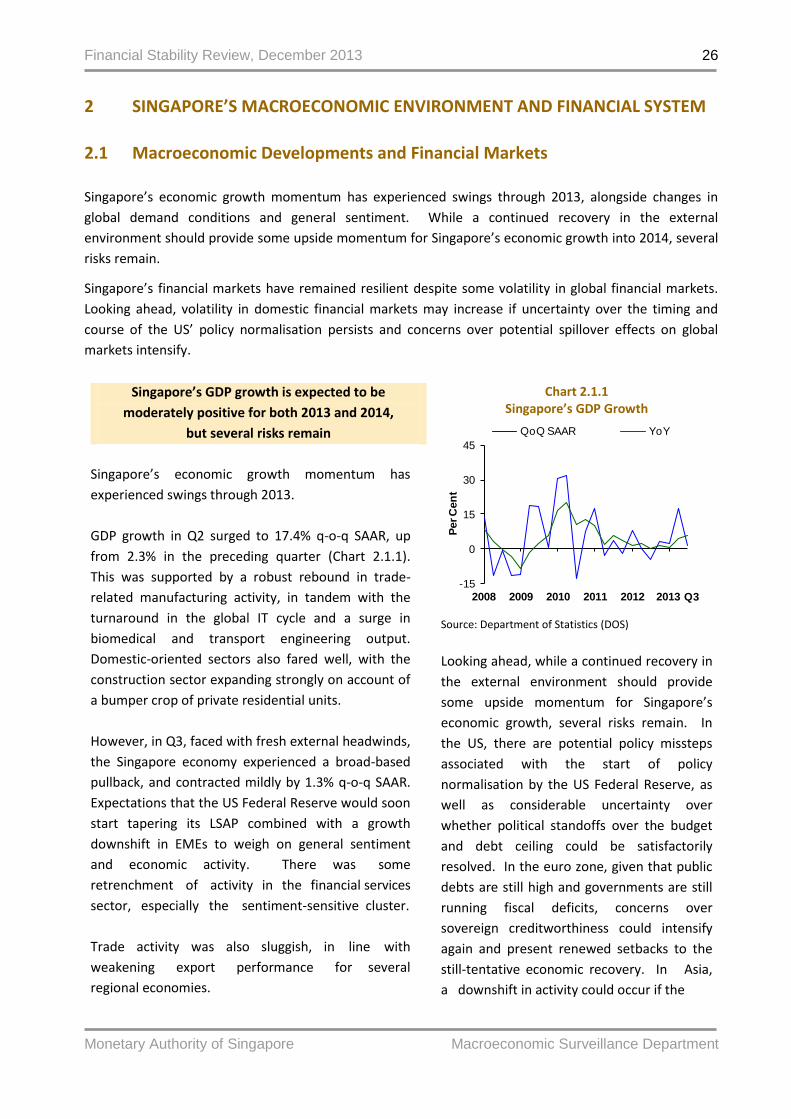

Singapore’s economic growth has held up in 2013

despite considerable swings in momentum, and is

expected to remain moderately positive in 2014.

Reflecting confidence in our economic

fundamentals and fiscal discipline, domestic

financial markets have stayed resilient.

Corporate and household balance sheets as

well as the banking system stay healthy …

Corporate and household balance sheets are

healthy in aggregate. The corporate sector’s

profitability has improved in a broad-based

manner while liquidity positions appear

adequate. Household net wealth continues to

grow, and stands at four times GDP.

The banking system has stayed resilient. Local

banks already meet Basel III capital requirements.

Loan growth has been firm, with increased

exposure to Asia. Asset quality remains healthy,

and Singapore Dollar (SGD) funding for domestic

lending remains adequate.

… but downside risks remain;

the need for vigilance is clear

However, several downside risks lie ahead. The

global environment could deteriorate, posing

uncertainties for Singapore’s growth outlook.

Interest rates – and therefore debt-servicing

burdens – could increase markedly and perhaps

unexpectedly soon. In turn, growth shocks and

financial market volatility could affect the

property market and the banking system.

Rising corporate and household sector

indebtedness could amplify strains

from higher interest rates

Corporate leverage has increased across almost

all sectors. Higher interest rates arising from G3

policy normalisation could leave the most

leveraged firms exposed to heavier debt-servicing

burdens.

Household sector debt has also trended up

alongside firm increases in assets and net wealth

over the past few years, albeit at a slower pace in

recent quarters. If mortgage rates rise by three

percentage points, the share of over-leveraged

households could rise to 10-15%. MAS has

introduced measures to encourage prudent

borrowing and help keep household debt in

check.

The property market continues to

warrant close monitoring

The Total Debt Servicing Ratio (TDSR) framework,

together with earlier policy measures by the

Government, has moderated property market

transaction activity and housing loan growth.

However, developer bids for land parcels remain

firm. The current uncertain environment

warrants continued caution and vigilance.

The banking sector needs to guard

against credit quality deterioration

and liquidity risks

The banking sector needs to guard against credit

quality deterioration and liquidity risks. In

particular, as banks expand their cross-border

lending to the region, they need to monitor these

exposures carefully.

In addition, banks need to continue managing

their liquidity risks prudently. The local banks

have been taking measures to improve their US

dollar (USD) funding profiles. They need to stay

vigilant on this front to avoid adverse effects

from any abrupt tightening in global USD

liquidity.

Macroeconomic Surveillance Department

Monetary Authority of Singapore

3 December 2013

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

1

GLOBAL ENVIRONMENT

1.1 G3 Macroeconomic Environment and Financial System

Macroeconomic and financial conditions in the G3 improved in 2013, supported by unconventional

monetary policies (UMP). However, loose monetary conditions cannot be in place indefinitely, and a

sustained economic recovery would need to be backed by appropriate structural reforms.

With the growth outlook in advanced economies still subject to considerable uncertainty, the mere

prospect of the US starting to normalise policy by tapering its large-scale asset purchase (LSAP)

programme triggered heightened volatility in global financial markets. This attests to the ramifications

that the G3’s economic growth, financial system resilience and policy actions can have globally.

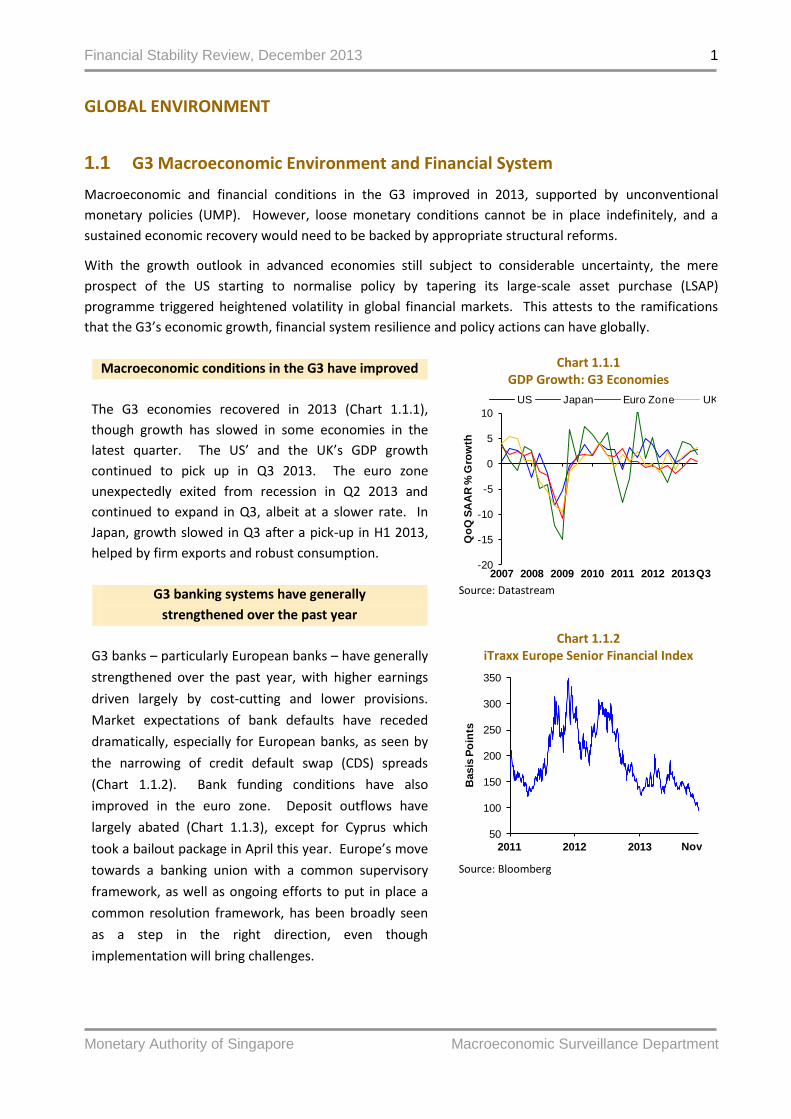

Macroeconomic conditions in the G3 have improved

The G3 economies recovered in 2013 (Chart 1.1.1),

though growth has slowed in some economies in the

latest quarter. The US’ and the UK’s GDP growth

continued to pick up in Q3 2013. The euro zone

unexpectedly exited from recession in Q2 2013 and

continued to expand in Q3, albeit at a slower rate. In

Japan, growth slowed in Q3 after a pick-up in H1 2013,

helped by firm exports and robust consumption.

G3 banking systems have generally

strengthened over the past year

G3 banks – particularly European banks – have generally

strengthened over the past year, with higher earnings

driven largely by cost-cutting and lower provisions.

Market expectations of bank defaults have receded

dramatically, especially for European banks, as seen by

the narrowing of credit default swap (CDS) spreads

(Chart 1.1.2). Bank funding conditions have also

improved in the euro zone. Deposit outflows have

largely abated (Chart 1.1.3), except for Cyprus which

took a bailout package in April this year. Europe’s move

towards a banking union with a common supervisory

framework, as well as ongoing efforts to put in place a

common resolution framework, has been broadly seen

as a step in the right direction, even though

implementation will bring challenges.

Chart 1.1.1 GDP Growth: G3 Economies

Source: Datastream

Chart 1.1.2 iTraxx Europe Senior Financial Index

Source: Bloomberg

-20

-15

-10

-5

0

5

10

2007 2008 2009 2010 2011 2012 2013

Qo

Q S

AA

R %

Gro

wth

US Japan Euro Zone UK

Q3

50

100

150

200

250

300

350

2011 2012 2013

Basis

Po

ints

Nov

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

2

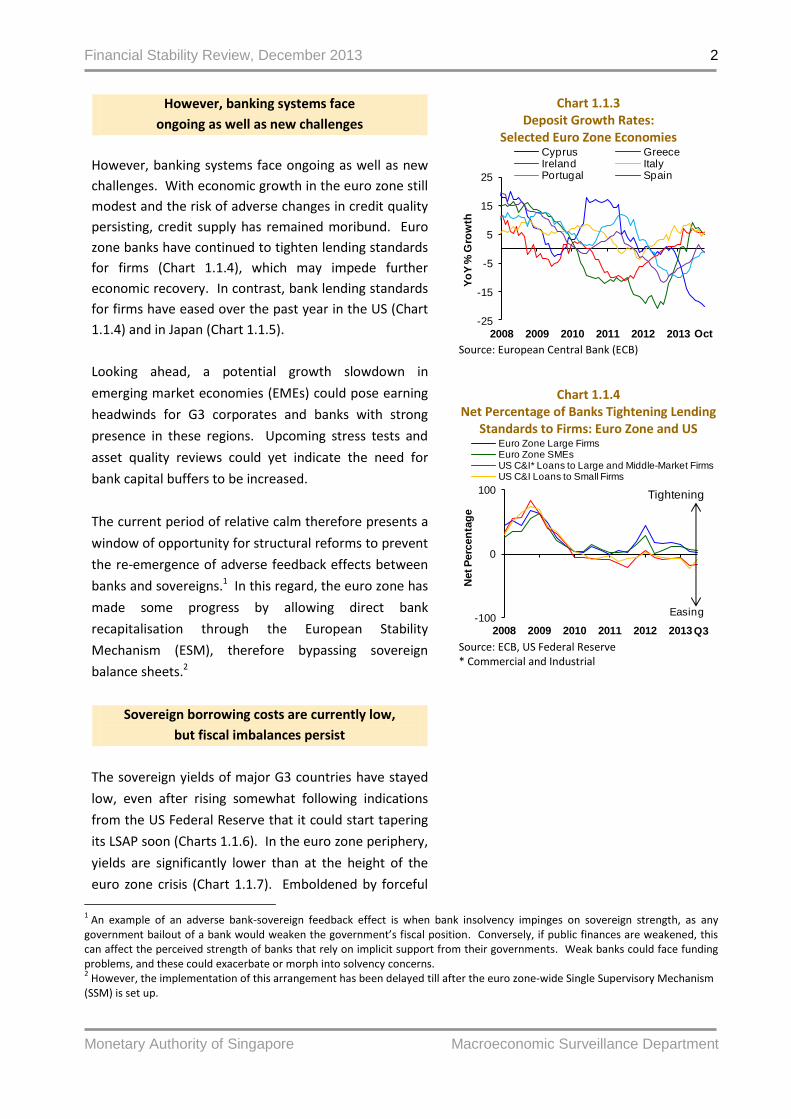

However, banking systems face

ongoing as well as new challenges

However, banking systems face ongoing as well as new

challenges. With economic growth in the euro zone still

modest and the risk of adverse changes in credit quality

persisting, credit supply has remained moribund. Euro

zone banks have continued to tighten lending standards

for firms (Chart 1.1.4), which may impede further

economic recovery. In contrast, bank lending standards

for firms have eased over the past year in the US (Chart

1.1.4) and in Japan (Chart 1.1.5).

Looking ahead, a potential growth slowdown in

emerging market economies (EMEs) could pose earning

headwinds for G3 corporates and banks with strong

presence in these regions. Upcoming stress tests and

asset quality reviews could yet indicate the need for

bank capital buffers to be increased.

The current period of relative calm therefore presents a

window of opportunity for structural reforms to prevent

the re-emergence of adverse feedback effects between

banks and sovereigns.1 In this regard, the euro zone has

made some progress by allowing direct bank

recapitalisation through the European Stability

Mechanism (ESM), therefore bypassing sovereign

balance sheets.2

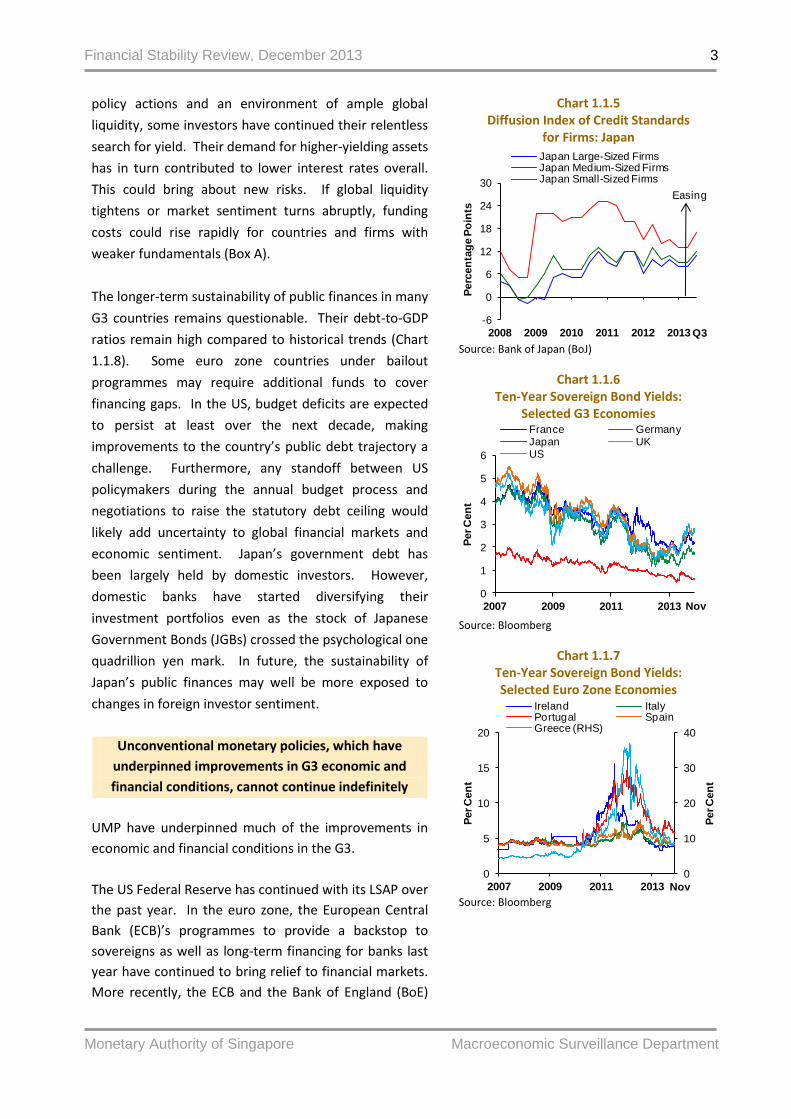

Sovereign borrowing costs are currently low,

but fiscal imbalances persist

The sovereign yields of major G3 countries have stayed

low, even after rising somewhat following indications

from the US Federal Reserve that it could start tapering

its LSAP soon (Charts 1.1.6). In the euro zone periphery,

yields are significantly lower than at the height of the

euro zone crisis (Chart 1.1.7). Emboldened by forceful

Chart 1.1.3 Deposit Growth Rates:

Selected Euro Zone Economies

Source: European Central Bank (ECB)

Chart 1.1.4 Net Percentage of Banks Tightening Lending

Standards to Firms: Euro Zone and US

Source: ECB, US Federal Reserve * Commercial and Industrial

1 An example of an adverse bank-sovereign feedback effect is when bank insolvency impinges on sovereign strength, as any

government bailout of a bank would weaken the government’s fiscal position. Conversely, if public finances are weakened, this can affect the perceived strength of banks that rely on implicit support from their governments. Weak banks could face funding problems, and these could exacerbate or morph into solvency concerns. 2 However, the implementation of this arrangement has been delayed till after the euro zone-wide Single Supervisory Mechanism

(SSM) is set up.

-25

-15

-5

5

15

25

2008 2009 2010 2011 2012 2013

Yo

Y %

Gro

wth

Cyprus GreeceIreland ItalyPortugal Spain

Oct

-100

0

100

2008 2009 2010 2011 2012 2013

Net P

erc

en

tag

e

Euro Zone Large Firms Euro Zone SMEsUS C&I* Loans to Large and Middle-Market FirmsUS C&I Loans to Small Firms

Q3

Easing

Tightening

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

3

policy actions and an environment of ample global

liquidity, some investors have continued their relentless

search for yield. Their demand for higher-yielding assets

has in turn contributed to lower interest rates overall.

This could bring about new risks. If global liquidity

tightens or market sentiment turns abruptly, funding

costs could rise rapidly for countries and firms with

weaker fundamentals (Box A).

The longer-term sustainability of public finances in many

G3 countries remains questionable. Their debt-to-GDP

ratios remain high compared to historical trends (Chart

1.1.8). Some euro zone countries under bailout

programmes may require additional funds to cover

financing gaps. In the US, budget deficits are expected

to persist at least over the next decade, making

improvements to the country’s public debt trajectory a

challenge. Furthermore, any standoff between US

policymakers during the annual budget process and

negotiations to raise the statutory debt ceiling would

likely add uncertainty to global financial markets and

economic sentiment. Japan’s government debt has

been largely held by domestic investors. However,

domestic banks have started diversifying their

investment portfolios even as the stock of Japanese

Government Bonds (JGBs) crossed the psychological one

quadrillion yen mark. In future, the sustainability of

Japan’s public finances may well be more exposed to

changes in foreign investor sentiment.

Unconventional monetary policies, which have

underpinned improvements in G3 economic and

financial conditions, cannot continue indefinitely

UMP have underpinned much of the improvements in

economic and financial conditions in the G3.

The US Federal Reserve has continued with its LSAP over

the past year. In the euro zone, the European Central

Bank (ECB)’s programmes to provide a backstop to

sovereigns as well as long-term financing for banks last

year have continued to bring relief to financial markets.

More recently, the ECB and the Bank of England (BoE)

Chart 1.1.5 Diffusion Index of Credit Standards

for Firms: Japan

Source: Bank of Japan (BoJ)

Chart 1.1.6 Ten-Year Sovereign Bond Yields:

Selected G3 Economies

Source: Bloomberg

Chart 1.1.7 Ten-Year Sovereign Bond Yields: Selected Euro Zone Economies

Source: Bloomberg

-6

0

6

12

18

24

30

2008 2009 2010 2011 2012 2013

Perc

en

tag

e P

oin

ts

Japan Large-Sized FirmsJapan Medium-Sized FirmsJapan Small-Sized Firms

Q3

Easing

0

1

2

3

4

5

6

2007 2009 2011 2013

Per C

en

t

France Germany Japan UKUS

Nov

0

10

20

30

40

0

5

10

15

20

2007 2009 2011 2013

Per C

en

t

Per C

en

t

Ireland ItalyPortugal SpainGreece (RHS)

Nov

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

4

have used forward guidance on interest rates to try to

allay concerns that premature interest rate rises could

derail Europe’s fledgling recovery. The BoJ also started

an aggressive quantitative easing programme in April to

replace its previous asset purchase programme.

However UMP cannot be in place indefinitely. Such

policies have led to sharp expansions in the balance

sheets of major central banks since 2008 (Chart 1.1.9).

This has potential implications for monetary and

financial stability, and could also lead to financial market

distortions.

Looking ahead, it is vital to normalise policy

in carefully-considered steps

Looking ahead, as G3 policymakers begin to consider

normalising policy, it is important that they pay

attention to the potential spillover effects. A case in

point is the heightened volatility in global financial

markets and spillover effects on EMEs after the US

Federal Reserve indicated that it could start tapering its

LSAP programme.

Leaders of the International Monetary and Financial

Committee (IMFC) have stressed that the eventual

transition toward the normalisation of monetary policy

should be well timed, carefully calibrated, and clearly

communicated. G20 leaders have also called for

cooperation to manage these spillovers to other

countries.

Chart 1.1.8 Public Debt-to-GDP Ratio:

Selected G3 Economies

Source: International Monetary Fund (IMF) World Economic Outlook (WEO)

Chart 1.1.9

Central Bank Assets: Selected G3 Economies

Source: Bloomberg

0

50

100

150

200

250

300

1990 1995 2000 2005 2010 2015

Per C

en

t

France GermanyGreece IrelandItaly JapanPortugal SpainUnited Kingdom United States

Estimates as at 2013

2018

50

150

250

350

450

2008 2009 2010 2011 2012 2013

Ind

ex (Jan

2008 =

100)

Federal Reserve ECBBank of England Bank of Japan

Nov

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

5

Box A

A Twist to the Search for Yield Story?

Rising search for yield in advanced economies may exacerbate risks

Over the past few years, UMP in the advanced economies and ample global liquidity have led to investors

migrating down the creditworthiness ladder in a search for yield. This search for yield is also evident in EMEs,

including Asia, where strong capital inflows have put upward pressure on asset prices. Indication by the US

Federal Reserve in May that it could start tapering its LSAP programme soon led to capital outflows from and

exchange rate volatility in EMEs. Looking ahead, as investors reassess the risk-return profile of EME

investments, the tide may turn, with investors, including those from EMEs, looking more to the advanced

economies for yield. This could result in a further build-up of risk in the more vulnerable market segments in

the advanced economies.

More signs of search for yield in advanced economies

There have been growing signs of search for yield in the advanced economies:

Sovereign bonds of euro zone periphery: Sovereign bond yields for peripheral euro zone countries have

remained low despite high public sector debts and slow progress in reforms to achieve fiscal

sustainability. While strong policy actions have staved off the risk of an immediate crisis in the euro

zone, some of the yield compression could also have been due to investors’ willingness to purchase

these sovereign bonds in the search for yield.

High-yield corporate debt in Europe and the US: Speculative-grade bond yields in Europe and the US

remain low (Chart A1), a sign of strong demand for high-yield debt. European high-yield corporate

bond issuance so far this year has exceeded the record issuance in 2012 (Chart A2), in spite of a dip in

June due to LSAP tapering concerns.

Chart A1 Speculative-Grade Corporate Bond Yields:

Europe and US

Source: Bloomberg

Chart A2 Speculative-Grade Corporate Bond Issuance:

Peripheral Euro Zone and Rest of Europe

Source: Dealogic

0

6

12

18

24

30

2008 2009 2010 2011 2012 2013

Per C

en

t

Europe US

Nov

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013Oct

ytd

€B

illio

n

Peripheral Euro Zone Rest of Europe

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

6

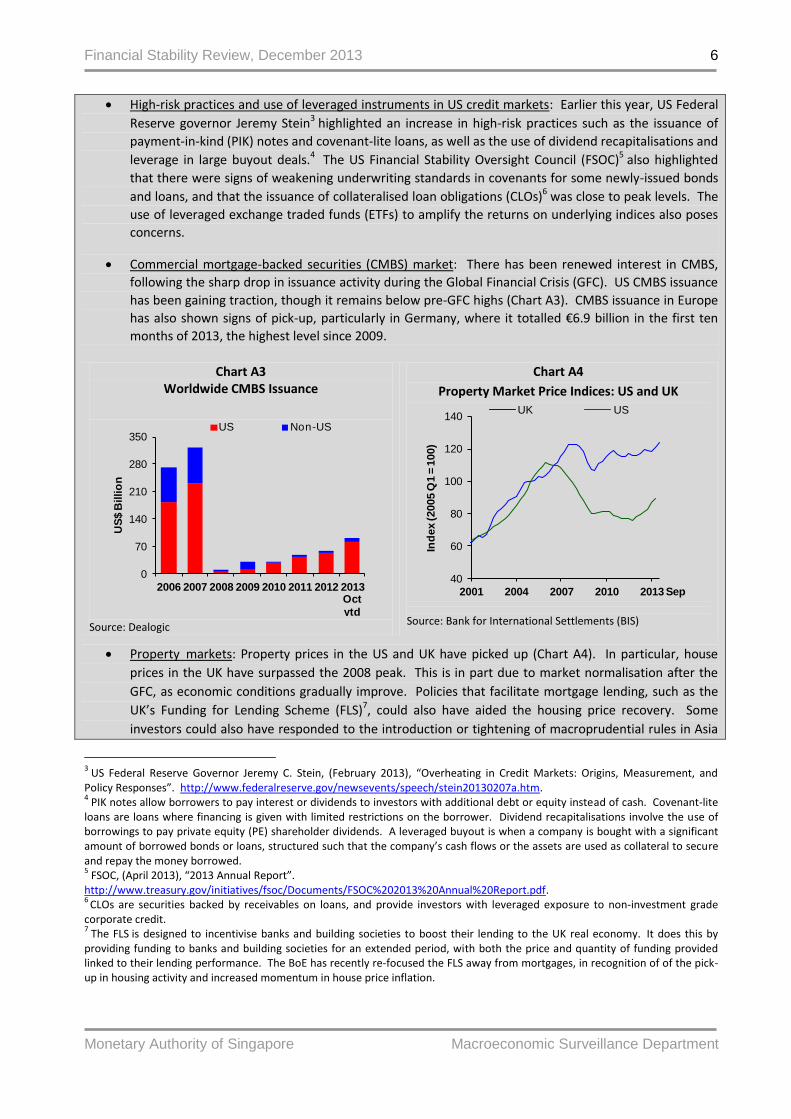

High-risk practices and use of leveraged instruments in US credit markets: Earlier this year, US Federal

Reserve governor Jeremy Stein3 highlighted an increase in high-risk practices such as the issuance of

payment-in-kind (PIK) notes and covenant-lite loans, as well as the use of dividend recapitalisations and

leverage in large buyout deals.4 The US Financial Stability Oversight Council (FSOC)5 also highlighted

that there were signs of weakening underwriting standards in covenants for some newly-issued bonds

and loans, and that the issuance of collateralised loan obligations (CLOs)6 was close to peak levels. The

use of leveraged exchange traded funds (ETFs) to amplify the returns on underlying indices also poses

concerns.

Commercial mortgage-backed securities (CMBS) market: There has been renewed interest in CMBS,

following the sharp drop in issuance activity during the Global Financial Crisis (GFC). US CMBS issuance

has been gaining traction, though it remains below pre-GFC highs (Chart A3). CMBS issuance in Europe

has also shown signs of pick-up, particularly in Germany, where it totalled €6.9 billion in the first ten

months of 2013, the highest level since 2009.

Chart A3 Worldwide CMBS Issuance

Source: Dealogic

Chart A4

Property Market Price Indices: US and UK

Source: Bank for International Settlements (BIS)

Property markets: Property prices in the US and UK have picked up (Chart A4). In particular, house

prices in the UK have surpassed the 2008 peak. This is in part due to market normalisation after the

GFC, as economic conditions gradually improve. Policies that facilitate mortgage lending, such as the

UK’s Funding for Lending Scheme (FLS)7, could also have aided the housing price recovery. Some

investors could also have responded to the introduction or tightening of macroprudential rules in Asia

3 US Federal Reserve Governor Jeremy C. Stein, (February 2013), “Overheating in Credit Markets: Origins, Measurement, and

Policy Responses”. http://www.federalreserve.gov/newsevents/speech/stein20130207a.htm. 4 PIK notes allow borrowers to pay interest or dividends to investors with additional debt or equity instead of cash. Covenant-lite

loans are loans where financing is given with limited restrictions on the borrower. Dividend recapitalisations involve the use of borrowings to pay private equity (PE) shareholder dividends. A leveraged buyout is when a company is bought with a significant amount of borrowed bonds or loans, structured such that the company’s cash flows or the assets are used as collateral to secure and repay the money borrowed. 5 FSOC, (April 2013), “2013 Annual Report”.

http://www.treasury.gov/initiatives/fsoc/Documents/FSOC%202013%20Annual%20Report.pdf. 6

CLOs are securities backed by receivables on loans, and provide investors with leveraged exposure to non-investment grade corporate credit. 7 The FLS is designed to incentivise banks and building societies to boost their lending to the UK real economy. It does this by

providing funding to banks and building societies for an extended period, with both the price and quantity of funding provided linked to their lending performance. The BoE has recently re-focused the FLS away from mortgages, in recognition of of the pick-up in housing activity and increased momentum in house price inflation.

0

70

140

210

280

350

2006 2007 2008 2009 2010 2011 2012 2013Oct

ytd

US

$ B

illio

n

US Non-US

40

60

80

100

120

140

2001 2004 2007 2010 2013

Ind

ex (2005 Q

1 =

100)

UK US

Sep

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

7

by seeking returns in other property markets.

Risks that could arise from the search for yield

Lack of impetus for change could result in build-up of longer-term risks in peripheral Europe

Low sovereign bond yields in peripheral Europe have reduced the immediate pressure on governments to take

hard decisions on fundamental structural reforms. Longer-term risks could build up and be more painful to

unwind down the road.

Have investors understood sufficiently the risk implications?

The strong demand for high-yield debt raises the question of whether investors have sufficiently priced in the

possibility of increased default rates and widening credit spreads should markets turn.

Signs of stress in the CMBS market have emerged – the number of CMBS defaults in Europe in H1 2013 was

double that in the same period last year, though the number of defaults later fell in Q3 2013. Falling prices for

commercial properties outside major cities could suggest that some loans which support CMBS arranged during

boom times have been failing to repay at maturity. The US FSOC8 has warned that the commercial real estate

sector remains vulnerable to refinancing risks in the event of a sharp rise in interest rates, which could lead to

more CMBS defaults.

The US Securities and Exchange Commission (SEC)9 had highlighted previously that some ETFs could have

unusual investment objectives or use complex investment strategies that might be difficult to understand. For

example, leveraged ETFs may be unsuitable as long-term investment tools, as their investment objectives are

typically set on a short-term basis, something which may not be clear to unsophisticated investors. At a

broader level, the Federal Reserve10 has warned that trading activity of leveraged ETFs during bouts of market

volatility could lead to a cascading reaction that may destabilise the broader market.

The strong demand for high-yield debt could also be encouraging products with structures that may be

disadvantageous to investors, such as PIK toggle deals which give borrowers the option to repay lenders with

more debt rather than cash. These disadvantageous structures could become apparent to investors only in the

future should defaults pick up or (re)financing suddenly becomes more difficult.

Could new asset bubbles be forming?

Could the pace of house price increases in the US and the UK be a sign that asset bubbles are forming again?

Beyond risks to investors, there are also concerns that another asset bubble could lead to renewed risks for

bank asset quality.

Policymakers must stand prepared to manage risks

Although all eyes have recently been on heightened volatility in EMEs, it is important to be watchful of capital

inflows to vulnerable sectors in the advanced economies, which could lead to a build-up of risks. Peripheral

euro zone countries need to implement structural reforms to improve their economic competitiveness and

fiscal sustainability. Investors need to exercise caution when dealing with high-yield debt and other new

investment products. Policymakers need to stay vigilant and be prepared to take measures to manage risks

that may emerge.

8 FSOC, (April 2013), “2013 Annual Report”.

http://www.treasury.gov/initiatives/fsoc/Documents/FSOC%202013%20Annual%20Report.pdf. 9 US SEC (August 2012), “Investor Bulletin: Exchange-Traded Funds (ETFs)”. http://www.sec.gov/investor/alerts/etfs.pdf.

10 Tugkan Tuzun, US Federal Reserve (July 2013), “Are Leveraged and Inverse ETFs the New Portfolio Insurers?”.

http://www.federalreserve.gov/pubs/feds/2013/201348/201348pap.pdf.

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

8

1.2 Asia Macroeconomic Environment and Financial System

Over the past few years, an unusual combination of factors – abundant global liquidity and risk appetite

underpinned by advanced economies’ UMP, record low interest rates and various fiscal measures in Asia –

has made it possible for Asia’s economic growth to hold up and financial markets to be buoyed by bullish

sentiment for the most part. This has been fuelled, in part, by a build-up of public and private sector debt.

The environment could soon change, as the US leads the way in starting to normalise monetary policy by

tapering its LSAP programme, even as uncertainties surround the G3 economic recovery and restructuring

efforts in Asia. Global financial tightening can lead to stresses, including interest rate increases, shifts in

sentiment and volatile capital flows. These stresses can manifest themselves quickly for borrowers,

financial markets and banking systems, with uneven impact on different parts of the region.

Asia as a region is more resilient today than during the Asian Financial Crisis (AFC). Various policy

measures have helped to reduce vulnerabilities to external shocks. Nonetheless, further progress in this

respect will strengthen the resilience of individual countries as well as the entire region.

Asia’s economic growth momentum has been

mixed, and considerable risks lie ahead

Asia’s economic growth momentum has been mixed,

slowing in some countries while exhibiting resilience

in others. Considerable downside risks remain.

Economic growth in several parts of Asia ex-Japan

moderated in 2013. This was due to certain country-

specific factors, still-tepid external demand from

major advanced economies and some effects of

China’s domestic restructuring efforts.

India’s growth slowed to 4.4% y-o-y in Q2 (Chart

1.2.1), the weakest pace since Q1 2009, reflecting a

broad-based deceleration across both the industrial-

and services sector, before picking up moderately to

4.8% y-o-y in Q3. From a longer-term perspective,

infrastructure gaps and policy gridlock have been key

factors behind persistent drags on growth.

In most parts of Southeast Asia, growth decelerated

(Chart 1.2.2), as domestic demand slowed and export

growth remained subdued. Thailand slipped into a

technical recession in Q2, as post-flood

reconstruction spending tapered off and private

Chart 1.2.1 GDP Growth: Selected Asian Economies

Source: Bloomberg

Chart 1.2.2 GDP Growth: Selected Asian Economies

Source: Bloomberg

-5

0

5

10

15

2010 2011 2012 2013

Yo

Y %

Gro

wth

China Hong Kong

India Korea

Taiwan

Q3

-10

-5

0

5

10

15

20

-6

-3

0

3

6

9

12

2010 2011 2012 2013

Yo

Y %

Gro

wth

Yo

Y %

Gro

wth

Indonesia Malaysia

Philippines Singapore (RHS)

Thailand (RHS)

Q3

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

9

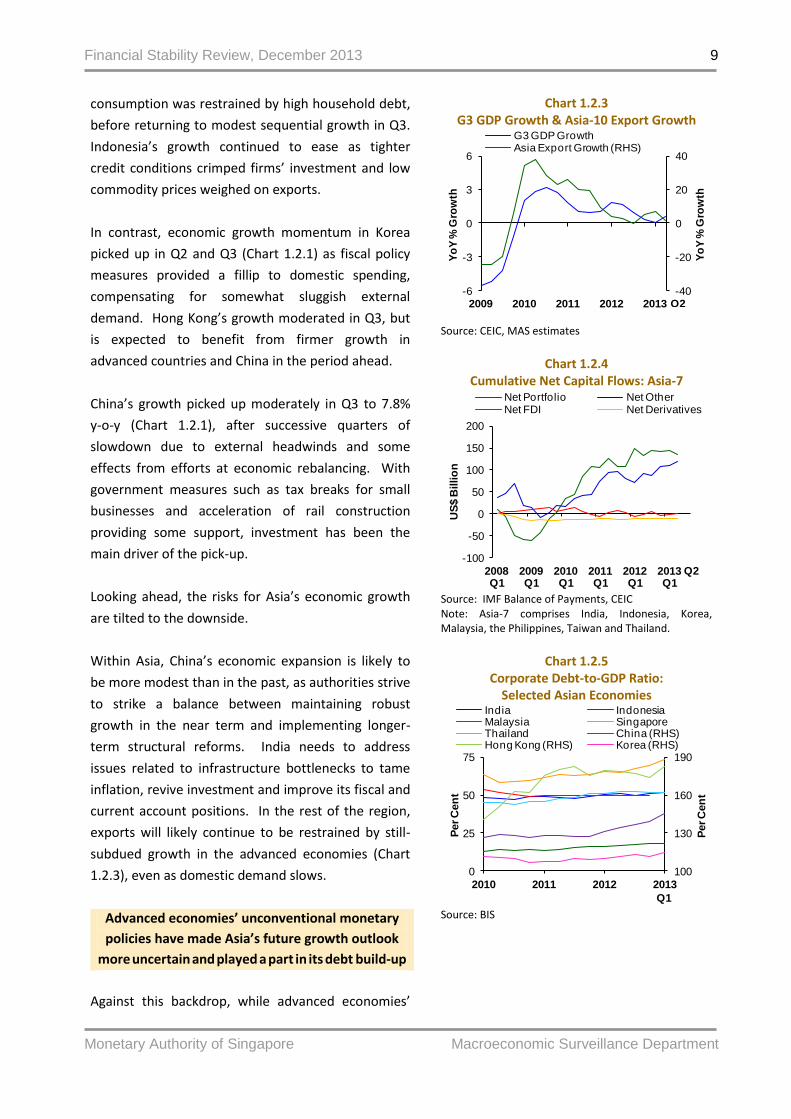

consumption was restrained by high household debt,

before returning to modest sequential growth in Q3.

Indonesia’s growth continued to ease as tighter

credit conditions crimped firms’ investment and low

commodity prices weighed on exports.

In contrast, economic growth momentum in Korea

picked up in Q2 and Q3 (Chart 1.2.1) as fiscal policy

measures provided a fillip to domestic spending,

compensating for somewhat sluggish external

demand. Hong Kong’s growth moderated in Q3, but

is expected to benefit from firmer growth in

advanced countries and China in the period ahead.

China’s growth picked up moderately in Q3 to 7.8%

y-o-y (Chart 1.2.1), after successive quarters of

slowdown due to external headwinds and some

effects from efforts at economic rebalancing. With

government measures such as tax breaks for small

businesses and acceleration of rail construction

providing some support, investment has been the

main driver of the pick-up.

Looking ahead, the risks for Asia’s economic growth

are tilted to the downside.

Within Asia, China’s economic expansion is likely to

be more modest than in the past, as authorities strive

to strike a balance between maintaining robust

growth in the near term and implementing longer-

term structural reforms. India needs to address

issues related to infrastructure bottlenecks to tame

inflation, revive investment and improve its fiscal and

current account positions. In the rest of the region,

exports will likely continue to be restrained by still-

subdued growth in the advanced economies (Chart

1.2.3), even as domestic demand slows.

Advanced economies’ unconventional monetary

policies have made Asia’s future growth outlook

more uncertain and played a part in its debt build-up

Against this backdrop, while advanced economies’

Chart 1.2.3 G3 GDP Growth & Asia-10 Export Growth

Source: CEIC, MAS estimates

Chart 1.2.4

Cumulative Net Capital Flows: Asia-7

Source: IMF Balance of Payments, CEIC Note: Asia-7 comprises India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

Chart 1.2.5

Corporate Debt-to-GDP Ratio: Selected Asian Economies

Source: BIS

-40

-20

0

20

40

-6

-3

0

3

6

2009 2010 2011 2012 2013

Yo

Y %

Gro

wth

Yo

Y %

Gro

wth

G3 GDP Growth Asia Export Growth (RHS)

Q2

-100

-50

0

50

100

150

200

2008Q1

2009Q1

2010Q1

2011Q1

2012Q1

2013Q1

US

$ B

illio

n

Net Portfolio Net OtherNet FDI Net Derivatives

Q2

100

130

160

190

0

25

50

75

2010 2011 2012 2013

Per C

en

t

Per C

en

t

India IndonesiaMalaysia SingaporeThailand China (RHS)Hong Kong (RHS) Korea (RHS)

Q1

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

10

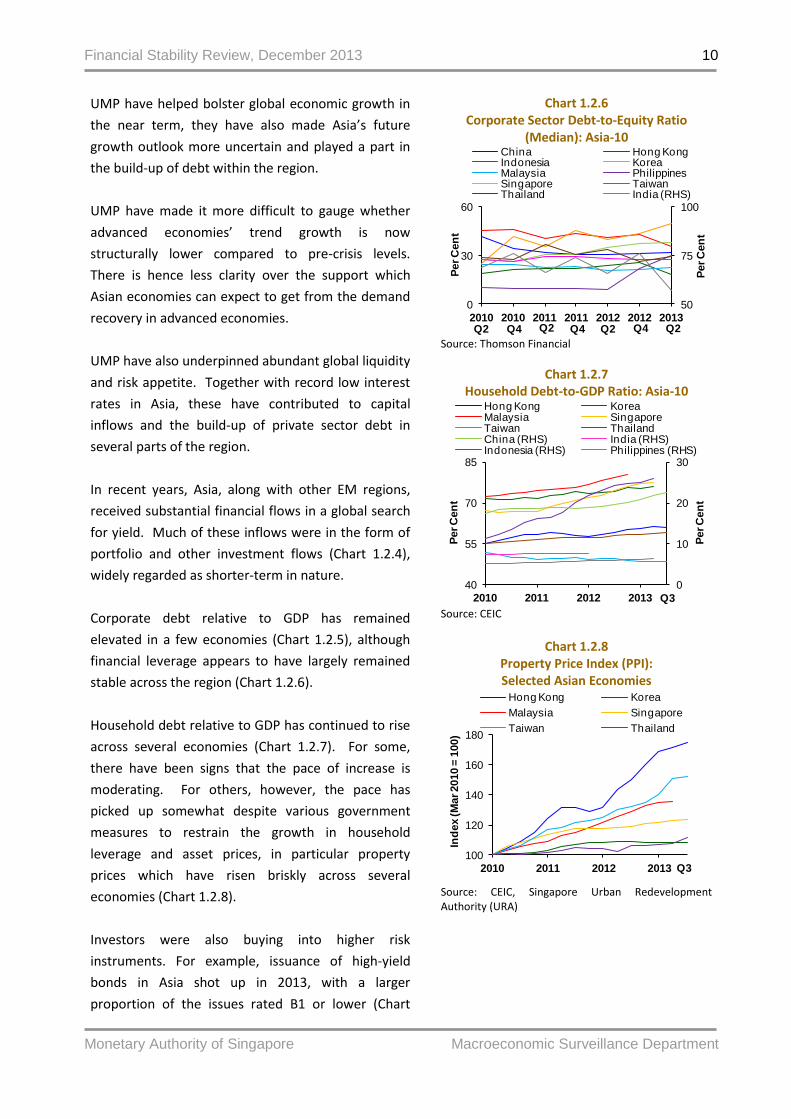

UMP have helped bolster global economic growth in

the near term, they have also made Asia’s future

growth outlook more uncertain and played a part in

the build-up of debt within the region.

UMP have made it more difficult to gauge whether

advanced economies’ trend growth is now

structurally lower compared to pre-crisis levels.

There is hence less clarity over the support which

Asian economies can expect to get from the demand

recovery in advanced economies.

UMP have also underpinned abundant global liquidity

and risk appetite. Together with record low interest

rates in Asia, these have contributed to capital

inflows and the build-up of private sector debt in

several parts of the region.

In recent years, Asia, along with other EM regions,

received substantial financial flows in a global search

for yield. Much of these inflows were in the form of

portfolio and other investment flows (Chart 1.2.4),

widely regarded as shorter-term in nature.

Corporate debt relative to GDP has remained

elevated in a few economies (Chart 1.2.5), although

financial leverage appears to have largely remained

stable across the region (Chart 1.2.6).

Household debt relative to GDP has continued to rise

across several economies (Chart 1.2.7). For some,

there have been signs that the pace of increase is

moderating. For others, however, the pace has

picked up somewhat despite various government

measures to restrain the growth in household

leverage and asset prices, in particular property

prices which have risen briskly across several

economies (Chart 1.2.8).

Investors were also buying into higher risk

instruments. For example, issuance of high-yield

bonds in Asia shot up in 2013, with a larger

proportion of the issues rated B1 or lower (Chart

Chart 1.2.6 Corporate Sector Debt-to-Equity Ratio

(Median): Asia-10

Source: Thomson Financial

Chart 1.2.7 Household Debt-to-GDP Ratio: Asia-10

Source: CEIC

Chart 1.2.8

Property Price Index (PPI): Selected Asian Economies

Source: CEIC, Singapore Urban Redevelopment Authority (URA)

50

75

100

0

30

60

2010 2010 2011 2011 2012 2012 2013

Per C

en

t

Per C

en

t

China Hong KongIndonesia KoreaMalaysia PhilippinesSingapore TaiwanThailand India (RHS)

Q2 Q4 Q2 Q4 Q2 Q4 Q2

0

10

20

30

40

55

70

85

2010 2011 2012 2013

Per C

en

t

Per C

en

t

Hong Kong KoreaMalaysia SingaporeTaiwan Thailand China (RHS) India (RHS)Indonesia (RHS) Philippines (RHS)

Q3

100

120

140

160

180

2010 2011 2012 2013

Ind

ex (M

ar 2010 =

100)

Hong Kong Korea

Malaysia Singapore

Taiwan Thailand

Q3

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

11

1.2.9). Further, Moody’s reported that many issuers

were able to refinance at lower rates (Chart 1.2.10)

Interest in Asian real estate investment trusts (REITs)

also grew, with the market capitalisation of Asian

REITs growing by 67% between 2010 and 2013 (Chart

1.2.11).

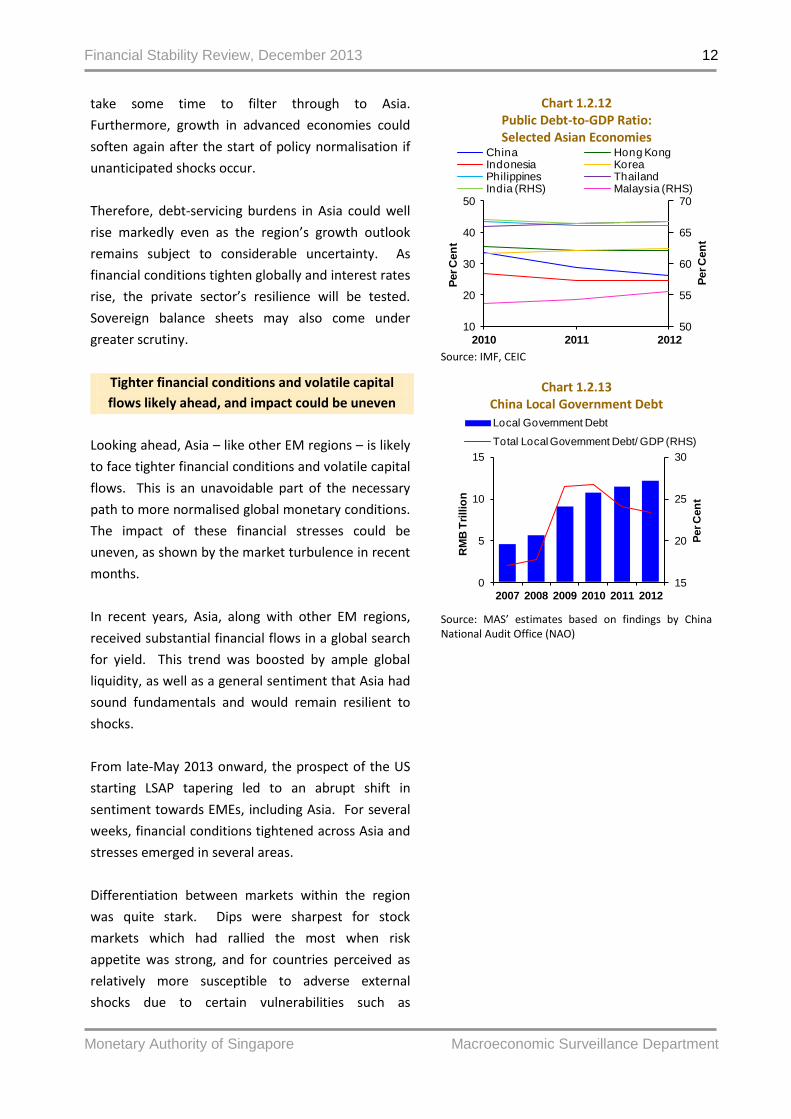

Meanwhile, some fiscal measures taken by

authorities to bolster growth are not without risks

Meanwhile, some fiscal measures taken by

authorities in different parts of Asia to bolster growth

and help lower-income groups are not without risks.

For example, some subsidies and assistance

programmes have contributed to increases in public

debts relative to GDP (Chart 1.2.12) but may not help

strengthen growth drivers in future. For China, while

central government finances appear sound,

estimates drawing from official sources indicate that

local government debt has more than doubled since

2007, rising to 23% of GDP (Chart 1.2.13).

The unusual combination of factors

making it possible for economic growth to hold up

and debt-servicing burdens to remain manageable

could soon change

The unusual combination of factors making it

possible for growth in Asia to hold up and debt-

servicing burdens to remain manageable could soon

change.

The US Federal Reserve plans to begin normalising its

monetary conditions when economic and financial

conditions justify such a move, through tapering its

LSAP. In the euro zone, while the ECB has committed

to keeping interest rates low for an extended period

of time, it could still raise rates earlier than expected

should the economic recovery there pick up speed.

While the start of policy normalisation is expected to

coincide with firmer growth recovery in the advanced

economies, the benefits of such a recovery would

Chart 1.2.9 Moody’s Rated Asian High-Yield Bond Issuance:

Ratings Composition

Source: Moody’s

Chart 1.2.10 Moody’s Rated Asian High-Yield Bond Issuance:

Weighted Average Coupons

Source: Moody’s

Chart 1.2.11

Market Capitalisation of Asian REITs

Source: Bloomberg

0

3

6

9

12

15

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2013Q1

2013Q3

US

$ B

illio

n

Ba1 Ba2 Ba3 B1 B2 B3 and below

48%rated in

B-

category

Oct

32%rated in

B-

category

43%rated in

B-

category

52%rated in

B-

category

0.0

2.5

5.0

7.5

10.0

12.5

0

5

10

15

20

25

2010 2011 2012 2013Oct

ytd

Per C

en

t / Y

ears

US

$ B

illio

nRated Bond IssuanceAverage Face AmountWeighted Average Coupon (RHS)Average Tenor (RHS)

0

30

60

90

2010 2011 2012 2013

US

$ B

illio

n

Sep

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

12

take some time to filter through to Asia.

Furthermore, growth in advanced economies could

soften again after the start of policy normalisation if

unanticipated shocks occur.

Therefore, debt-servicing burdens in Asia could well

rise markedly even as the region’s growth outlook

remains subject to considerable uncertainty. As

financial conditions tighten globally and interest rates

rise, the private sector’s resilience will be tested.

Sovereign balance sheets may also come under

greater scrutiny.

Tighter financial conditions and volatile capital

flows likely ahead, and impact could be uneven

Looking ahead, Asia – like other EM regions – is likely

to face tighter financial conditions and volatile capital

flows. This is an unavoidable part of the necessary

path to more normalised global monetary conditions.

The impact of these financial stresses could be

uneven, as shown by the market turbulence in recent

months.

In recent years, Asia, along with other EM regions,

received substantial financial flows in a global search

for yield. This trend was boosted by ample global

liquidity, as well as a general sentiment that Asia had

sound fundamentals and would remain resilient to

shocks.

From late-May 2013 onward, the prospect of the US

starting LSAP tapering led to an abrupt shift in

sentiment towards EMEs, including Asia. For several

weeks, financial conditions tightened across Asia and

stresses emerged in several areas.

Differentiation between markets within the region

was quite stark. Dips were sharpest for stock

markets which had rallied the most when risk

appetite was strong, and for countries perceived as

relatively more susceptible to adverse external

shocks due to certain vulnerabilities such as

Chart 1.2.12 Public Debt-to-GDP Ratio: Selected Asian Economies

Source: IMF, CEIC

Chart 1.2.13 China Local Government Debt

Source: MAS’ estimates based on findings by China National Audit Office (NAO)

50

55

60

65

70

10

20

30

40

50

2010 2011 2012

Per C

en

t

Per C

en

t

China Hong KongIndonesia KoreaPhilippines ThailandIndia (RHS) Malaysia (RHS)

15

20

25

30

0

5

10

15

2007 2008 2009 2010 2011 2012

Per C

en

t

RM

B T

rillio

n

Local Government Debt

Total Local Government Debt/ GDP (RHS)

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

13

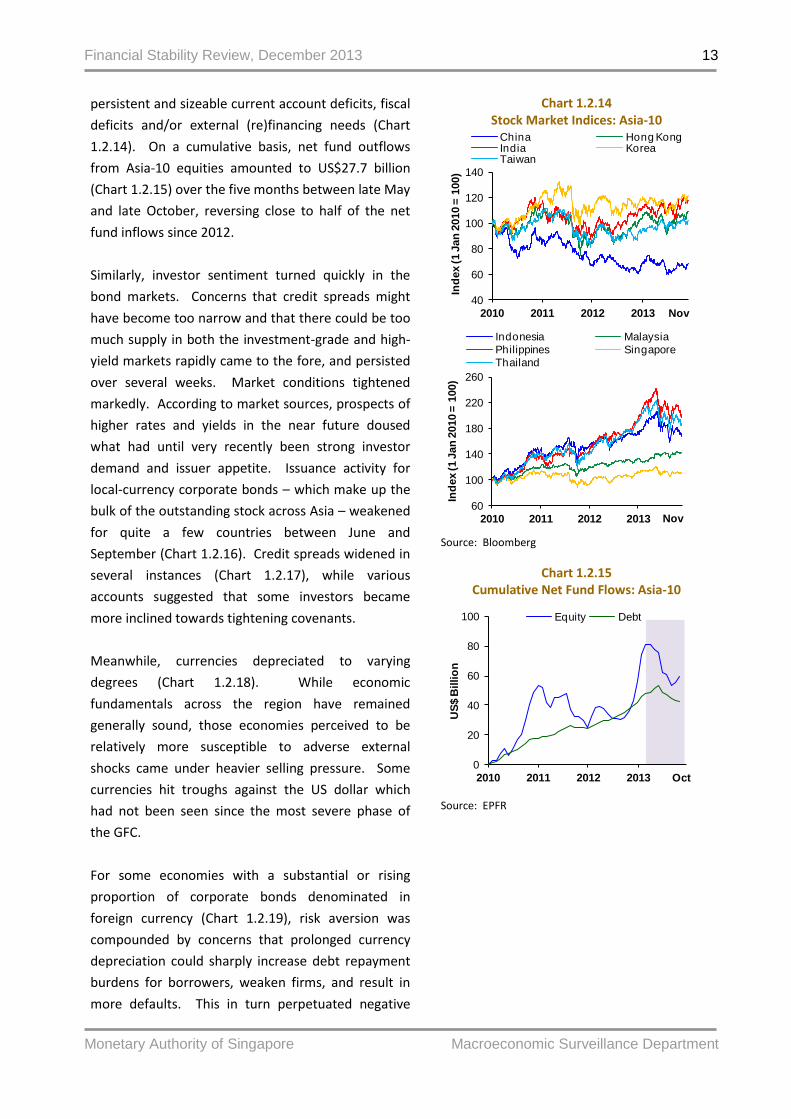

persistent and sizeable current account deficits, fiscal

deficits and/or external (re)financing needs (Chart

1.2.14). On a cumulative basis, net fund outflows

from Asia-10 equities amounted to US$27.7 billion

(Chart 1.2.15) over the five months between late May

and late October, reversing close to half of the net

fund inflows since 2012.

Similarly, investor sentiment turned quickly in the

bond markets. Concerns that credit spreads might

have become too narrow and that there could be too

much supply in both the investment-grade and high-

yield markets rapidly came to the fore, and persisted

over several weeks. Market conditions tightened

markedly. According to market sources, prospects of

higher rates and yields in the near future doused

what had until very recently been strong investor

demand and issuer appetite. Issuance activity for

local-currency corporate bonds – which make up the

bulk of the outstanding stock across Asia – weakened

for quite a few countries between June and

September (Chart 1.2.16). Credit spreads widened in

several instances (Chart 1.2.17), while various

accounts suggested that some investors became

more inclined towards tightening covenants.

Meanwhile, currencies depreciated to varying

degrees (Chart 1.2.18). While economic

fundamentals across the region have remained

generally sound, those economies perceived to be

relatively more susceptible to adverse external

shocks came under heavier selling pressure. Some

currencies hit troughs against the US dollar which

had not been seen since the most severe phase of

the GFC.

For some economies with a substantial or rising

proportion of corporate bonds denominated in

foreign currency (Chart 1.2.19), risk aversion was

compounded by concerns that prolonged currency

depreciation could sharply increase debt repayment

burdens for borrowers, weaken firms, and result in

more defaults. This in turn perpetuated negative

Chart 1.2.14 Stock Market Indices: Asia-10

Source: Bloomberg

Chart 1.2.15 Cumulative Net Fund Flows: Asia-10

Source: EPFR

40

60

80

100

120

140

2010 2011 2012 2013

Ind

ex (1 J

an

2010 =

100)

China Hong KongIndia KoreaTaiwan

Nov

60

100

140

180

220

260

2010 2011 2012 2013

Ind

ex (1 J

an

2010 =

100)

Indonesia Malaysia

Philippines Singapore

Thailand

Nov

0

20

40

60

80

100

2010 2011 2012 2013

US

$ B

illio

n

Equity Debt

Oct

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

14

sentiment and further weighed on financial

conditions.

The sovereign credit space was not immune. Asian

sovereign yields rose markedly (Chart 1.2.20), albeit

largely parallel to the rise in US Treasury rates. For

some countries, the magnitude of increases mirrored

the extent of yield tightening during the period of

strong capital inflows following advanced economies’

UMP. The reversal was notably sharp for countries

perceived to be relatively vulnerable to external

shocks. This was exacerbated by a sell-off of

domestic currencies by foreign investors who were

not fully hedged. Accordingly, foreign appetite for

Asian sovereign credit weakened significantly (Chart

1.2.21).

Bank credit conditions have remained resilient,

providing an important counterweight

to the recent financial market turbulence

An important counterweight to the recent turbulence

in financial markets is that bank credit conditions

have remained resilient.

For most Asian economies, loan growth has remained

buoyant in the double-digit range. This is despite

some moderation in recent months (Chart 1.2.22),

possibly due to concerns over imminent interest rate

increases amid still-uncertain economic conditions,

which have prompted firms and households to be

more cautious about taking on credit. Loan demand

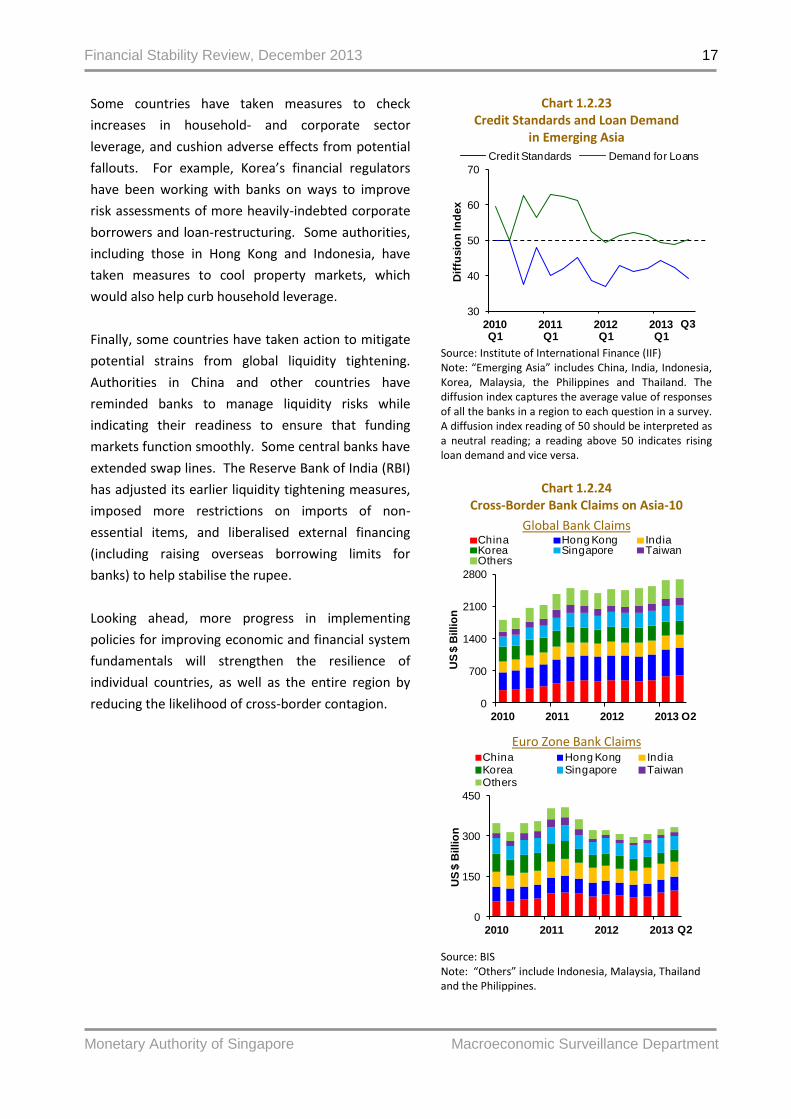

appears to be softening (Chart 1.2.23). In contrast,

Asian banks have not yet decisively tightened credit

and banks from outside Asia have continued to

increase their claims on Asia-10 moderately (Chart

1.2.24).

However bank credit conditions may become

less favourable in the period ahead

In the period ahead, several factors may make bank

credit conditions in Asia less favourable.

Chart 1.2.16 Local Currency Corporate Bond Issuance:

Selected Asian Economies

Source: Asian Development Bank (ADB) Asian Bonds Online

Chart 1.2.17

Corporate Bond Spreads: Asia-10

Source: JP Morgan Chase

0

40

80

120

0

10

20

30

2010 2011 2012 2013

US

$ B

illio

n

US

$ B

illio

n

Hong Kong IndonesiaMalaysia PhilippinesSingapore ThailandChina (RHS) Korea (RHS)

Sep

250

500

750

1000

1250

1500

100

200

300

400

500

600

2010 2011 2012 2013

Basis

Po

ints

Basis

Po

ints

Hong Kong India

Korea Taiwan

China (RHS)

Oct

250

500

750

1000

1250

1500

100

200

300

400

500

600

2010 2011 2012 2013

Basis

Po

ints

Basis

Po

ints

Malaysia Philippines

Singapore Thailand

Indonesia (RHS)

Oct

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

15

Credit quality deterioration has not materialised in a

broad-based manner so far, with notable increases in

banking-system non-performing loan (NPL) ratios

confined to India, Korea and the Philippines (Chart

1.2.25). However, some banks have reportedly

exercised greater “forbearance” towards certain

borrowers, in anticipation that an improvement in

economic conditions next year or a cyclical turn for

certain industries would enable these borrowers to

realise healthier incomes streams and repay their

loans.

In the meantime, some signs of strains have already

emerged in various sectors across different

economies. These range from small and medium-

sized enterprises (SMEs) in China, Korea and Malaysia

to utility firms and shipbuilders in Korea, as well as

borrowers from the aviation, textile and telecoms

industries in India.

Individually, some banks may have sizeable cross-

border exposures to borrowers whose capacities to

repay foreign currency-denominated debt have been

weakened by prolonged depreciation of their

domestic currencies.

In the coming months, alongside the possibility of

further increases in NPLs, funding conditions may

tighten for some banks as global financial conditions

change.

Furthermore, although foreign-currency loans

account for quite a small share of total loans for most

Asian banking systems, the corresponding loan-to-

deposit (LTD) ratios are quite high for several

economies (Chart 1.2.26). Banks in these economies

could come under foreign-currency funding pressure

if wholesale markets tighten alongside volatile capital

flows.

If global financial conditions tighten abruptly, and

especially if loan defaults rise, some Asian banks

could react by holding more liquid assets in the near

Chart 1.2.18 Currency Indices: Selected Asian Economies

Source: Bloomberg

Chart 1.2.19 Foreign Currency-Denominated Corporate

Bonds as a Share of Total Outstanding: Selected Asian Economies

Source: ADB Asian Bonds Online Chart 1.2.20

Sovereign Bond Yields: Asia-10

Source: Bloomberg

40

60

80

100

120

2008 2009 2010 2011 2012 2013

Ind

ex (1 J

an

2008 =

100)

India IndonesiaKorea MalaysiaPhilippines Thailand

Nov

0

20

40

60

80

2010 2011 2012 2013

Per C

en

t

China Hong KongIndonesia KoreaMalaysia PhilippinesSingapore Thailand

Q2

5

6

7

8

9

10

0.0

1.5

3.0

4.5

6.0

7.5

2010 2011 2012 2013

Per C

en

t

Per C

en

t

China Hong KongKorea TaiwanIndia (RHS)

Nov

0

4

8

12

0

2

4

6

2010 2011 2012 2013

Per C

en

t

Per C

en

t

Malaysia Singapore

Thailand Indonesia (RHS)

Philippines (RHS)

Nov

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

16

11

WMPs are typically short-term financial products marketed as high-yield alternatives to bank deposits in China. Banks issue the

majority of outstanding WMPs, though trust companies, insurers, brokerage firms and private equity funds are also issuers. Funds raised from WMPs are invested in a variety of assets including real estate loans and local government financing vehicle (LGFV) loans. WMPs pose potential maturity- and liquidity mismatch risks to banks (and other issuers) because investors may demand their monies quite soon whereas much of the proceeds which banks get from issuing these WMPs tends to be tied up in various illiquid longer-term assets.

term, reducing credit supply, setting more stringent

lending standards, and raising loan rates. This could

lead to a vicious cycle of worsening asset quality,

tightening credit conditions and slowing growth. The

impact could be compounded by a renewed

retraction of cross-border banking flows.

For the Chinese banks, authorities have

acknowledged that the increasing volume of wealth

management products (WMPs)11 offered by banks

poses some maturity- and liquidity mismatch risks.

Asia as a region is more resilient now

than during the Asian Financial Crisis,

but there is scope to reduce vulnerabilities further

Asia as a region is more resilient now than during the

AFC in the late 1990s.

Exchange rate regimes have become more flexible

over time. Reliance on foreign-currency external

borrowings has been reduced. International reserves

have been built up judiciously, so that coverage of

imports, for instance, has been maintained at

prudent levels (Chart 1.2.27).

Across the region, policies have become more

focused on reducing vulnerabilities to external

shocks. There has been greater emphasis on more

balanced growth, involving sustainable expansion of

domestic demand without straining public finances.

Several countries, including China, Korea, Malaysia

and Indonesia, have taken steps to make growth

drivers more broad-based, reduce fiscal- and current

account deficits or improve trade balances. China

has completed a comprehensive audit of local

government debt.

Chart 1.2.21

Share of Government Bonds Held by Foreigners: Selected Asian Economies

Source: ADB Asian Bonds Online

Chart 1.2.22 Loan Growth: Selected Asian Economies

Source: CEIC

0

10

20

30

40

2010 2011 2012 2013

Per C

en

t

Indonesia Korea

Malaysia Thailand

Sep

0

7

14

21

28

35

2010 2011 2012 2013

Yo

Y %

Gro

wth

China Hong KongIndia KoreaTaiwan

Sep

0

7

14

21

28

35

2010 2011 2012 2013

Yo

Y %

Gro

wth

Indonesia MalaysiaPhilippines SingaporeThailand

Sep

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

17

Some countries have taken measures to check

increases in household- and corporate sector

leverage, and cushion adverse effects from potential

fallouts. For example, Korea’s financial regulators

have been working with banks on ways to improve

risk assessments of more heavily-indebted corporate

borrowers and loan-restructuring. Some authorities,

including those in Hong Kong and Indonesia, have

taken measures to cool property markets, which

would also help curb household leverage.

Finally, some countries have taken action to mitigate

potential strains from global liquidity tightening.

Authorities in China and other countries have

reminded banks to manage liquidity risks while

indicating their readiness to ensure that funding

markets function smoothly. Some central banks have

extended swap lines. The Reserve Bank of India (RBI)

has adjusted its earlier liquidity tightening measures,

imposed more restrictions on imports of non-

essential items, and liberalised external financing

(including raising overseas borrowing limits for

banks) to help stabilise the rupee.

Looking ahead, more progress in implementing

policies for improving economic and financial system

fundamentals will strengthen the resilience of

individual countries, as well as the entire region by

reducing the likelihood of cross-border contagion.

Chart 1.2.23 Credit Standards and Loan Demand

in Emerging Asia

Source: Institute of International Finance (IIF) Note: “Emerging Asia” includes China, India, Indonesia, Korea, Malaysia, the Philippines and Thailand. The diffusion index captures the average value of responses of all the banks in a region to each question in a survey. A diffusion index reading of 50 should be interpreted as a neutral reading; a reading above 50 indicates rising loan demand and vice versa.

Chart 1.2.24

Cross-Border Bank Claims on Asia-10

Global Bank Claims

Euro Zone Bank Claims

Source: BIS Note: “Others” include Indonesia, Malaysia, Thailand and the Philippines.

30

40

50

60

70

2010 Q1

2011 Q1

2012Q1

2013 Q1

Dif

fusio

n In

dex

Credit Standards Demand for Loans

Q3

0

700

1400

2100

2800

2010 2011 2012 2013

US

$ B

illio

n

China Hong Kong IndiaKorea Singapore Taiwan Others

Q2

0

150

300

450

2010 2011 2012 2013

US

$ B

illio

n

China Hong Kong IndiaKorea Singapore TaiwanOthers

Q2

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

18

Chart 1.2.25 Non-Performing Loan (NPL) Ratios: Asia-10

Source: CEIC

Chart 1.2.27

International Reserves: Months of Import Cover: Selected Asian Economies

Source: IMF

Chart 1.2.26 Foreign-Currency Loan-to-Deposit Ratios and

Share of Total Loans Accounted for by Foreign-Currency Loans: Selected Asian Economies

Source: CEIC

-2

0

2

4

6

2010 2011 2012 2013

Per C

en

t

China Hong Kong IndiaIndonesia Korea MalaysiaPhilippines Singapore TaiwanThailand

Sep

0

5

10

15

20

25

Ch

ina

Ho

ng

Ko

ng

Ind

ia

Ind

on

esia

Ko

rea

Mala

ysia

Ph

ilip

pin

es

Sin

gap

ore

Th

ailan

d

Mo

nth

s

1997 2012

0

70

140

210

280

350

0 10 20 30 40 50

Fo

reig

n C

urr

en

cy

Lo

an

-to

-D

ep

osit

Rati

o (%

)

Foreign Currency Loans as % of Total Loans

Thailand

Malaysia

Taiwan

China

Korea

Indonesia

HongKong

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

19

Box B

Intermediating Banking Flows in Asia

Singapore hosts a rising amount of intra-region bank credit intermediation Singapore hosts a large number of banks for which cross-border credit intermediation has been a key activity.

Much of this activity is intra-Asia. Asia12 (excluding Singapore) is the source of about half of the cross-border

deposits and also the destination for the bulk of the cross-border loans (65% as of September 2013)

intermediated by banks in Singapore.

The nature of the risks which cross-border banking activity poses to Singapore’s banking system is changing as banks’ business models evolve Some banks’ business models have evolved over the past several years since the GFC. For example, before the

GFC, some banks tended to rely on interbank funding. Since the GFC, recurrent concerns over counterparty

credit risks have prompted some of these banks to depend more on cross-border intra-group funding to

underpin the expansion of their non-bank loans to the region. Further, UMP could have played a role in

keeping banking flows to Asia buoyant – with interest rates and yields kept low in advanced economies,

investors’ search for yield has centred on EMEs, including Asia.

With evolving business models, the nature of the risks that Singapore’s banking system faces from its cross-

border activities also changes over time. External shocks can be transmitted through several channels.

Firstly, adverse shocks which arise from or affect the home country of foreign banks in Singapore could lead to

cutbacks in head office funding, and therefore non-bank lending to Asian borrowers.

Secondly, cross-border banking activity may carry greater currency mismatch risk than intra-country lending.

Loans are more likely to be denominated in foreign currencies. Sharp or prolonged depreciation of domestic

currencies may weaken borrowers’ capacities to repay such foreign currency-denominated loans.

Thirdly, in the current environment where the US Federal Reserve is expected to start tapering its LSAP as a first

step to normalising monetary conditions, pronounced shifts in interest rate or yield gaps between the advanced

world and emerging Asia could lead to unexpectedly sharp changes in cross-border banking flows.

Banks based in Singapore have been lending more to China and India

Another significant trend is the growing importance of China and India as lending destinations for Singapore’s

banking system, even as they continue to provide material amounts of cross-border funding. The gross flows of

funds (both loans and deposits) post-Lehman between Singapore and China and between Singapore and India

have grown by 85% and 129% respectively, compared to pre-Lehman. However, a key difference is that China,

which was previously a net lender to Singapore, is now a net borrower from Singapore, whereas India has

remained a net borrower.

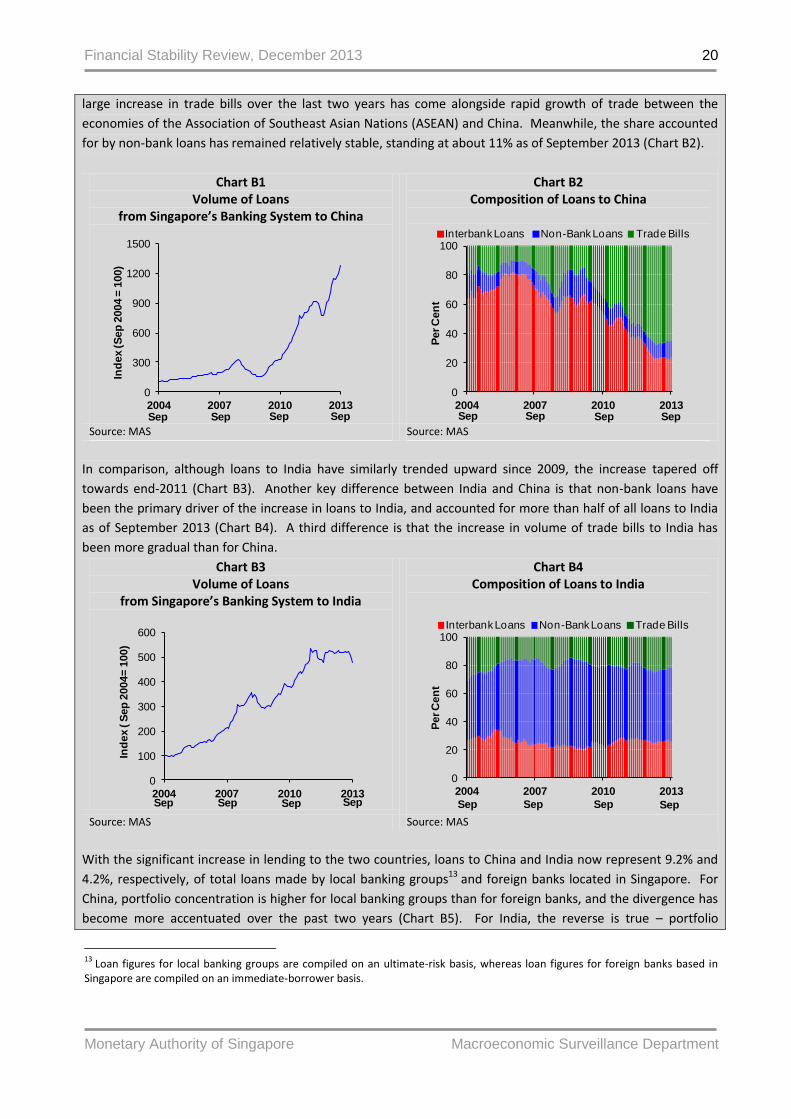

The total volume of loans (comprising interbank loans, non-bank loans and trade bills) to China has been

trending up since 2009 (Chart B1). During this period, the composition of loans has changed significantly. Since

August 2011, trade bills overtook interbank loans to become the primary contributor of loans to China. As of

September 2013, trade bills accounted for about 65% of total loans from Singapore to China (Chart B2). The

12

Asia includes Australia, Bangladesh, Brunei, Cambodia, China, Hong Kong, India, Indonesia, Japan, Korea, Laos, Macau, Malaysia, Myanmar, Nepal, Pakistan, the Philippines, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam and New Zealand.

Financial Stability Review, December 2013

Monetary Authority of Singapore Macroeconomic Surveillance Department

20

large increase in trade bills over the last two years has come alongside rapid growth of trade between the