Debt Liquidity Management Petroleum Trading Companies S2 15.00 - John Paul... · Debt Liquidity...

14

Debt Liquidity Management Petroleum Trading Companies Eurofinance Conference - Singapore May 2015

-

Upload

phungtuyen -

Category

Documents

-

view

217 -

download

2

Transcript of Debt Liquidity Management Petroleum Trading Companies S2 15.00 - John Paul... · Debt Liquidity...

Debt Liquidity Management Petroleum Trading Companies

Eurofinance Conference - Singapore

May 2015

AN INTRODUCTION TO SAHARA ENERGY RESOURCE LTD

2

Volumes in millions of metric tons oil equivalent (MMTOE) 2014 Products percentage split (in MMTOE)

CAGR 2009 to 2014: 22.1%

Key facts

Established 1996

Revenue 2014 $12.8 billion

Volumes 2014 109.4 million barrels

Number of banks 26

Credit line capacity $4.2 billion

Employees >150

Products Crude oil, naphtha, gasoline, gasoil,

Traded jet fuel, fuel oil, biofuel, bitumen & LPG

LOCAL KNOWLEDGE COUPLED WITH AN INTERNATIONAL PRESENCE

Singapore

Geneva, Switzerland

Dubai, UAE

Douglas, Isle of Man

HQ

Abuja, Nigeria

Abidjan, Ivory Coast

3

Geneva

(Trading & Centralized Risk Management)

Douglas

Isle of Man (Administrative)

Abuja, Nigeria

(Business Development)

Abidjan, Ivory Coast

(Logistical Support)

Dubai, UAE

(Trading & Business Development)

Singapore

(Trading & Business Development)

CRUDE OIL: AN IMBALANCED MARKET

Supply and demand are geographically mismatched

Source: BP statistical Review of World Energy, published in June 2014 4

CHALLENGING LOGISTICS

LPG (Butane & Propane) Light gasoline (naphtha) Heavy gasoline (super) Kerosene Gasoil-Diesel

Heating Oil

Heavy Fuels Bitumen

Crude Oil

boiler

Different crude oil grades do not necessarily match the requirements of local refineries

5

THE KEY ROLE PLAYED BY COMMODITY TRADERS

6

The trader superintends the processing, storage and transport of commodities

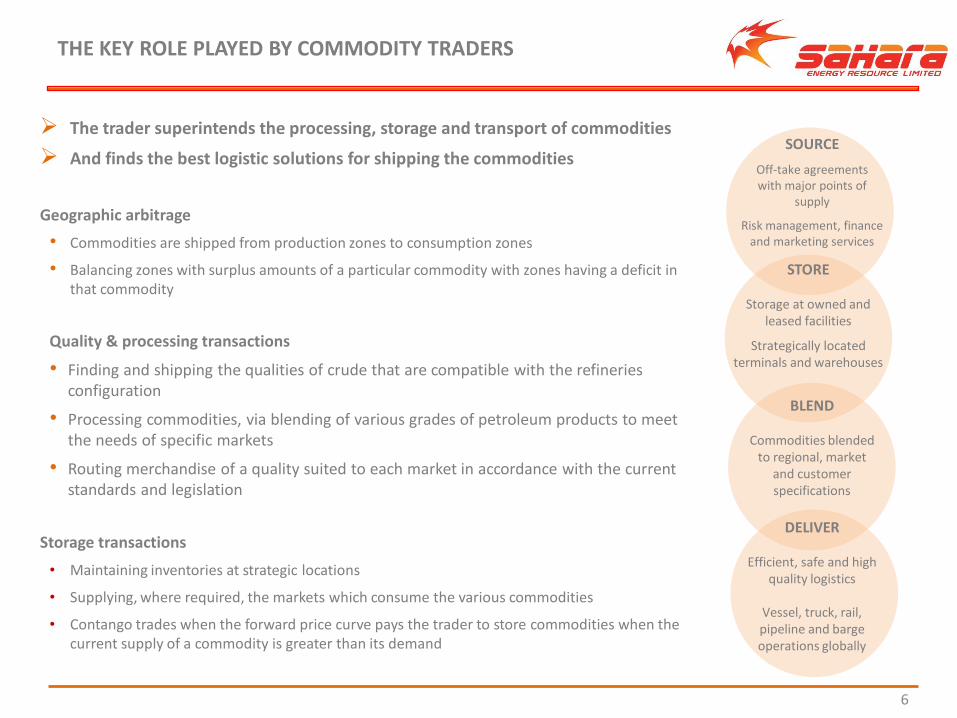

And finds the best logistic solutions for shipping the commodities

Geographic arbitrage

• Commodities are shipped from production zones to consumption zones

• Balancing zones with surplus amounts of a particular commodity with zones having a deficit in that commodity

Quality & processing transactions

• Finding and shipping the qualities of crude that are compatible with the refineries configuration

• Processing commodities, via blending of various grades of petroleum products to meet the needs of specific markets

• Routing merchandise of a quality suited to each market in accordance with the current standards and legislation

Storage transactions

• Maintaining inventories at strategic locations

• Supplying, where required, the markets which consume the various commodities

• Contango trades when the forward price curve pays the trader to store commodities when the current supply of a commodity is greater than its demand

SOURCE

Off-take agreements with major points of

supply

Risk management, finance and marketing services

STORE

Storage at owned and leased facilities

Strategically located terminals and warehouses

BLEND

Commodities blended to regional, market

and customer specifications

DELIVER

Efficient, safe and high quality logistics

Vessel, truck, rail, pipeline and barge operations globally

THE MANY PARAMETERS OF PETROLEUM TRADING

7

Negotiating the transaction

Product quality Delivery terms Incoterms Price formula Credit terms Logistics

Managing the risk

Futures Swaps Physical forwards

Risk monitoring Absolute price Quality differentials Inter-products Calendar spread Freight

How ? Brokers Exchanges Electronic trading Over the counter

Watching for opportunities

In regular contact with customers Prices and forward curves Shipping availability Logistics optimization Timing Market intelligence News - weather

COMMODITY TRADE FINANCE – MARKET STRUCTURE

8

Lender

Borrower Producer

Payer Off-taker

$ $

Producer Off-taker / end-

user Trader /

warehouse Processor

Goods

Purchase / Sale Contract

EXAMPLE BUY CRUDE + STORAGE + REFINED PRODUCT FINANCING FLOW

rki9

1) Lift 1.0 mln bbl cargo of crude Trader’s bank

issues L/C to Oil producer

Transit time 9 days

Transit time 14 days

Transit time 8 days

2) Offload 1.0 mln bbl cargo of crude Trader’s borrowing base finances the

storage

3) Trader sells a 1.0 mln bbl cargo of crude to a Indian

refinery, the refinery’s bank

issues an L/C to the Trader

4) Trader purchases 60K MT cargo of fuel oil from an Indian refinery

and sells it to an End user in Singapore who issues an L/C from its

bank to the Trader

EXAMPLE OF CONTAGO TRADE ARBITRAGE

10

Contango trade: purchase for immediate delivery at $60 per bbl + storage 6 months = sell forward at $66 per bbl, Secure profit margin $4 per bbl = $6 per bbl + blend crude grades of $2 per bbl – storage costs of $4 per bbl

Buy for immediate deliver 1 cargo crude oil (hedge – sell Dec futures contract)

Sell for future deliver 1 cargo crude oil (hedge - buy Jun futures contract)

INGREDIENTS FOR A SUCCESSFUL DEAL – THE TRADER

11

• Knowledgeable and influential in the trade

• Established relationship & track record with the produce / end-buyer

• Good shipping & trade finance team

• Robust and systematic risk management – hedge 100% of both flat price risk and basis risk

• Strong understanding of the end-buyers & utilisation

• Fungible commodity so alternative end-buyers available in case of need

• Acceptable collateral / security – such as assignment of receivables and or contracts, shipping docs, warehouse receipts, guarantees, insurance, charged accounts, claims on derivative hedges

• Reliable and honest

COMMODITY FINANCE –FINANCING TYPES

12

The purpose of these financing types and techniques is to provide solutions for all those involved in the commodity supply chain (oil producers, traders, terminal operators, refineries and end users)

• All financing products bilateral trade finance lines, borrowing bases, revolving credit facilities, term loans, reserve based lending (RBL – oil field financing) and pre-export financing (PXF – oil production)

• Risk hedging funding of initial margin and variation margin (commodity price, currency & interest rate risk)

• Arbitrage solutions geared to their needs, particularly in the emerging markets

The range of financial product solutions stretches from

• Short-term transactional finance (< 1 year)

• Commodity finance for companies active in trading of physical commodities

• Self-liquidating financing finance acquisition of the product (L/C + financing + hedging + storage + credit risk/performance risk)

To the medium and long term structured finance (2 to 10 years)

• Provided to oil producers, storage/pipeline operators and refinery companies for their growth and development projects (asset based term lending)

• Spans the entire range of medium and long-term structured finance for the energy and commodities

sector

BANKS BEHIND THESE FINANCINGS

13

From the historical perspective, commodity trading finance has largely been provided by European banks

• Which developed their expertise in transactional finance (in the 1970s)

• And applied this expertise to more structured types of financing (such as RBL…)

The North American banks play marginal role in this type of financing. Their focus has been on…

• Finance for the integrated oil majors on a corporate basis (ExxonMobil, Shell, BP, Total, Chevron, etc)

• Domestic US finance (fracking drillers/producers)

• Syndicates for structured transactions

The Asian and Middle Eastern banks historically focus on Intra-Asia/Intra-GCC financing for the needs of local clients but they are evolving quickly

Financing requirements are considerable (several billion each day)

Practically all of this financing is provided in USD

Worldwide Energy Trading (Isle of Man)

Thank you

![[Journal] the Effect of Debt, Firm Size and Liquidity on Investment](https://static.fdocuments.in/doc/165x107/577cc4d01a28aba7119a8653/journal-the-effect-of-debt-firm-size-and-liquidity-on-investment.jpg)