Dcaa 3rd annual conference presentation by duncan.turner

36

What Is and Isn’t “Reasonable” Compensation: Successful Approaches for Using Survey Data to Support Your Position American Conference Institute’s 3 rd DCAA Audit & Compliance Boot Camp

-

Upload

rachel-hamilton -

Category

Business

-

view

569 -

download

5

description

Transcript of Dcaa 3rd annual conference presentation by duncan.turner

What Is and Isn’t “Reasonable”

Compensation: Successful Approaches for

Using Survey Data to Support Your Position

American Conference Institute’s 3rd

DCAA Audit & Compliance Boot Camp

2

Introduction

Nancy Thorn Turner

Director, Ethics and Compliance

Orbital Sciences Corporation

Amber Duncan

Manager, Compensation Consulting

CBIZ Human Capital Services

Certified Compensation Professional (CCP)

3

Overview

• DCAA Compensation Methodology

• How to Support Reasonable Compensation

• Case Studies - Orbital and CBIZ Experience

• Conclusions

DCAA Compensation

Methodology

5

DCAA Methodology Based On:

• Federal Acquisition Regulation (FAR)

• DCAA Contract Audit Manual (CAM)

• Case Law – Armed Services Board of Contract Appeals

(ASBCA)

6

DCAA Compensation Methodology

• Reasonable executive compensation ranks third in terms

of questioned costs

7

Federal Acquisition Regulation (FAR)

• FAR 31.205-6, Compensation for Personal Services

– Must be for work performed in current year; no retroactive

adjustments

– Total compensation must be reasonable

– Consistent with established compensation plan or practices

– Otherwise allowable

• Amended June 26, 2013 – Cap now applies to ALL

employees, not just the top 5

– Costs incurred after January 1, 2012

– On contracts awarded after December 31, 2011

8

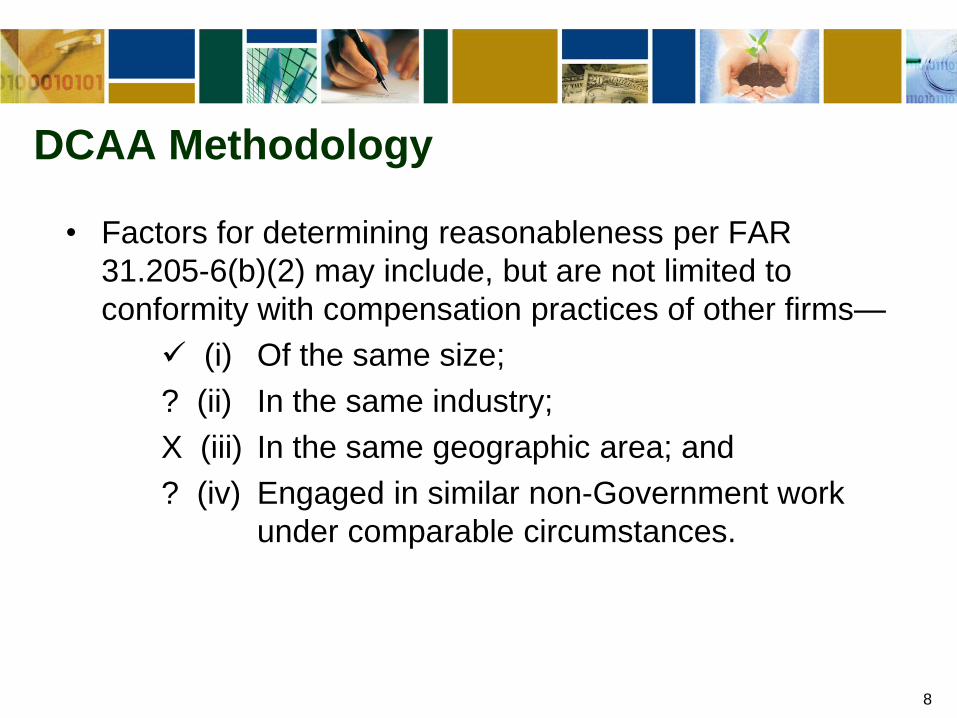

DCAA Methodology

• Factors for determining reasonableness per FAR

31.205-6(b)(2) may include, but are not limited to

conformity with compensation practices of other firms—

(i) Of the same size;

? (ii) In the same industry;

X (iii) In the same geographic area; and

? (iv) Engaged in similar non-Government work

under comparable circumstances.

9

DCAA Methodology – Case Law

• ASBCA No. 47849 – Information Systems & Network

Corporation

– Properly dated compensation data should be used

– No premium for owners performing multiple functions

– Company financial performance should be considered in

determining reasonable comp

– Compensation offsets should be considered

• ASBCA No. 41470, 45387, 45388 – Techplan Corporation

– No discount for owner-CEOs performing multiple functions

– Survey data should be for similarly sized companies

– Multiple survey sources should be used

– 10% ―range of reasonableness‖

10

DCAA Methodology – Case Law Recent

Developments

• ASBCA Nos. 56105 and 56322 – J.F. Taylor, Inc.

– ASBCA Rejected DCAA's Methodology for determining

reasonableness of executive compensation, citing that the DCAA

methodology was ――fatally flawed statistically and therefore

unreasonable.‖ Fatal flaws included:

• Ignoring dispersion of data and instead relying upon 10% range of

reasonableness

• Ignoring differences in survey response sizes

• Not initially considering financial performance

• Not considering any other drivers of compensation (security

clearances, customer satisfaction, etc.)

• Varying industry classification over 4-years in question

• Varying matches over same studies

11

DCAA Methodology – Case Law Recent

Developments – Fatal flaws included (continued):

• Relying upon different surveys each year

• Using median and average interchangeably from different surveys,

• Considered revenue responsibility of each person rather than

overall company

– Accepted opposing expert witness compensation methodology:

• 95% confidence range

• Weighting of surveys based upon number of respondents

12

DCAA Methodology – Case Law Recent

Developments • ASBCA No. 56624, 56751, and 56752 – Metron, Inc.

– Survey Data: ASBCA allowed Metron to rely upon one Radford Survey

rather than the DCAA’s multiple surveys that it found ―were not

sufficiently comprehensive, reliable, relevant to Metron's industry,

and/or the job matches were not sufficiently similar and representative

to warrant material reduction of the results obtained from use of the

Radford Survey data alone―

– Manipulation of Survey Data: ASBCA deemed the DCAA’s

manipulation of Radford survey data based upon prevalence of annual

incentives to be flawed

– Market Comparison Point: DCAA selected 66th and 41st percentile as

market comparison points on the basis of firm’s revenue compared to

peers only. ASBCA found methodology to calculate percentiles flawed.

Board also rejected the concept of assigning contractors a point on the

spectrum based on revenues and found Metron could pay above

average based upon required executive qualifications.

13

DCAA Methodology – Case Law Recent

Developments – Peer Group: ASBCA found peer group selected by DCAA to allow

―misleading comparisons with much larger companies with marke4ly

differing organizational and financial structures.‖

– Comparable Positions: DCAA matched Senior Engineers to mid-level

managers rather than Vice President level. Based upon review of

duties, ASBCA found to be a Vice-President or Top-level postion.

– Compensation Plans: Metron Case affirmed fact that compensation

plans and decisions should be documented in advance.

14

DCAA Mid-Atlantic Region Compensation

Review Process*

• Evaluate basis of contractor compensation

• Determine the position to be evaluated

• Identify appropriate surveys & positions

• Update surveys to appropriate date

• Identify and determine appropriate survey percentile

• Apply 10% Range of Reasonableness

• Adjust results for offsets as necessary

• Compare claimed comp to average of survey results

• Detailed review of contractor rebuttal

* DCAA Policy and Plans Directorate, April 2013

How to Support Reasonable

Compensation

16

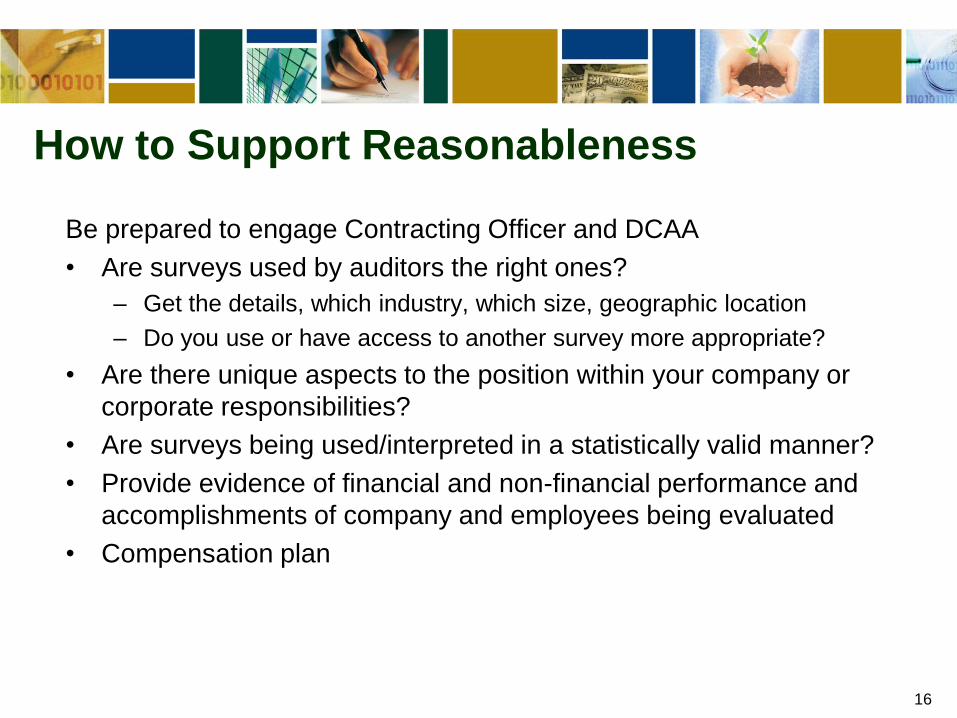

How to Support Reasonableness

Be prepared to engage Contracting Officer and DCAA

• Are surveys used by auditors the right ones?

– Get the details, which industry, which size, geographic location

– Do you use or have access to another survey more appropriate?

• Are there unique aspects to the position within your company or

corporate responsibilities?

• Are surveys being used/interpreted in a statistically valid manner?

• Provide evidence of financial and non-financial performance and

accomplishments of company and employees being evaluated

• Compensation plan

17

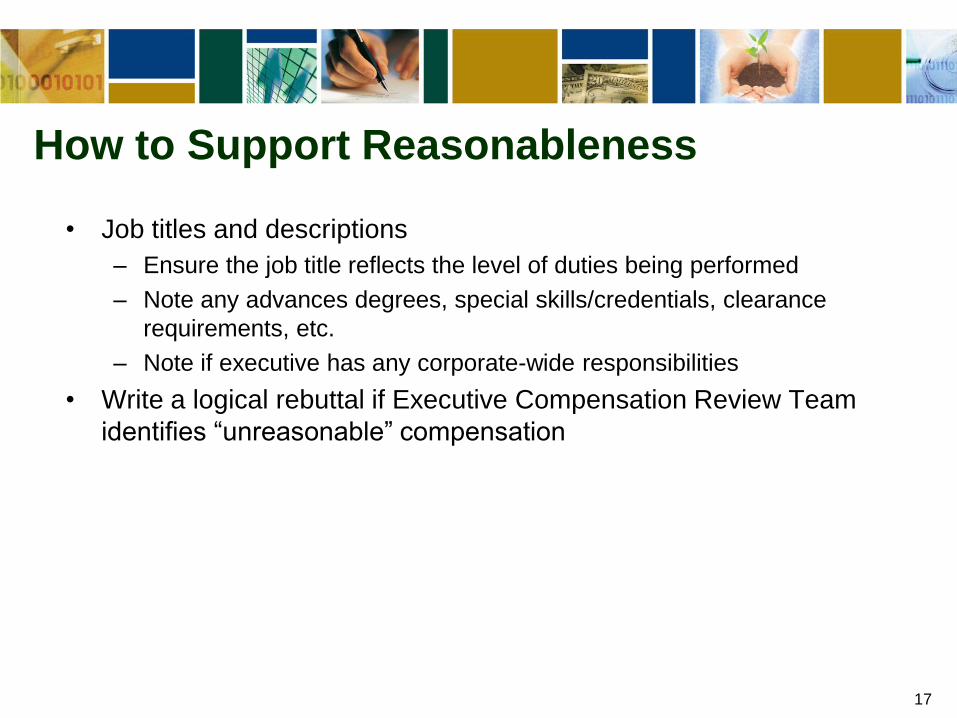

How to Support Reasonableness

• Job titles and descriptions

– Ensure the job title reflects the level of duties being performed

– Note any advances degrees, special skills/credentials, clearance

requirements, etc.

– Note if executive has any corporate-wide responsibilities

• Write a logical rebuttal if Executive Compensation Review Team

identifies ―unreasonable‖ compensation

Case Studies

19

DCAA Rebuttal Success - Example 1

20

Example 1 – Overview

• DCAA reviewed the compensation of the VP and Chief Scientist of a

division of a satellite manufacturer and found $89,500 of the total

cash compensation paid to the individual was unreasonable and

therefore unallowable.

• Matched to the 50th percentile in two surveys.

• Company was measured against the High Tech Manufacturing

Group, Manufacturing Durable Goods Group, Manufacturing All or

All Organizations in one survey (Mercer) and the Aerospace, Group,

High Technology Group or Durable Goods Manufacturing Group in

the other survey (Watson Wyatt). Which group was used depended

on the availability of data.

• It was not possible to discern which group was used for which

position.

21

Example 1 – DCAA Interaction

• Company argued the position was unique with responsibility for

large engineering function.

• Compared the position to VP of Chief Engineers position in a

different survey which focuses solely on High Tech Companies.

• Company argued that based on the unique position, financial and

technical performance of the division and company, and the

comparable industry, the comparison should be to the 75th

percentile.

• DCAA reviewed the rebuttal and found all compensation to be

allowable.

22

Example 1 – Lessons Learned

• 75th percentile compensation can be supported through

unique position, financial and technical performance of

the division and company

• Market matches and survey selection are up for

discussion

23

DCAA Rebuttal Success - Example 2

24

Example 2 – Overview

• The DCAA reviewed compensation at a small closely

held high-technology company and found maximum

allowable total cash compensation to be $263,151.

• Actual total cash compensation was $404,400.

• After reviewing DCAA results, CBIZ recognized that the

DCAA had matched the company’s CEO to a published

survey CEO and CTO, weighted 39% and 61%,

respectively, unfairly discounting the position.

• In addition, the DCAA compared this high-performing

company to a 50th percentile range of reasonableness.

25

Example 2 – DCAA Interaction

• CBIZ found maximum reasonable total compensation (including total

cash compensation, LTI, benefits and perquisites) to be $804,758,

for a difference of $541,607 from the DCAA allowable total cash

comp.

• The DCAA agreed to change market match to CEO and use 75th

percentile data as the market comparison point, but did not allow LTI

or geographic adjustment of the data. The DCAA also did not

consider perquisites or benefits.

• With the DCAA revisions, all actual compensation was found to be

allowable, saving the company nearly $150,000.

• CBIZ continues to provide client with pre-emptive compensation

studies.

26

Example 2 – Lessons Learned

• Pay close attention to how you title your executives.

• If performance can be proved to be at or above the 75th

percentile of an appropriate peer group, the DCAA may

allow a 75th percentile plus 10% range of

reasonableness.

27

DCAA Rebuttal Success – Example 3

28

Example 3 - Overview

• DCAA found reasonable total cash compensation to be

$680,551 for the 4-executive management team of this

high technology California company.

• Actual compensation was $968,945, for a total

questionable compensation expense of nearly $300,000.

• The executives were paid nearly identically (i.e. little

differentiation of pay by level).

• The DCAA used its standard median plus 10% range of

reasonableness and matched the positions to market

data based on title.

29

Example 3 – DCAA Interaction

• CBIZ demonstrated performance above the 75th percentile of peers

in key financial indicators listed in the CAM (revenue growth, net

income, return on shareholder’s equity, return on assets, return on

sales, earnings per share and return on capital).

• CBIZ argued the company’s positions titled CTO and Chief Business

Development Officer should be matched to a published survey COO

and Top Sales position, respectively.

• CBIZ determined maximum reasonable total compensation to be

$1,680,904, nearly $1 million above the DCAA total cash

compensation figure.

• The DCAA changed the matches and agreed to use 75th percentile

data, bringing DCAA total reasonable compensation to

approximately $930,000 and saving the company $250,000.

30

Example 3 – Lessons Learned

• Titles are key.

• Determine DCAA-acceptable financial performance

measures and peers in advance.

• If performance can be proved to be at or above the 75th

percentile of an appropriate peer group, the DCAA may

allow a 75th percentile plus 10% range of

reasonableness.

• While the DCAA allows offsets of compensation

components (i.e. benefits), high pay to one executive

and low to another cannot offset each other. Each

executive’s pay is reviewed individually.

31

DCAA Rebuttal Success - Example 4

32

Example 4 - Overview

• DCAA found reasonable compensation to be $466,402

for the company CEO and COO at this small high tech

government contractor.

• Actual total cash was $523,592.

• The DCAA used its standard median plus 10% range of

reasonableness.

33

Example 4 – DCAA Interaction

• Before hiring CBIZ, client tried to handle issue

themselves.

• DCAA’s questioned compensation increased based on

client arguments.

• CBIZ was able to prove performance above the 90th

percentile.

• CBIZ found maximum reasonable compensation (75th

percentile) to be $1,188,053.

• The DCAA agreed to revise its results by using 75th

percentile data saving the company $60,000.

34

Example 4 – Lessons Learned

• Determine DCAA-acceptable financial performance

measures and peers in advance.

• Always be courteous to our friends at the DCAA and

know rules before challenging.

35

Conclusions

• Compensation is a major focus of DCAA Audits

• Defining reasonable compensation is a multi-faceted

issue

• No way around caps

• Proactively document reasonable compensation and

allocations to contracts

– Purchase significant survey data; or

– Use outside compensation expertise

Questions?

Amber Duncan, CCP Nancy Thorn Turner

Manager, Compensation Director, Ethics and Compliance

CBIZ Human Capital Services Orbital Sciences Corporation

800-844-4510, ext. 295 or 703-404-7860

[email protected] [email protected]

36