Dbriefs Financial Reporting Series - IAS Plus · PDF file• Prospective for new or...

47

The Dbriefs Financial Reporting series presents: EITF Roundup: Highlights from the January Meeting Stuart Moss, Partner, Deloitte & Touche LLP Adrian Mills, Partner, Deloitte & Touche LLP Bryan Benjamin, Manager, Deloitte & Touche LLP Sean St. Germain, Senior Manager, Deloitte & Touche LLP January 28, 2013

Transcript of Dbriefs Financial Reporting Series - IAS Plus · PDF file• Prospective for new or...

The Dbriefs Financial Reporting series presents:

EITF Roundup: Highlights from the January Meeting Stuart Moss, Partner, Deloitte & Touche LLP Adrian Mills, Partner, Deloitte & Touche LLP Bryan Benjamin, Manager, Deloitte & Touche LLP Sean St. Germain, Senior Manager, Deloitte & Touche LLP January 28, 2013

Copyright © 2013 Deloitte Development LLC. All rights reserved.

11A CTA Upon Sale in a Foreign Entity

12D Joint and Several Liability

13A Benchmark Interest Rates

13C Unrecognized Tax Benefit Liability

12B Services Received from Affiliate

12H Service Concession Arrangements

12F Pushdown Accounting

Administrative matters

Question and answer

Agenda

Copyright © 2013 Deloitte Development LLC. All rights reserved.

This webcast does not provide official Deloitte & Touche LLP interpretive accounting guidance

Check with a qualified advisor before taking any action

See later slides for information on obtaining written summaries of issues discussed today

See FASB’s Web site for official minutes and ratified consensuses

Keep in mind

1

Copyright © 2013 Deloitte Development LLC. All rights reserved.

To enhance participants’ understanding of important accounting issues and developments pertaining to recent actions of the EITF

Learning objective

2

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Are you a financial statement preparer, user, auditor, or other interested party?

• Preparer • User • Auditor • Other

Poll question #1

EITF Developments

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background Issue 11-A: CTA upon sale in a foreign entity

Global Solar Panel, Inc. (USD reporting currency)

Foreign Entity in South America (Brazilian Real functional currency

with a CTA of 10)

Does the currency translation adjustment (CTA) attach here? • Follow ASC 830, Foreign

Currency Matters • No CTA release on disposal of

the manufacturing business (not a complete or substantially complete liquidation of the investment in the foreign entity)

Manufacturing business (CTA of 8)

Retail business (CTA of 2)

Or, does the CTA attach here? • Follow ASC 810, Consolidations • CTA of 8 is recognized in the gain

or loss on the disposal of the manufacturing business

Global Solar Panel, Inc. has sold its manufacturing business:

3

Copyright © 2013 Deloitte Development LLC. All rights reserved.

• Follow guidance in ASC 830-30 for sale of a subsidiary or group of net assets within a consolidated foreign entity

• Release entire balance of CTA upon losing a controlling financial interest in an investment in a consolidated foreign entity

• Release entire balance of CTA from an equity method investment in a foreign entity for a step acquisition

• Issue would not change requirement to release a pro-rata portion of CTA for a partial sale of an investment in an equity method investment

Final consensus Issue 11-A: CTA upon sale in a foreign entity

CTA attaches at the foreign entity level. Recycling of CTA depends on the derecognition of an investment in a foreign entity and

impacts the income statement 4

Copyright © 2013 Deloitte Development LLC. All rights reserved.

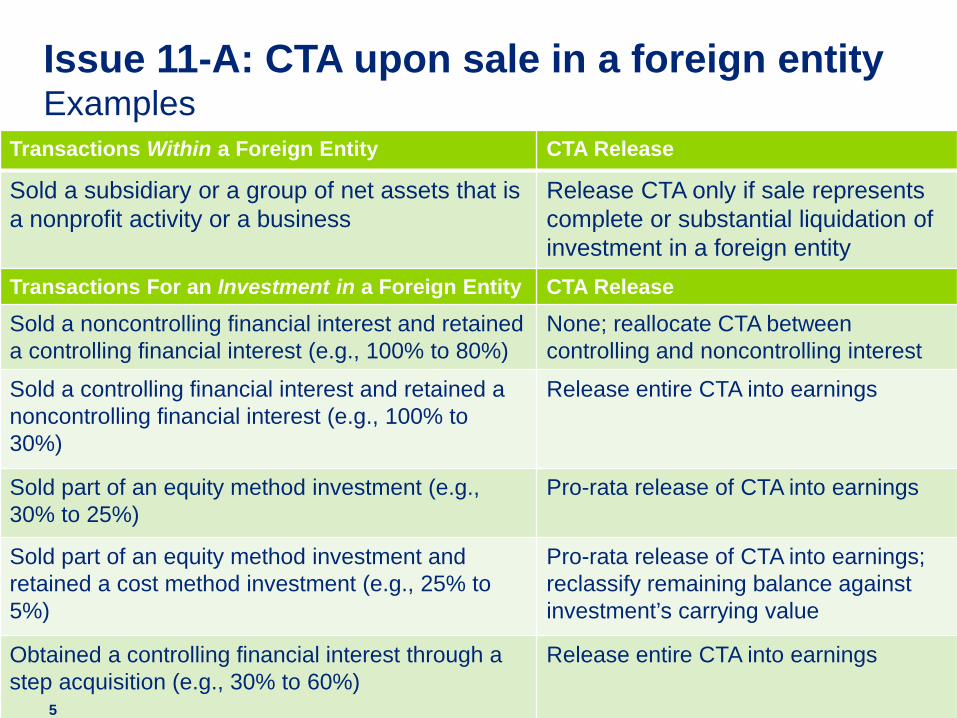

Examples Issue 11-A: CTA upon sale in a foreign entity

1

Transactions Within a Foreign Entity CTA Release

Sold a subsidiary or a group of net assets that is a nonprofit activity or a business

Release CTA only if sale represents complete or substantial liquidation of investment in a foreign entity

Transactions For an Investment in a Foreign Entity CTA Release

Sold a noncontrolling financial interest and retained a controlling financial interest (e.g., 100% to 80%)

None; reallocate CTA between controlling and noncontrolling interest

Sold a controlling financial interest and retained a noncontrolling financial interest (e.g., 100% to 30%)

Release entire CTA into earnings

Sold part of an equity method investment (e.g., 30% to 25%)

Pro-rata release of CTA into earnings

Sold part of an equity method investment and retained a cost method investment (e.g., 25% to 5%)

Pro-rata release of CTA into earnings; reclassify remaining balance against investment’s carrying value

Obtained a controlling financial interest through a step acquisition (e.g., 30% to 60%)

Release entire CTA into earnings

5

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Transition • Prospective from beginning of the fiscal year of adoption • Early adoption is permitted

Effective date • Public entities: fiscal years beginning on or after December

15, 2013 (and interim reporting periods therein) • Nonpublic entities: fiscal years beginning on or after

December 15, 2014 (and interim reporting periods therein)

Final consensus Issue 11-A: CTA upon sale in a foreign entity

6

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Will EITF Issue 11-A cause your organization to account for the release of CTA for transactions within a foreign entity and investments in a foreign entity differently than the organization’s past practice?

• Yes • No • Unsure

Poll question #2

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background Issue 12-D: Joint and several liability

Subsidiary A and B each: – Receive $100 in proceeds – Are joint and severally liable for

the full $200 obligation – Arrangement to each repay $100

Parent

Subsidiary A Subsidiary B

$100 $100

For standalone reporting of A and B: • Record the full $200

obligation? • Treat $200 obligation

as a guarantee arrangement and apply ASC 460?

• Treat $200 obligation as a contingent liability and record amount that is probable and can be reasonably estimated?

7

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Scope • All entities with a joint and several liability Recognition and measurement • Measure joint and several liability as amount agreed to

among co-obligors plus the amount an entity expects to pay on behalf of co-obligors

Final consensus Issue 12-D: Joint and several liability

Task Force removed guidance from consensus-for-exposure to apply ASC 460, Guarantees, when an entity’s

primary role is that of a guarantor 8

Copyright © 2013 Deloitte Development LLC. All rights reserved.

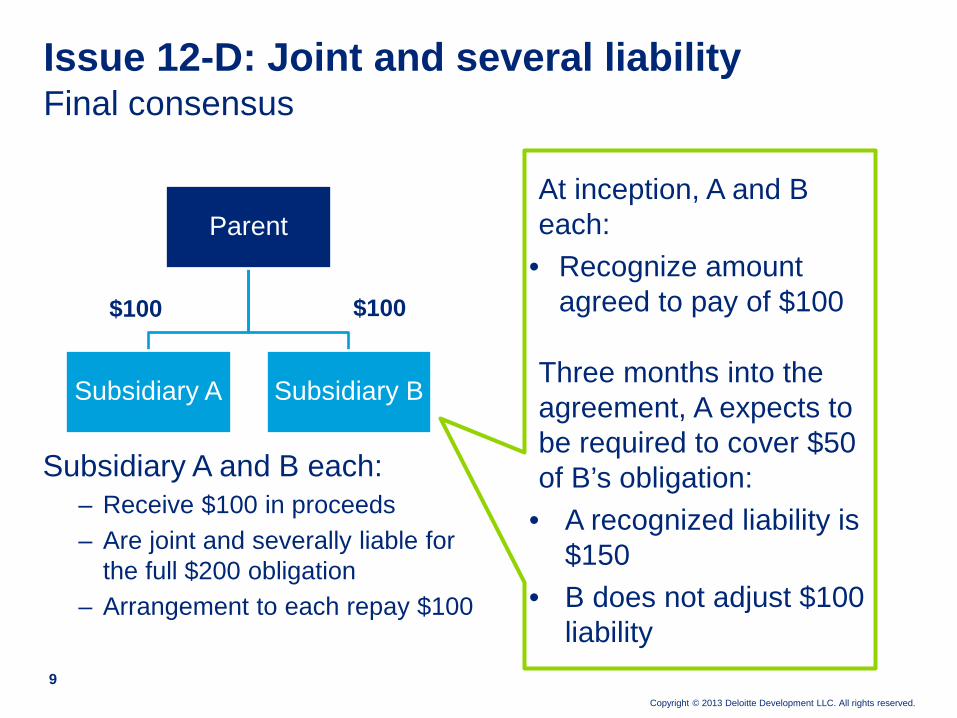

Final consensus Issue 12-D: Joint and several liability

Subsidiary A and B each: – Receive $100 in proceeds – Are joint and severally liable for

the full $200 obligation – Arrangement to each repay $100

Parent

Subsidiary A Subsidiary B

$100 $100

At inception, A and B each:

• Recognize amount agreed to pay of $100

Three months into the agreement, A expects to be required to cover $50 of B’s obligation:

• A recognized liability is $150

• B does not adjust $100 liability

9

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Disclosures (each liability or group of similar liabilities) • Information about the obligation’s nature (i.e., how it

originated, term, expected timing of settlement) • Total amount of the outstanding obligation for all entities

participating in the arrangement (excluding any possible recoveries from other entities)

• Carrying amounts of the obligation and any related receivable

• Information about the entity’s recourse provisions • The offsetting entry when the obligation is initially

recognized and measured or the measurement significantly changes

Final consensus Issue 12-D: Joint and several liability

10

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Transition • Modified retrospective approach (apply issue

retrospectively to obligations that exist at the beginning of the fiscal year of adoption)

• Early adoption is permitted

Effective date • Public entities: fiscal years beginning on or after December

15, 2013 (and interim reporting periods therein) • Nonpublic entities: fiscal years ending on or after December

15, 2014 (and interim and annual reporting period thereafter)

Final consensus Issue 12-D: Joint and several liability

11

Copyright © 2013 Deloitte Development LLC. All rights reserved.

True or False. According the EITF’s final consensus, each entity that is a co-obligor in an arrangement with joint and several liability should always record the entire amount of the joint obligation in its standalone financial statements.

• True • False

Poll question #3

Copyright © 2013 Deloitte Development LLC. All rights reserved.

• ASC 815 provides guidance on the benchmark interest rate risks that are permitted to be hedged

“…widely recognized and quoted rate in an active financial market that is broadly indicative of the overall level of interest rates attributable to high-credit-quality obligors in that market. . . . In theory, the benchmark interest rate should be a risk-free rate (that is, has no risk of default).”

• Entities may hedge only the benchmark component (e.g., LIBOR)

• Demand for fed funds-based products has grown due to increased volatility and the widening of the spread between LIBOR and OIS

Background Issue 13-A: Benchmark interest rates

Liquidity Duration

Credit

LIBOR

Borrowing Rate

12

Copyright © 2013 Deloitte Development LLC. All rights reserved.

• Treasury departments are concerned with managing the risk in the overnight rate

• Current U.S. benchmark interest rates remain: 1. U.S. Treasuries 2. LIBOR

• Federal Funds Effective Swap Rate would also be an acceptable benchmark interest rate in the United States

Consensus-for-exposure Issue 13-A: Benchmark interest rates

Interest rate swap

Company X

Periodic settlements based on an agreed

upon notional and fixed interest versus Fed Funds Effective rate

FF Fixed

Big Bank

13

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Transition and effective date • Prospective for new or designated hedges entered into on or

after adoption date • Early adoption would be permitted • Effective date to be determined at a future meeting

Consensus-for-exposure Issue 13-A: Benchmark interest rates

14

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background Issue 13-C: Unrecognized tax benefit liability

Balance Sheet Gross Net

Deferred Tax Assets 1,000 500

Other Assets 20,000 20,000

Total Assets 21,000 20,500

UTB Liability 500 -

Other Liabilities 14,000 14,000

Total Liabilities 14,500 14,000

Total Equity 6,500 6,500

Total Liabilities and Equity 21,000 20,500

Diversity in Practice

Currently entities present an unrecognized tax benefit (UTB) liability net of a net operating loss (NOL) or tax credit carryforward either when:

• The uncertain tax position would, or is available to, reduce the NOL or tax credit carryforward under the provisions of the tax law; or

• The UTB is directly associated with a tax position taken in a tax year that resulted in the recognition of a NOL carryforward for that year 15

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Presentation • A UTB should be presented as a reduction of a deferred tax

asset for a NOL or tax credit carryforward (rather than as a liability) when the uncertain tax position would, or is available to, reduce the NOL or tax credit carryforward under the provisions of the tax law

Consensus-for-exposure Issue 13-C: Unrecognized tax benefit liability

At the balance sheet date, if the taxing authority were to disallow an uncertain tax position (for which a UTB was recognized), does tax law allow an entity to offset the

taxable amount against an NOL, tax credit carryforward, or amount refundable in the tax return or is cash settlement

required? 16

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Transition and effective date • Retrospective to all prior periods presented • Early adoption would be permitted • Effective date to be determined at a future meeting

Consensus-for-exposure Issue 13-C: Unrecognized tax benefit liability

17

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Do you agree with the proposed transition method for EITF Issue 13-C to be applied retrospectively to all prior periods?

• Yes • No • Unsure

Poll question #4

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background Issue 12-B: Services received from an affiliate

Recipient NFP in Standalone F/S

ASC 958 requires the recipient NFP to recognize the contributed services at fair value when the following criteria are met:

• Services are regularly performed and provided by a separately governed affiliate under direction of recipient NFP; and

• Create or enhance a nonfinancial asset, or

• Require specialized skills that the NFP would otherwise need to purchase

A not for profit (NFP) entity may receive various types of services from employees of an affiliated entity under common control

Lega

l

18

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Issue • How should a NFP recognize and measure the receipt of

services from an affiliate under common control (for which the affiliate does charge for reimbursement of its costs) in its standalone financial statements?

Recognition and measurement • Recognize all personnel services that directly benefit

recipient NFP including certain "shared" personnel service • Measure personnel services at the actual direct costs

incurred by the affiliate (e.g., employee's direct compensation and benefits)

No final consensus reached (tentative decision made) Issue 12-B: Services received from an affiliate

19

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Presentation within statement of changes in net assets • If a performance indicator is presented, exclude from the

performance indicator (i.e., present as an equity transfer) • If a performance indicator is not presented, presentation

guidance would not be prescribed (contra expense not allowed)

Transition and effective date • Prospective with option to apply using a modified

retrospective approach • Early adoption would be permitted • Effective date to be determined at a future meeting

No final consensus reached (tentative decision made) Issue 12-B: Services received from an affiliate

20

Copyright © 2013 Deloitte Development LLC. All rights reserved.

FASB Staff performing additional research on the following questions: • Should personnel services contributed by certain affiliated

for-profit entities or individual donors be excluded from the Issue’s scope?

• Should the Issue’s recognition guidance be limited to the type of contributed services currently evaluated for recognition under ASC 958-605?

No final consensus reached (tentative decision made) Issue 12-B: Services received from an affiliate

21

Copyright © 2013 Deloitte Development LLC. All rights reserved.

• A private-sector entity (“operating entity”) pays a city-government (“grantor”) $100 million for the right to operate the city’s toll roads for the next 20-years

• The operating entity keeps all tolls collected (estimated $200 million)

• The grantor maintains the right to regulate the toll fees, provides certain other performance conditions, and maintains ownership of the toll roll during the entire contract period

Background Issue 12-H: Service concession arrangements

What accounting guidance should be applied to this transaction?

22

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Accounting guidance • U.S. GAAP does not specifically address the accounting for

service concession contracts (IFRS does) • Some operating entities account for these contracts as

leases (ASC 840) • Some operating entities account for these contracts as

intangible assets, financial assets, or both (in a manner similar to IFRS guidance)

Service concession contracts • Public-sector entities enter into contracts with private-sector

entities to operate (may also construct or maintain) its infrastructure that is used to provide public services

Background Issue 12-H: Service concession arrangements

23

Copyright © 2013 Deloitte Development LLC. All rights reserved.

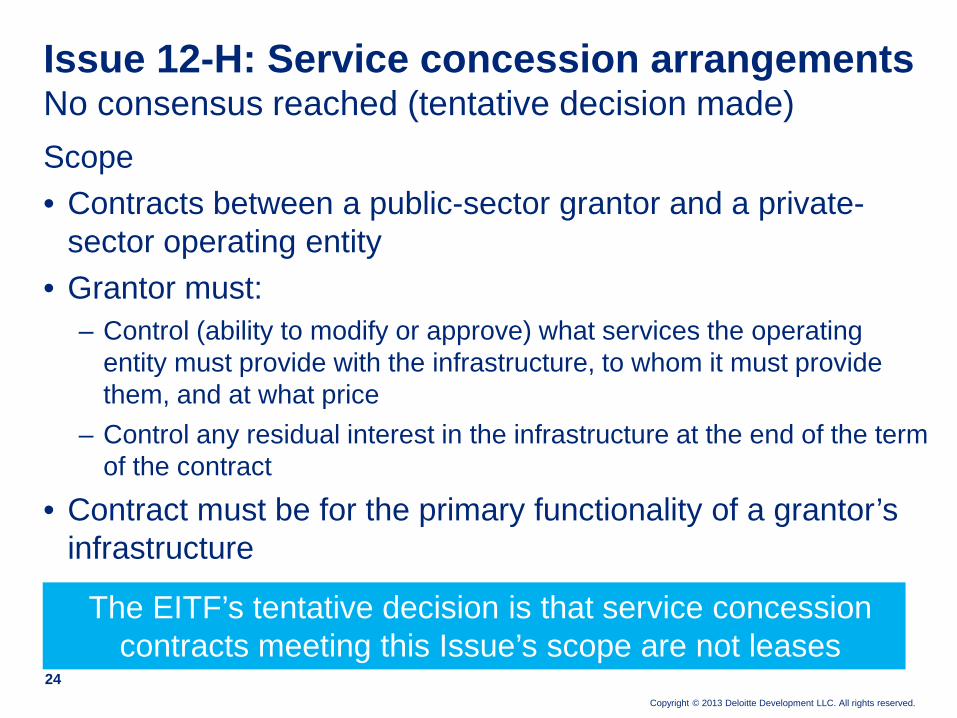

Scope • Contracts between a public-sector grantor and a private-

sector operating entity • Grantor must:

– Control (ability to modify or approve) what services the operating entity must provide with the infrastructure, to whom it must provide them, and at what price

– Control any residual interest in the infrastructure at the end of the term of the contract

• Contract must be for the primary functionality of a grantor’s infrastructure

No consensus reached (tentative decision made) Issue 12-H: Service concession arrangements

The EITF’s tentative decision is that service concession contracts meeting this Issue’s scope are not leases

24

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Recognition and measurement • Operating entity should account for its rights as:

– a financial asset for any unconditional contractual right to receive a specified or determinable amount of cash (or another financial asset) from the public-sector entity

– an intangible asset for any conditional rights to future cash flows based on usage by a third party

– a combination of a financial asset and an intangible asset

Transition and effective date • To be discussed at a future meeting

No consensus reached (tentative decision made) Issue 12-H: Service concession arrangements

25

Copyright © 2013 Deloitte Development LLC. All rights reserved.

• A operating entity pays a city-government $100 million for the right to operate the city’s toll roads for the next 20-years

• The operating entity keeps all tolls collected (estimated $200 million) and $60 million in tolls revenue is guaranteed by the grantor at $3 million each year (i.e., the grantor covers any toll short-falls)

• Tentative “combination” model for $100 million payment (ignoring time value of money) – $60 million financial asset – $40 million intangible asset – Subsequently measure each asset based on current U.S. GAAP

Example Issue 12-H: Service concession arrangements

26

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Do you think that the EITF should limit the personnel services received from an affiliate to only those services that meet the current contributed services guidance (instead of all personnel services that directly benefit recipient NFP)?

• Yes • No • Unsure

Poll question #5

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background Issue 12-F: Pushdown accounting

There is limited U.S. GAAP on pushdown accounting. SEC guidance applicable for SEC registrants is summarized below.

Acquire less than 80% of an

entity

Acquire 95% or more of an

entity

Acquire 80% to 95% of an

entity

Pushdown accounting is prohibited

Pushdown accounting is permitted

Pushdown accounting is required

27

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Task Force deliberated three alternatives for when an acquiring entity should “push down” the new accounting basis to an acquired entity’s standalone financial statements: • When “substantially all” of the controlling financial interests

are acquired • When an acquiring entity obtains control and consolidates

the acquired entity in accordance with ASC 810 • A new basis should not be established in an acquired entity's

standalone financial statements due to a change in its ownership

No consensus reached Issue 12-F: Pushdown accounting

FASB Staff to perform additional outreach on each of these three alternatives and applicability for nonpublic

entities 28

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Which alternative that the EITF is considering in Issue 12-F do you primarily support? That is, do you believe an acquiring entity should “push down” the new accounting basis to an acquired entity’s standalone financial statements when…

• “Substantially all” of the controlling financial interests are acquired

• An acquiring entity obtains control and consolidates the acquired entity in accordance with ASC 810

• A new basis should not be established in an acquired entity's standalone financial statements due to a change in its ownership

• Unsure

Poll question #6

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Ratification of EITF Issues considered during January 31, 2013 FASB meeting Next EITF meeting is March 14, 2013. Potential agenda includes: • Issue 12-B, Services received from an affiliate • Issue 12-F, Pushdown accounting • Issue 12-G, Consolidating a CFE • Issue 12-H, Service concession arrangements • New agenda topic

− Issue 13-B, Investments in Tax Credits (added December 2012)

EITF administrative matters

29

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Background • Low-Income Housing Tax Credit (LIHTC) provides tax credit

benefits to owners of entity owning qualifying property • Generally entities account for these investments as equity

method investments – Investment performance and tax benefits presented “gross”

• Some entities meet scope of ASC 323-740 and account for these investments under the effective yield method – Investment performance and tax benefits presented “net”

Scope • FASB Chairman limited Issue’s scope to the current scope in

ASC 323-740 for LIHTC investments

New issue overview Issue 13-B: Investments in tax credits

30

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Does your organization invest in tax credit programs, such as the LIHTC or other similar tax credit programs?

• Yes • No • Unsure

Poll question #7

Question and answer

Join us February 20 at 2 PM ET as our Financial Reporting series presents: Accounting for Financial Instruments: A Comprehensive Update on the Joint Project

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Eligible viewers may now download CPE certificates.

Click the CPE icon in the dock at the bottom of your screen.

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Contact info

Bryan Benjamin [email protected] Adrian Mills [email protected] Stuart Moss [email protected] Sean St. Germain [email protected]

Copyright © 2013 Deloitte Development LLC. All rights reserved.

CFE: Collateralized Financing Entity CTA: Currency Translation Adjustment FF: Federal Funds Effective Swap Rate IFRS: International Financial Reporting Standards LIBOR: London Interbank Offered Rate LIHTC: Low-Income Housing Tax Credit NFP: Not For Profit NOL: Net Operating Loss OIS: Overnight Index Swap UTB: Unrecognized Tax Benefit

Acronyms used in presentation

Copyright © 2013 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright © 2013 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited