Day 1 C2C - Deloitte - Government Support for ICT Development, Success strategies

16

Headline Verdana Bold Government Support for ICT Development, Success Strategies Connect 2 Connect 2016, Pretoria, South Africa Sharoda Rapeti 19 July 2016

-

Upload

myles-freedman -

Category

Technology

-

view

153 -

download

0

Transcript of Day 1 C2C - Deloitte - Government Support for ICT Development, Success strategies

Headline Verdana BoldGovernment Support for ICT Development, Success Strategies Connect 2 Connect 2016, Pretoria, South AfricaSharoda Rapeti19 July 2016

What my presentation will cover

WHATis the role of Government to advance ICT development and grow country competitiveness?

1WHATare the positive & negative implications of Government actions/ lag in actions to enable and grow the ICT industry?

2

HOWdoes the ICT industry contribute to GDP?

3CASESTUDIES4

Factors that play a major role in shaping and enabling the strength of the ICT industry

Inter-Government support

• Tax incentives • Ability to attract FDI• Co-development of policies e.g. M2M, security

etc• Digital Government • Creation of SEZs, IDZs• Immigration • Drive IoT solutions across Smart Cities based

programmes e.g. transport, safety, education, housing, health etc

Legal and Regulatory

• Access to spectrum• Competitive industry• Avoid duplicate

infrastructure investment • Pricing • Network security, Data

Security and Privacy • Labour legislation

Infrastructure

• Spectrum• Open Access Networks • Metro, Provincial, National and

International Infrastructure • Cost of Infrastructure • Non-telco infrastructure e.g.

electricity, housing, roads, airports

• Broadband Network Ownership model

Government Support (ICT)

• Political and economic stability

• Development of policies• R&D spend• Digital Government • Network security, Data

Security and Privacy • Job creation in primary and

secondary industries

Future Talent Pool

• Forecast and develop skills to support the 4th

Industrial Revolution/ (digital disruptors) requirements

• Understand trends of Millennials in the workplace • Establish skills base of legacy skillsets and

demographic of skills base• Innovation demands new, rare skills e.g. user

experience design, security, IoT/M2M, cloud, AI and data analytics

Cost of Telecommunications

• Cost of local and global connectivity

• Cost of data / IP based services

2

o The South African BPO industry accounted for 1% of the global BPO revenue

in 2014

o Revenues from South African BPOs is forecast to account for 4% of the global

revenue by 20301

o The number of jobs in South Africa to serve global clients increased by 23%,

from 21,700 in 2014 to 26,700 in 2015

o The most sought after service is from the Financial Services Industry vertical

i.e. finance, actuarial science and accounting skill sets accounting for ~50% of

the market

o The South African BPO industry contributes ~R50m to the national GDP p/a and employs

~ 215,000 people4

o Three South African cities feature in the Top 100 outsourcing destinations3:

• Johannesburg #20

• Cape Town #56

• Durban #100

South Africa has been able to position itself as an emerging offshoring destination

Cost vs Maturity (sized by labour pool)2

Maturity

Lab

ou

rcost

rati

o (

US

= 1

00

)

1. Source: Deloitte Cost Competitiveness – no longer the only differentiator for the BPO industry – July 2016, 2. Source: Gartner (February 2016), 3. Source: Mckinsey Study – South Africa’s big five bold priorities for inclusive growth 4. Source: Business Process Enabling South Africa (BPeSA)

KEY HIGHLIGHTS1

South Africa is categorised as a Primary

Outsourcing Location (overall value, cost and risk)

Russia, Belarus and Egypt offer lower rates, but

present higher risks for Intellectual Property

protection, legal maturity, security and ease of doing

business

South Africa and Egypt excel at BPO services

particularly in Call Centres

Russia and Belarus specialise in software development

and Poland, Hungary, the Czech Republic, Bulgaria and

Romania are well suited for Multifunction Delivery

Centres.

3

Lan

gu

ag

e

Govern

men

tS

up

port

Lab

ou

rP

ool

In

frastr

uctu

re

Ed

ucati

on

al

Syste

m

Cost

Poli

tical

&Econ

om

ic

En

vir

on

men

t

Cu

ltu

ral

Com

pati

bil

ity

APAC Region

China 5 7 5 7 6 7 6 5

India 8 9 9 5 7 8 8 7

Malaysia 8 7 6 7 6 7 6 6

Sri Lanka 6 6 4 4 5 7 5 5

Vietnam 5 5 6 5 5 8 5 5

Americas Region

Argentina 6 3 3 5 6 8 3 6

Chile 4 7 3 6 6 7 7 7

Colombia 5 7 4 6 4 7 6 7

Costa Rica 6 7 5 5 5 8 8 7

Mexico 6 7 7 6 4 6 6 8

Glo

bal

an

d L

eg

al

Matu

rit

y

4

5

6

5

4

3

7

6

5

7

Data

/ I

P S

ecu

rit

y a

nd

P

riv

acy

3

5

6

4

2

4

4

4

4

4

Lan

gu

ag

e

Govern

men

tS

up

port

Lab

ou

rP

ool

In

frastr

uctu

re

Ed

ucati

on

al

Syste

m

Cost

Poli

tical

& E

con

om

ic

En

vir

on

men

t

Cu

ltu

ral

Com

pati

bil

ity

EMEARegion

Bulgaria 5 5 4 6 5 6 6 8

Czech Republic

6 6 5 7 7 5 7 8

Egypt 4 5 4 4 6 7 3 4

Hungary 5 6 4 7 4 5 7 8

Poland 7 7 6 7 6 5 7 8

Romania 6 5 4 6 5 5 6 8

Russia 4 5 5 6 5 8 3 4

South Africa

9 6 4 5 4 5 4 9

Glo

bal

an

d L

eg

al

Matu

rit

y

6

7

4

7

7

6

3

6

Data

/ I

P S

ecu

rit

y

an

d P

riv

acy

5

7

4

7

7

5

3

4

………but needs to do more to achieve growth……….

Source: Gartner - Evaluate Offshore/Nearshore Countries for Outsourcing, Shared Services and CaptivesWorldwide 2016 (February 2016)

Most Eastern European countries are growing their service export industries by 10% - 15% annually

Governments have set up new Technology Parks, offer financial incentives to employers and employees and encourage universities to produce STEM graduates

4

Talent shortage is a major hurdle to sustainability and growth of US companies1

3.4 million Manufacturing jobs are likely to be needed over the next decade.

2.7 million

Baby Boomer retirements

700K manufacturing jobs expected from economic expansion.

Only 1.4 million

Jobs are likely to be filled.

An expected

2 million

Manufacturing jobs will remain unfilled due to the skills gap.

The US skills gap is widening

The implications are significant

Every job in manufacturing creates another 4.6new jobs throughout the entire economy

For every $1 invested in manufacturing, another $1.37 in additional value is created in other sectors

Other advanced nations such as Japan, Germany and South Korea face far more severe demographics challenges that in the US

The younger population segment (15 to 39 years) as a share of total population across all major nations is in decline.

By 2030, other nations like Japan, Germany and South Korea will have a higher proportion of aged population (65+ years) than in the US.

“Ageing of engineering and manufacturing workforce, without appropriate knowledge transfer will exacerbate skills shortage…….” Executive interview – US Manufacturing firm

Share of Younger Population(15-39 years) in Total Population

Share of Older Population(65+ years) in Total Population

China613

South Korea554

Japan536

Germany514

US481

Math PISA Score*

China580

Japan547

South Korea538

Germany524

US497

Science PISA Score*

1. Source: Manufacturing and Innovation - Deloitte and US Council on Competitiveness (May 2016)*Program or International Student Assessments (out of a total of 1,000) Source: National Center for Education Statistics 5

South East Asia – setting up at regional level for manufacturing success

Governments across the region developed an understanding of their electronics manufacturing industries’ needs ~ 3-4 decades ago, resulting in the right steps being taken to create enabling environments for the manufacturing industry

6

Africa – latent potential to establish a globally competitive manufacturing region

Source: SADC: Integrated Paper on Recent Economic Developments in SADC – please note data is dated and an excerpt from a 2015 study: Gauteng Provincial Government Local Manufacturing Feasibility Study. To size the opportunity for electronics manufacturing in SA and Gauteng, 2014 trade, GDP and manufacturing output data was used.

With a rapidly growing middle class, SSA countries can increasingly look to take advantage of domestic markets whilst targeting export markets as well

Automotive Avionics and aerospace

General electrical sub-components

Energy-saving technologies

Radar

Power electronics Consumer electronics

Telecommunications Medical devices

Lighting

Information Technology

Sizing of local manufacturing opportunity in South Africa:

~R189 billion for South Africa~ R61 billion for Gauteng Province

7

88

Case studies

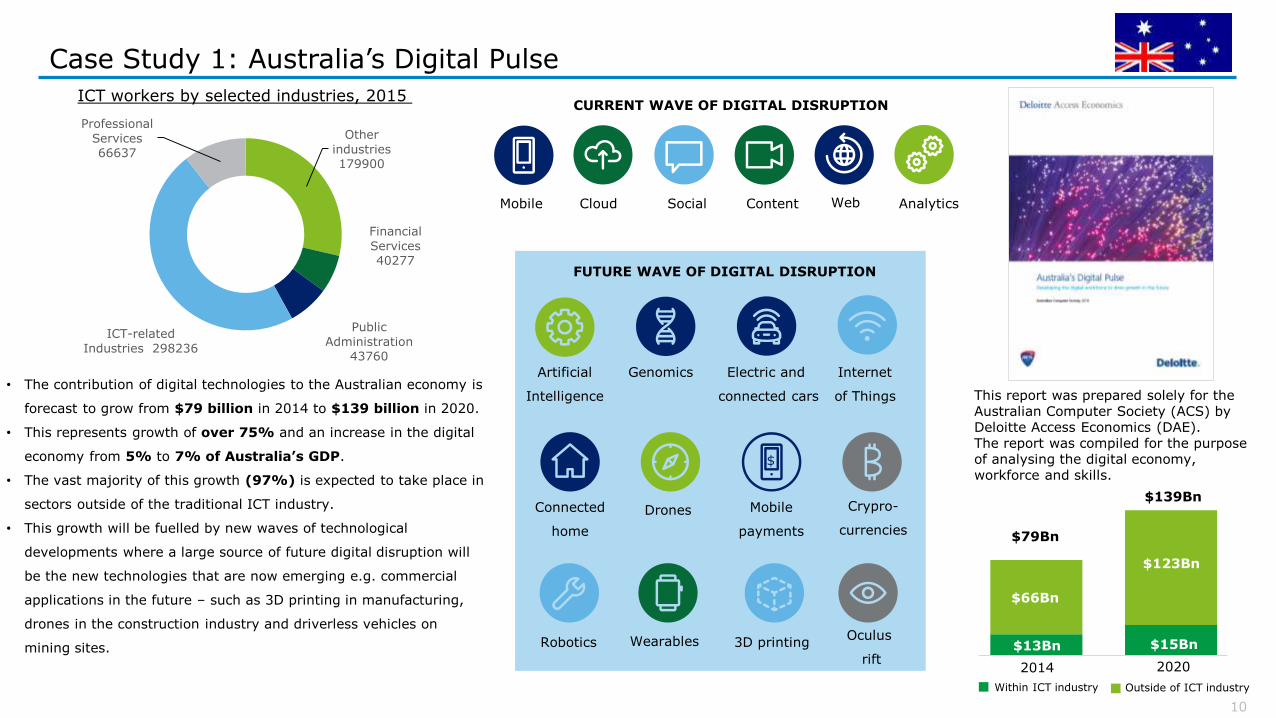

Case Study 1: Australia’s Digital Pulse

This report was prepared solely for the Australian Computer Society (ACS) by Deloitte Access Economics (DAE). The report was compiled for the purpose of analysing the digital economy, workforce and skills.

Other

industries

179900

Financial

Services40277

Public

Administration 43760

ICT-related

Industries 298236

Professional

Services 66637

ICT workers by selected industries, 2015

• The contribution of digital technologies to the Australian economy is

forecast to grow from $79 billion in 2014 to $139 billion in 2020.

• This represents growth of over 75% and an increase in the digital

economy from 5% to 7% of Australia’s GDP.

• The vast majority of this growth (97%) is expected to take place in

sectors outside of the traditional ICT industry.

• This growth will be fuelled by new waves of technological

developments where a large source of future digital disruption will

be the new technologies that are now emerging e.g. commercial

applications in the future – such as 3D printing in manufacturing,

drones in the construction industry and driverless vehicles on

mining sites.

CURRENT WAVE OF DIGITAL DISRUPTION

Mobile AnalyticsWebContentSocialCloud

FUTURE WAVE OF DIGITAL DISRUPTION

Artificial

Intelligence

Genomics

Crypro-

currencies

Internet

of Things

Electric and

connected cars

$

Connected

home

Mobile

payments

Oculus

rift

Drones

Robotics 3D printingWearables

2014 2020

$13Bn

$66Bn

$15Bn

$123Bn

$79Bn

$139Bn

3Within ICT industry Outside of ICT industry

10

Case Study 2: cellnex (ex Abertis Telecoms)

Abertis is currently a leading international group of toll-road operators, managing thousands of kilometers of high quality, high capacity roads and toll roads globally. Abertis has a market cap of ~€14Bn and owns 57% of Hispasat with a fleet of 7 satellites. As at Q1 2016, more than 70% of it’s EBITDA came from outside Spain.

Abertis owned Abertis Telecoms (now cellnex), a telecommunications infrastructure operator with headquarters in Barcelona, Spain. The company has a range of products and took the opportunity to acquire signal distribution infrastructure at a point when telecommunications companies were struggling and legislation allowed the companies to merge.

Abertis Telecoms (now cellnex) infrastructure includes:• DTT and Radio network;• IP Data Network;• Transport;• Mobile radio communications; and • Sea rescue networks

Abertis disposed of AbertisTelecoms as part of its strategy to focus on toll roads.

Key History Company and Financial Performance Highlights

2015 - cellnex IPO: Highly subscribed at top of the range. Value crystallisation exceeded expectations with ~€2.7Bn capital gains

2015 – 8% organic growth achieved through new PoPs being able to drive multi-tenancy with 4G rollout, closing coverage gaps and through network densification strategy. cellnex was also a key beneficiary of European consolidation through value accretive acquisitions

Q1 2016 – continued organic growth through increased multi-tenancy and infrastructure rationalisation. The company plays a strong industry leadership role to achieve operating synergies as a value creation driver for its shareholders and to fulfil national ICT vision and regulatory objectives for Spain.

• Cellnex continues to evolve from management of passive infrastructure to providing innovative value-added services, e.g. entered into a 8-year contract with Barcleona City Council to sell co-location services for Small Cells throughout the city.

• Cellnex also concluded an Agreement with Sigfox for the deployment of the first global IoT network in Spain.

cellnex is now the 25th largest Spanish company in terms of market cap as of FY 2015/6 year end (c.€4Bn) with ~ 15 000 network sites

Growth through Innovation

2016

20 June, Cellnex Telecom (CLNX: SM) joined the IBEX® 35 Index. The IBEX 35 Technical Advisory Committee approved CellnexTelecom’s inclusion in the benchmark index of Spain’s stock exchange, the IBEX® 35.

2015 Business Performance

Revenues (€Mn) Adjusted EDITDA (€Mn)

11

Case Study 3: Korea Telecoms

2010KT Group decided to form a property business by establishing a new subsidiary “KT Estate Ltd.” KT retained core property deemed essential to manage it’s telco business and handed over 99 properties to KT Estate. This was effectively to be used as the ‘seed capital’ to buckle down the KT Estate business.

As at December 31, 2015 KT Estate total assets and revenue for FY 2015 amounted to ~USD 1.5 billion and USD 300 million respectivelyKT Estates’ primary business consists of three types:1) property rentals,2) real estate management including inter-companies’ property as well as for third parties, and 3) development of its property e.g. property refurbishment, new developments, domestic housing development and a range of Smart City initiatives

₩revenue

KT Estate Ltd. founded in 2010

2011: KT 2 step migration office development project management; Busan Logistics Centre and apartment development

2012: Enforcement of KT-KT Estate asset management business. Founded KD Living Kay Realty business

2013: Achieved ISO 14001 certification- international environmental management standardConducted KT asset portfolio diagnostics Achieved credit rating A+ (stable)

2014: Commenced Brass Housing Development ProjectsCommencedYeongdeungpo rental housing construction Data Centre expansion projects

2015: Replacement of ageing security solutions in AndongKT real estate portfolio diagnosis andStrategy consulting Signed up Home Repair business agreement

KT Estate Ltd. Core offerings: (1) consultancy services, (2) planning and design services and solutions, (3) real estate finance (Project Financing), (4) construction management, (5) marketing, (6) leasing and management of real estate products to offer the best value to customers

KT Corp. launches new housing brand, expands real estate business – March 2016• KT Estate recently launched its very own rental housing brand called Remark Vill and through this move intends on becoming

a leading provider of rental apartments. The brand name is a combination of “Remaking Value,” “Remarkable Life,” and “Real Landmark.”

• KT Estate is planning to provide a total of 2,231 rental houses across four regions as part of the Remark Vill project development.

• 2012 - KT Estates set up a JV viz.; KD Living with Japan’s rental housing management firm Daiwa Living Co. KT owns 51% of KD Living , with Daiwa holding the remaining 49% stake.

12

In conclusion

01

02

03

13

Accelerate implementation of broadband rolloutand free up spectrum, in order to

enable growth within ICT industry and outside of ICT industry

whilst including Government’s own digitisation plan as an integral part of the rollout

Develop forecast of future skills requirementsand increase STEM graduates to underpin growth in services industries

as well as to attract FDI to increase local manufacturing and design

Develop regionally aligned policiesthat comprehensively addresses harmonised technology standards, strategic

procurement and local manufacturing,

as well as addresses the intersect between industries brought about by IoT -

XaaS, whilst maintaining a focus on security

Thank you

Sharoda Rapeti

Director

Direct: +2711 806 5973

Mobile: +2783 212 2251

Email: [email protected]

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms, and their related entities (collectively, the “Deloitte network”). None of the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2016. For information, contact Deloitte Touche Tohmatsu Limited