David Colby Executive Vice President & Chief Financial...

45

David Colby Executive Vice President & Chief Financial Officer May 5, 2005

Transcript of David Colby Executive Vice President & Chief Financial...

David ColbyExecutive Vice President & Chief Financial Officer

May 5, 2005

2

Safe Harbor Statement

The statements made during this presentation that are not historical facts are forward-looking statements within the meaning for the Federal securities laws, and may involve a number of risks and uncertainties.

Factors that could cause actual results to differ materially from expectations include, but are not limited to, the risks discussed in the Company’s most recent filings with the SEC, including its Annual Report on Form 10-K for the year ended December 31, 2004.

3

Agenda

WellPoint Profile

WellPoint Growth Model: Executing with Strength

Investment Considerations

4

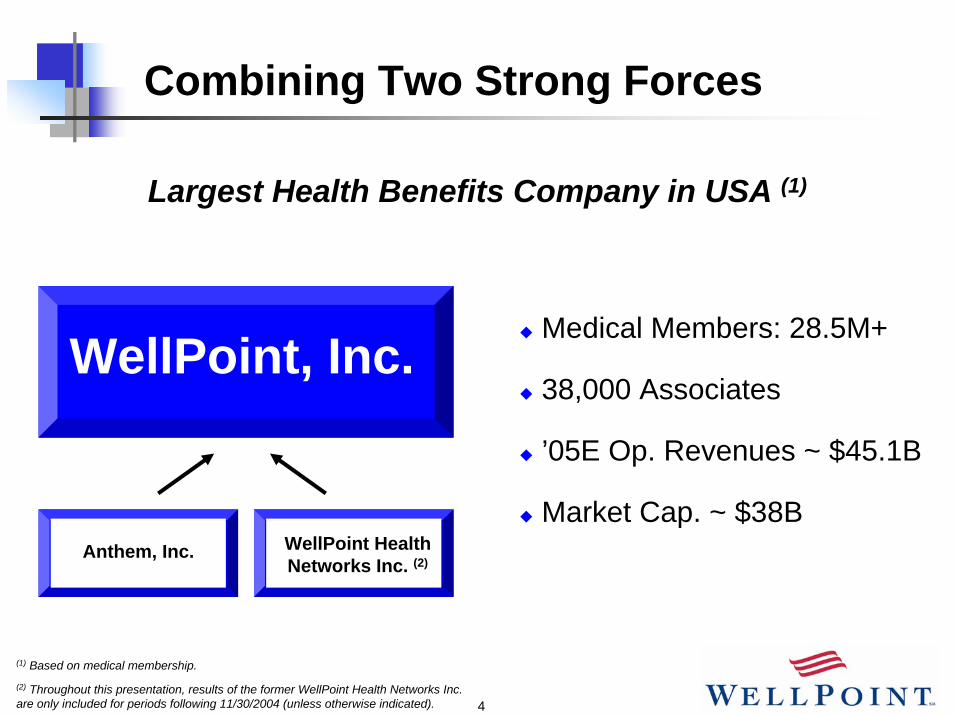

Combining Two Strong Forces

Largest Health Benefits Company in USA (1)

Medical Members: 28.5M+

38,000 Associates

’05E Op. Revenues ~ $45.1B

Market Cap. ~ $38BAnthem, Inc.

WellPoint, Inc.

WellPoint Health Networks Inc. (2)

(1) Based on medical membership.

(2) Throughout this presentation, results of the former WellPoint Health Networks Inc. are only included for periods following 11/30/2004 (unless otherwise indicated).

5

Leading Market Positions

NH

CT

ME

MA

VAKY

OHINIL

WI

MO

TX

COCA

NV

GA

BC or BCBS licensed plansUniCare and HealthLink >100K members

6

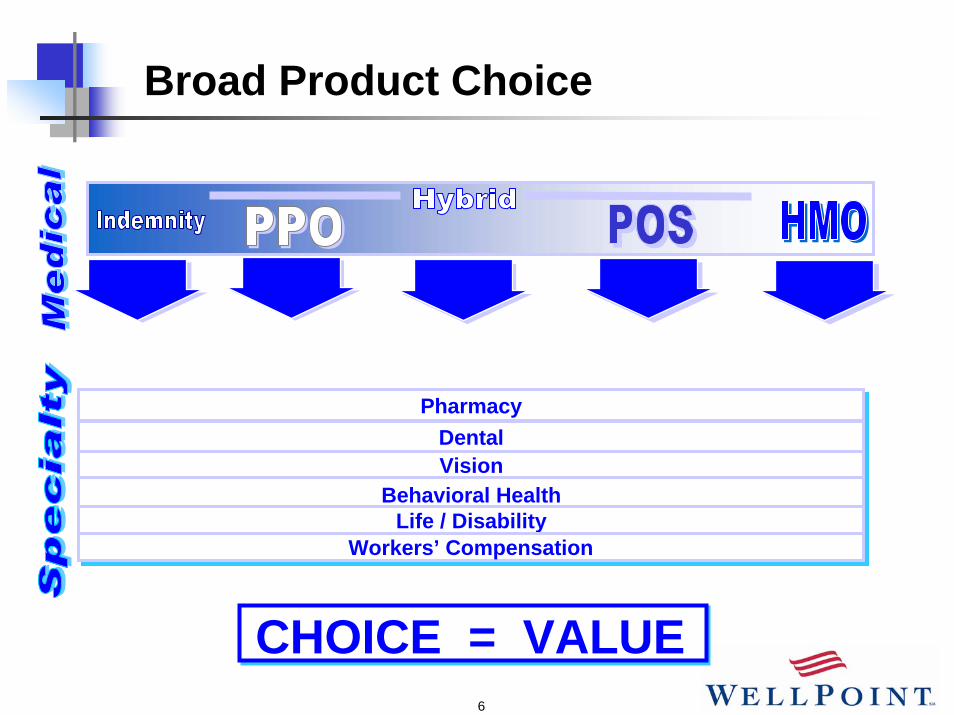

Broad Product Choice

CHOICE = VALUE

PharmacyPharmacyDentalDentalVisionVision

Behavioral HealthBehavioral HealthLife / DisabilityLife / Disability

Workers’ CompensationWorkers’ Compensation

7

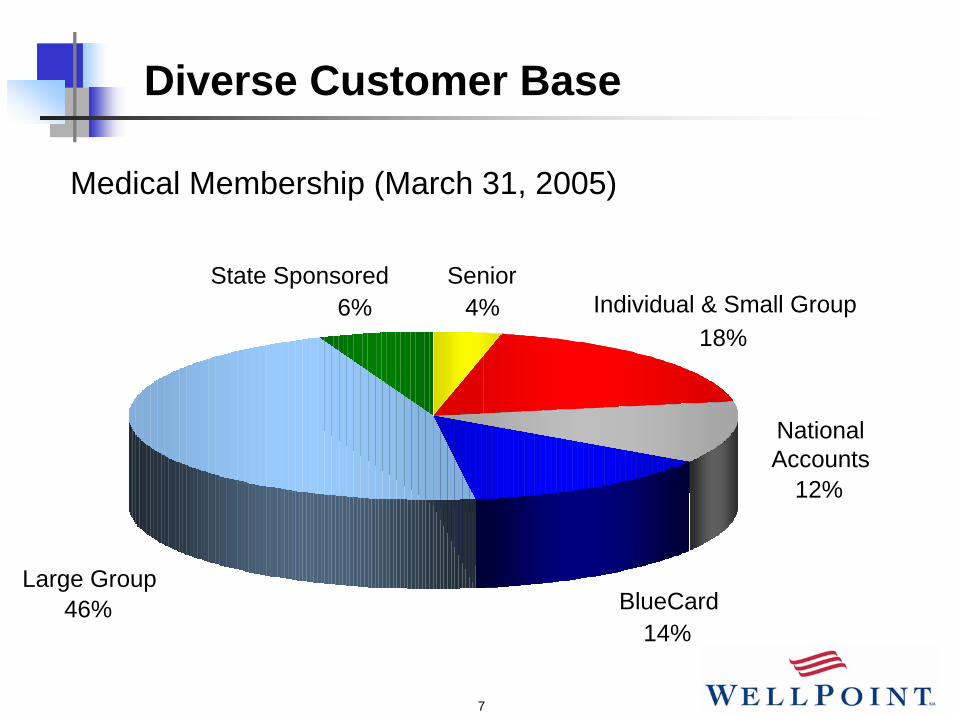

Diverse Customer Base

Medical Membership (March 31, 2005)

Large Group

Individual & Small Group

National Accounts

Senior4%

46%

12%

18%

State Sponsored6%

BlueCard14%

8

Senior Leadership

President and CEOLarry Glasscock

Chairman of the BoardLeonard Schaeffer

Chief Financial Officer - David Colby

General Counsel & Chief Public Affairs Officer - Angela Braly

Chief Medical Officer - Sam Nussbaum

Chief Actuary - Alice Rosenblatt

Chief Information Officer - Ron Ponder

Chief Strategy Officer - Mark Boxer

Chief Compliance Officer – Randall Lewis

9

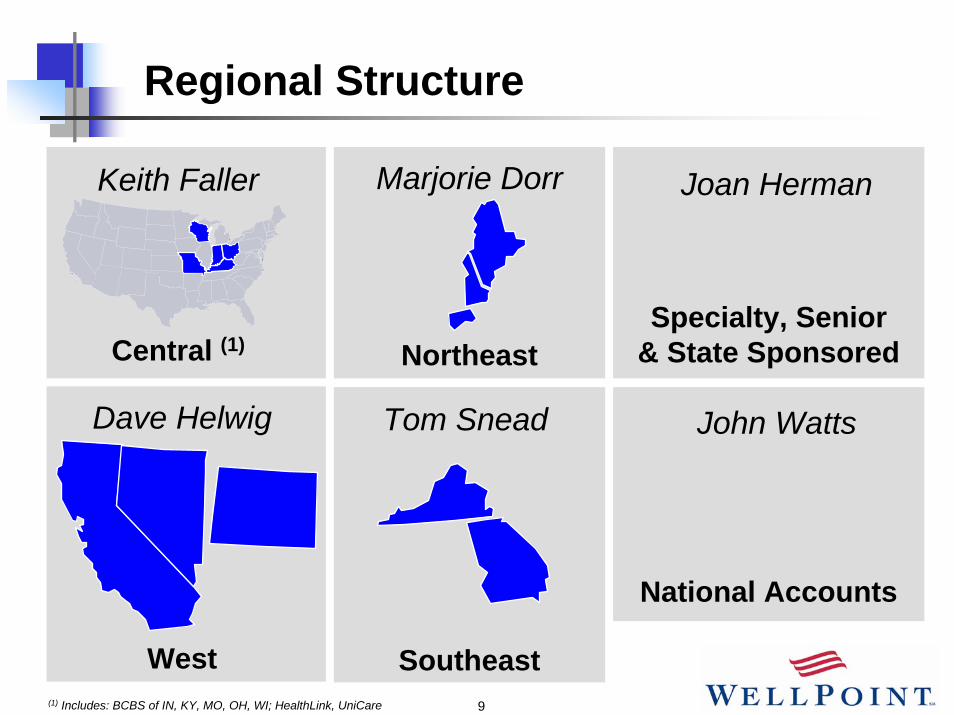

Regional Structure

Marjorie Dorr

Northeast

Joan Herman

Specialty, Senior & State Sponsored

Keith Faller

Central (1)

NV

Dave Helwig

West

John Watts

National Accounts

Tom Snead

Southeast(1) Includes: BCBS of IN, KY, MO, OH, WI; HealthLink, UniCare

10

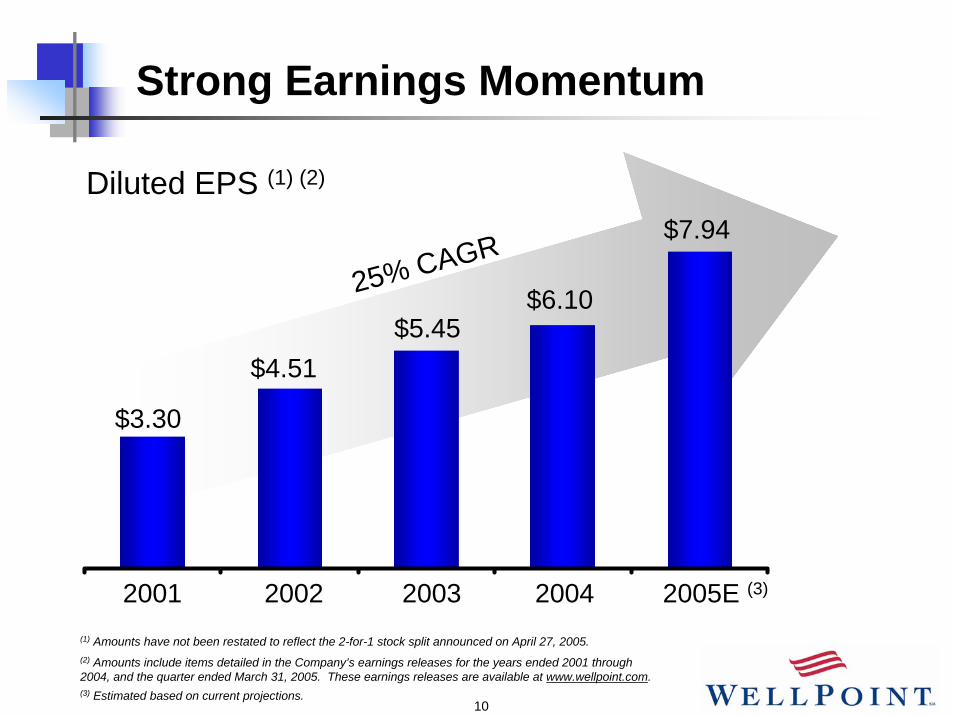

Strong Earnings Momentum

Diluted EPS (1) (2)

$6.1025% CAGR$7.94

$5.45$4.51

$3.30

2001 2002 2003 2004 2005E (3)

(2) Amounts include items detailed in the Company’s earnings releases for the years ended 2001 through 2004, and the quarter ended March 31, 2005. These earnings releases are available at www.wellpoint.com.

(1) Amounts have not been restated to reflect the 2-for-1 stock split announced on April 27, 2005.

(3) Estimated based on current projections.

11

Agenda

WellPoint Profile

WellPoint Growth Model: Executing with Strength

Investment Considerations

12

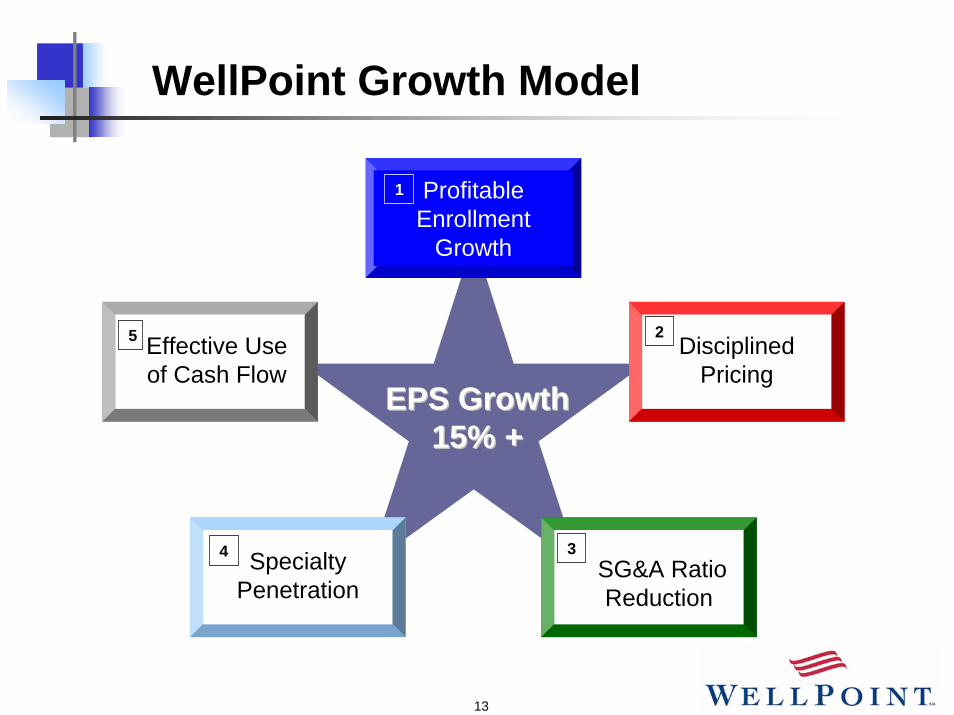

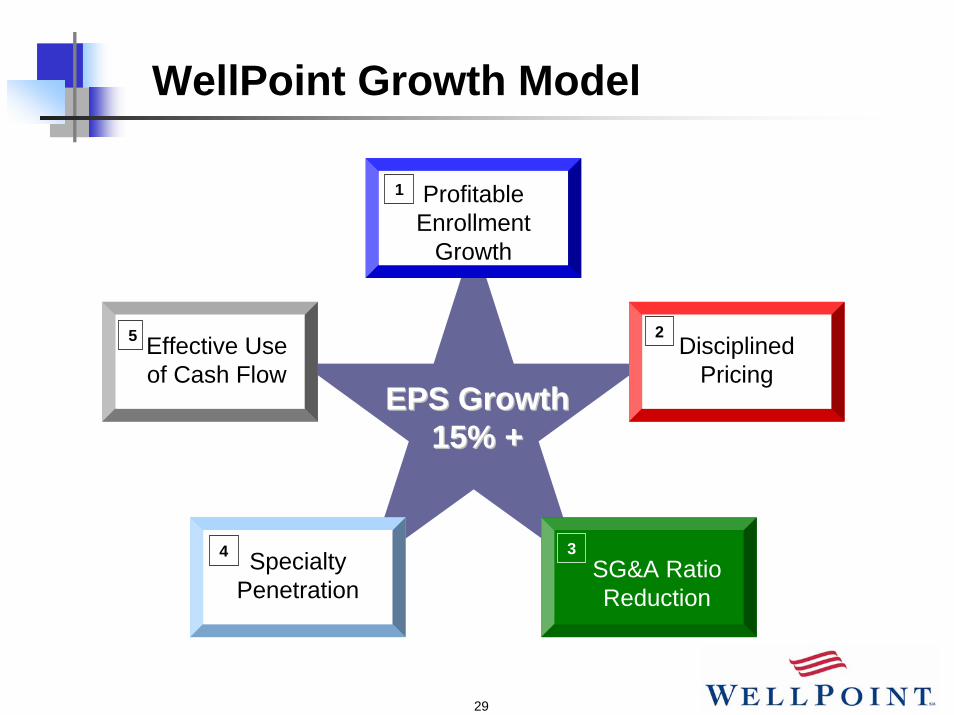

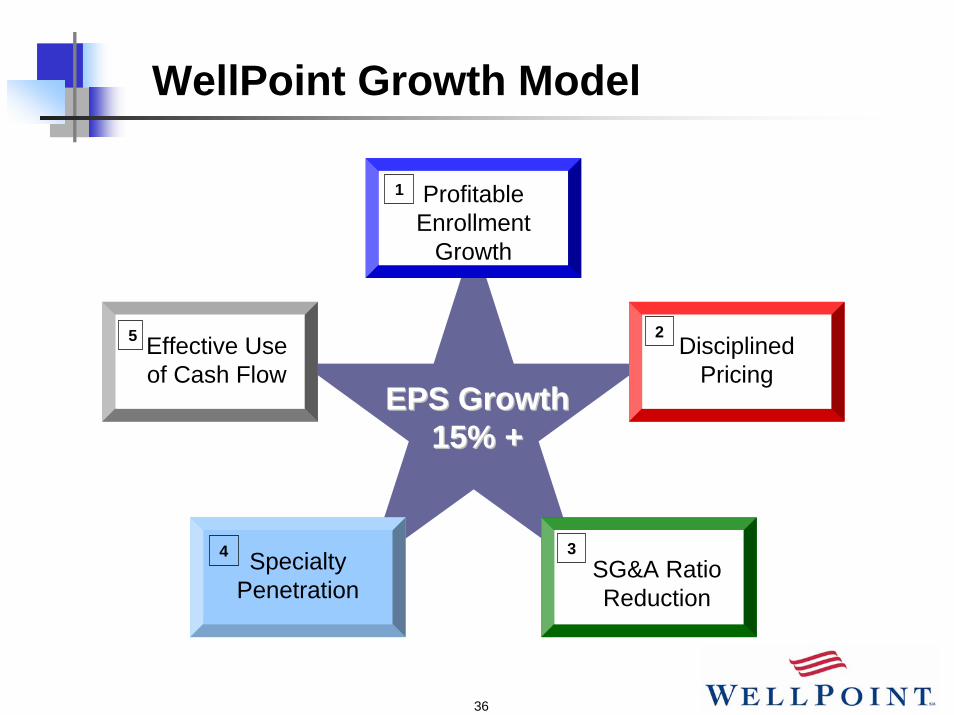

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A RatioReduction

Effective Useof Cash Flow

Specialty Penetration

5

4 3

2

1

13

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A RatioReduction

Effective Useof Cash Flow

Specialty Penetration

1

2

34

5

14

Profitable Enrollment Growth

1999 2000 2001 2002 2003 2004

Medical Membership (in millions)

6.3

11.17.97.3

27.7

11.9

“Same-store” membership Acquisition-related membership

10% “Same-Store” CAGR 28.7+

2005E (1)

(1) Estimated based on current projections. Refer to the Company’s earnings release for the quarter ended March 31, 2005, at www.wellpoint.com.

15

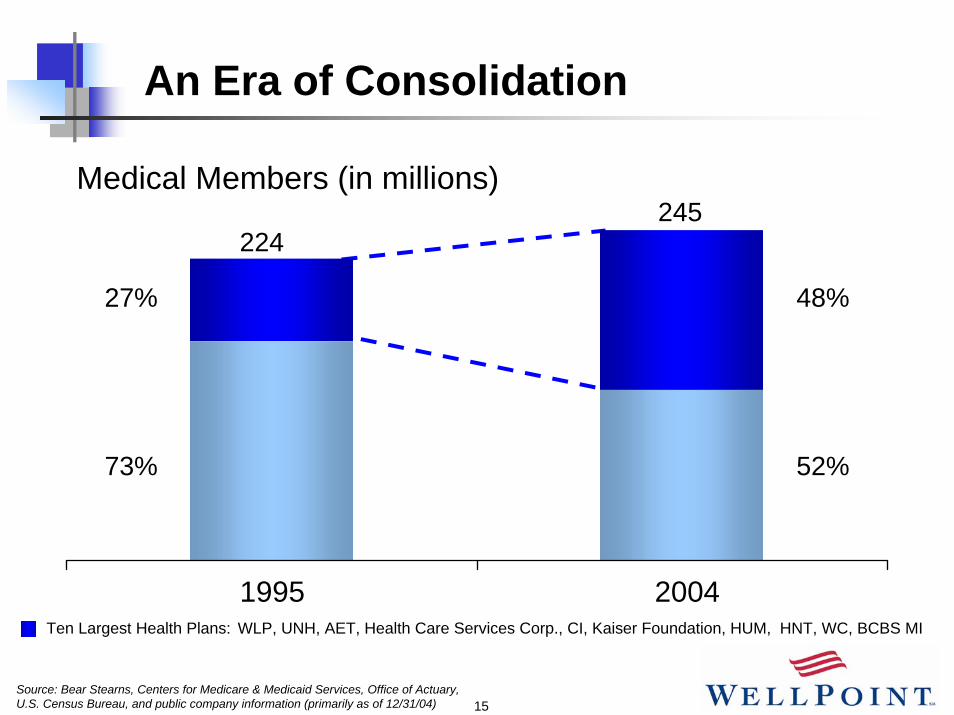

An Era of Consolidation

Medical Members (in millions)

1995 2004

27%

73%

48%

52%

224 245

Ten Largest Health Plans: WLP, UNH, AET, Health Care Services Corp., CI, Kaiser Foundation, HUM, HNT, WC, BCBS MI

Source: Bear Stearns, Centers for Medicare & Medicaid Services, Office of Actuary, U.S. Census Bureau, and public company information (primarily as of 12/31/04)

16

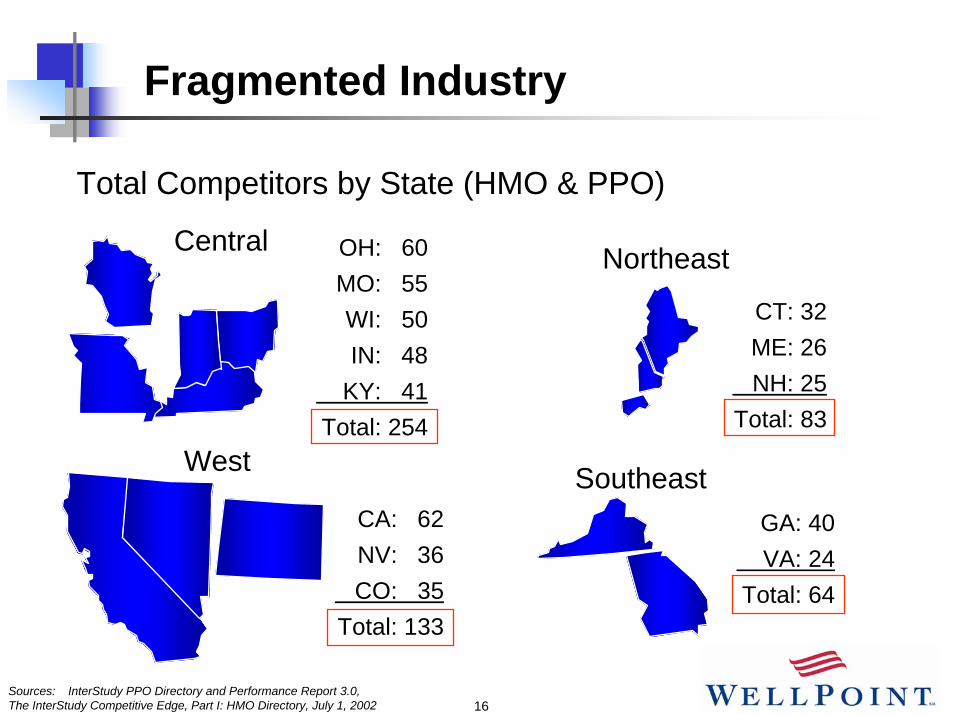

Fragmented Industry

Total Competitors by State (HMO & PPO)

Northeast

CT: 32ME: 26NH: 25

Total: 83

SoutheastGA: 40VA: 24

Total: 64

NV

West

CA: 62NV: 36CO: 35

Total: 133

Central OH: 60MO: 55WI: 50IN: 48

KY: 41Total: 254

Sources: InterStudy PPO Directory and Performance Report 3.0,The InterStudy Competitive Edge, Part I: HMO Directory, July 1, 2002

17

The Power of the Blues

Largest Provider Network

AttractiveDiscounts

Distinctive Customer Service

18

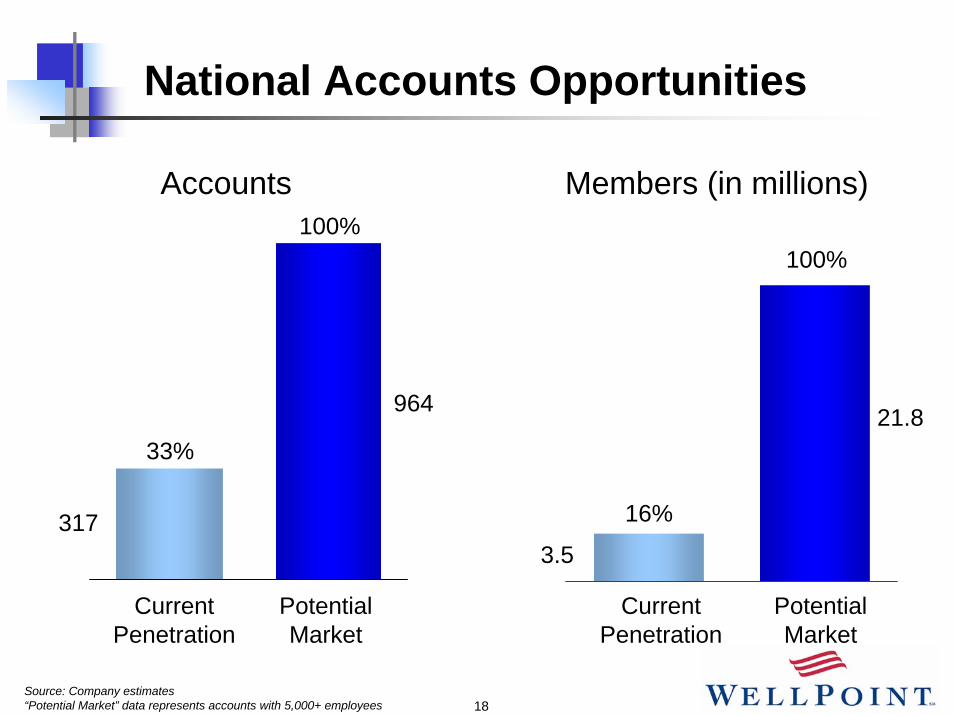

National Accounts Opportunities

Members (in millions)

21.8

3.5

CurrentPenetration

PotentialMarket

100%

16%

Accounts

317

964

CurrentPenetration

PotentialMarket

100%

33%

Source: Company estimates“Potential Market” data represents accounts with 5,000+ employees

19

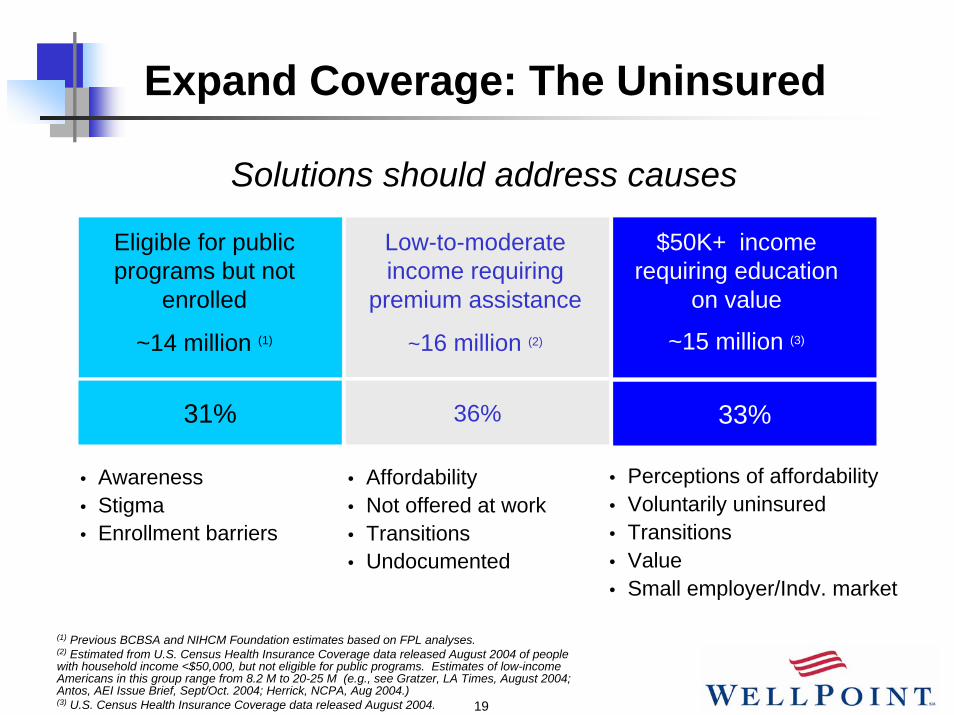

Expand Coverage: The Uninsured

Solutions should address causes

Low-to-moderate income requiring

premium assistance

~16 million (2)

Eligible for public programs but not

enrolled

~14 million (1)

36%

$50K+ income requiring education

on value

~15 million (3)

31% 33%

• Awareness• Stigma• Enrollment barriers

• Affordability • Not offered at work• Transitions• Undocumented

• Perceptions of affordability• Voluntarily uninsured• Transitions • Value • Small employer/Indv. market

(1) Previous BCBSA and NIHCM Foundation estimates based on FPL analyses.(2) Estimated from U.S. Census Health Insurance Coverage data released August 2004 of people with household income <$50,000, but not eligible for public programs. Estimates of low-income Americans in this group range from 8.2 M to 20-25 M (e.g., see Gratzer, LA Times, August 2004; Antos, AEI Issue Brief, Sept/Oct. 2004; Herrick, NCPA, Aug 2004.)(3) U.S. Census Health Insurance Coverage data released August 2004.

20

The Anthem HSA

Aligned with JPMorgan Chase

Available in all targeted markets

Lower premiums & potential tax savings for both employers & employees

Capitalizes on innovative, personalized web tools of Anthem ByDesign

21

Tonik Products for Individuals

Developed by and for the “Young Invincibles”

Educates audience

Offers low price points

Unique package of benefits

22

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A Ratio Reduction

Effective Useof Cash Flow

Specialty Penetration

1

2

34

5

23

WellPoint Actuarial Facts

Over 100 credentialed actuaries – FSA, ASA, MAAA

Approximately 100 actuarial students

Senior management in Corporate actuarial area – Chief Actuary of WellPoint and two former Chief Actuaries

Senior management in Regional actuarial areas – six former Chief Actuaries of stand-alone health plans

Hybrid model – best of legacy Anthem and legacy WellPoint Health Networks

Strong corporate controlsRegional actuaries closely integrated into operations

24

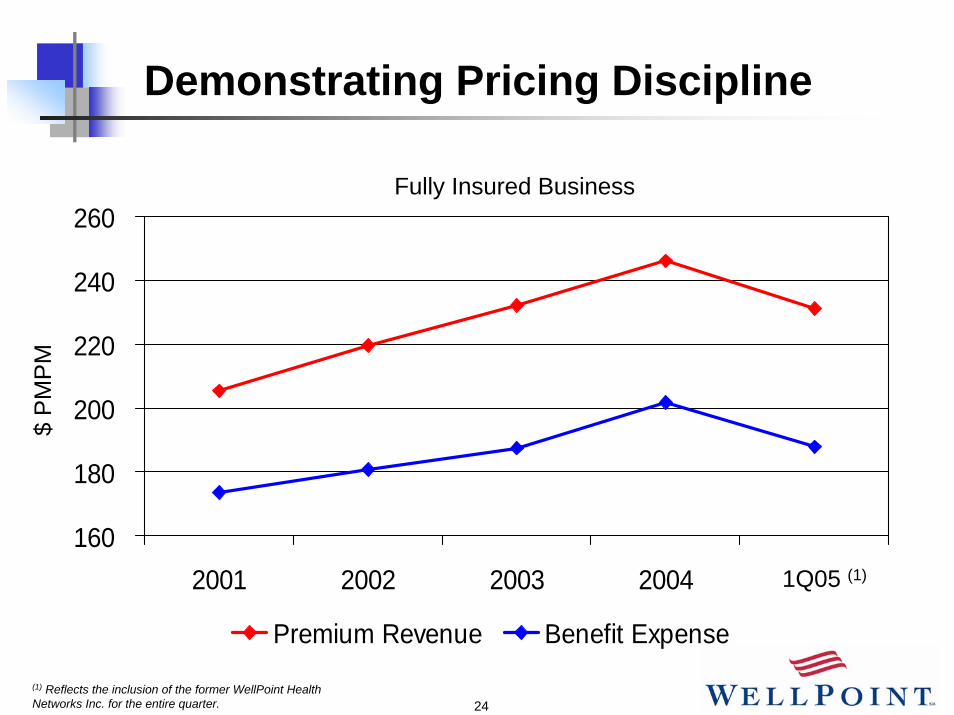

Demonstrating Pricing Discipline

160

180

200

220

240

260

2001 2002 2003 2004

Premium Revenue Benefit Expense

$ P

MP

M

Fully Insured Business

1Q05 (1)

(1) Reflects the inclusion of the former WellPoint Health Networks Inc. for the entire quarter.

25

Pricing Flexibility

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Flexible *

33%

8%

17%13%

29%

* “Flexible” renewals include individual and small group products in certain states where rates can generally be changed with 30-60 days notice.

Note: Patterns calculated as of November 2004

26

Regional Concentration

Health care is locally delivered and locally consumedBetter network leverageGreater actuarial precisionMore efficient marketing and operations

UniCare regions (also include IN, MD, OH and VA)

BC or BCBS licensed plans

HealthLink states (also include IL, VA, MO and TX)

27

Predictive Models: A Framework for Success

Demographics

Patient Reported Information

Claims DataData Warehouse

Targeted MedicalManagement Actuarial Precision

Trend Analysis

More Accurate Cost Prediction & Profitability

ModelRegression

Rules-based

Artificial Intelligence

Neural Networks

Combinations

Clinical Intervention

Quality Improvement & Financial Impact

28

Health Care Management Strategies

Increasing Health RiskCosts: 13% 24% 63%

Low RiskMembers

Moderate Risk Members

Members: 69% 24% 7%

Well Members

High RiskMembers

Complex & Intensive Care

Prevention and Early Identification – Risk AvoidanceCase Management

Integrated Advanced Care Models

Disease Management

Shared Decision Making (Web Support, Healthcare Advisor)

Pay for Performance

Centers of Excellence

IRIS Program

29

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A Ratio Reduction

Effective Useof Cash Flow

Specialty Penetration

1

2

34

5

30

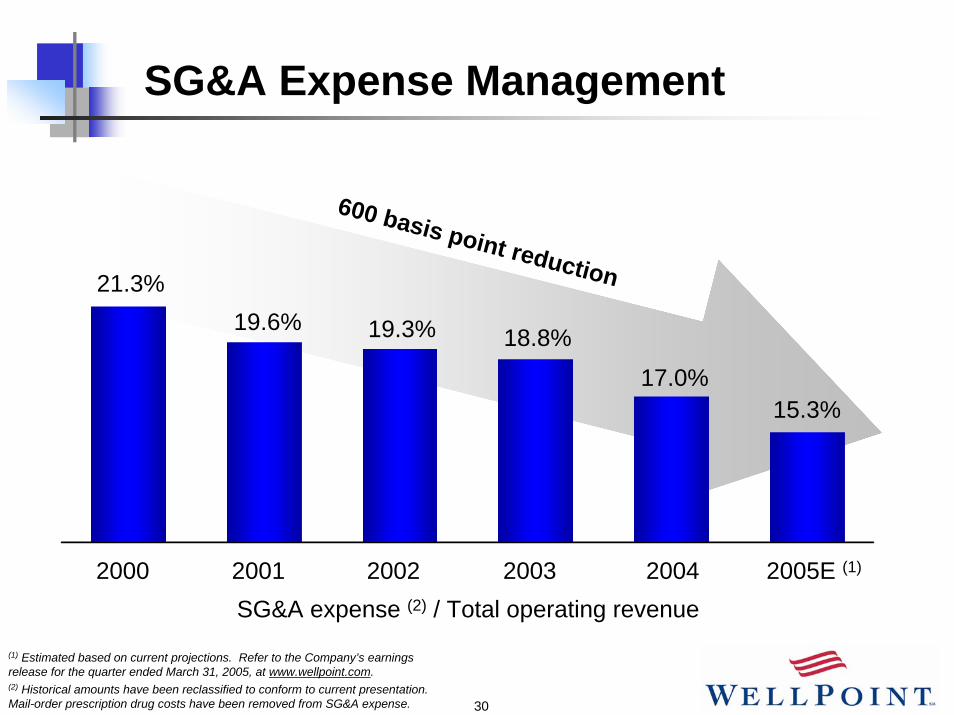

SG&A Expense Management

21.3%19.6% 19.3% 18.8%

17.0%

600 basis point reduction

2002 2003 200420012000

15.3%

2005E (1)

SG&A expense (2) / Total operating revenue

(1) Estimated based on current projections. Refer to the Company’s earnings release for the quarter ended March 31, 2005, at www.wellpoint.com.(2) Historical amounts have been reclassified to conform to current presentation. Mail-order prescription drug costs have been removed from SG&A expense.

31

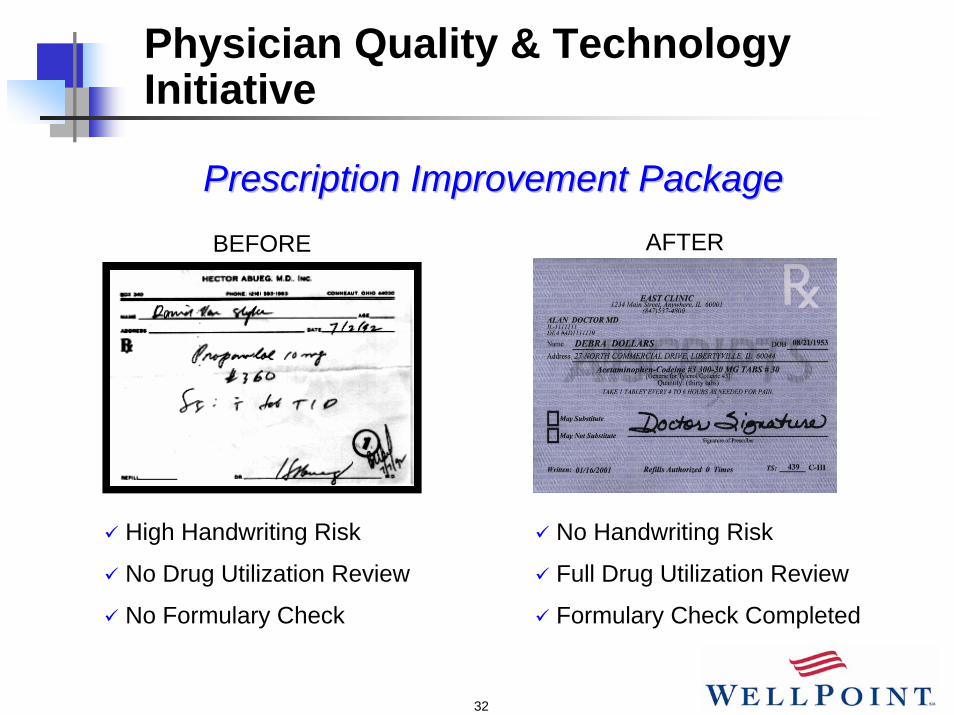

Physician Quality & Technology Initiative

Move from basic administrative services to transactions that support quality care

GOAL:

BasicConnectivity

ClaimsProcesses

MedicalManagement

Clinical Support

EligibilityMember BenefitsClaim StatusReferralsClaim SubmissionRe-CredentialingProvider Directory Provider Change

Preprocessing Claims Remittance Allowance Inquiry Claims CorrectionPlan AR Aging

E-prescribingOutcomes ResearchPatient RecruitmentDisease RegistriesElectronic Med RecordVirtual Visits

ER Notifications Formulary Management Alerts and Reminders Auto-AdjudicationPre-Certification Dz Mgmt Integration

32

Physician Quality & Technology Initiative

Prescription Improvement PackagePrescription Improvement PackageAFTERBEFORE

High Handwriting Risk

No Drug Utilization Review

No Formulary Check

No Handwriting Risk

Full Drug Utilization Review

Formulary Check Completed

33

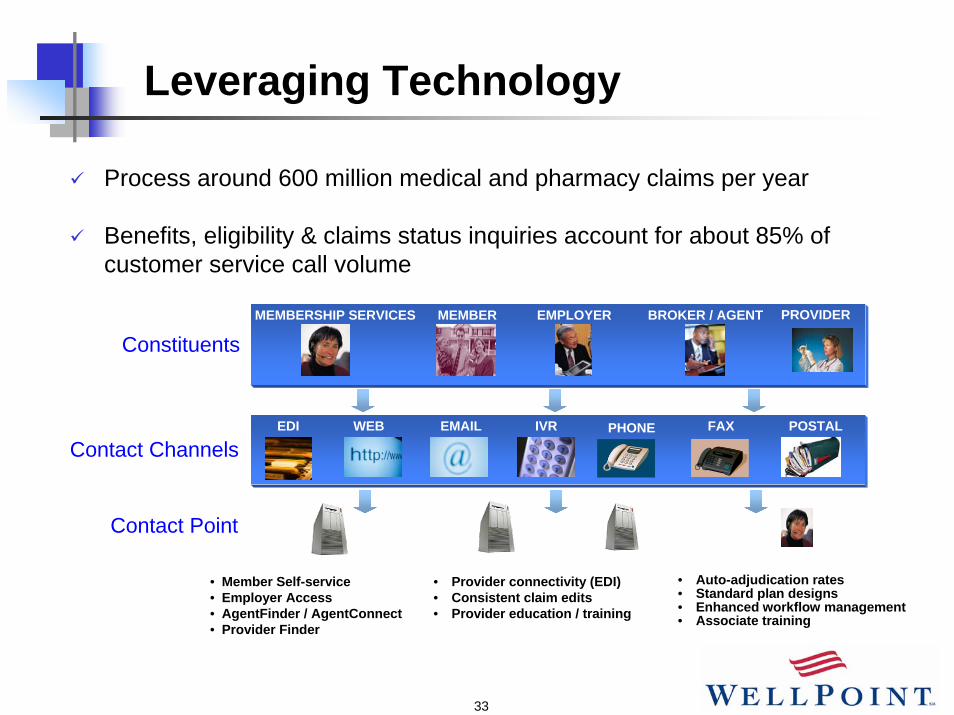

Leveraging Technology

Process around 600 million medical and pharmacy claims per year

Benefits, eligibility & claims status inquiries account for about 85% of customer service call volume

MEMBERMEMBERSHIP SERVICES EMPLOYER BROKER / AGENT

Membership Service

AssociateWeb EDIEET

PROVIDER

IVRWEB PHONEEMAIL FAX POSTALEDI

Constituents

Contact Channels

Contact Point

• Member Self-service• Employer Access• AgentFinder / AgentConnect• Provider Finder

• Auto-adjudication rates• Standard plan designs• Enhanced workflow management• Associate training

• Provider connectivity (EDI)• Consistent claim edits• Provider education / training

34

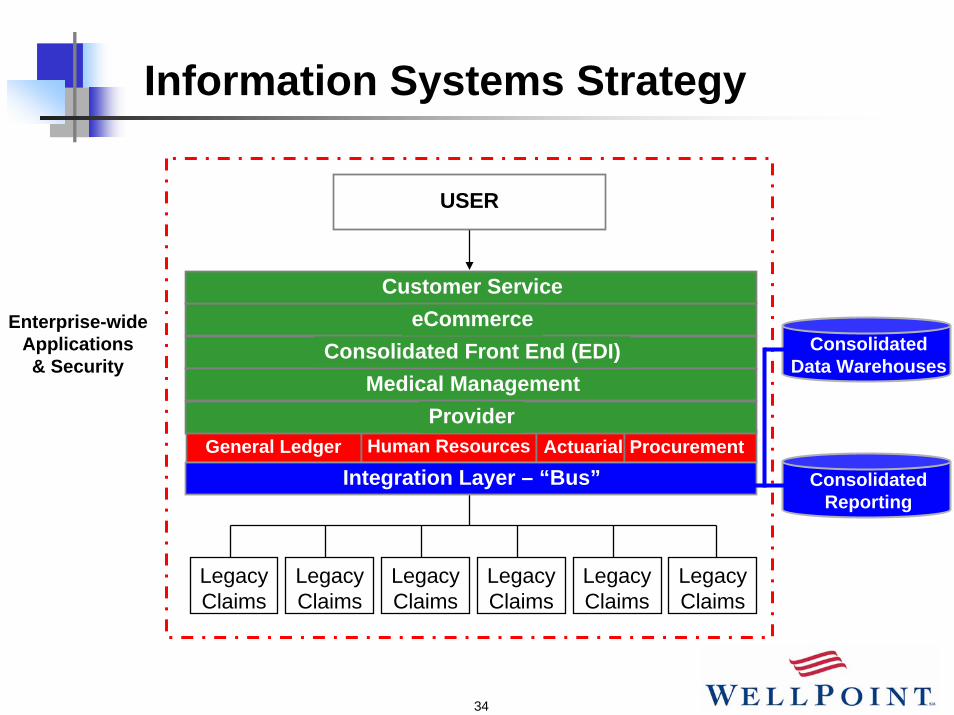

Information Systems Strategy

General Ledger Human Resources Actuarial Procurement

Consolidated Front End (EDI)

Provider

USER

Integration Layer – “Bus”

Medical Management

eCommerceCustomer Service

Enterprise-wideApplications& Security

Consolidated Reporting

LegacyClaims

LegacyClaims

LegacyClaims

LegacyClaims

LegacyClaims

LegacyClaims

ConsolidatedData Warehouses

35

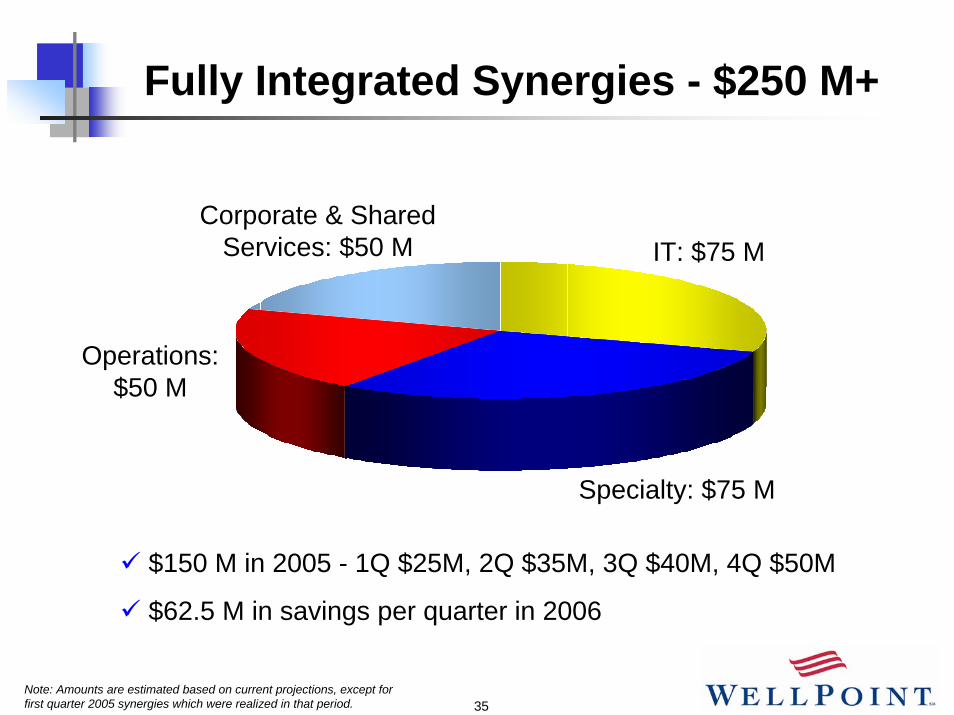

Fully Integrated Synergies - $250 M+

$150 M in 2005 - 1Q $25M, 2Q $35M, 3Q $40M, 4Q $50M

$62.5 M in savings per quarter in 2006

Corporate & Shared Services: $50 M IT: $75 M

Operations: $50 M

Specialty: $75 M

Note: Amounts are estimated based on current projections, except for first quarter 2005 synergies which were realized in that period.

36

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A Ratio Reduction

Effective Useof Cash Flow

Specialty Penetration

1

2

34

5

37

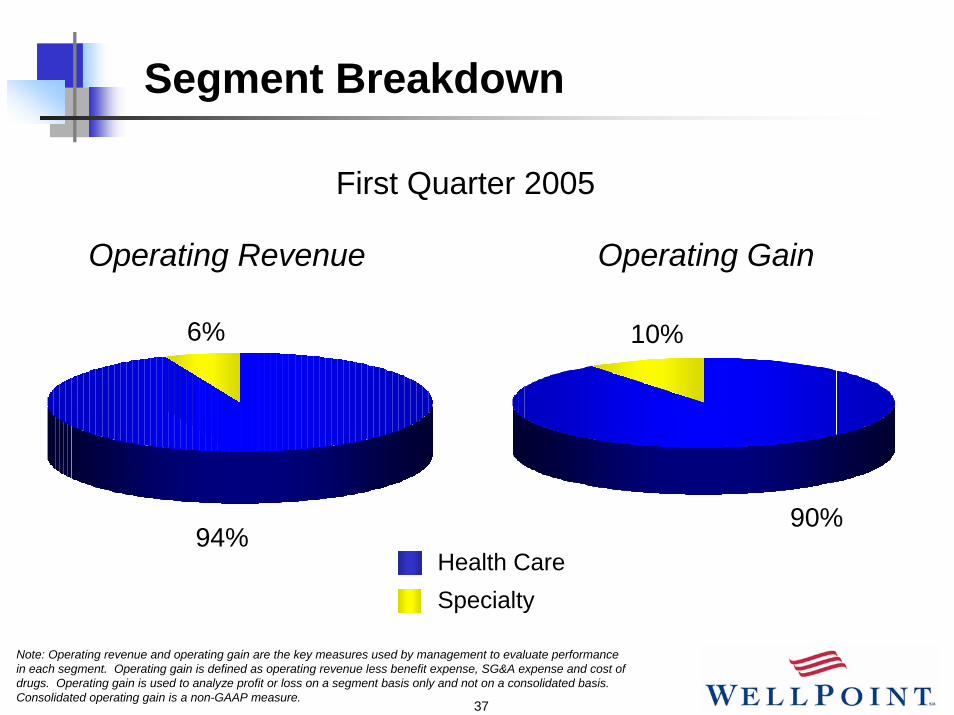

Segment Breakdown

94%

6% 10%

90%Health CareSpecialty

Operating Revenue Operating Gain

First Quarter 2005

Note: Operating revenue and operating gain are the key measures used by management to evaluate performance in each segment. Operating gain is defined as operating revenue less benefit expense, SG&A expense and cost of drugs. Operating gain is used to analyze profit or loss on a segment basis only and not on a consolidated basis. Consolidated operating gain is a non-GAAP measure.

38

Specialty Opportunity

Delivering more comprehensive benefit packages

Medical Benefits

Life/Disability PBM Behavioral Health

VisionDental Workers’ Comp

Increases profitability of medical membership

Improves retention rates

39

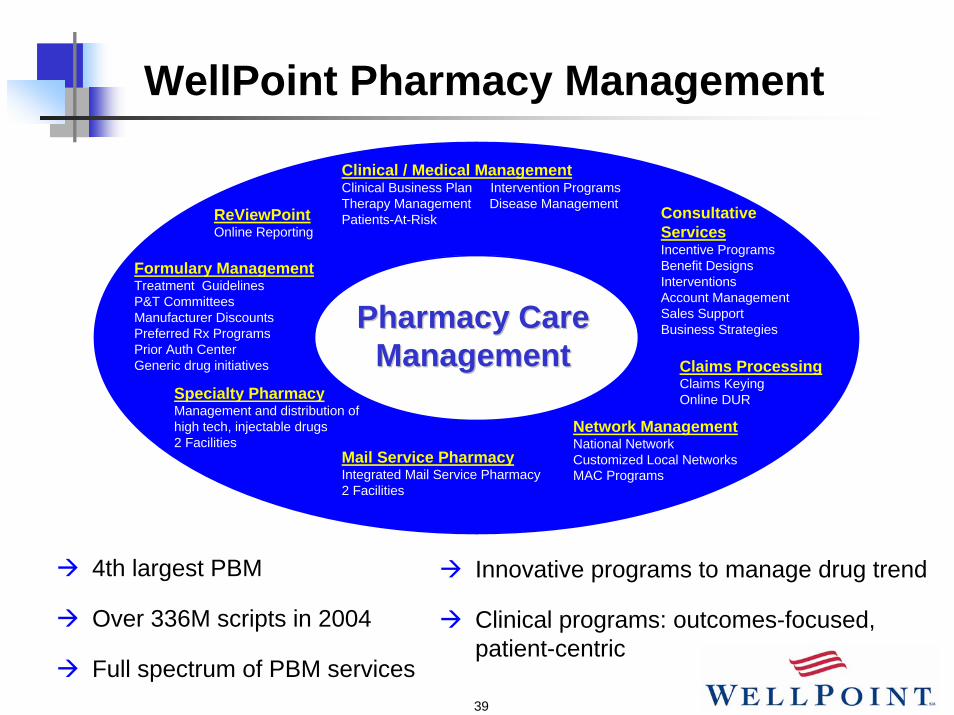

WellPoint Pharmacy Management

Clinical / Medical ManagementClinical Business Plan Intervention ProgramsTherapy Management Disease ManagementPatients-At-Risk

Formulary ManagementTreatment GuidelinesP&T CommitteesManufacturer DiscountsPreferred Rx ProgramsPrior Auth CenterGeneric drug initiatives

ReViewPointOnline Reporting

Claims ProcessingClaims KeyingOnline DUR

Network ManagementNational NetworkCustomized Local NetworksMAC Programs

ConsultativeServicesIncentive ProgramsBenefit DesignsInterventionsAccount ManagementSales SupportBusiness StrategiesPharmacy Care Pharmacy Care

ManagementManagement

Mail Service PharmacyIntegrated Mail Service Pharmacy2 Facilities

Specialty PharmacyManagement and distribution of high tech, injectable drugs2 Facilities

4th largest PBM

Over 336M scripts in 2004

Full spectrum of PBM services

Innovative programs to manage drug trend

Clinical programs: outcomes-focused, patient-centric

40

WellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment

Growth

DisciplinedPricing

SG&A Ratio Reduction

Specialty Penetration

Effective Useof Cash Flow

1

2

34

5

41

Effective Cash Management

Operating Cash Flow(in billions)

$0.5

$1.0$0.8

$1.2$1.0

$1.3

$3.0+

~ $2.5

2005E (1)20042002 2003Net Income Operating Cash Flow

(1) Estimated based on current projections. Refer to the Company’s earnings release for the quarter ended March 31, 2005, at www.wellpoint.com.

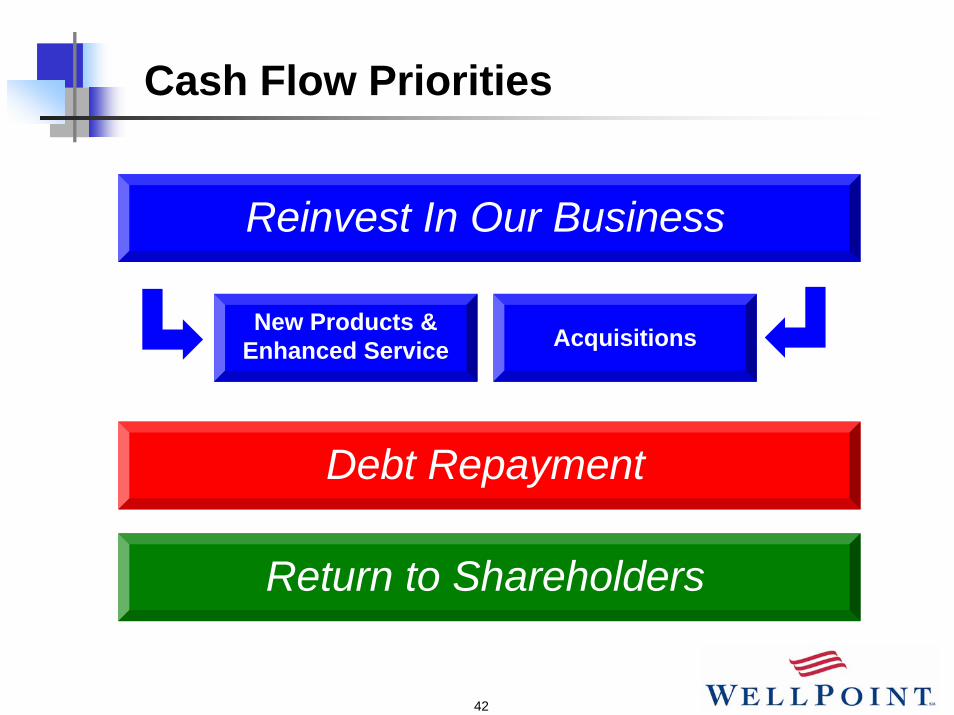

42

Cash Flow Priorities

Reinvest In Our Business

New Products & Enhanced Service Acquisitions

Debt Repayment

Return to Shareholders

43

Agenda

WellPoint Profile

WellPoint Growth Model: Executing with Strength

Investment Considerations

44

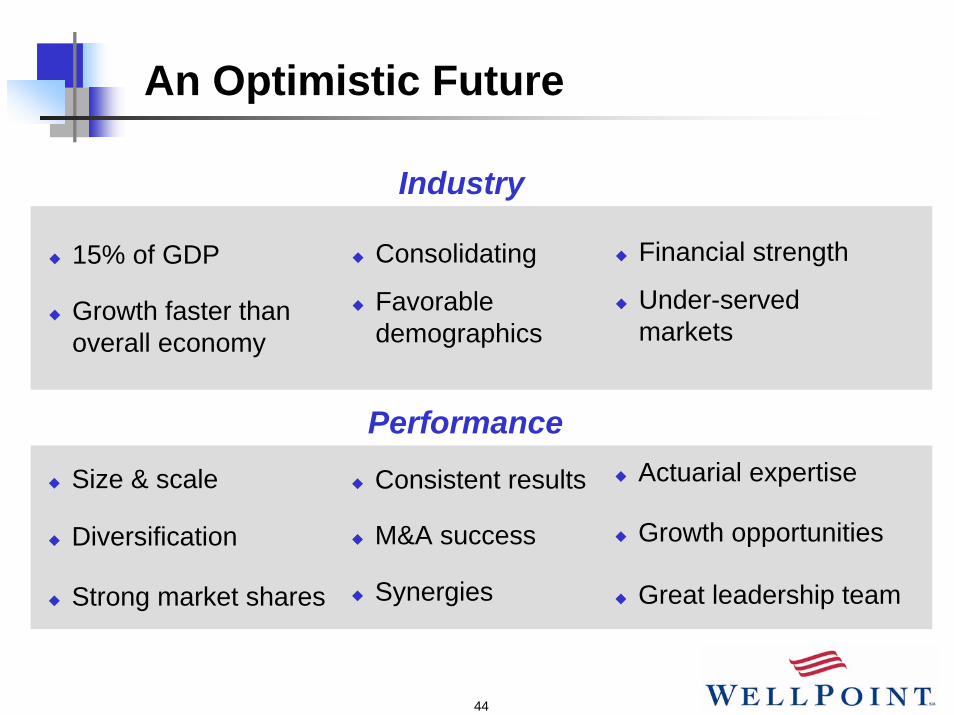

An Optimistic Future

Industry

15% of GDP

Growth faster than overall economy

Consolidating

Favorable demographics

Financial strength

Under-served markets

PerformanceSize & scale

Diversification

Strong market shares

Consistent results

M&A success

Synergies

Actuarial expertise

Growth opportunities

Great leadership team