Darwin Seafood Processing Facility

55

December 2021 Darwin Seafood Processing Facility Industry Workshops – Summary Outputs

Transcript of Darwin Seafood Processing Facility

December 2021

Darwin SeafoodProcessing Facility

Industry Workshops –Summary Outputs

2

Workshop Summary Outputs

Contents Item Page

Industry workshops - Summary of outputs 3

Background and context 6

Workshop 1: Products – overview, insights from guest speakers, key insights, participants 10

Workshop 2: Viability – overview, key insights, participants 15

Workshop 3: Location & Business Model – overview, insights from guest speakers, key insights, participants 20

Appendix - collated Mentimeter data 26

Addendum These have been

sent separately as supporting

documentation

1. Workshop packs incl. all questions and content covered

2. Raw Mentimeter data from each workshop

3. Pulse survey data

3

Summary of outputs

4

Workshop Summary Outputs

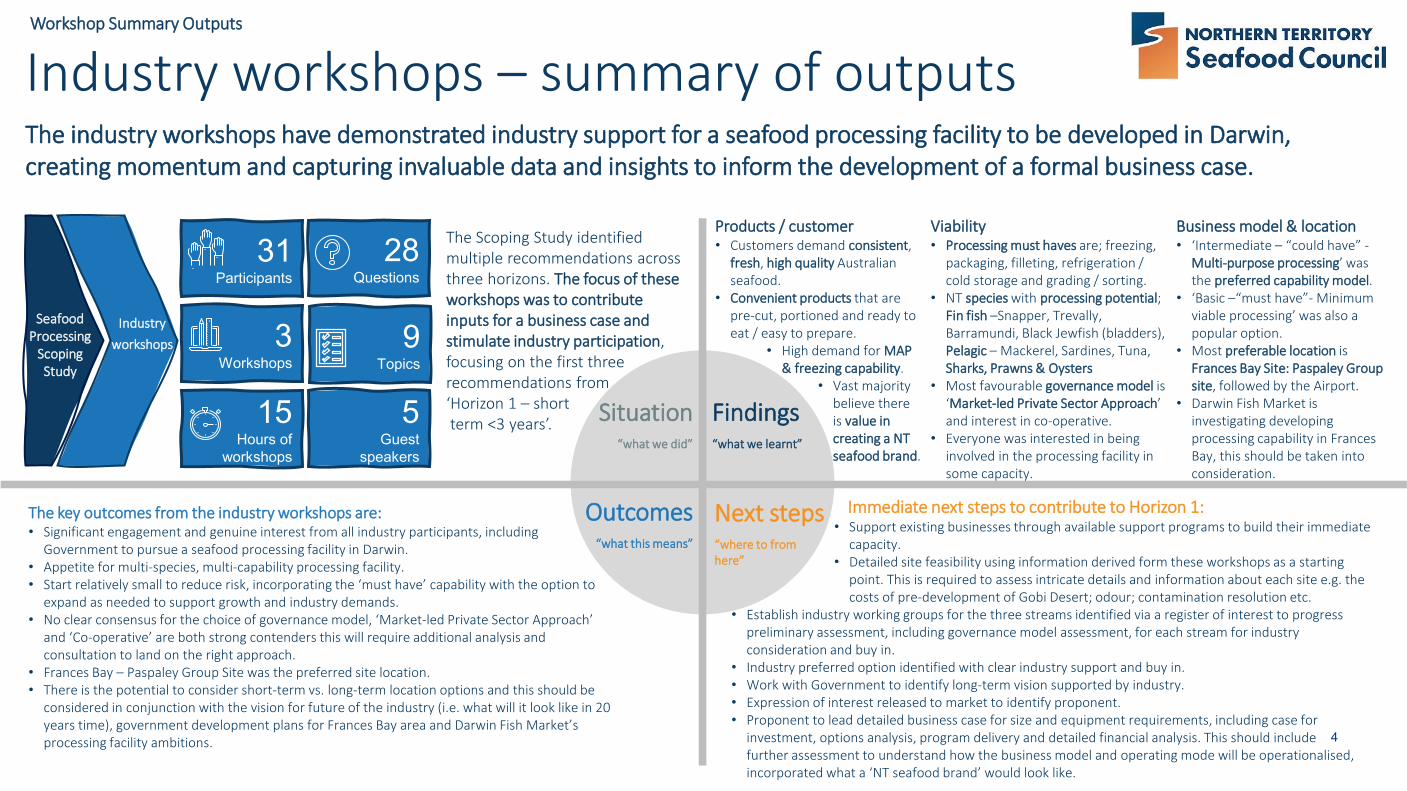

Products / customer• Customers demand consistent,

fresh, high quality Australian seafood.

• Convenient products that are pre-cut, portioned and ready to eat / easy to prepare.

• High demand for MAP & freezing capability.

• Vast majority believe there is value in creating a NT seafood brand.

The Scoping Study identified multiple recommendations across three horizons. The focus of these workshops was to contribute inputs for a business case and stimulate industry participation, focusing on the first three recommendations from‘Horizon 1 – shortterm <3 years’.

Industry workshops – summary of outputsThe industry workshops have demonstrated industry support for a seafood processing facility to be developed in Darwin, creating momentum and capturing invaluable data and insights to inform the development of a formal business case.

Situation“what we did”

Findings“what we learnt”

Outcomes“what this means”

Next steps“where to from here”

31 Participants

3 Workshops

15 Hours of

workshops

28Questions

Seafood Processing

Scoping Study

Industry workshops 9

Topics

5Guest

speakers

Viability• Processing must haves are; freezing,

packaging, filleting, refrigeration / cold storage and grading / sorting.

• NT species with processing potential; Fin fish –Snapper, Trevally, Barramundi, Black Jewfish (bladders), Pelagic – Mackerel, Sardines, Tuna, Sharks, Prawns & Oysters

• Most favourable governance model is ‘Market-led Private Sector Approach’ and interest in co-operative.

• Everyone was interested in being involved in the processing facility in some capacity.

Business model & location• ‘Intermediate – “could have” -

Multi-purpose processing’ was the preferred capability model.

• ‘Basic –“must have”- Minimum viable processing’ was also a popular option.

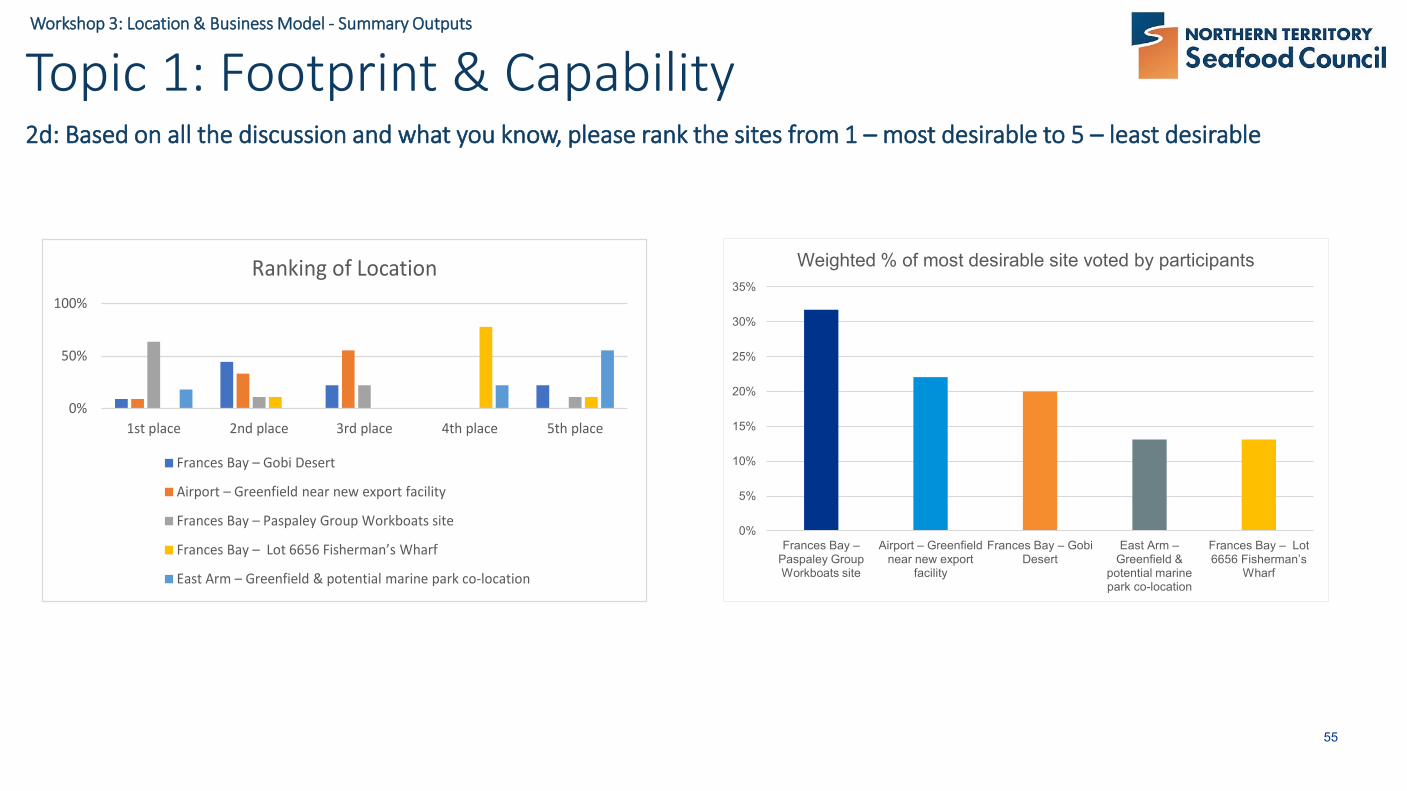

• Most preferable location is Frances Bay Site: Paspaley Group site, followed by the Airport.

• Darwin Fish Market is investigating developing processing capability in Frances Bay, this should be taken into consideration.

The key outcomes from the industry workshops are:• Significant engagement and genuine interest from all industry participants, including

Government to pursue a seafood processing facility in Darwin. • Appetite for multi-species, multi-capability processing facility.• Start relatively small to reduce risk, incorporating the ‘must have’ capability with the option to

expand as needed to support growth and industry demands. • No clear consensus for the choice of governance model, ‘Market-led Private Sector Approach’

and ‘Co-operative’ are both strong contenders this will require additional analysis and consultation to land on the right approach.

• Frances Bay – Paspaley Group Site was the preferred site location. • There is the potential to consider short-term vs. long-term location options and this should be

considered in conjunction with the vision for future of the industry (i.e. what will it look like in 20 years time), government development plans for Frances Bay area and Darwin Fish Market’s processing facility ambitions.

Immediate next steps to contribute to Horizon 1:• Support existing businesses through available support programs to build their immediate

capacity.• Detailed site feasibility using information derived form these workshops as a starting

point. This is required to assess intricate details and information about each site e.g. the costs of pre-development of Gobi Desert; odour; contamination resolution etc.

• Establish industry working groups for the three streams identified via a register of interest to progress preliminary assessment, including governance model assessment, for each stream for industry consideration and buy in.

• Industry preferred option identified with clear industry support and buy in.• Work with Government to identify long-term vision supported by industry.• Expression of interest released to market to identify proponent.• Proponent to lead detailed business case for size and equipment requirements, including case for

investment, options analysis, program delivery and detailed financial analysis. This should include further assessment to understand how the business model and operating mode will be operationalised, incorporated what a ‘NT seafood brand’ would look like.

5

Workshop Summary Outputs

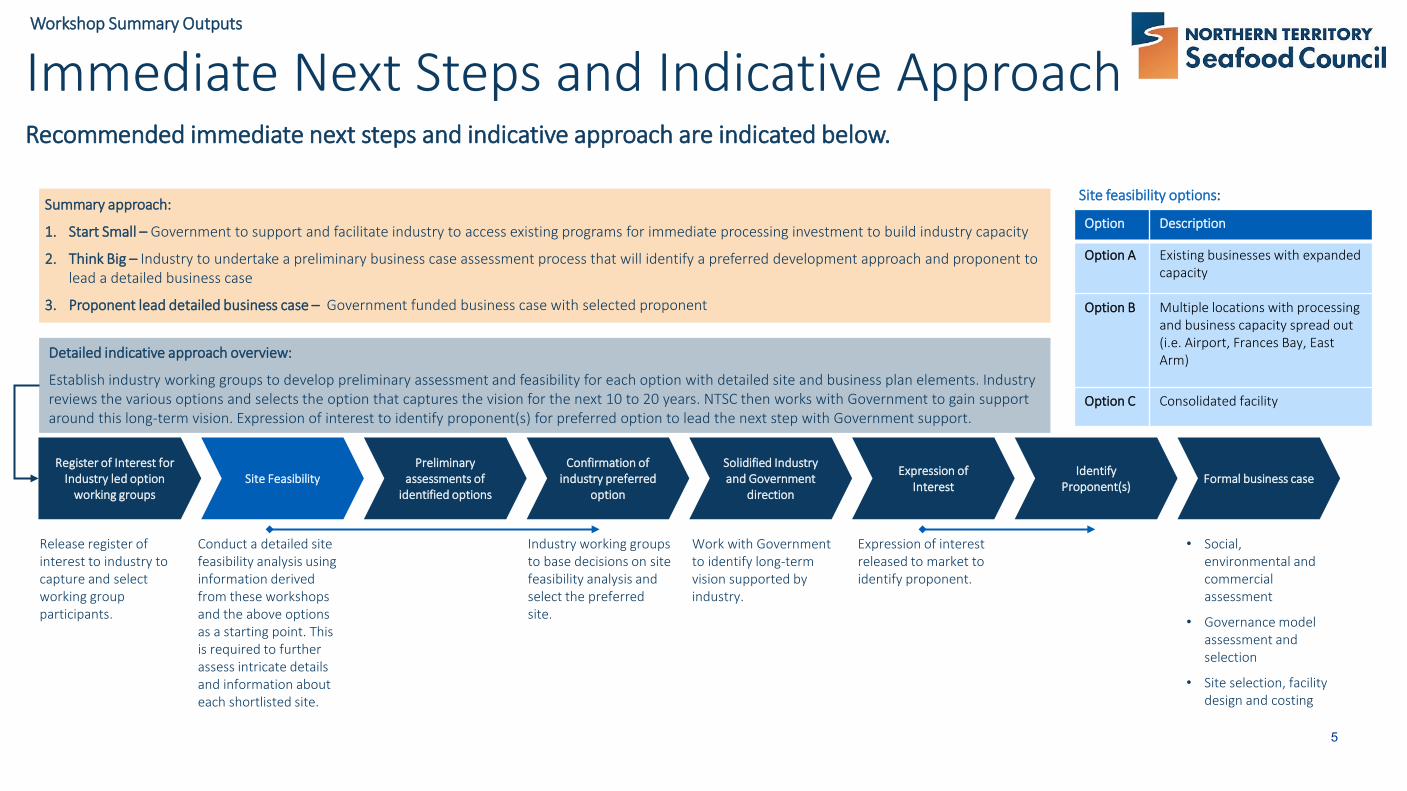

Immediate Next Steps and Indicative Approach Recommended immediate next steps and indicative approach are indicated below.

Register of Interest for Industry led option

working groupsSite Feasibility

Preliminary assessments of

identified options

Confirmation of industry preferred

option

Solidified Industry and Government

direction

Expression of Interest

Identify Proponent(s) Formal business case

Summary approach:

1. Start Small – Government to support and facilitate industry to access existing programs for immediate processing investment to build industry capacity

2. Think Big – Industry to undertake a preliminary business case assessment process that will identify a preferred development approach and proponent to lead a detailed business case

3. Proponent lead detailed business case – Government funded business case with selected proponent

Release register of interest to industry to capture and select working group participants.

Conduct a detailed site feasibility analysis using information derived from these workshops and the above options as a starting point. This is required to further assess intricate details and information about each shortlisted site.

Detailed indicative approach overview:

Establish industry working groups to develop preliminary assessment and feasibility for each option with detailed site and business plan elements. Industry reviews the various options and selects the option that captures the vision for the next 10 to 20 years. NTSC then works with Government to gain support around this long-term vision. Expression of interest to identify proponent(s) for preferred option to lead the next step with Government support.

• Social, environmental and commercial assessment

• Governance model assessment and selection

• Site selection, facility design and costing

Industry working groups to base decisions on site feasibility analysis and select the preferred site.

Expression of interest released to market to identify proponent.

Work with Government to identify long-term vision supported by industry.

Option Description

Option A Existing businesses with expandedcapacity

Option B Multiple locations with processing and business capacity spread out (i.e. Airport, Frances Bay, East Arm)

Option C Consolidated facility

Site feasibility options:

6

Background and context

7

Workshop Summary Outputs

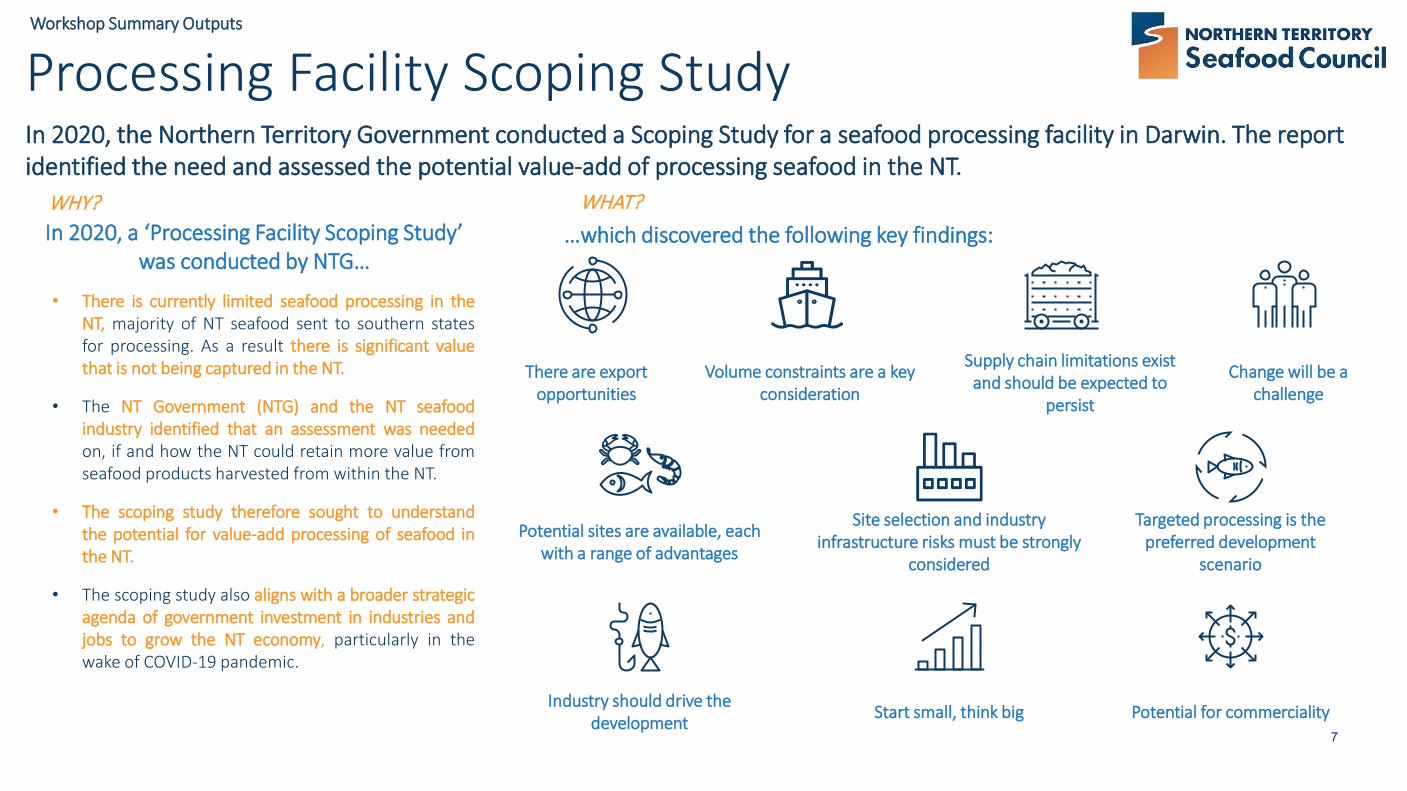

Processing Facility Scoping StudyIn 2020, the Northern Territory Government conducted a Scoping Study for a seafood processing facility in Darwin. The report identified the need and assessed the potential value-add of processing seafood in the NT.

• There is currently limited seafood processing in theNT, majority of NT seafood sent to southern statesfor processing. As a result there is significant valuethat is not being captured in the NT.

• The NT Government (NTG) and the NT seafoodindustry identified that an assessment was neededon, if and how the NT could retain more value fromseafood products harvested from within the NT.

• The scoping study therefore sought to understandthe potential for value-add processing of seafood inthe NT.

• The scoping study also aligns with a broader strategicagenda of government investment in industries andjobs to grow the NT economy, particularly in thewake of COVID-19 pandemic.

In 2020, a ‘Processing Facility Scoping Study’ was conducted by NTG…

…which discovered the following key findings: WHY? WHAT?

Volume constraints are a key consideration

Supply chain limitations exist and should be expected to

persist

There are export opportunities

Change will be a challenge

Potential sites are available, each with a range of advantages

Site selection and industry infrastructure risks must be strongly

considered

Potential for commerciality

Targeted processing is the preferred development

scenario

Industry should drive the development Start small, think big

8

Workshop Summary Outputs

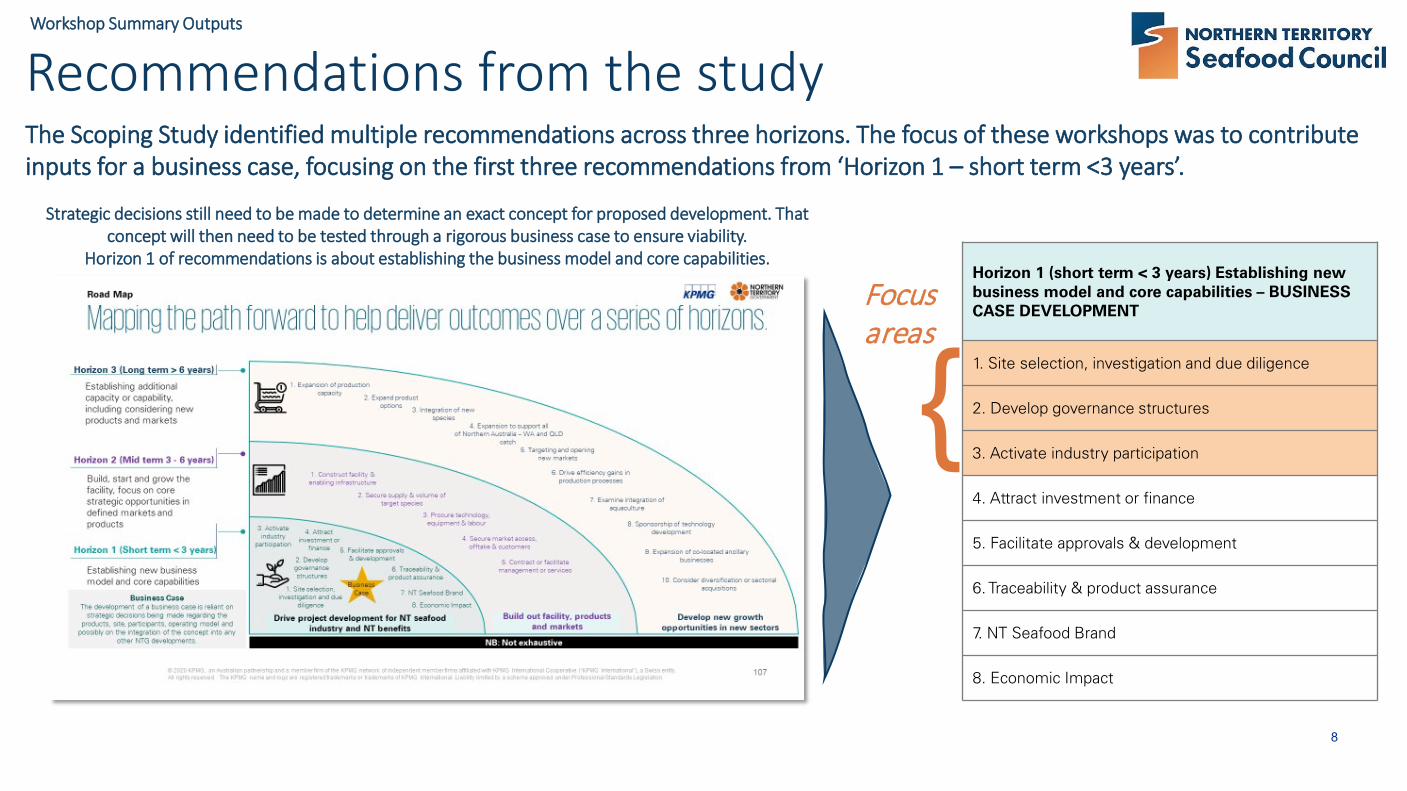

Recommendations from the study The Scoping Study identified multiple recommendations across three horizons. The focus of these workshops was to contribute inputs for a business case, focusing on the first three recommendations from ‘Horizon 1 – short term <3 years’.

Horizon 1 (short term < 3 years) Establishing new business model and core capabilities – BUSINESS CASE DEVELOPMENT

1. Site selection, investigation and due diligence

2. Develop governance structures

3. Activate industry participation

4. Attract investment or finance

5. Facilitate approvals & development

6. Traceability & product assurance

7. NT Seafood Brand

8. Economic Impact

{Focus areas

Strategic decisions still need to be made to determine an exact concept for proposed development. That concept will then need to be tested through a rigorous business case to ensure viability.

Horizon 1 of recommendations is about establishing the business model and core capabilities.

9

Workshop Summary Outputs

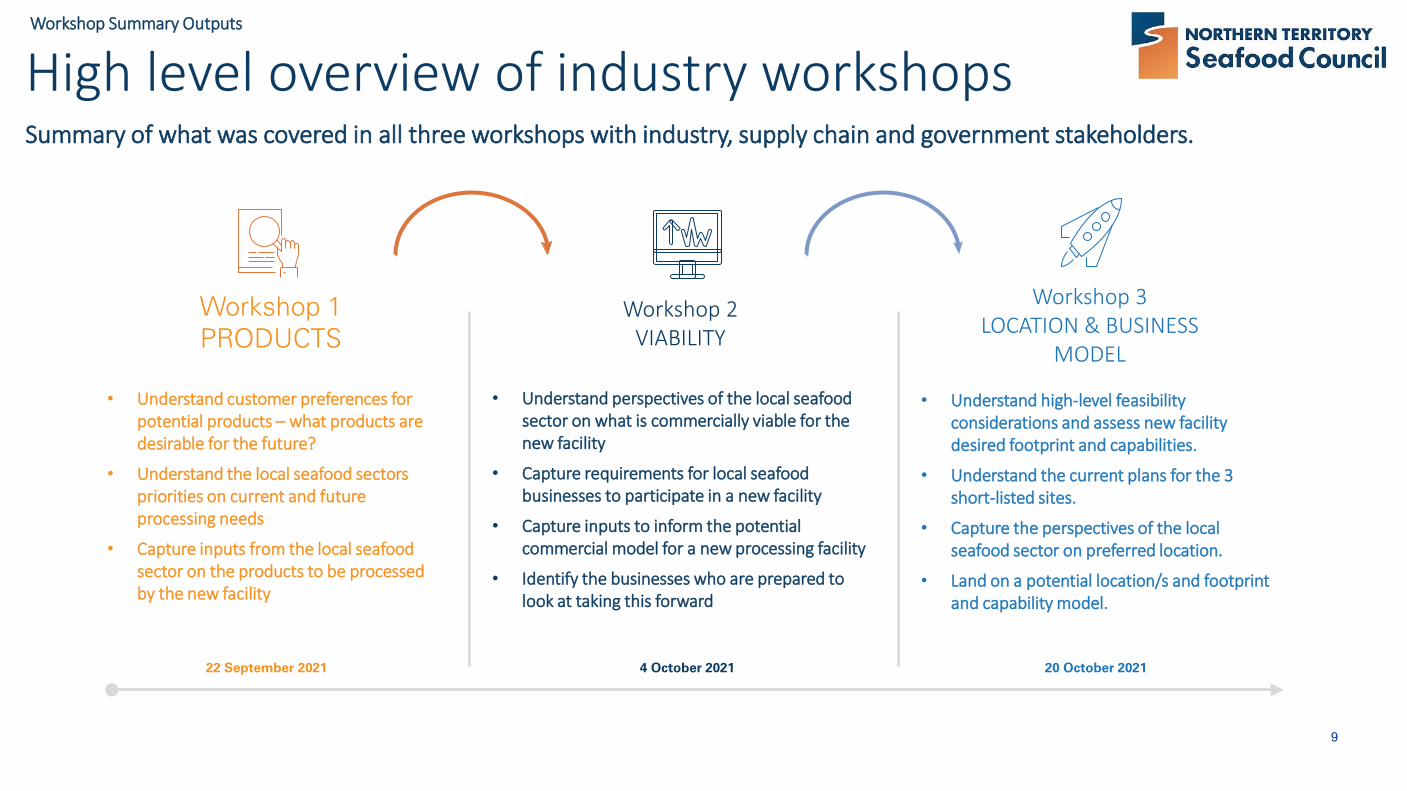

High level overview of industry workshopsSummary of what was covered in all three workshops with industry, supply chain and government stakeholders.

Workshop 2VIABILITY

Workshop 3LOCATION & BUSINESS

MODEL

• Understand high-level feasibility considerations and assess new facility desired footprint and capabilities.

• Understand the current plans for the 3 short-listed sites.

• Capture the perspectives of the local seafood sector on preferred location.

• Land on a potential location/s and footprint and capability model.

• Understand perspectives of the local seafood sector on what is commercially viable for the new facility

• Capture requirements for local seafood businesses to participate in a new facility

• Capture inputs to inform the potential commercial model for a new processing facility

• Identify the businesses who are prepared to look at taking this forward

4 October 2021 20 October 2021

Workshop 1 PRODUCTS

• Understand customer preferences for potential products – what products are desirable for the future?

• Understand the local seafood sectors priorities on current and future processing needs

• Capture inputs from the local seafood sector on the products to be processed by the new facility

22 September 2021

10

Workshop 1: Products

11

Workshop 1: Products - Summary Outputs

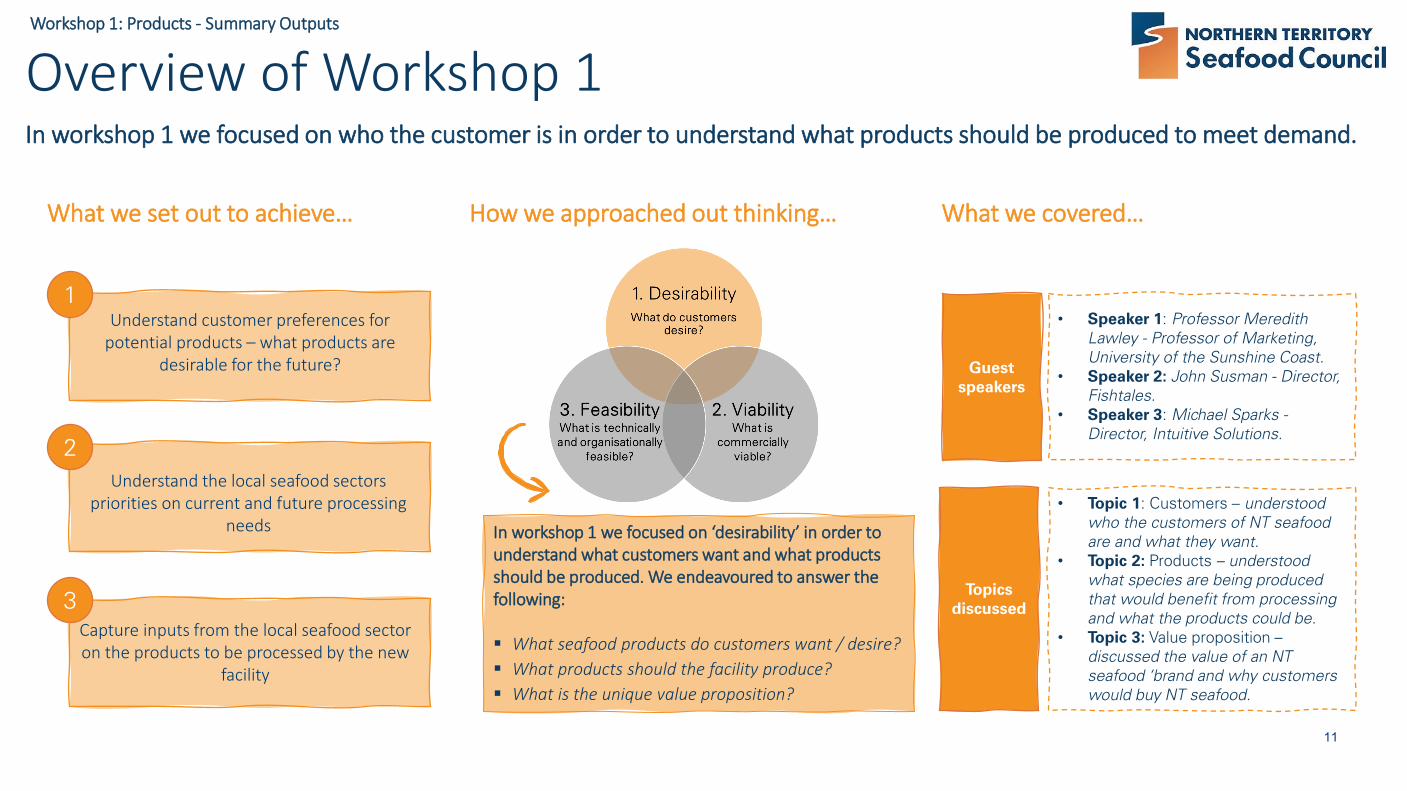

Overview of Workshop 1 In workshop 1 we focused on who the customer is in order to understand what products should be produced to meet demand.

Understand customer preferences for potential products – what products are

desirable for the future?

Understand the local seafood sectors priorities on current and future processing

needs

Capture inputs from the local seafood sector on the products to be processed by the new

facility

1

3

2

What we set out to achieve…

In workshop 1 we focused on ‘desirability’ in order to understand what customers want and what products should be produced. We endeavoured to answer the following:

What seafood products do customers want / desire? What products should the facility produce? What is the unique value proposition?

How we approached out thinking… What we covered…

Guest speakers

• Speaker 1: Professor Meredith Lawley - Professor of Marketing, University of the Sunshine Coast.

• Speaker 2: John Susman - Director, Fishtales.

• Speaker 3: Michael Sparks -Director, Intuitive Solutions.

Topics discussed

• Topic 1: Customers – understood who the customers of NT seafood are and what they want.

• Topic 2: Products – understood what species are being produced that would benefit from processing and what the products could be.

• Topic 3: Value proposition –discussed the value of an NT seafood ‘brand and why customers would buy NT seafood.

12

Workshop 1: Products - Summary Outputs

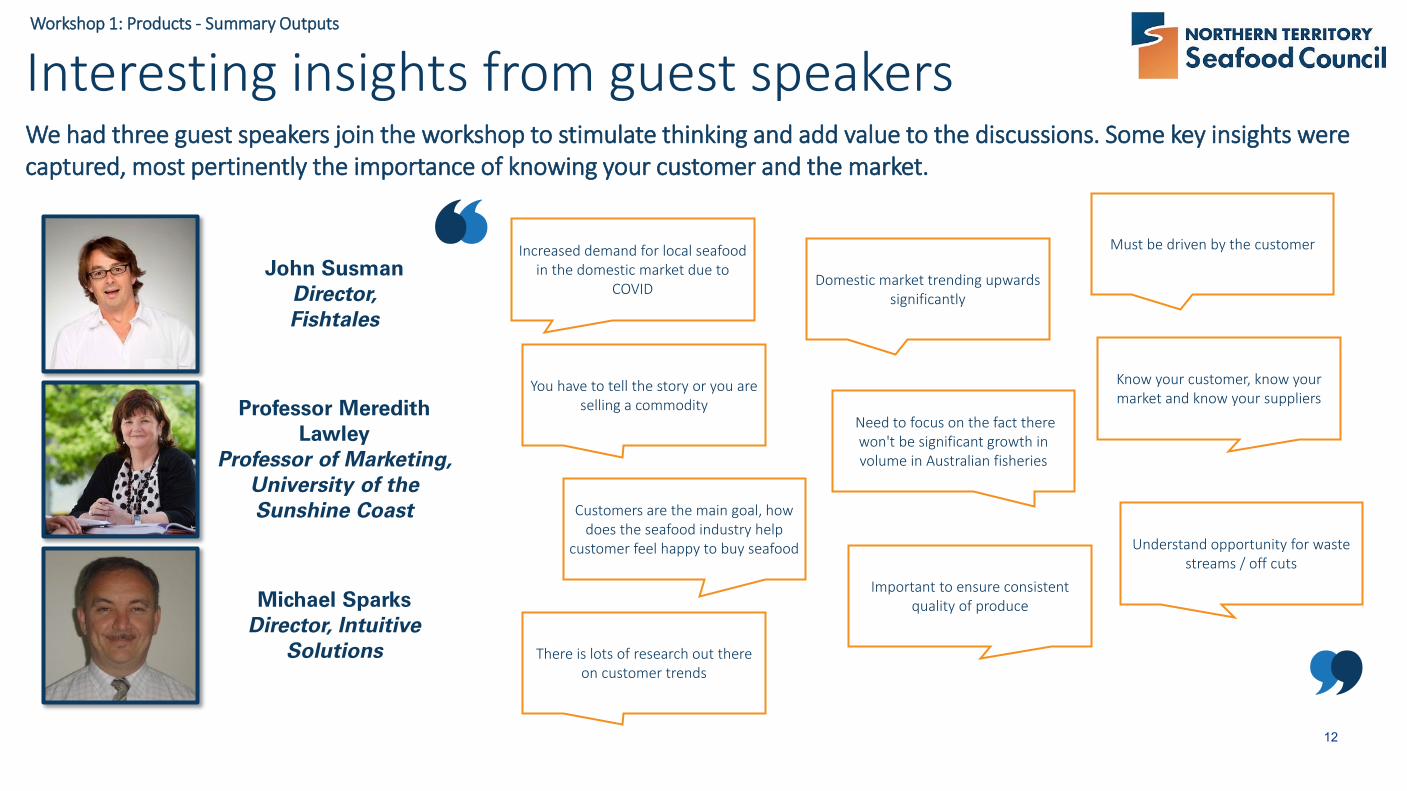

Interesting insights from guest speakersWe had three guest speakers join the workshop to stimulate thinking and add value to the discussions. Some key insights were captured, most pertinently the importance of knowing your customer and the market.

John SusmanDirector, Fishtales

Professor Meredith Lawley

Professor of Marketing, University of the Sunshine Coast

Michael SparksDirector, Intuitive

Solutions

Increased demand for local seafood in the domestic market due to

COVID

You have to tell the story or you are selling a commodity

Domestic market trending upwards significantly

Customers are the main goal, how does the seafood industry help

customer feel happy to buy seafood

Need to focus on the fact there won't be significant growth in volume in Australian fisheries

There is lots of research out there on customer trends

Must be driven by the customer

Know your customer, know your market and know your suppliers

Important to ensure consistent quality of produce

Understand opportunity for waste streams / off cuts

13

Workshop 1: Products - Summary Outputs

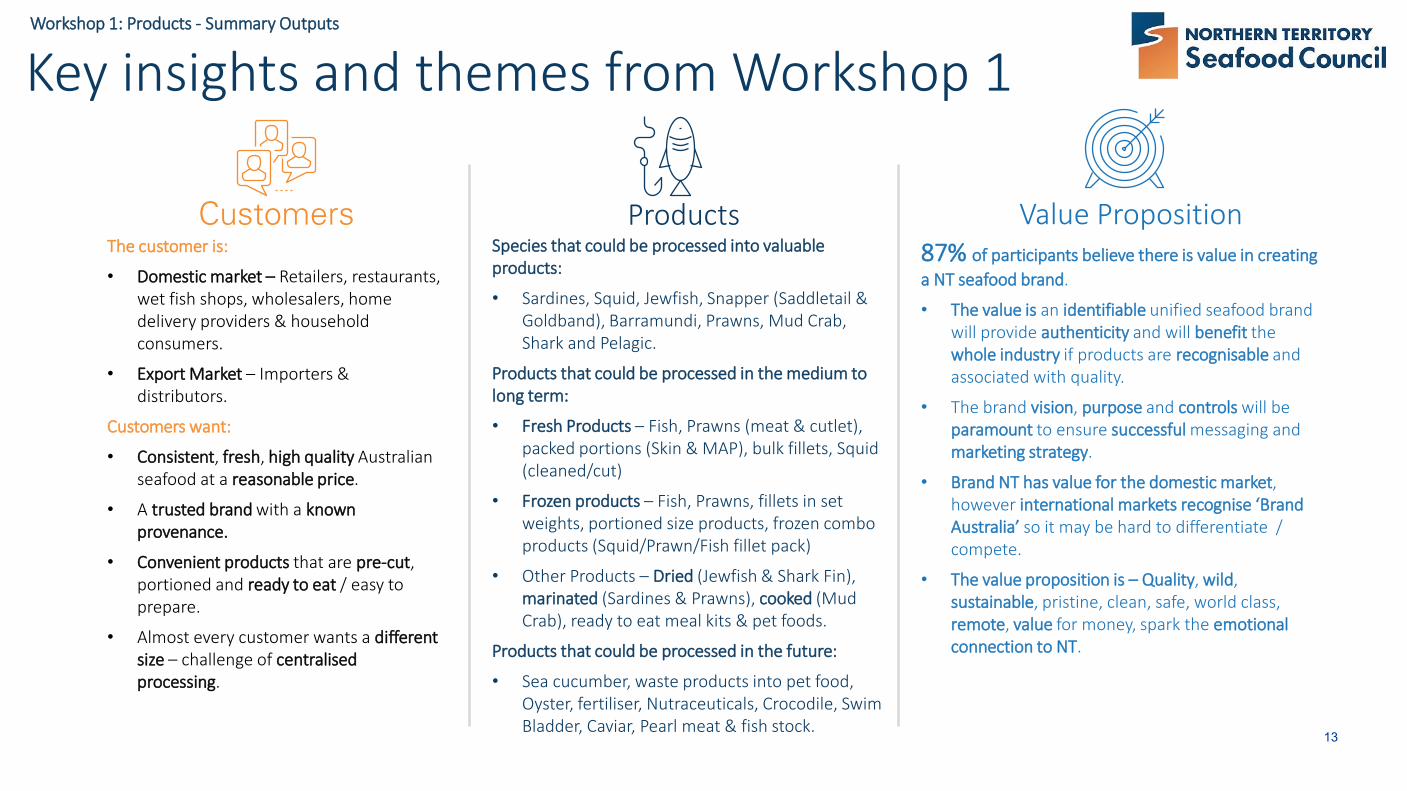

Key insights and themes from Workshop 1

Products Value Proposition87% of participants believe there is value in creating a NT seafood brand.

• The value is an identifiable unified seafood brand will provide authenticity and will benefit the whole industry if products are recognisable and associated with quality.

• The brand vision, purpose and controls will be paramount to ensure successful messaging and marketing strategy.

• Brand NT has value for the domestic market, however international markets recognise ‘Brand Australia’ so it may be hard to differentiate / compete.

• The value proposition is – Quality, wild, sustainable, pristine, clean, safe, world class, remote, value for money, spark the emotionalconnection to NT.

Species that could be processed into valuable products:

• Sardines, Squid, Jewfish, Snapper (Saddletail & Goldband), Barramundi, Prawns, Mud Crab, Shark and Pelagic.

Products that could be processed in the medium to long term:

• Fresh Products – Fish, Prawns (meat & cutlet), packed portions (Skin & MAP), bulk fillets, Squid (cleaned/cut)

• Frozen products – Fish, Prawns, fillets in set weights, portioned size products, frozen combo products (Squid/Prawn/Fish fillet pack)

• Other Products – Dried (Jewfish & Shark Fin), marinated (Sardines & Prawns), cooked (Mud Crab), ready to eat meal kits & pet foods.

Products that could be processed in the future:

• Sea cucumber, waste products into pet food, Oyster, fertiliser, Nutraceuticals, Crocodile, Swim Bladder, Caviar, Pearl meat & fish stock.

CustomersThe customer is:

• Domestic market – Retailers, restaurants, wet fish shops, wholesalers, home delivery providers & household consumers.

• Export Market – Importers & distributors.

Customers want:

• Consistent, fresh, high quality Australian seafood at a reasonable price.

• A trusted brand with a known provenance.

• Convenient products that are pre-cut, portioned and ready to eat / easy to prepare.

• Almost every customer wants a different size – challenge of centralised processing.

14

Workshop 1: Products - Summary Outputs

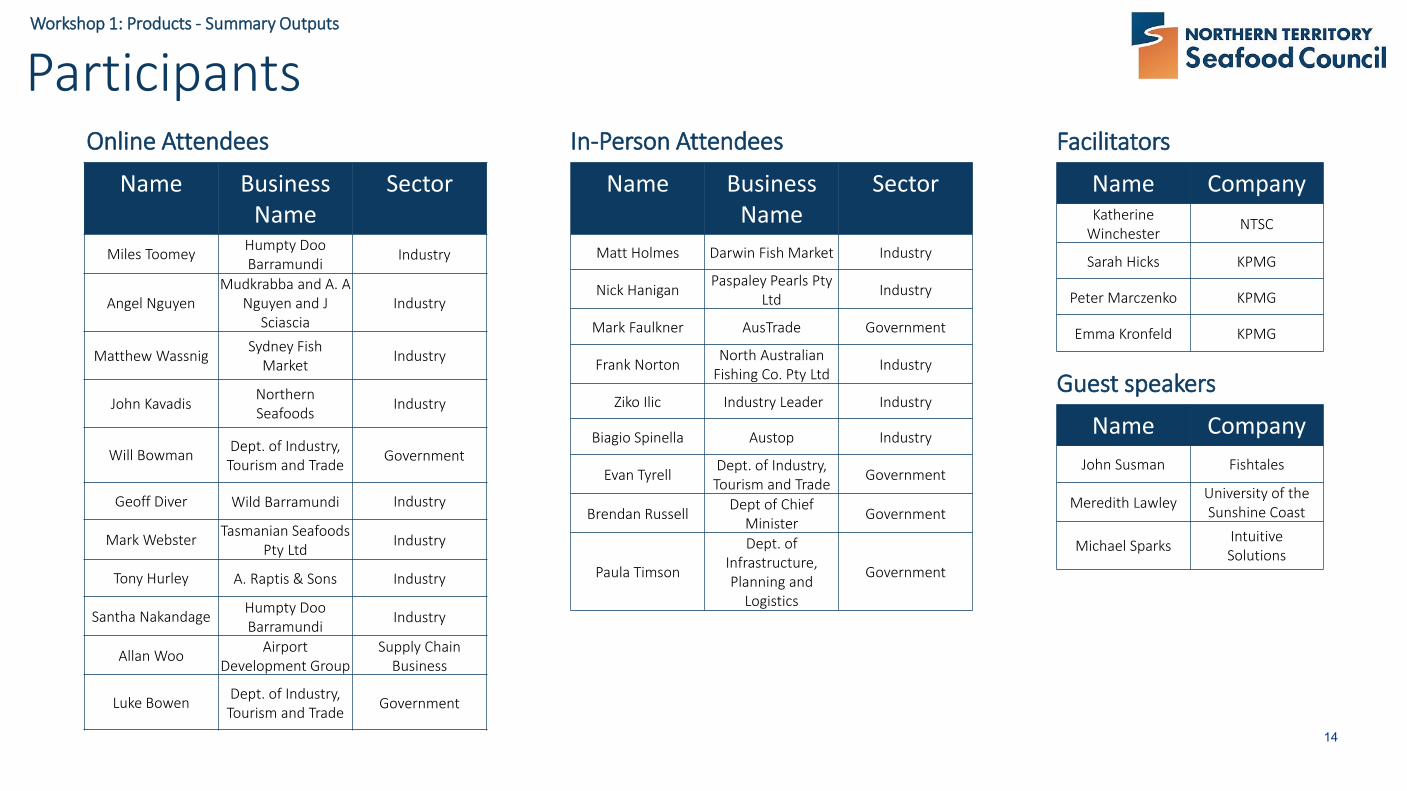

Participants

Name Business Name

Sector

Miles Toomey Humpty Doo Barramundi Industry

Angel Nguyen Mudkrabba and A. A

Nguyen and J Sciascia

Industry

Matthew Wassnig Sydney Fish Market Industry

John Kavadis Northern Seafoods Industry

Will Bowman Dept. of Industry, Tourism and Trade Government

Geoff Diver Wild Barramundi Industry

Mark Webster Tasmanian Seafoods Pty Ltd Industry

Tony Hurley A. Raptis & Sons Industry

Santha Nakandage Humpty Doo Barramundi Industry

Allan Woo Airport Development Group

Supply Chain Business

Luke Bowen Dept. of Industry, Tourism and Trade Government

Name Business Name

Sector

Matt Holmes Darwin Fish Market Industry

Nick Hanigan Paspaley Pearls Pty Ltd Industry

Mark Faulkner AusTrade Government

Frank Norton North Australian Fishing Co. Pty Ltd Industry

Ziko Ilic Industry Leader Industry

Biagio Spinella Austop Industry

Evan Tyrell Dept. of Industry, Tourism and Trade Government

Brendan Russell Dept of Chief Minister Government

Paula Timson

Dept. of Infrastructure, Planning and

Logistics

Government

Name CompanyKatherine

Winchester NTSC

Sarah Hicks KPMG

Peter Marczenko KPMG

Emma Kronfeld KPMG

Facilitators

Name CompanyJohn Susman Fishtales

Meredith Lawley University of the Sunshine Coast

Michael Sparks Intuitive Solutions

Guest speakers

In-Person AttendeesOnline Attendees

15

Workshop 2 : Viability

16

Workshop 2: Viability - Summary Outputs

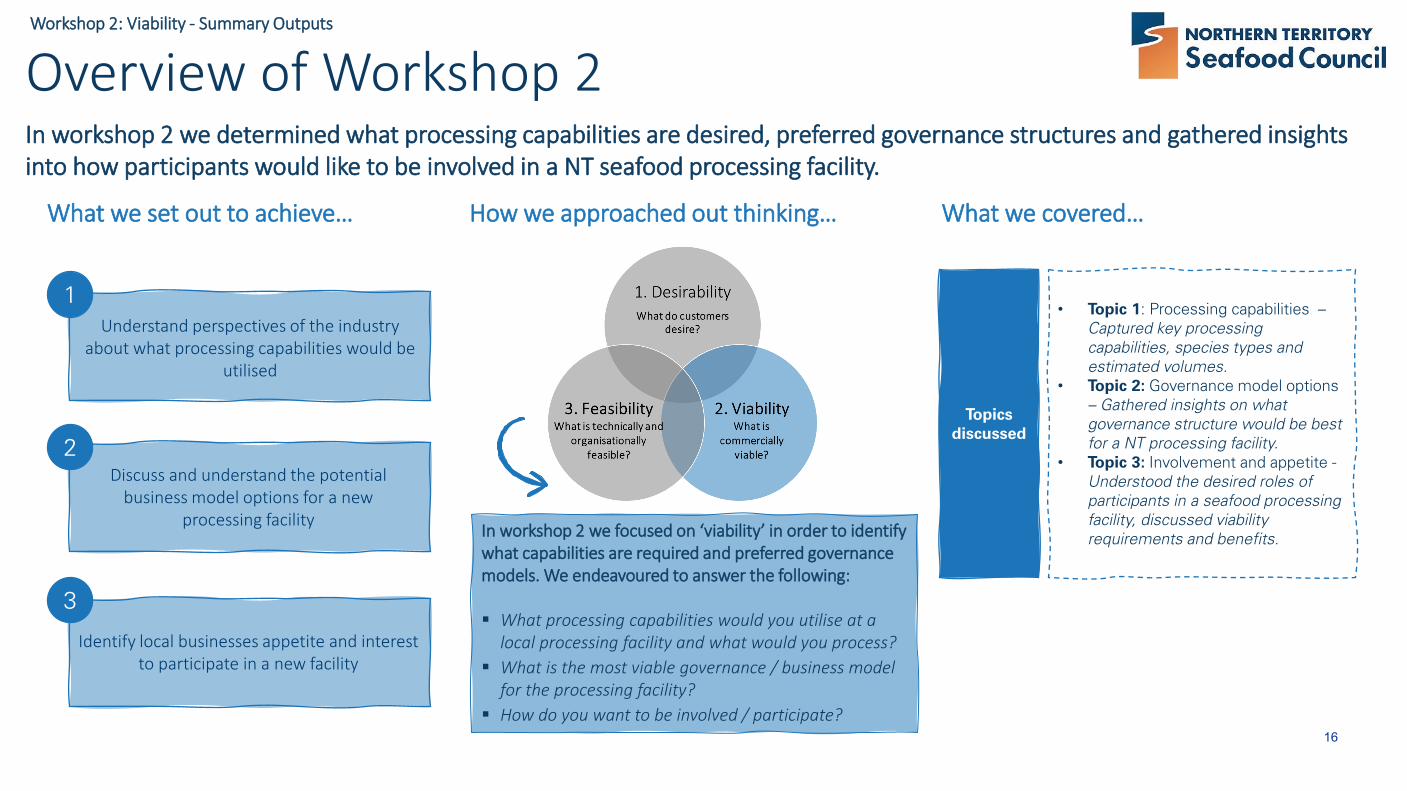

Overview of Workshop 2 In workshop 2 we determined what processing capabilities are desired, preferred governance structures and gathered insights into how participants would like to be involved in a NT seafood processing facility.

Understand perspectives of the industry about what processing capabilities would be

utilised

Discuss and understand the potential business model options for a new

processing facility

Identify local businesses appetite and interest to participate in a new facility

1

3

2

What we set out to achieve…

In workshop 2 we focused on ‘viability’ in order to identify what capabilities are required and preferred governance models. We endeavoured to answer the following:

What processing capabilities would you utilise at a local processing facility and what would you process?

What is the most viable governance / business model for the processing facility?

How do you want to be involved / participate?

How we approached out thinking… What we covered…

Topics discussed

• Topic 1: Processing capabilities –Captured key processing capabilities, species types and estimated volumes.

• Topic 2: Governance model options– Gathered insights on what governance structure would be best for a NT processing facility.

• Topic 3: Involvement and appetite -Understood the desired roles of participants in a seafood processing facility, discussed viability requirements and benefits.

17

Workshop 2: Viability - Summary Outputs

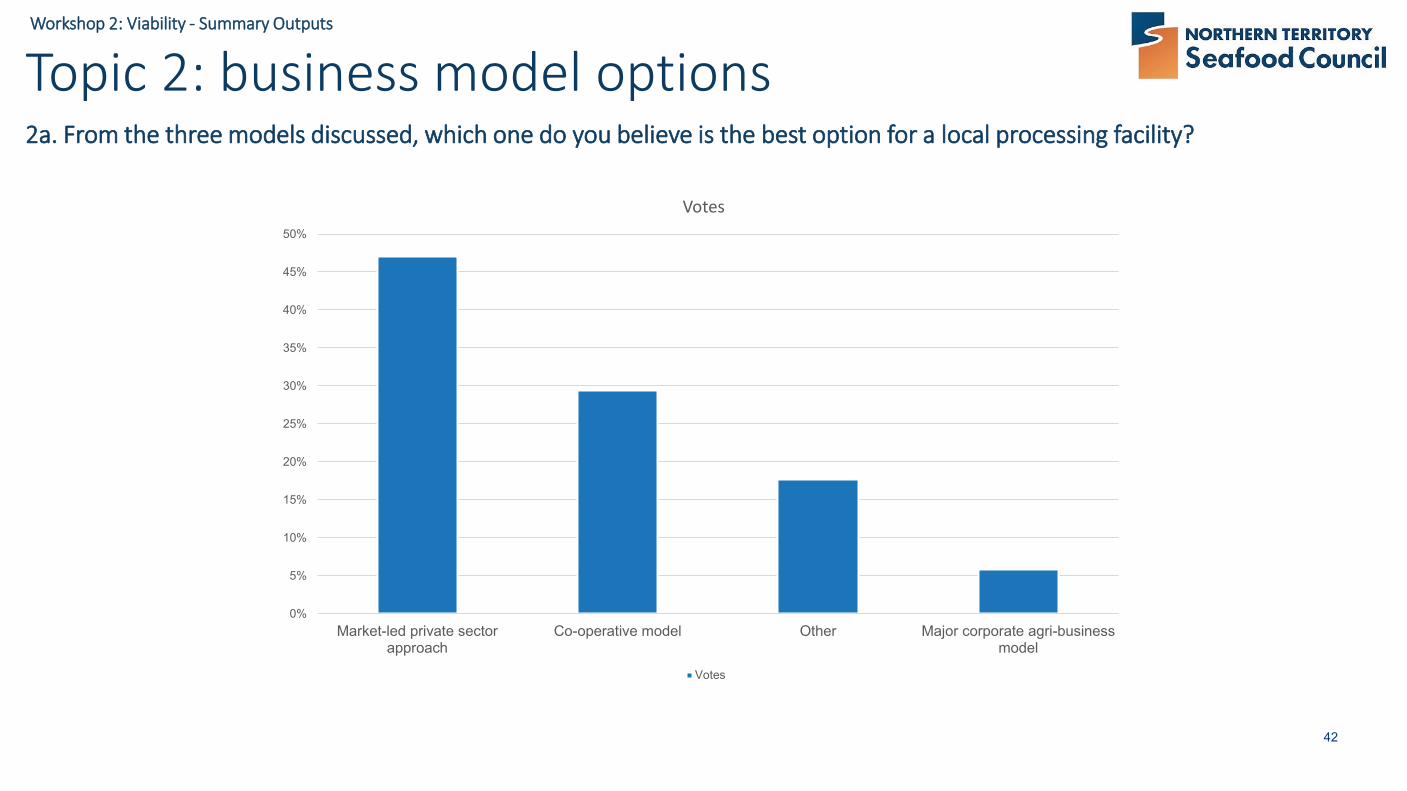

0%10%20%30%40%50%

Market-ledprivate sector

approach

Co-operativemodel

Other Majorcorporate

agri-businessmodelVotes

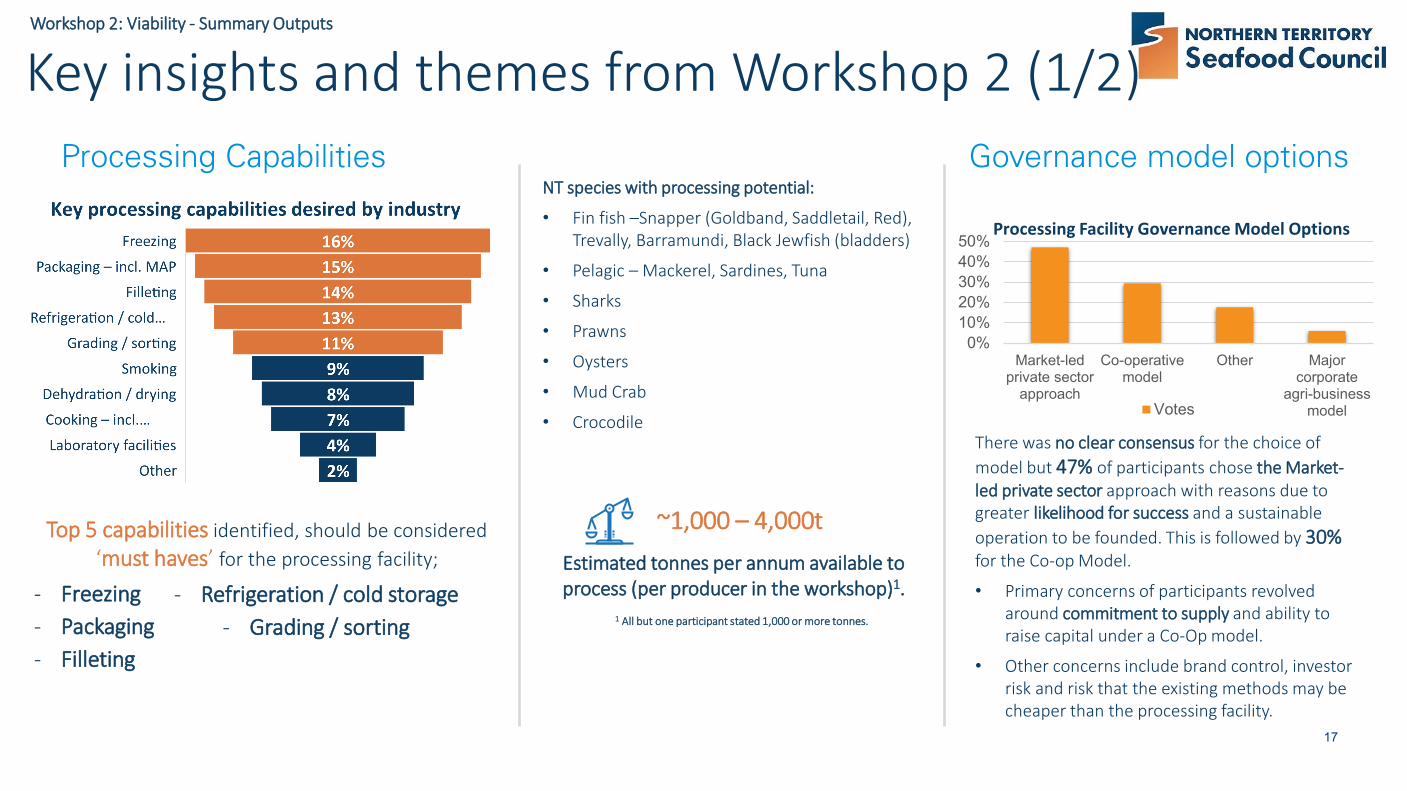

Key insights and themes from Workshop 2 (1/2)Processing Capabilities

NT species with processing potential:

• Fin fish –Snapper (Goldband, Saddletail, Red), Trevally, Barramundi, Black Jewfish (bladders)

• Pelagic – Mackerel, Sardines, Tuna

• Sharks

• Prawns

• Oysters

• Mud Crab

• Crocodile

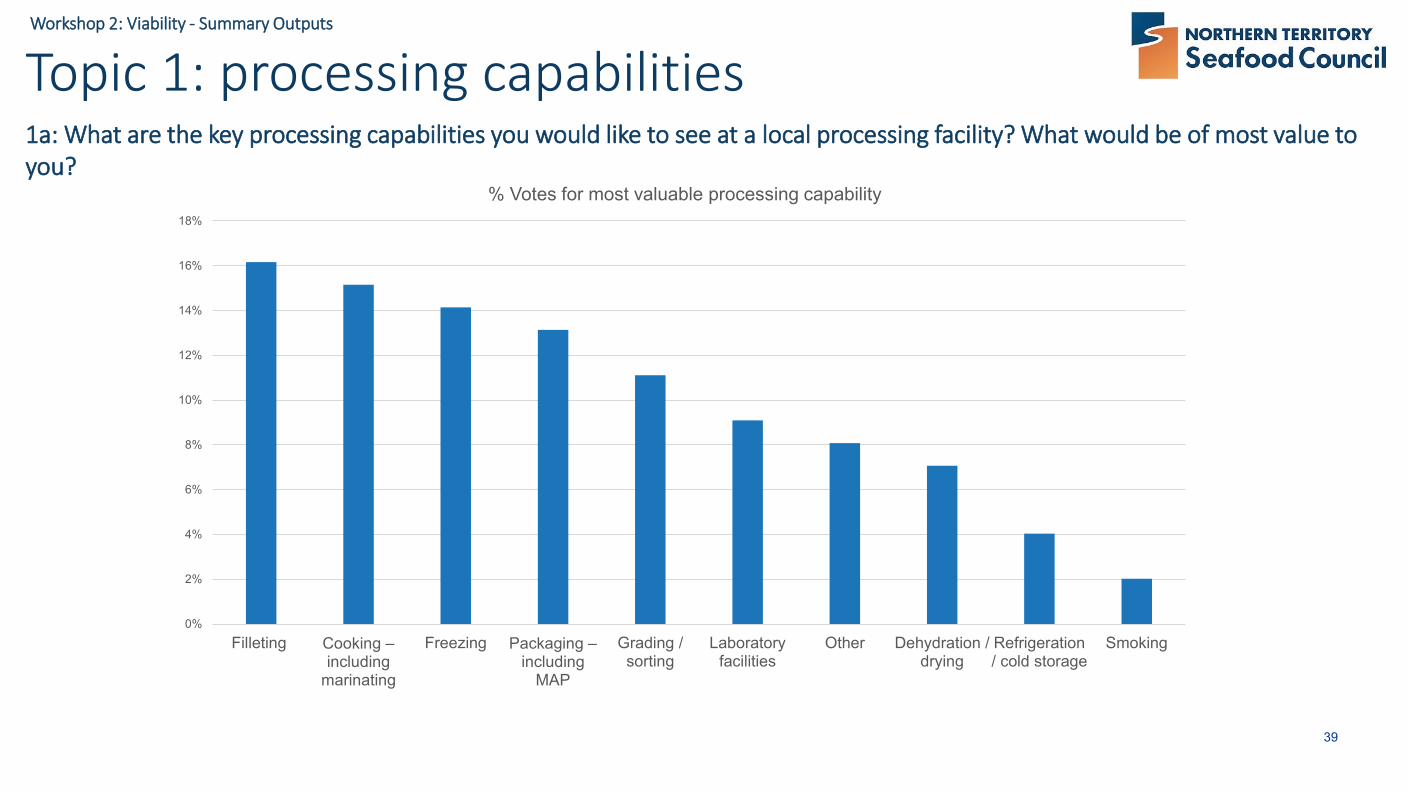

Top 5 capabilities identified, should be considered ‘must haves’ for the processing facility;

- Freezing - Packaging - Filleting

- Refrigeration / cold storage - Grading / sorting

Estimated tonnes per annum available to process (per producer in the workshop)1.

~1,000 – 4,000t

1 All but one participant stated 1,000 or more tonnes.

There was no clear consensus for the choice of model but 47% of participants chose the Market-led private sector approach with reasons due to greater likelihood for success and a sustainable operation to be founded. This is followed by 30%for the Co-op Model.

• Primary concerns of participants revolved around commitment to supply and ability to raise capital under a Co-Op model.

• Other concerns include brand control, investor risk and risk that the existing methods may be cheaper than the processing facility.

Processing Facility Governance Model Options

Governance model options

18

Workshop 2: Viability - Summary Outputs

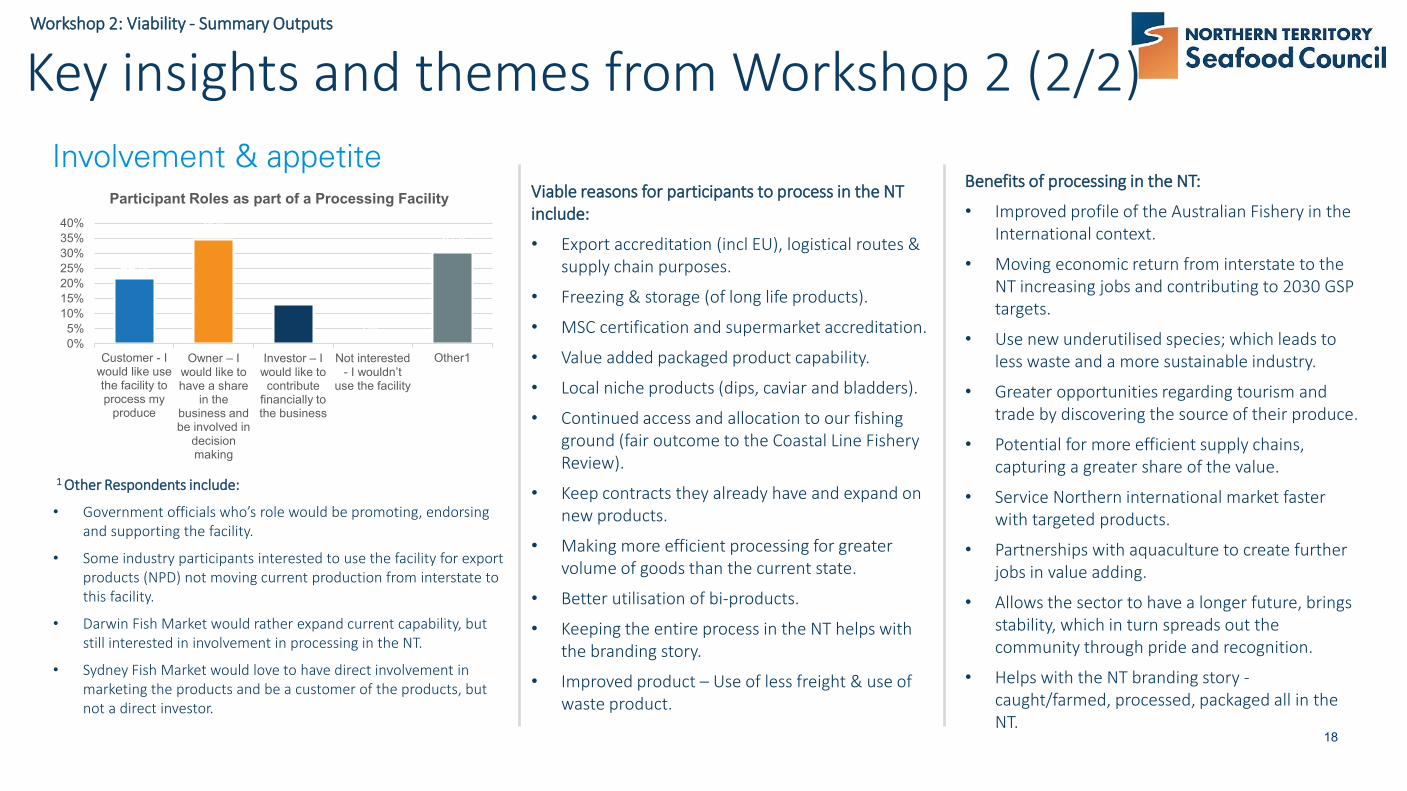

Key insights and themes from Workshop 2 (2/2)Involvement & appetite

1 Other Respondents include:

• Government officials who’s role would be promoting, endorsing and supporting the facility.

• Some industry participants interested to use the facility for export products (NPD) not moving current production from interstate to this facility.

• Darwin Fish Market would rather expand current capability, but still interested in involvement in processing in the NT.

• Sydney Fish Market would love to have direct involvement in marketing the products and be a customer of the products, but not a direct investor.

22%

35%

13%

0%

30%

0%5%

10%15%20%25%30%35%40%

Customer - Iwould like usethe facility toprocess my

produce

Owner – I would like to have a share

in the business and be involved in

decision making

Investor – I would like to contribute

financially to the business

Not interested - I wouldn’t

use the facility

Other1

Participant Roles as part of a Processing Facility Viable reasons for participants to process in the NT include:

• Export accreditation (incl EU), logistical routes & supply chain purposes.

• Freezing & storage (of long life products).

• MSC certification and supermarket accreditation.

• Value added packaged product capability.

• Local niche products (dips, caviar and bladders).

• Continued access and allocation to our fishing ground (fair outcome to the Coastal Line Fishery Review).

• Keep contracts they already have and expand on new products.

• Making more efficient processing for greater volume of goods than the current state.

• Better utilisation of bi-products.

• Keeping the entire process in the NT helps with the branding story.

• Improved product – Use of less freight & use of waste product.

Benefits of processing in the NT:

• Improved profile of the Australian Fishery in the International context.

• Moving economic return from interstate to the NT increasing jobs and contributing to 2030 GSP targets.

• Use new underutilised species; which leads to less waste and a more sustainable industry.

• Greater opportunities regarding tourism and trade by discovering the source of their produce.

• Potential for more efficient supply chains, capturing a greater share of the value.

• Service Northern international market faster with targeted products.

• Partnerships with aquaculture to create further jobs in value adding.

• Allows the sector to have a longer future, brings stability, which in turn spreads out the community through pride and recognition.

• Helps with the NT branding story -caught/farmed, processed, packaged all in the NT.

19

Workshop 2: Viability - Summary Outputs

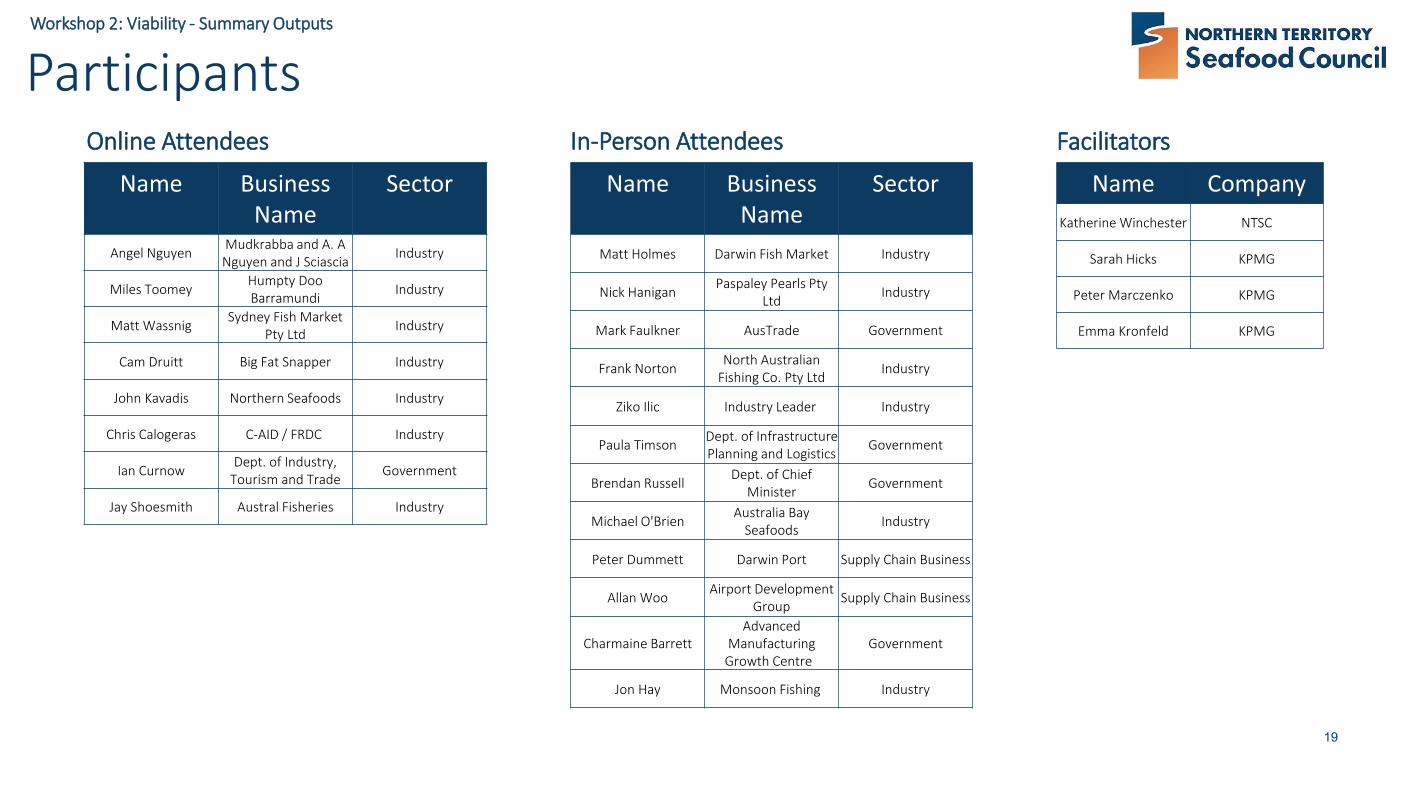

Participants

Name Business Name

Sector

Angel Nguyen Mudkrabba and A. A Nguyen and J Sciascia Industry

Miles Toomey Humpty Doo Barramundi Industry

Matt Wassnig Sydney Fish Market Pty Ltd Industry

Cam Druitt Big Fat Snapper Industry

John Kavadis Northern Seafoods Industry

Chris Calogeras C-AID / FRDC Industry

Ian Curnow Dept. of Industry, Tourism and Trade Government

Jay Shoesmith Austral Fisheries Industry

Name Business Name

Sector

Matt Holmes Darwin Fish Market Industry

Nick Hanigan Paspaley Pearls Pty Ltd Industry

Mark Faulkner AusTrade Government

Frank Norton North Australian Fishing Co. Pty Ltd Industry

Ziko Ilic Industry Leader Industry

Paula Timson Dept. of Infrastructure Planning and Logistics Government

Brendan Russell Dept. of Chief Minister Government

Michael O'Brien Australia Bay Seafoods Industry

Peter Dummett Darwin Port Supply Chain Business

Allan Woo Airport Development Group Supply Chain Business

Charmaine BarrettAdvanced

Manufacturing Growth Centre

Government

Jon Hay Monsoon Fishing Industry

Name CompanyKatherine Winchester NTSC

Sarah Hicks KPMG

Peter Marczenko KPMG

Emma Kronfeld KPMG

Facilitators In-Person AttendeesOnline Attendees

20

Workshop 3: Location & Business Model

21

Workshop 3: Location & Business Model - Summary Outputs

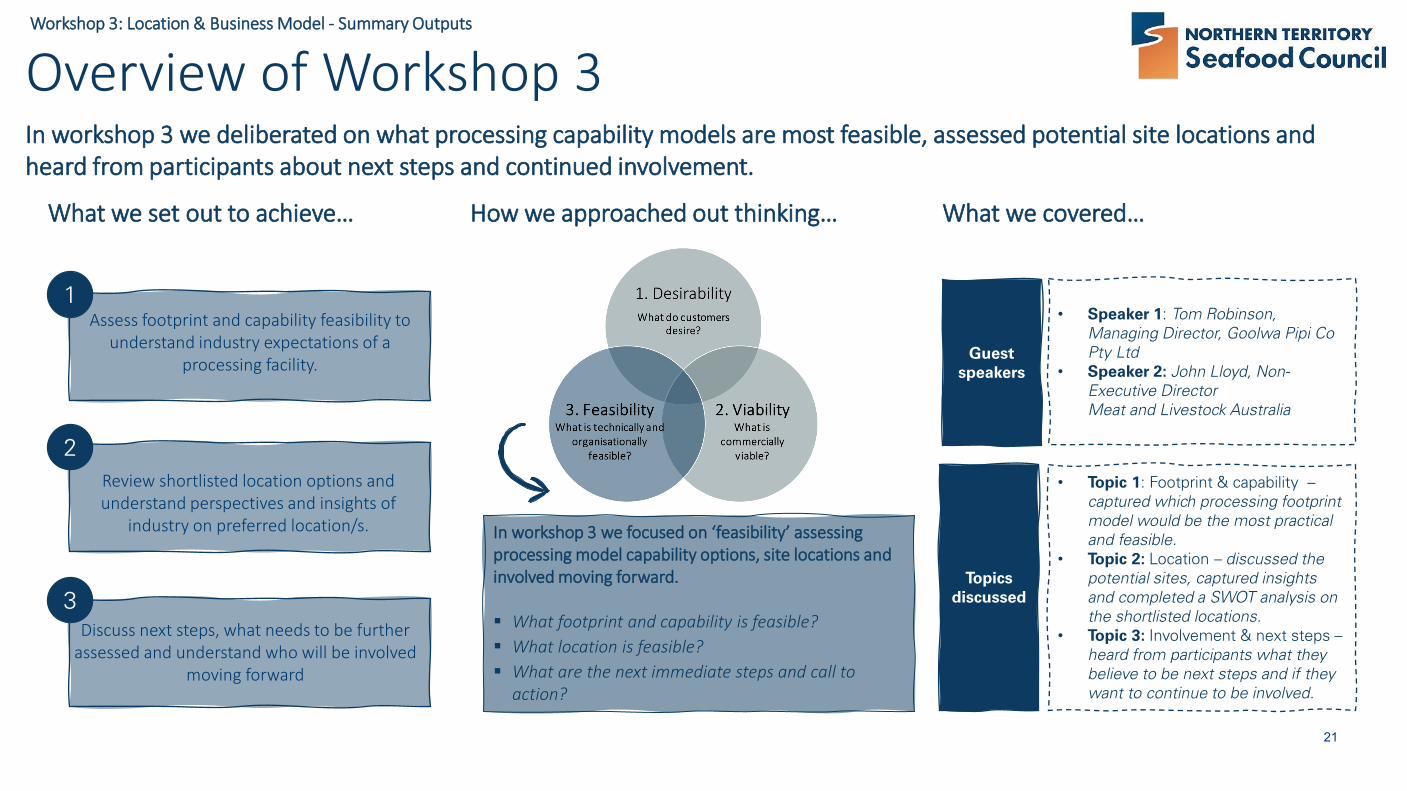

Overview of Workshop 3 In workshop 3 we deliberated on what processing capability models are most feasible, assessed potential site locations and heard from participants about next steps and continued involvement.

Assess footprint and capability feasibility to understand industry expectations of a

processing facility.

Review shortlisted location options and understand perspectives and insights of

industry on preferred location/s.

Discuss next steps, what needs to be further assessed and understand who will be involved

moving forward

1

3

2

What we set out to achieve…

In workshop 3 we focused on ‘feasibility’ assessing processing model capability options, site locations and involved moving forward.

What footprint and capability is feasible? What location is feasible? What are the next immediate steps and call to

action?

How we approached out thinking… What we covered…

Guest speakers

• Speaker 1: Tom Robinson, Managing Director, Goolwa Pipi Co Pty Ltd

• Speaker 2: John Lloyd, Non-Executive Director Meat and Livestock Australia

Topics discussed

• Topic 1: Footprint & capability –captured which processing footprint model would be the most practical and feasible.

• Topic 2: Location – discussed the potential sites, captured insights and completed a SWOT analysis on the shortlisted locations.

• Topic 3: Involvement & next steps –heard from participants what they believe to be next steps and if they want to continue to be involved.

22

Workshop 3: Location & Business Model - Summary Outputs

Interesting insights from guest speakersWe had two guest speakers join the workshop to share insights on seafood processing success stories and governance model insights. Tom and John aided robust discussion and provided invaluable insights to participants.

Tom Robinson Managing Director

Goolwa Pipi Co Pty Ltd

John LloydNon-Executive Director

Meat and Livestock Australia

Pipi industry producers were historically competitive, after

forming an alliance and working together under one brand, they

were able to reap greater benefits.

Key benefit of working collectively is the huge saving on logistics / freight costs by pooling weight together in one load and sharing the expense.

MAP packaging required in order to extend shelf life, especially due to

distance from major markets / customers.

Co-operatives can be successful if the operations of the co-op are separate from the commercial

activity.

Start small and then grow, especially if there are issues with utilisation of equipment (volumes

available to process).

Two major challenges with co-op model; access to capital and

governance.

Equal share and equal voting rights in the business, regardless of quota,

ensures the best interests of all producers are realised.

Often the best operators of processing facilities aren't the

industry, but a commercial entity.

Multiple- species processing is not common but multiple activity e.g. smoking & filleting happens, Huon and Tassal are good examples of

this.

23

Workshop 3: Location & Business Model - Summary Outputs

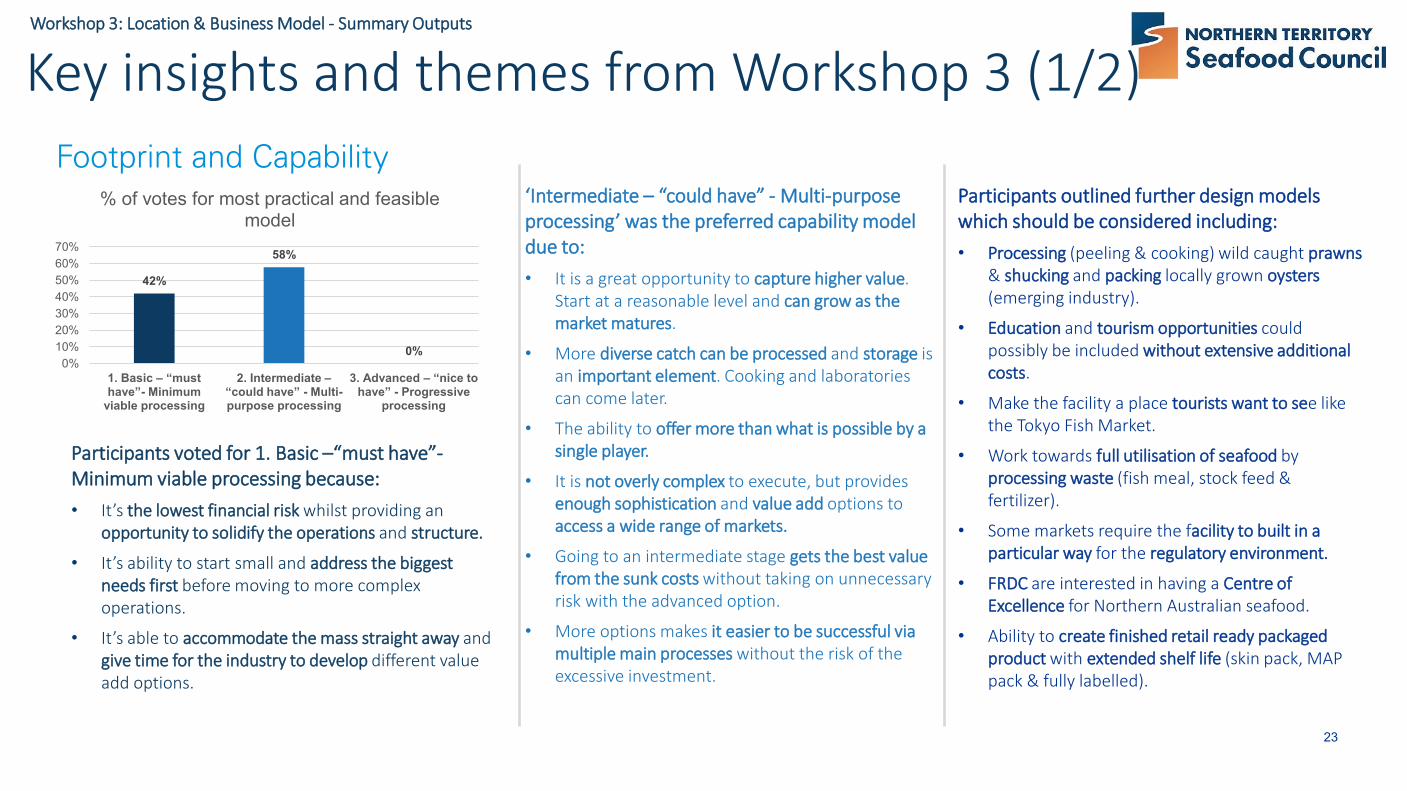

Key insights and themes from Workshop 3 (1/2)Footprint and Capability

42%

58%

0%0%

10%20%30%40%50%60%70%

1. Basic – “must have”- Minimum

viable processing

2. Intermediate –“could have” - Multi-purpose processing

3. Advanced – “nice to have” - Progressive

processing

% of votes for most practical and feasible model

Participants voted for 1. Basic –“must have”-Minimum viable processing because:• It’s the lowest financial risk whilst providing an

opportunity to solidify the operations and structure.

• It’s ability to start small and address the biggest needs first before moving to more complex operations.

• It’s able to accommodate the mass straight away and give time for the industry to develop different value add options.

‘Intermediate – “could have” - Multi-purpose processing’ was the preferred capability model due to:• It is a great opportunity to capture higher value.

Start at a reasonable level and can grow as the market matures.

• More diverse catch can be processed and storage is an important element. Cooking and laboratories can come later.

• The ability to offer more than what is possible by a single player.

• It is not overly complex to execute, but provides enough sophistication and value add options to access a wide range of markets.

• Going to an intermediate stage gets the best value from the sunk costs without taking on unnecessary risk with the advanced option.

• More options makes it easier to be successful via multiple main processes without the risk of the excessive investment.

Participants outlined further design models which should be considered including:• Processing (peeling & cooking) wild caught prawns

& shucking and packing locally grown oysters(emerging industry).

• Education and tourism opportunities could possibly be included without extensive additional costs.

• Make the facility a place tourists want to see like the Tokyo Fish Market.

• Work towards full utilisation of seafood by processing waste (fish meal, stock feed & fertilizer).

• Some markets require the facility to built in a particular way for the regulatory environment.

• FRDC are interested in having a Centre of Excellence for Northern Australian seafood.

• Ability to create finished retail ready packaged product with extended shelf life (skin pack, MAP pack & fully labelled).

24

Workshop 3: Location & Business Model - Summary Outputs

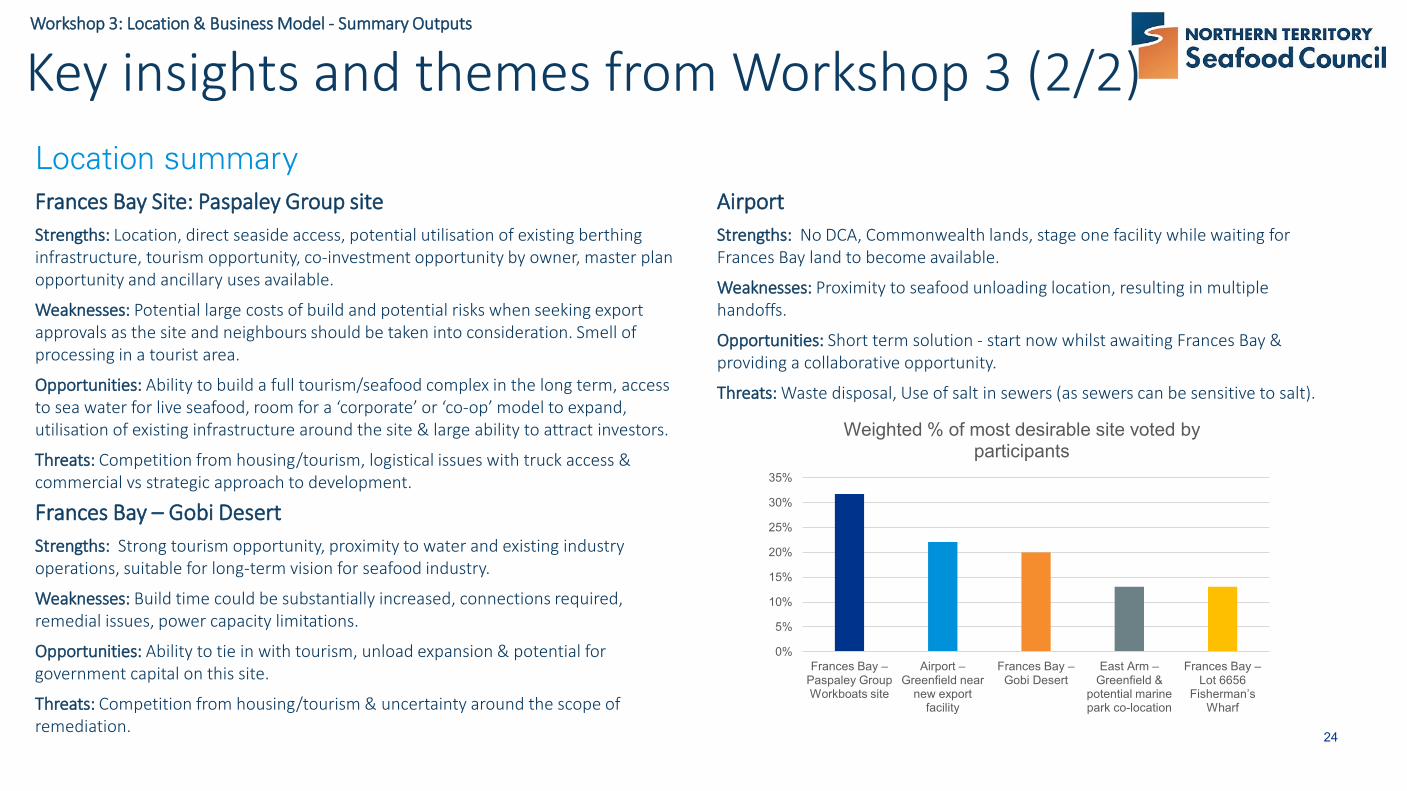

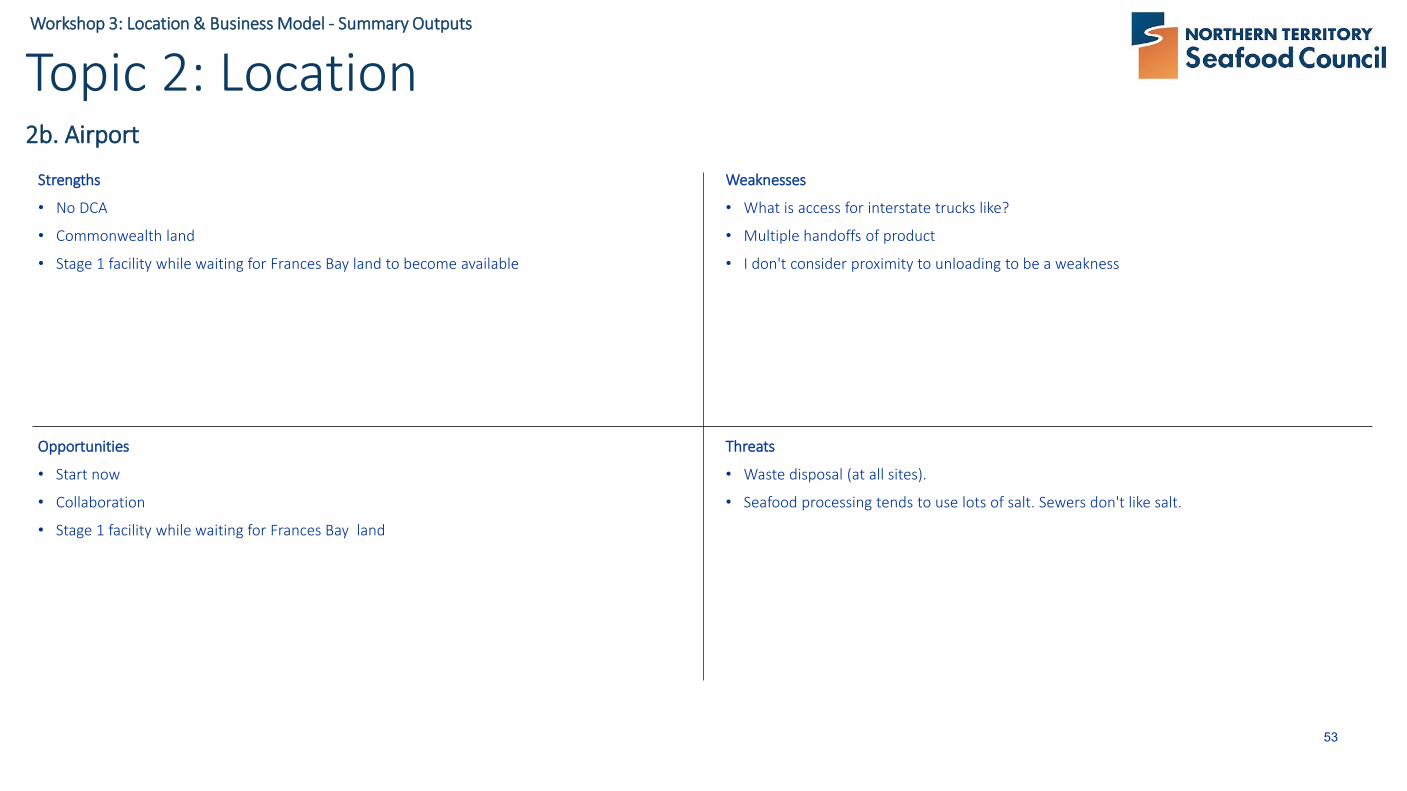

AirportStrengths: No DCA, Commonwealth lands, stage one facility while waiting for Frances Bay land to become available.

Weaknesses: Proximity to seafood unloading location, resulting in multiple handoffs.

Opportunities: Short term solution - start now whilst awaiting Frances Bay & providing a collaborative opportunity.

Threats: Waste disposal, Use of salt in sewers (as sewers can be sensitive to salt).

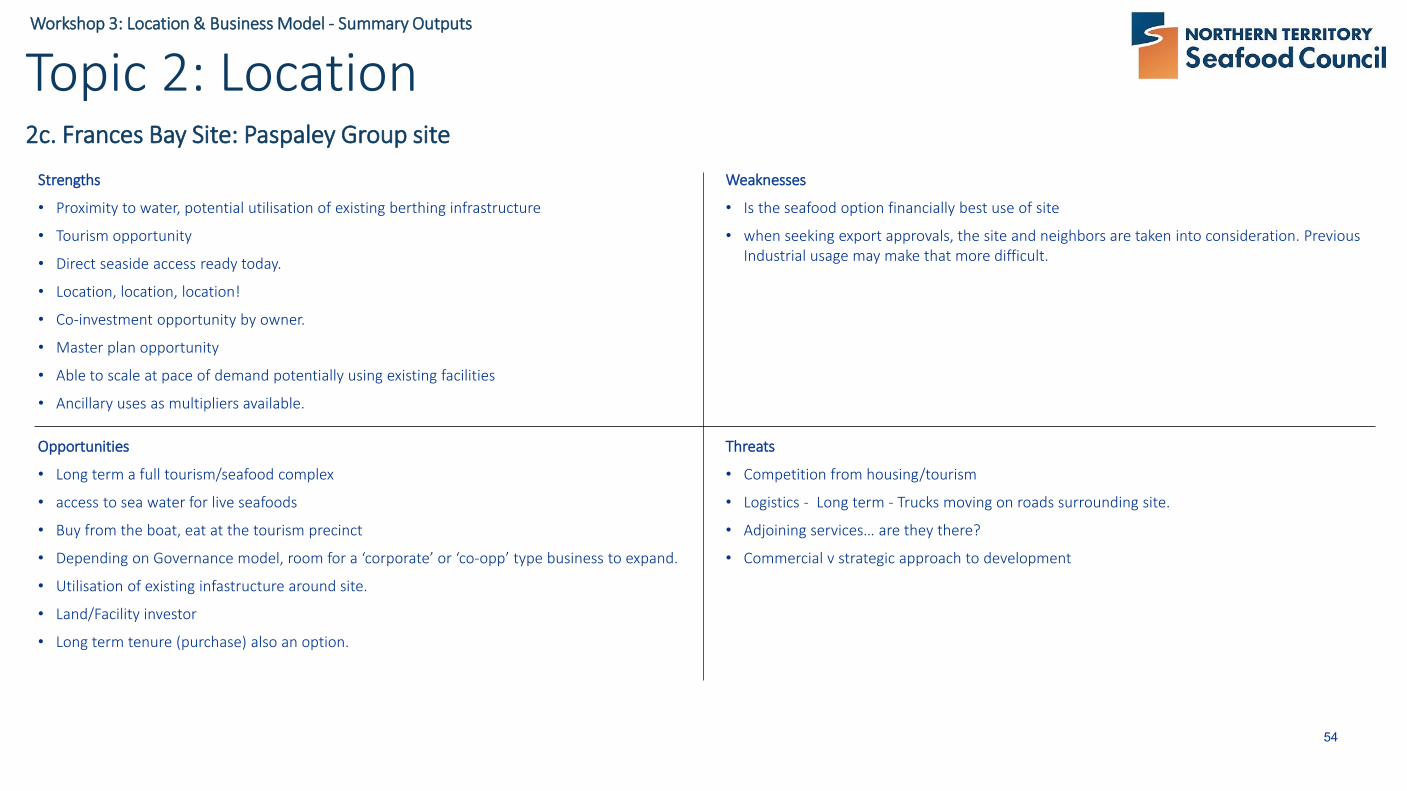

Frances Bay Site: Paspaley Group siteStrengths: Location, direct seaside access, potential utilisation of existing berthing infrastructure, tourism opportunity, co-investment opportunity by owner, master plan opportunity and ancillary uses available.

Weaknesses: Potential large costs of build and potential risks when seeking export approvals as the site and neighbours should be taken into consideration. Smell of processing in a tourist area.

Opportunities: Ability to build a full tourism/seafood complex in the long term, access to sea water for live seafood, room for a ‘corporate’ or ‘co-op’ model to expand, utilisation of existing infrastructure around the site & large ability to attract investors.

Threats: Competition from housing/tourism, logistical issues with truck access & commercial vs strategic approach to development.

Key insights and themes from Workshop 3 (2/2)

0%

5%

10%

15%

20%

25%

30%

35%

Frances Bay –Paspaley Group Workboats site

Airport –Greenfield near

new export facility

Frances Bay –Gobi Desert

East Arm –Greenfield &

potential marine park co-location

Frances Bay –Lot 6656

Fisherman’s Wharf

Weighted % of most desirable site voted by participants

Location summary

Frances Bay – Gobi DesertStrengths: Strong tourism opportunity, proximity to water and existing industry operations, suitable for long-term vision for seafood industry.

Weaknesses: Build time could be substantially increased, connections required, remedial issues, power capacity limitations.

Opportunities: Ability to tie in with tourism, unload expansion & potential for government capital on this site.

Threats: Competition from housing/tourism & uncertainty around the scope of remediation.

25

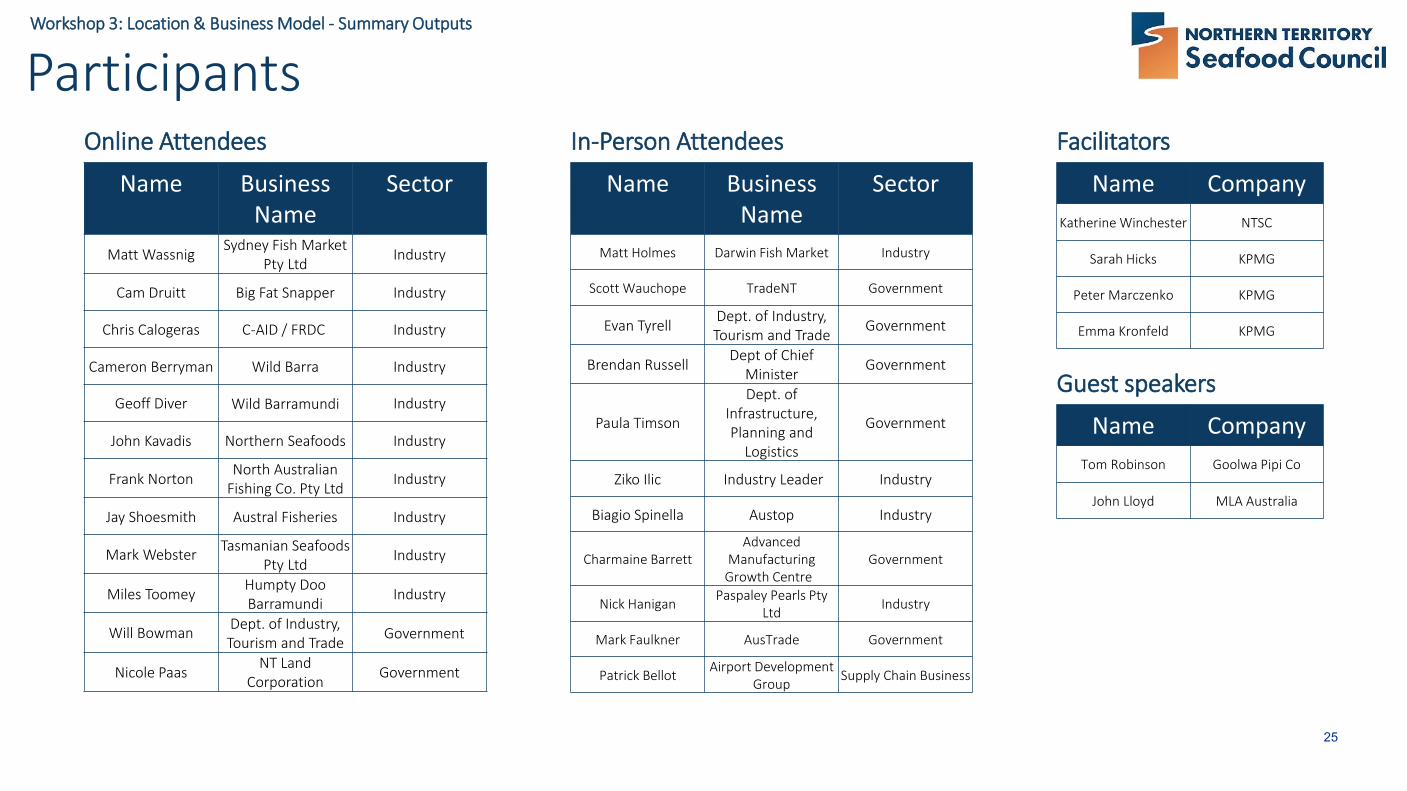

Workshop 3: Location & Business Model - Summary Outputs

Participants Online Attendees

Name Business Name

Sector

Matt Wassnig Sydney Fish Market Pty Ltd Industry

Cam Druitt Big Fat Snapper Industry

Chris Calogeras C-AID / FRDC Industry

Cameron Berryman Wild Barra Industry

Geoff Diver Wild Barramundi Industry

John Kavadis Northern Seafoods Industry

Frank Norton North Australian Fishing Co. Pty Ltd Industry

Jay Shoesmith Austral Fisheries Industry

Mark Webster Tasmanian Seafoods Pty Ltd Industry

Miles Toomey Humpty Doo Barramundi Industry

Will Bowman Dept. of Industry, Tourism and Trade Government

Nicole Paas NT Land Corporation Government

Name Business Name

Sector

Matt Holmes Darwin Fish Market Industry

Scott Wauchope TradeNT Government

Evan Tyrell Dept. of Industry, Tourism and Trade Government

Brendan Russell Dept of Chief Minister Government

Paula Timson

Dept. of Infrastructure, Planning and

Logistics

Government

Ziko Ilic Industry Leader Industry

Biagio Spinella Austop Industry

Charmaine BarrettAdvanced

Manufacturing Growth Centre

Government

Nick Hanigan Paspaley Pearls Pty Ltd Industry

Mark Faulkner AusTrade Government

Patrick Bellot Airport Development Group Supply Chain Business

In-Person Attendees

Name CompanyKatherine Winchester NTSC

Sarah Hicks KPMG

Peter Marczenko KPMG

Emma Kronfeld KPMG

Facilitators

Name CompanyTom Robinson Goolwa Pipi Co

John Lloyd MLA Australia

Guest speakers

26

AppendixPlease note all raw Mentimeter data has been included as an Addendum to this report

27

Workshop 1 – raw data

28

Workshop 1: Products - Summary Outputs

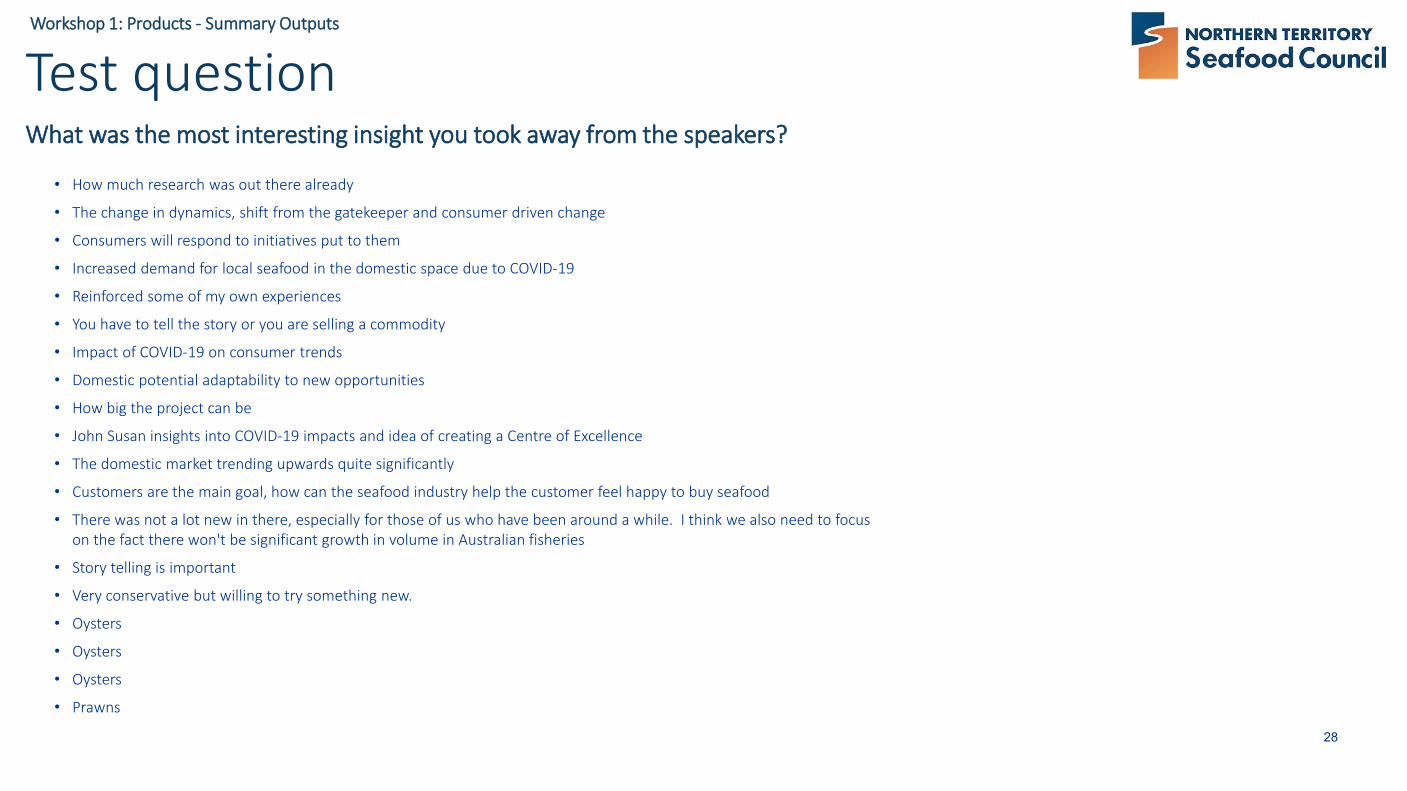

Test questionWhat was the most interesting insight you took away from the speakers?

• How much research was out there already

• The change in dynamics, shift from the gatekeeper and consumer driven change

• Consumers will respond to initiatives put to them

• Increased demand for local seafood in the domestic space due to COVID-19

• Reinforced some of my own experiences

• You have to tell the story or you are selling a commodity

• Impact of COVID-19 on consumer trends

• Domestic potential adaptability to new opportunities

• How big the project can be

• John Susan insights into COVID-19 impacts and idea of creating a Centre of Excellence

• The domestic market trending upwards quite significantly

• Customers are the main goal, how can the seafood industry help the customer feel happy to buy seafood

• There was not a lot new in there, especially for those of us who have been around a while. I think we also need to focus on the fact there won't be significant growth in volume in Australian fisheries

• Story telling is important

• Very conservative but willing to try something new.

• Oysters

• Oysters

• Oysters

• Prawns

29

Workshop 1: Products - Summary Outputs

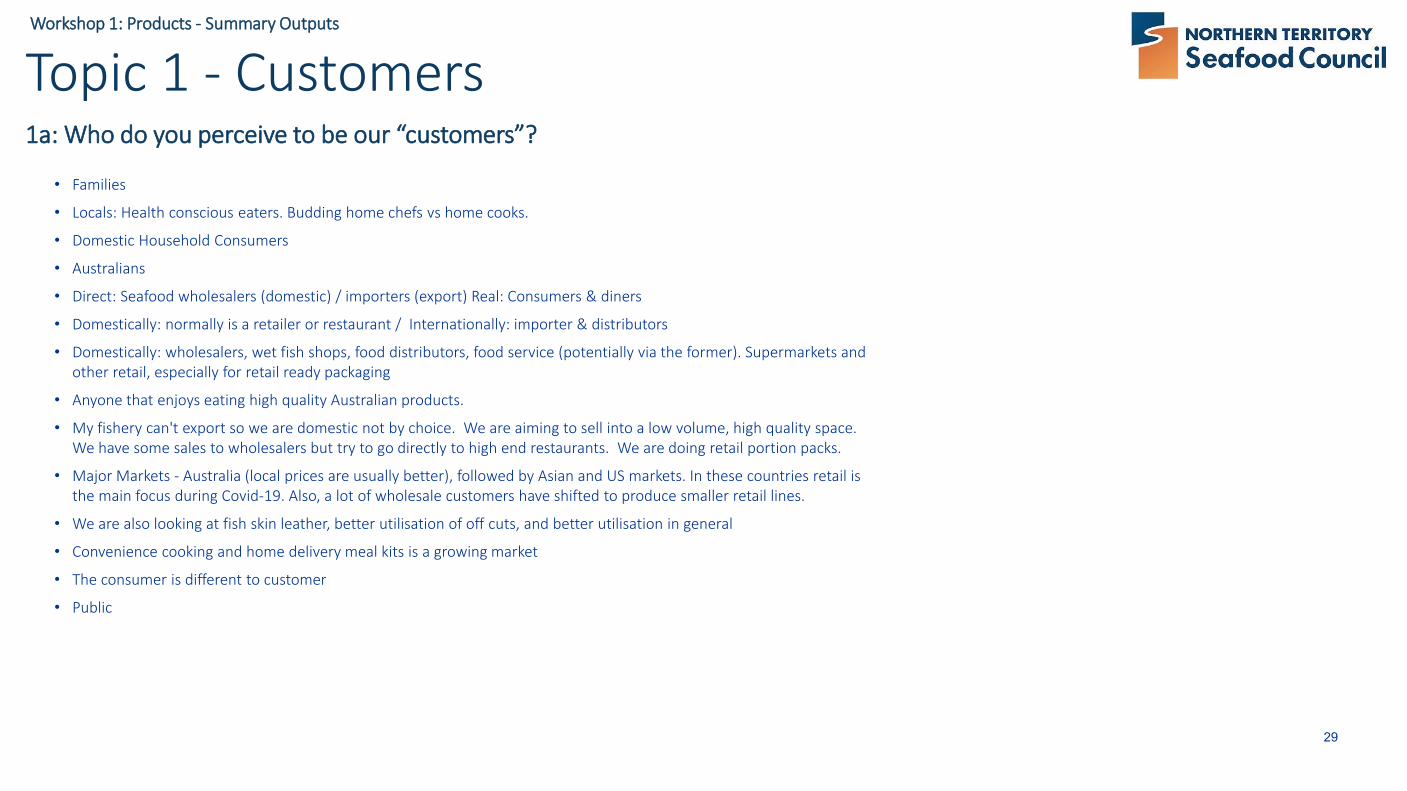

Topic 1 - Customers1a: Who do you perceive to be our “customers”?

• Families

• Locals: Health conscious eaters. Budding home chefs vs home cooks.

• Domestic Household Consumers

• Australians

• Direct: Seafood wholesalers (domestic) / importers (export) Real: Consumers & diners

• Domestically: normally is a retailer or restaurant / Internationally: importer & distributors

• Domestically: wholesalers, wet fish shops, food distributors, food service (potentially via the former). Supermarkets and other retail, especially for retail ready packaging

• Anyone that enjoys eating high quality Australian products.

• My fishery can't export so we are domestic not by choice. We are aiming to sell into a low volume, high quality space. We have some sales to wholesalers but try to go directly to high end restaurants. We are doing retail portion packs.

• Major Markets - Australia (local prices are usually better), followed by Asian and US markets. In these countries retail is the main focus during Covid-19. Also, a lot of wholesale customers have shifted to produce smaller retail lines.

• We are also looking at fish skin leather, better utilisation of off cuts, and better utilisation in general

• Convenience cooking and home delivery meal kits is a growing market

• The consumer is different to customer

• Public

30

Workshop 1: Products - Summary Outputs

Topic 1 - Customers1b. On the basis of what we just heard from the presenters, what products do you believe customers want / demand?

• Convenience and familiarity

• Products that are prepared and packaged to suit customers needs for storage and then utilisation.

• ‘Ready to cook' / ready to eat format - not whole fish

• Set packages to enable cooking success?.

• Easier to handle seafood, ready to cook

• Quality, consistently supplied, Australian wild and/or aquaculture products with known providence.

• Wholesalers have constrained labour - so harder to fillet (scale) / process etc. Need to balance cost / labour/ freshness

• Consistency and quality

• Fresh, Australian, not overly processed, easy to cook with, versatile

• Quality products at a reasonable price in a easy to use format.

• Easily sourced, simple to prepare, good tasting, quality seafoods.

• Pre cut pre package

• Wholesalers chasing bulk fillets in 3-5kg packaging - fresh & frozen. Prepared to pay a premium vs cut it themselves.

• Is there an opportunity to use marketing to develop markets for underutilised species (as consumers now want Australian product)?

• Wet fish shops and retailers looking for fresh fillets or value added product in 2-4kg. Modified Atmospheric Packaging. Long shelf life, can rip the lid off and tip into display. Low touch/over heads. Being done in aquaculture - salmon, prawns, etc.

• Consumers looking for trusted brands with a local provenance story attached,

• There is a range of desires across demographics. Some want price, some want quality.

• MSC certified, ready to eat or easy to prepare.

• Not overly processed or packaged. Still appearing fresh. Often an issue with imported retail product.

• Approachable, affordable and easy to cook with.

• Many customers want set weight packets. sometimes hard to do with wild. For example 100g per packet.

• Consumers looking for multiples of 120-140g portions at the supermarket - for singles/couples (269-300g) and bulk packs (400-500g)

• Under-utilised species that could have appeal to a new market in processed or value add form - e.g. Golden Snapper.

• Opened oysters

• Banana prawns

31

Workshop 1: Products - Summary Outputs

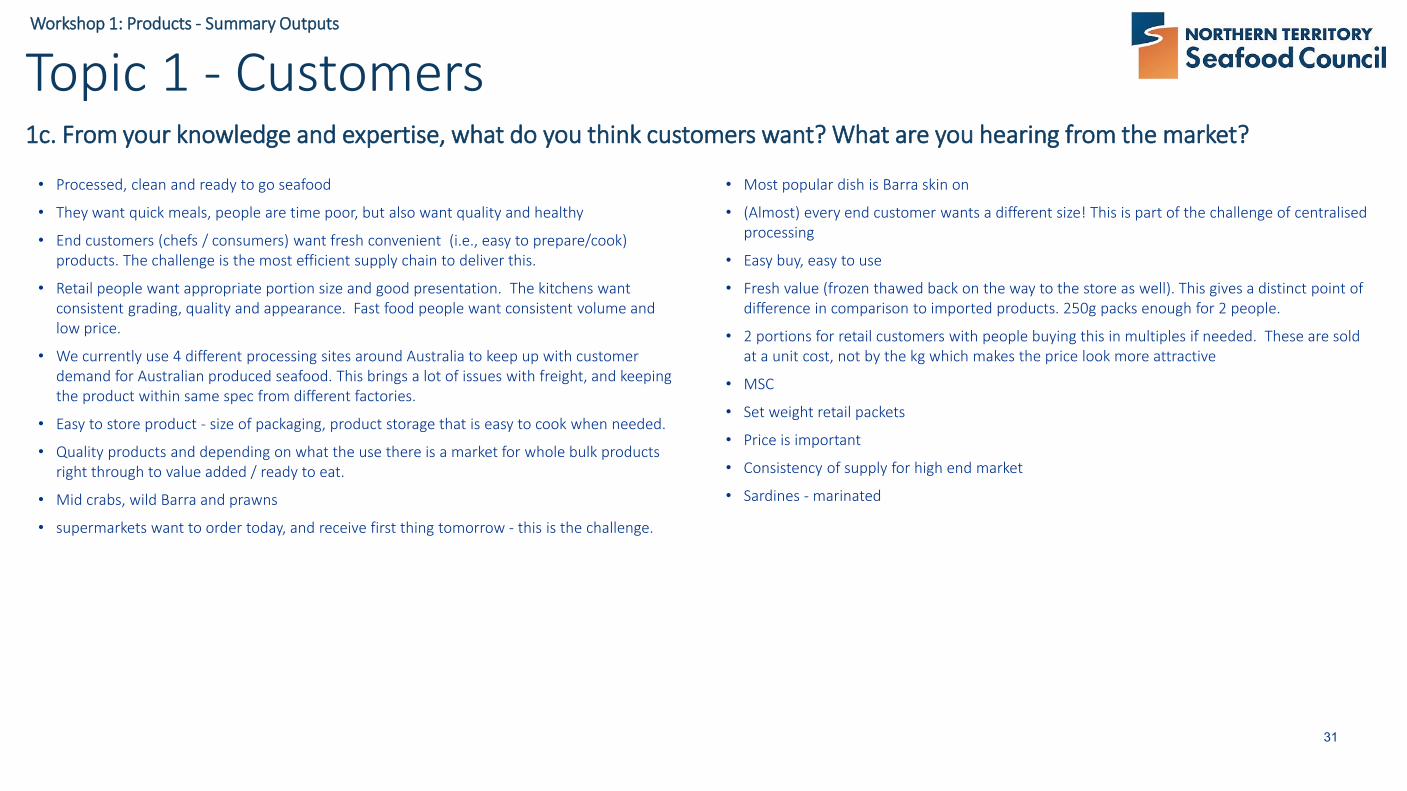

Topic 1 - Customers1c. From your knowledge and expertise, what do you think customers want? What are you hearing from the market?

• Processed, clean and ready to go seafood

• They want quick meals, people are time poor, but also want quality and healthy

• End customers (chefs / consumers) want fresh convenient (i.e., easy to prepare/cook) products. The challenge is the most efficient supply chain to deliver this.

• Retail people want appropriate portion size and good presentation. The kitchens want consistent grading, quality and appearance. Fast food people want consistent volume and low price.

• We currently use 4 different processing sites around Australia to keep up with customer demand for Australian produced seafood. This brings a lot of issues with freight, and keeping the product within same spec from different factories.

• Easy to store product - size of packaging, product storage that is easy to cook when needed.

• Quality products and depending on what the use there is a market for whole bulk products right through to value added / ready to eat.

• Mid crabs, wild Barra and prawns

• supermarkets want to order today, and receive first thing tomorrow - this is the challenge.

• Most popular dish is Barra skin on

• (Almost) every end customer wants a different size! This is part of the challenge of centralisedprocessing

• Easy buy, easy to use

• Fresh value (frozen thawed back on the way to the store as well). This gives a distinct point of difference in comparison to imported products. 250g packs enough for 2 people.

• 2 portions for retail customers with people buying this in multiples if needed. These are sold at a unit cost, not by the kg which makes the price look more attractive

• MSC

• Set weight retail packets

• Price is important

• Consistency of supply for high end market

• Sardines - marinated

32

Workshop 1: Products - Summary Outputs

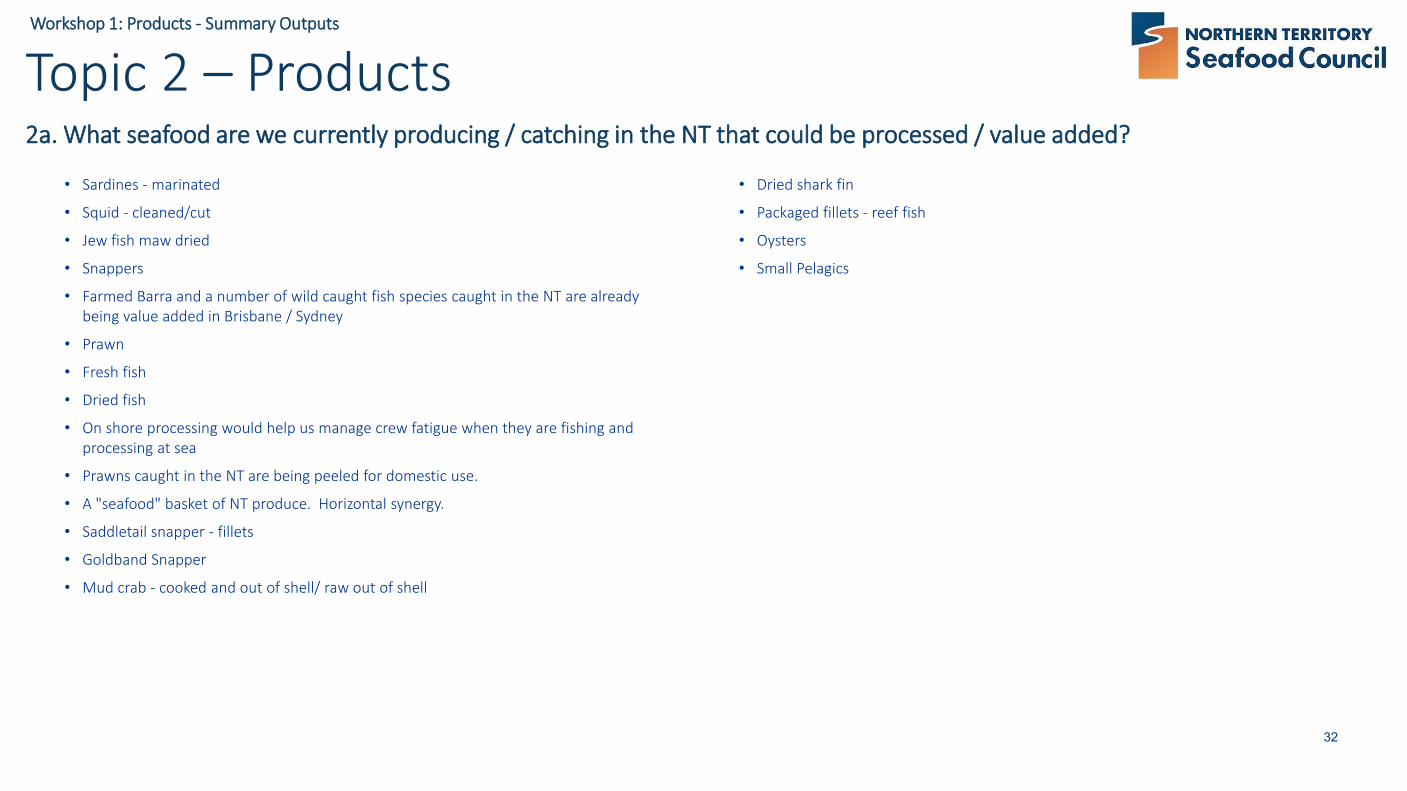

Topic 2 – Products2a. What seafood are we currently producing / catching in the NT that could be processed / value added?

• Sardines - marinated

• Squid - cleaned/cut

• Jew fish maw dried

• Snappers

• Farmed Barra and a number of wild caught fish species caught in the NT are already being value added in Brisbane / Sydney

• Prawn

• Fresh fish

• Dried fish

• On shore processing would help us manage crew fatigue when they are fishing and processing at sea

• Prawns caught in the NT are being peeled for domestic use.

• A "seafood" basket of NT produce. Horizontal synergy.

• Saddletail snapper - fillets

• Goldband Snapper

• Mud crab - cooked and out of shell/ raw out of shell

• Dried shark fin

• Packaged fillets - reef fish

• Oysters

• Small Pelagics

33

Workshop 1: Products - Summary Outputs

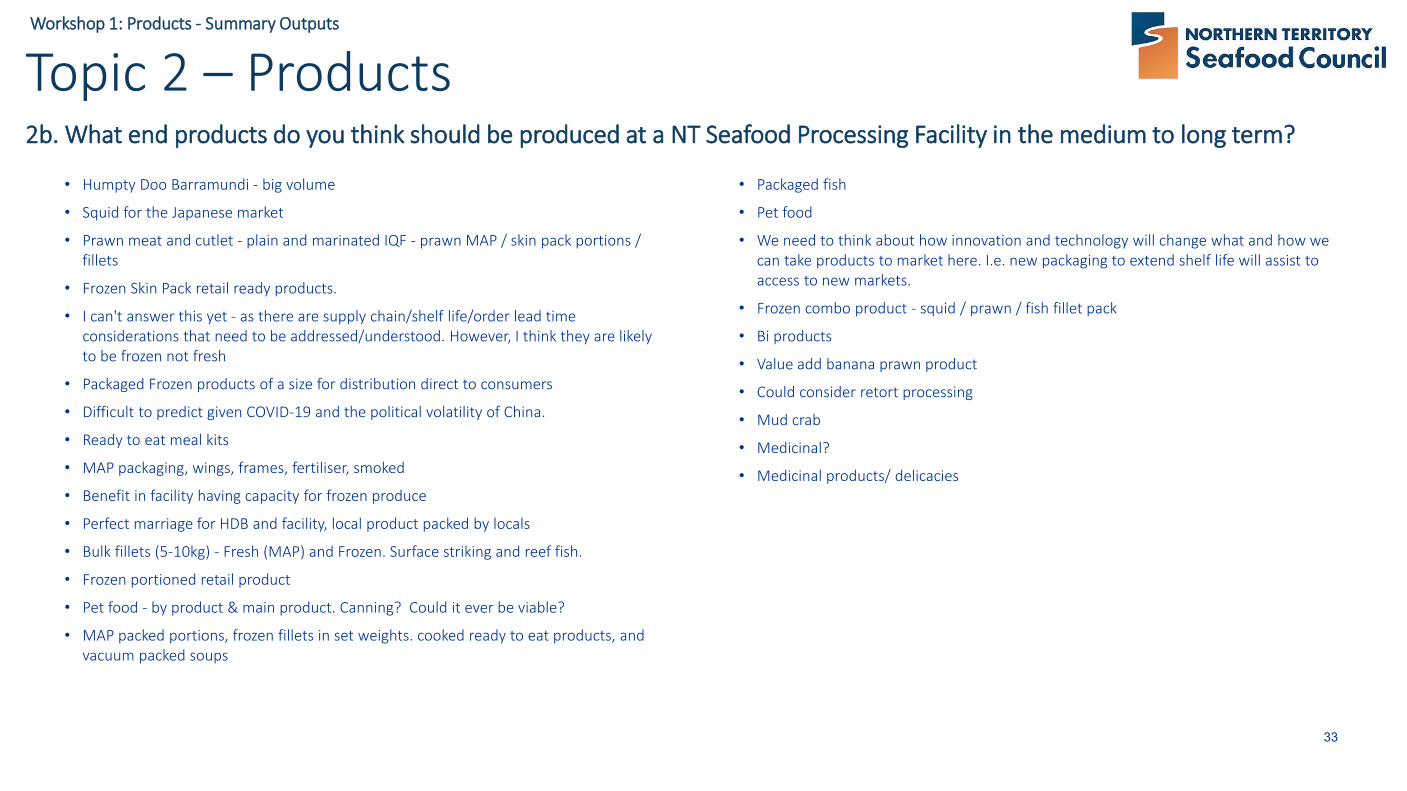

Topic 2 – Products2b. What end products do you think should be produced at a NT Seafood Processing Facility in the medium to long term?

• Humpty Doo Barramundi - big volume

• Squid for the Japanese market

• Prawn meat and cutlet - plain and marinated IQF - prawn MAP / skin pack portions / fillets

• Frozen Skin Pack retail ready products.

• I can't answer this yet - as there are supply chain/shelf life/order lead time considerations that need to be addressed/understood. However, I think they are likely to be frozen not fresh

• Packaged Frozen products of a size for distribution direct to consumers

• Difficult to predict given COVID-19 and the political volatility of China.

• Ready to eat meal kits

• MAP packaging, wings, frames, fertiliser, smoked

• Benefit in facility having capacity for frozen produce

• Perfect marriage for HDB and facility, local product packed by locals

• Bulk fillets (5-10kg) - Fresh (MAP) and Frozen. Surface striking and reef fish.

• Frozen portioned retail product

• Pet food - by product & main product. Canning? Could it ever be viable?

• MAP packed portions, frozen fillets in set weights. cooked ready to eat products, and vacuum packed soups

• Packaged fish

• Pet food

• We need to think about how innovation and technology will change what and how we can take products to market here. I.e. new packaging to extend shelf life will assist to access to new markets.

• Frozen combo product - squid / prawn / fish fillet pack

• Bi products

• Value add banana prawn product

• Could consider retort processing

• Mud crab

• Medicinal?

• Medicinal products/ delicacies

34

Workshop 1: Products - Summary Outputs

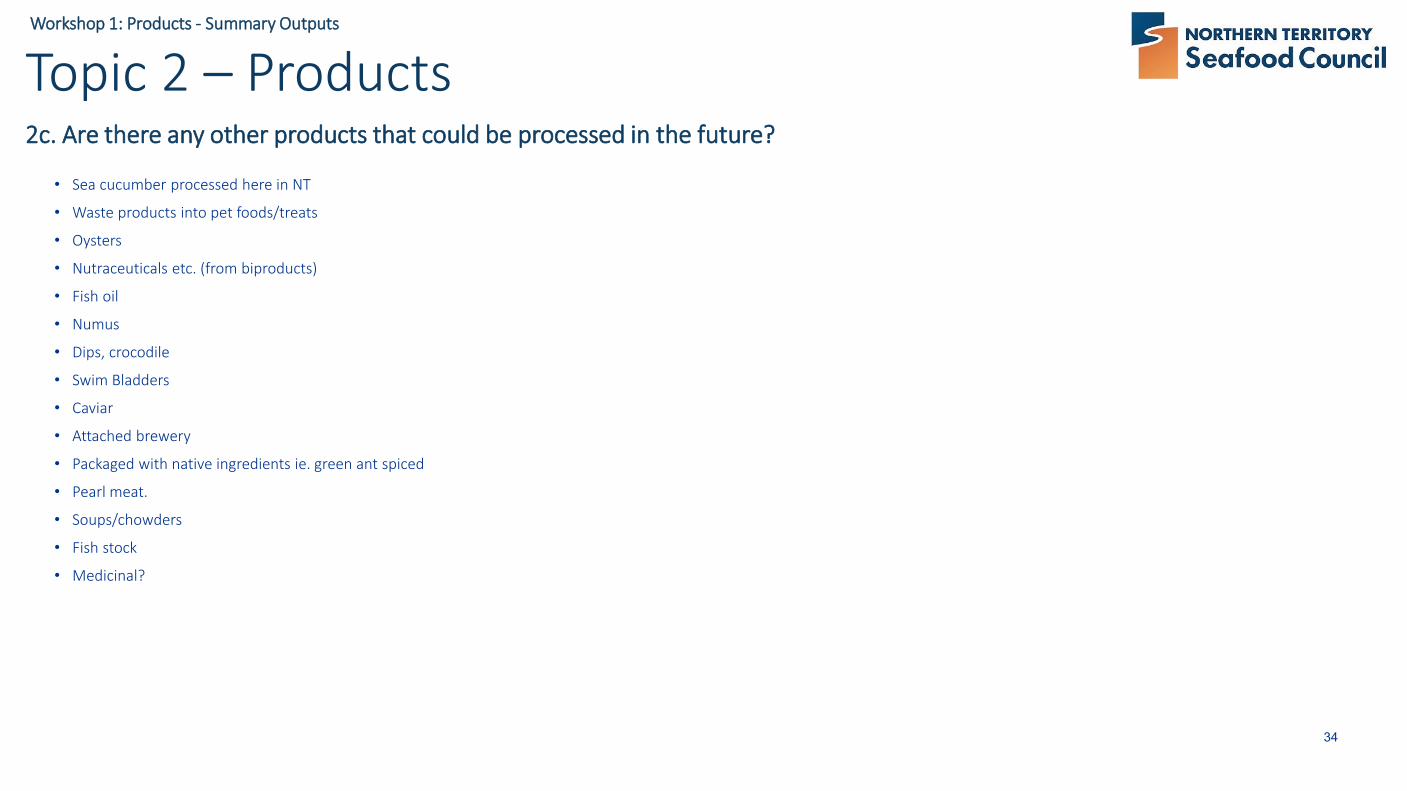

Topic 2 – Products2c. Are there any other products that could be processed in the future?

• Sea cucumber processed here in NT

• Waste products into pet foods/treats

• Oysters

• Nutraceuticals etc. (from biproducts)

• Fish oil

• Numus

• Dips, crocodile

• Swim Bladders

• Caviar

• Attached brewery

• Packaged with native ingredients ie. green ant spiced

• Pearl meat.

• Soups/chowders

• Fish stock

• Medicinal?

35

Workshop 1: Products - Summary Outputs

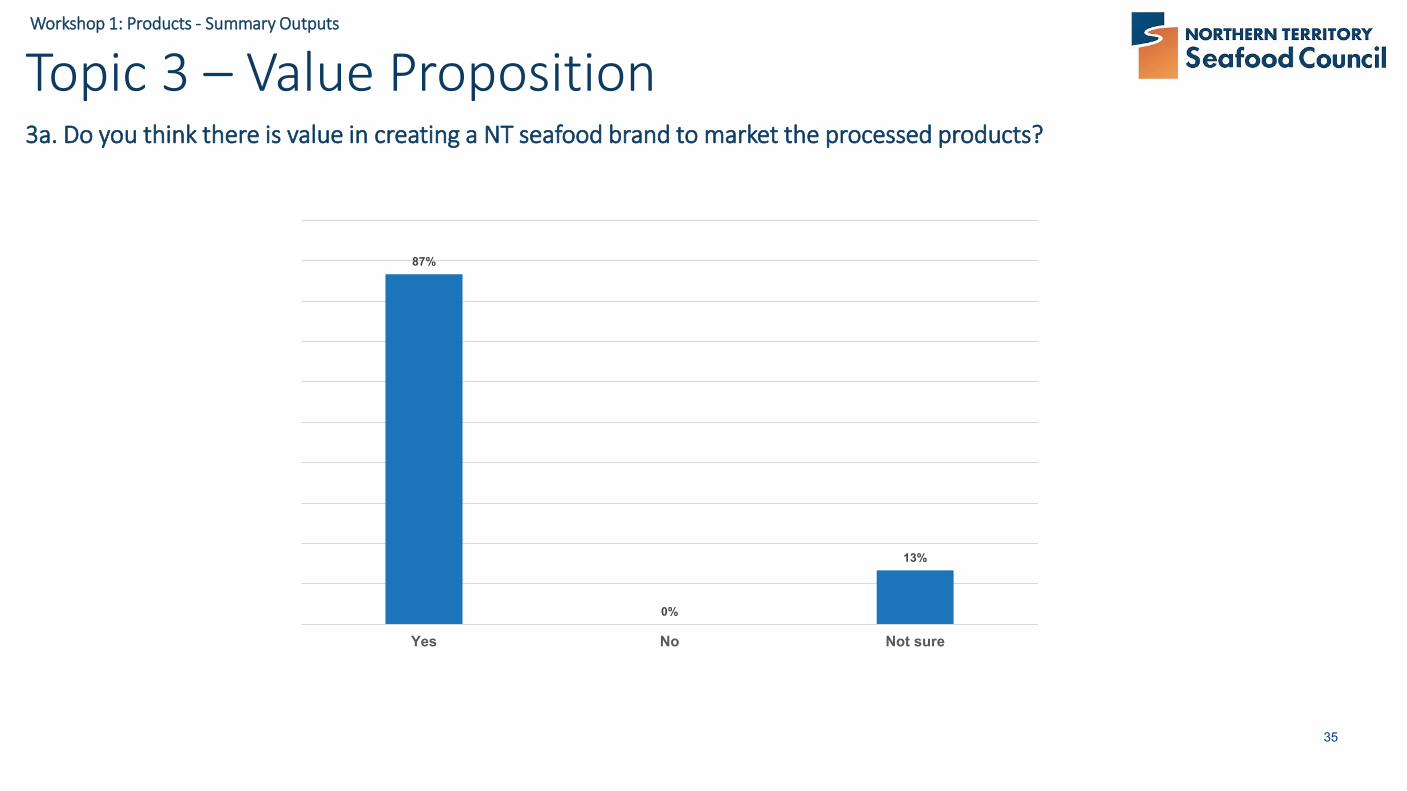

Topic 3 – Value Proposition3a. Do you think there is value in creating a NT seafood brand to market the processed products?

87%

0%

13%

Yes No Not sure

36

Workshop 1: Products - Summary Outputs

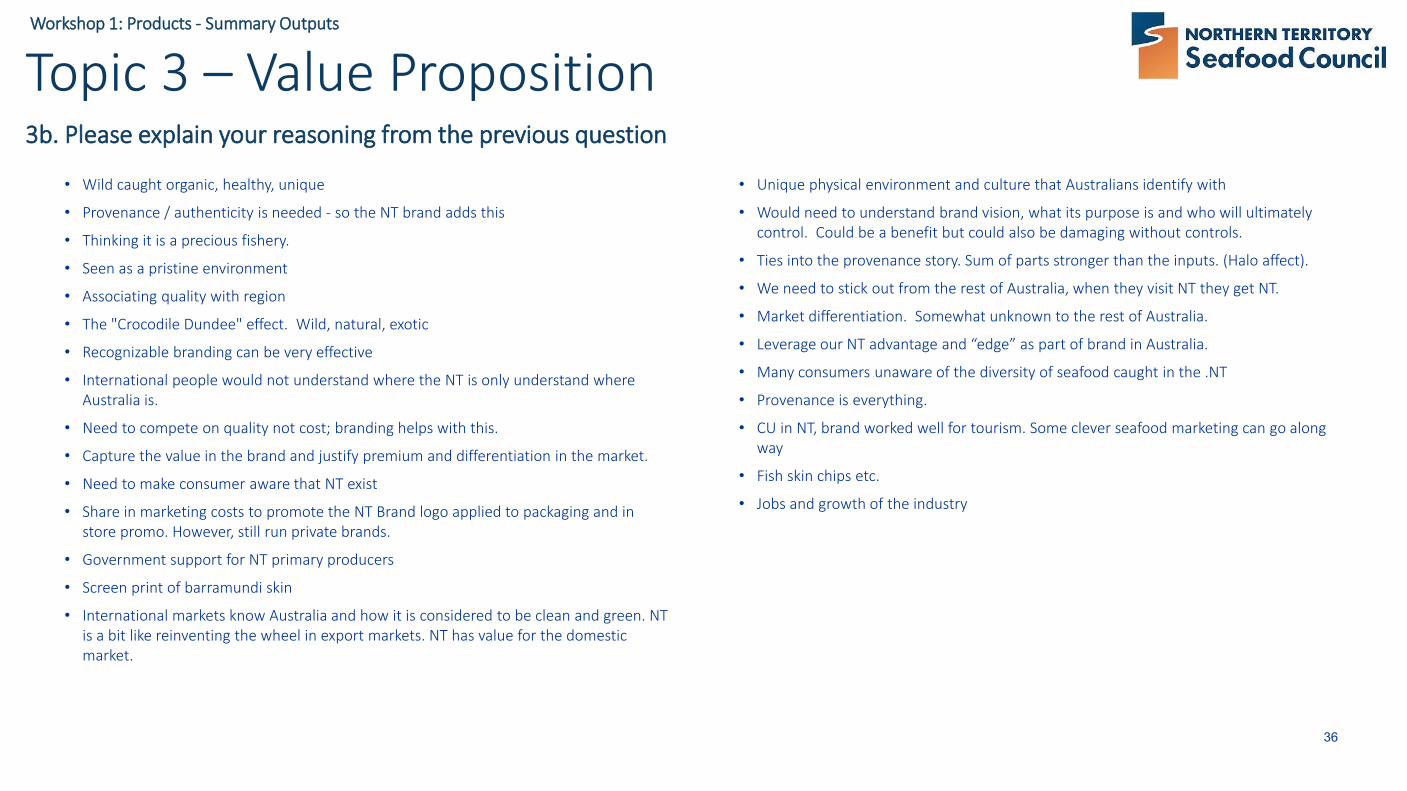

Topic 3 – Value Proposition3b. Please explain your reasoning from the previous question

• Wild caught organic, healthy, unique

• Provenance / authenticity is needed - so the NT brand adds this

• Thinking it is a precious fishery.

• Seen as a pristine environment

• Associating quality with region

• The "Crocodile Dundee" effect. Wild, natural, exotic

• Recognizable branding can be very effective

• International people would not understand where the NT is only understand where Australia is.

• Need to compete on quality not cost; branding helps with this.

• Capture the value in the brand and justify premium and differentiation in the market.

• Need to make consumer aware that NT exist

• Share in marketing costs to promote the NT Brand logo applied to packaging and in store promo. However, still run private brands.

• Government support for NT primary producers

• Screen print of barramundi skin

• International markets know Australia and how it is considered to be clean and green. NT is a bit like reinventing the wheel in export markets. NT has value for the domestic market.

• Unique physical environment and culture that Australians identify with

• Would need to understand brand vision, what its purpose is and who will ultimately control. Could be a benefit but could also be damaging without controls.

• Ties into the provenance story. Sum of parts stronger than the inputs. (Halo affect).

• We need to stick out from the rest of Australia, when they visit NT they get NT.

• Market differentiation. Somewhat unknown to the rest of Australia.

• Leverage our NT advantage and “edge” as part of brand in Australia.

• Many consumers unaware of the diversity of seafood caught in the .NT

• Provenance is everything.

• CU in NT, brand worked well for tourism. Some clever seafood marketing can go along way

• Fish skin chips etc.

• Jobs and growth of the industry

37

Workshop 1: Products - Summary Outputs

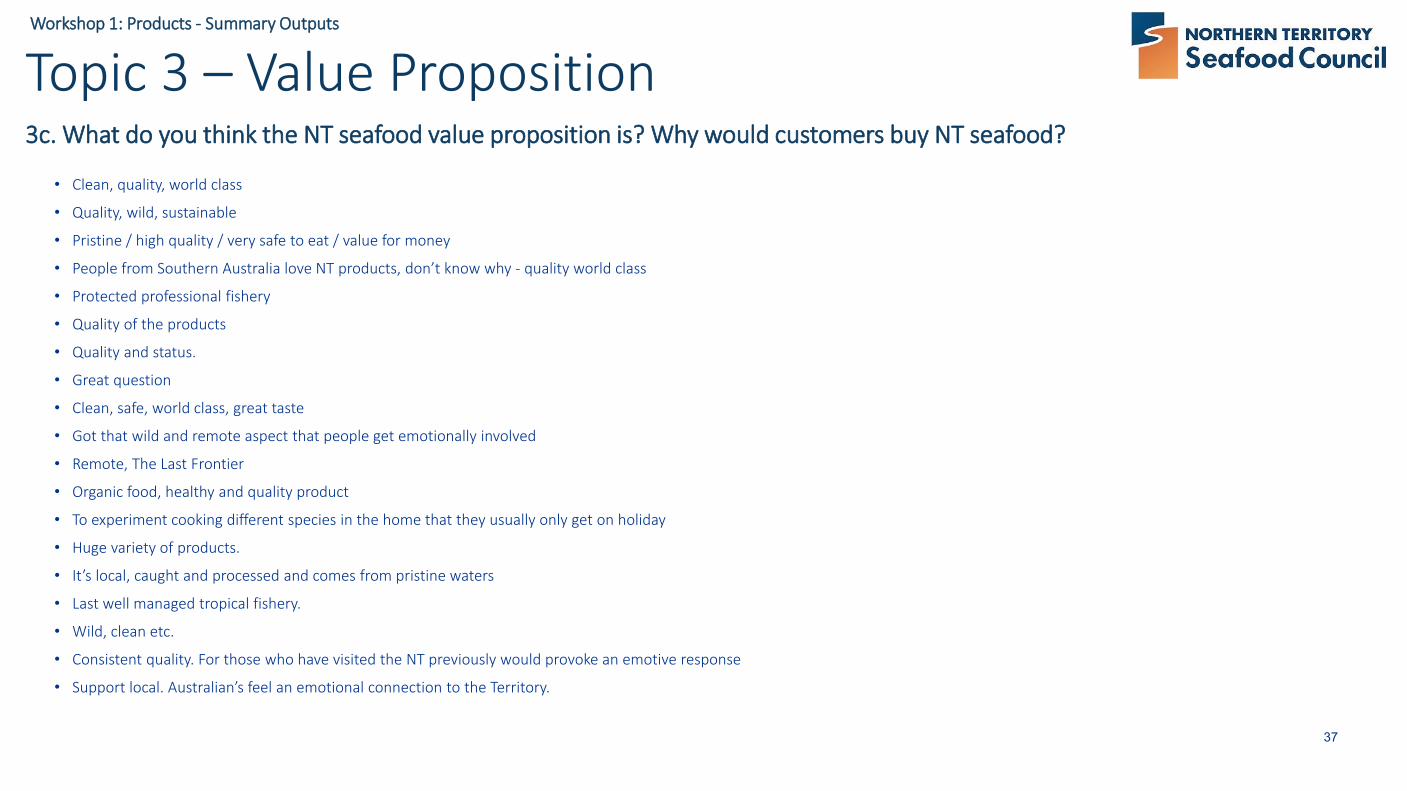

Topic 3 – Value Proposition3c. What do you think the NT seafood value proposition is? Why would customers buy NT seafood?

• Clean, quality, world class

• Quality, wild, sustainable

• Pristine / high quality / very safe to eat / value for money

• People from Southern Australia love NT products, don’t know why - quality world class

• Protected professional fishery

• Quality of the products

• Quality and status.

• Great question

• Clean, safe, world class, great taste

• Got that wild and remote aspect that people get emotionally involved

• Remote, The Last Frontier

• Organic food, healthy and quality product

• To experiment cooking different species in the home that they usually only get on holiday

• Huge variety of products.

• It’s local, caught and processed and comes from pristine waters

• Last well managed tropical fishery.

• Wild, clean etc.

• Consistent quality. For those who have visited the NT previously would provoke an emotive response

• Support local. Australian’s feel an emotional connection to the Territory.

38

Workshop 2 – raw data

39

Workshop 2: Viability - Summary Outputs

Topic 1: processing capabilities1a: What are the key processing capabilities you would like to see at a local processing facility? What would be of most value to you?

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Filleting Cooking –including

marinating

Freezing Packaging –including

MAP

Grading /sorting

Laboratoryfacilities

Other Dehydration /drying

Refrigeration/ cold storage

Smoking

% Votes for most valuable processing capability

40

Workshop 2: Viability - Summary Outputs

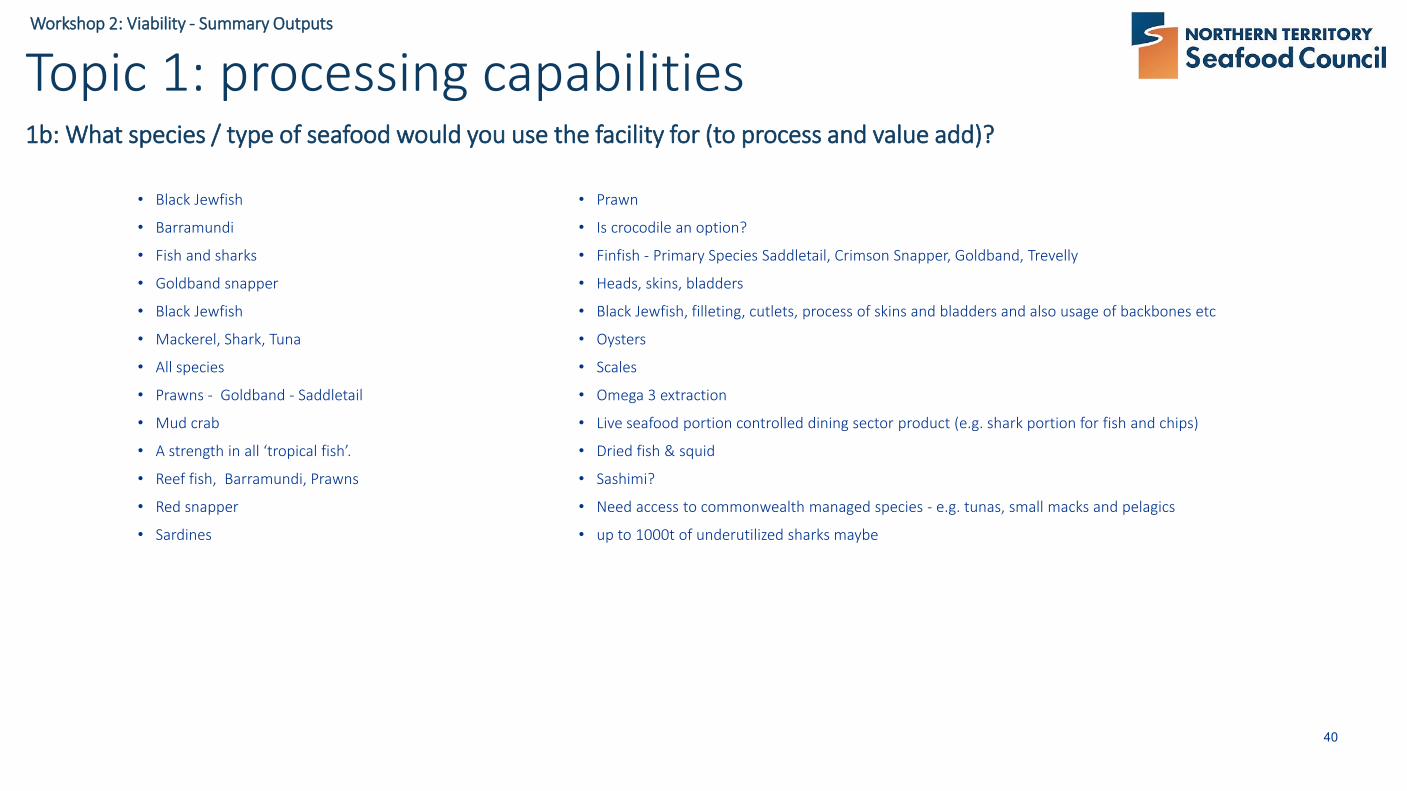

Topic 1: processing capabilities1b: What species / type of seafood would you use the facility for (to process and value add)?

• Black Jewfish

• Barramundi

• Fish and sharks

• Goldband snapper

• Black Jewfish

• Mackerel, Shark, Tuna

• All species

• Prawns - Goldband - Saddletail

• Mud crab

• A strength in all ‘tropical fish’.

• Reef fish, Barramundi, Prawns

• Red snapper

• Sardines

• Prawn

• Is crocodile an option?

• Finfish - Primary Species Saddletail, Crimson Snapper, Goldband, Trevelly

• Heads, skins, bladders

• Black Jewfish, filleting, cutlets, process of skins and bladders and also usage of backbones etc

• Oysters

• Scales

• Omega 3 extraction

• Live seafood portion controlled dining sector product (e.g. shark portion for fish and chips)

• Dried fish & squid

• Sashimi?

• Need access to commonwealth managed species - e.g. tunas, small macks and pelagics

• up to 1000t of underutilized sharks maybe

41

Workshop 2: Viability - Summary Outputs

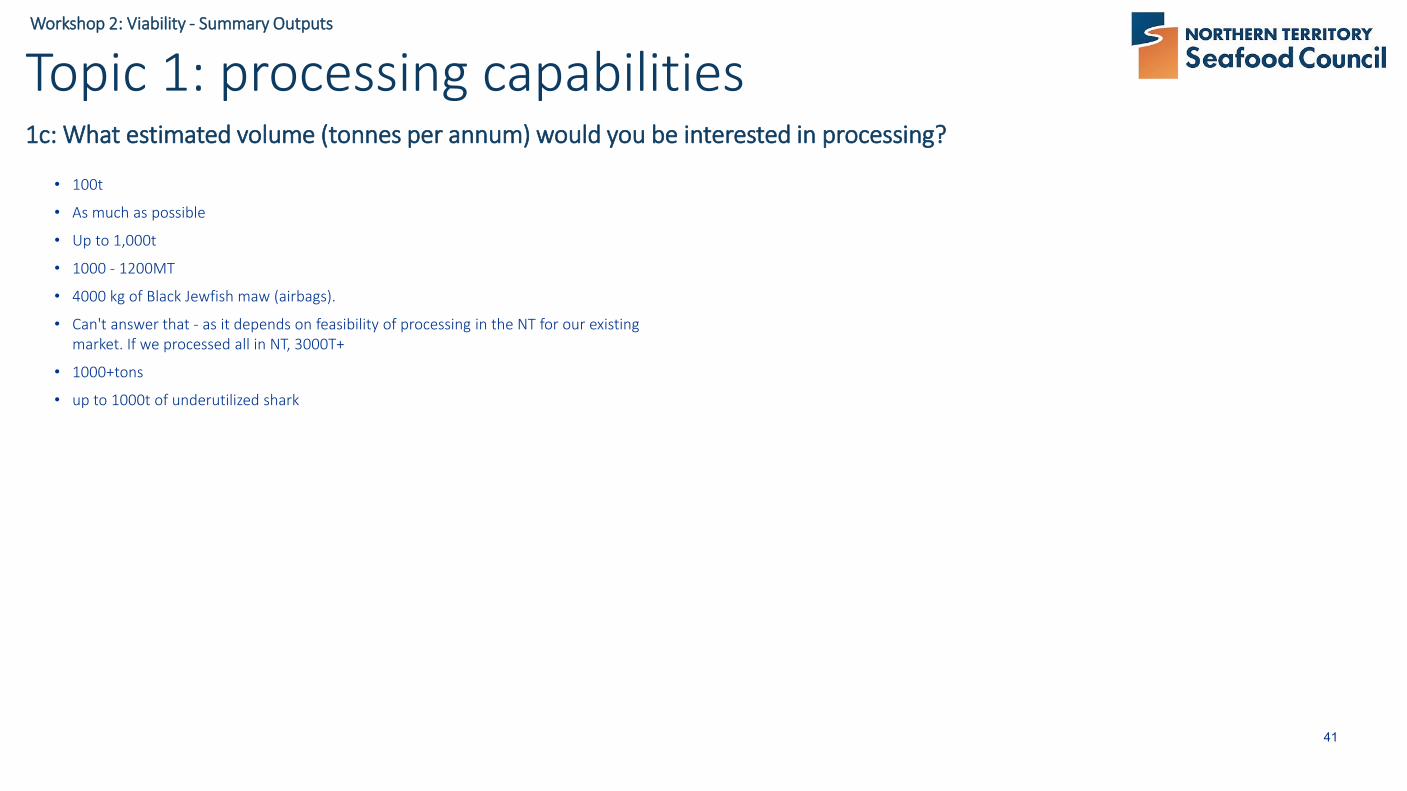

Topic 1: processing capabilities1c: What estimated volume (tonnes per annum) would you be interested in processing?

• 100t

• As much as possible

• Up to 1,000t

• 1000 - 1200MT

• 4000 kg of Black Jewfish maw (airbags).

• Can't answer that - as it depends on feasibility of processing in the NT for our existing market. If we processed all in NT, 3000T+

• 1000+tons

• up to 1000t of underutilized shark

42

Workshop 2: Viability - Summary Outputs

Topic 2: business model options2a. From the three models discussed, which one do you believe is the best option for a local processing facility?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Market-led private sectorapproach

Co-operative model Other Major corporate agri-businessmodel

Votes

Votes

43

Workshop 2: Viability - Summary Outputs

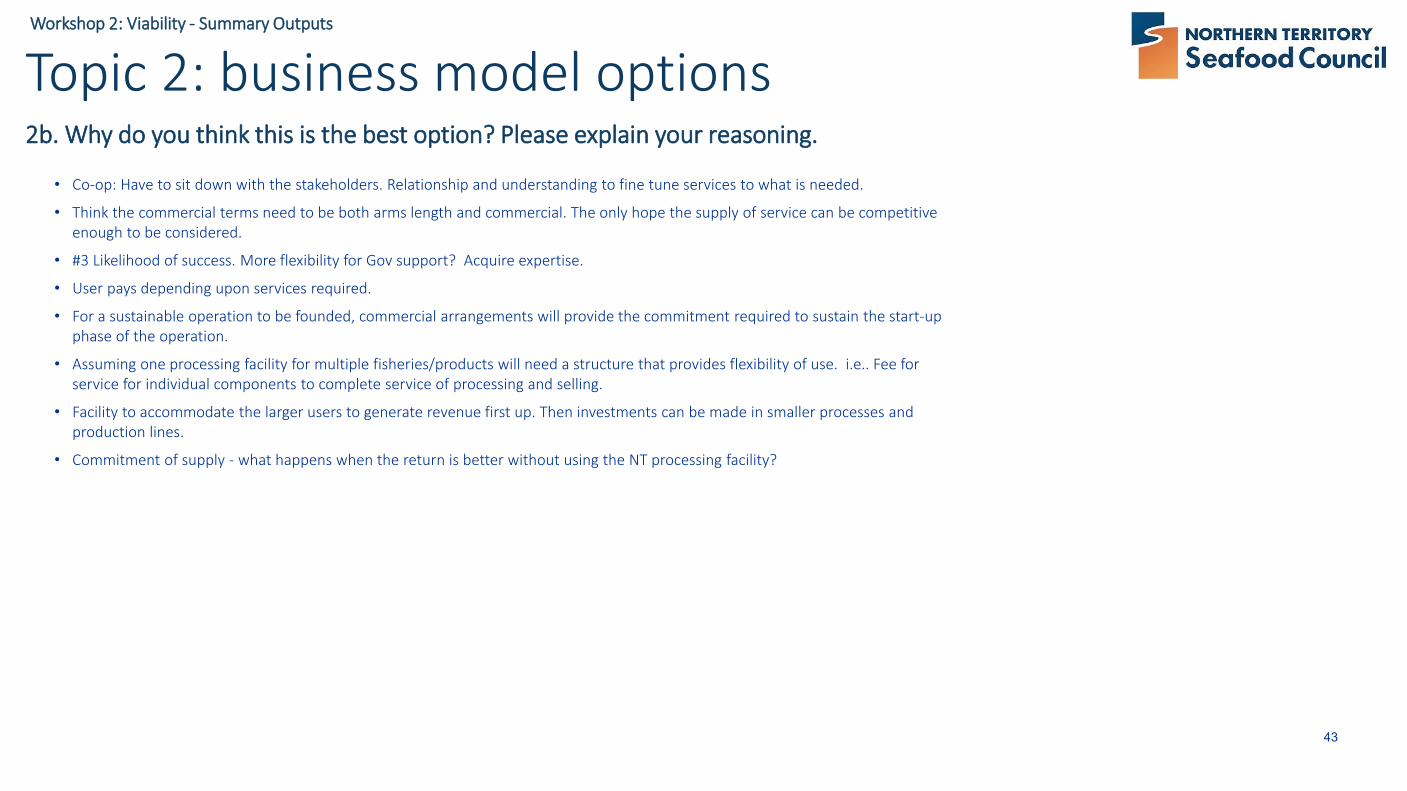

Topic 2: business model options2b. Why do you think this is the best option? Please explain your reasoning.

• Co-op: Have to sit down with the stakeholders. Relationship and understanding to fine tune services to what is needed.

• Think the commercial terms need to be both arms length and commercial. The only hope the supply of service can be competitiveenough to be considered.

• #3 Likelihood of success. More flexibility for Gov support? Acquire expertise.

• User pays depending upon services required.

• For a sustainable operation to be founded, commercial arrangements will provide the commitment required to sustain the start-up phase of the operation.

• Assuming one processing facility for multiple fisheries/products will need a structure that provides flexibility of use. i.e.. Fee for service for individual components to complete service of processing and selling.

• Facility to accommodate the larger users to generate revenue first up. Then investments can be made in smaller processes and production lines.

• Commitment of supply - what happens when the return is better without using the NT processing facility?

44

Workshop 2: Viability - Summary Outputs

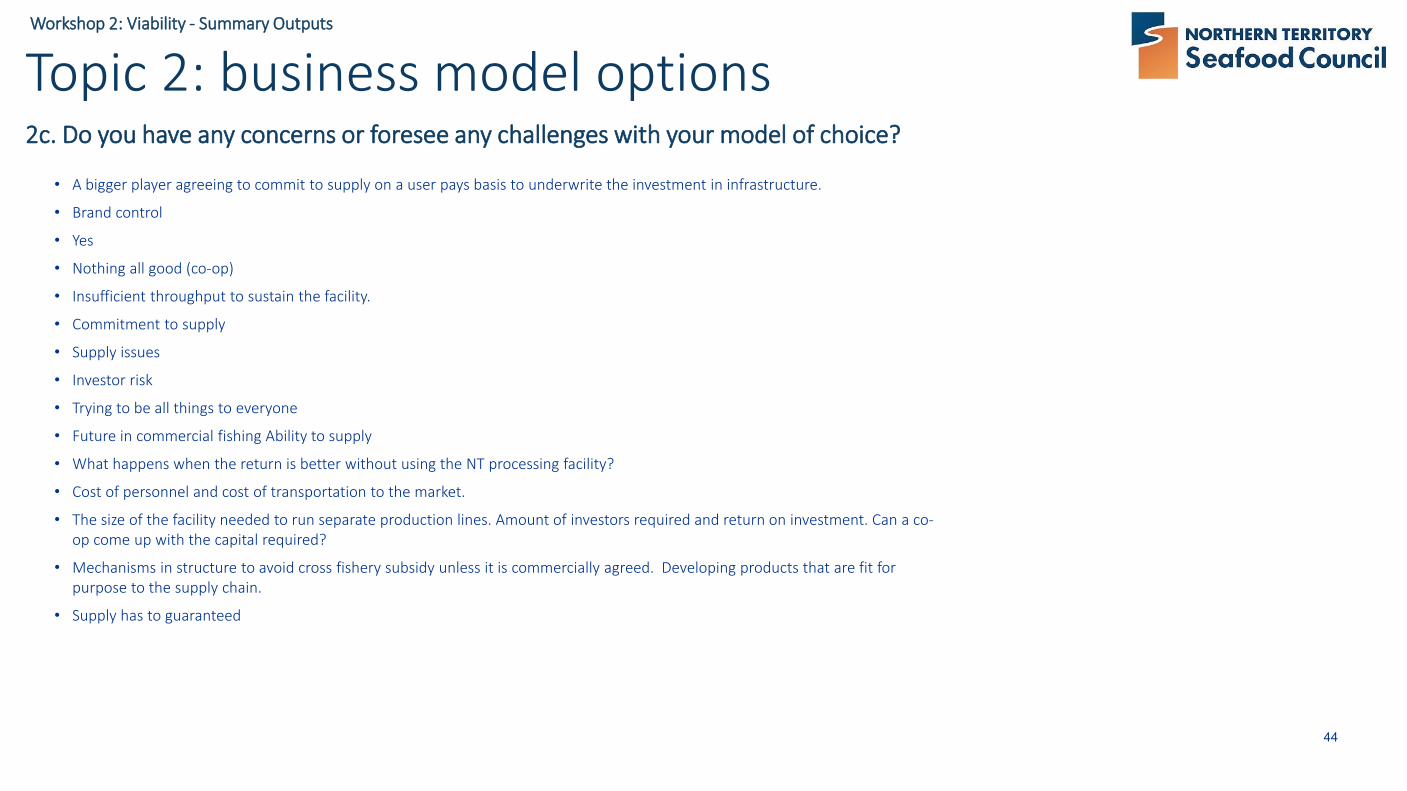

Topic 2: business model options2c. Do you have any concerns or foresee any challenges with your model of choice?

• A bigger player agreeing to commit to supply on a user pays basis to underwrite the investment in infrastructure.

• Brand control

• Yes

• Nothing all good (co-op)

• Insufficient throughput to sustain the facility.

• Commitment to supply

• Supply issues

• Investor risk

• Trying to be all things to everyone

• Future in commercial fishing Ability to supply

• What happens when the return is better without using the NT processing facility?

• Cost of personnel and cost of transportation to the market.

• The size of the facility needed to run separate production lines. Amount of investors required and return on investment. Can a co-op come up with the capital required?

• Mechanisms in structure to avoid cross fishery subsidy unless it is commercially agreed. Developing products that are fit for purpose to the supply chain.

• Supply has to guaranteed

45

Workshop 2: Viability - Summary Outputs

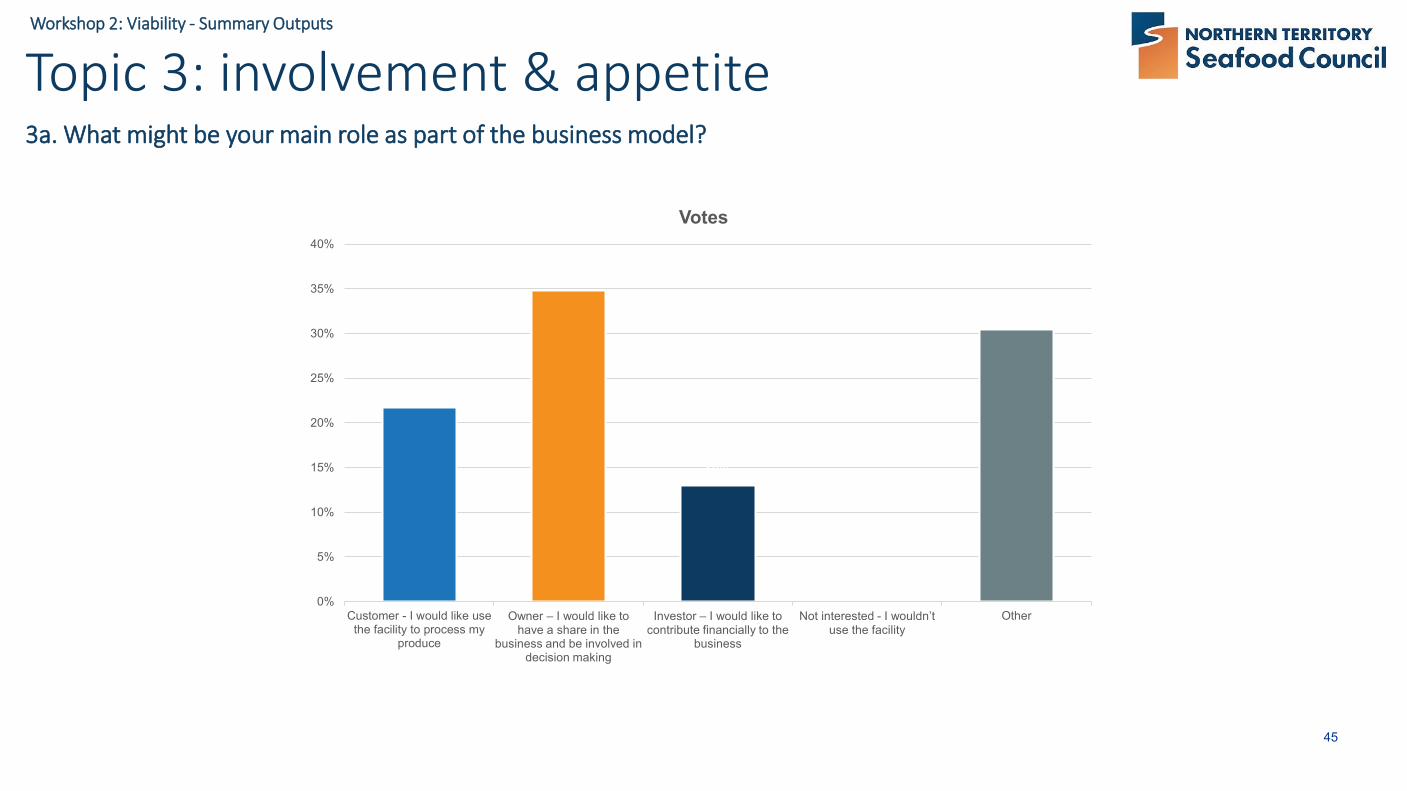

Topic 3: involvement & appetite3a. What might be your main role as part of the business model?

22%

35%

13%

0%

30%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Customer - I would like usethe facility to process my

produce

Owner – I would like to have a share in the

business and be involved in decision making

Investor – I would like to contribute financially to the

business

Not interested - I wouldn’t use the facility

Other

Votes

46

Workshop 2: Viability - Summary Outputs

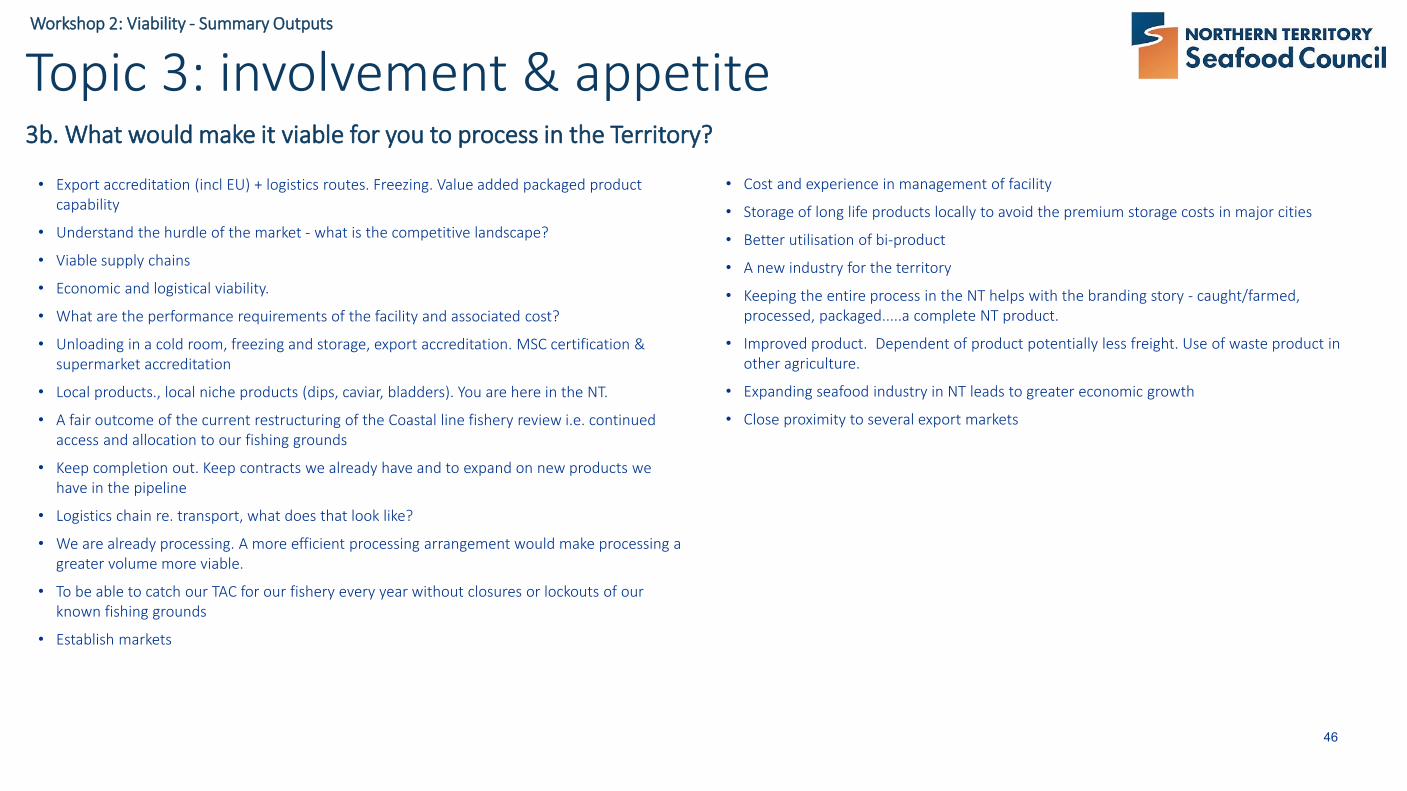

Topic 3: involvement & appetite3b. What would make it viable for you to process in the Territory?

• Export accreditation (incl EU) + logistics routes. Freezing. Value added packaged product capability

• Understand the hurdle of the market - what is the competitive landscape?

• Viable supply chains

• Economic and logistical viability.

• What are the performance requirements of the facility and associated cost?

• Unloading in a cold room, freezing and storage, export accreditation. MSC certification & supermarket accreditation

• Local products., local niche products (dips, caviar, bladders). You are here in the NT.

• A fair outcome of the current restructuring of the Coastal line fishery review i.e. continued access and allocation to our fishing grounds

• Keep completion out. Keep contracts we already have and to expand on new products we have in the pipeline

• Logistics chain re. transport, what does that look like?

• We are already processing. A more efficient processing arrangement would make processing a greater volume more viable.

• To be able to catch our TAC for our fishery every year without closures or lockouts of our known fishing grounds

• Establish markets

• Cost and experience in management of facility

• Storage of long life products locally to avoid the premium storage costs in major cities

• Better utilisation of bi-product

• A new industry for the territory

• Keeping the entire process in the NT helps with the branding story - caught/farmed, processed, packaged.....a complete NT product.

• Improved product. Dependent of product potentially less freight. Use of waste product in other agriculture.

• Expanding seafood industry in NT leads to greater economic growth

• Close proximity to several export markets

47

Workshop 2: Viability - Summary Outputs

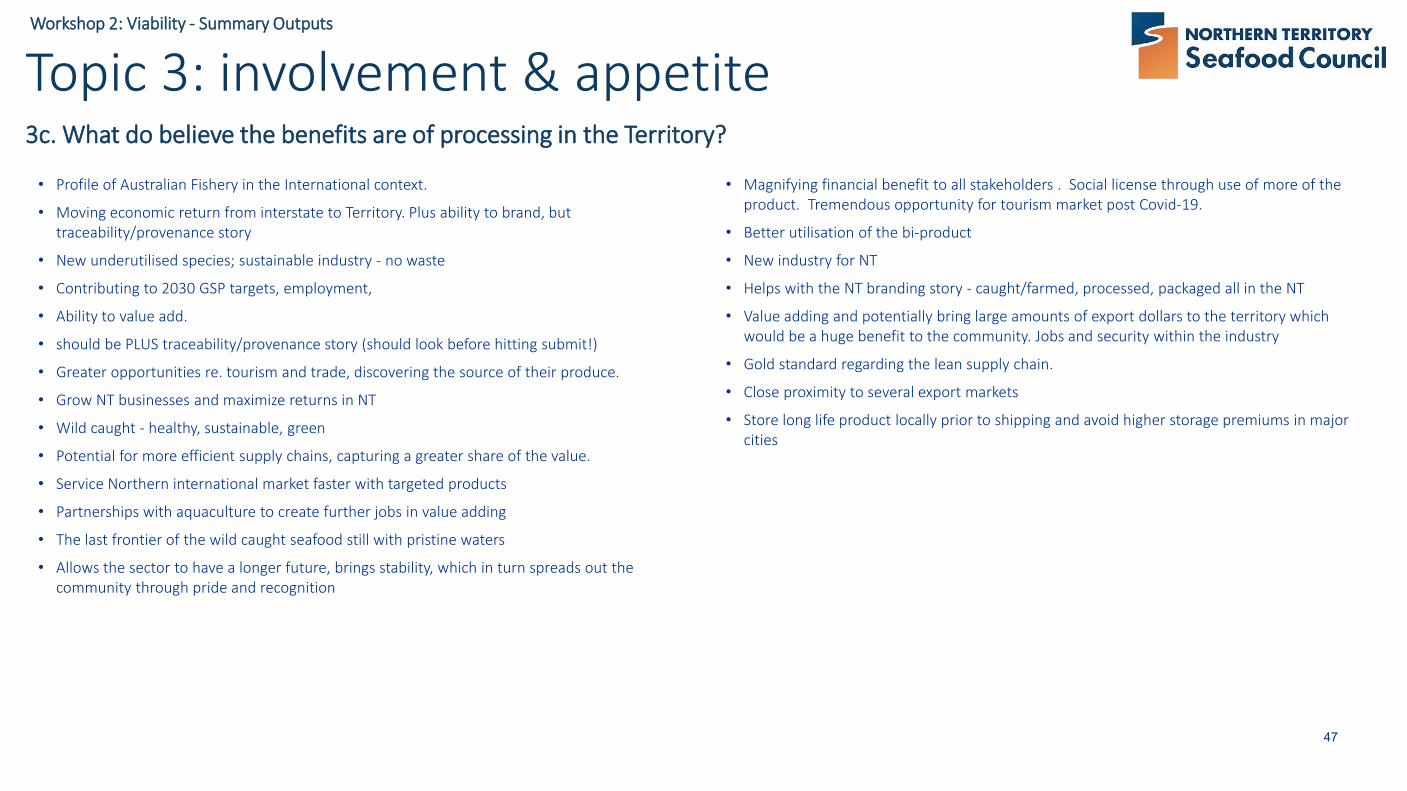

Topic 3: involvement & appetite3c. What do believe the benefits are of processing in the Territory?

• Profile of Australian Fishery in the International context.

• Moving economic return from interstate to Territory. Plus ability to brand, but traceability/provenance story

• New underutilised species; sustainable industry - no waste

• Contributing to 2030 GSP targets, employment,

• Ability to value add.

• should be PLUS traceability/provenance story (should look before hitting submit!)

• Greater opportunities re. tourism and trade, discovering the source of their produce.

• Grow NT businesses and maximize returns in NT

• Wild caught - healthy, sustainable, green

• Potential for more efficient supply chains, capturing a greater share of the value.

• Service Northern international market faster with targeted products

• Partnerships with aquaculture to create further jobs in value adding

• The last frontier of the wild caught seafood still with pristine waters

• Allows the sector to have a longer future, brings stability, which in turn spreads out the community through pride and recognition

• Magnifying financial benefit to all stakeholders . Social license through use of more of the product. Tremendous opportunity for tourism market post Covid-19.

• Better utilisation of the bi-product

• New industry for NT

• Helps with the NT branding story - caught/farmed, processed, packaged all in the NT

• Value adding and potentially bring large amounts of export dollars to the territory which would be a huge benefit to the community. Jobs and security within the industry

• Gold standard regarding the lean supply chain.

• Close proximity to several export markets

• Store long life product locally prior to shipping and avoid higher storage premiums in major cities

48

Workshop 3 – raw data

49

Workshop 3: Location & Business Model - Summary Outputs

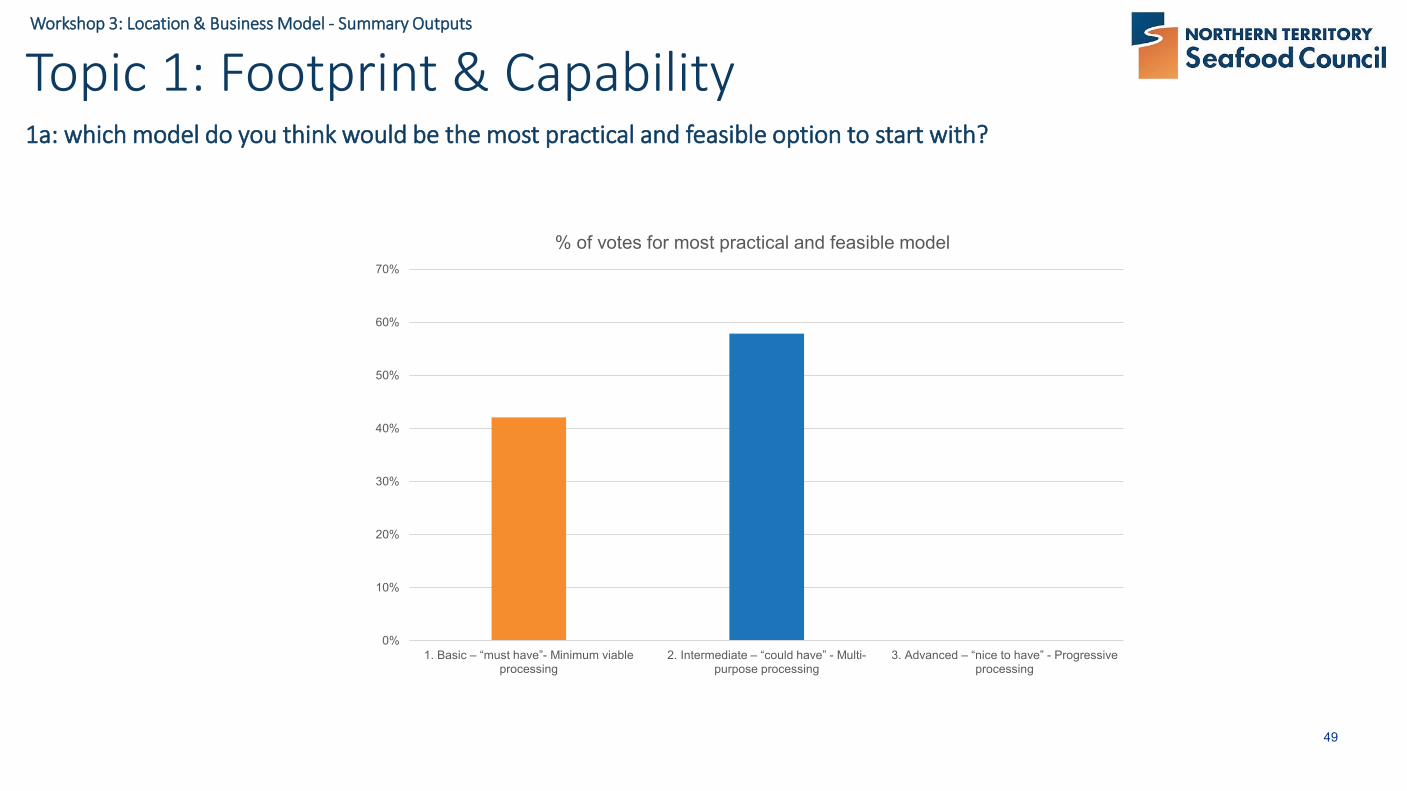

Topic 1: Footprint & Capability1a: which model do you think would be the most practical and feasible option to start with?

0%

10%

20%

30%

40%

50%

60%

70%

1. Basic – “must have”- Minimum viable processing

2. Intermediate – “could have” - Multi-purpose processing

3. Advanced – “nice to have” - Progressive processing

% of votes for most practical and feasible model

50

Workshop 3: Location & Business Model - Summary Outputs

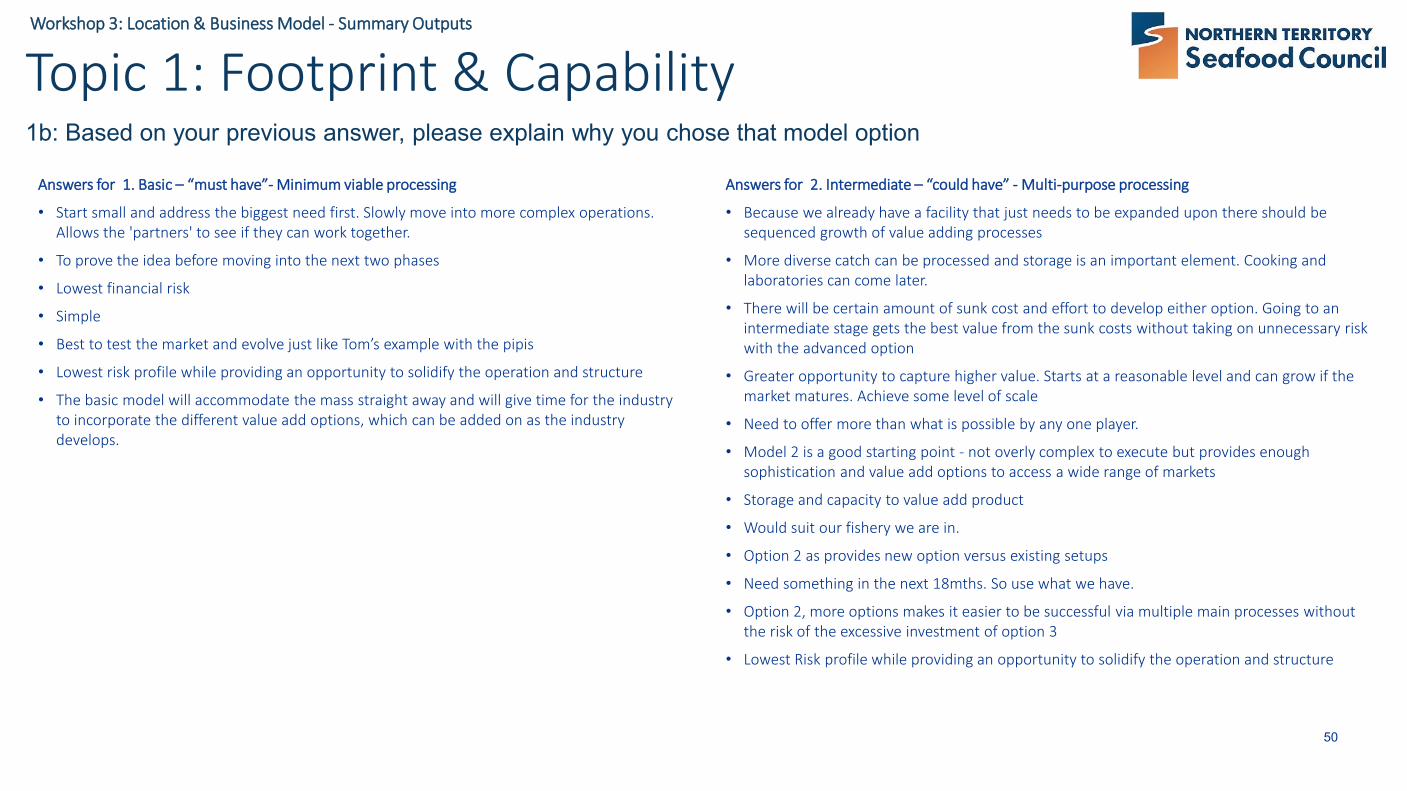

Answers for 1. Basic – “must have”- Minimum viable processing

• Start small and address the biggest need first. Slowly move into more complex operations. Allows the 'partners' to see if they can work together.

• To prove the idea before moving into the next two phases

• Lowest financial risk

• Simple

• Best to test the market and evolve just like Tom’s example with the pipis

• Lowest risk profile while providing an opportunity to solidify the operation and structure

• The basic model will accommodate the mass straight away and will give time for the industry to incorporate the different value add options, which can be added on as the industry develops.

Topic 1: Footprint & Capability1b: Based on your previous answer, please explain why you chose that model option

Answers for 2. Intermediate – “could have” - Multi-purpose processing

• Because we already have a facility that just needs to be expanded upon there should be sequenced growth of value adding processes

• More diverse catch can be processed and storage is an important element. Cooking and laboratories can come later.

• There will be certain amount of sunk cost and effort to develop either option. Going to an intermediate stage gets the best value from the sunk costs without taking on unnecessary risk with the advanced option

• Greater opportunity to capture higher value. Starts at a reasonable level and can grow if the market matures. Achieve some level of scale

• Need to offer more than what is possible by any one player.

• Model 2 is a good starting point - not overly complex to execute but provides enough sophistication and value add options to access a wide range of markets

• Storage and capacity to value add product

• Would suit our fishery we are in.

• Option 2 as provides new option versus existing setups

• Need something in the next 18mths. So use what we have.

• Option 2, more options makes it easier to be successful via multiple main processes without the risk of the excessive investment of option 3

• Lowest Risk profile while providing an opportunity to solidify the operation and structure

51

Workshop 3: Location & Business Model - Summary Outputs

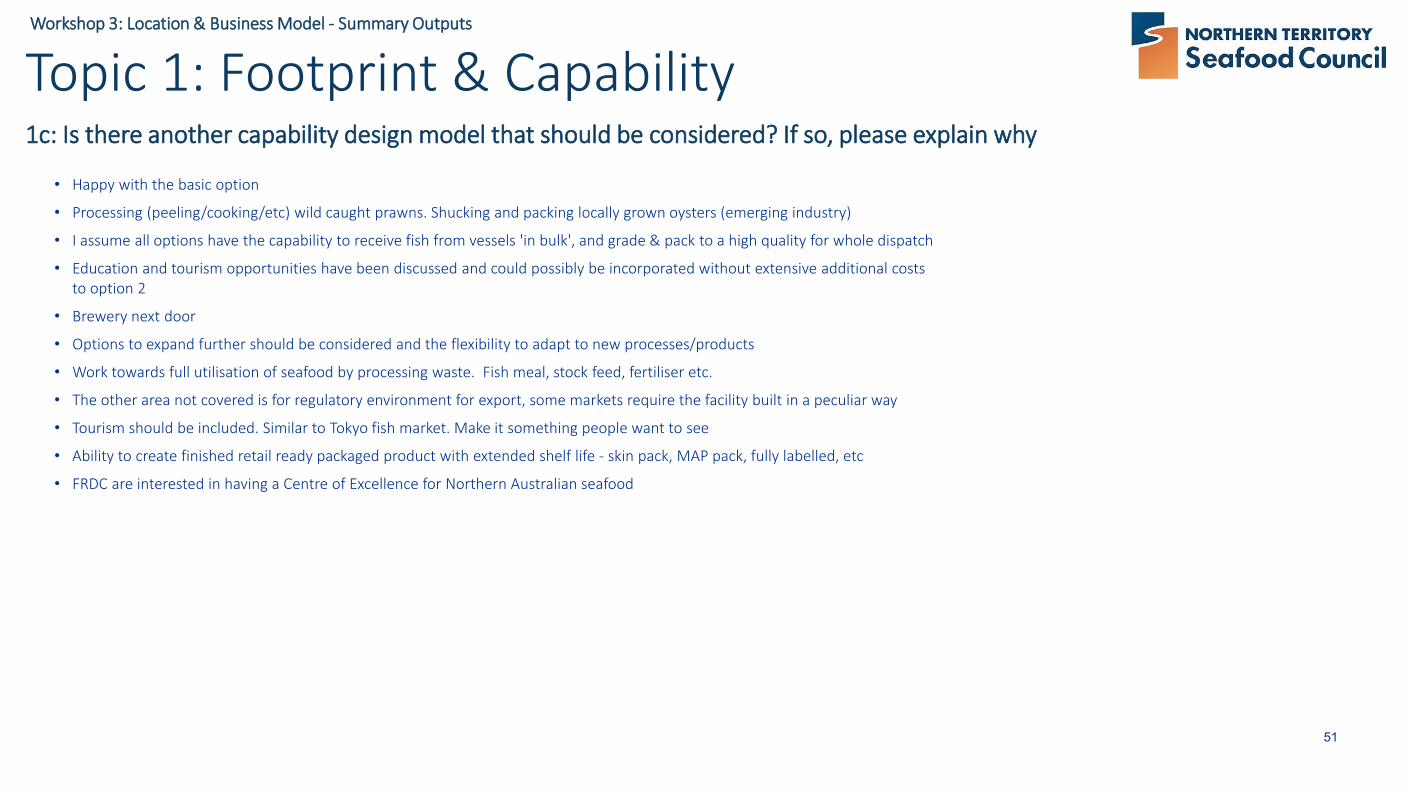

Topic 1: Footprint & Capability1c: Is there another capability design model that should be considered? If so, please explain why

• Happy with the basic option

• Processing (peeling/cooking/etc) wild caught prawns. Shucking and packing locally grown oysters (emerging industry)

• I assume all options have the capability to receive fish from vessels 'in bulk', and grade & pack to a high quality for whole dispatch

• Education and tourism opportunities have been discussed and could possibly be incorporated without extensive additional coststo option 2

• Brewery next door

• Options to expand further should be considered and the flexibility to adapt to new processes/products

• Work towards full utilisation of seafood by processing waste. Fish meal, stock feed, fertiliser etc.

• The other area not covered is for regulatory environment for export, some markets require the facility built in a peculiar way

• Tourism should be included. Similar to Tokyo fish market. Make it something people want to see

• Ability to create finished retail ready packaged product with extended shelf life - skin pack, MAP pack, fully labelled, etc

• FRDC are interested in having a Centre of Excellence for Northern Australian seafood

52

Workshop 3: Location & Business Model - Summary Outputs

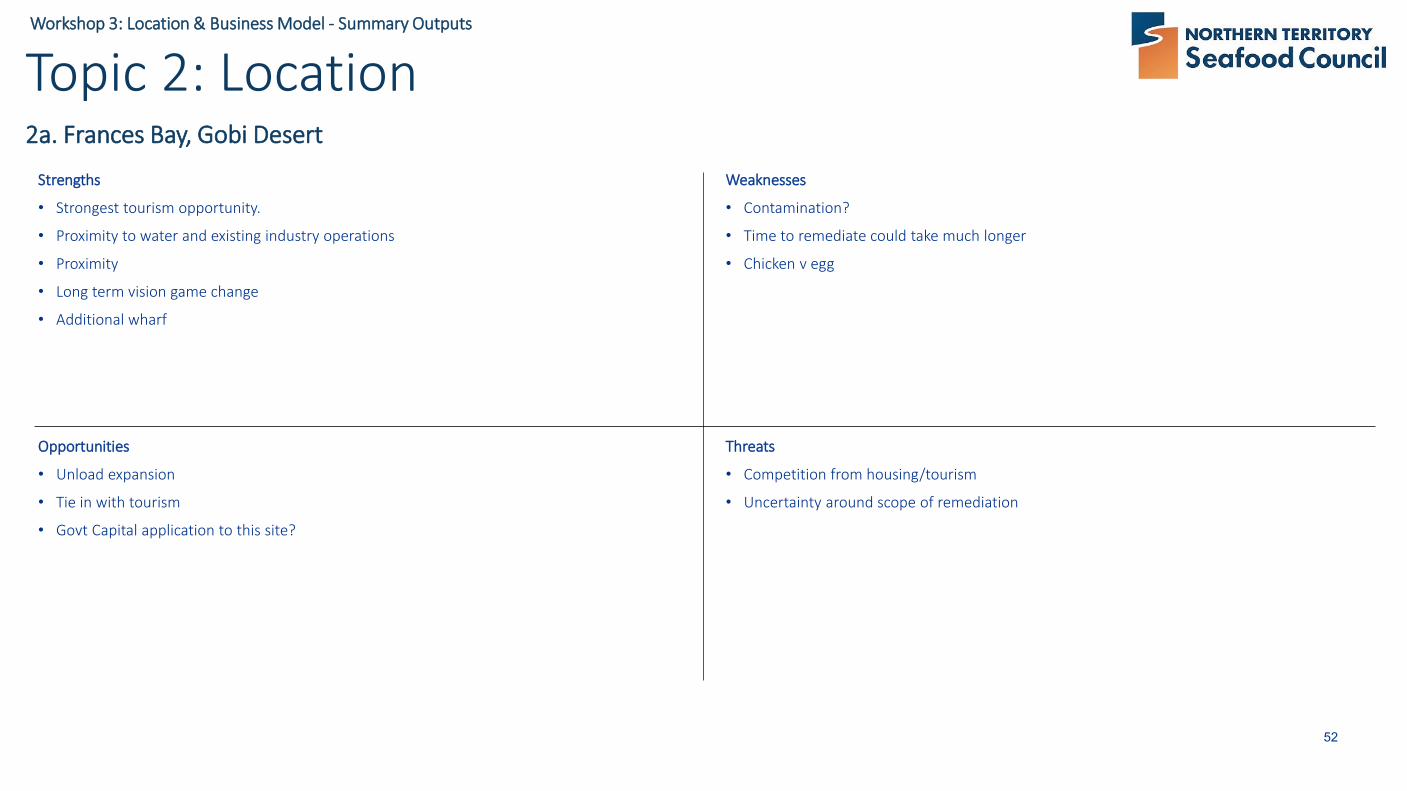

Topic 2: Location2a. Frances Bay, Gobi Desert

Strengths

• Strongest tourism opportunity.

• Proximity to water and existing industry operations

• Proximity

• Long term vision game change

• Additional wharf

Weaknesses

• Contamination?

• Time to remediate could take much longer

• Chicken v egg

Opportunities

• Unload expansion

• Tie in with tourism

• Govt Capital application to this site?

Threats

• Competition from housing/tourism

• Uncertainty around scope of remediation

53

Workshop 3: Location & Business Model - Summary Outputs

Topic 2: Location2b. Airport

Strengths

• No DCA

• Commonwealth land

• Stage 1 facility while waiting for Frances Bay land to become available

Weaknesses

• What is access for interstate trucks like?

• Multiple handoffs of product

• I don't consider proximity to unloading to be a weakness

Opportunities

• Start now

• Collaboration

• Stage 1 facility while waiting for Frances Bay land

Threats

• Waste disposal (at all sites).

• Seafood processing tends to use lots of salt. Sewers don't like salt.

54

Workshop 3: Location & Business Model - Summary Outputs

Topic 2: Location2c. Frances Bay Site: Paspaley Group site

Strengths

• Proximity to water, potential utilisation of existing berthing infrastructure

• Tourism opportunity

• Direct seaside access ready today.

• Location, location, location!

• Co-investment opportunity by owner.

• Master plan opportunity

• Able to scale at pace of demand potentially using existing facilities

• Ancillary uses as multipliers available.

Weaknesses

• Is the seafood option financially best use of site

• when seeking export approvals, the site and neighbors are taken into consideration. Previous Industrial usage may make that more difficult.

Opportunities

• Long term a full tourism/seafood complex

• access to sea water for live seafoods

• Buy from the boat, eat at the tourism precinct

• Depending on Governance model, room for a ‘corporate’ or ‘co-opp’ type business to expand.

• Utilisation of existing infastructure around site.

• Land/Facility investor

• Long term tenure (purchase) also an option.

Threats

• Competition from housing/tourism

• Logistics - Long term - Trucks moving on roads surrounding site.

• Adjoining services… are they there?

• Commercial v strategic approach to development

55

Workshop 3: Location & Business Model - Summary Outputs

Topic 1: Footprint & Capability2d: Based on all the discussion and what you know, please rank the sites from 1 – most desirable to 5 – least desirable

0%

50%

100%

1st place 2nd place 3rd place 4th place 5th place

Ranking of Location

Frances Bay – Gobi Desert

Airport – Greenfield near new export facility

Frances Bay – Paspaley Group Workboats site

Frances Bay – Lot 6656 Fisherman’s Wharf

East Arm – Greenfield & potential marine park co-location

0%

5%

10%

15%

20%

25%

30%

35%

Frances Bay –Paspaley Group Workboats site

Airport – Greenfield near new export

facility

Frances Bay – Gobi Desert

East Arm –Greenfield &

potential marine park co-location

Frances Bay – Lot 6656 Fisherman’s

Wharf

Weighted % of most desirable site voted by participants