Dallas - 4th Quarter 2009 - Executive Management Series

96

-

Upload

texas-housing-conference -

Category

Documents

-

view

215 -

download

1

description

This workbook was designed specifically for the Dallas, Texas seminar held on December 1, 2009.

Transcript of Dallas - 4th Quarter 2009 - Executive Management Series

TEXAS AFFILIATION OF AFFORDABLE HOUSING PROVIDERS

814 San Jacinto Blvd., Ste. 480, Austin, TX, 78701 l Tel: 512.476.9901 l Fax: 512-476-9903 l www.taahp.prg l www.texashousingconference.org

December 1, 2009 Welcome to the Texas Affiliation of Affordable Housing Providers (TAAHP) 4th Quarter Executive Management Series on housing production. TAAHP is pleased to have the opportunity of providing you with a comprehensive look at financing today. As our industry struggles to secure a financing product in today’s market, the US Department of Housing and Urban Development (HUD) and the Texas Department of Housing and Community Affairs (TDHCA) will present viable options in helping you meet your business plan. The TAAHP 4th Quarter Executive Management Series is supported and underwritten by our following partners: Coats Rose, Davis-Penn Mortgage Co., Dougherty Mortgage, LLC, Gardere, and Shackelford, Melton & McKinley Attorneys and Counselors. The TAAHP Executive Management Series provides informative and “how to” educational sessions to the housing industry throughout the year. We encourage you to take a few minutes and go to our website www.taahp.org for a general overview of our member services as well as www.taahp.org/education.html for future Executive Management Series and scheduling. You can help us improve on our Series by sharing your comments regarding the 4th quarter sessions or inquiries into future educational needs at [email protected] or tell us while at www.taahp.org . We hope you will mark your calendars for the State’s premier 2010 Texas Housing Conference, July 26 – 28, 2010, Four Seasons Hotel, Austin, Texas. The Summer Executive Management Educational Series and networking with fellow “housers”, suppliers, vendors and professional services providers will provide unlimited opportunities to enhance your bottom line. We look forward to seeing you again soon and at the Texas Housing Conference in July. Best Regards,

Jim T. Brown Executive Director

OFFICERS: PRESIDENT: LINDA MCMAHON NEIGHBORHOOD STRATEGIES, LLC IMMEDIATE PAST PRESIDENT: MIKE SUGRUE SOLUTIONS PLUS! PRESIDENT-ELECT: DAN MARKSON THE NRP GROUP VICE PRESIDENT: TONI JACKSON COATS ROSE VICE PRESIDENT: BARRY KAHN HETTIG-KAHN TREASURER: GEORGE LITTLEJOHN NOVOGRADAC & CO. LLP SECRETARY: NICOLE FLORES PNC MULTIFAMILY

CAPITAL DIRECTORS: MAHESH AIYER WELLS FARGO BANK SARAH ANDERSON S. ANDERSON

CONSULTING SALLY GASKIN SGI VENTURES, INC. DENNIS HOOVER HAMILTON VALLEY MANAGEMENT, INC. ROBERT JOHNSTON NATIONAL EQUITY FUND MARK MAYFIELD TEXAS HOUSING

FOUNDATION JEFFREY SPICER STATE STREET HOUSING ADVISORS, L.P. RON WILLIAMS SOUTHEAST TEXAS

HOUSING FINANCE CORPORATION JERRY WRIGHT DOUGHERTY & COMPANY, LLC EXECUTIVE DIRECTOR: JIM T. BROWN

rev. - August 2009

O f f i c e r s President Linda McMahon (11) Neighborhood Strategies LLC 4460 St. Andrews Blvd Irving, TX 75038 T: (214) 596-9162 F: N/A [email protected] ---------------------------------------------- Immediate Past President Mike Sugrue (10) Solutions Plus 1302 South 3rd, Ste. 105 Mabank, TX 75147 T: (903) 887-4344 F: (903) 334-4355 [email protected] ---------------------------------------------- President Elect Dan Markson (10) The NRP Group 111 Soledad, Ste. 1220 San Antonio, TX 78205 T: (210) 487-7878 F: (210) 487-7880 [email protected] ---------------------------------------------- Vice President Toni Jackson (11) Coats Rose 3 Greenway, Ste. 2000 Houston, TX 77046 T: (713) 653-7392 F: (713) 890-3928 [email protected] ---------------------------------------------- Vice President Barry Kahn (10) Hettig-Kahn Development, Co. 5325 Katy Freeway, Ste. One Houston, TX 77007 T: (713) 871-0063 F: (713) 871-1916 [email protected] ----------------------------------------------

Treasurer George Littlejohn (10) Novogradac & Company LLP 11044 Research Blvd., Bldg. C, Ste. 400 Austin, TX 78759 T: (512) 340-0420 F: (512) 340-0421 george.littlejohn@ novoco.com ---------------------------------------------- Secretary Nicole Flores (12) PNC MultiFamily Capital 1717 W. 6th St., Ste. 262 Austin, TX 78703 T: (512) 391-9084 F: (512) 454-8021 [email protected] ----------------------------------------------

D i r e c t o r s Mahesh Aiyer (12) Wells Fargo Bank, N.A. 1000 Louisiana, Suite 1030 Houston, TX 77002 T: (713) 319-1489 F: (713) 319-1794 mahesh.aiyer@ wellsfargo.com Sarah Anderson (12) S. Anderson Consulting 1305 E. 6th, #12 Austin, TX 78702 T: (512) 554-4721 F: (512) 231-8580 sarah@ sarahandersonconsulting.com Mike Clark (10) Alpha-Barnes Real Estate Services 12720 Hillcrest, Ste. 400 Dallas, TX 75230 T: (972) 643-3205 F: (972) 503-7569 [email protected] Sally Gaskin (11) SGI Ventures, Inc. 1800 Bering Dr., Ste. 501 Houston, TX 77057 T: (713) 334-4911 F: (713) 334-5614 [email protected] Dennis Hoover (12) Hamilton Valley Mgmt., Inc. P.O. Box 190 Burnet, TX 78611 T: (512) 756-6809 F: (512) 756-9885 dennishoover@ hamiltonvalley.com

“Increasing the supply and quality of affordable housing for Texans with limited incomes and special needs”

Texas Affiliation of Affordable Housing Providers: Board of Directors: 2009 - 2010

rev. - August 2009

D i r e c t o r s Robert Johnston (11) National Equity Fund P.O. Box 835727 Richardson, TX 75083 T: (972) 342-6621 F: N/A [email protected] Mark Mayfield (10) Texas Housing Foundation 1110 Broadway Marble Falls, TX 78654 T: (830) 693-4521 F: (830) 693-5128 [email protected] Jeffrey Spicer (12) State Street Housing Advisors, L.P. 5843 Royal Crest Dr. Dallas, TX 75230 T: (214) 346-0707 F: (214) 346-0713 jspicer@ statestreethousing.com Ron Williams (11) Southeast Texas Housing Finance Corp. 11111 S. Sam Houston Pkwy. East Houston, TX 77089 T: (281) 484-4663 x108 F: (281) 484-1971 [email protected] Jerry Wright (11) Jerry L. Wright Dougherty & Company LLC 410 East 5th Street, Suite 112 Austin, TX 78701 T: (512) 708-1555 F: (612) 235-3356 JWright@ doughertymarkets.com

E x - O f f i c i o Edwina Carrington (1999) Reznick Group, P.C. 100 Congress Ave., Ste. 480 Austin, TX 78701 T: (512) 494-9100 F: (512) 494-9101 edwina.carrington@ reznickgroup.com JOT Couch (02) Texas Inter-Faith 3131 West Alabama, Ste. 300 Houston, TX 77089 T: (713) 526-6634 ext. 22 F: (713) 526-7019 [email protected] Dick Kilday (00) Kilday Realty Corp. 1717 Saint James Pl., Suite 150 Houston, TX 77056-3421 T: (713) 914-9400 F: (713) 914-9439 [email protected]

Mike Lankford (04) Lankford Interests, LLC 4900 Woodway, Ste. 750 Houston, TX 77056 T: (713) 626-9655 F: (713) 621-4947 mlankford@ lankfordinterests.com Granger MacDonald (07) MacDonald & Assoc., Inc. 2951 Fall Creek Kerrville, TX 78028 T: (830) 257-5323 F: (830) 251-3168 gmacdonald@ macdonald-companies.com Diana McIver (06) DMA Development Co., LLC 4101 Parkstone Heights Dr., Ste. 310 Austin, TX 78746 T: (512) 328-3232 ext. 65 F: (512) 328-4584 [email protected] John R. Pitts (09) John R. Pitts P.O. Box 27130 Houston, TX 77227 T: (713) 552-1854 F: N/A [email protected]

Past Presidents--- - - - - - - - - - - - - - - - - - - - - - - - - - 2008 - 2009: Mike Sugrue, Solutions Plus!

2007 - 2008: Mike Clark, Alpha-Barnes Real Estate Services

2006 - 2007: Granger MacDonald, MacDonald & Associates

2005 - 2006: Diana McIver, DMA Development Co., LLC

2004 - 2005: Jerry Wright, Dougherty & Company LLC

2003 - 2004: Mike Lankford, Lankford Interests, LLC

2002 - 2003: Chris Bergman, TCR Affordable Housing, Inc.

2001 - 2002: JOT Couch, Texas Inter-faith Supportive Services

2000 - 2001: Sally Gaskin, SGI Ventures, Inc.

1999 - 2000: Dick Kilday, Kilday Realty Corp

“TAAHP is the leading organization of affordable housing professionals representing the affordable housing industry in Texas.”

www.taahp.org

who we areThe Texas A� liation of A�ordable Housing Providers (TAAHP) is an organization of more than 180 state and national housing providers dedicated to ensuring everyone has a safe and a�ordable place to live. Our members include single and multifamily developers, builders and owners, property managers, investors, lenders, syndicators, architects, attorneys, market analysts, engineers, and nonpro�t organizations.

Through its government relations e�orts, TAAHP projects a powerful voice advocating the interests of the a�ordable housing industry in Texas. TAAHP addresses the e�ects of housing shortages on low income individuals ranging from school teachers, EMS personnel, �re�ghters, police o� cers, nurses, social service workers, and others whose income level falls between government assistance and market rate rental housing standards. Since 1997 TAAHP members have placed in service tens of thousands of a�ordable rental housing units across the state of Texas and the Nation.

what we do Build successful business relationships

Represent tens of thousands of a�ordable housing units

Work for laws, regulations, and programs necessary for the development of a viable a�ordable housing inventory in Texas

Support our members through various services ranging from merchandising to health care programs

community

taahp.org

taahp-pac

Your Voice and Vigilance in Austin

impact

legislative representation

“TAAHP is the leading organization of a�ordable housing professionals representing the a�ordable housing industry in Texas.”

health bene�tprogram

become a member today - see reverse side for detailsFor more information visit www.taahp.org or call (512) 476-9901.

American Express Discover MasterCard VISA

Check (make payable to

Credit Card #_______________________________________________

Expiration Date________________Veri�cation Number_____________

Name (as it appears on card)___________________________________

Signature___________________________________________________A 3% processing fee will be added to all credit card transactions.

Member Information

Date______________________________________________________________

Company/Organization__________________________________________

Name___________________________________________________________

Address_________________________________________________________

Tel________________________________________________________________

Fax_______________________________________________________________

State_____________________________Zip_____________________________

Website__________________________________________________________

Email ____________________________________________________________

Title_____________________________________________________________

City______________________________________________________________

Method of Investment

Voting Membership

Lifetime Membership - $10,000.00A member in this category shall have all privileges of an Active Member, and is entitled to this designation by paying a one-time membership dues fee as determined annually by the TAAHP Board of Directors. Member-ship services (excluding meeting registration fees) shall continue for the business entity’s lifetime, their resignation, or demise of the organization, whichever occurs �rst.

Active Membership - $550.00Any business, �rm, corporation, partnership, sole proprietorship, individual professional or other legal business entity which is involved in the a�ordable housing industry or provides services, supplies or equipment for the a�ordable housing industry and is directly interested in its welfare, complies with TAAHP Bylaws, pays current dues, and meets required membership quali�cations, is eligible for active membership in TAAHP and is entitled to one vote per membership, eligibility for service on the Board of Directors, and all committees following appointment.

Second Active Membership (non-voting)-$250.00

Third Active Membership (non-voting)-$100.00

Non-Voting Membership

Governmental / Regulatory Membership - $150.00Any individual associated with or responsible in any manner within the title of this category may join TAAHP after meeting the quali�ca-tions and paying dues determined by the Board of Directors.

Educators / Student Membership - $50.00Any individual directly associated with an institution of higher learning and whose �eld of study and expertise is related to the �eld of a�ordable housing may join the Organization by meeting the quali�cations and paying dues determined by the Board of Directors. Separate dues may be established for these two classi�cations: Educators and Student.

Federal Income Tax Notice: Membership Investments are not deductible as charitable contributions for federal incomes tax purposes; however, investments are deductible by members as an ordinary business expense. A portion of investments are not deductible as an ordinary business expense to the extent TAAHP engages in lobbying. The non-deductible portion of investments for 2010 is 10%.

_____________________________

______________________________________________________________

_________________________________________________________

_____________________________Zip_____________________________

______________________________________________________________

_________________________________________________________

_____________________________

______________________________________________________________

_____________________________

______________________________________________________________

Texas A� liation of A�ordable Housing Providers2010 Membership Investment Form

814 San Jacinto Blvd., Suite 408 Austin, TX 78701 512.476.991 512.476.9903 www.taahp.org

Send to: Mail 814 San Jacinto Blvd., Suite 408 Fax 512.476.9903 Online www.taahp.org

SAVETHE

DATE

2010 - A HOUSING ODYSSEY

texashous ing

conference

JOIN NAT IONAL &INTERNAT IONAL

AFFORDABLE HOUSING

INDUSTRY PROFESSIONALS IN

AUST IN, TX TO EXCHANGE

KNOWLEDGE, D ISCOVER

SOLUT IONS, AND NETWORK!

2009 PLAT INUM PARTNERS

WAS YOUR STATEAMONG THOSEREPRESENTEDIN 2009?

26 - 28, 2010FOUR SEASONS HOTEL

AUSTIN, TEXAS

www.texashous ingconference.org

Texas Housing Conference

QUICK FACTS

30%

23%9%

8%

6%

6%

6%

4%3%

3%2%

Developer/Owner

Investor/Lender/Syndicator

Government

Housing Finance Corporation/Market

Analysis/Professional Services

Property Management/Real Estate Services

Trade Associations/Others

Legal Services

Architects/Engineers/Construction

Vendor/Supplier

Local Public Housing

Utility Providers

www . t e xa shous i n gcon f e r e nce . o r g

Texas Housing ConferenceATTENDANCEBY SERVICE

2010 Marks the 12th anniversary of the Texas Housing Conference; Texas’ premier housing conference.

2010's Conference will be held at Austin’s magnificent Four Seasons Hotel located on Ladybird Lake in Austin’s cultural, central business and recreational district.

Expected attendance at the 2010 Texas Housing Conference is 500+.

Conference participants have helped provide over 300,000 affordable multifamily and single family housing units in Texas alone and more throughout the United States using USDA, HUD, and Tax Credit programs.

Regular attendance and participation of key Texas officials: Administrative and Legislative.

Regular support, attendance, and participation by the Governing Board and Executive Officers of the Texas Department of Housing and Community Affairs (TDHCA).

Conference partners range from affordable housing service providers to construction material and appliance suppliers.

Over 20 educational sessions addressing legislative policies, sustainable design, market issues, financing, equity, compliance and construction related issues will be offered.

Local, national, and international speakers.

ATAA TORNEYS & COUNSELORS

Texas Department of Housing and Community

Affairs

2010 Regional Allocation

Estimated State Credit Ceiling is $51 million

85% of the State Credit Ceiling to be divided

between the 13 State Service Regions and

further split into urban and rural areas

Statewide rural collapse (first) Statewide urban/rural collapse (second)

13 State Service Regions

2010 Regional Allocation

Region Geographic RegionRegional Amount

Regional %

Rural Amount Rural %

Urban Amount

Urban %

1 Lubbock $ 1,581,297 3.6% $ 614,986 38.9% $ 966,311 61.1%

2 Abilene $ 787,781 1.8% $ 556,545 70.6% $ 231,236 29.4%

3 Dallas/Ft Worth Metro $ 10,741,365 24.7% $ 1,123,991 10.5% $ 9,617,373 89.5%

4 Tyler $ 1,618,171 3.7% $ 908,883 56.2% $ 709,288 43.8%

5 Beaumont $ 1,189,640 2.7% $ 655,179 55.1% $ 534,460 44.9%

6 Houston Metro $ 9,455,772 21.8% $ 892,787 9.4% $ 8,562,985 90.6%

7 Austin Metro $ 2,942,660 6.8% $ 617,443 21.0% $ 2,325,216 79.0%

8 Waco $ 2,141,376 4.9% $ 594,798 27.8% $ 1,546,578 72.2%

9 San Antonio Metro $ 3,456,058 8.0% $ 631,952 18.3% $ 2,824,106 81.7%

10 Corpus Christi $ 1,495,468 3.4% $ 592,835 39.6% $ 902,633 60.4%

11 Brownsville/Harlingen $ 5,134,386 11.8% $ 1,877,986 36.6% $ 3,256,401 63.4%

12 San Angelo $ 889,167 2.0% $ 559,410 62.9% $ 329,757 37.1%

13 El Paso $ 1,990,508 4.6% $ 590,535 29.7% $ 1,399,973 70.3%

Total $ 43,423,648 100% $ 10,217,329 23.5% $ 33,206,319 76.5%

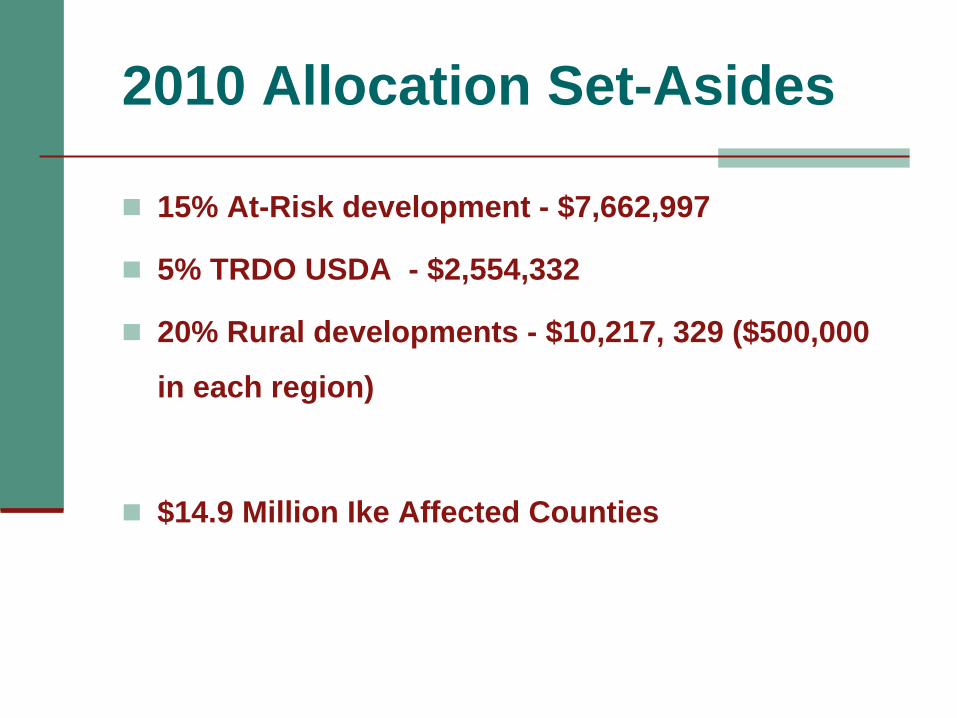

15% At-Risk development - $7,662,997

5% TRDO USDA - $2,554,332

20% Rural developments - $10,217, 329 ($500,000

in each region)

$14.9 Million Ike Affected Counties

2010 Allocation Set-Asides

At-Risk Set-Aside Requirements

Development must be at risk of losing all affordability from all of the financial benefits available on the Development.

Sections 221(d)(3) and (5), National Housing Act (12 U.S.C. §17151);Section 236, National Housing Act (12 U.S.C. §1715z-1);Section 202, Housing Act of 1959 (12 U.S.C. §1701q);Section 101, Housing and Urban Development Act of 1965 (12 U.S.C. §1701s);Section 8 Additional Assistance Program for housing Developments with HUD-Insured and HUD-Held Mortgages administered by the United States Department of Housing and Urban Development;Section 8 Housing Assistance Program for the Disposition of HUD- Owned Projects administered by the United States Department of Housing and Urban Development;Sections 514, 515, and 516, Housing Act of 1949 (§42 U.S.C. §§1484, 1485, and 1486); and/orSection 42, of the Internal Revenue Code of 1986 (26 U.S.C. §42)

One Mile / Three Year Rule One Mile / Three Year Rule Applies to counties over 1 million in populationApplies to counties over 1 million in populationDevelopments proposing new construction or Developments proposing new construction or Adaptive Reuse within one mile of another Adaptive Reuse within one mile of another development serving the same population that development serving the same population that received housing tax credits in the previous received housing tax credits in the previous three yearsthree yearsLocal ResolutionLocal Resolution§§2306.6703(a)(3) Texas Government Code2306.6703(a)(3) Texas Government Code

Texas Statutory LimitationsTexas Statutory Limitations

Texas Statutory LimitationsTexas Statutory Limitations

2 X Per Capita 2 X Per Capita Municipality or County that has twice the Municipality or County that has twice the state average of units per capita supported state average of units per capita supported by housing tax credits or private activity by housing tax credits or private activity bonds. bonds. Local ResolutionLocal Resolution§§2306.6703(a)(4) Texas Government Code2306.6703(a)(4) Texas Government Code

Texas Statutory LimitationsTexas Statutory Limitations

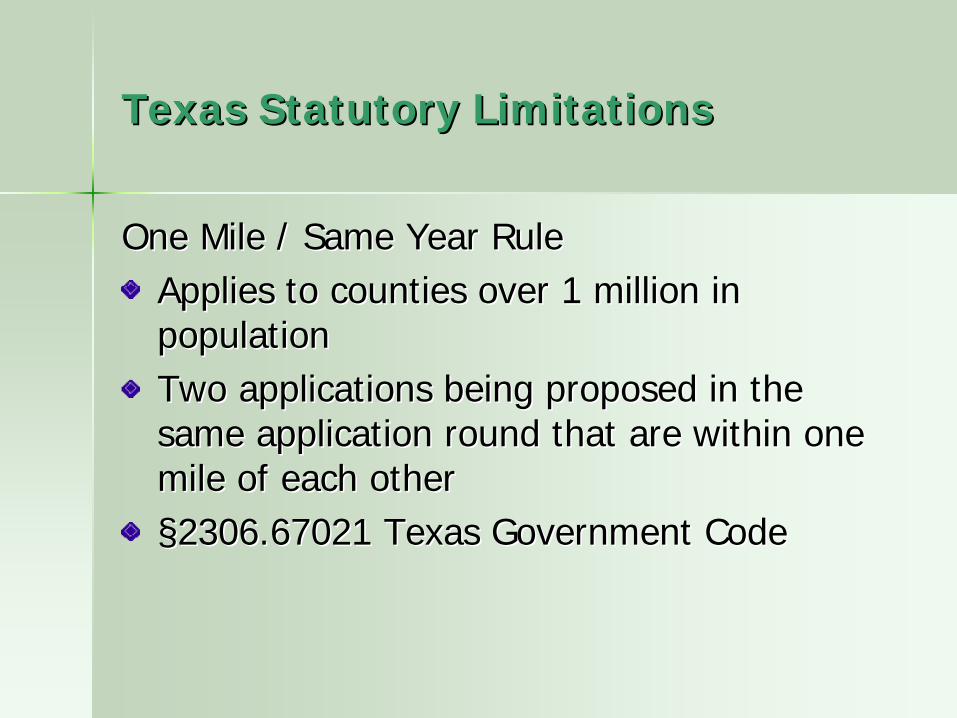

One Mile / Same Year Rule One Mile / Same Year Rule Applies to counties over 1 million in Applies to counties over 1 million in populationpopulationTwo applications being proposed in the Two applications being proposed in the same application round that are within one same application round that are within one mile of each othermile of each other§§2306.67021 Texas Government Code2306.67021 Texas Government Code

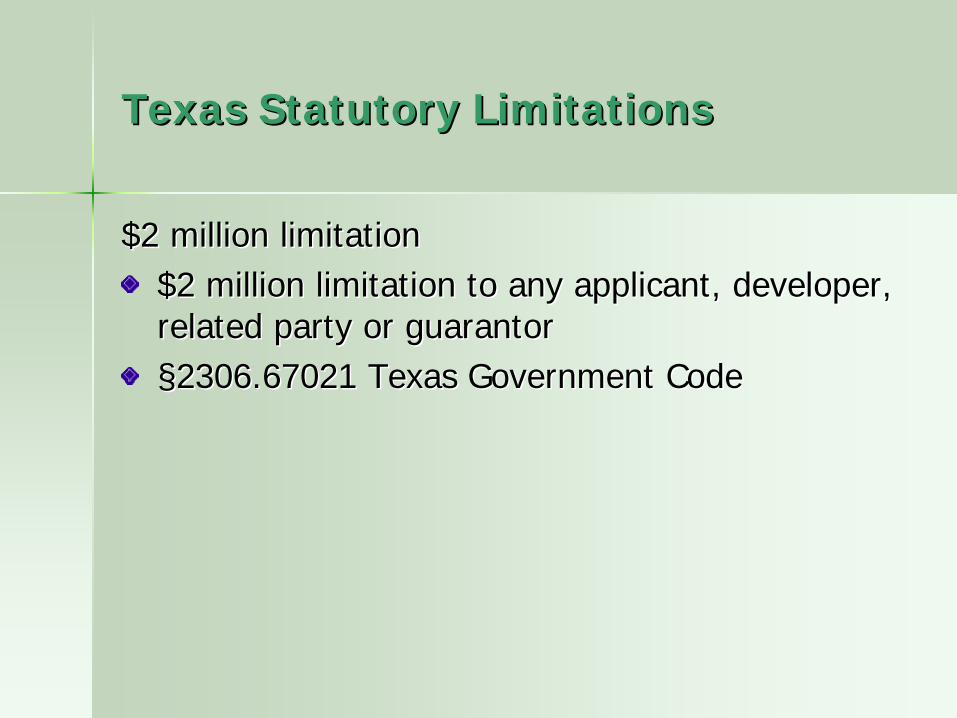

$2 million limitation$2 million limitation$2 million limitation to any applicant, developer, $2 million limitation to any applicant, developer, related party or guarantorrelated party or guarantor§§2306.67021 Texas Government Code2306.67021 Texas Government Code

Texas Statutory LimitationsTexas Statutory Limitations

Texas Development LimitationsTexas Development Limitations

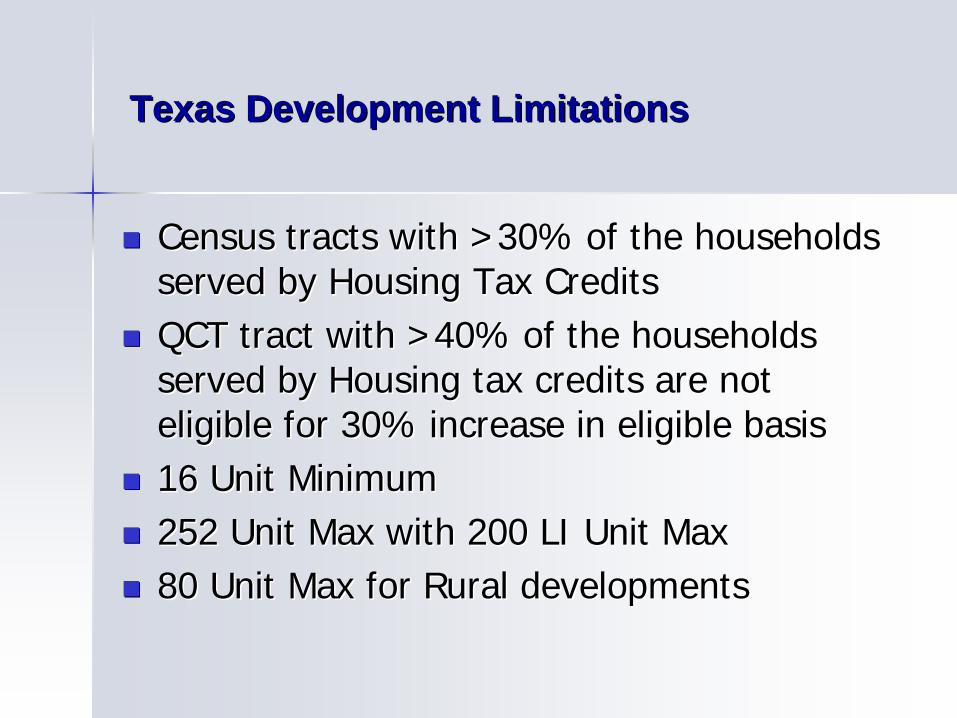

Census tracts with >30% of the households Census tracts with >30% of the households served by Housing Tax Creditsserved by Housing Tax Credits

QCT tract with >40% of the households QCT tract with >40% of the households served by Housing tax credits are not served by Housing tax credits are not eligible for 30% increase in eligible basiseligible for 30% increase in eligible basis

16 Unit Minimum16 Unit Minimum 252 Unit Max with 200 LI Unit Max252 Unit Max with 200 LI Unit Max 80 Unit Max for Rural developments80 Unit Max for Rural developments

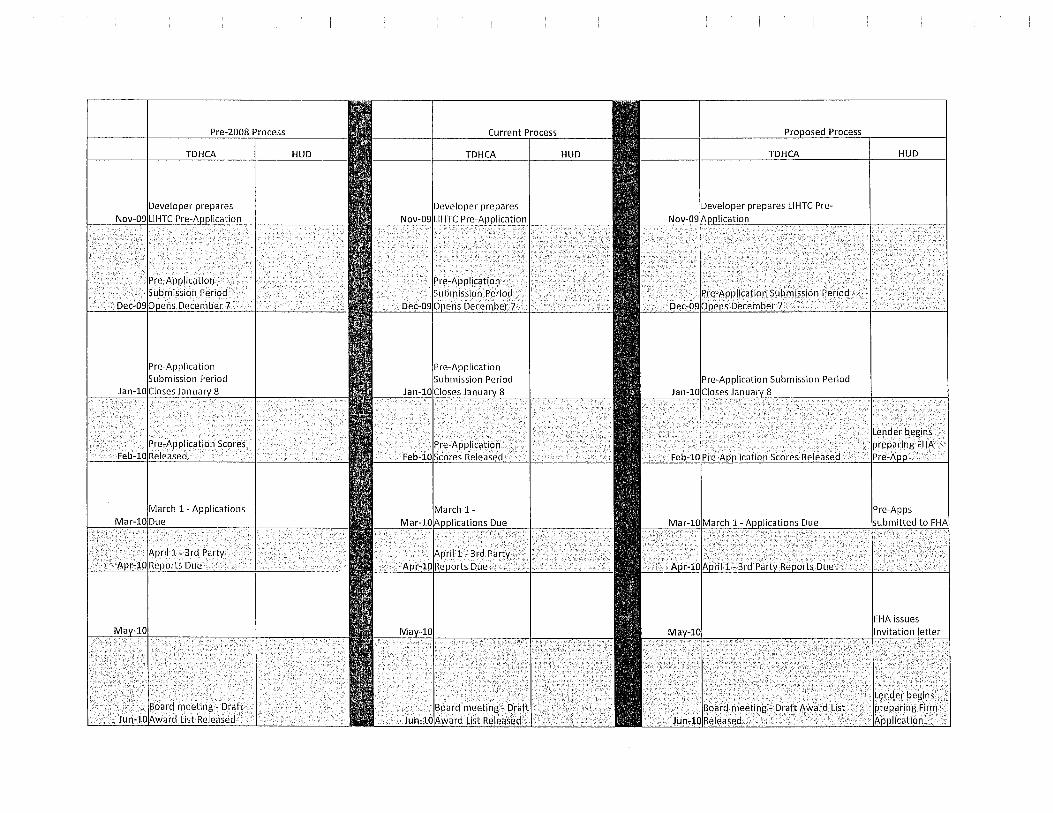

HousingTax CreditTimeline

12/08/200912/08/2009 2010 Application Acceptance 2010 Application Acceptance Period BeginsPeriod Begins

01/08/201001/08/2010 2010 Pre2010 Pre--Application DeadlineApplication Deadline

02/15/201002/15/2010 Experience Certification RequestExperience Certification Request

03/01/201003/01/2010 2010 Full Applications Due 2010 Full Applications Due

04/01/201004/01/2010 ThirdThird--Party Reports / Resolutions Party Reports / Resolutions DueDue

MidMid--MayMay Final Scoring Notices IssuedFinal Scoring Notices Issued

Late JuneLate June Release of Eligible Applications Release of Eligible Applications for Consideration for Award in for Consideration for Award in JulyJuly

2010 Housing Tax Credit Timeline2010 Housing Tax Credit Timeline

Late JulyLate July Final AwardsFinal Awards

MidMid--AugAug Commitments IssuedCommitments Issued

11/01/201011/01/2010 Carryover Documentation DueCarryover Documentation Due

06/30/201106/30/2011 10% Test Documentation10% Test Documentation

12/01/201112/01/2011 Documentation of Documentation of Commencement of Commencement of Substantial Construction Due Substantial Construction Due

12/31/201212/31/2012 Placement in ServicePlacement in Service

2010 Housing Tax Credit Timeline2010 Housing Tax Credit Timeline

Texas Bond Volume Cap

Approximately $481 million in 2010 regular volume cap for multifamily housing

TDHCA Set Aside is approximately $96 million

Application Materials

2010 Application Submission Procedures Manual (ASPM) 2010 Payment Receipt 2010 Uniform Application 2010 Intent to Request 2010 Competitive 9% HTC Pre-Application2010 Quantifiable Community Participation Packet

www.tdhca.state.tx.us/multifamily/Applications.htm

Application Reference Material

2010 HTC Reference Manual 2010 Final Qualified Allocation Plan and Rules (Will be provided when signed by Governor Rick Perry)www.tdhca.state.tx.us/multifamily/Applications.htm

2010 Multifamily Bond Rules2010 Multifamily Bond Pre-Applicationwww.tdhca.state.tx.us/multifamily/bond/index.htm

Common Mistakes

Application or Applicant is ineligible;

Documents were not correctly executed;

All deficiencies were not fully satisfied by the

deadline;

3rd Party Reports were not submitted by deadline;

Documents were not in the correct applicant name;

Inconsistent information in the Application; or

Age of documentation limit was exceeded.

Electronic Submission

The following information may be submitted directly on the TDHCA website: Application Third Party Reports Deficiencies Any large documents required to fulfill application

requirements Post Award Documentation

Regulations, Statues and RulesRegulations, Statues and Rules

oo §§§§42 and 142 of the Internal Revenue Code42 and 142 of the Internal Revenue Codeoo §§2306 of the Texas Government Code2306 of the Texas Government Codeoo §§1372 of the Texas Government Code1372 of the Texas Government Codeoo CFR 24 (Code of Federal Regulations) HOMECFR 24 (Code of Federal Regulations) HOMEoo 10 TAC 10 TAC §§50 Qualified Allocation Plan and Rules50 Qualified Allocation Plan and Rulesoo 10 TAC 10 TAC §§33 Multifamily Revenue Bond Rules33 Multifamily Revenue Bond Rulesoo 10 TAC 10 TAC §§§§1.311.31--1.37 Real Estate Analysis Rules1.37 Real Estate Analysis Rulesoo 10 TAC 10 TAC §§53 HOME Rules 53 HOME Rules oo 10 TAC 10 TAC §§51 Housing Trust Fund Rules51 Housing Trust Fund Rules

Texas Department of Housing and Community Affairs

Multifamily Contacts:

Robbye Meyer [email protected] of Multifamily Finance – (512) 475-2213

Teresa Morales [email protected] / 4% HTC Program Administrator – (512) 475-3344

Raquel Morales [email protected] HTC Program Administrator – (512) 475-1676

Teresa Shell [email protected] Program Exchange Administrator – (512) 936-7834

Lisa Fehr [email protected] Program Exchange Specialist – (512) 936-7833

Ben Sheppard [email protected] Housing Specialist, HTC Amendments – (512) 475-2122

Shannon Roth [email protected] Housing Specialist, Bond/ 4% – (512) 475-3929

Nicole Fisher [email protected] Housing Specialist, QCP – (512) 475-2201

Multifamily Contacts:

Kent Bedell [email protected] Housing Specialist, HTC Extensions, Bond/ 4% – (512) 475-3882

Elizabeth Henderson [email protected] Housing Specialist, HTC Ownership Transfer – (512) 475-9784

Valentin Deleon [email protected] Housing Specialist, Experience Certificates – (512) 475-3061

Liz Cline [email protected] Housing Specialist, IRS Reporting – (512) 475-3227

Jason Burr [email protected] Administrator- Application Technical Assistance – (512) 475-3986

Misael Arroyo [email protected] Executive Assistant – (512) 475-2596

Main Multifamily Telephone – (512) 475-3340Multifamily Facsimile – (512) 475-0764 or (512) 475-1895

Texas Department of Housing and Community Affairs

Real Estate Analysis Contacts:

Brent Stewart [email protected] of Real Estate Analysis, (512) 475-2973

Audrey Martin [email protected] of Real Estate Analysis, (512) 475-3872

Compliance and Asset Management Contacts:

Patricia Murphy [email protected] of Compliance and Asset Management, (512) 475-3140

Wendy Quackenbush [email protected] of Compliance, (512) 305-8860

Texas Department of Housing and Community Affairs

HOME and Tax Credit Assistance Program Contacts:

Cameron Dorsey [email protected] Program Manager – (512) 475-2669

Chris Law [email protected] Program Administrator – (512) 305-8854

Lisa Vecchietti [email protected] Credit Assistance Program Administrator – (512) 936-7791

Laura DeBellas [email protected] Credit Assistance Program Specialist – (512) 475-3821

Texas Department of Housing and Community Affairs

The FHA Advantage High Loan to Cost – Low DSC – Long Amortization

Experience Underwriting Affordable Housing – NonRecourse

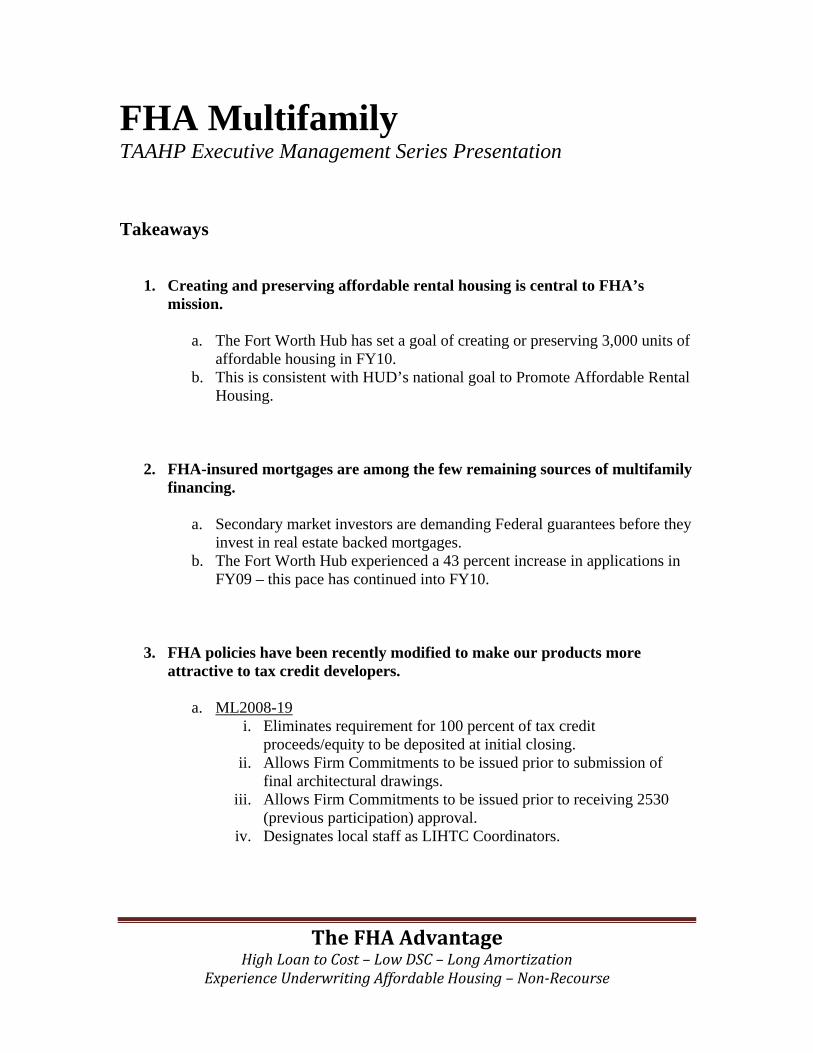

FHA Multifamily TAAHP Executive Management Series Presentation Takeaways

1. Creating and preserving affordable rental housing is central to FHA’s mission.

a. The Fort Worth Hub has set a goal of creating or preserving 3,000 units of affordable housing in FY10.

b. This is consistent with HUD’s national goal to Promote Affordable Rental Housing.

2. FHA-insured mortgages are among the few remaining sources of multifamily financing.

a. Secondary market investors are demanding Federal guarantees before they invest in real estate backed mortgages.

b. The Fort Worth Hub experienced a 43 percent increase in applications in FY09 – this pace has continued into FY10.

3. FHA policies have been recently modified to make our products more attractive to tax credit developers.

a. ML2008-19 i. Eliminates requirement for 100 percent of tax credit

proceeds/equity to be deposited at initial closing. ii. Allows Firm Commitments to be issued prior to submission of

final architectural drawings. iii. Allows Firm Commitments to be issued prior to receiving 2530

(previous participation) approval. iv. Designates local staff as LIHTC Coordinators.

The FHA Advantage High Loan to Cost – Low DSC – Long Amortization

Experience Underwriting Affordable Housing – NonRecourse

b. ML2009-24 i. Eliminates requirement for subsidy layering review.

ii. Eliminates requirement for HUD cost certification on projects with less than an 80 percent loan-to-proceeds ratio.

iii. Eliminates the requirement to escrow tax credit equity.

4. FHA and TDHCA are working together closer than ever.

a. Co-presenting at training events. b. Monthly conference calls during LITHC application/review cycle.

5. Engaging FHA earlier in the process is the key to receiving a timely commitment.

a. Historically developers have chosen to wait on submitting an application for FHA insurance until tax credit awards are announced (July/August).

b. This practice creates unnecessary timing conflicts. c. Engage an FHA-approved lender as early in the process as possible. d. We recommend that you consult with FHA staff formally (submission of a

pre-Application package) or informally (schedule a concept meeting) as soon as you decide to submit an Application to TDHCA (February/March).

Fort Worth Multifamily Hub

Ft. Worth (North Texas & New Mexico) Robert Waterhouse, LIHTC Coordinator (817) 978-5785 San Antonio (Central Texas, Rio Grande Valley, & Southern Gulf Coast) Tom Goade, LIHTC Coordinator (210) 475-6800 x2240 Houston (Greater Houston & North Gulf Coast) Crystal Rienth, LIHTC Coordinator (713) 718-3156 Little Rock (Arkansas) June Clark, LIHTC Coordinator (501) 918-5723 New Orleans (Louisiana) Ty Harris, LIHTC Coordinator (504) 671-3776

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT

WASHINGTON, DC 20410-8000

ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER

www.hud.gov espanol.hud.gov

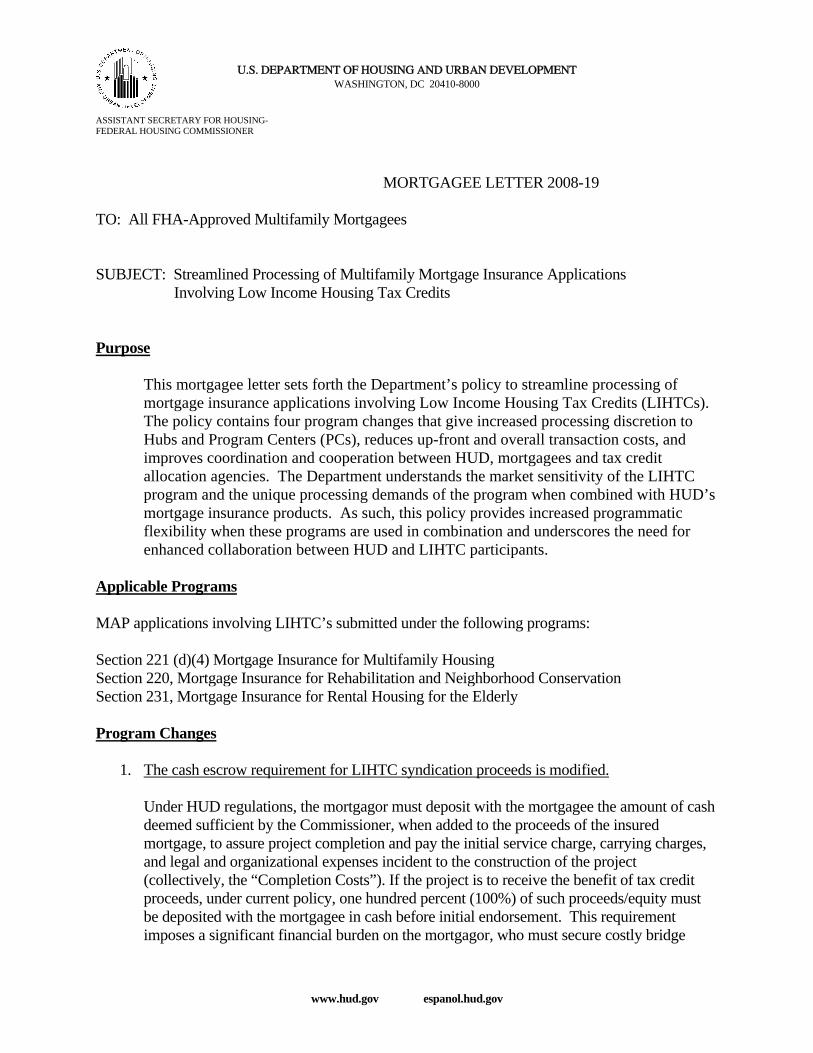

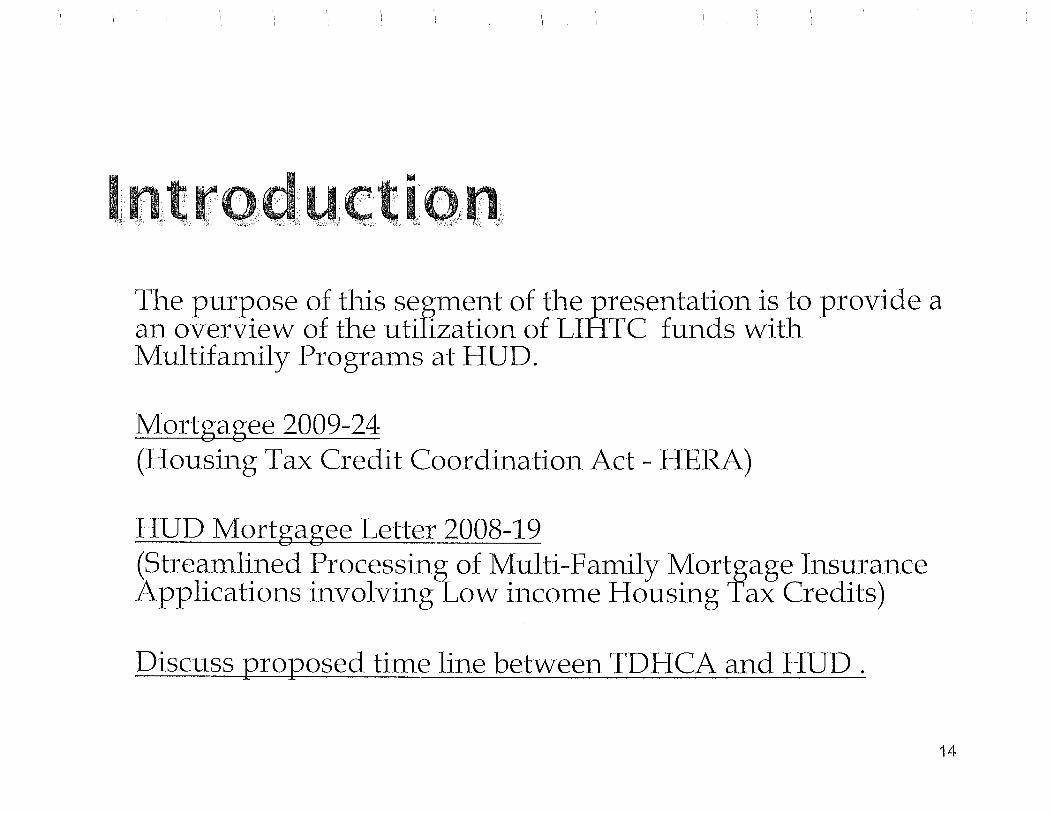

MORTGAGEE LETTER 2008-19

TO: All FHA-Approved Multifamily Mortgagees SUBJECT: Streamlined Processing of Multifamily Mortgage Insurance Applications

Involving Low Income Housing Tax Credits Purpose This mortgagee letter sets forth the Department’s policy to streamline processing of

mortgage insurance applications involving Low Income Housing Tax Credits (LIHTCs). The policy contains four program changes that give increased processing discretion to Hubs and Program Centers (PCs), reduces up-front and overall transaction costs, and improves coordination and cooperation between HUD, mortgagees and tax credit allocation agencies. The Department understands the market sensitivity of the LIHTC program and the unique processing demands of the program when combined with HUD’s mortgage insurance products. As such, this policy provides increased programmatic flexibility when these programs are used in combination and underscores the need for enhanced collaboration between HUD and LIHTC participants.

Applicable Programs MAP applications involving LIHTC’s submitted under the following programs:

Section 221 (d)(4) Mortgage Insurance for Multifamily Housing Section 220, Mortgage Insurance for Rehabilitation and Neighborhood Conservation Section 231, Mortgage Insurance for Rental Housing for the Elderly Program Changes

1. The cash escrow requirement for LIHTC syndication proceeds is modified.

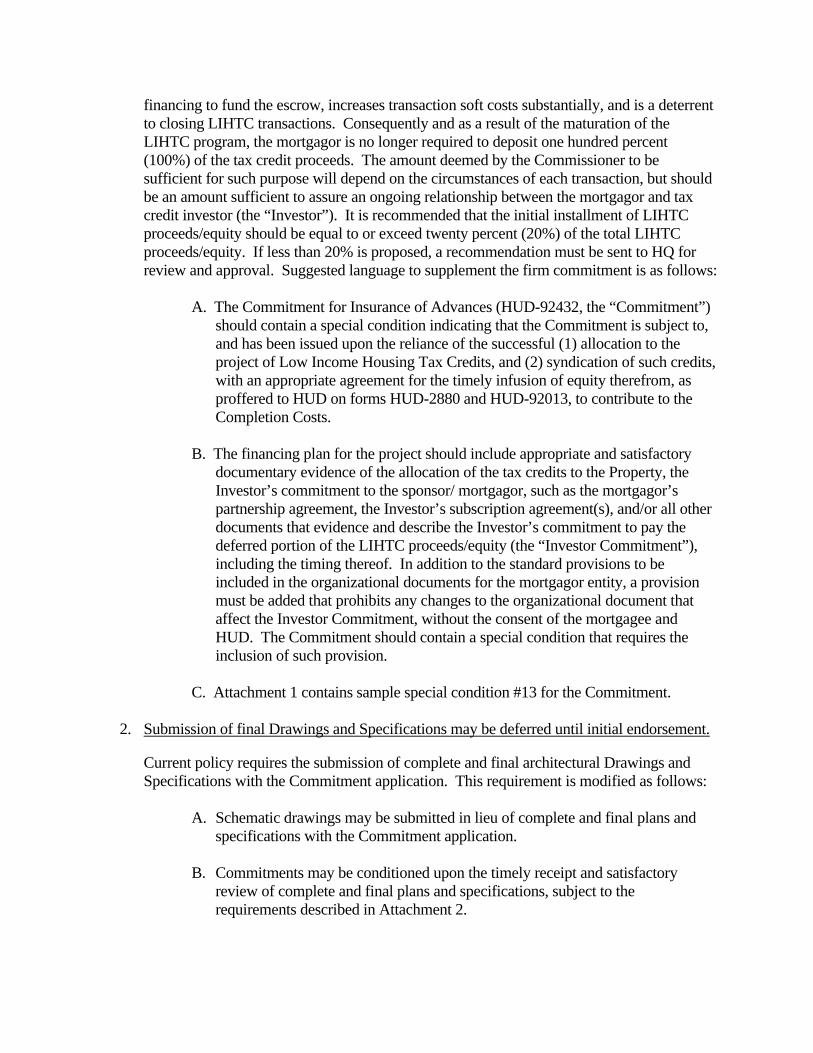

Under HUD regulations, the mortgagor must deposit with the mortgagee the amount of cash deemed sufficient by the Commissioner, when added to the proceeds of the insured mortgage, to assure project completion and pay the initial service charge, carrying charges, and legal and organizational expenses incident to the construction of the project (collectively, the “Completion Costs”). If the project is to receive the benefit of tax credit proceeds, under current policy, one hundred percent (100%) of such proceeds/equity must be deposited with the mortgagee in cash before initial endorsement. This requirement imposes a significant financial burden on the mortgagor, who must secure costly bridge

financing to fund the escrow, increases transaction soft costs substantially, and is a deterrent to closing LIHTC transactions. Consequently and as a result of the maturation of the LIHTC program, the mortgagor is no longer required to deposit one hundred percent (100%) of the tax credit proceeds. The amount deemed by the Commissioner to be sufficient for such purpose will depend on the circumstances of each transaction, but should be an amount sufficient to assure an ongoing relationship between the mortgagor and tax credit investor (the “Investor”). It is recommended that the initial installment of LIHTC proceeds/equity should be equal to or exceed twenty percent (20%) of the total LIHTC proceeds/equity. If less than 20% is proposed, a recommendation must be sent to HQ for review and approval. Suggested language to supplement the firm commitment is as follows:

A. The Commitment for Insurance of Advances (HUD-92432, the “Commitment”) should contain a special condition indicating that the Commitment is subject to, and has been issued upon the reliance of the successful (1) allocation to the project of Low Income Housing Tax Credits, and (2) syndication of such credits, with an appropriate agreement for the timely infusion of equity therefrom, as proffered to HUD on forms HUD-2880 and HUD-92013, to contribute to the Completion Costs.

B. The financing plan for the project should include appropriate and satisfactory

documentary evidence of the allocation of the tax credits to the Property, the Investor’s commitment to the sponsor/ mortgagor, such as the mortgagor’s partnership agreement, the Investor’s subscription agreement(s), and/or all other documents that evidence and describe the Investor’s commitment to pay the deferred portion of the LIHTC proceeds/equity (the “Investor Commitment”), including the timing thereof. In addition to the standard provisions to be included in the organizational documents for the mortgagor entity, a provision must be added that prohibits any changes to the organizational document that affect the Investor Commitment, without the consent of the mortgagee and HUD. The Commitment should contain a special condition that requires the inclusion of such provision.

C. Attachment 1 contains sample special condition #13 for the Commitment.

2. Submission of final Drawings and Specifications may be deferred until initial endorsement.

Current policy requires the submission of complete and final architectural Drawings and Specifications with the Commitment application. This requirement is modified as follows:

A. Schematic drawings may be submitted in lieu of complete and final plans and specifications with the Commitment application.

B. Commitments may be conditioned upon the timely receipt and satisfactory

review of complete and final plans and specifications, subject to the requirements described in Attachment 2.

C. Mortgagees, Hubs and PCs must review the level of experience of all proposed development team members and must determine that only those with adequate knowledge of HUD’s development, design and building requirements are approved for deferred plan submission. Hubs and PCs should also consider the complexity of the proposed design and construction when determining whether to permit deferred plan submission.

D. Hubs and PCs should determine that the project will achieve initial closing

within 60 days after issuance of a Commitment conditioned upon final plan submission. In addition, full and final plans must be submitted 30 days prior to the scheduled initial endorsement to provide adequate time for HUD review and approval.

E. Attachment 1 contains sample special condition #14 to be added to the

Commitment when the submission of deferred plans is approved.

3. Commitments may be conditioned upon HUD-2530 approval.

For LIHTC transactions, the existing policy requiring HUD-2530 clearance to be obtained prior to the issuance of the Commitment is modified as follows:

A. Two categories of HUD-2530s may qualify and permit the issuance of a Commitment that is subject to the final resolution of the HUD-2530 clearance:

1) HUD-2530s without critical findings that the field has the authority to resolve pursuant to Attachment #3 (Office of Multifamily Housing Programs January 17, 2007 memorandum entitled Critical Findings – Modification To Previous Participation Review and Approval Process); and

2) HUD-2530s containing flags that must be resolved by HQ, but that are not required to be presented to the Multifamily Participation Review Committee (MPRC). Hubs/PCs proposing to issue a Commitment with this category of 2530 must receive confirmation from the Policy and Participation Standards Division (PPSD) that a complete recommendation has been received and that a referral to the MPRC will not be made. For this category of HUD-2530, the following conditions apply:

a. Complete HUD-2530s for all project principals must be filed with the firm

commitment application. b. All HUD-2530s requiring PPSD review must be referred to the PPSD within

3 business days of receipt of the firm commitment application from the participant. The referral package must be complete. Please refer to Attachment #4, Office of Multifamily Housing Programs June 21, 2007 Memorandum regarding review of HUD-2530, and HUD Handbook 4065.1 for referral package instructions.

c. If filed by paper, fax one copy of the HUD-2530 to PPSD, labeled “LIHTC-2530”; send original by express mail to PPSD. If filed electronically, send an email with subject line “LIHTC-2530” to Audrey Hinton and William Hill. The email must indicate which E2530 submission numbers require review.

d. PPSD will place all complete submissions on a 15 business day target

completion review track. Incomplete referral packages will be returned to the field for correction within 5 business days.

e. PPSD will notify the Hub/PC when the HUD-2530 is cleared or that a

referral will not be made to the MPRC and that the firm commitment may be conditioned.

B. Notwithstanding the issuance of the Commitment, HUD-2530 approval must be obtained prior to and as a condition of initial endorsement.

C. Commitments may only be conditionally issued when the Commitment processing is

otherwise completed and all project principals are determined to be acceptable (i.e., mortgagor entity is sufficiently capitalized, has satisfactory experience, capacity and demonstrated track record of performance; the general contractor passes the working capital analysis and has adequately performed on other comparable projects, etc.).

D. Hubs/PCs must assign firm commitment applications a project number upon receipt

of the application from the mortgagee. Project number assignment at this stage will permit the HUD-2530 review process to commence concurrently with receipt of the firm commitment application.

E. Attachment 1 contains sample special condition #15 to be added to the Commitment

for either category of HUD-2530 listed in paragraph 3.A for which clearance is pending.

4. Each Hub and PC must designate a LIHTC Coordinator.

Currently, there are variations of knowledge and experience throughout Hubs and PCs with respect to the LIHTC program and HUD processing requirements when LIHTCs are combined with HUD’s mortgage insurance products. The designation of a LIHTC Coordinator in each Hub and PC will accomplish three objectives: enhance staff understanding of the LIHTC program, increase processing consistency among offices, and improve marketing and outreach of HUD’s mortgage insurance programs. A staff member from Headquarters’ Office of Multifamily Development will be designated to coordinate this effort. It is contemplated that the Coordinators will convene via teleconference on an on-going basis to cross-train, exchange information, and strategize regarding how HUD’s insured programs may be further refined when combined with LIHTCs to meet participants’ needs. The Coordinator will also work with the local housing credit allocation agency to synchronize tax credit funding cycles and the FHA application process to better meet client needs.

Sincerely, Brian D. Montgomery Assistant Secretary for Housing – Federal Housing Commissioner

Attachments:

1. Commitment Special Conditions 2. Requirements applicable to the submission of deferred Drawings and Specifications 3. January 17, 2007 Office of Multifamily Housing Programs Memorandum 4. June 21, 2007 Office of Multifamily Housing Programs Memorandum

Attachment 1 [Note: The Commitment should be annotated to reflect the attachment of an additional numbered paragraph(s).] 13. This commitment is subject to, and has been issued upon the reliance of, the successful (a)

allocation to the project of Low Income Housing Tax Credits, and (b) syndication of such credits, with an appropriate agreement for the timely infusion of equity therefrom, as proffered to HUD on forms HUD-2880 and HUD-92013, to assure completion of the project and pay other associated and incidental costs. In addition to the standard provisions that must be included in the organizational documents for the mortgagor entity, a provision must be added that prohibits any changes to the organizational documents that affect the obligations of the tax credit investor without the written consent of the Mortgagee and HUD.

14. As an accommodation, this commitment has been issued and based upon schematic drawings,

instead of the final Drawings and Specifications. At least 30 days prior to the scheduled date for initial endorsement, the Commissioner must receive the final Drawings and Specifications for review and approval to ensure consistency of design and cost. In the event that there is a net cumulative construction cost increase or change in the design concept, or a net cumulative construction cost decrease in the amount of more than two percent (2%), this commitment shall be subject to and conditioned upon the further approval of the Commissioner, to be evidenced in writing, and may be terminated and voided by the Commissioner, or additional conditions may be imposed, at the Commissioner’s option.

15. Notwithstanding the issuance of this commitment, this commitment remains subject to, and the

Commissioner’s obligations hereunder are conditioned upon the satisfactory resolution, as determined by the Commissioner, of the adverse items determined by HUD during the HUD-2530 review process.

Attachment 2 Processing Instructions for Deferred Submission of Final Drawings and Specifications MAP lenders and Hub/PCs must review the level of experience of all development team members and must determine that only those with adequate knowledge of HUD’s development, design and building requirements are accepted for this streamline process. Hubs and PCs should also consider the complexity of the proposed design and construction when determining whether to permit the deferred submission of final Drawings and Specifications. Hubs and PCs should determine that the project will achieve initial closing within 60 days after issuance of a firm commitment conditioned upon final plan submission. The Phase I (ASTM Practice E 1527-06 or most current) environmental report must contain no significant unresolved environmental issues that would justify a Form HUD 4128 “Environmental Assessment & Compliance Findings for the Related Laws” rejection finding. Impact on MAP A& E and Cost Application Requirements & Exhibits: The mortgagee’s submission of less than 100% of the Drawings and Specifications (i.e., schematic/line/working drawings) must provide the following detail:

1. The static footprint of the building as it rests on the surveyed site plan. 2. The gross building and net residential footage. 3. Unit layouts for each major unit type. 4. Sufficient design detail to make a Davis-Bacon Wage rate classification

determination. 5. Sufficient design detail to determine compliance with accessibility

requirements found at Appendix 5 of the MAP Guide. The mortgagee’s submission must also contain the following exhibits:

1. A written cost estimate (HUD-2328) from the general contractor proposed to participate in the project.

2. For Pre-applications: Exhibit #8 of Appendix 4A of the MAP Guide 3. For Firm Commitment applications: Exhibits A.16, 17, 24, 25, 27, and B.3

of Appendix 4A of the MAP Guide as applicable. Scope of HUD Review and determinations required in order to issue a Commitment:

an assessment that the estimated project cost based on form HUD 2328 is reasonable and in line with comparable HUD LIHTC project data;

an assessment that the proposed general contractor is acceptable pursuant to outstanding requirements (sufficient working capital, experience, etc.)

an assessment that the sketch plans are in compliance with all applicable requirements on a preliminary basis, with appropriately qualified

certifications executed; an assessment, based on a site visit by the appraiser, that the requested land

or “as is” rehabilitation value, rent and expense estimates are reasonable and supported by the appraisal, and that the form HUD-4128 may be approved.

Modification of Commitment to reflect deferred Drawings and Specification condition.

For those projects determined to be eligible for deferred plan submission, the following changes/additions language should be added to the Commitment:

As an accommodation, this commitment has been issued based upon schematic drawings, instead of the final Drawings and Specifications. Within 30 days after the acceptance by Mortgagee of this commitment, the Commissioner must receive the final Drawings and Specifications for review and approval to ensure consistency of design and cost. In the event that there is a net cumulative construction cost increase or change in the design concept, or a net cumulative construction cost decrease in the amount of more than two percent (2%), this commitment shall be subject to and conditioned upon the further approval of the Commissioner, to be evidenced in writing, and may be terminated and voided by the Commissioner, or additional conditions may be imposed, at the Commissioner’s discretion.

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT

WASHINGTON, DC 20410-8000

ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER

www.hud.gov espanol.hud.gov

July 29, 2009

MORTGAGEE LETTER 2009-24 TO: ALL FHA-APPROVED MULTIFAMILY MORTGAGEES SUBJECT: Housing Tax Credit Coordination Act of 2008 On July 30, 2008, the Housing and Economic Development Recovery Act of 2008 (HERA) became Public Law 110-289. Title VIII of HERA, in subtitle B, cited as the “Housing Tax Credit Coordination Act of 2008,” made changes to the multifamily programs of the Federal Housing Administration (FHA) to facilitate the use of such programs with Low-Income Housing Tax Credits. In anticipation of HERA, and to further the Department’s goal of encouraging the use of FHA multifamily programs with these tax credits, the Department issued Mortgagee Letter 2008-19 titled Streamlined Processing of Multifamily Mortgage Insurance Applications Involving Low-Income Housing Tax Credits, and released initial policy and procedures on the use of Master Leases that permit a combination of investment by one or more investors under one or more tax credit programs. Now, under the authority of HERA, we are able to further promote the use of FHA programs with Low-Income Housing Tax Credits. This Mortgagee Letter describes the additional authority granted under HERA and the Department’s implementation of Sections 2832 and 2834 of the Act.

Section 2832 of HERA requires the Secretary to implement administrative and procedural changes to expedite the approval of multifamily housing projects utilizing FHA mortgage insurance programs with either Low-Income Housing Tax Credits or tax-exempt housing bonds. The Department has already taken certain steps to achieve expedited approval of such projects. First, all of the provisions of Mortgagee Letter 2008-19 that streamline FHA multifamily mortgage insurance processing remain in effect. Second, we are in the process of obtaining Departmental clearance of a final Master Lease policy to facilitate the use of tax credits. In addition, HERA requires the Secretary to consult with the Commissioner of the Internal Revenue Service, the product of which may result in additional administrative and procedural changes to expedite the approval of FHA mortgage insurance programs with Low-Income Housing Tax Credits or tax-exempt housing bonds. Finally, the Department published a Federal Register Notice soliciting recommendations from the public regarding further administrative and procedural changes that may be implemented to facilitate the approval of FHA mortgage insurance with Low-Income Housing Tax Credits or tax-exempt housing bonds.

2

Section 2834 of HERA provides three substantive changes to the Department’s processing of certain FHA mortgage insurance applications. The first change eliminates mortgage insurance provided pursuant to Title II of the National Housing Act (12 U.S.C. 1707, et. seq.) as a basis to require the statutorily prescribed certification from the Secretary that existing subsidy layering requirements have been satisfied. This Mortgagee Letter supersedes all previously issued subsidy layering guidance by either a Mortgagee Letter, HUD Notice, HUD Handbook, etc. with respect to mortgage insurance under Title II of the National Housing Act. The second substantive change affects the mortgagor’s obligation under section 227 of the National Housing Act (12 U.S.C. 1715r) to certify “actual cost” upon completion of project construction, rehabilitation or repair for mortgage insurance transactions involving low-income housing tax credits. If the Secretary determines at the time of Firm Commitment issuance that the ratio of loan proceeds to the actual cost of such projects is less than 80 percent, the mortgagor will not be required to certify actual costs to HUD. For example, in cost programs such as 221(d)(4) and 220, when the “Maximum Insurable Mortgage” derived utilizing Form HUD 92264-A is less than 80 percent of the Total Estimated Replacement Cost of Project derived under section G. of Form HUD-92264, the mortgagor will not be required to certify actual cost to HUD. Attachment 1 provides an example of this computation. In cases that are exempt from cost certification, a Cost Certification Audit Fee, line 66, Section G., Form HUD-92264 is not applicable. The exemption from cost certification requirements provided by HERA applies to applications for mortgage insurance involving Low-Income Housing Tax Credits under the following programs: Sections 213, 220, 221(d)(3), 221(d)(4), and 231.

For projects that are exempt from providing a cost certification, when the project reaches 100% substantial completion as deemed by the HUD Inspector, the Mortgagee will be notified of the substantial completion date.

The Mortgagor must account for all operating income during construction and

ending three months prior to the originally scheduled date of the first principal payment under the mortgage. Therefore an income and expense statement must be submitted covering the period from first occupancy (if occupancy occurred during construction) or from the date of substantial completion (as deemed by the HUD Inspector) up through the period ending three months prior to the date of the first principal payment under the mortgage as originally scheduled. The statement must be submitted to HUD, at least 30 days prior to the date scheduled for Final Endorsement,

If the income and expenses statement evidence receipt of income (Excess Funds) during this period, the mortgagor will be required to deposit the Excess Funds into the reserve fund for replacements established under the Regulatory Agreement, unless the HFA has notified HUD that the funds must be used in another manner to be

3

in compliance with IRC Section 42, low-income housing tax credit requirements.

If during construction the project experiences significant cost overruns that result in the mortgagor requesting a mortgage increase, the mortgagor will be required to justify and support such request with documentation satisfactory to HUD that provides a suitable basis for a mortgage increase. Finally, the last substantive change under section 2834 involves the requirement under 24 CFR 200.54 that the mortgagor deposit with the mortgagee the amount of “cash deemed by the Commissioner to be sufficient, when added to the proceeds of the insured mortgage, to assure project completion and pay the initial service charge, carrying charges, and legal and organizational expenses incident to the construction of the project.” HERA provides that if the project is to receive the benefit of equity from Low-Income Housing Tax Credits, the Department may not require the escrowing of any of such equity, or accept any form of security in place thereof, such as a letter of credit. The Department is in the process of making a conforming rule change to 24 CFR 200.54 to implement this provision of HERA. While low-income housing tax credit equity will not be escrowed, an appropriate amount of tax credit equity must be invested at the time of initial endorsement to provide a reasonable degree of assurance that the relationship between the mortgagor and the tax credit investor will be maintained. We believe that an expenditure of 20% of the total low-income housing tax credit equity at the time of initial endorsement is sufficient to ensure the investor’s continued commitment. If less than 20% is proposed, the Lender must address in the Underwriting Summary Report how the lesser amount is appropriate as an initial investment of the tax credit equity. An annotated example of information derived from Form HUD-92264-A to assist with the calculation of the amount of the initial and subsequent infusions of tax credit equity is attached hereto as Attachment 2.

If you have any questions concerning this Mortgagee Letter, please contact Joseph Sealey, Director of the Technical Support Division, Office of Multifamily Housing Development at (202) 402-2559.

________________________________ David H. Stevens, Assistant Secretary for Housing –Federal Housing Commissioner

4

ATTACHMENT 1 The following examples illustrate the applicability of cost certification under HERA legislation. Criteria 11 is used in the examples since it will often control as the Maximum Insurable Mortgage under LIHTC applications. Section 221(d)(4) Form HUD 92264-A Criteria 11. 11. Amount Based on Deduction of Grants, Loans, Tax Credits and Gifts for Mortgageable Items:

Total Project Replacement Cost (from Section G. Form HUD 92264) $ 13,000,000 LIHTCs for Mortgageable Items …………………………………… 5,000,000 Maximum Insurable Mortgage Amount…………………………….. $ 8,000,000 $ 8,000,000 / $13,000,000 = 62%. In this example a cost certification is not required under HERA for a LIHTC application. The ratio of loan proceeds to the firm commitment estimated project replacement cost is less than 80%.

ATTACHMENT 2

5

Equity Contribution Clarification

Pursuant to the Housing and Economic Recovery Act of 2008, HUD may no longer require that a mortgagor place in escrow low income housing tax credit proceeds/equity (LIHTC Equity). HUD will require, however, that an appropriate amount of the LIHTC Equity be invested in the project and applied to HUD approved items at the time of Initial Endorsement. The amount deemed by the Commissioner to be sufficient for such purposes will depend on the circumstances of each transaction, but should be an amount that assures an ongoing relationship between the mortgagor and the tax credit investor (Investor). It is recommended that the initial installment of LIHTC Equity be an amount that is equal to or exceeds twenty percent (20%) of the total LIHTC Equity that will be available for the project. If less than 20% is proposed, a recommendation must be sent to HQ for review and approval. Clarification of such requirement is provided in the example below: There is no change in the computation to determine the cash requirements and/or front money escrow on HUD Form 92264-A. However, the calculation of the initial installment of LIHTC equity is calculated as follows:

Example of LIHTC equity contribution calculation adapted from Form HUD-92264A, Section II Total Requirements for Settlement – Part B.

1. a. Development Cost ………………… $14,381,216 1. b-c Total of lines a & b ………………… $14,381,216 2. Land Indebtedness $ 625,000 3. Subtotal (lines 1c + 2) …………………… $15,006,216 4. a. Mortgage Amount …………………… $10,935,000 4. b. Home funds ……………………… $ 650,000 5. Fees not to be paid in cash … …………………$ 0 6. Subtotal (lines 4a+4b+5) ……………. $11,585,000 7. Cash investment require $ 3,421,216 8. Initial Operating Deficit …………………. $ 488,772 9. Other Cost (Bond cost $312,617) and $15,000 ……….… … $ 327,617 10. Working Capital …………………………………………….… $ 218,700 11. Other: Social Services Escrow $55,000 + Fee $2,066,897) … $ 2,121,897 12. Total estimated cash requirement (sum of lines 7+8+9+10+11) $ 6,578,202 Front money escrow, if any (subtract line 6 from line 1) … $ 2,796,216

Section III Source of Funds to Meet Cash Requirements Source: A Tax Credit Equity ………… $5,027,301 B Developer funds …… $1,550,901 Total available cash for project $6,578,202 The initial 20% calculation of the tax credit equity (should be the same as the tax credit equity amount reflected in Criterion 11) for mortgeagable items is $1,005,460. This

6

is based on the mortgageable tax credit allocation of $5,027,301 x 20% = $1,005,460, it is not based on the total cash requirements for the project. The remaining cash requirements not being satisfied with Low Income Housing Tax Credits will/must be satisfied in accordance with outstanding instructions.

As discussed in Mortgagee Letter 2008-19, titled “Streamlined Processing of Multifamily Mortgage Insurance Applications Involving Low Income Housing Tax Credits,” the Commitment for Insurance of Advances, form HUD-92432 (Commitment), should contain, among other special conditions, a requirement for the delivery of evidence satisfactory to HUD of an agreement that binds the Investor to timely and periodically pay to the mortgagor LIHTC Equity to contribute to the completion costs, in the aggregate amounts proffered to HUD on forms HUD-2880 and HUD-92013.

For instance, a contribution schedule that could be acceptable to HUD might

require the 2nd installment of LIHTC Equity to be contributed at 50% construction completion, the 3rd installment at 75% construction completion, with the final infusion of LIHTC Equity required to complete construction and pay third party soft costs, exclusive of developer’s fee, by 90% construction completion. HUD is aware that there may be LIHTC Equity pay-ins related to required reserve capitalization and/or developer’s fee scheduled subsequent to construction completion and the achievement of certain Investor tax-related benchmarks established per the partnership or operating agreement controlling the mortgagor entity.

After the first installment of LIHTC Equity is disbursed at Initial Endorsement, the subsequent contributions should be made at a time and in a manner during construction to ensure that the statutory limitations based on actual costs for the applicable FHA mortgage program are maintained during construction. To maintain the appropriate balance of LIHTC Equity and mortgage loan proceeds, at each infusion of LIHTC Equity, those funds may need to be utilized before the next disbursement of mortgage loan proceeds.

Financing Affordable Rental Properties

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

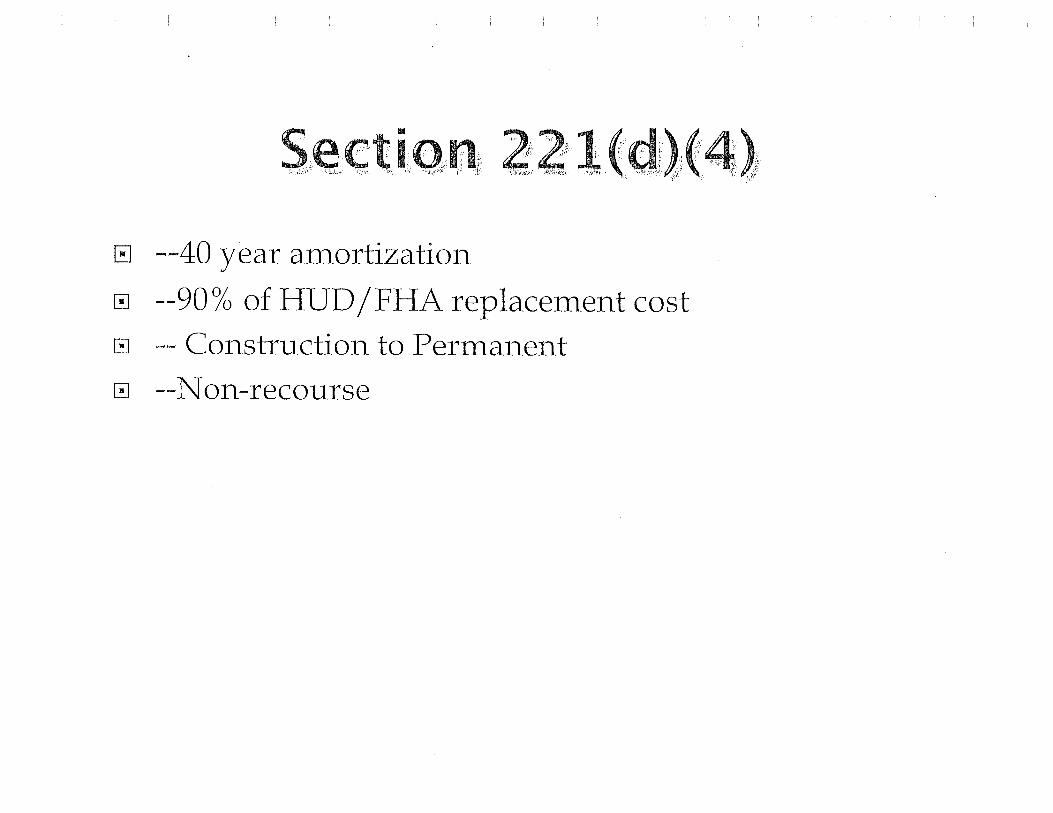

• HUD 221(d)4 Program RequirementsHUD 221(d)4 Program Requirements– Amortization up to 40 years

• Interest only during constructionInterest only during construction

• Draw down loan

• Fully amortizing, no balloon paymentsy g, p y

– 1.11x Debt Service Coverage Ratio

– Permanent Loan is Rate Locked at Closinge a e oa s a e oc ed a os g

– No NOI/Stabilization Requirement for Permanent Loan Conversion

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• HUD 221(d)4 Program RequirementsHUD 221(d)4 Program Requirements – Davis Bacon Wage Rules

General Contractor must supply one of the– General Contractor must supply one of the following: 1)Payment and Performance Bond or,2) Letter of Credit equal to 15% of the contractLetter of Credit equal to 15% of the contract

– Annual Audit is required

– Cash Distributions limited to Surplus CashCash Distributions limited to Surplus Cash

– Payment of Social Services

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• The 221(d)4 Loan ProcessThe 221(d)4 Loan Process– Feasibility Package

• Market Study & NOI Analysis• Phase One ESA (avoid 100 year Flood Plains, Wetlands, Railroad tracks, Airports, Electrical Transmission Lines, Natural Gas Lines and Storage Tanks)Natural Gas Lines and Storage Tanks)

• Site , Floor and Interior Wall Section Plans, Elevations • Show Site Control, Development Team Resumes• Non‐profit owners

– Contract for Housing Consultant Services– Preliminary Determination as a Non‐profit Sponsor– Development Agreement

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• HUD Processing – 45 DaysHUD Processing 45 Days– Rejection or Invitation Letter is Issued

– Invitation Letter allows for 120 days (with three 30‐Invitation Letter allows for 120 days (with three 30day extensions) to file for the Firm Application

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• Firm Application Processingpp g– Who is a Principal

• Any GP, LPs with more than a 25% interest, Stockholders or members of a corporation or LLC with more than 10% ownership, p p,Officers of the Board of a non‐profit sponsor, General Contractor, Managing Agent

– What Principals must provide• Previous Participation Certification (2530), Financial Statements, Credit Report, Supplement listing credit references (92013), Listing of Other Business Concerns

Architectural and Engineering Drawings– Architectural and Engineering Drawings• Plans and Construction Contract to be reviewed by lender/HUD• HERA allows Firm Application filing subject to Plan and Cost ReviewReview

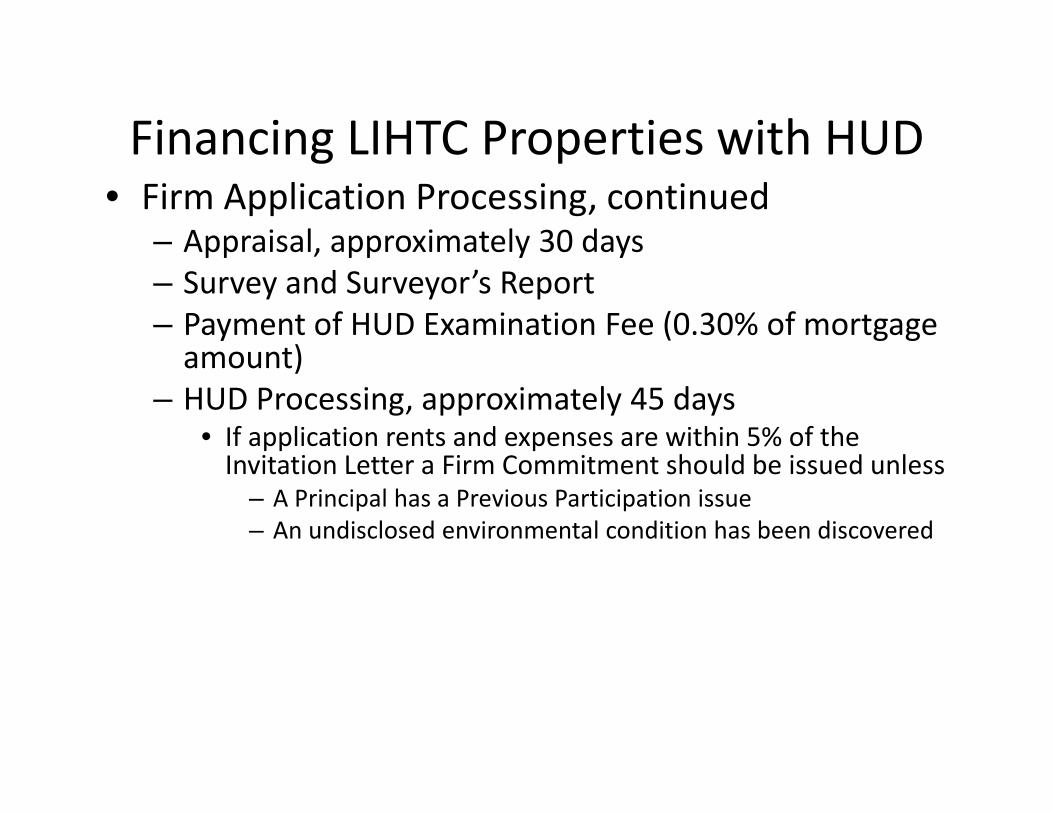

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD• Firm Application Processing, continued

– Appraisal, approximately 30 dayspp , pp y y– Survey and Surveyor’s Report– Payment of HUD Examination Fee (0.30% of mortgage amount)amount)

– HUD Processing, approximately 45 days• If application rents and expenses are within 5% of the I it ti L tt Fi C it t h ld b i d lInvitation Letter a Firm Commitment should be issued unless

– A Principal has a Previous Participation issue– An undisclosed environmental condition has been discovered

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• Issuance of HUD Commitment– Determination of Construction and Permanent Interest Rates

• Requires a Good Faith Deposit of 0 50%Requires a Good Faith Deposit of 0.50%• Lock out and prepayment provisions may vary according to market conditions

– May Require Lender to Reprocess Commitment atMay Require Lender to Reprocess Commitment at Locked Interest Rate (one week)

– Submit Closing Package to HUD LegalCl i f k f l ki i– Closing two to four weeks after locking interest rate

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• Closingg– Held at the local HUD Office– Owner, General Contractor and Architect all sign plans and specs AND attend a pre construction conferenceand specs AND attend a pre‐construction conference

– HERA processing requires on 20% of LIHTC equity at closing

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

• Construction Phase– Monthly inspection attended by HUD inspector, GC and ArchitectDraw requests include construction interest– Draw requests include construction interest

– Change Orders require payment with the request– Construction Cut Off Date

• 100% completion• No additional funds other than 60 days of construction interest

– Cost Certification– Subsidy Layering

Financing LIHTC Properties with HUDFinancing LIHTC Properties with HUD

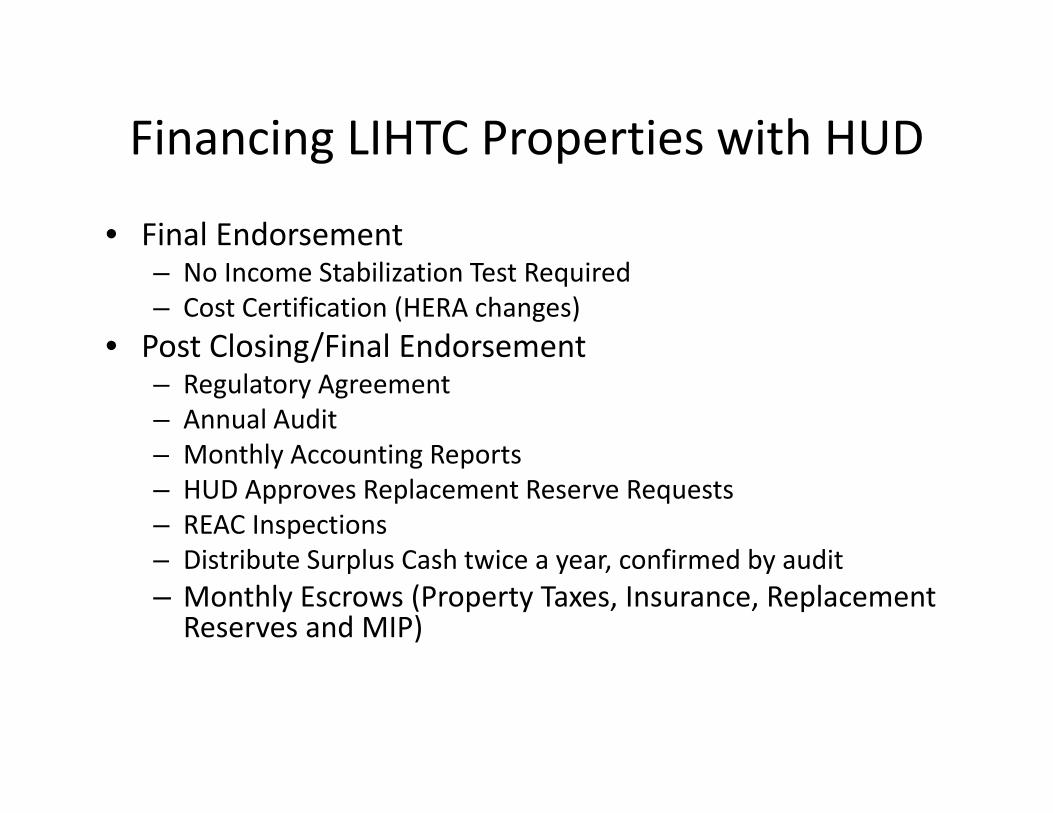

• Final Endorsement– No Income Stabilization Test Required– Cost Certification (HERA changes)

• Post Closing/Final EndorsementPost Closing/Final Endorsement– Regulatory Agreement– Annual Audit– Monthly Accounting ReportsMonthly Accounting Reports– HUD Approves Replacement Reserve Requests– REAC Inspections– Distribute Surplus Cash twice a year confirmed by audit– Distribute Surplus Cash twice a year, confirmed by audit– Monthly Escrows (Property Taxes, Insurance, Replacement Reserves and MIP)

HUD/TAX CREDIT TRANSACTIONS

• HUD closing documents are NON-NEGOTIABLE – be sure all parties

(including your lender and investor) are aware of this.

• Strict compliance with HUD requirements and requests essential – don’t risk

losing the deal!

• Legal Opinion – HUD requirements much more involved than regular tax

credit opinion.

• Important to submit review package early to HUD (avoid future delay).

• Obtain third-party documents (e.g., architect) ASAP for submission to HUD

- timing is key!

• Subordinate Debt – Maturity Date

• HUD requires specific language in LURA (see MAP Guide). Current issue

with TDHCA.

• Closing table – HUD has specific procedures (e.g., title

commitment/recording prior to closing).

• Closing Attorney and Title Agent – knowledge of HUD closing procedures

essential for a smooth and successful closing. For example:

‐ 8 originals of each on every document on closing checklist required at the closing table

‐ All documents must be pre-approved by HUD (including title policy) – no surprises!

‐ Everything should be completed, finalized and executed in advance of

HUD closing ‐ The day of closing – be organized and have everything in packages ready

for submission as per HUD’s request

• HUD disbursement requirements - 20% funding at closing from syndicator.

• HUD Mixed Finance Issues

‐ Leases for Fee Estate – HUD requirements concerning landlord/tenant rights.

‐ Equity and Loan Documents – When PHA involved, need to negotiate Developer’s right to notice and cure of PHA default.

‐ Rights of Syndicator – Syndicator needs to be aware of HUD’s restrictions on syndicator’s rights under LPA (i.e. removal of general partner).

‐ Reserves – HUD may require certain reserves be maintained for the project. Need to contemplate in budget.