Daily Agri Tech Report

9

Commodities Daily Report Agricultural Commodities Wednesday| January 16, 2013 www.angelcommodities.com Content News & Market Highlights Chana Sugar Oilseed Complex Spices Complex Kapas/Cotton Angel Commodities Broking Pvt. Ltd. Registered Office: G-1, Ackruti Trade Centre, Rd. No. 7, MIDC, Andheri (E), Mumbai - 400 093. Corporate Office: 6th Floor , Ackruti Star, MIDC, Andheri (E), Mumbai - 400 093. Tel: (022) 2921 2000 MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302 Disclaimer: The information and opinions contained in the document have been compiled from sources believed to be reliable. The company does not warrant its accuracy, completeness and correctness. The document is not, and should not be construed as an offer to sell or solicitation to buy any commodities. This document may not be reproduced, distributed or published, in whole or in part, by any recipient hereof for any purpose without prior permission from “Angel Commodities Broking (P) Ltd”. Your feedback is appreciated on [email protected] Research Team Vedika Narvekar - Sr. Research Analyst Anuj Choudhary - Research Analyst [email protected] [email protected] (022) 2921 2000 Extn. 6130 (022) 2921 2000 Extn. 6132

-

Upload

angel-broking -

Category

Documents

-

view

220 -

download

0

Transcript of Daily Agri Tech Report

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 1/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Content

News & Market Highlights

Chana

Sugar

Oilseed Complex

Spices Complex

Kapas/Cotton

Angel Commodities Broking Pvt. Ltd.

Registered Office: G-1, Ackruti Trade Centre, Rd. No. 7, MIDC, Andheri (E), Mumbai - 400 093.

Corporate Office: 6th Floor, Ackruti Star, MIDC, Andheri (E), Mumbai - 400 093. Tel: (022) 2921 2000

MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

Disclaimer: The information and opinions contained in the document have been compiled from sources believed to be reliable. The company does not warrant its accuracy, completeness andcorrectness. The document is not, and should not be construed as an offer to sell or solicitation to buy any commodities. This document may not be reproduced, distributed or published, in whole or inpart, by any recipient hereof for any purpose without prior permission from “Angel Commodities Broking (P) Ltd”. Your feedback is appreciated on [email protected]

Research TeamVedika Narvekar - Sr. Research Analyst Anuj Choudhary - Research [email protected] [email protected]

(022) 2921 2000 Extn. 6130 (022) 2921 2000 Extn. 6132

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 2/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights (% change) as on Jan 15, 2013

Last Prev. day WoW MoM Yo

Sensex 19987 0.40 1.24 3.86 23.Nifty 6057 0.54 0.91 3.39 24.

INR/$ 54.61 0.15 -0.65 -0.46 6.Nymex Crude Oil - $/bbl 93.28 -0.91 0.14 6.97 #NComex Gold - $/oz 1683 0.87 1.32 -0.80 #N

.Source: Reute

Fresh purchases heat up groundnut oilGroundnut oil and cotton oil moved up on Tuesday following freshbuying by repackers and manufacturers of branded oils. However, theretail demand was below normal. According to market sources, prices of both edible oils may gain in the coming days as supply is weak due toshortage of raw material for crushing. A Rajkot miller said that arrivals of groundnut have been poor so far this year and groundnut production isestimated lower. “Trading is at a low key as traders and shellin g units aprotesting against new export rules,” he said. (Source: Business Line)

U.S. Loses Korea Corn Sales to Brazil on Drought-Driven RallyShipments of American corn tumbled to a seven-year low of 2.84 millionmetric tons last year, from 6.02 million tons in 2011, according to data onthe Korea Customs Service’s website today. Imports from Brazil jumpedto 1.96 million tons from 122,704 tons, while purchases from Argentinarose to 1.08 million tons from 1,957 tons, the data show. “Korean buyerslast year shunned U.S. supplies because of the price surge triggered bythe drought, and, coincidently, Latin America had a bumper crop,” LeeTae Woong, a deputy general manager at Nonghyup Feed Inc., thenation’s biggest feed -grain buyer said. ( Source: Bloomberg)

Nodal agency to clear Basmati exports to MauritiusPost Mauritius' concerns on adulterated Basmati eing exported by India,the commerce ministry has nominated the Export Inspection Council as

the nodal agency, which will issue a Certificate of Authenticity for allBasmati rice exports to Mauritius. The EIC is also in the process of drafting an MoU in this regard, which will be signed by the EIC andMauritius government. New Delhi, in fact, is quite keen “to extend anyassistance with regard to meeting requirements of Mauritius for rice asBasmati rice is a unique geographical indication product under the WTO”.The development comes a day after foreign investors, especially thosefrom Mauritius, got a breather from the finance ministry that deferredthe General Anti-Avoidance Rules by two years. ( Source: Financial Express)

USDA launches micro loan program for small farmersThe U.S. Department of Agriculture announced a new program onTuesday to help small farming operations, including those run byminority or socially disadvantaged farmers, improve their access tocredit. The program, administered through USDA's Farm Service Agency,will offer various loans of up to $35,000 for terms of up to seven years tohelp recipients deal with farming's often prohibitive start-up costs. ( SourReuters)

UK wheat imports surpass one million tonnesUK wheat imports surpassed one million tonnes during the first fivemonths of the 2012/13 season, exceeding the total for the entireprevious marketing year, customs data showed on Tuesday. Imports hadsoared this season after a poor wheat crop in Britain with yields slumpingto a 23-year low and quality hurt by high diseases levels. Wheat importsin November totalled 225,262 tns, of which 200,957 tns came fromwithin the European Union. The cumulative total for the 2012/13 season,which started on July 1, 2012, rose to 1.04 mn tns, almost triple the366,636 tns shipped in the same period a year earlier. Imports for thewhole 2011/12 season were 907,032 tns. ( Source: Reuters)

News in brief China to Start Selling Cotton from MondayChina has finalized the selling of cotton reserves from Monday to meetdemand from domestic textile companies. The price at which the sellingis to be done is slightly lower than domestic prices but 25-30% higherthan international prices. Approx. 3 million tons of cotton reserve isexpected to be sold, by China. The prices might show improvement asimports are also likely to go up as domestic prices in China are higherthan domestic cotton so traders can leverage their position. ( Source:

Agriwatch)

Govt may increase import duty on edible oils, export morewheatThe government is considering increasing the import duty on edible oilsto give a fillip to domestic crushing and protect the interest of growers. Itis also considering allowing the export of more wheat to clear stocksahead of the new procurement season.“The decisions in this regard were taken at ahigh - level meeting betweenFinance Minister PChidambaram, Food Minister K V Thomas andAgriculture Minister Sharad Pawar. A Cabinet note on all the decisionswill be moved soon,” a senior government official said. ( Source: BusinessStandard)

Now, 20% special margin on potato contracts, to curb pricevolatilityThe Forward Markets Commission (FMC), the commodity derivativesmarket regulator, has levied a 20 per cent special margin on the buy sideon all potato contracts, effective today, to control a sudden price spurt inthe vegetable. With this levy, the overall margin on the long side goes upto 30 per cent from the existing normal margin of 10 per cent, while theshort side margin remains unchanged at 10 per cent. Potato contracts fornear month delivery on the Multi Commodity Exchange rose 11.4 percent in the past 10 days due to extreme change in the weather and theresulting fear of crop loss this year. Supply to mandis was also hit by a

shortage of transport and labourers in farms and the markets. In the spotmarket, too, prices rose 15 per cent in the past two weeks. ( Source: BusinessStandard)

IMD launches App for weather forecastsNext time you plan to board a flight from Chennai to Delhi in the winters,you can check for fog on ‘India Weather’, a mobile application (App)launched on Tuesday by India Meteorological Department (IMD). TheIMD’s App is meant for smartphones and tablets and can be downloadedthrough Google Play Store. To begin with, the App is available in fourmetros – Delhi, Chennai, Mumbai and Kolkata – and will offer currentweather observations along with four-day forecasts. The App will be laterextended to other parts of the country. Launching the App as part of thecelebrations of IMD’s 138 th foundation day here, Union Minister forScience & Technology and Earth Sciences Jaipal Reddy said reliability of monsoon forecast was key to ensuring food security, and added thatthere was need to focus attention on predicting extreme weatherelements, which had become quite common. ( Source: Business Line)

Indian tea delegation puts off visit to PakistanThe present tension along the India-Pakistan border and the consequentdevelopments have cast a shadow over Indian Tea Association’s plan totake a tea delegation to Pakistan. The situation, it is felt, is not conduciveto undertaking such a tour. “We propose to take the delegation in Marchand hopefully the tension will ease by that tim e,” Arun N. Singh,Chairman of ITA, told Business Line. “We’ve already written to the TeaBoard in this regard”. Pakistan has emerged a major buyer of India tea,particularly the cheap South Indian variety. In 2011, India exported 25million kgs to Pakistan, the highest ever, and the figure for 2012 is

estimated at 21 mkgs or so. ( Source: Business Line)

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 3/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights as on Jan 15, 2013

% changeUnit Last Prev day WoW MoM Y

Chana Spot - NCDEX(Delhi)

Rs/qtl 3947 -0.89 -1.49 -2.31 14

Chana- NCDEXJan'13 Futures

Rs/qtl 3989 -1.24 -1.85 -2.71 14

Source: Reuter

Technical Chart - Chana NCDEX April contract

Source: Telequo

Technical Outlook valid for Jan 16, 2013

Contract Unit Support Resistance

Chana Apr Futures Rs./qtl 3450-3475 3525-3550

ChanaChana January contract as well as spot prices witnessed downward trendon Tuesday and settled 1.24% and 0.89% lower respectively on accountof continuous rise in imports which is easing supplies in the domesticmarkets coupled with higher output expectations for the coming season.However, April contract settled 0.4% higher on short coverings.

Although chana prices witnessed 17% gains in 2012 on the back of loweravailability, sentiments have turned negative since December 2012 onaccount of continuous supplies of imported chana from Australia coupledwith higher output expectations.Sowing progressTotal pulses acreage as on 11th Jan 2013 stood at 140.87 lakh ha, up by0.4% yoy. As on 4 th Jan 2013, pulses acreage was down by 0.4%.

Chana sowing is almost complete and acreage so far is at 91.68 lakh ha,up by 5.4% as on 11th Jan.

Chana acreage is marginally higher by 3% this year in Rajasthan at 14.80lakh ha, In Maharashtra Chana acreage is up at 10.92 lakh ha as on 11 th Jan 2013 vs normal area of 10.6 lakh ha and 2012 area of 7.04 lakh ha.While in AP it is up at 7.14 lakh ha as on 11 th Jan 2013, up by 26%.(Source: State farm dept)

Demand supply fundamentalsChana fresh crop arrival has started in Karnataka & Andhra Pradesh andwould pick up soon in Maharashtra too. However, arrival pressure willbuilt up February onwards when harvesting commence in MP.

Farm ministry has targeted 7.9 mn tn Chana output for 2012-13 season,higher compared to 7.58 mn tn in 2011-12.

According to the first advance estimates of 2012-13 season, kharif pulsesoutput is estimated lower by 14.6% at 5.26 million tonnes compared with6.16 mn tn last year.

The Commission for Agriculture Costs and Prices (CACP) has suggested 10per cent import duty on pulses to encourage domestic production. in thefirst six months of the new fiscal that is from April to September thisyear, imports were an estimated 12 lakh tonnes.

Assocham estimates, 21 mn tn of pulses demand in 2012-13 and is likelyto reach at 21.42 mn tn in 2013-14 and 21.91 MT in 2014-15. (Source:Agriwatch).

Trade ScenarioUSDA revealed that Myanmar beans and pulses export is up by 56 percent to 110498 MT as compared with same period in last year. Out of thetotal export, 73 percent (80721 MT) was exported to India followed bySingapore (11316 MT). (Source: Agriwatch dated Dec 27)

In Australia, total chickpea production in 2012 –13 is estimated to haveincreased to a record of around 746000 tones as compared with 485000tons in 2011-12. India imports Chana mainly from Australia and Canadaand higher availability in these countries at comparatively cheaper ratesis seen boosting imports of Chana to meet the domestic shortfall.

OutlookChana April contract may trade with a negative bias due to highershipments of imported chana and expectations of better output nextseason. Any adverse report with respect to weather may bring a reboundin the prices and thus a close watch on weather is crucial at this point of time.

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 4/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights as on Jan 15, 2013 % Change

Unit Last Prev. day WoW MoM YoYSugar Spot- NCDEX(Kolhapur) Rs/qtl 3253 0.10 0.57 -2.37 1

Sugar M- NCDEXJan'13 Futures Rs/qtl 3228 0.09 0.56 0.88 1

Source: R

International Prices as on Jan 15, 2013

% ChangeUnit Last Prev day WoW MoM Y

Sugar No 5- Liffe-Mar'13 Futures

$/tonne 502 -1.12 -0.75 -1.22 -20

Sugar No 11-ICEMar '13 Futures

$/tonne 413.78 -1.48 -0.27 -1.38 -21

.Source: R

Technical Chart - Sugar NCDEX Feb contract

Source: Tele

Technical Outlook valid for Jan 16, 2013

Contract Unit Support Resistance

Sugar Feb NCDEX Futures Rs./qtl 3230-3245 3265-3280

SugarSugar futures witnessed marginal losses in the futures markets, however,have started showing some signs of recovery in the physical market asdemand is seen emerging at lower levels. Also report of lower caneplanting is seen supporting an upside in the sugar prices.

There are reports that drought in parts of Maharashtra and Karnatakahas hurt fresh sugarcane plantings, which may affect cane availability forsugar year 2013-14 starting October.

Although this will have long term implications, outlook for short termremains bleak amid sufficient supplies. Government has allocated total70 lac tons of non-levy sugar quota for Dec-March 2012-13 period whichis higher from 59.5 lac tons last year.

Raw sugar futures on ICE as well as Liffe white sugar corrected sharplyextending previous day’s losses and settled 1.12% and 1.48% lower onTuesday on account of a supply glut situation on the back of a sugarsurplus for the third consecutive year.

Domestic Production and Exports

Mills in the country have produced 7.96 mln tn sugar in the first threemonths of the season, up nearly 2.5% a year ago.

In Maharashtra, the largest sugar producer in the country, 155 mills areoperational and have produced 1.88 mln tn sugar till Dec 15, comparedwith 1.83 mln produced a year ago by 165 mills.

In Uttar Pradesh, the second largest sugar producer in the country, totaloutput as on Dec 15 was 1.03 mln tn, about 20% lower on year, as somemills in the eastern part of the state are still to commence cane crushing.

The producers body has estimated sugar output lower at 24 mn tn, downby 2mn tn compared to the current year.Industry body ISMA has estimated 6.5 mn tn stocks for the new seasonbeginning October 01, 2012 compared to 5.5 mn tn year ago. India may

export 1.5 mn tn sugar in 2012-13.With the opening stocks of 6.5 mn tn, domestic Sugar supplies areestimated at 30.5 mn tn against the domestic consumption of around 22.5mln tn for 2012-13.Global Sugar UpdatesAccording to the Brazil Agriculture Ministry, The 2012/13 cane crush wasat 531.35 million tonnes as of Dec. 31, up from 491.16 million tonnescrushed the previous year. The 2013/14 crush will likely surpass thecurrent one.

Brazil's main center-south cane crop will produce between 580 millionand 590 million tonnes of sugar cane in 2013/14. Brazil will likely favorethanol production over sugar from the 2013/14 cane crop.

The 2012/13 sugar crop in Thailand, the world's second-biggest exporter,could drop below a forecast 9.4 million tonnes due to lower-than-expected yield. The crushing season started on Nov. 15 and 1.9 milliontonnes of sugar has been produced so far (Source: Reuters)

Outlook

Sugar prices may recover further in the coming weeks as demand is seenemerging at lower levels. Reports of lower cane planting in some parts of Maharashtra and Karnataka may also bring some stability in the prices.Further, it is expected that government will take some measure tocontrol prices, which are below the cost of production levels, from fallingfurther so as to protect the interest of the millers.

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 5/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights as on Jan 15, 2013

% Change

Unit Last Prev day WoW MoM Y

Soybean Spot- NCDEX(Indore)

Rs/qtl 3239 0.90 1.41 -4.31 32

Soybean- NCDEX Jan '13Futures

Rs/qtl 3200 0.46 2.83 -4.41 28

Ref Soy oil Spot-NCDEX(Indore)

Rs/10 kgs 743.8 0.65 3.79 1.52 4

Ref Soy oil- NCDEX Jan '13Futures

Rs/10 kgs 737.8 0.55 4.03 1.70 3

Source: Reuters

as on Jan 15, 2

International Prices Unit LastPrevday WoW MoM Y

Soybean- CBOT-Jan'13 Futures

USc/Bushel 1414 -0.32 -0.44 -4.27 19

Soybean Oil - CBOT-Jan'13 Futures

USc/lbs 50.87 0.83 3.31 4.63 0.

Source: Reuters

Crude Palm Oil as on Jan 15, 2013 % Change

Unit LastPrevday WoW MoM Y

CPO-BursaMalaysia – Jan '13Contract

MYR/Tonne 2330 2.37 1.61 14.10 -2

CPO-MCX-Jan '13Futures

Rs/10 kg 432.8 1.03 -2.15 5.43 -1

Source: Reu

RM Seed as on Jan 15, 2013

Unit LastPrevday WoW MoM

RM Seed Spot-NCDEX (Jaipur)

Rs/100 kgs 4300 2.14 1.42 1.84 21

RM Seed- NCDEXJan'13 Futures

Rs/100 kgs 4228 0.28 0.96 4.68 12

Source: Reuters

Technical Chart –Soybean NCDEX Feb contra

Source: Telequ

Technical Outlook valid for Jan 16, 2013

Contract Unit Support Resistance

Soy Oil Feb NCDEX Futures Rs./qtl 700-706 714-718

Soybean NCDEX Feb Futures Rs./qtl 3140-3175 3255-3300

RM Seed NCDEX Apr Futures Rs./qtl 3400-3430 3490-3525CPO MCX Jan Futures Rs./qtl 425-429 437-442

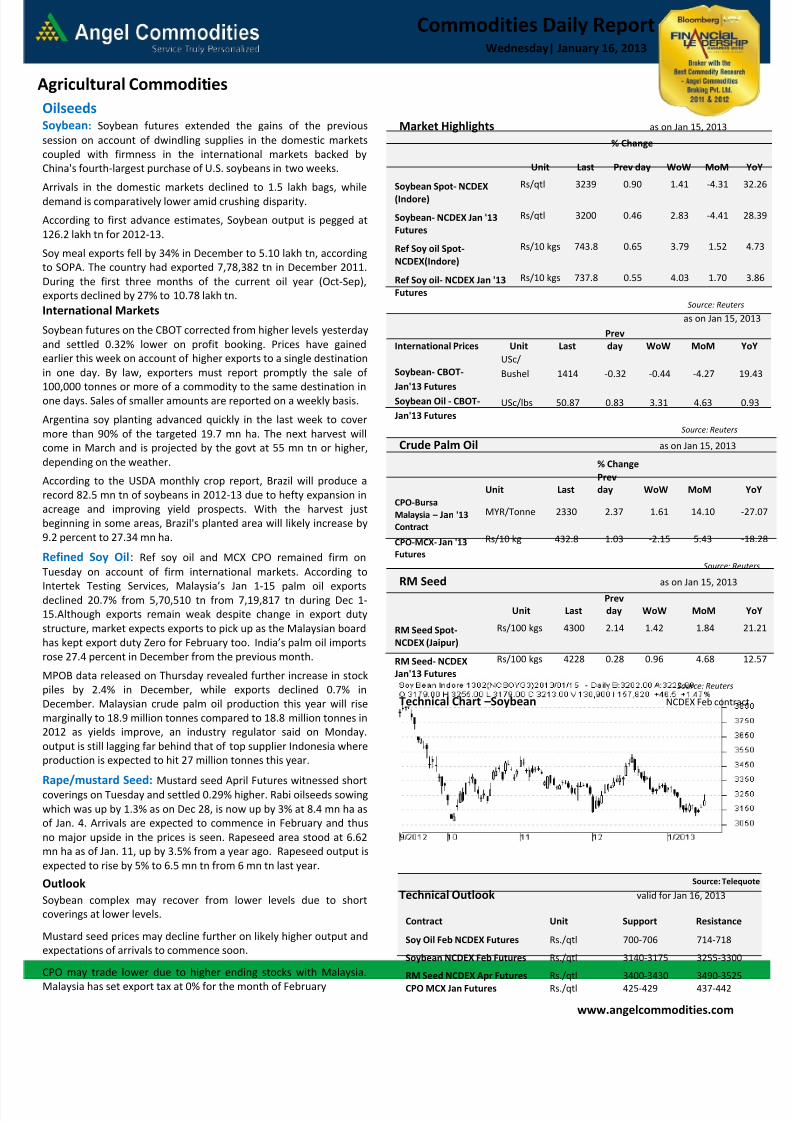

OilseedsSoybean : Soybean futures extended the gains of the previoussession on account of dwindling supplies in the domestic marketscoupled with firmness in the international markets backed byChina's fourth-largest purchase of U.S. soybeans in two weeks.

Arrivals in the domestic markets declined to 1.5 lakh bags, whiledemand is comparatively lower amid crushing disparity.

According to first advance estimates, Soybean output is pegged at126.2 lakh tn for 2012-13.

Soy meal exports fell by 34% in December to 5.10 lakh tn, accordingto SOPA. The country had exported 7,78,382 tn in December 2011.During the first three months of the current oil year (Oct-Sep),exports declined by 27% to 10.78 lakh tn.International Markets

Soybean futures on the CBOT corrected from higher levels yesterdayand settled 0.32% lower on profit booking. Prices have gainedearlier this week on account of higher exports to a single destinationin one day. By law, exporters must report promptly the sale of 100,000 tonnes or more of a commodity to the same destination inone days. Sales of smaller amounts are reported on a weekly basis.

Argentina soy planting advanced quickly in the last week to covermore than 90% of the targeted 19.7 mn ha. The next harvest willcome in March and is projected by the govt at 55 mn tn or higher,depending on the weather.

According to the USDA monthly crop report, Brazil will produce arecord 82.5 mn tn of soybeans in 2012-13 due to hefty expansion inacreage and improving yield prospects. With the harvest justbeginning in some areas, Brazil's planted area will likely increase by9.2 percent to 27.34 mn ha.

Refined Soy Oil : Ref soy oil and MCX CPO remained firm onTuesday on account of firm international markets. According to

Intertek Testing Services, Malaysia’s Jan 1 -15 palm oil exportsdeclined 20.7% from 5,70,510 tn from 7,19,817 tn during Dec 1-15.Although exports remain weak despite change in export dutystructure, market expects exports to pick up as the Malaysian boardhas kept export duty Zero for February too. India’s pa lm oil importsrose 27.4 percent in December from the previous month.

MPOB data released on Thursday revealed further increase in stockpiles by 2.4% in December, while exports declined 0.7% inDecember. Malaysian crude palm oil production this year will risemarginally to 18.9 million tonnes compared to 18.8 million tonnes in2012 as yields improve, an industry regulator said on Monday.output is still lagging far behind that of top supplier Indonesia whereproduction is expected to hit 27 million tonnes this year.

Rape/mustard Seed: Mustard seed April Futures witnessed shortcoverings on Tuesday and settled 0.29% higher. Rabi oilseeds sowingwhich was up by 1.3% as on Dec 28, is now up by 3% at 8.4 mn ha asof Jan. 4. Arrivals are expected to commence in February and thusno major upside in the prices is seen. Rapeseed area stood at 6.62mn ha as of Jan. 11, up by 3.5% from a year ago. Rapeseed output isexpected to rise by 5% to 6.5 mn tn from 6 mn tn last year.

OutlookSoybean complex may recover from lower levels due to shortcoverings at lower levels.

Mustard seed prices may decline further on likely higher output andexpectations of arrivals to commence soon.

CPO may trade lower due to higher ending stocks with Malaysia.Malaysia has set export tax at 0% for the month of February

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 6/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights as on Jan 15, 2013 % Change

Unit Last Prev day WoW MoM YoY

Pepper Spot-NCDEX (Kochi)

Rs/qtl 38644 0.42 1.66 0.06 22.5

Pepper- NCDEXFeb'13 Futures

Rs/qtl 36955 2.57 6.38 -5.44 20.7

Source: Reut

Technical Chart – Black Pepper NCDEX Feb contract

Source: Telequo

Technical Outlook valid for Jan 16, 2013

Contract Unit Support Resistance

Black Pepper NCDEX Feb Futures Rs/qtl 36340-36690 37350-37700

Black PepperPepper Futures traded on a bullish note yesterday due to low stocks andthin supplies. Good winter demand also supported the prices. Prices havealso increased over the last few days due to arrivals of good qualitypepper from Kerala. Earlier, prices had corrected as Food Safety andStandards Authority of India sealed the entire quantity of pepper stored

in six warehouses in Kerala of about 5,000 tonnes. Harvesting of the freshcrop has commenced and is expected to gain momentum in the comingdays. However, winter demand coupled with low stocks in the domesticmarkets has supported prices at lower levels. FMC is probing intocomplaints against movement in the pepper market which haspressurized prices. Exports demand for Indian pepper in the internationalmarkets is also weak due to price parity. The Spot settled as well as theFutures settled 0.42% and 2.57% higher on Tuesday.Spices Board has announced plans to import high yielding Madagascarvariety that was behind the record productivity in Vietnam. It could raiseproductivity of Indian pepper from 2,000 kg/ha to 7,000 kg/ha.Pepper prices in the international market are being quoted at$7,800/tn(C&F Europe). Vietnam and Indonesia Austa variety are quotedat $7,000/tn and Malaysia Austa reported at $6950-7000/tn.

Exports and ImportsAccording to Spices Board of India, exports of pepper in April 2012 fell by47% and stood at 1,200 tonnes as compared to 2,266 tonnes in April2011. India imported 1,848 tonnes of pepper till March 2012 and hasbecome the third country to import such large quantity after UAE andSingapore. ( Source: Agriwatch )

According to Vietnam Ministry of Agriculture and Rural Development(MARD) exports of pepper during Jan-Oct 2012 stood at 102,340 mt,lower by 12% as compared to 1,15,780 mt in the same period last year.Total exports in 2012 are forecasted at around 1,10,000 tonnes.Pepper imports by U.S. the largest consumer of the spice declined 26%during January-September 2012 period to 41,923 tn as compared to52,489 tn in the same period previous year.

Exports from Indonesia posted significant decrease of 42% as comparedto previous year. Exports stood at 36,500 tonnes as compared to 62,599tonnes in the last year. Brazil exported 25,900 tn pepper during Jan-Nov2012, around 20% lower compared with 32,650 tn in the same periodlast year. Exports from Malaysia 8,300 tn pepper during Jan-Oct 2012,lower by 30% last year while exports in October stood at 1,077 mt in.Production and ArrivalsThe arrivals in the spot market were reported at 21 tonnes while off takes were reported at 20 tonnes on Tuesday.As per IPC, Global pepper production in 2012 is projected at 3.27 lk tn, upcompared with 3.18 lk tn in 2011. Production for 2013 is projected at316832 tn. Indonesian pepper output is expected to rise by 24% and inVietnam by 10%.According to previous estimates, pepper output in Vietnam is estimated

to be 1 lakh tonne in 2012 as compared to 1.1 lakh tonne in 2011. Brazilis also expected to produce 22,000 tn this year.Domestic consumption of Pepper in the world is expected to grow by3.03% to 1.25 lakh tonnes while exports are likely to grow by 1.48% to2.46 lakh tonnes in 2012 . (Source: Pepper trade board ) Pepper production in2012-13 is expected around 60,000-63,000 tonnes. Currently, pepper isin the fruit formation stage in Kerala.OutlookPepper prices are expected to rise on account of low stocks coupled withthin arrivals. Winter buying coupled with arrivals of good quality cropmay also support prices. However, increasing supplies coupled withhigher output expectations may cap sharp gains. FSSAI’s sealing of hugequantity of pepper and FMC’s probe into complaints aga inst pricemovement may also pressurise the prices.

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 7/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

www.angelcommodities.com

Market Highlights as on Jan 15, 2013 % Change

Unit LastPrevday WoW MoM Y

Jeera Spot- NCDEX

(Unjha)

Rs/qtl 14255 -0.60 -2.34 -4.89 -11

Jeera- NCDEX Mar'13 Futures

Rs/qtl 13828 1.34 -4.75 -5.40 -11

Source: Reute

Technical Chart – Jeera NCDEX March contract

Source: Telequot

Market Highlights as on Jan 15, 2013 % Change

Unit LastPrevday WoW MoM YoY

Turmeric Spot-NCDEX (N'zmbad)

Rs/qtl 5693 0.00 -1.03 10.07 10.16

Turmeric- NCDEXApr '13 Futures

Rs/qtl 6566 -1.08 -4.54 23.65 40.90

Technical Chart – Turmeric NCDEX April contrac

Source: Telequot

Technical Outlook Valid for Jan 16, 2013

Unit Support Resistance

Jeera NCDEX March Futures Rs/qtl 13400-13620 14000-14210

Turmeric NCDEX April Futures Rs/qtl 6420-6500 6670-6750

JeeraJeera Futures recovered from lower levels on account of shortcoverings coupled with fresh enquiries at lower levels. Prices havecorrected sharply and made fresh lows on account of higher sowing aswell as conducive weather in Gujarat, the main jeera growing region.Sowing is almost complete and is in its final stage. According to

Gujarat State Agri Dept. sowing in Gujarat is reported at 3.244 lakh hatill Jan, 2013 compared with 3.64 lakh ha last year. In Rajasthan,sowing is expected to increase by 10-15%. The spot settled 0.6% lowerwhile the Futures settled 1.34% higher on Tuesday.According to markets sources about 75% exports target has alreadybeen achieved due to a supply crunch in the global markets. Supplyconcerns from Syria and Turkey still exists. Expectations are thatexport orders may still be diverted to India from the internationalmarkets due to lack of supplies from Syria on back of the ongoing civilwar. Production in Syria and Turkey is being reported around 17,000tonnes and around 4,000-5,000 tonnes, lesser than expectations.Jeera prices of Indian origin are being offered in the internationalmarket at $2,875-2,900 tn (c&f) while Syria and Turkey are notoffering. Carryover stocks of Jeera in the domestic market is expectedto be around 5-6 lakh bags.

Production, Arrivals and ExportsArrivals in Unjha were reported at 2,500 tn on Tuesday. Production of Jeera in 2011-12 is expected around 40 lakh bags as against 29 lakhbags in 2010-11 (55 kgs each).According to Spices Board of India, exports of Jeera in April 2012 stoodat 2,500 tonnes as compared to 2,369 tonnes in April 2011, anincrease of 6%.

OutlookJeera prices may trade on a mixed note. Fresh export enquiries maylimit a sharp downside. Demand from domestic traders and millers atlower levels may also support prices. However, higher sowing figuresin Gujarat may pressurize prices. In the medium term, prices are likelyto stay firm as there are limited stocks with Syria and Turkey.

TurmericTurmeric Futures corrected yesterday on account of long liquidationdue to huge carryover stocks.. Good demand from upcountry markethas supported the prices over the last few weeks. Lower productionestimates have also supported the prices. Also, arrivals of good qualitycrop have supported prices.There are reports of some crop damage in Erode region. Expectationsare that production may be lower by 40-50%. Production is expectedaround 55 lakh bags. It is estimated that next year’s carryover stockswould be around 10 lakh bags. There are reports that TurmericFarmers’ Association of India have decided to fix their own MSP of Rs.10000/qtl. The Spot remained closed on account of Pongal andMakar Sankranti while the Futures settled 1.08% lower on Tuesday.

Production, Arrivals and ExportsThe spot markets remained closed on account of Pongal festival.Turmeric production in 2012-13 is expected around 64-65 lakh bags.Production in 2011-12 is projected at historical high of 10.62 lakh tn.According to Spices Board of India, exports of Turmeric in April 2012increased by 1% at 7,300 tn as compared to 7,230 tn in April 2011.OutlookTurmeric may correct from higher levels in the intraday extendingprevious day’s losses. Higher carryover stocks a nd weak overseasdemand may pressurize prices. However, demand from stockists andweather concerns may support prices. Lower production expectationsmay also support prices.

7/30/2019 Daily Agri Tech Report

http://slidepdf.com/reader/full/daily-agri-tech-report 8/8

Commodities Daily Report

Agricultural Commodities

Wednesday| January 16, 2013

Market Highlights as on Jan 15, 2013 % Change

Unit Last Prev. day WoW MoM YNCDEX KapasFutures

Rs/20 kgs 922.5 0.65 -2.28 -10.78

MCX Cotton Futures Rs/Bale 16310 0.37 -0.85 -0.85

Source: Re

International Prices as on Jan 15, 2013

% ChangeUnit Last Prev day WoW MoM

ICE Cotton USc/Lbs 76.21 0.91 1.45 1.75

Cot look A Index 81.35 0.00 0.00 0.00

Source: Reu

Technical Chart - Kapas NCDEX April contract

Source: Tele

Technical Chart - Cotton MCX Jan contract

Source: Tele

Technical Outlook valid for Jan 16, 2013

Contract Unit Support Resistance

Kapas NCDEX April Futures Rs/20 kgs 910-917 928-935

Cotton MCX Jan Futures Rs/bale 16200-16250 16350-16400

KapasNCDEX Kapas as well as MCX Cotton witnessed short coverings andsettled 0.65% and 0.37% higher on Tuesday. Prices had declinedconsiderably in the past few weeks on account of lower demand andhigher output expectations.

However, demand is expected to pick up at lower levels to meet thecotton yarn export registrations. Registration for exports of cotton yarnhas hit the highest in at least two years on burgeoning demand fromIndia’s perennially importing cou ntries i.e. Bangladesh and China.

Although, Cotton advisory Board has pegged cotton output lower at 334lakh bales, Cotton Association of India (CAI), expects output to be around353 lakh bales in 2012-13..

According to the data released by Cotton Corporation of India, Suppliesuntil Jan 13 are down 6.3 percent to 12.5 mn bales of 170 kg each, downfrom 12.9 mn bales a year earlier. Arrivals were down by 10 percent ason 16 th Dec.ICE Cotton traded on a positive note on account of index buying.Concerns about the quality of cotton to be released by China also pulledup the prices. ICE cotton Futures settled 0.91% higher on Tuesday.

Domestic Production and Consumption

According to Cotton Advisory Board’s (CAB) estimates (4th Oct 2012) for2012-13 season that commenced in October, domestic cottonproduction is pegged 334 lakh bales, down 5.6% from the previous year’sestimates of 353 lakh bales.

Lower opening stocks coupled with estimated lower output will result inlower supplies this season at 374 lakh bales, a decline of 8.7% comparedwith last year’s 410.77 lakh bales. On the consumption front, domesticconsumption is estimated higher at 270 lakh bales on the back of highermill consumption.

However, after witnessing record exports in 2011-12 season, Indian

exports could witness significant fall this season on the back of loweravailability along with unattractive domestic cotton prices. CABestimates cotton exports at 70 lakh bales this season, compared with128.8 lakh bales last year.

Global Cotton UpdatesChina, the world's biggest buyer of cotton, began selling a tiny fraction of its massive stockpile of the fibre on Monday, in a move to ease domesticsupply shortages.Beijing has been building a strategic stockpile of cotton since 2011,paying above global prices to support its farmers, but the policy has hurtChina's textile mills, which have been struggling with tight supplies, andhigh prices, at home.Many in the industry were expecting China to reward mills that buy state

reserves with new import quotas enabling them to buy cheaper overseassupplies. But no such deal was announced.

Brazil’s 2012 -13 cotton production forecast at 6.3 million bales, down 27percent from 2011/12 production now estimated at 8.6 million bales.(USDA attaché report)

Outlook

Cotton prices may trade downwards today. Higher output expectationsby Cotton Association of India have turned the sentiments negative forthe cotton prices. However, downside may be limited as farmers may notsell their stocks at lower prices. Reports that the Government maypurchase cotton from farmers to avoid distress sales may also supportprices.