DA NANG PRESS CONFERENCE Q3 2013 - cbrevietnam.com … · Gold price •Global gold price (US$,...

33

DA NANG PRESS CONFERENCE Q3 2013 Presented by: Adam Bury & Thao Le 18 th November, 2013

Transcript of DA NANG PRESS CONFERENCE Q3 2013 - cbrevietnam.com … · Gold price •Global gold price (US$,...

DA NANG PRESS CONFERENCE Q3 2013 Presented by: Adam Bury & Thao Le

18th November, 2013

2 CBRE MARKET INSIGHTS | Q3/2013

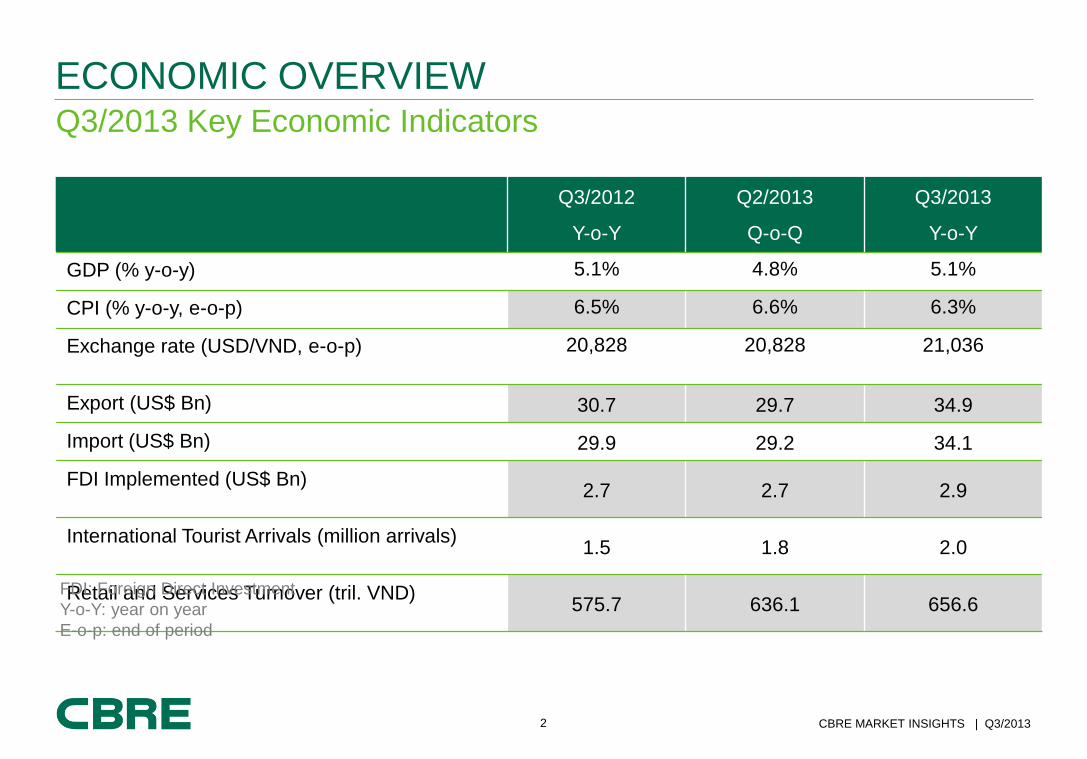

Q3/2013 Key Economic Indicators

ECONOMIC OVERVIEW

Q3/2012

Y-o-Y

Q2/2013

Q-o-Q

Q3/2013

Y-o-Y

GDP (% y-o-y) 5.1% 4.8% 5.1%

CPI (% y-o-y, e-o-p) 6.5% 6.6% 6.3%

Exchange rate (USD/VND, e-o-p) 20,828 20,828 21,036

Export (US$ Bn) 30.7 29.7 34.9

Import (US$ Bn) 29.9 29.2 34.1

FDI Implemented (US$ Bn) 2.7 2.7 2.9

International Tourist Arrivals (million arrivals) 1.5 1.8 2.0

Retail and Services Turnover (tril. VND) 575.7 636.1 656.6

FDI: Foreign Direct Investment

Y-o-Y: year on year

E-o-p: end of period

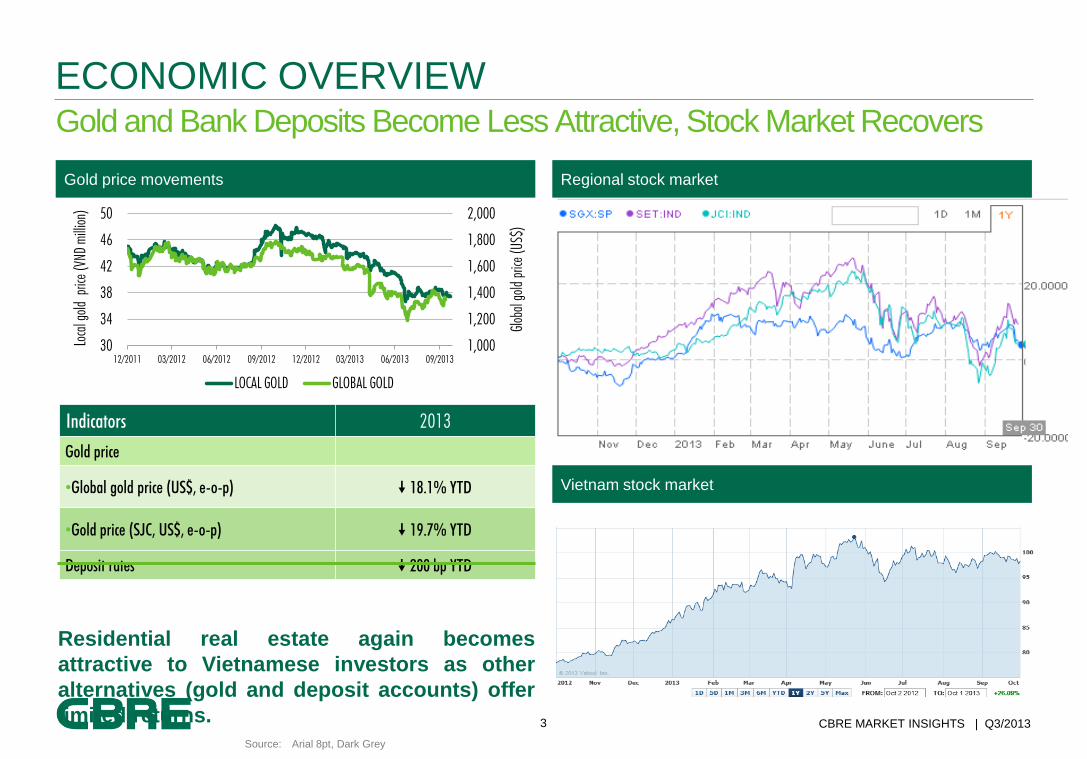

3 CBRE MARKET INSIGHTS | Q3/2013

Gold and Bank Deposits Become Less Attractive, Stock Market Recovers

ECONOMIC OVERVIEW

Gold price movements Regional stock market

Source: Arial 8pt, Dark Grey

Indicators 2013

Gold price

•Global gold price (US$, e-o-p) 18.1% YTD

•Gold price (SJC, US$, e-o-p) 19.7% YTD

Deposit rates 200 bp YTD

Residential real estate again becomes

attractive to Vietnamese investors as other

alternatives (gold and deposit accounts) offer

limited returns.

1,000

1,200

1,400

1,600

1,800

2,000

30

34

38

42

46

50

12/2011 03/2012 06/2012 09/2012 12/2012 03/2013 06/2013 09/2013

Glo

bal gold

price

(U

S$

)

Loca

l gold

price

(VN

D m

illion)

LOCAL GOLD GLOBAL GOLD

Vietnam stock market

4 CBRE MARKET INSIGHTS | Q3/2013

LEGISLATION OVERVIEW

Supporting legislation from the government:

Resolution 19 on allowing foreign individuals

to buy property in Vietnam;

Submitted draft on raising the ceiling for

foreign ownership ratio in listed companies

from 49% to 60%;

A single visa for tourists to Vietnam, Thailand

and Cambodia.

The Government is Listening

5 CBRE MARKET INSIGHTS | Q3/2013

More Opportunities for Foreigners to Buy Houses in Vietnam

LEGISLATION OVERVIEW

Current Law

(Resolution No.19, effective 2009 - 2013)

Proposed Amended Law

(effective 2014 IF approved)

Foreign Individual

Buyers

YES with restrictions such as:

• Individual investors who make direct investment in

Vietnam;

• Expatriates at managerial positions;

• Individuals who possess special skills that are

needed in Vietnam;

• Individuals who are married to Vietnamese citizens;

YES for all foreigners who have a visa to the country that

is valid for at least three months

Foreign

Organisations

ONLY foreign-invested companies operating in

Vietnam which are not in the real estate business but

have the need to provide accommodation to their

employees.

YES to all foreign investment funds, banks, Vietnamese

branches and representative offices of overseas

companies.

Sub-lease NO YES

Products Apartments only. Apartments + landed property (less than 500 sm)

Number of

Products

One unit only For individuals:

Option 1: Unlimited

6 CBRE MARKET INSIGHTS | Q3/2013

26

83

7

2

16

23

$1,827.50

$667.60

$171.50

$152.20

$106.50

$21.40

0 500 1000 1500 2000

Real estate

Processing and manufacturing …

Education

Beverages

Textile, garment and footwear

Information technology

US$ million

Total registered capital ($US mil) No. of projects

National comparison, GDP (%, y-o-y), 9M/2013

Vietnam HCMC Da Nang Hanoi

5.1% 10.3% 7.2% 7.9%

Highlight

Q3 2013 DA NANG ECONOMIC OVERVIEW

FDI in Da Nang by sectors – Q3/2013

Source: Vietnamese General Statistics Office

Top 5 countries investing in Da Nang – Q3/2013

Country

No. of

projects

Registered

capital (US$)

Market

share

Korea 35 705.645,309 22.55%

British Virgin Islands

16 682,856,356 21.82%

Singapore 12 416,507,718 13.31%

Japan 65 352,150,774 11.25%

USA 30 346,175,020 11.06%

Source: Da Nang IPC

Key growth areas:

Services – 8.8% y-o-y

Industry – 11.1% y-o-y

YTD, Da Nang has seen 13 FDI projects increased their

committed capital – totally an additional US$140.7m of

investment.

• Coca Cola notable in investing a further US$16m.

• Noted that the amount of newly registered FDI is

down however

INFRASTRUCTURE

8 CBRE MARKET INSIGHTS | Q3/2013

DA NANG ECONOMC OVERVIEW Infrastructure

Third Ba Na Hills cable car route, which has achieved 4

world records, opened in 2013 help to increase domestic

tourists.

The multi-level flyover project broke ground on 28th Sep. This

will help to relieve traffic congestion and number of accidents

at Hue T-junction, meet regional planning and ensure

transport safety on the National Highway 1A

The 10ha Software Park No 2 has been planned Hai Chau

District’s Da Phuoc Residential Area – emphasising Da

Nang’s focus on IT.

The construction of 341-hectare IT Park, invested by Rocky

Lai & Associates Inc started in 2013. This project will be the

most modern IT Park of the central region and highlands of

Viet Nam.

Da Nang plans to build a 11,000m2 riverside park, a

7,700m2 tourism services area, a 3,592m2 passenger pick-up

area for trip boats, on the west bank of the river.

9 CBRE MARKET INSIGHTS | Q3/2013

Improving and Still Room for Growth

AIR INFRASTRUCTURE

Airline From Flights/ week Airline From Flights/week

Silk Air Singapore 3 China Eastern Airlines Kunming 2

Silk Air Siem Riep 3 Shanghai Airlines Shanghai 2

Vietnam Airlines Siem Riep 7 Vietnam Airlines Chengdu 2

Dragon Airlines Hong Kong 4 Vietnam Airlines Seoul 3

Air Macau Macau 3 Korean Air Seoul 4

Vietnam Airlines Guangzhou 2 Asiana Airlines Seoul 2

Vietnam Airlines Wenzhou 2 Lao airlines Vientiane 3

China Eastern Airlines Beijing 2 Lao airlines Pakse 3

International scheduled flights to Da Nang airport per week 47 flights/week

Danang is becoming a regionally important hub, that has considerable capacity for further

growth;

Above scheduled flights will expand further in the coming months, most notably with new

expanding services to Hong Kong, Siem Reap and Singapore through Dragon Air And Silk Air.

There is also expectations of direct flights to Thailand and Japan in the near future

In addition, there are 247 domestic flights operated by Vietnam Airlines, Vietjet Air, and Jetstar

airlines.

Source: danang.gov.vn

10 CBRE MARKET INSIGHTS | Q3/2013

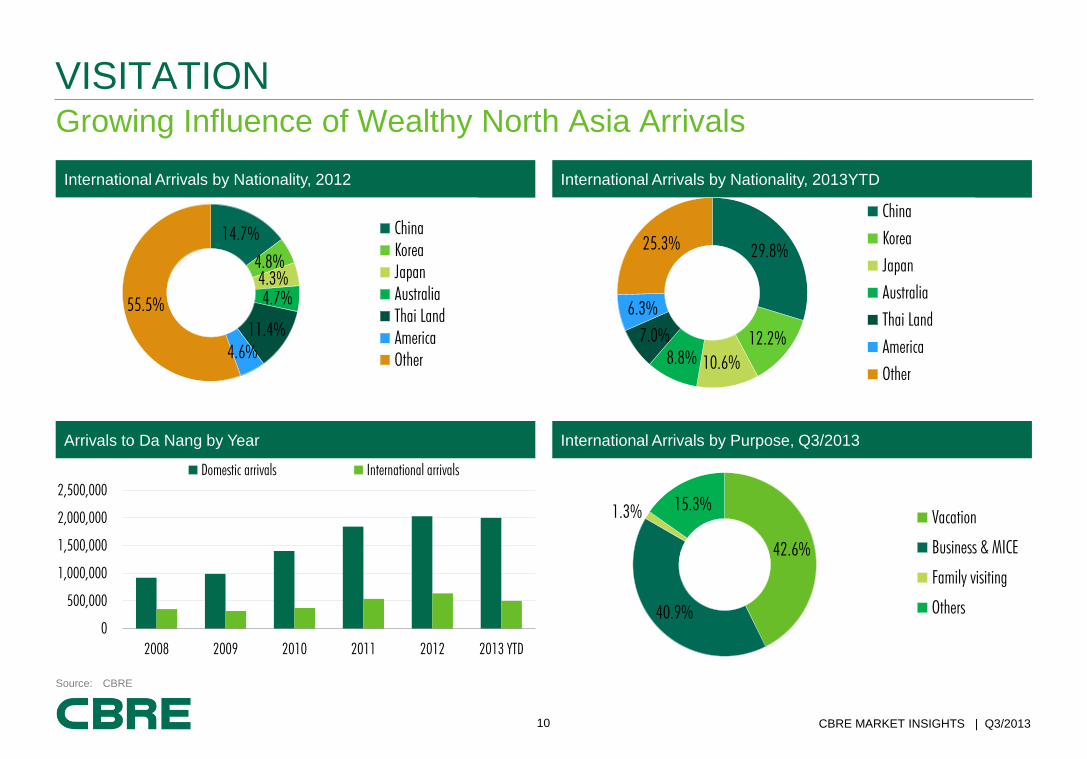

Growing Influence of Wealthy North Asia Arrivals

VISITATION

International Arrivals by Nationality, 2012 International Arrivals by Nationality, 2013YTD

Arrivals to Da Nang by Year International Arrivals by Purpose, Q3/2013

Source: CBRE

29.8%

12.2%

10.6% 8.8%

7.0%

6.3%

25.3%

China

Korea

Japan

Australia

Thai Land

America

Other

14.7%

4.8%

4.3%

4.7%

11.4%

4.6%

55.5%

China

Korea

Japan

Australia

Thai Land

America

Other

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2008 2009 2010 2011 2012 2013 YTD

Domestic arrivals International arrivals

42.6%

40.9%

1.3% 15.3%

Vacation

Business & MICE

Family visiting

Others

HOSPITALITY Hotel/Resort

12 CBRE MARKET INSIGHTS | Q3/2013

Q3 2013

SNAPSHOT

5 star 4 star 3 star Total

Number of hotels 9 10 29 48

Total supply (room) 2,072 1,776 2,043 5,891

New supply (room) 0 745 90 835

Average occupancy rate (%) 62.4% 44.5%

Q-o-q change (pp) 5.1 pps 6.1 pps

Y-o-y change (pp) 6.3 pps -1.2 pps

Average daily rate (US$/room/night) 153.75 63.65

Q-o-q change (%) 3.6% -2.2%

Y-o-y change (%) 44.8% 19.0%

Source: CBRE

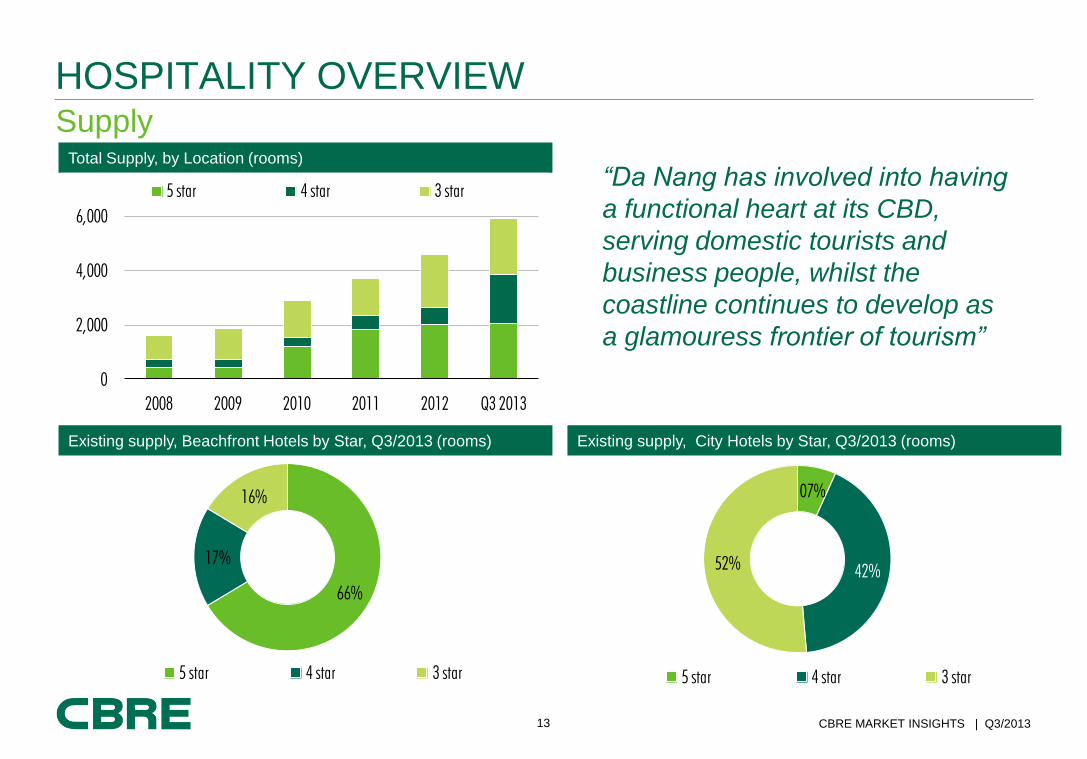

13 CBRE MARKET INSIGHTS | Q3/2013

Supply

HOSPITALITY OVERVIEW

“Da Nang has involved into having

a functional heart at its CBD,

serving domestic tourists and

business people, whilst the

coastline continues to develop as

a glamouress frontier of tourism”

Total Supply, by Location (rooms)

0

2,000

4,000

6,000

2008 2009 2010 2011 2012 Q3 2013

5 star 4 star 3 star

Existing supply, Beachfront Hotels by Star, Q3/2013 (rooms) Existing supply, City Hotels by Star, Q3/2013 (rooms)

66%

17%

16%

5 star 4 star 3 star

07%

42%52%

5 star 4 star 3 star

14 CBRE MARKET INSIGHTS | Q3/2013

Management

HOSPITALITY OVERVIEW

Existing Supply, Branded hotels by Star, Q3/2103 (rooms) Existing supply, Self-managed hotels by Star, Q3/2103 (rooms)

72%

28%

00% 5 star

4 star

3 star

11%

32%57%

5 star

4 star

3 star

Total Supply, by Management type (rooms)

0

1,000

2,000

3,000

4,000

2008 2009 2010 2011 2012 Q3 2013

Branded Self managed

Source: CBRE

15 CBRE MARKET INSIGHTS | Q3/2013

Changing Supply Dynamics

HOSPITALITY

4-5 STAR HOTEL SUPPLY

2012 – Q3/2013

2009 – 2011

Prior 2008

Year 2009 2010 2011 2012 9M/2013

Change by year (rooms) 238 1,050 809 979 1,299

16 CBRE MARKET INSIGHTS | Q3/2013

Occupancy

HOSPITALITY

“Unsurprisingly, established hotels have shown the best occupancy rates, though newly

inaugurated properties are swiftly improving as they develop their own reputations – this

is culminating in beachfront properties having record occupancies”

Occupancy Rate by Location and Star (%)

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013

5 star - Beachfornt 5 star - City Hotel 4 star - Beachfornt 4 star - City Hotel

Source: CBRE

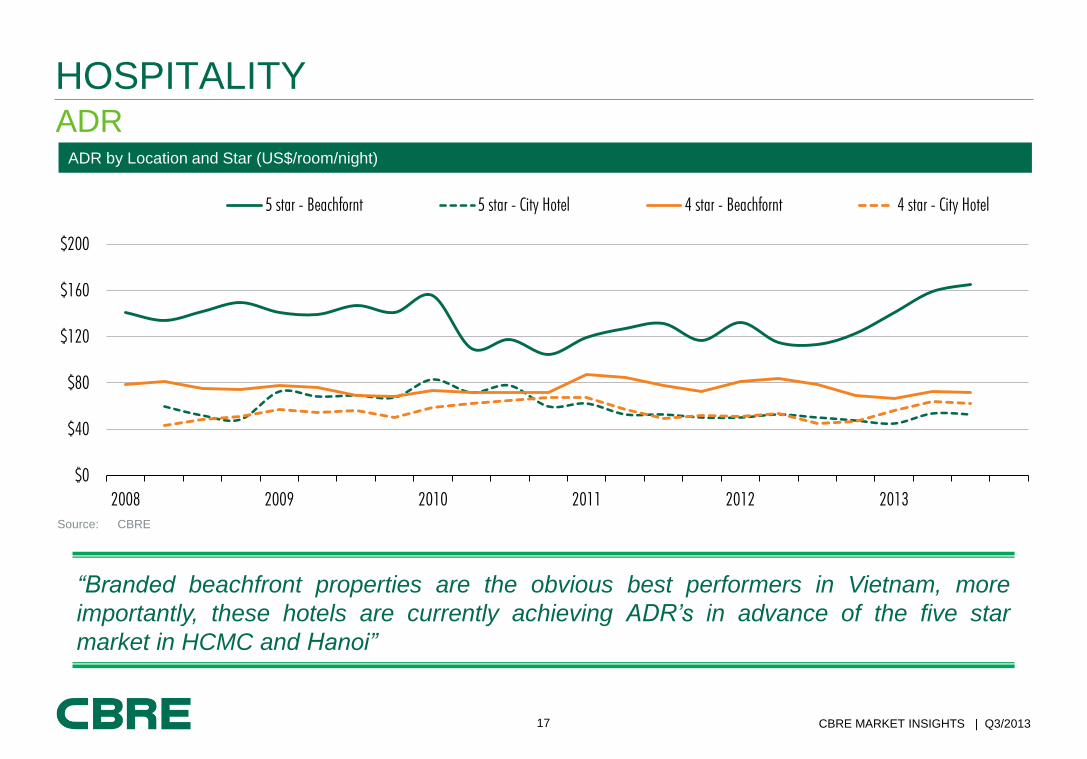

17 CBRE MARKET INSIGHTS | Q3/2013

ADR

HOSPITALITY

“Branded beachfront properties are the obvious best performers in Vietnam, more

importantly, these hotels are currently achieving ADR’s in advance of the five star

market in HCMC and Hanoi”

ADR by Location and Star (US$/room/night)

$0

$40

$80

$120

$160

$200

2008 2009 2010 2011 2012 2013

5 star - Beachfornt 5 star - City Hotel 4 star - Beachfornt 4 star - City Hotel

Source: CBRE

18 CBRE MARKET INSIGHTS | Q3/2013

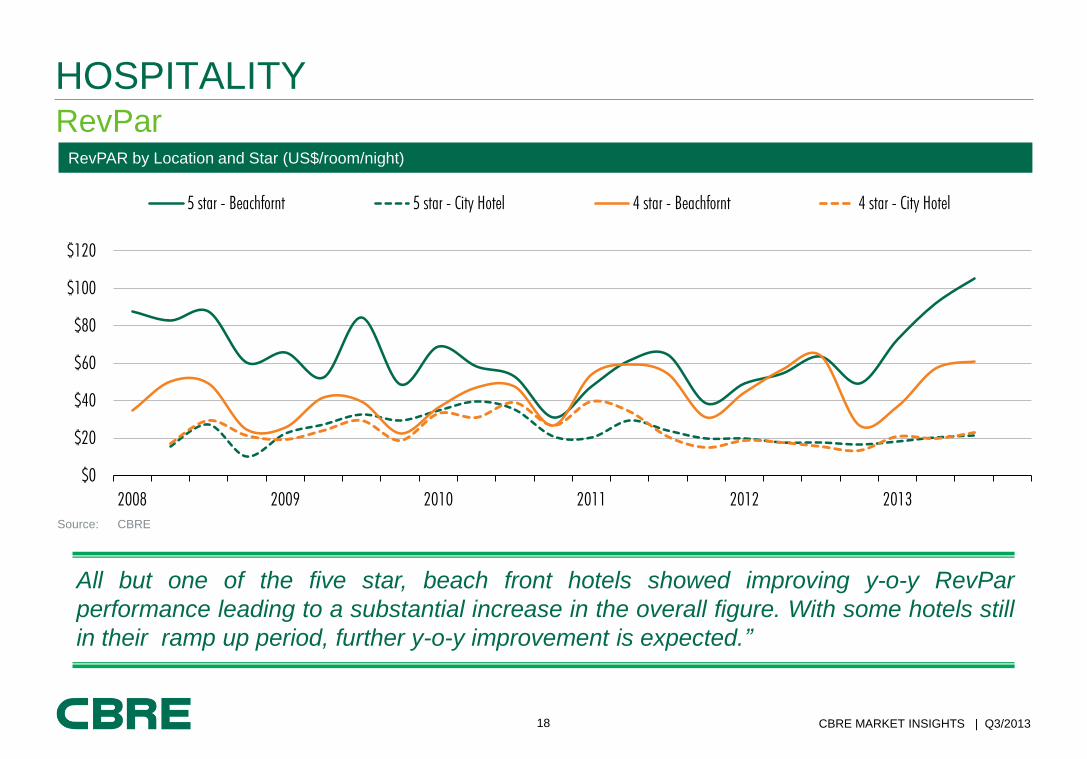

RevPar

HOSPITALITY

All but one of the five star, beach front hotels showed improving y-o-y RevPar

performance leading to a substantial increase in the overall figure. With some hotels still

in their ramp up period, further y-o-y improvement is expected.”

RevPAR by Location and Star (US$/room/night)

$0

$20

$40

$60

$80

$100

$120

2008 2009 2010 2011 2012 2013

5 star - Beachfornt 5 star - City Hotel 4 star - Beachfornt 4 star - City Hotel

Source: CBRE

19 CBRE MARKET INSIGHTS | Q3/2013

FUTURE SUPPLY

HOSPITALITY

Future Supply (rooms), Q3/2013

Future Supply, by Location (rooms), 2014-2016 Project under construction breakdown (rooms)

47%

53%

Under construction

Under planning/pending

45%

30%

11%

13% Beachfront - branded

Beachfront - self managed

City Hotel - branded

City Hotel - self managed

36%

45%

0%

19%Beachfront - branded

Beachfront - self managed

City Hotel - branded

City Hotel - self managed

Source: CBRE

“There are 4,000+ rooms planned

in the 3 – 5 star sector in Da Nang

(City & Beachfront); many of these

projects are delayed or calling for

investment and thus it is unlikely

additional supply will be much

less.”

20 CBRE MARKET INSIGHTS | Q3/2013

Further Growth Anticipated

OUTLOOK

Expanded flight schedule likely;

• Greater connectivity in to major hubs,

linkages to Thailand will prove beneficial;

• Multi-country visa for Vietnam, Cambodia,

Loas and Thailand, would help further

improve tourism arrivals;

• Chinese visitors will continue to prove

increasingly improtant to the area – the

gaming and golf facilities proving significant

pull factors;

The performance of branded beachfront

properties will see continued improvement as

new projects enter into a stabilised stage of

operation;

Supply pressures in the city will continue to

prohibit any performance improvements,

particularly for 3 star hotels;

RESIDENTIAL MARKET Condominium

22 CBRE MARKET INSIGHTS | Q3/2013

Q3 2013 Snapshot

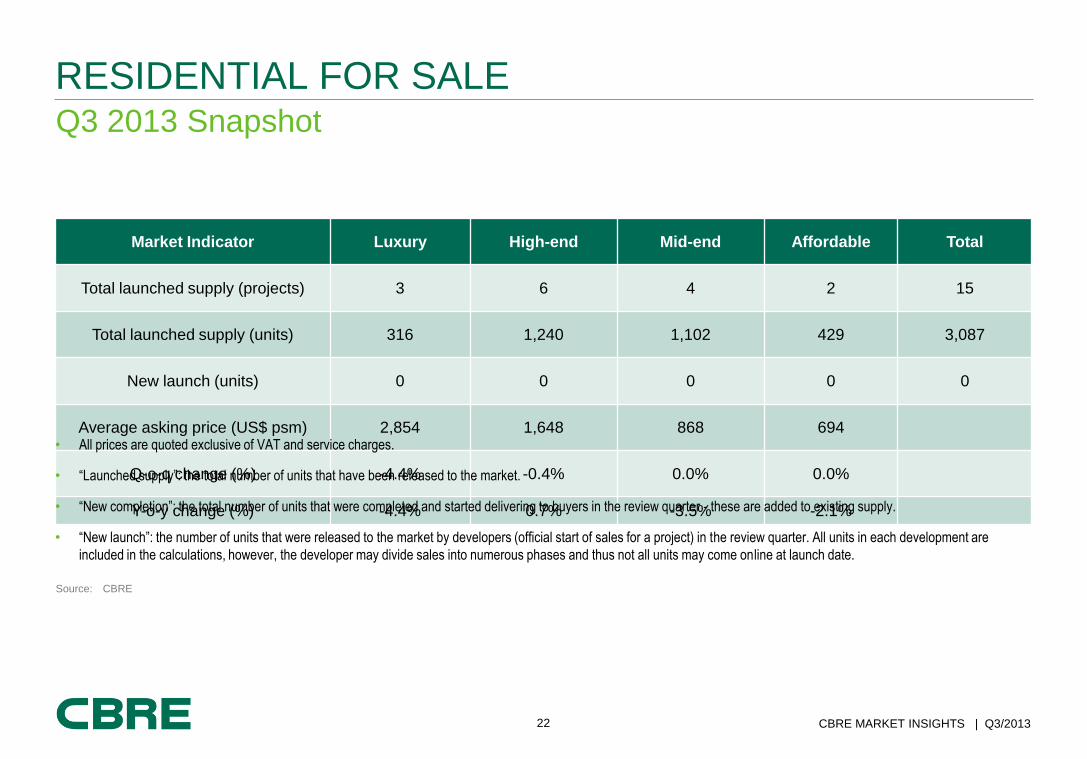

RESIDENTIAL FOR SALE

Market Indicator Luxury High-end Mid-end Affordable Total

Total launched supply (projects) 3 6 4 2 15

Total launched supply (units) 316 1,240 1,102 429 3,087

New launch (units) 0 0 0 0 0

Average asking price (US$ psm) 2,854 1,648 868 694

Q-o-q change (%) -4.4% -0.4% 0.0% 0.0%

Y-o-y change (%) -4.4% 0.7% -3.5% -2.1%

Source: CBRE

• All prices are quoted exclusive of VAT and service charges.

• “Launched supply”: the total number of units that have been released to the market.

• “New completion”: the total number of units that were completed and started delivering to buyers in the review quarter - these are added to existing supply.

• “New launch”: the number of units that were released to the market by developers (official start of sales for a project) in the review quarter. All units in each development are

included in the calculations, however, the developer may divide sales into numerous phases and thus not all units may come online at launch date.

23 CBRE MARKET INSIGHTS | Q3/2013

Highlights

CONDOMINIUM FOR SALES

• No new supply. The total supply remains at 3,087 apartments.

Supply

• Q3/2013, unsold stock accumulated to 1,469 units, a decrease of 6.0% q-o-q

• Six delayed projects made up 58% (854 units) of total unsold inventory.

• Positive sales activities recorded with sales volumes increasing in two consecutive quarters (Q2 and Q3). All sales made at completed or nearly completed projects

Sales activity

• Apart from Fusion Suites and OceanViews, construction of the other launched projects progressed very slowly during the third quarter. There is no sign of construction activities on 12 future pipeline projects during the quarter;

Construction work

0

400

800

1,200

1,600

2,000

New Launch Unsold

Inventory

Unsold stock from

Paused/delayed

Q1.2013 Q2.2013 Q3.2013

Unsold Inventory

Launch Supply Vs Completion

0

800

1,600

2,400

2009 2010 2011 2012 Q3/2013Q1/13 Q2/13 Q3/13

Launch Supply Completion

24 CBRE MARKET INSIGHTS | Q3/2013

Market performance

CONDOMINIUM FOR SALES

Sales Volume/Pricing by Quarter Sales Volume by Grade

Asking Price by Grade (US$/m2)

Source: CBRE

Promotions at luxury projects have helped to increase

performance, whilst a notable affordable project

seems to have lost momentum as it has moved

through its sales cycle.

The headline asking price of mid-end and affordable

developments remain unchanged. Developers offered

discounts and promotions instead of officially reducing

prices.

1,250

1,300

1,350

1,400

1,450

1,500

1,550

1,600

0

40

80

120

160

200

240

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013

Sale

s volu

mes

Avera

ge p

rice

(U

S$/s

m)

0

700

1,400

2,100

2,800

3,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013

Luxury High-end Mid-end Affordable

34.9% 27.6%

7.2%

61.9%56.3%

4.3%

0%

20%

40%

60%

80%

100%

the 9st months

of 2012

the 9st months

of 2013

Affordable Mid-end High-end Luxury

25 CBRE MARKET INSIGHTS | Q3/2013

Highlights

SECOND HOME VILLAS

• No launches recorded in Q3/2013.

Supply

• Unsold stock was approximately 400 units, a decline of 5.3% y-o-y .

• Sales in the period were noted at Hyatt Regency, the Dunes and Ocean Villas

Sale activity

• Apart from Vietstar Non Nuoc resort and the Empire (hotel component), construction progress appeared limited throughout Q3/2013

Construction work

26 CBRE MARKET INSIGHTS | Q3/2013

Market performance

SECOND HOME VILLAS

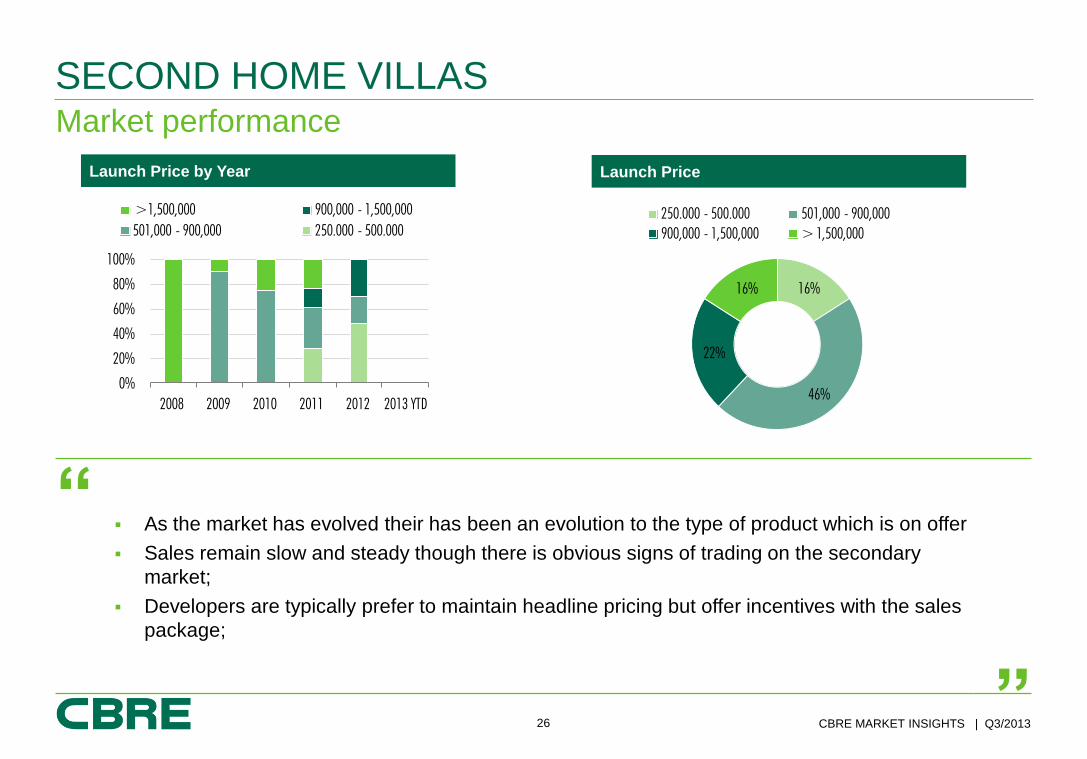

“ As the market has evolved their has been an evolution to the type of product which is on offer

Sales remain slow and steady though there is obvious signs of trading on the secondary

market;

Developers are typically prefer to maintain headline pricing but offer incentives with the sales

package;

”

Launch Price

16%

46%

22%

16%

250.000 - 500.000 501,000 - 900,000

900,000 - 1,500,000 > 1,500,000

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 YTD

>1,500,000 900,000 - 1,500,000

501,000 - 900,000 250.000 - 500.000

Launch Price by Year

27 CBRE MARKET INSIGHTS | Q3/2013

In the city purchases were mostly made in price range of approximately US$100,000 per unit due to low

investment cost and more potential for buy-to-let.

Condotel concepts which applied the guaranteed return program appears to have captured buyers ‘attention –

notable examples include OceanViews and Fusion Suites, we expect this trend to grow.

Location, price and construction progress remain the central consideration for buyers – the ability to lease units is

also becoming more important.

No significant new launches are expected in the next 2 quarters.

Promotional packages, as oppose to out and out price decreases remain the likely options for developers hoping

to further stimulate the market.

Outlook

RESIDENTIAL MARKET

Azura

339 Tran Hung

Dao Str, Son Tra

Dist.

@$1,575/m2

Da Nang

Lakeside

Ham Nghi Str,

Hai Chau Dist.

@$590/m2

Da Nang Plaza

Nguyen Du Str,

Hai Chau Dist.

@$1,080/m2

Harmony Tower

Pham Van Dong

Str, Son Tra Dist.

@$1,100/m2

Hyatt Regency

Truong Sa Str,

Ngu Hanh Son

Dist.

@$3,716/m2

Fusion Suites

Hoang Sa Str,

Son Tra Dist.

@$1,768/m2

Projects have sale activity in quarter

COMMERCIAL MARKET Office

29 CBRE MARKET INSIGHTS | Q3/2013

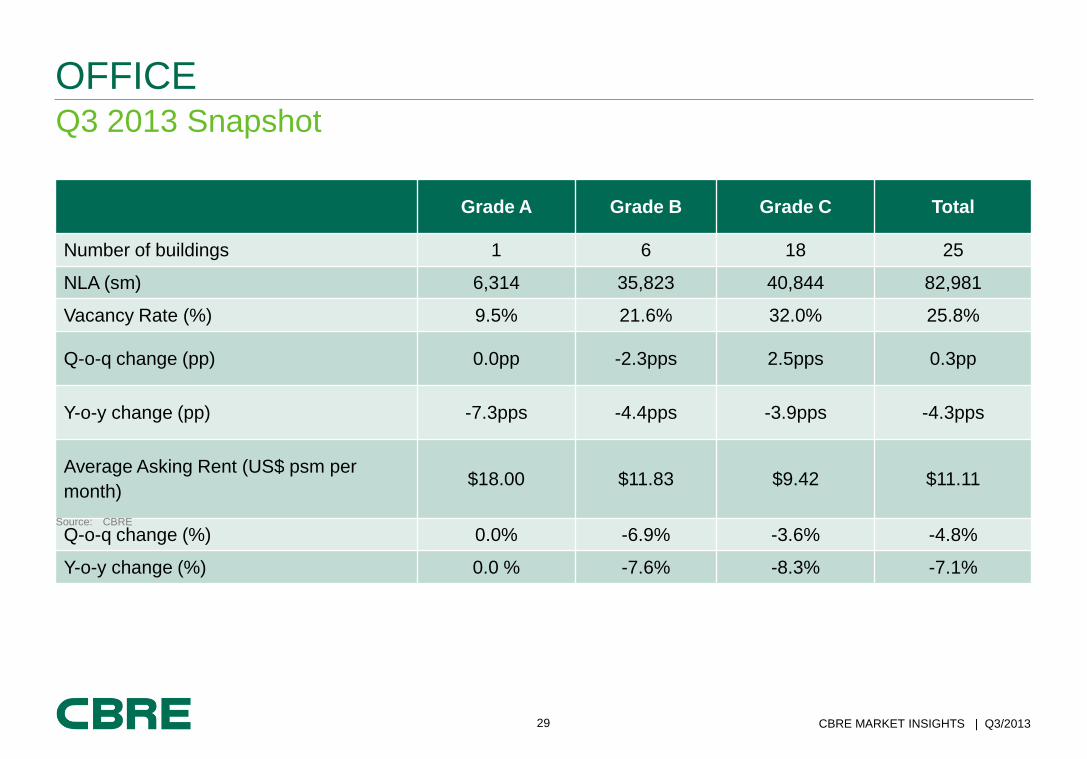

Q3 2013 Snapshot

OFFICE

Grade A Grade B Grade C Total

Number of buildings 1 6 18 25

NLA (sm) 6,314 35,823 40,844 82,981

Vacancy Rate (%) 9.5% 21.6% 32.0% 25.8%

Q-o-q change (pp) 0.0pp -2.3pps 2.5pps 0.3pp

Y-o-y change (pp) -7.3pps -4.4pps -3.9pps -4.3pps

Average Asking Rent (US$ psm per

month) $18.00 $11.83 $9.42 $11.11

Q-o-q change (%) 0.0% -6.9% -3.6% -4.8%

Y-o-y change (%) 0.0 % -7.6% -8.3% -7.1%

Source: CBRE

30 CBRE MARKET INSIGHTS | Q3/2013

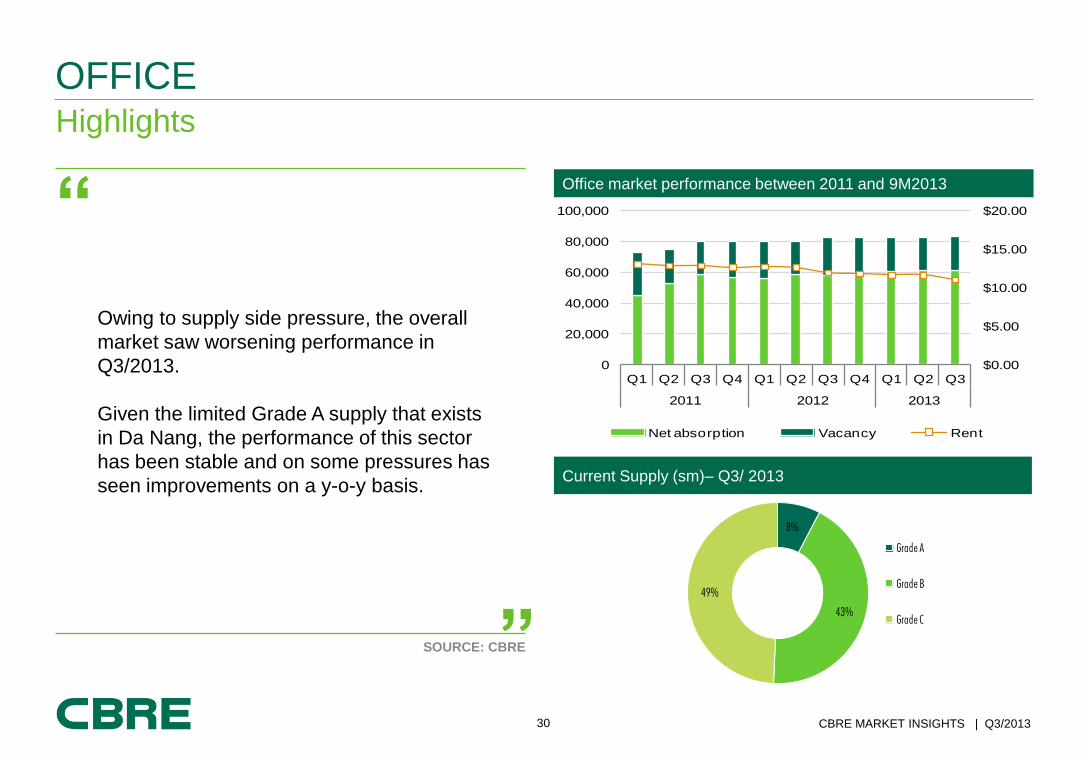

Highlights

OFFICE

“

Owing to supply side pressure, the overall

market saw worsening performance in

Q3/2013.

Given the limited Grade A supply that exists

in Da Nang, the performance of this sector

has been stable and on some pressures has

seen improvements on a y-o-y basis.

” SOURCE: CBRE

Current Supply (sm)– Q3/ 2013

Office market performance between 2011 and 9M2013

$0.00

$5.00

$10.00

$15.00

$20.00

0

20,000

40,000

60,000

80,000

100,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013

Net absorption Vacancy Rent

8%

43%

49%

Grade A

Grade B

Grade C

31 CBRE MARKET INSIGHTS | Q3/2013

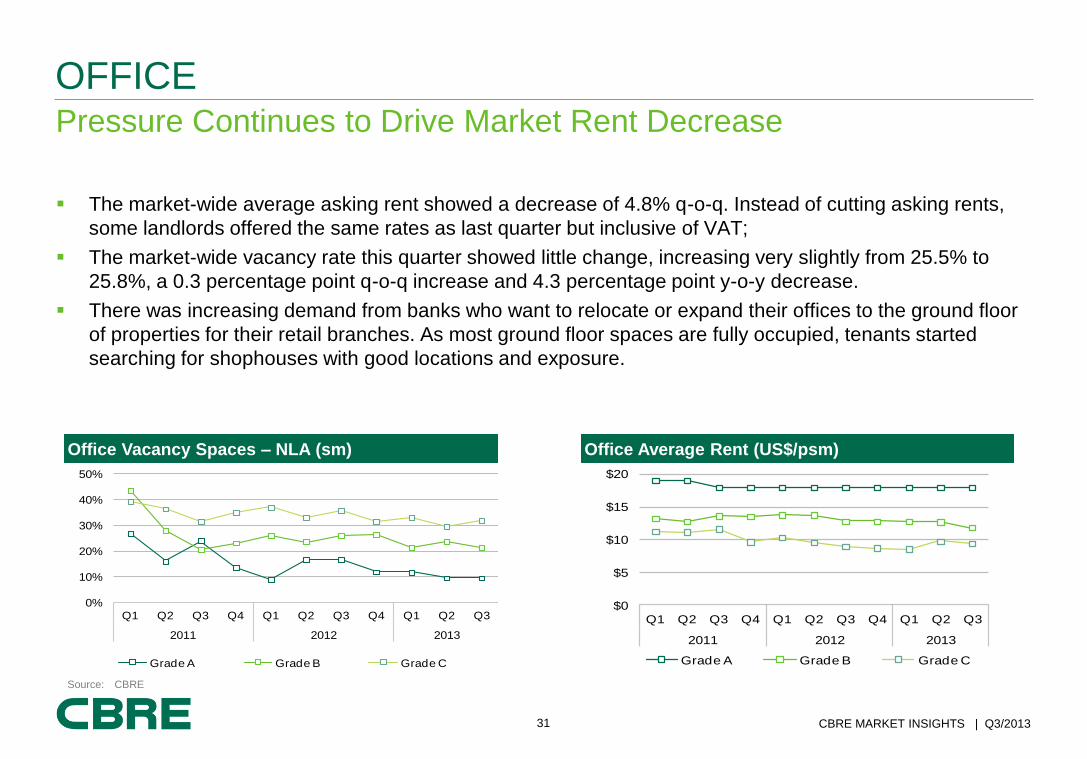

The market-wide average asking rent showed a decrease of 4.8% q-o-q. Instead of cutting asking rents,

some landlords offered the same rates as last quarter but inclusive of VAT;

The market-wide vacancy rate this quarter showed little change, increasing very slightly from 25.5% to

25.8%, a 0.3 percentage point q-o-q increase and 4.3 percentage point y-o-y decrease.

There was increasing demand from banks who want to relocate or expand their offices to the ground floor

of properties for their retail branches. As most ground floor spaces are fully occupied, tenants started

searching for shophouses with good locations and exposure.

Pressure Continues to Drive Market Rent Decrease

OFFICE

Office Vacancy Spaces – NLA (sm) Office Average Rent (US$/psm)

$0

$5

$10

$15

$20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013

Grade A Grade B Grade C

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013

Grade A Grade B Grade C

Source: CBRE

32 CBRE MARKET INSIGHTS | Q3/2013

Outlook

OFFICE

VIETTIN BANK

Construction at 17th floor –

August 2013 GFA 27,611 sqm DA NANG POST OFFICE

Fitting out– August 2013 GFA

14,449 sqm

New supply in the form of

VietinBank Building and Da

Nang office building is

nearing completion and will

certainly come to market in

2014;

New buildings will be in the

Grade B sector and are not

comparable with the only

Grade A property currently

within the market;

New buildings are expected

to attract Vietnamese

tenants;

2014 will remain a tenants

market.

Future projects will put the market under further pressure

CBRE Vietnam – Research & Consulting – Da Nang office T +84.511.2222.111

F +84.511.2222.100

CBRE QUARTERLY REPORT

Available NOW… CBRE offers better-priced sector reports with longer

historical data and In-depth analysis