CYPRUS – LITHUANIA TAX STRUCTURING Alecos Papalexandrou Tax Partner Lithuania, June 2012.

20

CYPRUS – LITHUANIA TAX STRUCTURING Alecos Papalexandrou Tax Partner Lithuania, June 2012

-

Upload

paula-terry -

Category

Documents

-

view

217 -

download

0

Transcript of CYPRUS – LITHUANIA TAX STRUCTURING Alecos Papalexandrou Tax Partner Lithuania, June 2012.

CYPRUS – LITHUANIATAX STRUCTURING

Alecos Papalexandrou

Tax Partner

Lithuania, June 2012

Holding Company - Inbound Investment

Plan

• Establish Cyprus company to hold operating subsidiary in Lithuania for dividend stream income

Benefits

• Eliminate withholding tax in Lithuania on dividend payment to Cyprus

• Participation exemption on dividend income – No tax in Cyprus

• No withholding tax on dividends to parent whether EU or Non-EU

• No CFC rules in Cyprus

Parent Non-EU

Lithuania Opco

CyprusHoldco

0% withholding tax on dividends

EU Parent – Subsidiary Directive

Parent EU \ ЕС

0% withholding tax on dividends

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 2

Holding Company - Inbound Investment

• Investor from a country with no DTT with Lithuania

• Investment through Cyprus

• Dividends received by Cyprus holding Co exempt from tax (subject to conditions)

• No withholding taxes on payments out of Cyprus

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 3

Treaty Subsidiary

Treaty Subsidiary

LithuanianInvestor Co Lithuanian

Investor Co

Holding Company - Outbound investment

Plan

• Lithuanian investor establishes Cyprus company to hold various EU and non-EU operating subsidiaries for dividend stream income

Benefits

• Access to EU directives and DTTs of Cyprus in relation to holding EU and non-EU subsidiaries – No or low withholding tax on dividend (for example 5% in Russia, 0% in Ukraine)

• Full participation exemption on dividend income - No tax in Cyprus

• No withholding tax on dividends to Lithuanian parent

• No CFC rules in Cyprus

CyprusHoldco CyprusHoldco

EU Subsidiary

EU Subsidiary

Dividend payment 0% withholding tax

Dividend payment0% or low withholding tax

Dividend income 0% tax

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 4

Holding Company - Outbound investment

Plan

• Lithuanian investor establishes Cyprus company to hold various operating subsidiaries for dividend stream income

Benefits

• Access to favorable treaties

– No withholding tax on dividend from Ukraine

– Withholding Tax in accordance with Treaty

• Full participation exemption on dividend income - No tax in Cyprus

• No withholding tax on dividends to parent

• No CFC rules in Cyprus

LithuanianInvestor

CyprusHoldco

Dividend payment 0% withholding tax

Dividend payment0% withholding tax

Dividend income 0% tax

UkrainianOpco

UkrainianOpco

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 5

Holding Company with Foreign PE

In Cyprus :

1. Profits from PE abroad exempt provided:• Active income>50% or• Tax burden >5%

2. Losses of PE set off against Cyprus Co’s other income (but recapture rule)

3. Profits in PE country exempt if they relate to construction and/or assembly activities lasting within the periods specified in the Cyprus DTT Network.

Example:

Austria <24 months

Romania <12 months

RussiaUkraine

<12 months<24 months

Other Eastern

European Countries <12 months

Cyprus Co Cyprus Co

Investor Investor

Foreign PE Foreign PE

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 6

Financing Company - Inbound

• Interest deductible in operating country (Lithuania)

• No WHT in Lithuania based on EU Interest & Royalties Directive

• Small margin taxable in Cyprus at 10%

• No withholding taxes on payments out of Cyprus

Interest Payable

Interest Receivable

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 7

Finance Company - Outbound investment

Plan

• Lithuanian investor establishes Cyprus company to be the group finance company of EU and non – EU operations.

• Capitalisation with equity

Benefits

• Tax on profit margin 10%

• Access to EU interest directive and DTT network of Cyprus

– No or low withholding tax on interest

• Interest deductibility in paying company

• No WHT on dividends paid from Cyprus

Cyprus FinancingCompany

LithuanianInvestor

EU / non-EU

Opco

Dividend payment 0% withholding tax

Interest payment0% or low withholding tax

Profit Margin - 10% tax

Cyprus – Lithuania: Tax restructuring © 2012 Deloitte Limited 8

Financing Company - Outbound

• Profits reduced in operating company

• Low or no WHT in operating company based on DTT or EU Directive

• Small margin taxable in Cyprus at 10%

• No withholding taxes on payments out of Cyprus to Lithuania

Interest Payable

Interest Receivable

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 9

Financing Company

Margins on Loans – back to back structures

Transfer Pricing Considerations –

Acceptable indicative profit margins where low financing risk retained in Cyprus:

• Up to EUR€50m 0.35%

• From EUR€50m - EUR€200m 0.25%

• Above EUR€200m 0.125%

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 10

Intellectual Property Rights

Royalty Company (Inbound):

• Royalty premiums deductible in Lithuania• No WHT in Lithuania based on EU Interest &

Royalties Directive (subject to conditions)• Small margin taxed at 10% in Cyprus• No withholding taxes on payments out of

Cyprus

• As from 1/1/2012: cost of acquisition of IP can be

amortised over 5 years 80% of the profits from royalties,

including the profit from disposal of the IP, exempt from 10% corporation tax in Cyprus

Royalty Payable

Royalty Receivable

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 11

Cyprus IP Co.

Cyprus IP Co.

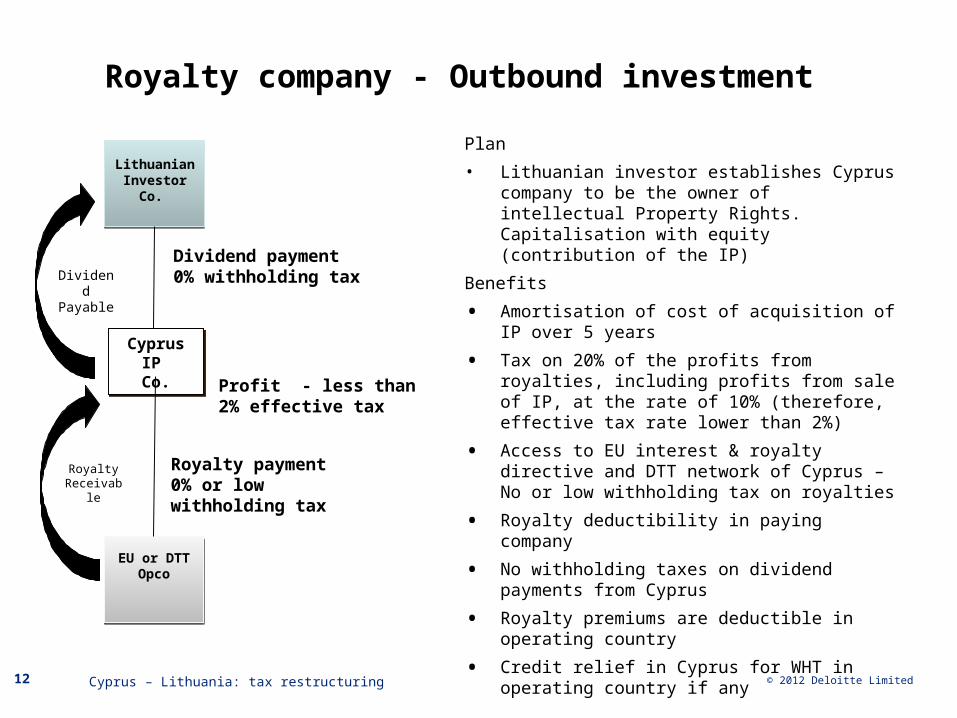

Royalty company - Outbound investment

LithuanianInvestor Co.

EU or DTTOpco

Dividend payment 0% withholding tax

Royalty payment0% or low withholding tax

Profit - less than 2% effective tax

Dividend Payable

Royalty Receivable

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 12

Plan

• Lithuanian investor establishes Cyprus company to be the owner of intellectual Property Rights. Capitalisation with equity (contribution of the IP)

Benefits

• Amortisation of cost of acquisition of IP over 5 years

• Tax on 20% of the profits from royalties, including profits from sale of IP, at the rate of 10% (therefore, effective tax rate lower than 2%)

• Access to EU interest & royalty directive and DTT network of Cyprus – No or low withholding tax on royalties

• Royalty deductibility in paying company

• No withholding taxes on dividend payments from Cyprus

• Royalty premiums are deductible in operating country

• Credit relief in Cyprus for WHT in operating country if any

Trading in Securities

• Profit is exempt from tax

• Use of Double Tax Treaties

• No withholding tax on payments out of Cyprus

• Result = 0% tax in Cyprus

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 13

Non Resident Trading Company

• Managed and controlled outside Cyprus

• Exempt from tax in Cyprus

• Non resident Cyprus registered company

• Use of EU VAT number and reputation

• Result = 0% tax in Cyprus

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 14

Employment Company

• Cyprus Company employs staff

• Charges at cost plus

• Profits taxable in Cyprus at 10%

• Profits reduced in operating country

• Employee costs reduced as employees pay less tax and S.I. Contributions *

• Employees exempt from tax in Cyprus

* Depends on nationality of employees and rules of operating country

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 15

Cyprus International Trusts

Plan• Set up a trust under the Cyprus International Trusts

Law of 2012

Benefits• Exempt from any taxation in Cyprus

• Exempt from any Capital Gains and Inheritance Tax

• Protection of Property

• Confidentiality

• Trading activities through the set up of a company owned by the trust

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 16

International Collective Investment Schemes

• An ICIS can take one of the following legal forms:

– Fixed Capital Company;

– Variable Capital Company;

– Unit Trust Scheme;

– Investment Limited Partnership.

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 17

An example:

OverseasInvestments

OverseasInvestments

Cyprus HoldCo Cyprus HoldCo

ICIS Partnership ICIS Partnership

General Partner(CyprusCo)

General Partner(CyprusCo)

Limited Partners Limited Partners

Lithuanian ParentLithuanian Parent

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 18

Thank you!

For more information you may contact:

Alecos PapalexandrouTel: + 357 25 868686E-mail: [email protected]

Cyprus – Lithuania: tax restructuring © 2012 Deloitte Limited 19