Customs and International Trade Presentation by: Peter Nganga … · Customs and International...

22

Customs and International Trade Presentation by: Peter Nganga Chief Manager, Licensing, C&BC, KRA Friday, 11 th May 2018

-

Upload

nguyenhuong -

Category

Documents

-

view

232 -

download

1

Transcript of Customs and International Trade Presentation by: Peter Nganga … · Customs and International...

Customs and International Trade

Presentation by:Peter Nganga

Chief Manager, Licensing, C&BC, KRAFriday, 11th May 2018

Session Objectives

Have a Background Knowledge on Customs & Border operations

Appreciate the role of Customs & Border Control

Understand the legal framework within which customs & Border control operate.

Define and apply customs valuation and its concepts

Be able to name and use the six different methods of Customs valuation

Background

Established by an Act of Parliament in 1978. Previously Known as Customs & Excise Department

Adopted EACCMA, 2004 in compliance with the protocol on the establishment of the EAC Customs Union.

Before the EAC Act was put in place, the Customs & Excise Act CAP 472 was in operation.

Customs and Border Control Mandate

Collection of revenue Trade facilitation (AEO,PCA, Risk Mgt) Collection and capturing of trade statistics Ensuring boarder security. Enforce adherence to international treaties and

conventions

Legal References for Customs Operations

East Africa Community Customs Management Act, 2004 (EACCMA)

East Africa Community Customs Management Regulations (2010)

Common External Tariff, Rules of Origin HB VAT Act cap 476 Customs and excise act cap 472 Conventions, protocols, Treaties that Kenya has

signed. Any Other Law in force within Kenya

Customs Valuation

Valueworth, desirability; purchasing power; equivalent of a thing … which may be substituted or exchanged for a thingvaluationProcedure applied to determine the value of goods for the purpose of levying ad valorem customs duties.

Customs Valuation Methods

Six Methods of ValuationThere are six methods that are used to determine customs value depending on market realities. The methods must be applied in sequence are listed below.i. Transaction Value;ii. The transaction value of identical goods;iii. The transaction Value of similar good;iv. The deductive value method;v. The computed Value method;vi. The fallback method.

Method 1Transaction Value

This is the ‘basis of Customs Value’

`Transaction Value’ is the price actually paid or payable for the goods when sold for export to the country of importation adjusted in accordance with the provisions of paragraph 9 of 4th schedule, EACCMA 2004.

Paragraph 9 (Exclusions & Inclusions to TV)

Transaction Value….

Evidences Of Sale✓ Commercial Invoices,✓ Sales Contract,✓ Bank Remittances Slips,✓ Export Price List.

Four Conditions for Transaction value

I. No restrictions as to goods by the buyer that can affect the value of the goods;

II. Price of the goods is not subject to some condition or consideration for which a value cannot be determined

III. No part of the proceeds of the goods will accrue directly or indirectly to the seller unless adjusted.

IV. The buyer & seller are not related, unless the relationship did not influence the price.

Transaction value…

If the price for the imported goods is affected by factors external to the goods themselves then the use of transaction value is generally precludedLeading to application of method 2

Method 2 Transaction v. of Identical goods

‘Identical Goods’ are goods which are the same in all respects, including physical characteristics, quality and reputation. Minor differences in appearance would not preclude goods otherwise conforming to the definition from being regarded as identical.

Minor Differences In Appearance:- Colour & size- Pattern

TV of Identical goods…General requirements

• The goods must be identical to the imported goods;• They must be produced in the same country as the

goods being valued;• They must have been exported at or about the same

time as the goods being valued; • Same quantity & commercial level as the goods

being valued, or proper adjustments to be made;• Same Producer;

Method 3TV of Similar goods

`Similar Goods’ are goods which are not alike in all respects, have like characteristics and like component materials which enable them to perform the same functions and to be commercially interchangeable.SpecificationsSame Function & Use:

- same purpose- performing same function with same result

Commercially Interchangeable:- being accepted as a substitute

TV of Similar goods…General requirements

Similar quantity or proper adjustments should be undertaken;

Same commercial level or proper adjustment to be undertaken

The goods must have been exported on or about the same time.

The goods produced by another producer in the same country can be used incase there are no goods produced by the same producer;

Method 4Deductive value

`Deductive value’ is the price at which the imported identical or similar goods are sold to unrelated buyers in the condition as imported in the greatest aggregate quantity in the country of importation. Specifications Of Deductive Value• Only sales made in the country of importation

will be considered, • Those sales must be for domestic consumption

and not for export

Deductive value….

Specifications..• Usual costs of insurance incurred within the

country of importation.• Customs duties & other taxes payable in the

country of importation.

Deductive value….

Deductions…✓ Commissions or profit & general expenses in

connection with sales of imported goods of the same kind;

✓ Costs of transport within the country of importation

✓ Customs duties & other taxes payable in the country of importation.

✓ Insurance within country of importation

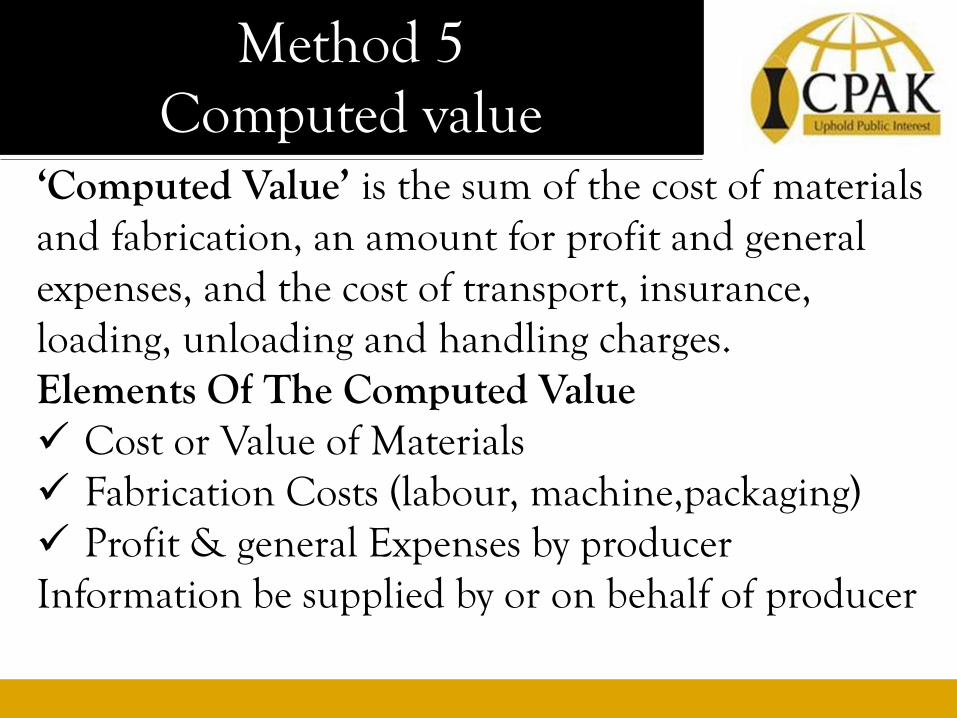

Method 5Computed value

‘Computed Value’ is the sum of the cost of materials and fabrication, an amount for profit and general expenses, and the cost of transport, insurance, loading, unloading and handling charges.Elements Of The Computed Value✓ Cost or Value of Materials✓ Fabrication Costs (labour, machine,packaging)✓ Profit & general Expenses by producerInformation be supplied by or on behalf of producer

Method 6Fall Back Method

Customs value to be determined using reasonable means consistent with the principles and general provisions of the fourth Schedule and on the basis of data available in the Partner state.✓ Customs values determined under this method

should, to the greatest extent possible, be based on previously determined customs values.

✓ Methods 1 to 5 should be applied flexibly to determine customs values under this method for imported goods.

Fall Back Method..

Flexible Approaches✓ 90 days for comparison can be extended to 180

days (under methods 2,3 & 4).✓ Country of production for identical or similar

goods can be different.✓ Deductive values for goods sold after further

processing can be applied. Method 1 through to 5 must be applied in the hierarchical order under Fallback Method.

Discussions