Current Monetary Order and its Potential Reforms Money vs. Fixed Money • The traditional view...

24

Current Monetary Order and its Potential Reforms Mojmír Hampl CNB Vice-Governor Corvinus University, Budapest, November 24, 2017

Transcript of Current Monetary Order and its Potential Reforms Money vs. Fixed Money • The traditional view...

Current Monetary Order and its

Potential Reforms

Mojmír Hampl CNB Vice-Governor

Corvinus University, Budapest, November 24, 2017

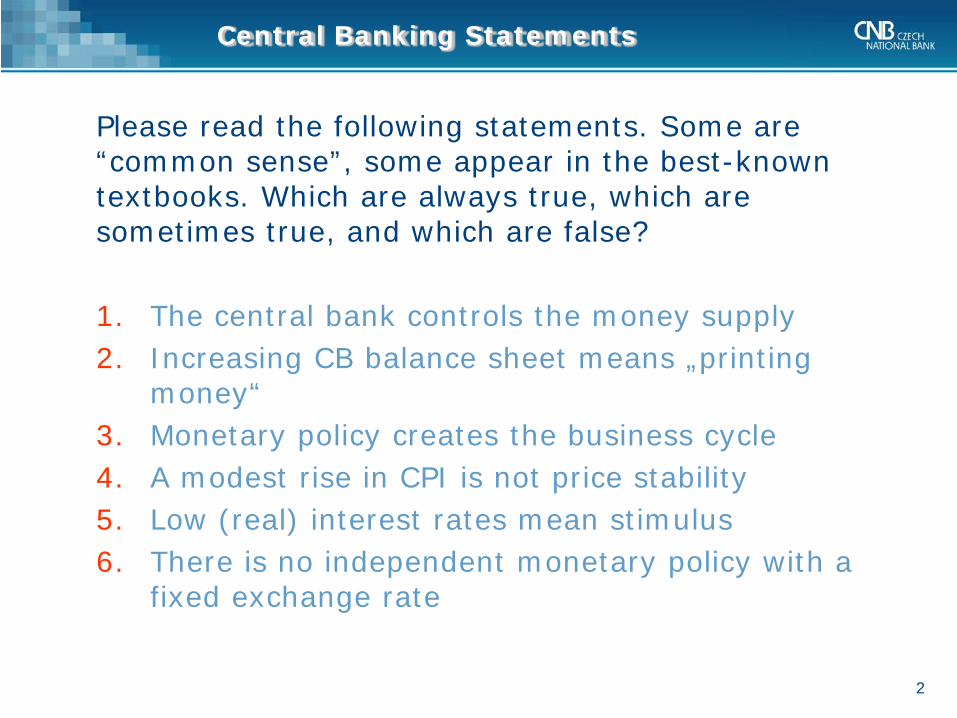

Central Banking Statements

Please read the following statements. Some are “common sense”, some appear in the best-known textbooks. Which are always true, which are sometimes true, and which are false? 1. The central bank controls the money supply 2. Increasing CB balance sheet means „printing

money“ 3. Monetary policy creates the business cycle 4. A modest rise in CPI is not price stability 5. Low (real) interest rates mean stimulus 6. There is no independent monetary policy with a

fixed exchange rate

2

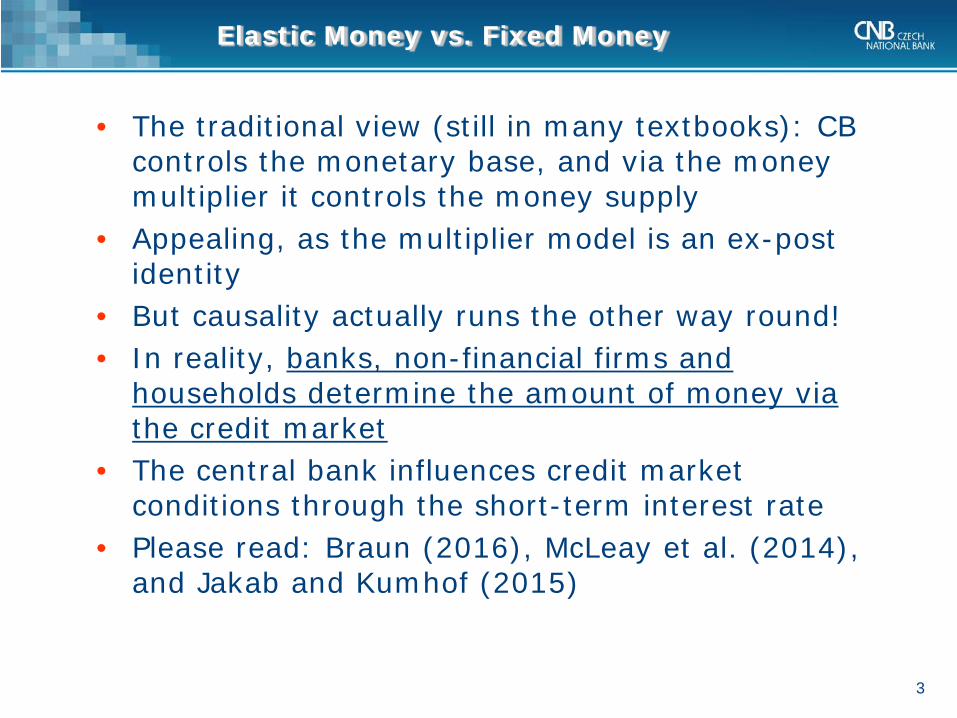

Elastic Money vs. Fixed Money

• The traditional view (still in many textbooks): CB controls the monetary base, and via the money multiplier it controls the money supply

• Appealing, as the multiplier model is an ex-post identity

• But causality actually runs the other way round! • In reality, banks, non-financial firms and

households determine the amount of money via the credit market

• The central bank influences credit market conditions through the short-term interest rate

• Please read: Braun (2016), McLeay et al. (2014), and Jakab and Kumhof (2015)

3

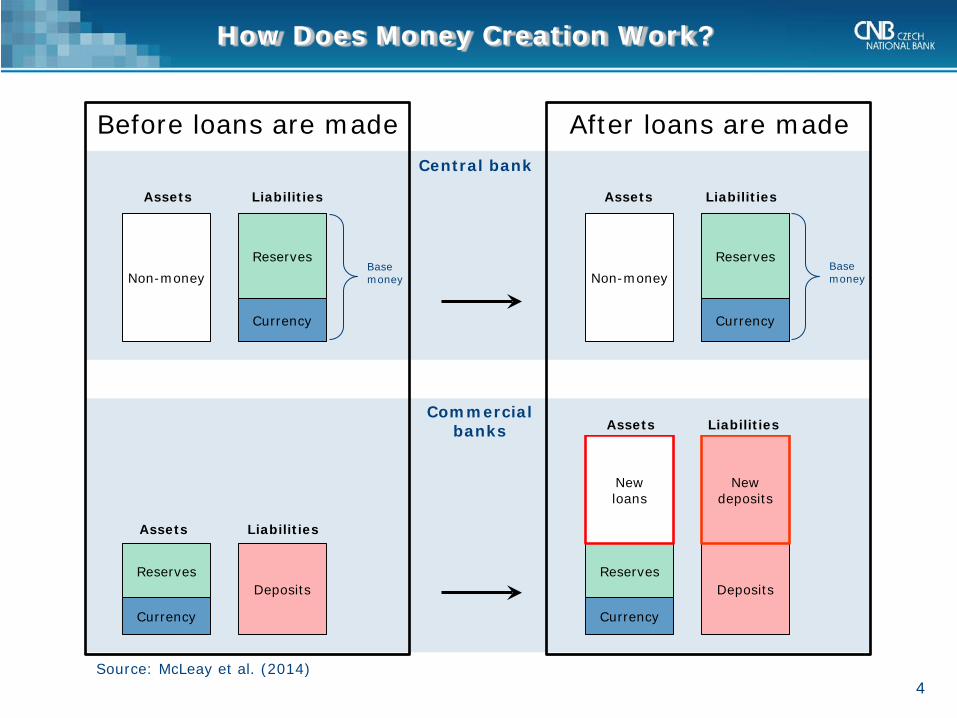

How Does Money Creation Work?

4 Source: McLeay et al. (2014)

Non-money

Currency

Non-money

Currency

Reserves Reserves Base money

Assets Liabilities Assets Liabilities

Before loans are made After loans are made Central bank

Currency

Deposits

Currency

Deposits Reserves Reserves

New loans

New deposits

Commercial banks

Base money

Assets Liabilities

Assets Liabilities

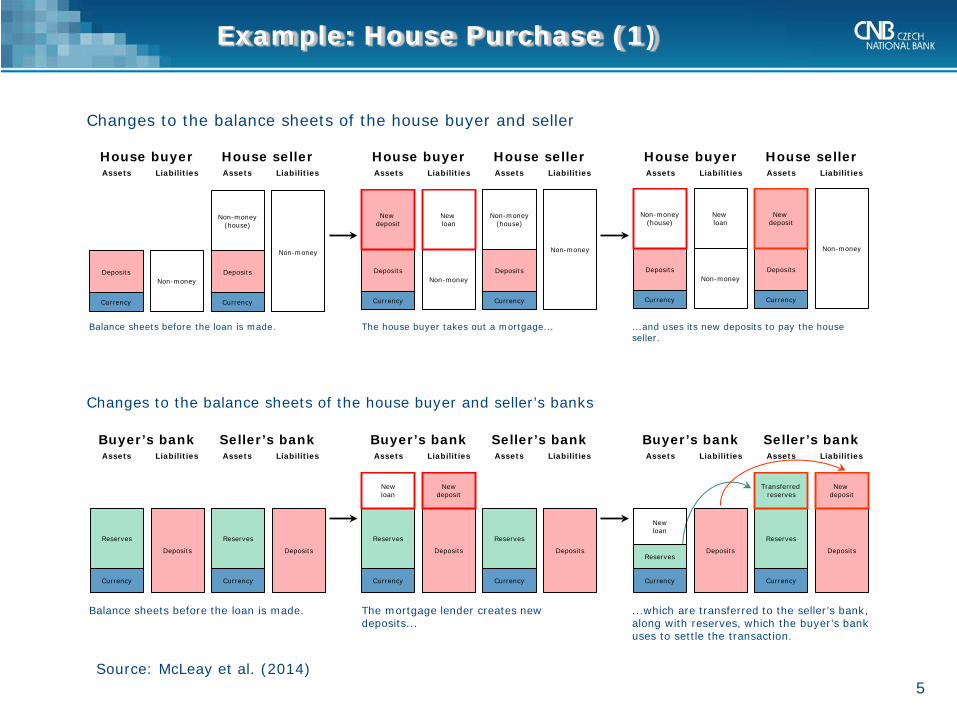

Example: House Purchase (1)

5 Source: McLeay et al. (2014)

Changes to the balance sheets of the house buyer and seller’s banks

Buyer’s bank Seller’s bank Buyer’s bank Seller’s bank Buyer’s bank Seller’s bank Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities

Balance sheets before the loan is made. The mortgage lender creates new deposits...

...which are transferred to the seller’s bank, along with reserves, which the buyer’s bank uses to settle the transaction.

Currency

Deposits

Currency

Deposits

Reserves Reserves

Currency

Deposits

Currency

Deposits

Reserves Reserves

New loan

New deposit

Currency

Deposits

Currency

Deposits Reserves

Reserves

New loan

Transferred reserves

New deposit

Changes to the balance sheets of the house buyer and seller

House buyer House seller House buyer House seller House buyer House seller Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities Assets Liabilities

Balance sheets before the loan is made. The house buyer takes out a mortgage... ...and uses its new deposits to pay the house seller.

Currency

Non-money

Currency

Non-money

Deposits Deposits

New deposit

New loan

Non-money (house)

Currency

Non-money

Currency

Non-money

Deposits Deposits

Non-money (house)

New loan

New deposit

Currency

Non-money

Currency

Non-money

Deposits Deposits

Non-money (house)

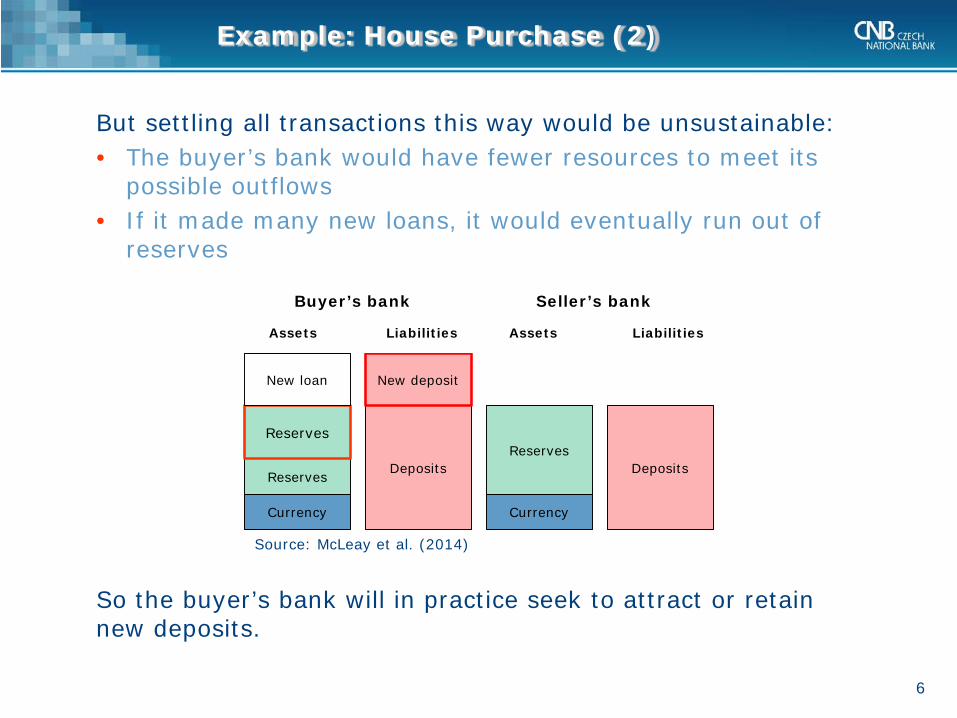

Example: House Purchase (2)

But settling all transactions this way would be unsustainable: • The buyer’s bank would have fewer resources to meet its

possible outflows • If it made many new loans, it would eventually run out of

reserves

So the buyer’s bank will in practice seek to attract or retain new deposits.

6

Currency

Deposits

Currency

Deposits Reserves

Reserves Reserves

New loan New deposit

Buyer’s bank Seller’s bank

Assets Liabilities Assets Liabilities

Source: McLeay et al. (2014)

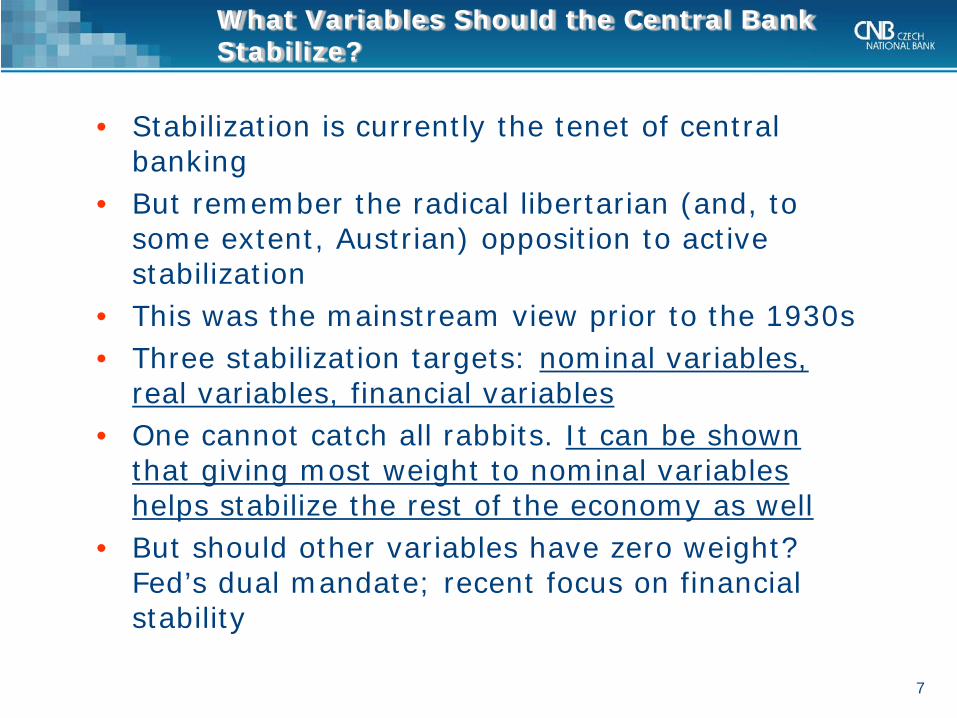

What Variables Should the Central Bank Stabilize?

• Stabilization is currently the tenet of central banking

• But remember the radical libertarian (and, to some extent, Austrian) opposition to active stabilization

• This was the mainstream view prior to the 1930s • Three stabilization targets: nominal variables,

real variables, financial variables • One cannot catch all rabbits. It can be shown

that giving most weight to nominal variables helps stabilize the rest of the economy as well

• But should other variables have zero weight? Fed’s dual mandate; recent focus on financial stability

7

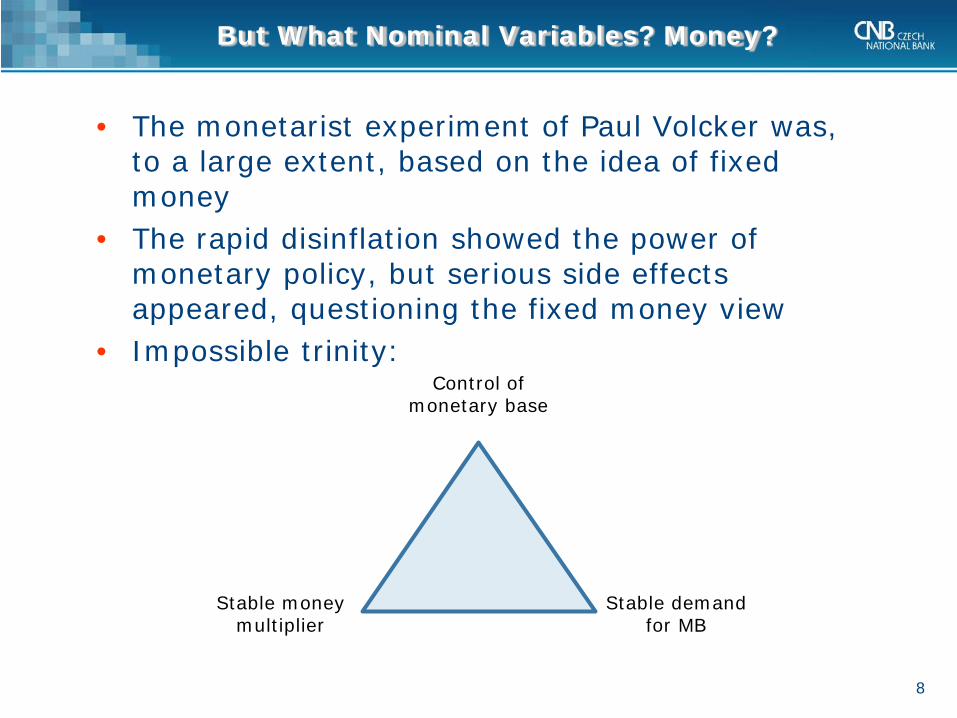

But What Nominal Variables? Money?

• The monetarist experiment of Paul Volcker was, to a large extent, based on the idea of fixed money

• The rapid disinflation showed the power of monetary policy, but serious side effects appeared, questioning the fixed money view

• Impossible trinity:

8

Control of monetary base

Stable demand for MB

Stable money multiplier

“New Monetarists” in “Old Central Banks”

• It turns out that the old monetarist goal (price stability) is best achieved via inflation targeting

• Two crucial building blocks of modern monetary policy: rational expectations and rigidities (or rational inattention; Sims, 2003)

• Rational expectations imply long-term neutrality of monetary policy (although see Aghion et al., 2012)

• Rigidities imply short-term effectiveness in affecting real variables, such as GDP and employment

• Inflation targeting anchors expectations: inflation is more palpable to households than money supply

9

Inflation Targeting: Why 2%?

• Most central banks in developed countries define a 2% increase in CPI as price stability

• The reason is that CPI overstates inflation – it doesn’t account for the increasing quality of goods, the substitution effect and the outlet bias when relative prices change (Gordon, 2006)

• A positive target on CPI growth also creates a buffer against the zero lower bound on the interest rate, which is the primary instrument of central banks

• The key concept is the equilibrium interest rate, at which monetary policy is neutral (balance between easing and tightening)

10

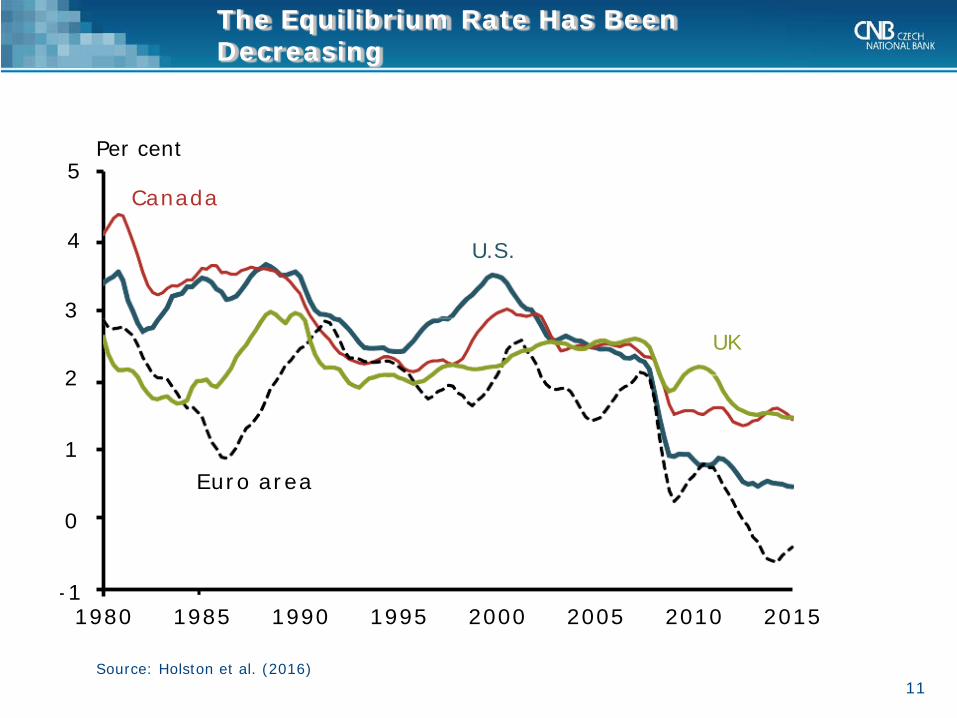

The Equilibrium Rate Has Been Decreasing

3UK

2

1Euro area

0

-1

4

5

1980 1985 1990 1995 2000 2005 2010 2015

e ce t

U.S.

Canada

11 Source: Holston et al. (2016)

Per cent

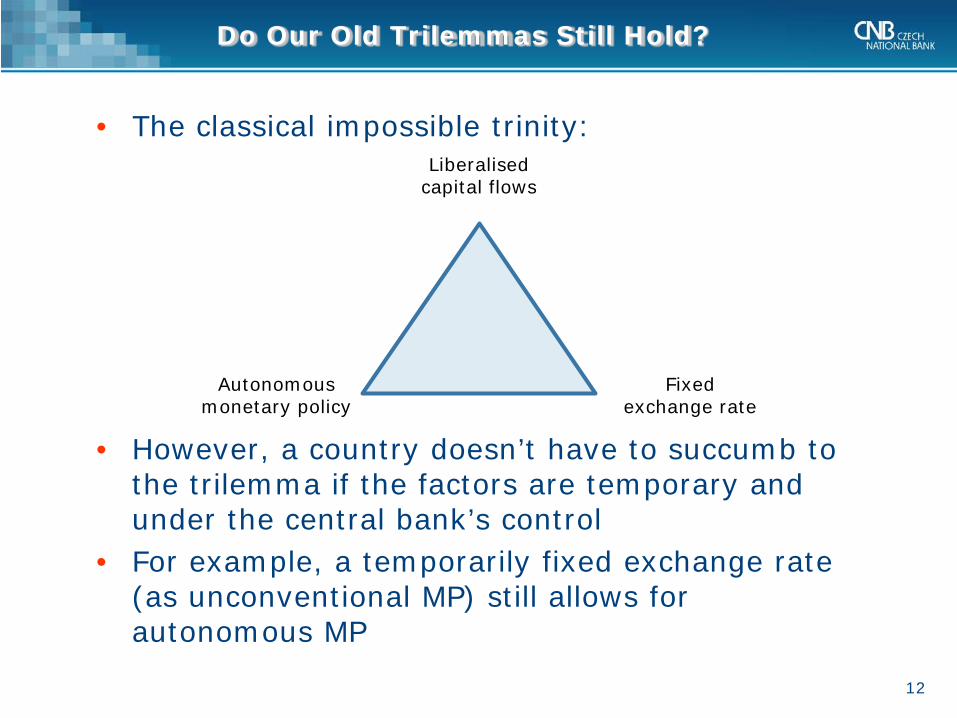

Do Our Old Trilemmas Still Hold?

• The classical impossible trinity:

• However, a country doesn’t have to succumb to the trilemma if the factors are temporary and under the central bank’s control

• For example, a temporarily fixed exchange rate (as unconventional MP) still allows for autonomous MP

12

Liberalised capital flows

Fixed exchange rate

Autonomous monetary policy

Digital Currencies Emitted by Central Banks

Now to reforms: • In some countries, cash accounts for a small and

shrinking percentage of total money supply • The CB loses seigniorage revenue, almost all

money is generated at the credit market • That’s why the Riksbank is planning e-krona:

a digital alternative to cash (Skingsley, 2016) • The concept is very similar to standard electronic

deposits, but now held at the central bank

13

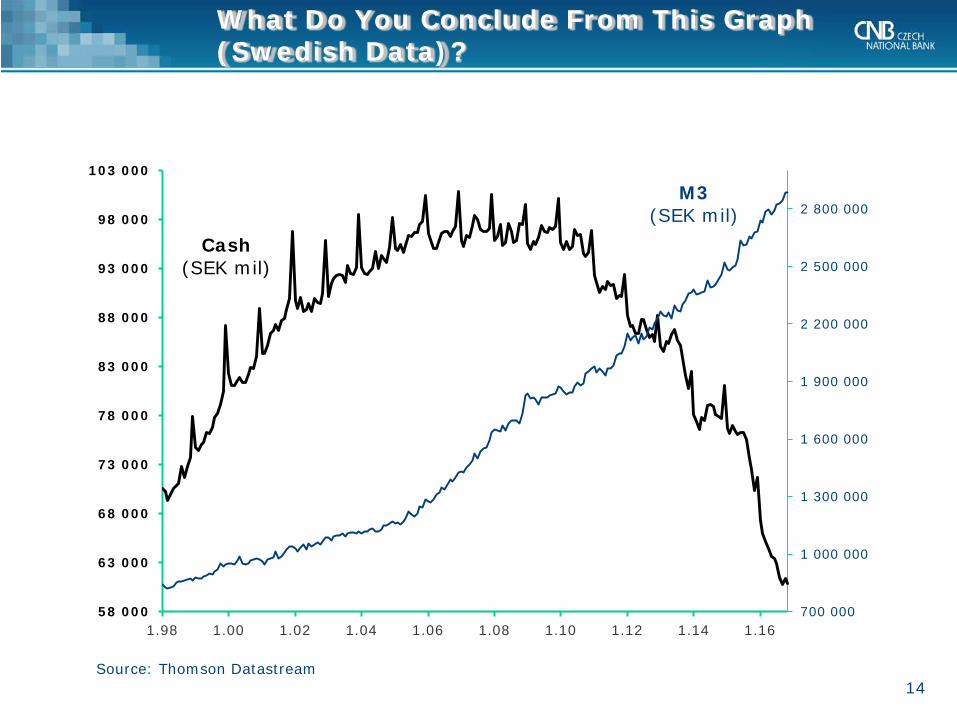

What Do You Conclude From This Graph (Swedish Data)?

700 000

1 000 000

1 300 000

1 600 000

1 900 000

2 200 000

2 500 000

2 800 000

58 000

63 000

68 000

73 000

78 000

83 000

88 000

93 000

98 000

103 000

1.98 1.00 1.02 1.04 1.06 1.08 1.10 1.12 1.14 1.16

M3 (SEK mil)

Cash (SEK mil)

14 Source: Thomson Datastream

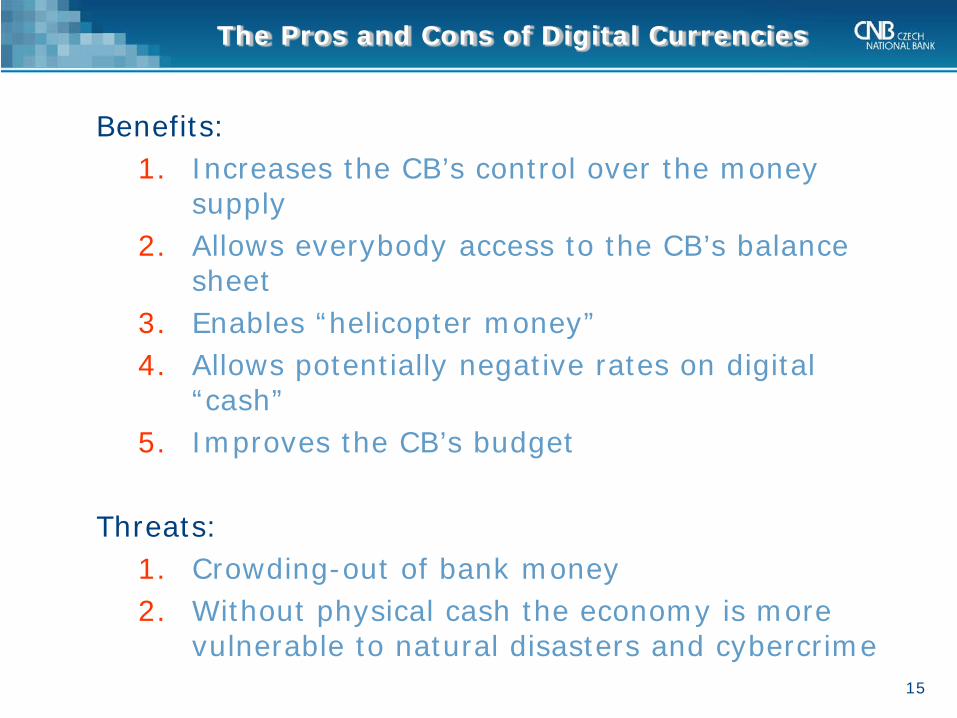

The Pros and Cons of Digital Currencies

Benefits: 1. Increases the CB’s control over the money

supply 2. Allows everybody access to the CB’s balance

sheet 3. Enables “helicopter money” 4. Allows potentially negative rates on digital

“cash” 5. Improves the CB’s budget

Threats:

1. Crowding-out of bank money 2. Without physical cash the economy is more

vulnerable to natural disasters and cybercrime 15

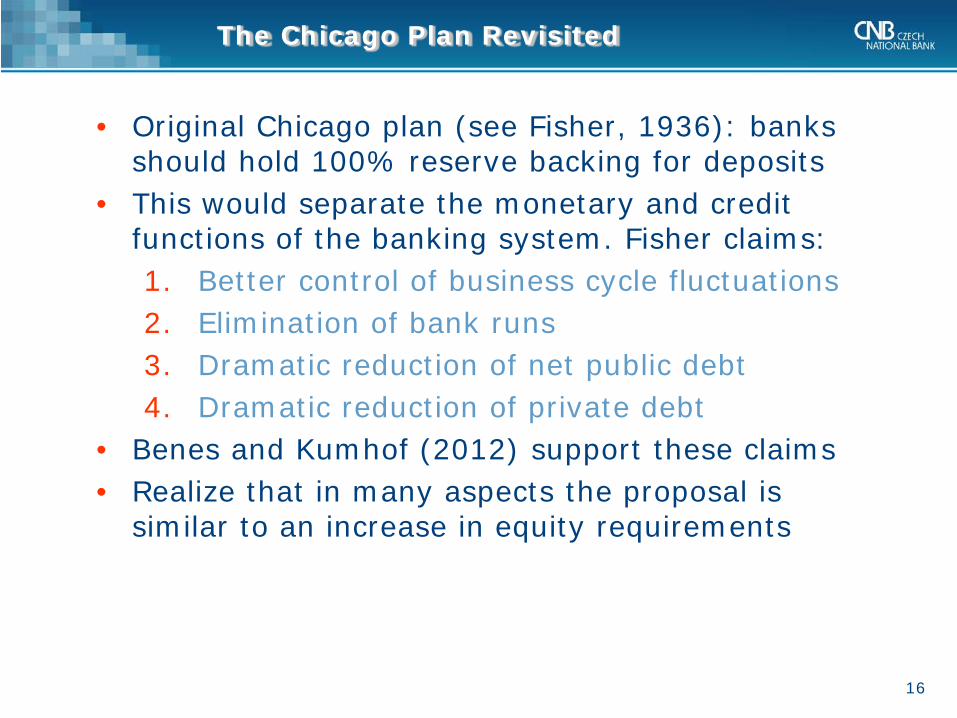

The Chicago Plan Revisited

• Original Chicago plan (see Fisher, 1936): banks should hold 100% reserve backing for deposits

• This would separate the monetary and credit functions of the banking system. Fisher claims: 1. Better control of business cycle fluctuations 2. Elimination of bank runs 3. Dramatic reduction of net public debt 4. Dramatic reduction of private debt

• Benes and Kumhof (2012) support these claims • Realize that in many aspects the proposal is

similar to an increase in equity requirements

16

Cryptocurrencies: Old Wine in New Bottles?

• Bitcoin presents an innovation that could be especially useful in countries with a defunct financial system (think Venezuela, Zimbabwe)

• From the monetary policy perspective, though, cryptocurrencies are nothing new

• Technically they account for commodity-backed “currencies or even commodities”; in this case the commodity is data on collecting value

• One can design a digital currency backed by gold, silver, or wheat, for example

• Why have we abandoned commodity backing?

17

Private Money and Currency Competition

• Bitcoin is just the most visible global quasi-currency competitor to established currencies (or, more precisely, to cash)

• In the credit market, peer-to-peer lending may one day become a major source of financing

• In principle, even in P2P lending some sort of intermediary is always needed to monitor the debtor. The intermediary collects a fee for this activity

• There is no free lunch: without the intermediary the expected return is larger, but so is the risk

18

What To Do About the Zero Lower Bound?

• We discussed decreasing equilibrium rates • Because the average cut in the policy rate in a

recession is 5 p.p., we might very well hit the zero lower bound in the next recession as well

• What has been tried: exchange rate interventions (small open economies) and QE (large economies)

• What has been proposed: significantly negative rates (mildly negative rates have very limited expansionary effects) and helicopter money

19

Helicopter Money

• Proposed by Friedman (1969) • Previously discarded by most central bankers

and economists: necessary to cooperate with the government (tax credit); problems for independence

• But with digital currencies (think e-krona), the CB can implement helicopter money easily

• It can send each month to every person an amount of money that can only be consumed (limited validity)

• More effective than QE (directly affects consumption)

• QE expands the CB’s balance sheet, helicopter money creates a loss, but doesn’t affect the total value of the balance sheet

20

Negative Interest Rates

• The main problem with negative rates: when they become sufficiently negative, people switch to cash • When the scope for negative rates is so limited,

the benefits do not outweigh the costs (uncertainty, financial instability, unintuitiveness)

• That’s why recent experiments with negative rates haven’t been universally successful

• Clever solution by Agarwal and Kimball (2015) and Kimball (2015): create an exchange rate between cash and electronic money (deposit fee on cash); only use it in crisis

• Already used by Kublai Khan in the 13th century: a paper note was exchangeable for the unit of account (gold), but for less than the note’s face value

21

References – Elastic Money

1. Aghion, Philippe & Farhi, Emmanuel & Kharroubi, Enisse, 2012. “Monetary Policy, Liquidity, and Growth.” Working Papers 18072/2012, The National Bureau of Economic Research.

2. Braun, Benjamin, 2016. “Speaking to the People? Money, Trust, and Central Bank Legitimacy in the Age of Quantitative Easing.” Discussion Paper 12/2016, Max Planck Institute for the Study of Societies.

3. Gordon, Robert J., 2006. “The Boskin Commission Report: A Retrospective One Decade Later.” International Productivity Monitor, Centre for the Study of Living Standards, pp. 7–22.

4. Holston, Kathryn & Laubach, Thomas & Williams, John C., 2016. “Measuring the Natural Rate of Interest: International Trends and Determinants.” Working Paper Series 11/2016, Federal Reserve Bank of San Francisco.

5. Jakab, Zoltan & Kumhof, Michael, 2015. “Banks Are Not Intermediaries of Loanable Funds – And Why This Matters.” Working Papers 529/2015, Bank of England.

6. McLeay, Michael & Amar, Radia & Ryland, Thomas, 2014. “Money in the Modern Economy: An Introduction.” Bank of England Quarterly Bulletin, vol. 54(1), pp. 4–13.

7. Rachel, Lukas & Smith, Thomas, 2016. “Towards a Global Narrative on Long-Term Real Interest Rates.” VoxEU, January 15, 2016, http://voxeu.org/article/towards-global-narrative-long-term-real-interest-rates.

8. Sims, Christopher A., 2003. “Implications of Rational Inattention.” Journal of Monetary Economics, vol. 50(3), pp. 665–690. 22

References – Reforms of the Monetary Order

1. Agarwal, Ruchir & Kimball, Miles, 2015. “Breaking Through the Zero Lower Bound,” Working Papers 224/2015, International Monetary Fund.

2. Federal Reserve Bank of Minneapolis, 2016. “The Minneapolis Plan to End Too Big To Fail,” Technical report, https://www.minneapolisfed.org/publications/special-studies/endingtbtf.

3. Fisher, Irving, 1936. “100% Money and the Public Debt,” Economic Forum, Spring Number, April-June 1936, pp. 406–420.

4. Friedman, Milton, 1969. “The Optimum Quantity of Money,” Aldine Pub. Co.

5. Kimball, Miles, 2015. “Negative Interest Rate Policy as Conventional Monetary Policy,” National Institute Economic Review, National Institute of Economic and Social Research, vol. 234(1), pp. 5–14.

6. Kumhof, Michael & Benes, Jaromir, 2012. “The Chicago Plan Revisited,“ Working Papers 202/2012, International Monetary Fund.

7. Skingsley, Cecilia, 2016. “Should the Riksbank Issue E-Krona?” http://www.riksbank.se/en/Press-and-published/Speeches/2016/Skingsley-Should-the-Riksbank-issue-e-krona/.

8. Hampl, Mojmír & Havránek, Tomáš, 2017. “Should Inflation Measures Used by Central Banks Incorporate House Prices? The Czech National Bank’s Approach“, CNB, RPN, 1/2017.

23