CSE · Amendments to LKAS 32 Financial Instruments: Prese ntation , with regard to offsetting...

34

[DC 2] ENTRUST SECURITIES PLC FINANCIAL STATEMENTS 31 MARCH 2015

Transcript of CSE · Amendments to LKAS 32 Financial Instruments: Prese ntation , with regard to offsetting...

[DC 2]

ENTRUST SECURITIES PLC

FINANCIAL STATEMENTS

31 MARCH 2015

[DC 2]

ENTRUST SECURITIES PLC

CONTENT

PAGE

Independent auditor's report 1

Statement of financial position 2

Statement of comprehensive income 3

Statement of changes in equity 4

Statement of cash flows 5

Notes to the financial statements 6 - 32

FINANCIAL STATEMENTS - 31 MARCH 2015

[DC 2] Page 2

ENTRUST SECURITIES PLC

Statement of financial position

(all amounts in Sri Lanka Rupees)

Notes 31 March 31 March

2015 2014

ASSETS

Cash and cash equivalents 6 2,347,761 857,739

Financial assets

- Fair value through profit or loss 7.1 3,260,301,446 3,345,034,808

- Loans and receivables 7.2 13,965,579,690 8,982,910,707

Deposits, prepayments and other receivables 8 14,286,094 24,947,322

Gratuity fund investment 9 6,649,360 5,578,032

Assets held for sale 10 - 2,224,832

Property, plant and equipment 11 78,983,223 82,453,810

Total assets 17,328,147,574 12,444,007,250

EQUITY AND LIABILITIES

Capital and reserves

Stated capital 12 220,000,070 220,000,000

Special risk reserve 220,551,925 165,393,583

Retained earnings 739,594,231 627,249,225

Total equity 1,180,146,226 1,012,642,808

LIABILITIES

Financial liabilities

- Other financial liabilities 13 16,105,066,376 11,373,802,669

Accruals, provisions and other payables 14 35,334,288 51,640,099

Post-employment benefit obligation-gratuity 15 7,600,684 5,921,674

Total liabilities 16,148,001,348 11,431,364,442

Total equity and liabilities 17,328,147,574 12,444,007,250

Net assets per share 35.76 30.69

Sgd. Sgd.

Nipuna Sanjeewa Sanjeewa Dayarathne

Manager - Finance General Manager

Sgd. Sgd.

Isira D B Dassanayake Romesha D Senerath

Chairman Group Executive Director | GCOO

14th July 2015 14th July 2015

Date Date

The Notes on pages 6 to 32 form an integral part of these financial statements.

Independent auditors' report - page 1.

I certify that these financial statements have been prepared in compliance with the requirements of the Companies

Act, No. 07 of 2007.

The Board of Directors is responsible for the preparation and presentation of these financial statements. These

financial statements were authorised for issue by Board of Directors on 8th July 2015.

[DC 2] Page 3

ENTRUST SECURITIES PLC

Statement of comprehensive income

(all amounts in Sri Lanka Rupees)

Notes

2015 2014

Interest income from government securities 16 1,287,297,397 1,158,723,560

Interest expense from government securities 17 (1,018,251,931) (976,342,224)

Net interest income from government securities 269,045,466 182,381,336

Capital gain from sale of government securities 205,085,100 170,845,673

Brokerage fee (18,144,208) (12,503,027)

(Loss) / gain from revaluation of government securities 18 (121,295,000) 57,773,000

Other income 19 1,121,582 903,394

Sales and promotion costs (2,997,469) (5,276,758)

Administration costs (112,307,620) (120,111,317)

Operating profit 20 220,507,851 274,012,301

Other finance income 22 408,422 507,323

Other finance costs 22 - (15,945)

Profit for the year 220,916,273 274,503,679

Other comprehensive loss

Items that will not be reclassified to profit or loss

Remeasurement of defined benefit obligations-gratuity 15 (282,902) (146,432)

Total other comprehensive loss for the year (282,902) (146,432)

Total comprehensive income for the year 220,633,371 274,357,247

Earnings per share

- basic 25 6.69 8.32

The Notes on pages 6 to 32 form an integral part of these financial statements.

Independent auditors' report - page 1.

Year ended 31 March

[DC 2] Page 4

ENTRUST SECURITIES PLC

Statement of changes in equity

(all amounts in Sri Lanka Rupees)

Stated Special risk Retained Total

capital reserve earnings

Balance at 1 April 2013 220,000,000 96,804,271 421,481,290 738,285,561

Total comprehensive

income for the year

Profit for the year - - 274,503,679 274,503,679

Other comprehensive

loss for the year - - (146,432) (146,432)

Total comprehensive income - - 274,357,247 274,357,247

Transfer to special

risk reserve - 68,589,312 (68,589,312) -

At 31 March 2014 220,000,000 165,393,583 627,249,225 1,012,642,808

Balance at 1 April 2014 220,000,000 165,393,583 627,249,225 1,012,642,808

Adjustment (Refer note 12) 70 - - 70

Total comprehensive

income for the year

Profit for the year - - 220,916,273 220,916,273

Other comprehensive

loss for the year - - (282,902) (282,902)

Total comprehensive income - - 220,633,371 220,633,371

Dividend paid - - (53,130,023) (53,130,023)

Transfer to special

risk reserve - 55,158,342 (55,158,342) -

At 31 March 2015 220,000,070 220,551,925 739,594,231 1,180,146,226

The Notes on pages 6 to 32 form an integral part of these financial statements.

Independent auditors' report - page 1.

As directed by the Central Bank of Sri Lanka, 25% of annual profit is transferred to the special risk reserve.

[DC 2] Page 5

ENTRUST SECURITIES PLC

Statement of cash flows

(all amounts in Sri Lanka Rupees)

2015 2014

Cash generated from operations 27 53,879,368 3,252,109

Gratuity paid 15 (99,000) (165,000)

Proceeds received as gratuity for staff transfers 15 91,000 -

53,871,368 3,087,109

Cash flows from investing activities

Purchase of property, plant and equipment 11 (665,947) (9,600,634)

property, plant and equipment 245,825 4,056,227

2,240,057 -

Movement in gratuity fund investment 9 (1,071,328) (342,323)

748,607 (5,886,730)

Cash flows from financing activities

Dividend paid (53,130,023) -

Cash inflow due to adjustment in promoters shares 70 -

(53,129,953) -

Increase / (decrease) in cash and cash equivalents 1,490,022 (2,799,621)

Movement in cash and cash equivalents

At beginning of year 857,739 3,657,360

Increase / (decrease) 1,490,022 (2,799,621)

Cash and cash equivalents at end of the year 6 2,347,761 857,739

The Notes on pages 6 to 32 form an integral part of these financial statements.

Independent auditors' report - page 1.

Year ended 31 March

investing activities

Net cash generated from operating activities

Sales proceeds from disposal of

Net cash generated from / (used in)

Net cash used in financing activities

Sales proceeds from disposal of assets held for sale

[DC 2] Page 6

ENTRUST SECURITIES PLC

Notes to the financial statements

(In the notes all amounts are shown in Sri Lanka Rupees unless otherwise stated)

1 General information

2 Changes in accounting policy and disclosures

(a) New accounting standards, amendments and interpretations adopted in 2014.

(i)

(ii)

(iii)

(iv)

(v)

(vi)

Amendment to LKAS 1 ‘Financial Statement Presentation’, regarding other comprehensive income.

The main change resulting from these amendments is a requirement for entities to group items

presented in ‘Other Comprehensive Income’ (OCI) on the basis of whether they are potentially

reclassifiable to profit or loss subsequently (reclassification adjustments).

Amendments to LKAS 32 ‘Financial Instruments: Presentation’, with regard to offsetting financial

assets and financial liabilities. This amendment clarifies that the right of set-off must not be

contingent on a future event. It must also be legally enforceable for all counterparties in the normal

course of business, as well as in the event of default, insolvency or bankruptcy. The amendment

also considers settlement mechanisms.

Amendments to LKAS 36 ‘Impairment of Assets’, regarding recoverable amount disclosures for

non-financial assets. This amendment removed certain disclosures of the recoverable amount of

‘Cash-Generating Units’(CGUs) which had been included in LKAS 36 by the issue of SLFRS 13.

Entrust Securities PLC ("the Company") was incorporated and commenced business operations on 29

February 2000. The primary dealer license was issued to the Company on 1 April 2000. The Company's

principal activity is buying and selling of government securities for customers and leveraging on own

portfolio in the money market.

The parent and ultimate parent Company of the Entrust Securities PLC is Entrust Holdings Limited and

Entrust Capital Partners (Private) Limited respectively.

SLFRS 12 ‘Disclosure of Interests in Other Entities’, includes the disclosure requirements for all

forms of interests in other entities, including joint arrangements, associates, special purpose

vehicles and other off balance sheet vehicles.

SLFRS 13 ‘Fair Value Measurement’, aims to improve consistency and reduce complexity by

providing a precise definition of fair value and a single source of fair value measurement and

disclosure requirements for use across Sri Lanka Accounting Standards.

IFRIC 21 ‘Levies’, establishes the accounting for an obligation to pay a levy if that liability is within

the scope of LKAS 37 ‘Provisions’. The interpretation addresses what the obligating event which

gives rise to pay a levy and when a liability should be recognised.

The Company is a Public Limited Company incorporated and domiciled in Sri Lanka. The address of its

registered office is at Level 23, East Tower, World Trade Center, Echelon Square, Colombo 1. The

Company carries out business as a primary dealer in accordance with Registered Stock and Securities

Ordinance and Local Treasury Bill Ordinance, and subject to the regulatory controls of the Central Bank of

Sri Lanka. The Company was listed on the Dirisavi Board of the Colombo Stock Exchange on 29 November

2011.

The following standards have been adopted by the Company for the first time with effect from financial

year beginning on 1 April 2014.Those standards did not have a significant effect on the financial

statements.

[DC 2] Page 7

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

2 Changes in accounting policy and disclosures (contd)

(a) New accounting standards, amendments and interpretations adopted in 2014. (contd)

(vii)

(b) New accounting standards, amendments and interpretations issued but not yet adopted.

(i)

(ii)

There are no other standards or IFRIC interpretations that are not yet effective that would be

expected to have a material impact to the Company.

Amendments to LKAS 39 ‘Financial Instruments: Recognition and Measurement’, on novation of

derivatives and the continuation of hedge accounting. This amendment considers legislative

changes to ‘over-the-counter’ derivatives and the establishment of central counterparties. Under

LKAS 39 novation of derivatives to central counterparties would result in discontinuance of hedge

accounting. The amendment provides relief from discontinuing hedge accounting when novation of

a hedging instrument meets specified criteria.

A number of new standards and amendments to standards and interpretations are effective for annual

periods beginning after 1 January 2014, and have not been applied in preparing these financial

statements.

SLFRS 9 ‘Financial Instruments’, addresses the classification, measurement and recognition of

financial assets and financial liabilities. The complete version of SLFRS 9 was issued in July 2014.

It replaces the guidance in LKAS 39 that relates to the classification and measurement of financial

instruments. SLFRS 9 retains but simplifies the mixed measurement model and establishes three

primary measurement categories for financial assets: amortised cost, fair value through OCI and

fair value through profit or loss. The basis of classification depends on the entity’s business model

and the contractual cash flow characteristics of the financial asset. Investments in equity

instruments are required to be measured at fair value through profit or loss with the irrevocable

option at inception to present changes in fair value in OCI not recycling. There is now a new

expected credit losses model that replaces the incurred loss impairment model used in LKAS 39.

For financial liabilities there were no changes to classification and measurement except for the

recognition of changes in own credit risk in other comprehensive income, for liabilities designated

at fair value through profit or loss. SLFRS 9 relaxes the requirements for hedge effectiveness by

replacing the bright line hedge effectiveness tests. It requires an economic relationship between

the hedged item and hedging instrument and for the ‘hedged ratio’ to be the same as the one

management actually use for risk management purposes. Contemporaneous documentation is still

required but is different to that currently prepared under LKAS 39. The standard is effective for

accounting periods beginning on or after 1 April 2018. Early adoption is permitted. The Company is

yet to assess the full impact of SLFRS 9.

SLFRS 15, ‘Revenue from Contracts with Customers’, deals with revenue recognition and

establishes principles for reporting useful information to users of financial statements about the

nature, amount, timing and uncertainty of revenue and cash flows arising from an entity’s contracts

with customers. Revenue is recognised when a customer obtains control of a good or service and

thus has the ability to direct the use and obtain the benefits from the good or service. The standard

replaces LKAS 18 and LKAS 11 and related interpretations. This standard will be effective for

annual periods beginning on or after 1 April 2017 and earlier application is permitted.

[DC 2] Page 8

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies

3.1 Basis of preparation

- Financial instruments at fair value through profit or loss, which are measured at fair value;

- Financial instruments at held to maturity, which are measured at amortized cost; and

- Post employment benefit obligation which is measured at the present value of the obligation.

3.2 Foreign currencies

(a) Functional and presentation currency

(b) Transactions and balances

3.3 Financial assets

3.3.1 Classification

(a) Financial assets at fair value through profit or loss

The financial statements have been prepared in accordance with and comply with Sri Lanka Accounting

Standards ("SLAS") under the historical cost convention except for following financial statement line items.

Foreign exchange gains and losses (if any) arising from translation are included in the statement of

comprehensive income.

Items included in the financial statements are measured using the currency of the primary economic

environment in which the entity operates ('the functional currency'). The financial statements are presented

in Sri Lankan Rupees, which is the Company's functional and presentation currency.

Foreign currency transactions are translated into the functional currency using the exchange rates

prevailing at the dates of the transactions. Foreign currency assets and liabilities are translated into the

functional currency using the exchange rate prevailing at the statement of financial position date.

The Company allocates financial assets to the following categories; financial assets at fair value through

profit or loss; loans and receivables; held-to-maturity investments; and available-for-sale financial assets.

Management determines the classification of its financial instruments at initial recognition.At the financial

position date and during the reporting period,there were no financial assets classified as held to maturity

and available for sale.

This category comprises of financial assets classified as held for trading. A financial asset is classified as

held for trading if it is acquired or incurred principally for the purpose of selling or repurchasing it in the near

term or if it is part of a portfolio of identified financial instruments that are managed together and for which

there is evidence of a recent actual pattern of short - term profit - taking. Financial assets held for trading

consist of treasury bonds and treasury bills issued by the Government of Sri Lanka. They are recognized in

the statement of financial position as ‘financial assets at fair value through profit or loss’.

The principal accounting policies applied in the preparation of these financial statements are set out below.

These policies have been consistently applied to all the years presented unless otherwise stated.

[DC 2] Page 9

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.3 Financial assets (contd)

3.3.1 Classification (contd)

(b) Loans and receivables

•

•

•

3.3.2 Recognition

Loans and recievables are carried at amortized cost.When the Company purchases a financial asset and

simultaneously enters into an agreement to resell the asset (or a substantially similar asset) at a fixed price

on a future date ("reverse repo"), the arrangement is accounted for as a loan or receivable, and the

underlying asset is not recognized in the Company’s financial statements.The carrying value of the

securities purchased under agreement to sell is recorded at cost. The difference between sale and

repurchase price is treated as interest and accrued over the life of the agreements using the effective

interest rate method.

Financial instruments included in this category are recognized initially at fair value; transaction costs are

taken directly to the statement of comprehensive income.The fair value gains and losses arising from

revaluation of held for trading revaluation assets are included in the statement of comprehensive income as

gains and losses from revaluation of trading securities. This instruments are derecognised when the rights

to receive cash flows have expired or the Company has transferred substantially all the risks and rewards of

ownership and the transfer qualifies for derecognising.

those that the Company upon initial recognition designates as available for sale; or

those for which the holder may not recover substantially all of its initial investment, other than

because of credit deterioration.

The chosen valuation technique makes maximum use of market inputs and incorporates all factors that

market participants would consider in setting a price. It is consistent with accepted economic

methodologies for pricing financial instruments. Inputs to valuation techniques reasonably represent market

expectations and measures of the risk-return factors inherent in the financial instrument. The Company

calibrates valuation techniques and tests them for validity using prices from observable current market

transactions in the same instrument or based on other available observable market data.

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not

quoted in an active market, other than:

The Company initially recognizes financial assets on the date at which they are originated. Regular way

purchases of financial assets are recognized on the value date at which the Company commits to purchase

the asset. All other financial assets are initially recognized on the value date at which the Company

becomes a party to the contractual provisions of the instrument. A financial asset is measured initially at fair

value plus, for an item not at fair value through profit or loss, transaction costs that are directly attributable

to its acquisition or issue.

those that the Company intends to sell immediately or in the short term, which are classified as

held for trading, and those that the entity upon initial recognition designates as at fair value

through profit or loss;

In the case of an impairment, the impairment loss is reported as a deduction from the carrying value of the

loans and recievables recognised in the statement of income as ‘loans and recievable impairment charges’.

[DC 2] Page 10

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.3 Financial assets (contd)

3.3.3 Derecognition

3.3.4 Impairment of financial assets

3.4 Reclassification of financial assets

Government securities furnished by the Company under securities repurchased under resale agreements

and securities sold under repurchase agreements are not de-recognised because the Company retains

substantially all the risks and rewards on the basis of the predetermined repurchase price, and the criteria

for de-recognition are therefore not met.

The Company considers evidence of impairment for loans and receivables at both a specific asset and

collective level. All individually significant loans and receivables are assessed for specific impairment. All

individually significant loans and receivables found not to be specifically impaired are then collectively

assessed for any impairment that has been incurred but not yet identified. Loans and receivables that are

not individually significant are collectively assessed for impairment by grouping together loans and

receivables with similar risk characteristics. Impairment losses on assets carried at amortized cost are

measured as the difference between the carrying amount of the financial asset and the present value of

estimated future cash flows discounted at the asset's original effective interest rate. Impairment losses are

recognized in profit or loss and reflected in an allowance account against loans and receivables. Interest on

impaired assets continues to be recognized through the unwinding of the discount. When a subsequent

event causes the amount of impairment loss to decrease, the decrease in impairment loss is reversed

through profit or loss.

At each reporting date the Company assesses whether there is objective evidence that financial assets not

carried at fair value through profit or loss are impaired. A financial asset or a group of financial assets is

(are) impaired when objective evidence demonstrates that a loss event has occurred after the initial

recognition of the asset(s), and that the loss event has an impact on the future cash flows of the asset(s)

that can be estimated reliably. Objective evidence that financial assets are impaired can include significant

financial difficulty of the counter party or issuer, default or delinquency by a counter party, indications that a

counterparty or issuer will enter bankruptcy or other observable data relating to a group of assets such as

adverse changes in the payment status of counterparty or issuers in the group, or economic conditions that

correlate with defaults in the group.

Financial assets are derecognised when the contractual rights to receive the cash flows from these assets

have ceased to exist or the assets have been transferred and substantially all the risks and rewards of

ownership of the assets are also transferred (that is, if substantially all the risks and rewards have not been

transferred, the Company tests control to ensure that continuing involvement on the basis of any retained

powers of control does not prevent derecognition).

The Company writes off certainsecurities purchased under resale agreements and government securities

when they are determined to be uncollectible.

The Company may choose to reclassify a financial asset held for trading out of the held-for-trading category

if the financial asset is no longer held for the purpose of selling it in the near-term. Financial assets are

permitted to be reclassified out of the held for trading category to available-for-sale category only in rare

circumstances arising from a single event that is unusual and highly unlikely to recur in the near-term. In

addition, the Company may choose to reclassify financial assets that would meet the definition of loans and

receivables out of the held-for-trading category if the Company has the intention and ability to hold these

financial assets for the foreseeable future or until maturity at the date of reclassification. Held-to maturity

assets must be reclassified to available-for-sale category if the loan portfolio become tainted following the

sale of other than an insignificant amount of held-to-maturity assets prior to its maturity.

[DC 2] Page 11

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.4 Reclassification of financial assets (contd)

3.5 Financial liabilities

(a) Liabilities measured at amortised cost

3.6 Offsetting financial instruments

3.7 Revenue recognition

(a) Interest income and expense

The effective interest method is a method of calculating the amortised cost of a financial asset or

a financial liability and of allocating the interest income or interest expense over the relevant

period. The effective interest rate is the rate that exactly discounts estimated future cash

payments or receipts through the expected life of the financial instrument or, when appropriate, a

shorter period to the net carrying amount of the financial asset or financial liability. When

calculating the effective interest rate, the company estimates cash flows considering all

contractual terms of the financial instrument (for example, prepayment options) but does not

consider future credit losses. The calculation includes all fees and points paid or received

between parties to the contract that are an integral part of the effective interest rate, transaction

costs and all other premiums or discounts.

Financial liabilities that are not classified as at fair value through profit or loss fall into this category and are

measured at amortised cost. The amortized cost of a financial liability is the amount at which the financial

liability is measured at initial recognition, minus principal repayments, plus the cumulative amortization

using the effective interest method of any difference between the initial amount recognized and the maturity

amount.

A financial liability is measured initially at fair value and initially recognized on the trade date at which the

Company becomes a party to the contractual provisions of the instrument. The Company’s holding in

financial liabilities is at amortised cost and represent mainly from securities sold under repurchase

agreements. The Company derecognizes a financial liability when its contractual obligations are discharged

or cancelled or expired.

Reclassifications are made at fair value as of the reclassification date. Fair value becomes the new cost or

amortised cost as applicable, and no reversals of fair value gains or losses recorded before reclassification

date are subsequently made.

Once a financial asset or a group of similar financial assets has been written down as a result of

an impairment loss, interest income is recognised using the rate of interest used to discount the

future cash flows for the purpose of measuring the impairment loss.

When the Company enters into an agreement to repurchase an asset (or a substantially similar asset) at a

fixed price on a future date (“repo”), the counterparty liability is included as securities sold under

repurchase agreements, as appropriate and the underlying asset will continued to be recognised in the

company’s financial statements. The difference between sale and repurchase price is treated as interest

and accrued over the life of the agreement using the effective interest method.

Financial assets and liabilities are offset and the net amount reported in the statement of financial position

when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle

on a net basis or realise the asset and settle the liability simultaneously.

Interest income and expense for all interest-bearing financial instruments are recognised within

‘interest income’ and ‘interest expense’ in the statement of comprehensive income using the

effective interest method.

[DC 2] Page 12

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.7 Revenue recognition (contd)

(b)

3.8 Impairment of non-financial assets

3.9 Cash and cash equivalents

3.10 Property, plant and equipment

Computers and accessories 3 years

Furniture and other equipment 3-4 years

Motor vehicles 5 years

Capital gain

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each

reporting period.

Land is not depriciated.Depreciation is calculated on the straight line method to amortise the cost of each

asset to their residual values over their estimated useful life as follows:

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as

appropriate, only when it is probable that future economic benefits associated with the item will flow to the

Company and the cost of the item can be measured reliably. The carrying amount of the replaced part is

derecognised. All other repairs and maintenance are charged to the statement of income during the

financial period in which they are incurred.

All property, plant and equipment is stated at historical cost less accumulated depreciation. Historical cost

includes expenditure that is directly attributable to the acquisition of the items. Property, plant and

equipment are initially recognised when the asset is in the location and condition necessary for it to be

capable of operating in the manner intended by the Company and only when it is probable that future

economic benefits associated with the item will flow to the Company and the cost of the item can be

measured reliably.Land is stated at cost.

Carrying amount of property, plant and equipment are de-recognised when the assets cease to be in the

condition necessary for it to be capable of operating in the manner intended by the Company or on disposal

of such asset or no future economic benefits are expected from its use or disposal.

Net capital gains on sale of government securities are accounted for on the date of sale by

deducting the carrying value of the securities from the sale proceeds.

Assets that have an indefinite useful life are not subject to amortisation and are tested annually for

impairment. Assets are reviewed for impairment whenever events or changes in circumstances indicate

that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which

the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an

asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are

grouped at the lowest levels for which there are separately identifiable cash inflows (cash-generating units).

The impairment test also can be performed on a single asset when the fair value less cost to sell or the

value in use can be determined reliably. Non-financial assets that suffered impairment are reviewed for

possible reversal of the impairment at each reporting date.

Cash and cash equivalents comprise balances with less than three months’ maturity from the date of

acquisition for day to day operations, including cash in hand and deposits held with banks.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying

amount is greater than its estimated recoverable amount.

[DC 2] Page 13

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.10 Property, plant and equipment (contd)

3.11 Non current assets held for sale

3.12 Provisions

3.13 Employee benefits

(a) Defined contribution plans

(b) Defined benefit obligation

Non-current assets held for sale are de-recognised when the consideration are received or right to receive

the cash or consideration is established. The gains or losses are recognised within 'other income' in the

statement of comprehensive income when the financial transaction takes place.

Provisions are recognised when the Company has a present legal or constructive obligation as a result of

past events, it is probable that an outflow of resources embodying economic benefits will be required to

settle the obligation, and a reliable estimate of the amount of the obligation can be made.

Non-current assets are classified as assets held for sale when their carrying amount is to be recovered

principally through a sale transaction rather than through continuing use and a sale is considered highly

probable within one year from the date of the classification. They are stated at the lower of carrying amount

and fair value less costs to sell.

A defined contribution plan is a pension plan under which the company pays fixed contributions

into a separate entity. The Company has no legal or constructive obligations to pay further

contributions if the fund does not hold sufficient assets to pay all employees the benefits relating

to employee service in the current and prior periods.

Actuarial gains and losses arising from experience adjustments and changes in actuarial

assumptions are charged or credited to equity in other comprehensive income in the period in

which they arise.

Past-service costs are recognised immediately in the statement of comprehensive income.

The liability recognised in the statement of financial position in respect of defined benefit

obligation plans is the present value of the defined benefit obligation at the end of the reporting

period. The defined benefit obligation is calculated annually using the projected unit credit

method using the formular prescribed in Sri Lanka Accounting Standard ( LKAS 19) - Employee

Benefits. The present value of the defined benefit obligation is determined by discounting the

estimated future cash outflows using the market rates on Government bonds.

Gains and losses on disposals are determined by comparing the proceeds with the carrying amount and

are recognised within ‘other income’ in the statement of comprehensive income.

All employees of the Company are members of the Employees' Provident Fund and Employees'

Trust Fund, to which the Company contributes 12% and 3% respectively of such employees'

basic or consolidated wage or salary, cost of living and all other allowances.

A defined benefit plan is a plan that is not a defined contribution plan. Typically defined benefit

plans define an amount of benefit that an employee will receive on retirement, usually dependent

on one or more factors such as age, years of service and compensation. The defined benefit plan

comprises of the gratuity payable under the Gratuity Act No 13 of 1983.

[DC 2] Page 14

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

3 Summary of significant accounting policies (contd)

3.14 Stated capital

3.15 Dividend distribution

4 Critical accounting estimates,assumptions and judgments

4.1 Defined benefit obligation - gratuity

Estimates, assumptions and judgments are continually evaluated and are based on historical experience

and other factors, including expectations of future events that are believed to be reasonable under the

circumstances.

Dividend distribution to the Company’s shareholders is recognised as a reduction in retained earnings in

the Company’s financial statements in the period in which the dividends are approved by the company’s

shareholders, the Central Bank of Sri Lanka and are paid.

The Company makes estimates and assumptions concerning the future. The resulting accounting

estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that

have a significant risk of causing a material adjustment to the carrying amount of assets and liabilities

within the next financial year are discussed below.

The present value of the gratuity obligations depends on a number of factors that are determined on the

projected unit credit method using a number of assumptions. The assumptions used in determining the net

cost (income) for gratuity include the discount rate. Any changes in these assumptions will impact the

carrying amount of pension obligations.

Ordinary shares are classified as equity.

Incremental costs directly attributable to the issue of new ordinary shares or options are shown in equity as

a deduction, net of tax, from the proceeds.

Other key assumptions for gratuity obligations are based in part on current market conditions. Additional

information is disclosed in Note 15.

The Company determines the appropriate discount rate at the end of each year. This is the interest rate that

should be used to determine the present value of estimated future cash outflows expected to be required to

settle the gratuity obligations. In determining the appropriate discount rate, the Company considers the

interest rates of government bonds that are denominated in the currency in which the benefits will be paid,

and that have terms to maturity approximating the terms of the related gratuity obligation.

[DC 2] Page 15

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

5 Financial risk management

5.1 Financial risk management

Rs. % Rs. %

Trading portfolio - fair value through profit or loss

Government securities - treasury bonds 3,122,767,755 18% 2,743,177,532 22%

- treasury bills 137,533,691 1% 601,857,276 5%

Loans and receivables

- Government securities purchased

under resale agreements (Reverse repo) 13,965,579,690 81% 8,982,910,707 73%

Total 17,225,881,136 100% 12,327,945,515 100%

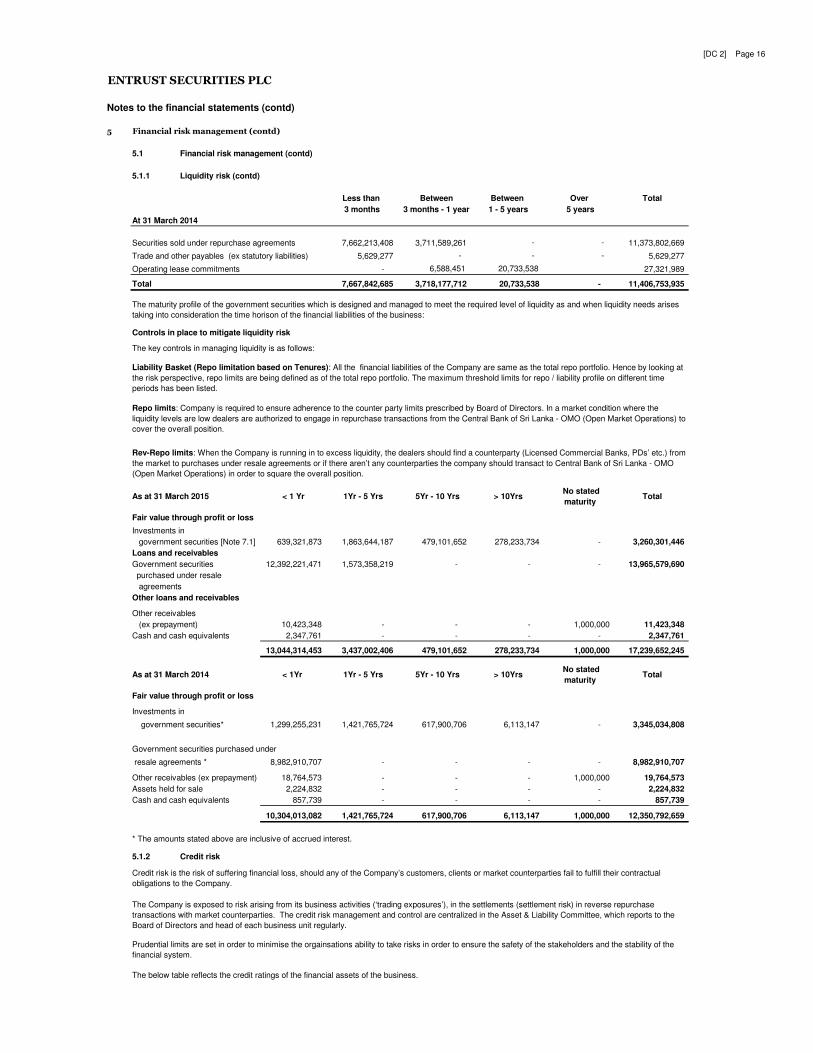

5.1.1 Liquidity risk

Less than Between Between Over Total

3 months 3 months - 1 year 1 - 5 years 5 years

At 31 March 2015

Securities sold under repurchase agreements 13,765,768,265 2,339,298,110 - - 16,105,066,376

Trade and other payables (ex statutory liabilities) 4,272,702 - - - 4,272,702

Operating lease commitments - 9,750,281 7,170,796 - 16,921,077

Total 13,770,040,967 2,349,048,391 7,170,796 - 16,126,260,155

Cash flow forecasting is performed by both front office and treasury divisions on a daily basis. The treasury operations division daily monitors and forecasts

the liquidity requirement of front office (dealing division) to ensure it has sufficient cash to meet operational needs.

Managing liquidity is a fundamental component in risk management. This involves prudently managing assets and liabilities (on- and off-balance sheet) to

ensure that cash inflows have an appropriate relationship to approaching cash outflows. This needs to be supported by a process of liquidity planning which

assesses potential future liquidity needs, taking into account the changes in economic, regulatory or other operating requirements. Such planning involves

identifying known, expected and potential cash outflows and weighing alternative asset/liability management strategies to ensure that adequate cash

inflows will be available to the Company to meet these needs.

The table below analyses the Company’s financial liabilities into relevant maturity groupings based on the remaining period at the statement of financial

position date to the contractual maturity date. The amounts disclosed in the table are the contractual undiscounted cash flows.

The Company’s overall risk management programme seeks to maximise the returns derived for the level of risk to which the Company is exposed and

seeks to minimise potential adverse effects on the Company’s financial performance.

The Company is also exposed to operational risks such as custody risk. Custody risk is the risk of loss of securities held in custody occasioned by the

insolvency or negligence of the custodian. Although an appropriate legal framework is in place that eliminates the risk of loss of value of the securities held

by the custodian, in the event of its failure, the ability of the Company to transfer securities might be temporarily impaired.

The core functions of the Company’s risk management are to identify all significant risks exposed, measure these risks, manage the risk positions and

determine capital allocations. The Company frequently reviews its risk management policies and systems in order to respond to the changes in Sri Lankan

economy and specially related to Sri Lankan money market.

The Company’s aim is to achieve an appropriate balance between risk and return and minimise potential adverse effects on the Company’s financial

performance. The Company’s activities expose it to a variety of financial risks: market risk (interest rate risk), credit risk and liquidity risk.

Another type of risk that the Company exposed to is settlement risk, where a counterparty does not deliver a security or its value as per agreement.

The following is a high level summary of the investment exposures by the Company’s investment and trading portfolios as at 31 March 2015 and 31 March

The Company’s use of leverage can increase the Company’s exposure to these risks, which in turn can also increase the potential returns the Company

can achieve. The Company has specific limits to manage the overall potential exposure within the risk and return policy framework. These limits include the

ability to purchase government securities, ability to engage repo and reverse repo transactions. As per the Central Bank of Sri Lanka directions, the

minimum capital requirement is the higher of Rs 300 million (minimum capital) or the capital sufficient to meet the interest rate sensitivity of the trading

portfolio plus reverse repo and capital for disallowances (capital charge) and capital for counterparty credit risk.

20142015

As evident from the investment exposures reflected in the above table, the business maintains an optimum exposure to identified asset classes to generate

investment returns without excessive exposure to high risk assets.

The risk officer at middle office overlooks the risk management function of the Company. As the company's portfolio solely consists of government

securities, no significant credit risk has been identified since the product is issued by the Central Bank of Sri Lanka. The exposure to interest rate risk is

regularly reviewed by the Integrated Risk Management Committee and the Board of Directors. In addition, internal audit is responsible for the independent

review of risk management and the control environment.

Liquidity is the availability of funds, or assurance that funds will be available, to honour all cash outflow obligations as and when they fall due. These

commitments are generally met through cash inflows, supplemented by assets readily convertible to cash or through the Company’s capacity to enter into

repurchase agreements.

[DC 2] Page 16

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

5 Financial risk management (contd)

5.1 Financial risk management (contd)

5.1.1 Liquidity risk (contd)

Less than Between Between Over Total

3 months 3 months - 1 year 1 - 5 years 5 years

At 31 March 2014

Securities sold under repurchase agreements 7,662,213,408 3,711,589,261 - - 11,373,802,669

Trade and other payables (ex statutory liabilities) 5,629,277 - - - 5,629,277

Operating lease commitments - 6,588,451 20,733,538 27,321,989

Total 7,667,842,685 3,718,177,712 20,733,538 - 11,406,753,935

Controls in place to mitigate liquidity risk

As at 31 March 2015 < 1 Yr 1Yr - 5 Yrs 5Yr - 10 Yrs > 10Yrs No stated

maturity Total

Fair value through profit or loss

Investments in

government securities [Note 7.1] 639,321,873 1,863,644,187 479,101,652 278,233,734 - 3,260,301,446

Loans and receivables

Government securities 12,392,221,471 1,573,358,219 - - - 13,965,579,690

purchased under resale

agreements

Other loans and receivables

Other receivables

(ex prepayment) 10,423,348 - - - 1,000,000 11,423,348

Cash and cash equivalents 2,347,761 - - - - 2,347,761

13,044,314,453 3,437,002,406 479,101,652 278,233,734 1,000,000 17,239,652,245

As at 31 March 2014 < 1Yr 1Yr - 5 Yrs 5Yr - 10 Yrs > 10Yrs No stated

maturity Total

Fair value through profit or loss

Investments in

government securities* 1,299,255,231 1,421,765,724 617,900,706 6,113,147 - 3,345,034,808

Government securities purchased under

resale agreements * 8,982,910,707 - - - - 8,982,910,707

Other receivables (ex prepayment) 18,764,573 - - - 1,000,000 19,764,573

Assets held for sale 2,224,832 - - - - 2,224,832

Cash and cash equivalents 857,739 - - - - 857,739

10,304,013,082 1,421,765,724 617,900,706 6,113,147 1,000,000 12,350,792,659

* The amounts stated above are inclusive of accrued interest.

5.1.2 Credit risk

Prudential limits are set in order to minimise the orgainsations ability to take risks in order to ensure the safety of the stakeholders and the stability of the

financial system.

Rev-Repo limits: When the Company is running in to excess liquidity, the dealers should find a counterparty (Licensed Commercial Banks, PDs’ etc.) from

the market to purchases under resale agreements or if there aren’t any counterparties the company should transact to Central Bank of Sri Lanka - OMO

(Open Market Operations) in order to square the overall position.

The key controls in managing liquidity is as follows:

Liability Basket (Repo limitation based on Tenures): All the financial liabilities of the Company are same as the total repo portfolio. Hence by looking at

the risk perspective, repo limits are being defined as of the total repo portfolio. The maximum threshold limits for repo / liability profile on different time

periods has been listed.

Credit risk is the risk of suffering financial loss, should any of the Company’s customers, clients or market counterparties fail to fulfill their contractual

obligations to the Company.

The below table reflects the credit ratings of the financial assets of the business.

The Company is exposed to risk arising from its business activities (‘trading exposures’), in the settlements (settlement risk) in reverse repurchase

transactions with market counterparties. The credit risk management and control are centralized in the Asset & Liability Committee, which reports to the

Board of Directors and head of each business unit regularly.

The maturity profile of the government securities which is designed and managed to meet the required level of liquidity as and when liquidity needs arises

taking into consideration the time horison of the financial liabilities of the business:

Repo limits: Company is required to ensure adherence to the counter party limits prescribed by Board of Directors. In a market condition where the

liquidity levels are low dealers are authorized to engage in repurchase transactions from the Central Bank of Sri Lanka - OMO (Open Market Operations) to

cover the overall position.

[DC 2] Page 17

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

5 Financial risk management (contd)

5.1 Financial risk management (contd)

5.1.2 Credit risk (contd)

As at 31 March 2015 Sovereign risk AAA AA A Non rated Total

Fair value through profit or loss

Investments in government securities

[Note 7.1] 3,260,301,446 - - - - 3,260,301,446

Loans and receivables

Government securities purchased

under resale agreements

[Note 7.2] 13,965,579,690 - - - - 13,965,579,690

Other receivables

(excluding prepayments) - - - - 11,423,348 11,423,348

Cash and cash

equivalents 1,241,950 247,915 303,911 545,075 8,910 2,347,761

17,227,123,086 247,915 303,911 545,075 11,432,258 17,239,652,245

As at 31 March 2014 Sovereign risk AAA AA A Non rated Total

Fair value through profit or loss

Investments in 3,345,034,808 - - - - 3,345,034,808

government securities

Loans and receivables

Government securities purchased

under resale agreements 8,982,910,707 - - - - 8,982,910,707

Other receivables - - - - 19,764,573 19,764,573

(excluding prepayments)

Assets held for sale - - - - 2,224,832 2,224,832

Cash and cash equivalents 272,576 247,915 198,751 118,497 20,000 857,739

12,328,218,091 247,915 198,751 118,497 22,009,405 12,350,792,659

5.1.3 Market risk

5.1.3.1 Interest rate risk

As at 31 March 2015

Fixed interest Non interest

bearing

Total

Financial assets

Securities purchased under resale agreements* [Note 7.2] 13,965,579,690 - 13,965,579,690

Cash and cash equivalents [Note 6] 145,892 2,201,869 2,347,761

13,965,725,582 2,201,869 13,967,927,451

Financial liabilities

Securities sold under repurchase agreements* 16,105,066,376 - 16,105,066,376

Cash flow interest rate risk is the risk that the future cash flows of a financial instrument will fluctuate because of changes in market interest rates. Fair

value interest rate risk is the risk that the value of a financial instrument will fluctuate because of changes in market interest rates. The Company takes on

exposure to the effects of fluctuations in the prevailing levels of market interest rates on both its fair value and cash flow risks. Interest margins may

increase as a result of such changes but may reduce losses in the event that unexpected movements arise. The Board of Directors sets limits on the level

of mismatch of interest rate re-pricing and value at risk that may be undertaken, which is monitored daily by the risk officer at middle office.

The Company is exposed to market risks, where the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in

market prices/yields. Market risks arise from open positions in interest rate, of which are exposed to general and specific market movements and changes

in the level of volatility of market rates of securities or price of securities. The Company separates exposures to market risk into either financial assets held

to maturity or financial assets fair value through profit or loss. The Company's the primary source of market risks are interest rate risk.

Credit and liquidity risks are defined and managed as separate risks. However, assessment of market risk does consider the interdependence between

interest rate risks, and credit and liquidity risk (eg; loss incurred in the marked to market of the trading portfolio arises due to the liquidity shortfall in the

money market).

The risk of an adverse financial impact due to changes in the absolute level of interest rates, in the shape or curvature of the yield curve or in any other

interest rate relationship including volatility and spread between different yield curves.

The table below summarizes the nature of the interest rate risk associated with financial assets and financial liabilities:

[DC 2] Page 18

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

5 Financial risk management (contd)

5.1 Financial risk management (contd)

5.1.3 Market risk (contd)

5.1.3.1 Interest rate risk

As at 31 March 2014

Fixed interest Non interest

bearing

Total

Financial assets

Securities purchased under resale agreements* 8,982,910,707 - 8,982,910,707

Cash and cash equivalents - 857,739 857,739

8,982,910,707 857,739 8,983,768,446

Financial liabilities

Securities sold under repurchase agreements* 11,373,802,669 - 11,373,802,669

* The amounts stated above are inclusive of accrued interest.

5.1.3.2 Price risk

5.1.3.3 Sensitivity analysis on interest rate risk

Impact to;Net asset value Profit before tax

Net asset

value

Profit before

tax

Interest rate risk

+100 basis points

Government securities (91,262,829) (91,262,829) (64,288,000) (64,288,000)

-100 basis points

Government securities 97,047,203 97,047,203 67,013,000 67,013,000

Controls in place to mitigate market Risk

5.2 Capital management

5.2.1 Capital adequacy ratio

The capital adequacy ratios at 31st March 2015 and 31st March 2014 were as follows:

31 March 31 March

2015 2014

Total risk weighted assets 5,792,434,693 5,092,272,000

Stated capital 220,000,070 220,000,000

Reserve capital 960,146,156 792,642,808

1,180,146,226 1,012,642,808

Capital adequacy ratio 20.37% 19.88%

The sensitivity analysis for interest rate risk illustrates how changes in the fair value or future cash flows of a financial instrument at the reporting date will

fluctuate in response to assumed movements in market interest rates. The management monitors the sensitivity of reported fair value of financial

instrument on a regular basis by assessing the projected changes in the fair value of financial instruments held by the portfolios in response to assumed

parallel shift in the yield curve by +/- 100 basis points.

The Company’s approach to managing capital involves managing assets, liabilities and risks in a coordinated and concerted manner, assessing shortfalls

between reported and required capital levels on a regular basis and taking appropriate actions to influence the capital position of the Company in light of

changes in economic conditions and risk appetites. An important aspect of the Company's overall capital management process is the setting of target risk

adjusted rates of return which are aligned to performance objectives and risk appetite to ensure that the Company is focused on the creation of value for all

stakeholders.

Funding strategies: The Company has established a funding strategy that provides effective diversification in the sources and tenure of funding. It should

maintain an ongoing presence in its chosen funding markets and strong relationships with funding sources to promote effective diversification. Over-

reliance on a single source of funding should be avoided through implementing counter party limits and in-turn mitigate any adverse interest rate impact.

Volume limits of the Trading portfolio: Though maximum tolerance levels are stated for the trading portfolio of the company, the limits on individual tenor

and volume to be decide by dealers based on the prevailing market conditions and forwarded to Asset and Liability Committee (ALCO) and Board of

Directors for formal approval.

The Company’s objectives when managing capital are to safeguard the Company’s ability to continue as a going concern in order to provide returns for

shareholders and benefits for other stakeholders and to maintain an optimal capital structure to reduce the cost of capital.

In order to maintain or adjust the capital structure, the Company may adjust the amount of dividends paid to shareholders, return the capital to

shareholders, issue new shares or sell assets to reduce debt.

Consistent with others in the industry, the Company monitors capital on the basis of risk weighted capital adequacy ratio as prescribed by the Central Bank

of Sri Lanka. This ratio is calculated as available capital divided by risk weighted assets. The minimum capital adequacy ratio is 8%. Total capital is

calculated as ‘equity’ including preference shares.

20142015

Cut loss policy of the trading portfolio: In an adverse interest rate scenario dealers should implement the cut loss policy and should exit from the trading

portfolio as laid down by policy paper.

The Company is exposed to government securities price risk. This arises from investments held by the Company for which prices in the future are

uncertain. The Company’s policy requires that the overall market position is monitored on a daily basis by the company’s chief dealer and senior dealers

and also is reviewed on a quarterly basis by the Board of Directors. Compliance with the Company’s investment policies are reported to the Board.

[DC 2] Page 19

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

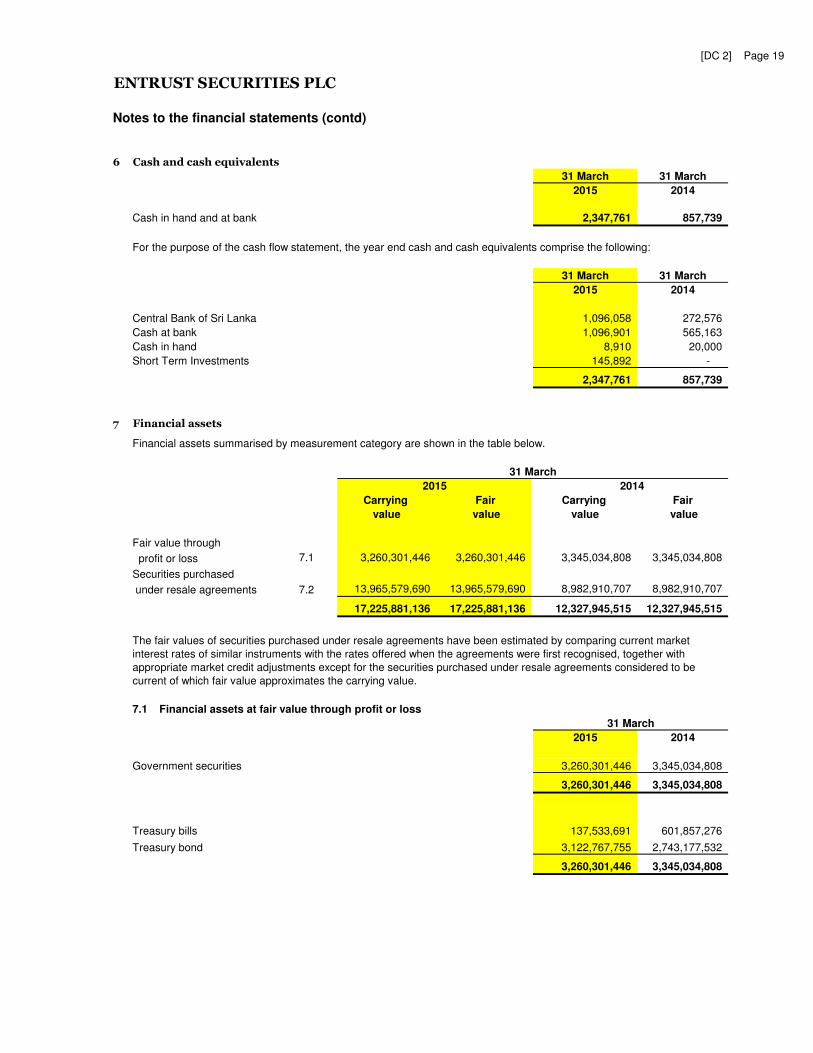

6 Cash and cash equivalents

31 March 31 March

2015 2014

Cash in hand and at bank 2,347,761 857,739

For the purpose of the cash flow statement, the year end cash and cash equivalents comprise the following:

31 March 31 March

2015 2014

Central Bank of Sri Lanka 1,096,058 272,576

Cash at bank 1,096,901 565,163

Cash in hand 8,910 20,000

Short Term Investments 145,892 -

2,347,761 857,739

7 Financial assets

Financial assets summarised by measurement category are shown in the table below.

Carrying Fair Carrying Fair

value value value value

Fair value through

profit or loss 7.1 3,260,301,446 3,260,301,446 3,345,034,808 3,345,034,808

Securities purchased

under resale agreements 7.2 13,965,579,690 13,965,579,690 8,982,910,707 8,982,910,707

17,225,881,136 17,225,881,136 12,327,945,515 12,327,945,515

7.1 Financial assets at fair value through profit or loss

2015 2014

Government securities 3,260,301,446 3,345,034,808

3,260,301,446 3,345,034,808

Treasury bills 137,533,691 601,857,276

Treasury bond 3,122,767,755 2,743,177,532

3,260,301,446 3,345,034,808

The fair values of securities purchased under resale agreements have been estimated by comparing current market

interest rates of similar instruments with the rates offered when the agreements were first recognised, together with

appropriate market credit adjustments except for the securities purchased under resale agreements considered to be

current of which fair value approximates the carrying value.

31 March

2015

31 March

2014

[DC 2] Page 20

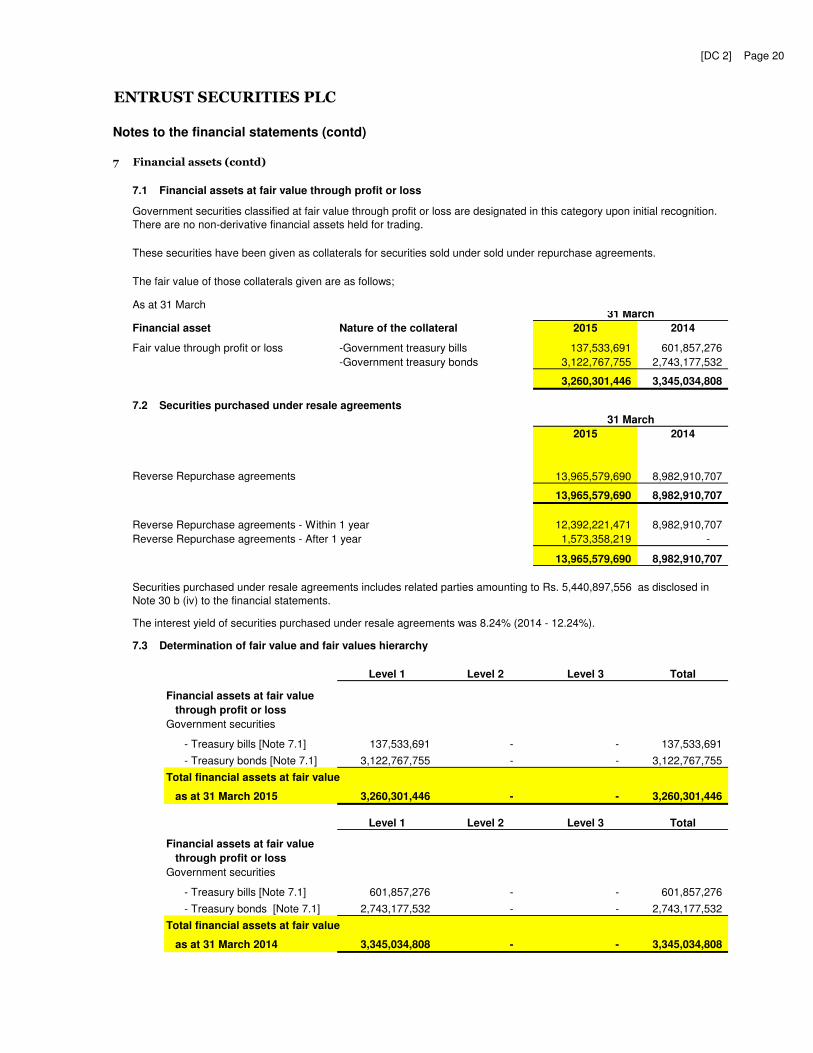

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

7 Financial assets (contd)

7.1 Financial assets at fair value through profit or loss

These securities have been given as collaterals for securities sold under sold under repurchase agreements.

The fair value of those collaterals given are as follows;

As at 31 March

Financial asset Nature of the collateral 2015 2014

Fair value through profit or loss -Government treasury bills 137,533,691 601,857,276

-Government treasury bonds 3,122,767,755 2,743,177,532

3,260,301,446 3,345,034,808

7.2 Securities purchased under resale agreements

2015 2014

Reverse Repurchase agreements 13,965,579,690 8,982,910,707

13,965,579,690 8,982,910,707

Reverse Repurchase agreements - Within 1 year 12,392,221,471 8,982,910,707

Reverse Repurchase agreements - After 1 year 1,573,358,219 -

13,965,579,690 8,982,910,707

The interest yield of securities purchased under resale agreements was 8.24% (2014 - 12.24%).

7.3 Determination of fair value and fair values hierarchy

Level 1 Level 2 Level 3 Total

Financial assets at fair value

through profit or loss

Government securities

- Treasury bills [Note 7.1] 137,533,691 - - 137,533,691

- Treasury bonds [Note 7.1] 3,122,767,755 - - 3,122,767,755

Total financial assets at fair value

as at 31 March 2015 3,260,301,446 - - 3,260,301,446

Level 1 Level 2 Level 3 Total

Financial assets at fair value

through profit or loss

Government securities

- Treasury bills [Note 7.1] 601,857,276 - - 601,857,276

- Treasury bonds [Note 7.1] 2,743,177,532 - - 2,743,177,532

Total financial assets at fair value

as at 31 March 2014 3,345,034,808 - - 3,345,034,808

Government securities classified at fair value through profit or loss are designated in this category upon initial recognition.

There are no non-derivative financial assets held for trading.

31 March

31 March

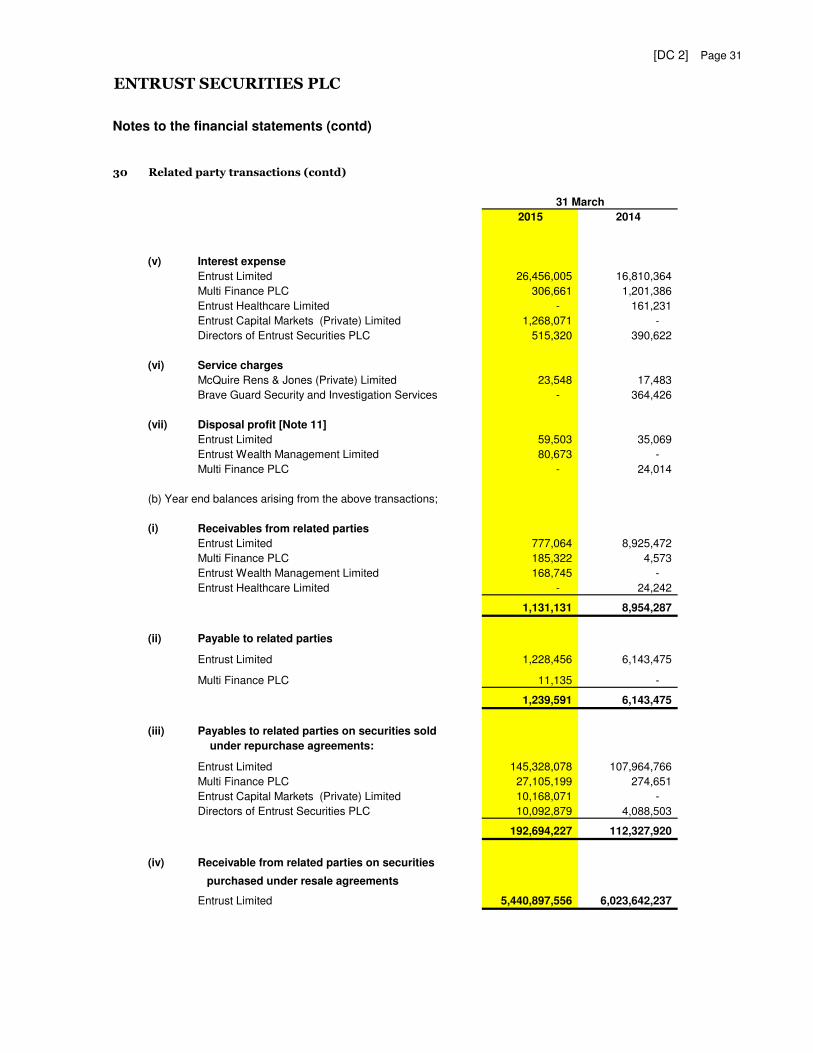

Securities purchased under resale agreements includes related parties amounting to Rs. 5,440,897,556 as disclosed in

Note 30 b (iv) to the financial statements.

[DC 2] Page 21

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

7 Financial assets (contd)

7.4 Fair value estimation

•

•

•

Level 1 31 March 31 March

2015 2014

Assets

Financial assets at fair value through profit or loss

- Government securities 3,260,301,446 3,345,034,808

3,260,301,446 3,345,034,808

Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that

is, as prices) or indirectly (that is, derived from prices) (Level 2);

Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs) (Level 3).

The table below analyses financial instruments carried at fair value, by valuation method. The different levels have been

defined as follows:

The following table presents the Company’s assets and liabilities that are measured at fair value at 31st March 2014 and

31st March 2015.

Quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1);

[DC 2] Page 22

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

8 Deposits, prepayments and other receivables

31 March 31 March

2015 2014

Deposits in Lanka Financial Services Bureau 1,000,000 1,000,000

Advances and prepayments 2,862,746 5,182,749

Other receivables 9,292,217 9,810,286

Receivable from related parties [Note 30 b (i)] 1,131,131 8,954,287

14,286,094 24,947,322

9 Gratuity fund investment

31 March 31 March

2015 2014

Fund asset at beginning of year 5,578,032 5,235,709

Increase of Investment to the fund 761,905 -

408,423 507,323

Settlements during the year (99,000) (165,000)

Fund asset at the end of year 6,649,360 5,578,032

10

Net book value value Net book value Realised value

Furniture and fittings - - 1,380,932 477,942

Office equipment - - 837,161 1,752,515

Computer equipment - - 6,739 9,600

- - 2,224,832 2,240,057

31 March 201431 March 2015

Interest received on the assets

Above balance represents the fund maintained in a separate securities purchased under resale agreement

to meet employees' retirement gratuity obligation.

During the last financial year the Company has shifted to new office location which results to cease some of

its fixed assets used in previous premises. Management has decided to recover the carrying value of those

assets through sale and accordingly re-classified above fixed assets not in use as “Assets held for sale”.

The carrying value and realisable value of assets held for sale was as follows;

Assets held for sale

[DC 2] Page 23

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

11 Property, plant and equipment

Land Furniture Computer and Office Motor Total

equipment equipment vehicle

At 31 March 2013

Cost 72,025,400 5,856,940 12,079,899 5,127,939 5,200,182 100,290,360

Accumulated depreciation - (3,279,463) (9,625,254) (3,326,249) (1,711,693) (17,942,659)

Net book amount 72,025,400 2,577,477 2,454,645 1,801,690 3,488,489 82,347,701

Year ended 31 March 2014

Opening net book amount 72,025,400 2,577,477 2,454,645 1,801,690 3,488,489 82,347,701

Additions during the year - 6,357,669 953,590 2,289,375 - 9,600,634

Disposals during the year - (16,185) (46,883) (42,443) (3,404,665) (3,510,176)

Re-classification - Cost - (1,380,932) (6,739) (837,161) - (2,224,832)

Depreciation charges [Note 20] - (1,422,426) (1,378,306) (874,961) (83,824) (3,759,517)

Closing net book amount 72,025,400 6,115,603 1,976,307 2,336,500 - 82,453,810

At 31 March 2014

Cost 72,025,400 6,295,671 12,747,982 3,892,601 118,448 95,080,102

Accumulated depreciation - (180,068) (10,771,675) (1,556,101) (118,448) (12,626,292)

Net book amount 72,025,400 6,115,603 1,976,307 2,336,500 - 82,453,810

Year ended 31 March 2015

Opening net book amount 72,025,400 6,115,603 1,976,307 2,336,500 - 82,453,810

Additions during the year - 55,161 494,757 116,029 - 665,947

Disposals during the year-Cost - - (520,806) (118,448) (639,254)

Accumilated depriciation of disposals 372,866 118,448 491,314

Re-classification-Cost (Refer below C) 955,155 (955,155) -

' -Accumulated depriciation (943,177) 943,177 -

Depreciation charges [Note 20] - (1,943,005) (1,193,438) (852,151) - (3,988,594)

Closing net book amount 72,025,400 4,227,759 1,141,664 1,588,400 - 78,983,223

At 31 March 2015

Cost 72,025,400 6,350,832 13,677,088 3,053,475 - 95,106,795

Accumulated depreciation - (2,123,073) (12,535,424) (1,465,075) - (16,123,572)

Net book amount 72,025,400 4,227,759 1,141,664 1,588,400 - 78,983,223

(C)During the year company has reclassified office equipments worth of Rs.972,226(accumulated depriciation - Rs 959,684) to computer

equipements & Rs.17,070 (Accumulated depriciation- Rs.16,508) vice versa.

(a) The cost of fully depreciated assets still in use as at 31 March 2015 amounted to Rs 11,618,881 (2013 - Rs 9,743,526).

(b) Land owned by the Company comprises of 17.29 perches and is located in Colombo 3. The market value of the land as at 31st March

2015 is Rs. 100 Million approximately.

[DC 2] Page 24

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

11 Property, plant and equipment (contd)

(a)

(b)

31 March 31 March

2015 2014

- 4,900,700

- (1,511,049)

Disposals - (3,389,651)

- -

12 Stated capital

Number of Value

shares (Rs)

As at 31 March 2015 33,000,014 220,000,070

As at 31 March 2014 33,000,014 220,000,000

13 Financial liabilities

31 March 31 March

2015 2014

- Government securities sold under repurchase agreements 16,105,066,376 11,373,802,669

Accumulated depreciation

During the year, the company transferred property, plant and equipment which net book value of Rs

60,660 (2014 - Rs 162,639) to related parties and generated a disposal profit of Rs 140,176 (2014 -

Rs. 59,083).

Payable under repurchase agreements includes related parties as disclosed in Note 30 b (iii) to the

financial statements.

Cost- capitalised finance leases

Property, plant and equipment includes motor vehicle acquired under finance lease, the net book

value of which is made up as follows:

Net book amount as at year end

Average interest paid percentage on government securities sold under repurchase agreements was 7.41%

(2014 - 10.99%)

The addition of Rs. 70 represents the value of seven (7) ordinary shares of Rs. 10 each, initially allotted to

the promoters of the Company which were subsequently transferred to the holding Company, Entrust

Limited at the time of the Company's listing on the Colombo Stock Exchange. With the restructuring of

Entrust Group on 27 May 2014, Entrust Limited transferred its existing shareholding of Entrust Securities

PLC to the new holding Company i.e. Entrust Holdings Limited. Since the value of the above mentioned

Promoters' shares had been omitted from the Company's books of accounts since inception and also since

the amount is immaterial, the Company has subsequently adjusted this omission, during the current year.

[DC 2] Page 25

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

14 Accruals, provisions and other payables

31 March 31 March

2015 2014

Accrued expenses [refer (a) below] 3,462,658 4,543,911

Other payables [refer (b) below] 30,632,039 40,952,713

Payable to related parties [Note 30 b (ii)] 1,239,591 6,143,475

35,334,288 51,640,099

(a)

(b)

15 Post-employment benefit obligation - gratuity

31 March 31 March

2015 2014

Present value of unfunded obligation 7,600,684 5,921,674

Liability in the statement of financial position 7,600,684 5,921,674

31 March 31 March

2015 2014

At beginning of year 5,921,674 4,709,182

Current service costs 814,906 697,392

Interest costs 589,202 533,668

Actuarial loss 282,902 146,432

Receipts due to staff in-transfers 91,000 -

Payments made during the year (99,000) (165,000)

At end of year 7,600,684 5,921,674

The amounts recognised in the statement of comprehensive income are as follows:

31 March 31 March

2015 2014

Statement of income:

- Current service cost 814,906 697,392

- Interest cost 589,202 533,668

Total included in the staff costs [Note 21] 1,404,108 1,231,060

Other comprehensive loss:

- Actuarial loss 282,902 146,432

The movement in the defined benefit obligation over the year is as follows:

Accrued expenses mainly consist of printing and publication expenses Rs 1,400,000 (2014 - Rs

1,500,000) and sales commission Rs 262,480 (2014 - Rs 164,389).

Other payables mainly consist of bonus payable of Rs 26,359,337 (2014 - Rs. 35,323,436) and

miscellaneous payable of Rs 727,966 (2014 - Rs 3,039,025) relating to unpresented cheques.

Post-employment benefit obligation comprises of provision for gratuity. The amounts recognised in the

statement of financial position are determined as follows:

[DC 2] Page 26

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

15 Post-employment benefit obligation - gratuity (contd)

The principal actuarial assumptions used were as follows:

31 March 31 March

2015 2014

Discount rate per annum 10.03% 12.13%

Annual salary increment rate 12.00% 12.00%

Retiring age 55 55

Staff turnover 12.50% 22.22%

Sensitivity analysis of key actuarial assumptions used:

1% increase 1% decrease 1% increase 1% decrease

54,575 (51,588) (52,026) 56,105

- - 58,745 (58,744)

16 Interest income on government securities

2015 2014

Interest income on investment and trading securities 342,359,848 318,308,390

944,937,549 840,415,170

1,287,297,397 1,158,723,560

17 Interest expense

2015 2014

Interest expenses on government securities sold

under repurchase agreements (1,018,251,931) (976,342,224)

18 (Losses) /gains from revaluation of government securities

2015 2014

Treasury bonds (120,441,000) 57,015,000

Treasury bills (854,000) 758,000

(121,295,000) 57,773,000

Year ended 31 March

Interest income on securities purchased under resale agreements

Discount rate

Year ended 31 March

Year ended 31 March

Future salary increases

- Interest

The effect on;

-The current service cost

[DC 2] Page 27

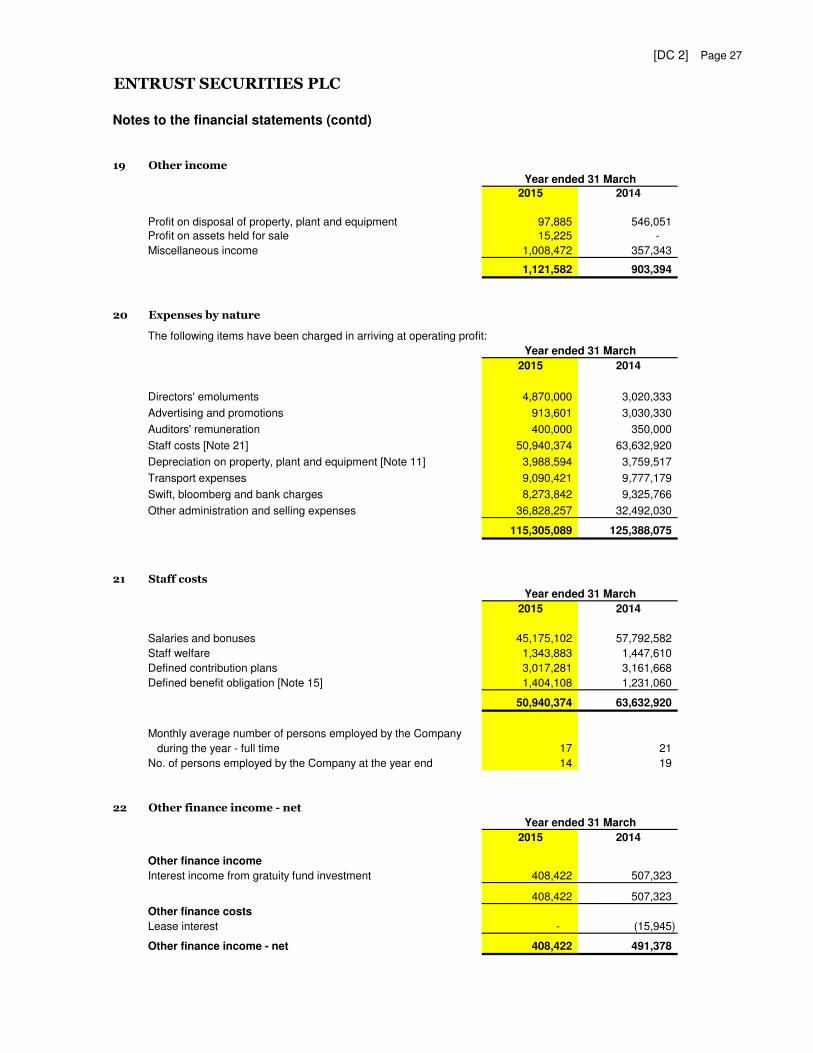

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

19 Other income

2015 2014

Profit on disposal of property, plant and equipment 97,885 546,051

Profit on assets held for sale 15,225 -

Miscellaneous income 1,008,472 357,343

1,121,582 903,394

20 Expenses by nature

2015 2014

Directors' emoluments 4,870,000 3,020,333

Advertising and promotions 913,601 3,030,330

Auditors' remuneration 400,000 350,000

Staff costs [Note 21] 50,940,374 63,632,920

Depreciation on property, plant and equipment [Note 11] 3,988,594 3,759,517

Transport expenses 9,090,421 9,777,179

Swift, bloomberg and bank charges 8,273,842 9,325,766

Other administration and selling expenses 36,828,257 32,492,030

115,305,089 125,388,075

21 Staff costs

2015 2014

Salaries and bonuses 45,175,102 57,792,582

Staff welfare 1,343,883 1,447,610

Defined contribution plans 3,017,281 3,161,668

Defined benefit obligation [Note 15] 1,404,108 1,231,060

50,940,374 63,632,920

Monthly average number of persons employed by the Company

during the year - full time 17 21

No. of persons employed by the Company at the year end 14 19

22 Other finance income - net

2015 2014

Other finance income

Interest income from gratuity fund investment 408,422 507,323

408,422 507,323

Other finance costs

Lease interest - (15,945)

Other finance income - net 408,422 491,378

The following items have been charged in arriving at operating profit:

Year ended 31 March

Year ended 31 March

Year ended 31 March

Year ended 31 March

[DC 2] Page 28

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

23 Income taxes and VAT on financial services

(a)

(b)

24 Withholding Tax

25 Earnings per share

2015 2014

Net profit attributable to shareholders (Rs) 220,916,273 274,503,679

Weighted average number of ordinary shares in issue 33,000,014 33,000,014

Earnings per share (Rs)

- basic 6.69 8.32

26 Dividend per share

(a)

The Company pays Withholding Tax at source on purchase of treasury Bills and treasury Bonds. The

Company recognises interest income from those instruments net of Withholding Tax paid.

No income tax is provided as the management is of the view that the Company's interest income

is not liable and not a part of its assessable income for income tax under section 32 as it is in the

business of primary dealer. Further, the company does not pay VAT on financial services under

section 25 (A) as the management is of the opinion that the Company is not in the business of

providing financial services. Except as noted in Note 23 (b), the Company has not received any

assessment of income tax and VAT on financial services from the Department of Inland

Revenue.

Earnings per share is calculated by dividing the net profit attributable to shareholders by the weighted

average number of ordinary shares in issue during the year.

The Department of Inland Revenue has issued an assessment for the income tax for the year of

assessment 2003/2004. The appeal made by the Company against the said notice of

assessment had been determined by the Commissioner General of Inland Revenue reducing the

assessable income. Accordingly, the income tax payable for the year of assessment 2003 / 2004

is LKR 29,099,850 (excluding penalty that is limited to a maximum of 50% of the amount of tax

outstanding).The Company is of the opinion that there's no further tax liability with the

representations made by tax advisor according to the Inland Revenue Act No.10 of 2006.

However, The Company made a petition of appeal to the Board of Review against the said

determination of the Commissioner General of Inland Revenue and the Board of Review has

made its determination confirming the determination of the Commissioner General of Inland

Revenue.

Therefore, the Company filed a case in the Court of Appeal seeking the determination on the

questions of law arising on the stated case of the Board of Review. The case is still pending.

Year ended 31 March

The Company has distributed a dividend of Rs 1.61 per share amounting to Rs 53.13 million on

10 October 2014.

[DC 2] Page 29

ENTRUST SECURITIES PLC

Notes to the financial statements (contd)

27 Cash generated from operations

Reconciliation of profit before tax to cash generated from operations:

2015 2014

Profit before income tax 220,916,273 274,503,679

Adjustments for:

Depreciation [Note 11] 3,988,594 3,759,517

Loss / (gain) from revaluation of government securities 121,295,000 (57,773,000)

Provision for gratuity [Note 15] 1,404,108 1,231,060

Changes in operating assets and liabilities:

- Financial assets Fair value through profit or loss (36,561,638) (1,168,157,829)

- Securities purchased under resale agreements (4,982,668,983) (4,233,566,201)