Crude Palm Oil - Nirmal Bang · PDF file2 Crude Palm Oil Market Outlook & Future Prospects May...

10

Crude Palm Oil Market Outlook & Future Prospects Crude Palm Oil Market Outlook & Future Prospects

-

Upload

doankhuong -

Category

Documents

-

view

220 -

download

3

Transcript of Crude Palm Oil - Nirmal Bang · PDF file2 Crude Palm Oil Market Outlook & Future Prospects May...

Crude Palm OilMarket Outlook

&Future Prospects

Crude Palm OilMarket Outlook

&Future Prospects

2

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

It has been a roller-coaster ride for the edible oil industry since palm-oil production nosedived in

the mid-2015 thereby shaking up countless industries closely linked with it. The demand for food,

detergent, cosmetic and bio-fuels have depicted an ever-increasing trend with an over-

dependence on palm oil, the key-ingredient. With the recent supply bottleneck, the palm oil

industry, which is reeling under the perils set by a drought, is further pushed to a crisis mode.

Being a high-yielding crop and having a higher concentration of saturated fat makes palm oil a

preferred (cheaper) component for foods, cosmetics and bio-fuel use. The shortage of this edible

oil, which accounts for over 55% of the total vegetable oils produced and traded across the globe,

has sent shock waves to the major industries making use of it. The suppliers of palm oil are a few,

while the demand is driven from various corners of the globe. However, recently few other

regions in Africa and Latin America have also joined the palm producers’ bandwagon under the

cloak of major trading companies. Hopefully, with the expansion of plantations as well as with

the development of newer ones in non-conventional regions, the supply-side issues are expected

Low High

Med

Kunal Shah Research Head-Commodities

Anish G Research Analyst

Edible Oils & Oilseeds

PALM OIL - FUELLING THE EDIBLE OIL RALLY?

3

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

to slow down.

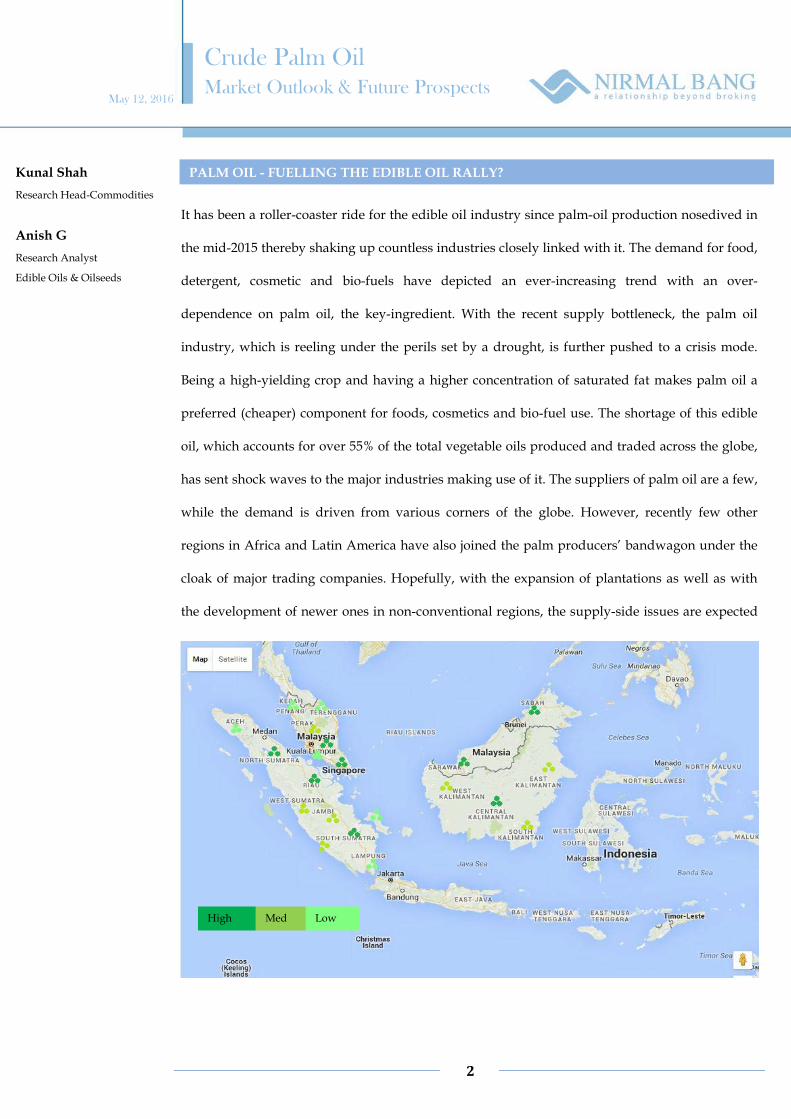

The output from major regions in Indonesia (especially Sumatra and Kalimantan) and Malaysia,

which supplies the bulk of palm oil produced across the globe, have been depicted alongside

using color gradient. (Source: NB Research)

The warmer and drier conditions in the past few months shadowed the prospects of many

agrarian economies including that of India. Without doubt, one can easily decipher the losses

incurred due to the El-Nino induced drought in South-Asia. Now that the IMD has observed that

the 2016 monsoon is almost likely to be either above normal (greater than 5% above normal) or

neutral (within 5% of normal), at 41% and 50% respectively, the crop conditions are expected to

revive. Most importantly, the clout of La Nina may be experienced during the second half of 2016,

post the ENSO-neutral in early summer.

It is observed that since April 2016, below average SST (Sea-Surface Temperature) are apparent in

the equatorial Pacific Ocean near the South American continent, while the El-Nino conditions are

supposed to take an exit stage left by mid-June. The major palm oil producers will finally get a

breather from the drier conditions which spanned the latter half of 2015 till early 2016.

At the time of drafting this report, the news of crop damage due to heavy rains in Argentina had

rattled the soy market globally. On 21st of April 2016, the CBOT soy oil climbed till 35.14 cents/lb,

while DCE soy oil touched CNY 6,514 per MT. The NCDEX soy oil futures jumped to Rs. 682.70

per 10 kg gaining cues from the trend overseas.

The ready-to-be-harvested patches of soybeans in Argentina (the largest supplier of soybean meal

and 3rd largest producer of soybeans globally) were drenched by heavy downpours, which lifted

COMPETING SOYBEAN OIL

WEATHER

4

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

the prices to unexpected highs. A preliminary survey by the industry experts pointed at a grim

scenario with around 1/3rd of farms being water-logged and around 4 million metric tonnes of

losses anticipated upfront. The concerns of lower yield and reduced quality are also in the loom.

Meanwhile, many regions affected by rains have started complaining about pest attacks, which

are likely to diminish the quality and quantity of the output. The global soybean surplus is likely

to be reduced thereby providing an elaborate window for a positive price trend further.

Of late, the Argentine ports have resumed shipping of soybean consignments, after heavy rains

had disrupted the movement. The weather conditions are returning to normalcy which has made

the harvesting speedier. With adverse environmental conditions in the loom, Argentina will have

to battle hard to retain itself as the No.1 soybean meal exporter in the world. With Brazil

devaluing Real and incentivizing exports, it will set a tough battle for its peers in the global

soybean trade.

It is also anticipated that in few regions in the US, farmers will shift from corn to soybean and

cotton. The rains that fell during the end of March this year on Louisiana, Mississippi, and

Arkansas have wreaked more damage to the fields that hadn’t recovered from the torrential rains

during mid-March 2016. The rains washed off around 10% of the state’s total corn crop during

mid-March, with further rains causing additional harm to the prevailing crop. Frequent and

heavy rains have also led many in Missisippi to replant the region with soybean. Soybean

planting can continue till June 7th, 2016.

Meantime, the plantations in Indonesia and Malaysia are expected to recover from the low yields

and declining production as the precipitation and temperature conditions have already started to

regain strength. The yield levels have dropped by 4-5% in majority of the regions in South-East

Asia. The deficit production of palm oil from Indonesia and Malaysia had triggered a rally in the

TRADE SCENARIO

5

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

prices beginning from the tail end of the 4th quarter in 2015. The rally extended till the end of first

quarter in 2016 when finally the news of resumption of the production hit the markets. While the

island nations have witnessed favourable weather returning to the oil palm plantations gradually,

the output concerns are still on the loom. However, the recent reports from Malaysia pointing at

the gradual rise in production came as a relief to the major importers.

The price trend of crude palm oil in Bursa Malaysia and MCX-India has been depicted during the

period Jan-Apr in the year 2015 and 2016. The price of crude palm oil has surged almost 23%

during January till April in 2016 in comparison to the prices prevailing during 2015.

(Source: NB Research)

The increasing prices of rivaling oils (caused by the South American floods) helped the CPO

prices to gain strength. In India, with the monsoon likely to be above LPA, the upcoming kharif

oilseed crop would be at par with the 5-year average. As the yield and production of oilseeds

realigns with the expectations, the oil extraction will turn out to be feasible and it is expected that

the market will recover from its perils.

300

350

400

450

500

550

600

650

1900

2150

2400

2650

2900

3150

3400

INR/

10Kg

MYR

/Met

ric

Tonn

e

BMD Futures 2015 BMD Futures 2016 MCX Futures 2015 MCX Futures 2016

6

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

The exports of Crude Palm Oil from Malaysia during Jan-Apr 2016 in comparison to that of 2015

have been represented graphically as under.

(Source: MPOB, NB Research)

The deficit production of palm oil triggered higher off take by traders, expecting the prices to

climb high. The exports of crude palm oil picked up while stockpiles in the island nation began to

deplete. The production showed signs of recovery by the month of March. But still, the traders in

Malaysia expect a higher price due to lower stockpiles.

The imports of crude palm oil during 2015-16 surged owing to the failure of domestic oilseed crop

during the kharif season 2015. Also, the demand for imported oils surged as the domestic oilseed

crop prices were found to be unviable for crushing. As a result, many crushing units were shut

for a brief period of time, citing losses. Also, imported oils fetched a better price compared to

those produced in the home country. The CPO prices were ruling low during mid-2015 which

provided ample opportunity for the importers to stockpile crude palm oil and RBD palm oil. The

spike in palm oil prices were much anticipated as the drought conditions were reported to be

severe in many of the regions in Indonesia and Malaysia. Indonesia, in particular, Sumatra and

0 20000 40000 60000 80000

100000 120000 140000 160000

in M

etri

c To

nnes

Exports-2016 Exports-2015

INDIAN IMPORTS OF CRUDE PALM OIL

7

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

Kalimantan were fuming with forest fires which aggravated the situation. The forest fires had

created a blanket of smoke around nearby island nations as well, threatening the prospects of

crop growth in those areas.

(Source: Solvent Extractors’ Association of India)

The stockpiling of palm oil by India and the renewed bio-diesel policy by Indonesia provided

hopes for a spike in prices, which had already climbed to MYR 2420, the highest level since 18

months. As further news of production losses poured in, crude palm oil touched MYR 2742,

highest in 23 months.

The palm oil production has started to show the signs of revival from the drought that had

grappled the major producers. However, the productivity of the oil palm hasn’t depicted much

needed strength. It may take another few months to resuscitate the palm plantations and to

bridge the demand-supply gap. Meanwhile, the soybean and soy oil from Latin America has

started to fill the import basket of many economies. We can witness an increased off take of soy

derivatives by China, thereby reducing the dependence on Palm products. With the focus shifting

to soy derivatives, palm oil exports is likely to take a hit. It is expected that China will create a

0 100000 200000 300000 400000 500000 600000 700000 800000 900000

1000000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

in M

etri

c To

nnes

2014-15 2015-16

GLOBAL SCENARIO & PRICE OUTLOOK

8

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

new record in terms of the volumes of soybean and its derivatives being imported. The meal

market in China is likely to support the import of soybean and soy meal.

With a prediction of above normal monsoon in India, the kharif oilseeds production may return

to the beaten tracks. If so, India’s dependency on Palm oil constituents may ease a little. Also,

taking into account the drought faced by many states India, the government policies are likely to

support oilseeds and other crops which are less dependent on water, rather than on cotton and

sugar, which require high water consumption.

Though the produce from Argentina might decline in quality and quantity, Brazil’s bumper crop

can suffice for the requirements. It is to be noted that the floods in Argentina have washed away a

part of the soybeans that would have added to the world surplus. Still, in the global perspective,

we are running a surplus of 6-7 million metric tonnes. Also, the US soybean plantings have begun

with some shifts from corn to soybean being observed in few regions. The output from US

plantings is also expected to be higher, if not be the same as that of the previous year.

Noteworthy is the fact that last year Malaysian Ringgit was the only Asian currency that

underwent a sharp depreciation with respect to US Dollar, thereby incentivizing the exports from

Malaysia. The currency factor holds to be an important aspect in determining the prices of palm

products exported from the country.

Also, the recent step taken by France to impose softer tax on palm oil used for food may be

replicated elsewhere, with an intention to promote environment-friendly palm products. This has

raised eyebrows of top producers who have vehemently opposed this move. However, with

environmentalists across the globe voicing their concerns to promote RSPO certified palm oil, the

traditional slash-and-burn expansions may not be encouraged.

9

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

Price Outlook: Currently, CPO is trading at MYR 2690 at BMD. After a detailed analysis of the

situation, it is expected that the palm oil prices may return to MYR 2480 post June 2016.

However, the upside movement is likely to be capped at MYR 2700. It is also suggested to keep a

close watch on the currency fluctuations as well. A temporary surge in the palm oil prices in near

term may be fuelled by festivities. Nevertheless, another bull run is unlikely on the long term.

In MCX, the CPO futures may find a support at Rs. 510 per 10 kg by June 2016. The upside

movement is likely to remain capped at Rs. 570 per 10 kg.

(Source: Reuters)

As observed from the graph above, the spread between soy oil (NCDEX June) and CPO (MCX

June) have narrowed from 220.70 (Q4, 2015) to 103.00 (Q1, 2016) which has now reached 114.40. It

is expected that the palm oil prices will witness a decline from the present levels while soy oil

may remain supported due to the squeezing supplies in the domestic market. The spread between

soy oil and palm oil is expected to gradually stride to 160.00 levels in the subsequent quarter.

10

Crude Palm Oil Market Outlook & Future Prospects

May 12, 2016

Disclaimer: This Document has been prepared by N.B. Commodity Research (A Division of Nirmal Bang Commodities Pvt. Ltd). The information, analysis and estimates contained herein are based on N.B. Commodities Research assessment and have been obtained from sources believed to be reliable. This document is meant for the use of the intended recipient only. This document, at best, represents N.B. Commodities Research opinion and is meant for general information only. N.B. Commodities Research, its directors, officers or employees shall not in any way be responsible for the contents stated herein. N.B. Commodities Research expressly disclaims any and all liabilities that may arise from information, errors or omissions in this connection. This document is not to be considered as an offer to sell or a solicitation to buy any securities. N.B. Commodities Research, its affiliates and their employees may from time to time hold positions in securities referred to herein. N.B. Commodities Research or its affiliates may from time to time solicit from or perform investment banking or other services for any company mentioned in this document.

Address: Nirmal Bang Commodities Pvt. Ltd., B2, 301 / 302, 3rd Floor, Marathon Innova, Opp. Peninsula Corporate Park, Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013, India

Research Team

Kunal Shah Head of Research [email protected]

Devidas Rajadhikary Sr. Technical Analyst [email protected]

Harshal Mehta Sr. Technical Analyst [email protected]

Mohammed Azeem Technical Analyst [email protected]

Ravi D’souza Research Analyst [email protected]

Anish G Research Associate [email protected]

Nikhil Murali Research Associate [email protected]

Smit Bhayani Research Associate [email protected]