Crowdfunding Real Estate: Reg A+ Offerings and Intrastate...

70

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Presenting a live 90-minute webinar with interactive Q&A Crowdfunding Real Estate: Reg A+ Offerings and Intrastate Exemptions Leveraging New Capital Raising Opportunities for Real Estate Fund Sponsors and Developers Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific THURSDAY, APRIL 7, 2016 Kenneth A. Kecskes, Partner, Fox Rothschild, San Francisco & Los Angeles Anthony J. Zeoli, Partner, Freeborn & Peters, Chicago

Transcript of Crowdfunding Real Estate: Reg A+ Offerings and Intrastate...

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Crowdfunding Real Estate: Reg A+

Offerings and Intrastate Exemptions Leveraging New Capital Raising Opportunities for Real Estate Fund Sponsors and Developers

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, APRIL 7, 2016

Kenneth A. Kecskes, Partner, Fox Rothschild, San Francisco & Los Angeles

Anthony J. Zeoli, Partner, Freeborn & Peters, Chicago

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Crowdfunding Your Next Real Estate Project

An Overview of the Intrastate and “eFund” options

Introduction

• About Me

– Partner with the law firm of Freeborn & Peters LLP in Chicago

– Specialize in securities, commercial finance, real estate and general corporate law

– Industry recognized expert in crowdfunding

– Drafted the Illinois Crowdfunding Exemption Bill (Illinois House Bill 3420)

6

• Traditionally capital options available to real estate developers included mainly:

– Bank financing

– “Friends and Family” financing

– “Angel Investor” financing

• Today there are multiple crowdfunding based options to raise capital for real estate projects

Capital Options

7

What Is Crowdfunding?

• Today the term “crowdfunding” can take on many contexts but it is, by definition, the practice of funding a project or venture by raising small amounts of money from a large number of people, most commonly via the Internet

• When a person/business attempts to raise money through crowdfunding, this process is often called a “crowdfunding campaign” or simply a “campaign”

8

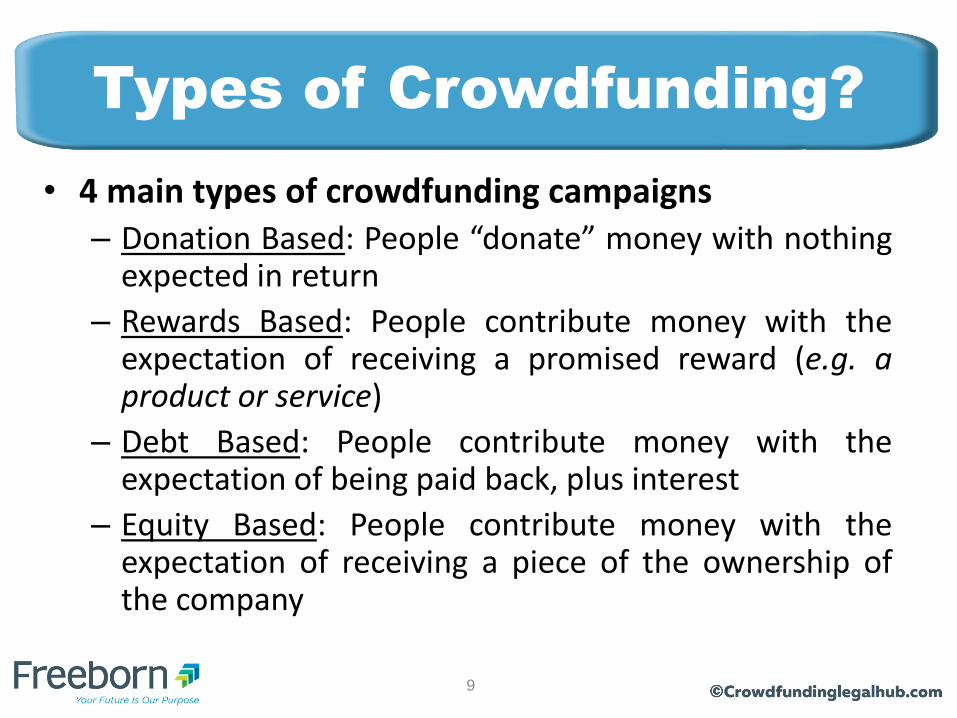

Types of Crowdfunding?

• 4 main types of crowdfunding campaigns – Donation Based: People “donate” money with nothing

expected in return

– Rewards Based: People contribute money with the expectation of receiving a promised reward (e.g. a product or service)

– Debt Based: People contribute money with the expectation of being paid back, plus interest

– Equity Based: People contribute money with the expectation of receiving a piece of the ownership of the company

9

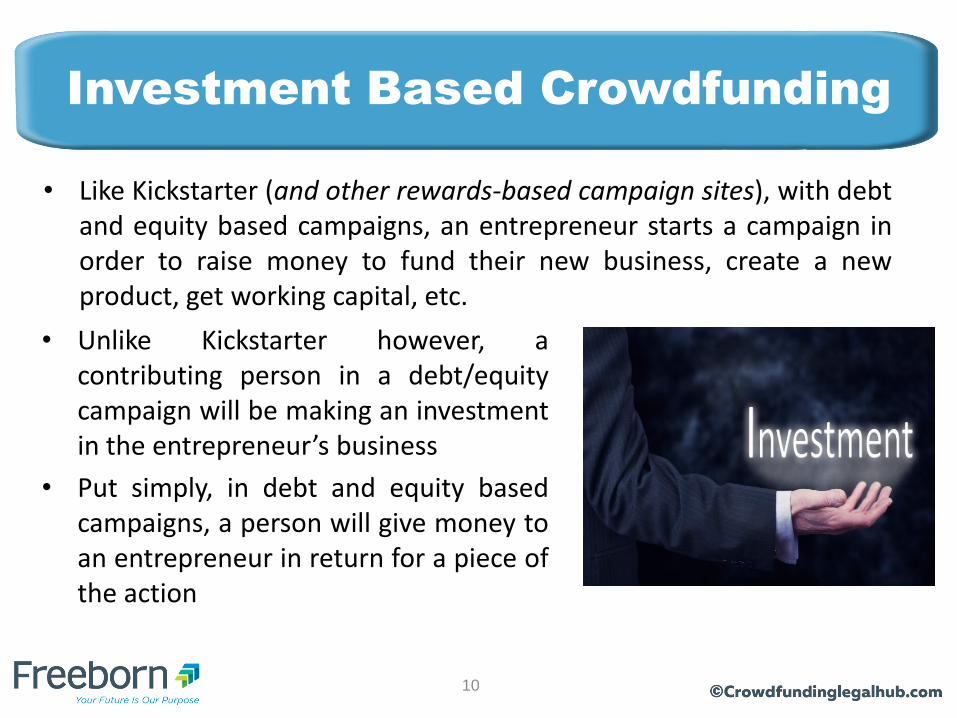

Investment Based Crowdfunding

• Like Kickstarter (and other rewards-based campaign sites), with debt and equity based campaigns, an entrepreneur starts a campaign in order to raise money to fund their new business, create a new product, get working capital, etc.

• Unlike Kickstarter however, a contributing person in a debt/equity campaign will be making an investment in the entrepreneur’s business

• Put simply, in debt and equity based campaigns, a person will give money to an entrepreneur in return for a piece of the action

10

• JOBS Act: – On March 27, 2012, Congress passed the Jumpstart Our Business Startups

(JOBS) Act, a bipartisan effort in both the House and the Senate to ease the regulatory burdens on smaller companies and facilitate capital formation. President Obama signed the legislation into law on April 5, 2012

• Provisions of Interest For Real Estate Developers:

– Title II: Allows for “crowdfunding” by, and public solicitation of, “accredited investors” (i.e. you can now solicit “accredited investors” via the internet)

– Title III: Allows for “crowdfunding” by, and public solicitation of, all investors (i.e. accredited and non-accredited)

– Title IV (Regulation A+): Modifying the existing “Regulation A” to provide for, among other things, an expansion of the exemption to cover offerings of securities up to $50 million (versus the previous $5 million) in any 12-month period

Federal Regulations

11

• Intrastate offerings:

– “Intrastate” simply means that the Issuer and the investors all reside in the same state

– Can solicit “accredited and “non-accredited” investors

– Often state statutes have higher cap amounts than the $1 MM Title III cap and significantly less administrative hurdles

• Status of Intrastate Exemptions:

– Currently 30 states have enacted an Intrastate exemption and 7 states in various stages of enacting/considering legislation

– See www.crowdfundinglegalhub.com

State Regulations

(“Intrastate Offerings”)

12

• Which types of real estate projects will crowdfunding typically work best for? – Fix & flip financing – Value add financing – Construction financing – Income producing property acquisition/

syndication – Syndications of existing properties/portfolios

of properties

• Which types of real estate projects will crowdfunding typically NOT work for? – Acquisition financing (other than for income

producing properties) – Projects with a hard closing/commencement

date of 90 days or less

Real Estate Crowdfunding

13

– Depends on multiple variables, particularly company or project specific risks

– On equity investments, generally expecting between 8-17% ROI (preferred and cumulative )

– On debt investments, generally expecting between 7-15% interest (paid quarterly or annually)

Real Estate Crowdfunding

• What types of returns are investors expecting?

14

How Does It Work?

• All Starts with the “Crowdfunding Portal” – “Crowdfunding Portal” just means

the website through which the offering is being made

– Portal is the go between the investors and the company

– Portal is typically responsible for documenting the deal as well as being the pass through of all informational materials to investors

• Differentiation – Portals typically differentiate themselves by type of

crowdfudnding (e.g. debt, equity, etc.) as well as niche focus (e.g. fix and flip, value add, etc.)

15

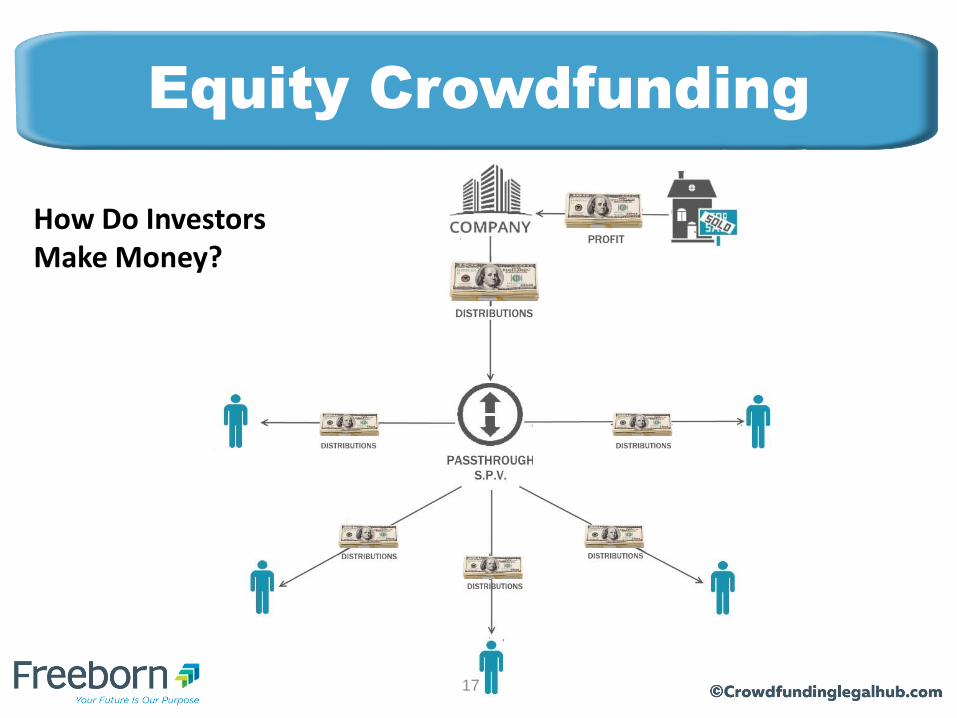

What is happening in an Equity-Based crowdfunding campaign?

Equity Based Crowdfunding Equity Crowdfunding

16

Equity Based Crowdfunding Equity Crowdfunding

How Do Investors Make Money?

17

Debt Crowdfunding

What is happening in a Debt-Based crowdfunding campaign?

18

Debt Crowdfunding

How Do Investors Make Money?

19

Intrastate Offerings

(Generally)

• Company must:

– Be formed and doing business in the state where they are raising funds

– Must meet 80-80-80 test

– Must not be subject to disqualification

• Company must have current financial statements

– Balance sheet, Income Statement, Equity Statement

– May or may not need to be audited (depends on the respective state law and, generally, the maximum amount being raised)

20

Intrastate Offerings

(Generally)

• A company can typically raise between $1-2 Million dollars, per year, from state residents – Note: Most states have the maximum amount

set on a “per company” basis making it effectively a per “project basis” (assuming each project is set up under a new entity)

• Offerings can be debt or equity based

• Investors can generally be “accredited” or “non-accredited” (i.e. anyone so long as they are a resident of the state) – Non-accredited investors will often have

investment caps (based on a straight amount, income level, etc.);

– Generally no limit as to the amount an accredited investor can invest

21

Intrastate Offerings

(Generally)

• Company must establish a maximum minimum offering amount and a funding deadline

– Will need to raise at least the minimum about before the company will receive any money

• Company must enter into an escrow agreement with a qualified escrowee

– Cannot accept money directly; all investor funds will be held in escrow

– Funds will not go to the company until the minimum offering amount is reached

22

Intrastate Offerings

(Generally)

• This can include:

– The minimum/maximum offering amount and deadline

– A copy of the Escrow Agreement

– A description of the company (name, address, etc.) – A detailed description of intended use of the

offering proceeds (including project budget & timeline and fees to be paid to managers)

– Identity of all persons/entities owning > 10% of voting equity

– Identity of all directors/managing officers – Name of all crowdfunding portals, and other

agents, being used in the offering and a description of the consideration

– A description of applicable risk factors

• The company will be required to deliver certain documents/information to prospective investors.

23

Intrastate Offerings

(Generally)

• The company may need to file certain documents with/pay certain fees to the applicable state authority before the offering starts and/or before they can do any marketing of the offering

– Filing requirements and fees vary but are generally not onerous

• Offerings are typically (and in many cases are required to be) conducted through a qualified Internet portal

– In many states, portals will have their own registration requirements

24

Intrastate Offerings

(Generally)

• Only residents of the subject state can view offering materials and invest

– Refers to a person’s “principal residence”

– Company must take reasonable measures to limit access to offering information only to residents of the state

• Cannot just hand out information about the offering to anyone (except for general announcement information)

– Vetting of investors generally done by the portal

• If the company has reason to believe a person is not a resident they must tell the portal

25

Intrastate Offerings

(Generally)

• The company may advertise the offering but ONLY in certain limited ways

• Best practice is to limit advertising to a “general announcement” providing no more than:

– A statement that an offering is being made

– The name and contact information of the company

– The name & web address of crowdfunding portal; and

– Max/min offering amount

• General announcement may be made by any means, including physical signs outside of the property, social media, etc.

• All advertising materials should have a disclaimer saying participation in the opportunity is limited to residents

26

Intrastate Offerings

(Generally)

– Typically only internally prepared statements are required

– May require certification by a senior officer

• Can fulfill requirement by posting financial statements on the company’s website or through the portal

– Must alert investors

• In certain states, the company will be required to deliver quarterly and/or annual financials to investors

27

• Pre-Offering Expenses: – Financial statements (audited)

– State filing fee

– Project development plan/pitch deck

– Offering documents (generally paid through portal)

• Offering Expenses: – Portal fees (generally 4-8% of offering

amount)

– Marketing materials/fees (generally 1-3% of offering amount)

$500 (NewCo) - $10,000

$100 - $500

$2,000 - $5,000

$5,000 - $10,000

$12,000 Avg.

$40,000 - $80,000

$10,000 - $30,000

$75,000 Avg.

Intrastate Offerings

(Generally)

28

• Ongoing Expenses: – Quarterly/Annual Fin. Statements

– Preferred distributions (if any)

– Debt Expenses (P&I)

• All amounts/documents owed to investors are typically sent through to the Portal: – Portal handles transfer of

distributions and payments

– Portal disseminates financial statements and tax documents

Intrastate Offerings

(Generally)

29

• You NEED to have a clear business plan

• Show investors how you are going to use the money to make them money

Intrastate Offerings

(Keys To A Successful Offering)

30

• You NEED to market your offering – Offerings do not sell themselves

– Leverage all modes of advertising

– BUT stick only to the “general announcement” information

• You NEED to be responsive to investors – Answer questions as often and as

fully as possible

– Keep investors in the loop as to status changes (positive or negative)

– Manage expectations

Intrastate Offerings

(Keys To A Successful Offering)

31

• You NEED to budget appropriately

– Budgets should be precise but include a contingency amount

– Things come up, plan accordingly

• You NEED to set realistic goals and timelines – Don’t ask for $4 MM if you know you

won’t get it or don’t need it

– Don’t wait until the last minute (estimate between 45-90 days to close)

Intrastate Offerings

(Keys To A Successful Offering)

32

• You NEED to have your material company/project agreements properly documented including

– Operating Agreement (or other governing document)

– Development/Management Agreements and other material project agreements

– Credit Documents

– Permits

– Etc.

Intrastate Offerings

(Keys To A Successful Offering)

33

• You NEED to properly identify the inherent project and company risks to investors, including:

– Project specific risks

– Company specific risks

– Industry risks

– Market risks

– Etc.

• Rule of thumb

– When in doubt, disclose it

Intrastate Offerings

(Keys To A Successful Offering)

34

• Are there other benefits to crowdfunding besides raising capital?

– Marketing

– Local job creation

– Positive publicity and community support

Intrastate Offerings

(F.A.Q)

35

• So I can just start an Intrastate crowdfunding campaign and I will get money right?

– Many companies will not make it onto a portal at all (not prepared, project too risky, etc.)

– No guaranty that an offering will be successful

Intrastate Offerings

(F.A.Q)

36

• Why should I do an Intrastate crowdfunding campaign rather than a national crowdfunding campaign?

– Lower fees

– Less competition

– Investor base and/or project is local

– Allows for investment by accredited and non-accredited investors (with much less hassle than with Title III)

Intrastate Offerings

(F.A.Q)

37

• If equity investors are “non- voting” I can run the company/project any way I want right?

– Fiduciary duties still apply

– Must act in the best interest of equity holders

– Cannot self-deal; arm’s length transactions

– Business judgement rule

Intrastate Offerings

(F.A.Q)

38

• Benefits of the fund structure over project based crowdfunding include: – Availability of acquisition funds;

– Enhanced flexibility to act quickly and execute deals as they arise;

– Ability to earn management fees (e.g. 2/20 model)

• 2 general types: – Rule 506(b) & Regulation A

– Both types have to have specific investment strategy (no “blank check” funds)

Rise Of The “eFund”

• Real Estate Development Companies are starting to leverage the new crowdfunding rules to create real estate funds that can be sold over the internet (i.e “eFunds”)

39

Rule 506(b) based eFunds (Private):

• Can be sold over the internet but:

– Can only be sold to “accredited investors”

– Cannot be generally advertised

• Example:

– $10 Million fund started by alphaflow.com in late 2015

– Investment Strategy: 1st lien residential debt offerings (with a max LTV of 75%)

Rise Of The “eFund”

40

506(b) Pros & Cons:

• Pros:

– No offering cap

– Significantly less costly than Regulation A+ funds

– Less required public disclosure regarding the company, its operations and its officers;

– No mandated initial or ongoing disclosure requirements

• Cons:

– Cannot sell to non-accredited investors

– Highly illiquid

– Limited only to 100 investors (to avoid restriction of “Investment Company Act”)

Rise Of The “eFund”

41

Regulation A+ based eFunds (Public):

• Can be freely advertised and sold over the internet to both accredited and non-accredited investors

• Examples:

– $50 Million “eREIT” started by Fundrise.com in late 2015

• Not technically a “REIT”

• Investment Strategy: acquire and fund commercial real estate loans (no specific projects)

– $50 Million “eREIT” started by Medalist

• Traditional REIT structure

• Investment Strategy: acquire, renovate and lease 4 specific commercial properties

• SEC approval Still Pending

Rise Of The “eFund”

42

Regulation A+ Pros & Cons:

• Pros:

– Can sell to non-accredited investors

– Generally more liquid (e.g tradable on the OTC and soon to be created venture exchanges)

– Significantly greater number of permitted investors (generally 2,000 total, 500 non-accredited)

• Cons:

– Offering capped ($50 Million for Tier 1/ $20 Million for Tier 2)

– Significant upfront costs

– Significant required public disclosure regarding the company, its operations and its officers;

– Significant ongoing disclosure requirements (Tier 2)

Rise Of The “eFund”

43

Contact Info:

Anthony J. Zeoli, Partner

Freeborn & Peters LLP

(312) 360-6798

www.freeborn.com

Web Site: www.IllinoisCrowdfundingNow.com

Blog: www.CrowdfundLegalHub.com

Twitter: @ajzeoli

QUESTIONS??

Thank You

44

© 2015 Fox Rothschild

Using Regulation A+ to Fund

Real Estate Projects

Kenneth A. Kecskes, Esq.

Partner

San Francisco

These are educational materials, not legal advice.

Federal JOBS Act

• Signed by President Obama in 2012 to

encourage small business and startup funding

• Directed the SEC to:

– Eliminate the ban on general solicitation and general

advertising in Rule 506 offerings when sales are only

to “accredited investors”

– Establish a small offering exemption for crowdfunding

– Create a new exemption for offerings up to $50 million

46

Regulation A+

• SEC finalized amendments to Regulation A in

March 2015

• Now known as Regulation A+

• Regulation A+ has two “tiers”

– Tier 1

– Tier 2

47

Tier 1 and Tier 2 Summary

Tier 1 Tier 2

Offering limit $20 million annually $50 million annually

Investment limit on selling security holders

$6 million annually $15 million annually

Limits on investors? No limits (i.e., can sell to non-accredited investors)

Limits for non-accredited investors only

Restrictions on resale? None, except affiliates None, except affiliates

SEC filing requirements File Form 1-A File Form 1-A

“Blue Sky” review? Yes, SEC and state review No, only SEC review*

“Test the waters” Yes, prior to filing Form 1-A Yes, prior to filing Form 1-A

48

Tier 1 and Tier 2 Summary

Tier 1 Tier 2

Offering communications Sales materials can be used before and after filing Form 1-A and after qualification

Sales materials can be used before and after filing Form 1-A and after qualification

Financial statements Unaudited balance sheet and income statement for two years, with some exceptions

Audited financial statements required

Ongoing reporting Basically none other than termination report

Yes, current reports, semi-annual reports, and annual reports until obligations terminated or suspended

49

Who can issue Reg A+ securities?

• Companies “organized” and “principal place of

business” in US or Canada

50

Who can’t? Ineligible issuers

• SEC-reporting companies

• Investment companies required to be registered

under Investment Company Act of 1940

• Blank check companies

• Fractional undivided interests in oil & gas

• Issuers who have not filed ongoing reports

required by Regulation A for two years

• “Bad boys”

51

What types of securities

can be issued?

• Equity securities, including warrants

• Debt securities

• Debt securities convertible or exchangeable into

equity interests, including any guarantees of

such securities

• “Asset-backed securities” as such term is

defined in Item 1101(c) of Regulation AB are not

eligible securities.

52

What is an “asset-backed security”?

Regulation AB defines an “asset-backed security” as:

• “a security that is primarily serviced by the cash

flows of a discrete pool of receivables or other

financial assets,”

• “either fixed or revolving,”

• “that by their terms convert into cash within a finite

time period,”

• “plus any rights or other assets designed to assure

the servicing or timely distributions of proceeds to

the security holders . . .”

53

Common ABS Examples

in Real Estate Context

• Residential mortgage backed securities - RMBS

• Commercial mortgage backed securities - CMBS

54

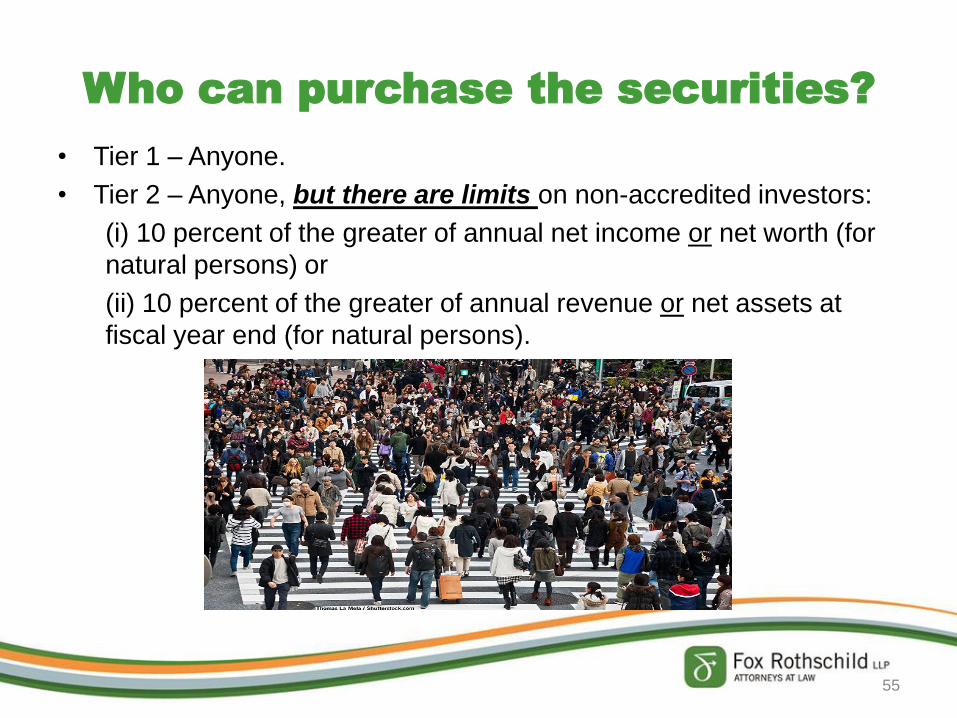

Who can purchase the securities?

• Tier 1 – Anyone.

• Tier 2 – Anyone, but there are limits on non-accredited investors:

(i) 10 percent of the greater of annual net income or net worth (for

natural persons) or

(ii) 10 percent of the greater of annual revenue or net assets at

fiscal year end (for natural persons).

55

Are there limits on resale

of Reg A+ securities?

• Non-affiliate? No secondary sales limit.

• Affiliate? Must comply with following:

– Tier 1: $6M maximum limit for 12 months following

initial qualification

– Tier 2: $15M maximum limit for 12 months following

initial qualification

56

Structuring Alternatives: Debt

• Company owns or is purchasing revenue

producing real estate, such as an office building

• Company will offer participations in debt service

from real estate secured note

57

Borrower pays debt

service

Lender collects

payments

Investors receive

participation

Structuring Alternatives: Equity

• Investors purchase LLC membership interests or

LP interests in a single real estate investment or

in a fund that invests in one or more assets

58

Investors

Asset Asset Asset

Holding Company

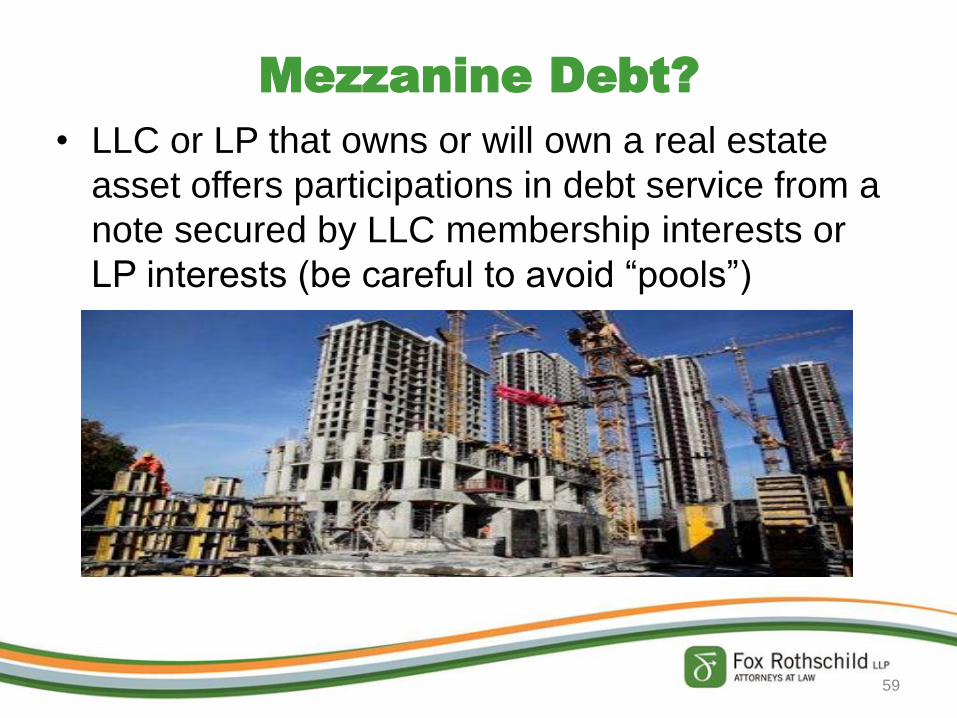

Mezzanine Debt?

• LLC or LP that owns or will own a real estate

asset offers participations in debt service from a

note secured by LLC membership interests or

LP interests (be careful to avoid “pools”)

59

Big time: Tier 2 Mini-IPO

• May list securities on national exchange by filing

Form 8-A, a short-form registration statement

• Registration would thereafter require 12(b)

reporting

60

You can “Test the Waters”

• Informal way to solicit interest

• Publicize, including on social media or by email

• Must be accurate and not misleading

• Include legends regarding status of offering

• Cost-effective way to gage interest

• “Testing” can be done until offering has been

“qualified” for fundraising by the SEC

61

Filing Requirements

• File SEC Form 1-A for both Tier 1 and Tier 2

– Basic issuer information

– Identify material risks

– Explain use of proceeds

– Disclosures about executive officers and comp

– Beneficial ownership

– Financial statements (form differs between Tier 1 & 2)

• Offering statements must be filed on EDGAR

62

Non-Public Review

• Issuer may submit offering statement to SEC for

non-public review

• Offering statement must be filed publicly not less

than 21 days before qualification

63

Offering Communications

• Generally flexible

• Must file solicitation materials with SEC

• After an offering circular is filed, solicitation materials

must include a link to the offering circular or a copy

• Solicitation must include SEC required legends

64

On-going reporting

• Tier 1 – Essentially none

– Exit reports (after termination or completion)

• Tier 2 – Current, semi-annual and annual reports (but less

onerous than Exchange Act reporting for public companies)

– Exit reports (after termination or completion)

– No requirement to provide auditor’s attestation of effectiveness of internal control

– No Exchange Act or SOX disclosures

65

Factors to consider

• Timing. SEC review times still unclear, some have taken 5 months, others as short as three weeks.

• Manage Costs. “Test the waters” before incurring filing costs. Audit costs, attorney fees, blue sky fees

• Reporting obligations. Tier 2 reporting.

• Who are your investors? You can reach anyone with an internet connection, but keep in mind Tier 2 limitations on investment by non-accredited investors

• Will SEC challenge typical real estate fees?

• Affiliate sales limits.

• Secured or unsecured?

66

Factors to consider (continued)

• Processing may be faster for Regulation A+

offerings that identify a specific project

• Underwriter not required

• Voting rights to investors not required, recently

approved filings show

• If a participation in debt offering, consider structuring

as a non-recourse loan with bad boy carve-outs

• Consider REIT structure

• Contractually provide for redemption mechanism in

lieu of secondary market, until one develops

67

Some opportunities . . .

• Companies that can’t or don’t want to rely wholly

on “friends and family” for initial equity

• Mini-RE fund with a well-defined market strategy

• Small- to medium-sized land entitlement deals

• Projects where investors can provide market

information, political support, and patronage

• Another way to exit after holding an asset?

68

Why use Regulation A+?

• Regulation A+ strengths – Can solicit an unlimited number of non-accredited

investors (but Tier 2 requires some investor diligence)

– Essentially no restrictions on the resale of securities

– General solicitation and general advertising allowed

– $50 million per year is a lot of money!

• Rule 506 of Regulation D strengths

– Simple notice filing

– No limit on amount of capital that can be raised

– No limit on number of “accredited investors”

– General solicitation and general advertising allowed in some cases

69