State Ownership, Firm Profitability, and Management Turnover

Upload

barcelona-graduate-school-of-economics-gseCategory

view

34download

0

Cross ownership and firm performance

Octavi Castells Pera, Jaime López Sastre, Berenice Ramirez Hart*

Barcelona Graduate School of Economics

Abstract: This paper assesses the impact of cross ownership on firm performance and

industry competition through an analysis of shareholder´s networks in Spain using a panel

regression model on a sample of non-financial listed companies between the years 2004 and

2012. The results show that there is a positive and significant effect of the number of

connections a firm has with other industry rivals through the common ownership mechanism

on its markup.

Keywords: Institutional ownership, Firm performance, Industry competition.

Classification: Empirical work – research

* E-mail Addresses: [email protected] (O. Castells Pera), [email protected] (J. López Sastre),

[email protected] (B. Ramirez Hart)

1. Introduction

The analysis of cross ownership of companies within the same industry has been a

topic of increasing interest for market regulators and researchers. As firms aim to maximize

shareholders´ value, this may incentivize them to compete less aggressively in the market,

therefore creating negative externalities for consumers.

Most of the literature in this area focuses on analyzing companies and investors in

the U.S. In our case, we target the Spanish market, for which we believe our paper is

innovative and provides important insights into the mechanics of cross ownership in this

country. We focus on three specific sectors: Food, Pharmaceutical and Energy, for which we

show the evolution of cross ownership concentration from 2004 to 2012, and the impact of

the largest shareholders on this.

Our main objective is to study the impact of common ownership on industry

competition and firm performance. We measure them by firm-level markups and market

share, respectively. However, we also acknowledge that markups contain information about

individual performance, since companies with higher markups obtain profits above the

equilibrium ones implied by perfect competitive markets. Thus, we will observe those firms

outperforming their industry rivals. The chief hypothesis we present is that more connected

firms coordinate their market strategies to compete less aggressively and perform better than

their less connected rivals.

Our results suggest that there has been an increase in the concentration of cross

ownership among Spanish listed companies in the last ten years. The impact of the largest

shareholders on this seems to vary a lot across the three industries under analysis. We find a

positive and significant effect of our measure of cross ownership on markups, which is

robust to several variations in our main specification. We do not find a significant effect on

firms´ market share.

The rest of the paper is organized as follows. Section 2 provides an overview of

related literature. Section 3 describes the theoretical base on which we base our empirical

analysis. Section 4 includes information on the data used. In Section 5, we show the

methodology applied for both the descriptive and inferential analyses. Section 6 and 7 present

our main descriptive and regression results, respectively. Finally, Section 8 concludes.

2. Literature review

From the seminal work of Bain (1951) the industry concentration has been a topic

that has generated much interest on the part of researchers, who have carried out several

studies on the relationship between this, different measures of profit rates and other

characteristics of the company. Consequently, one branch of studies derived from Bain’s

work reflects an increasing interest on the effects of the growing interconnection of

businesses through common stock ownership and how this can affect corporate

performance (Schmalensee, 1989; Demsetz and Villalonga, 2001; Bhattacharya and Graham,

2009; Azar, 2012).

In the cases described in the literature, researchers study partial control scenarios, in which

the acquiring company does not own 100% of the acquired company, presenting a situation

in which the interest of the first may or may not have an influence on the corporate decisions

of the second one changing the strategic interaction between the companies in the same

industry. On the one hand, the cross-holder has incentives to make the companies in the

portfolio compete less aggressively with the intention to maximize the aggregate profit of

these ones. Also, he may assist implicit or explicit coordination between the firms in the

portfolio. On the other hand, the acquiring firm might have some constraints to influence

the acquired one, for example the influence of other shareholders, corporate governance

structure and corporate law, leading to a scenario in which every firm maximizes its own

profit by taking care of the interest of all its shareholders.

Within the assessment of the effect of cross-ownership on market power and firm

performance, we can identify studies that evaluate two different types of cross ownership:

Partial Ownership and Institutional Shareholders. The first ones stress the competitive effect

of Partial ownership, defined as the acquisition of some percentage of a rival´s firm stock

(O'Brien, D. P., and Salop, S. C., 2000). The second ones evaluate how the presence of

institutional shareholders in companies of the same industry affects these companies

behavior. In both cases the presence of cross-ownership is expected to provide an effective

framework of incentives to influence corporate performance leading to a positive correlation

between cross-ownership and firm performance (Azar, J., 2012; He, J., and Huang, J.,2014)

, this last one measured as profit rate, Tobin’s Q and market share, among others.

Nonetheless, the authors find mixed results, showing that cross-ownership does not have a

positive correlation with firm performance (Demsetz, H. and Villalonga, B., 2001;

Bhattacharya, P. S., and Graham, M. A., 2009).

3. Theoretical review and development of hypothesis

In this section, we provide a brief overview of a theoretical model developed by Azar,

Schmalz, and Tecu (2015), in which they show the relationship between cross ownership

among industry participants and their profit maximization mechanism in a Cournot setting.

In this way, we illustrate the intuition behind our main hypothesis, which we explain next.

In a given industry with N firms and M investors companies maximize their

shareholder´s value. βij is defined as the share of equity of investor i on firm j, and πj are the

profits of company j. Thus, an investor´s total profits from his portfolio of companies are

given by 𝜋𝑖 = ∑ 𝛽𝑖𝑘𝜋𝑘𝑘 . Consequently, each firm maximizes a weighted average of its

shareholders portfolio profits, where the weights are given by βij1, and where xj is the strategy

of firm j.

max𝑥𝑗

𝜋�̂� = ∑ 𝛽𝑖𝑗

𝑀

𝑖=1

∑ 𝛽𝑖𝑘𝜋𝑘

𝑁

𝑘=1

By rearranging the formula and dividing by ∑ 𝛽𝑖𝑗𝑖 , we can rewrite the objective function as

max𝑥𝑗

𝜋�̂� = 𝜋𝑗 + ∑∑ 𝛽𝑖𝑘𝑖

∑ 𝛽𝑖𝑗𝑖𝑘≠𝑗

𝜋𝑘

This formula shows that companies are interested in maximizing their own profits

plus a linear combination of the profits of other companies where its shareholders have

equity stakes. The weight each company puts in the profits of the rest of the firms is given

by ∑ 𝛽𝑖𝑘𝑖

∑ 𝛽𝑖𝑗𝑖, which can be seen as a measure of the degree of connectivity between two

companies as a result of their cross ownership. The closer this ratio is to one, the more

interest company j has on company´s k profits, and therefore its shareholders will compare

the potential gains obtained from taking certain strategic actions (for example, increasing the

quantity of goods offered in the market) to increase j´s performance, with the losses from

the effect of these actions on firm k. Note that investors realize these potential losses on the

1 Azar, Schamlz, and Tecu (2015) use control rights to define the weight of each shareholder in the profit maximization function of each firm. They argue that control rights may differ from ownership share in practice, as different types of shares may provide different levels of power to make decisions within the company. However, because for our empirical analysis we are not able to obtain data on control rights, we assume that control of the firm is given by the share of ownership each shareholder has inside a firm, measured as the percentage of total shares held by that investor.

entire portfolio of companies belonging to the same industry, thus inducing them to compete

less aggressively.

Based on this model, we would expect companies which are more connected in terms

of sharing major shareholders to perform better and have higher markups. Thus, our main

hypothesis is that there exists a positive effect of our measure of cross ownership on markups

and market share for Spanish listed companies.

4. Sample Selection and Data

We use quarterly accounting data from Spanish listed companies and obtain

ownership data from these. Information from the first is obtained from the database

Compustat Global. We remove companies from the Financial Services industry2 (SIC 60),

and SICAVs (“Sociedades de Inversión de Capital Variable”). In the first case, we believe

that this sector is very different from others in many aspects, such as leverage, profitability

levels, and regulation and therefore if we were to include them, this could bias our results. In

the case of the SICAVs, the main reason is that they do not have a proper economic activity

other than investing their funds, thus we cannot treat them as regular companies. We also

drop those firms with missing values in their Operating Revenues or Operating Costs.

At the investor´s level, data is obtained from Thomson Reuters institutional

holdings. By merging both samples, we end with 250,977 observations to perform our

descriptive analysis, and 809 firm-quarterly observations for the regressions. In this last

analysis, we only include companies belonging to the Food (SIC 20), Pharmaceutical (SIC

28), and Energy sectors (SIC 49), as they are the industries with more complete data and we

believe that there is enough heterogeneity between them to obtain a good insight into the

cross ownership environment of Spain.

5. Methodology

Our analysis of common ownership networks in Spain is divided into two main

sections. Firstly, we perform a descriptive study of the evolution of networks for our sample

period, reporting changes in their density over time as well as measuring the impact of the

largest shareholders on the total number of connections generated. Secondly, we develop a

2 We use the first two digits of the Standard Industry Classification (SIC) system to classify industries from our data.

series of regressions to assess the effect of cross-ownership on firm performance and market

competition among industry participants.

5.1 Descriptive Analysis

Following Azar, Schmalz, and Tecu (2015) and Azar (2012), we define two

companies as being connected in the network if they have at least one investor with a stake

of equity3 above x% in both companies. There does not seem to be a theoretical base to

establish a threshold for two firms to be connected in the network. For example, Azar (2012)

uses thresholds of 3%, 5%, and 7% to analyze the evolution of cross-ownership in the United

States, but does not explain the rationale for this decision. In our case, we use thresholds of

1% and 3% to build the network of all listed companies in the Spanish market, and 1% to

construct the different industry sub-networks under analysis. The motivation for this

decision is that the size of the Spanish stock market, in terms of the number of firms and

investors, is considerably smaller than the US market. Thus, if we were to choose higher

thresholds, we would observe almost no connections among firms in the sample.

Additionally, it is important to consider that the size of the investments of American

shareholders is in general much larger that their Spanish counterparts. Therefore, holding a

stake of 3% in a listed Spanish company may convert an investor into the major shareholder

of that company.

We construct the adjacency matrix of each network at each point in time. For every

pair of firms (nodes) in the matrix, a value of “1” represents a connection (edge) generated

by a common shareholder, whereas a “0” represents no connection. Then, we calculate the

density of each network as a measure of how connected firms are through the cross-

ownership mechanism. A perfectly connected network would be one in which all nodes have

edges to each other, thus the density measures the percentage of existing connections over

the maximum number of potential connections. As reported by Azar (2012), the density of

a network is calculated with the following formula:

𝐷𝑒𝑛𝑠𝑖𝑡𝑦 = ∑ ∑ 𝑦𝑖𝑗𝑗≠𝑖

𝑘𝑖=1

𝑘(𝑘 − 1)/2

3 Due to data availability, we do not make distinction among the different types of shares that investors own in the sample companies (common shares, preferred shares, convertible shares, etc.). However, we are aware that shares with different voting rights enable shareholders to a different degree of influence in the decision-making of firms.

where k is the number of companies in the network, and 𝑦𝑖𝑗 equals 1 if firm i and firm j are

connected in the network. Note that by definition, the adjacency matrix is symmetric and

contains zeros in the diagonal, since a firm is not said to be connected to itself.

We also consider it useful to report the percentage of connections generated in each

network by the largest shareholders, and their evolution over time. This relates to the concept

of how concentrated the connections are within a network, as it is not the same that a high-

density network is due to a lot of different investors holding few blockholdings, or a few

number of large institutional investors holding a big number of blockholdings. First, we

consider the largest shareholders to be the ones who have held the largest number of

blockholdings during the period, where a blockholding is defined as a stake in a company

above the thresholds previously mentioned. Note that we do not require the blockholdings

to be from different companies, meaning that, for example, a shareholder with blockholdings

in three companies during the entire sample period would have held 120 blockholdings (3*40

periods). We did not consider the investors with the highest portfolio value as the largest

shareholders for the reason that there are some firms where the largest shareholder is an

individual investor holding up to 90% of the shares of the company (normally the founder

or CEO of the firm), but he/she does not hold stakes in any other company, and thus, does

not generate any connections in the networks.

5.2 Inferential Analysis

We perform a series of regressions to evaluate the effect of common ownership on

market competition of the selected industries and firm performance. In the context of our

paper, market competition and firm performance are very closely related in the following

sense: less competitive industries indicate the presence of companies that obtain profits

above the equilibrium profits implied by perfect competitive markets. Thus, we will observe

those firms outperforming their industry rivals.

We use markups as our measure of market competition and market power. We

calculate firms´ markups for every period for the companies in the three industries under

study. They are calculated in the following way:

𝑀𝑎𝑟𝑘𝑢𝑝𝑖,𝑡 = 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑅𝑒𝑣𝑒𝑛𝑢𝑒𝑠𝑖,𝑡

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐸𝑥𝑝𝑒𝑛𝑠𝑒𝑠𝑖,𝑡

We differ from Azar (2012) in the way of calculating markups, as he uses Total Cost

instead of Operating Costs. We believe that by using Operating Expenses we are able to

examine the price charged in excess of the marginal cost of producing goods for the

company, whereas if we used Total Costs we would also be considering other costs, such as

interest expenses that may differ a lot among different companies and thus, may bias our

results. Another option would be to use Cost of Goods Sold, as it would allow us to examine

the change in revenues for a company associated with an increase/decrease of the quantity

of goods sold, and thus observe how prices evolve in response to these changes. In this

sense, if revenues were to increase in a higher proportion than the cost of goods sold, we

could be observing anti-competitive incentives in companies. However, we find that Cost of

Goods Sold data from Spanish listed companies in Compustat varies a lot in the way firms

report it because of the different accounting methods used by them. This lack of

homogeneity in the reporting standards forces us to use an alternative measure, and thus

decide to use Operating Expenses4, which are reported in the same way for all companies

under study.

Our selected measure of firm performance is market share, which we define in the

following way:

𝑀𝑎𝑟𝑘𝑒𝑡 𝑆ℎ𝑎𝑟𝑒𝑖,𝑡 =𝑆𝑎𝑙𝑒𝑠𝑖,𝑡

∑ 𝑆𝑎𝑙𝑒𝑠𝑖,𝑡𝑘𝑖=1

where k is the number of firms in the industry. By using market share as our dependent

variable in the regression, the parameter of interest will reflect the expected change in the

market share of a given company due to a change in its cross-ownership measure.

To assess the effect of cross-ownership on industry competition we build a panel

regression using ordinary least squares (OLS) with the following specification:

𝑀𝑎𝑟𝑘𝑢𝑝𝑖,𝑡 = 𝛼 + 𝛽𝑁𝑐𝑜𝑛𝑛𝑒𝑐𝑡𝑖𝑜𝑛𝑠𝑖,𝑡 + 𝛾𝑋𝑖,𝑡 + 𝛿𝑍𝑖,𝑡 + 𝐹𝑖𝑟𝑚𝑖 + 휀𝑖,𝑡 (1)

where Markup is the dependent variable measuring competition. The main variable of interest

is Nconnections, which is our measure of cross-ownership. It measures the number of edges

each company has with other industry firms in the common ownership network, for every

period. We normalized this measure by dividing it by the number of firms in the network in

each quarter, since this changes over time. X is a vector of industry time-varying

characteristics, which include Average Industry Markup and Density. Z is a vector of firm-

4 Operating Expenses in Compustat data include Cost of Goods Sold, Selling, General, and Administrative Expenses, and Other Operating Expenses.

specific control variables that may have an effect in a company´s markup, such as Debt to

Assets, Ln (Assets) and Sales Growth. Finally, the variable Firm captures firm fixed effects.

As reported by He and Huang (2014), including firm fixed effects may help solve the

problem of omitted unobservable time-invariant characteristics that can be correlated with

both markup and connections, leading us to wrong interpretations of the results.

We run a second OLS regression using panel data to analyze the effect of cross-

ownership on firm performance:

𝑀𝑎𝑟𝑘𝑒𝑡 𝑆ℎ𝑎𝑟𝑒𝑖,𝑡 = 𝛼 + 𝛽𝑁𝑐𝑜𝑛𝑛𝑒𝑐𝑡𝑖𝑜𝑛𝑠𝑖,𝑡 + 𝛾𝑋𝑖,𝑡 + 𝛿𝑍𝑖,𝑡 + 𝐹𝑖𝑟𝑚𝑖 + 휀𝑖,𝑡 (2)

where Market Share is the dependent variable measuring firm performance. The independent

variables are the same ones used in the previous regression, also including firm fixed effects.

6. Descriptive analysis

6.1 Biggest shareholders in Spain based on total portfolio value

In this section, we make an introduction about major shareholders in Spain. As we

can see in Figures 1 and 2, there is a big decrease in all investors´ portfolio value around

2008. This is due to the financial crisis, as the assets held by these investors decreased in

value by large amounts. As we can observe, the major shareholders in Spain do not increase

their position to 2007 levels. The principal shareholders, ranked by total portfolio value, are

Spanish banks, such as La Caixa, Banco Santander, BBVA; international investment

institutions like Nordea, Blackrock, and Fidelity; and finally, we can also find individuals or

family groups with the majority of their shares in one company, such as Amancio Ortega

(major shareholder of Inditex), or the Entrecanales family (major shareholders of Acciona).

As we can observe in Figure 2, the major shareholder in Spain in 2012 is Amancio

Ortega, who owns shares of Inditex. La Caixa ranks second for that year, with major

positions in companies belonging to the energy sector such as Repsol or Gas natural, and

holding shares of the insurance company Abertis. La Caixa also has minor positions in a wide

range of other Spanish companies. Finally, Enel SPA, which bought the Spanish energy

company Endesa, also has a big portfolio value, although this is not very relevant for our

analysis as it only holds shares of this company.

For what we have seen, the major shareholders in Spain have invested huge amounts,

but only in a few companies. An exception to this would be La Caixa. As we are interested

in those investors with considerably big positions in different companies, we decide to take

a different approach to define and rank the largest shareholders in Spain. Specifically, we will

consider the major shareholders to be the ones who have held the largest number of block

holdings during the period under study, where a blockholding is defined as a stake in a

company’s equity above thresholds of 1% and 3%, as described in Section 4.

6.2 Biggest shareholders in Spain based on total number of blockholdings

As we can see in Tables 1 and 2, the biggest shareholder in Spain on a blockholding

basis is Bestinver. Bestinver is a fund company that invests a large part of its capital in Spain.

The company is owned by Acciona, which is held by the aforementioned Entrecanales

family. One of the other major shareholders is La Caixa, also mentioned previously, as one

of the biggest shareholders in a total portfolio value basis. Finally, we can see NBIM, which

is a Norwegian investment bank, the fund manager Fidelity, and the American investment

advisor Dimensional Fund Advisors.

At the individual industry level, we can observe that Bestinver is the major investor

in the food sector (see Table 3), and also the second biggest in the pharmaceutical sector (see

Table 4), but it does not have a big position in the energy sector (see Table 5). We can also

see some of the major players at the entire Spanish market level such as Fidelity and NBIM

having important positions in the energy and pharmaceutical industries, respectively.

6.3 Density analysis

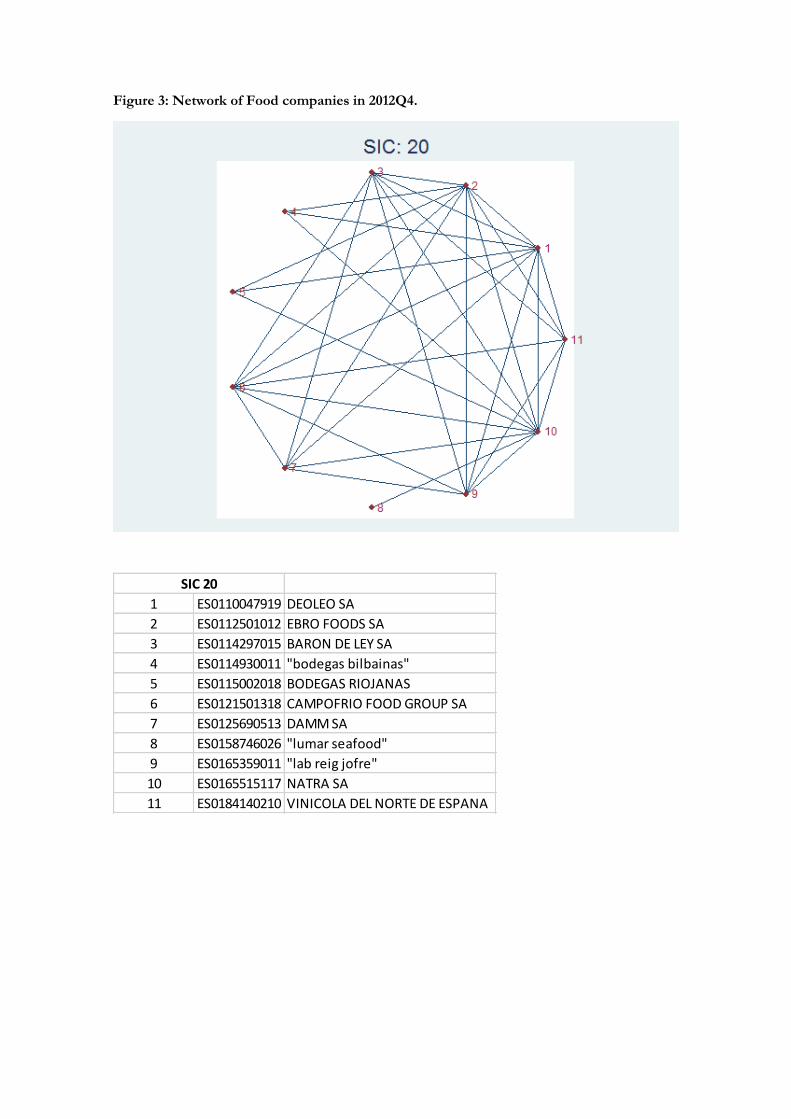

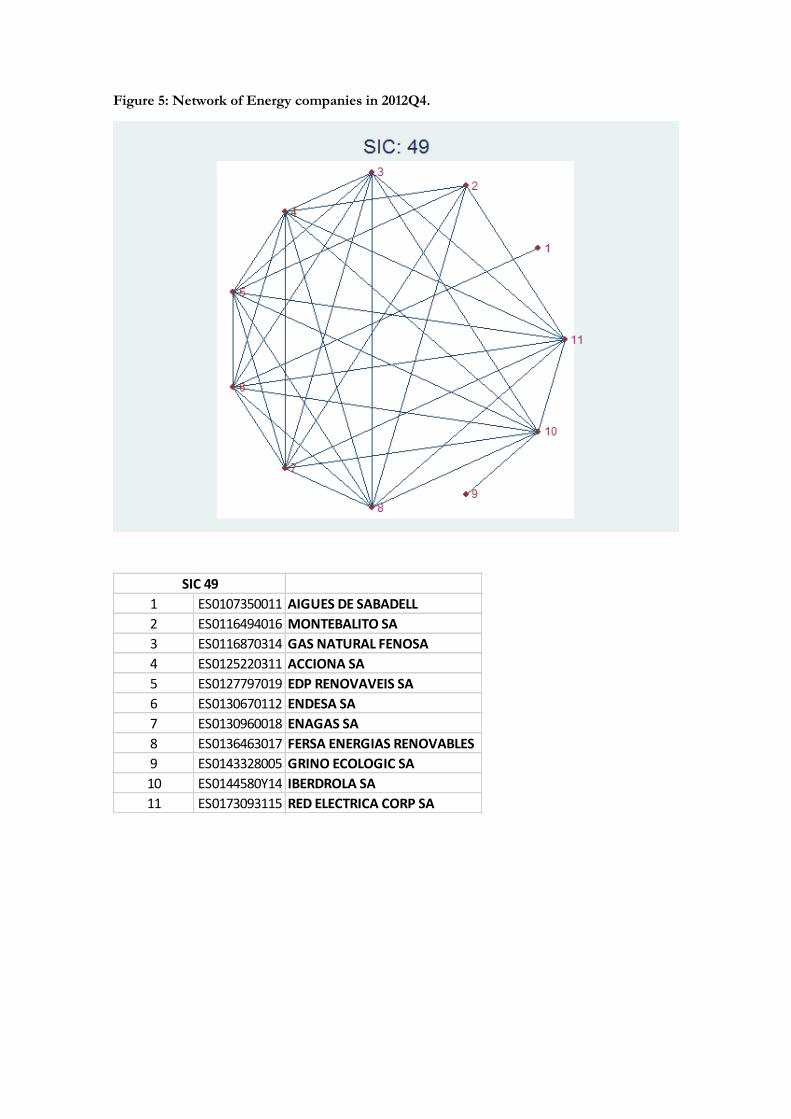

In Figures 3, 4, and 5, we provide a picture of the cross ownership networks of the

three industries (SIC 20, 28, and 49) at a specific point in time; in this case the last quarter of

2012. In this way, we visually show the level of interconnections among companies belonging

to the same industry.

With respect to the evolution of densities, we observe how, overall, the density has

increased during the reported period for the three industries under analysis (see Figure 6).

We can see a decrease from 2005-2006 for the three sectors. However, we generally observe

an increasing density over time. It can be seen how the density moves from 5%-10% on the

first years to 20% in the last ones. The pharmaceutical sector is the one that has experienced

a higher increasing trend as we can notice a network density growth from approximately 0%

to 70%.

The percentage of connections generated by the largest shareholders is very volatile

throughout our sample period for the three industries reported (see Figure 7). We can

observe how the Food and Energy sectors follow similar patterns, reaching minimum levels

in 2006. After this, they increase in 2007 to then fall again from 2008 until the end of the

period, being around 0% and 10%, respectively. In the case of the Pharmaceutical industry,

the percentage of connections generated by the major shareholders is 0% from 2004 until

the fourth quarter of 2009, when they experience a sharp increase, reaching a maximum of

around 85% during 2011. Finally, they decrease during 2012, as also happened with the Food

and Energy industries.

It is interesting to compare the evolution of densities and connections generated by

the largest shareholders between Spanish and American listed companies, which are analyzed

by Azar (2012). In both countries industry densities have had an increasing trend over time,

indicating a higher degree of connectivity among firms through their cross ownership.

Whereas in the U.S. the largest shareholders generate a big percentage of the connections5

(between 80% and 90%), and they stay flat from 2004 to 2012, in the case of Spain they vary

a lot over time. This indicates that institutional investors have a very high influence and

presence in American listed companies, while in Spain this is more ambiguous.

7. Empirical results

In this section, we present the results of our regression on the effect of cross

ownership in industry competition and firm performance.

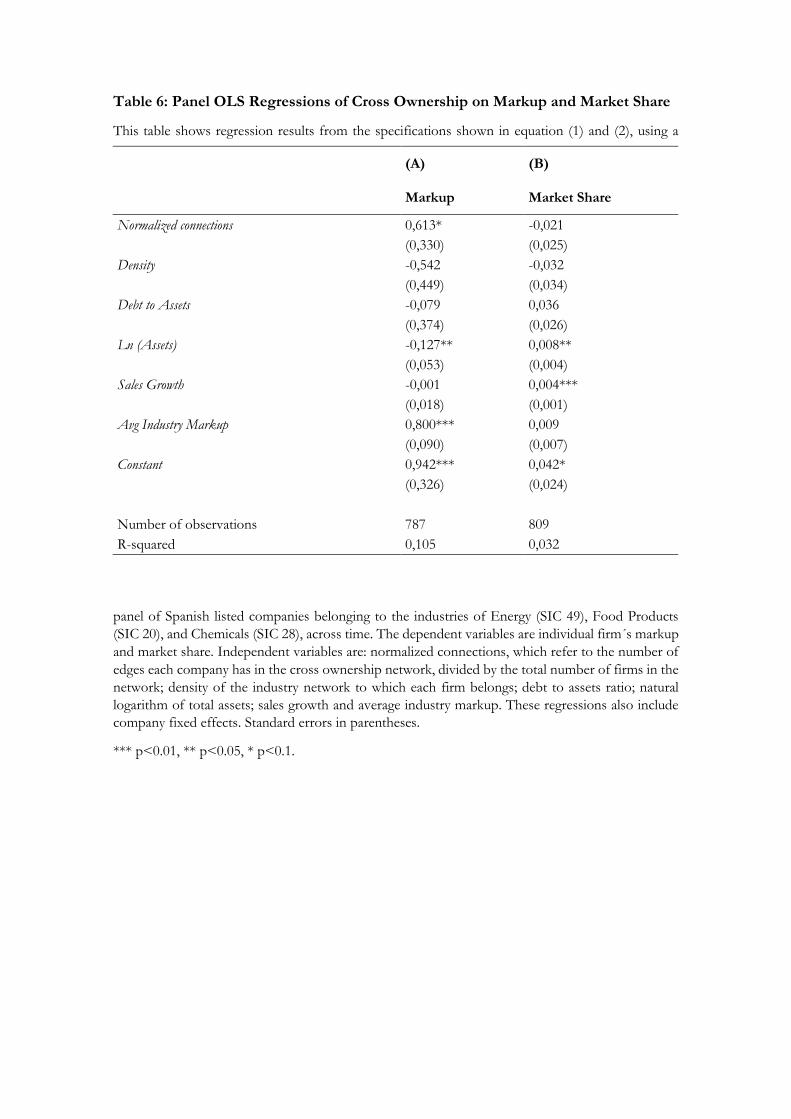

Table 6 shows the estimation results from our two main panel regressions using

equations (1) and (2) described in Section 4. With respect to our main variable of interest,

Nconnections, we observe a positive and significant effect on Markup, although only at a 10%

significance level. This implies that companies which share investors with large stakes in their

equity with other industry rivals tend to have higher markups, suggesting the presence of

anti-competitive incentives of cross ownership. To show the economic magnitude of this

effect, the coefficient of Nconnections on Markup (0.613) conveys that a firm which is

connected to 10% of its within-industry rivals, will have a markup higher by 0.0613 points

than a company with no connections in the network. We do not find significant effect of the

overall industry density of the network on markups. These results differ from the ones

obtained by Azar (2012), where he shows a significantly negative effect of the average

number of connections of firms in the same industry on average (industry) markups, and a

significantly positive effect of common shareholder density on the same dependent variable.

This suggests that in the U.S., cross ownership concentration has an effect on markups at

5 See Chapter 4 of Azar (2012).

the industry level, whereas in Spain this relationship occurs at the individual (firm) level. The

fact that the number of listed companies in each industry in the U.S. is higher than in Spain

may also be driving these differences.

With respect to firm performance, measured by market share, we do not observe any

significant effect of the normalized number of connections on the above variable, as reported

in Column A of Table 6. In this sense, we differ from He and Huang (2014), which found a

positive and significant effect of different measures of cross ownership on market share

growth, for a sample of U.S. public companies.

Finally, we conduct a series of robustness checks to assess the quality of our main

regression results, which are presented in Tables 7 and 8, corresponding to variations in

specifications (1) and (2), respectively. In Column A of both tables, we remove company

fixed effects and perform a Generalised Least Squares (GLS) regression allowing for random

effects. Several reasons lead us to this decision. Firstly, we cannot assume that company time

variance is not present in our data. These time variances are existent in unobservable factors

on which we cannot have data. For example, manager efficiency can vary over time and

firms. Moreover, it is an unobservable factor that, because we include a 10-year sample, it

cannot be assumed to be constant over this period. Another example is the location of the

activity. Some firms during this 10-year period may move their production centers across

autonomic communities or even outside of the country. This can highly affect markups due

to the regulatory differences across Spanish regions. Moreover, each community has their

own grant programs that can have an effect as well. The level of exports of each firm may

also play an important role. Some firms in the same industry may have a different level of

exposure to international markets and currency fluctuations. For example, as a result of

exchange rates, firms competing in the same sector with higher exports can become more

competitive and get better results if exchange rates vary favorably. These changes (which

happened during our 10-year period) are not observable and affect the results over time.

We observe how the coefficient of Nconnections is still positive and significant (now at

5% significance level) for the effect on Markup. In addition, the coefficient of Density now is

significant at a 10% level, indicating that the higher the overall concentration of cross

ownership at an industry level, the lower the individual markup of companies. With respect

to the Market Share regression, both parameters remain negative and statistically not

significant.

In Column B, we also use random effects but include industry dummies to account

for the potential existence of differences across industries not included in the control

variables. The effect of Nconnections on Markup is still positive and significant, now at a 1%

level; and remains negative and not significant for the case of Market Share.

Column C reports the same GLS regression, but without industry dummies and

accounting for potential seasonality effects, for which we included quarter dummies. Again,

the parameter of our cross ownership measure remains positive and significant for the case

of Markup (at a 5% level), and negative and not significant for Market Share.

Overall, our main result from these regressions is that cross ownership of within-

industry companies by the same institutional investors increases markups of those firms,

which is consistent with our main hypothesis that common shareholders tend to relax

competition of their portfolio companies in order to obtain more gains and limit their losses.

8. Conclusions

In this paper, we provide both a descriptive and empirical analysis on the effects of cross

ownership on the strategic interaction of firms within an industry. We find a positive and

significant relationship between our measure of cross ownership and firm markups, which

provides evidence of collusive behavior among natural competitors, creating a deadweight

loss for consumers. However, we do not find a significant effect on firms´ market share.

Our results have an important implication on the regulation of the ownership structure

of firms. For this reason, we suggest that further empirical research is conducted with respect

to this topic, in order to assess regulators in setting up a new policy framework that considers

more carefully the implications that cross ownership may have in market competition.

9. References

Azar, J. (2011). A new look at oligopoly: Implicit collusion through portfolio diversification. Available at SSRN

1993364.

Azar, J., Schmalz, M. C., and Tecu, I. (2014). Anti-competitive effects of common ownership. Ross School of Business

Paper, (1235).

Bain, J. S. (1951). Relation of profit rate to industry concentration: American manufacturing, 1936-1940. The Quarterly

Journal of Economics, 293-324.

Bhattacharya, P. S., and Graham, M. A. (2009). On institutional ownership and firm performance: A disaggregated

view. Journal of Multinational Financial Management, 19(5), 370-394.

Demsetz, H., and Villalonga, B. (2001). Ownership structure and corporate performance. Journal of Corporate

Finance, 7(3), 209-233.

Edmans, A., Levit, D., and Reilly, D. (2014). Governance and Comovement Under Common Ownership.

He, J., and Huang, J. (2014). Product market competition in a world of cross ownership: Evidence from institutional

blockholdings. Available at SSRN 2380426.

O'Brien, D. P., and Salop, S. C. (2000). Competitive effects of partial ownership: Financial interest and corporate

control. Antitrust Law Journal, 559-614.

Schmalensee, R. (1989). Inter-industry studies of structure and performance. Handbook of Industrial Organization, 2.

Appendix

Figure 1: Top 25 Shareholders in Spain ranked by Total Portfolio Value.

Figure 2: Top 7 Shareholders in Spain ranked by Total Portfolio Value.

$0.00

$10,000,000,000.00

$20,000,000,000.00

$30,000,000,000.00

$40,000,000,000.00

$50,000,000,000.00

$60,000,000,000.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Banco Bilbao Vizcaya Argentaria S.A.Banco Santander SABlackRock Institutional Trust Company, N.A.Caja de Ahorros y Pensiones de Barcelona (La Caixa)Capital Research Global Investors

Figure 3: Network of Food companies in 2012Q4.

1 ES0110047919 DEOLEO SA

2 ES0112501012 EBRO FOODS SA

3 ES0114297015 BARON DE LEY SA

4 ES0114930011 "bodegas bilbainas"

5 ES0115002018 BODEGAS RIOJANAS

6 ES0121501318 CAMPOFRIO FOOD GROUP SA

7 ES0125690513 DAMM SA

8 ES0158746026 "lumar seafood"

9 ES0165359011 "lab reig jofre"

10 ES0165515117 NATRA SA

11 ES0184140210 VINICOLA DEL NORTE DE ESPANA

SIC 20

Figure 4: Network of Pharmaceutical companies in 2012Q4.

1 ES0109659013 AB-BIOTICS SA

2 ES0125140A14 ERCROS SA

3 ES0134950F36 FAES FARMA SA

4 ES0157097017 ALMIRALL SA

5 ES0157261019 LABORATORIOS FARMACEUTOCOS

6 ES0163960018

7 ES0165380017 SNIACE SA

8 ES0171996004 GRIFOLS SA B class

9 ES0171996012 GRIFOLS SA

10 ES0172233118 BIOSEARCH SA

SIC 28

Figure 5: Network of Energy companies in 2012Q4.

1 ES0107350011 AIGUES DE SABADELL

2 ES0116494016 MONTEBALITO SA

3 ES0116870314 GAS NATURAL FENOSA

4 ES0125220311 ACCIONA SA

5 ES0127797019 EDP RENOVAVEIS SA

6 ES0130670112 ENDESA SA

7 ES0130960018 ENAGAS SA

8 ES0136463017 FERSA ENERGIAS RENOVABLES

9 ES0143328005 GRINO ECOLOGIC SA

10 ES0144580Y14 IBERDROLA SA

11 ES0173093115 RED ELECTRICA CORP SA

SIC 49

Figure 6: Network density evolution for the reported industries at 1% threshold.

Figure 7: Percentage of connections generated by the largest shareholders at 1% threshold.

Table 1: Major shareholders by block holdings all sectors at 1%.

All Companies at 1% Total number of blockholdings for the period

Bestinver Gestión S.G.I.I.C. S.A. 726

Norges Bank Investment Management (NBIM) 550

Fidelity Worldwide Investment (UK) Ltd. 305

Caja de Ahorros y Pensiones de Barcelona (La Caixa) 257

Dimensional Fund Advisors, LP 231

Table 2: Major shareholders by block holdings all sectors at 3%.

All Companies at 3% Total number of blockholdings for the period

Bestinver Gestión S.G.I.I.C. S.A. 503

Caja de Ahorros y Pensiones de Barcelona (La Caixa) 257

Banco Bilbao Vizcaya Argentaria S.A. 216

Kutxabank Gestion, SGIIC, S.A.U. 168

Caixanova, Caixa de Aforros de Vigo, Ourense e Pontevedra 162

Table 3: Major shareholders by block holdings SIC 20.

SIC 20 Total number of blockholdings for the period

Bestinver Gestión S.G.I.I.C. S.A. 78

Kutxabank Gestion, SGIIC, S.A.U. 49

Libertas 7 SA 45

Lafuente Family 42

Boag de Valores, S.L. 40

Table 4: Major shareholders by block holdings SIC 28.

SIC 28 Total number of blockholdings for the period

Norges Bank Investment Management (NBIM) 56

Bestinver Gestión S.G.I.I.C. S.A. 51

Promociones Arier, S.A. 40

BBVA Patrimonios Gestora S.G.I.I.C., S.A. 39

Ebro Foods SA 38

Table 5: Major shareholders by block holdings SIC 49.

SIC 49 Total number of blockholdings for the period

Fidelity Worldwide Investment (UK) Ltd. 65

Sociedad Estatal de Participaciones Industriales 59

Caja de Ahorros y Pensiones de Barcelona (La Caixa) 58

Kutxabank Gestion, SGIIC, S.A.U. 53

Gdf Suez SA 49

Table 6: Panel OLS Regressions of Cross Ownership on Markup and Market Share

This table shows regression results from the specifications shown in equation (1) and (2), using a

panel of Spanish listed companies belonging to the industries of Energy (SIC 49), Food Products

(SIC 20), and Chemicals (SIC 28), across time. The dependent variables are individual firm´s markup

and market share. Independent variables are: normalized connections, which refer to the number of

edges each company has in the cross ownership network, divided by the total number of firms in the

network; density of the industry network to which each firm belongs; debt to assets ratio; natural

logarithm of total assets; sales growth and average industry markup. These regressions also include

company fixed effects. Standard errors in parentheses.

*** p<0.01, ** p<0.05, * p<0.1.

(A) (B)

Markup Market Share

Normalized connections 0,613* -0,021

(0,330) (0,025)

Density -0,542 -0,032

(0,449) (0,034)

Debt to Assets -0,079 0,036

(0,374) (0,026)

Ln (Assets) -0,127** 0,008**

(0,053) (0,004)

Sales Growth -0,001 0,004***

(0,018) (0,001)

Avg Industry Markup 0,800*** 0,009

(0,090) (0,007)

Constant 0,942*** 0,042*

(0,326) (0,024)

Number of observations 787 809

R-squared 0,105 0,032

Table 7: Panel GLS Regression of Cross Ownership on Markup – Robustness Tests

Dependent variable: Markup

(A) (B) (C)

Normalized connections 0,782** 0,830*** 0,787**

(0,314) (0,315) (0,314)

Density -0,751* -0,757* -0,753*

(0,440) (0,441) (0,446)

Debt to Assets -0,339 -0,299 -0,338

(0,344) (0,346) (0,344)

Ln (Assets) -0,030 -0,068 -0,031

(0,029) (0,044) (0,030)

Sales Growth 0,001 0,002 0,002

(0,018) (0,018) (0,018)

Avg Industry Markup 0,821*** 0,800*** 0,822***

(0,089) (0,091) (0,091)

SIC20 0,023

(0,282)

SIC49 0,425

(0,376)

Quarter2 -0,027

(0,081)

Quarter3 -0,015

(0,081)

Quarter4 -0,045

(0,081)

Constant 0,515** 0,517* 0,539**

(0,253) (0,292) (0,264)

Number of observations 787 787 787

This table reports robustness test results for the effect of the cross ownership measure on markups.

In the three regressions included in this table, we use a GLS regression with random effects to

account for unobserved differences among companies. Column A includes the same independent

variables used in Table 1. Column B also includes industry dummies, which are SIC20 and SIC49.

Finally, column C includes quarter dummies to account for potential seasonality effects (Quarter2,

Quarter3, and Quarter4). Robust standard errors are in parentheses.

*** p<0.01, ** p<0.05, * p<0.1.

Table 8: Panel GLS Regression of Cross Ownership on Market Share – Robustness

Tests

Dependent variable: Market Share

(A) (B) (C)

Normalized connections -0,014 -0,016 -0,016

(0,025) (0,025) (0,025)

Density -0,035 -0,039 -0,042

(0,034) (0,034) (0,034)

Debt to Assets 0,044* 0,039 0,042*

(0,025) (0,025) (0,025)

Ln (Assets) 0,006* 0,011*** 0,007**

(0,003) (0,004) (0,003)

Sales Growth 0,004*** 0,004*** 0,003**

(0,001) (0,001) (0,001)

Avg Industry Markup 0,007 0,009 0,005

(0,007) (0,007) (0,007)

SIC20 -0,013

(0,055)

SIC49 -0,144**

(0,056)

Quarter2 0,005

(0,006)

Quarter3 -0,002

(0,006)

Quarter4 0,019***

(0,006)

Constant 0,049* 0,092** 0,042

(0,030) (0,043) (0,031)

Number of observations 809 809 809

This table reports robustness test results for the effect of the cross ownership measure on market

share. In all columns, we use a GLS regression with random effects to account for unobserved

differences among companies. Column A includes the same independent variables used in Table 1.

Column B also includes industry dummies, which are SIC20 and SIC49. Finally, column C includes

quarter dummies to account for potential seasonality effects (Quarter2, Quarter3, and Quarter4). Robust

standard errors are in parentheses.

*** p<0.01, ** p<0.05, * p<0.1.