Cross Border Funding 2015: FROM SOLOMON CAPITAL EVENT

31

SOLOMONCAPITAL AUG 2014 ”WE PROVIDE ONLY BEST innovative solutions for Fundraising, Debt Financing, Restructuring and M&A.” David Solomon, Group CEO April 2015 Cross Border Investment Banking

-

Upload

david-solomon -

Category

Business

-

view

13 -

download

0

Transcript of Cross Border Funding 2015: FROM SOLOMON CAPITAL EVENT

SOLOMONCAPITAL

AUG 2014

”WE PROVIDE ONLY BEST innovative solutions for Fundraising, Debt Financing, Restructuring and M&A.” David Solomon, Group CEO

April 2015

Cross Border Investment Banking

> About Solomon Capital

> Cross Border Fundraising

> Our Approach

Contents

2

SOLOMONCAPITAL

April 2015

3

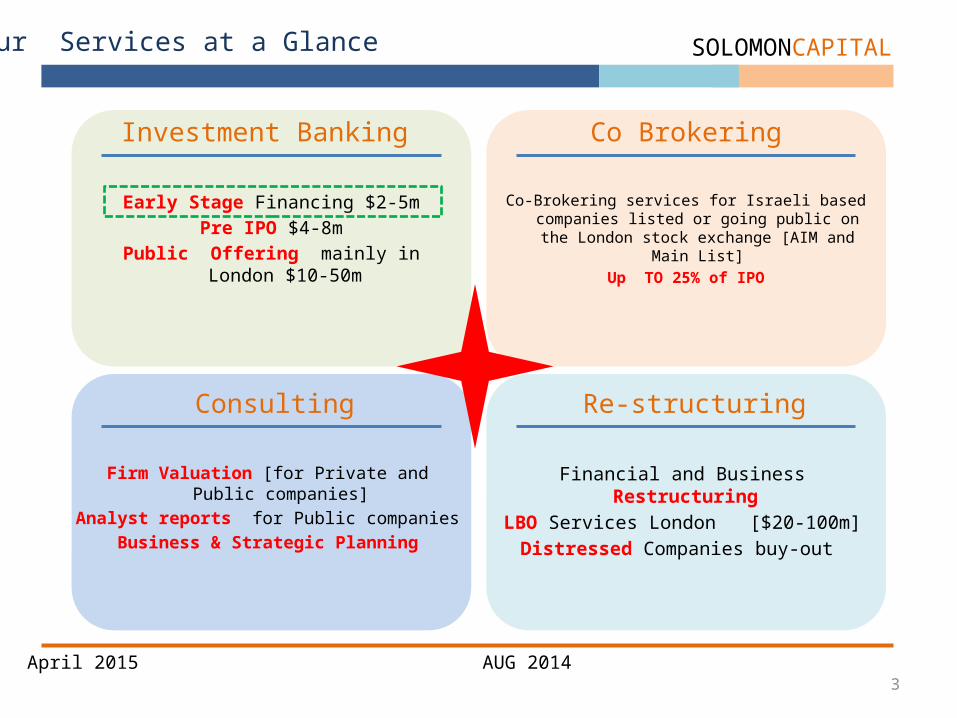

Our Services at a Glance

Investment Banking

Early Stage Financing $2-5mPre IPO $4-8m

Public Offering mainly in London $10-50m

Consulting

Firm Valuation [for Private and Public companies]Analyst reports for Public companies

Business & Strategic Planning Financial and Business Restructuring LBO Services London [$20-100m]

Distressed Companies buy-out

LBO & Restructuring

SOLOMONCAPITAL

Co Brokering

Co-Brokering services for Israeli based companies listed or going public on the

London stock exchange [AIM and Main List]Up TO 25% of IPO

Re-structuring

Financial and Business Restructuring LBO Services London [$20-100m]

Distressed Companies buy-out

AUG 2014April 2015

4April 2015

4StartUPSהזנק לחברות עיסקי ויעוץ START UPS - Only The BEST Innovative Solutions ליווי

עיסקי תכנון תהליכי הון גיוסי עיסקי פיתוח החברות להנהלת שוטף וליוויה יעוץ

A part of Solomon Capital Group

SOLOMONCAPITAL

5

DS Experience at-a-Glance

Note : Clients and or David Solomon Experience at-a-Glance

April 2015

6

SOLOMONCAPITALFirm Valuation & Analyst Reports - Coverage

Note : Firm valuations and independent analysts coverage reports distribute to the public and or to our clients

April 2015

7

SOLOMONCAPITALLondon : Business Contact at a Glance

April 2015

Experience at a Glance

David Solomon Books : [Sold out]

8

SOLOMONCAPITAL

April 2015

From The Press…

9

SOLOMONCAPITAL

April 2015

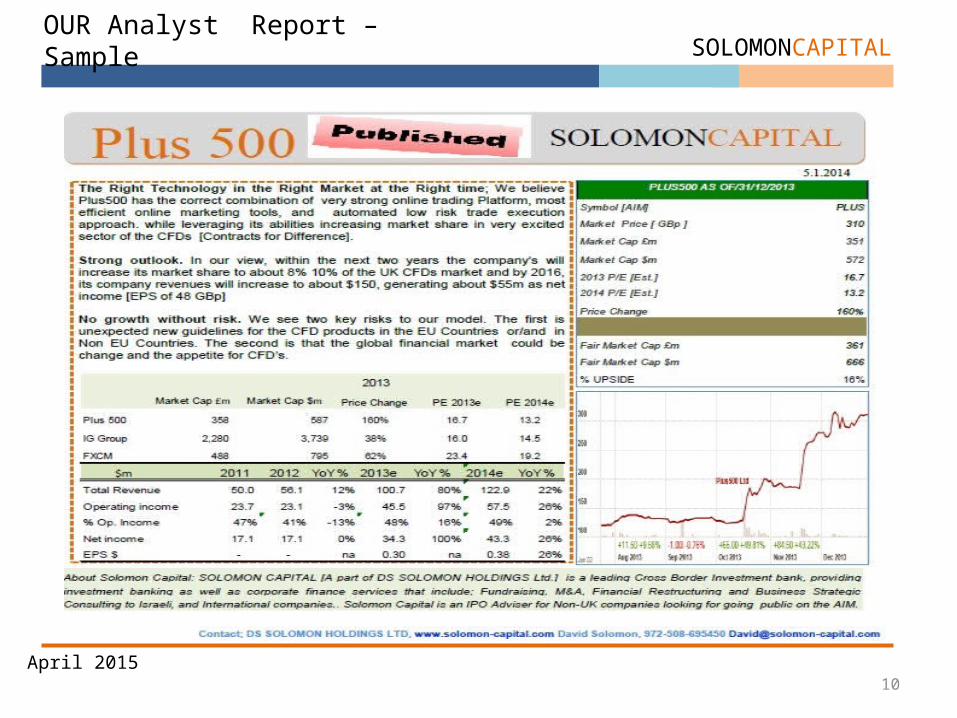

OUR Analyst Report –Sample

10

SOLOMONCAPITAL

April 2015

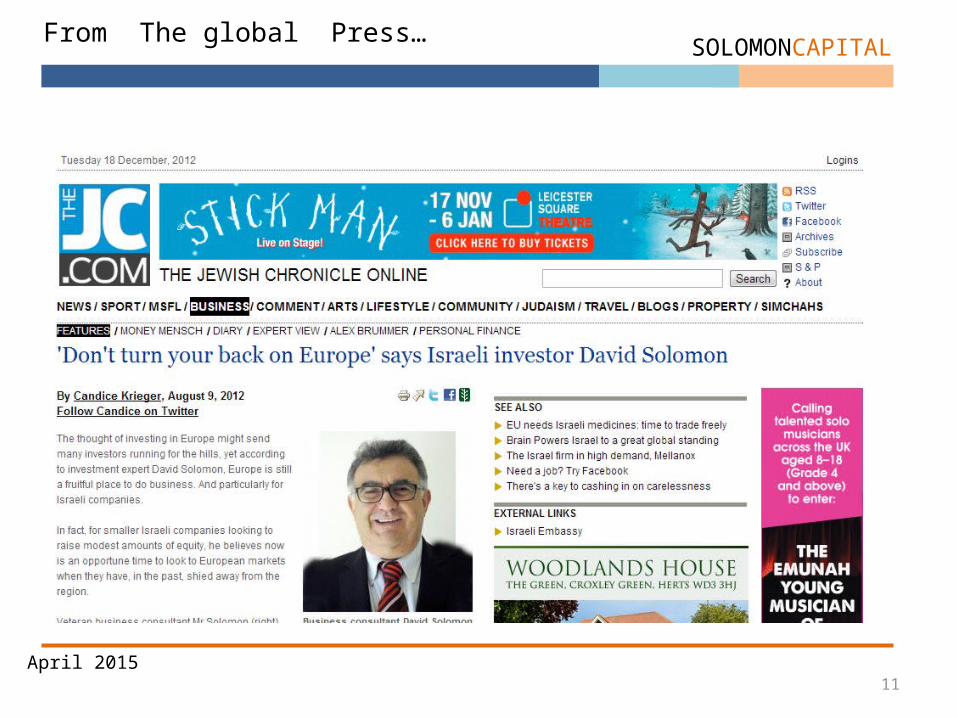

From The global Press…

11

SOLOMONCAPITAL

April 2015

12

SOLOMONCAPITAL

April 2015

> About Solomon Capital

> Cross Border Fundraising

> Our Approach

13

SOLOMONCAPITAL

April 2015

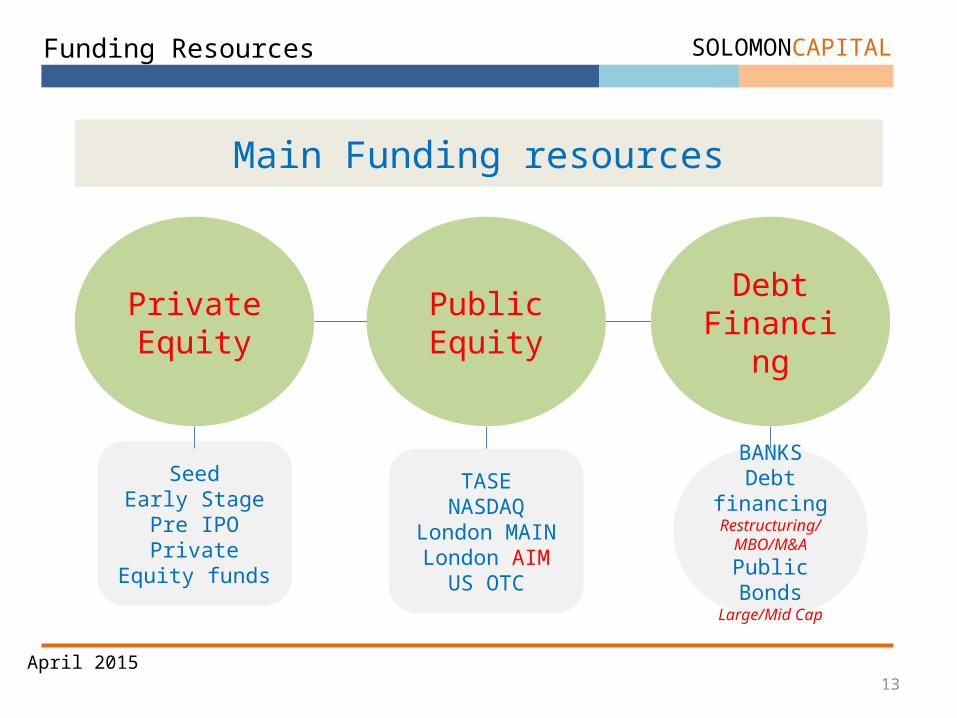

Main Funding resources

Private Equity

Public Equity

Debt Financing

SeedEarly Stage

Pre IPOPrivate Equity

funds

TASENASDAQ

London MAINLondon AIM

US OTC

BANKSDebt financing

Restructuring/MBO/M&A

Public BondsLarge/Mid Cap

Funding Resources

IPO Solution -LONDON SOLOMONCAPITAL

IPO Solution -LONDONfor Small-Mid Companies

Transaction size: $10m -$50m Technology, Growth, Pre Market Cap $50m -$200m

• Sales: > $5, Next Year> $8m• 4 Quarter sales• EBITDA>1, Next Year>$2-4• Strong Management Team [CFO]• Strong Story

IPO Criteria• PE• EV/EBITDA• DCF [Not Likely]• Sector Benchmarks

Valuation

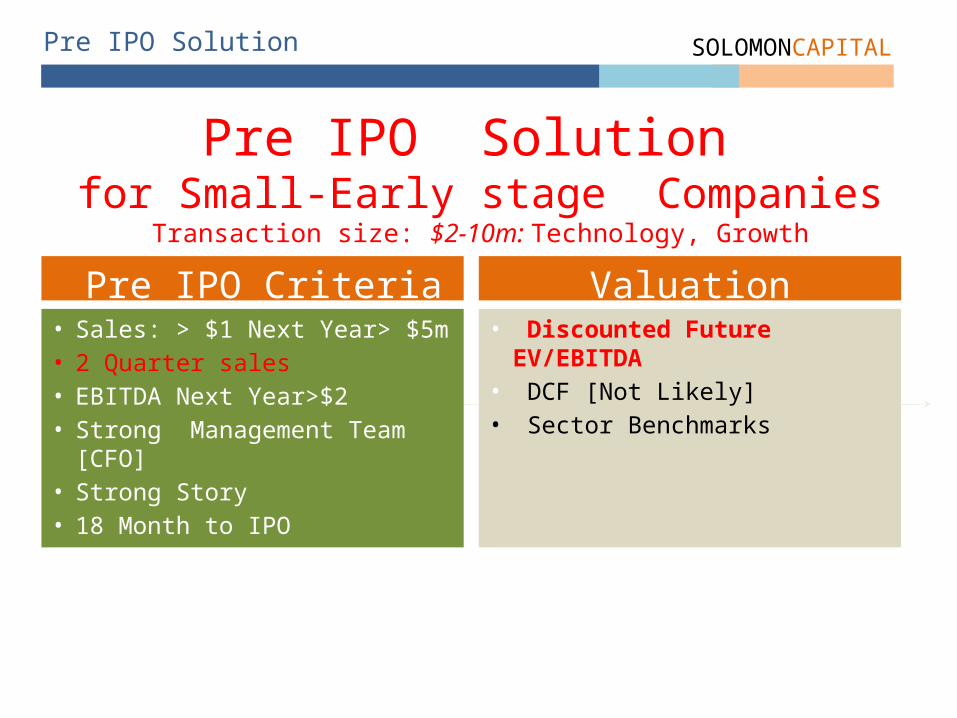

Pre IPO Solution SOLOMONCAPITAL

Pre IPO Solution for Small-Early stage Companies

Transaction size: $2-10m: Technology, Growth

• Sales: > $1 Next Year> $5m• 2 Quarter sales• EBITDA Next Year>$2• Strong Management Team [CFO]• Strong Story• 18 Month to IPO

Pre IPO Criteria• Discounted Future EV/EBITDA• DCF [Not Likely]• Sector Benchmarks

Valuation

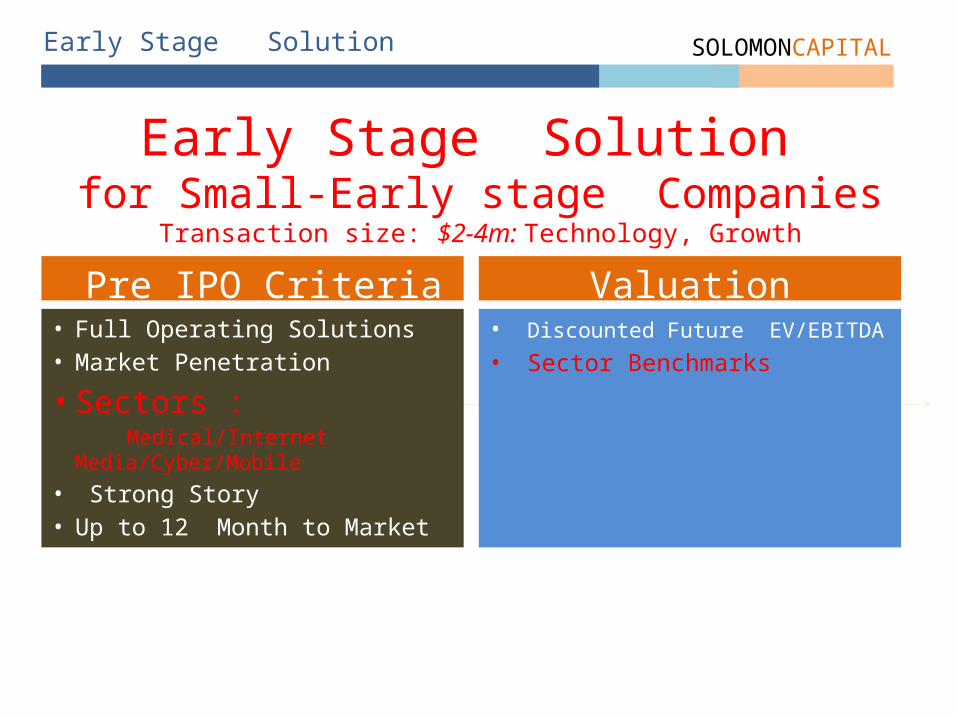

Early Stage Solution SOLOMONCAPITAL

Early Stage Solution for Small-Early stage Companies

Transaction size: $2-4m: Technology, Growth

• Full Operating Solutions• Market Penetration

• Sectors : Medical/Internet Media/Cyber/Mobile• Strong Story• Up to 12 Month to Market

Pre IPO Criteria• Discounted Future EV/EBITDA• Sector Benchmarks

Valuation

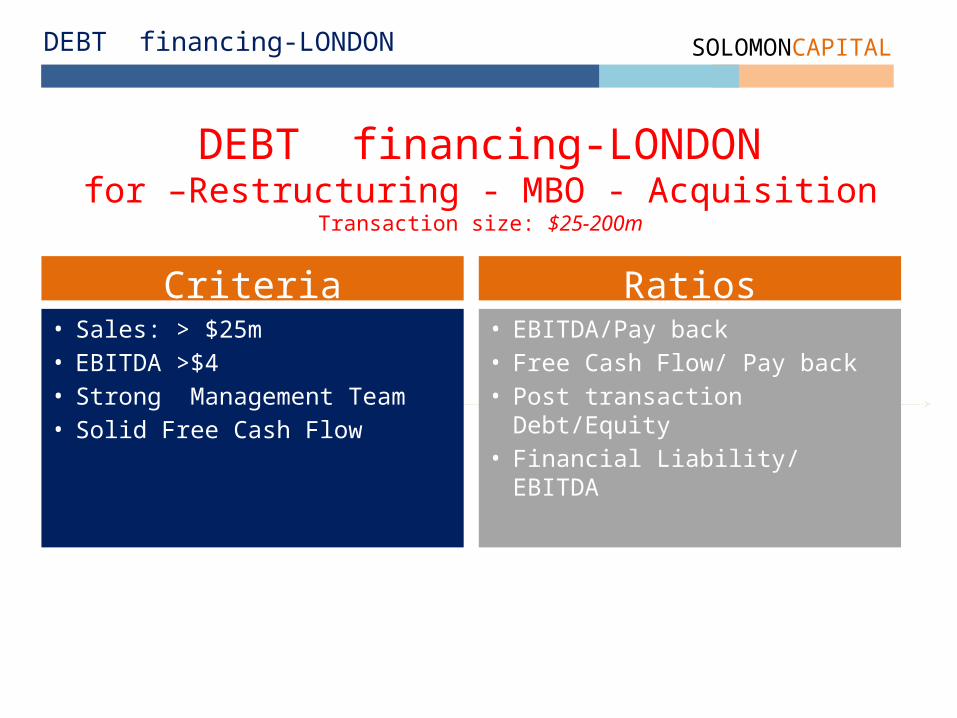

DEBT financing-LONDON SOLOMONCAPITAL

DEBT financing-LONDONfor –Restructuring - MBO - Acquisition

Transaction size: $25-200m

• Sales: > $25m• EBITDA >$4• Strong Management Team• Solid Free Cash Flow

Criteria• EBITDA/Pay back• Free Cash Flow/ Pay back• Post transaction Debt/Equity• Financial Liability/ EBITDA

Ratios

18

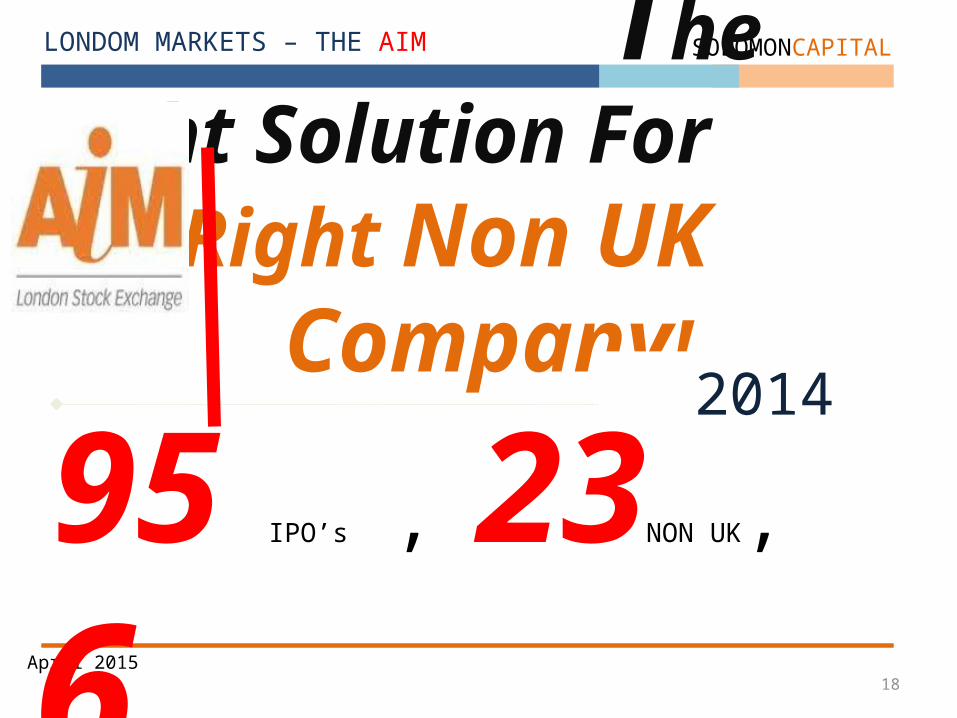

LONDOM MARKETS – THE AIM SOLOMONCAPITAL

April 2015

The Right Solution For the Right Non UK Company!

95 IPO’s , 23NON UK, 6 ISRAELIS

2014

19

SOLOMONCAPITAL

April 2015

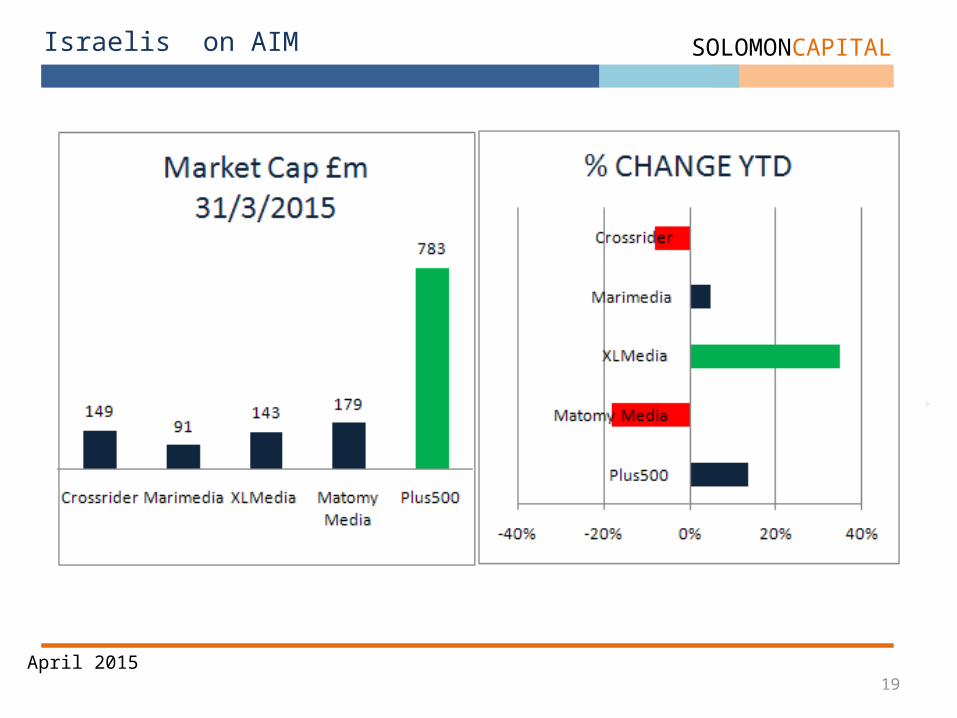

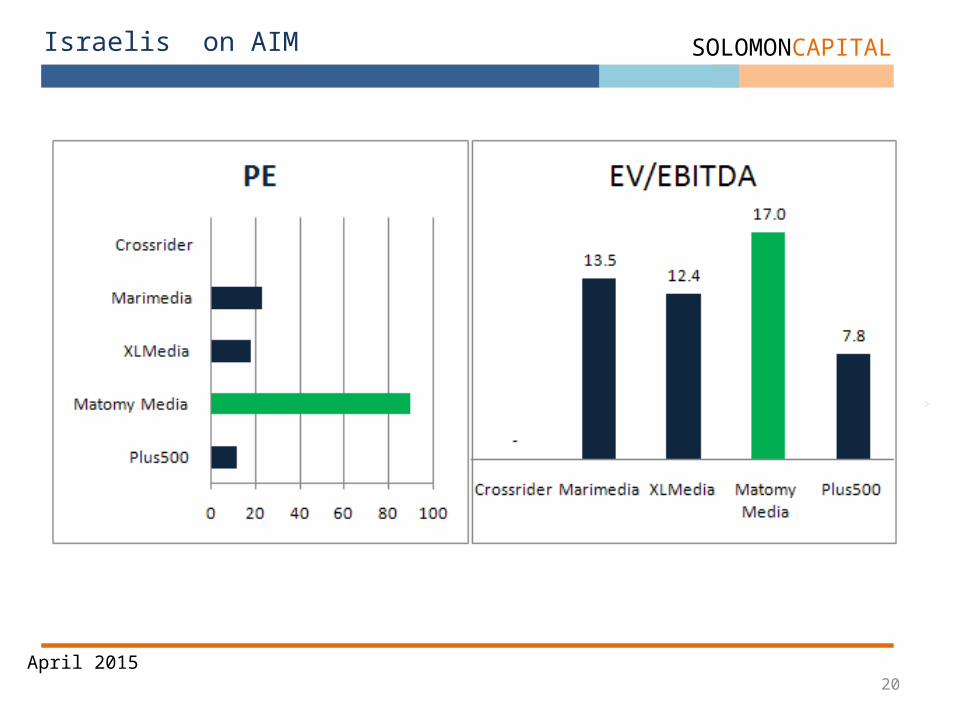

Israelis on AIM

20

Israelis on AIM SOLOMONCAPITAL

April 2015

21

SOLOMONCAPITAL

April 2015

> About Solomon Capital

> Cross Border Fundraising

> Our Approach

22

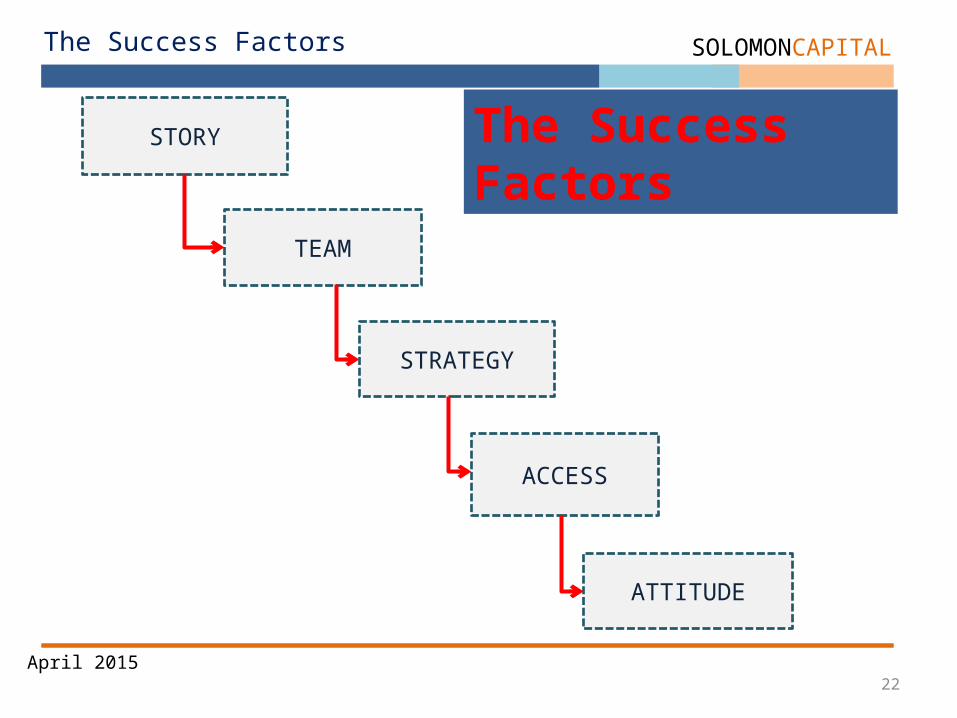

The Success Factors SOLOMONCAPITAL

April 2015

TEAM

STORY

STRATEGY

ACCESS

The Success Factors

ATTITUDE

23

The Investor Perspective SOLOMONCAPITAL

April 2015

The Investor Perspective

Remember !!

It is all About Risk Management

The Company is focusing on the

OPPORTUNITY the Investor on the RISK

24

Main Causes for Unsuccessful Fundraising SOLOMONCAPITAL

April 2015

Main Causes for Unsuccessful Fundraising• STRATEGY - Lack of Clear strategy or wrong strategy [wrong source, wrong timing,

wrong valuation]

• PREPARATION - Poor Preparation

• COMMUNICATION - Poor Company/Investor Communication,..Losing Credibility

• BAD LUCK…

If you fail to plan you plan to fail

25

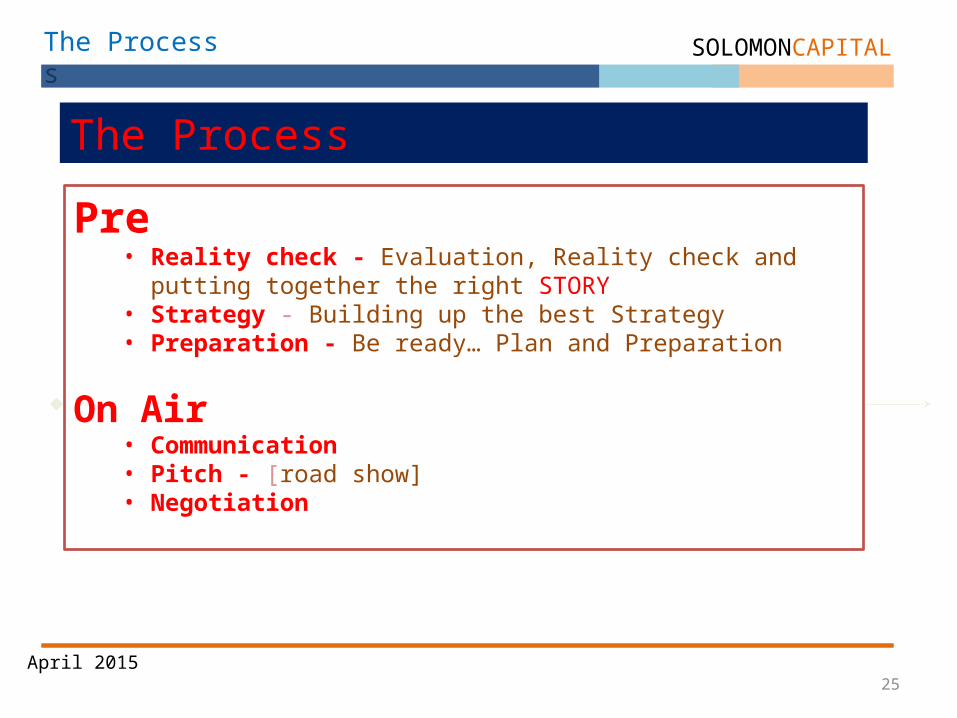

The Processs

SOLOMONCAPITAL

April 2015

The Process

Pre • Reality check - Evaluation, Reality check and putting together the right

STORY• Strategy - Building up the best Strategy• Preparation - Be ready… Plan and Preparation

On Air• Communication• Pitch - [road show]• Negotiation

26

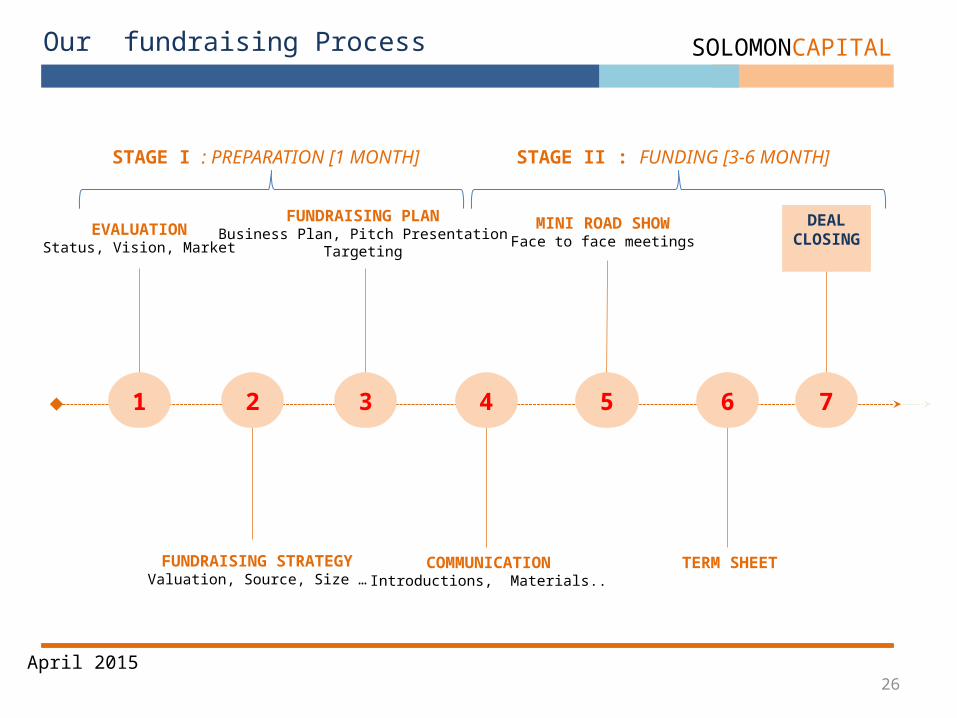

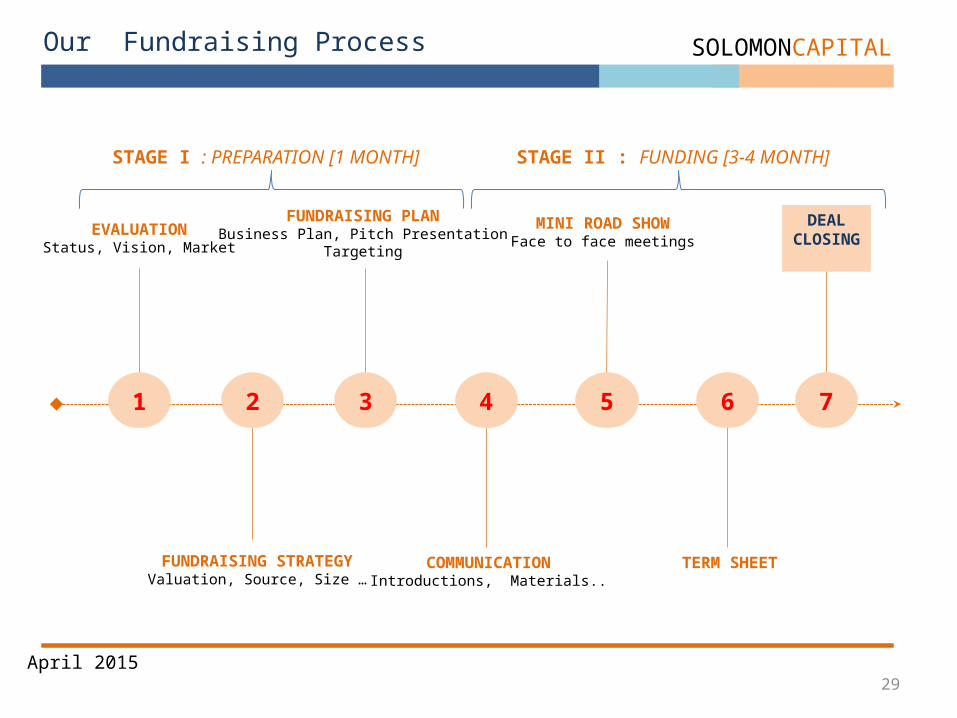

Our fundraising Process SOLOMONCAPITAL

April 2015

1 2 3 4

EVALUATIONStatus, Vision, Market

FUNDRAISING STRATEGYValuation, Source, Size …

FUNDRAISING PLANBusiness Plan, Pitch Presentation

Targeting

COMMUNICATIONIntroductions, Materials..

5

MINI ROAD SHOWFace to face meetings

6

TERM SHEET

7

DEAL CLOSING

STAGE I : PREPARATION [1 MONTH] STAGE II : FUNDING [3-6 MONTH]

27

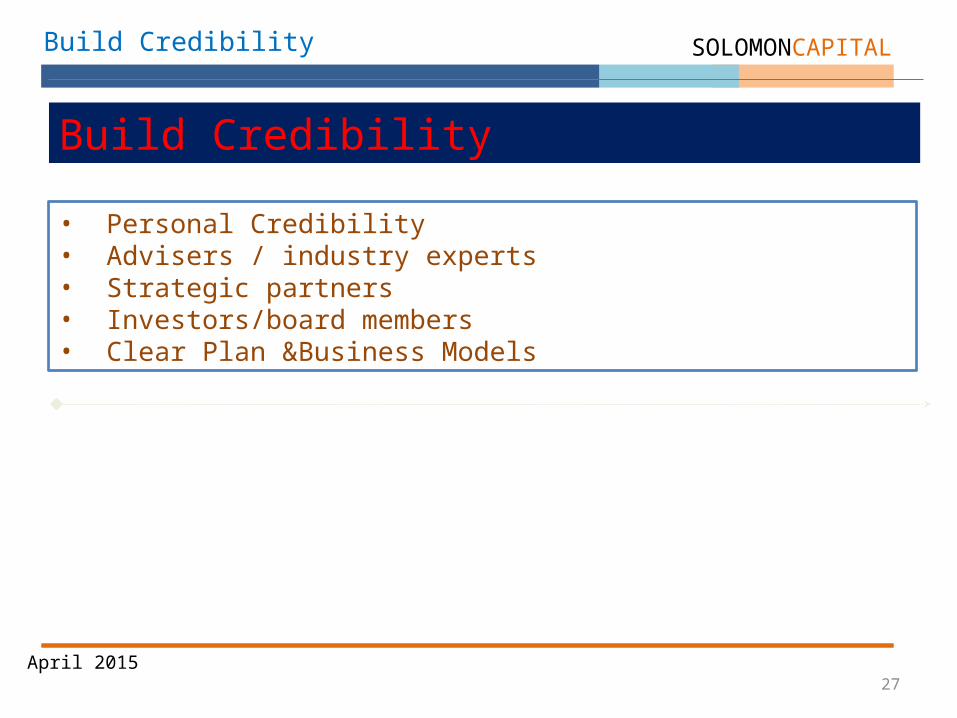

Build Credibility SOLOMONCAPITAL

April 2015

Build Credibility

• Personal Credibility• Advisers / industry experts• Strategic partners• Investors/board members• Clear Plan &Business Models

28

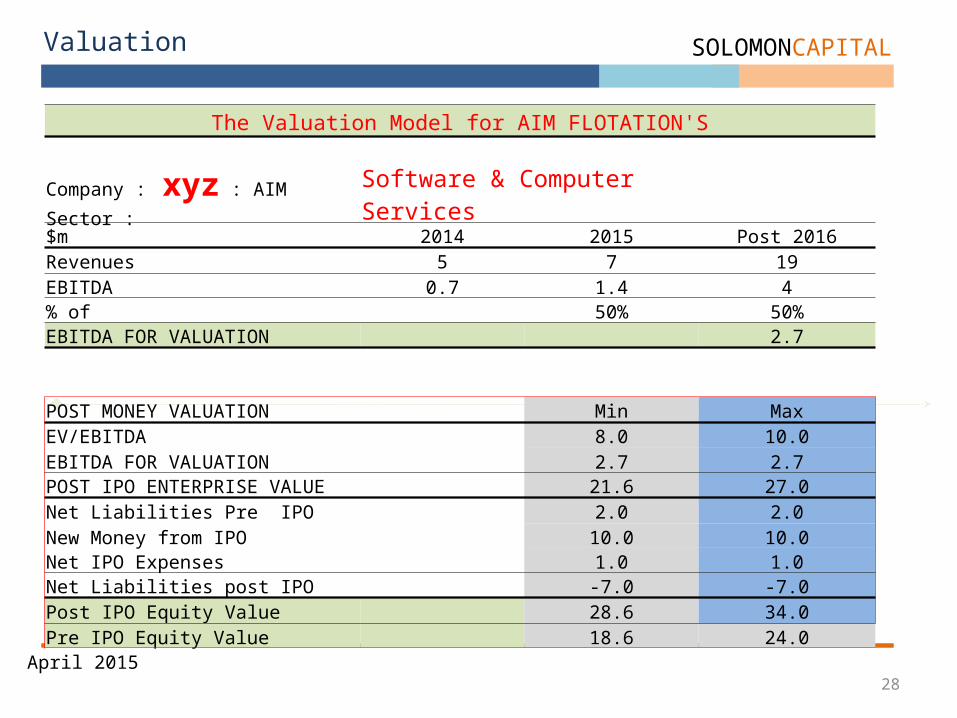

Valuation SOLOMONCAPITAL

April 2015

The Valuation Model for AIM FLOTATION'S

Company : xyz : AIM Sector : Software & Computer Services$m 2014 2015 Post 2016Revenues 5 7 19EBITDA 0.7 1.4 4% of 50% 50%EBITDA FOR VALUATION 2.7

POST MONEY VALUATION Min MaxEV/EBITDA 8.0 10.0EBITDA FOR VALUATION 2.7 2.7POST IPO ENTERPRISE VALUE 21.6 27.0Net Liabilities Pre IPO 2.0 2.0New Money from IPO 10.0 10.0Net IPO Expenses 1.0 1.0Net Liabilities post IPO -7.0 -7.0Post IPO Equity Value 28.6 34.0Pre IPO Equity Value 18.6 24.0

29

Our Fundraising Process

1 2 3 4

EVALUATIONStatus, Vision, Market

FUNDRAISING STRATEGYValuation, Source, Size …

FUNDRAISING PLANBusiness Plan, Pitch Presentation

Targeting

COMMUNICATIONIntroductions, Materials..

5

MINI ROAD SHOWFace to face meetings

6

TERM SHEET

7

DEAL CLOSING

STAGE I : PREPARATION [1 MONTH] STAGE II : FUNDING [3-4 MONTH]

SOLOMONCAPITAL

April 2015

30

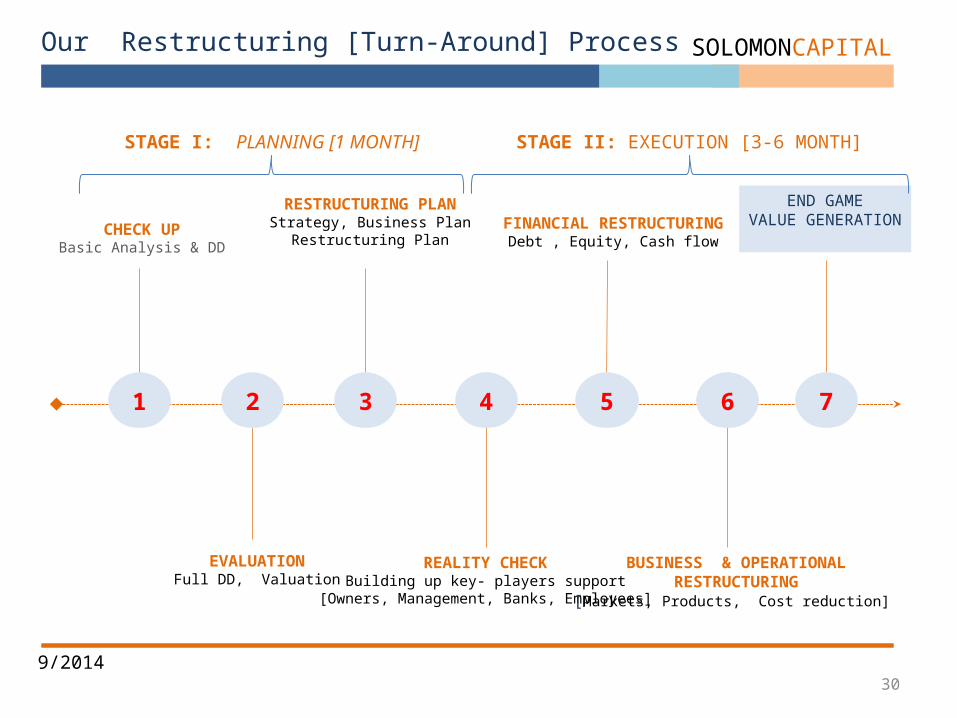

Our Restructuring [Turn-Around] Process

1 2 3 4

CHECK UPBasic Analysis & DD

EVALUATIONFull DD, Valuation

RESTRUCTURING PLANStrategy, Business Plan

Restructuring Plan

REALITY CHECKBuilding up key- players support

[Owners, Management, Banks, Employees]

5

FINANCIAL RESTRUCTURINGDebt , Equity, Cash flow

6

BUSINESS & OPERATIONALRESTRUCTURING

[Markets, Products, Cost reduction]

7

END GAMEVALUE GENERATION

STAGE II: EXECUTION [3-6 MONTH]STAGE I: PLANNING [1 MONTH]

SOLOMONCAPITAL

9/2014

SOLOMON CAPITALRaanana Israelwww.solomon-capital.com972-508-695450david@solomon-capital.com

Strictly private and confidential31

SOLOMONCAPITAL April 2015