CreditRisikDefaultModelsCreditDerivatives

192

Credit Risk, Default Models and Credit Derivatives Master of Finance, Special Course WS 2011 Prof. Dr. Wolfgang M. Schmidt Frankfurt School of Finance & Management September/October 2011 – Typeset by Foil T E X –

Transcript of CreditRisikDefaultModelsCreditDerivatives

Credit Risk, Default Models and Credit DerivativesMaster of Finance, Special Course WS 2011

Prof. Dr. Wolfgang M. Schmidt

Frankfurt School of Finance & Management

September/October 2011

– Typeset by FoilTEX –

AbstractThe course provides an introduction to the modeling and management of credit risk.

Main emphasis of the course are default models that are used in banking practice in the

fields of risk management and credit derivatives.

The first part of the course deals with credit derivatives. To understand the market for

credit derivatives, a comprehensive examination of credit default swaps is indispensable.

We investigate further important types of credit derivative products, such as, for example,

credit indices, basket default swaps or CDOs, including their modeling and valuation.

In the second part we extend the analysis of risk as covered in the core course on

risk management by investigating credit risk management in more depth. We study the

rationale behind the new Basel II accord concerning credit risk as well as industry standard

models for portfolio credit risk.

Recommended further reading are [Blum et al., 2003], [Duffie and Singleton, 2003],

[Lando, 2004], [Saunders and Allen, 2002]. For a comprehensive source on all aspects of

risk management we refer to [Jorion, 2009].

– Typeset by FoilTEX – 1

Contents

I Credit Derivatives 9

1 Introduction to credit derivatives: applications, the market and market participants 10

2 The first credit derivative: asset swap 16

3 Credit default swaps 21

3.1 First applications, cash flows and quotation . . . . . . . . . . . . . . . . . . 21

3.2 No-arbitrage relationships . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.3 The cash–CDS basis, CDS strategies of market participants . . . . . . . . . . 33

– Typeset by FoilTEX – 2

3.4 Credit linked notes, funded CDS . . . . . . . . . . . . . . . . . . . . . . . . 38

4 Mark-to-market and the CDS curve 40

4.1 Pricing directly from spread differences . . . . . . . . . . . . . . . . . . . . 41

4.2 Deriving the default probabilities from market data . . . . . . . . . . . . . . . 43

4.3 Mark-to-market valuation of credit default swaps . . . . . . . . . . . . . . . . 52

4.4 How critical are the assumptions on the recovery rate? . . . . . . . . . . . . . 53

5 Lessons from the credit crisis 55

5.1 Issues highlighted by the crisis . . . . . . . . . . . . . . . . . . . . . . . . 55

5.2 Private sectors initiatives . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

– Typeset by FoilTEX – 3

6 Strategies with CDS 62

6.1 Funding cost strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

6.2 Curve trades . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

6.3 Credit vs equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

6.4 Sub vs senior . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

7 Default modeling 68

7.1 Default intensity, hazard rate out of today . . . . . . . . . . . . . . . . . . 69

7.2 Models for the default time . . . . . . . . . . . . . . . . . . . . . . . . . . 73

7.2.1 Structural models . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

7.2.2 Reduced form models . . . . . . . . . . . . . . . . . . . . . . . . . 76

– Typeset by FoilTEX – 4

8 CDS Indices 80

9 Correlation products 85

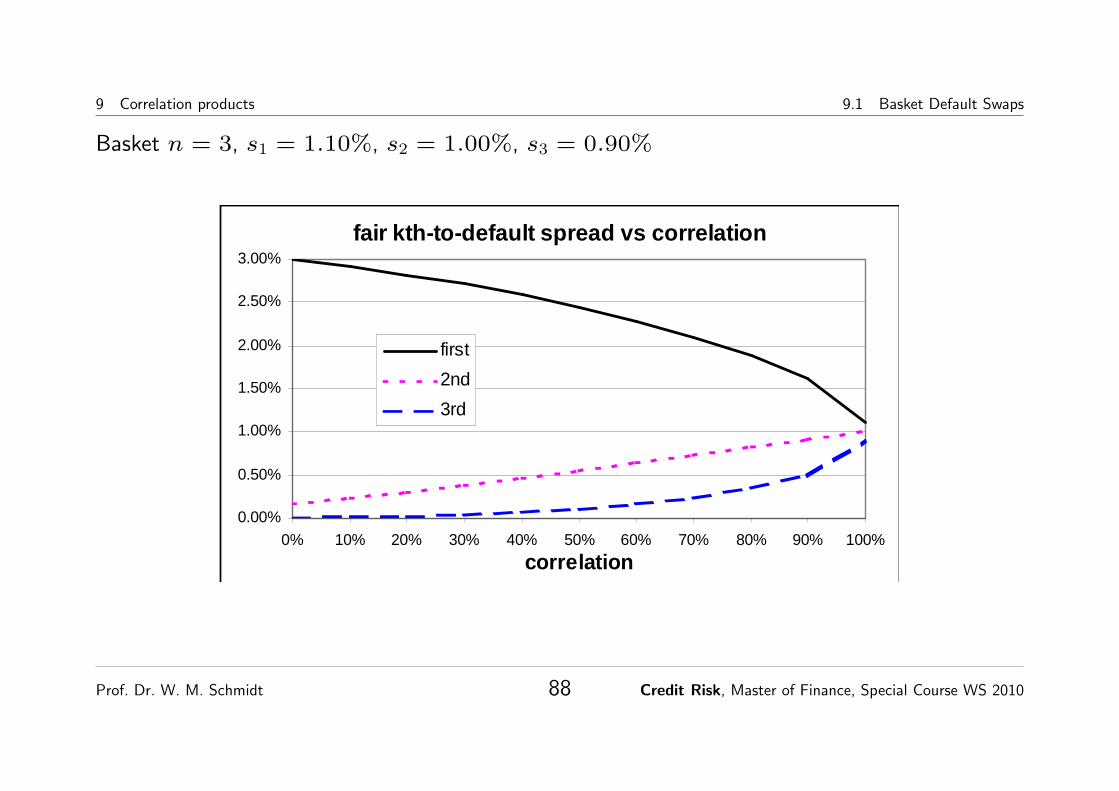

9.1 Basket Default Swaps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

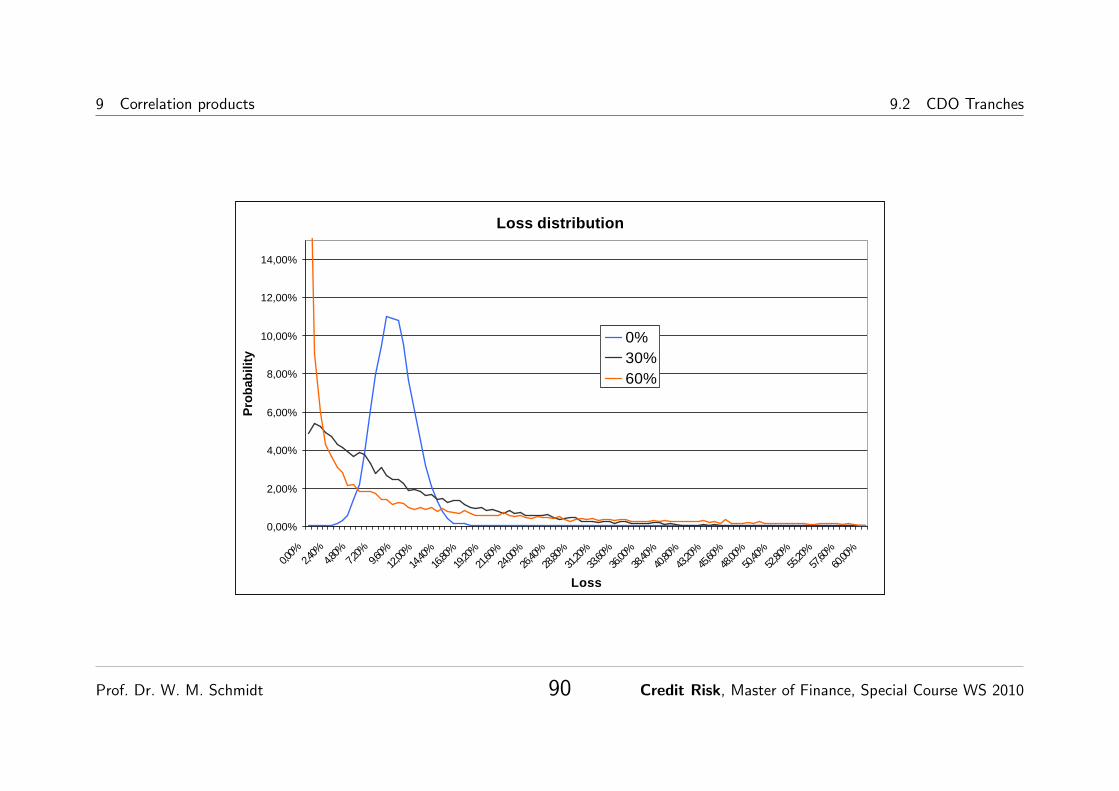

9.2 CDO Tranches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

9.3 Synthetic CDO tranches on the benchmark index . . . . . . . . . . . . . . . 91

10 What is default correlation? 94

10.1 Event correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

10.2 Asset correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

11 Monte-Carlo valuation 100

– Typeset by FoilTEX – 5

11.1 How to simulate default times? . . . . . . . . . . . . . . . . . . . . . . . . 101

11.2 How to generate dependent simulations? . . . . . . . . . . . . . . . . . . . 102

11.3 Normal copula and asset correlation . . . . . . . . . . . . . . . . . . . . . . 104

11.4 Pricing basket CDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

11.5 Pricing tranches of CDOs . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

II Credit Risk Management 113

12 Credit risk 114

13 Modeling default 117

– Typeset by FoilTEX – 6

14 Credit risk management, credit-value-at-risk and Basel II 122

14.1 Traditional methods of credit risk management . . . . . . . . . . . . . . . . 122

14.2 Traditional approaches to credit risk assessment . . . . . . . . . . . . . . . . 124

14.3 Economic capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

14.4 Portfolio risk - the correlation problem . . . . . . . . . . . . . . . . . . . . . 129

14.5 Regulatory requirements, Basel II . . . . . . . . . . . . . . . . . . . . . . . 133

15 Credit risk management in banks and industry standard models 141

15.1 Estimating default probabilities . . . . . . . . . . . . . . . . . . . . . . . . 141

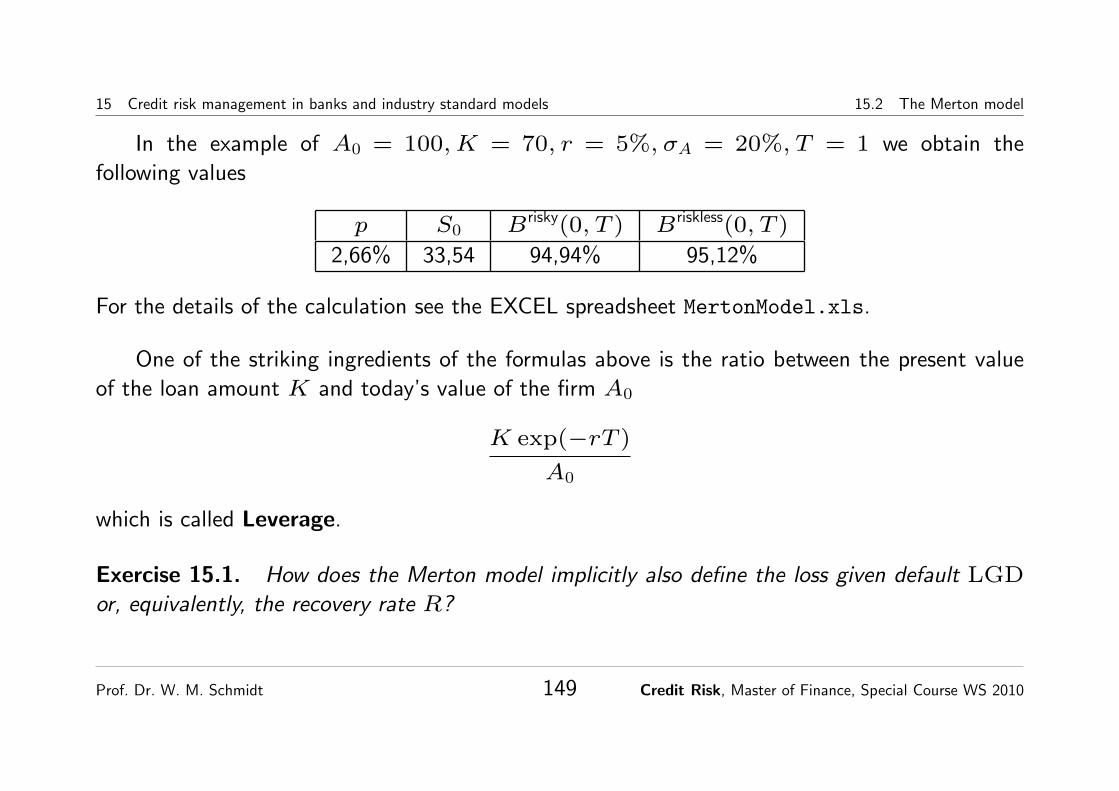

15.2 The Merton model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

15.3 The KMV model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

– Typeset by FoilTEX – 7

15.3.1 Dependent defaults in the Merton model . . . . . . . . . . . . . . . . 152

15.3.2 1-Factor dependence and the Basel II formula . . . . . . . . . . . . . 156

15.4 CreditMetrics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

15.5 Credit Risk+ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

15.6 Comparison KMV/CreditMetrics versus CreditRisk+ . . . . . . . . . . . . . . 184

Prof. Dr. W. M. Schmidt 8 Credit Risk, Master of Finance, Special Course WS 2010

Part I

Credit Derivatives

Prof. Dr. W. M. Schmidt 9 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

1 Introduction to credit derivatives: applications, the marketand market participants

Credit derivatives allow for a customized and flexible transfer of credit risk independently of some

funding. Traditional credit products such as loans or bonds are restricted in terms of available

conditions, in addition they require an initial investment of capital (funding).

The rationale and economic motivation of market participants to enter into credit derivatives

to take on “positive” or “negative” credit risk exposures can be quite different.

Credit derivatives can be used to

• reduce/hedge credit risk,

• actively take certain credit risks,

• generate extra returns,

• set up tailor made structured credit risk profiles,

Prof. Dr. W. M. Schmidt 10 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

• generate synthetic bonds/loans that are not available in the market in this form (time to

maturity, currency, etc.).

Credit derivatives play an important role in efficient allocation of risk and capital.

The market size in credit derivatives still continues to grow dramatically every year.

The outstanding volume in credit derivatives nowadays exceeds the volume in equity derivatives

and corporate bond issuance.

Prof. Dr. W. M. Schmidt 11 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

In

te

rn

atio

na

l to

pic

s

Cu

rre

nt Issue

s

Author

Christian Weistroffer*

+49 69 910-31881

Editor

Bernhard Speyer

Technical Assistant

Angelika Greiner

Deutsche Bank Research

Frankfurt am Main

Germany

Internet:www.dbresearch.com

E-mail: [email protected]

Fax: +49 69 910-31877

Managing Director

Norbert Walter

The use of credit default swaps (CDSs) has become increasingly popular

over time. Between 2002 and 2007, gross notional amounts outstanding grew

from below USD 2 trillion to nearly USD 60 trillion.

The recent crisis has revealed several shortcomings in CDS market

practices and structure. Lack of information on the whereabouts of open

positions as well as on the extent of economic risk borne by the financial sector

are partly to blame for the heavy reactions observed during the crisis. In addition,

management of counterparty risk has proved insufficient, as has in some

instances the settlement of contracts following a credit event.

Past problems should not distract from the potential benefits of these

instruments. In particular, CDSs help complete markets, as they provide an

effective means to hedge and trade credit risk. CDSs allow financial institutions to

better manage their exposures, and investors benefit from an enhanced

investment universe. In addition, CDS spreads provide a valuable market-based

assessment of credit conditions.

Currently, the CDS market is transforming into a more stable system. Various

private-led measures are being put in place that help enhance market

transparency and mitigate operational and systemic risk. In particular, central

counterparties have started to operate, which will eventually lead to an improved

management of individual as well as system-wide risks.

Meanwhile, regulation should be designed with caution and be restricted to

averting clear market failures. Regulators should avoid choking the market for

bespoke credit derivatives, as many end-users are highly dependent on tailor-

made solutions. From an analytical point of view, it has yet to be established under

which conditions CDS trading – as opposed to hedging – does more harm than

good, and whether central trading – in addition to central clearing – is required to

achieve systemic stability.

*The author thanks Anja Baum for outstanding research assistance including the preparation of

a first draft of this paper.

Credit default swaps

Heading towards a more stable system December 21, 2009

0

10,000

20,000

30,000

40,000

50,000

60,000

Dec 02 Dec 03 Dec 04 Dec 05 Dec 06 Dec 07 Dec 08

Multi-name instruments Single-name instruments

From nought to sixty in 5 years

Sources: BIS (2009), ISDA (2009)

Gross notional amount outstanding, USD bn.

Notional amount of outstanding debt securities is USD 80 trillion (IWF, 2008).

Prof. Dr. W. M. Schmidt 12 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

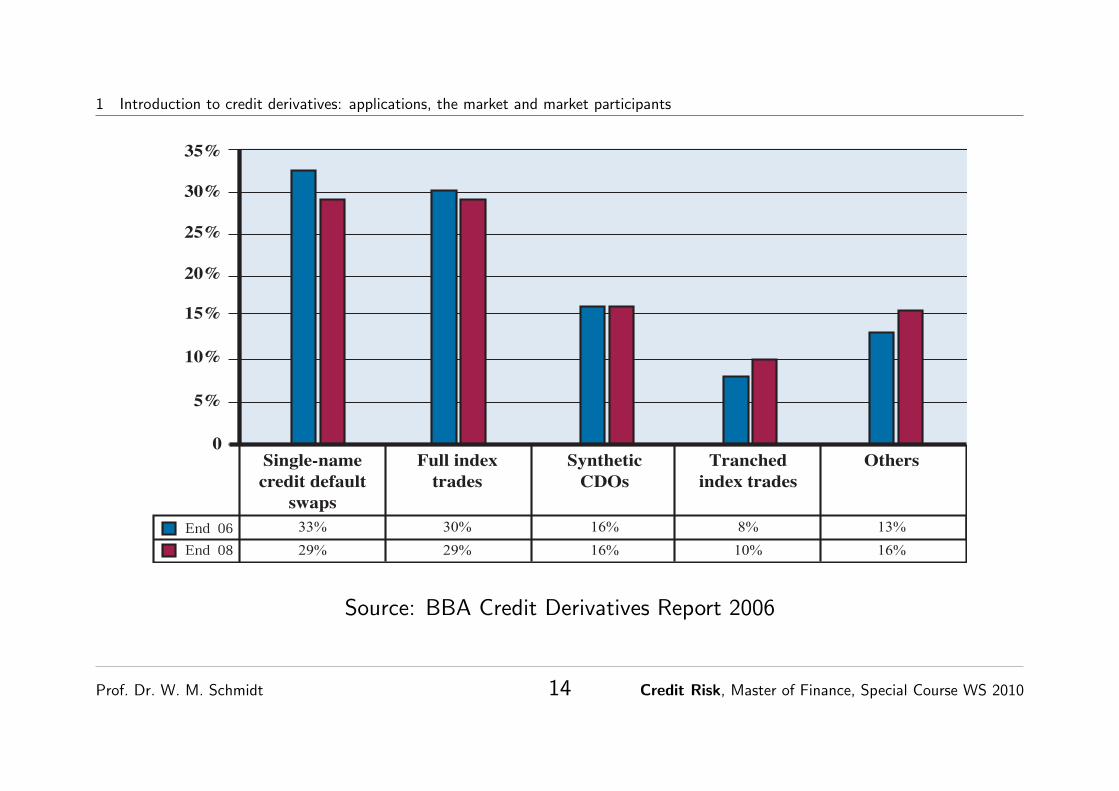

The dominating credit derivative product are still single name credit default swap (CDS)followed by index products, which are expected to grow further.

activity due to ‘Banks – Trading Activities’ and ‘Banks – Loan Portfolio’ to provide an emphasis on whyactivity was taking place rather than a distinction between the types of banks involved. This has high-lighted that almost two thirds of banks’ derivatives volume is due to trading and a third is related to theirloan book.

4. Product rangeIn line with the view of the BBA Credit Derivatives Panel, the range of products included in the surveyquestionnaire has been heavily revised to reflect current market trends. Single name credit default swapsstill represent a substantial section of the market, however the share has fallen to 33%. Index trades havebecome the second largest product representing 30% as at Q1 2006. The last two years have seen atremendous increase in the speed of development of credit derivatives products, with continuing diversi-fication expected. Synthetic CDOs (collateralised debt obligation) have continued to maintain position at16% of the market.

Credit Derivatives Products

British Bankers’ Association – Credit Derivatives Report 2006

6

0

5%

10%

15%

20%

25%

30%

35%

End 06

End 08

Single-name

credit default

swaps

33%

29%

Full index

trades

30%

29%

Synthetic

CDOs

16%

16%

Tranched

index trades

8%

10%

Others

13%

16%

Type 2000 2002 2004 2006

Basket products 6.0% 6.0% 4.0% 1.8%

Credit linked notes 10.0% 8.0% 6.0% 3.1%

Credit spread options 5.0% 5.0% 2.0% 1.3%

Equity linked credit products n/a n/a 1.0% 0.4%

Full index trades n/a n/a 9.0% 30.1%

Single-name credit default swaps 38.0% 45.0% 51.0% 32.9%

Swaptions n/a n/a 1.0% 0.8%

Synthetic CDOs – full capital n/a n/a 6.0% 3.7%

Synthetic CDOs – partial capital n/a n/a 10.0% 12.6%

Tranched index trades n/a n/a 2.0% 7.6%

Others 41.0% 36.0% 8.0% 5.7%

Source: BBA Credit Derivatives Report 2006

Prof. Dr. W. M. Schmidt 13 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

activity due to ‘Banks – Trading Activities’ and ‘Banks – Loan Portfolio’ to provide an emphasis on whyactivity was taking place rather than a distinction between the types of banks involved. This has high-lighted that almost two thirds of banks’ derivatives volume is due to trading and a third is related to theirloan book.

4. Product rangeIn line with the view of the BBA Credit Derivatives Panel, the range of products included in the surveyquestionnaire has been heavily revised to reflect current market trends. Single name credit default swapsstill represent a substantial section of the market, however the share has fallen to 33%. Index trades havebecome the second largest product representing 30% as at Q1 2006. The last two years have seen atremendous increase in the speed of development of credit derivatives products, with continuing diversi-fication expected. Synthetic CDOs (collateralised debt obligation) have continued to maintain position at16% of the market.

Credit Derivatives Products

British Bankers’ Association – Credit Derivatives Report 2006

6

0

5%

10%

15%

20%

25%

30%

35%

End 06

End 08

Single-name

credit default

swaps

33%

29%

Full index

trades

30%

29%

Synthetic

CDOs

16%

16%

Tranched

index trades

8%

10%

Others

13%

16%

Type 2000 2002 2004 2006

Basket products 6.0% 6.0% 4.0% 1.8%

Credit linked notes 10.0% 8.0% 6.0% 3.1%

Credit spread options 5.0% 5.0% 2.0% 1.3%

Equity linked credit products n/a n/a 1.0% 0.4%

Full index trades n/a n/a 9.0% 30.1%

Single-name credit default swaps 38.0% 45.0% 51.0% 32.9%

Swaptions n/a n/a 1.0% 0.8%

Synthetic CDOs – full capital n/a n/a 6.0% 3.7%

Synthetic CDOs – partial capital n/a n/a 10.0% 12.6%

Tranched index trades n/a n/a 2.0% 7.6%

Others 41.0% 36.0% 8.0% 5.7%

Source: BBA Credit Derivatives Report 2006

Prof. Dr. W. M. Schmidt 14 Credit Risk, Master of Finance, Special Course WS 2010

1 Introduction to credit derivatives: applications, the market and market participants

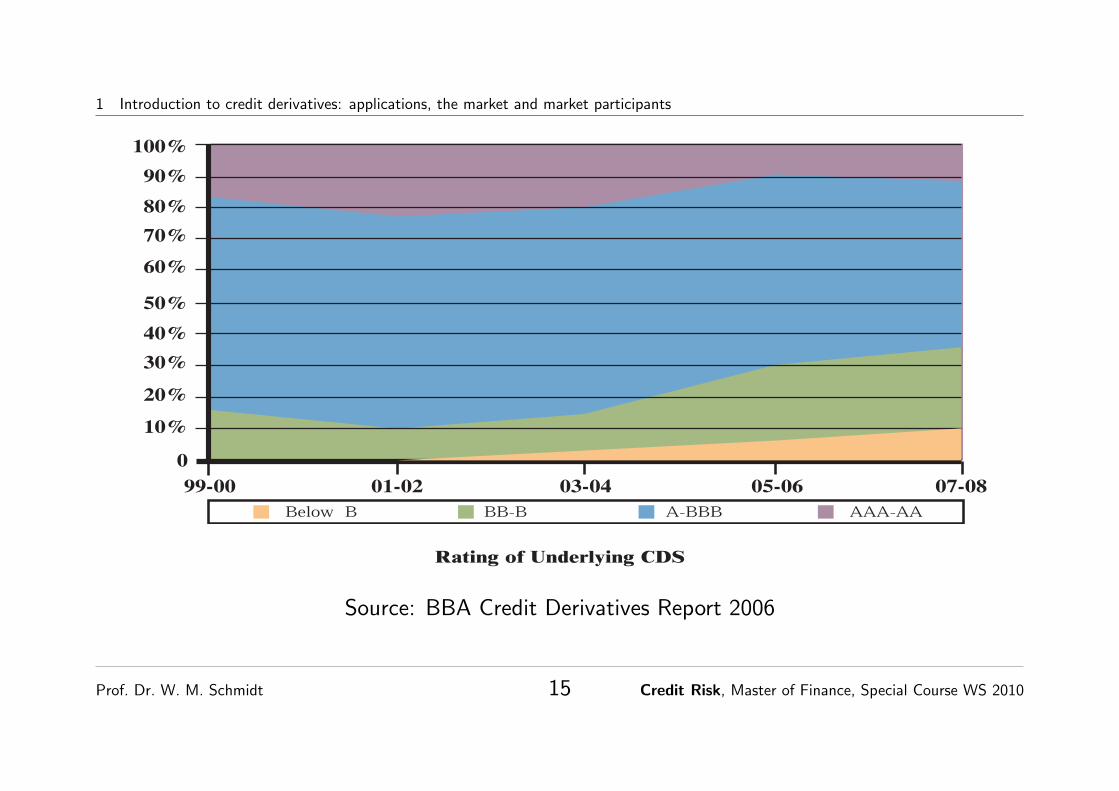

5. Rating of underlying assets

In this year’s survey a much more granular view has been taken of the ratings of the underlying assets thanpreviously. Underlying ratings of assets in CDS and Indices are now split out. Overall there has been adownward migration of average rating of underlying assets. For CDS the AAA – BBB category has fallenfrom 65% in 2004 to 59% in 2006 and this is estimated to continue to fall to 52% by end of 2008.Conversely the BB - B category has expanded from 13% to 23% and is expected to continue to grow to27% by end 2008.

Rating of Underlying CDS

6. Credit events

Every respondent has experienced credit events that triggered payment over the period. The highestnumber of credit events occurred in the high yield sector. There was an even spread of events across thecategories specified: Investment grade Europe, Investment grade US, Emerging markets, high yield,Asia/Australia and other. Delphi, Dana Corp, and Delta were the credits most frequently referred to as trig-gering payment.

7. Payouts

In contrast to the 2004 survey physical settlement has dropped from 86% down to 73%. The main shifthas been toward cash settlement which has more than doubled to 23% from 11% last year. Fixed amountsettlement remained the same at 3%. Quarterly settlement has continued to have an impact on firms.

Selected Participant Comment:

1. In the long term, the move to quarterly settlement will improve credit derivatives markets by increasingstandardization of product, which in turn drives liquidity. In the short term, quarterly settlement has madethe business more operationally intensive which has increased costs. Therefore, the short term benefit isless clear given the increased operational intensity.

British Bankers’ Association – Credit Derivatives Report 2006

7

0

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

99-00 01-02 03-04 05-06 07-08

Below B BB-B A-BBB AAA-AA

Source: BBA Credit Derivatives Report 2006

Prof. Dr. W. M. Schmidt 15 Credit Risk, Master of Finance, Special Course WS 2010

2 The first credit derivative: asset swap

Time to maturity of CDS are mainly 5 years and with increasing liquidity in 3 and 7-10 years.

Major market participants are banks, insurance companies, corporates, hedge funds and

pension funds. Banks are protection buyers as well as protection sellers whereas insurance

companies are mainly protection sellers. Hedge funds enter into CDS as protection seller for yield

enhancement or leverage, or as protection buyer, e.g., in case of convertible bonds arbitrage.

2 The first credit derivative: asset swap

The purpose of an asset swap is to exchange the fixed coupons of a bond versus Libor ± some

corresponding spread. The intention of the investor owning the fixed coupon bond is basically

to exchange that bond for a par floater with the same default risk and same maturity. Since

the exchange of the notional amount of both bonds cancel out, what is left is just the exchange

of the fixed versus floating coupons. Motivation of the transaction is to reduce the sensitivity

of the investment with respect to changes in market interest rates, since the floater has almost

Prof. Dr. W. M. Schmidt 16 Credit Risk, Master of Finance, Special Course WS 2010

2 The first credit derivative: asset swap

(depending on the spread) no duration. On the other hand, the spread over Libor extracts the

premium paid in return for taking the default risk.

Contrary to a plain interest rate swap there are some tricky details to take care of which

are necessary to achieve the above goal of the transaction. We discuss the most popular type

of an asset swap, the so-called par-par asset swap. First, at inception of the asset swap there

is an upfront payment of dirty price Pd of the bond minus 100 (par). In principle this can be

interpreted as the investor selling his bond at Pd and buying at the same time a par floater. On

the fixed side of the swap there is always a full first coupon payment, even if the swap start is

somewhere in the middle of a coupon period. However, on the floating side there is normally a

short first floating period ranging from the asset swap start to the first regular fixed coupon date:

Prof. Dr. W. M. Schmidt 17 Credit Risk, Master of Finance, Special Course WS 2010

2 The first credit derivative: asset swap

-time

swap start

6

dirty price - 100

6

6 6 6

? ?

maturityof the bond

6

?

+100

-100coupon payments

Libor ± spread s

Evaluating an asset swap just requires discounting its cash flows with the discount factors of the

Prof. Dr. W. M. Schmidt 18 Credit Risk, Master of Finance, Special Course WS 2010

2 The first credit derivative: asset swap

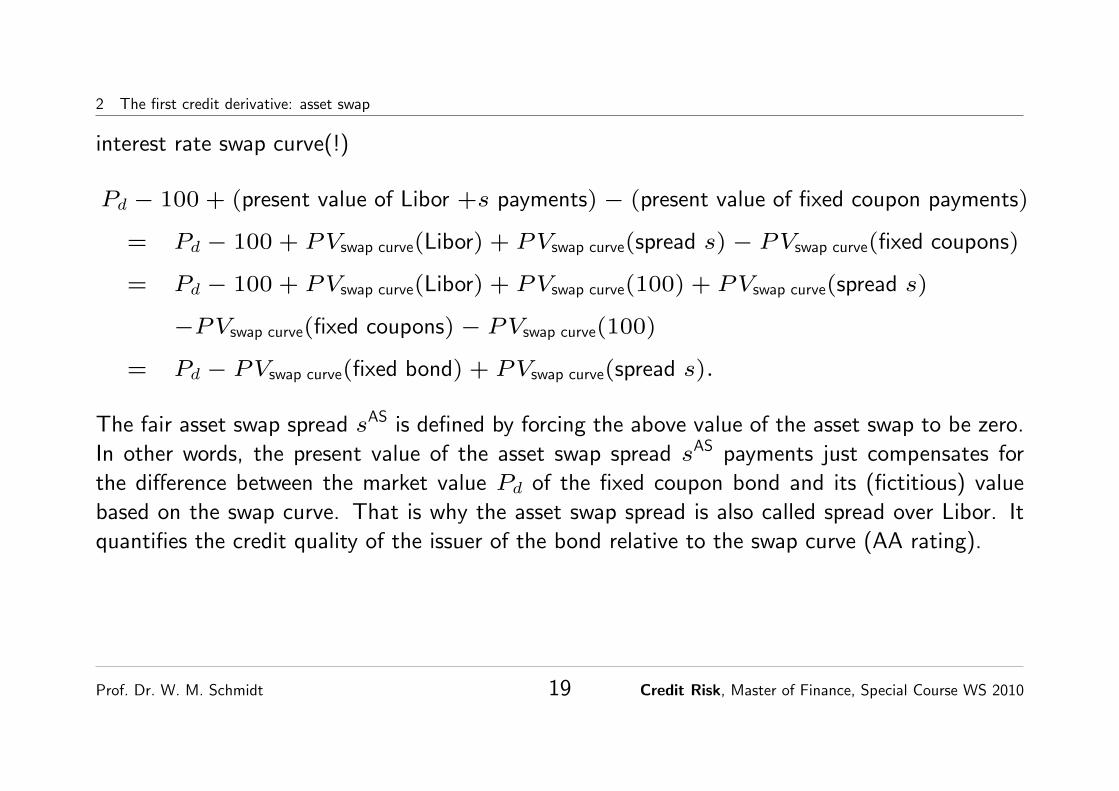

interest rate swap curve(!)

Pd − 100 + (present value of Libor +s payments)− (present value of fixed coupon payments)

= Pd − 100 + PVswap curve(Libor) + PVswap curve(spread s)− PVswap curve(fixed coupons)

= Pd − 100 + PVswap curve(Libor) + PVswap curve(100) + PVswap curve(spread s)

−PVswap curve(fixed coupons)− PVswap curve(100)

= Pd − PVswap curve(fixed bond) + PVswap curve(spread s).

The fair asset swap spread sAS is defined by forcing the above value of the asset swap to be zero.

In other words, the present value of the asset swap spread sAS payments just compensates for

the difference between the market value Pd of the fixed coupon bond and its (fictitious) value

based on the swap curve. That is why the asset swap spread is also called spread over Libor. It

quantifies the credit quality of the issuer of the bond relative to the swap curve (AA rating).

Prof. Dr. W. M. Schmidt 19 Credit Risk, Master of Finance, Special Course WS 2010

2 The first credit derivative: asset swap

Often, asset swaps are traded as so-called packages, i.e., the underlying fixed coupon bond

plus the asset swap. At inception an asset swap package is always worth par. The investor gets a

synthetic default risky par floater paying Libor plus asset swap spread.

Computer Exercise 2.1. Calculate the fair asset swap spread for a bond with annual coupon

of C = 5%, issue date of the bond 20.04.1999 and time to maturity 10 years. Today the bond

trades at a (clean) price of 103,31. Use the EXCEL sheet ZinsPricer.xls with the given swap

curve there.

Prof. Dr. W. M. Schmidt 20 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps

3 Credit default swaps

3.1 First applications, cash flows and quotation

In a credit default swap (CDS) counter party A pays an insurance premium to counter party Band receives in return some payment from B in case a specified credit event (related to some

entity C) takes place during the lifetime of the swap. Normally the credit event is the default of

one or more underlying reference assets (e.g., bonds) issued by a certain reference entity C.

A credit default swap is nothing else but an insurance contract. The protection buyer Apays an insurance fee (premium, spread) and receives in return from the protection seller Bcompensation for the loss in case the insured event happens.

The (insurance) premium is quoted in basis points referring to some notional amount and is

paid on a regular basis during the life time of the CDS.

If the insured event takes place during the life time of the CDS the protection buyer normally

Prof. Dr. W. M. Schmidt 21 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

delivers the defaulted reference asset (or some other qualified equivalent asset) with the agreed

notional amount and in return gets compensated by a payment of the full notional amount from

the protection seller. This is called physical settlement. Alternatively, one can agree on cashsettlement, that is, the cash amount of par minus the market price of the defaulted asset is paid

to the protection buyer. Most of the trades settle physically. However, if for example, the CDS is

part of a synthetic CDO construction then there will be cash settlement.

protection buyer protection seller

A-

�

premium (spread) s

in case of default: par - defaulted asset B

Prof. Dr. W. M. Schmidt 22 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

To specify a credit default swap one has to determine the following terms of the trade:

• reference entity, reference assets, e.g., bonds issued by ABC,

• credit event to be insured, normally default,

• notional amount NPA, e.g., 10 Mio. EUR,

• start of the CDS, start of the spread payments, protection start T0,

• time to maturity Tn,

• frequency and day count convention of spread payments, e.g.,quarterly, act/360,

• premium, spread s, e.g., s = 1.00%,

• payment in case of insurance event and its settlement (physical, cash).

To simplify we will always think of the credit event as being just default of the reference

entity.

Prof. Dr. W. M. Schmidt 23 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

The cash flows of a CDS can be visualized as follows. Starting with the start date T0 the spread

period dates T0, T1, . . . , Tn are determined according to the given frequency. Non-business days

are usually adjusted applying the convention Modified Following.

Denote by τ the time of default of the reference entity. Today the precise value of τ is

not known, it is a random variable. For entities with low default risk the probability that τ will

“happen” in the near future is very low.

-

T0 T1 T2 Tn

6 6 6

?

τ

66

. . .

Prof. Dr. W. M. Schmidt 24 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

Payments to the protection seller

For each period [Ti−1, Ti] at the end Ti of the period the protection seller receives the

amount NPA s ∆i as long as there has been no default until Ti. Here ∆i denotes the length

of the period [Ti−1, Ti] according to the given day count convention. If there happens to be a

default inside the period [Ti−1, Ti], i.e., Ti−1 < τ < Ti, there will be normally a payment of the

spread accrued over the period [Ti−1, τ ]. The spread payments terminate at the time of default

or maturity whatever comes first.

Payments to the protection buyer

In case of a default during the lifetime of the CDS the protection buyer receives “at” the

time τ of default a compensation which is worth NPA(1 − R), where R denotes the recoveryrate. In case of cash settlement this is exactly the cash amount paid to the protection buyer,

for physical settlement the delivered defaulted reference asset is worth −NPAR for which the

protection buyer gets a compensation of NPA (par).

Prof. Dr. W. M. Schmidt 25 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

The fair default swap spread sCDS (short: CDS spread) is defined by the fact that the

underlying CDS is worth zero, i.e., fair. In most cases, at inception of a CDS the premium is

agreed to be fair.

The market quotes credit default swaps by their fair spreads sCDS. We emphasize that fair

means that the market considers a CDS with this spread as being worth 0. We will have to

discuss later on what this means in relation to other products, e.g., asset swaps. Also observe the

analogy to interest rate swaps where the market quotes fair swap rates.

Prof. Dr. W. M. Schmidt 26 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

Prof. Dr. W. M. Schmidt 27 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.1 First applications, cash flows and quotation

Remark:In addition to the credit risk of the reference entity of the CDS we are also facing a credit risk

with respect to the counter party. The default risk of the protection seller is obviously particularly

important. If the default of the reference entity is “highly correlated” with the default of the

protection seller, then the CDS gives basically no protection to the protection buyer. In the

following we will ignore the default risk of the CDS counter parties. In practice this risk is often

managed by requiring some collateral.

Exercise 3.1. Often default swaps are interpreted solely as insurance against default. Why is

this wrong and how does a CDS also offer insurance against changes in credit quality?

Prof. Dr. W. M. Schmidt 28 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.2 No-arbitrage relationships

3.2 No-arbitrage relationships

In this section we discuss the problem of what the fair premium (CDS spread) for protection in a

CDS should be.

The default risk of credit risky investments such as bonds is quantified by various different

notions of spread used by practitioners. There are, e.g., the so-called yield spread, asset swap

spread, discount spread etc. So how do these spreads relate to the CDS spread?

In our discussion we first assume an idealized market for getting some fundamental theoretical

insights into the relationship of the CDS spread to other spreads in the market. However, in

practice things get much more involved and in real life one often observes derivations from the

theoretical relationships. We shall investigate these problems afterwards.

The valuation of derivatives is based on the no-arbitrage principle. In the simplest case

an arbitrage is a clever combination of transactions which yields a risk free gain without any

investment. The market would exploit those opportunities immediately and in an idealized world

arbitrage opportunities do not exist, i.e., prices in the market are in an arbitrage free relationship.

Prof. Dr. W. M. Schmidt 29 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.2 No-arbitrage relationships

We start by discussing the so-called par-spread. Imagine there is a floating rate bond issued

by the reference entity of our credit default swap. The bond pays as coupon Libor + spread and

trades at a price of 100 (par). The corresponding spread is called the par-spread spar and the

bond is a par-floater.

We have the following relationship:

CDS Spread ≈ Par-Spread

Here is the argument: investing into a par floater and, at the same time, buying protection

on the issuer via a CDS yields an investment where the investor gets a net coupon payment of

Libor + (spar − sCDS

).

But the combined position consisting of the par floater and the CDS is equivalent to a risk free

floating rate bond. Indeed, in case of a default of the risky par floater the CDS will cover exactly

the loss and we will get always a full redemption of our investment. In a risk free floater the

Prof. Dr. W. M. Schmidt 30 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.2 No-arbitrage relationships

coupon is just Libor and therefore, to avoid arbitrage,

0 = spar − sCDS

.

Exercise 3.2. There are several gaps in the above argument, find out where! In particular

analyse exactly the cash flows of the involved transactions in the situation of a default.

Adapt the reasoning further, taking into account that buying the par floater the investor has to

finance the investment by his own refinancing conditions.

In reality par floaters rarely exist. The above discussion is just a preparation to analyse the

relationship between the CDS spread sCDS and the asset swap spread sAS.

As discussed in Section 2 an asset swap package can be seen as a synthetic par floater and

we get from that and the preceding discussion immediately the following relationship:

Prof. Dr. W. M. Schmidt 31 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.2 No-arbitrage relationships

CDS Spread ≈ Asset Swap Spread

But again there are several gaps in the argument. Compared to a par floater the behavior of

the asset swap package in default is different. If there happens to be a default of the underlying

bond the investor of the asset swap package receives the recovery from the bond, but in addition

to that he is still exposed as a fixed rate (coupon) payer in the interest rate swap. Depending

on the prevailing market conditions (swap curve) the interest rate swap has some (positive or

negative) market value contributing to the overall recovery of the package.

Anyway, independently of the many details to take into account, the asset swap spread gives

a first rough indication what the fair CDS spread should be.

Prof. Dr. W. M. Schmidt 32 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.3 The cash–CDS basis, CDS strategies of market participants

3.3 The cash–CDS basis, CDS strategies of market participants

In practice one observes quite often significant differences between the quoted fair CDS premiums

and the spreads in the cash market (bonds, asset swaps). This difference is called the cash–CDSbasis. The reasons for these differences are mainly supply and demand (liquidity) in the different

markets. Theoretically this would yield arbitrage opportunities but in reality one is in most cases

not able to take advantage of them.

The following table shows observed differences between the CDS spread and the asset swap

spread as quoted in the market.

Prof. Dr. W. M. Schmidt 33 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.3 The cash–CDS basis, CDS strategies of market participants

Default Swap Asset Swap Basis

Bid/Offer Bid/Offer (Bid-Offer)

Bank of America 48/55 46/43 5

Bank One Corp 60/75 65/60 0

Chase Corp 40/48 35/30 10

Citigroup 38/45 30/27 11

First Union 68/85 66/63 5

Goldman 45/55 46/41 4

Lehman Br 70/80 68/63 7

Merrill Lynch 40/50 28/23 17

Morgan Stanley 45/55 28/23 22

The basis, i.e., CDS minus asset swap spread, can be both, positive or negative. For the

telecommunication sector the basis was as high as 80 basis points as observed in February 2001

for Deutsche Telekom. However, as a result of relative value strategies exploited by market

participants the basis stays inside certain bounds.

Prof. Dr. W. M. Schmidt 34 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.3 The cash–CDS basis, CDS strategies of market participants

For example, in case the basis is positive, i.e., sCDS > sAS, one could try to realize an

arbitrage gain by selling protection and at the same time shorting the bond. However, in practice

shorting a bond is not easy and may require additional costs so this theoretical arbitrage strategy

can often not be realized. In general a CDS is the perfect instrument to short credit risk by buying

protection whereas in the cash market it is difficult to enter into a negative credit exposure.

There are typical situations where the demand for buying protection is particularly high and

therefore the CDS spreads are rising. One example is when convertible bonds are newly issued:

Prof. Dr. W. M. Schmidt 35 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.3 The cash–CDS basis, CDS strategies of market participants

Credit Default Swap Handbook – 31 January 2002

19

opportunities to sell protection and generate compelling relative value.

A typical situation where such a discrepancy can occur is during and following theissuance of a convertible bond. In such circumstances CB investors may look tounlock “cheap” equity volatility by hedging credit risk – the credit derivativemarket typically offers the most effective means of doing this quickly in largesize. Another factor that can drive default swap spreads on a broader range ofcredits is the launch of large synthetic CDO transactions. In order to sell syntheticcredit risk into these structures, the originating investment banks will typicallyhave to build up long credit positions (sell protection) before or immediately afterthe transaction which will tend to pull default swap spreads tighter. Sometimesthe investment bank may buy this credit exposure in the cash market but theliquidity for major names in the default swap market combined with a wish toavoid basis risk tends to favour selling protection.

Chart 18: Fiat Default Swap Basis Widened Sharply Following Its CB Issue

50

70

90

110

130

150

170

190

210

16-Oct-01 30-Oct-01 13-Nov-01 27-Nov-01 11-Dec-01 25-Dec-01 8-Jan-02 22-Jan-02

5yr Default FIAT 5.75% May-2006 Asset Swap

Spread (bp)

Source: Merrill Lynch

� Unfunded vs. Funded

A key difference between selling protection and buying an asset swap is that thedefault swap is unfunded. However, due to the nature of the transaction, theprotection seller is effectively locking a spread above LIBOR. Thus for aninvestor which is funded above LIBOR selling protection tends to be particularlyattractive. In our opinion, this represents a key advantage for the synthetic marketfor two reasons:

1. Most market participants and “street” trading desks fund their credit books atspreads above LIBOR. Default swaps therefore give the opportunity ofgenerating greater carry than similarly yielding asset swaps.

2. Losing the necessity to fund the credit purchase, makes it easier for creditbuyers to leverage their credit views without actually borrowing.

� Investment Flexibility

We believe that a major advantage of default swaps for credit investors is that theycan greatly enhance investment flexibility for investors who are reliant wholly onthe cash market.

Default swaps offer a means of taking a generic credit view on a Reference Entity.This is probably most important when that view is negative, as buying protectionis typically much more straightforward than borrowing and shorting bonds. Inaddition to outright bear strategies, this can be extremely useful for holders ofilliquid securities (such as loans) who wish to hedge credit exposure. Indeed the

…notably from new-issue CBsand synthetic CDOs

Default swaps effectively lockin funding at libor

Easier to short credit…

Fiat issues a $2.2bnConvertible Bond

In the process of arranging a synthetic CDO the bank issuing the CDO has to synthesize

the credit risk of the pool by selling protection in the CDS market. This causes CDS spreads to

decline.

Prof. Dr. W. M. Schmidt 36 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.3 The cash–CDS basis, CDS strategies of market participants

The strategies of the market participants are heavily dependent to their funding costs. For

a bank with funding above Libor entering into a CDS selling protection normally yields higher

returns as compared to entering into a cash position (bond).

Whenever the CDS spread trades below the asset swap spread there is the following arbitrage

strategy. Suppose the investors funding is L+ x (L=Libor) and the bond pays in the asset swap

L+ sAS. Now in case that

sCDS

< sAS − x

the investor can realize a risk free gain of sAS − x − sCDS > 0 by entering into the asset swap

and buying protection in the CDS market. Therefore the basis between CDS and asset swap is

bounded below by the funding spread of the “best” market player.

Exercise 3.3. Think again if the gain of the above strategy really risk-free?

Prof. Dr. W. M. Schmidt 37 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.4 Credit linked notes, funded CDS

3.4 Credit linked notes, funded CDS

Credit defaults swap are not only used to buy or sell insurance on existing default risky positions,but also to create interesting new investment opportunities. This is done by so-called CreditLinked Notes (CLN).

default swap B CLN investor

bond A

-

�

-

�

6

?

payment in default

spread s

100

C + s

100 C

Prof. Dr. W. M. Schmidt 38 Credit Risk, Master of Finance, Special Course WS 2010

3 Credit default swaps 3.4 Credit linked notes, funded CDS

A credit linked note can be seen as a synthetic bond whose credit risk is linked to some

reference entity. Investing in a credit linked note the investor gets a package consisting of a

(usually “risk free”) bond issued by some issuer A, e.g., a bond issued by a AA bank or a

Pfandbrief etc., but in addition to that the investor enters into a credit default swap selling

protection on the default of some reference B. From the CDS the investor receives the premium

payments s which, together with the coupon C of the bond, yield an overall coupon of C + s.

In case of a default of the reference B of the CDS the risk free bond is sold to cover the losses

from the CDS and the remaining proceeds are the recovery of the credit linked note. In principle

the investor of a CLN is exposed to the default risk of both, the issuer of the bond A and the

reference B of the CDS.

Credit linked notes are a powerful tool to create synthetic default risky bonds with any

maturity and currency, which are otherwise not available in the market.

Entering into a CLN requires an initial investment by the investor. That is why a CLN is also

called a funded CDS. The underling risk free bond serves as a kind collateral for the credit risk

the protection buyer in the CDS runs with respect to the investor.

Prof. Dr. W. M. Schmidt 39 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve

4 Mark-to-market and the CDS curve

In the previous section we investigated the relationship between the CDS and the asset swap

spread. These relative value relationships together with supply and demand in the market yield

the market quoted fair CDS spreads.

If we are looking for a CDS today the market gives us directly the corresponding fair premium

for buying or selling protection.

Observe again the analogy to the interest rate swap market where the market quotes directly

the fair swap rates which are a result of supply and demand in the swap market and of relative

value relationships to the bond market.

The problem of evaluating a credit default swap appears only if we are looking for a re-

evaluation of an existing CDS position relative to the actual market (mark-to-market). The

primary input into the valuation are the currently quoted fair CDS premiums. Depending on the

Prof. Dr. W. M. Schmidt 40 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.1 Pricing directly from spread differences

difference between the spread in our existing CDS position and the quoted fair market spread, the

position possesses a positive or negative market value.

4.1 Pricing directly from spread differences

Imagine some time ago we have entered into a CDS with initial maturity Tn where we pay a

spread s0 (at inception of the trade this was the fair premium) for protection. Today, at time

t, the life time of the CDS has shortened to Tn − t. Suppose the market quotes today for a

Tn − t maturity CDS a fair premium of st. Then the difference st − s0 “counted” over the

remaining life time Tn − t should give us about the market value of our CDS position. In case

the actual spread st is higher than the spread s0 in the CDS the market value of the position

should be positive. Indeed, today in the market one would have to pay a much higher premium

st for protection compared to what we have to pay in our existing CDS. Our gain relative to the

market is the difference (st − s0) over the remaining life time. In case the actual market spread

st is below our premium s0, the CDS has a negative mark-to-market value.

Prof. Dr. W. M. Schmidt 41 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.1 Pricing directly from spread differences

To calculate the mark-to-market value of our CDS position we have to value the difference

(st − s0) over the remaining time Tn − t:

(st − s0)DV 01Tn−t,

where DV 01Tn−t denotes the present value of an annuity over the time Tn − t (present value

of a basis point).

However this is not completely correct. Since the premium payments in a CDS stop at the

time of default the difference (st − s0) is in our favor only up and until the time of default or

maturity. That means our annuity present value factor has to take that into account. For that

we need the probabilities of default until a certain point in time. These probabilities are implicitly

contained in the market quoted spreads and their derivation is the goal of the next section.

Prof. Dr. W. M. Schmidt 42 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

4.2 Deriving the default probabilities from market data

We use the following notation

DF(t) discount factor for time t as derived form the interest rate swap curve,

τ random time of default ,

q(t) = P(τ > t) survival probability for time t,

R recovery rate.

The present value of a default risky cash flow of one unit at time T is then

DF(T )q(T ),

i.e., the cash flow has to be discounted by the risk free discount factor and in addition it has to

be multiplied with the probability that the default does not happen until time T . Observe here

the qualitative analogy between a discount factor and a survival probability. Multiplying with the

survival probability is a kind of “additional discounting” for the default risk of the cash flow1.1Mathematically the multiplication of the discount factor and the survival probability assumes independence between riskless interest

Prof. Dr. W. M. Schmidt 43 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

The (cumulative) probability of default until time T can be easily calculated from the survival

probability as

1− q(T ).

The risk free present value factor for an annuity with period length ∆i is defined as

DV 01Tn−t =∑Ti>t

∆iDF(Ti).

For a corresponding annuity which stops at the time of default we have

DV 01riskyTn−t =

∑Ti>t

∆iDF(Ti)q(Ti).

To calculate the mark-to-market value of our existing CDS position we have to utilize the risky

present value of a basis point

(st − s0)∑Ti>t

∆iDF(Ti)q(Ti).

rates and defaults.

Prof. Dr. W. M. Schmidt 44 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

The question is now: where do we get the appropriate default or, equivalently, survival

probabilities from?

These probabilities are implicitly contained in the market prices such as prices of default risky

bonds or fair CDS premiums.

However, market prices or spreads reflect simultaneously the probability of default as well as

the potential recovery value in case of default. To extract the default probabilities we are forced

to make an assumption on the recovery rate R, for example, we could assume R = 15%. We

will have to discuss the implications of those assumptions later.

Prof. Dr. W. M. Schmidt 45 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

To start with, consider the market price of a default risk bond. How do the survival

probabilities and the recovery rate R enter into the price of a bond with coupon C and face

value of 1? The dirty price Pd of the bond is given by the equation

Pd = C∑i

∆iDF(Ti)q(Ti) + DF(Tn)q(Tn) + R

∫ Tn

T0

DF(u)[q(u)− q(u+ du)]. (1)

The coupon payments and the redemption of the face value have to be discounted by the riskless

discount factors and the survival probabilities. The last expression in the equation above needs

some more explanation. It is the present value of the recovery ”payment”. At the time of default

the investor get paid the recovery rate R. Since we do not know if and when there will be a

default we have to consider all points in time u from T0 to Tn. If the default occurs at time u

we have to discount the recovery with the discount factor DF(u). The probability of a default

around time u, more precisely in the small interval [u, u + du], is just (q(u) − q(u + du)).

All those contributions have to be added up over all points u in time between T0 and Tn.

Prof. Dr. W. M. Schmidt 46 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

Given the market price Pd of the bond, the curve of riskless discount factors DF(t) and

making an assumption on the recovery rate R, the market implied default probabilities have to

satisfy the pricing equation (1). Now we can try to “solve” this equation for the unknown default

probabilities.

Exercise 4.1. Given the market price of a default risky bond. To extract the implied default

probabilities we have to make a guess on the unknown recovery rate R, lets say R = 15%. How

will the implied default probabilities change if we make a different assumption on the recovery, for

example R = 30%. Will the corresponding default probabilities be higher or lower?

Since our main goal is the valuation of credit default swaps and since the CDS market quotes

the fair premiums we will be more interested in getting the default probabilities extracted from

the CDS market and not from prices of bonds (recall that there is often a significant difference

between the cash and the CDS market!).

Prof. Dr. W. M. Schmidt 47 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

The CDS market quotes fair premiums (spreads). If we denote by s(n) the fair premium for

maturity Tn, the following equality has to be fulfilled

0 = − value of premium flows s(n)

+ value of the payment (1− R) at default

= −s(n)

n∑i=1

∆iDF(Ti)q(Ti)− s(n)

n∑i=1

∫ Ti

Ti−1

∆i

u− Ti−1

Ti − Ti−1

DF(u)[q(u)− q(u+ du)]

+(1− R)

∫ Tn

T0

DF(u)[q(u)− q(u+ du)]

≈ −s(n)

n∑i=1

∆iDF(Ti)q(Ti)− s(n)

n∑i=1

∆i

2DF

(Ti−1 + Ti

2

)[q(Ti−1)− q(Ti)]

+(1− R)

n∑i=1

DF

(Ti−1 + Ti

2

)[q(Ti−1)− q(Ti)]. (2)

Prof. Dr. W. M. Schmidt 48 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

Again we have obtained an equation which we can try to resolve for the implied default

probabilities.

If there is a quoted fair spread s(1), . . . , s(n) for every maturity T1, . . . , Tn the

corresponding probabilities q(T1), . . . , q(Tn) can be extracted by a bootstrapping algorithm.

This is quite similar to the calculation of the riskless discount factors from the interest rate swap

curve.

Lets illustrate this by an example. For the first grid point T1 equation (2) reduces to

0 = −s(1)∆1DF(T1)q(T1)−s(1)∆1

2DF(T1/2)(1−q(T1))+(1−R)DF(T1/2)(1−q(T1)).

Observe that (1− q(T1)) is just the probability of a default during the interval (0, T1).

Computer Exercise 4.2. Consider a credit default swap with 1Y time to maturity, T1 = 1,

which starts today at T0 = 0. Let the fair premium quoted in the market be s(1) = 1%. We

assume for simplicity that the premium is paid annually with a 30/360 day count convention,

i.e., ∆1 = 1. From the interest rate swap curve the following discount factors are given

Prof. Dr. W. M. Schmidt 49 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

DF(0.5) = 0, 9853,DF(1) = 0, 9714. For the recovery rate we assume R = 15%.

Calculate the implied survival probability q(1) for 1 year! How does the result change if we

assume a recovery of R = 30%?

Once the survival probabilities q(T1), . . . , q(Tn) for the grid points T1, . . . , Tn have been

extracted from the market spreads, we have to define a method to interpolate the survival

probability. For a time point t ∈ (Ti−1, Ti) the survival probability q(t) is interpolated according

to the formula

q(t) = q(Ti−1) exp(−λi(t− Ti−1)), t ∈ (Ti−1, Ti),

with

λi = ln

(q(Ti−1)

q(Ti)

)/(Ti − Ti−1).

The quantity λi is also called the default rate or default intensity (hazard rate) for the interval

[Ti−1, Ti]. The probability of a default during a small interval [t, t + ∆] given that there has

been no default so far is approximately λ∆; we will discuss this in more detail in Section 7.1.

Summarizing, survival probabilities are interpolated assuming a constant default rate in the

intervals [Ti−1, Ti].

Prof. Dr. W. M. Schmidt 50 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.2 Deriving the default probabilities from market data

Remarks1. How should one interpret the default or survival probabilities which have been extracted from

the market? These probabilities are market implied probabilities, i.e., they reflect the opinion

of the market on the risk of default. They are not necessarily related to the “true” default

probabilities which are anyway not accessible at all! Out of historical data one can estimate

empirical default probabilities which might be a reasonable indication for the “true” probabilities.

However, the valuation of credit derivatives is based on the general principles of dynamic hedging

and arbitrage free pricing. Therefore for the purpose of valuation one has to utilize probabilities

as extracted from prices of traded instruments.

2. In the framework of risk-neutral valuation the price of a derivative is its “discounted”

expectation under the risk neutral distribution. In that context the market implied probabilities

can be seen as risk-neutral default probabilities.

3. The extracted survival probabilities where always “relative” to the interest rate swap curve

which has been interpreted as risk free. Recall that the price of a default risk payment of one

unit at time T was written as DF(T )q(T ). The default risk of the interest rate swap curve (AA

curve) relative to a truly default free discount curve (e.g. from government bonds) is already

“contained” in the discount factor DF(T ).

Prof. Dr. W. M. Schmidt 51 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.3 Mark-to-market valuation of credit default swaps

4.3 Mark-to-market valuation of credit default swaps

In the previous section we have learned how to build the curve of market implied survival

probabilities. Now the valuation of any credit default swap is straightforward. We utilize the

curve of survival probabilities q(t), the curve of risk free discount factors DF(t) from the interest

rate swap market and (of course!) the same assumption on the recovery rate R as used in the

process of extracting the probabilities from the market. The value of an arbitrary credit default

swap is then calculated from the formula2

−sn∑i=1

∆iDF(Ti)q(Ti)− sn∑i=1

∆i

2DF

(Ti−1 + Ti

2

)[q(Ti−1)− q(Ti)]

+(1− R)

n∑i=1

DF

(Ti−1 + Ti

2

)[q(Ti−1)− q(Ti)]. (3)

2As in (2) we have approximated the respective integrals bei their mid-point sums. So the result is in fact an (quite good) approximationof the true value.

Prof. Dr. W. M. Schmidt 52 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.4 How critical are the assumptions on the recovery rate?

This formula assumes the position of a protection buyer. For the protection seller we have to

switch just signs.

Computer Exercise 4.3. Evaluate a 100 Mio 5Y CDS with a spread s = 80 basis points paid

semi annually act/360. Use the spread sheet CDSPricer.xls with the interest curve, default

curve and recovery rate as specified there.

4.4 How critical are the assumptions on the recovery rate?

Extracting the default probabilities from market data we had to make a subjective assumption on

the recovery rate R. Rating agencies have collected historical data on realized recoveries that

can be used as an indication on the level of recovery. In practice one assumes recoveries in the

range between 15% to 50%. In any case one should try to make a realistic assumption.

However, it not yet clear how sensitive our valuations are with respect to the assumed

recovery rate. Fortunately and at a first glance somewhat surprising it turns out that the results

Prof. Dr. W. M. Schmidt 53 Credit Risk, Master of Finance, Special Course WS 2010

4 Mark-to-market and the CDS curve 4.4 How critical are the assumptions on the recovery rate?

show very little sensitivity with respect to the assumed recovery. The reason is that the recovery

enters at two places where their impact is offsetting. First in the process of extracting the

probabilities from market data, and, secondly, in the mark-to-market valuation of a CDS. It is

clearly important to use one and the same recovery in both places. As long as the premium of

the underlying CDS is not extremely far away from the fair market premium the impact of the

recovery assumption is negligible.

Computer Exercise 4.4. Evaluate an existing CDS with remaining life time of 4Y. The spread

in the CDS is s = 2%. How does the mark-to-market value change of we change the assumed

recovery from R = 15% to R = 50% in both places, the default curve generation and the

mark-to-market valuation?

Remark. In contrast to standard credit default swaps there exist so-called Digital DefaultSwaps where the insurance payment in case of a default is not linked to the recovery of the

reference asset but is a predefined amount. The valuation of those products can be carried

out following exactly the same lines as for a standard CDS. However the valuation is now

quite sensitive to the recovery assumed for extracting the probabilities. In this case a realistic

assumption on the recovery is particularly important.

Prof. Dr. W. M. Schmidt 54 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis

5 Lessons from the credit crisis

5.1 Issues highlighted by the crisis

Let us first summarize selected pros and cons on credit derivatives, in particular, CDS:

• Pro:

– Hedging of credit risk (buy protection); easy way to short credit exposure; means to

transfer the credit risk without transferring the underlying loan, bond etc.; enables financial

institutions to continue to make loans;

– Take on credit risk (sell protection), no funding needed; access to exposure even if no

client/business relationship;

– Efficient allocation of risk and capital; credit risks borne by those who are best able to bear

them;

– Smooth out fluctuations in regulatory capital accounts under mark-to-market accounting -

CDS hedges mtm of loans, bonds;

Prof. Dr. W. M. Schmidt 55 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.1 Issues highlighted by the crisis

– Liquid credit trading reveals valuable information about credit risk;

• Con:

– Size of CDS market created systemic risk for the economy;

– CDS create excessive risk;

– CDS are used to manipulate the market;

– Credit derivatives enabled the boom that finally led to the crisis;

– Warren Buffett (2002): CDS are “weapons of financial mass destruction”

– Buying protection without having exposure is like buying fire insurance on the house of the

neighbor→ sets wrong incentives;

We discuss the above criticisms and their role played in the crisis. See also [Stulz, 2009].

Size of CDS market threatens the economy:

Face value of outstanding CDS contracts exceed the volume of outstanding debt, but overall

CDS volume is deceptive - it consists of long and short credit risk positions! For example, A sells

protection on 100 Mio and hedges later by buying protection on 50 Mio yields a outstanding CDS

volume of 150 Mio but the net exposure is only 50 Mio.

Prof. Dr. W. M. Schmidt 56 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.1 Issues highlighted by the crisis

However, the true outstanding net exposure in the market was not transparent. Nowadays major

dealers register their trades with the Depository Trust & Clearing Corporation.

Risk Category / Instrument Jun 2007 Dec 2007 Jun 2008 Dec 2008 Jun 2009 Jun 2007 Dec 2007 Jun 2008 Dec 2008 Jun 2009

Total contracts 516,407 595,738 683,814 547,371 604,622 11,140 15,834 20,375 32,244 25,372

Foreign exchange contracts 48,645 56,238 62,983 44,200 48,775 1,345 1,807 2,262 3,591 2,470 Forwards and forex swaps 24,530 29,144 31,966 21,266 23,107 492 675 802 1,615 870 Currency swaps 12,312 14,347 16,307 13,322 15,072 619 817 1,071 1,421 1,211 Options 11,804 12,748 14,710 9,612 10,596 235 315 388 555 389

Interest rate contracts 347,312 393,138 458,304 385,896 437,198 6,063 7,177 9,263 18,011 15,478 Forward rate agreements 22,809 26,599 39,370 35,002 46,798 43 41 88 140 130 Interest rate swaps 272,216 309,588 356,772 309,760 341,886 5,321 6,183 8,056 16,436 13,934 Options 52,288 56,951 62,162 41,134 48,513 700 953 1,120 1,435 1,414

Equity-linked contracts 8,590 8,469 10,177 6,159 6,619 1,116 1,142 1,146 1,051 879 Forwards and swaps 2,470 2,233 2,657 1,553 1,709 240 239 283 323 225 Options 6,119 6,236 7,521 4,607 4,910 876 903 863 728 654

Commodity contracts 7,567 8,455 13,229 3,820 3,729 636 1,898 2,209 829 689 Gold 426 595 649 332 425 47 70 68 55 43 Other commodities 7,141 7,861 12,580 3,489 3,304 589 1,829 2,141 774 646

Forwards and swaps 3,447 5,085 7,561 1,995 1,772 Options 3,694 2,776 5,019 1,493 1,533

Credit default swaps 42,581 58,244 57,403 41,883 36,046 721 2,020 3,192 5,116 2,987 Single-name instruments 24,239 32,486 33,412 25,740 24,112 406 1,158 1,901 3,263 1,953 Multi-name instruments 18,341 25,757 23,991 16,143 11,934 315 862 1,291 1,854 1,034

Unallocated 61,713 71,194 81,719 65,413 72,255 1,259 1,790 2,303 3,645 2,868

Memorandum Item:

Gross Credit Exposure 2,672 3,256 3,859 4,555 3,744

Instrument / counterparty Jun 2007 Dec 2007 Jun 2008 Dec 2008 Jun 2009 Jun 2007 Dec 2007 Jun 2008 Dec 2008 Jun 2009

Total contracts 48,645 56,238 62,983 44,200 48,775 1,345 1,807 2,262 3,591 2,470

reporting dealers 19,173 21,334 24,845 18,810 18,891 455 594 782 1,459 892

other financial institutions 19,144 24,357 26,775 17,223 21,441 557 806 995 1,424 1,066

non-financial customers 10,329 10,548 11,362 8,166 8,442 333 407 484 708 512

Outright forwards and foreign

exchange swaps 24,530 29,144 31,966 21,266 23,107 492 675 802 1,615 870

reporting dealers 8,800 9,899 10,897 8,042 7,703 190 228 281 635 301

other financial institutions 10,010 13,102 14,444 8,646 10,653 185 292 348 636 374

non-financial customers 5,720 6,143 6,624 4,577 4,751 117 154 172 343 195

Currency swaps 12,312 14,347 16,307 13,322 15,072 619 817 1,071 1,421 1,211

reporting dealers 4,909 5,487 6,599 5,807 6,330 155 215 315 544 402

other financial institutions 5,262 6,625 7,367 5,610 6,717 291 406 520 627 568

non-financial customers 2,141 2,234 2,341 1,906 2,025 173 196 237 250 241

Options 11,804 12,748 14,710 9,612 10,596 235 315 388 555 389

reporting dealers 5,464 5,948 7,349 4,961 4,858 111 151 186 280 190

other financial institutions 3,872 4,629 4,964 2,968 4,071 81 108 127 161 125

non-financial customers 2,468 2,171 2,397 1,683 1,666 43 57 75 115 75

Notional amounts outstanding Gross market values

Table 20A: Amounts outstanding of OTC foreign exchange derivativesBy instrument and counterpartyIn billions of US dollars

Table 19: Amounts outstanding of over-the-counter (OTC) derivativesBy risk category and instrumentIn billions of US dollars

Notional amounts outstanding Gross market values

BIS Quarterly Review, December 2009 A 103

Source: BIS 2009

Prof. Dr. W. M. Schmidt 57 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.1 Issues highlighted by the crisis

CDS create excessive risk:

For each protection seller there is be a protection buyer. Defaults of the CDS reference entity

hurt the protection seller and benefit the buyer - on net it is a redistribution of wealth.

However, even if dealers hedge their positions by offsetting trades, there might be a

considerable counter party risk. Defaults of a dealer can cause unexpected havoc. Losses from

dealer default could be large, even with collateral agreements. Also large seller position carry

wrong way risk: a decline of the CDS reference entity might cause the credit worthiness of the

seller to decline as well.

Interconnections of large market players fed concerns that a default of a major player has

devastating effects in the whole sector, see the AIG case.

CDS are used to manipulate the market:

CDS are a measure of market sentiment of the credit worthiness and note a cause of corporate

ills.

[Mason, 2009]: “Blaming CDSs for corporate debt problems is like blaming the thermometer for

the temperature.”

Prof. Dr. W. M. Schmidt 58 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.2 Private sectors initiatives

Credit derivatives enabled the boom that finally led to the crisis:

Due to the separation of risk bearing from funding, lenders have less incentive to check the

quality of the borrower and to monitor the position. Example: hedging subprime mortgages with

CDS on subprime mortgage securitizations.

Huge investors demand for selling protection via the Subprime mortgage CDS ABX indices:

investors take more exposure than there were such mortgages.

Problems with the physical settlement of CDS:

If the volume of outstanding protection exceeds the volume of debt qualified for physical delivery

in case of default, physical settlement becomes problematic. This happened also for positions in

the subprime mortgage ABX indices.

5.2 Private sectors initiatives

In the meantime, most of the above issues have been addressed by the market.

In 2009 the International Swaps and Derivatives Association (ISDA), issued two amendments

Prof. Dr. W. M. Schmidt 59 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.2 Private sectors initiatives

to their CDS Master Agreement, the so called “big bang” and “small bang” protocols. The

agreements of these protocols came into force in June resp. July 2009.

The major changes are:

• Standardization of CDS contracts:

Fix spread payments of 25, 100, 500 or 100 bps (Europe), period dates 20th of

Mar/Jun/Sep/Dec., full first period

prices are settled by an upfront payment.

This allows for a perfect netting of cash flows for offsetting trades.

• Rolling lock back effective dates:

Protection effectively starts 60 days (credit events) and 90 days (succession events) before

trade date.

This leads to a better netting of yet unobserved credit events for offsetting trades.

• Quoting standards and standardized pricing:

In the past it was common to quote so-called par spreads. Since the spread payments are now

Prof. Dr. W. M. Schmidt 60 Credit Risk, Master of Finance, Special Course WS 2010

5 Lessons from the credit crisis 5.2 Private sectors initiatives

standardized it is more appropriate to show so-called quoted spreads. These are used in a flat

curve to determine the mark-to-market of standardized CDSs, the recovery is assumed to be

40%.

A standardized CDS pricing tool including source code was made available free of charge:

http://www.cdsmodel.com.

• Occurrence of credit event will be determined by the Determination Committee.

There are 5 regional committees consisting of 15 ISDA members.

• CDS settlement in case of credit event:

Both, for physical and cash settlement, there is now a mandatory auction. This guarantees a

uniform recovery rate for all settlements.

Auction protocols are publicly available at www.isda.org/protocol/cdsprotocols.html.

For example, the 2008 Lehman CDS protocol explains how the final settlement of a recovery

of R = 8.625% was determined.

• Clearing through central counterparties.

European CCPs are ICE Clear and Eurex Clearing. Academic research, [Duffie and Zhu, 2009],

suggest that too many CCPs do not reduce counter party risks.

Prof. Dr. W. M. Schmidt 61 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS

6 Strategies with CDS

6.1 Funding cost strategies

As discussed in Section 3.3, the break-even premium for protection is about the asset swap spread

minus the funding spread. For institutions with different funding spreads there are interesting

CDS investment strategies. These strategies are an important sources of market activities.

Consider the following example:

bps

funding spread AAA institution -20

funding spread A institution 30

asset swap spread BBB asset 45

CDS Spread same BBB asset 35

Investing in the BBB asset the AAA institution would generate a return of 65 bps whereas the

return for the A institution would be only 15 bps. For A ist would be advantageous to invest

Prof. Dr. W. M. Schmidt 62 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS 6.2 Curve trades

unfunded via CDS since this would yield a higher spread of 35 bps. On the other hand AAA

might look for buying protection via CDS (for example, from A), which would still return a spread

of 65-35 = 30 bps, with AAA then being mainly exposed to the risk of a joint default of BBB

and A.

6.2 Curve trades

Even though the 5 years maturity is most liquid in the CDS market, maturities of 3Y, 7Y and

10Y are gaining more and more liquidity, at least for selected names. This calls for CDS curve

strategies. In case of an increasing CDS curve, a Flattener would, e.g., involve buying 5Y

protection and selling 10Y protection. Vice versa a corresponding Steepener would bet on the

curve further steepening. Combining CDS positions of different maturities the notional amounts

can be chosen depending on the risk perceptions

• identical notional amounts, i.e., no default exposure during the joint life time,

Prof. Dr. W. M. Schmidt 63 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS 6.3 Credit vs equity

• DV01-hedged, i.e., no sensitivity of the overall position with respect to parallel shifts of the

CDS curve,

• carry neutral, i.e., the spread payments of the individual CDS are netting each other.

Most efficiently, curve trades can be set up using CDS indices (to be discussed later in

Section 8), since those indices allow for sufficient liquidity in the standard maturities.

6.3 Credit vs equity

Dependencies between credit and equity offer an interesting and challenging play ground. Clearly,

a worsening credit quality is most likely accompanied by a declining stock price and vice versa.

In case of a default (stock price = 0), a put option on equity with strike K would yield a

payoff of K. Therefore, to a certain extend a put options contains something very similar to

a credit default swap. The further out of the money the put, the higher is the percentage of

contained default protection.

Prof. Dr. W. M. Schmidt 64 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS 6.4 Sub vs senior

Obviously there is a significant relationship between equity price and volatility on one hand

and the credit spread on the other hand. Modeling this relationship is far from being trivial and

could be done, e.g., based on a structural model of default, see Section 7.2.1. The web page

www.creditgrades.com offers a relative value tool between credit and equity.

Equity default swaps are very similar to credit default swaps, however the protection event is

not default but the event that the stock price falls below a certain threshold, e.g., 30% of the

current spot price. A protection premium is paid on a regular basis (e.g., quarterly, act/360) until

the event occurs or the deal matures. Equity default swaps are the ideal tools to realize relative

value strategies between credit and equity.

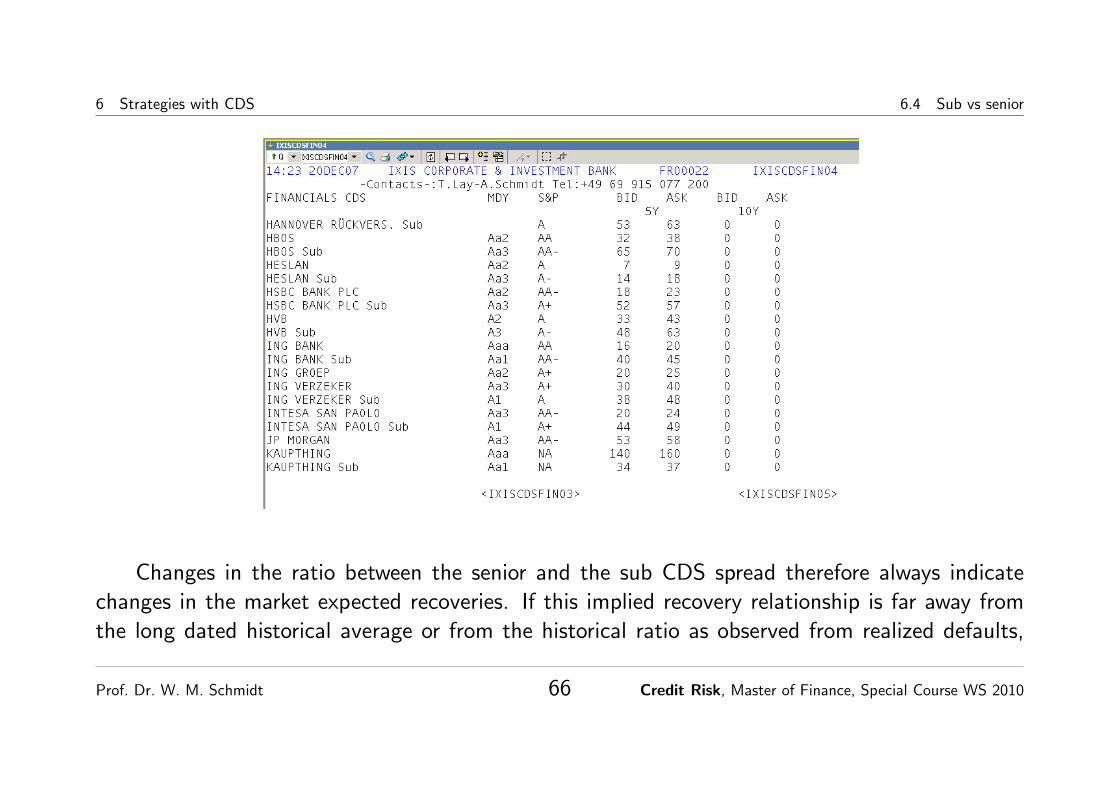

6.4 Sub vs senior

For European banks and insurance companies the market quotes at the same time CDS referring

to senior and subordinated debt. By definition both debt classes will default at the same time.

Different CDS premiums for senior and subordinated reflect different expectations on the recovery

rate.

Prof. Dr. W. M. Schmidt 65 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS 6.4 Sub vs senior

Changes in the ratio between the senior and the sub CDS spread therefore always indicate

changes in the market expected recoveries. If this implied recovery relationship is far away from

the long dated historical average or from the historical ratio as observed from realized defaults,

Prof. Dr. W. M. Schmidt 66 Credit Risk, Master of Finance, Special Course WS 2010

6 Strategies with CDS 6.4 Sub vs senior

this might give the opportunity to implement relative value strategies.

Based on the formula (7) we get the following theoretical relationship between the spreads

and the expected recovery ratessCDSsen

sCDSsub=

1− Rsen

1− Rsub.

Prof. Dr. W. M. Schmidt 67 Credit Risk, Master of Finance, Special Course WS 2010

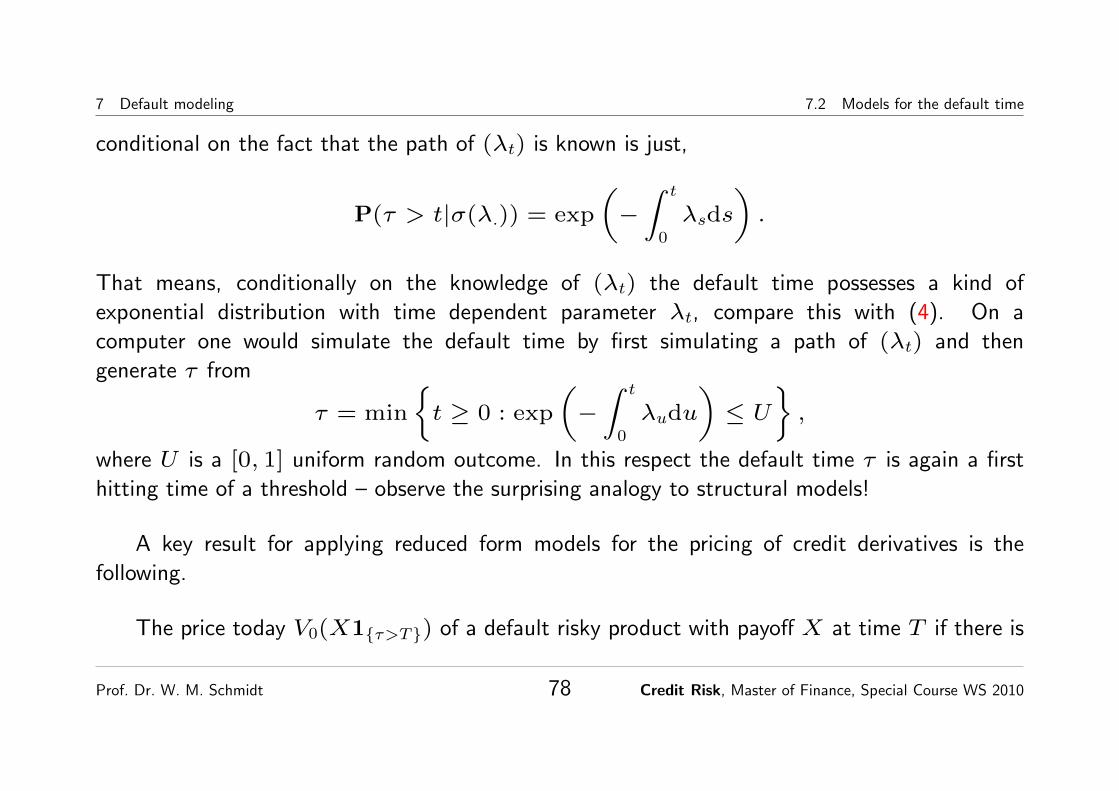

7 Default modeling

7 Default modeling

To evaluate a default risky position, e.g., a CDS or a bond, so far we have only used the CDS

curve of survival probabilities. There was no need for a complicated valuation model. However,

for more complex products such as options or correlation products we need a stochastic model

describing the default and the evolution of the spreads over time. Clearly such a model has to be

in line with the observed market information, primarily the CDS curve, i.e., the model has to be

calibrated to match the given CDS curve.

Observe again the analogy to interest rate models: to evaluate bonds, swaps or FRAs all that

is needed is the discount curve. More complex products require a term structure model which has

to be calibrated to the interest rate curve.

Prof. Dr. W. M. Schmidt 68 Credit Risk, Master of Finance, Special Course WS 2010

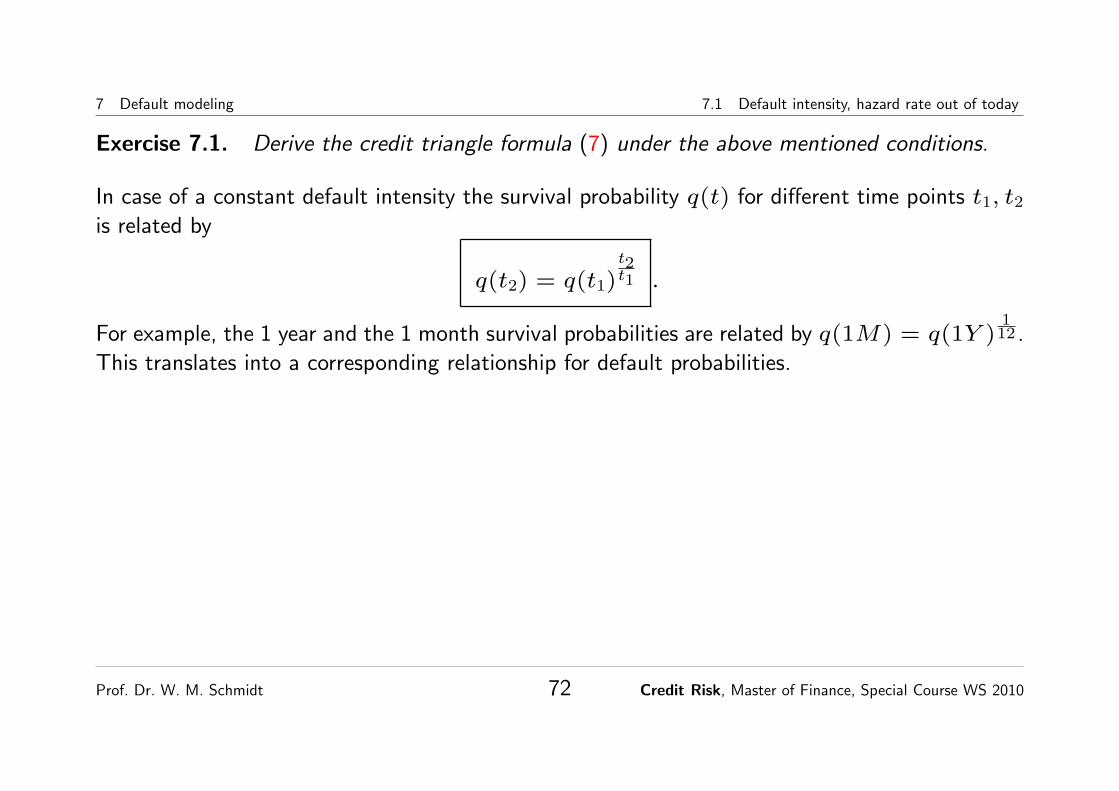

7 Default modeling 7.1 Default intensity, hazard rate out of today

7.1 Default intensity, hazard rate out of today

The valuation of any credit derivative product is based on the curve of risk-neutral survival

probabilities derived from actual market data (CDS spreads, prices of bonds).

Let τ denote again the random time of default. Then

F (t) = P(τ < t), t ≥ 0

is the distribution function of τ , and

q(t) = P(τ ≥ t) = 1− F (t), t ≥ 0,

is the curve of survival probabilities (survival function).

Prof. Dr. W. M. Schmidt 69 Credit Risk, Master of Finance, Special Course WS 2010

7 Default modeling 7.1 Default intensity, hazard rate out of today

The conditional probability of default in the interval [t, t+ ∆], given that there has been no

default until time t is calculated as

P(τ ∈ [t, t+ ∆]|τ > t) =F (t+ ∆)− F (t)

1− F (t)

≈F ′(t)

1− F (t)∆.

Here λ0(t) := F ′(t)1−F (t) is called the hazard rate or default intensity. Intuitively this is just the

default rate per year as of today. Using the default intensity we get

λ0(t) = −q′(t)

q(t)

q(t) = P(τ > t) = exp

(−∫ t

0

λ0(s)ds

). (4)

Prof. Dr. W. M. Schmidt 70 Credit Risk, Master of Finance, Special Course WS 2010

7 Default modeling 7.1 Default intensity, hazard rate out of today