Credit Unions and Caisses Populaires Act, 1994 · Message from Parliamentary Assistant to the...

24

2014 Credit Unions and Caisses Populaires Act, 1994 Five-Year Review Consultation Paper

Transcript of Credit Unions and Caisses Populaires Act, 1994 · Message from Parliamentary Assistant to the...

2014

Credit Unions and Caisses Populaires Act, 1994 Five-Year Review Consultation Paper

Message from Minister of Finance

It has been five years since the last set of significant amendments to the Credit Unions and Caisses Populaires Act, 1994 came into effect. It is now time to review the legislation and regulations to ensure the credit union sector can continue to contribute to the province’s economy and meet the changing needs of its members. The Ontario government is committed to continuously updating and adapting Ontario’s financial services regulation. This review provides an opportunity to modernize the regulatory framework, enhance consumer protection where needed, and enable credit unions to pursue opportunities for sustainable success. I have asked my Parliamentary Assistant Laura Albanese to lead the five-year review of the Credit Unions and Caisses Populaires Act, 1994. She will travel across the province to listen to the views of Ontarians on how the legislation, regulations and regulatory structures relating to the credit union sector may be improved. I have asked that she submit final recommendations to me by the fall of 2015. Your input to the consultation process is essential so that we can identify changes that are needed to modernize our credit union regulatory framework and support the government’s plan to invest in people, build modern infrastructure and support a dynamic and innovative business climate. The Honourable Charles Sousa Minister of Finance

Message from Parliamentary Assistant to the Minister of Finance

On September 30, 2014, the Minister of Finance appointed me to lead the five-year review of the Credit Unions and Caisses Populaires Act, 1994. I am pleased to take on this task with the overall objective of making recommendations on ways to improve the legislative framework so that credit unions and caisses populaires can continue to contribute to Ontario’s economy and serve their members well. Ontario’s credit unions and caisses populaires play an important role in the financial services sector and the economy overall. Over the past five years, the sector has experienced significant change. It is crucial to examine the legislative framework to ensure it remains current and in line with the needs of the sector and the members that it serves. The legislative review will be substantial in scope and address key issues impacting Ontario’s credit unions and caisses populaires which are outlined in the attached consultation paper. I am interested in receiving your input on these issues to help me form the recommendations that I will make to the Minister. Thank you for contributing your views to this important review. Laura Albanese The Parliamentary Assistant to the Minister of Finance

Table of Contents

Introduction ..................................................................................................................................... 1

Sector Overview .............................................................................................................................. 3

Areas to be Examined ...................................................................................................................... 4

Vision and Strategic Priorities ......................................................................................................... 5

Capital Adequacy ............................................................................................................................. 5

Lending and Investment Restrictions .............................................................................................. 7

Rules Based on Size ......................................................................................................................... 9

Governance ..................................................................................................................................... 9

Consumer Protection .................................................................................................................... 10

Roles of Regulators ........................................................................................................................ 11

Deposit Insurance Coverage Limit ................................................................................................. 12

Operations Across Provincial Borders ........................................................................................... 13

Technical Amendments ................................................................................................................. 14

Summary of Consultation Questions ............................................................................................. 14

1

Credit Unions and Caisses Populaires Act, 1994 – Five-Year Review

INTRODUCTION Thank you for your interest in contributing to the discussion on the five-year review of the Credit Unions and Caisses Populaires Act, 1994 and regulations. The requirement to conduct a review of the Act and regulations every five years is found in section 334 of the Act. This is the first five-year review since that provision was enacted. We want your views This consultation paper sets out a number of key areas on which your views are being sought. Additionally, if there are any other issues you wish to raise or comment on, you are encouraged to submit them. How to share your views with us

Attend one of the regional consultation sessions that will be held across the province to express your views in person. Dates and locations, as well as details regarding the registration process can be found on the Ministry of Finance website at: http://www.fin.gov.on.ca/en/consultations/

Mail, fax, or email written comments to:

Laura Albanese Parliamentary Assistant to the Minister of Finance c/o Budget Secretariat Frost Building North, 3rd Floor 95 Grosvenor Street Toronto ON M7A 1Z1 Fax: 416-325-0969 Email: [email protected]

NEW DEADLINE! The submission deadline has been extended. Submissions will be accepted up to February 5, 2015. (*Deadline extended January 5, 2015)

2

Public consultation Please note that these are public consultations. All submissions and comments received will be made publicly available to improve the transparency of the consultation and policy-making process. All comments may be posted to the Ministry of Finance website at www.fin.gov.on.ca. Any comments or other materials received, or summaries of them, may be disclosed to other interested parties during and after the consultation. Personal information will not be disclosed without prior consent. If for any reason you feel your comments should not be posted publicly or shared with other parties, please indicate this in your covering letter. Please note that all submissions received are subject to the Freedom of Information and Protection of Privacy Act. If you have any questions about this consultation or how any element of your submission may be used or disclosed, please contact [email protected].

3

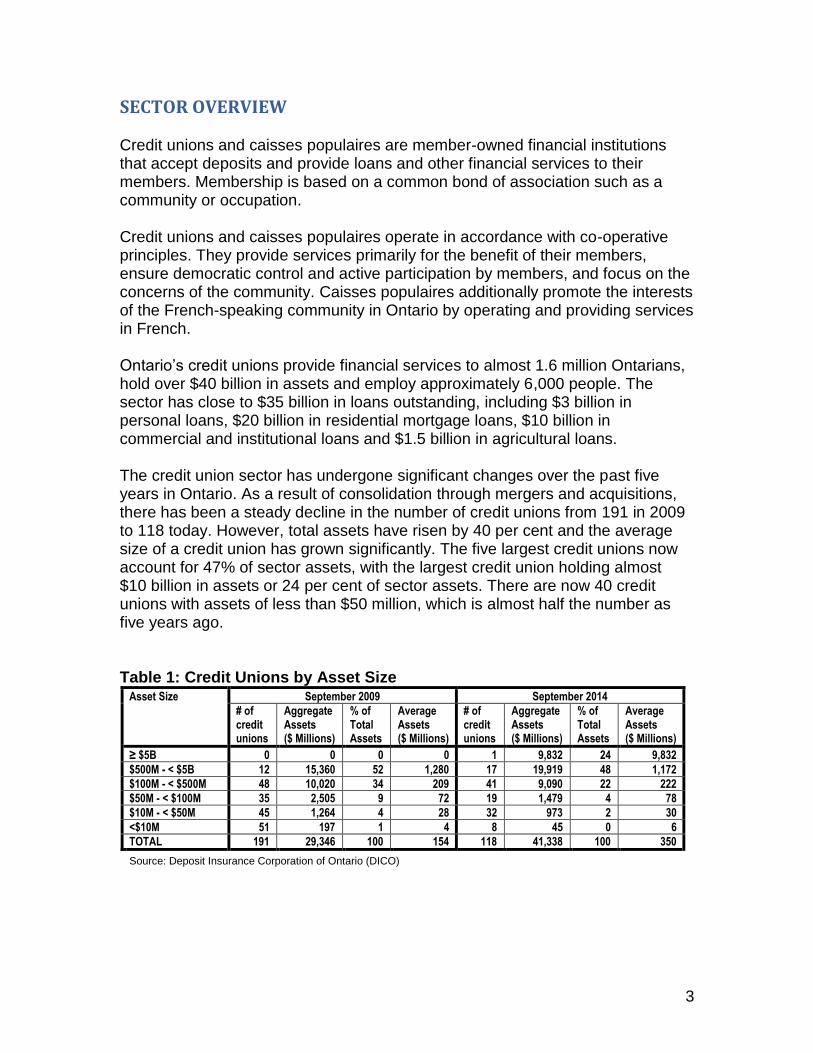

SECTOR OVERVIEW Credit unions and caisses populaires are member-owned financial institutions that accept deposits and provide loans and other financial services to their members. Membership is based on a common bond of association such as a community or occupation. Credit unions and caisses populaires operate in accordance with co-operative principles. They provide services primarily for the benefit of their members, ensure democratic control and active participation by members, and focus on the concerns of the community. Caisses populaires additionally promote the interests of the French-speaking community in Ontario by operating and providing services in French. Ontario’s credit unions provide financial services to almost 1.6 million Ontarians, hold over $40 billion in assets and employ approximately 6,000 people. The sector has close to $35 billion in loans outstanding, including $3 billion in personal loans, $20 billion in residential mortgage loans, $10 billion in commercial and institutional loans and $1.5 billion in agricultural loans. The credit union sector has undergone significant changes over the past five years in Ontario. As a result of consolidation through mergers and acquisitions, there has been a steady decline in the number of credit unions from 191 in 2009 to 118 today. However, total assets have risen by 40 per cent and the average size of a credit union has grown significantly. The five largest credit unions now account for 47% of sector assets, with the largest credit union holding almost $10 billion in assets or 24 per cent of sector assets. There are now 40 credit unions with assets of less than $50 million, which is almost half the number as five years ago. Table 1: Credit Unions by Asset Size

Asset Size September 2009 September 2014

# of credit unions

Aggregate Assets ($ Millions)

% of Total Assets

Average Assets ($ Millions)

# of credit unions

Aggregate Assets ($ Millions)

% of Total Assets

Average Assets ($ Millions)

≥ $5B 0 0 0 0 1 9,832 24 9,832

$500M - < $5B 12 15,360 52 1,280 17 19,919 48 1,172

$100M - < $500M 48 10,020 34 209 41 9,090 22 222

$50M - < $100M 35 2,505 9 72 19 1,479 4 78

$10M - < $50M 45 1,264 4 28 32 973 2 30

<$10M 51 197 1 4 8 45 0 6

TOTAL 191 29,346 100 154 118 41,338 100 350

Source: Deposit Insurance Corporation of Ontario (DICO)

4

AREAS TO BE EXAMINED During the past five years, the financial services sector has been rapidly evolving to face challenges and seize opportunities arising from the dynamic economic and competitive environment. These challenges include: continued low interest rates, changing technology needs of consumers, unsettled international financial markets, and increased competition. Credit unions in particular have been faced with aging member demographics and structural challenges. In 2009, significant amendments were made to the Credit Unions and Caisses Populaires Act, 1994 (CUCPA). The changes strengthened the governance of credit unions, enhanced their ability to manage risk, streamlined regulatory requirements while promoting effective regulatory oversight, created flexibility to pursue growth and innovation and enhanced consumer protection standards. It is now time to take stock of these changes and evaluate the current act and regulations. The consultation paper sets out the following key areas for consideration: vision and strategic priorities, capital adequacy, lending and investment restrictions, rules based on size, governance, consumer protection, roles of regulators, deposit insurance coverage limit, operations across provincial borders and technical amendments.

5

VISION AND STRATEGIC PRIORITIES Credit unions are facing a challenging economic and competitive environment. Downward pressures on interest rate margins, increased costs of investing in technology infrastructure, an aging membership base and aggressive competition in the financial services marketplace are driving change in Ontario’s credit union sector. Many credit unions are questioning whether the status quo will be sufficient and what it will take to succeed and ensure system sustainability in the future. A spectrum of strategic options is being identified by credit unions as they explore a vision for the future, individually and as a credit union system. These options include continuing to pursue consolidation among small and medium sized credit unions to ensure system sustainability. As well, consideration is being given to ways to improve structural design and potential collaboration models to enhance operational efficiency and asset growth.

Questions for Consideration:

What is your vision for the credit union sector in Ontario? What are the top three strategic priorities that are essential to foster such a vision? What is the government’s role in enabling the credit union sector to achieve this vision?

CAPITAL ADEQUACY Capital adequacy is one of the key measures of financial soundness of a deposit-taking institution. Capital is important not only as a source of funds to support growth, but also as a cushion to protect depositors and creditors against potential future losses. Ontario credit unions are required to meet minimum capital adequacy standards that are set out in the CUCPA. It is important that these standards remain up-to-date and, where appropriate, harmonized with other Canadian jurisdictions and in line with international standards. In Ontario, all credit unions must meet a leverage test which measures the amount of regulatory capital they hold as a percentage of total assets. Smaller, less complex credit unions (Class 1 credit unions) must maintain regulatory capital equal to at least five per cent of total assets. Credit unions with more than $50 million in assets or that make commercial loans (Class 2 credit unions) are subject to a four per cent leverage test; however they must also maintain regulatory capital equal to at least eight per cent of risk weighted assets. This latter test is based on international standards set by the Basel Committee on Banking Supervision, and is commonly referred to as the Basel II capital adequacy test.

6

Basel III In response to the global financial crisis, the Basel Committee revised the capital standards and developed a new framework referred to as Basel III. The new standards increase emphasis on the quality and permanence of capital held by financial institutions, including a focus on common equity (considered to be high-quality capital) to absorb losses. The federal Office of the Superintendent of Financial Institutions (OSFI) has implemented the Basel III framework for Canadian banks. The Credit Union Prudential Supervisors Association (CUPSA), an interprovincial association composed of credit union deposit insurers and prudential supervisors across Canada, has endorsed a common set of capital adequacy principles. Among other things, CUPSA advocates that capital adequacy standards for credit unions should be modelled on the Basel III framework for the quality and quantity of capital and on OSFI’s published guideline for risk weighting, including charges for credit risk, operational risk and market risk. In addition, the quantity of capital should include capital conservation and countercyclical buffers. Credit unions have unique capital attributes in that they do not issue common shares, and do not access the capital markets in the same manner as publicly-traded financial institutions. Consequently, in considering the application of Basel III standards to credit unions, consideration would need to be given to identifying what modifications, if any, to the framework are desirable.

Questions for Consideration:

Should the Basel III capital framework be adopted for Ontario credit unions? What modifications to the framework, if any, should be considered to reflect the unique capital structure of credit unions?

Group Capital As a result of legislative amendments made in 2009, two or more credit unions may enter into an agreement with a league to form a group for the purposes of satisfying the capital adequacy requirements. To date, some credit unions and leagues have expressed interest in this concept, but have indicated that the prescribed conditions to form a group are unworkable.

7

Questions for Consideration:

Should the existing group capital provisions be maintained? If so, how could the provisions be improved to make them more workable from a practical standpoint while ensuring the safety and soundness of the credit union system?

LENDING AND INVESTMENT RESTRICTIONS

One of the core functions of a credit union is to provide loans to its members. While the financial return on loans and investments is important, the safety and liquidity of the portfolio is of paramount concern. For this reason, the CUCPA sets out the types of permissible investments and places limits on the size and composition of loans. Generally, Class 1 credit unions (those with less than $50 million in assets/no commercial loans) are subject to rules that set out classes of loans, limits on aggregate loans of the same class, limits on loans to persons or connected persons, prohibited investments and a list of eligible investments. Class 2 credit unions are also subject to some limits and prohibitions, but otherwise establish their own prudent lending limits and investment policies.

Questions for Consideration: What changes, if any, should be considered to the lending and investment limits or prohibitions and why? For each recommended change, quantify the financial impact or expected benefit and demonstrate how prudential goals would be maintained.

Syndicated Loans

A credit union can only lend money to a member or participate in a loan syndication in which the borrower is a member of one of the credit unions in the syndicate. Under a syndicated loan, all of the lenders agree to fund a specified portion of the loan. Syndicated loans are often used by credit unions to provide commercial loans or mortgage loans to members where the size of the loan would otherwise exceed the lending limits of the credit union. As a result, it enables credit unions to continue to serve the economic needs of their members and communities.

8

As well, syndicated loans provide an opportunity for credit unions to diversify their loan portfolio while often receiving a higher yield or return.

Lenders in a syndicated loan can include Ontario credit unions, banks or other types of financial institutions; however credit unions from other provinces are not currently permitted lenders in loan syndications.

Questions for Consideration: Should the prescribed parties to a syndicated loan in which an Ontario credit union participates include credit unions from other provinces? If so, quantify the estimated benefits to Ontario credit unions and demonstrate how prudential goals would be maintained. What other changes to the rules regarding syndicated loans should be considered?

Investments in Subsidiaries

Credit unions are prohibited from controlling more than 30 per cent of the voting rights or equity of an entity unless the entity is on the list of prescribed subsidiaries. Prescribed subsidiaries generally operate businesses that are complementary to the business of a credit union such as a financial institution (e.g. bank, insurer, trust corporation), information services corporation, mutual fund corporation, securities dealer or mortgage brokerage. The list of prescribed subsidiaries is substantially harmonized with the types of subsidiaries banks are permitted to own under the Bank Act. Some credit unions have been advocating for an expanded list of prescribed subsidiaries.

Question for Consideration:

Should the list of prescribed subsidiaries that credit unions are permitted to own be modified? If so indicate why and how the change would be consistent with the prudential framework.

9

RULES BASED ON SIZE

In 2009, Ontario’s legislative framework was amended to ease the regulatory burden of small credit unions by streamlining the capital, investment and lending requirements while continuing to ensure consumer protection and system soundness. At the same time, the rules for larger credit unions in more complex lines of business such as commercial lending were modernized to recognize their unique risk profile and business needs. Given the rapid rate of consolidation that has occurred over the past five years in the sector, there are now fewer credit unions with less than $50 million in assets yet a greater number of larger credit unions of significant size.

Ontario needs to consider whether the existing threshold of $50 million in assets/ no commercial lending is still appropriate for differentiating classes of credit unions and the rules that apply to them. In addition, consideration should be given to whether differentiated rules for the largest credit unions are needed to address their more complex business operations and unique risk profiles.

Questions for Consideration:

Should Ontario continue to apply different regulatory requirements based on the size of institution? If so, what are the appropriate thresholds or triggers for differentiated rules? Should consideration be given to creating rules tailored to Ontario’s largest credit unions? Are there other regulatory requirements that should be tailored based on the size of institution?

GOVERNANCE

Good corporate governance is essential for ensuring the sustainability and financial viability of a credit union. As democratically owned and controlled financial institutions, it is important that credit union members elect directors that act in the membership’s best interests in an effective, transparent and accountable manner. Following the global financial downturn, there has been increased scrutiny and focus across jurisdictions on the roles and responsibilities of board of directors in strengthening corporate governance.

10

Board effectiveness and performance is a function not only of technical competency and financial literacy, but of a strong understanding of the regulatory environment, risk management principles, and strategic vision. In addition to the processes, roles and responsibilities set out in the CUCPA, the Deposit Insurance Corporation of Ontario (DICO) has proactively worked to enhance corporate governance in the credit union system through the publication of guidance notes on various best practices including director competencies and training.

Questions for Consideration:

Are further enhancements to credit union corporate governance necessary or desirable? What challenges do credit unions face in ensuring corporate governance practices, rules and procedures meet the best interests of their members?

CONSUMER PROTECTION

Credit unions are continuously developing new and innovative products and services to better meet the evolving needs of their members and to remain competitive in the marketplace. As a result, it is important to ensure that consumers are well informed and understand the costs, risks and suitability of the products and services that they are purchasing. While the CUCPA includes a consumer protection framework that requires mandatory disclosures regarding the cost of borrowing, interest paid on accounts and unclaimed deposits, as well as a complaints-handling procedure, there are additional areas of consumer protection that could be addressed, including:

additional disclosures (e.g. mortgage insurance and account charges)

maximum cheque holding periods

prohibition on charging fees for cashing government cheques

credit card business practices

branch closure notices

prohibition on negative option billing

account opening requirements

11

Most recently, the federal government has announced Canada’s banks have voluntarily committed to provide no cost accounts to specific vulnerable groups as well as to enhance their disclosure measures on collateral charge mortgages and power of attorney arrangements. Ontario could consider similar commitments by credit unions if they are brought forward.

Question for Consideration:

Are there specific additional consumer protection provisions that should be addressed in the CUCPA? Should the government explore the possibility of voluntary commitments with the credit union sector, as opposed to legislative measures, to address certain areas of consumer protection?

ROLES OF REGULATORS

In an effort to promote effective and efficient regulatory oversight, many functions of the Superintendent of Financial Services at the Financial Services Commission of Ontario (FSCO) were transferred to DICO in 2009. These included regulatory oversight and approvals related to capital and liquidity requirements, restrictions on borrowing, lending and investments and enforcement.

Related amendments were made to allow DICO to exercise powers that the Superintendent can also exercise and to provide for certain information or notices to be given to DICO. At the same time, the functions related to the incorporation of credit unions were transferred from the Minister to the Superintendent. It is now appropriate to examine the current regulatory framework and evaluate whether the allocation of roles promotes effective regulatory oversight of the credit union sector.

Questions for Consideration:

Is the allocation of regulatory responsibilities between FSCO and DICO clear and appropriate? Are any changes to the mandate or governance structure for FSCO or DICO necessary to improve regulatory oversight of the credit union sector?

12

DEPOSIT INSURANCE COVERAGE LIMIT

Deposit insurance is a key component of Ontario’s regulatory safety net for the credit union sector. Its purpose is to protect small depositors from loss and promote stability and confidence in the credit union system while enabling an orderly process for dealing with failed institutions. International best practices recommend that deposit insurance coverage should be limited, as opposed to unlimited, in order to minimize moral hazard. Moral hazard refers to the situation where financial institutions are more likely to take risks in their investment and lending decisions knowing that the potential costs or losses from those risks will be borne by others (e.g. by a deposit insurance scheme or the government). Depositors, especially large corporate and commercial depositors who otherwise contribute to market discipline, can also succumb to moral hazard by undertaking less due diligence when selecting their deposit taking institution if their funds are fully insured. The need to minimize moral hazard is one of the key lessons learned from the global financial meltdown. Ontario’s deposit insurance coverage limit is $100,000 for aggregate insured accounts held by a member at each credit union. However, deposits in certain registered accounts, including registered retirement savings plans, registered retirement income funds, registered education savings plans, registered disability savings plans, and tax-free savings accounts are fully insured. Combined, unregistered and registered insured deposits in Ontario are valued at approximately $34 billion, with registered accounts representing $9 billion of the total amount. The average amount deposited per member in insured accounts with Ontario credit unions is approximately $20,000 which is well within the $100,000 limit.

While Ontario’s $100,000 coverage is harmonized with Quebec and the federal jurisdiction, other provinces have higher limits, and in some cases, unlimited coverage for all deposits.

13

Ontario’s deposit insurance regime is ultimately funded by credit union members through annual premiums paid by credit unions to DICO.

Questions for Consideration: Should Ontario increase its deposit insurance coverage limit? If yes, at what level should the limit be set? Please explain the rationale for the limit proposed and quantify the expected costs and benefits to credit union members, and to the stability of the system as a whole.

OPERATIONS ACROSS PROVINCIAL BORDERS Traditionally, and based on their historic roots as community-based provincially-incorporated financial institutions, credit unions in Canada have not sought to carry on business across provincial borders. However, as credit unions increase in size, expand their membership base, grow their branch network and take advantage of economies of scale through mergers and acquisitions, the option of operating across provincial borders may become more appealing. There is no coordinated or clear framework among provincial jurisdictions to enable credit unions to register and carry on business in multiple provinces. The development of a framework would need to address issues such as regulatory overlap and duplication, harmonization of standards and costs of regulation. Under the CUCPA, Ontario permits an extra-provincial credit union to register in Ontario if the Government of Ontario has entered into an agreement with another province or territory which provides for reciprocal rights for Ontario credit unions, subject to prescribed conditions. No substantive agreements are currently in place and no conditions have been prescribed to date. However the CUCPA does require that any deposits taken in Ontario must be insured by the jurisdiction where the extra-provincial credit union was incorporated. In 2012 the federal government implemented amendments to the Bank Act to enable the incorporation of federal credit unions. Under the framework, federal credit unions are able to operate across provincial borders and are subject to federal oversight, including regulatory supervision by OSFI and deposit insurance coverage provided by the Canada Deposit Insurance Corporation. To date, no federal credit unions have been incorporated, and no provincial credit unions have applied for continuance as a federal credit union.

14

Questions for Consideration:

In light of the recently implemented federal framework for credit unions, is there a need for the CUCPA to continue to provide a framework for the registration of extra-provincial credit unions? If so, what should be the key elements of the framework? For example, whose standards should apply to extra-provincial credit unions and which jurisdiction should be responsible for enforcing those standards?

TECHNICAL AMENDMENTS The five-year review of the CUCPA is also an opportunity to identify and address any technical amendments that are necessary to improve the clarity of the legislation and enable better compliance with its provisions.

Questions for Consideration: Are there any technical amendments to the CUCPA that are necessary? Are there any provisions that are obsolete or contain an error that needs to be corrected?

SUMMARY OF CONSULTATION QUESTIONS Vision and Strategic Priorities

1. What is your vision for the credit union sector in Ontario? What are the top three strategic priorities that are essential to foster such a vision? What is the government’s role in enabling the credit union sector to achieve this vision?

Capital Adequacy

2. Should the Basel III capital framework be adopted for Ontario credit unions? What modifications to the framework, if any, should be considered to reflect the unique capital structure of credit unions?

3. Should the existing group capital provisions be maintained? If so, how could the provisions be improved to make them more workable from a practical standpoint while ensuring the safety and soundness of the credit union system?

15

Lending and Investment Restrictions

4. What changes, if any, should be considered to the lending and investment limits or prohibitions and why? For each recommended change, quantify the financial impact or expected benefit and demonstrate how prudential goals would be maintained.

5. Should the list of prescribed subsidiaries that credit unions are permitted to own be modified? If so indicate why and how the change would be consistent with the prudential framework.

6. Should the prescribed parties to a syndicated loan in which an Ontario credit union participates include credit unions from other provinces? If so, quantify the estimated benefits to Ontario credit unions and demonstrate how prudential goals would be maintained. What other changes to the rules regarding syndicated loans should be considered?

Rules Based on Size

7. Should Ontario continue to apply different regulatory requirements based on the size of institution? If so, what are the appropriate thresholds or triggers for differentiated rules? Should consideration be given to creating rules tailored to Ontario’s largest credit unions? Are there other regulatory requirements that should be tailored based on the size of institution?

Corporate Governance

8. Are further enhancements to credit union corporate governance necessary or desirable? What challenges do credit unions face in ensuring corporate governance practices, rules and procedures meet the best interests of its members?

Consumer Protection

9. Are there additional consumer protection provisions that should be addressed in the CUCPA?

10. Should the government explore the possibility of voluntary commitments with the credit union sector, as opposed to legislative measures, to address certain areas of consumer protection?

16

Roles of Regulators

11. Is the allocation of regulatory responsibilities between FSCO and DICO clear and appropriate? Are any changes to the mandate or governance structure for FSCO or DICO necessary in order to improve regulatory oversight of the credit union sector?

Deposit Insurance Coverage Limit

12. Should Ontario increase its deposit insurance coverage limit? If yes, at what level should the limit be set? Please explain the rationale for the limit proposed and quantify the expected costs and benefits to credit union members, and to the stability of the system as a whole.

Operations across Provincial Borders

13. In light of the recently implemented federal framework for credit unions, is there a need for the CUCPA to continue to provide a framework for the registration of extra-provincial credit unions? If so, what should be the key elements of the framework? For example, whose standards should apply to extra-provincial credit unions and which jurisdiction should be responsible for enforcing those standards?

Technical Amendments

14. Are there any technical amendments to the CUCPA that are necessary? Are there any provisions that are obsolete or contain an error that needs to be corrected?