CREDIT UNION IFRS FINANCIAL STATEMENTS - DICO · PDF fileCREDIT UNION IFRS FINANCIAL...

41

CREDIT UNION IFRS FINANCIAL STATEMENTS Tips to help prepare and improve (2012 & Beyond) BDO CANADA LLP February 1, 2013 Page 1

Transcript of CREDIT UNION IFRS FINANCIAL STATEMENTS - DICO · PDF fileCREDIT UNION IFRS FINANCIAL...

CREDIT UNION IFRS FINANCIAL STATEMENTS Tips to help prepare and improve (2012 & Beyond)

BDO CANADA LLPFebruary 1, 2013

Page 1

With an introduction from With an introduction from Richard DaleRichard Dale, , Director, Regulatory AffairsDirector, Regulatory Affairs

of DICOof DICO

CREDIT UNION IFRS FINANCIAL STATEMENTS CREDIT UNION IFRS FINANCIAL STATEMENTS Facilitators

Craig Cross

Paul Vetrone

Page 3

CREDIT UNION IFRS FINANCIAL STATEMENTS CREDIT UNION IFRS FINANCIAL STATEMENTS Agenda

IFRS UpdateIFRS Update• 2012 Financial Statements

- New or amended standards for December 31, 2012- Tips for improving financial statement disclosures p p g

• Standards effective in 2013- New or amended standards for December 31, 2013

• 2014 and beyond!- IASB work plan and developments

Page 4

AGENDAAGENDA2012 Financial Statements - Amended Standards

Page 5

STANDARDS EFFECTIVE IN 2012STANDARDS EFFECTIVE IN 2012Amendments to Standards Effective for 2012

Years beginning on or after

IFRS 1 Exemption for severe hyperinflation July 1, 2011

IFRS 1 Removal of fixed dates July 1, 2011

IFRS 7 Disclosures on transfers of financial assets July 1, 2011

IAS 12 Accounting for investment properties January 1, 2012

Page 6

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: Disclosures

• Result of the financial crisis• Result of the financial crisis

• Extended disclosures for continuing exposure in:- Financial Assets not derecognized in their entirety (minor)- Financial Assets derecognized in their entirety (major)g y ( j )

• Presented in single note

• Comparative information not required

• Effective for annual period beginning on or after 1 July 2011 with early Effective for annual period beginning on or after 1 July 2011, with early application permitted

Page 7

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: Disclosures

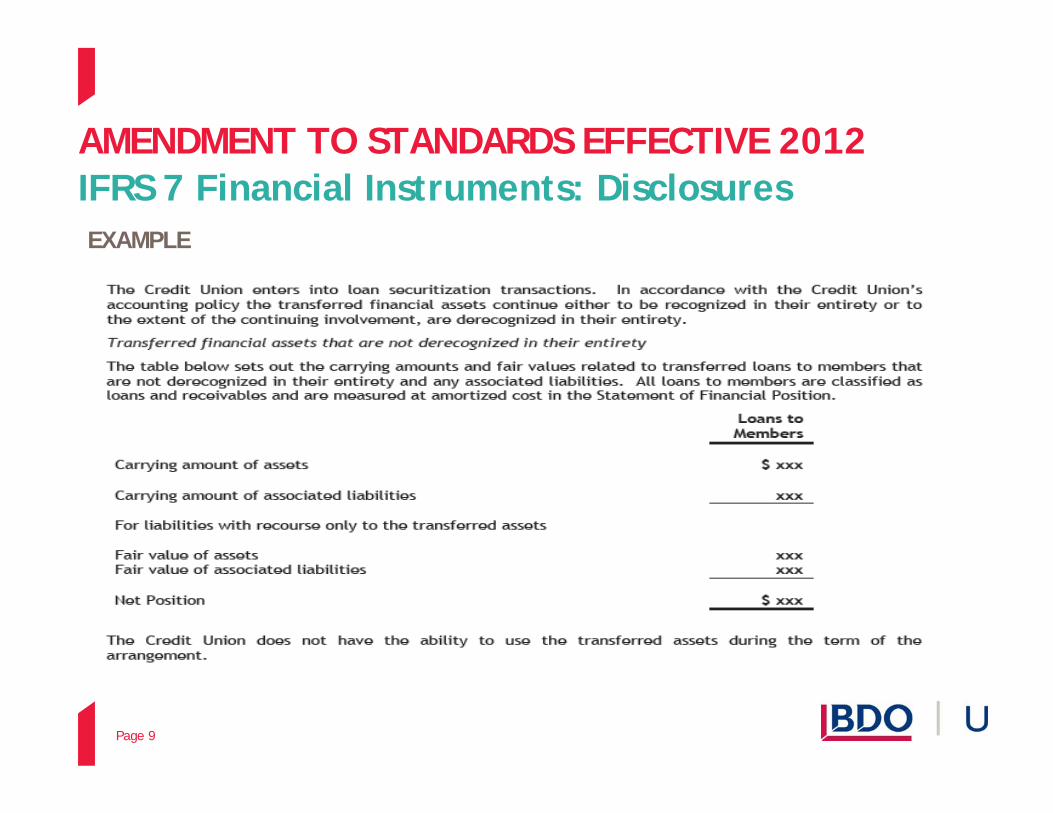

Disclosures for financial assets that are NOT derecognized in their entirety Disclosures for financial assets that are NOT derecognized in their entirety

• Description of nature and relationship between transferred assets and associated liabilities, including restrictions arising from the transfer on the reporting entity’s use of the transferred assetsreporting entity s use of the transferred assets

• When the counterparty (counterparties) to the associated liabilities has (have) recourse only to the transferred assets, a schedule should be included that sets out:

the fair value of the transferred assets;

the fair value of the associated liabilities; and

the net position (the difference between the fair value of the p (transferred assets and the associated liabilities)

Page 8

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: DisclosuresEXAMPLE

Page 9

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: Disclosures

Transferred financial assets that ARE derecognized in their entiretyTransferred financial assets that ARE derecognized in their entirety

• Nature and purpose of continuing involvement

• The carrying amount of contingent involvement and maximum exposure to lossloss

• Future cash outflows to repurchase derecognized assets

• Gain / loss at derecognition

I f i i i l• Income from continuing involvement

• Details if derecognition activity is not evenly distributed over financial year

Page 10

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: DisclosuresEXAMPLE

Page 11

AMENDMENT TO STANDARDS EFFECTIVE 2012 AMENDMENT TO STANDARDS EFFECTIVE 2012 IFRS 7 Financial Instruments: DisclosuresEXAMPLE

Page 12

2012 FINANCIAL STATEMENTSf f l d lTips for improving financial statement disclosures

Page 13

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

C di l i Common disclosure issues: A. IFRS Transition notes – remove!B. Business combinations / Amalgamations / MergersC J d t d ti tC. Judgments and estimatesD. Additional GAAP measures

Page 14

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

B) Business CombinationsB) Business Combinations• Disclosure deficiencies have been noted in the following areas:

- Reason for business combination- Qualitative description of what makes up goodwill (if any)- Bargain purchases- Revenue and profit or loss since acquisition date- Pro forma revenue and profit or loss- Gross contractual amounts of acquired receivable and an estimate of amounts not expected to be Gross contractual amounts of acquired receivable and an estimate of amounts not expected to be

collected - Business combinations completed after the reporting period but before financial statements are

authorized for issue

Page 15

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

C) J d t d E ti t C) Judgments and Estimates • Focus on the most significant judgments and estimates; • Provide clear distinction between judgments and estimates;

P id ffi i t d t il t d t d th t f th j d t th f t • Provide sufficient detail to understand the nature of the judgment, the factors considered and the basis for management’s determination; and

• Ensure the basis for judgment is well documented.

Page 16

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosuresC) Judgments and Estimates Sources of Estimation Uncertainty and Judgements:From the CICA HANDBOOK – PART I – IAS 1 Presentation of Financial Statements

- An entity shall disclose, in the summary of significant accounting policies or other notes, the judgements apart from those involving estimations (see paragraph 125) that management has judgements, apart from those involving estimations (see paragraph 125), that management has made in the process of applying the entity’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements (IAS 1.122)

- In the process of applying the entity's accounting policies, management makes various judgements, apart from those involving estimations, that can significantly affect the amounts it recognises in the financial statements. For example, management makes judgements in determining:- Whether financial assets are held-to-maturity investments; - When substantially all the significant risks and rewards of ownership of financial assets and

lease assets are transferred to other entities; - Whether, in substance, particular sales of goods are financing arrangements and therefore do

not give rise to revenue; and - Whether the substance of the relationship between the entity and a special purpose entity

indicates that the entity controls the special purpose entity (IAS 1.123)

Page 17

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosuresC) Judgments and Estimates Common Judgment Areas for a Credit Union• Member loan loss provision;

- Objective evidence of impairment of individually significant financial assets; C ll ti t b l ith i il dit i k h t i ti- Collective assessment - group member loans with similar credit risk characteristics

• Other Financial Assets;- Available-for-sale carried at cost- Objective evidence of impairmentj p- Derecognition through loan securitization transactions

• Hedge accounting; • Income taxes; • PP&E and intangible asset depreciation / amortization rates;• Member shares classification;• Lease – operating or finance

Page 18

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

C) Judgments and Estimates C) Judgments and Estimates Sources of Estimation Uncertainty and Judgements:From the CICA HANDBOOK – PART I – IAS 1 Presentation of Financial StatementsIAS 1 125IAS 1.125

Sources of estimation uncertainty. An entity shall disclose information about the assumptions it makes about the future, and other major sources of estimation uncertainty at the end of the reporting period, that have a y p g p ,significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year. In respect of those assets and liabilities, the notes shall include details of:

• Their nature; and

• Their carrying amount as at the end of the reporting period

Page 19

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

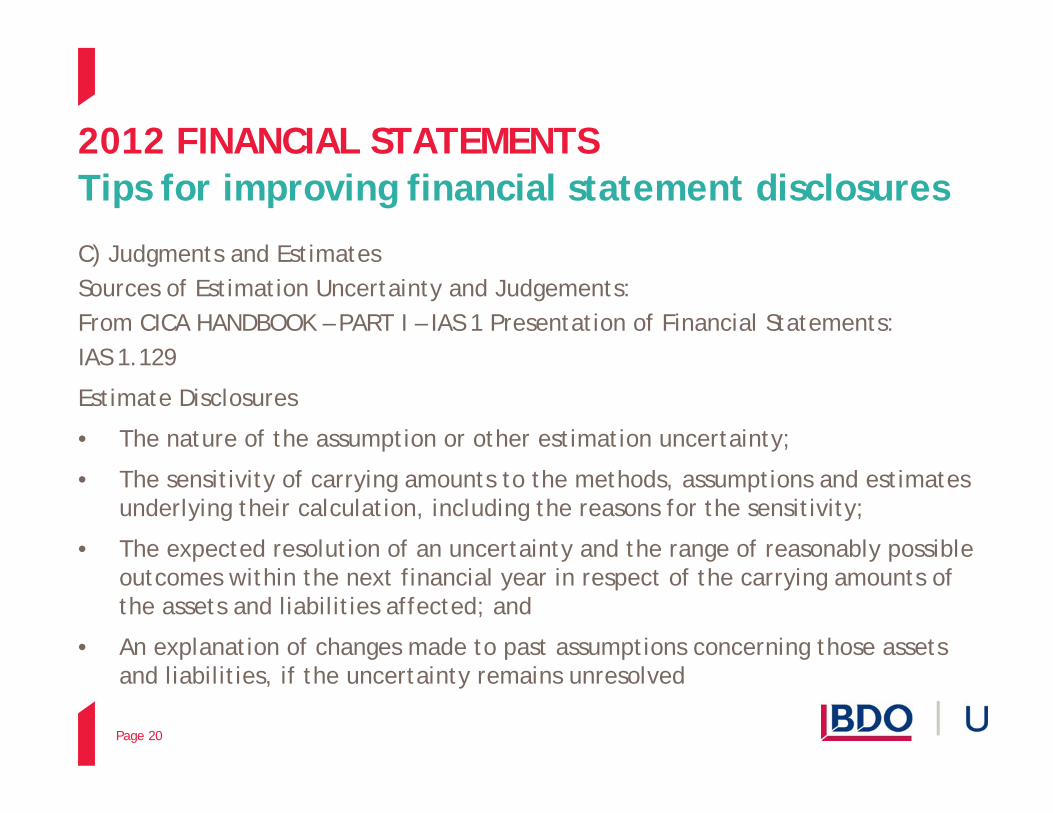

C) Judgments and Estimates C) Judgments and Estimates Sources of Estimation Uncertainty and Judgements:From CICA HANDBOOK – PART I – IAS 1 Presentation of Financial Statements: IAS 1 129IAS 1.129

Estimate Disclosures

• The nature of the assumption or other estimation uncertainty;

• The sensitivity of carrying amounts to the methods, assumptions and estimates underlying their calculation, including the reasons for the sensitivity;

• The expected resolution of an uncertainty and the range of reasonably possible p y g y poutcomes within the next financial year in respect of the carrying amounts of the assets and liabilities affected; and

• An explanation of changes made to past assumptions concerning those assets and liabilities, if the uncertainty remains unresolved

Page 20

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

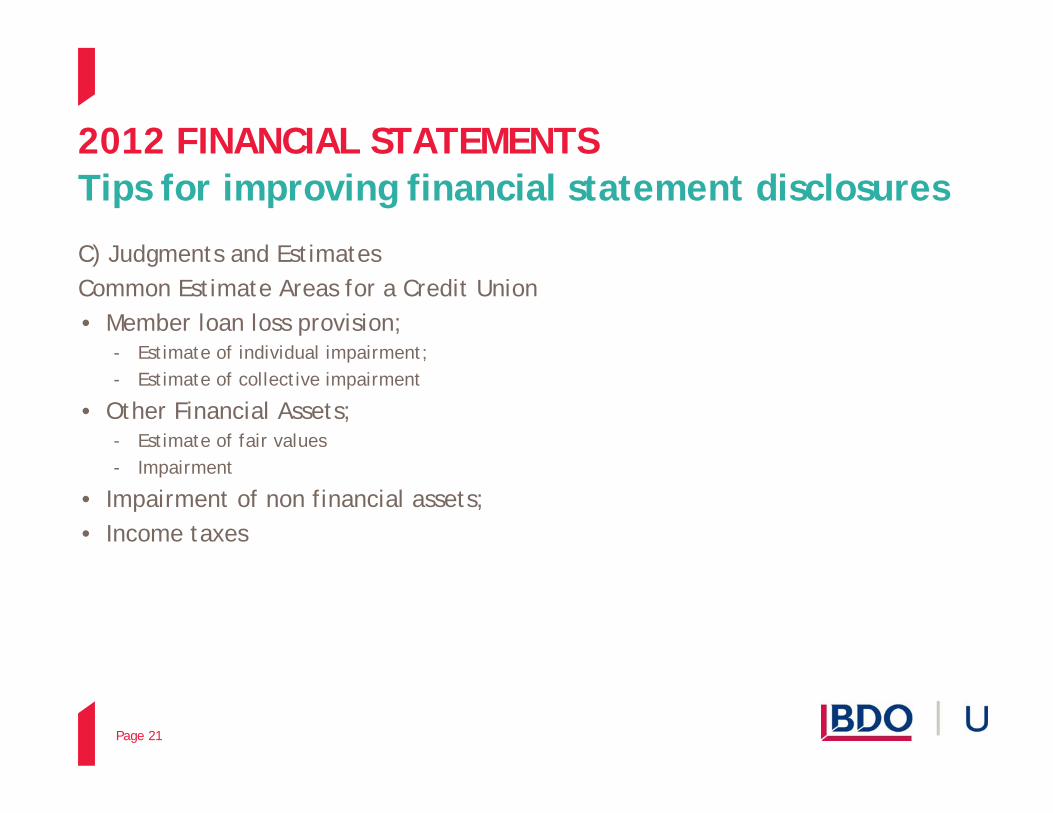

C) Judgments and Estimates C) Judgments and Estimates Common Estimate Areas for a Credit Union• Member loan loss provision;

- Estimate of individual impairment; Estimate of individual impairment; - Estimate of collective impairment

• Other Financial Assets; - Estimate of fair values- Impairment

• Impairment of non financial assets; • Income taxes

Page 21

2012 FINANCIAL STATEMENTS 2012 FINANCIAL STATEMENTS Tips for improving financial statement disclosures

D) Additi l GAAP MD) Additional GAAP Measures• Items to consider when presenting an additional GAAP measure:

- Is the line item/subtotal unnamed? - Is the name inappropriate and include generic identifiers?Is the name inappropriate and include generic identifiers?

- (e.g. “before the undernoted” or “other items”) - Does the presentation of the additional GAAP measure confuse, obscure or exceed the prominence

of minimum disclosure items? - Is additional disclosure required to clearly explain the measure? q y p- Is there a discussion and analysis of the measure?

Page 22

AGENDAAGENDANew Standards or Amendments for 2013

Page 23

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013

Years beginning on or after

IFRS 10 Consolidated Financial Statements January 1, 2013

IFRS 11 Joint Arrangements January 1, 2013

IFRS 12 Disclosure of Interests in Other Entities January 1 2013IFRS 12 Disclosure of Interests in Other Entities January 1, 2013

IAS 27 Separate Financial Statements January 1, 2013

IAS 28 Investments in Associates and Joint Ventures January 1, 2013

IFRS 13 Fair Value Measurement January 1, 2013

IAS 19 Employee Benefits January 1, 2013

IAS 1 Presentation of Financial Statements July 1, 2012

IFRIC 20 Stripping costs in the production phase of a surface mine January 1, 2013

Amendment to IFRS 1 First-Time Adoption of IFRS – Government Loans January 1 2013

Page 24

January 1, 2013

STANDARDS EFFECTIVE FOR 2013 STANDARDS EFFECTIVE FOR 2013 Interaction Between IFRS 10, 11, 12 and IAS 28

Consolidation in accordance

CONTROL ALONE?

YES NO

YES NO

Joint control?Consolidation in accordance with IFRS 10

Disclosures in accordance with IFRS 12

Define type of joint arrangement in accordance with IFRS 11 Significant influence?

JOINT VENTUREJOINT OPERATION YES NO

Account for an investment in accordance with IAS 28

Disclosures in accordance

Account for assets, liabilities, revenues and expenses

Disclosures in accordance

IFRS 9

JOINT VENTUREJOINT OPERATION YES NO

with IFRS 12

Page 25

with IFRS 12

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013IFRS 10 – Three Elements of Control

POWER LINKEDEXPOSURE

TO VARIABLE RETURNS

Existing rights Principal vs. agentPotential to vary with

investee’s performance

Current ability to direct

Relevant activities Di id d

Substance

Relevant activities

Substantive not just protective

Dividends, remuneration,

economies of scale,etc.

Page 26

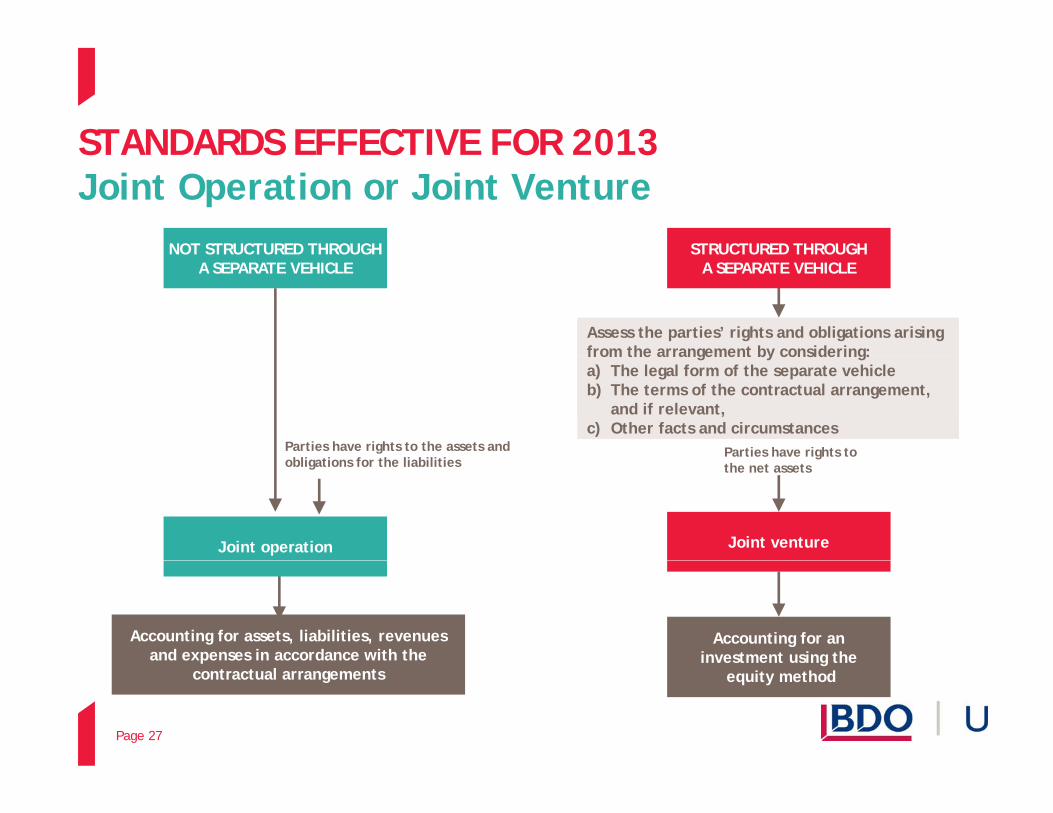

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013Joint Operation or Joint Venture

STRUCTURED THROUGH NOT STRUCTURED THROUGH

Assess the parties’ rights and obligations arising from the arrangement by considering:

STRUCTURED THROUGH A SEPARATE VEHICLE

NOT STRUCTURED THROUGH A SEPARATE VEHICLE

from the arrangement by considering:a) The legal form of the separate vehicleb) The terms of the contractual arrangement,

and if relevant,c) Other facts and circumstances

Parties have rights to the assets and bli ti f th li biliti

Parties have rights to obligations for the liabilities

gthe net assets

Joint ventureJoint operation

Accounting for assets, liabilities, revenues and expenses in accordance with the

Accounting for an investment using the

Page 27

pcontractual arrangements

gequity method

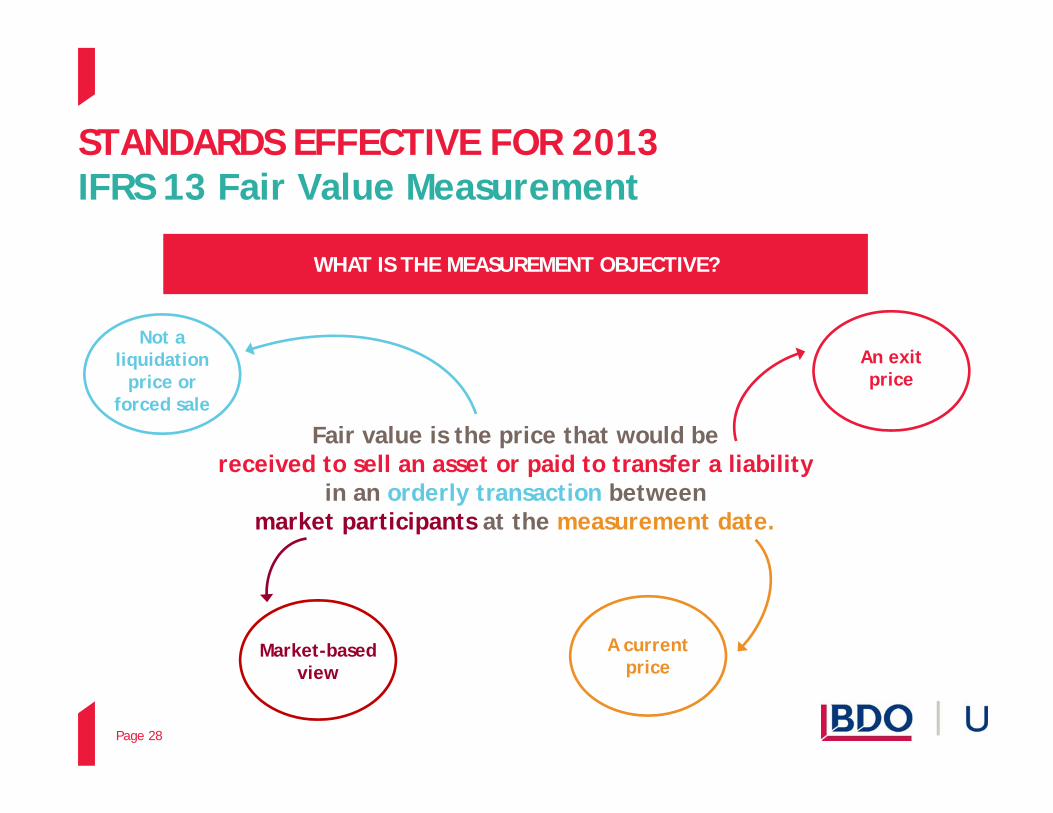

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013IFRS 13 Fair Value Measurement

WHAT IS THE MEASUREMENT OBJECTIVE?

Not a li id ti An exit

Fair value is the price that would be i d t ll t id t t f li bilit

liquidation price or

forced sale

An exit price

received to sell an asset or paid to transfer a liability in an orderly transaction between

market participants at the measurement date.

A current i

Market-based

Page 28

priceview

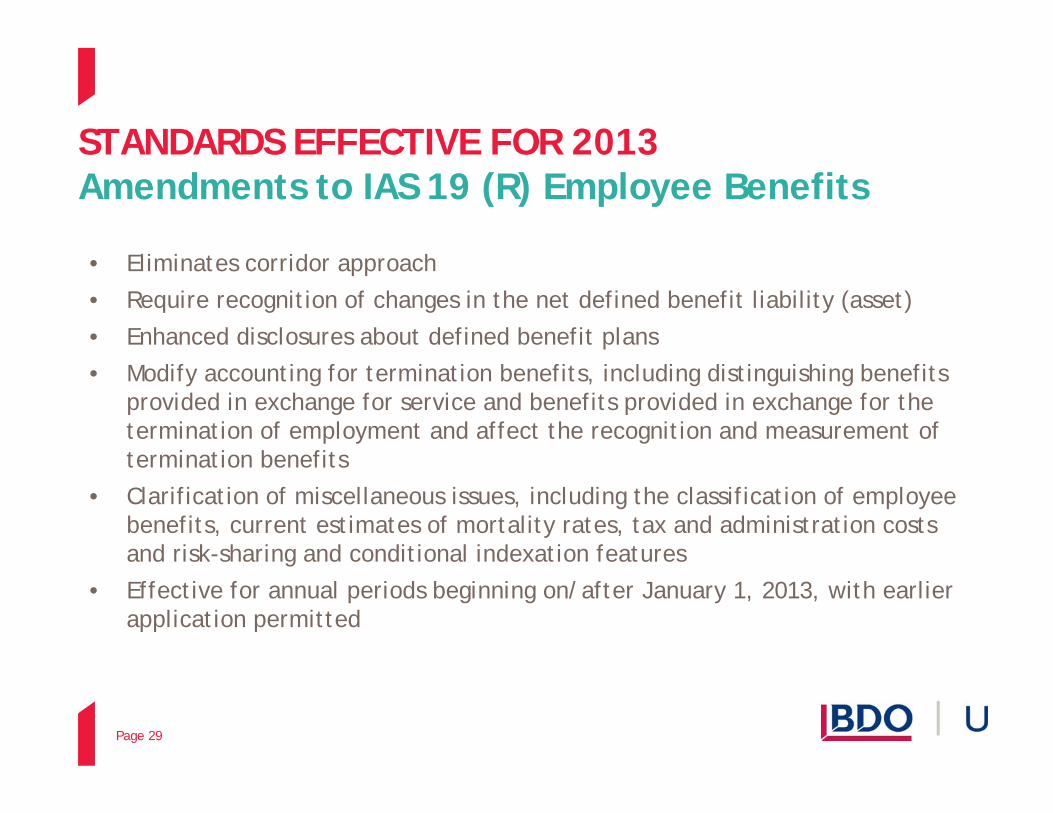

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013Amendments to IAS 19 (R) Employee Benefits

• Eliminates corridor approach

• Require recognition of changes in the net defined benefit liability (asset)

• Enhanced disclosures about defined benefit plans

• Modify accounting for termination benefits, including distinguishing benefits provided in exchange for service and benefits provided in exchange for the termination of employment and affect the recognition and measurement of termination benefits termination benefits

• Clarification of miscellaneous issues, including the classification of employee benefits, current estimates of mortality rates, tax and administration costs and risk-sharing and conditional indexation features and risk sharing and conditional indexation features

• Effective for annual periods beginning on/after January 1, 2013, with earlier application permitted

Page 29

STANDARDS EFFECTIVE FOR 2013

Changes in the net defined benefit liability (asset) into three components to be

STANDARDS EFFECTIVE FOR 2013Amendments to IAS 19 (R) Employee Benefits

Changes in the net defined benefit liability (asset) into three components, to bepresented as follows:

a) Service cost – presented in profit or loss

b) Net interest on the net defined benefit liability (asset) presented in profit b) Net interest on the net defined benefit liability (asset) – presented in profit or loss; and

c) Remeasurement of the net defined benefit liability (asset) – presented in other comprehensive income (OCI) and not recycled through profit or loss. other comprehensive income (OCI) and not recycled through profit or loss.

Page 30

STANDARDS EFFECTIVE FOR 2013STANDARDS EFFECTIVE FOR 2013

Pre IAS 19R $

Amendments to IAS 19 (R) Employee Benefits

Original liability 3,000,000

Unamortized actuarial loss 1,000,000

Equity before Adjustment 4 500 000Equity before Adjustment 4,500,000

Post IAS 19R

Liability post IAS 19R 4,000,000

Unamortized actuarial loss 0

Equity after adjustment (through retained earnings) 3,500,000

Effect on regulatory capital (assume total assets $250 000 000)Effect on regulatory capital (assume total assets $250,000,000)

Regulatory capital prior to IAS 19R 12,000,000 4.80%

Regulatory capital post IAS 19R 11,000,000 4.40%

Page 31

STANDARDS EFFECTIVE FOR 2013

• Option to present OCI in a separate statement or as part of the statement of

STANDARDS EFFECTIVE FOR 2013IAS 1 Presentation of Financial Statements

• Option to present OCI in a separate statement or as part of the statement of profit or loss and other comprehensive income

• Requires entities to present line items for OCI amount by nature and distinguish those that will be reclassified to profit or loss; and those that that distinguish those that will be reclassified to profit or loss; and those that that will not be reclassified

• Present components of OCI either net of related tax effects or before tax with one amount shown for the aggregate amount of income tax relating to those components

• Effective for annual periods beginning on / after July 1, 2012, with earlier application permitted

Page 32

ANNUAL IMPROVEMENTSANNUAL IMPROVEMENTS2009-2011 Cycle

TOPIC

Repeated Application of IFRS 1p pp

IFRS 1 Borrowing Costs

IAS 1 Comparative Informationp

IAS 16 Classification of Servicing Equipment

IAS 32 Tax Effects of Distribution to Holders of Equity Instruments

IAS 34 Total Asset and Total Liability Disclosure

Page 33

AGENDAAGENDA2014 and Beyond

Page 34

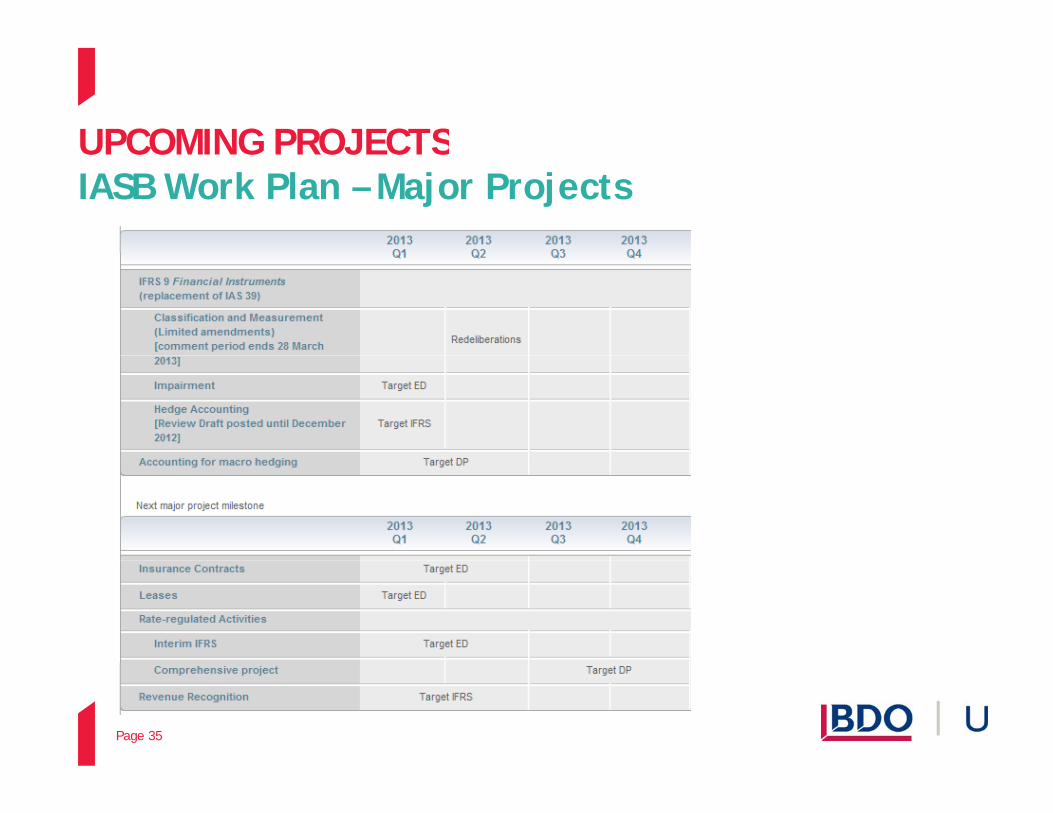

UPCOMING PROJECTSUPCOMING PROJECTSIASB Work Plan – Major Projects

Page 35

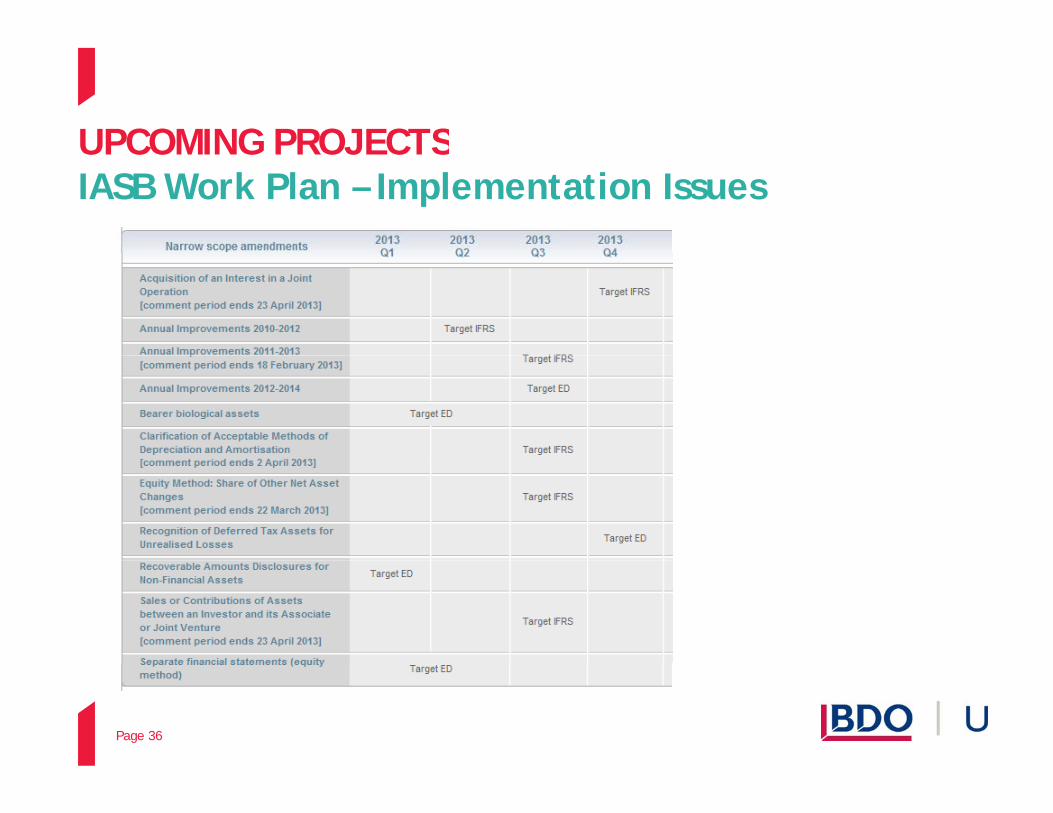

UPCOMING PROJECTSUPCOMING PROJECTSIASB Work Plan – Implementation Issues

Page 36

UPCOMING PROJECTSUPCOMING PROJECTSIASB Work Plan – Interpretations

Page 37

Upcoming Projects

• Lessee accounting – One approach at initial recognition no change in

Upcoming ProjectsIAS 17 – Leases

Lessee accounting One approach at initial recognition, no change in fundamental approach- Recognition of a liability to make lease payments and a right to use (ROU) asset

- Both measured at the present value of the lease payments

- Lease term: non-cancellable period, plus any options where there is a “significant economic incentive” to extend or not terminate

- Subsequent measurement of liability using the effective interest method

- For all leases (other than short term leases)For all leases (other than short term leases)

• Amortization of ROU – two models based on the nature of the underlying asset

Page 38

CREDIT UNION IFRS FINANCIAL STATEMENTS CREDIT UNION IFRS FINANCIAL STATEMENTS

QUESTIONS?Q

Page 39

CREDIT UNION IFRS FINANCIAL STATEMENTS CREDIT UNION IFRS FINANCIAL STATEMENTS Facilitators

BDO LLPSenior Manager

Craig Cross

National Accounting Standards 416 865 0111 ext [email protected]

BDO LLPManager – Client servicePeterborough Office

Paul Vetrone

Peterborough Office705-742 [email protected]

Page 40

CREDIT UNION IFRS FINANCIAL STATEMENTS CREDIT UNION IFRS FINANCIAL STATEMENTS

THANK YOU

Page 41