Credit Transactions Cases Nov 14, 2015

79

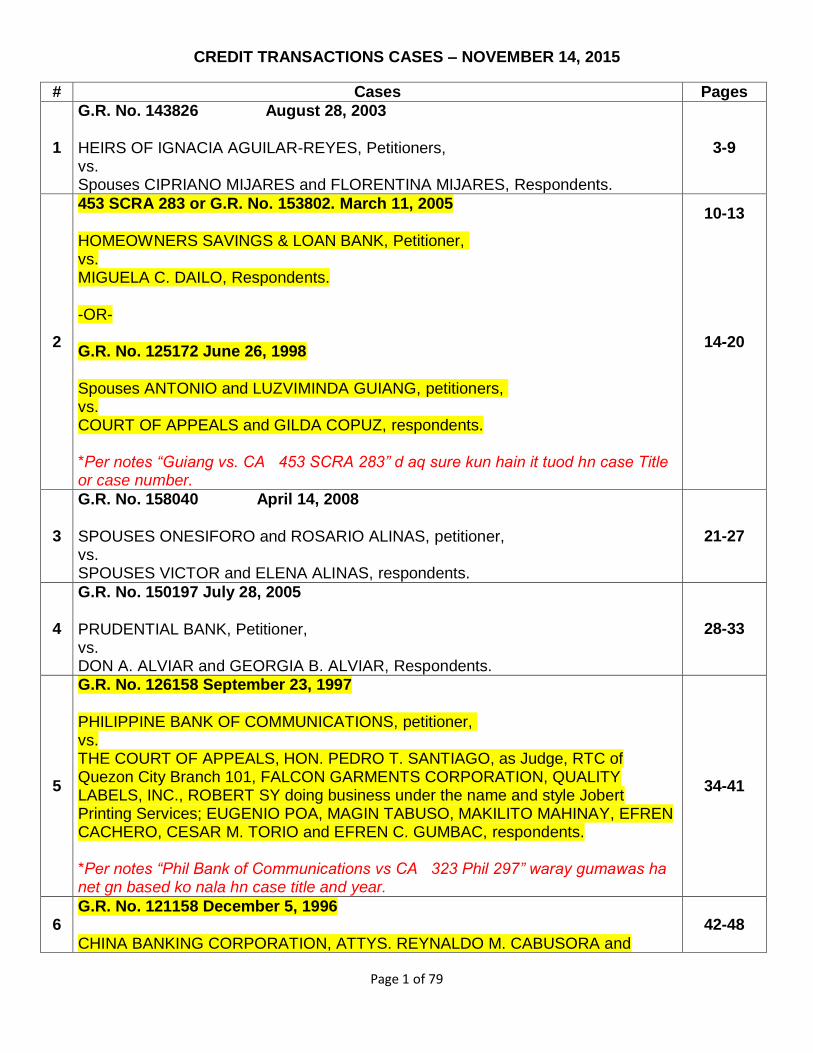

Page 1 of 79 CREDIT TRANSACTIONS CASES – NOVEMBER 14, 2015 # Cases Pages 1 G.R. No. 143826 August 28, 2003 HEIRS OF IGNACIA AGUILAR-REYES, Petitioners, vs. Spouses CIPRIANO MIJARES and FLORENTINA MIJARES, Respondents. 3-9 2 453 SCRA 283 or G.R. No. 153802. March 11, 2005 HOMEOWNERS SAVINGS & LOAN BANK, Petitioner, vs. MIGUELA C. DAILO, Respondents. -OR- G.R. No. 125172 June 26, 1998 Spouses ANTONIO and LUZVIMINDA GUIANG, petitioners, vs. COURT OF APPEALS and GILDA COPUZ, respondents. *Per notes “Guiang vs. CA 453 SCRA 283” d aq sure kun hain it tuod hn case Title or case number. 10-13 14-20 3 G.R. No. 158040 April 14, 2008 SPOUSES ONESIFORO and ROSARIO ALINAS, petitioner, vs. SPOUSES VICTOR and ELENA ALINAS, respondents. 21-27 4 G.R. No. 150197 July 28, 2005 PRUDENTIAL BANK, Petitioner, vs. DON A. ALVIAR and GEORGIA B. ALVIAR, Respondents. 28-33 5 G.R. No. 126158 September 23, 1997 PHILIPPINE BANK OF COMMUNICATIONS, petitioner, vs. THE COURT OF APPEALS, HON. PEDRO T. SANTIAGO, as Judge, RTC of Quezon City Branch 101, FALCON GARMENTS CORPORATION, QUALITY LABELS, INC., ROBERT SY doing business under the name and style Jobert Printing Services; EUGENIO POA, MAGIN TABUSO, MAKILITO MAHINAY, EFREN CACHERO, CESAR M. TORIO and EFREN C. GUMBAC, respondents. *Per notes “Phil Bank of Communications vs CA 323 Phil 297” waray gumawas ha net gn based ko nala hn case title and year. 34-41 6 G.R. No. 121158 December 5, 1996 CHINA BANKING CORPORATION, ATTYS. REYNALDO M. CABUSORA and 42-48

-

Upload

lalalaniba -

Category

Documents

-

view

33 -

download

3

description

Credit Transactions Cases Nov 14, 2015

Transcript of Credit Transactions Cases Nov 14, 2015

Page 1 of 79

CREDIT TRANSACTIONS CASES – NOVEMBER 14, 2015

# Cases Pages

1

G.R. No. 143826 August 28, 2003

HEIRS OF IGNACIA AGUILAR-REYES, Petitioners, vs. Spouses CIPRIANO MIJARES and FLORENTINA MIJARES, Respondents.

3-9

2

453 SCRA 283 or G.R. No. 153802. March 11, 2005

HOMEOWNERS SAVINGS & LOAN BANK, Petitioner, vs. MIGUELA C. DAILO, Respondents.

-OR-

G.R. No. 125172 June 26, 1998

Spouses ANTONIO and LUZVIMINDA GUIANG, petitioners, vs. COURT OF APPEALS and GILDA COPUZ, respondents.

*Per notes “Guiang vs. CA 453 SCRA 283” d aq sure kun hain it tuod hn case Title or case number.

10-13

14-20

3

G.R. No. 158040 April 14, 2008

SPOUSES ONESIFORO and ROSARIO ALINAS, petitioner, vs. SPOUSES VICTOR and ELENA ALINAS, respondents.

21-27

4

G.R. No. 150197 July 28, 2005

PRUDENTIAL BANK, Petitioner, vs. DON A. ALVIAR and GEORGIA B. ALVIAR, Respondents.

28-33

5

G.R. No. 126158 September 23, 1997

PHILIPPINE BANK OF COMMUNICATIONS, petitioner, vs. THE COURT OF APPEALS, HON. PEDRO T. SANTIAGO, as Judge, RTC of Quezon City Branch 101, FALCON GARMENTS CORPORATION, QUALITY LABELS, INC., ROBERT SY doing business under the name and style Jobert Printing Services; EUGENIO POA, MAGIN TABUSO, MAKILITO MAHINAY, EFREN CACHERO, CESAR M. TORIO and EFREN C. GUMBAC, respondents.

*Per notes “Phil Bank of Communications vs CA 323 Phil 297” waray gumawas ha net gn based ko nala hn case title and year.

34-41

6 G.R. No. 121158 December 5, 1996

CHINA BANKING CORPORATION, ATTYS. REYNALDO M. CABUSORA and

42-48

Page 2 of 79

RENATO C. TAGUIAM, petitioners, vs. COURT OF APPEALS, HON. PEDRO T. SANTIAGO, SPS. SO CHING and CRISTINA SO, and NATIVE WEST INTERNATIONAL TRADING CORP., respondents.

*Per notes “Chinabank vs CA 333 Phil 158” waray gumawas ha net gn based ko nala hn case title and year.

7

G.R. No. 186560 November 17, 2010

GOVERNMENT SERVICE INSURANCE SYSTEM, Petitioner, vs. FERNANDO P. DE LEON, Respondent.

49-56

8

G.R. No. 97412 July 12, 1994

EASTERN SHIPPING LINES, INC., petitioner, vs. HON. COURT OF APPEALS AND MERCANTILE INSURANCE COMPANY, INC., respondents.

57-65

9

G.R. No. 190755 November 24, 2010

LAND BANK OF THE PHILIPPINES, Petitioner, vs. ALFREDO ONG, Respondent.

66-74

10

G.R. No. 176143 November 09, 2009

MIGUEL P. SORIANO, JR. AND JULIETA B. SORIANO, Petitioner, vs. BANK OF THE PHILIPPINE ISLANDS, Respondent.

75-76

11

G.R. No. 168782 October 10, 2008

SPOUSES JOVENAL TORING and CECILIA ESCALONA-TORING, petitioners, vs. SPOUSES ROSALIE GANZON-OLAN and GILBERT OLAN, and ROWENA OLAN, respondents.

77-79

Page 3 of 79

Republic of the Philippines SUPREME COURT

Manila

FIRST DIVISION

G.R. No. 143826 August 28, 2003

HEIRS OF IGNACIA AGUILAR-REYES, Petitioners, vs. Spouses CIPRIANO MIJARES and FLORENTINA MIJARES, Respondents.

D E C I S I O N

YNARES-SANTIAGO, J.:

Under the regime of the Civil Code, the alienation or encumbrance of a conjugal real property requires the consent of the wife. The absence of such consent renders the entire transaction1 merely voidable and not void.2The wife may, during the marriage and within ten years from the transaction questioned, bring an action for the annulment of the contract entered into by her husband without her consent.3

Assailed in this petition for review on certiorari are the January 26, 2000 Decision4 and June 19, 2000,

Resolution5 of the Court of Appeals in CA-G.R. No. 28464 which declared respondents as purchasers in good faith and set aside the May 31, 1990 and June 29, 1990 Orders of the Regional Trial Court of Quezon City, Branch 101, in Civil Case No. Q-48018.

The controversy stemmed from a dispute over Lot No. 4349-B-2,6 approximately 396 square meters, previously covered by Transfer Certificate of Title (TCT) No. 205445, located in Balintawak, Quezon City and registered in the name of Spouses Vicente Reyes and Ignacia Aguilar-Reyes.7 Said lot and the apartments built thereon were part of the spouses’ conjugal properties having been purchased using conjugal funds from their garments business.8

Vicente and Ignacia were married in 1960, but had been separated de facto since 1974.9 Sometime in 1984, Ignacia learned that on March 1, 1983, Vicente sold Lot No. 4349-B-2 to respondent spouses Cipriano and Florentina Mijares for P40,000.00.10 As a consequence thereof, TCT No. 205445 was cancelled and TCT No. 306087 was issued on April 19, 1983 in the name of respondent spouses.11 She likewise found out that Vicente filed a petition for administration and appointment of guardian with the Metropolitan Trial Court of Quezon City, Branch XXI. Vicente misrepresented therein that his wife, Ignacia, died on March 22, 1982, and that he and their 5 minor children were her only heirs.12 On September 29, 1983, the court appointed Vicente as the guardian of their minor children.13 Subsequently, in its Order dated October 14, 1983, the court authorized Vicente to sell the estate of Ignacia.14

On August 9, 1984, Ignacia, through her counsel, sent a letter to respondent spouses demanding the return of her ½ share in the lot. Failing to settle the matter amicably, Ignacia filed on June 4, 1996 a complaint15 for annulment of sale against respondent spouses. The complaint was thereafter amended to include Vicente Reyes as one of the defendants.16

In their answer, respondent spouses claimed that they are purchasers in good faith and that the sale was valid because it was duly approved by the court.17 Vicente Reyes, on the other hand, contended that what he sold to the spouses was only his share in Lot No. 4349-B-2, excluding the share of his wife, and that he never represented that the latter was already dead.18 He likewise testified that respondent spouses, through the counsel they provided him, took advantage of his illiteracy by filing a petition for the issuance of letters of administration and appointment of guardian without his knowledge.19

Page 4 of 79

On February 15, 1990, the court a quo rendered a decision declaring the sale of Lot No. 4349-B-2 void with respect to the share of Ignacia. It held that the purchase price of the lot was P110,000.00 and ordered Vicente to return ½ thereof or P55,000.00 to respondent spouses. The dispositive portion of the said decision, reads-

WHEREFORE, premises above considered, judgment is hereby rendered declaring the subject Deed of Absolute Sale, dated March [1,] 1983 signed by and between defendants Vicente Reyes and defendant Cipriano Mijares NULL AND VOID WITH RESPECT TO ONE-HALF (1/2) OF THE SAID PROPERTY;

The Register of Deeds of Quezon City is hereby ordered to cancel TCT No. 306083 (sic) in the names of defendant spouses Cipriano Mijares and Florentina Mijares and to issue a new TCT in the name of the plaintiff Ignacia Aguilar-Reyes as owner in fee simple of one-half (1/2) of said property and the other half in the names of defendant spouses Cipriano Mijares and Florentin[a] Mijares, upon payment of the required fees therefore;

Said defendant spouses Mijares are also ordered to allow plaintiff the use and exercise of rights, as well as obligations, pertinent to her one-half (1/2) ownership of the subject property;

Defendant Vicente Reyes is hereby ordered to reimburse P55,000.00 with legal rate of interest from the execution of the subject Deed of Absolute Sale on March 1, 1983, to the defendant spouses Cipriano Mijares and Florentina Mijares which corresponds to the one-half (1/2) of the actual purchase price by the said Mijares but is annulled in this decision (sic);

Defendant Vicente Reyes is hereby further ordered to pay plaintiff the amount of P50,000.00 by way of moral and exemplary damages, plus costs of this suit.

SO ORDERED.20

Ignacia filed a motion for modification of the decision praying that the sale be declared void in its entirety and that the respondents be ordered to reimburse to her the rentals they collected on the apartments built on Lot No. 4349-B-2 computed from March 1, 1983.1âwphi1

On May 31, 1990, the trial court modified its decision by declaring the sale void in its entirety and ordering Vicente Reyes to reimburse respondent spouses the purchase price of P110,000, thus –

WHEREFORE, premises considered, judgment is hereby rendered declaring the subject Deed of Absolute Sale, dated March 1, 1983 signed by and between defendants Vicente Reyes and defendant Cipriano Mijares as nulland void ab initio, in view of the absence of the wife’s conformity to said transaction.

Consequent thereto, the Register of Deeds for Quezon City is hereby ordered to cancel TCT No. 306083 (sic) in the name of Cipriano Mijares and Florentin[a] Mijares and issue a new TCT in the name of the plaintiff and defendant Ignacia Aguilar-Reyes and Vicente Reyes as owners in fee simple, upon payment of required fees therefore.

Defendant Vicente Reyes is hereby ordered to pay the amount of one hundred ten thousand pesos (P110,000.00) with legal rate of interest at 12% per annum from the execution of the subject Deed of Absolute Sale on March 1, 1983.

Further, defendant Vicente Reyes is ordered to pay the amount of P50,000.00 by way of moral and exemplary damages, plus costs of this suit.

SO ORDERED.21

On motion22 of Ignacia, the court issued an Order dated June 29, 1990 amending the dispositive portion of the May 31, 1990 decision by correcting the Transfer Certificate of Title of Lot No. 4349-B-2, in the name of

Page 5 of 79

Cipriano Mijares and Florentina Mijares, from TCT No. 306083 to TCT No. 306087; and directing the Register of Deeds of Quezon City to issue a new title in the name of Ignacia Aguilar-Reyes and Vicente Reyes. The Order likewise specified that Vicente Reyes should pay Ignacia Aguilar-Reyes the amount of P50,000.00 as moral and exemplary damages.23

Both Ignacia Aguilar-Reyes and respondent spouses appealed the decision to the Court of Appeals.24 Pending the appeal, Ignacia died and she was substituted by her compulsory heirs.25

Petitioners contended that they are entitled to reimbursement of the rentals collected on the apartment built on Lot No. 4349-B-2, while respondent spouses claimed that they are buyers in good faith. On January 26, 2000, the Court of Appeals reversed and set aside the decision of the trial court. It ruled that notwithstanding the absence of Ignacia’s consent to the sale, the same must be held valid in favor of respondents because they were innocent purchasers for value.26 The decretal potion of the appellate court’s decision states –

WHEREFORE, premises considered, the Decision appealed from and the Orders dated May 31, 1990 and June 29, 1990, are SET ASIDE and in lieu thereof a new one is rendered –

1. Declaring the Deed of Absolute Sale dated March 1, 1983 executed by Vicente Reyes in favor of spouses Cipriano and [Florentina] Mijares valid and lawful;

2. Ordering Vicente Reyes to pay spouses Mijares the amount of P30,000.00 as attorney’s fees and legal expenses; and

3. Ordering Vicente Reyes to pay spouses Mijares P50,000.00 as moral damages.

No pronouncement as to costs.

SO ORDERED.27

Undaunted by the denial of their motion for reconsideration,28 petitioners filed the instant petition contending that the assailed sale of Lot No. 4392-B-2 should be annulled because respondent spouses were not purchasers in good faith.

The issues for resolution are as follows: (1) What is the status of the sale of Lot No. 4349-B-2 to respondent spouses? (2) Assuming that the sale is annullable, should it be annulled in its entirety or only with respect to the share of Ignacia? (3) Are respondent spouses purchasers in good faith?

Articles 166 and 173 of the Civil Code,29 the governing laws at the time the assailed sale was contracted, provide:

Art.166. Unless the wife has been declared a non compos mentis or a spendthrift, or is under civil interdiction or is confined in a leprosarium, the husband cannot alienate or encumber any real property of the conjugal partnership without the wife’s consent. If she refuses unreasonably to give her consent, the court may compel her to grant the same…

Art. 173. The wife may, during the marriage and within ten years from the transaction questioned, ask the courts for the annulment of any contract of the husband entered into without her consent, when such consent is required, or any act or contract of the husband which tends to defraud her or impair her interest in the conjugal partnership property. Should the wife fail to exercise this right, she or her heirs after the dissolution of the marriage, may demand the value of property fraudulently alienated by the husband.

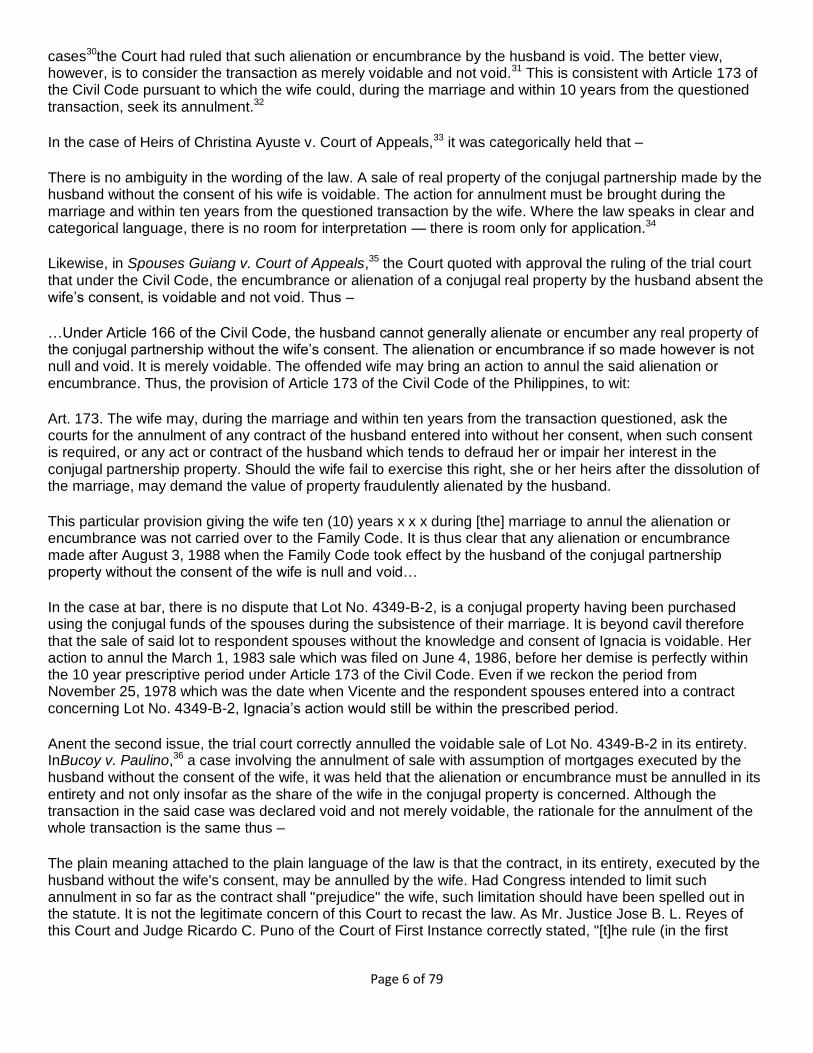

Pursuant to the foregoing provisions, the husband could not alienate or encumber any conjugal real property without the consent, express or implied, of the wife otherwise, the contract is voidable. Indeed, in several

Page 6 of 79

cases30the Court had ruled that such alienation or encumbrance by the husband is void. The better view, however, is to consider the transaction as merely voidable and not void.31 This is consistent with Article 173 of the Civil Code pursuant to which the wife could, during the marriage and within 10 years from the questioned transaction, seek its annulment.32

In the case of Heirs of Christina Ayuste v. Court of Appeals,33 it was categorically held that –

There is no ambiguity in the wording of the law. A sale of real property of the conjugal partnership made by the husband without the consent of his wife is voidable. The action for annulment must be brought during the marriage and within ten years from the questioned transaction by the wife. Where the law speaks in clear and categorical language, there is no room for interpretation — there is room only for application.34

Likewise, in Spouses Guiang v. Court of Appeals,35 the Court quoted with approval the ruling of the trial court that under the Civil Code, the encumbrance or alienation of a conjugal real property by the husband absent the wife’s consent, is voidable and not void. Thus –

…Under Article 166 of the Civil Code, the husband cannot generally alienate or encumber any real property of the conjugal partnership without the wife’s consent. The alienation or encumbrance if so made however is not null and void. It is merely voidable. The offended wife may bring an action to annul the said alienation or encumbrance. Thus, the provision of Article 173 of the Civil Code of the Philippines, to wit:

Art. 173. The wife may, during the marriage and within ten years from the transaction questioned, ask the courts for the annulment of any contract of the husband entered into without her consent, when such consent is required, or any act or contract of the husband which tends to defraud her or impair her interest in the conjugal partnership property. Should the wife fail to exercise this right, she or her heirs after the dissolution of the marriage, may demand the value of property fraudulently alienated by the husband.

This particular provision giving the wife ten (10) years x x x during [the] marriage to annul the alienation or encumbrance was not carried over to the Family Code. It is thus clear that any alienation or encumbrance made after August 3, 1988 when the Family Code took effect by the husband of the conjugal partnership property without the consent of the wife is null and void…

In the case at bar, there is no dispute that Lot No. 4349-B-2, is a conjugal property having been purchased using the conjugal funds of the spouses during the subsistence of their marriage. It is beyond cavil therefore that the sale of said lot to respondent spouses without the knowledge and consent of Ignacia is voidable. Her action to annul the March 1, 1983 sale which was filed on June 4, 1986, before her demise is perfectly within the 10 year prescriptive period under Article 173 of the Civil Code. Even if we reckon the period from November 25, 1978 which was the date when Vicente and the respondent spouses entered into a contract concerning Lot No. 4349-B-2, Ignacia’s action would still be within the prescribed period.

Anent the second issue, the trial court correctly annulled the voidable sale of Lot No. 4349-B-2 in its entirety. InBucoy v. Paulino,36 a case involving the annulment of sale with assumption of mortgages executed by the husband without the consent of the wife, it was held that the alienation or encumbrance must be annulled in its entirety and not only insofar as the share of the wife in the conjugal property is concerned. Although the transaction in the said case was declared void and not merely voidable, the rationale for the annulment of the whole transaction is the same thus –

The plain meaning attached to the plain language of the law is that the contract, in its entirety, executed by the husband without the wife's consent, may be annulled by the wife. Had Congress intended to limit such annulment in so far as the contract shall "prejudice" the wife, such limitation should have been spelled out in the statute. It is not the legitimate concern of this Court to recast the law. As Mr. Justice Jose B. L. Reyes of this Court and Judge Ricardo C. Puno of the Court of First Instance correctly stated, "[t]he rule (in the first

Page 7 of 79

sentence of Article 173) revokes Baello vs. Villanueva, 54 Phil. 213 and Coque vs. Navas Sioca, 45 Phil. 430," in which cases annulment was held to refer only to the extent of the one-half interest of the wife…

The necessity to strike down the contract of July 5, 1963 as a whole, not merely as to the share of the wife, is not without its basis in the common-sense rule. To be underscored here is that upon the provisions of Articles 161, 162 and 163 of the Civil Code, the conjugal partnership is liable for many obligations while the conjugal partnership exists. Not only that. The conjugal property is even subject to the payment of debts contracted by either spouse before the marriage, as those for the payment of fines and indemnities imposed upon them after the responsibilities in Article 161 have been covered (Article 163, par. 3), if it turns out that the spouse who is bound thereby, "should have no exclusive property or if it should be insufficient." These are considerations that go beyond the mere equitable share of the wife in the property. These are reasons enough for the husband to be stopped from disposing of the conjugal property without the consent of the wife. Even more fundamental is the fact that the nullity is decreed by the Code not on the basis of prejudice but lack of consent of an indispensable party to the contract under Article 166.37

With respect to the third issue, the Court finds that respondent spouses are not purchasers in good faith. A purchaser in good faith is one who buys property of another, without notice that some other person has a right to, or interest in, such property and pays full and fair price for the same, at the time of such purchase, or before he has notice of the claim or interest of some other persons in the property. He buys the property with the belief that the person from whom he receives the thing was the owner and could convey title to the property. A purchaser cannot close his eyes to facts which should put a reasonable man on his guard and still claim he acted in good faith.38

In the instant case, there existed circumstances that should have placed respondent spouses on guard. The death certificate of Ignacia, shows that she died on March 22, 1982. The same death certificate, however, reveals that – (1) it was issued by the Office of the Civil Registrar of Lubao Pampanga on March 10, 1982; (2) the alleged death of Ignacia was reported to the Office of the Civil Registrar on March 4, 1982; and (3) her burial or cremation would be on March 8, 1982.39 These obvious flaws in the death certificate should have prompted respondents to investigate further, especially so that respondent Florentina Mijares admitted on cross examination that she asked for the death certificate of Ignacia because she was suspicious that Ignacia was still alive.40 Moreover, respondent spouses had all the opportunity to verify the claim of Vicente that he is a widower because it was their lawyer, Atty. Rodriguito S. Saet, who represented Vicente in the special proceedings before the Metropolitan Trial Court.

Neither can respondent spouses rely on the alleged court approval of the sale. Note that the Order issued by the Metropolitan Trial Court of Quezon City, Branch XXXI, appointing Vicente as guardian of his 5 minor children, as well as the Order authorizing him to sell the estate of Ignacia were issued only on September 29, 1983 and October 14, 1983, respectively. On the other hand, the sale of the entire Lot No. 4349-B-2 to respondent spouses appears to have been made not on March 1, 1983, but even as early as November 25, 1978. In the "Agreement" dated November 25, 1978, Vicente in consideration of the amount of P110,000.00, sold to Cipriano Mijares Lot No. 4349-B-2 on installment basis, with the first installment due on or before July 31, 1979.41 This was followed by a "Memorandum of Understanding" executed on July 30, 1979, by Vicente and Cipriano – (1) acknowledging Cipriano’s receipt of Vicente’s down payment in the amount of P50,000.00; and (2) authorizing Florentina Mijares to collect rentals.42 On July 14, 1981, Vicente and Cipriano executed another "Memorandum of Agreement," stating, among other, that out of the purchase price of P110,000.00 Vicente had remaining balance of P19,000.00.43 Clearly therefore, the special proceedings before the Metropolitan Trial Court of Quezon City, Branch XXXI, could not have been the basis of respondent spouses’ claim of good faith because the sale of Lot No. 4349-B-2 occurred prior thereto.

Respondent spouses cannot deny knowledge that at the time of the sale in 1978, Vicente was married to Ignacia and that the latter did not give her conformity to the sale. This is so because the 1978 "Agreement" described Vicente as "married" but the conformity of his wife to the sale did not appear in the deed. Obviously, the execution of another deed of sale in 1983 over the same Lot No. 4349-B-2, after the alleged death of Ignacia on March 22, 1982, as well as the institution of the special proceedings were, intended to correct the

Page 8 of 79

absence of Ignacia’s consent to the sale. Even assuming that respondent spouses believed in good faith that Ignacia really died on March 22, 1982, after they purchased the lot, the fact remains that the sale of Lot No. 4349-B-2 prior to Ignacia’s alleged demise was without her consent and therefore subject to annulment. The October 14, 1983 order authorizing the sale of the estate of Ignacia, could not have validated the sale of Lot No. 4349-B-2 because said order was issued on the assumption that Ignacia was already dead and that the sale dated March 1, 1983 was never categorically approved in the said order.

The fact that the 5 minor children44 of Vicente represented by the latter, signed the March 1, 1983 deed of sale of Lot No. 4349-B-2 will not estop them from assailing the validity thereof. Not only were they too young at that time to understand the repercussions of the sale, they likewise had no right to sell the property of their mother who, when they signed the deed, was very much alive.

If a voidable contract is annulled, the restoration of what has been given is proper. The relationship between parties in any contract even if subsequently annulled must always be characterized and punctuated by good faith and fair dealing. Hence, for the sake of justice and equity, and in consonance with the salutary principle of non-enrichment at another’s expense, the Court sustains the trial court’s order directing Vicente to refund to respondent spouses the amount of P110,000.00 which they have paid as purchase price of Lot No. 4349-B-2.45The court a quo correctly found that the subject of the sale was the entire Lot No. 4349-B-2 and that the consideration thereof is not P40,000.00 as stated in the March 1, 1983 deed of sale, but P110,000.00 as evidenced by the – (1) "Agreement" dated November 25, 1978 as well as the July 30, 1979 "Memorandum of Understanding" and the July 14, 1981 "Memorandum of Agreement" which served as receipts of the installment payments made by respondent Cipriano Mijares; and (2) the receipt duly signed by Vicente Reyes acknowledging receipt of the amount of P110,000.00 from respondent spouses as payment of the sale of the controverted lot.46

The trial court, however, erred in imposing 12% interest per annum on the amount due the respondents. InEastern Shipping Lines, Inc. v. Court of Appeals,47 it was held that interest on obligations not constituting a loan or forbearance of money is six percent (6%) annually. If the purchase price could be established with certainty at the time of the filing of the complaint, the six percent (6%) interest should be computed from the date the complaint was filed until finality of the decision. In Lui v. Loy,48 involving a suit for reconveyance and

annulment of title filed by the first buyer against the seller and the second buyer, the Court, ruling in favor of the first buyer and annulling the second sale, ordered the seller to refund to the second buyer (who was not a purchaser in good faith) the purchase price of the lots. It was held therein that the 6% interest should be computed from the date of the filing of the complaint by the first buyer. After the judgment becomes final and executory until the obligation is satisfied, the amount due shall earn interest at 12% per year, the interim period being deemed equivalent to a forbearance of credit.49

Accordingly, the amount of P110,000.00 due the respondent spouses which could be determined with certainty at the time of the filing of the complaint shall earn 6% interest per annum from June 4, 1986 until the finality of this decision. If the adjudged principal and the interest (or any part thereof) remain unpaid thereafter, the interest rate shall be twelve percent (12%) per annum computed from the time the judgment becomes final and executory until it is fully satisfied.

Petitioner’s prayer for payment of rentals should be denied. Other than the allegation of Ignacia in her Sinumpaang Salaysay that the apartments could be rented at P1,000.00 a month, no other evidence was presented to substantiate her claim. In awarding rentals which are in the nature of actual damages, the Court cannot rely on mere assertions, speculations, conjectures or guesswork but must depend on competent proof and on the best evidence obtainable regarding the actual amount of loss.50 None, having been presented in the case at bar, petitioner’s claim for rentals must be denied.

While as a general rule, a party who has not appealed is not entitled to affirmative relief other than the ones granted in the decision of the court below, law and jurisprudence authorize a tribunal to consider errors, although unassigned, if they involve (1) errors affecting the lower court’s jurisdiction over the subject matter, (2) plain errors not specified, and (3) clerical errors.51 In this case, though defendant Vicente Reyes did not

Page 9 of 79

appeal, the "plain error" committed by the court a quo as to the award of moral and exemplary damages must be corrected. These awards cannot be lumped together as was done by the trial court.52 Moral and exemplary damages are different in nature, and require separate determination. Moral damages are awarded where the claimant experienced physical suffering, mental anguish, fright, serious anxiety, besmirched reputation, wounded feelings, moral shock, social humiliation, and similar injury as a result of the act complained of.53 The award of exemplary damages, on the other hand, is warranted when moral, temperate, liquidated, or compensatory damages were likewise awarded by the court.54

Hence, the trial court’s award of "P50,000.00 by way of moral and exemplary damages" should be modified. Vicente Reyes should be ordered to pay the amounts of P25,000.00 as moral damages and P25,000.00 as exemplary damages. Since Vicente Reyes was among the heirs substituted to the late Ignacia Aguilar-Reyes, payment of moral and exemplary damages must be made by Vicente to his children, petitioners in this case.

WHEREFORE, in view of all the foregoing, the petition is PARTIALLY GRANTED. The January 26, 2000 Decision and June 19, 2002, Resolution of the Court of Appeals in CA-G.R. No. 28464 are REVERSED and SET ASIDE. The May 31, 1990 Order of the Regional Trial Court of Quezon City, Branch 101, in Civil Case No. Q-48018, which annulled the March 1, 1983 Deed of Absolute Sale over Lot No. 4349-B-2, and ordered the Register of Deeds of Quezon City to cancel TCT No. 306087 in the name of respondent spouses Cipriano Mijares and Florentina Mijares covering the same property; as well as the June 29, 1990 Order correcting the typographical errors in the order dated March 1, 1983, are REINSTATED, with the following modifications –

(1) The Register of Deeds of Quezon City is ordered to issue a new certificate of title over Lot No. 4349-B-2, in the name of petitioners as co-owners thereof;

(2) Vicente Reyes is ordered to reimburse the respondent spouses the amount of P110,000.00 as purchase price of Lot No. 4349-B-2, with interest at 6% per annum from June 4, 1986, until finality of this decision. After this decision becomes final, interest at the rate of 12% per annum on the principal and interest (or any part thereof) shall be imposed until full payment.

(3) Defendant Vicente Reyes is ordered to pay the heirs of the late Ignacia Aguilar-Reyes, the amounts of P25,000.00 as moral damages and P25,000.00 as exemplary damages.

SO ORDERED.

Davide, Jr., C.J., (Chairman), Vitug, Carpio, and Azcuna, JJ., concur.

Page 10 of 79

SECOND DIVISION

G.R. No. 153802. March 11, 2005

HOMEOWNERS SAVINGS & LOAN BANK, Petitioner,

vs. MIGUELA C. DAILO, Respondents.

D E C I S I O N

TINGA, J.:

This is a petition for review on certiorari under Rule 45 of the Revised Rules of Court, assailing the Decision1 of the Court of Appeals in CA-G.R. CV No. 59986 rendered on June 3, 2002, which affirmed with modification the October 18, 1997 Decision2 of the Regional Trial Court, Branch 29, San Pablo City, Laguna in Civil Case No. SP-4748 (97).

The following factual antecedents are undisputed.

Respondent Miguela C. Dailo and Marcelino Dailo, Jr. were married on August 8, 1967. During their marriage, the spouses purchased a house and lot situated at Barangay San Francisco, San Pablo City from a certain Sandra Dalida. The subject property was declared for tax assessment purposes under Assessment of Real Property No. 94-051-2802. The Deed of Absolute Sale, however, was executed only in favor of the late Marcelino Dailo, Jr. as vendee thereof to the exclusion of his wife.3

On December 1, 1993, Marcelino Dailo, Jr. executed a Special Power of Attorney (SPA) in favor of one Lilibeth Gesmundo, authorizing the latter to obtain a loan from petitioner Homeowners Savings and Loan Bank to be secured by the spouses Dailo’s house and lot in San Pablo City. Pursuant to the SPA, Gesmundo obtained a loan in the amount of P300,000.00 from petitioner. As security therefor, Gesmundo executed on the same day a Real Estate Mortgage constituted on the subject property in favor of petitioner. The abovementioned transactions, including the execution of the SPA in favor of Gesmundo, took place without the knowledge and consent of respondent.4

Upon maturity, the loan remained outstanding. As a result, petitioner instituted extrajudicial foreclosure proceedings on the mortgaged property. After the extrajudicial sale thereof, a Certificate of Sale was issued in favor of petitioner as the highest bidder. After the lapse of one year without the property being redeemed, petitioner, through its vice-president, consolidated the ownership thereof by executing on June 6, 1996 an Affidavit of Consolidation of Ownership and a Deed of Absolute Sale.5

In the meantime, Marcelino Dailo, Jr. died on December 20, 1995. In one of her visits to the subject property, respondent learned that petitioner had already employed a certain Roldan Brion to clean its premises and that her car, a Ford sedan, was razed because Brion allowed a boy to play with fire within the premises.

Claiming that she had no knowledge of the mortgage constituted on the subject property, which was conjugal in nature, respondent instituted with the Regional Trial Court, Branch 29, San Pablo City, Civil Case No. SP-2222 (97) for Nullity of Real Estate Mortgage and Certificate of Sale, Affidavit of Consolidation of Ownership, Deed of Sale, Reconveyance with Prayer for Preliminary Injunction and Damages against petitioner. In the latter’s Answer with Counterclaim, petitioner prayed for the dismissal of the complaint on the ground that the property in question was the exclusive property of the late Marcelino Dailo, Jr.

After trial on the merits, the trial court rendered a Decision on October 18, 1997. The dispositive portion thereof

reads as follows:

Page 11 of 79

WHEREFORE, the plaintiff having proved by the preponderance of evidence the allegations of the Complaint, the Court finds for the plaintiff and hereby orders:

ON THE FIRST CAUSE OF ACTION:

1. The declaration of the following documents as null and void:

(a) The Deed of Real Estate Mortgage dated December 1, 1993 executed before Notary Public Romulo Urrea and his notarial register entered as Doc. No. 212; Page No. 44, Book No. XXI, Series of 1993.

(b) The Certificate of Sale executed by Notary Public Reynaldo Alcantara on April 20, 1995.

(c) The Affidavit of Consolidation of Ownership executed by the defendant

(c) The Affidavit of Consolidation of Ownership executed by the defendant over the residential lot located at Brgy. San Francisco, San Pablo City, covered by ARP No. 95-091-1236 entered as Doc. No. 406; Page No. 83, Book No. III, Series of 1996 of Notary Public Octavio M. Zayas.

(d) The assessment of real property No. 95-051-1236.

2. The defendant is ordered to reconvey the property subject of this complaint to the plaintiff.

ON THE SECOND CAUSE OF ACTION

1. The defendant to pay the plaintiff the sum of P40,000.00 representing the value of the car which was burned.

ON BOTH CAUSES OF ACTION

1. The defendant to pay the plaintiff the sum of P25,000.00 as attorney’s fees;

2. The defendant to pay plaintiff P25,000.00 as moral damages;

3. The defendant to pay the plaintiff the sum of P10,000.00 as exemplary damages;

4. To pay the cost of the suit.

The counterclaim is dismissed.

SO ORDERED.6

Upon elevation of the case to the Court of Appeals, the appellate court affirmed the trial court’s finding that the subject property was conjugal in nature, in the absence of clear and convincing evidence to rebut the presumption that the subject property acquired during the marriage of spouses Dailo belongs to their conjugal partnership.7The appellate court declared as void the mortgage on the subject property because it was constituted without the knowledge and consent of respondent, in accordance with Article 124 of the Family Code. Thus, it upheld the trial court’s order to reconvey the subject property to respondent.8 With respect to the damage to respondent’s car, the appellate court found petitioner to be liable therefor because it is responsible for the consequences of the acts or omissions of the person it hired to accomplish the assigned task.9 All told, the appellate court affirmed the trial court’s Decision, but deleted the award for damages and attorney’s fees for lack of basis.10

Page 12 of 79

Hence, this petition, raising the following issues for this Court’s consideration:

1. WHETHER OR NOT THE MORTGAGE CONSTITUTED BY THE LATE MARCELINO DAILO, JR. ON THE SUBJECT PROPERTY AS CO-OWNER THEREOF IS VALID AS TO HIS UNDIVIDED SHARE.

2. WHETHER OR NOT THE CONJUGAL PARTNERSHIP IS LIABLE FOR THE PAYMENT OF THE LOAN OBTAINED BY THE LATE MARCELINO DAILO, JR. THE SAME HAVING REDOUNDED TO THE BENEFIT OF THE FAMILY.11

First, petitioner takes issue with the legal provision applicable to the factual milieu of this case. It contends that Article 124 of the Family Code should be construed in relation to Article 493 of the Civil Code, which states:

ART. 493. Each co-owner shall have the full ownership of his part and of the fruits and benefits pertaining thereto, and he may therefore alienate, assign or mortgage it, and even substitute another person in its enjoyment, except when personal rights are involved. But the effect of the alienation or the mortgage, with respect to the co-owners, shall be limited to the portion which may be allotted to him in the division upon the termination of the co-ownership.

Article 124 of the Family Code provides in part:

ART. 124. The administration and enjoyment of the conjugal partnership property shall belong to both spouses jointly. . . .

In the event that one spouse is incapacitated or otherwise unable to participate in the administration of the conjugal properties, the other spouse may assume sole powers of administration. These powers do not include the powers of disposition or encumbrance which must have the authority of the court or the written consent of the other spouse. In the absence of such authority or consent, the disposition or encumbrance shall be void. . . .

Petitioner argues that although Article 124 of the Family Code requires the consent of the other spouse to the mortgage of conjugal properties, the framers of the law could not have intended to curtail the right of a spouse from exercising full ownership over the portion of the conjugal property pertaining to him under the concept of co-ownership.12 Thus, petitioner would have this Court uphold the validity of the mortgage to the extent of the late Marcelino Dailo, Jr.’s share in the conjugal partnership.

In Guiang v. Court of Appeals,13 it was held that the sale of a conjugal property requires the consent of both the

husband and wife.14 In applying Article 124 of the Family Code, this Court declared that the absence of the consent of one renders the entire sale null and void, including the portion of the conjugal property pertaining to the husband who contracted the sale. The same principle in Guiang squarely applies to the instant case. As shall be discussed next, there is no legal basis to construe Article 493 of the Civil Code as an exception to Article 124 of the Family Code.

Respondent and the late Marcelino Dailo, Jr. were married on August 8, 1967. In the absence of a marriage settlement, the system of relative community or conjugal partnership of gains governed the property relations between respondent and her late husband.15 With the effectivity of the Family Code on August 3, 1988, Chapter 4 on Conjugal Partnership of Gains in the Family Code was made applicable to conjugal partnership of gains already established before its effectivity unless vested rights have already been acquired under the Civil Code or other laws.16

The rules on co-ownership do not even apply to the property relations of respondent and the late Marcelino Dailo, Jr. even in a suppletory manner. The regime of conjugal partnership of gains is a special type of partnership, where the husband and wife place in a common fund the proceeds, products, fruits and income from their separate properties and those acquired by either or both spouses through their efforts or by

Page 13 of 79

chance.17 Unlike the absolute community of property wherein the rules on co-ownership apply in a suppletory manner,18 the conjugal partnership shall be governed by the rules on contract of partnership in all that is not in conflict with what is expressly determined in the chapter (on conjugal partnership of gains) or by the spouses in their marriage settlements.19 Thus, the property relations of respondent and her late husband shall be governed, foremost, by Chapter 4 on Conjugal Partnership of Gains of the Family Code and, suppletorily, by the rules on partnership under the Civil Code. In case of conflict, the former prevails because the Civil Code provisions on partnership apply only when the Family Code is silent on the matter.

The basic and established fact is that during his lifetime, without the knowledge and consent of his wife, Marcelino Dailo, Jr. constituted a real estate mortgage on the subject property, which formed part of their conjugal partnership. By express provision of Article 124 of the Family Code, in the absence of (court) authority or written consent of the other spouse, any disposition or encumbrance of the conjugal property shall be void.

The aforequoted provision does not qualify with respect to the share of the spouse who makes the disposition or encumbrance in the same manner that the rule on co-ownership under Article 493 of the Civil Code does. Where the law does not distinguish, courts should not distinguish.20 Thus, both the trial court and the appellate court are correct in declaring the nullity of the real estate mortgage on the subject property for lack of respondent’s consent.

Second, petitioner imposes the liability for the payment of the principal obligation obtained by the late Marcelino Dailo, Jr. on the conjugal partnership to the extent that it redounded to the benefit of the family.21

Under Article 121 of the Family Code, "[T]he conjugal partnership shall be liable for: . . . (3) Debts and obligations contracted by either spouse without the consent of the other to the extent that the family may have been benefited; . . . ." For the subject property to be held liable, the obligation contracted by the late Marcelino Dailo, Jr. must have redounded to the benefit of the conjugal partnership. There must be the requisite showing then of some advantage which clearly accrued to the welfare of the spouses. Certainly, to make a conjugal partnership respond for a liability that should appertain to the husband alone is to defeat and frustrate the avowed objective of the new Civil Code to show the utmost concern for the solidarity and well-being of the family as a unit.22

The burden of proof that the debt was contracted for the benefit of the conjugal partnership of gains lies with the creditor-party litigant claiming as such.23 Ei incumbit probatio qui dicit, non qui negat (he who asserts, not he who denies, must prove).24 Petitioner’s sweeping conclusion that the loan obtained by the late Marcelino Dailo, Jr. to finance the construction of housing units without a doubt redounded to the benefit of his family, without adducing adequate proof, does not persuade this Court. Other than petitioner’s bare allegation, there is nothing from the records of the case to compel a finding that, indeed, the loan obtained by the late Marcelino Dailo, Jr. redounded to the benefit of the family. Consequently, the conjugal partnership cannot be held liable for the payment of the principal obligation.

In addition, a perusal of the records of the case reveals that during the trial, petitioner vigorously asserted that the subject property was the exclusive property of the late Marcelino Dailo, Jr. Nowhere in the answer filed with the trial court was it alleged that the proceeds of the loan redounded to the benefit of the family. Even on appeal, petitioner never claimed that the family benefited from the proceeds of the loan. When a party adopts a certain theory in the court below, he will not be permitted to change his theory on appeal, for to permit him to do so would not only be unfair to the other party but it would also be offensive to the basic rules of fair play, justice and due process.25 A party may change his legal theory on appeal only when the factual bases thereof would not require presentation of any further evidence by the adverse party in order to enable it to properly meet the issue raised in the new theory.26

WHEREFORE, the petition is DENIED. Costs against petitioner.

SO ORDERED.

Page 14 of 79

Republic of the Philippines SUPREME COURT

Manila

FIRST DIVISION

G.R. No. 125172 June 26, 1998

Spouses ANTONIO and LUZVIMINDA GUIANG, petitioners,

vs. COURT OF APPEALS and GILDA COPUZ, respondents.

PANGANIBAN, J.:

The sale of a conjugal property requires the consent of both the husband and the wife. The absence of the consent of one renders the sale null and void, while the vitiation thereof makes it merely voidable. Only in the latter case can ratification cure the defect.

The Case

These were the principles that guided the Court in deciding this petition for review of the Decision 1 dated January 30, 1996 and the Resolution 2 dated May 28, 1996, promulgated by the Court of Appeals in CA-GR CV No. 41758, affirming the Decision of the lower court and denying reconsideration, respectively.

On May 28, 1990, Private Respondent Gilda Corpuz filed an Amended Complainant 3 against her husband

Judie Corpuz and Petitioner-Spouses Antonio and Luzviminda Guiang. The said Complaint sought the declaration of a certain deed of sale, which involved the conjugal property of private respondent and her husband, null and void. The case was raffled to the Regional Trial Court of Koronadal, South Cotabato, Branch 25. In due course, the trial court rendered a Decision 4 dated September 9, 1992, disposing as follow: 5

ACCORDINGLY, judgment is rendered for the plaintiff and against the defendants,

1. Declaring both the Deed of Transfer of Rights dated March 1, 1990 (Exh. "A") and the "amicable settlement" dated March 16, 1990 (Exh. "B") as null void and of no effect;

2. Recognizing as lawful and valid the ownership and possession of plaintiff Gilda Corpuz over the remaining one-half portion of Lot 9, Block 8, (LRC) Psd-165409 which has been the subject of the Deed of Transfer of Rights (Exh. "A");

3. Ordering plaintiff Gilda Corpuz to reimburse defendants Luzviminda Guiang the amount of NINE THOUSAND (P9,000.00) PESOS corresponding to the payment made by defendants Guiangs to Manuel Callejo for the unpaid balance of the account of plaintiff in favor of Manuel Callejo, and another sum of P379.62 representing one-half of the amount of realty taxes paid by defendants Guiangs on Lot 9, Block 8, (LRC) Psd-165409, both with legal interests thereon computed from the finality of the decision.

No pronouncement as to costs in view of the factual circumstances of the case.

Page 15 of 79

Dissatisfied, petitioners-spouses filed an appeal with the Court of Appeals. Respondent Court, in its challenged Decision, ruled as follow: 6

WHEREFORE, the appealed of the lower court in Civil Case No. 204 is hereby AFFIRMED by this Court. No costs considering plaintiff-appellee's failure to file her brief despite notice.

Reconsideration was similarly denied by the same court in its assailed Resolution: 7

Finding that the issues raised in defendants-appellants motion for reconsideration of Our decision in this case of January 30, 1996, to be a mere rehash of the same issues which we have already passed upon in the said decision, and there [being] no cogent reason to disturb the same, this Court RESOLVED to DENY the instant motion for reconsideration for lack of merit.

The Facts

The facts of this case are simple. Over the objection of private respondent and while she was in Manila seeking employment, her husband sold to the petitioners-spouses one half of their conjugal peoperty, consisting of their residence and the lot on which it stood. The circumstances of this sale are set forth in the Decision of Respondent Court, which quoted from the Decision of the trial court as follows: 8

1. Plaintiff Gilda Corpuz and defendant Judie Corpuz are legally married spouses. They were married on December 24, 1968 in Bacolod City, before a judge. This is admitted by defendants-spouses Antonio and Luzviminda Guiang in their answer, and also admitted by defendant Judie Corpuz when he testified in court (tsn. p. 3, June 9, 1992), although the latter says that they were married in 1967. The couple have three children, namely: Junie — 18 years old, Harriet — 17 years of age, and Jodie or Joji, the youngest, who was 15 years of age in August, 1990 when her mother testified in court.

Sometime on February 14, 1983, the couple Gilda and Judie Corpuz, with plaintiff-wife Gilda Corpuz as vendee, bought a 421 sq. meter lot located in Barangay Gen. Paulino Santos (Bo. 1), Koronadal, South Cotabato, and particularly known as Lot 9, Block 8, (LRC) Psd-165409 from Manuel Callejo who signed as vendor through a conditional deed of sale for a total consideration of P14,735.00. The consideration was payable in installment, with right of cancellation in favor of vendor should vendee fail to pay three successive installments (Exh. "2", tsn p. 6, February 14, 1990).

2. Sometime on April 22, 1988, the couple Gilda and Judie Corpuz sold one-half portion of their Lot No. 9, Block 8, (LRC) Psd-165409 to the defendants-spouses Antonio and Luzviminda Guiang. The latter have since then occupied the one-half portion [and] built their house thereon (tsn. p. 4, May 22, 1992). They are thus adjoining neighbors of the Corpuzes.

3. Plaintiff Gilda Corpuz left for Manila sometime in June 1989. She was trying to look for work abroad, in [the] Middle East. Unfortunately, she became a victim of an unscrupulous illegal recruiter. She was not able to go abroad. She stayed for sometime in Manila however, coming back to Koronadal, South Cotabato, . . . on March 11, 1990. Plaintiff's departure for Manila to look for work in the Middle East was with the consent of her husband Judie Corpuz (tsn. p. 16, Aug. 12, 1990; p. 10 Sept. 6, 1991).

After his wife's departure for Manila, defendant Judie Corpuz seldom went home to the conjugal dwelling. He stayed most of the time at his place of work at Samahang Nayon Building, a hotel, restaurant, and a cooperative. Daughter Herriet Corpuz went to school at King's College, Bo. 1, Koronadal, South Cotabato, but she was at the same time working as household help of, and

Page 16 of 79

staying at, the house of Mr. Panes. Her brother Junie was not working. Her younger sister Jodie (Jojie) was going to school. Her mother sometimes sent them money (tsn. p. 14, Sept. 6, 1991.)

Sometime in January 1990, Harriet Corpuz learned that her father intended to sell the remaining one-half portion including their house, of their homelot to defendants Guiangs. She wrote a letter to her mother informing her. She [Gilda Corpuz] replied that she was objecting to the sale. Harriet, however, did not inform her father about this; but instead gave the letter to Mrs. Luzviminda Guiang so that she [Guiang] would advise her father (tsn. pp. 16-17, Sept. 6, 1991).

4. However, in the absence of his wife Gilda Corpuz, defendant Judie Corpuz pushed through the sale of the remaining one-half portion of Lot 9, Block 8, (LRC) Psd-165409. On March 1, 1990, he sold to defendant Luzviminda Guiang thru a document known as "Deed of Transfer of Rights" (Exh. "A") the remaining one-half portion of their lot and the house standing thereon for a total consideration of P30,000.00 of which P5,000.00 was to be paid in June, 1990. Transferor Judie Corpuz's children Junie and Harriet signed the document as witness.

Four (4) days after March 1, 1990 or on March 5, 1990, obviously to cure whatever defect in defendant Judie Corpuz's title over the lot transferred, defendant Luzviminda Guiang as vendee executed another agreement over Lot 9, Block 8, (LRC) Psd-165408 (Exh. "3"), this time with Manuela Jimenez Callejo, a widow of the original registered owner from whom the couple Judie and Gilda Corpuz originally bought the lot (Exh. "2"), who signed as vendor for a consideration of P9,000.00. Defendant Judie Corpuz signed as a witness to the sale (Exh. "3-A"). The new sale (Exh. "3") describes the lot sold as Lot 8, Block 9, (LRC) Psd-165408 but it is obvious from the mass of evidence that the correct lot is Lot 8, Block 9, (LRC) Psd-165409, the very lot earlier sold to the couple Gilda and Judie Corpuz.

5. Sometimes on March 11, 1990, plaintiff returned home. She found her children staying with other households. Only Junie was staying in their house. Harriet and Joji were with Mr. Panes. Gilda gathered her children together and stayed at their house. Her husband was nowhere to be found. She was informed by her children that their father had a wife already.

6. For staying in their house sold by her husband, plaintiff was complained against by defendant Luzviminda Guiang and her husband Antonio Guiang before the Barangay authorities of Barangay General Paulino Santos (Bo. 1), Koronadal, South Cotabato, for trespassing (tsn. p. 34, Aug. 17, 1990). The case was docketed by the barangay authorities as Barangay Case No. 38 for "trespassing". On March 16, 1990, the parties thereat signed a document known as "amicable settlement". In full, the settlement provides for, to wit:

That respondent, Mrs. Gilda Corpuz and her three children, namely: Junie, Hariet and Judie to leave voluntarily the house of Mr. and Mrs. Antonio Guiang, where they are presently boarding without any charge, on or before April 7, 1990.

FAIL NOT UNDER THE PENALTY OF THE LAW.

Believing that she had received the shorter end of the bargain, plaintiff to the Barangay Captain of Barangay Paulino Santos to question her signature on the amicable settlement. She was referred however to the Office-In-Charge at the time, a certain Mr. de la Cruz. The latter in turn told her that he could not do anything on the matter (tsn. p. 31, Aug. 17, 1990).

This particular point not rebutted. The Barangay Captain who testified did not deny that Mrs. Gilda Corpuz approached him for the annulment of the settlement. He merely said he forgot whether Mrs. Corpuz had approached him (tsn. p. 13, Sept. 26, 1990). We thus conclude that

Page 17 of 79

Mrs. Corpuz really approached the Barangay Captain for the annulment of the settlement. Annulment not having been made, plaintiff stayed put in her house and lot.

7. Defendant-spouses Guiang followed thru the amicable settlement with a motion for the execution of the amicable settlement, filing the same with the Municipal Trial Court of Koronadal, South Cotabato. The proceedings [are] still pending before the said court, with the filing of the instant suit.

8. As a consequence of the sale, the spouses Guiang spent P600.00 for the preparation of the Deed of Transfer of Rights, Exh. "A", P9,000.00 as the amount they paid to Mrs. Manuela Callejo, having assumed the remaining obligation of the Corpuzes to Mrs. Callejo (Exh. "3"); P100.00 for the preparation of Exhibit "3"; a total of P759.62 basic tax and special education fund on the lot; P127.50 as the total documentary stamp tax on the various documents; P535.72 for the capital gains tax; P22.50 as transfer tax; a standard fee of P17.00; certification fee of P5.00. These expenses particularly the taxes and other expenses towards the transfer of the title to the spouses Guiangs were incurred for the whole Lot 9, Block 8, (LRC) Psd-165409.

Ruling of Respondent Court

Respondent Court found no reversible error in the trial court's ruling that any alienation or encumbrance by the husband of the conjugal propety without the consent of his wife is null and void as provided under Article 124 of the Family Code. It also rejected petitioners' contention that the "amicable sttlement" ratified said sale, citing Article 1409 of the Code which expressly bars ratification of the contracts specified therein,

particularly those "prohibited or declared void by law."

Hence, this petition. 9

The Issues

In their Memorandum, petitioners assign to public respondent the following errors: 10

I

Whether or not the assailed Deed of Transfer of Rights was validly executed.

II

Whether or not the Cour of Appeals erred in not declairing as voidable contract under Art. 1390 of the Civil Code the impugned Deed of Transfer of Rights which was validly ratified thru the execution of the "amicable settlement" by the contending parties.

III

Whether or not the Court of Appeals erred in not setting aside the findings of the Court a quo which recognized as lawful and valid the ownership and possession of private respondent over the remaining one half (1/2) portion of the properly.

In a nutshell, petitioners-spouses contend that (1) the contract of sale (Deed of Transfer of Rights) was merely voidable, and (2) such contract was ratified by private respondent when she entered into an amicable sttlement with them.

This Court's Ruling

Page 18 of 79

The petition is bereft of merit.

First Issue: Void or Voidable Contract?

Petitioners insist that the questioned Deed of Transfer of Rights was validly executed by the parties-litigants in good faith and for valuable consideration. The absence of private respondent's consent merely rendered the Deed voidable under Article 1390 of the Civil Code, which provides:

Art. 1390. The following contracts are voidable or annullable, even though there may have been no damage to the contracting parties:

xxx xxx xxx

(2) Those where the consent is vitiated by mistake, violence, intimidation, undue influence or fraud.

These contracts are binding, unless they are annulled by a proper action in court. They are susceptible of ratification.(n)

The error in petitioners' contention is evident. Article 1390, par. 2, refers to contracts visited by vices of consent,i.e., contracts which were entered into by a person whose consent was obtained and vitiated through mistake, violence, intimidation, undue influence or fraud. In this instance, private respondent's consent to the contract of sale of their conjugal property was totally inexistent or absent. Gilda Corpuz, on direct examination, testified thus:11

Q Now, on March 1, 1990, could you still recall where you were?

A I was still in Manila during that time.

xxx xxx xxx

ATTY. FUENTES:

Q When did you come back to Koronadal, South Cotabato?

A That was on March 11, 1990, Ma'am.

Q Now, when you arrived at Koronadal, was there any problem which arose concerning the ownership of your residential house at Callejo Subdivision?

A When I arrived here in Koronadal, there was a problem which arose regarding my residential house and lot because it was sold by my husband without my knowledge.

This being the case, said contract properly falls within the ambit of Article 124 of the Family Code, which was correctly applied by the teo lower court:

Art. 124. The administration and enjoyment of the conjugal partnerhip properly shall belong to both spouses jointly. In case of disgreement, the husband's decision shall prevail, subject recourse to the court by the wife for proper remedy, which must be availed of within five years from the date of the contract implementing such decision.

Page 19 of 79

In the event that one spouse is incapacitated or otherwise unable to participate in the administration of the conjugal properties, the other spouse may assume sole powers of administration. These powers do not include the powers of disposition or encumbrance which must have the authority of the court or the written consent of the other spouse. In the absence of such authority or consent, the disposition or encumbrance shall be void. However, the transaction shall be construed as a continuing offer on the part of the consenting spouse and the third person, and may be perfected as a binding contract upon the acceptance by the other spouse or authorization by the court before the offer is withdrawn by either or both offerors. (165a) (Emphasis supplied)

Comparing said law with its equivalent provision in the Civil Code, the trial court adroitly explained the amendatory effect of the above provision in this wise: 12

The legal provision is clear. The disposition or encumbrance is void. It becomes still clearer if we compare the same with the equivalent provision of the Civil Code of the Philippines. Under Article 166 of the Civil Code, the husband cannot generally alienate or encumber any real property of the conjugal partnershit without the wife's consent. The alienation or encumbrance if so made however is not null and void. It is merely voidable. The offended wife may bring an action to annul the said alienation or encumbrance. Thus the provision of Article 173 of the Civil Code of the Philippines, to wit:

Art. 173. The wife may, during the marriage and within ten years from the transaction questioned, ask the courts for the annulment of any contract of the husband entered into without her consent, when such consent is required, or any act or contract of the husband which tends to defraud her or impair her interest in the conjugal partnership property. Should the wife fail to exercise this right, she or her heirs after the dissolution of the marriage, may demand the value of property fraudulently alienated by the husband.(n)

This particular provision giving the wife ten (10) years . . . during [the] marriage to annul the alienation or encumbrance was not carried over to the Family Code. It is thus clear that any alienation or encumbrance made after August 3, 1988 when the Family Code took effect by the husband of the conjugal partnership property without the consent of the wife is null and void.

Furthermore, it must be noted that the fraud and the intimidation referred to by petitioners were perpetrated in the execution of the document embodying the amicable settlement. Gilda Corpuz alleged during trial that barangay authorities made her sign said document through misrepresentation and coercion. 13 In any event, its execution does not alter the void character of the deed of sale between the husband and the petitioners-spouses, as will be discussed later. The fact remains that such contract was entered into without the wife's consent.

In sum, the nullity of the contract of sale is premised on the absence of private respondent's consent. To constitute a valid contract, the Civil Code requires the concurrence of the following elements: (1) cause, (2) object, and (3) consent, 14 the last element being indubitably absent in the case at bar.

Second Issue: Amicable Settlement

Insisting that the contract of sale was merely voidable, petitioners aver that it was duly ratified by the contending parties through the "amicable settlement" they executed on March 16, 1990 in Barangay Case No. 38.

The position is not well taken. The trial and the appellate courts have resolved this issue in favor of the private respondent. The trial court correctly held: 15

Page 20 of 79

By the specific provision of the law [Art. 1390, Civil Code] therefore, the Deed to Transfer of Rights (Exh. "A") cannot be ratified, even by an "amicable settlement". The participation by some barangay authorities in the "amicable settlement" cannot otherwise validate an invalid act. Moreover, it cannot be denied that the "amicable settlement (Exh. "B") entered into by plaintiff Gilda Corpuz and defendent spouses Guiang is a contract. It is a direct offshoot of the Deed of Transfer of Rights (Exh. "A"). By express provision of law, such a contract is also void. Thus, the legal provision, to wit:

Art. 1422. Acontract which is the direct result of a previous illegal contract, is also void and inexistent. (Civil Code of the Philippines).

In summation therefore, both the Deed of transfer of Rights (Exh. "A") and the "amicable settlement" (Exh. "3") are null and void.

Doctrinally and clearly, a void contract cannot be ratified. 16

Neither can the "amicable settlement" be considered a continuing offer that was accepted and perfected by the parties, following the last sentence of Article 124. The order of the pertinent events is clear: after the sale, petitioners filed a complaint for trespassing against private respondent, after which the barangay authorities secured an "amicable settlement" and petitioners filed before the MTC a motion for its execution. The settlement, however, does not mention a continuing offer to sell the property or an acceptance of such a continuing offer. Its tenor was to the effect that private respondent would vacate the property. By no stretch of the imagination, can the Court interpret this document as the acceptance mentioned in Article 124.

WHEREFORE, the Court hereby DENIES the petition and AFFIRMS the challenged Decision and Resolution. Costs against petitioners.

SO ORDERED.

Page 21 of 79

Republic of the Philippines SUPREME COURT

Baguio City

THIRD DIVISION

G.R. No. 158040 April 14, 2008

SPOUSES ONESIFORO and ROSARIO ALINAS, petitioner, vs. SPOUSES VICTOR and ELENA ALINAS, respondents.

D E C I S I O N

AUSTRIA-MARTINEZ, J.:

This resolves the Petition for Review on Certiorari under Rule 45 of the Rules of Court, praying that the

Decision1of the Court of Appeals (CA) dated September 25, 2002, and the CA Resolution2 dated March 31, 2003, denying petitioners' motion for reconsideration, be reversed and set aside.

The factual antecedents of the case are as follows.

Spouses Onesiforo and Rosario Alinas (petitioners) separated sometime in 1982, with Rosario moving to Pagadian City and Onesiforo moving to Manila. They left behind two lots identified as Lot 896-B-9-A with a bodega standing on it and Lot 896-B-9-B with petitioners' house. These two lots are the subject of the present petition.

Petitioner Onesiforo Alinas (Onesiforo) and respondent Victor Alinas (Victor) are brothers. Petitioners allege that they entrusted their properties to Victor and Elena Alinas (respondent spouses) with the agreement that any income from rentals of the properties should be remitted to the Social Security System (SSS) and to the Rural Bank of Oroquieta City (RBO), as such rentals were believed sufficient to pay off petitioners' loans with said institutions. Lot 896-B-9-A with the bodega was mortgaged as security for the loan obtained from the RBO, while Lot 896-B-9-B with the house was mortgaged to the SSS. Onesiforo alleges that he left blank papers with his signature on them to facilitate the administration of said properties.

Sometime in 1993, petitioners discovered that their two lots were already titled in the name of respondent spouses.

Records show that after Lot 896-B-9-A was extra-judicially foreclosed, Transfer Certificate of Title (TCT) No. T-118533 covering said property was issued in the name of mortgagee RBO on November 13, 1987. On May 2, 1988, the duly authorized representative of RBO executed a Deed of Installment Sale of Bank's Acquired Assets4conveying Lot 896-B-9-A to respondent spouses. RBO's TCT over Lot 896-B-9-A was then cancelled and on February 22, 1989, TCT No. T-126645 covering said lot was issued in the name of respondent spouses.

Lot 896-B-9-B was also foreclosed by the SSS and on November 17, 1986, the Ex-Oficio City Sheriff of Ozamis City issued a Certificate of Sale6 over said property in favor of the SSS. However, pursuant to a Special Power of Attorney7 signed by Onesiforo in favor of Victor, dated March 10, 1989, the latter was able to redeem, on the same date, Lot 896-B-9-B from the SSS for the sum of P111,110.09. On June 19, 1989, a Certificate of Redemption8 was issued by the SSS.

Onesiforo's signature also appears in an Absolute Deed of Sale9 likewise dated March 10, 1989, selling Lot 896-B-9-B to respondent spouses. The records also show a notarized document dated March 10, 1989 and

Page 22 of 79

captioned Agreement10 whereby petitioner Onesiforo acknowledged that his brother Victor used his own money to redeem Lot 896-B-9-B from the SSS and, thus, Victor became the owner of said lot. In the same Agreeement, petitioner Onesiforo waived whatever rights, claims, and interests he or his heirs, successors and assigns have or may have over the subject property. On March 15, 1993, by virtue of said documents, TCT No. 1739411 covering Lot 896-B-9-B was issued in the name of respondent spouses.

On June 25, 1993, petitioners filed with the Regional Trial Court (RTC) of Ozamis City a complaint for recovery of possession and ownership of their conjugal properties with damages against respondent spouses.

After trial, the RTC rendered its Decision dated November 13, 1995, finding that:

1. Plaintiffs have not proven that they entrusted defendant spouses with the care and administration of their properties. It was Valeria Alinas, their mother, whom plaintiff Onesiforo requested/directed to "take care of everything and sell everything" and Teresita Nuñez, his elder sister, to whom he left a "verbal" authority to administer his properties.

2. Plaintiffs have not proven their allegation that defendant spouses agreed to pay rent of P1,500.00 a month for the occupancy of plaintiffs' house, which rent was to be remitted to the SSS and Rural Bank of Oroquieta to pay off plaintiffs' loan and to keep for plaintiffs the rest of the rent after the loans would have been paid in full.

3. Plaintiff Onesiforo's allegation that defendants concocted deeds of conveyances (Exh. "M", "N" & "O") with the use of his signatures in blank is not worthy of credence. Why his family would conspire to rob him at a time when life had struck him with a cruel blow in the form of a failed marriage that sent him plummeting to the depths of despair is not explained and likewise defies comprehension. That his signatures appear exactly on the spot where they ought to be in Exhs. "M", "N" & "O" belies his pretension that he affixed them on blank paper only for the purpose of facilitating his sister Terry's acts of administration.

This Court, therefore, does not find that defendant spouses had schemed to obtain title to plaintiffs' properties or enriched themselves at the expense of plaintiffs.12

with the following dispositive portion:

WHEREFORE, this Court renders judgment:

1. declaring [respondents] Victor Jr. and Elena Alinas owners of Lot 896-B-9-A with the building (bodega) standing thereon and affirming the validity of their acquisition thereof from the Rural Bank of Oroquieta, Inc.;

2. declaring [petitioners] Onesiforo and Rosario Alinas owners of Lot 896-B-9-B with the house standing thereon, plaintiff Onesiforo's sale thereof to defendants spouses without the consent of his wife being null and void and defendant spouses' redemption thereof from the SSS not having conferred its ownership to them;

3. ordering [petitioners] to reimburse [respondents] Victor Jr. and Elena Alinas the redemption sum ofP111,100.09, paid by them to the SSS (without interest as it shall be compensated with the rental value of the house they occupy) within sixty days from the finality of this judgment;

4. ordering [respondents] to vacate the subject house within thirty days from receiving the reimbursement mentioned in No. 3 above; and

Page 23 of 79

5. reinstating TCT No. T-7248 in the name of [petitioners] and cancelling TCT No. T-17394 in the name of [respondents].

No costs.

SO ORDERED.13

Only respondent spouses appealed to the CA assailing the RTC's ruling that they acquired Lot 896-B-9-B from the SSS by mere redemption and not by purchase. They likewise question the reimbursement by petitioners of the redemption price without interest.

On September 25, 2002, the CA promulgated herein assailed Decision, the dispositive portion of which reads:

WHEREFORE, in view of the foregoing disquisitions, the first paragraph of the dispositive portion of the assailed decision is AFFIRMED and the rest MODIFIED as follows:

1. declaring [respondents] Victor Jr. and Elena Alinas owners of Lot 896-B-9-A with the building (bodega) standing thereon and affirming the validity of their acquisition thereof from the Rural Bank of Oroquieta, Inc.;

2. declaring Onesiforo's sale of Lot 896-B-9-B together with the house standing thereon to [respondents] in so far as Rosario Alinas, his wife's share of one half thereof is concerned, of no force and effect;

3. ordering [petitioners] Rosario Alinas to reimburse [respondents] the redemption amount ofP55,550.00 with interest of 12% per annum from the time of redemption until fully paid.

4. ordering the [respondents] to convey and transfer one half portion of Lot 896-B-9-B unto Rosario Alinas, which comprises her share on the property simultaneous to the tender of the above redemption price, both to be accomplished within sixty (60) days from finality of this judgment.

5. in the event of failure of [respondents] to execute the acts as specified above, [petitioner] Rosario Alinas may proceed against them under Section 10, Rule 39 of the 1997 Rules of Civil Procedure.

6. on the other hand, failure of [petitioner] Rosario Alinas to reimburse the redemption price within sixty (60) days from the finality of this decision will render the conveyance and sale of her share by her husband to [respondents], of full force and effect.

No costs.

SO ORDERED.14

Petitioners moved for reconsideration but the CA denied said motion per herein assailed Resolution dated March 31, 2003.

Hence, the present petition on the following grounds:

The Honorable Court of Appeals abuse [sic] its discretion in disregarding the testimony of the Register of Deeds, Atty. Nerio Nuñez, who swore that the signatures appearing on various TCTs were not his own;

Page 24 of 79

The Honorable Court of Appeals manifestly abuse [sic] its discretion in declaring the respondents to be the owners of Lot 896-B-9-A with the building (bodega) standing thereon when they merely redeemed the property and are therefore mere trustees of the real owners of the property;

It was pure speculation and conjecture and surmise for the Honorable Court of Appeals to impose an obligation to reimburse upon petitioners without ordering respondents to account for the rentals of the properties from the time they occupied the same up to the present time and thereafter credit one against the other whichever is higher.15

The first issue raised by petitioners deserves scant consideration. By assailing the authenticity of the Registrar of Deeds' signature on the certificates of title, they are, in effect, questioning the validity of the certificates.

Section 48 of Presidential Decree No. 1529 provides, thus:

Sec. 48. Certificate not subject to collateral attack. - A certificate of title shall not be subject to collateral

attack. It cannot be altered, modified, or cancelled except in a direct proceeding in accordance with law.

Pursuant to said provision, the Court ruled in De Pedro v. Romasan Development Corporation16 that:

It has been held that a certificate of title, once registered, should not thereafter be impugned, altered, changed, modified, enlarged or diminished except in a direct proceeding permitted by law. x x x

The action of the petitioners against the respondents, based on the material allegations of the complaint,is one for recovery of possession of the subject property and damages. However, such action is not a direct, but a collateral attack of TCT No. 236044.17 (Emphasis supplied)

As in De Pedro, the complaint filed by herein petitioners with the RTC is also one for recovery of possession

and ownership. Verily, the present case is merely a collateral attack on TCT No. T-17394, which is not allowed by law and jurisprudence.

With regard to the second issue, petitioners’ claim that it was the CA which declared respondent spouses owners of Lot 896-B-9-A (with bodega) is misleading. It was the RTC which ruled that respondent spouses are the owners of Lot 896-B-9-A and, therefore, since only the respondent spouses appealed to the CA, the issue of ownership over Lot 896-B-9-A is not raised before the appellate court. Necessarily, the CA merely reiterated in the dispositive portion of its decision the RTC's ruling on respondent spouses' ownership of Lot 896-B-9-A.

It is a basic principle that no modification of judgment or affirmative relief can be granted to a party who did not appeal.18 Hence, not having appealed from the RTC Decision, petitioners can no longer seek the reversal or modification of the trial court's ruling that respondent spouses had acquired ownership of Lot 896-B-9-A by virtue of the sale of the lot to them by RBO.